MNO_2Step_Strategy_MOU_KAKU (Publish-Clear)//@version=5

strategy("MNO_2Step_Strategy_MOU_KAKU (Publish-Clear)", overlay=true, pyramiding=0,

max_labels_count=500, max_lines_count=500,

initial_capital=100000,

default_qty_type=strategy.percent_of_equity, default_qty_value=10)

// =========================

// Inputs

// =========================

emaSLen = input.int(5, "EMA Short (5)")

emaMLen = input.int(13, "EMA Mid (13)")

emaLLen = input.int(26, "EMA Long (26)")

macdFast = input.int(12, "MACD Fast")

macdSlow = input.int(26, "MACD Slow")

macdSignal = input.int(9, "MACD Signal")

macdZeroTh = input.float(0.2, "MOU: MACD near-zero threshold", step=0.05)

volLookback = input.int(5, "Volume MA days", minval=1)

volMinRatio = input.float(1.3, "MOU: Volume ratio min", step=0.1)

volStrong = input.float(1.5, "Strong volume ratio (Breakout/KAKU)", step=0.1)

volMaxRatio = input.float(3.0, "Volume ratio max (filter)", step=0.1)

wickBodyMult = input.float(2.0, "Pinbar: lowerWick >= body*x", step=0.1)

pivotLen = input.int(20, "Resistance lookback", minval=5)

pullMinPct = input.float(5.0, "Pullback min (%)", step=0.1)

pullMaxPct = input.float(15.0, "Pullback max (%)", step=0.1)

breakLookbackBars = input.int(5, "Pullback route: valid bars after break", minval=1)

// --- Breakout route (押し目なし初動ブレイク) ---

useBreakoutRoute = input.bool(true, "Enable MOU Breakout Route (no pullback)")

breakConfirmPct = input.float(0.3, "Break confirm: close > R*(1+%)", step=0.1)

bigBodyLookback = input.int(20, "Break candle body MA length", minval=5)

bigBodyMult = input.float(1.2, "Break candle: body >= MA*mult", step=0.1)

requireCloseNearHigh = input.bool(true, "Break candle: close near high")

closeNearHighPct = input.float(25.0, "Close near high threshold (% of range)", step=1.0)

allowMACDAboveZeroInstead = input.bool(true, "Breakout route: allow MACD GC above zero instead")

// 表示

showEMA = input.bool(true, "Plot EMAs")

showMouLabels = input.bool(true, "Show MOU/MOU-B labels")

showKakuLabels = input.bool(true, "Show KAKU labels")

showDebugTbl = input.bool(true, "Show debug table (last bar)")

showStatusLbl = input.bool(true, "Show status label (last bar always)")

locChoice = input.string("Below Bar", "Label location", options= )

lblLoc = locChoice == "Below Bar" ? location.belowbar : location.abovebar

// =========================

// 必ず決済が起きる設定(投稿クリア用)

// =========================

enableTPSL = input.bool(true, "Enable TP/SL")

tpPct = input.float(2.0, "Take Profit (%)", step=0.1, minval=0.1) // ←投稿クリア向けに近め

slPct = input.float(1.0, "Stop Loss (%)", step=0.1, minval=0.1) // ←投稿クリア向けに近め

maxHoldBars = input.int(30, "Max bars in trade (force close)", minval=1)

entryMode = input.string("MOU or KAKU", "Entry trigger", options= )

// ✅ 保険:トレード0件を避ける(投稿クリア用)

// 1回でもクローズトレードができたら自動で沈黙

publishAssist = input.bool(true, "Publish Assist (safety entry if 0 trades)")

// =========================

// EMA

// =========================

emaS = ta.ema(close, emaSLen)

emaM = ta.ema(close, emaMLen)

emaL = ta.ema(close, emaLLen)

plot(showEMA ? emaS : na, color=color.new(color.yellow, 0), title="EMA 5")

plot(showEMA ? emaM : na, color=color.new(color.blue, 0), title="EMA 13")

plot(showEMA ? emaL : na, color=color.new(color.orange, 0), title="EMA 26")

emaUpS = emaS > emaS

emaUpM = emaM > emaM

emaUpL = emaL > emaL

goldenOrder = emaS > emaM and emaM > emaL

above26_2days = close > emaL and close > emaL

baseTrendOK = (emaUpS and emaUpM and emaUpL) and goldenOrder and above26_2days

// =========================

// MACD

// =========================

= ta.macd(close, macdFast, macdSlow, macdSignal)

macdGC = ta.crossover(macdLine, macdSig)

macdUp = macdLine > macdLine

macdNearZero = math.abs(macdLine) <= macdZeroTh

macdGCAboveZero = macdGC and macdLine > 0 and macdSig > 0

macdMouOK = macdGC and macdNearZero and macdUp

macdBreakOK = allowMACDAboveZeroInstead ? (macdMouOK or macdGCAboveZero) : macdMouOK

// =========================

// Volume

// =========================

volMA = ta.sma(volume, volLookback)

volRatio = volMA > 0 ? (volume / volMA) : na

volumeMouOK = volRatio >= volMinRatio and volRatio <= volMaxRatio

volumeStrongOK = volRatio >= volStrong and volRatio <= volMaxRatio

// =========================

// Candle patterns

// =========================

body = math.abs(close - open)

upperWick = high - math.max(open, close)

lowerWick = math.min(open, close) - low

pinbar = (lowerWick >= wickBodyMult * body) and (lowerWick > upperWick) and (close >= open)

bullEngulf = close > open and close < open and close >= open and open <= close

bigBull = close > open and open < emaM and close > emaS and (body > ta.sma(body, 20))

candleOK = pinbar or bullEngulf or bigBull

// =========================

// Resistance / Pullback route

// =========================

res = ta.highest(high, pivotLen)

pullbackPct = res > 0 ? (res - close) / res * 100.0 : na

pullbackOK = pullbackPct >= pullMinPct and pullbackPct <= pullMaxPct

brokeRes = ta.crossover(close, res )

barsSinceBreak = ta.barssince(brokeRes)

afterBreakZone = (barsSinceBreak >= 0) and (barsSinceBreak <= breakLookbackBars)

pullbackRouteOK = afterBreakZone and pullbackOK

// =========================

// Breakout route (押し目なし初動ブレイク)

// =========================

breakConfirm = close > res * (1.0 + breakConfirmPct / 100.0)

bullBreak = close > open

bodyMA = ta.sma(body, bigBodyLookback)

bigBodyOK = bodyMA > 0 ? (body >= bodyMA * bigBodyMult) : false

rng = math.max(high - low, syminfo.mintick)

closeNearHighOK = not requireCloseNearHigh ? true : ((high - close) / rng * 100.0 <= closeNearHighPct)

mou_breakout = useBreakoutRoute and baseTrendOK and breakConfirm and bullBreak and bigBodyOK and closeNearHighOK and volumeStrongOK and macdBreakOK

mou_pullback = baseTrendOK and volumeMouOK and candleOK and macdMouOK and pullbackRouteOK

mou = mou_pullback or mou_breakout

// =========================

// KAKU (Strict): 8条件 + 最終三点

// =========================

cond1 = emaUpS and emaUpM and emaUpL

cond2 = goldenOrder

cond3 = above26_2days

cond4 = macdGCAboveZero

cond5 = volumeMouOK

cond6 = candleOK

cond7 = pullbackOK

cond8 = pullbackRouteOK

all8_strict = cond1 and cond2 and cond3 and cond4 and cond5 and cond6 and cond7 and cond8

final3 = pinbar and macdGCAboveZero and volumeStrongOK

kaku = all8_strict and final3

// =========================

// Entry (strategy)

// =========================

entrySignal = entryMode == "KAKU only" ? kaku : (mou or kaku)

canEnter = strategy.position_size == 0

newEntryKaku = canEnter and kaku and entrySignal

newEntryMouB = canEnter and (not kaku) and mou_breakout and entrySignal

newEntryMou = canEnter and (not kaku) and mou_pullback and entrySignal

// --- Publish Assist(保険エントリー) ---

// 条件が厳しすぎて「トレード0件」だと投稿時に警告が出る。

// closedtradesが0の間だけ、軽いEMAクロスで1回だけ拾う(その後は沈黙)。

assistFast = ta.ema(close, 5)

assistSlow = ta.ema(close, 20)

assistEntry = publishAssist and strategy.closedtrades == 0 and canEnter and ta.crossover(assistFast, assistSlow)

// 実エントリー

if newEntryKaku or newEntryMouB or newEntryMou or assistEntry

strategy.entry("LONG", strategy.long)

// ラベル(視認)

if showMouLabels and newEntryMou

label.new(bar_index, low, "猛(IN)", style=label.style_label_up, color=color.new(color.lime, 0), textcolor=color.black)

if showMouLabels and newEntryMouB

label.new(bar_index, low, "猛B(IN)", style=label.style_label_up, color=color.new(color.lime, 0), textcolor=color.black)

if showKakuLabels and newEntryKaku

label.new(bar_index, low, "確(IN)", style=label.style_label_up, color=color.new(color.yellow, 0), textcolor=color.black)

if assistEntry

label.new(bar_index, low, "ASSIST(IN)", style=label.style_label_up, color=color.new(color.aqua, 0), textcolor=color.black)

// =========================

// Exit (TP/SL + 強制クローズ)

// =========================

inPos = strategy.position_size > 0

tpPx = inPos ? strategy.position_avg_price * (1.0 + tpPct/100.0) : na

slPx = inPos ? strategy.position_avg_price * (1.0 - slPct/100.0) : na

if enableTPSL

strategy.exit("TP/SL", from_entry="LONG", limit=tpPx, stop=slPx)

// 最大保有バーで強制決済(これが「レポート無し」回避の最後の保険)

var int entryBar = na

if strategy.position_size > 0 and strategy.position_size == 0

entryBar := bar_index

if strategy.position_size == 0

entryBar := na

forceClose = inPos and not na(entryBar) and (bar_index - entryBar >= maxHoldBars)

if forceClose

strategy.close("LONG")

// =========================

// 利確/損切/強制クローズのラベル

// =========================

closedThisBar = (strategy.position_size > 0) and (strategy.position_size == 0)

avgPrev = strategy.position_avg_price

tpPrev = avgPrev * (1.0 + tpPct/100.0)

slPrev = avgPrev * (1.0 - slPct/100.0)

hitTP = closedThisBar and high >= tpPrev

hitSL = closedThisBar and low <= slPrev

// 同一足TP/SL両方は厳密に判断できないので、表示は「TP優先」で簡略(投稿ギリギリ版)

if hitTP

label.new(bar_index, high, "利確", style=label.style_label_down, color=color.new(color.lime, 0), textcolor=color.black)

else if hitSL

label.new(bar_index, low, "損切", style=label.style_label_up, color=color.new(color.red, 0), textcolor=color.white)

else if closedThisBar and forceClose

label.new(bar_index, close, "時間決済", style=label.style_label_left, color=color.new(color.gray, 0), textcolor=color.white)

// =========================

// Signals (猛/猛B/確)

// =========================

plotshape(showMouLabels and mou_pullback and not kaku, title="MOU_PULLBACK", style=shape.labelup, text="猛",

color=color.new(color.lime, 0), textcolor=color.black, location=lblLoc, size=size.tiny)

plotshape(showMouLabels and mou_breakout and not kaku, title="MOU_BREAKOUT", style=shape.labelup, text="猛B",

color=color.new(color.lime, 0), textcolor=color.black, location=lblLoc, size=size.tiny)

plotshape(showKakuLabels and kaku, title="KAKU", style=shape.labelup, text="確",

color=color.new(color.yellow, 0), textcolor=color.black, location=lblLoc, size=size.small)

// =========================

// Alerts

// =========================

alertcondition(mou, title="MNO_MOU", message="MNO: MOU triggered")

alertcondition(mou_breakout, title="MNO_MOU_BREAKOUT", message="MNO: MOU Breakout triggered")

alertcondition(mou_pullback, title="MNO_MOU_PULLBACK", message="MNO: MOU Pullback triggered")

alertcondition(kaku, title="MNO_KAKU", message="MNO: KAKU triggered")

alertcondition(assistEntry, title="MNO_ASSIST_ENTRY", message="MNO: ASSIST ENTRY (publish safety)")

// =========================

// Status label(最終足に必ず表示)

// =========================

var label status = na

if showStatusLbl and barstate.islast

label.delete(status)

statusTxt =

"MNO RUNNING " +

"ClosedTrades: " + str.tostring(strategy.closedtrades) + " " +

"BaseTrend: " + (baseTrendOK ? "OK" : "NO") + " " +

"MOU: " + (mou ? "YES" : "no") + " (猛=" + (mou_pullback ? "Y" : "n") + " / 猛B=" + (mou_breakout ? "Y" : "n") + ") " +

"KAKU: " + (kaku ? "YES" : "no") + " " +

"VolRatio: " + (na(volRatio) ? "na" : str.tostring(volRatio, format.mintick)) + " " +

"Pull%: " + (na(pullbackPct) ? "na" : str.tostring(pullbackPct, format.mintick)) + " " +

"Pos: " + (inPos ? "IN" : "OUT")

status := label.new(bar_index, high, statusTxt, style=label.style_label_left, textcolor=color.white, color=color.new(color.black, 0))

// =========================

// Debug table(最終足のみ)

// =========================

var table t = table.new(position.top_right, 2, 14, border_width=1, border_color=color.new(color.white, 60))

fRow(_name, _cond, _r) =>

bg = _cond ? color.new(color.lime, 70) : color.new(color.red, 80)

tx = _cond ? "OK" : "NO"

table.cell(t, 0, _r, _name, text_color=color.white, bgcolor=color.new(color.black, 0))

table.cell(t, 1, _r, tx, text_color=color.white, bgcolor=bg)

if showDebugTbl and barstate.islast

table.cell(t, 0, 0, "MNO Debug", text_color=color.white, bgcolor=color.new(color.black, 0))

table.cell(t, 1, 0, "", text_color=color.white, bgcolor=color.new(color.black, 0))

fRow("BaseTrend", baseTrendOK, 1)

fRow("MOU Pullback", mou_pullback, 2)

fRow("MOU Breakout", mou_breakout, 3)

fRow("Break confirm", breakConfirm, 4)

fRow("Break big body", bigBodyOK, 5)

fRow("Break close high", closeNearHighOK, 6)

fRow("Break vol strong", volumeStrongOK, 7)

fRow("Break MACD", macdBreakOK, 8)

fRow("KAKU all8", all8_strict, 9)

fRow("KAKU final3", final3, 10)

fRow("AssistEntry", assistEntry, 11)

fRow("ClosedTrades>0", strategy.closedtrades > 0, 12)

Candlestick analysis

Trend Following $ZEC - Multi-Timeframe Structure Filter + Revers# Trend Following CRYPTOCAP:ZEC - Strategy Guide

## 📊 Strategy Overview

Trend Following CRYPTOCAP:ZEC is an enhanced Turtle Trading system designed for cryptocurrency spot trading, combining Donchian Channel breakouts, multi-timeframe structure filtering, and ATR-based dynamic risk management for both long and short positions.

---

## 🎯 Core Features

1. Multi-Timeframe Structure Filtering

- Uses Swing High/Low to identify market structure

- Customizable structure timeframe (default: 1 minute)

- Only enters trades in the direction of the trend, avoiding counter-trend positions

2. Reverse Signal Exit

- No fixed stop-loss or fixed-period exits

- Exits only when a reverse entry signal triggers

- Maximizes trend profits, reduces premature exits

3. ATR Dynamic Pyramiding

- Adds positions when price moves 0.5 ATR in favorable direction

- Supports up to 2 units maximum (adjustable)

- Pyramid scaling to enhance profitability

4. Complete Risk Management

- Fixed position size (5000 USD per unit)

- Commission fee 0.06% (Binance spot rate)

- Initial capital 10,000 USD

---

## 📈 Trading Logic

Entry Conditions

✅ Long Entry:

- Close price breaks above 20-period high

- Structure trend is bullish (price breaks above Swing High)

✅ Short Entry:

- Close price breaks below 20-period low

- Structure trend is bearish (price breaks below Swing Low)

Add Position Conditions

- Long: Price rises ≥ 0.5 ATR

- Short: Price falls ≥ 0.5 ATR

- Maximum 2 units including initial entry

Exit Conditions

- Long Exit: When short entry signal triggers (price breaks 20-period low + structure turns bearish)

- Short Exit: When long entry signal triggers (price breaks 20-period high + structure turns bullish)

---

## ⚙️ Parameter Settings

Channel Settings

- Entry Channel Period: 20 (Donchian Channel breakout period)

- Exit Channel Period: 10 (reserved parameter, actually uses reverse signal exit)

ATR Settings

- ATR Period: 20

- Stop Loss ATR Multiplier: 2.0 (reserved parameter)

- Add Position ATR Multiplier: 0.5

Structure Filter

- Swing Length: 160 (Swing High/Low calculation period)

- Structure Timeframe: 1 minute (can change to 5/15/60, etc.)

Position Management

- Maximum Units: 2 (including initial entry)

- Capital Per Unit: 5000 USD

---

## 🎨 Visualization Features

Background Colors

- Light Green: Bullish structure

- Light Red: Bearish structure

- Dark Green: Long entry

- Dark Red: Short entry

Optional Display (Default: OFF)

- Entry/exit channel lines

- Structure high/low lines

- ATR stop-loss line

- Next add position indicator

- Entry/exit labels

---

## 📱 Alert Message Format

Strategy sends notifications on entry/exit with the following format:

- Entry: `1m Long EP:428.26`

- Add Position: `15m Add Long 2/2 EP:429.50`

- Exit: `1m Close Long Reverse Signal`

Where:

- `1m`/`15m` = Current chart timeframe

- `EP` = Entry Price

---

## 💰 Backtest Settings

Capital Allocation

- Initial Capital: 10,000 USD

- Per Entry: 5,000 USD (split into 2 entries)

- Leverage: 0x (spot trading)

Trading Costs

- Commission: 0.06% (Binance spot VIP0)

- Slippage: 0

---

## 🎯 Use Cases

✅ Best Scenarios

- Trending markets

- Moderate volatility assets

- 1-minute to 4-hour timeframes

⚠️ Not Suitable For

- Highly volatile choppy markets

- Low liquidity small-cap coins

- Extreme market conditions (black swan events)

---

## 📊 Usage Recommendations

Timeframe Suggestions

| Timeframe | Trading Style | Suggested Parameter Adjustment |

|-----------|--------------|-------------------------------|

| 1-5 min | Scalping | Swing Length 100-160 |

| 15-30 min | Short-term | Swing Length 50-100 |

| 1-4 hour | Swing Trading | Swing Length 20-50 |

Optimization Tips

1. Adjust swing length based on backtest results

2. Different coins may require different parameters

3. Recommend backtesting on 1-minute chart first before live trading

4. Enable labels to observe entry/exit points

---

## ⚠️ Risk Disclaimer

1. Past Performance Does Not Guarantee Future Results

- Backtest data is for reference only

- Live trading may be affected by slippage, delays, etc.

2. Market Condition Changes

- Strategy performs better in trending markets

- May experience frequent stops in ranging markets

3. Capital Management

- Do not invest more than you can afford to lose

- Recommend setting total capital stop-loss threshold

4. Commission Impact

- Frequent trading accumulates commission fees

- Recommend using exchange discounts (BNB fee reduction, etc.)

---

## 🔧 Troubleshooting

Q: No entry signals?

A: Check if structure filter is too strict, adjust swing length or timeframe

Q: Too many labels displayed?

A: Turn off "Show Labels" option in settings

Q: Poor backtest performance?

A:

1. Check if the coin is suitable for trend-following strategies

2. Adjust parameters (swing length, channel period)

3. Try different timeframes

Q: How to set alerts?

A:

1. Click "Alert" in top-right corner of chart

2. Condition: Select "Strategy - Trend Following CRYPTOCAP:ZEC "

3. Choose "Order filled"

4. Set notification method (Webhook/Email/App)

---

## 📞 Contact Information

Strategy Name: Trend Following CRYPTOCAP:ZEC

Version: v1.0

Pine Script Version: v6

Last Updated: December 2025

---

## 📄 Copyright Notice

This strategy is for educational and research purposes only.

All risks of using this strategy for live trading are borne by the user.

Commercial use without authorization is prohibited.

---

## 🎓 Learning Resources

To understand the strategy principles in depth, recommended reading:

- "The Complete TurtleTrader" - Curtis Faith

- "Trend Following" - Michael Covel

- TradingView Pine Script Official Documentation

---

Happy Trading! Remember to manage your risk 📈

Multi-MA + RSI Pullback Strategy (Jordan)1️⃣ Strategy logic I’ll code

From your screenshots:

Indicators

• EMAs: 600 / 200 / 100 / 50

• RSI: length 6, levels 80 / 20

Rules (simplified so a script can handle them):

• Use a higher-timeframe trend filter (15m or 1h) using the EMAs.

• Take entries on the chart timeframe (you can use 1m or 5m).

• Long:

• Higher-TF trend is up.

• Price is pulling back into a zone (between 50 EMA and 100 EMA on the entry timeframe – this approximates your 50–61% retrace).

• RSI crosses below 20 (oversold).

• Short:

• Higher-TF trend is down.

• Price pulls back between 50 & 100 EMAs.

• RSI crosses above 80 (overbought).

• Exits: ATR-based stop + take-profit with adjustable R:R (2:1 or 3:1).

• Max 4 trades per day.

News filter & “only trade gold” you handle manually (run it on XAUUSD and avoid news times yourself – TradingView can’t read the economic calendar from code).

Strategia S&P 500 vs US10Y YieldThis strategy explores the macroeconomic relationship between the equity market (S&P 500) and the debt market (10-Year Treasury Yield). Historically, rapid spikes in bond yields often exert downward pressure on equity valuations, leading to corrections or bear markets.

The goal of this strategy is capital preservation. It attempts to switch to cash when yields are rising too aggressively and re-enter the stock market when the bond market stabilizes.

Strategia S&P 500 vs US10Y Yield (od 2000)This strategy explores the macroeconomic relationship between the equity market (S&P 500) and the debt market (10-Year Treasury Yield). Historically, rapid spikes in bond yields often exert downward pressure on equity valuations, leading to corrections or bear markets.

The goal of this strategy is capital preservation. It attempts to switch to cash when yields are rising too aggressively and re-enter the stock market when the bond market stabilizes.

Hammer Breakout (Adjustable RR)Hammer candle detection and strat for back testing.

diamond indicates a detected hammer candle, the position is entered at the hammer candle close.

Stop loss below the hammer candle wick.

Adjustbale rr based on the distance to the stop (bottom of wick)

Scalping EMA + Pinbar Strategy (London & NY only, BE @ 1R)The scalping trading system uses two types of indicators:

EMA 10, EMA 21, EMA 50

Pinbar Indicator

Rules for entering a buy order:

If the closing price is above the EMA 50, the trend is uptrend and only buy orders should be considered.

The EMA 10 and EMA 21 lines must simultaneously be above the EMA 50.

The price must correct down at least 50% of the area created by the EMA 10 and EMA 21, or correct further down.

A Type 1 Pinbar candle (marked by the Pinbar indicator) must appear; this Pinbar candle must react to at least one of the three EMA lines (EMA 10, EMA 21, EMA 50) and close above the EMA 50.

This Pinbar candle must have a Pinbar strength value (marked by the Pinbar indicator) less than 2 to be considered valid. Check if the closing price of this pinbar candle is higher than the 50-day EMA and if the 10-day and 21-day EMAs are also higher than the 50-day EMA. If so, the conditions have been met and you can begin trading.

Place a buy stop order 0.1 pip higher than the highest price of the pinbar candle, and a stop loss order 0.1 pip lower than the lowest price of the pinbar candle. Set the take profit at 3R.

If the price moves past the previously set stop loss, cancel the pending order.

When the price moves 1R, move the stop loss back to the entry point.

The next trade can only be executed after the previous trade has moved the stop loss back to the entry point.

Rules for placing sell orders:

If the closing price is below the 50-day EMA, the trend is bearish, and only sell orders should be considered. The 10-day and 21-day EMAs must both be below the 50-day EMA.

The price must correct downwards by at least 50% of the area formed by the 10-day and 21-day EMAs, or even further.

A Type 1 pinbar candle (marked by the Pinbar indicator) must appear. This pinbar candle must react to at least one of the three EMAs (EMA 10, EMA 21, EMA 50) and close below the EMA 50.

This pinbar is valid if its strength (indicated by the Pinbar indicator) is less than 2. Verify that the closing price of this pinbar candle is below the EMA 50 and that both the EMA 10 and EMA 21 are below the EMA 50. If all conditions are met, the trade can be executed.

(This appears to be a separate entry rule and not part of the previous text.) Place a sell stop order 0.1 pip below the lowest point of the pinbar candle, and a stop loss order 0.1 pip above the highest point of the pinbar candle. Set the take profit point at 3R.

If the price moves past the previously set stop-loss point, cancel the pending order.

When the price moves 1R, move the stop-loss point back to the entry point.

The next trade can only be executed after the previous trade has moved the stop-loss point back to the entry point.

ETH UU Reversion Strategy Strategy Overview

The "ETH UU Reversion Strategy" is a sophisticated mean-reversion trading system designed to capture price reversals at standard deviation extremes. Unlike typical strategies that enter trades immediately at market price, this script employs a proprietary **Limit Order Execution Mechanism** combined with volatility filtering to optimize entry prices and reduce slippage.

Originality & Key Features

This script addresses the common pitfalls of standard Bollinger Band strategies by introducing advanced order management logic:

1. Limit Order Execution:** Instead of market orders, the strategy calculates an optimal entry price based on ATR offsets. This allows traders to capitalize on "wicks" and secure better risk-reward ratios.

2. Smart Timeout Logic:To prevent "catching a falling knife," pending orders are automatically cancelled if not filled within a customizable number of bars (default: 15). This ensures orders do not remain active when market structure shifts.

3. Dynamic Risk Recalculation:** Stop Loss (SL) and Take Profit (TP) levels are recalculated at the exact moment of execution using the real-time ATR, ensuring risk parameters adapt to current market volatility.

How to Use

1. Setup: Apply the strategy to ETH/USDT (or other crypto pairs) on 15m or 1h timeframes.

2. Configuration:

* Adjust `BB Length` and `RSI Length` to fit your timeframe.

* Set `Order Timeout` to define how long a pending order should remain active.

* Toggle `Use ADX Filter` to avoid trading against strong trends.

3. *Visuals: The chart displays distinct labels for pending orders (Gray), active entries (Blue/Red), and cancellations, providing full transparency of the strategy's logic.

Risk Disclaimer

This script is for educational and quantitative analysis purposes only. Past performance regarding backtesting or live trading does not guarantee future results. Cryptocurrency trading involves high risk and high volatility. Please use proper risk management and trade at your own discretion.

-------------------------------------------------------------

Chinese Translation (中文说明)

策略概述

“ETH UU 均值回归策略”是一个旨在捕捉标准差极端位置价格反转的交易系统。与立即以市价入场的典型策略不同,本策略采用独特的**挂单执行机制**结合波动率过滤,以优化入场价格并减少滑点。

原创性与核心功能

本脚本通过引入高级订单管理逻辑,解决了普通布林带策略的常见缺陷:

1. 挂单交易模式: 策略不使用市价单,而是根据 ATR 偏移计算最佳入场价(Limit Orders)。这允许交易者捕捉K线的“影线”,获得更好的盈亏比。

2. 智能超时撤单: 为了防止“接飞刀”,如果挂单在指定K线数内(默认15根)未成交,系统会自动撤单。这确保了当市场结构发生变化时,旧的挂单不会被错误触发。

3. 动态风控重算: 止损和止盈在成交的瞬间根据实时 ATR 重新计算,确保风控参数始终适应当前的市场波动率。

风险提示

本脚本仅供教育和量化分析使用。回测或实盘的过往表现并不预示未来结果。加密货币交易具有极高的风险和波动性,请务必做好仓位管理,并自行承担使用本策略的风险。

Customer Short strategy A5.1 + Session + CBL SLFor my customer.

HalfTrend Directional Framework (A5.1)

Used for primary trend recognition and breakout validation.

Session-Based Volatility Windows

Trades only occur within specific high-liquidity windows (e.g., 08:30–12:30 and 12:30–16:30), improving fill quality and reducing noise.

Three-Bar Opening Range Model

The first three 5-minute bars define:

session high

session low

These become structural breakout levels:

price > range high → long-bias

price < range low → short-bias

CBL (Guppy Count-Back Line) Stop-Loss

Instead of using ATR or static percentage stops, Libra_S relies on CBL to:

avoid premature exits during healthy pullbacks

capture trend persistence

provide structure-based invalidation

Strong Candle Probability Levels Tester [SYNC & TRADE]### Strategy Description: Strong Candle Probability Levels Tester

This strategy is a powerful tool for testing and visualizing probability levels based on strong candles, incorporating Volume Delta, Supertrend, and dynamic Fibonacci grids. Designed as a tester/trainer for traders analyzing price behavior around key support/resistance levels formed by strong impulse candles. It combines indicator elements for signal visualization with backtesting of trading scenarios, allowing evaluation of entry and exit effectiveness in real market conditions.

The main goal is to help traders understand how strong candles (with high volume and delta) influence subsequent price movement and test strategies based on Fibonacci extensions. It's not just an indicator but a full tester that simulates orders, stop-losses, take-profits, and advanced position management rules. Useful for beginners and experienced traders: enables practicing risk management, analyzing historical data, and optimizing approaches without real losses. Ultimately, you get visual feedback on level achievement probabilities, PNL statistics, and insights into market manipulations.

#### How the Strategy Works

The strategy identifies "strong candles" — impulse bars with elevated volume and significant delta (difference between buys and sells). Based on them, it builds a Fibonacci grid for potential entries (retracements) and exits (extensions). Additionally integrated are ATR filters for candle strength confirmation and Supertrend for trend context. The tester simulates pyramiding (adding positions), trailing stops, partial closes, and other rules to model real trading.

- **Volume Delta Analysis**: Visualizes volume deltas across timeframes to detect manipulations and impulse strength. Helpful for spotting when a candle is "strong" (high delta in the direction of movement) or "manipulative" (delta opposite to candle color).

- **Supertrend Filter**: Adds a trend indicator with an adaptive multiplier considering delta. Helps filter signals in trends, avoiding false entries.

- **Fibonacci Grid**: Automatically plots entry levels (retracements from 0% to 78.6%) and take-profits (extensions from 127.2% to 462%). The grid is "smart" — with advanced rules for profit protection and market adaptation.

The strategy does not reveal internal algorithms for strong candle detection but focuses on practical application: the tester shows how price reacts to these levels, aiding in assessing goal achievement probabilities.

#### How to Use

1. **Add to Chart**: In TradingView, select the tool, specify symbol (stocks, crypto, forex), and timeframe (recommended M5 to D1 for Volume Delta accuracy).

2. **Configure Settings**:

- **Volume Delta Section**: Enable strong candles and manipulations display. Set ATR period for filter (default 3) and minimum body size (ATR multiplier, default 0.5). This ignores weak impulses.

*(Add photo here: example chart with strong candle marked by circle and delta as colored layers on bar.)*

- **Supertrend Section**: Enable for trend filtering. Set ATR length (default 5) and multiplier (default 2.62). Delta or strong candle filter options enhance signals.

*(Photo: chart with Supertrend line colored by z-score strength and trend background.)*

- **Fibonacci Basics**: Choose direction (long/short/both), stop-loss mode (crossover or body close). Specify lot per level (default 0.1) and max active grids (default 7).

*(Photo: grid with entry and TP levels on real chart, with orders.)*

- **Advanced Rules**: Activate options like protection at 161.8%/261.8%, grid lock after 127.2%, trailing after TP1, partial close on pullback, pyramiding, time/momentum exits, or "news". This simulates complex scenarios.

- **Risk Management**: Enable exposure limit (max entry amount in USD) for safe testing.

*(Photo: PNL and risk stats in strategy table.)*

- **Entry/TP Levels**: Enable desired Fibonacci levels (retracements for entries, extensions for TP).

*(Photo: full grid with filled orders and partial TP.)*

- **Visualization**: Enable grid level display for clarity.

*(Photo: multiple grids on chart with base price and SL lines.)*

3. **Interpret Signals**:

- **Strong Candle**: Marked by circle (blue for long, red for short). Z-label in circle shows strength (2+ for significant).

- **Manipulation**: Cross (X) indicates potential trap (delta opposite to candle).

- **Grid**: Forms on strong candle. Entries — limit orders on retracements, TP on extensions. Monitor fills and closes in strategy report.

- **Supertrend**: Trend line with color gradation by strength (darker = stronger). Background highlights direction.

4. **Testing**:

- Run backtest in TradingView (select period, capital). Analyze metrics: PNL, drawdown, win-rate.

- Train: Change settings, observe rule impacts (e.g., trailing reduces risks but may miss profits).

- For live chart: Use as indicator for manual entries, ignoring orders.

#### Purpose and Benefits

This strategy is an ideal trainer for mastering probability trading based on strong candles and Fibonacci. It provides:

- **Probability Visualization**: Shows how often price hits levels (127.2%, 161.8%, etc.), helping assess risk/reward.

- **Risk Management Training**: Simulates real scenarios with pyramiding, trailing, partial closes, and exposure limits, reducing emotional errors.

- **Manipulation Analysis**: Volume Delta reveals hidden signals (weak/strong delta), useful for avoiding traps in volatile markets.

- **Trend Filter**: Supertrend with delta adaptation improves entry accuracy in trends.

- **Stats and Insights**: Report includes unrealized/realized PNL, average entry price, risk to SL. Aids in optimizing strategies for different assets.

Useful for: idea testing without risk, beginner education (visually intuitive), pro discipline improvement. Recommended to combine with other tools for signal confirmation. Remember: this is a tester, not financial advice — always demo test!

SMC Pro [Stansbooth]

🔮 SMC × Fibonacci Confluence Engine — The Hidden Algorithm of the Markets

Welcome to a level of chart analysis where mathematics , market psychology , and institutional logic merge into one ultra-intelligent system.

This indicator decodes the true structure of price delivery by combining Smart Money Concepts with the timeless precision of Fibonacci ratios , revealing what retail traders can’t see — *the algorithmic heartbeat of the market*.

✨ What Makes This Indicator Different

Instead of drawing random lines or reacting to late signals, this tool **anticipates** market behavior by reading the footprints left behind by institutional algorithms. Every element is placed with purpose — every zone, every shift, every fib level — all forming a seamless narrative that explains *why* price moves the way it does.

🔥 Core Intelligence Features

Advanced BOS/CHOCH Auto-Detection — Spot structure shifts before momentum even forms.

Institutional Liquidity Mapping

— Identify liquidity pools, engineered sweeps, equal highs/lows, and trap zones designed by smart money.

Fibonacci-Aligned Precision Zones

— Auto-generated fib grids synced with SMC levels for pinpoint reversal and continuation setups.

Imbalance Engine

— FVGs, displacement, inefficiencies, and mitigation blocks displayed with crystal clarity.

Premium/Discount Algorithm

— Understand instantly whether price is in a zone of accumulation or distribution.

🚀 Designed for Traders Who Want an Edge

Whether you're scalping fast moves, capturing intraday swings, or holding higher-timeframe plays, this indicator provides a professional lens into the market. It turns complex price action into a structured, predictable system where every move has logic and every entry has confluence.

You don’t just see the chart —

you see the intention behind every push, pull, manipulation, and reversal.

💎 Why It Feels Like a Cheat Code

Because it mirrors the way institutions analyze the market:

— Identify liquidity

— Seek equilibrium

— Deliver price

— Create inefficiency

— Mitigate

— Continue the narrative

Using SMC and Fibonacci together unlocks the “algorithmic geometry” behind price movement, giving you clarity where others see chaos.

⚡ Trade With Confidence, Confluence & Control

This indicator isn’t just a tool.

It’s a complete trading framework — structured, intelligent, and deadly accurate.

Master the markets.

Decode the algorithm.

Trade like smart money .

GIX-KC-MAStrategia folosește doar KC si SMA 50 (filter + HTF SMA).

Intrările sunt agresive și foarte filtrate (close > SMA + break + HTF confirm).

Se folosesc pending orders automatizate, cu:

Entry = High ± pips

SL = Low ± pips

Expirare automată după X bare

Anulare la semnal opus

KC are 3 moduri de TP

Keltner Channels Strategy NewThe strategy is chenging the same as an original copy, but this one is for tests, so I will publish it and check results

Trend Flow & Breakout Professional [Strategy]Description:

🌪️ Overview

Stop guessing. Start following the flow.

The Trend Flow & Breakout Professional is a high-precision visual trading system designed to solve the biggest problem traders face: Choppy Markets & Fakeouts.

Instead of relying on lagging indicators that generate false signals, this engine uses a proprietary "Momentum Alignment Algorithm" to identify when price action is entering a genuine expansion phase. It transforms complex trend data into a clean, easy-to-read visual roadmap, allowing you to catch the meat of the move while filtering out the noise.

🔮 Key Features

1. The "Traffic Light" Visual System Trading is 90% psychology. This script reduces mental fatigue by coloring the chart background to reflect the dominant market state:

🟢 Green Zone (Bullish Flow): Momentum is accelerating upwards. The system suggests holding long positions and ignoring minor pullbacks.

🔴 Red Zone (Bearish Flow): Structure has broken down. The system suggests defensive measures or short entries.

Note: The background remains active as long as the trend structure holds, preventing you from exiting trades too early.

2. Smart Noise Filtering Unlike standard crossover strategies that get destroyed in sideways ranges, this system includes a Multi-Layer Trend Filter. It only triggers a signal when:

Short-term momentum aligns perfectly with the medium-term direction.

Volatility expands significantly (breakout confirmation).

Price successfully clears key long-term structural resistance (The "Blue Sky" Zone).

3. Built-in "Smart Strategy" Backtester We have integrated a professional-grade position management module. You can customize how the strategy executes trades in the settings:

Mode A: Sniper (Trend Reversal): Enters heavily on the first confirmed breakout and holds until the trend reverses. Ideal for swing traders.

Mode B: Builder (Pyramiding): Adds to the position incrementally as the trend confirms its strength, maximizing profit during strong runs.

4. Cooldown Mechanism To prevent over-trading, the algorithm includes a smart "Cooldown Period" that prevents signal spamming during high-volatility consolidations.

⚙️ How to Trade This System

Wait for the Signal:

Look for the "Buy" / "Sell" labels accompanied by a bright Neon Candle.

Ensure the background color shifts (e.g., from Grey/Red to Green).

Ride the Zone:

Do not exit just because of one red candle. As long as the Background remains Green, the trend is healthy.

The background color acts as your "psychological anchor," helping you let profits run.

Exit / Reversal:

A complete background color flip (e.g., Green to Red) indicates a structural trend failure. This is your signal to close positions or flip directions.

⚠️ Disclaimer

This tool is for educational and technical analysis purposes only. Past performance does not guarantee future results. Always use proper risk management.

2 Dip/Tepe + Destek/Direnç + Tek Sinyal Stratejisi⭐ A Brief Summary of What the Strategy Does

🎯 1) Market analysis is being released (bottom-top analysis)

It automatically finds pivot bottoms and pivot tops on the strategic chart. Then:

If the bottoms are rising (HL – High Low): the trend is upward

If the tops are falling (LH – Lower High): the trend is downward

it interprets this.

🎯 2) Support and resistance lines are formed

Last pivot top = resistance line

Last pivot bottom = support line

These lines are automatically drawn on the chart.

🎯 3) Breakout is expected according to the trend structure

For LONG:

The last two bottoms will be rising bottoms

The price will rise above the last resistance line

This gives a single LONG signal.

For SHORT:

The last two peaks will be falling peaks

The price will fall below the support line

This gives a single SHORT signal.

N1E_UTBOATN1E_UTBOAT

ATR trailing stop

Optional Heikin Ashi source

Buy/Sell signals based on a crossover of price vs ATR trailing stop

Strategy long/short entries

2026 CHRISTMAS PRESENT CHRISTMAS PRESENT

Overview

The Cash Detector is a comprehensive trading strategy that combines momentum analysis with price action confirmation to identify high-probability entry points. This strategy is designed to capture trend reversals and continuation moves by requiring multiple confirming signals before entry, significantly reducing false signals common in single-indicator systems.

Strategy Background

The strategy is built on the principle of confluence trading requiring multiple technical factors to align before taking a position. It focuses on two critical phases of market rotation:

Q2 Momentum Phase: Uses MACD crossovers to identify shifts in market momentum, signaling when bulls or bears are gaining control.

Q4 Trigger Phase: Employs engulfing candlestick patterns to confirm strong directional pressure and validate the momentum signal with actual price action.

By combining these elements, the strategy filters out weak signals and focuses only on setups where both momentum AND price action agree on direction.

Key Features

Dual Confirmation System: Requires both MACD momentum shift and engulfing candle pattern

RSI Filter: Optional overbought/oversold filter to avoid extreme conditions

Built-in Risk Management: Configurable stop loss and take profit levels

Performance Dashboard: Real-time ROI metrics displayed on chart

Full Backtesting: Strategy mode allows historical performance analysis

Trading Rules

LONG ENTRY BUY

All conditions must occur on the same candle:

1. Momentum Confirmation:

MACD line crosses above signal line bullish crossover

2. Price Action Confirmation:

Bullish engulfing pattern forms:

Current close greater than previous open

Current open less than previous close

Current close greater than current open

3. RSI Filter Optional:

RSI less than 70 not overbought

Visual Signal: Green LONG label appears below the candle

SHORT ENTRY SELL

All conditions must occur on the same candle:

1. Momentum Confirmation:

MACD line crosses below signal line bearish crossover

2. Price Action Confirmation:

Bearish engulfing pattern forms:

Current close less than previous open

Current open greater than previous close

Current close less than current open

3. RSI Filter Optional:

RSI greater than 30 not oversold

Visual Signal: Red SHORT label appears above the candle

Exit Rules

Stop Loss Default 2 percent

Long: Exit if price drops 2 percent below entry

Short: Exit if price rises 2 percent above entry

Take Profit Default 4 percent

Long: Exit if price rises 4 percent above entry

Short: Exit if price drops 4 percent below entry

Input Parameters

Indicator Settings

MACD Fast Length: 12 default

MACD Slow Length: 26 default

RSI Length: 14 default

Risk Management

Use Stop Loss: Enable or disable stop loss

Stop Loss percent: Percentage risk per trade default 2 percent

Use Take Profit: Enable or disable take profit

Take Profit percent: Target profit per trade default 4 percent

Filters

Use RSI Filter: Enable or disable RSI overbought oversold filter

RSI Overbought: Upper threshold default 70

RSI Oversold: Lower threshold default 30

Performance Metrics

The built-in dashboard displays:

Net Profit: Total profit loss in currency and percentage

Total Trades: Number of completed trades

Win Rate: Percentage of profitable trades

Profit Factor: Ratio of gross profit to gross loss

Average Win Loss: Mean profit per winning losing trade

Max Drawdown: Largest peak to trough decline

Best Practices

1. Timeframe Selection: Works on multiple timeframes test on 15min 1H 4H and daily

2. Market Conditions: Most effective in trending markets with clear momentum

3. Risk Reward Ratio: Default 1:2 ratio 2 percent risk 4 percent reward is conservative adjust based on backtesting

4. Combine with Context: Consider overall market trend and support resistance levels

5. Backtest First: Always backtest on your specific instrument and timeframe before live trading

Risk Disclaimer

This strategy is for educational purposes. Past performance does not guarantee future results. Always:

Backtest thoroughly on historical data

Paper trade before using real capital

Use proper position sizing and risk management

Never risk more than you can afford to lose

Customization Tips

Aggressive traders: Reduce stop loss to 1.5 percent increase take profit to 5 percent

Conservative traders: Increase stop loss to 3 percent reduce take profit to 3 percent

Ranging markets: Enable RSI filter to avoid false breakouts

Strong trends: Disable RSI filter to catch all momentum shifts

Technical Details

Indicators Used:

Moving Average Convergence Divergence MACD

Relative Strength Index RSI

Candlestick Pattern Recognition

Strategy Type: Trend following with momentum confirmation

Best Suited For: Stocks Forex Crypto Indices

Version 1.0

Compatible with Pine Script v5

Fibonacci Vision ProFibonacci Precision Signals Pro | Smart Buy & Sell Alerts

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

OVERVIEW

This indicator combines Fibonacci mathematics with advanced signal filtering to deliver precise buy and sell signals. It automatically detects swing structure, calculates the key 0.618 retracement level, and generates signals only when multiple confirmation factors align.

Clean. Accurate. Professional.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

HOW IT WORKS

The script identifies swing highs and lows, then calculates Fibonacci retracement levels automatically. When price interacts with the 0.618 zone and all filters confirm, a signal appears:

▲ buy — Long entry opportunity

▼ sell — Short entry opportunity

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

6-LAYER CONFIRMATION SYSTEM

Every signal must pass through:

Trend Direction Analysis

Fibonacci Level Interaction

EMA Trend Filter (50-period default)

RSI Momentum Validation (14-period default)

Volume Spike Detection

Candlestick Pattern Recognition (Pin bars, Engulfing, Momentum candles)

This multi-layer approach significantly reduces false signals.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

BUILT-IN RISK MANAGEMENT

Every trade includes automatic stop loss and take profit levels:

Stop Loss: 100 pips

Take Profit: 200 pips

Risk-Reward Ratio: 1:2

Adjust these values in settings to match your trading style.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

KEY FEATURES

✅ Automatic Fibonacci calculation — no manual drawing

✅ Multi-timeframe compatibility — M15 to Daily

✅ Universal market support — Forex, Crypto, Stocks, Indices

✅ Clean minimalist signals — white triangles with text

✅ Customizable filters — adjust sensitivity to your preference

✅ Built-in alerts — never miss a signal

✅ No repainting — signals remain fixed once confirmed

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Swing Detection:

Swing Length — Controls sensitivity to market structure (default: 10)

Confirmation Bars — Bars required to confirm signal (default: 1)

Signal Filters:

EMA Trend Filter — Toggle trend confirmation on/off

EMA Length — Adjust trend filter period (default: 50)

RSI Filter — Toggle momentum confirmation on/off

RSI Length — Adjust momentum period (default: 14)

Volume Filter — Toggle volume confirmation on/off

Volume Multiplier — Set volume threshold (default: 1.2x average)

Risk Management:

Stop Loss Pips — Set your stop loss distance (default: 100)

Take Profit Pips — Set your profit target (default: 200)

Pip Value — Adjust for your instrument (0.0001 for most Forex, 0.01 for JPY pairs)

Visuals:

Show Signals — Toggle signal visibility

Show Cloud — Toggle Fibonacci zone visibility

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

BEST PRACTICES

Use on H1 or H4 timeframes for optimal results

Trade in direction of the higher timeframe trend

Avoid trading during major news events

Combine with proper position sizing

Always use the built-in stop loss

Be patient — quality signals over quantity

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

MARKETS SUPPORTED

Forex — All major, minor, and exotic pairs

Crypto — BTC, ETH, and altcoins

Stocks — Any equity on TradingView

Indices — S&P500, NASDAQ, DAX, FTSE, etc.

Commodities — Gold, Silver, Oil, etc.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

WHY FIBONACCI?

The 0.618 ratio (Golden Ratio) is observed by traders worldwide. When price retraces to this level, it often:

Reverses direction

Finds support or resistance

Creates high-probability entry opportunities

This script automates the detection of these key moments.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ALERTS INCLUDED

Set up notifications to receive signals on:

Mobile push notifications

Desktop popups

Email alerts

Webhook integrations

Never miss a trading opportunity again.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

WHAT MAKES THIS DIFFERENT

Most indicators give too many signals. This one focuses on quality.

Most indicators clutter your chart. This one keeps it clean.

Most indicators ignore risk management. This one includes it.

Most indicators work on one market. This one works on all.

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

DISCLAIMER

This indicator is a trading tool, not financial advice. Trading involves substantial risk of loss. Past performance does not guarantee future results. Always use proper risk management and never trade with money you cannot afford to lose. Test on a demo account before trading live.

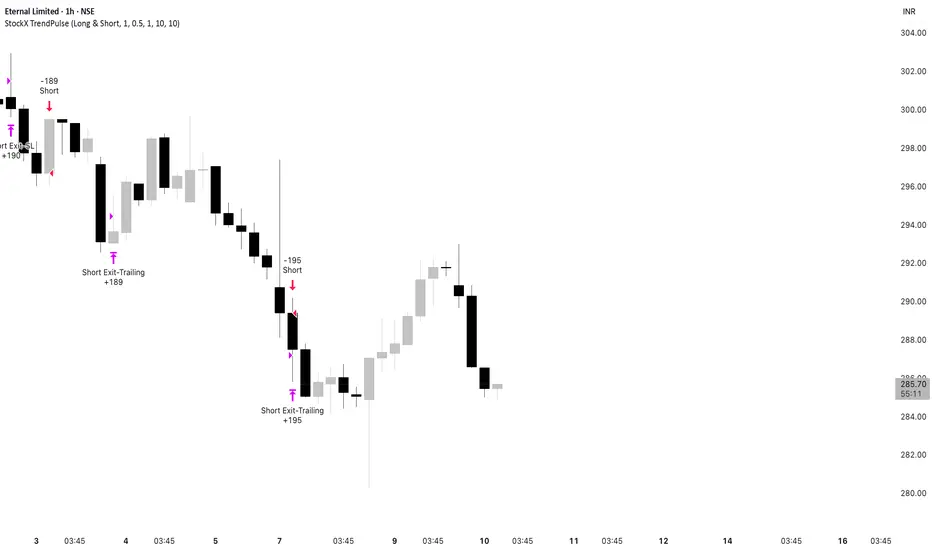

StockX TrendPulseThis is one of our premium, high-grade trading scripts built specifically for highly liquid stocks. It’s a fully automated system designed to deliver consistent performance, adapt to changing market conditions, and maintain strict risk control. With enhanced trade management and built-in performance tracking, it provides a reliable, disciplined framework for stock traders who demand precision and robustness.

StockX TrendPulse removes emotion from trading decisions and provides complete transparency through detailed performance metrics. The strategy is fully backtested and ready for live deployment.

Ready to Trade Like a Pro?

StockX TrendPulse is a premium strategy with limited availability.

Email brijamohanjha@gmail.com

to request access and pricing.

Reversal WaveThis is the type of quantitative system that can get you hated on investment forums, now that the Random Walk Theory is back in fashion. The strategy has simple price action rules, zero over-optimization, and is validated by a historical record of nearly a century on both Gold and the S&P 500 index.

Recommended Markets

SPX (Weekly, Monthly)

SPY (Monthly)

Tesla (Weekly)

XAUUSD (Weekly, Monthly)

NVDA (Weekly, Monthly)

Meta (Weekly, Monthly)

GOOG (Weekly, Monthly)

MSFT (Weekly, Monthly)

AAPL (Weekly, Monthly)

System Rules and Parameters

Total capital: $10,000

We will use 10% of the total capital per trade

Commissions will be 0.1% per trade

Condition 1: Previous Bearish Candle (isPrevBearish) (the closing price was lower than the opening price).

Condition 2: Midpoint of the Body The script calculates the exact midpoint of the body of that previous bearish candle.

• Formula: (Previous Open + Previous Close) / 2.

Condition 3: 50% Recovery (longCondition) The current candle must be bullish (green) and, most importantly, its closing price must be above the midpoint calculated in the previous step.

Once these parameters are met, the system executes a long entry and calculates the exit parameters:

Stop Loss (SL): Placed at the low of the candle that generated the entry signal.

Take Profit (TP): Calculated by projecting the risk distance upward.

• Calculation: Entry Price + (Risk * 1).

Risk:Reward Ratio of 1:1.

About the Profit Factor

In my experience, TradingView calculates profits and losses based on the percentage of movement, which can cause returns to not match expectations. This doesn’t significantly affect trending systems, but it can impact systems with a high win rate and a well-defined risk-reward ratio. It only takes one large entry candle that triggers the SL to translate into a major drop in performance.

For example, you might see a system with a 60% win rate and a 1:1 risk-reward ratio generating losses, even though commissions are under control relative to the number of trades.

My recommendation is to manually calculate the performance of systems with a well-defined risk-reward ratio, assuming you will trade using a fixed amount per trade and limit losses to a fixed percentage.

Remember that, even if candles are larger or smaller in size, we can maintain a fixed loss percentage by using leverage (in cases of low volatility) or reducing the capital at risk (when volatility is high).

Implementing leverage or capital reduction based on volatility is something I haven’t been able to incorporate into the code, but it would undoubtedly improve the system’s performance dramatically, as it would fix a consistent loss percentage per trade, preventing losses from fluctuating with volatility swings.

For example, we can maintain a fixed loss percentage when volatility is low by using the following formula:

Leverage = % of SL you’re willing to risk / % volatility from entry point to exit or SL

And if volatility is high and exceeds the fixed percentage we want to expose per trade (if SL is hit), we could reduce the position size.

For example, imagine we only want to risk 15% per SL on Tesla, where volatility is high and would cause a 23.57% loss. In this case, we subtract 23.57% from 15% (the loss percentage we’re willing to accept per trade), then subtract the result from our usual position size.

23.57% - 15% = 8.57%

Suppose I use $200 per trade.

To calculate 8.57% of $200, simply multiply 200 by 8.57/100. This simple calculation shows that 8.57% equals about $17.14 of the $200. Then subtract that value from $200:

$200 - $17.14 = $182.86

In summary, if we reduced the position size to $182.86 (from the usual $200, where we’re willing to lose 15%), no matter whether Tesla moves up or down 23.57%, we would still only gain or lose 15% of the $200, thus respecting our risk management.

Final Notes

The code is extremely simple, and every step of its development is detailed within it.

If you liked this strategy, which complements very well with others I’ve already published, stay tuned. Best regards.

specific breakout FiFTOStrategy Description: 10:14 Breakout Only

Overview This is a time-based intraday trading strategy designed to capture momentum bursts that occur specifically after the 10:14 AM candle closes. It operates on the logic that if price breaks the high of this specific candle within a short window, a trend continuation is likely.

Core Logic & Rules

The Setup Candle (10:14 AM)

The strategy waits specifically for the minute candle at 10:14 to complete.

Once this candle closes, the strategy records its High price.

Defining the Entry Level

It calculates a trigger price by taking the 10:14 High and adding a user-defined Buffer (e.g., +1 point).

Formula: Entry Level = 10:14 High + Buffer

The "Active Window" (Expiry)

The trade setup does not remain open all day. It has a strict time limit.

By default, the setup is valid from 10:15 to 10:20.

If the price does not break the Entry Level by the expiry time (default 10:20), the setup is cancelled and no trade is taken for the day.

Entry Trigger

If a candle closes above the Entry Level while the window is open, a Long (Buy) position is opened immediately.

Exits (Risk Management)

Stop Loss: A fixed number of points below the entry price.

Target: A fixed number of points above the entry price.

Visual & Automation Features

Visual Boxes: Upon entry, the strategy draws a "Long Position" style visual on the chart. A green box highlights the profit zone, and a red box highlights the loss zone. These boxes extend automatically until the trade closes.

JSON Alerts: The strategy is pre-configured to send data-rich alerts for automation (e.g., Telegram bots).

Entry Alert: Includes Symbol, Entry Price, SL, and TP.

Exit Alerts: Specific messages for "Target Hit" or "SL Hit".

Summary of User Inputs

Entry Buffer: Extra points added to the high to filter false breaks.

Fixed Stop Loss: Risk per trade in points.

Fixed Target: Reward per trade in points.

Expiry Minute: The minute (10:xx) at which the setup becomes invalid if not triggered.

AlasmarPrivet strategy in the beginning .

hope it will help to give you a good advice when to in and out from SPX500.

i test it in options only and you can use it and try if it works with stocks or no.

pls feel free to contact me if needed.

best regards,

Alasmar