Rocket's New Acquisitions Could Redefine the Business, If Integration Doesn't Break It

Rocket Companies, Inc. ![]() RKT has long been synonymous with mortgages, although arguably it was a company built for low interest rates. Yet, under the surface lies a business that has quietly spent the past two years rebuilding its foundation for a new cycle. Rocket is reshaping itself from a pure lender into something far broader, an end-to-end housing platform.

RKT has long been synonymous with mortgages, although arguably it was a company built for low interest rates. Yet, under the surface lies a business that has quietly spent the past two years rebuilding its foundation for a new cycle. Rocket is reshaping itself from a pure lender into something far broader, an end-to-end housing platform.

The core thesis is that the Rocket of today is fundamentally different from the one that thrived in the 2020-2021 refinance boom. With that in mind, in this article, I will explore Rocket's journey from its current operations, through its present reinvention via strategic moves, and onto the future it's aiming for in a very different mortgage landscape.

From Boom to Bust

Rocket has been a disruptor throughout its life. Founded by Dan Gilbert in 1985 as Rock Financial, the company's first innovation was "Mortgage In A Box" in 1996. This simple concept of allowing clients to complete a mortgage application at home and mail it in was a revolutionary idea that proved the viability of a new, simplified process. In 1999, the company launched RockLoans.com, fully embracing a centralized, online-only model. The culmination of this digital-first strategy arrived in 2015 with the launch of Rocket Mortgage, the world's first completely online mortgage process. The platform was a runaway success, enabling the company to scale at an unprecedented pace. By 2017, Rocket had surpassed nearly 30,000 other lending institutions to become the largest residential mortgage lender in the United States. This high-velocity, capital-light approach, which involves originating loans and selling them into the secondary market, worked brilliantly in a favorable environment, culminating in a peak mortgage volume of $351 billion in 2021.

That boom, however, turned to bust. By October 2023, the Federal Reserve's aggressive campaign to combat inflation sent interest rates soaring, with the 30-year mortgage rates peaking near 7.8% (a 5% jump from early 2021). Housing affordability crumbled, and home financing demand plunged. In fact, 2023 marked the slowest year for U.S. home sales in nearly three decades at just 4.09 million transactions, down 18.7% from 2022. This put Rocket in a tough spot. Originations collapsed from $351 billion in 2021 to only about $79 billion in 2023. The company's core business (taking in applications and selling loans) was suddenly starved of volume.

Source: Freddie Mac Primary Mortgage Market Survey and Market Yield on U.S. Treasury Securities at 10-Year Constant Maturity

This has revealed a significant vulnerability. A business model that was heavily reliant on mortgage originations. This model is particularly successful during periods of low interest rates and high refinancing activity but struggles in a high-interest environment making it inherently cyclical.

By 2023, investor sentiment was low. Rocket's stock, which had briefly spiked above $30 in 2021, fell into the single digits as the market questioned whether this was just a cyclical lender with a tech sheen.

Building the Housing Platform

To strengthen the business and reduce cyclicality to a certain extent, Rocket Companies initiated a strategic transformation in an effort to build on both organic initiatives and large-scale acquisitions. In a span of weeks, Rocket announced two all-stock deals. A $1.75 billion acquisition of Redfin and a $9.4 billion agreement to acquire Mr. Cooper Group (NASDAQ:COOP). The idea is not only to generate synergies but also to build a deeper funnel. Buyers find the house on Redfin, get the mortgage from Rocket and then the loan is handed to Mr. Cooper to service. Furthermore, AI will help the process, but the goal is for the entire homebuyer life cycle to run through Rocket.

Redfin is the most-visited real estate brokerage website in the country with roughly 50 million people using Redfin's platform each month to search for homes. By joining forces, Rocket gains a popular top-of-funnel channel. A direct pipeline to homebuyers before they start shopping for mortgages. In Rocket's words, this union connects Redfin's monthly visitors to Rocket's mortgage products. For homebuyers, the integration promises a seamless journey, browsing listings, engaging an agent, and getting pre-qualified for a loan all in one place. For Rocket, it's a way to capture customers organically instead of paying heavily for leads, serving as a direct pipeline for its mortgage and other financial products. The vision is for an AI-powered ecosystem where a customer can seamlessly go from searching for a home to securing financing to closing, all within a single platform. The company can potentially save hundreds of millions in marketing, given that it now owns a major portal where high-intent buyers congregate. Moreover, Rocket is offering preferred pricing to incentivize homebuyers to go through the whole journey using Rocket/Redfin. Clients who finance their home through Rocket Mortgage and buy a home listed by a Redfin agent or purchase with the help of a Redfin agent will have a one percentage point reduction in their interest rate for the first year of their loan or receive a lender credit at

closing, up to $6,000.

It's also a bet on synergies. This vertical integration is expected to generate over $200 million in annual run-rate synergies by 2027, with $140 million coming from cost savings and more than $60 million from revenue enhancements. While Redfin itself was unprofitable (losing over $164 million in 2024), Rocket sees value in Redfin's brand, data, and audience. Early signs are promising. In Rocket's latest quarter, management noted that Redfin is already boosting the purchase loan funnel and conversion rates as integration begins.

If Redfin is the front door, Mr. Cooper is the back end of Rocket's new blueprint. Mr. Cooper Group is the largest non-bank mortgage servicer in America. When this pending $9.4 billion merger closes (expected by Q4 2025), Rocket will inherit Mr. Cooper's colossal servicing portfolio, with a combined loan volume of over $2.1 trillion, or roughly one in every six U.S. mortgages. This is a transformational scale. In a rate-sensitive industry, servicing is a stabilizer, with fees that keep flowing even when new originations are slow. It also cuts Rocket's cost to acquire customers. Instead of spending big to find the next borrower, Rocket will have gained nearly 7 million additional clients and 150 million annual customer interactions to whom it can cross-sell refinance loans, home equity lines, insurance, or other products. The acquisition is expected to generate approximately $500 million in annual run-rate synergies, primarily from increased "recapture" of existing clients and operational cost savings.

As Rocket's CEO Varun Krishna said "Servicing is a critical pillar of homeownership alongside home search and mortgage origination." With these two acquisitions, Rocket can now provide the full journey. In effect, Rocket wants to own the client relationship from the moment they start dreaming on a home-search site, through the loan closing, and then for the decades of homeownership that follow, setting up a lifetime customer value far beyond a one-off mortgage transaction.

Of course, these projections are not without risk. While I prefer organic growth, these additions look promising. However, the successful integration of two large, complex organizations is a significant challenge, and there is always the possibility that the anticipated synergies will not be fully realized. Redfin is the most-trafficked real estate brokerage site in the U.S., with roughly 50 million monthly users. Capturing meaningful conversion from that funnel will take careful integration. Mr. Cooper's $1.56 trillion servicing portfolio is more than 2.5 Rocket's current $609 billion book, a scale that will nearly triple the company's servicing base overnight. If the integration falters, these massive additions could overwhelm Rocket's operations rather than strengthen them.

Source: Rocket Companies

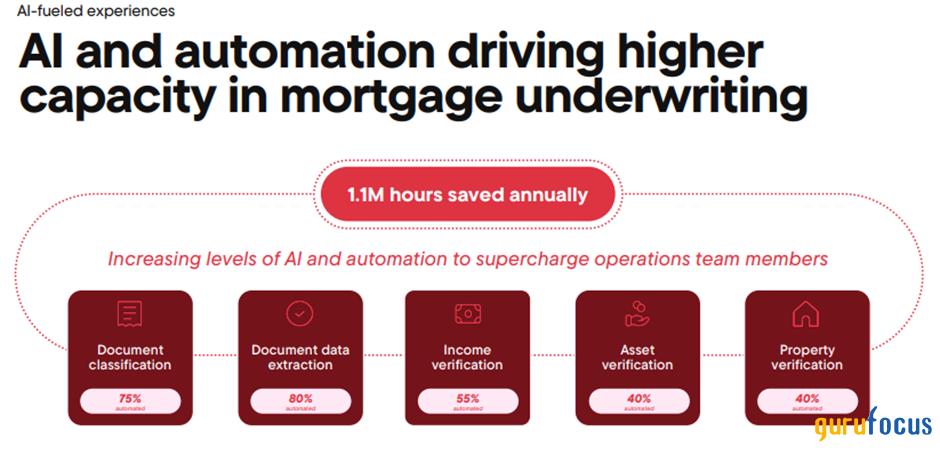

Beyond these headline acquisitions, Rocket has been busy organically expanding its offerings and cutting costs. The company has invested in technology and AI to streamline what has historically been a labor-intensive mortgage process. With a trove of over 14 petabytes of data from millions of client interactions, Rocket is training its AI models to personalize the homebuying journey and remove friction at each step. For example, Rocket highlighted that it's now using Agentic AI with Model Context Protocol (MCP) to automate tasks like verifying homebuyers' earnest money deposits. This now covers 80% of purchase agreements, saving nearly 20,000 hours annually. With Rocket AI, homebuyers spend less time answering questions and confirming details for mortgage bankers. The technology also helps give clients confidence by letting them know quickly, with certainty, if they are qualified for a mortgage, among other benefits. AI enables Rocket to handle spikes in volume (23x surges) without adding staff, which directly supports margin expansion as volumes recover.

Internally, Rocket also simplified its corporate structure in mid-2025 by collapsing the complex Up-C arrangement. Under the old structure, most of the operating company's earnings were attributed to Dan Gilbert and other insiders as non-controlling interest, leaving only a small slice of profit available to public shareholders. This often made Rocket's GAAP net income look artificially thin, even in strong quarters. With the Up-C collapse, Rocket Companies, Inc. now directly owns a larger share of the business, which makes earnings more transparent and better aligned with the performance of the underlying operations.

Rocket's reinvention is developing, but the housing market is still tough because homes are expensive for buyers. Mortgage rates remain anchored near 7%, and the knock-on effect is captured by the National Association of Realtors' Housing Affordability Index. For the third month in a row, in July, the national index came out below 100, meaning the median family does not earn enough to qualify for a median-priced home. There were 1.55 million homes for sale at the end of July, an increase of 15.7% from the same month last year, pushing inventory to its highest level since May 2020. More inventory is clearly putting pressure on prices, with the price index falling for the third month in a row. The latest signals that the market is slowly shifting in favor of buyers.

However, it is still a difficult environment, but Rocket is navigating it. In the second quarter of 2025, the company generated $1.34 billion in adjusted revenue, up 9% year-over-year (YoY) despite the tough climate. Closed loan originations were $29.1 billion, up 18% from the prior year's quarter, and net rate lock volume also rose by 13% to $28.4 billion. Adjusted EBITDA was $172 million, down from $225 million a year ago, while non-GAAP EPS was 0.04. Despite the higher revenue YoY, GAAP net income turned negative due to one-time transaction costs tied to the Redfin and Mr. Cooper deals.

The gain-on-sale margin (essentially the profit margin on selling mortgages) was just 2.8% in Q2, down 19 basis points (bps) from a year ago. Higher funding costs and intense competition for limited volume have compressed margins across the industry.

One silver lining of high rates has been Rocket's growing servicing income. Rocket's own servicing portfolio stood at $609 billion in unpaid principal across 2.8 million loans. Home equity loan volume nearly doubled YoY because homeowners are postponing refinancing as they don't want to lose their low old mortgage rates. This means Rocket continues earning servicing fees on them for longer. Once Mr. Cooper's $1.56 trillion servicing book is added, this cushion will become a huge pillar of Rocket's revenue. The company has finished the quarter with a strong liquidity position, with $9.1 billion in total, including over $5 billion in cash and cash equivalents.

It's also worth noting that the Redfin acquisition raised scrutiny from senators, who warned about potential price increases for households and misuse of consumer data. Still, the regulatory deadline expired without challenge, and the Trump administration allowed the merger to proceed. While political and antitrust risks remain, Rocket has so far cleared that hurdle.

Looking Ahead

Rocket's future now turns on executing this vision. As it stands, Rocket appears to be slightly expensive after the recent rally. The price-to-earnings (P/E) ratio is currently useless as the company is unprofitable over the trailing twelve months (TTM). The price-to-sales (P/S) ratio is at 0.96x after bottoming below 0.5x at the beginning of the year and the price to book is currently around 5.2x.

Source: Gurufocus

This is partly a math quirk (earnings are depressed at the cycle's trough), but it feeds the bear case that Rocket is expensive. The premium becomes clearer by looking at servicing portfolios, the most stable part of the business. Rocket's $40.8 billion market cap sits against $609 billion in servicing unpaid principal balance, which works out to about $6.70 of equity value for every $100 serviced. United Wholesale Mortgage ![]() UWMC, by comparison, trades closer to $4.60 per $100, while LoanDepot

UWMC, by comparison, trades closer to $4.60 per $100, while LoanDepot ![]() LDI is under $1. On that basis, Rocket is more expensive than its peers for similar servicing exposure. However, higher is not necessarily worse. Investors are already paying up for higher expectations, with Redfin at the front end, Mr. Cooper on the back end, and AI driving efficiencies. But this math changes dramatically once Mr. Cooper is folded in. The combined servicing portfolio would be about $2.17 trillion, dropping Rocket's market cap per $100 serviced from $6.70 today to just $1.88. That would leave Rocket trading well below UWM's $4.60 and closer to LoanDepot's $0.87, showing how the Redfin and Mr. Cooper deals can alter the valuation debate entirely.

LDI is under $1. On that basis, Rocket is more expensive than its peers for similar servicing exposure. However, higher is not necessarily worse. Investors are already paying up for higher expectations, with Redfin at the front end, Mr. Cooper on the back end, and AI driving efficiencies. But this math changes dramatically once Mr. Cooper is folded in. The combined servicing portfolio would be about $2.17 trillion, dropping Rocket's market cap per $100 serviced from $6.70 today to just $1.88. That would leave Rocket trading well below UWM's $4.60 and closer to LoanDepot's $0.87, showing how the Redfin and Mr. Cooper deals can alter the valuation debate entirely.

Still, the near-term environment is challenging. The company is unprofitable on a GAAP basis, and with the integration of Redfin, the costs will rise before the synergies start to kick in. In the third quarter, management expects an increase of $335 million in expenses, with roughly $275 million related to Redfin and $90 million in one-off costs from refinancing Mr. Cooper's debt.

The company is expecting sales to be between $1.6 and $1.75 billion, including Redfin or between $1.325 and $1.475 billion on a standalone basis. This means that for the next quarter, the company expects Redfin's accretive sales to be roughly offset by integration costs.

However, if we look forward, the picture could change dramatically. The acquisitions and initiatives underway are aimed at supercharging Rocket's earnings power in the coming years. In the first three weeks post Redfin close, 200,000 people clicked the pre-qualification button within Redfin, of those 23% became contactable leads and 12% started an application. Clients referred from Rocket to Redfin were 30% more likely to upgrade to verified approval letters. This suggests early revenue synergies may exceed the $60 million target management originally set, boosting forward earnings potential.

So, consider the pieces coming together. Once Mr. Cooper is absorbed, Rocket expects to obtain about $500 million in annual run-rate cost and revenue synergies from that deal alone. Redfin is expected to contribute another $200 million in synergies by 2027 through cost cuts and cross-selling. These will come from tangible areas like eliminating duplicate overhead, leveraging Rocket's tech at scale, and capturing more refinance recapture from that massive servicing portfolio. On top of that, Rocket's diversification means it can earn money in many ways. Origination fees, gain-on-sale, servicing fees, real estate commissions (via Redfin agents), and even subscription revenue (Rocket Money, their personal finance app).

And there are signs the cycle might have bottomed, and the macro should start to ease. The 30-year fixed-rate mortgage fell 15 bps in the 1st week of September, the largest weekly drop in the past year. Mortgage rates are headed in the right direction and homebuyers have noticed, as purchase applications posted their fastest YoY growth in more than four years. This comes as the Fed has already delivered its first 25 bps cut, with markets now expecting three more reductions over the next four meetings. And while the Fed moves act directly on the short end of the curve (not the 30-year mortgage benchmark), easier policy still helps the housing cycle indirectly. Rate cuts lower short-term borrowing costs for banks and investors, improve liquidity in credit markets, and often anchor long-term yields as expectations shift. That combination can gradually bring mortgage rates lower, unlocking affordability and giving players like Rocket more volume to capture.

It's also important to note that falling rates can put pressure on the value of mortgage servicing rights, since borrowers are more likely to refinance and escrow balances generate less income. That said, this trade-off is usually balanced by the lift in affordability and the increase in applications that come with lower borrowing costs.

Rocket's forward earnings (on an adjusted basis) are projected to rise significantly. Some analysts project non-GAAP EPS to grow from a current $0.20 to approximately $0.95 within the next two to three years, a five-fold improvement. If those estimates materialize and the company maintains current valuation multiples, the stock price could, in theory, follow a similar trajectory. Of course, this projection carries risks (the successful integration of Redfin and Mr. Cooper), but it highlights the potential disconnect between the company's current valuation and its future earnings power. The stock is not cheap on current multiples, but if earnings and synergies play out (even with some multiple compression) the return potential remains significant, making the long-term opportunity more compelling.

In a tough housing market, Rocket is performing better than expected, with early traction from Redfin integration and tangible efficiency gains from AI. The stock may appear pricey today, but investors are positioning for the next phase. That conviction was reflected in last quarter's guru activity, with smart money aligning with my take. Out of twelve disclosed transactions, nine were new buys or additions. The three reductions were minor, coming from relatively small holders. By contrast, the new and expanded positions were meaningful, with Renaissance Technologies (Trades, Portfolio), Steven Cohen (Trades, Portfolio), and Daniel Loeb (Trades, Portfolio) all opening fresh stakes, while First Eagle, ValueAct Capital (Trades, Portfolio), and VA Partners increased their exposure (with the latter two holding sizable allocations).

My Final Takeaway

Rocket has shown it can navigate the current housing cycle better than many expected. Moreover, the Redfin acquisition funnels new clients into the system at the start of their homebuying journey, with integration already showing early results. The Mr. Cooper acquisition will create a massive, stable servicing base that provides a constant source of future origination and recapture opportunities, regardless of market conditions. Finally, Rocket's in-house AI and fintech offerings create a sticky ecosystem that keeps customers engaged and monetizable over their lifetime. This approach completely changes the business. Despite the stock being pricey today, with the cycle turning and a more complete business in place, I believe Rocket offers a good opportunity.