OPEN-SOURCE SCRIPT

已更新 D-VaR position sizing

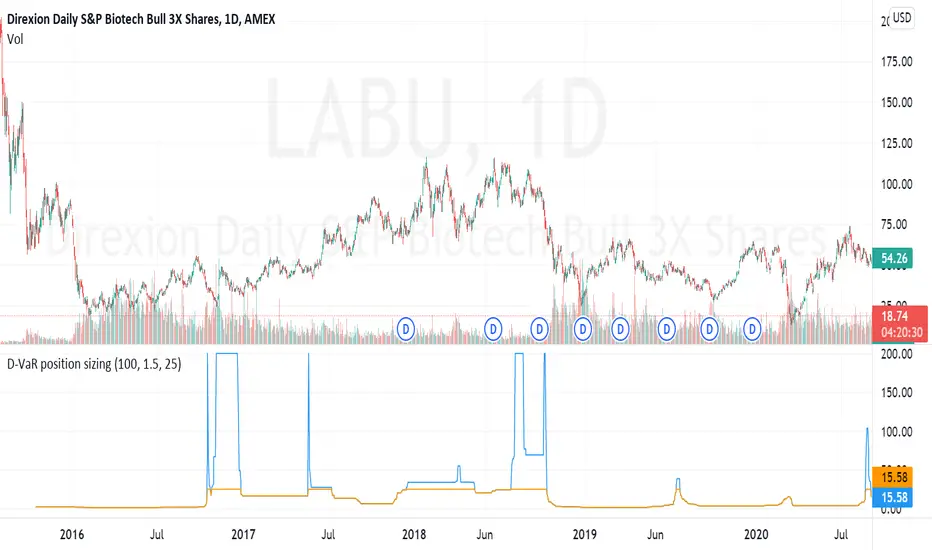

The D-VaR position sizing method was created by David Varadi. It's based on the concept of Value at Risk (VaR) - a widely used measure of the risk of loss in a portfolio based on the statistical analysis of historical price trends and volatilities. You can set the Percent Risk between 1 (lower) and 1.5 (higher); as well as, cap the % of Equity used in the position. The indicator plots the % of equity recommended based on the parameters you set.

發行說明

Fixed error in percentile_rank formula where it was not accounting for rolling returns. Added a cap of 200% of max equity to position size to limit plot size run-up and reduce exposure to large DVAR calculation when tail-size is extremely small number (i.e. 0.0001, etc.).開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

Need seasonals for futures data on NQ, ES, YM, or other commodities. Check out agresticresearch.com.

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。

開源腳本

秉持TradingView一貫精神,這個腳本的創作者將其設為開源,以便交易者檢視並驗證其功能。向作者致敬!您可以免費使用此腳本,但請注意,重新發佈代碼需遵守我們的社群規範。

Need seasonals for futures data on NQ, ES, YM, or other commodities. Check out agresticresearch.com.

免責聲明

這些資訊和出版物並非旨在提供,也不構成TradingView提供或認可的任何形式的財務、投資、交易或其他類型的建議或推薦。請閱讀使用條款以了解更多資訊。