INVITE-ONLY SCRIPT

已更新 Live Mini Terminal 3 : Relative Forex & Futures Change Data

This script displays relative data changes occurring in the adjustable period and/or adaptive automatic period in the rest liquid futures.

It was inspired by the data terminals used by commercial traders.

Period selection can be set in the menu.

This script uses the adaptive period algorithm used by Autonomous LSTM and Relativity scripts.

Or you can set the period manually from the menu.

For more information about adaptive period:

![Autonomous LSTM [Noldo]](https://s3.tradingview.com/e/ExPy48mQ_mid.png)

This script works only for 1 day (1D) and 1 week (1W) time frames.

Since COT data is used, the most efficient time frame is 1 week (1W) .

Features

INSTRUMENTS

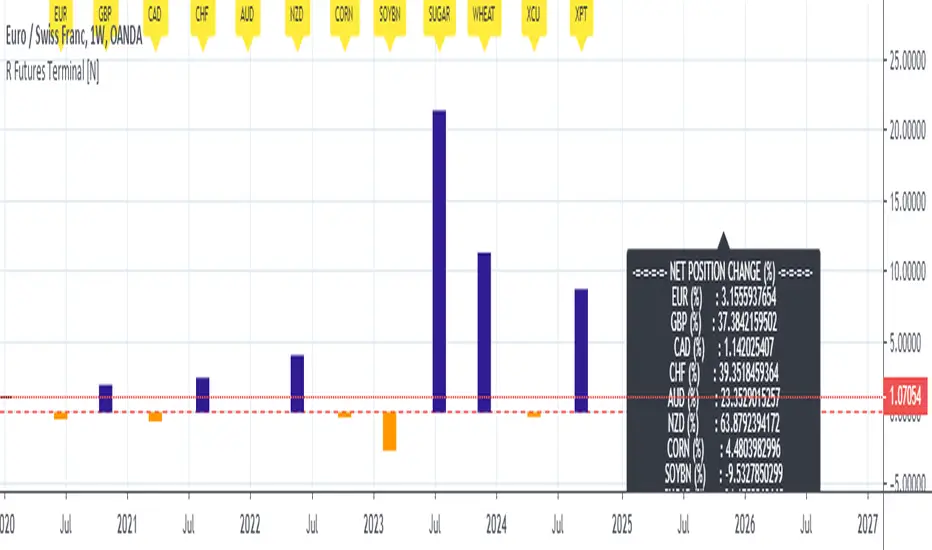

Position Change InfoPanel

USAGE

The script can be used as an indicator by putting it under the chart as shown above.

It is necessary to enlarge to see clearly.

Since it is not often looked at, such use under chart is the best method for healthy interpretation.

Regards.

It was inspired by the data terminals used by commercial traders.

Period selection can be set in the menu.

This script uses the adaptive period algorithm used by Autonomous LSTM and Relativity scripts.

Or you can set the period manually from the menu.

For more information about adaptive period:

This script works only for 1 day (1D) and 1 week (1W) time frames.

Since COT data is used, the most efficient time frame is 1 week (1W) .

Features

- Value changes on a percentage basis (%)

- Commitment of Traders position changes on a percentage basis :

Net position percentage is calculated as Short - Long and there is no inverse relationship.

Direct relationship is provided.

- Due to the advantage of movement, future data were drawn instead of spot values on the required instruments.

- The script provides the opportunity to comment on all major and minor Forex parities with liquid futures.

INSTRUMENTS

- Euro Futures (EURUSD)

- British Pound Futures (GBPUSD)

- Canadian Dollar Futures (CADUSD)

- Swiss Franc Futures (CHFUSD)

- Australian Dollar Futures (AUDUSD)

- New Zealand Dollar Futures (NZDUSD)

- Corn Futures

- Soybeans Futures

- Sugar Futures

- Wheat Futures

- Copper Futures (XCU)

- Platinum Futures (XPT)

Position Change InfoPanel

- Position definition for the related instruments and data were taken and the calculations were made.

USAGE

The script can be used as an indicator by putting it under the chart as shown above.

It is necessary to enlarge to see clearly.

Since it is not often looked at, such use under chart is the best method for healthy interpretation.

Regards.

發行說明

Unnecessary codes have been deleted.COT Commercial Positions were translated into Long-Short for ease of interpretation.

發行說明

Codes simplified.免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。