OPEN-SOURCE SCRIPT

已更新 Pocket Pivot with extrapolated Volume and Moving Averages

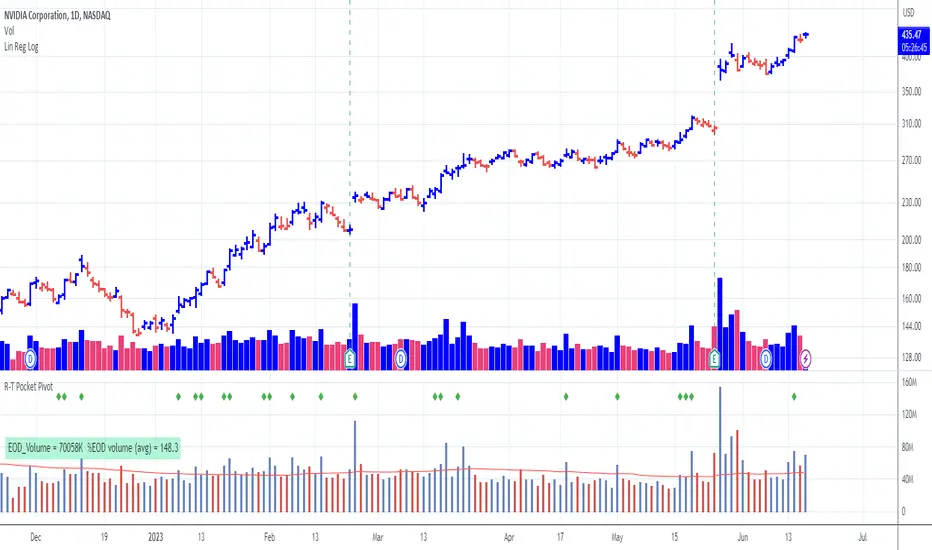

The script shows historical pocket pivots, much as other scripts with a green diamond shape on the volume pane.

When the market is open, the current bar, however, is extrapolated to the end of the day using a sixth-order polynomial.

Thus real-time pocket pivots are shown. To work properly, the user must input a time-zone offset parameter; the default is west coast USA.

Time-zone offset is -12 hours to +12 hours compared to the NYSE exchange time zone (USA west coast: -3.)

The volume extrapolation polynomial is based on a historical NASDAQ intraday volume model developed locally by a team.

Only ten-day lookback pocket pivots are computed as defined initially by Dr. Chris Kacher. (The default lookback can be changed by the user.)

Only pocket pivots are shown where the low of the daily bar is within user-defined proximity to the 50-day moving average or 10-day moving average (for continuation pocket pivots.)

When the market is open, the current bar, however, is extrapolated to the end of the day using a sixth-order polynomial.

Thus real-time pocket pivots are shown. To work properly, the user must input a time-zone offset parameter; the default is west coast USA.

Time-zone offset is -12 hours to +12 hours compared to the NYSE exchange time zone (USA west coast: -3.)

The volume extrapolation polynomial is based on a historical NASDAQ intraday volume model developed locally by a team.

Only ten-day lookback pocket pivots are computed as defined initially by Dr. Chris Kacher. (The default lookback can be changed by the user.)

Only pocket pivots are shown where the low of the daily bar is within user-defined proximity to the 50-day moving average or 10-day moving average (for continuation pocket pivots.)

發行說明

Original script incorrectly computed end of trading day and beginning of trading day by subtracting the timezone offset from the NYSE market time.The corrected script adds the timezone offset to correctly use that term.

發行說明

The prior indicator applied extrapolation to volume on weekends: this is not proper. Added line to test if the market is closed (session.ismarket ==false).Also tweaked the lineWidth default value to equal 4.

發行說明

Modified method to turn off extrapolation on weekends by testing if dayofweek(time) == dayofweek.saturday or dayofweek.sunday.Erroneously extrapolating volume on weekends has been a bug since the beginning and it has taken me time to learn of the above test. The remaining hole in the strategy are market holidays and short trading sessions. I do not have a method for this.

發行說明

Removed requirement for setting local time zone offset發行說明

Yet again getting the extrapolation disabled on weekends. My errors.發行說明

Yet again trying to disable the extrapolation function on weekends...發行說明

Minor cleanup. I noticed that the extrapolation wasn't working at a time when the market was open. The volume extrapolation is supposed to work when the market is open.發行說明

Added test for chart timeframe. Volume extrapolation is only valid on daily charts. Extrapolation is disabled for other timeframes. 2023-06-16開源腳本

本著TradingView的真正精神,此腳本的創建者將其開源,以便交易者可以查看和驗證其功能。向作者致敬!雖然您可以免費使用它,但請記住,重新發佈程式碼必須遵守我們的網站規則。

免責聲明

這些資訊和出版物並不意味著也不構成TradingView提供或認可的金融、投資、交易或其他類型的意見或建議。請在使用條款閱讀更多資訊。

免責聲明

這些資訊和出版物並不意味著也不構成TradingView提供或認可的金融、投資、交易或其他類型的意見或建議。請在使用條款閱讀更多資訊。