DayFlow VWAP Relay Forex Majors StrategySummary in one paragraph

DayFlow VWAP Relay is a day-trading strategy for major FX pairs on intraday timeframes, demonstrated on EURUSD 15 minutes. It waits for alignment between a daily anchored VWAP regime check, residual percentiles, and lower-timeframe micro flow before suggesting trades. The originality is the fusion of daily VWAP residual percentiles with a live micro-flow score from 1 minute data to switch between fade and breakout behavior inside the same session. Add it to a clean chart and use the markers and alerts.

Scope and intent

• Markets: Major FX pairs such as EURUSD, GBPUSD, USDJPY, AUDUSD, USDCHF, USDCAD

• Timeframes: One minute to one hour

• Default demo in this publication: EURUSD on 15 minutes

• Purpose: Reduce false starts by acting only when context, location and micro flow agree

• Limits: This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Core novelty: Residual percentiles to daily anchored VWAP decide “balanced versus expanding day”. A separate 1 minute micro-flow score confirms direction, so the same model fades extremes in balance and rides range breaks in expansion

• Failure modes addressed: Chop fakeouts and unconfirmed breakouts are filtered by the expansion gate and micro-flow threshold

• Testability: Every input is exposed. Bands, background regime color, and markers show why a suggestion appears

• Portable yardstick: Stops and targets are ATR multiples converted to ticks, which transfer across symbols

• Open source status: No reused third-party code that requires attribution

Method overview in plain language

The day is anchored with a VWAP that updates from the daily session start. Price minus VWAP is the residual. Percentiles of that residual measured over a rolling window define location extremes for the current day. A regime score compares residual volatility to price volatility. When expansion is low, the day is treated as balanced and the model fades residual extremes if 1 minute micro flow points back to VWAP. When expansion is high, the model trades breakouts outside the VWAP bands if slope and micro flow agree with the move.

Base measures

• Range basis: True Range smoothed by ATR for stops and targets, length 14

• Return basis: Not required for signals; residuals are absolute price distance to VWAP

Components

• Daily Anchor VWAP Bands. VWAP with standard-deviation bands. Slope sign is used for trend confirmation on breakouts

• Residual Percentiles. Rolling percentiles of close minus VWAP over Signal length. Identify location extremes inside the day

• Expansion Ratio. Standard deviation of residuals divided by standard deviation of price over Signal length. Classifies balanced versus expanding day

• Micro Flow. Net up minus down closes from 1 minute data across a short span, normalized to −1..+1. Confirms direction and avoids fades against pressure

• Session Window optional. Restricts trading to your configured hours to avoid thin periods

• Cooldown optional. Bars to wait after a position closes to prevent immediate re-entry

Fusion rule

Gating rather than weighting. First choose regime by Expansion Ratio versus the Expansion gate. Inside each regime all listed conditions must be true: location test plus micro-flow threshold plus session window plus cooldown. Breakouts also require VWAP slope alignment.

Signal rule

• Long suggestion on balanced day: residual at or below the lower percentile and micro flow positive above the gate while inside session and cooldown is satisfied

• Short suggestion on balanced day: residual at or above the upper percentile and micro flow negative below the gate while inside session and cooldown is satisfied

• Long suggestion on expanding day: close above the upper VWAP band, VWAP slope positive, micro flow positive, session and cooldown satisfied

• Short suggestion on expanding day: close below the lower VWAP band, VWAP slope negative, micro flow negative, session and cooldown satisfied

• Positions flip on opposite suggestions or exit by brackets

What you will see on the chart

• Markers on suggestion bars: L for long, S for short

• Exit occurs on reverse signal or when a bracket order is filled

• Reference lines: daily anchored VWAP with upper and lower bands

• Optional background: teal for balanced day, orange for expanding day

Inputs with guidance

Setup

• Signal length. Residual and regime window. Typical 40 to 100. Higher smooths, lower reacts faster

Micro Flow

• Micro TF. Lower timeframe used for micro flow, default 1 minute

• Micro span bars. Count of lower-TF bars. Typical 5 to 20

• Micro flow gate 0..1. Minimum absolute flow. Raising it demands stronger confirmation and reduces trade count

VWAP Bands

• VWAP stdev multiplier. Band width. Typical 0.8 to 1.6. Wider bands reduce breakout frequency and increase fade distance

• Expansion gate 0..3. Threshold to switch from fades to breakouts. Raising it favors fades, lowering it favors breakouts

Sessions

• Use session filter. Enable to trade only inside your window

• Trade window UTC. Default 07:00 to 17:00

Risk

• ATR length. Stop and target basis. Typical 10 to 21

• Stop ATR x. Initial stop distance in ATR multiples

• Target ATR x. Profit target distance in ATR multiples

• Cooldown bars after close. Wait bars before a new entry

• Side. Both, long only, or short only

View

• Show VWAP and bands

• Color bars by residual regime

Properties visible in this publication

• Initial capital 10000

• Base currency Default

• request.security uses lookahead off everywhere

• Strategy: Percent of equity with value 3. Pyramiding 0. Commission cash per order 0.0001 USD. Slippage 3 ticks. Process orders on close ON. Bar magnifier ON. Recalculate after order is filled OFF. Calc on every tick OFF. Using standard OHLC fills ON.

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Fills and slippage vary by venue. Shapes can move while a bar forms and settle on close. Strategies must run on standard candles for signals and orders.

Honest limitations and failure modes

High impact news, session opens, and thin liquidity can invalidate assumptions. Very quiet days can reduce contrast between residuals and price volatility. Session windows use the chart exchange time. If both stop and target are touched within a single bar, TradingView’s standard OHLC price-movement model decides the outcome.

Expect different behavior on illiquid pairs or during holidays. The model is sensitive to session definitions and feed time. Past results never guarantee future outcomes.

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Fx

Forex Midpoint Stratejisi For Nasdaq English Knowledge:

Midpoint Strategy;

The general calculation method is a strategy that helps determine direction by the intersection of a MA line and the value obtained by dividing the lowest and highest price in the specified length range.

Başlangıç Periyodu: The data length of the Midpoint Line.

Kaydırma Seviyesi: The number of steps forward or backward of the Midpoint Line.

Yüzde Seviyesi: the amount of vertical scrolling.

Uzunluk: The length of the MA line

represents.

This strategy is prepared for the Nasdaq 5-minute period. It needs to be optimized for use on other instruments.

There are take profit and stop loss levels within the codes. Friends who want to use it can remove the invisibility from the relevant sections. Also, I removed the midpoint and the MA line so that it does not crowd the image, you can add it if you want.

Thank you.

Turkish Knowledge:

Midpoint Stratejisi;

Genel hesaplama yöntemi, belirlenen uzunluk aralığındaki en düşük ve en yüksek fiyatın ikiye bölümü ile elde edilen değer ve bir ortalama çizgisinin kesişimleriyle yön belirlemeye yardımcı bir stratejidir.

Başlangıç Period: Midpoint Çizgisinin veri uzunluğunu.

Kaydırma Seviyesi: Midpoint Çizgisinin ileri veya geri adım sayısını.

Yüzde Seviyesi: dikey kaydırma miktarını.

Uzunluk: Ortalama çizgisinin uzunluğunu

temsil etmektedir.

Bu strateji Nasdaq 5 dakikalık periot için hazırlanmıştır. Diğer enstrümanlarda kullanılması için optimize edilmesi gerekir.

Kodların içinde Kar alma , zarar durdurma seviyeleri mevcuttur. Kullanmak isteyen arkadaşlar ilgili bölümlerden görünmezliği kaldırabilirler. ayrıca midpoint ve ortalama çizgisinide görüntü kalabalığı yapmaması için ben kaldırdım isterseniz siz ekleyebilirsiniz.

Teşekkürler.

Strategy NNFX Tester Strategy NNFX, Baseline, QQEs Fast C1, Slow C2, ATR, Volume and Exit

This is a Strategy Tester designed to work with Study (Alerts) of the same.

At time of creation based on Revision 8 of the Study.

DO NOT USE the Currency/Money Management section under settings. use the position sizing under "Inputs" - "Money Management" - "Risk per trade" which is defaulted to 2%

This has adjustable Baselines, Exits, ATR calculations, C1 and C2 are currently QQE & QQE Histo with adjustable settings but I'll include more choice of C1 & C2 as time goes on.

Find settings that work for you, then move them over to the Study version for best results.

Forward plans are to add much more options to both Alert/Strategy.

If anyone wants to collaborate or anything hit me up.

GBP/JPY Daily time FX Strategy ATR W% BaselineThis is a preety good strategy suited for long term trading.

It has been adapted and optimized in this case for GBP/JPY 1D time frame.

Its made of Kiojun baseline, together with ATR for stop loss and size calculation and Williams % R

For the purpose of this example we simulate that we have a leverage of 100x in order to be able to buy the ammount of lots required for our stop loss to be in same page with the risk % of our capital.

For entry we have for long, ascending R in the last 2 candles and crossover of close with KIOJUN baseline. For short the same but in reverse.

We exit if we reach the TP -100 points in this example, or SL , which is based on ATR of the last x days.

If you have any questions feel free to write me in private !

Combo Backtest 123 Reversal & FX Sniper: T3-CCI This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

This simple indicator gives you a lot of useful information - when to enter, when to exit

and how to reduce risks by entering a trade on a double confirmed signal.

You can use in the xPrice any series: Open, High, Low, Close, HL2, HLC3, OHLC4 and ect...

WARNING:

- For purpose educate only

- This script to change bars colors.

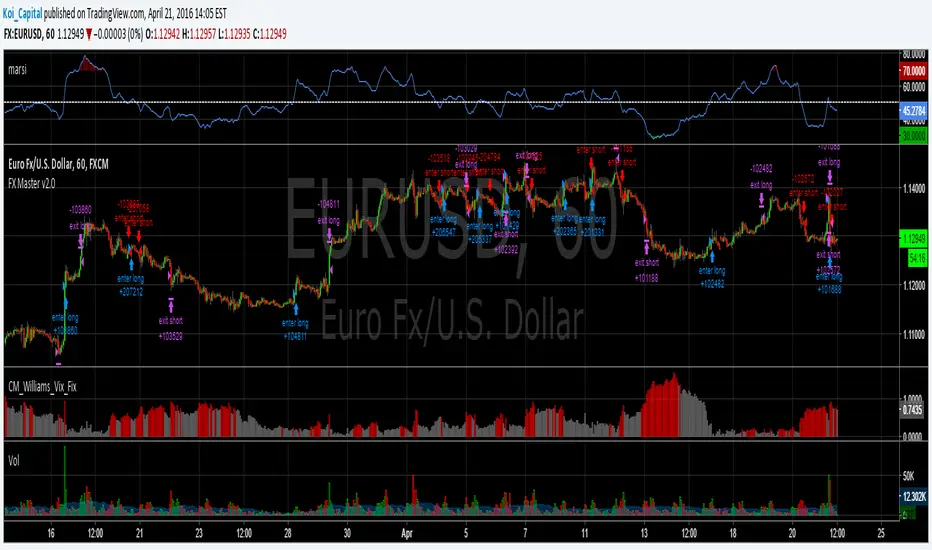

Forex Master v2.0 (EUR/USD)This is version 2 of my Forex Master algorithm originally posted here:

BACKTEST CONDITIONS:

Initial equity = $100,000 (no leverage)

Order size = 100% of equity

Pyramiding = disabled

TRADING RULES:

Long entry = EMA5(RSI20) cross> 50

Profit limit = 50 pips

Stop loss = 50 pips

Short entry = EMA5(RSI20) cross< 50

Profit limit = 50 pips

Stop loss = 50 pips

Long entry = Short exit

Short entry = long exit

DISCLAIMER: None of my ideas and posts are investment advice. Past performance is not an indication of future results. This strategy was constructed with the benefit of hindsight and its future performance cannot be guaranteed.

Forex Master (EUR/USD)ATTENTION:

This is a symmetrical algorithm designed only for trading EUR/USD on the 1h time frame. For other currency pairs and time frames, you need to re-calibrate the RSI-EMAs as well as the profit targets and stop losses.

BACKTEST CONDITIONS:

Initial equity = $100,000 (no leverage)

Order size = 100% of equity

Pyramiding = disabled

TRADING RULES:

Long entry = EMA20(RSI10) cross> 50

Profit limit = 50 pips

Stop loss = 50 pips

Short entry = EMA30(RSI30) cross< 50

Profit limit = 50 pips

Stop loss = 50 pips

Long entry = Short exit

Short entry = long exit

DISCLAIMER: None of my ideas and posts are investment advice. Past performance is not an indication of future results. This strategy was constructed with the benefit of hindsight and its future performance cannot be guaranteed.