Boston Beer is back to growth !

After a tumultuous 5 years which saw bubble highs and new lows, premium brewer Boston Beer Co. ![]() SAM now looks like it's got its groove back. Boston Beer has carved out a economic moat based on its brands, strong distribution and leadership in on-trend alcoholic categories like malted beverages, hard seltzer and ciders and premium beers.

SAM now looks like it's got its groove back. Boston Beer has carved out a economic moat based on its brands, strong distribution and leadership in on-trend alcoholic categories like malted beverages, hard seltzer and ciders and premium beers.

Here are the top five Boston Beer Company brands, organized by category:

- Beer: Samuel Adams The flagship craft beer line, featuring Boston Lager, seasonal releases, and specialty brews.

- Malt Beverage: Twisted Tea A popular hard iced tea malt beverage available in a variety of flavors and alcohol strengths.

- Hard Seltzer: Truly A leading hard seltzer brand with a wide range of fruit flavors.

- Hard Cider: Angry Orchard A well-known hard cider brand offering both classic and seasonal varieties.

- Vodka-Based Ready-to-Drink (RTD): Sun Cruiser A ready-to-drink hard iced tea and lemonade made with real brewed tea and premium vodka.

These brands showcase Boston Beer's most prominent offerings across beer, malt beverages, hard seltzers, hard cider, and ready-to-drink cocktails.

Boston has recently launched a new product under the brand Sun Cruiser; it is a vodka spiked iced tea made with real brewed tea and premium vodka. It contains no malt or malted grains, but instead combines iced tea or lemonade with vodka, resulting in a gluten-free, 4.5% ABV alcoholic drink with a smooth, refreshing taste and a hint of sweetness. The launch is showing good results.

Boston Beer Company's notable acquisitions include Dogfish Head Brewery in 2019 and the Oregon Ale and Beer Company in 1997. The Dogfish Head deal, valued at around $300 million, was intended to combine two innovative craft brewers and strengthen Boston Beer's position in the craft segment, but it has been financially disappointing due to repeated impairment charges and underperformance relative to expectations. The Oregon Ale and Beer Company acquisition in 1997 helped Boston Beer expand its production capacity and market reach, supporting its national growth at the time. Beyond these, Boston Beer has focused more on organic growth and partnerships, such as its current collaboration with PepsiCo for HARD MTN DEW, rather than a series of high-profile acquisitions. Overall, while the Oregon Ale and Beer Company acquisition supported operational expansion, the Dogfish Head acquisition has not delivered the anticipated financial success.

Trading near 5 year lows

I became interested in Boston Beer for two reasons. It recently showed up on a screen close to 52-week lows and 5 year lows. As you can see the stock went into a huge bubble during the pandemic which burst in recent years. As busts typically do, the price may have fallen more than justified hence creating a value opportunity.

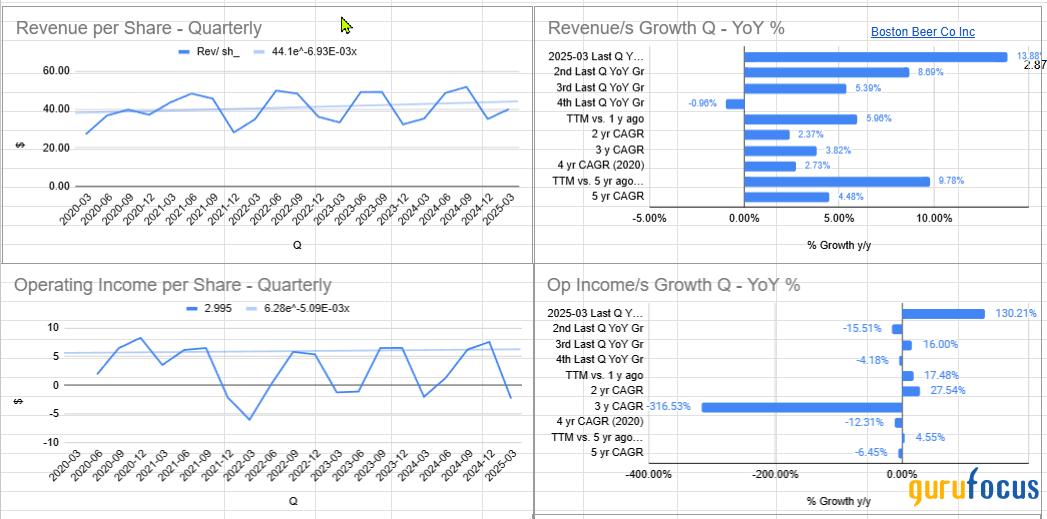

Recovery in Revenue and Operating income

The company is showing recovery in both revenue per share and operating income per share. This dynamic is evident in the charts given below and constants with the price action. My rule of thumb is that I want to see actual improvement in revenue per share and operating income per share on a TTM basis as well in at least two of the last four most recent quarters. The results given below meets my rule of thumb criteria. This gives me some confidence that the business is turning around.

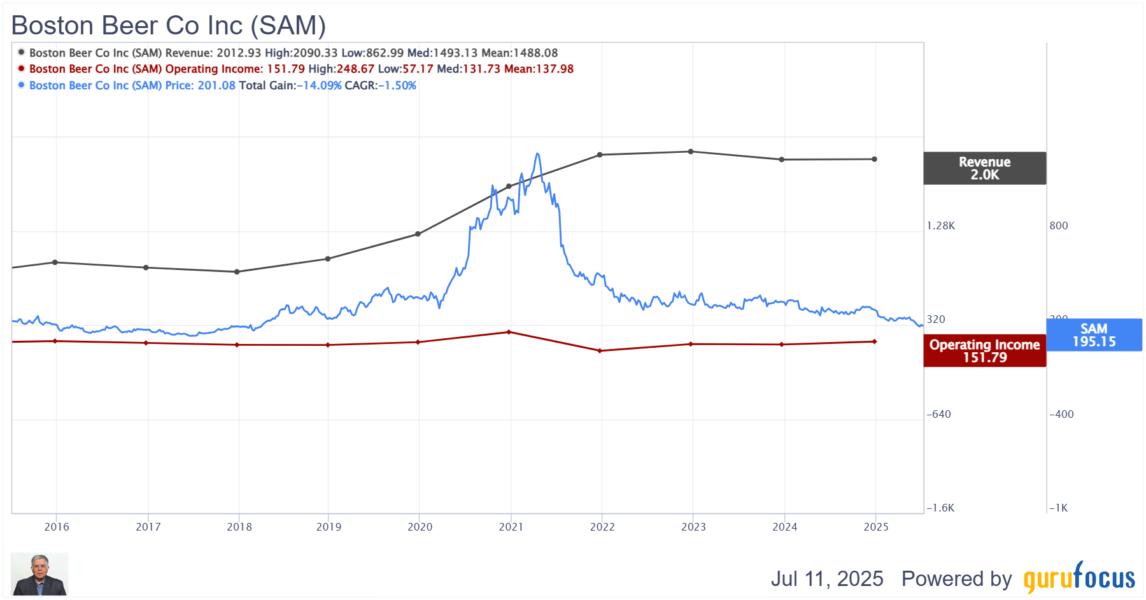

The following 10 year annual chart also shows that revenue has held up pretty well and operating income is now recovering.

SAM Data by GuruFocus

Valuation

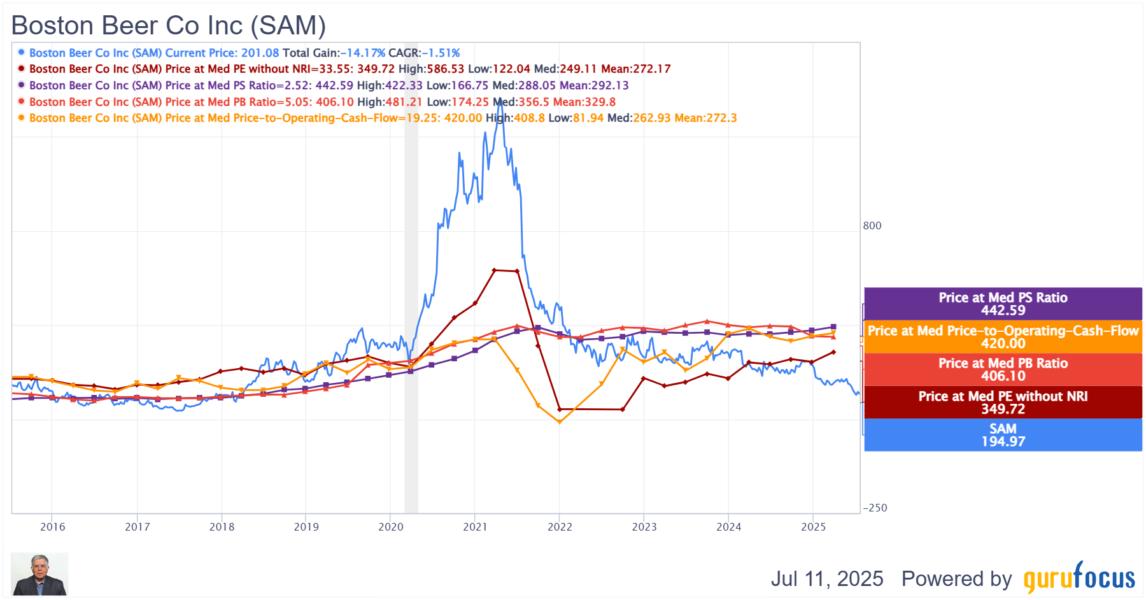

The company's current price ratio's are much lower than its 10 year median price ratio's across the board indicating significant undervaluation compared to recent history.

| Price Ratio's - Current | 10 yr median Price Ratio's | ||

| PE Ratio without NRI | 18.73 | PE Ratio (10y Median) | 38.39 |

| PS Ratio | 1.1 | PS Ratio (10y Median) | 2.52 |

| PB Ratio | 2.43 | PB Ratio (10y Median) | 5.01 |

| Price-to-Operating-Cash-Flow | 8.93 | Price-to-Operating-Cash-Flow (10y Median) | 19.32 |

| EV-to-Forward-EBITDA | 8.62 | EV-to-EBITDA (10y Median) | 18.77 |

SAM Data by GuruFocus

Boston Beer has also being buying back stock at a feverish pace which indicates the company realizes that the stock is undervalued.

Competitive Analysis

These companies compete with Boston Beer across various categories, including traditional beer, hard seltzer, hard tea, cider, and innovative ready-to-drink products. Boston Beer's EV/EBITDA compares favorably to its peers but note that it is much smaller than the global brewers like Anheuser=Busch and Heineken.

| Ticker | Company | Market Cap ($M) | Operating Margin % | Operating Margin % (10y Median) | 10-Year Revenue Growth Rate (Per Share) | 10-Year Operating Income Growth Rate (Per Share) | EV-to- EBITDA | EV-to-Forw ard-EBITDA |

| SAM | Boston Beer Co Inc | 2,173.25 | 8.32 | 11.69 | 12.40 | -0.70 | 7.98 | 8.62 |

| HEINY | Heineken NV | 49,591.77 | 11.69 | 13.29 | 4.40 | 1.80 | 12.45 | 9.02 |

| DEO | Diageo PLC | 57,758.90 | 28.90 | 29.42 | 6.40 | 7.30 | 11.98 | 8.47 |

| STZ | Constellation Brands Inc | 30,355.96 | 31.69 | 30.20 | 6.10 | 8.60 | 92.27 | 11.02 |

| TAP | Molson Coors Beverage Co | 10,119.19 | 15.04 | 13.69 | 10.30 | 13.90 | 6.65 | 6.52 |

| BUD | Anheuser-Busch InBev SA/NV | 131,556.14 | 25.62 | 27.64 | 1.40 | -1.20 | 13.50 | 9.03 |

Another issue to note is Boston Beer's relatively lower operating margin as compared to its bigger peers. This is likely due to its higher marketing spend as a percentage of revenue. Gross Margins are also lower due to lower volume. The following table provides U.S. Market Share and estimate volume of beer sold.

| Company | U.S. Market Share (2023) | Estimated U.S. Beer Volume (Barrels, 2023) | Notes |

|---|---|---|---|

| AB InBev (Budweiser) | 34% | ~65.3 million | Industry leader, 2x larger than Molson Coors |

| Molson Coors (TAP) | 22% | ~42.2 million | Clear #2 in U.S. market |

| Constellation (STZ) | 15% | ~28.8 million | Strong, rapidly growing portfolio (Corona, Modelo) |

| Heineken | Not top 10 (no official share listed) | N/A, but likely <1% of U.S. volume | Major global player, but U.S. share is minor |

| Boston Beer | 4% | ~7.7 million | Largest craft brewer, but much smaller than big three. |

Ownership

Boston Beer Company is controlled by its founder, Jim Koch, through ownership of all the company's Class B Common Stock, which carries full voting rights. While the company's Class A shares are publicly traded under the ticker "SAM," these shares do not have voting rights, so public shareholders and institutional investorsincluding major holders like Vanguard, BlackRock, and Fidelitydo not control the company's governance. In addition to Jim Koch, Sam Calagione, co-founder of Dogfish Head (acquired by Boston Beer in 2019), is a significant non-institutional shareholder. However, ultimate control remains with Koch due to his exclusive ownership of voting shares.

Guru investors holding this stock include Ken Fisher (Trades, Portfolio), Steven Cohen (Trades, Portfolio), Mason Hawkins (Trades, Portfolio). However they hold relatively minor positions.

Conclusion

Boston Beer Company is a leading U.S. craft beverage producer best known for its flagship Samuel Adams beer, as well as Twisted Tea, Truly Hard Seltzer, and Angry Orchard cider, among others. The company has a reputation for innovation, quickly expanding into new beverage categories such as hard seltzer, ready-to-drink cocktails, and most recently, cannabis-infused beverages in Canada. Its diversified brand portfolio allows it to adapt to changing consumer preferences, with products ranging from traditional beer to non-alcoholic and cannabis beverages.

Despite its strong brand recognition and history of revenue growth, Boston Beer has faced significant share price volatility and underperformance in recent years. Over the past five years, the stock has declined sharply, with a 62% drop, including a 30% decrease in the last year alone. This poor stock performance stands in contrast to steady revenue growth and improving profitability, suggesting that market sentiment may be more negative than the company's fundamentals warrant. The company's price-to-earnings ratio is relatively high, reflecting expectations for future growth, but also highlighting the risk if growth does not accelerate.

Boston Beer's recent financial results have been mixed. While it reported strong quarterly earnings and revenue growth driven by product innovation and increased shipments, some core brands, such as Twisted Tea, have struggled with volume growth. The company's strategic investments in advertising and new product lines, including cannabis beverages, indicate a focus on long-term growth and diversification, but these initiatives come with execution risk.

Analyst sentiment on the stock is generally neutral, with most rating it a Hold and price targets suggesting potential for recovery if the company can deliver consistent results. Boston Beer is currently debt free, marking a significant improvement from five years ago when the company had a debt to equity ratio of 13%. With no outstanding debt, SAM does not require operating cash flow to cover debt obligations, and interest coverage is not a concern since there are no interest payments to manage. This strong financial position reflects effective debt reduction and prudent financial management. It gives the company flexibility to pursue growth projects.

Boston Beer Co Inc has experienced long-term declines in both gross margin and operating margin, with gross margin falling at an average annual rate of 2.1% and operating margin declining by 10.8% per year over the past five years. Despite these margin pressures, the company demonstrates several financial strengths: it maintains comfortable interest coverage with enough cash to cover all debt, a low likelihood of earnings manipulation according to its Beneish M-Score, and valuation ratios (PB, PE, and PS) that are close to multi-year lows, suggesting the stock may be attractively priced. Revenue per share has shown consistent growth, and the company's financial strength is underscored by a strong Altman Z-score and a robust balance sheet. Overall, Boston Beer is low risk, with solid fundamentals and characteristics that support a long-term holding perspective.

In summary, Boston Beer's qualitative outlook reflects a well-managed, innovative company with strong brands and a healthy balance sheet, but also one facing market skepticism due to recent stock underperformance and mixed results across its portfolio. Success will depend on its ability to drive growth in emerging categories and revitalize its core brands in a competitive and evolving beverage market.