Wily courtroom financiers demand wilier reforms

The marketization of everything continues apace. The business of bankrolling U.S. lawsuits for a slice of the winnings has, improbably, grown into an $18 billion industry, according to legal researcher Chambers and Partners. Skeptical legislators have taken notice, coming just short of slapping a 32% tax on proceeds from such transactions. Should the proposal resurface, it may simply move litigation finance offshore.

Institutionalized gambling on courtroom outcomes, despite the unseemly appearance, offers one of the great prizes for active investors: returns totally uncorrelated to the broader market. The great mass of people, corporations and countries seeking their day before a judge are, in this view, an untapped well of possible investments. Major litigation funder Burford Capital runs more than $7 billion in assets, while Softbank-owned Fortress Investment Group has pumped $6.8 billion into cases worldwide. Typically, funders advance money to cover legal costs in exchange for a share, typically 20% to 40%, of any eventual settlement or judgement.

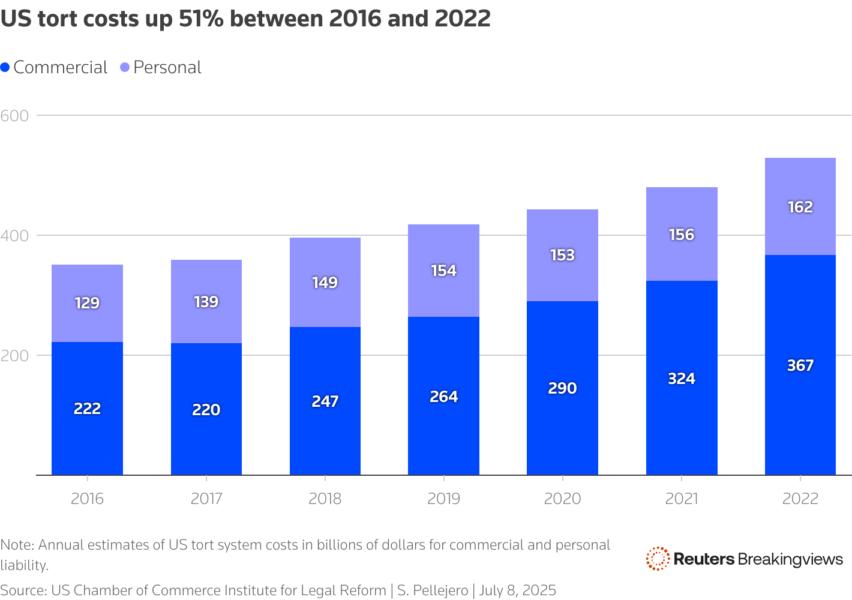

Standing across from them are legal liability insurers. Tort costs — that is, the overall bill for lawsuits — rose 7% a year between 2016 and 2022, reaching $529 billion, says the U.S. Chamber of Commerce’s Institute for Legal Reform. Policy providers responded with hiked premiums and skimpier coverage. Major underwriters like Chubb and Hartford Insurance Group ![]() HIG have seen their stocks match or outperform the S&P 500 Index

HIG have seen their stocks match or outperform the S&P 500 Index ![]() SPX every year since 2015.

SPX every year since 2015.

The argument against litigation finance is that dangling rewards for putting more ammo behind lawsuits will exacerbate this dynamic by encouraging frivolous claims and creating conflicts of interest between funders and plaintiffs, who may value risk and reward differently. Certainly, the reason to propose taxing the practice wasn’t the revenue: the Congressional Budget Office projected that Republicans’ proposed levy, stripped by arcane Senate rules at the last minute, would have raised $8.8 billion over the next decade, equal to less than .01% of federal spending.

Whether it would have even stopped financiers is unclear. By establishing off-shore special-purpose vehicles in the Caymans and characterizing profits as capital gains, for instance, the Internal Revenue Service could perhaps be outfoxed. Indeed, foreign capitals may become more welcoming: in the UK, a public body recommended reversing a court ruling that prevented funders from claiming winnings.

For more durable reforms, look at the Netherlands, which okays externally funded class action suits so long as the backer stays at arm’s length from plaintiffs. In Ontario, weak class actions get tossed early thanks to stricter approval tests and fast-track dismissal hearings. The best approach is to tweak what has already become a market, not to play whack-a-mole with the returns.

Follow Sebastian Pellejero on LinkedIn.

CONTEXT NEWS

Senate Republicans had proposed a 31.8% tax on litigation finance loan proceeds, along with rules barring funders from offsetting gains with losses and removing tax shields for exempt organizations backing these deals.

However, these measures were removed from recently passed tax-and-spending legislation after the Senate parliamentarian ruled that they did not comply with budget reconciliation rules.