Globe Life: Quietly Compounding at a Bargain Valuation

Introduction

Globe Life isn't a stock that grabs headlines or sparks debate on financial talk shows. It sells life and supplemental health insurance, compounds float, and buys back stock, quietly, consistently, and profitably. While the market chases volatility and innovation, Globe Life delivers something harder to find: reliability. At under 8x forward earnings and just over 1x tangible book, the company screens like a no-growth insurer. But beneath that surface is a capital-light business with 20%+ ROE, disciplined underwriting, and a multi-decade record of shareholder-friendly capital allocation.

Its embedded float model, where premiums are collected long before claims are paid, generates stable cash flow that fuels consistent buybacks. And while its business lacks glamour, its economics resemble those favored by the smartest value investors in the game.

History of Compounding

At its core, Globe Life is a cash-efficient, high-retention insurer built around three revenue engines: individual life insurance, supplemental health coverage, and investment income from float. But what separates it from most insurers isn't the product; it's the structure and discipline behind how it earns. Roughly 70% of Globe Life's underwriting income comes from individual life policies, many of which are sold directly to consumers. These policies are small, affordable, and sticky, exactly the kind of recurring revenue that compounds predictably over decades. Its other underwriting segments, including supplemental health insurance and accident coverage, offer higher margins and lower lapse rates than traditional health plans. Still, the real engine is floating, the premium dollars Globe Life collects long before it must pay out claims. That float is invested conservatively in high-grade bonds, contributing a steady stream of investment income that amplifies earnings without added risk.

This model is low-capital, high-margin, and relentlessly repeatable. Unlike property and casualty insurers exposed to catastrophic risks, Globe Life's book is built for stability, with mortality tables and premium structures dialed in over decades. Unlike newer fintech insurers prioritizing growth, Globe Life prioritizes cash generation and capital return, hallmarks of long-term value creation. Its underwriting margin consistently exceeds 20%, and its return on equity remains above 20% a signal that the economics of this model are still intact, even in a higher rate world.

Globe Life doesn't make headlines with flashy dividends or special distributions, but behind the scenes, its capital return strategy is among the most disciplined in the industry. Over the past five years, the company has returned over $4 billion to shareholders, largely through share repurchases that have quietly shrunk the outstanding share count by more than 25%. This isn't opportunistic timing or short-term engineering. Globe Life's buybacks are part of a long-term structural strategy. Management targets return on equity above 20%, and when reinvestment opportunities are limited, excess capital flows directly to repurchases, executed at valuations that enhance per-share value.

Dividends play a smaller but consistent role. The company has increased its dividend for 17 consecutive years, though the yield remains modest at around 1%, reflecting its focus on tax-efficient buybacks over headline payout ratios. What's notable is how quietly effective this return model has been. While competitors often chase growth through M&A or expansion into riskier lines, Globe Life's capital deployment is focused on a narrow, high-return niche, creating long-term compounding without taking on operational sprawl or financial complexity.

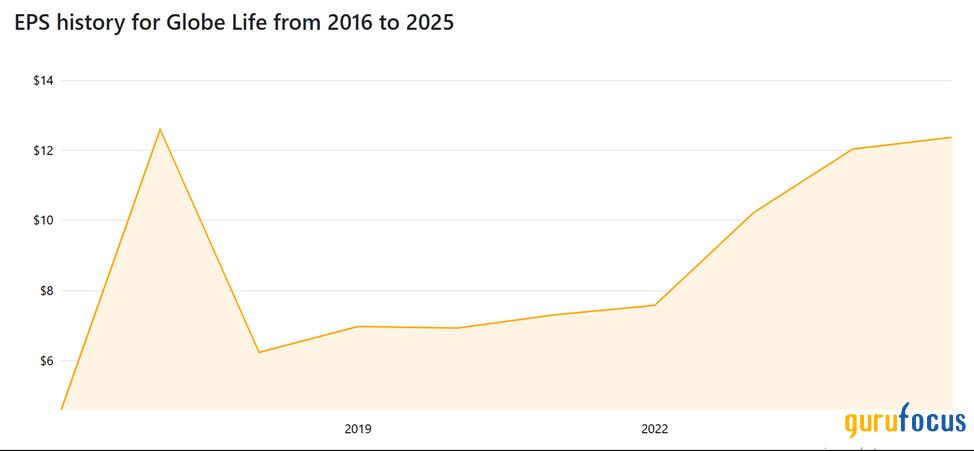

As a result, tangible book value per share has steadily grown, and earnings per share have compounded even in periods of flat top-line growth. This kind of internal efficiency is rare and often overlooked in favor of louder, less durable capital strategies.

Valuation vs Peers

On paper, Globe Life doesn't screen as expensive, but even that understates the opportunity. The stock trades at just ~7.8x forward earnings and ~1.1x tangible book, despite delivering a 20%+ return on equity and a consistent record of buybacks. Those metrics put it in a different league from most peers.

| Metric | Globe Life | MetLife | Prudential | Lincoln |

|---|---|---|---|---|

| Forward P/E | ~7.8x | ~10.5x | ~11.8x | ~5.9x |

| Price/Tangible Book | ~1.1x | ~1.3x | ~1.4x | ~0.5x |

| Return on Equity | ~20%+ | ~13% | ~12% | ~9% |

| Shareholder Yield | ~6.5% | ~5.9% | ~6.2% | ~4.3% |

While Lincoln appears cheaper on headline multiples, its lower ROE and volatile book value create a less predictable compounding base. MetLife and Prudential, by contrast, command premium valuations despite returns that trail Globe Life's by a wide margin. That valuation spread suggests investors are overlooking what matters: capital efficiency and consistency. Globe Life doesn't need double-digit top-line growth to deliver attractive returns. With its float-driven earnings model and disciplined capital return framework, the company quietly compounds per-share value year after year.

If Globe Life were to re-rate to the average P/E of its peers (around 1012x), the stock could see 2540% upside from current levels, without needing any improvement in earnings or fundamentals.

Who is buying?

Richard Pzena (Trades, Portfolio), founder of Pzena Investment Management and a well-known deep value investor, owns nearly 941,000 shares of Globe Life, worth over $120 million. Despite a slight trim this past quarter, Pzena's long-standing position and average cost of $95.08 suggest a high-conviction view that the stock's intrinsic value far exceeds its current multiple. His firm typically targets companies with strong free cash flow, temporarily depressed sentiment, and long-term earnings visibility, traits that define Globe Life's business model.

Meanwhile, George Soros's (Trades, Portfolio) fund recently increased its position by nearly 87%, signaling fresh conviction at current prices. Though not a core holding, this kind of aggressive increase at an average cost of $114.71 reflects a belief in the company's defensive value and consistent capital return profile, particularly in an uncertain macro environment.

Cliff Asness' AQR Capital, a quantitative value powerhouse, also added nearly 160,000 shares in the last quarter, bringing their total to over 700,000 shares. For a fund that relies heavily on valuation screens and return on equity metrics, Globe Life fits the profile, with high ROE, stable margins, and a low-multiple entry point.

These aren't speculative trades; their long-horizon positions are built on real fundamentals. The fact that multiple strategy types, quantitative, fundamental deep value, and macro, are converging on Globe Life suggests a broader recognition of its structural mispricing.

Investor Considerations

Globe Life isn't without risks; no insurer is. Macroeconomic downturns can slow policy sales, rising interest rates can pressure investment returns, and tighter regulation may raise costs or limit underwriting flexibility. But unlike many of its peers, Globe Life has built its entire model to weather such pressures. It maintains a conservative, long-duration debt profile with minimal near-term maturities and consistently exceeds CET1 capital ratios above 13%, ensuring financial resilience.

More importantly, the market is already pricing in these risks. Globe Life trades at just ~7.8x forward earnings and ~1.1x tangible book, even while generating a 20%+ return on equity. Those are the kind of multiples typically reserved for structurally challenged businesses, not for high-margin, capital-light insurers with multi-decade histories of compounding.

Its shareholder base further reinforces this disconnect. Some of the most respected investors in the world, including Richard Pzena (Trades, Portfolio), George Soros (Trades, Portfolio), and AQR Capital, have built long-horizon positions in Globe Life, signaling conviction that the company is fundamentally mispriced. In a market obsessed with growth narratives and flash, Globe Life remains quiet, stable, and relentlessly efficient. It doesn't need a turnaround, a new product launch, or macro tailwinds. All it needs is recognition.