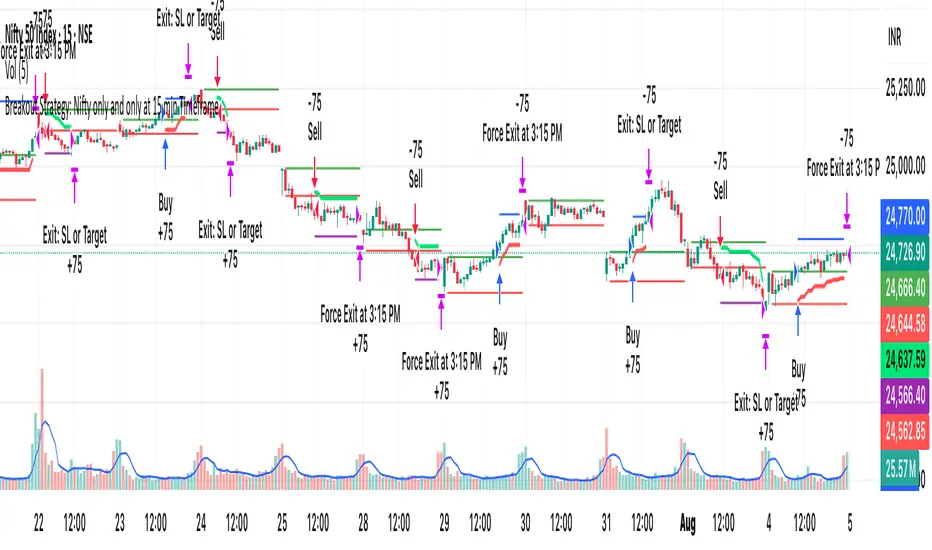

[PS]Breakout Strategy: Nifty/BN only at 15 min TimeframeIt only works on 15 min timeframe for nifty and Bank nifty.

Options

VIX Sentiment Table – ResolutionThis indicator provides verbal representation of the current VIX value and likely market trend for easy to view and interpret

Max Profit Min Loss Options Strategyoption when to buy and sell calls and puts indicator. it uses the rsi macd and volume indicators. it has high profit and low loses

NY/LDN/TOK Stock Exchange Opening HoursThis indicator displays vertical dotted lines marking the exact opening times of the three major global stock exchanges: New York (NYSE), London (LSE), and Tokyo (TSE). Perfect for traders who need to track market opening sessions across different time zones.

Features:

New York Stock Exchange (NYSE): 9:30 AM EST/EDT

London Stock Exchange (LSE): 8:00 AM GMT/BST

Tokyo Stock Exchange (TSE): 9:00 AM JST

Key Highlights:

✓ Automatic daylight saving time adjustments for NY and London

✓ Individual color customization for each market

✓ Toggle on/off functionality for each exchange

✓ Clean vertical dotted lines (1-pixel width) that extend across the entire chart

✓ Interactive legend in bottom-right corner showing active markets

✓ Weekdays only (Monday-Friday) - no weekend lines

✓ Uses official local time zones for accurate timing

Customizable Settings:

Enable/disable individual exchanges

Custom color selection for each market line

Dynamic legend that shows only enabled markets

Time Zone Handling:

The indicator automatically handles daylight saving time transitions using official time zones:

America/New_York (EST/EDT)

Europe/London (GMT/BST)

Asia/Tokyo (JST - no DST)

Perfect for:

Multi-market traders

Session overlap analysis

Global market timing coordination

Institutional trading schedules

Simply add to your chart and customize colors/visibility in the indicator settings. The legend will automatically update to show your active markets in their respective colors.

🟡🔵🟢🔴Beginner's Assistant by carljchapman🟡🔵🟢🔴

Overview

This indicator dynamically marks highs and lows of the premarket (4:00am-9:30amEST) and opening range. It displays Fair Value Gaps, 9 and 21 period Exponential Moving Averages (EMA) and the Volume Weighted Average Price (VWAP). To really help beginners, it marks suggested entry points on the chart with green or red triangles, when a reasonable trend appears.

Features

Automatically draws blue lines for Premarket High and Low values

Dynamically marks the opening Range region

Visual entry signals for long and short opportunities

Primarily used for stocks/funds , but works with forex and crypto

Quick configuration settings to tailor details for your experience level

Mobile friendly mode

Supports alerts

How To Use

Open your chart, and select a 1 or 2 minute timeframe.

Watch for green triangles and red triangles, hinting at entries for long or short positions. Pay particular attention to the price action as it approaches the bounds of the opening range and the premarket levels. I suggest also using a MACD indicator for confirmation of the trend.

For scalping 0dte Options, switch frequently between the 1 ,2 and 5 minute or higher timeframes. Do this so you will not miss an entry opportunity or be unaware of the overall trend.

As a beginner, until you have refined your strategy and develop risk management, take profits as low as 10%. A small profit can quickly become a much larger loss. With 0dte options, time will devour your profits even when the price doesn’t budge.

What makes this indicator so beginner friendly?

Charts with too many lines and colors are are a nightmare for beginners! And empty charts do not tell the whole story. Simple checkboxes in the configuration settings let you turn on and off features to match your comfort level. As you become more familiar you might try turning off the suggested entries to see if you would have selected the same or better ones yourself. Just one example of how you will learn and verify your knowledge. You will quickly spot Opening Range Breakouts and more.

Why are the triangle pointers not simply above or below the bars?

As a beginner, I like to review charts to see how much the price changed, then estimate how much a contract would move based on its delta. A mouthful, I know. But what price does an arrow pointing up below a bar reflect? Would I have entered at the open or close, low or high? This indicator helps by putting the marker close to the price when indicated. It can even display the actual price on the bar. This is helpful for you to make fast calculations without a measuring tool.

I am an experienced trader. Can this help me make winning trades?

Sure. It can also help you make losing ones! Profit is not guaranteed with any indicator or strategy. This indicator is designed to assist you as you learn and while you trade. You won't see the words BUY or SELL. This is not a signal bot! It is merely a tool to assist you. You can learn a lot by spending time observing price movement using this indicator without ever making a single trade.

🟡🔵🟢🔴

Position Size Calculator with Fees# Position Size Calculator with Portfolio Management - Manual

## Overview

The Position Size Calculator with Portfolio Management is an advanced Pine Script indicator designed to help traders calculate optimal position sizes based on their total portfolio value and risk management strategy. This tool automatically calculates your risk amount based on portfolio allocation percentages and determines the exact position size needed while accounting for trading fees.

## Key Features

- **Portfolio-Based Risk Management**: Calculates risk based on total portfolio value

- **Tiered Risk Allocation**: Separates trading allocation from total portfolio

- **Automatic Trade Direction Detection**: Determines long/short based on entry vs stop loss

- **Fee Integration**: Accounts for trading fees in position size calculations

- **Risk Factor Adjustment**: Allows scaling of position size up or down

- **Visual Display**: Shows all calculations in a clear, color-coded table

- **Automatic Risk Calculation**: No need to manually input risk amount

## Input Parameters

### Total Portfolio ($)

- **Purpose**: The total value of your investment portfolio

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

- **Example**: If your total portfolio is worth $100,000, enter 100000

### Trading Portfolio Allocation (%)

- **Purpose**: The percentage of your total portfolio allocated to active trading

- **Default**: 20.0%

- **Range**: 0.0% to 100.0%

- **Step**: 0.01

- **Example**: If you allocate 20% of your portfolio to trading, enter 20

### Risk from Trading (%)

- **Purpose**: The percentage of your trading allocation you're willing to risk per trade

- **Default**: 0.1%

- **Range**: Any positive value

- **Step**: 0.01

- **Example**: If you risk 0.1% of your trading allocation per trade, enter 0.1

### Entry Price ($)

- **Purpose**: The price at which you plan to enter the trade

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Stop Loss ($)

- **Purpose**: The price at which you will exit if the trade goes against you

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Risk Factor

- **Purpose**: A multiplier to scale your position size up or down

- **Default**: 1.0 (no scaling)

- **Range**: 0.0 to 10.0

- **Step**: 0.1

- **Examples**:

- 1.0 = Normal position size

- 2.0 = Double the position size

- 0.5 = Half the position size

### Fee (%)

- **Purpose**: The percentage fee charged per transaction

- **Default**: 0.01% (0.01)

- **Range**: 0.0% to 1.0%

- **Step**: 0.001

## How Risk Amount is Calculated

The script automatically calculates your risk amount using this formula:

```

Risk Amount = Total Portfolio × Trading Allocation (%) × Risk % ÷ 10,000

```

### Example Calculation:

- Total Portfolio: $100,000

- Trading Allocation: 20%

- Risk per Trade: 0.1%

**Risk Amount = $100,000 × 20 × 0.1 ÷ 10,000 = $20**

This means you would risk $20 per trade, which is 0.1% of your $20,000 trading allocation.

## Portfolio Structure Example

Let's say you have a $100,000 portfolio:

### Allocation Structure:

- **Total Portfolio**: $100,000

- **Trading Allocation (20%)**: $20,000

- **Long-term Investments (80%)**: $80,000

### Risk Management:

- **Risk per Trade (0.1% of trading)**: $20

- **Maximum trades at risk**: Could theoretically have 1,000 trades before risking entire trading allocation

## How Position Size is Calculated

### Trade Direction Detection

- **Long Trade**: Entry price > Stop loss price

- **Short Trade**: Entry price < Stop loss price

### Position Size Formulas

#### For Long Trades:

```

Position Size = -Risk Factor × Risk Amount / (Stop Loss × (1 - Fee) - Entry Price × (1 + Fee))

```

#### For Short Trades:

```

Position Size = -Risk Factor × Risk Amount / (Entry Price × (1 - Fee) - Stop Loss × (1 + Fee))

```

## Output Display

The indicator displays a comprehensive table with color-coded sections:

### Portfolio Information (Light Blue Background)

- **Portfolio (USD)**: Your total portfolio value

- **Trading Portfolio Allocation (%)**: Percentage allocated to trading

- **Risk as % of Trading**: Risk percentage per trade

### Trade Setup (Gray Background)

- **Entry Price**: Your specified entry price

- **Stop Loss**: Your specified stop loss price

- **Fee (%)**: Trading fee percentage

- **Risk Factor**: Position size multiplier

### Risk Analysis (Red Background)

- **Risk Amount**: Automatically calculated dollar risk

- **Effective Entry**: Actual entry cost including fees

- **Effective Exit**: Actual exit value including fees

- **Expected Loss**: Calculated loss if stop loss is hit

- **Deviation from Risk %**: Accuracy of risk calculation

### Final Result (Blue Background)

- **Position Size**: Number of shares/units to trade

## Usage Examples

### Example 1: Conservative Long Trade

- **Total Portfolio**: $50,000

- **Trading Allocation**: 15%

- **Risk per Trade**: 0.05%

- **Entry Price**: $25.00

- **Stop Loss**: $24.00

- **Risk Factor**: 1.0

- **Fee**: 0.01%

**Calculated Risk Amount**: $50,000 × 15% × 0.05% ÷ 100 = $3.75

### Example 2: Aggressive Short Trade

- **Total Portfolio**: $200,000

- **Trading Allocation**: 30%

- **Risk per Trade**: 0.2%

- **Entry Price**: $150.00

- **Stop Loss**: $155.00

- **Risk Factor**: 2.0

- **Fee**: 0.01%

**Calculated Risk Amount**: $200,000 × 30% × 0.2% ÷ 100 = $120

**Actual Risk**: $120 × 2.0 = $240 (due to risk factor)

## Color Coding System

- **Green/Red Header**: Trade direction (Long/Short)

- **Light Blue**: Portfolio management parameters

- **Gray**: Trade setup parameters

- **Red**: Risk-related calculations and results

- **Blue**: Final position size result

## Best Practices

### Portfolio Management

1. **Keep trading allocation reasonable** (typically 10-30% of total portfolio)

2. **Use conservative risk percentages** (0.05-0.2% per trade)

3. **Don't risk more than you can afford to lose**

### Risk Management

1. **Start with small risk factors** (1.0 or less) until comfortable

2. **Monitor your total exposure** across all open positions

3. **Adjust risk based on market conditions**

### Trade Execution

1. **Always validate calculations** before placing trades

2. **Account for slippage** in volatile markets

3. **Consider position size relative to liquidity**

## Risk Management Guidelines

### Conservative Approach

- Trading Allocation: 10-20%

- Risk per Trade: 0.05-0.1%

- Risk Factor: 0.5-1.0

### Moderate Approach

- Trading Allocation: 20-30%

- Risk per Trade: 0.1-0.15%

- Risk Factor: 1.0-1.5

### Aggressive Approach

- Trading Allocation: 30-40%

- Risk per Trade: 0.15-0.25%

- Risk Factor: 1.5-2.0

## Troubleshooting

### Common Issues

1. **Position Size shows 0**

- Verify all portfolio inputs are greater than 0

- Check that entry price differs from stop loss

- Ensure calculated risk amount is positive

2. **Very small position sizes**

- Increase risk percentage or risk factor

- Check if your risk amount is too small for the price difference

3. **Large risk deviation**

- Normal for very small positions

- Consider adjusting entry/stop loss levels

### Validation Checklist

- Total portfolio value is realistic

- Trading allocation percentage makes sense

- Risk percentage is conservative

- Entry and stop loss prices are valid

- Trade direction matches your intention

## Advanced Features

### Risk Factor Usage

- **Scaling up**: Use risk factors > 1.0 for high-confidence trades

- **Scaling down**: Use risk factors < 1.0 for uncertain trades

- **Never exceed**: Risk factors that would risk more than your comfort level

### Multiple Timeframe Analysis

- Use different risk factors for different timeframes

- Consider correlation between positions

- Adjust trading allocation based on market conditions

## Disclaimer

This tool is for educational and planning purposes only. Always verify calculations manually and consider market conditions, liquidity, and correlation between positions. The automated risk calculation assumes you're comfortable with the mathematical relationship between portfolio allocation and individual trade risk. Past performance doesn't guarantee future results, and all trading involves risk of loss.

MA Crossover Strategy with TP/SL (5 EMA Filter)How the Strategy Works on a 5-Minute Chart:

Data Input (5-Minute Candles):

Every single data point (candle) on your chart will represent 5 minutes of price action (Open, High, Low, Close for that 5-minute period).

All calculations (MAs, EMA, signals) will be based on these 5-minute price data points.

Moving Average Calculations:

Fast MA (10-period SMA): This will be the Simple Moving Average of the closing prices of the last 10 five-minute candles. It reacts relatively quickly to recent price changes.

Slow MA (30-period SMA): This will be the Simple Moving Average of the closing prices of the last 30 five-minute candles. It represents a slightly longer-term trend compared to the Fast MA.

5 EMA (5-period EMA): This is the Exponential Moving Average of the closing prices of the last 5 five-minute candles. Being an EMA, it gives more weight to the most recent 5-minute prices, making it very responsive to immediate price action.

Signal Generation (Entry Conditions):

Long Entry Signal:

The 10-period SMA crosses above the 30-period SMA (indicating a potential bullish shift in the short-to-medium term trend).

AND the current 5-minute candle's closing price is above the 5-period EMA (confirming that the immediate price momentum is also bullish and supporting the crossover).

If both conditions are met at the close of a 5-minute candle, a "Buy" signal is generated.

Short Entry Signal:

The 10-period SMA crosses below the 30-period SMA (indicating a potential bearish shift).

AND the current 5-minute candle's closing price is below the 5-period EMA (confirming immediate bearish momentum).

If both conditions are met at the close of a 5-minute candle, a "Sell" signal is generated.

Trade Execution:

When a signal is triggered, the strategy enters a trade (long or short) at the closing price of that 5-minute candle.

Immediately upon entry, it places two contingent orders:

Take Profit (Target): Set at 2% (by default) away from your entry price. For a long trade, it's 2% above; for a short trade, 2% below.

Stop Loss: Set at 1% (by default) away from your entry price. For a long trade, it's 1% below; for a short trade, 1% above.

The trade will remain open until either the Take Profit or Stop Loss price is hit by subsequent 5-minute candles.

Implications for Trading on a 5-Minute Chart:

Increased Trade Frequency: You will likely see many more signals and trades compared to higher timeframes (like 1-hour or daily charts). This means more potential opportunities but also more transaction costs (commissions, slippage).

Sensitivity to Noise: Lower timeframes are more prone to "market noise" – small, random price fluctuations that don't indicate a true trend. While the 5 EMA filter helps, some false signals might still occur.

Faster Price Action: Price movements can be very rapid on a 5-minute chart. Your take profit or stop loss levels might be hit very quickly, sometimes within the same or next few candles.

Parameter Optimization is Crucial: The default MA lengths (10, 30) and EMA (5) might not be optimal for every asset or market condition on a 5-minute chart. You'll need to backtest extensively and potentially adjust these lengths, as well as the targetPerc and stopPerc, to find what works best for the specific instrument you're trading.

Risk Management: The fixed percentage stop loss is vital on a 5-minute chart due to its volatility. Without it, a few unfavorable moves could lead to significant losses.

Easy Position Size Calculator with Fees# Easy Position Size Calculator with Fees - Manual

## Overview

The Easy Position Size Calculator is a Pine Script indicator designed to help traders calculate the optimal position size for their trades while accounting for trading fees. This tool automatically determines whether you're planning a long or short position and calculates the exact position size needed to risk a specific dollar amount.

## Key Features

- **Automatic Trade Direction Detection**: Determines if you're going long or short based on entry price vs stop loss

- **Fee Integration**: Accounts for trading fees in position size calculations

- **Risk Management**: Calculates position size based on your specified risk amount

- **Risk Factor Adjustment**: Allows you to scale your position size up or down

- **Visual Display**: Shows all calculations in a clear, organized table

## Input Parameters

### Entry Price ($)

- **Purpose**: The price at which you plan to enter the trade

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Stop Loss ($)

- **Purpose**: The price at which you will exit the trade if it goes against you

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Risk ($)

- **Purpose**: The maximum dollar amount you're willing to lose on this trade

- **Default**: 0.0

- **Range**: Any positive value

- **Step**: 0.01

### Risk Factor

- **Purpose**: A multiplier to scale your position size up or down

- **Default**: 1.0 (no scaling)

- **Range**: 0.0 to 10.0

- **Step**: 0.1

- **Examples**:

- 1.0 = Normal position size

- 2.0 = Double the position size

- 0.5 = Half the position size

### Fee (%)

- **Purpose**: The percentage fee charged per transaction (buy/sell)

- **Default**: 0.01% (0.01)

- **Range**: 0.0% to 1.0%

- **Step**: 0.001

## How It Works

### Trade Direction Detection

The script automatically determines your trade direction:

- **Long Trade**: Entry price > Stop loss price

- **Short Trade**: Entry price < Stop loss price

### Position Size Calculation

#### For Long Trades:

```

Position Size = -Risk Factor × Risk Amount / (Stop Loss × (1 - Fee) - Entry Price × (1 + Fee))

```

#### For Short Trades:

```

Position Size = -Risk Factor × Risk Amount / (Entry Price × (1 - Fee) - Stop Loss × (1 + Fee))

```

### Fee Adjustment

The script accounts for fees on both entry and exit:

- **Long trades**: You pay fees when buying (entry) and selling (exit)

- **Short trades**: You pay fees when shorting (entry) and covering (exit)

## Output Display

The indicator displays a table with the following information:

### Trade Information

- **Trade Type**: Shows whether it's a LONG, SHORT, or INVALID trade

- **Entry Price**: Your specified entry price

- **Stop Loss**: Your specified stop loss price

- **Fee (%)**: The fee percentage being used

### Risk Parameters

- **Risk Amount**: The dollar amount you're willing to risk

- **Risk Factor**: The multiplier being applied

### Calculated Values

- **Effective Entry**: The actual cost per share including fees

- **Effective Exit**: The actual exit value per share including fees

- **Expected Loss**: The calculated loss if stop loss is hit

- **Deviation from Risk %**: Shows how close the expected loss is to your target risk

- **Position Size**: The number of shares/units to trade

## Usage Examples

### Example 1: Long Trade

- Entry Price: $100.00

- Stop Loss: $95.00

- Risk Amount: $500.00

- Risk Factor: 1.0

- Fee: 0.01%

**Result**: The script will calculate how many shares to buy so that if the stop loss is hit, you lose approximately $500 (accounting for fees). Position Size: 99.61152

### Example 2: Short Trade

- Entry Price: $50.00

- Stop Loss: $55.00

- Risk Amount: $300.00

- Risk Factor: 1.0

- Fee: 0.01%

**Result**: The script will calculate how many shares to short so that if the stop loss is hit, you lose approximately $300 (accounting for fees). Position Size: 59.87426

## Important Notes

### Validation Requirements

For the script to work properly, all of the following must be true:

- Entry price > 0

- Stop loss > 0

- Risk amount > 0

- Entry price ≠ Stop loss (to determine direction)

### Negative Position Sizes

The script may show negative position sizes, which is normal:

- **Negative values for long trades**: Represents shares to buy

- **Negative values for short trades**: Represents shares to short

### Risk Deviation

The "Deviation from Risk %" shows how closely the calculated position size matches your target risk. Small deviations are normal due to:

- Fee calculations

- Rounding

- Market precision

## Color Coding

The table uses color coding for easy identification:

- **Green**: Long trade information

- **Red**: Short trade information

- **Gray**: Invalid trade (when inputs are incorrect)

- **Blue**: Final position size

- **Red background**: Risk-related calculations

## Troubleshooting

### Common Issues

1. **Position Size shows 0**

- Check that all inputs are greater than 0

- Ensure entry price is different from stop loss

2. **Trade Type shows INVALID**

- Verify that entry price and stop loss are both positive

- Make sure entry price ≠ stop loss

3. **Large Risk Deviation**

- This is normal for very small position sizes

- Consider adjusting your risk amount or price levels

## Best Practices

1. **Always validate your inputs** before placing actual trades

2. **Double-check the trade direction** shown in the table

3. **Review the expected loss** to ensure it aligns with your risk management

4. **Consider the effective entry/exit prices** which include fees

5. **Use appropriate risk factors** - avoid extreme values that could lead to overexposure

## Disclaimer

This tool is for educational and planning purposes only. Always verify calculations manually and consider market conditions, liquidity, and other factors before placing actual trades. The script assumes that fees are charged on both entry and exit transactions.

Option Maxpain & WallsThis simple script plots three lines on your chart based on options data: Call Wall, Put Wall and Max Pain. These three numbers must be obtained elsewhere. While Tradingview has delayed options data, to my knowledge Pinescript does not allow looping through this data to calculate the numbers within the script. So the user must obtain or calculate them elsewhere then type them into the input dialog. Labels and alerts are included as user options.

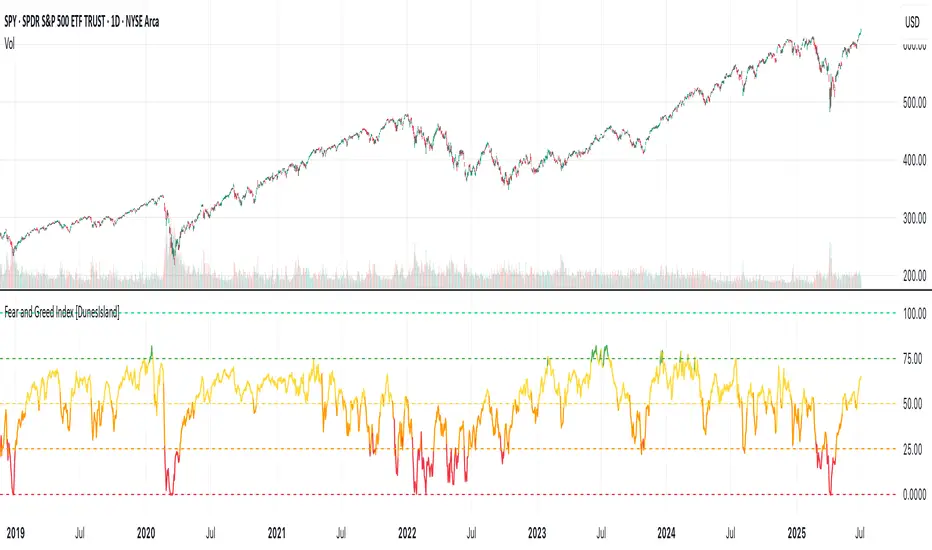

Fear and Greed Index [DunesIsland]The Fear and Greed Index is a sentiment indicator designed to measure the emotions driving the stock market, specifically investor fear and greed. Fear represents pessimism and caution, while greed reflects optimism and risk-taking. This indicator aggregates multiple market metrics to provide a comprehensive view of market sentiment, helping traders and investors gauge whether the market is overly fearful or excessively greedy.How It WorksThe Fear and Greed Index is calculated using four key market indicators, each capturing a different aspect of market sentiment:

Market Momentum (30% weight)

Measures how the S&P 500 (SPX) is performing relative to its 125-day simple moving average (SMA).

A higher value indicates that the market is trading well above its moving average, signaling greed.

Stock Price Strength (20% weight)

Calculates the net number of stocks hitting 52-week highs minus those hitting 52-week lows on the NYSE.

A greater number of net highs suggests strong market breadth and greed.

Put/Call Options (30% weight)

Uses the 5-day average of the put/call ratio.

A lower ratio (more call options being bought) indicates greed, as investors are betting on rising prices.

Market Volatility (20% weight)

Utilizes the VIX index, which measures market volatility.

Lower volatility is associated with greed, as investors are less fearful of large market swings.

Each component is normalized using a z-score over a 252-day lookback period (approximately one trading year) and scaled to a range of 0 to 100. The final Fear and Greed Index is a weighted average of these four components, with the weights specified above.Key FeaturesIndex Range: The index value ranges from 0 to 100:

0–25: Extreme Fear (red)

25–50: Fear (orange)

50–75: Neutral (yellow)

75–100: Greed (green)

Dynamic Plot Color: The plot line changes color based on the index value, visually indicating the current sentiment zone.

Reference Lines: Horizontal lines are plotted at 0, 25, 50, 75, and 100 to represent the different sentiment levels: Extreme Fear, Fear, Neutral, Greed, and Extreme Greed.

How to Interpret

Low Values (0–25): Indicate extreme fear, which may suggest that the market is oversold and could be due for a rebound.

High Values (75–100): Indicate greed, which may signal that the market is overbought and could be at risk of a correction.

Neutral Range (25–75): Suggests a balanced market sentiment, neither overly fearful nor greedy.

This indicator is a valuable tool for contrarian investors, as extreme readings often precede market reversals. However, it should be used in conjunction with other technical and fundamental analysis tools for a well-rounded view of the market.

F&O Time Zones – Final Fixed📌 This indicator highlights high-probability intraday time zones used in Indian F&O (Futures & Options) strategies. Ideal for scalping, breakout setups, and trap avoidance.

🕒 Covered Time Zones:

• 9:15 – 9:21 AM → Flash Trades (first 1-minute volatility)

• 9:21 – 9:30 AM → Smart Money Trap (VWAP fakeouts)

• 9:30 – 9:50 AM → Fake Breakout Zone

• 9:50 – 10:15 AM → Institutional Entry Timing

• 10:15 – 10:45 AM → VWAP Range Scalps

• 10:45 – 11:15 AM → Second Trap Zone

• 11:15 – 1:00 PM → Trend Continuation Window

• 1:00 – 1:45 PM → Volatility Compression

• 1:45 – 2:15 PM → Institutional Exit Phase 1

• 2:15 – 2:45 PM → Trend Acceleration / Reversals

• 2:45 – 3:15 PM → Expiry Scalping Zone

• 3:15 – 3:30 PM → Dead Zone (square-off time)

🔧 Features:

✓ Clean vertical lines per zone

✓ Optional label positions (top or bottom)

✓ Adjustable line style, width, and color

🧠 Best used on: NIFTY, BANKNIFTY, FINNIFTY (5-min or lower)

---

🔒 **Disclaimer**:

This script is for **educational purposes only**. It is not financial advice. Trading involves risk. Please consult a professional or do your own research before taking any positions.

—

👤 Script by: **JoanJagan**

🛠️ Built in Pine Script v5

Options Strategy V1.3📈 Options Strategy V1.3 — EMA Crossover + RSI + ATR + Opening Range

Overview:

This strategy is designed for short-term directional trades on large-cap stocks or ETFs, especially when trading options. It combines classic trend-following signals with momentum confirmation, volatility-based risk management, and session timing filters to help identify high-probability entries with predefined stop-loss and profit targets.

🔍 Strategy Components:

EMA Crossover (Fast/Slow)

Entry signals are triggered by the crossover of a short EMA above or below a long EMA — a traditional trend-following method to detect shifts in momentum.

RSI Filter

RSI confirms the signal by avoiding entries in overbought/oversold zones unless certain momentum conditions are met.

Long entry requires RSI ≥ Long Threshold

Short entry requires RSI ≤ Short Threshold

ATR-Based SL & TP

Stop-loss is set dynamically as a multiple of ATR below (long) or above (short) the entry price.

Take-profit is placed as a ratio (TP/SL) of the stop distance, ensuring consistent reward/risk structure.

Opening Range Filter (Optional)

If enabled, the strategy only triggers trades after price breaks out of the 09:30–09:45 EST range, ensuring participation in directional moves.

Session Filters

No trades from 04:00 to 09:30 and from 16:00 to 20:00 EST, avoiding low-liquidity periods.

All open trades are closed at 15:55 EST, to avoid overnight risk or expiration issues for options.

⚙️ Built-in Presets:

You can choose one of the built-in ticker-specific presets for optimal conditions:

Ticker EMAs RSI (Long/Short) ATR SL×ATR TP/SL

SPY 8/28 56 / 26 14 1.4× 4.0×

TSLA 23/27 56 / 33 13 1.4× 3.6×

AAPL 6/13 61 / 26 23 1.4× 2.1×

MSFT 25/32 54 / 26 14 1.2× 2.2×

META 25/32 53 / 26 17 1.8× 2.3×

AMZN 28/32 55 / 25 16 1.8× 2.3×

You can also choose "Custom" to fully configure all parameters to your own market and strategy preferences.

📌 Best Use Case:

This strategy is especially suited for intraday options trading, where timing and risk control are critical. It works best on liquid tickers with strong trends or clear breakout behavior.

Smart Money Trap SignalSmart Money Trap Signal – Indicator Description

The Smart Money Trap Signal is a precision-based trading tool designed to identify areas where institutional traders (smart money) are likely to trap retail traders through false breakouts and liquidity grabs. These traps often occur near key highs and lows, where retail traders are lured into trades just before price reverses sharply.

🔍 Key Features:

Liquidity Sweep Detection

Identifies false breakouts of recent swing highs or lows, signaling potential liquidity grabs by large players.

Reversal Confirmation

Confirms the trap using a classic price action reversal pattern (bullish or bearish engulfing), helping filter out weak signals.

Optional Volume Spike Filter

Allows additional confirmation based on a significant spike in volume, indicating potential institutional involvement.

Buy and Sell Trap Signals

🔴 Smart Money Short (SMT↓) – Triggered when price sweeps a high and reverses down.

🟢 Smart Money Long (SMT↑) – Triggered when price sweeps a low and reverses up.

Alerts & Labels

Real-time alert conditions and on-chart labels to help you catch setups without missing opportunities.

📈 How to Use:

Apply on Higher Timeframes (1H, 4H, Daily) for cleaner signals.

Look for SMT signals at key supply/demand zones or market structure points.

Combine with your existing trading strategy, such as order blocks or break of structure (BoS), for higher accuracy.

Use volume filter only if you're analyzing markets where volume data is reliable.

⚠️ Disclaimer:

This tool is meant to assist with trade identification, not trade execution. Always use proper risk management and validate setups with your trading plan.

Previous 2 Days High/LowCan you give me a summary of this indicator

The "Previous 2 Days High/Low" indicator, written in Pine Script v5 for TradingView, plots horizontal lines representing the combined high and low prices of the previous two trading days on a chart. Here's a summary of its functionality, purpose, and key features:

Purpose

The indicator helps traders identify significant price levels by displaying the highest high and lowest low from the previous two days, which can act as potential support or resistance levels. These levels are plotted as lines that extend across the current trading day, making it easier to visualize key price zones for trading decisions.

Key Features

Calculates Combined High and Low:

Retrieves the high and low prices of the previous day and the day before using request.security on the daily timeframe ("D").

Computes the combined high as the maximum of the two days' highs and the combined low as the minimum of the two days' lows.

Dynamic Line Plotting:

Draws two horizontal lines:

Red Line: Represents the combined high, plotted at the highest price of the previous two days.

Green Line: Represents the combined low, plotted at the lowest price of the previous two days.

Lines are created at the start of a new trading day and extended to the right edge of the chart using line.set_x2, ensuring they span the entire current day.

Labels for Clarity:

Adds labels to the right of the chart, displaying the exact price values of the combined high ("Combined High: ") and combined low ("Combined Low: ").

Labels are updated to move with the lines, maintaining alignment at the current bar.

Clutter Prevention:

Deletes old lines and labels at the start of each new trading day to avoid overlapping or excessive objects on the chart.

Dynamic Requests:

Uses dynamic_requests=true in the indicator() function to allow request.security calls within conditional blocks (if ta.change(time("D"))), enabling daily data retrieval within the script's logic.

Inside Bar Detector - 15min

🔍 What is an Inside Bar?

An **Inside Bar** is a candle that forms **entirely within the high and low of the previous candle**. It represents **consolidation**, **indecision**, or **potential reversal**, and is a key signal in The Strat trading method.

🔧 What the Script Does:

1. **Timeframe Restriction**:

* The script activates **only on the 15-minute timeframe**, avoiding clutter on other timeframes.

2. **Inside Bar Logic**:

* It checks whether the **current bar’s high is lower than the previous bar’s high**, **AND** the **current bar’s low is higher than the previous bar’s low**.

* If both conditions are true, it confirms an Inside Bar.

3. **Visual Display**:

* When an Inside Bar is detected, the script **plots a yellow label ("1") above the bar**.

* The label represents the Strat 1-bar and helps you easily spot potential setups.

🎯 Use Case:

* Ideal for **Strat traders**, **price action analysts**, or **any trader** looking for breakout or reversal opportunities.

* Common setups include **1-2**, **1-3**, or **double inside bar** breakouts.

Sticky Notes📌 Sticky Notes - On-Chart Memo Tool

A convenient indicator that lets you display trading ideas and important notes directly on your charts!

✨ Key Features:

📝 Create memos with custom text input

📍 Place anywhere on chart (top/middle/bottom)

🖥️ Screen-fixed display mode (corner positions)

🎨 Fully customizable text and background colors

📏 5 text size options (tiny to huge)

⏰ Time-based display functionality

📐 Text alignment options (left/center/right)

💡 Use Cases:

Trading strategy reminders

Important price level notes

Economic event schedules

Entry/exit point memos

Simple and user-friendly design to enhance your trading analysis!

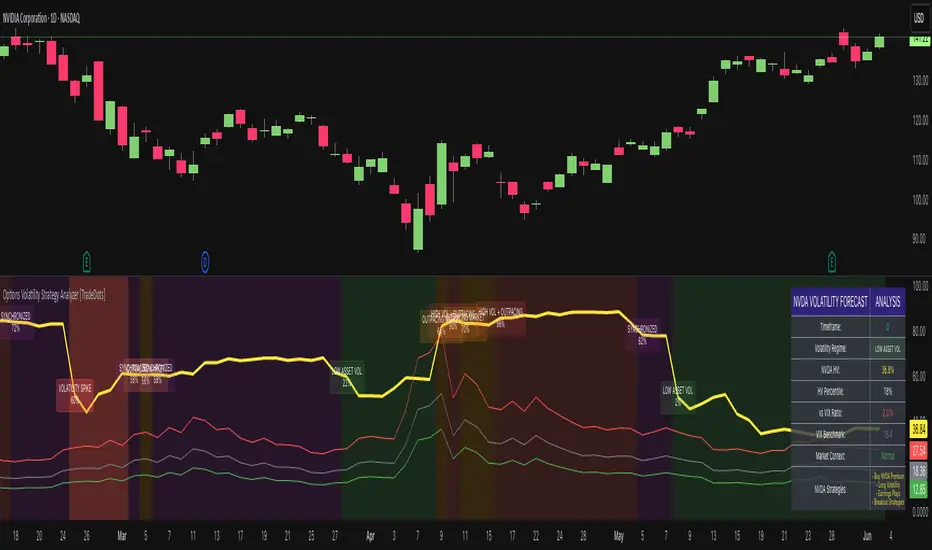

Options Volatility Strategy Analyzer [TradeDots]The Options Volatility Strategy Analyzer is a specialized tool designed to help traders assess market conditions through a detailed examination of historical volatility, market benchmarks, and percentile-based thresholds. By integrating multiple volatility metrics (including VIX and VIX9D) with color-coded regime detection, the script provides users with clear, actionable insights for selecting appropriate options strategies.

📝 HOW IT WORKS

1. Historical Volatility & Percentile Calculations

Annualized Historical Volatility (HV): The script automatically computes the asset’s historical volatility using log returns over a user-defined period. It then annualizes these values based on the chart’s timeframe, helping you understand the asset’s typical volatility profile.

Dynamic Percentile Ranks: To gauge where the current volatility level stands relative to past behavior, historical volatility values are compared against short, medium, and long lookback periods. Tracking these percentile ranks allows you to quickly see if volatility is high or low compared to historical norms.

2. Multi-Market Benchmark Comparison

VIX and VIX9D Integration: The script tracks market volatility through the VIX and VIX9D indices, comparing them to the asset’s historical volatility. This reveals whether the asset’s volatility is outpacing, lagging, or remaining in sync with broader market volatility conditions.

Market Context Analysis: A built-in term-structure check can detect market stress or relative calm by measuring how VIX compares to shorter-dated volatility (VIX9D). This helps you decide if the present environment is risk-prone or relatively stable.

3. Volatility Regime Detection

Color-Coded Background: The analyzer assigns a volatility regime (e.g., “High Asset Vol,” “Low Asset Vol,” “Outpacing Market,” etc.) based on current historical volatility percentile levels and asset vs. market ratios. A color-coded background highlights the regime, enabling traders to quickly interpret the market’s mood.

Alerts on Regime Changes & Spikes: Automated alerts warn you about any significant expansions or contractions in volatility, allowing you to react swiftly in changing conditions.

4. Strategy Forecast Table

Real-Time Strategy Suggestions: At the close of each bar, an on-chart table generates suggested options strategies (e.g., selling premium in high volatility or buying premium in low volatility). These suggestions provide a quick summary of potential tactics suited to the current regime.

Contextual Market Data: The table also displays key statistics, such as VIX levels, asset historical volatility percentile, or ratio comparisons, helping you confirm whether volatility conditions warrant more conservative or more aggressive strategies.

🛠️ HOW TO USE

1. Select Your Timeframe: The script supports multiple timeframes. For short-term trading, intraday charts often reveal faster shifts in volatility. For swing or position trading, daily or weekly charts may be more stable and produce fewer false signals.

2. Check the Volatility Regime: Observe the background color and on-chart labels to identify the current regime (e.g., “HIGH ASSET VOL,” “LOW VOL + LAGGING,” etc.).

3. Review the Forecast Table: The table suggests strategy ideas (e.g., iron condors, long straddles, ratio spreads) depending on whether volatility is elevated, subdued, or spiking. Use these as a starting point for designing trades that match your risk tolerance.

4. Combine with Additional Analysis: For optimal results, confirm signals with your broader trading plan, technical tools (moving averages, price action), and fundamental research. This script is most effective when viewed as one component in a comprehensive decision-making process.

❗️LIMITATIONS

Directional Neutrality: This indicator analyzes volatility environments but does not predict price direction (up/down). Traders must combine with directional analysis for complete strategy selection.

Late or Missed Signals: Since all calculations require a bar to close, sharp intrabar volatility moves may not appear in real-time.

False Positives in Choppy Markets: Rapid changes in percentile ranks or VIX movements can generate conflicting or premature regime shifts.

Data Sensitivity: Accuracy depends on the availability and stability of volatility data. Significant gaps or unusual market conditions may skew results.

Market Correlation Assumptions: The system assumes assets generally correlate with S&P 500 volatility patterns. May be less effective for:

Small-cap stocks with unique volatility drivers

International stocks with different market dynamics

Sector-specific events disconnected from broad market

Cryptocurrency-related assets with independent volatility patterns

RISK DISCLAIMER

Options trading involves substantial risk and is not suitable for all investors. Options strategies can result in significant losses, including the total loss of premium paid. The complexity of options strategies requires thorough understanding of the risks involved.

This indicator provides volatility analysis for educational and informational purposes only and should not be considered as investment advice. Past volatility patterns do not guarantee future performance. Market conditions can change rapidly, and volatility regimes may shift without warning.

No trading system can guarantee profits, and all trading involves the risk of loss. The indicator's regime classifications and strategy suggestions should be used as part of a comprehensive trading plan that includes proper risk management, directional analysis, and consideration of broader market conditions.

NY ORB + Fakeout Detector🗽 NY ORB + Fakeout Detector

This indicator automatically plots the New York Opening Range (ORB) based on the first 15 minutes of the NY session (15:30–15:45 CEST / 13:30–13:45 UTC) and detects potential fakeouts (false breakouts).

🔍 Key Features:

✅ Plots ORB high and low based on the 15-minute NY open range

✅ Automatically detects fake breakouts (price wicks beyond the box but closes back inside)

✅ Visual markers:

🔺 "Fake ↑" if a fake breakout occurs above the range

🔻 "Fake ↓" if a fake breakout occurs below the range

✅ Gray background highlights the ORB session window

✅ Designed for scalping and short-term breakout strategies

🧠 Best For:

Intraday traders looking for NY volatility setups

Scalpers using ORB-based entries

Traders seeking early-session fakeout traps to avoid false signals

Those combining with EMA 12/21, volume, or other confluence tools

HARSI PRO v2 - Advanced Adaptive Heikin-Ashi RSI OscillatorThis script is a fully re-engineered and enhanced version of the original Heikin-Ashi RSI Oscillator created by JayRogers. While it preserves the foundational concept and visual structure of the original indicatorusing Heikin-Ashi-style candles to represent RSI movementit introduces a range of institutional-grade engines and real-time analytics modules.

The core idea behind HARSI is to visualize the internal structure of RSI behavior using candle representations. This gives traders a clearer sense of trend continuity, exhaustion, and momentum inflection. In this upgraded version, the system is extended far beyond basic visualization into a comprehensive diagnostic and context-tracking tool.

Core Enhancements and Features

1. Heikin-Ashi RSI Candles

The base HARSI logic transforms RSI values into open, high, low, and close components, which are plotted as Heikin-Ashi-style candles. The open values are smoothed with a user-controlled bias setting, and the high/low are calculated from zero-centered RSI values.

2. Smoothed RSI Histogram and Plot

A secondary RSI plot and histogram are available for traditional RSI interpretation, optionally smoothed using a custom midpoint EMA process.

3. Dynamic Stochastic RSI Ribbon

The indicator optionally includes a smoothed Stochastic RSI ribbon with directional fill to highlight acceleration and reversal zones.

4. Real-Time Meta-State Engine

This engine determines the current market environmentneutral, breakout, or reversalbased on multiple adaptive conditions including volatility compression, momentum thrust, volume behavior, and composite reversal scoring.

5. Adaptive Overbought/Oversold Zone Engine

Instead of using fixed RSI thresholds, this engine dynamically adjusts OB/OS boundaries based on recent RSI range and normalized price volatility. This makes the OB/OS levels context-sensitive and more accurate across different instruments and regimes.

6. Composite Reversal Score Engine

A real-time score between 0 and 5 is generated using four components:

* OB/OS proximity (zone score)

* RSI slope behavior

* Volume state (burst or exhaustion)

* Trend continuation penalty based on position versus trend bias

This score allows for objective filtering of reversal zones and breakout traps.

7. Kalman Velocity Filter

A Kalman-style adaptive smoothing filter is applied to RSI for calculating velocity and acceleration. This allows for real-time detection of stalls and thrusts in RSI behavior.

8. Predictive Breakout Estimator

Uses ATR compression and RSI thrusting conditions to detect likely breakout environments. This logic contributes to the Meta-State Engine and the Breakout Risk dashboard metric.

9. Volume Acceleration Model

Real-time detection of volume bursts and fades based on VWMA baselines. Volume exhaustion warnings are used to qualify or disqualify reversals and breakouts.

10. Trend Bias and Regime Detection

Uses RSI slope, HARSI body impulse, and normalized ATR to classify the current trend state and directional bias. This forms the basis for filtering false reversals during strong trends.

11. Dashboard with Tooltips

A clean, table displays six key metrics in real time:

* Meta State

* Reversal Score

* Trend Bias

* Volume State

* Volatility Regime

* Breakout Risk

Each cell includes a descriptive tooltip explaining why the value is being shown based on internal state calculations.

How It Works Internally

* The system calculates a zero-centered RSI and builds candle structures using high, low, and smoothed open/close values.

* Volatility normalization is used throughout the script, including ATR-based thresholds and dynamic scaling of OB/OS zones.

* Momentum is filtered through smoothed slope calculations and HARSI body size measurements.

* Volume activity is compared against VWMA using configurable multipliers to detect institutional-level activity or exhaustion.

* Each regime detection module contributes to a centralized metaState classifier that determines whether the environment is conducive to reversal, breakout, or neutral action.

* All major signal and context values are continuously updated in a dashboard table with logic-driven color coding and tooltips.

Based On and Credits

This script is based on the original Heikin-Ashi RSI Oscillator by JayRogers . All visual elements from the original version, including candle plotting and color configurations, have been retained and extended. Significant backend enhancements were added by AresIQ for the 2025 release. The script remains open-source under the original attribution license. Credit to JayRogers is preserved and required for any derivative versions.

Enhanced Daily Sentiment & Auction Area Trading StrategyDetermine Daily Sentiment (Anchor Chart - Daily TF):

Analyze Yesterday's Daily Candle: Look at the previous day's daily candlestick (high, low, open, close). This is the "most important information."

Establish Bias: If yesterday's candle was bullish (closed higher), the bias for today is generally long (approx. 80% of the time). If bearish, the bias is short.

Moving Average Context: Note if the daily price is above or below its short-term moving average (e.g., 21 or 50 MA). This should align with the candle's bias (e.g., bullish daily candle above its MA).

Pre-Market & Opening Analysis (Information Gathering):

Check for Gaps: Observe if the market is gapping up or down in the pre-market session relative to yesterday's close. This provides an early clue to current sentiment.

Consider Overall Sentiment: Briefly factor in relevant news or overarching market sentiment (e.g., data releases, overall market feeling from yields, gold etc.). Trading Window: Focus primarily on trading within the first hour of the U.S. market open, as this is when volatility is typically highest, which the strategy relies on.

Setup 5-Minute Chart for Execution (Trading TF - 5-min):

Apply Moving Average: Use the same short-term moving average (e.g., 21 or 50 MA) as on the daily chart.

Seek Alignment (Crucial): The 5-minute chart's trend and price action relative to its MA must align with the daily chart's bias and MA relationship.

If Daily bias is LONG (price above daily MA), the 5-minute chart should also show price establishing itself above its 5-min MA, ideally with a similar "45-degree angle" uptrend.

If Daily bias is SHORT (price below daily MA), the 5-minute chart should also show price establishing itself below its 5-min MA, with a similar downtrend. If there's no clear alignment between the daily and 5-minute chart structure/MA, do not trade.

Identify the "Auction Area" (Value/Congestion) on the 5-Minute Chart:

This is a recent area of congestion, a small support/resistance flip, or where price has paused, consolidated, and is retesting, often near the 5-minute MA.

Uptrend (Long Bias): Look for a pullback (a small "V" shape dip) towards the 5-minute MA or a recent small resistance-turned-support area. This is the "auction retest" before a potential breakout higher.

Downtrend (Short Bias): Look for a pullback rally (an inverted "V" shape) towards the 5-minute MA or a recent small support-turned-resistance area.

$ADD LevelsThis Pine Script is designed to track and visualize the NYSE Advance-Decline Line (ADD). The Advance-Decline Line is a popular market breadth indicator, showing the difference between advancing and declining stocks on the NYSE. It’s often used to gauge overall market sentiment and strength.

1. //@version=5

This line tells TradingView to use Pine Script v5, the latest and most powerful version of Pine.

2. indicator(" USI:ADD Levels", overlay=false)

• This creates a new indicator called ” USI:ADD Levels”.

• overlay=false means it will appear in a separate pane, not on the main price chart.

3. add = request.security(...)

This fetches real-time data from the symbol USI:ADD (Advance-Decline Line) using a 1-minute timeframe. You can change the timeframe if needed.

add_symbol = input.symbol(" USI:ADD ", "Market Breadth Symbol")

add = request.security(add_symbol, "1", close)

4. Key Thresholds

These define the market sentiment zones:

Zone. Value. Meaning

Overbought +1500 Extremely bullish

Bullish +1000 Generally bullish trend

Neutral ±500 Choppy, unclear market

Bearish -1000 Generally bearish trend

Oversold -1500 Extremely bearish

5. Plot the ADD Line hline(...)

Draws static lines at +1500, +1000, +500, -500, -1000, -1500 for reference so you can visually assess where ADD stands.

6. Horizontal Threshold Lines bgcolor(...)

• Green background if ADD > +1500 → extremely bullish.

• Red background if ADD < -1500 → extremely bearish.

7. Background Highlights alertcondition(...)

• Green background if ADD > +1500 → extremely bullish.

• Red background if ADD < -1500 → extremely bearish.

8. Alert Conditions. alertcondition(...)

Lets you create automatic alerts for:

• USI:ADD being very high or low.

• Crosses above +1000 (bullish trigger).

• Crosses below -1000 (bearish trigger).

You can use these to trigger trades or monitor sentiment shifts.

Summary: When to Use It

• Use this script in a market breadth dashboard.

• Combine it with price action and volume analysis.

• Monitor for ADD crosses to signal potential market reversals or momentum.

TICK Extreme Levels & AlertsAutomatically draws horizontal lines at +1000 and -1000 TICK levels

Sends alerts when TICK crosses those levels (for potential scalping/reversal setups)

Strategy: How to Use TICK in Real-Time Trading

1. Confirm Market Breadth

Use TICK to confirm broad participation in the move:

• Long S&P futures or SPY? Only buy breakouts if TICK is above +600 to +1000

• Shorting? Confirm with TICK below –600 to –1000

2. Fade Extremes for Scalps

Look for reversals at extreme levels:

• Fade +1200+: market likely overbought short term → scalp short

• Fade –1200–: market likely oversold → scalp long

Use in combo with other signals (like price exhaustion, candlestick reversal, or VWAP touches)

3. Avoid Trading in the Choppy Zone

If TICK remains between –400 and +400, institutions are not committed. This is where fakeouts are common.

4. Time Entries with TICK Swings

For example:

• TICK moves from –800 to +600 = momentum shift → look for long entries

• TICK stalling around +1000 = momentum climax → partial profit or fade play