An $18 bln health deal faces risks outside the lab

It’s one thing carefully assembling a complex deal in the lab. Taking it out into the real world, especially for healthcare companies facing new risks, is another thing entirely. Medical analysis equipment maker Waters on Monday agreed to combine with a unit of Becton Dickinson in a $17.5 billion deal that spares a tax bill and comes in at a cheap price — one that gets even better if promised cost and revenue synergies emerge. Snag is, it’s a big combination that adds debt and comes just as U.S. government cuts are hitting researchers.

There’s little reason for BD, sporting a market value of $50 billion, to retain its biosciences and diagnostics business. By pairing it off with Waters, the company can focus on its core line of selling products for surgery and devices to deliver medicine, which has enjoyed a boost thanks to demand for pre-filled syringes for GLP-1 weight loss drugs, even despite multiple recalls of infusion pumps.

The unit was also able to win a premium to BD's own drab valuation, even if it was far from a knock-out price. Unusually for a so-called reverse Morris trust transaction, under which the subsidiary will be spun out and then merged, Waters will gain majority ownership. It is paying about 5 times estimated 2025 revenue of $3.4 billion to do so. That’s about 20% less than peer Danaher’s multiple, and nearly 30% below Waters’ own.

By combining, Waters thinks it can cut $200 million of costs in three years. Taxed and capitalized, that’s offers perhaps $1.6 billion of value split between the buyer’s 61% stake and BD shareholders’ 39% post-deal ownership. Waters also promises $290 million of profit boosts from increased sales, though says these might take five years to realize. While they nudge the effective price further down, the cost savings aren’t huge and promises of additional revenue have a way of going awry.

The risk to the buyer is two-fold. First, the $21 billion valued Waters will now become much more complex, more than doubling revenue. Second, it is aggressively scaling up — taking on $4 billion of new debt to do so — just as the U.S. government is slashing funding for basic research. While BD’s subsidiary has a diagnostics business that should be unperturbed, some 45% of its revenue in 2024 came from biosciences, which may well be affected.

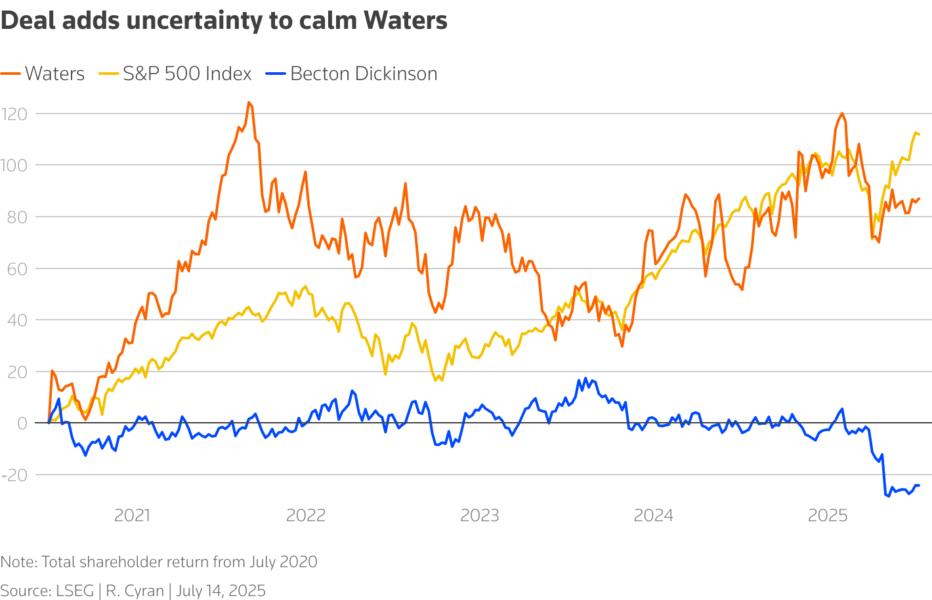

That danger may explain why shareholders sent Waters’ stock price down 12% on Monday morning. No matter the careful engineering, there’s always a chance of unexpected adverse reactions.

Follow Robert Cyran on Bluesky.

CONTEXT NEWS

Laboratory equipment company Waters said on July 14 that it would merge with Becton, Dickinson and Company’s Biosciences & Diagnostic Solutions unit in a transaction valued at $17.5 billion. The tax-free combination will see the BD unit spun off to shareholders and merged with a wholly owned subsidiary of Waters.

BD shareholders will own about 39% of the combined company, while existing Waters shareholders will own about 61%. Becton will also receive $4 billion in cash, subject to adjustments, while Waters is expected to assume approximately $4 billion of incremental debt.