[blackcat] L3 Market Pulse InsightOVERVIEW

The L3 Market Pulse Insight provides comprehensive analytics by evaluating key price metrics to reveal critical market sentiment and potential trade opportunities 📊🔍. This advanced indicator leverages proprietary calculations involving Simple Moving Averages (SMAs), Exponential Moving Averages (EMAs), and custom thresholds to deliver detailed insights into current market dynamics 🚀✨.

By plotting various lines representing core fundamentals and directional cues, traders gain visibility into underlying trends and shifts within the market pulse. The visual aids simplify complex data interpretation, making it easier for users to make strategic decisions based on clear, actionable information ✅⛈️.

FEATURES

Advanced Calculation Techniques:

Employs sophisticated formulas integrating SMAs and EMAs for precise trend analysis.

Incorporates fundamental lines and confirmations based on recent price extremes.

Comprehensive Visualization:

Plots multiple informational lines: Fundamental Line, Thresholds, Institutional Directions, etc., each reflecting unique aspects of price behavior.

Uses distinct colors for easy differentiation between bearish and bullish indications.

Customizable Alerts:

Generates "Buy" and "Sell" labels at pivotal moments, highlighting entry/exit points visually.

Offers flexibility to modify alert styles and positions according to user preferences.

Dynamic Adaptability:

Continuously updates plots and alerts based on incoming real-time data for timely responses.

Provides dynamic support/resistance levels adapting to evolving market conditions.

HOW TO USE

Installing the Indicator:

To start using the L3 Market Pulse Insight, add it via the Pine Editor on TradingView:

Open the editor from the bottom panel.

Copy-paste the provided script code.

Click “Add to Chart” after pasting.

Understanding Key Lines:

Familiarize yourself with what each plotted line signifies:

Fundamental Line: Represents core price movements adjusted through SMA transformations.

Low Confirmation & Warnings: Provide early signals about potential reversals or continuation scenarios.

Threshold B: Acts as a significant barrier indicating overbought/sold conditions.

Institutional Directions: Offer insights into larger player activities and intentions.

Interpreting Signals:

Pay close attention to generated "Buy" and "Sell" labels appearing directly on your chart:

"Buy" Label: Indicates favorable momentum crossing from below the confirmation level upwards.

"Sell" Label: Suggests bearish transitions when moving beneath set thresholds.

Adjusting Parameters:

While this version primarily uses default settings derived from optimal testing ranges, feel free to experiment:

Modify lookback periods in SMA/EMA functions if different timeframes align better with your strategy.

Customize plot colors/styles for enhanced readability and personal taste.

Integrating with Other Tools:

Enhance the reliability of signals produced by combining them with complementary indicators like RSI, MACD, or volume profiles for thorough validation.

Continuous Monitoring:

Regularly review performance and refine strategies incorporating insights gathered from L3 Market Pulse Insight across varying markets and assets.

LIMITATIONS

Data Dependency: Performance heavily relies on accurate historical data without anomalies.

Market Conditions Variability: Effectiveness may vary during extreme volatility or thin liquidity environments.

Parameter Fine-Tuning: Optimal configuration might differ significantly across instruments; continuous adjustments are necessary.

No Guarantees: Like any tool, this doesn't ensure profits and should be part of a broader analytical framework.

NOTES

Ensure solid grounding in technical analysis principles before deploying solely upon these insights.

Utilize backtesting rigorously under diverse market cycles to assess robustness thoroughly.

Consider external factors such as economic reports, geopolitical events influencing asset prices beyond purely statistical models.

Maintain discipline adhering predefined risk management protocols regardless of signal strength displayed here.

THANKS

We appreciate every member's contributions who have engaged actively throughout our development journey, offering constructive feedback driving improvements continually 🙏. Together we strive toward creating ever-more robust tools empowering traders worldwide!

中心震盪指標

[blackcat] L1 Swing Reversal IndexOVERVIEW

The indicator is crafted to assist traders in identifying potential swing reversal points within various markets 📈✨. This sophisticated tool combines elements from price deviations, smoothed moving averages, and relative strength indices (RSIs) to generate actionable trade signals, making it easier for users to spot lucrative entry/exit opportunities. By visualizing key market conditions through customizable plots and labels, this indicator simplifies complex analyses into straightforward decisions.

Ideal for day traders or swing traders looking to capitalize on short-to-medium-term trends, the offers invaluable insights into market sentiment changes enabling precise timing of trades.

FEATURES

Dynamic Price Deviation Calculation: Computes adaptive price deviations considering both typical prices and volatility metrics.

Smoothed Deviations: Utilizes dual-smoothing techniques ensuring accurate reflection of underlying trends without excessive noise interference.

Enhanced RSI Integration: Includes a modified version of Relative Strength Index providing clearer overbought/oversold conditions.

Visual Signal Representation:

Colored columns indicating bullish/bearish pressure levels directly on the chart.

Dynamic labels marking specific buy/sell conditions enhancing clarity.

Customizable Parameters: Allows tweaking smoothing, volatility, and RSI periods according to user preferences facilitating tailored usage.

Alert Notifications: Supports real-time alerts via TradingView’s integrated system keeping traders informed promptly ✅🔔.

HOW TO USE

Script Setup:

Save the provided code under Indicators > Add Custom Indicator in your TradingView workspace.

Name appropriately and activate across desired charts.

Parameter Adjustments:

Configure Smoothing, Volatility, and RSI periods based on preferred trading styles or asset characteristics:

Shorter durations suit fast-paced environments while longer ones align better with slower-moving assets.

Experiment iteratively optimizing settings maximizing accuracy for specific needs.

Interpreting Plots/Labels:

Observe colored columns representing current market sentiment:

Green columns signify bullish momentum suggesting possible buying opportunities.

Red columns indicate bearish tendencies hinting at selling chances.

Note dynamic "BUY" & "SELL" labels triggered under predefined criteria guiding timely actions.

Incorporating Signals:

Integrate these generated cues within broader strategies leveraging support/resistance lines, volume data, etc., ensuring robust validation before executing trades.

Cross-reference alongside other complementary tools (e.g., MACD, Bollinger Bands) for added confirmation bolstering decision-making confidence.

Setting Up Alerts:

Enable alert notifications corresponding to crucial conditions ensuring timely updates via TradingView’s notification infrastructure.

Fine-tune alert messages reflecting personal requirements maintaining seamless workflow integration.

Testing & Validation:

Conduct thorough backtesting employing historical datasets verifying effectiveness amidst varying market scenarios.

Continuously refine parameter configurations enhancing overall performance mitigating false positives/negatives.

EXAMPLE SCENARIOS

Short-Term Trades: Capitalize on fleeting reversals by focusing primarily on shorter-period RSIs combined with swift price deviation movements.

Swing Strategies: Utilize medium-range settings identifying intermediate trend shifts maximizing profit potentials while minimizing risks.

LIMITATIONS

Accuracy relies heavily upon correctly configured inputs; hence regular re-evaluation aligning evolving dynamics proves imperative.

Excessive dependence solely on this metric might lead to missed opportunities during sideways/choppy phases necessitating additional confirmatory indicators.

Always complement outputs with fundamental analyses securing comprehensive perspectives effectively managing associated risks.

NOTES

Educational Insights: Gain deeper understanding exploring underlying principles behind price deviations and their role in technical analysis fostering better comprehension.

Risk Management Protocols: Employ strict risk management practices encompassing stop-loss/profit targets preserving capital integrity amid unpredictable market fluctuations.

Continuous Learning: Stay abreast exploring emerging financial landscapes incorporating innovative methodologies augmenting script utility and relevance.

THANKS

Thanks go out to everyone contributing towards refining and improving this script. Your valuable feedback fuels ongoing enhancements propelling superior trading experiences!

Smart Trend Lines [The_lurker]

Smart Trend Lines

A multi-level trend classifier that detects bullish and bearish conditions using a methodology based on drawing trend lines—main, intermediate, and short-term—by identifying peaks and troughs. The tool highlights trend strength by applying filters such as the Average Directional Index (ADX) (A), Relative Strength Index (RSI) (R), and Volume (V), making it easier to interpret trend strength. The filter markers (V, A, R) in the Smart Trend Lines indicator are powerful tools for assessing the reliability of breakouts. Breakouts containing are the most reliable, as they indicate strong volume support, trend strength, and favorable momentum. Breakouts with partial filters (such as or ) require additional confirmation, while breakouts without filters ( ) should be avoided unless supported by other strong signals. By understanding the meaning of each filter and the market context.

Core Functionality

1. Trend Line Types

The indicator generates three distinct trend line categories, each serving a specific analytical purpose:

Main Trend Lines: These are long-term trend lines designed to capture significant market trends. They are calculated based on pivot points over a user-defined period (default: 50 bars). Main trend lines are ideal for identifying macro-level support and resistance zones.

Mid Trend Lines: These are medium-term trend lines (default: 21 bars) that focus on intermediate price movements. They provide a balance between short-term fluctuations and long-term trends, suitable for swing trading strategies.

Short Trend Lines: These are short-term trend lines (default: 9 bars) that track rapid price changes. They are particularly useful for scalping or day trading, highlighting immediate support and resistance levels.

Each trend line type can be independently enabled or disabled, allowing traders to tailor the indicator to their preferred timeframes.

2. Breakout Detection

The indicator employs a robust breakout detection system that identifies when the price crosses a trend line, signaling a potential trend reversal or continuation. Breakouts are validated using the following filters:

ADX Filter: The Average Directional Index (ADX) measures trend strength. A user-defined threshold (default: 20) ensures that breakouts occur during strong trends, reducing false signals in range-bound markets.

RSI Filter: The Relative Strength Index (RSI) identifies overbought or oversold conditions. Breakouts are filtered based on RSI thresholds (default: 65 for overbought, 35 for oversold) to avoid signals in extreme market conditions.

Volume Filter: Breakouts are confirmed only when trading volume exceeds a moving average (default: 20 bars) and aligns with the breakout direction (e.g., higher volume on bullish breakouts when the candle closes higher).

Breakout events are marked with labels on the chart, indicating the type of trend line broken (Main, Mid, or Short) and the filters satisfied (Volume, ADX, RSI). Alerts are triggered for each breakout, providing real-time notifications.

3. Customization Options

The indicator offers extensive customization through input settings, organized into logical groups for ease of use:

Main Trend Line Settings

Length: Defines the number of bars used to calculate pivot points (default: 50).

Bullish Color: Color for upward-sloping (bullish) main trend lines (default: green).

Bearish Color: Color for downward-sloping (bearish) main trend lines (default: red).

Style: Line style options include solid, dashed, or dotted (default: solid).

Mid Trend Line Settings

Length: Number of bars for mid-term pivot points (default: 21).

Show/Hide: Toggle visibility of mid trend lines (default: enabled).

Bullish Color: Color for bullish mid trend lines (default: lime).

Bearish Color: Color for bearish mid trend lines (default: maroon).

Style: Line style (default: dashed).

Short Trend Line Settings

Length: Number of bars for short-term pivot points (default: 9).

Show/Hide: Toggle visibility of short trend lines (default: enabled).

Bullish Color: Color for bullish short trend lines (default: teal).

Bearish Color: Color for bearish short trend lines (default: purple).

Style: Line style (default: dotted).

General Display Settings

Break Check Price: Selects the price type for breakout detection (Close, High, or Low; default: Close).

Show Previous Trendlines: Option to display historical main trend lines (default: disabled).

Label Size: Size of breakout labels (Tiny, Small, Normal, Large, Huge; default: Small).

Filter Settings

ADX Threshold: Minimum ADX value for trend strength confirmation (default: 25).

Volume MA Period: Period for the volume moving average (default: 20).

RSI Filter: Enable/disable RSI filtering (default: enabled).

RSI Upper Threshold: Upper RSI limit for overbought conditions (default: 65).

RSI Lower Threshold: Lower RSI limit for oversold conditions (default: 35).

4. Technical Calculations

The indicator relies on several technical calculations to ensure accuracy:

Pivot Points: Pivot highs and lows are detected using the ta.pivothigh and ta.pivotlow functions, with separate lengths for Main, Mid, and Short trend lines.

Slope Calculation: The slope of each trend line is calculated as the change in price divided by the change in bar index between two pivot points.

ADX Calculation: ADX is computed using a 14-period Directional Movement Index (DMI), with smoothing over 14 bars.

RSI Calculation: RSI is calculated over a 14-period lookback using the ta.rsi function.

Volume Moving Average: A simple moving average (SMA) of volume is used to determine if current volume exceeds the average.

5. Strict Mode Validation

To ensure the reliability of trend lines, the indicator employs a strict mode check:

For bearish trend lines, all prices between pivot points must remain below the projected trend line.

For bullish trend lines, all prices must remain above the projected trend line.

Post-pivot break checks ensure that no breakouts occur between pivot points, enhancing the validity of the trend line.

6. Trend Line Extension

Trend lines are dynamically extended forward until a breakout occurs. The extension logic:

Projects the trend line using the calculated slope.

Continuously validates the extension using strict mode checks.

Stops extension upon a breakout, fixing the trend line at the breakout point.

7. Alerts and Labels

Labels: Breakout labels are placed above (for bearish breakouts) or below (for bullish breakouts) the price bar. Labels include:

A prefix indicating the trend line type (B for Main, M for Mid, S for Short).

A suffix showing satisfied filters (e.g., for Volume, ADX, and RSI).

Alerts: Each breakout triggers a one-time alert per bar close, with a descriptive message indicating the trend line type and filters met.

Detailed Code Breakdown

1. Initialization and Inputs

The script begins by defining the indicator with indicator('Smart Trend Lines ', overlay = true), ensuring it overlays on the price chart. Input settings are grouped into categories (Main, Mid, Short, General Display, Filters) for user convenience. Each input includes a tooltip in both English and Arabic, enhancing accessibility.

2. Technical Indicator Calculations

Volume MA: Calculated using ta.sma(volume, volPeriod) to compare current volume against the average.

ADX: Computed using custom dirmov and adx functions, which calculate the Directional Movement Index and smooth it over 14 periods.

RSI: Calculated with ta.rsi(close, rsiPeriod) over 14 periods.

Price Selection: The priceToCheck function selects the price type (Close, High, or Low) for breakout detection.

3. Pivot Detection

Pivot points are detected using ta.pivothigh and ta.pivotlow for each trend line type. The lookback period is set to the respective trend line length (e.g., 50 for Main, 21 for Mid, 9 for Short).

4. Trend Line Logic

For each trend line type (Main, Mid, Short):

Bearish Trend Lines: Identified when two consecutive pivot highs form a downward slope. The script validates the trend line using strict mode and post-pivot break checks.

Bullish Trend Lines: Identified when two consecutive pivot lows form an upward slope, with similar validation.

Trend lines are drawn using line.new, with separate lines for the initial segment (between pivots) and the extended segment (from the second pivot forward).

5. Breakout Detection and Labeling

Breakouts are detected when the selected price crosses the trend line level. The script checks:

Volume conditions (above average and aligned with candle direction).

ADX condition (above threshold).

RSI condition (within thresholds if enabled). Labels are created with label.new, and alerts are triggered with alert.

6. Trend Line Extension

The extendTrendline function dynamically updates the trend line’s endpoint unless a breakout occurs. It uses strict mode checks to ensure the trend line remains valid.

7. Previous Trend Lines

If enabled, previous main trend lines are stored in arrays (previousBearishStartLines, previousBullishTrendLines, etc.) and displayed on the chart, providing historical context.

Disclaimer:

The information and publications are not intended to be, nor do they constitute, financial, investment, trading, or other types of advice or recommendations provided or endorsed by TradingView.

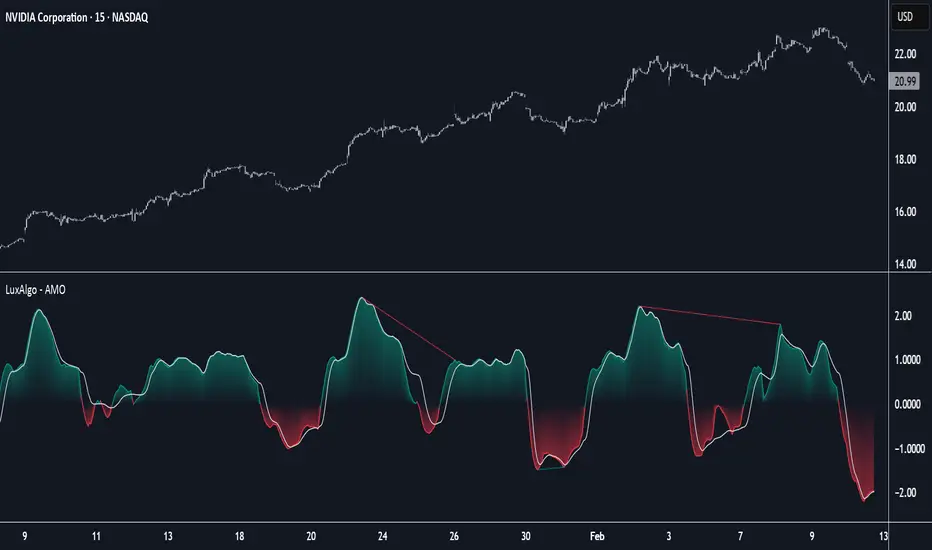

Adaptive Momentum Oscillator [LuxAlgo]The Adaptive Momentum Oscillator tool allows traders to measure the current relative momentum over a given period using the maximum delta in price.

It features a histogram with gradient color, divergences, and an adaptive moving average that allows traders to clearly see the smoothed trend direction.

🔶 USAGE

This unbounded oscillator has positive momentum when values are above 0 and negative momentum when values are below 0. The adaptive moving average is used as a minimum lag smoothing tool over the momentum histogram.

🔹 Signal Line

There are two main uses for the signal line drawn on the chart above.

Momentum crosses above or below the signal line: acceleration in momentum.

Signal line crosses the 0 value: positive or negative momentum.

🔹 Data Length

On the chart above, we can compare different length sizes and how the tool values change, allowing traders to get a shorter or longer-term view of current market strength.

🔹 Smoothing Length

In the previous figure, we can compare how different Smoothing Length values affect the oscillator output.

🔹 Divergences

The divergence detector is disabled by default. Traders can enable it and adjust the divergence length from the settings panel.

As we can see in the chart above, by changing the length of the divergences, traders can fine-tune their detection, a small number will detect smaller divergences, and use a larger number for larger divergences.

🔶 SETTINGS

Data: Select data source, close price by default

Data Length: Select the length for data gathering

Smoothing Length: Select the length for data smoothing

Divergences: Enable/Disable divergences detection and length

[blackcat] L2 Trend Guard OscillatorOVERVIEW

📊 The L2 Trend Guard Oscillator is a comprehensive technical analysis framework designed specifically to identify market trend reversals using adaptive filtering algorithms that combine price action dynamics with statistical measures of volatility and momentum.

Key Purpose:

Generate reliable early warning signals before major trend changes occur

Provide clear directional bias indicators aligned with institutional investor behavior patterns

Offer risk-managed entry/exit opportunities suitable for various timeframes

TECHNICAL FOUNDATION EXPLAINED

🎓 Core Mechanism Breakdown:

→ Advanced smoothing technique emphasizing recent data points more heavily than older ones

↓ Reduces lag while maintaining signal integrity compared to traditional MA approaches

• Short-term Momentum Assessment:

🔶 Relative strength between closing prices vs lower bounds

• Long-term Directional Bias Analysis:

📈 Extended timeframe comparison generating structural context

• Defense Level Generation:

➜ Protective boundary calculation incorporating EMAs for stability enhancement

PARAMETER CONFIGURATION GUIDE

🔧 Adjustable Settings Explained In Detail:

Timeframe Selection:**

↔ Controls lookback period sensitivity affecting responsiveness

↕ Adjusts reaction speed vs accuracy trade-off dynamically

Weight Factor Specification:**

⚡ Influences emphasis on newer versus historical observations

🎯 Defines key decision-making thresholds clearly

ALGORITHM EXECUTION FLOW

💻 Processing Sequence Overview:

:

→ Gather raw pricing inputs across required periods

↓ Normalize values preparing them for subsequent processing stages

:

✔ Calculate relative strength positions against established ranges

❌ Filter outliers maintaining signal integrity consistently

⟶ Apply dual-pass filtering reducing false signals effectively

➡ Generate actionable trading opportunities systematically

VISUALIZATION ARCHITECTURE

🎨 Display Elements Designated Purpose:

🔵 Primary Indicator Traces:

→ Aqua Trace: Buy/Sell Signal Progression

↑ Red Line: Opposing Force Boundary

🟥 Gray Dashed: Zero Reference Point

🏷️ Label System For Critical Events:

✅ BUY: Bullish Opportunity Markers

❌ SELL: Bearish Setup Validations

STRATEGIC IMPLEMENTATION FRAMEWORK

📋 Practical Deployment Steps:

Initial Integration Protocol:

• Select appropriate timeframe matching strategy objectives

• Configure input parameters aligning with target asset behavior traits

• Conduct thorough backtesting under simulated environments initially

Active Monitoring Procedures:

→ Regular observation of labeled event placements versus actual movements

↓ Track confirmation patterns leading up to signaled opportunities carefully

↑ Evaluate overall framework reliability across different regime types regularly

Execution Guidelines Formulation:

✔ Enter positions only after achieving minimum number of confirming inputs

❌ Avoid isolated occurrences lacking adequate supporting evidence always

➞ Look for convergent factors strengthening conviction before acting decisively

PERFORMANCE OPTIMIZATION TECHNIQUES

🚀 Continuous Improvement Strategies:

Parameter Calibration Approach:

✓ Start testing default suggested configurations thoroughly

↕ Gradually adjust individual components observing outcome changes methodically

✨ Document findings building personalized version profile incrementally

Context Adaptability Methods:

🔄 Add supplementary indicators enhancing overall reliability when needed

🔧 Remove unnecessary complexity layers avoiding confusion/distracted decisions

💫 Incorporate custom rules adapting specific security behaviors effectively

Efficiency Improvement Tactics:

⚙️ Streamline redundant computational routines wherever possible efficiently

♻️ Leverage shared data streams minimizing resource utilization significantly

⏳ Optimize refresh frequencies balancing update speed vs overhead properly

[blackcat] L3 Smart Money FlowCOMPREHENSIVE ANALYSIS OF THE L3 SMART MONEY FLOW INDICATOR

🌐 OVERVIEW:

The L3 Smart Money Flow indicator represents a sophisticated multi-dimensional analytics tool combining traditional momentum measurements with advanced institutional investor tracking capabilities. It's particularly effective at identifying large-scale capital movement dynamics that often precede significant price shifts.

Core Objectives:

• Detect subtle but meaningful price action anomalies indicating major player involvement

• Provide clear entry/exit markers based on multiple validated criteria

• Offer risk-managed positioning strategies suitable for various account sizes

• Maintain operational efficiency even during high volatility regimes

THEORETICAL BACKDROP AND METHODOLOGY

🎓 Conceptual Foundation Principles:

Utilizes Time-Varying Moving Averages (TVMA) responding adaptively to changing market states

Implements Extended Smoothing Algorithm (XSA) providing enhanced filtration characteristics

Employs asymmetric weight distribution favoring recent price observations over historical ones

→ Analyzes price-weighted closing prices incorporating volume influence indirectly

← Applies Asymmetric Local Maximum (ALMA) filters generating institution-specific trends

⟸ Combines multiple temporal perspectives producing robust directional assessments

✓ Calculates normalized momentum ratios comparing current state against extended range extremes

✗ Filters out insignificant fluctuations via double-stage verification process

⤾ Generates actionable alerts upon exceeding predefined significance boundaries

CONFIGURABLE PARAMETERS IN DEPTH

⚙️ Input Customization Options Detailed Explanation:

Temporal Resolution Control:

→ TVMA Length Setting:

Minimum value constraint ensuring mathematical validity

Higher numbers increase smoothing effect reducing reaction velocity

Lower intervals enhance responsiveness potentially increasing noise exposure

Validation Threshold Definition:

↓ Bull-Bear Boundary Level:

Establishes fundamental acceptance/rejection zones

Typically set near extreme values reflecting rare occurrence probability

Can be adjusted per instrument liquidity profiles if necessary

ADVANCED ALGORITHMIC PROCEDURES BREAKDOWN

💻 Internal Operation Architecture:

Base Calculations Infrastructure:

☑ Raw Data Preparation and Normalization

☐ High/Low/Closing Aggregation Processes

☒ Range Estimation Algorithms

Intermediate Transform Engine:

📈 Momentum Ratio Computation Workflow

↔ First Pass XSA Application Details

➖ Second Stage Refinement Mechanics

Final Output Synthesis Framework:

➢ Composite Reading Compilation Logic

➣ Validation Status Determination Process

➤ Alert Trigger Decision Making Structure

INTERACTIVE VISUAL INTERFACE COMPONENTS

🎨 User Experience Interface Elements:

🔵 Plotting Series Hierarchy:

→ Primary FundFlow Signal: White trace marking core oscillator progression

↑ Secondary Confirmation Overlay: Orange/Yellow highlighting validation status

🟥 Risk/Reward Boundaries: Aqua line delineating strategic areas requiring attention

🏷️ Interactive Marker System:

✔ "BUY": Green upward-pointing labels denoting confirmed long entries

❌ "SELL": Red downward-facing badges signaling short setups

PRACTICAL APPLICATION STRATEGY GUIDE

📋 Operational Deployment Instructions:

Strategic Planning Initiatives:

• Define precise profit targets considering realistic reward/risk scenarios

→ Set maximum acceptable loss thresholds protecting available resources adequately

↓ Develop contingency plans addressing unexpected adverse developments promptly

Live Trading Engagement Protocols:

→ Maintaining vigilant monitoring of label placement activities continuously

↓ Tracking order fill success rates across implemented grids regularly

↑ Evaluating system effectiveness compared alternative methodologies periodically

Performance Optimization Techniques:

✔ Implement incremental improvements iteratively throughout lifecycle

❌ Eliminate ineffective component variations systematically

⟹ Ensure proportional growth capability matching user needs appropriately

EFFICIENCY ENHANCEMENT APPROACHES

🚀 Ongoing Development Strategy:

Resource Management Focus Areas:

→ Minimizing redundant computation cycles through intelligent caching mechanisms

↓ Leveraging parallel processing capabilities where feasible efficiently

↑ Optimizing storage access patterns improving response times substantially

Scalability Consideration Factors:

✔ Adapting to varying account sizes/market capitalizations seamlessly

❌ Preventing bottlenecks limiting concurrent operation capacity

⟹ Ensuring balanced growth capability matching evolving requirements accurately

Maintenance Routine Establishment:

✓ Regular codebase updates incorporation keeping functionality current

↓ Periodic performance audits conducting verifying continued effectiveness

↑ Documentation refinement updating explaining any material modifications made

SYSTEMATIC RISK CONTROL MECHANISMS

🛡️ Comprehensive Protection Systems:

Position Sizing Governance:

∅ Never exceed predetermined exposure limitations strictly observed

± Scale entries proportionally according to available resources carefully

× Include slippage allowances within planning stages realistically

Emergency Response Procedures:

↩ Well-defined exit strategies including trailing stops activation logic

🌀 Contingency plan formulation covering worst-case scenario contingencies

⇄ Recovery procedure documentation outlining restoration steps methodically

CoffeeShopCrypto Supply Demand PPO AdvancedCoffeeShopCrypto PPO Advanced is a structure-aware momentum oscillator and price-trend overlay designed to help traders interpret momentum strength, exhaustion, and continuation across evolving market conditions. It’s not a “buy/sell” signal tool — it's a momentum context tool that helps confirm trend intent.

Original Code derived from the Price Oscillator Indicators (PPO) found in the TradingView Technical Indicators categories. You can view the info and calculation for the original PPO here

www.tradingview.com

Much like the MACD, the PPO uses a couple lagging indicators to present Momentum as a percentage. But it lacks context to market structure.

What It’s Based On

This tool is based on a dual-moving-average PPO oscillator structure (Percentage Price Oscillator) enhanced by:

Oscillator pivot structure: detection of Lower Highs (LH) and Higher Lows (HL) inside the oscillator.

Detection of Supply and Demand Trends via Market Absorption

Ability to transfer its average plots to price action

Detection of Trend Exhaustion

Real-time price-based exhaustion levels: projecting potential future supply and demand using trendlines from weakening momentum.

Integrated fast and slow Moving Averages on price using the same inputs as the oscillator, to visualize alignment between short- and long-term trends.

These elements combine momentum context with price action in a visual, intuitive system.

How It Works

1. Oscillator Structure

LHs (above zero): momentum weakening in uptrends.

HLs (below zero): momentum strengthening in downtrends.

Only valid pivots are shown (e.g., an LH must be preceded by a valid LL).

2. Exhaustion Levels

Green demand lines: price is making new lows, but oscillator prints HL → potential exhaustion.

Red supply lines: price is making new highs, but oscillator prints LH → potential exhaustion.

These lines are future-facing, projecting likely reaction zones based on momentum weakening.

3. Moving Averages on Price

Two MAs are drawn on the price chart:

Fast MA (same length as PPO short input)

Slow MA (same length as PPO long input)

These are not signal lines — they're visual guides for trend alignment.

MA crossover = PO crosses zero. This indicates short- and long-term momentum are syncing — a powerful signal of trend conviction.

When price is above both MAs, and the PO is rising above zero, bullish momentum is dominant.

When price is below both MAs, and the PO is falling below zero, bearish momentum dominates.

How Traders Can Use It

✅ Spot Trend Initiation

Wait for clear trend confirmation in price.

Use PPO Momentum+ to confirm momentum structure is aligned (e.g., HH/HL in oscillator + price above both MAs).

🔁 Track Continuations

In uptrends, look for oscillator HH and HL sequences with price holding above both MAs.

In downtrends, seek LL and LH sequences with price below both MAs.

⚠️ Watch for Exhaustion

Price breaking below red (supply) lines after oscillator LH = bearish exhaustion signal.

Price breaking above green (demand) lines after oscillator HL = bullish exhaustion signal.

These levels act like pre-mapped S/R zones, showing where momentum previously failed and price may react.

Why This Is Different

Momentum tools often lag or mislead when used blindly. This tool visualizes structural failure in momentum and maps potential outcomes. The integration of oscillator and price-based tools ensures traders are always reading context, not just raw signals.

Demand Trendlines

Demand trendlines show us Wykoff's law of "Absorbed Supply Reversal" In real time.

When aggressive selling pressure is persistently absorbed by passive buying interest without significant downward price continuation, and supply becomes exhausted, the market structure shifts as demand regains control—resulting in a directional reversal to the upside.

This commonly happens in a 3 phase interaction of price.

1. Selling pressure is absorbed quickly by buyers.

This PPO tool will calculate the trend of this absorption process

2. After there is a notable Bearish Exhaustion of price action, the PPO tool will draw a trendline of this absorption showing us the potential future prices where aggressive buyers will want to step in at lower prices.

3. After higher lows are defined in the oscillator, you'll see prices react in a strong bullish pattern at this trendline where aggressive buyers stepped in to reverse price action to the upside.

Supply Trendlines

Supply trendlines show us Wykoff's law of "Absorbed Demand Reversal" In real time.

When aggressive buying pressure is persistently absorbed by passive selling interest without significant downward price continuation, and demand becomes exhausted, the market structure shifts as supply regains control—resulting in a directional reversal to the downside.

This commonly happens in a 3 phase interaction of price.

1. Buying pressure is absorbed quickly by sellers.

This PPO tool will calculate the trend of this absorption process.

2. After there is a notable Bullish Exhaustion of price action, the PPO tool will draw a trendline of this absorption showing us the potential future prices where aggressive sellers will want to step in at higher prices.

3. After lower highs are defined in the oscillator, you'll see prices react in a strong bearish pattern at this trendline where aggressive sellers stepped in to reverse price action to the downside.

Lower High and Higher Low Signals

When the oscillator signals Lower Highs or High Lows its only noting that momentum in that trend direction is slowing. THis indicates a coming pause in the market and the proceeding longs of an uptrend or shorts of a downtrend should be taken with caution.

**These LH and HL markers are not reading as divergences in price vs momentum.**

They are simply registering against the highs and lows of itself..

Moving Averages on Price Action

The Oscillator will cross over its ZERO level the same time your Short and Long MAs cross each other. This will indicate that the short term average trend is moving ahead of the long term.

Crossovers are not an entry signal. It's a method in determining you current timeframe trend strength. Always observe price action as it passes through each of your moving averages and compare it to the positioning and direction of the oscillator.

If price dips in between the moving averages while the oscillator still shows a strong trend strength, you can wait for price to move ahead of your fast moving average.

Bar Colors and Signal Line for Trend Strength

Good Bullish Trend = Oscillator above zero + Signal rising below Oscillator

Weak Bullish Trend = Oscillator above zero + Signal above Oscillator

Good Bearish Trend = Oscillator below zero + Signal falling above Oscillator

Weak Bearish Trend = Oscillator below zero + Signal below Oscillator

Bar Colors

Bars are colored to match Oscillator Momentum Strength. Colors are set by user.

Why alter the known PPO (Percentage Price Oscillator) in this manner?

The PPO tool is great for measuring the strength as percentage of price action over and average amount of candles however, with these changes,

you know have the ability to correlate:

Wycoff theory of supply and demand,

Measure the depth of reversals and pullback by price positioning against moving averages,

Project potential reversal and exhaustion pricing,

Visibly note the structure of momentum much like you would note market structure,

Its not enough to know there is momentum. Its better to know

A) Is it enough

B) Is there something in the way which will cause price to push back

C) Does this momentum correlate to the prevailing trend

Parameter Free RSI [InvestorUnknown]The Parameter Free RSI (PF-RSI) is an innovative adaptation of the traditional Relative Strength Index (RSI), a widely used momentum oscillator that measures the speed and change of price movements. Unlike the standard RSI, which relies on a fixed lookback period (typically 14), the PF-RSI dynamically adjusts its calculation length based on real-time market conditions. By incorporating volatility and the RSI's deviation from its midpoint (50), this indicator aims to provide a more responsive and adaptable tool for identifying overbought/oversold conditions, trend shifts, and momentum changes. This adaptability makes it particularly valuable for traders navigating diverse market environments, from trending to ranging conditions.

PF-RSI offers a suite of customizable features, including dynamic length variants, smoothing options, visualization tools, and alert conditions.

Key Features

1. Dynamic RSI Length Calculation

The cornerstone of the PF-RSI is its ability to adjust the RSI calculation period dynamically, eliminating the need for a static parameter. The length is computed using two primary factors:

Volatility: Measured via the standard deviation of past RSI values.

Distance from Midpoint: The absolute deviation of the RSI from 50, reflecting the strength of bullish or bearish momentum.

The indicator offers three variants for calculating this dynamic length, allowing users to tailor its responsiveness:

Variant I (Aggressive): Increases the length dramatically based on volatility and a nonlinear scaling of the distance from 50. Ideal for traders seeking highly sensitive signals in fast-moving markets.

Variant II (Moderate): Combines volatility with a scaled distance from 50, using a less aggressive adjustment. Strikes a balance between responsiveness and stability, suitable for most trading scenarios.

Variant III (Conservative): Applies a linear combination of volatility and raw distance from 50. Offers a stable, less reactive length adjustment for traders prioritizing consistency.

// Function that returns a dynamic RSI length based on past RSI values

// The idea is to make the RSI length adaptive using volatility (stdev) and distance from the RSI midpoint (50)

// Different "variant" options control how aggressively the length changes

parameter_free_length(free_rsi, variant) =>

len = switch variant

// Variant I: Most aggressive adaptation

// Uses standard deviation scaled by a nonlinear factor of distance from 50

// Also adds another distance-based term to increase length more dramatically

"I" => math.ceil(

ta.stdev(free_rsi, math.ceil(free_rsi)) *

math.pow(1 + (math.ceil(math.abs(50 - (free_rsi - 50))) / 100), 2)

) +

(

math.ceil(math.abs(free_rsi - 50)) *

(1 + (math.ceil(math.abs(50 - (free_rsi - 50))) / 100))

)

// Variant II: Moderate adaptation

// Adds the standard deviation and a distance-based scaling term (less nonlinear)

"II" => math.ceil(

ta.stdev(free_rsi, math.ceil(free_rsi)) +

(

math.ceil(math.abs(free_rsi - 50)) *

(1 + (math.ceil(math.abs(50 - (free_rsi - 50))) / 100))

)

)

// Variant III: Least aggressive adaptation

// Simply adds standard deviation and raw distance from 50 (linear scaling)

"III" => math.ceil(

ta.stdev(free_rsi, math.ceil(free_rsi)) +

math.ceil(math.abs(free_rsi - 50))

)

2. Smoothing Options

To refine the dynamic RSI and reduce noise, the PF-RSI provides smoothing capabilities:

Smoothing Toggle: Enable or disable smoothing of the dynamic length used for RSI.

Smoothing MA Type for RSI MA: Choose between SMA and EMA

Smoothing Length Options for RSI MA:

Full: Uses the entire calculated dynamic length.

Half: Applies half of the dynamic length for smoother output.

SQRT: Uses the square root of the dynamic length, offering a compromise between responsiveness and smoothness.

The smoothed RSI is complemented by a separate moving average (MA) of the RSI itself, further enhancing signal clarity.

3. Visualization Tools

The PF-RSI includes visualization options to help traders interpret market conditions at a glance.

Plots:

Dynamic RSI: Displayed as a white line, showing the adaptive RSI value.

RSI Moving Average: Plotted in yellow, providing a smoothed reference for trend and momentum analysis.

Dynamic Length: A secondary plot (in faint white) showing how the calculation period evolves over time.

Histogram: Represents the RSI’s position relative to 50, with color gradients.

Fill Area: The space between the RSI and its MA is filled with a gradient (green for RSI > MA, red for RSI < MA), highlighting momentum shifts.

Customizable bar colors on the price chart reflect trend and momentum:

Trend (Raw RSI): Green (RSI > 50), Red (RSI < 50).

Trend (RSI MA): Green (MA > 50), Red (MA < 50).

Trend (Raw RSI) + Momentum: Adds momentum shading (lighter green/red when RSI and MA diverge).

Trend (RSI MA) + Momentum: Similar, but based on the MA’s trend.

Momentum: Green (RSI > MA), Red (RSI < MA).

Off: Disables bar coloring.

Intrabar Updating: Optional real-time updates within each bar for enhanced responsiveness.

4. Alerts

The PF-RSI supports customizable alerts to keep traders informed of key events.

Trend Alerts:

Raw RSI: Triggers when the RSI crosses above (uptrend) or below (downtrend) 50.

RSI MA: Triggers when the moving average crosses 50.

Off: Disables trend alerts.

Momentum Alerts:

Triggers when the RSI crosses its moving average, indicating rising (RSI > MA) or declining (RSI < MA) momentum.

Alerts are fired once per bar close, with descriptive messages including the ticker symbol (e.g., " Uptrend on: AAPL").

How It Works

The PF-RSI operates in a multi-step process:

Initialization

On the first run, it calculates a standard RSI with a 14-period length to seed the dynamic calculation.

Dynamic Length Computation

Once seeded, the indicator switches to a dynamic length based on the selected variant, factoring in volatility and distance from 50.

If smoothing is enabled, the length is further refined using an SMA.

RSI Calculation

The adaptive RSI is computed using the dynamic length, ensuring it reflects current market conditions.

Moving Average

A separate MA (SMA or EMA) is applied to the RSI, with a length derived from the dynamic length (Full, Half, or SQRT).

Visualization and Alerts

The results are plotted, and alerts are triggered based on user settings.

This adaptive approach minimizes lag in fast markets and reduces false signals in choppy conditions, offering a significant edge over fixed-period RSI implementations.

Why Use PF-RSI?

The Parameter Free RSI stands out by eliminating the guesswork of selecting an RSI period. Its dynamic length adjusts to market volatility and momentum, providing timely signals without manual tweaking.

Liquid Pulse Liquid Pulse by Dskyz (DAFE) Trading Systems

Liquid Pulse is a trading algo built by Dskyz (DAFE) Trading Systems for futures markets like NQ1!, designed to snag high-probability trades with tight risk control. it fuses a confluence system—VWAP, MACD, ADX, volume, and liquidity sweeps—with a trade scoring setup, daily limits, and VIX pauses to dodge wild volatility. visuals include simple signals, VWAP bands, and a dashboard with stats.

Core Components for Liquid Pulse

Volume Sensitivity (volumeSensitivity) controls how much volume spikes matter for entries. options: 'Low', 'Medium', 'High' default: 'High' (catches small spikes, good for active markets) tweak it: 'Low' for calm markets, 'High' for chaos.

MACD Speed (macdSpeed) sets the MACD’s pace for momentum. options: 'Fast', 'Medium', 'Slow' default: 'Medium' (solid balance) tweak it: 'Fast' for scalping, 'Slow' for swings.

Daily Trade Limit (dailyTradeLimit) caps trades per day to keep risk in check. range: 1 to 30 default: 20 tweak it: 5-10 for safety, 20-30 for action.

Number of Contracts (numContracts) sets position size. range: 1 to 20 default: 4 tweak it: up for big accounts, down for small.

VIX Pause Level (vixPauseLevel) stops trading if VIX gets too hot. range: 10 to 80 default: 39.0 tweak it: 30 to avoid volatility, 50 to ride it.

Min Confluence Conditions (minConditions) sets how many signals must align. range: 1 to 5 default: 2 tweak it: 3-4 for strict, 1-2 for more trades.

Min Trade Score (Longs/Shorts) (minTradeScoreLongs/minTradeScoreShorts) filters trade quality. longs range: 0 to 100 default: 73 shorts range: 0 to 100 default: 75 tweak it: 80-90 for quality, 60-70 for volume.

Liquidity Sweep Strength (sweepStrength) gauges breakouts. range: 0.1 to 1.0 default: 0.5 tweak it: 0.7-1.0 for strong moves, 0.3-0.5 for small.

ADX Trend Threshold (adxTrendThreshold) confirms trends. range: 10 to 100 default: 41 tweak it: 40-50 for trends, 30-35 for weak ones.

ADX Chop Threshold (adxChopThreshold) avoids chop. range: 5 to 50 default: 20 tweak it: 15-20 to dodge chop, 25-30 to loosen.

VWAP Timeframe (vwapTimeframe) sets VWAP period. options: '15', '30', '60', '240', 'D' default: '60' (1-hour) tweak it: 60 for day, 240 for swing, D for long.

Take Profit Ticks (Longs/Shorts) (takeProfitTicksLongs/takeProfitTicksShorts) sets profit targets. longs range: 5 to 100 default: 25.0 shorts range: 5 to 100 default: 20.0 tweak it: 30-50 for trends, 10-20 for chop.

Max Profit Ticks (maxProfitTicks) caps max gain. range: 10 to 200 default: 60.0 tweak it: 80-100 for big moves, 40-60 for tight.

Min Profit Ticks to Trail (minProfitTicksTrail) triggers trailing. range: 1 to 50 default: 7.0 tweak it: 10-15 for big gains, 5-7 for quick locks.

Trailing Stop Ticks (trailTicks) sets trail distance. range: 1 to 50 default: 5.0 tweak it: 8-10 for room, 3-5 for fast locks.

Trailing Offset Ticks (trailOffsetTicks) sets trail offset. range: 1 to 20 default: 2.0 tweak it: 1-2 for tight, 5-10 for loose.

ATR Period (atrPeriod) measures volatility. range: 5 to 50 default: 9 tweak it: 14-20 for smooth, 5-9 for reactive.

Hardcoded Settings volLookback: 30 ('Low'), 20 ('Medium'), 11 ('High') volThreshold: 1.5 ('Low'), 1.8 ('Medium'), 2 ('High') swingLen: 5

Execution Logic Overview trades trigger when confluence conditions align, entering long or short with set position sizes. exits use dynamic take-profits, trailing stops after a profit threshold, hard stops via ATR, and a time stop after 100 bars.

Features Multi-Signal Confluence: needs VWAP, MACD, volume, sweeps, and ADX to line up.

Risk Control: ATR-based stops (capped 15 ticks), take-profits (scaled by volatility), and trails.

Market Filters: VIX pause, ADX trend/chop checks, volatility gates. Dashboard: shows scores, VIX, ADX, P/L, win %, streak.

Visuals Simple signals (green up triangles for longs, red down for shorts) and VWAP bands with glow. info table (bottom right) with MACD momentum. dashboard (top right) with stats.

Chart and Backtest:

NQ1! futures, 5-minute chart. works best in trending, volatile conditions. tweak inputs for other markets—test thoroughly.

Backtesting: NQ1! Frame: Jan 19, 2025, 09:00 — May 02, 2025, 16:00 Slippage: 3 Commission: $4.60

Fee Typical Range (per side, per contract)

CME Exchange $1.14 – $1.20

Clearing $0.10 – $0.30

NFA Regulatory $0.02

Firm/Broker Commis. $0.25 – $0.80 (retail prop)

TOTAL $1.60 – $2.30 per side

Round Turn: (enter+exit) = $3.20 – $4.60 per contract

Disclaimer this is for education only. past results don’t predict future wins. trading’s risky—only use money you can lose. backtest and validate before going live. (expect moderators to nitpick some random chart symbol rule—i’ll fix and repost if they pull it.)

About the Author Dskyz (DAFE) Trading Systems crafts killer trading algos. Liquid Pulse is pure research and grit, built for smart, bold trading. Use it with discipline. Use it with clarity. Trade smarter. I’ll keep dropping badass strategies ‘til i build a brand or someone signs me up.

2025 Created by Dskyz, powered by DAFE Trading Systems. Trade smart, trade bold.

Sine Swing OscillatorThe Sine Swing Oscillator (SSO) is a custom momentum indicator that transforms price movement into a sine-based oscillator ranging from -1 to +1. It does this by measuring the deviation of the current price from a reference price, which is updated at fixed bar intervals. The price deviation is normalized using the Average True Range (ATR) over the same interval, then mapped through a sine transformation to create a bounded oscillator. This transformation helps identify cyclical price behavior in a consistent range.

The resulting sine values are smoothed using a Simple Moving Average (SMA), and a signal line is derived by applying an Exponential Moving Average (EMA) to the smoothed oscillator. Traders can use signal line crossovers, or moves through the zero line, to help identify potential entry or exit signals based on cyclical momentum shifts.

The oscillator and signal line are plotted in a separate pane, with user-configurable smoothing lengths and colors. The zero line is also included for reference.

MACD-V with Volatility Normalisation [DCD]MACD-V with Volatility Normalisation

This indicator is a modified version of the traditional MACD, designed to account for market volatility by normalizing the MACD line using the Average True Range (ATR). It provides a more adaptive approach to identifying momentum shifts and potential trend reversals. This indicator was developed by Alex Spiroglou in this paper:

Spiroglou, Alex, MACD-V: Volatility Normalised Momentum (May 3, 2022).

Features:

Volatility Normalization: The MACD line is adjusted using ATR to standardize its values across different market conditions.

Customizable Parameters: Users can adjust the MACD fast length, slow length, signal line smoothing, and ATR length to suit their trading style.

Histogram Visualization: The histogram highlights the difference between the MACD and signal lines, with customizable colors for positive and negative momentum.

Crossover Signals: Green and red dots indicate bullish and bearish crossovers between the MACD and signal lines.

Background Highlighting: The chart background changes to green when the MACD is above 0 and red when it is below 0, providing a clear visual cue for bullish and bearish conditions.

Horizontal Levels: Dotted horizontal lines are plotted at key levels for better visualization of MACD values.

How to Use:

Look for crossovers between the MACD and signal lines to identify potential buy or sell signals.

Use the histogram to gauge the strength of momentum.

Pay attention to the background color for quick identification of bullish (green) or bearish (red) conditions.

This indicator is ideal for traders who want a more dynamic MACD that adapts to market volatility. Customize the settings to align with your trading strategy and timeframe.

New Momentum H/LNew Momentum H/L shows when momentum, defined as the rate of price change over time, exceeds the highest or lowest values observed over a user-defined period. These events shows points where momentum reaches new extremes relative to that period, and the indicator plots a column to mark each occurrence.

Increase in momentum could indicate the start of a trend phase from a low volatile or balanced state. However in developed trends, extreme momentum could also mark potential climaxes which can lead to trend termination. This reflects the dual nature of the component.

This indicator is based on the MACD calculated as the difference between a 3-period and a 10-period simple moving average. New highs are indicated when this value exceeds all previous values within the lookback window; new lows when it drops below all previous values. The default lookback period is set to 40 bars, which corresponds with two months on a daily chart.

The indicator also computes a z-score of the MACD line over the past 100 bars. This standardization helps compare momentum across different periods and normalizes the values of current moves relative to recent history.

In practice, use the indicator to confirm presence of momentum at the start of a move from a balanced state (often following a volatility expansion), track how momentum develops inside of a trend structure and locate potential climactic events.

Momentum should in preference be interpreted from price movement. However, to measure and standardize provides structure and helps build more consistent models. This should be used in context of price structure and broader market conditions; as all other tools.

Price OI Division Price OI Division Indicator

Overview

The Price OI Division indicator (`P_OI_D`) is a custom TradingView script designed to analyze the relationship between price momentum and open interest (OI) momentum. It visualizes the divergence between these two metrics using a modified MACD (Moving Average Convergence Divergence) approach, normalized to percentage values. The indicator is plotted as a histogram and two lines (MACD and Signal), with color-coded signals for easier interpretation.

Key Features

- Normalized Price MACD : Compares short-term and long-term price momentum.

- OI-Adjusted MACD : Incorporates open interest data to reflect market positioning.

- Divergence Histogram : Highlights the difference between price and OI momentum.

- Signal Line : Smoothed EMA of the divergence for trend confirmation.

- Threshold Lines : Horizontal reference lines at ±10% and 0 for quick visual analysis.

Interpretation Guide

- Bullish Signal :

Histogram turns red (positive & increasing).

MACD (red line) crosses above Signal (blue line).

Divergence above +10% indicates extreme bullish conditions.

- Bearish Signal :

Histogram turns green (negative & increasing).

MACD (lime line) crosses below Signal (maroon line).

Divergence below -10% indicates extreme bearish conditions.

- Neutral/Reversal :

Histogram fading (teal/pink) suggests weakening momentum.

Crossings near the Zero Line may signal trend shifts.

Usage Notes

Asset Compatibility : Works best with futures/perpetual contracts where OI data is available.

Timeframe : Suitable for all timeframes, but align `fastLength`/`slowLength` with your strategy.

Data Limitations : Relies on exchange-specific OI symbols (e.g., `BTC:USDT.P_OI`). Verify data availability for your asset.

Confirmation : Pair with volume analysis or support/resistance levels for higher accuracy.

Disclaimer

This indicator is for educational purposes only. Trading decisions should not be based solely on this tool. Always validate signals with additional analysis and risk management.

Dual-Phase Trend Regime Oscillator (Zeiierman)█ Overview

Trend Regime: Dual-Phase Oscillator (Zeiierman) is a volatility-sensitive trend classification tool that dynamically switches between two oscillators, one optimized for low volatility, the other for high volatility.

By analyzing standard deviation-based volatility states and applying correlation-derived oscillators, this indicator reveals not only whether the market is trending but also what kind of trend regime it is in —Bullish or Bearish —and how that regime reacts to market volatility.

█ Its Uniqueness

Most trend indicators assume a static market environment; they don't adjust their logic when the underlying volatility shifts. That often leads to false signals in choppy conditions or late entries in trending phases.

Trend Regime: Dual-Phase Oscillator solves this by introducing volatility-aware adaptability. It switches between a slow, stable oscillator in calm markets and a fast, reactive oscillator in volatile ones, ensuring the right sensitivity at the right time.

█ How It Works

⚪ Volatility State Engine

Calculates returns-based volatility using standard deviation of price change

Smooths the current volatility with a moving average

Builds a volatility history window and performs median clustering to determine typical "Low" and "High" volatility zones

Dynamically assigns the chart to one of two internal volatility regimes: Low or High

⚪ Dual Oscillators

In Low Volatility, it uses a Slow Trend Oscillator (longer lookback, smoother)

In High Volatility, it switches to a Fast Trend Oscillator (shorter lookback, responsive)

Both oscillators use price-time correlation as a measure of directional strength

The output is normalized between 0 and 1, allowing for consistent interpretation

⚪ Trend Regime Classification

The active oscillator is compared to a neutral threshold (0.5)

If above: Bullish Regime, if below: Bearish Regime, else: Neutral

The background and markers update to reflect regime changes visually

Triangle markers highlight bullish/bearish regime shifts

█ How to Use

⚪ Identify Current Trend Regime

Use the background color and chart table to immediately recognize whether the market is trending up or down.

⚪ Trade Regime Shifts

Use triangle markers (▲ / ▼) to spot fresh regime entries, which are ideal for confirming breakouts within trends.

⚪ Pullback Trading

Look for pullbacks when the trend is in a stable condition and the slow oscillator remains consistently near the upper or lower threshold. Watch for moments when the fast oscillator retraces back toward the midline, or slightly above/below it — this often signals a potential pullback entry in the direction of the prevailing trend.

█ Settings Explained

Length (Slow Trend Oscillator) – Used in calm conditions. Longer = smoother signals

Length (Fast Trend Oscillator) – Used in volatile conditions. Shorter = more responsive

Volatility Refit Interval – Controls how often the system recalculates Low/High volatility levels

Current Volatility Period – Lookback used for immediate volatility measurement

Volatility Smoothing Length – Applies an SMA to the raw volatility to reduce noise

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

AP_Ultimate CCI MTF v5**AP Ultimate CCI Multi-Timeframe Indicator**

*Track Commodity Channel Index trends across multiple timeframes in one view!*

**Overview:**

Adapted from ChrisMoody's popular RSI MTF concept, this enhanced version brings powerful multi-timeframe analysis to the CCI indicator. Perfect for traders who want to confirm trends across different time horizons without switching charts.

**Key Features:**

📈 **Dual CCI Analysis**

- Primary CCI (Default: 1H) + Secondary CCI (Default: 4H)

- Fully customizable timeframes for both indicators

- Independent length settings (14-50 periods recommended)

🚦 **Visual Trading Signals**

- Automatic Buy/Sell markers on crossovers

- 🟢 **B** Signals: When CCI crosses above -100 (Oversold reversal)

- 🔴 **S** Signals: When CCI crosses below +100 (Overbought reversal)

- Clean triangular markers at chart edges for clear visibility

🎨 **Customizable Visuals**

- Adjustable overbought/oversold levels (Default: ±100)

- Background highlights for extreme zones

- Modern color schemes with transparency control

- Optional zero line display

⚙️ **Technical Specs**

- Built in Pine Script v6

- Non-repainting calculations

- Timeframe-aware alerts support

- Optimized for all asset classes

**How to Use (my use case):**

1. Apply to 15M-4H charts for intraday trading

2. Default setup: Compare 1H vs 4H CCI

3. Look for confluence between timeframes:

- Strong trend = Both CCIs moving in same direction

- Reversal signal = Crossovers with volume confirmation

4. Combine with price action or support/resistance

**Why this Indicator:**

✅ Eliminates manual timeframe switching

✅ Identifies hidden divergences between time horizons

✅ Works equally well for stocks, forex, and crypto

✅ Perfect for momentum and mean-reversion strategies

*Pro Tip: Pair with volume indicators and moving averages for enhanced confirmation!*

MACD Multi-Timeframe x4 (Custom Params)■About this indicator

・This indicator can display 4 MACD lines for different time frames. (Multi-time framework)

・The color of the MACD line changes when the MACD has a golden or dead cross.

All MACDs can be set individually for long time period, short time period, and signal smoothing.

All MACDs can show/hide MACD lines, signal lines, histograms, and select colors.

■Explanation of effective usage

By displaying MACDs in multiple time frames, you can time the push.

For example, let's say you have three MACDs: one weekly, one daily, and one hour.

With the weekly and daily MACDs continuing to golden cross, the timing for the hourly MACD to golden cross is considered a push opportunity.

An example chart is attached below for your reference.

The area circled vertically is a push-buying opportunity.

Yellow-green: Weekly Green: Daily Light blue: Hourly

-------------------------------------------------------------------------------------------------------------

■このインジケーターについて

・このインジケーターは別の時間軸の4本のMACDを表示させることが出来ます。(マルチタイムフレームワーク)

・MACDがゴールデンクロス・デッドクロスした場合にMACDラインの色が変化します。

・全てのMACDについて個別に長期の期間・短期の期間・シグナルの平滑化を設定できます。

・全てのMACDはMACDライン・シグナルライン・ヒストグラムの表示/非表示、色の選択ができます。

■有効な使い方の説明

マルチタイムフレームでMACDを表示することで、押し目のタイミングを計ることが出来ます。

例えば、3本のMACDを1週間・1日・1時間とします。

週足と日足のMACDがゴールデンクロスを継続した状態で、1時間足のMACDがゴールデンクロスしてくるタイミングは押し目買いのチャンスと考えられます。

以下に例題のチャートを付けますので、参考にしてください。

縦に囲った辺りが押し目買いのチャンスになります。

黄緑:週足 緑:日足 水色:1時間足

Quad Rotation StochasticQuad Rotation Stochastic

The Quad Rotation Stochastic is a powerful and unique momentum oscillator that combines four different stochastic setups into one tool, providing an incredibly detailed view of market conditions. This multi-timeframe stochastic approach helps traders better anticipate trend continuations, reversals, and momentum shifts with greater precision than traditional single stochastic indicators.

Why this indicator is useful:

Multi-layered Momentum Analysis: Instead of relying on one stochastic, this script tracks four independent stochastic readings, smoothing out noise and confirming stronger signals.

Advanced Divergence Detection: It automatically identifies bullish and bearish divergences for each stochastic, helping traders spot potential reversals early.

Background Color Alerts: When a configurable number (e.g., 3 or 4) of the stochastics agree in direction and position (overbought/oversold), the background colors green (bullish) or red (bearish) to give instant visual cues.

ABCD Pattern Recognition: The script recognizes "shield" patterns when Stochastic 4 remains stuck at extreme levels (above 90 or below 10) for a set time, warning of potential trend continuation setups.

Super Signal Alerts: If all four stochastics align in extreme conditions and slope in the same direction, the indicator plots a special "Super Signal," offering high-confidence entry opportunities.

Why this indicator is unique:

Quad Confirmation Logic: Combining four different stochastics makes this tool much less prone to false signals compared to using a single stochastic.

Customizable Divergence Coloring: Traders can choose to have divergence lines automatically match the stochastic color for clear visual association.

Adaptive ABCD Shields: Innovative use of bar counting while a stochastic remains extreme acts as a "shield," offering a unique way to filter out minor fake-outs.

Flexible Configuration: Each stochastic's sensitivity, divergence settings, and visual styling can be fully customized, allowing traders to adapt it to their own strategy and asset.

Example Usage: Trading Bitcoin with Quad Rotation Stochastic

When trading Bitcoin (BTCUSD), you might set the minimum count (minCount) to 3, meaning three out of four stochastics must be in agreement to trigger a background color.

If the background turns green, and you notice an ABCD Bullish Shield (Green X), you might look for bullish candlestick patterns or moving average crossovers to enter a long trade.

Conversely, if the background turns red and a Super Down Signal appears, it suggests high probability for further downside, giving you strong confirmation to either short BTC or avoid entering new longs.

By combining divergence signals with background colors and the ABCD shields, the Quad Rotation Stochastic provides a layered confirmation system that gives traders greater confidence in their entries and exits — particularly in fast-moving, volatile markets like Bitcoin.

Institutional Composite Moving Average (ICMA) [Volume Vigilante]Institutional Composite Moving Average (ICMA)

The Next Evolution of Moving Averages — Built for Real Traders.

ICMA blends the strength of four powerful averages (SMA, EMA, WMA, HMA) into a single ultra-responsive, ultra-smooth signal.

It reacts faster than traditional MAs while filtering out noise, giving you clean trend direction with minimal lag.

🔹 Key Features:

• Faster reaction than SMA, EMA, or WMA individually

• Smoother and more stable than raw HMA

• Naturally adapts across trend, momentum, and consolidation conditions

• Zero gimmicks. Zero repainting. Full institutional quality.

🔹 Designed For:

• Scalping

• Swing trading

• Signal engines

• Algorithmic systems

📎 How to Use:

• Overlay it on any chart

• Fine-tune the length per timeframe

• Combine with your entries/exits for maximum edge

Created by Volume Vigilante 🧬 — Delivering Real-World Trading Tools.

RSI Strength & Consolidation Zones (Zeiierman)█ Overview

RSI Strength & Consolidation Zones (Zeiierman) is a hybrid momentum and volatility visualization tool that blends enhanced RSI interpretation with ADX-driven consolidation detection. This indicator doesn't just show where RSI is trending — it interprets how strong that trend is, when that strength changes, and where the market may be consolidating in anticipation of breakout movement.

Using a combination of Kalman-filtered RSI, custom-built DMI/ADX, and low-volatility zone recognition, it gives traders a dynamic RSI with strength-based coloring, while also highlighting consolidation zones to spot breakout opportunities.

█ Its uniqueness

Traditional RSI indicators lack context. They may show you when the market is overbought or oversold, but they won’t tell you how strong that condition is, or whether it’s likely to result in continuation or consolidation.

This tool aims to solve that by introducing adaptive strength metrics and structural compression zones, allowing traders to anticipate when the market is likely preparing for a move.

█ How It Works

⚪ Enhanced RSI

Combines traditional RSI and a custom RSI implementation

Smooths both through a Kalman filter for trend direction

Final RSI line reflects smoothed consensus between manual and built-in RSI

Adds an RSI + Strength overlay to show when the directional conviction is increasing

⚪ ADX-Driven Strength Layer

Directional Movement Index (DMI) is calculated both manually and with built-in smoothing

The average ADX value is used to calculate a strength modifier

When ADX exceeds 20, RSI is dynamically enhanced or dampened to reflect directional force

Resulting visual: RSI appears stronger or weaker based on confirmed trend conditions

⚪ Consolidation Zone Detection

When ADX falls below 20, the indicator enters a consolidation zone state

Boxes are drawn dynamically to contain the price within these low-volatility structures

Once the price breaks out of the zone, the indicator plots a breakout signal (▲ or ▼)

⚪ Breakouts

Breakout markers are placed at the first close outside the consolidation box

These signals serve as early indicators for potential trend continuation or reversal

█ How to Use

⚪ Confirm Momentum Strength

Use the RSI + Strength line to determine whether current momentum is backed by trend conviction. If strength expands alongside rising RSI, the move has confirmation.

⚪ Consolidations Zones

When RSI is around the midline, and a consolidation box appears, expect lower volatility and a range-bound market, followed by a breakout.

⚪ Use Breakout Signals for Entry

Look for ▲ or ▼ markers as early triggers. These often coincide with volume expansions or structural breaks.

█ Settings Explained

RSI Length – Number of bars used for RSI. Shorter = more sensitive.

DMI Length – Used in both custom and built-in ADX/DI calculations.

ADX Smoothing – Smooths the trend strength signal. Higher values = smoother strength detection.

Trend Confirmation (Filter Strength) – Adjusts the responsiveness of the Kalman filter.

-----------------

Disclaimer

The content provided in my scripts, indicators, ideas, algorithms, and systems is for educational and informational purposes only. It does not constitute financial advice, investment recommendations, or a solicitation to buy or sell any financial instruments. I will not accept liability for any loss or damage, including without limitation any loss of profit, which may arise directly or indirectly from the use of or reliance on such information.

All investments involve risk, and the past performance of a security, industry, sector, market, financial product, trading strategy, backtest, or individual's trading does not guarantee future results or returns. Investors are fully responsible for any investment decisions they make. Such decisions should be based solely on an evaluation of their financial circumstances, investment objectives, risk tolerance, and liquidity needs.

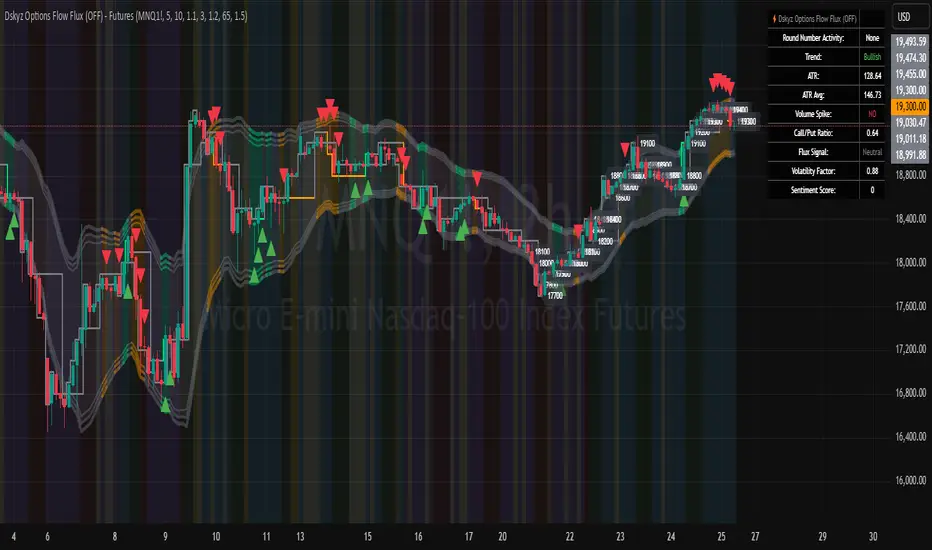

Dskyz Options Flow Flux (OFF) - FuturesDskyz Options Flow Flux (OFF) - Futures

*This is a repost due to moderator intervention on use of ™ in my scripts. I'm in the process of getting this rectified. This was originally posted around mid-night CDT.

🧠 The Dskyz Options Flow Flux (OFF) - Futures indicator is a game changer for futures traders looking to tap into institutional activity with limited resources. Designed for TradingView this tool simulates options flow data (call/put volume and open interest) for futures contracts like MNQ MES NQ and ES giving u actionable insights through volume spike detection volatility adjustments and stunning visuals like aurora flux bands and round number levels. Whether u’re a beginner learning the ropes or a pro hunting for an edge this indicator delivers real time market sentiment and key price levels to boost ur trading game

Key Features

⚡ Simulated Options Flow: Breaks down call/put volume and open interest using market momentum and volatility

📈 Spike Detection: Spots big moves in volume and open interest with customizable thresholds

🧠 Volatility Filter: Adapts to market conditions using ATR for smarter spike detection

✨ Aurora Flux Bands: Glows with market sentiment showing u bullish or bearish vibes at a glance

🎯 Round Number Levels: Marks key psychological levels where big players might step in

📊 Interactive Dashboard: Real time metrics like sentiment score and volatility factor right on ur chart

🚨 Alerts: Get notified of bullish or bearish spikes so u never miss a move

How It Works

🧠 This indicator is built to make complex options flow analysis simple even with the constraints of Pine Script. Here’s the step by step:

Simulated Volume Data (Dynamic Split):

Pulls daily volume for ur chosen futures contract (MNQ1! MES1! NQ1! ES1!)

Splits it into call and put volume based on momentum (ta.mom) and volatility (ATR vs its 20 period average)

Estimates open interest (OI) for calls and puts (1.15x for calls 1.1x for puts)

Formula: callRatio = 0.5 + (momentum / close) * 10 + (volatility - 1) * 0.1 capped between 0.3 and 0.7

Why It Matters: Mimics how big players might split their trades giving u a peek into institutional sentiment

Spike Detection:

Compares current volume/OI to short term (lookbackShort) and long term (lookbackLong) averages

Flags spikes when volume/OI exceeds the average by ur set threshold (spikeThreshold for regular highConfidenceThreshold for strong)

Adjusts for volatility so u’re not fooled by choppy markets

Output: optionsSignal (2 for strong bullish -2 for strong bearish 1 for bullish -1 for bearish 0 for neutral)

Why It Matters: Pinpoints where big money might be stepping in

Volatility Filter:

Uses ATR (10 periods) and its 20 period average to calculate a volatility factor (volFactor = ATR / avgAtr)

Scales spike thresholds based on market conditions (volAdjustedThreshold = spikeThreshold * max(1 volFactor * volFilter))

Why It Matters: Keeps ur signals reliable whether the market is calm or wild

Sentiment Score:

Calculates a call/put ratio (callVolume / putVolume) and adjusts for volatility

Converts it to a 0 to 100 score (higher = bullish lower = bearish)

Formula: sentimentScore = min(max((volAdjustedSentiment - 1) * 50 0) 100)

Why It Matters: Gives u a quick read on market bias

Round Number Detection:

Finds the nearest round number (e.g. 100 for MNQ1! 50 for MES1!)

Checks for volume spikes (volume > 3 period SMA * spikeThreshold) and if price is close (within ATR * atrMultiplier)

Updates the top activity level every 15 minutes when significant activity is detected

Why It Matters: Highlights psychological levels where price often reacts

Visuals and Dashboard:

Combines aurora flux bands glow effects round number lines and a dashboard to make insights pop (see Visual Elements below)

Plots triangles for call/put spikes (green/red for strong lime/orange for regular)

Sets up alerts for key market moves

Why It Matters: Makes complex data easy to read at a glance

Inputs and Customization

⚙️ Beginners can tweak these settings to match their trading style while pros can dig deeper for precision:

Futures Symbol (symbol): Pick ur contract (MNQ1! MES1! NQ1! ES1!). Default: MNQ1!