Accumulation & Distribution Days HistogramWHAT IT TRACKS:

• Distribution Days (Selling Pressure): Price closes down >0.2% on higher volume than previous day

• Accumulation Days (Buying Pressure): Price closes up >0.2% on higher volume than previous day

HOW IT WORKS:

The histogram displays a rolling count of distribution and accumulation days within your chosen lookback period (default: 20 bars). Green bars show accumulation days above the zero line, while red bars show distribution days below the zero line. A white line plots the net difference (accumulation minus distribution) to show the overall balance.

SETTINGS:

• Lookback Period: Number of bars to count (default: 20)

• Price Threshold: Minimum % move required (default: 0.2%)

• Colors: Fully customizable histogram colors

USAGE:

Use this to gauge the balance between buying and selling pressure. When accumulation exceeds distribution, it suggests bullish pressure. When distribution exceeds accumulation, it suggests bearish pressure.

The indicator can also serve as a market health filter:

• 0-3 Distribution Days: Bullish market condition - healthy for long positions

• 4-5 Distribution Days: Cautious - monitor for potential trend change

• 6+ Distribution Days: Bearish signal - institutional selling intensifying

Other potential uses to explore:

• Divergence analysis: Price making new highs while distribution days cluster

• Sector rotation: Compare distribution/accumulation across different sectors

• Entry timing: Wait for accumulation to exceed distribution before entering

• Risk management: Reduce position size as distribution days increase

Experiment with different lookback periods and thresholds to match your trading timeframe and style.

If you discover effective ways to use this indicator, please share in the comments below - your insights could help others, enjoy.

Distribution

Chaikin Oscillator Z-Score With Divergences [MAXmks]Hello Traders,

This is my take on the Chaikin Oscillator — statistically normalized into a Z-Score with built-in divergence detection.

The problem with raw Chaikin

The standard ChO is unbounded and extremely sensitive to volume spikes. A single anomalous bar can flatten the entire oscillator, making it hard to compare signals across time or between instruments.

The fix

Z-Score normalization with asinh (inverse hyperbolic sine) transformation. While standard Z-Scores assume a normal distribution, market data often features "fat tails" (extreme outliers). This transformation compresses those spikes effectively, ensuring the indicator remains responsive without getting stuck during high-volatility events. The result: a more comparable scale across instruments.

What's inside:

Adaptive normalization + EMA-based variance for smooth Z calculation

Regular and hidden divergence detection with segment validation (fewer false signals)

Gradient coloring that intensifies toward extremes

Dashboard with current Z value

Pre-built alerts for OB/OS entries/exits and all divergence types

Note: This is a volume-based indicator. No volume = no signal. If you see "No Volume Data" in the dashboard, switch to a data source that provides volume.

Works on any timeframe. Feedback welcome.

For analysis purposes, not financial advice.

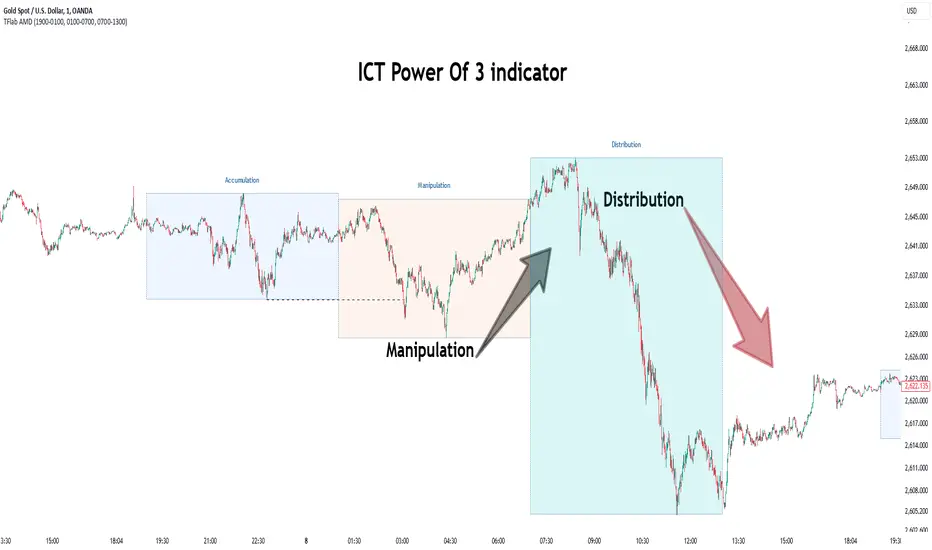

eBacktesting - Learning: Power of 3eBacktesting - Learning: Power of 3 highlights ICT’s “Power of 3” intraday story:

- Accumulation: price builds a quiet range

- Manipulation: a sweep grabs liquidity above or below that range (the classic stop hunt)

- Distribution: the real move expands away from that range, often in the opposite direction of the sweep

Use it to train your eyes to recognize when price is likely “setting up” vs when the session is actually “moving,” and to build a clean daily narrative around liquidity and expansion.

These indicators are built to pair perfectly with the eBacktesting extension, where traders can practice these concepts step-by-step. Backtesting concepts visually like this is one of the fastest ways to learn, build confidence, and improve trading performance.

Educational use only. Not financial advice.

Wyckoff Map (TR + S/D + Springs/Upthrusts)Wyckoff Map is a context-aware market structure overlay that visualizes key Wyckoff concepts directly on the price chart — without repainting and without relying on black-box signals.

Instead of generating isolated buy/sell alerts, this tool maps the environment in which price is operating, helping traders understand where supply and demand are interacting, where liquidity is being swept, and which phase the market is likely in.

What the script shows

Trading Range (TR)

Automatically detects a recent trading range

Displays the range as a shaded box for immediate context

Supply & Demand Zones

Demand zone near the range low (buyers’ area)

Supply zone near the range high (sellers’ area)

Zones adapt dynamically as the range evolves

Wyckoff Events

Spring: downside liquidity sweep followed by a reclaim (potential accumulation behavior)

Upthrust: upside liquidity sweep followed by failure (potential distribution behavior)

Events are filtered by range context and optional volume confirmation

Market Phase (Heuristic)

Labels the current environment as:

Accumulation

Distribution

Neutral Trading Range

Markup / Markdown

Phase is inferred from price position within the range and moving-average slope

Legend & Visual Guidance

A floating legend explains all zones and events

Designed to remain readable during replay and live trading

How to use

This script is not a standalone trading strategy.

It is best used to:

Avoid chasing breakouts into supply

Identify failed breakdowns near demand

Recognize accumulation vs distribution behavior

Add context to lower-timeframe entries

Combine with your own execution model (structure, risk, or order flow)

Higher-timeframe context is strongly recommended.

⚙️ Customization

You can adjust:

Trading range length

Zone thickness (ATR-based)

Pivot sensitivity

Volume confirmation

Event confirmation strictness

Visibility of zones, events, phase labels, and legend

Disclaimer

Wyckoff analysis is contextual and probabilistic, not deterministic.

This tool visualizes structural behavior — it does not predict future price.

Use proper risk management.

TL;DR (Short Description)

A non-repainting Wyckoff market structure overlay that maps trading ranges, supply/demand zones, Springs, Upthrusts, and accumulation/distribution phases directly on the chart.

RSI Distribution [Kodexius]RSI Distribution is a statistics driven visualization companion for the classic RSI oscillator. In addition to plotting RSI itself, it continuously builds a rolling sample of recent RSI values and projects their distribution as a forward drawn histogram, so you can see where RSI has spent most of its time over the selected lookback window.

The indicator is designed to add context to oscillator readings. Instead of only treating RSI as a single point estimate that is either “high” or “low”, you can evaluate the current RSI level relative to its own recent history. This makes it easier to recognize when the market is operating inside a familiar regime, and when RSI is pushing into rarer tail conditions that tend to appear during momentum bursts, exhaustion, or volatility expansion.

To complement the histogram, the script can optionally overlay a Gaussian curve fitted to the sample mean and standard deviation. It also runs a Jarque Bera normality check, based on skewness and excess kurtosis, and surfaces the result both visually and in a compact dashboard. On the oscillator panel itself, RSI is presented with a clean gradient line and standard overbought and oversold references, with fills that become more visible when RSI meaningfully extends beyond key thresholds.

🔹 Features

1. Distribution Histogram of Recent RSI Values

The script stores the last N RSI values in an internal sample and uses that rolling window to compute a frequency distribution across a user selected number of bins. The histogram is drawn into the future by a configurable width in bars, which keeps it readable and prevents it from colliding with the active RSI plot. The result is a compact visual summary of where RSI clusters most often, whether it is spending more time near the center, or shifting toward higher or lower regimes.

2. Gaussian Overlay for Shape Intuition

If enabled, a fitted bell curve is drawn on top of the histogram using the sample mean and standard deviation. This overlay is not intended as a direct trading signal. Its purpose is to provide a fast visual comparator between the empirical RSI distribution and a theoretical normal shape. When the histogram diverges strongly from the curve, you can quickly spot skew, heavy tails, or regime changes that often occur when market structure or volatility conditions shift.

3. Jarque Bera Normality Check With Clear PASS/FAIL Feedback

The script computes skewness and excess kurtosis from the RSI sample, then forms the Jarque Bera statistic and compares it to a fixed 95% critical value. When the distribution is closer to normal under this test, the status is marked as PASS, otherwise it is marked as FAIL. This result is displayed in the dashboard and can also influence the histogram styling, giving immediate feedback about whether the recent RSI behavior resembles a bell shaped distribution or a more distorted, regime driven profile.

Jarque Bera is a goodness of fit test that evaluates whether a dataset looks consistent with a normal distribution by checking two shape properties: skewness (asymmetry) and kurtosis (tail heaviness, expressed here as excess kurtosis where a perfect normal has 0). Under the null hypothesis of normality, skewness should be near 0 and excess kurtosis should be near 0. The test combines deviations in both into a single statistic, which is then compared to a chi square threshold. A PASS in this script means the sample does not show strong evidence against normality at the chosen threshold, while a FAIL means the sample is meaningfully skewed, heavy tailed, or both. In practical trading terms, a FAIL often suggests RSI is behaving in a regime where extremes and asymmetry are more common, which is typical during strong trends, volatility expansions, or one sided market pressure. It is still a statistical diagnostic, not a prediction tool, and results can vary with lookback length and market conditions.

4. Integrated Stats Dashboard

A compact table in the top right summarizes key distribution moments and the normality result: Mean, StdDev, Skewness, Kurtosis, and the JB statistic with PASS/FAIL text. Skewness is color coded by sign to quickly distinguish right skew (more time at higher RSI) versus left skew (more time at lower RSI), which can be helpful when diagnosing trend bias and momentum persistence.

5. RSI Visual Quality and Context Zones

RSI is plotted with a gradient color scheme and standard overbought and oversold reference lines. The overbought and oversold areas are filled with a smart gradient so visual emphasis increases when RSI meaningfully extends beyond the 70 and 30 regions, improving readability without overwhelming the panel.

🔹 Calculations

This section summarizes the main calculations and transformations used internally.

1. RSI Series

RSI is computed from the selected source and length using the standard RSI function:

rsi_val = ta.rsi(rsi_src, rsi_len)

2. Rolling Sample Collection

A float array stores recent RSI values. Each bar appends the newest RSI, and if the array exceeds the configured lookback, the oldest value is removed. Conceptually:

rsi_history.push(rsi_val)

if rsi_history.size() > lookback

rsi_history.shift()

This maintains a fixed size window that represents the most recent RSI behavior.

3. Mean, Variance, and Standard Deviation

The script computes the sample mean across the array. Variance is computed as sample variance using (n - 1) in the denominator, and standard deviation is the square root of that variance. These values serve both the dashboard display and the Gaussian overlay parameters.

4. Skewness and Excess Kurtosis

Skewness is calculated from the standardized third central moment with a small sample correction. Kurtosis is computed as excess kurtosis (kurtosis minus 3), so the normal baseline is 0. These two metrics summarize asymmetry and tail heaviness, which are the core ingredients for the Jarque Bera statistic.

5. Jarque Bera Statistic and Decision Rule

Using skewness S and excess kurtosis K, the Jarque Bera statistic is computed as:

JB = (n / 6.0) * (S^2 + 0.25 * K^2)

Normality is flagged using a fixed critical value:

is_normal = JB < 5.991

This produces a simple PASS/FAIL classification suitable for fast chart interpretation.

6. Histogram Binning and Scaling

The RSI domain is treated as 0 to 100 and divided into a configurable number of bins. Bin size is:

bin_size = 100.0 / bins

Each RSI sample maps to a bin index via floor(rsi / bin_size), with clamping to ensure the index stays within valid bounds. The script counts occurrences per bin, tracks the maximum frequency, and normalizes each bar height by freq/max_freq so the histogram remains visually stable and comparable as the window updates.

7. Gaussian Curve Overlay (Optional)

The Gaussian overlay uses the normal probability density function with mu as the sample mean and sigma as the sample standard deviation:

normal_pdf(x) = (1 / (sigma * sqrt(2*pi))) * exp(-0.5 * ((x - mu)/sigma)^2)

For drawing, the script samples x across the histogram width, evaluates the PDF, and normalizes it relative to its peak so the curve fits within the same visual height scale as the histogram.

MFI Volume Profile [Kodexius]The MFI Volume Profile indicator blends a classic volume profile with the Money Flow Index so you can see not only where volume traded, but also how strong the buying or selling pressure was at those prices. Instead of showing a simple horizontal histogram of volume, this tool adds a money flow dimension and turns the profile into a price volume momentum heat map.

The script scans a user controlled lookback window and builds a set of price levels between the lowest and highest price in that period. For every bar inside that window, its volume is distributed across the price levels that the bar actually touched, and that volume is combined with the bar’s MFI value. This creates a volume weighted average MFI for each price level, so every row of the profile knows both how much volume traded there and what the typical money flow condition was when that volume appeared.

On the chart, the indicator plots a stack of horizontal boxes to the right of current price. The length of each box represents the relative amount of volume at that price, while the color represents the average MFI there. Levels with stronger positive money flow will lean toward warmer shades, and levels with weaker or negative money flow will lean toward cooler or more neutral shades inside the configured MFI band. Each row is also labeled in the format Volume , so you can instantly read the exact volume and money flow value at that level instead of guessing.

This gives you a detailed map of where the market really cared about price, and whether that interest came with strong inflow or outflow. It can help you spot areas of accumulation, distribution, absorption, or exhaustion, and it does so in a compact visual that sits next to price without cluttering the candles themselves.

Features

Combined volume profile and MFI weighting

The indicator builds a volume profile over a user selected lookback and enriches each price row with a volume weighted average MFI. This lets you study both participation and money flow at the same price level.

Volume distributed across the bar price range

For every bar in the window, volume is not assigned to a single price. Instead, it is proportionally distributed across all price rows between the bar low and bar high. This creates a smoother and more realistic profile of where trading actually happened.

MFI based color gradient between 30 and 70

Each price row is colored according to its average MFI. The gradient is anchored between MFI values of 30 and 70, which covers typical oversold, neutral and overbought zones. This makes strong demand or distribution areas easier to spot visually.

Configurable structure resolution and depth

Main user inputs are the lookback length, the number of rows, the width of the profile in bars, and the label text size. You can quickly switch between coarse profiles for a big picture and higher resolution profiles for detailed structure.

Numeric labels with volume and MFI per row

Every box is labeled with the total volume at that level and the average MFI for that level, in the format Volume . This gives you exact values while still keeping the visual profile clean and compact.

Calculations

Money Flow Index calculation

currentMfi is calculated once using ta.mfi(hlc3, mfiLen) as usual,

Creation of the profileBins array

The script creates an array named profileBins that will hold one VPBin element per price row.

Each VPBin contains

volume which is the total volume accumulated at that price row

mfiProduct which is the sum of volume multiplied by MFI for that row

The loop;

for i = 0 to rowCount - 1 by 1

array.push(profileBins, VPBin.new(0.0, 0.0))

pre allocates a clean structure with zero values for all rows.

Finding highest and lowest price across the lookback

The script starts from the current bar high and low, then walks backward through the lookback window

for i = 0 to lookback - 1 by 1

highestPrice := math.max(highestPrice, high )

lowestPrice := math.min(lowestPrice, low )

After this loop, highestPrice and lowestPrice define the full price range covered by the chosen lookback.

Price range and step size for rows

The code computes

float rangePrice = highestPrice - lowestPrice

rangePrice := rangePrice == 0 ? syminfo.mintick : rangePrice

float step = rangePrice / rowCount

rangePrice is the total height of the profile in price terms. If the range is zero, the script replaces it with the minimum tick size for the symbol. Then step is the price height of each row. This step size is used to map any price into a row index.

Processing each bar in the lookback

For every bar index i inside the lookback, the script checks that currentMfi is not missing. If it is valid, it reads the bar high, low, volume and MFI

float barTop = high

float barBottom = low

float barVol = volume

float barMfi = currentMfi

Mapping bar prices to bin indices

The bar high and low are converted into row indices using the known lowestPrice and step

int indexTop = math.floor((barTop - lowestPrice) / step)

int indexBottom = math.floor((barBottom - lowestPrice) / step)

Then the indices are clamped into valid bounds so they stay between zero and rowCount - 1. This ensures that every bar contributes only inside the profile range

Splitting bar volume across all covered bins

Once the top and bottom indices are known, the script calculates how many rows the bar spans

int coveredBins = indexTop - indexBottom + 1

float volPerBin = barVol / coveredBins

float mfiPerBin = volPerBin * barMfi

Here the total bar volume is divided equally across all rows that the bar touches. For each of those rows, the same fraction of volume and volume times MFI is used.

Accumulating into each VPBin

Finally, a nested loop iterates from indexBottom to indexTop and updates the corresponding VPBin

for k = indexBottom to indexTop by 1

VPBin binData = array.get(profileBins, k)

binData.volume := binData.volume + volPerBin

binData.mfiProduct := binData.mfiProduct + mfiPerBin

Over all bars in the lookback window, each row builds up

total volume at that price range

total volume times MFI at that price range

Later, during the drawing stage, the script computes

avgMfi = bin.mfiProduct / bin.volume

for each row. This is the volume weighted average MFI used both for coloring the box and for the numeric MFI value shown in the label Volume .

Tactical Holding [SwissAlgo]Tactical Holding

A visual framework for managing long-term positions across market cycles

--------------------------------------------------------------

Purpose

Instead of holding a fixed position through all market conditions , you can use this framework to adjust your exposure tactically . By reducing positions during distribution phases and accumulating during favorable accumulation zones, you may end up holding more units of the asset over complete market cycles - even if you temporarily exit or reduce exposure during unfavorable periods. This approach aims to help you compound your holdings by taking advantage of market volatility rather than simply enduring it.

--------------------------------------------------------------

Recommended Settings

Timeframe : Weekly (1W) chart

Chart Type : Standard candlesticks (select 'Bar' type Candles)

This indicator is designed for higher timeframe analysis. While it can be applied to other timeframes, the logic and signal generation are optimized for weekly charts to filter out short-term noise and focus on major market cycles.

--------------------------------------------------------------

Key Features

♦ Market State Classification

The indicator aims to categorize potential market conditions into five color-coded states based on technical confluences:

* Bull (bright green): Multiple bullish indicators align

* Bull Retrace (teal): Bullish structure with temporary weakness

* Bull ⇆ Bear Reversal (yellow): Transitional phase between trends

* Bear (bright red): Multiple bearish indicators align

* Bear Retrace (Pale Red/Maroon): Bearish structure with temporary strength

♦ Visual Elements

* Candles change color based on the current market state

* A 50-period EMA tracks with the same color coding, providing visual trend context

* Small arrow markers appear when specific pattern conditions are met (zones for potential distribution or accumulation)

* A legend table (toggle on/off) explains the color system

* A label shows the current state name on the chart

♦ Pattern Recognition

The system monitors for two types of potential entry/exit zones:

1. State transition patterns after periods of market regime consistency

2. RSI divergence patterns (when price and momentum move in opposite directions)

♦ Customization

* Toggle the legend table visibility through settings

* All calculations are transparent and use standard technical analysis methods

--------------------------------------------------------------

How It Works

Think of this indicator as a traffic light system for your portfolio:

♦ Green zones suggest the asset might be in an environment where long-term holders historically have remained invested

Bright green (Bull) : Multiple technical indicators align in a potentially strong bullish phase

Pale green (Bull Retrace) : Bullish structure remains intact, but momentum shows temporary weakness - often a pullback within an uptrend

♦ Red zones suggest conditions where long-term holders might consider reducing exposure or waiting for better entry points

Dark red (Bear) : Multiple technical indicators align in a potentially strong bearish phase

Pale red (Bear Retrace) : Bearish structure remains intact but shows temporary strength - often a bounce within a downtrend

♦ Yellow zones indicate the market is in transition between bull and bear regimes - a time for increased attention as the trend direction becomes uncertain

The system doesn't predict future prices. Instead, it helps you understand the current technical environment by doing the heavy lifting of analyzing multiple indicators at once and presenting them in a simple visual format.

Example: During the 2022 crypto bear market, the indicator would have displayed extended red periods, signaling defensive conditions for holders. When accumulation arrows appeared in late 2022-early 2023, it highlighted potential re-entry zones as the technical regime transitioned back toward green, before the 2024 recovery.

--------------------------------------------------------------

Who This Is For

♦ Long-term investors who want to hold assets through cycles but prefer a systematic approach to position sizing and timing rather than buying and never selling .

♦ Portfolio managers looking for a visual tool to help determine when to increase or decrease exposure to specific assets based on technical regime changes.

♦ Swing traders on higher timeframes who want to align their positions with the broader market structure rather than fighting the trend.

This is not designed for:

* Day traders or scalpers

* Those seeking exact entry/exit prices

* Automated trading systems (this is a visual decision-support tool)

--------------------------------------------------------------

Understanding the Visuals

When you apply Tactical Holding to a chart, you'll see:

1. Colored candles - Instantly see what market regime the asset is in

2. Colored EMA line (thick line) - Provides a dynamic support/resistance reference that changes color with market conditions

3. Small arrows (↑ ↓) - Mark bars where specific technical patterns complete

4. State label - Shows current market classification

5. Legend table (top right) - Quick reference guide for the color system

6. Warning banner (top center) - Reminds you to use weekly charts

The visual design prioritizes clarity over complexity. You should be able to glance at a chart and immediately understand the current technical environment.

--------------------------------------------------------------

Important Limitations

This indicator cannot:

* Predict future price movements

* Guarantee profitable trades

* Work equally well on all assets or timeframes

* Replace your own research and risk management

Technical considerations:

* Divergence detection has a 3-bar confirmation lag (by design, to avoid false signals)

* State transitions require multiple technical confirmations, which may cause delayed reactions to rapid market changes

* The system is reactive, not predictive - it responds to price action after it occurs

* Performance varies significantly between trending assets (like Solana) and stable assets (like Apple)

--------------------------------------------------------------

Practical Application

Consider using this indicator as one component of a broader investment framework:

♦ Understanding Position Context:

The color-coded states can help frame your thinking about current holdings:

Bull: Technical conditions that have historically been associated with sustained uptrends

Bull Retrace: Pullbacks within an overall bullish structure- these periods may offer opportunities to evaluate entry points or reassess existing positions

Reversal (Yellow): Transitional phases where the trend direction is unclear - periods that may warrant closer monitoring

Bear Retrace: Temporary strength within an overall bearish structure - rallies that historically have often faded

Bear: Technical conditions that have historically been associated with sustained downtrends

♦ Interpreting Signal Arrows:

Arrow markers indicate when specific technical pattern conditions have been met. These are observation points, not instructions:

A signal appearing doesn't mean immediate action is required

Treat arrows as prompts for further analysis rather than automatic triggers

Consider the broader context: fundamentals, your investment timeline, risk tolerance, and overall market conditions

Signals show when historical technical patterns have formed - not whether those patterns will lead to the same outcomes as in the past

The framework is designed to organize information visually, not to tell you what to do. Your investment decisions should incorporate this technical perspective alongside other factors relevant to your situation.

--------------------------------------------------------------

Technical Methodology

For transparency, the indicator uses:

* RSI (14) with a 14-period SMA to assess momentum direction

* MACD (12,26,9) to confirm trend strength and histogram momentum

* Stochastic RSI with K and D line crossovers for additional confirmation

* 50-period EMA as the primary trend filter

* Linear regression-based slope analysis to detect flat/transitional periods

* Pivot-based divergence detection following standard technical analysis principles

All calculations use publicly available technical analysis formulas. Nothing is hidden or proprietary beyond the specific combination and weighting of these standard tools.

--------------------------------------------------------------

Disclaimer

This indicator is an educational and analytical tool only. It is not financial advice.

* Trading and investing involve substantial risk of loss

* Past performance of any technical system does not indicate future results

* No indicator can predict market movements with certainty

* Always conduct your own research and consult with qualified financial professionals

* Never invest more than you can afford to lose

* The creators of this indicator are not responsible for any trading losses

* This tool is not affiliated with, endorsed by, or connected to TradingView, 3Commas, or any other trading platform

* Use of this indicator is at your own risk

Risk Management: Regardless of what any indicator shows, always use proper position sizing, stop losses, and risk management appropriate to your personal financial situation.

This indicator provides a framework for analysis. Your decisions, research, and risk management determine your results.

Central Limit Theorem Reversion IndicatorDear TV community, let me introduce you to the first-ever Central Limit Theorem indicator on TradingView.

The Central Limit Theorem is used in statistics and it can be quite useful in quant trading and understanding market behaviors.

In short, the CLT states: "When you take repeated samples from any population and calculate their averages, those averages will form a normal (bell curve) distribution—no matter what the original data looks like."

In this CLT indicator, I use statistical theory to identify high-probability mean reversion opportunities in the markets. It calculates statistical confidence bands and z-scores to identify when price movements deviate significantly from their expected distribution, signaling potential reversion opportunities with quantifiable probability levels.

Mathematical Foundation

The Central Limit Theorem (CLT) says that when you average many data points together, those averages will form a predictable bell-curve pattern, even if the original data is completely random and unpredictable (which often is in the markets). This works no matter what you're measuring, and it gets more reliable as you use more data points.

Why using it for trading?

Individual price movements seem random and chaotic, but when we look at the average of many price movements, we can actually predict how they should behave statistically. This lets us spot when prices have moved "too far" from what's normal—and those extreme moves tend to snap back (mean reversion).

Key Formula:

Z = (X̄ - μ) / (σ / √n)

Where:

- X̄ = Sample mean (average return over n periods)

- μ = Population mean (long-term expected return)

- σ = Population standard deviation (volatility)

- n = Sample size

- σ/√n = Standard error of the mean

How I Apply CLT

Step 1: Calculate Returns

Measures how much price changed from one bar to the next (using logarithms for better statistical properties)

Step 2: Average Recent Returns

Takes the average of the last n returns (e.g., last 100 bars). This is your "sample mean."

Step 3: Find What's "Normal"

Looks at historical data to determine: a) What the typical average return should be (the long-term mean) and b) How volatile the market usually is (standard deviation)

Step 4: Calculate Standard Error

Determines how much sample averages naturally vary. Larger samples = smaller expected variation.

Step 5: Calculate Z-Score

Measures how unusual the current situation is.

Step 6: Draw Confidence Bands

Converts these statistical boundaries into actual price levels on your chart, showing where price is statistically expected to stay 95% and 99% of the time.

Interpretation & Usage

The Z-Score:

The z-score tells you how statistically unusual the current price deviation is:

|Z| < 1.0 → Normal behavior, no action

|Z| = 1.0 to 1.96 → Moderate deviation, watch closely

|Z| = 1.96 to 2.58 → Significant deviation (95%+), consider entry

|Z| > 2.58 → Extreme deviation (99%+), high probability setup

The Confidence Bands

- Upper Red Bands: 95% and 99% overbought zones → Expect mean reversion downward as the price is not likely to cross these lines.

- Center Gray Line: Statistical expectation (fair value)

- Lower Blue Bands: 95% and 99% oversold zones → Expect mean reversion upward

Trading Logic:

- When price exceeds the upper 95% band (z-score > +1.96), there's only a 5% probability this is random noise → Strong sell/short signal

- When price falls below the lower 95% band (z-score < -1.96), there's a 95% statistical expectation of upward reversion → Strong buy/long signal

Background Gradient

The background color provides real-time visual feedback:

- Blue shades: Oversold conditions, expect upward reversion

- Red shades: Overbought conditions, expect downward reversion

- Intensity: Darker colors indicate stronger statistical significance

Trading Strategy Examples

Hypothetically, this is how the indicator could be used:

- Long: Z-score < -1.96 (below 95% confidence band)

- Short: Z-score > +1.96 (above 95% confidence band)

- Take profit when price returns to center line (Z ≈ 0)

Input Parameters

Sample Size (n) - Default: 100

Lookback Period (m) - Default: 100

You can also create alerts based on the indicator.

Final notes:

- The indicator uses logarithmic returns for better statistical properties

- Converts statistical bands back to price space for practical use

- Adaptive volatility: Bands automatically widen in high volatility, narrow in low volatility

- No repainting: yay! All calculations use historical data only

Feedback is more than welcome!

Henri

First Passage Time - Distribution AnalysisThe First Passage Time (FPT) Distribution Analysis indicator is a sophisticated probabilistic tool that answers one of the most critical questions in trading: "How long will it take for price to reach my target, and what are the odds of getting there first?"

Unlike traditional technical indicators that focus on what might happen, this indicator tells you when it's likely to happen.

Mathematical Foundation: First Passage Time Theory

What is First Passage Time?

First Passage Time (FPT) is a concept in stochastic processes that measures the time it takes for a random process to reach a specific threshold for the first time. Originally developed in physics and mathematics, FPT has applications in:

Quantitative Finance: Option pricing, risk management, and algorithmic trading

Neuroscience: Modeling neural firing patterns

Biology: Population dynamics and disease spread

Engineering: Reliability analysis and failure prediction

The Mathematics Behind It

This indicator uses Geometric Brownian Motion (GBM), the same stochastic model used in the Black-Scholes option pricing formula:

dS = μS dt + σS dW

Where:

S = Asset price

μ = Drift (trend component)

σ = Volatility (uncertainty component)

dW = Wiener process (random walk)

Through Monte Carlo simulation, the indicator runs 1,000+ price path simulations to statistically determine:

When each threshold (+X% or -X%) is likely to be hit

Which threshold is hit first (directional bias)

How often each scenario occurs (probability distribution)

🎯 How This Indicator Works

Core Algorithm Workflow:

Calculate Historical Statistics

Measures recent price volatility (standard deviation of log returns)

Calculates drift (average directional movement)

Annualizes these metrics for meaningful comparison

Run Monte Carlo Simulations

Generates 1,000+ random price paths based on historical behavior

Tracks when each path hits the upside (+X%) or downside (-X%) threshold

Records which threshold was hit first in each simulation

Aggregate Statistical Results

Calculates percentile distributions (10th, 25th, 50th, 75th, 90th)

Computes "first hit" probabilities (upside vs downside)

Determines average and median time-to-target

Visual Representation

Displays thresholds as horizontal lines

Shows gradient risk zones (purple-to-blue)

Provides comprehensive statistics table

📈 Use Cases

1. Options Trading

Selling Options: Determine if your strike price is likely to be hit before expiration

Buying Options: Estimate probability of reaching profit targets within your time window

Time Decay Management: Compare expected time-to-target vs theta decay

Example: You're considering selling a 30-day call option 5% out of the money. The indicator shows there's a 72% chance price hits +5% within 12 days. This tells you the trade has high assignment risk.

2. Swing Trading

Entry Timing: Wait for higher probability setups when directional bias is strong

Target Setting: Use median time-to-target to set realistic profit expectations

Stop Loss Placement: Understand probability of hitting your stop before target

Example: The indicator shows 85% upside probability with median time of 3.2 days. You can confidently enter long positions with appropriate position sizing.

3. Risk Management

Position Sizing: Larger positions when probability heavily favors one direction

Portfolio Allocation: Reduce exposure when probabilities are near 50/50 (high uncertainty)

Hedge Timing: Know when to add protective positions based on downside probability

Example: Indicator shows 55% upside vs 45% downside—nearly neutral. This signals high uncertainty, suggesting reduced position size or wait for better setup.

4. Market Regime Detection

Trending Markets: High directional bias (70%+ one direction)

Range-bound Markets: Balanced probabilities (45-55% both directions)

Volatility Regimes: Compare actual vs theoretical minimum time

Example: Consistent 90%+ bullish bias across multiple timeframes confirms strong uptrend—stay long and avoid counter-trend trades.

First Hit Rate (Most Important!)

Shows which threshold is likely to be hit FIRST:

Upside %: Probability of hitting upside target before downside

Downside %: Probability of hitting downside target before upside

These always sum to 100%

⚠️ Warning: If you see "Low Hit Rate" warning, increase this parameter!

Advanced Parameters

Drift Mode

Allows you to explore different scenarios:

Historical: Uses actual recent trend (default—most realistic)

Zero (Neutral): Assumes no trend, only volatility (symmetric probabilities)

50% Reduced: Dampens trend effect (conservative scenario)

Use Case: Switch to "Zero (Neutral)" to see what happens in a pure volatility environment, useful for range-bound markets.

Distribution Type

Percentile: Shows 10%, 25%, 50%, 75%, 90% levels (recommended for most users)

Sigma: Shows standard deviation levels (1σ, 2σ)—useful for statistical analysis

⚠️ Important Limitations & Best Practices

Limitations

Assumes GBM: Real markets have fat tails, jumps, and regime changes not captured by GBM

Historical Parameters: Uses recent volatility/drift—may not predict regime shifts

No Fundamental Events: Cannot predict earnings, news, or macro shocks

Computational: Runs only on last bar—doesn't give historical signals

Remember: Probabilities are not certainties. Use this indicator as part of a comprehensive trading plan with proper risk management.

Created by: Henrique Centieiro. feedback is more than welcome!

Distribution DaysThis script marks Distribution Days according to the Investors Business Daily method -- a significant decline on higher volume:

(1.) Price has declined > 0.2% from the prior day's close

(2.) Trading volume is greater than the prior day's volume

Volume-Weighted Money Flow [sgbpulse]Overview

The VWMF indicator is an advanced technical analysis tool that combines and summarizes five leading momentum and volume indicators (OBV, PVT, A/D, CMF, MFI) into one clear oscillator. The indicator helps to provide a clear picture of market sentiment by measuring the pressure from buyers and sellers. Unlike single indicators, VWMF provides a comprehensive view of market money flow by weighting existing indicators and presenting them in a uniform and understandable format.

Indicator Components

VWMF combines the following indicators, each normalized to a range of 0 to 100 before being weighted:

On-Balance Volume (OBV): A cumulative indicator that measures positive and negative volume flow.

Price-Volume Trend (PVT): Similar to OBV, but incorporates relative price change for a more precise measure.

Accumulation/Distribution Line (A/D): Used to identify whether an asset is being bought (accumulated) or sold (distributed).

Chaikin Money Flow (CMF): Measures the money flow over a period based on the close price's position relative to the candle's range.

Money Flow Index (MFI): A momentum oscillator that combines price and volume to measure buying and selling pressure.

Understanding the Normalized Oscillators

The indicator combines the five different momentum indicators by normalizing each one to a uniform range of 0 to 100 .

Why is Normalization Important?

Indicators like OBV, PVT, and the A/D Line are cumulative indicators whose values can become very large. To assess their trend, we use a Moving Average as a dynamic reference line . The Moving Average allows us to understand whether the indicator is currently trending up or down relative to its average behavior over time.

How Does Normalization Work?

Our normalization fully preserves the original trend of each indicator.

For Cumulative Indicators (OBV, PVT, A/D): We calculate the difference between the current indicator value and its Moving Average. This difference is then passed to the normalization process.

- If the indicator is above its Moving Average, the difference will be positive, and the normalized value will be above 50.

- If the indicator is below its Moving Average, the difference will be negative, and the normalized value will be below 50.

Handling Extreme Values: To overcome the issue of extreme values in indicators like OBV, PVT, and the A/D Line , the function calculates the highest absolute value over the selected period. This value is used to prevent sharp spikes or drops in a single indicator from compromising the accuracy of the normalization over time. It's a sophisticated method that ensures the oscillators remain relevant and accurate.

For Bounded Indicators (CMF, MFI): These indicators already operate within a known range (for example, CMF is between -1 and 1, and MFI is between 0 and 100), so they are normalized directly without an additional reference line.

Reference Line Settings:

Moving Average Type: Allows the user to choose between a Simple Moving Average (SMA) and an Exponential Moving Average (EMA).

Volume Flow MA Length: Allows the user to set the lookback period for the Moving Average, which affects the indicator's sensitivity.

The 50 line serves as the new "center line." This ensures that, even after normalization, the determination of whether a specific indicator supports a bullish or bearish trend remains clear.

Settings and Visual Tools

The indicator offers several customization options to provide a rich analysis experience:

VWMF Oscillator (Blue Line): Represents the weighted average of all five indicators. Values above 50 indicate bullish momentum, and values below 50 indicate bearish momentum.

Strength Metrics (Bullish/Bearish Strength %): Two metrics that appear on the status line, showing the percentage of indicators supporting the current trend. They range from 0% to 100%, providing a quick view of the strength of the consensus.

Dynamic Background Colors: The background color of the chart automatically changes to bullish (a blue shade by default) or bearish (a default brown-gray shade) based on the trend. The transparency of the color shows the consensus strength—the more opaque the background, the more indicators support the trend.

Advanced Settings:

- Background Color Logic: Allows the user to choose the trigger for the background color: Weighted Value (based on the combined oscillator) or Strength (based on the majority of individual indicators).

- Weights: Provides full control over the weight of each of the five indicators in the final oscillator.

Using the Data Window

TradingView provides a useful Data Window that allows you to see the exact numerical values of each normalized oscillator separately, in addition to the trend strength data.

You can use this window to:

Get more detailed information on each indicator: Viewing the precise numerical data of each of the five indicators can help in making trading decisions.

Calibrate weights: If you want to manually adjust the indicator weights (in the settings menu), you can do so while tracking the impact of each indicator on the weighted oscillator in the Data Window.

The indicator's default setting is an equal weight of 20% for each of the five indicators.

Alert Conditions

The indicator comes with a variety of built-in alerts that can be configured through the TradingView alerts menu:

VWMF Cross Above 50: An alert when the VWMF oscillator crosses above the 50 line, indicating a potential bullish momentum shift.

VWMF Cross Below 50: An alert when the VWMF oscillator crosses below the 50 line, indicating a potential bearish momentum shift.

Bullish Strength: High But Not Absolute Consensus: An alert when the bullish trend strength reaches 60% or more but is less than 100%, indicating a high but not absolute consensus.

Bullish Strength at 100%: An alert when all five indicators (MFI, OBV, PVT, A/D, CMF) show bullish strength, indicating a full and absolute consensus.

Bearish Strength: High But Not Absolute Consensus: An alert when the bearish trend strength reaches 60% or more but is less than 100%, indicating a high but not absolute consensus.

Bearish Strength at 100%: An alert when all five indicators (MFI, OBV, PVT, A/D, CMF) show bearish strength, indicating a full and absolute consensus.

Summary

The VWMF indicator is a powerful, all-in-one tool for analyzing market momentum, money flow, and sentiment. By combining and normalizing five different indicators into a single oscillator, it offers a holistic and accurate view of the market's underlying trend. Its dynamic visual features and customizable settings, including the ability to adjust indicator weights, provide a flexible experience for both novice and experienced traders. The built-in alerts for momentum shifts and trend consensus make it an effective tool for spotting trading opportunities with confidence. In essence, VWMF distills complex market data into clear, actionable signals.

Important Note: Trading Risk

This indicator is intended for educational and informational purposes only and does not constitute investment advice or a recommendation for trading in any form whatsoever.

Trading in financial markets involves significant risk of capital loss. It is important to remember that past performance is not indicative of future results. All trading decisions are your sole responsibility. Never trade with money you cannot afford to lose.

Risk Distribution HistogramStatistical risk visualization and analysis tool for any ticker 📊

The Risk Distribution Histogram visualizes the statistical distribution of different risk metrics for any financial instrument. It converts risk data into histograms with quartile-based color coding, so that traders can understand their risk, tail-risks, exposure patterns and make data-driven decisions based on empirical evidence rather than assumptions.

The indicator supports multiple risk calculation methods, each designed for different aspects of market analysis, from general volatility assessment to tail risk analysis.

Risk Measurement Methods

Standard Deviation

Captures raw daily price volatility by measuring the dispersion of price movements. Ideal for understanding overall market conditions and timing volatility-based strategies.

Use case: Options trading and volatility analysis.

Average True Range (ATR)

Measures true range as a percentage of price, accounting for gaps and limit moves. Valuable for position sizing across different price levels.

Use case: Position sizing and stop-loss placement.

The chart above illustrates how ATR statistical distribution can be used by looking at the ATR % of price distribution. For example, 90% of the movements are below 5%.

Downside Deviation

Only considers negative price movements, making it ideal for checking downside risk and capital protection rather than capturing upside volatility.

Use case: Downside protection strategies and stop losses.

Drawdown Analysis

Tracks peak-to-trough declines, providing insight into maximum loss potential during different market conditions.

Use case: Risk management and capital preservation.

The chart above illustrates tale risk for the asset (TQQQ), showing that it is possible to have drawdowns higher than 20%.

Entropy-Based Risk (EVaR)

Uses information theory to quantify market uncertainty. Higher entropy values indicate more unpredictable price action, valuable for detecting regime changes.

Use case: Advanced risk modeling and tail-risk.

VIX Histogram

Incorporates the market's fear index directly into analysis, showing how current volatility expectations compare to historical patterns. The CAPITALCOM:VIX histogram is independent from the ticker on the chart.

Use case: Volatility trading and market timing.

Visual Features

The histogram uses quartile-based color coding that immediately shows where current risk levels stand relative to historical patterns:

Green (Q1): Low Risk (0-25th percentile)

Yellow (Q2): Medium-Low Risk (25-50th percentile)

Orange (Q3): Medium-High Risk (50-75th percentile)

Red (Q4): High Risk (75-100th percentile)

The data table provides detailed statistics, including:

Count Distribution: Historical observations in each bin

PMF: Percentage probability for each risk level

CDF: Cumulative probability up to each level

Current Risk Marker: Shows your current position in the distribution

Trading Applications

When current risk falls into upper quartiles (Q3 or Q4), it signals conditions are riskier than 50-75% of historical observations. This guides position sizing and portfolio adjustments.

Key applications:

Position sizing based on empirical risk distributions

Monitoring risk regime changes over time

Comparing risk patterns across timeframes

Risk distribution analysis improves trade timing by identifying when market conditions favor specific strategies.

Enter positions during low-risk periods (Q1)

Reduce exposure in high-risk periods (Q4)

Use percentile rankings for dynamic stop-loss placement

Time volatility strategies using distribution patterns

Detect regime shifts through distribution changes

Compare current conditions to historical benchmarks

Identify outlier events in tail regions

Validate quantitative models with empirical data

Configuration Options

Data Collection

Lookback Period: Control amount of historical data analyzed

Date Range Filtering: Focus on specific market periods

Sample Size Validation: Automatic reliability warnings

Histogram Customization

Bin Count: 10-50 bins for different detail levels

Auto/Manual Bin Width: Optimize for your data range

Visual Preferences: Custom colors and font sizes

Implementation Guide

Start with Standard Deviation on daily charts for the most intuitive introduction to distribution-based risk analysis.

Method Selection: Begin with Standard Deviation

Setup: Use daily charts with 20-30 bins

Interpretation: Focus on quartile transitions as signals

Monitoring: Track distribution changes for regime detection

The tool provides comprehensive statistics including mean, standard deviation, quartiles, and current position metrics like Z-score and percentile ranking.

Enjoy, and please let me know your feedback! 😊🥂

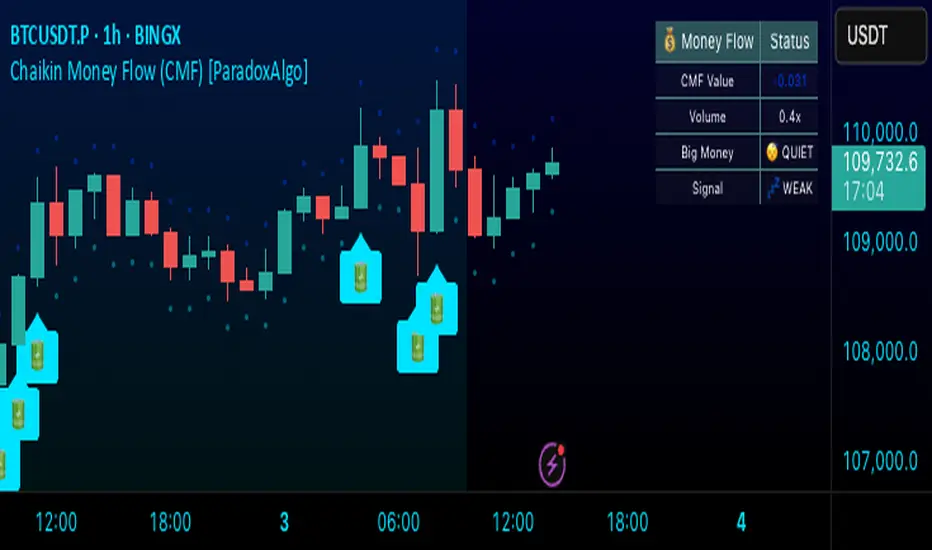

Chaikin Money Flow (CMF) [ParadoxAlgo]OVERVIEW

This indicator implements the Chaikin Money Flow oscillator as an overlay on the price chart, designed to help traders identify institutional money flow patterns. The Chaikin Money Flow combines price and volume data to measure the flow of money into and out of a security, making it particularly useful for detecting accumulation and distribution phases.

WHAT IS CHAIKIN MONEY FLOW?

Chaikin Money Flow was developed by Marc Chaikin and measures the amount of Money Flow Volume over a specific period. The indicator oscillates between +1 and -1, where:

Positive values indicate money flowing into the security (accumulation)

Negative values indicate money flowing out of the security (distribution)

Values near zero suggest equilibrium between buying and selling pressure

CALCULATION METHOD

Money Flow Multiplier = ((Close - Low) - (High - Close)) / (High - Low)

Money Flow Volume = Money Flow Multiplier × Volume

CMF = Sum of Money Flow Volume over N periods / Sum of Volume over N periods

KEY FEATURES

Big Money Detection:

Identifies significant institutional activity when CMF exceeds user-defined thresholds

Requires volume confirmation (volume above average) to validate signals

Uses battery icon (🔋) for institutional buying and lightning icon (⚡) for institutional selling

Visual Elements:

Background coloring based on money flow direction

Support and resistance levels calculated using Average True Range

Real-time dashboard showing current CMF value, volume strength, and signal status

Customizable Parameters:

CMF Period: Calculation period for the money flow (default: 20)

Signal Smoothing: EMA smoothing applied to reduce noise (default: 5)

Big Money Threshold: CMF level required to trigger institutional signals (default: 0.15)

Volume Threshold: Volume multiplier required for signal confirmation (default: 1.5x)

INTERPRETATION

Signal Types:

🔋 (Battery): Indicates strong institutional buying when CMF > threshold with high volume

⚡ (Lightning): Indicates strong institutional selling when CMF < -threshold with high volume

Background color: Green tint for positive money flow, red tint for negative money flow

Dashboard Information:

CMF Value: Current Chaikin Money Flow reading

Volume: Current volume as a multiple of 20-period average

Big Money: Status of institutional activity (BUYING/SELLING/QUIET)

Signal: Strength assessment (STRONG/MEDIUM/WEAK)

TRADING APPLICATIONS

Trend Confirmation: Use CMF direction to confirm price trends

Divergence Analysis: Look for divergences between price and money flow

Volume Validation: Confirm breakouts with corresponding money flow

Accumulation/Distribution: Identify phases of institutional activity

PARAMETER RECOMMENDATIONS

Day Trading: CMF Period 14-21, higher sensitivity settings

Swing Trading: CMF Period 20-30, moderate sensitivity

Position Trading: CMF Period 30-50, lower sensitivity for major trends

ALERTS

Optional alert system notifies users when:

Big money buying is detected (CMF above threshold with volume confirmation)

Big money selling is detected (CMF below negative threshold with volume confirmation)

LIMITATIONS

May generate false signals in low-volume conditions

Best used in conjunction with other technical analysis tools

Effectiveness varies across different market conditions and timeframes

EDUCATIONAL PURPOSE

This open-source indicator is provided for educational purposes to help traders understand money flow analysis. It demonstrates the practical application of the Chaikin Money Flow concept with visual enhancements for easier interpretation.

TECHNICAL SPECIFICATIONS

Overlay indicator (displays on price chart)

No repainting - all calculations are based on closed bar data

Suitable for all timeframes and asset classes

Minimal resource usage for optimal performance

DISCLAIMER

This indicator is for educational and informational purposes only. Past performance does not guarantee future results. Always conduct your own analysis and consider risk management before making trading decisions.

Smarter Money Flow Divergence Detector [PhenLabs]📊 Smarter Money Flow Divergence Detector

Version: PineScript™ v6

📌 Description

SMFD was developed to help give you guys a better ability to “read” what is going on behind the scenes without directly having access to that level of data. SMFD is an enhanced divergence detection indicator that identifies money flow patterns from advanced volume analysis and price action correspondence. The detection portion of this indicator combines intelligent money flow calculations with multi timeframe volume analysis to help you see hidden accumulation and distribution phases before major price movements occur.

The indicator measures institutional trading activity by looking at volume surges, price volume dynamics, and the factors of momentum to construct an overall picture of market sentiment. It’s built to assist traders in identifying high probability entries by identifying if smart money is positioning against price action.

🚀 Points of Innovation

● Advanced Smart Money Flow algorithm with volume spike detection and large trade weighting

● Multi timeframe volume analysis for enhanced institutional activity detection

● Dynamic overbought/oversold zones that adapt to current market conditions

● Enhanced divergence detection with pivot confirmation and strength validation

● Color themes with customizable visual styling options

● Real time institutional bias tracking through accumulation/distribution analysis

🔧 Core Components

● Smart Money Flow Calculation: Combines price momentum, volume expansion, and VWAP analysis

● Institutional Bias Oscillator: Tracks accumulation/distribution patterns with volume pressure analysis

● Enhanced Divergence Engine: Detects bullish/bearish divergences with multiple confirmation factors

● Dynamic Zone Detection: Automatically adjusts overbought/oversold levels based on market volatility

● Volume Pressure Analysis: Measures buying vs selling pressure over configurable periods

● Multi factor Signal System: Generates entries with trend alignment and strength validation

🔥 Key Features

● Smart Money Flow Period: Configurable calculation period for institutional activity detection

● Volume Spike Threshold: Adjustable multiplier for detecting unusual institutional volume

● Large Trade Weight: Emphasis factor for high volume periods in flow calculations

● Pivot Detection: Customizable lookback period for accurate divergence identification

● Signal Sensitivity: Three tier system (Conservative/Medium/Aggressive) for signal generation

● Themes: Four color schemes optimized for different chart backgrounds

🎨 Visualization

● Main Oscillator: Line, Area, or Histogram display styles with dynamic color coding

● Institutional Bias Line: Real time tracking of accumulation/distribution phases

● Dynamic Zones: Adaptive overbought/oversold boundaries with gradient fills

● Divergence Lines: Automatic drawing of bullish/bearish divergence connections

● Entry Signals: Clear BUY/SELL labels with signal strength indicators

● Information Panel: Real time statistics and status updates in customizable positions

📖 Usage Guidelines

Algorithm Settings

● Smart Money Flow Period

○ Default: 20

○ Range: 5-100

○ Description: Controls the calculation period for institutional flow analysis.

Higher values provide smoother signals but reduce responsiveness to recent activity

● Volume Spike Threshold

○ Default: 1.8

○ Range: 1.0-5.0

○ Description: Multiplier for detecting unusual volume activity indicating institutional participation. Higher values require more extreme volume for detection

● Large Trade Weight

○ Default: 2.5

○ Range: 1.5-5.0

○ Description: Weight applied to high volume periods in smart money calculations. Increases emphasis on institutional sized transactions

Divergence Detection

● Pivot Detection Period

○ Default: 12

○ Range: 5-50

○ Description: Bars to analyze for pivot high/low identification.

Affects divergence accuracy and signal frequency

● Minimum Divergence Strength

○ Default: 0.25

○ Range: 0.1-1.0

○ Description: Required price change percentage for valid divergence patterns.

Higher values filter out weaker signals

✅ Best Use Cases

● Trading with intraday to daily timeframes for institutional position identification

● Confirming trend reversals when divergences align with support/resistance levels

● Entry timing in trending markets when institutional bias supports the direction

● Risk management by avoiding trades against strong institutional positioning

● Multi timeframe analysis combining short term signals with longer term bias

⚠️ Limitations

● Requires sufficient volume for accurate institutional detection in low volume markets

● Divergence signals may have false positives during highly volatile news events

● Best performance on liquid markets with consistent institutional participation

● Lagging nature of volume based calculations may delay signal generation

● Effectiveness reduced during low participation holiday periods

💡 What Makes This Unique

● Multi Factor Analysis: Combines volume, price, and momentum for comprehensive institutional detection

● Adaptive Zones: Dynamic overbought/oversold levels that adjust to market conditions

● Volume Intelligence: Advanced algorithms identify institutional sized transactions

● Professional Visualization: Multiple display styles with customizable themes

● Confirmation System: Multiple validation layers reduce false signal generation

🔬 How It Works

1. Volume Analysis Phase:

● Analyzes current volume against historical averages to identify institutional activity

● Applies multi timeframe analysis for enhanced detection accuracy

● Calculates volume pressure through buying vs selling momentum

2. Smart Money Flow Calculation:

● Combines typical price with volume weighted analysis

● Applies institutional trade weighting for high volume periods

● Generates directional flow based on price momentum and volume expansion

3. Divergence Detection Process:

● Identifies pivot highs/lows in both price and indicator values

● Validates divergence strength against minimum threshold requirements

● Confirms signals through multiple technical factors before generation

💡 Note: This indicator works best when combined with proper risk management and position sizing. The institutional bias component helps identify market sentiment shifts, while divergence signals provide specific entry opportunities. For optimal results, use on liquid markets with consistent institutional participation and combine with additional technical analysis methods.

MVRV Ratio [Alpha Extract]The MVRV Ratio Indicator provides valuable insights into Bitcoin market cycles by tracking the relationship between market value and realized value. This powerful on-chain metric helps traders identify potential market tops and bottoms, offering clear buy and sell signals based on historical patterns of Bitcoin valuation.

🔶 CALCULATION The indicator processes MVRV ratio data through several analytical methods:

Raw MVRV Data: Collects MVRV data directly from INTOTHEBLOCK for Bitcoin

Optional Smoothing: Applies simple moving average (SMA) to reduce noise

Status Classification: Categorizes market conditions into four distinct states

Signal Generation: Produces trading signals based on MVRV thresholds

Price Estimation: Calculates estimated realized price (Current price / MVRV ratio)

Historical Context: Compares current values to historical extremes

Formula:

MVRV Ratio = Market Value / Realized Value

Smoothed MVRV = SMA(MVRV Ratio, Smoothing Length)

Estimated Realized Price = Current Price / MVRV Ratio

Distance to Top = ((3.5 / MVRV Ratio) - 1) * 100

Distance to Bottom = ((MVRV Ratio / 0.8) - 1) * 100

🔶 DETAILS Visual Features:

MVRV Plot: Color-coded line showing current MVRV value (red for overvalued, orange for moderately overvalued, blue for fair value, teal for undervalued)

Reference Levels: Horizontal lines indicating key MVRV thresholds (3.5, 2.5, 1.0, 0.8)

Zone Highlighting: Background color changes to highlight extreme market conditions (red for potentially overvalued, blue for potentially undervalued)

Information Table: Comprehensive dashboard showing current MVRV value, market status, trading signal, price information, and historical context

Interpretation:

MVRV ≥ 3.5: Potential market top, strong sell signal

MVRV ≥ 2.5: Overvalued market, consider selling

MVRV 1.5-2.5: Neutral market conditions

MVRV 1.0-1.5: Fair value, consider buying

MVRV < 1.0: Potential market bottom, strong buy signal

🔶 EXAMPLES

Market Top Identification: When MVRV ratio exceeds 3.5, the indicator signals potential market tops, highlighting periods where Bitcoin may be significantly overvalued.

Example: During bull market peaks, MVRV exceeding 3.5 has historically preceded major corrections, helping traders time their exits.

Bottom Detection: MVRV values below 1.0, especially approaching 0.8, have historically marked excellent buying opportunities.

Example: During bear market bottoms, MVRV falling below 1.0 has identified the most profitable entry points for long-term Bitcoin accumulation.

Tracking Market Cycles: The indicator provides a clear visualization of Bitcoin's market cycles from undervalued to overvalued states.

Example: Following the progression of MVRV from below 1.0 through fair value and eventually to overvalued territory helps traders position themselves appropriately throughout Bitcoin's market cycle.

Realized Price Support: The estimated realized price often acts as a significant

support/resistance level during market transitions.

Example: During corrections, price often finds support near the realized price level calculated by the indicator, providing potential entry points.

🔶 SETTINGS

Customization Options:

Smoothing: Toggle smoothing option and adjust smoothing length (1-50)

Table Display: Show/hide the information table

Table Position: Choose between top right, top left, bottom right, or bottom left positions

Visual Elements: All plots, lines, and background highlights can be customized for color and style

The MVRV Ratio Indicator provides traders with a powerful on-chain metric to identify potential market tops and bottoms in Bitcoin. By tracking the relationship between market value and realized value, this indicator helps identify periods of overvaluation and undervaluation, offering clear buy and sell signals based on historical patterns. The comprehensive information table delivers valuable context about current market conditions, helping traders make more informed decisions about market positioning throughout Bitcoin's cyclical patterns.

Statistical Trailing Stop [LuxAlgo]The Statistical Trailing Stop tool offers traders a way to lock in profits in trending markets with four statistical levels based on the log-normal distribution of volatility.

The indicator also features a dashboard with statistics of all detected signals.

🔶 USAGE

The tool works out of the box, traders can adjust the data used with two parameters: data & distribution length.

By default, the tool takes volatility measures of groups of 10 candles, and statistical measures of the last 100 of these groups then traders can adjust the base level to use as trailing, the larger the level, the more resistant the tool will be to moves against the trend.

🔹 Base Levels

Traders can choose up to 4 different levels of trailing, all based on the statistical distribution of volatility.

As we can see in the chart above, each higher level is more resistant to market movements, so level 0 is the most reactive and level 3 the least.

It is up to the trader to determine the best level for each underlying, time frame and market conditions.

🔹 Dashboard

The tool provides a dashboard with the statistics of all trades, making it very easy to assess the performance of the parameters used for any given market.

As we can see on the chart, all Daily BTC signals with default parameters but different base levels, level 2 is the best performing of all four, giving a positive expectation of $2435 per trade, taking into account all long and short trades.

Of note are the long trades with a win rate of 76.47% and a risk-to-reward of 3.34, giving a positive expectation of $4839 per trade, with winners having an average duration of 210 days and losers 32 days.

This, compared to short trades with negative expectation, speaks to the uptrend bias of this particular market.

🔶 SETTINGS

Data Length: Select how many bars to use per data point

Distribution Length: Select how many data points the distribution will have

Base Level: Choose between 4 different trailing levels

🔹 Dashboard

Show Statistics: Enable/disable dashboard

Position: Select dashboard position

Size: Select dashboard size

OBV & AD Oscillators with Dual Smoothing OptionsOn Balance Volume and Accumulation/Distribution

Overlaid into 1 and then some,

Now it is an oscillator!

3 customizable moving average types

- Ehlers Deviation Scaled Moving Average

- Volatility Dynamic Moving Average

- Simple Moving Average

Each with customizable periods

And with the ability to overlay a second set too

Default Settings have a longer period MA of 377 using Ehlers DSMA to better capture the standard view of OBV and A/D.

An extra overlay of a shorter period using a Volatility DMA uses Average True Range with its own custom settings, seeks to act more as an RSI

Elastic Volume-Weighted Student-T TensionOverview

The Elastic Volume-Weighted Student-T Tension Bands indicator dynamically adapts to market conditions using an advanced statistical model based on the Student-T distribution. Unlike traditional Bollinger Bands or Keltner Channels, this indicator leverages elastic volume-weighted averaging to compute real-time dispersion and location parameters, making it highly responsive to volatility changes while maintaining robustness against price fluctuations.

This methodology is inspired by incremental calculation techniques for weighted mean and variance, as outlined in the paper by Tony Finch:

📄 "Incremental Calculation of Weighted Mean and Variance" .

Key Features

✅ Adaptive Volatility Estimation – Uses an exponentially weighted Student-T model to dynamically adjust band width.

✅ Volume-Weighted Mean & Dispersion – Incorporates real-time volume weighting, ensuring a more accurate representation of market sentiment.

✅ High-Timeframe Volume Normalization – Provides an option to smooth volume impact by referencing a higher timeframe’s cumulative volume, reducing noise from high-variability bars.

✅ Customizable Tension Parameters – Configurable standard deviation multipliers (σ) allow for fine-tuned volatility sensitivity.

✅ %B-Like Oscillator for Relative Price Positioning – The main indicator is in form of a dedicated oscillator pane that normalizes price position within the sigma ranges, helping identify overbought/oversold conditions and potential momentum shifts.

✅ Robust Statistical Foundation – Utilizes kurtosis-based degree-of-freedom estimation, enhancing responsiveness across different market conditions.

How It Works

Volume-Weighted Elastic Mean (eμ) – Computes a dynamic mean price using an elastic weighted moving average approach, influenced by trade volume, if not volume detected in series, study takes true range as replacement.

Dispersion (eσ) via Student-T Distribution – Instead of assuming a fixed normal distribution, the bands adapt to heavy-tailed distributions using kurtosis-driven degrees of freedom.

Incremental Calculation of Variance – The indicator applies Tony Finch’s incremental method for computing weighted variance instead of arithmetic sum's of fixed bar window or arrays, improving efficiency and numerical stability.

Tension Calculation – There are 2 dispersion custom "zones" that are computed based on the weighted mean and dynamically adjusted standard student-t deviation.

%B-Like Oscillator Calculation – The oscillator normalizes the price within the band structure, with values between 0 and 1:

* 0.00 → Price is at the lower band (-2σ).

* 0.50 → Price is at the volume-weighted mean (eμ).

* 1.00 → Price is at the upper band (+2σ).

* Readings above 1.00 or below 0.00 suggest extreme movements or possible breakouts.

Recommended Usage

For scalping in lower timeframes, it is recommended to use the fixed α Decay Factor, it is in raw format for better control, but you can easily make a like of transformation to N-bar size window like in EMA-1 bar dividing 2 / decayFactor or like an RMA dividing 1 / decayFactor.

The HTF selector catch quite well Higher Time Frame analysis, for example using a Daily chart and using as HTF the 200-day timeframe, weekly or monthly.

Suitable for trend confirmation, breakout detection, and mean reversion plays.

The %B-like oscillator helps gauge momentum strength and detect divergences in price action if user prefer a clean chart without bands, this thanks to pineScript v6 force overlay feature.

Ideal for markets with volume-driven momentum shifts (e.g., futures, forex, crypto).

Customization Parameters

Fixed α Decay Factor – Controls the rate of volume weighting influence for an approximation EWMA approach instead of using sum of series or arrays, making the code lightweight & computing fast O(1).

HTF Volume Smoothing – Instead of a fixed denominator for computing α , a volume sum of the last 2 higher timeframe closed candles are used as denominator for our α weight factor. This is useful to review mayor trends like in daily, weekly, monthly.

Tension Multipliers (±σ) – Adjusts sensitivity to dispersion sigma parameter (volatility).

Oscillator Zone Fills – Visual cues for price positioning within the cloud range.

Posible Interpretations

As market within indicators relay on each individual edge, this are just some key ideas to glimpse how the indicator could be interpreted by the user:

📌 Price inside bands – Market is considered somehow "stable"; price is like resting from tension or "charging batteries" for volume spike moves.

📌 Price breaking outer bands – Potential breakout or extreme movement; watch for reversals or continuation from strong moves. Market is already in tension or generating it.

📌 Narrowing Bands – Decreasing volatility; expect contraction before expansion.

📌 Widening Bands – Increased volatility; prepare for high probability pull-back moves, specially to the center location of the bands (the mean) or the other side of them.

📌 Oscillator is just the interpretation of the price normalized across the Student-T distribution fitting "curve" using the location parameter, our Elastic Volume weighted mean (eμ) fixed at 0.5 value.

Final Thoughts

The Elastic Volume-Weighted Student-T Tension indicator provides a powerful, volume-sensitive alternative to traditional volatility bands. By integrating real-time volume analysis with an adaptive statistical model, incremental variance computation, in a relative price oscillator that can be overlayed in the chart as bands, it offers traders an edge in identifying momentum shifts, trend strength, and breakout potential. Think of the distribution as a relative "tension" rubber band in which price never leave so far alone.

DISCLAIMER: