Trendlines & SR ZonesIt's a comprehensive indicator (Pine Script v6) that represents two powerful technical analysis tools: automatic trendline detection based on pivot points and volume delta analysis with support/resistance zone identification. This overlay indicator helps traders identify potential trend directions and key price levels where significant buying or selling pressure has occurred.

Features: =

1. Price Trendlines

The indicator automatically identifies and draws trendlines based on pivot points, creating dynamic support and resistance levels.

Key Components:

Pivot Detection: Uses configurable left and right bars to identify significant pivot highs and lows

Trendline Filtering: Only draws downward-sloping resistance trendlines and upward-sloping support trendlines

Zone Creation: Creates filled zones around trendlines based on average price volatility

Automatic Management: Maintains only the 3 most recent significant trendlines to avoid chart clutter

Customization Options:

Left/Right Bars for Pivot: Adjust sensitivity of pivot detection (default: 10 bars each side)

Extension Length: Control how far trendlines extend past the second pivot (default: 50 bars)

Average Body Periods: Set the lookback period for volatility calculation (default: 100)

Tolerance Multiplier: Adjust the width of the trendline zones (default: 1.0)

Color Customization: Separate colors for high (resistance) and low (support) trendlines and their fills

2. Volume Delta % Bars

The indicator analyzes volume distribution across price levels to identify significant supply and demand zones.

Key Components:

Volume Profile Analysis: Divides the price range into rows and calculates volume delta at each level

Delta Visualization: Displays horizontal bars showing the percentage difference between buying and selling volume

Zone Identification: Automatically identifies the most significant supply and demand zones

Visual Integration: Connects volume delta bars with corresponding support/resistance zones on the price chart

Customization Options:

Lookback Period: Set the number of bars to analyze for volume (default: 200)

Price Rows: Control the granularity of the volume analysis (default: 50 rows)

Delta Sections: Adjust the number of horizontal delta bars displayed (default: 20)

Panel Appearance: Customize width, position, and direction of the delta panel

Zone Settings: Control the number of supply/demand zones and their extension (default: 3 zones)

How It Works-

Trendline Logic:

The script continuously scans for pivot highs and lows based on the specified left and right bars

When a pivot is detected, it creates a horizontal line at that price level

The script then looks for the previous pivot of the same type (high or low)

It connects these pivots with a trendline, extending it based on the user-specified setting

A parallel line is created to form a zone, with the distance based on average price volatility

The script filters out invalid trendlines (upward-sloping resistance and downward-sloping support). Only the 3 most recent trendlines are maintained to prevent chart clutter

Volume Delta Logic:

The script divides the price range over the lookback period into the specified number of rows

For each bar in the lookback period, it categorizes volume as bullish (close > open) or bearish (close < open). This volume is assigned to the appropriate price level based on the HLC3 price.

The price levels are grouped into sections, and the net delta (bullish - bearish volume) is calculated for each Horizontal bars are drawn to represent these delta percentages.

The most significant positive and negative deltas are identified and displayed as support and resistance zones. These zones are extended to the left on the price chart and connected to the delta panel with dotted lines.

Ideal Timeframes:

The indicator is versatile and can be used across multiple timeframes, but it performs optimally on specific timeframes depending on your trading style:

For Day Trading:

Optimal Timeframes: 15-minute to 1-hour charts

Why: These timeframes provide a good balance between noise reduction and sufficient volume data. The volume delta analysis is particularly effective on these timeframes as it captures intraday accumulation/distribution patterns while the trendlines remain reliable enough for intraday trading decisions.

For Swing Trading:

Optimal Timeframes: 1-hour to 4-hour charts

Why: These timeframes offer the best combination of reliable trendline formation and meaningful volume analysis. The trendlines on these timeframes are less prone to whipsaws, while the volume delta analysis captures multi-day trading sessions and institutional activity.

For Position Trading:

Optimal Timeframes: Daily and weekly charts

Why: On these higher timeframes, trendlines become extremely reliable as they represent significant market structure points. The volume delta analysis reveals longer-term accumulation and distribution patterns that can define major support and resistance zones for weeks or months.

Timeframe-Specific Adjustments:

Lower Timeframes (1-15 minutes):

Reduce left/right bars for pivots (5-8 bars)

Decrease lookback period for volume delta (50-100 bars)

Increase tolerance multiplier (1.2-1.5) to account for higher volatility

Higher Timeframes (Daily+):

Increase left/right bars for pivots (15-20 bars)

Extend lookback period for volume delta (300-500 bars)

Consider increasing the number of price rows (70-100) for more detailed volume analysis

Usage Guidelines-

For Trendline Analysis:

Use the trendlines as dynamic support and resistance levels

Price reactions at these levels can indicate potential trend continuation or reversal points

The filled zones around trendlines represent areas of price volatility or uncertainty

Consider the slope of the trendline as an indication of trend strength

For Volume Delta Analysis:

The horizontal delta bars show where buying or selling pressure has been concentrated

Green bars indicate areas where buying volume exceeded selling volume (demand)

Red bars indicate areas where selling volume exceeded buying volume (supply)

The highlighted supply and demand zones on the price chart represent significant price levels

These zones can act as future support or resistance areas as price revisits them

Customization Tips:

Trendline Sensitivity: Decrease left/right bars values to detect more pivots (more sensitive) or increase them for fewer, more significant pivots

Zone Width: Adjust the tolerance multiplier to make trendline zones wider or narrower based on your trading style

Volume Analysis: Increase the lookback period for a longer-term volume profile or decrease it for more recent activity

Visual Clarity: Adjust colors and transparency settings to match your chart theme and preferences

Conclusion:

This indicator provides traders with a comprehensive view of both trend dynamics and volume-based support/resistance levels. With these two analytical approaches, the indicator offers valuable insights for identifying potential entry and exit points, trend strength, and key price levels where significant market activity has occurred. The extensive customization options allow traders to adapt the indicator to various trading styles and timeframes, with optimal performance on 15-minute to daily charts depending on their trading horizon.

Chart Attached: NSE HINDZINC, EoD 12/12/25

DISCLAIMER: This information is provided for educational purposes only and should not be considered financial, investment, or trading advice. Please do boost if you like it. Happy Trading.

Educational

ZigZag++ UltraAlgo EditionLagging indicator used to understand trends and entry / exit points. Suggest using at 4h - 1d intervals first, then 1-2h, to identify zones of opportunities and validate your position.

GVWAP_Core (CalendarSpan + EventSpike)GVWAP Core Indicator

General Description (Public)

GVWAP (Generalized Volume-Weighted Average Price) is an advanced anchoring and averaging framework designed to reveal market structure rather than predict price. Unlike traditional VWAP, GVWAP is not limited to volume weighting or session-based anchoring. It can operate on any input series (price, indicators, transforms) and supports multiple weighting schemes, decay behavior, and structural reset logic.

At its core, GVWAP answers a simple question: “Where is the statistically relevant center of activity since the last meaningful structural event?”

The indicator continuously updates a weighted average of the input series, gradually forgetting older data using exponential decay. The anchor point can reset on calendar boundaries (day, week, month, etc.) or on statistically significant events such as abnormal volume spikes. Robust dispersion bands based on mean absolute deviation (MAD) surround the average, providing context for trend, rotation, and compression regimes.

GVWAP is not a trading signal by itself. It is best used as a structural reference layer or as an intermediate transform feeding other indicators, strategies, or regime filters.

Mathematical Description (Quantitative)

Let x_t be an arbitrary input series and w_t a selectable weight function. GVWAP is defined as a normalized exponentially decayed weighted estimator:

GVWAP_t = N_t / D_t

with recursive updates:

N_t = (1 − α)·N_{t−1} + α·w_t·x_t

D_t = (1 − α)·D_{t−1} + α·w_t

where α = 1 − 2^(−1/H) and H is the decay half-life in bars.

Weights may be defined as:

• w_t = V_t (volume)

• w_t = 1 (equal weight)

• w_t = 1 / ATR_t (volatility-normalized)

• w_t = f(n_t) (time-weighted, where n_t is bars since reset)

The estimator resets when a structural condition R_t is satisfied, at which point:

N_t = w_t·x_t, D_t = w_t

For event-based anchoring, volume surprise is computed using a Student‑t–compressed z‑score:

z_t = (V_t − μ_V) / σ_V

tZ_t = z_t / sqrt(1 + z_t² / ν)

A reset occurs when tZ_t exceeds a threshold τ.

Dispersion is measured via a decayed Mean Absolute Deviation:

MAD_t = (Σ λ^{t−i} w_i |x_i − GVWAP_t|) / (Σ λ^{t−i} w_i)

Bands are defined as GVWAP_t ± k·MAD_t.

GVWAP therefore represents a bounded-memory, robust, non‑Gaussian estimator of the local conditional expectation of x_t under dynamic anchoring and weighting.

S&R Detector by Rakesh Sharma📊 Support & Resistance Auto-Detector

Automatically identifies key Support and Resistance levels with strength ratings

✨ Key Features:

🎯 Intelligent S/R Detection

Automatically finds Support and Resistance levels based on swing highs/lows

Shows strength rating (Very Strong, Strong, Medium, Weak)

Displays number of touches at each level

📅 Key Time-Based Levels

Previous Day High/Low (PDH/PDL) - Blue lines

Previous Week High/Low (PWH/PWL) - Purple lines

Optional Round Numbers for psychological levels

⚙️ Fully Customizable

Adjust sensitivity (5-20 pivot length)

Filter by minimum touches (1-10)

Control maximum levels displayed (3-20)

Optional S/R zones (shaded areas)

📊 Live Dashboard

Shows nearest Support/Resistance

Distance to key levels

Total S/R levels detected

🔔 Smart Alerts

PDH/PDL breakout signals

Visual markers on chart

Perfect for: Intraday traders, Swing traders, Price action analysis

Support & Resistance Auto-Detector by Rakesh SharmaVersion 1.1 Update:

- Fixed: S/R lines now extend infinitely to the right

- Fixed: Lines move with chart when scrolling

- Added: Toggle to control line extension

- Improved: Better visibility across all timeframes

VX-Session-Boxes-(AM/PM Split)(Customizable) by Ikaru-s-VX-Session-Boxes-(AM/PM Split) is a session-based visualization tool for TradingView that highlights major market sessions directly on the chart using dotted range boxes and an optional AM/PM split.

The indicator allows traders to visually separate market behavior across different sessions while keeping the chart clean and readable.

🔹 Key Features

Custom Session Definitions

Define up to 4 independent sessions using TradingView’s session format (HHMM-HHMM + weekdays).

Timezone-Aware

All sessions are calculated using a user-defined timezone (IANA or UTC offset), ensuring accurate session alignment across markets.

Dotted Session Boxes

Each session is drawn as a dotted box based on the session’s high/low range, providing a clear view of volatility and price structure.

AM / PM Split Visualization

Sessions can be visually split into AM and PM parts:

Separate box shading for AM and PM

Optional dotted vertical split line at the AM → PM transition (12:00 in the selected timezone)

Session Labels

Optional labels at the start of each session for quick identification (e.g. Sydney, Tokyo, London, New York).

Fully Customizable Visuals

Adjustable opacity, border width, and visibility toggles for boxes, split lines, and labels.

🔹 Use Cases

Session-based market analysis (Asia / London / New York)

Identifying session ranges and volatility expansion

Observing price behavior differences between AM and PM

Studying session transitions and liquidity shifts

🔹 Notes

Session boxes are based on session high and low, not full chart height.

AM/PM split is based on 12:00 (noon) in the selected timezone.

Designed for clarity and performance on intraday timeframes.

🔹 Compatibility

Pine Script® v6

Works on all intraday timeframes

Overlay indicator (draws directly on the price chart)

Breakout/Breakdown DetectorBreakout/Breakdown Detector - Quick Overview

What it does:

This indicator automatically identifies when price breaks through key support or resistance levels, signaling potential trading opportunities.

Key Features:

📈 Breakout Detection - Alerts when price breaks ABOVE resistance (bullish signal)

📉 Breakdown Detection - Alerts when price breaks BELOW support (bearish signal)

🔊 Volume Confirmation - Optionally requires high volume to confirm the break (filters false signals)

📊 Visual Signals - Shows green triangles (breakout) and red triangles (breakdown) on chart

🎨 Support/Resistance Lines - Automatically draws key levels based on recent price action

Settings You Can Adjust:

Lookback Period (default 20) - How many candles back to find support/resistance

Volume Multiplier (default 1.5x) - How much volume needed to confirm

Breakout Threshold (default 0.5%) - How far price must break through the level

How to Use:

Add to any chart (stocks, crypto, forex, etc.)

Green triangle below bar = BUY signal (breakout)

Red triangle above bar = SELL signal (breakdown)

Set alerts to get notified automatically

Perfect for: Swing traders, breakout traders, and anyone who wants to catch momentum moves early! 🚀

Neosha Concept V4 (NY Time)

Imagine the financial market as a huge ocean. Millions of traders throw orders into it every second. But beneath all the noise, there is a powerful current that quietly controls where the waves move. That current is not a person, not a trader, and not random—it is an algorithm.

This algorithm is called the Interbank Price Delivery Algorithm (IPDA).

Think of it as the “navigation system” that guides price through the market.

IPDA has one job:

to move prices in a way that keeps the market efficient and liquid.

To do this, it constantly looks for two things:

1. Where liquidity is hiding

Liquidity is usually found above highs and below lows—where traders place stop losses. The algorithm moves price there first to collect that liquidity.

2. Where price became unbalanced

Sometimes price moves too fast and creates gaps or imbalances. IPDA returns to those areas later to “fix” the missing orders.

Once you start looking at the charts with this idea in mind, everything makes more sense:

Why price suddenly spikes above a high and crashes down

Why big moves leave gaps that price later fills

Why the market reverses right after taking stops

Why trends begin only after certain levels are hit

These are not accidents.

They are the algorithm doing its job.

Price moves in a repeating cycle:

Gather liquidity

Make a strong move (displacement)

Return to fix inefficiency

Deliver to the next target

Most beginners only see the candles.

But once you understand IPDA, you see the intention behind the candles.

Instead of guessing where price might go, you begin to understand why it moves there.

And once you understand the “why,” your trading becomes clearer, calmer, and far more accurate.

S&R Detector by Rakesh SharmaSupport & Resistance Auto-Detector

Automatically identifies key Support and Resistance levels with strength ratings

✨ Key Features:

🎯 Intelligent S/R Detection

Automatically finds Support and Resistance levels based on swing highs/lows

Shows strength rating (Very Strong, Strong, Medium, Weak)

Displays number of touches at each level

📅 Key Time-Based Levels

Previous Day High/Low (PDH/PDL) - Blue lines

Previous Week High/Low (PWH/PWL) - Purple lines

Optional Round Numbers for psychological levels

⚙️ Fully Customizable

Adjust sensitivity (5-20 pivot length)

Filter by minimum touches (1-10)

Control maximum levels displayed (3-20)

Optional S/R zones (shaded areas)

📊 Live Dashboard

Shows nearest Support/Resistance

Distance to key levels

Total S/R levels detected

🔔 Smart Alerts

PDH/PDL breakout signals

Visual markers on chart

Perfect for: Intraday traders, Swing traders, Price action analysis

Prince Break and RetestHow to use the new visuals (super simple)

When the script prints RETEST BUY or RETEST SELL, you will instantly see:

ENTRY line (lime)

SL line (orange)

TP1 line (teal)

TP2 line (purple)

Entry Mode options

Close = enter at the close of the retest signal candle (simplest)

Box Edge = enter at the box edge (more “limit-order-ish”)

For your style (break + retest), start with Close.

S&R Detector by Rakesh Sharma📊 Support & Resistance Auto-Detector

Automatically identifies key Support and Resistance levels with strength ratings

✨ Key Features:

🎯 Intelligent S/R Detection

Automatically finds Support and Resistance levels based on swing highs/lows

Shows strength rating (Very Strong, Strong, Medium, Weak)

Displays number of touches at each level

📅 Key Time-Based Levels

Previous Day High/Low (PDH/PDL) - Blue lines

Previous Week High/Low (PWH/PWL) - Purple lines

Optional Round Numbers for psychological levels

⚙️ Fully Customizable

Adjust sensitivity (5-20 pivot length)

Filter by minimum touches (1-10)

Control maximum levels displayed (3-20)

Optional S/R zones (shaded areas)

📊 Live Dashboard

Shows nearest Support/Resistance

Distance to key levels

Total S/R levels detected

🔔 Smart Alerts

PDH/PDL breakout signals

Visual markers on chart

Perfect for: Intraday traders, Swing traders, Price action analysis

Smart WhaleOverview The Smart Whale Breakout System is a pure momentum strategy designed for Swing Traders who want to capture high-probability breakouts while managing risk with a mechanical trailing stop.

Unlike indicators that try to guess "bottoms," this system follows the "Smart Money" approach: buying strength when institutional volume enters, and riding the trend until the momentum breaks.

How it Works

1. The Entry (The Hunter) The system identifies a valid BREAKOUT signal only when four specific conditions align:

Trend Filter: Price must be above the 150 SMA. We only trade with the long-term trend.

Momentum: RSI > 50. Ensuring bulls are in control.

Volume Spike (Whale Activity): Current volume must be significantly higher than the average (Default: 1.5x). This filters out weak retail moves.

Price Action: A bullish candle closing higher than it opened.

2. The Exit (The Manager) Once in a trade, the system activates a dynamic Trailing Stop line. You never have to guess when to sell. You can choose between two exit logic modes in the settings:

ATR Trailing (Default): Adapts to volatility. The stop moves up based on a multiple of the Average True Range (ATR). Great for volatile stocks (e.g., TSLA, NVDA).

Percent Trailing: A fixed percentage drop from the highest high. (e.g., "Sell if price drops 10% from peak").

3. The Context (Optional Filter)

Squeeze Filter: Includes a built-in Bollinger/Keltner squeeze detection. If enabled in settings, the system will only signal a buy if the price recently broke out of a consolidation (squeeze). Default is OFF to catch all momentum moves.

Key Features

NO Repainting: Signals are confirmed at candle close.

Visual Risk Management: A Red Trailing Stop line clearly shows where your invalidation point is.

Fully Customizable: Adjust the Volume multiplier, ATR sensitivity, or Percentage drop to fit your asset class (Crypto/Stocks/Forex).

Clean Visuals: Only colors the Breakout and Sell candles to keep your chart clean.

Settings Guide

Trend SMA Length: Define the long-term trend baseline (Default: 150).

Volume Spike (xAvg): How much volume is needed to trigger a buy? (1.5 = 150% of average).

Exit Method: Choose between "ATR Trailing" or "Percent Trailing".

ATR Multiplier: Tighter stop (2.0) vs Looser stop (3.0).

Require Squeeze?: Check this to filter for breakouts that only happen after a consolidation period.

Disclaimer This tool is for educational purposes only. Always use proper risk management.

Bassi MA Entry Helper MTF EMA , VWMA Swing , ADX , SMA200 , TPBassi MA Entry Helper is an advanced multi-timeframe confluence system designed to identify high-probability entries using trend, volume, market structure, and volatility filters.

It is built for traders who want cleaner signals, fewer false entries, and strong multi-confirmation setups.

Key Features

Multi-Timeframe EMA Crossovers – HTF signal engine

SMA200 Trend Filter – prevents counter-trend trades

VWMA Swing Confirmation – volume-validated micro-swings

ADX Filter – only trade when the trend has strength

Fractal Structure Mapping – identifies swing highs/lows

Retracement Filter – confirms pullbacks before entries

TP/SL Automation – ATR or percentage based

Clean Entry Labels – main & additional entry signals

Highly Customizable – mode, timeframe, filters, visuals

This script is ideal for:

Scalping • Intraday • Swing • Trend continuation • Volume-based setups • Multi-timeframe alignment

How It Works

Main Buy/Sell Signals

Triggered when:

✔ Fast EMA crosses Slow EMA (HTF)

✔ Price aligned with trend

✔ SMA200 filter valid

✔ VWMA confirmation (optional)

✔ ADX strong

✔ Retracement valid (optional)

Additional Buy/Sell Signals

Triggered when VWMA crosses Slow EMA during trend continuation.

TP/SL System

You can choose between:

%-based take-profit & stop-loss

ATR-based dynamic levels

Automatically projects clean visual levels on your chart.

Notes

This indicator does not repaint and is suitable for both real-time and historical analysis.

Always combine signals with proper risk management.

Initial Release – v1.0

Added multi-timeframe EMA engine

Added SMA200 trend filter

Added VWMA swing entries

Added ADX strength filter

Added retracement filter

Added fractal swing detection

Added TP/SL auto plotting

Added main & additional entry labels

Performance optimized

ORB + FVG + PDH/PDL ORB + FVG + PDH/PDL is an all-in-one day-trading overlay that plots:

Opening Range (ORB) high/low with optional box and extension

Fair Value Gaps (FVG) with optional “unmitigated” levels + mitigation lines

Previous Day High/Low history (PDH/PDL) drawn as one-day segments (yesterday’s levels plotted across today’s session only)

Includes presets (ORB only / FVG only / Both) and optional alerts for ORB touches, ORB break + retest, FVG entry, and PDH/PDL touches.

Cup & Handle Finder by Mashrab🚀 New Tool Alert: The "Perfect Cup" Finder

Hey everyone! I’ve built a custom indicator to help us find high-quality Cup & Handle setups before they breakout.

Most scripts just look for random highs and lows, but this one uses a geometric algorithm to ensure the base is actually round (avoiding those messy V-shapes).

How it works:

🔵 Blue Arc: This marks a verified, institutional-quality Cup.

🟠 Orange Box: This is the "Handle Zone." If you see this connecting to the current candle, it means the setup is live and ready for a potential entry!

Best Usage:

Works best on Weekly (1W) charts.

It’s designed to be an "Early Warning" system—alerting you while the handle is still forming so you don't miss the move.

Give it a try and let me know what you find! 📉📈

S&R + EMA ToolkitThis script is a market-structure toolkit that combines several indicators into a single view to help understand where price is, where it may react, and what the current trend context is.

EMAs (12, 26, 50, 200)

Help define short-, medium-, and long-term trend context and momentum alignment.

Support & Resistance Channels

Help identify key price zones where the market has historically reacted (areas of acceptance, rejection, and consolidation).

Supertrend

Helps confirm directional bias and trend persistence.

Oversold / Overbought RSI Zones (external source)

Help identify market conditions rather than timing entries.

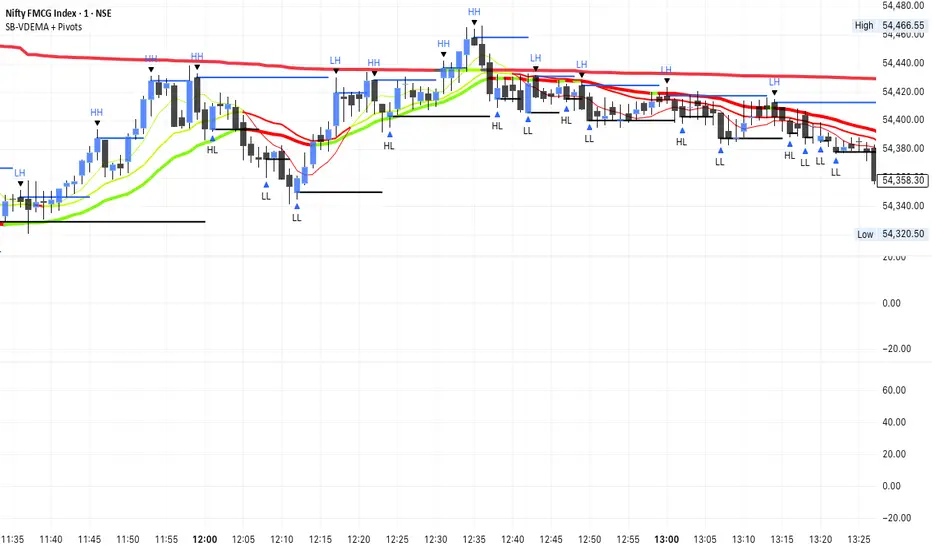

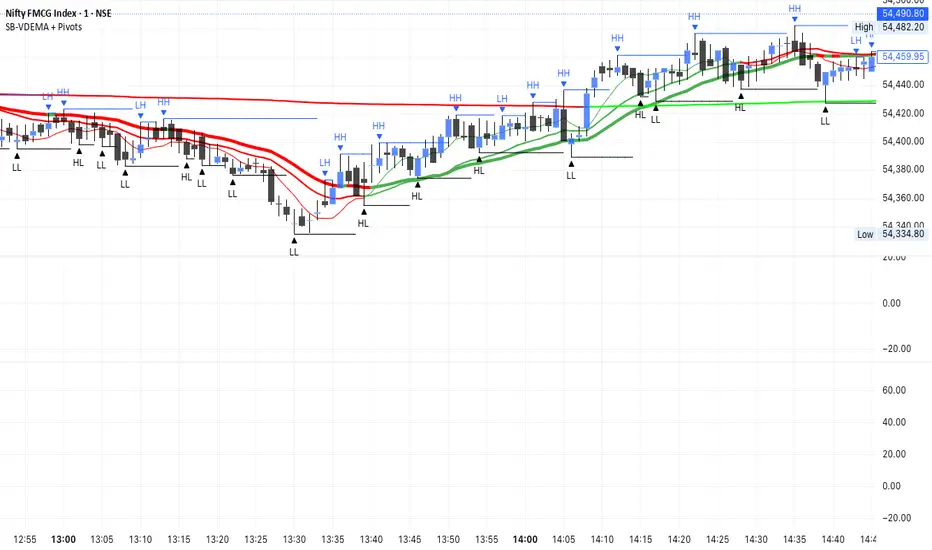

SB-VDEMA + PivotsBest use - Intraday Scalping ( 1 Mt, 3 Mts, 5 Mts )

Uses Volatility weighted DEMA for smoother and reliable signals.

One can use dynamic colour coding of VWDEMA for entering call or puts. VWAP and Henkin ashi Supertrend is also there but, i think VWDEMA is quite enogh for decision making.

SB - Ultimate Clean Trend Pro Uses dynamic Moving colour coding for spotting chage of bias. Use set up with keeping VWAP in reference.

Auto Trend [theUltimator5]The Auto Trend indicator was designed to be a unique pattern detection indicator without the use of standard pivot point logic or high/low lines. It is a study in pattern detection by using iterative best-fit logic.

The indicator automatically identifies and draws trend channels by analyzing price action across configurable lookback periods. It finds optimal high and low trendlines that contain price movement, with a middle line marking the trend's center.

Key Features:

Automatic Pattern Detection - Intelligently searches for the best lookback period where price stays within the channel boundaries

Dual Pattern Modes - Choose between Short (20-66 bars) for quick patterns or Long (50-500 bars) for extended trends. Note - the long pattern is fully configurable and can be set anywhere up to 5000 bars.

Smart Caching - Optimized performance that only recalculates when necessary

Customizable Starting Point - Click directly on the chart to set where the trend channel begins

Flexible Lookback Range - Set minimum and maximum lookback periods to match your trading style

Visual Debugging - Optional label displays the active lookback period and violation count

How It Works:

The indicator divides the lookback period into thirds, finds the highest and lowest closes in the first and last thirds, then draws trendlines connecting these points. It can automatically search through different lookback periods to find the one with the fewest price violations (closes outside the channel).

Settings:

Use Auto Lookback - Enable automatic optimal lookback detection

Pattern Length - Short (faster, 1-bar increments) or Long (broader, 5-bar increments)

Min/Max Lookback - Define the search range for the Long pattern

Manual Lookback - Override auto-detection with a fixed period

Custom Colors - Personalize the high, low, and middle line colors

Starting Point - Select where the trend analysis begins

Use Cases:

Identify dominant trend channels across different timeframes

Spot potential support and resistance levels

Determine trend strength and consistency

Time entries and exits based on channel position

The indicator supports up to 5000 bars of historical data for comprehensive trend analysis.

FL Core Signals Only FL Core shows only what matters: where to enter, where to exit, and where prof

No indicator noise — just confirmed decision points on a clean chart.

Designed for traders who value structure, patience, and clarity.

What FL Core Does

FL Core marks:

ENTER LONG

ENTER SHORT

AND

EXIT SHORT

TP1 / TP2 / TP3 profit targets

All signals are generated using a fixed, non-repainting ruleset and are confirmed only after candle close.

How It Trades (High Level)

Identifies momentum shifts using internal trend logic

Requires a full candle confirmation before signaling entries

Holds trades until momentum breaks, then signals exit

Tracks profit targets automatically in points

No guessing. No anticipation. No repainting.

Session Rules

FL Core is hard-wired to operate only between 4:00 AM and 4:00 PM (exchange time).

Signals outside of this window are intentionally ignored to avoid low-liquidity and overnight conditions.

Chart Design Philosophy

This version intentionally hides all underlying indicators and displays only:

Clean entry markers

Clean exit markers

Profit plate

A single gold Exit Rail that visually guides trade management

The focus stays on execution and decision-making, not indicator interpretation.

Profit Targets

Default profit targets are:

TP1: 25 points

TP2: 40 points

TP3: 60 p

Targets can be adjusted by the user.

Note: Default profit targets are optimized for NQ/MNQ, which was the primary instrument used during testing.

Traders using ES/MES should reduce target distances to better match volatility.

Important Notes

FL Core is an indicator, not an automated trading system

Stop-loss placement is handled manually according to your trading plan

Signals are designed to encourage discipline and patience, not over-trading

Marker placement (above/below bar) is intentional and should not be changed

Who This Is For

✔ Beginner traders

✔ Traders overwhelmed by indicators

✔ Traders who want clear structure and rules

✔ Traders focused on execution discipline

Who This Is NOT For

✘ Traders looking for fully automated execution

✘ Traders who want constant signals

✘ Traders who ignore risk management

Final Thought

FL Core does not try to predict the market.

It helps you wait for confirmation, execute cleanly, and manage trades with structure.

If you want fewer decisions, clearer trades, and a calmer trading experience — this is where you start.

Session Levels (Daily & Weekly Targets)This indicator provides market structure and contextual reference only. It does not generate trade signals, entries, or trading advice.

Plots rolling previous daily and weekly highs/lows as potential target levels. Levels automatically remove once touched (including wicks). Default visibility is NY session with optional toggles for London and Asia. Designed for intraday structure, confluence, and target identification.

Fibonacci Fibonacci automatic drawing - Last 144 barFibonacci automatic drawing:

It automatically plots Fibonacci based on the last 144 bars.

According to the drawing rules, it calculates itself from bottom to top and from top to bottom.

This will answer the most challenging questions about drawing the right thing.

If 144 bar is not reached, it draws using manual input.

This will be a useful and practical perspective.

This is for those who want to see the most valuable Fibonacci values on a chart.

BIGG CHIEFF RWB MASTER v2.0 (Indicator) [v1.0]Here is a **clean, professional TradingView indicator description** you can paste directly into the script description. It explains the *logic and philosophy* without exposing proprietary specifics, while still sounding robust and credible.

---

## 📊 Indicator Overview

This indicator is a **rule-based EMA crossover strategy built on price action, opening range structure, directional bias, and momentum confirmation**.

It is designed for intraday trading during the New York session and adapts to both time-based and tick-based charts.

The system focuses on **clarity, patience, and consistency**, filtering out low-quality conditions while aligning trades with higher-probability market structure.

---

## 🧭 Core Concepts

### Opening Range Structure

* The strategy uses the **first 15 minutes of the New York session** to define an Opening Range.

* This range establishes **key intraday structure**, including:

* High

* Low

* Midpoint

* The Opening Range remains visible for the entire session and resets each day.

* Trades are framed around **breaks, retests, and rejections** of this structure.

---

## 📈 Trend, Bias & Momentum

### Directional Bias

Bias is determined by:

* **EMA stacking order**

* **Price location relative to the Opening Range**

* Optional **higher-timeframe trend alignment**

Once bias is confirmed:

* Trades are only taken **in the direction of that bias**

* Opposing trades are locked out until structure meaningfully changes

This prevents overtrading and reduces whipsaws in choppy conditions.

---

### Higher-Timeframe Alignment (Optional)

A higher-timeframe trend filter can be enabled to:

* Keep trades aligned with the broader market direction

* Improve win rate during trending sessions

* Reduce countertrend entries

---

## ⚡ Volatility & Time Filters

To avoid low-quality trades, the system includes:

* **Volatility filtering** to prevent entries during compressed or dead markets

* **Session time windows** to focus on the most liquid trading hours

* Optional **no-trade time blocks** for news or known high-risk periods

---

## 💧 Liquidity Awareness

The indicator accounts for **key liquidity zones**, such as:

* Prior session highs and lows

* Overnight and premarket extremes

Trades are filtered to ensure there is **sufficient room for reward** before running into nearby liquidity, helping avoid premature exits.

---

## ✅ Entry Logic (Primary Mode)

Trades are based on **structure first, confirmation second**:

* Breakouts must be confirmed by **candle closes**, not wicks

* Entries occur on **retracements and rejection candles**, not chase candles

* Priority is given to cleaner retests closer to structure

* Optional controls allow limiting trades to **first-touch setups only**

This encourages patience and avoids emotional entries.

---

## 🛑 Risk Management & Trade Management

The system is built around **R-multiple consistency**, not fixed targets.

* Stops are volatility-based

* Multiple profit targets can be enabled

* Optional partial profits and trailing stop logic are included

* Trailing behavior can follow momentum or structure once price moves favorably

Everything is designed to **protect capital first and scale winners second**.

---

## 🧠 Philosophy

This indicator is not designed to predict the market.

It is designed to **react intelligently** to what price is already confirming.

It prioritizes:

* Structure over indicators

* Bias over impulse

* Confirmation over hope

* Risk management over win rate

Best results come from disciplined execution, patience, and respecting the filters.