INVITE-ONLY SCRIPT

已更新 RS++ High Beta Majors Allocation | viResearch

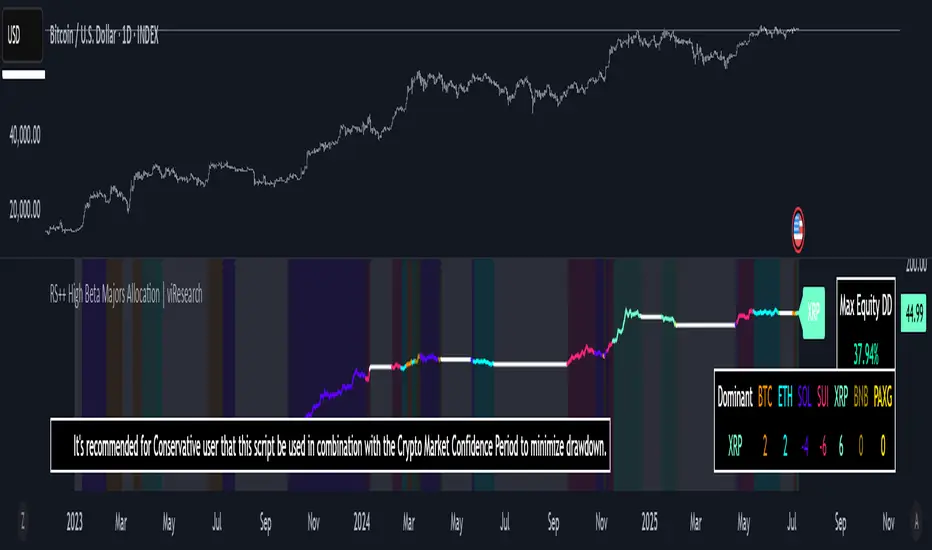

RS++ High Beta Majors Allocation | viResearch

Conceptual Foundation and Innovation

The "RS++ High Beta Majors Allocation" is a next-generation portfolio rotation algorithm designed to capture alpha from high-volatility (high-beta) crypto assets. Building on the RS+ framework, this strategy expands the asset pool beyond BTC, ETH, and SOL to include newer and more volatile contenders like SUI and XRP. The goal is to rotate dynamically among these five majors—allocating to the strongest trending asset while minimizing exposure during broad-market weakness.

The strategy introduces enhanced comparative scoring using a multi-layered relative strength matrix that accounts for cross-asset momentum in real-time. Combined with a regime-based trend filter, it adapts not only to market leadership but also to prevailing risk conditions, significantly improving capital efficiency over traditional buy-and-hold strategies.

Technical Composition and Calculation

At the heart of the RS++ model lies a sophisticated five-asset ratio matrix. Each asset is evaluated against the others using relative price ratios, and each pair is scored through a hybrid strength model based on universal trend filters and statistical thresholds.

Expanded Universe: The script evaluates BTC, ETH, SOL, SUI, and XRP—each chosen for their liquidity and volatility profile, enhancing the potential for outperformance.

Relative Strength Matrix: A 5x5 matrix compares all assets against one another to determine momentum dominance. The asset with the highest cumulative score is considered the dominant major.

Trend Regime Filter: Before allocation, both the market regime (via BTC or a custom source) and the individual asset must pass trend confirmation to qualify for inclusion, reducing whipsaw exposure.

Equity Tracking: A real-time system equity line tracks portfolio performance from a custom user-defined start date.

Drawdown Measurement: Maximum drawdown is computed in real-time to assess risk exposure.

Performance Metrics

The script measures key quantitative metrics to evaluate performance robustness:

Max Drawdown: Assesses capital risk and largest equity dip from peak to trough.

Sharpe/Sortino/Omega Ratios (optional in previous versions): Can be adapted for future inclusion.

ROC-Based Returns: Allocation logic and equity growth are tied to ROC (rate of change), making it highly responsive to price action.

User Interface and Features

This version introduces user-centric customization and quality-of-life improvements:

Asset Toggle via Tickers: Simply switch any ticker to "USDT" to exclude it from the rotation universe.

Equity Chart Overlay: Real-time equity plotted with color-coded trend backgrounds for easy interpretation of active holdings.

Dominant Asset Panel: A dashboard displays the currently allocated asset and scores of all assets for comparative insights.

Usage Recommendation: The script includes an embedded suggestion to pair this strategy with the Crypto Market Confidence Period indicator for even better macro-filtering.

Timeframe Guardrail: A soft enforcement feature suggests usage on the 1D timeframe for optimal accuracy.

Practical Applications

This strategy is ideal for traders who prefer a tactical, risk-managed approach to high-beta crypto portfolios. Use cases include:

Active Rotation Management: Switches capital between the strongest trending assets to capture momentum across cycles.

Macro Regime Sensitivity: The trend filter avoids allocation during weak macro trends, moving to cash and preserving equity.

High-Volatility Environments: Particularly effective in bull phases or during sector rotations where traditional assets underperform.

Strategic Value and Advantages

The RS++ script blends alpha-generation with institutional-level risk filtering, making it a powerful tool for active portfolio managers. The expanded universe allows for exposure to emerging market leaders while the scoring and filtering mechanism ensures trades are made with precision. Real-time equity visualization and intuitive alerts help traders stay aligned with system output without constant screen-watching.

Summary and Usage Tips

The "RS++ High Beta Majors Allocation" script offers a versatile and powerful method for crypto portfolio allocation with an emphasis on dynamic strength, risk control, and adaptability. Traders are encouraged to:

* Use the recommended 1D timeframe for stability.

* Pair the strategy with macro filters like the Crypto Market Confidence Period.

As always, backtest thoroughly and remember that no model guarantees future performance. Use this tool as part of a broader risk-managed trading framework.

Conceptual Foundation and Innovation

The "RS++ High Beta Majors Allocation" is a next-generation portfolio rotation algorithm designed to capture alpha from high-volatility (high-beta) crypto assets. Building on the RS+ framework, this strategy expands the asset pool beyond BTC, ETH, and SOL to include newer and more volatile contenders like SUI and XRP. The goal is to rotate dynamically among these five majors—allocating to the strongest trending asset while minimizing exposure during broad-market weakness.

The strategy introduces enhanced comparative scoring using a multi-layered relative strength matrix that accounts for cross-asset momentum in real-time. Combined with a regime-based trend filter, it adapts not only to market leadership but also to prevailing risk conditions, significantly improving capital efficiency over traditional buy-and-hold strategies.

Technical Composition and Calculation

At the heart of the RS++ model lies a sophisticated five-asset ratio matrix. Each asset is evaluated against the others using relative price ratios, and each pair is scored through a hybrid strength model based on universal trend filters and statistical thresholds.

Expanded Universe: The script evaluates BTC, ETH, SOL, SUI, and XRP—each chosen for their liquidity and volatility profile, enhancing the potential for outperformance.

Relative Strength Matrix: A 5x5 matrix compares all assets against one another to determine momentum dominance. The asset with the highest cumulative score is considered the dominant major.

Trend Regime Filter: Before allocation, both the market regime (via BTC or a custom source) and the individual asset must pass trend confirmation to qualify for inclusion, reducing whipsaw exposure.

Equity Tracking: A real-time system equity line tracks portfolio performance from a custom user-defined start date.

Drawdown Measurement: Maximum drawdown is computed in real-time to assess risk exposure.

Performance Metrics

The script measures key quantitative metrics to evaluate performance robustness:

Max Drawdown: Assesses capital risk and largest equity dip from peak to trough.

Sharpe/Sortino/Omega Ratios (optional in previous versions): Can be adapted for future inclusion.

ROC-Based Returns: Allocation logic and equity growth are tied to ROC (rate of change), making it highly responsive to price action.

User Interface and Features

This version introduces user-centric customization and quality-of-life improvements:

Asset Toggle via Tickers: Simply switch any ticker to "USDT" to exclude it from the rotation universe.

Equity Chart Overlay: Real-time equity plotted with color-coded trend backgrounds for easy interpretation of active holdings.

Dominant Asset Panel: A dashboard displays the currently allocated asset and scores of all assets for comparative insights.

Usage Recommendation: The script includes an embedded suggestion to pair this strategy with the Crypto Market Confidence Period indicator for even better macro-filtering.

Timeframe Guardrail: A soft enforcement feature suggests usage on the 1D timeframe for optimal accuracy.

Practical Applications

This strategy is ideal for traders who prefer a tactical, risk-managed approach to high-beta crypto portfolios. Use cases include:

Active Rotation Management: Switches capital between the strongest trending assets to capture momentum across cycles.

Macro Regime Sensitivity: The trend filter avoids allocation during weak macro trends, moving to cash and preserving equity.

High-Volatility Environments: Particularly effective in bull phases or during sector rotations where traditional assets underperform.

Strategic Value and Advantages

The RS++ script blends alpha-generation with institutional-level risk filtering, making it a powerful tool for active portfolio managers. The expanded universe allows for exposure to emerging market leaders while the scoring and filtering mechanism ensures trades are made with precision. Real-time equity visualization and intuitive alerts help traders stay aligned with system output without constant screen-watching.

Summary and Usage Tips

The "RS++ High Beta Majors Allocation" script offers a versatile and powerful method for crypto portfolio allocation with an emphasis on dynamic strength, risk control, and adaptability. Traders are encouraged to:

* Use the recommended 1D timeframe for stability.

* Pair the strategy with macro filters like the Crypto Market Confidence Period.

As always, backtest thoroughly and remember that no model guarantees future performance. Use this tool as part of a broader risk-managed trading framework.

發行說明

Update | changing alert name 發行說明

update| added option to turn off Drawdown table發行說明

Update | added BNB, PAXG. also reduce the number of indicators used to just one發行說明

update| UI發行說明

update| added PAXG alert, sorry發行說明

update| name error 發行說明

update | improved alert logic for all allocationsNow triggers only on confirmed signal change at bar close with dynamic symbol names.

發行說明

Update to Pine Script v6 | nothing changed 僅限邀請腳本

只有經作者批准的使用者才能訪問此腳本。您需要申請並獲得使用權限。該權限通常在付款後授予。如欲了解更多詳情,請依照以下作者的說明操作,或直接聯絡viResearch。

除非您完全信任其作者並了解腳本的工作原理,否則TradingView不建議您付費或使用腳本。您也可以在我們的社群腳本中找到免費的開源替代方案。

作者的說明

DM via TradingView for access, Thanks

免責聲明

這些資訊和出版物並不意味著也不構成TradingView提供或認可的金融、投資、交易或其他類型的意見或建議。請在使用條款閱讀更多資訊。

僅限邀請腳本

只有經作者批准的使用者才能訪問此腳本。您需要申請並獲得使用權限。該權限通常在付款後授予。如欲了解更多詳情,請依照以下作者的說明操作,或直接聯絡viResearch。

除非您完全信任其作者並了解腳本的工作原理,否則TradingView不建議您付費或使用腳本。您也可以在我們的社群腳本中找到免費的開源替代方案。

作者的說明

DM via TradingView for access, Thanks

免責聲明

這些資訊和出版物並不意味著也不構成TradingView提供或認可的金融、投資、交易或其他類型的意見或建議。請在使用條款閱讀更多資訊。