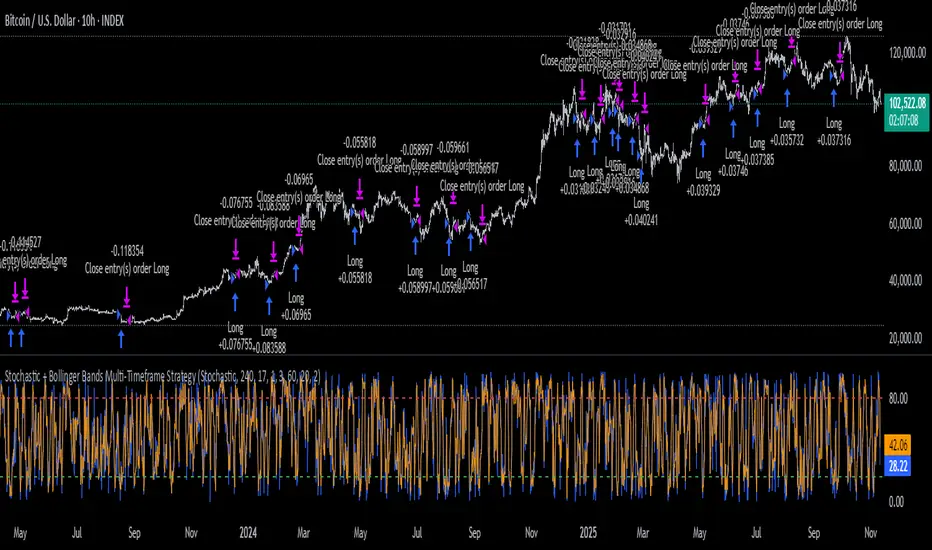

Stochastic + Bollinger Bands Multi-Timeframe StrategyThis strategy fuses the Stochastic Oscillator from the 4-hour timeframe with Bollinger Bands from the 1-hour timeframe, operating on a 10-hour chart to capture a unique volatility rhythm and temporal alignment discovered through observational alpha.

By blending momentum confirmation from the higher timeframe with short-term volatility extremes, the strategy leverages what some traders refer to as “rotating volatility” — a phenomenon where multi-timeframe oscillations sync to reveal hidden trade opportunities.

🧠 Strategy Logic

✅ Long Entry Condition:

Stochastic on the 4H timeframe:

%K crosses above %D

Both %K and %D are below 20 (oversold zone)

Bollinger Bands on the 1H timeframe:

Price crosses above the lower Bollinger Band, indicating a potential reversal

→ A long trade is opened when both momentum recovery and volatility reversion align.

✅ Long Exit Condition:

Stochastic on the 4H:

%K crosses below %D

Both %K and %D are above 80 (overbought zone)

Bollinger Bands on the 1H:

Price reaches or exceeds the upper Bollinger Band, suggesting exhaustion

→ The long trade is closed when either signal suggests a potential reversal or overextension.

🧬 Temporal Structure & Alpha

This strategy is deployed on a 10-hour chart — a non-standard timeframe that may align more effectively with multi-timeframe mean reversion dynamics.

This subtle adjustment exploits what some traders identify as “temporal drift” — the desynchronization of volatility across timeframes that creates hidden rhythm in price action.

→ For example, Stochastic on 4H (lookback 17) and Bollinger Bands on 1H (lookback 20) may periodically sync around 10H intervals, offering unique alpha windows.

📊 Indicator Components

🔹 Stochastic Oscillator (4H, Length 17)

Detects momentum reversals using %K and %D crossovers

Helps define overbought/oversold zones from a mid-term view

🔹 Bollinger Bands (1H, Length 20, ±2 StdDev)

Measures price volatility using standard deviation around a moving average

Entry occurs near lower band (support), exits near upper band (resistance)

🔹 Multi-Timeframe Logic

Uses request.security() to safely reference 4H and 1H indicators from a 10H chart

Avoids repainting by using closed higher-timeframe candles only

📈 Visualization

A plot selector input allows toggling between:

Stochastic Plot (%K & %D, with overbought/oversold levels)

Bollinger Bands Plot (Upper, Basis, Lower from 1H data)

This helps users visually confirm entry/exit triggers in real time.

🛠 Customization

Fully configurable Stochastic and BB settings

Timeframes are independently adjustable

Strategy settings like position sizing, slippage, and commission are editable

⚠️ Disclaimer

This strategy is intended for educational and informational purposes only.

It does not constitute financial advice or a recommendation to buy or sell any asset.

Market conditions vary, and past performance does not guarantee future results.

Always test any trading strategy in a simulated environment and consult a licensed financial advisor before making real-world investment decisions.

Momentumtrading

Turtles StrategyBorn from the 1980s "Turtle" experiment, this method of trading captures breakouts and places or closes trades with intrabar entries or exits and realized-equity risk controls.

How It Works

The strategy buys/sells on breakouts from recent highs/lows, using ATR for volatility-adjusted stops and sizing. It risks a fixed % (default 1%) of realized equity per trade—initial capital plus closed P&L, ignoring open positions for conservatism. Drawdown protection auto-reduces risk by 20% at 10% drops (up to three times), resetting only on full peak recovery. Single positions only, with 1-tick slippage simulated for realistic fills. Best for trending assets like forex,commodities, crypto, stocks. Backtest for optimal parameters.

Main Operations

The strategy works on any timeframe but it's meant to be used on daily charts.

Entry Signals:

Long: Buy-stop 1 tick above 20-bar high (default "Entry Period") when no position—enters intrabar on breakout.

Short: Sell-stop 1 tick below 20-bar low. OCA cancels opposites.

Size: (Realized equity × adjusted risk %) ÷ (2× ATR stop distance), scaled by point value.

Exit Signals:

Longs: Stop at tighter of (entry - 2× ATR) or (10-bar low - 1 tick trailing, default "Exit Period").

Shorts: Stop at tighter of (entry + 2× ATR) or (10-bar high + 1 tick trailing).

Locks profits in trends, exits fast on fades.

Risk Controls:

Tracks realized equity peak.

10% drawdown: Risk ×0.8; 20%/30%: Further ×0.8 (max 3x).

Full reset above peak—preserves capital in slumps.

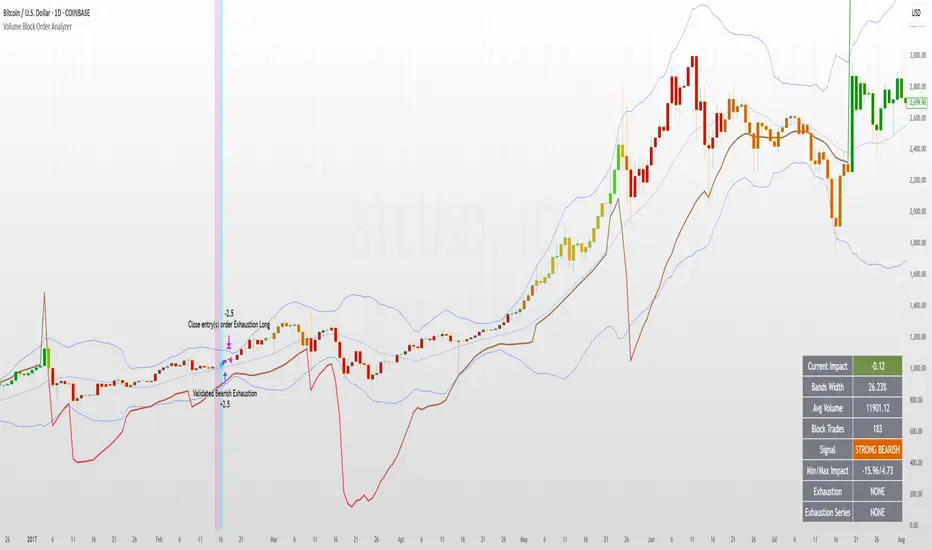

Volume Block Order AnalyzerCore Concept

The Volume Block Order Analyzer is a sophisticated Pine Script strategy designed to detect and analyze institutional money flow through large block trades. It identifies unusually high volume candles and evaluates their directional bias to provide clear visual signals of potential market movements.

How It Works: The Mathematical Model

1. Volume Anomaly Detection

The strategy first identifies "block trades" using a statistical approach:

```

avgVolume = ta.sma(volume, lookbackPeriod)

isHighVolume = volume > avgVolume * volumeThreshold

```

This means a candle must have volume exceeding the recent average by a user-defined multiplier (default 2.0x) to be considered a significant block trade.

2. Directional Impact Calculation

For each block trade identified, its price action determines direction:

- Bullish candle (close > open): Positive impact

- Bearish candle (close < open): Negative impact

The magnitude of impact is proportional to the volume size:

```

volumeWeight = volume / avgVolume // How many times larger than average

blockImpact = (isBullish ? 1.0 : -1.0) * (volumeWeight / 10)

```

This creates a normalized impact score typically ranging from -1.0 to 1.0, scaled by dividing by 10 to prevent excessive values.

3. Cumulative Impact with Time Decay

The key innovation is the cumulative impact calculation with decay:

```

cumulativeImpact := cumulativeImpact * impactDecay + blockImpact

```

This mathematical model has important properties:

- Recent block trades have stronger influence than older ones

- Impact gradually "fades" at rate determined by decay factor (default 0.95)

- Sustained directional pressure accumulates over time

- Opposing pressure gradually counteracts previous momentum

Trading Logic

Signal Generation

The strategy generates trading signals based on momentum shifts in institutional order flow:

1. Long Entry Signal: When cumulative impact crosses from negative to positive

```

if ta.crossover(cumulativeImpact, 0)

strategy.entry("Long", strategy.long)

```

*Logic: Institutional buying pressure has overcome selling pressure, indicating potential upward movement*

2. Short Entry Signal: When cumulative impact crosses from positive to negative

```

if ta.crossunder(cumulativeImpact, 0)

strategy.entry("Short", strategy.short)

```

*Logic: Institutional selling pressure has overcome buying pressure, indicating potential downward movement*

3. Exit Logic: Positions are closed when the cumulative impact moves against the position

```

if cumulativeImpact < 0

strategy.close("Long")

```

*Logic: The original signal is no longer valid as institutional flow has reversed*

Visual Interpretation System

The strategy employs multiple visualization techniques:

1. Color Gradient Bar System:

- Deep green: Strong buying pressure (impact > 0.5)

- Light green: Moderate buying pressure (0.1 < impact ≤ 0.5)

- Yellow-green: Mild buying pressure (0 < impact ≤ 0.1)

- Yellow: Neutral (impact = 0)

- Yellow-orange: Mild selling pressure (-0.1 < impact ≤ 0)

- Orange: Moderate selling pressure (-0.5 < impact ≤ -0.1)

- Red: Strong selling pressure (impact ≤ -0.5)

2. Dynamic Impact Line:

- Plots the cumulative impact as a line

- Line color shifts with impact value

- Line movement shows momentum and trend strength

3. Block Trade Labels:

- Marks significant block trades directly on the chart

- Shows direction and volume amount

- Helps identify key moments of institutional activity

4. Information Dashboard:

- Current impact value and signal direction

- Average volume benchmark

- Count of significant block trades

- Min/Max impact range

Benefits and Use Cases

This strategy provides several advantages:

1. Institutional Flow Detection: Identifies where large players are positioning themselves

2. Early Trend Identification: Often detects institutional accumulation/distribution before major price movements

3. Market Context Enhancement: Provides deeper insight than simple price action alone

4. Objective Decision Framework: Quantifies what might otherwise be subjective observations

5. Adaptive to Market Conditions: Works across different timeframes and instruments by using relative volume rather than absolute thresholds

Customization Options

The strategy allows users to fine-tune its behavior:

- Volume Threshold: How unusual a volume spike must be to qualify

- Lookback Period: How far back to measure average volume

- Impact Decay Factor: How quickly older trades lose influence

- Visual Settings: Labels and line width customization

This sophisticated yet intuitive strategy provides traders with a window into institutional activity, helping identify potential trend changes before they become obvious in price action alone.

Bitcoin Momentum StrategyThis is a very simple long-only strategy I've used since December 2022 to manage my Bitcoin position.

I'm sharing it as an open-source script for other traders to learn from the code and adapt it to their liking if they find the system concept interesting.

General Overview

Always do your own research and backtesting - this script is not intended to be traded blindly (no script should be) and I've done limited testing on other markets beyond Ethereum and BTC, it's just a template to tweak and play with and make into one's own.

The results shown in the strategy tester are from Bitcoin's inception so as to get a large sample size of trades, and potential returns have diminished significantly as BTC has grown to become a mega cap asset, but the script includes a date filter for backtesting and it has still performed solidly in recent years (speaking from personal experience using it myself - DYOR with the date filter).

The main advantage of this system in my opinion is in limiting the max drawdown significantly versus buy & hodl. Theoretically much better returns can be made by just holding, but that's also a good way to lose 70%+ of your capital in the inevitable bear markets (also speaking from experience).

In saying all of that, the future is fundamentally unknowable and past results in no way guarantee future performance.

System Concept:

Capture as much Bitcoin upside volatility as possible while side-stepping downside volatility as quickly as possible.

The system uses a simple but clever momentum-style trailing stop technique I learned from one of my trading mentors who uses this approach on momentum/trend-following stock market systems.

Basically, the system "ratchets" up the stop-loss to be much tighter during high bearish volatility to protect open profits from downside moves, but loosens the stop loss during sustained bullish momentum to let the position ride.

It is invested most of the time, unless BTC is trading below its 20-week EMA in which case it stays in cash/USDT to avoid holding through bear markets. It only trades one position (no pyramiding) and does not trade short, but can easily be tweaked to do whatever you like if you know what you're doing in Pine.

Default parameters:

HTF: Weekly Chart

EMA: 20-Period

ATR: 5-period

Bar Lookback: 7

Entry Rule #1:

Bitcoin's current price must be trading above its higher-timeframe EMA (Weekly 20 EMA).

Entry Rule #2:

Bitcoin must not be in 'caution' condition (no large bearish volatility swings recently).

Enter at next bar's open if conditions are met and we are not already involved in a trade.

"Caution" Condition:

Defined as true if BTC's recent 7-bar swing high minus current bar's low is > 1.5x ATR, or Daily close < Daily 20-EMA.

Trailing Stop:

Stop is trailed 1 ATR from recent swing high, or 20% of ATR if in caution condition (ie. 0.2 ATR).

Exit on next bar open upon a close below stop loss.

I typically use a limit order to open & exit trades as close to the open price as possible to reduce slippage, but the strategy script uses market orders.

I've never had any issues getting filled on limit orders close to the market price with BTC on the Daily timeframe, but if the exchange has relatively low slippage I've found market orders work fine too without much impact on the results particularly since BTC has consistently remained above $20k and highly liquid.

Cost of Trading:

The script uses no leverage and a default total round-trip commission of 0.3% which is what I pay on my exchange based on their tier structure, but this can vary widely from exchange to exchange and higher commission fees will have a significantly negative impact on realized gains so make sure to always input the correct theoretical commission cost when backtesting any script.

Static slippage is difficult to estimate in the strategy tester given the wide range of prices & liquidity BTC has experienced over the years and it largely depends on position size, I set it to 150 points per buy or sell as BTC is currently very liquid on the exchange I trade and I use limit orders where possible to enter/exit positions as close as possible to the market's open price as it significantly limits my slippage.

But again, this can vary a lot from exchange to exchange (for better or worse) and if BTC volatility is high at the time of execution this can have a negative impact on slippage and therefore real performance, so make sure to adjust it according to your exchange's tendencies.

Tax considerations should also be made based on short-term trade frequency if crypto profits are treated as a CGT event in your region.

Summary:

A simple, but effective and fairly robust system that achieves the goals I set for it.

From my preliminary testing it appears it may also work on altcoins but it might need a bit of tweaking/loosening with the trailing stop distance as the default parameters are designed to work with Bitcoin which obviously behaves very differently to smaller cap assets.

Good luck out there!