PSP Suite for Algo 1HTF -25% Target## 🔹 PSP Suite for Algo 1HTF – 25% Target

**(Nifty Options – CE / PE)**

### 📌 What this indicator is for

PSP Suite for Algo is a **trend-based directional options indicator** designed specifically for **NIFTY index options trading**.

It helps traders capture **high-probability directional moves** with **clear CE / PE signals**, controlled risk, and predefined targets.

---

## ⏱ Best Timeframe

* **Primary Timeframe:** ✅ **1 Hour (1H TF)**

* Do **not** use on lower timeframes for best accuracy

* Works best during **trending sessions**

---

## 📊 Instrument Best Suited

* **NIFTY Index**

* **NIFTY Weekly Options**

* Buy **CE** on BUY signal

* Buy **PE** on SELL signal

⚠️ Avoid Bank Nifty / Fin Nifty unless properly back-tested.

---

## 🟢 How to Trade (Simple Rules)

### ▶ BUY CE Signal

* When **BUY CE** label appears:

* Buy **ATM or slight ITM CE**

* Prefer same-week expiry

* Enter **after candle close** on 1H timeframe

### ▶ BUY PE Signal

* When **SELL PE** label appears:

* Buy **ATM or slight ITM PE**

* Prefer same-week expiry

* Enter **after candle close** on 1H timeframe

🚫 No over-trading: **Only one position per signal**

---

## 🎯 Target & Stop Loss (Strict Rule)

* **Target:** 🎯 **25% Option Premium**

* **Stop Loss:** ❌ **25% Option Premium**

* **Risk : Reward:** ⚖️ **1 : 1**

👉 When trade moves strongly in your favor, **manual trailing is recommended** (as shown on chart).

---

## 💰 Expected Returns on Nifty

* **Per Trade:**

* ~ **100 – 250 Nifty points equivalent move**

* Option premium typically gives **20–40% moves**

* **Accuracy:** High during **clear trends**

* Best results when market is **not sideways**

---

## 📅 Ideal Market Conditions

✅ Trending Market

✅ Expansion after consolidation

❌ Avoid very low-volatility / choppy sessions

---

## 🔔 Alerts

* Built-in alerts available for:

* **BUY CE**

* **BUY PE**

* Recommended to enable **Once Per Bar Close**

---

## 🧠 Important Notes

* This is **not a scalping tool**

* Designed for **positional intraday / short swing**

* Follow **discipline in SL & position sizing**

* Works best with **trend confirmation from price structure**

---

## ⚠️ Disclaimer

This indicator is for **educational and analytical purposes only**.

Options trading involves risk. Please trade responsibly.

Optionsstrategies

ATR Price ZoneThe ATR Price Zone is an indicator which takes the Daily Average True Range of a stock and shows how high and low the price of the stock could possibly go from the opening price.

Key features:

The ATR Price Zone is an indicator which takes the Daily Average True Range of a stock and shows how high and low the priced the stock could possibly go from the opening price.

Key features:

ATR Price Zone uses zones looking forward to help strategize possible movements in price.

This indicator is customizable with zones, horizontal lines, a quick reference chart and colors.

The indicator continues to move forward with the chart.

It references the Daily True Average Range regardless of which Time Frame you are using.

It also references the opening candle with a blue arrow when using less than daily time frames.

Create by BothwellTrader

Adaptive Bull Ratio Strategy█ Overview: Why This Strategy

Most option strategies fall into two traps:

They are too rigid: A "Call Ratio Spread" works great in slow markets but gets destroyed if the market rallies hard.

They are too simple: A simple "Buy Call" suffers from time decay (Theta) if the market chops sideways.

The Adaptive Bull Ratio Strategy solves both . It is a living strategy that "shifts gears" based on price action.

It is called "Adaptive" because it morphs its structure three times during a trade. It starts conservative to harvest Time Decay, but if the market explodes upwards, it "uncaps" itself to ride the trend aggressively.

█ The Entry Philosophy: Why Supertrend?

The default setting uses the Supertrend indicator as the trigger. This is intentional:

Volatility Awareness: Supertrend adapts to market noise using ATR. In high volatility, bands widen to prevent false entries.

Trend Confirmation: Since Phase 1 involves selling options, entering "too early" against a falling market is dangerous. Supertrend forces patience, waiting for a confirmed reversal (Close > Trend Line), ensuring the momentum is actually in your favor before you commit capital.

The "Drift" Benefit: This strategy excels in markets that "drift" upwards. Supertrend identifies these trends while filtering out short-term chop.

Flexibility with External Sources:

While Supertrend is the default, the strategy is designed to be flexible. You can enable the 'Enable External Source' option in the settings to plug in any custom indicator (e.g., Moving Averages, Parabolic SAR, or a proprietary trendline).

The Golden Rule for External Sources: The script interprets a Bullish Signal whenever your External Source line is below the Close price (Ext Source < Close).

Compatibility: As long as your custom indicator behaves like a support line in an uptrend (plotting below the candles), it will work seamlessly with this strategy's logic.

█ The "Long Only" Rationale: Avoiding the Volatility Trap

Why not trade this on the short side (Puts) during crashes?

The Volatility Trap (Vega Risk): In Bull markets, Implied Volatility (IV) usually drops, helping your sold options decay faster. In Bear markets, IV explodes (panic). Selling OTM Puts during a crash is dangerous as their value skyrockets, neutralizing gains.

Velocity Risk: Bear markets crash fast ("Elevator Down"). Prices can blow through adjustment levels faster than the strategy can safely roll down, causing slippage.

Structural Skew: OTM Puts are inherently more expensive. Buying expensive ITM Puts and selling expensive OTM Puts shifts the breakeven further away, making V-shape recoveries painful.

█ How It Works & Stands Out

This strategy actively transforms risk profiles based on market movement:

Phase 1: The "Safe" Start (Entry)

Setup: Initiates a Call Ratio Spread (Buy 2 ITM, Sell 4 OTM) + Protective Puts.

Logic: Profits from sideways drift or slow rallies via Time Decay (Theta). The sold options finance the trade.

Phase 2: The "Shift" (Adjustment Level 1)

Trigger: Market moves above Leg 2 (3 OTM Call).

Action: Rolls Up the position. Exits initial legs, enters new higher legs, and adds a Short Put to finance the roll.

Impact: Aggressive. You bet the trend is strong enough to support the added downside risk of the short put.

Phase 3: The "Uncap" (Adjustment Level 2)

Trigger: Market moves above Leg 3 (4 OTM Call).

Action: Exits all Sold Calls.

Impact: Uncaps profit potential. The trade becomes a Net Long position (Long Calls + Short Puts), allowing you to ride a massive rally without a ceiling.

Phase 4: The "Lock-In" (Optional Trail Adjustment)

Trigger: The market goes parabolic (price rises X levels above Leg 3, configurable in settings).

Action (If Enabled):

Call Adj: Exits the Phase 3 calls and buys fresh 1-OTM calls (Rolling Up to lock profits).

Put Adj: Exits all Put legs (Removing downside risk completely).

Impact: Maximum Safety. This phase is about "banking" the windfall from a massive rally and leaving a smaller, risk-free runner to capture any final extension.

█ How to Start: A Quick Setup Guide

Step 1: Map Expiry Dates

Manually input your trading expiry dates in Settings -> Expiry Management.

Format: YYYY-MM-DD (e.g., 2025-12-25). Strict adherence required for DhanHQ.

Step 2: Configure Symbol & Size

Exchange/Symbol: Enter NSE and NIFTY (or your ticker).

Lot Multiplier: Default is 1. Set to 2 to double all quantities (e.g., Buy 2 becomes Buy 4).

Step 3: Understand Visuals

Entry Window (Light Blue): Strategy is scanning for new trades.

Non-Entry Window (Dark Blue): Trading blocked (Day before Expiry & Expiry Day). Only management allowed.

Green Box: Valid Late Entry Zone.

Red Dashed Line: Invalidation Level (if price touches this, no late entry).

Fuchsia Line: Trigger level for Special Trail Adjustments (Phase 4).

IMPORTANT: Broker & Technology Heads-Up:

The alerts generated by this script ({"secret": "...", "alertType": "multi_leg_order"...}) are specifically formatted for the DhanHQ webhook structure.

Dhan Users: Plug-and-play.

Other Brokers: You need middleware (NextLevelBot, Quantiply) to parse the JSON.

█ Risk Disclaimer & Advice

Trading options involves substantial risk.

The Whipsaw Risk: In Phase 2, you are Long Calls and Short Puts. A sharp reversal causes losses on both sides.

Margin: Selling options requires significant margin. Keep a 15-20% cash buffer to handle adjustments instantly.

Testing: This strategy is optimized for NIFTY Weekly Options. Effectiveness on BankNifty or Stocks is untested and may require parameter tuning.

Advice:

Backtest: Use TradingView Replay.

Paper Trade: Run for at least one expiry cycle before live deployment.

Consult: Seek professional financial advice before trading.

Practical Tips for Smooth Execution

For a new trader deploying this system, these operational tips are vital:

Capital Buffer: Do not trade at your limit. Always keep 10-15% free cash in your broker account. Adjustments (specifically Phase 2, where you sell an extra Put) require additional margin instantly. If margin is short, the order fails, and your hedge breaks.

Liquidity Awareness : The script trades "Far Deep OTM" options (Leg 4) to reduce margin. On indices like Nifty/BankNifty, this is fine. On individual stocks, these deep strikes might be illiquid. Check the option chain volume before deploying on stocks.

Trust the Process (but Verify) : While the algo drives, you are the pilot.

Check your API connection every morning.

Ensure the "Entry Window" background color on the chart matches your real-world date.

Verify that your broker executed all legs of a multi-leg order (partial fills are rare but possible).

The "Human" Stop: If major news breaks (e.g., unexpected election results, war announcements), volatility can expand faster than any algo can react. It is acceptable—and smart—to pause the strategy during known "Black Swan" events or earnings releases.

█ Timeframe Selection: The 30-Minute Standard

Critical Requirement: This indicator must be applied to a 30-minute chart.

Why?

Noise Filtering: The Supertrend logic is tuned to capture multi-day trends. Lower timeframes (5m, 15m) are full of "noise"—random fluctuations that look like trend changes but aren't.

Execution Logic (The Hybrid Engine): The script has a built-in "Dual Timeframe" architecture.

Decision Layer (30m): Uses the chart timeframe to decide when to be Bullish or Bearish.

Execution Layer (5m): Internally fetches 5-minute data to manage the how (Adjustments, Late Entries, and precise invalidation).

The Risk of Lower Timeframes: If you run the main chart on 5-minutes, you destroy this hierarchy. You will get too many signals, pay too much brokerage, and the internal logic may behave erratically.

Recommendation: Always keep your TradingView chart interval at 30m. Do not switch to lower timeframes expecting "faster" signals; you will likely just get "false" signals.

█ Testing Scope, Feedback

⚠️ Important Note on Asset Classes:

This strategy logic and the associated strike step calculations have been rigorously tested ONLY on NIFTY Index Options with Weekly Expiry.

BankNifty / Sensex / FinNifty: The volatility characteristics (ATR) and strike intervals of these instruments differ significantly from NIFTY. The effectiveness of this strategy on these other scripts has not been verified and may require different parameter tuning (e.g., strike_step or ATR Length).

Stocks: Individual stock options often lack the liquidity required for the "Deep OTM" legs, leading to potential execution failures.

We encourage traders to backtest this logic on other indices and share their findings! If you find a robust parameter set for BankNifty or observe unique behaviors on other scripts, please let us know in the comments below so we can improve the algorithm for everyone. Your feedback is appriciated.

jitfxjitfx

This indicator plots Central Pivot Range (CPR) along with daily Support & Resistance levels up to 5 levels directly on the price chart. It is designed for intraday and positional traders who want a clean, rule-based structure for market bias, entries, and targets.

Features

Today’s CPR (Pivot, BC, TC)

Next Day CPR calculated from the completed daily candle (useful after market close)

Support & Resistance levels: S1–S5 and R1–R5

On/Off toggles for CPR, Next Day CPR, and S/R levels

Plots neatly on the price chart (overlay)

How to Use

Price above CPR → bullish bias

Price below CPR → bearish bias

Narrow CPR → potential breakout day

Wide CPR → range-bound / mean reversion

Use R levels as potential resistance/targets and S levels as demand/bounce zones

Best For

Index & stock intraday trading

Pre-market planning using Next Day CPR

Identifying structure, bias, and objective targets

Max Pain Options [QuantLabs] v5 (Balanced)Institutional Grade Options Analysis: Max Pain, Gamma & Pin Risk

For years, TradingView users have been flying blind without access to Options Chain data. QuantLabs: Max Pain & Gamma Exposure changes that. This is not just a support/resistance indicator—it is a sophisticated, algorithmic model that reverse-engineers the incentives of Market Makers using synthetic Black-Scholes logic.

This tool visualizes the "invisible hand" of the market: the hedging requirements of large dealers who are forced to buy or sell to keep their books neutral.

CORE FEATURES:

🔴 Max Pain Gravity Model The bright red line represents the "Max Pain" strike—the price level where the maximum amount of Options Open Interest (Calls + Puts) expires worthless.

Theory: As OpEx (Expiration) approaches, Market Makers maximize profits by pinning the price to this level.

Strategy: Use this as a mean-reversion target. If price is far away, look for a snap-back to the red line.

🟣 Gamma Exposure Profiles (The Purple Lines) These neon histograms show you the estimated "Gamma Walls."

Long Gamma: Dealers trade against the trend (stabilizing price).

Short Gamma: Dealers trade with the trend (accelerating volatility).

Visual: The larger the purple bar, the harder it will be for price to break through that level.

📦 Algorithmic "Pin Risk" Zones The dashed red box highlights the "Kill Zone." When price enters this area near expiration, volatility often dies as dealers pin the asset to kill retail premiums.

Warning: Do not expect breakouts while inside the Pin Zone.

📊 Institutional HUD A clean, non-intrusive dashboard provides real-time Greeks and risk analysis:

Pin Risk: High/Medium/Low probability of a pinned close.

Exp Mode: Detects if the market is in "Short Gamma" (Squeeze territory) or "Long Gamma" (Chop territory).

HOW IT WORKS (The Math): Since live options data is not available via Pine Script, this engine uses a proprietary Synthetic OI Distribution Model. It inputs Volume, Volatility (IV), and Time-to-Expiry into a modified Black-Scholes equation to probability-map where the heavy open interest likely sits.

SETTINGS & CUSTOMIZATION:

Responsiveness: Tuned for the "Goldilocks Zone" (Spread: 12, Decay: 22) to catch local liquidity walls without over-fitting.

Visuals: Designed for Dark Mode. High-contrast Neon aesthetics for maximum readability.

I4I Inside Vortex Strike RateThis indicator identifies what I call an "Inside Vortex": It's similar to a Doji but more strict in having to be inside a keltner and also have a lower ATR than a blended average.

The bar itself is not that special. But it indicates that a potential big move might come in the next 2 periods.

After the patter: It then looks at what I call the Market Maker High and Low: A % of a blended ATR. It then looks back 100-200 or more bars and calculates the overall strike % in history for the High and low after the pattern happens.

This allows us to know how often these levels are hit within the next 2 periods to find if we have any edge on spread, call or put prices or use them as targets.

So its:

Pattern:

Levels

Strike Rate.

Very unique and EXTREME useful. Especially for options traders.

Gamma Exposure Levels by OMG (Oh My Gamma)OMG (Oh My Gamma) - Daily GEX Levels

An operational framework for Gamma analysis with daily data.

Indicator's Purpose & Demo Data

This indicator plots key strategic levels derived from Gamma Exposure (GEX) analysis. It showcases the operational logic of OhMyGamma analytical engine.

IMPORTANT: The levels plotted by this public script are based on a past date's snapshot for demonstration purposes. They are not valid for live trading and will not update automatically.

The real edge comes from using the fresh data structure provided daily.

How to Read the Levels

This indicator is designed to provide actionable intelligence, not just data. Here's how to read it:

The Levels: Each line represents a key strategic zone (Zero Gamma, Call/Put Walls, etc.) where a market reaction is statistically probable due to dealer hedging flows.

Line Thickness = Strategic Importance: The thickness of each line directly corresponds to its strategic rating. Thicker, solid lines represent higher-conviction zones.

Labels & Tooltips: Hover over a level's label on your chart to see its full description, confluences, and strategic rating.

Pro Tip: The Power of Confluence

This indicator is not a standalone "system". It's an institutional-grade intelligence layer. Its predictive power increases exponentially when used to find confluence with your own analysis.

The highest-probability trades occur when a key Gamma level aligns with:

Price Action: Key support/resistance zones, order blocks, or liquidity pools.

Volumetric Indicators: High/Low Volume Nodes (HVN/LVN) from Volume Profile, VWAP, and Anchored VWAP.

Use these levels to confirm your setups and gain the conviction to act.

How to Get the Daily Updated Script

This indicator requires a new Pine Script code each day to load the current session's data.

To get the daily updated code feel free to visit www.ohmygamma.com

Feedback & Suggestions

This tool is built for the community. Suggestions for improvements and new features are highly welcome and help the project evolve. Feel free to get in touch via the contact form on the website.

Disclaimer: This tool is for informational and educational purposes only. Trading involves significant risk. The authors assume no responsibility for any trading decisions.

Multi Straddle-Strangle ChartThis powerful indicator is designed for options traders who want to visualize and track the combined premium of multiple straddle and strangle strategies in a single, dedicated pane.

Quickly analyze and compare up to five different options strategies at a glance, directly on your chart. This tool is perfect for monitoring volatility, tracking potential profits/losses on a position, and spotting key support and resistance levels based on option premiums.

Key Features:

Plot Up to 5 Strategies: Simultaneously plot any combination of up to 5 straddles or strangles.

Real-Time Data: Fetches live data for both Call and Put options to give you an up-to-the-second view of the combined price.

Dynamic Symbol Generation: Automatically detects the underlying symbol (e.g., NIFTY, BANKNIFTY, stocks) and builds the correct option symbols based on your input.

Customizable Inputs: Easily configure the expiry date, strike prices and line colors for each of the 5 lines.

In-Chart Summary Table: A clean and clear table in the corner of your chart provides a quick summary of each enabled strategy and its current price.

Important Note on Usage:

This tool requires you to input a strike price in all fields, even if you do not plan to use all five lines. This is necessary because of a fundamental rule in the Pine Script language: every input must have a constant, non-empty default value. The indicator is optimized to only fetch data for the lines you have explicitly enabled with the "Enable Line X" checkbox.

Volatility Cone Forecaster Lite [PhenLabs]📊 Volatility Cone Forecaster

Version: PineScript™v6

📌Description

The Volatility Cone Forecaster (VCF) is an advanced indicator designed to provide traders with a forward-looking perspective on market volatility. Instead of merely measuring past price fluctuations, the VCF analyzes historical volatility data to project a statistical “cone” that outlines a probable range for future price movements. Its core purpose is to contextualize the current market environment, helping traders to anticipate potential shifts from low to high volatility periods (and vice versa). By identifying whether volatility is expanding or contracting relative to historical norms, it solves the critical problem of preparing for significant market moves before they happen, offering a clear statistical edge in strategy development.

This indicator moves beyond lagging measures by employing percentile analysis to rank the current volatility state. This allows traders to understand not just what volatility is, but how significant it is compared to the recent past. The VCF is built for discretionary traders, system developers, and options strategists who need a sophisticated understanding of market dynamics to manage risk and identify high-probability opportunities.

🚀Points of Innovation

Forward-Looking Volatility Projection: Unlike standard indicators that only show historical data, the VCF projects a statistical cone of future volatility.

Percentile-Based Regime Analysis: Ranks current volatility against historical data (e.g., 90th, 75th percentiles) to provide objective context.

Automated Regime Detection: Automatically identifies and labels the market as being in a ‘High’, ‘Low’, or ‘Normal’ volatility regime.

Expansion & Contraction Signals: Clearly indicates whether volatility is currently increasing or decreasing, signaling shifts in market energy.

Integrated ATR Comparison: Plots an ATR-equivalent volatility measure to offer a familiar point of reference against the statistical model.

Dynamic Visual Modeling: The cone visualization directly on the price chart provides an intuitive guide for future expected price ranges.

🔧Core Components

Realized Volatility Engine: Calculates historical volatility using log returns over multiple user-defined lookback periods (short, medium, long) for a comprehensive view.

Percentile Analysis Module: A custom function calculates the 10th, 25th, 50th, 75th, and 90th percentiles of volatility over a long-term lookback (e.g., 252 days).

Forward Projection Calculator: Uses the calculated volatility percentiles to mathematically derive and draw the upper and lower bounds of the future volatility cone.

Volatility Regime Classifier: A logic-based system that compares current volatility to the historical percentile bands to classify the market state.

🔥Key Features

Customizable Lookback Periods: Adjust short, medium, and long-term lookbacks to fine-tune the indicator’s sensitivity to different market cycles.

Configurable Forward Projection: Set the number of days for the forward cone projection to align with your specific trading horizon.

Interactive Display Options: Toggle visibility for percentile labels, ATR levels, and regime coloring to customize the chart display.

Data-Rich Information Table: A clean, on-screen table displays all key metrics, including current volatility, percentile rank, regime, and trend.

Built-in Alert Conditions: Set alerts for critical events like volatility crossing the 90th percentile, dropping below the 10th, or switching between expansion and contraction.

🎨Visualization

Volatility Cone: Shaded bands projected onto the future price axis, representing the probable price range at different statistical confidence levels (e.g., 75th-90th percentile).

Color-Coded Volatility Line: The primary volatility plot dynamically changes color (e.g., red for high, green for low) to reflect the current volatility regime, providing instant context.

Historical Percentile Bands: Horizontal lines plotted across the indicator pane mark the key percentile levels, showing how current volatility compares to the past.

On-Chart Labels: Clear labels automatically display the current volatility reading, its percentile rank, the detected regime, and trend (Expanding/Contracting).

📖Usage Guidelines

Setting Categories

Short-term Lookback: Default: 10, Range: 5-50. Controls the most sensitive volatility calculation.

Medium-term Lookback: Default: 21, Range: 10-100. The primary input for the current volatility reading.

Long-term Lookback: Default: 63, Range: 30-252. Provides a baseline for long-term market character.

Percentile Lookback Period: Default: 252, Range: 100-1000. Defines the period for historical ranking; 252 represents one trading year.

Forward Projection Days: Default: 21, Range: 5-63. Determines how many bars into the future the cone is projected.

✅Best Use Cases

Breakout Trading: Identify periods of deep consolidation when volatility falls to low percentile ranks (e.g., below 25th) and begins to expand, signaling a potential breakout.

Mean Reversion Strategies: Target trades when volatility reaches extreme high percentile ranks (e.g., above 90th), as these periods are often unsustainable and lead to contraction.

Options Strategy: Use the cone’s projected upper and lower bounds to help select strike prices for strategies like iron condors or straddles.

Risk Management: Widen stop-losses and reduce position sizes when the indicator signals a transition into a ‘High’ volatility regime.

⚠️Limitations

Probabilistic, Not Predictive: The cone represents a statistical probability, not a guarantee of future price action. Extreme, unpredictable news events can drive prices outside the cone.

Lagging by Nature: All calculations are based on historical price data, meaning the indicator will always react to, not pre-empt, market changes.

Non-Directional: The indicator forecasts the *magnitude* of future moves, not the *direction*. It should be paired with a directional analysis tool.

💡What Makes This Unique

Forward Projection: Its primary distinction is projecting a data-driven, statistical forecast of future volatility, which standard oscillators do not do.

Contextual Analysis: It doesn’t just provide a number; it tells you what that number means through percentile ranking and automated regime classification.

🔬How It Works

1. Data Calculation:

The indicator first calculates the logarithmic returns of the asset’s price. It then computes the annualized standard deviation of these returns over short, medium, and long-term lookback periods to generate realized volatility readings.

2. Percentile Ranking:

Using a 252-day lookback, it analyzes the history of the medium-term volatility and determines the values that correspond to the 10th, 25th, 50th, 75th, and 90th percentiles. This builds a statistical map of the asset’s volatility behavior.

3. Cone Projection:

Finally, it takes these historical percentile values and projects them forward in time, calculating the potential upper and lower price bounds based on what would happen if volatility were to run at those levels over the next 21 days.

💡Note:

The Volatility Cone Forecaster is most effective on daily and weekly charts where statistical volatility models are more reliable. For lower timeframes, consider shortening the lookback periods. Always use this indicator as part of a comprehensive trading plan that includes other forms of analysis.

FluidFlow OscillatorFluidFlow Oscillator: Study Material for Traders

Overview

The FluidFlow Oscillator is a custom technical indicator designed to measure price momentum and market flow dynamics by simulating fluid motion concepts such as velocity, viscosity, and turbulence. It helps traders identify potential buy and sell signals along with trend strength, momentum direction, and volatility conditions.

This study explains the underlying calculation concepts, signal logic, visual cues, and how to interpret the professional dashboard table that summarizes key indicator readings.

________________________________________

How the FluidFlow Oscillator Works

Core Mechanisms

1. Price Flow Velocity

o Measures the rate of change of price over a specified flow length (default 40 bars).

o Calculated as a percentage change of closing price: roc=close−closelen_flowcloselen_flow×100\text{roc} = \frac{\text{close} - \text{close}_{len\_flow}}{\text{close}_{len\_flow}} \times 100roc=closelen_flowclose−closelen_flow×100

o Smoothed by an EMA (Exponential Moving Average) to reduce noise, generating a "flow velocity" value.

2. Viscosity Factor

o Analogous to fluid viscosity, it adjusts the flow velocity based on recent price volatility.

o Volatility is computed as the standard deviation of close prices over the flow length.

o The viscosity acts as a damping factor to slow down the flow velocity in highly volatile conditions.

o This results in a "flow with viscosity" value, that smooths out the velocity considering market turbulence.

3. Turbulence Burst

o Captures sudden changes or bursts in the flow by measuring changes between successive viscosity-adjusted flows.

o The turbulence value is a smoothed absolute change in flow.

o A burst boost factor is added to the oscillator to incorporate this rapid change component, amplifying signals during sudden shifts.

4. Oscillator Calculation

o The raw oscillator value is the sum of flow with viscosity plus burst boost, scaled by 10.

o Clamped between -100 and +100 to limit extremes.

o Finally, smoothed again by EMA for cleaner visualization.

________________________________________

Signal Logic

The oscillator works with complementary components to produce actionable signals:

• Signal Line: An EMA-smoothed version of the oscillator for generating crossover-based signals.

• Momentum: The rate of change of the oscillator itself, smoothed by EMA.

• Trend: Uses fast (21-period EMA) and slow (50-period EMA) moving averages of price to identify market trend direction (uptrend, downtrend, or sideways).

Signal Conditions

• Bullish Signal (Buy): Oscillator crosses above the oversold threshold with positive momentum.

• Bearish Signal (Sell): Oscillator crosses below the overbought threshold with negative momentum.

Statuses

The oscillator provides descriptive market states based on level and momentum:

• Overbought

• Oversold

• Buy Signal

• Sell Signal

• Bullish / Bearish (momentum-driven)

• Neutral (no clear trend)

________________________________________

Color System and Visualization

The oscillator uses a sophisticated HSV color model adapting hues according to:

• Oscillator value magnitude and sign (positive or negative)

• Acceleration of oscillator changes

• Smooth color gradients to facilitate intuitive understanding of trend strength and momentum shifts

Background colors highlight overbought (red tint) and oversold (green tint) zones with transparency.

________________________________________

How to Understand the Professional Dashboard Table

The FluidFlow Oscillator offers an integrated table at the bottom center of the chart. This dashboard summarizes critical indicator readings in 8 columns across 3 rows:

Column Description

SIGNAL Current signal status (e.g., Buy, Sell, Overbought) with color coding

OSCILLATOR Current oscillator value (-100 to +100) with color reflecting intensity and direction

MOMENTUM Momentum bias indicating strength/direction of oscillator changes (Strong Up, Up, Sideways, Down, Strong Down)

TREND Current trend status based on EMAs (Strong Uptrend, Uptrend, Sideways, Downtrend, Strong Downtrend)

VOLATILITY Volatility percentage relative to average, indicating market activity level

FLOW Flow velocity value describing price momentum magnitude and direction

TURBULENCE Turbulence level indicating sudden bursts or spikes in price movement

PROGRESS Oscillator's position mapped as a percentage (0% to 100%) showing proximity to extreme levels

Rows Explained

• Row 1 (Header): Labels for each metric.

• Row 2 (Values): Current numerical or descriptive values color-coded along a professional scheme:

o Green or lime tones indicate positive or bullish conditions.

o Red or orange tones indicate caution, sell signals, or bearish conditions.

o Blue tones indicate neutral or stable conditions.

• Row 3 (Status Indicators): Emoji-like icons and bars provide a quick visual gauge of each metric's intensity or signal strength:

o For example, "🟢🟢🟢" suggests very strong bullish momentum, while "🔴🔴🔴" suggests strong bearish momentum.

o Progress bar visually demonstrates oscillator movement toward oversold or overbought extremes.

________________________________________

Practical Interpretation Tips

• A Buy signal with green colors and strong momentum usually precedes upward price moves.

• An Overbought status with red background and red table colors warns of potential price corrections or reversals.

• Watch the Turbulence to gauge market instability; spikes may precede price shocks or volatility bursts.

• Confirm signals with the Trend and Momentum columns to avoid false entries.

• Use the Progress bar to anticipate oscillations approaching key threshold levels for timing trades.

________________________________________

Alerts

The oscillator supports alerts for:

• Buy and sell signals based on oscillator crossovers.

• Overbought and oversold levels reached.

These help traders automate awareness of important market conditions.

________________________________________

Disclaimer

The FluidFlow Oscillator and its signals are for educational and informational purposes only. They do not guarantee profits and should not be considered as financial advice. Always conduct your own research and use proper risk management when trading. Past performance is not indicative of future results.

________________________________________

This detailed explanation should help you understand the workings of the FluidFlow Oscillator, its components, signal logic, and how to analyze its professional dashboard for informed trading decisions.

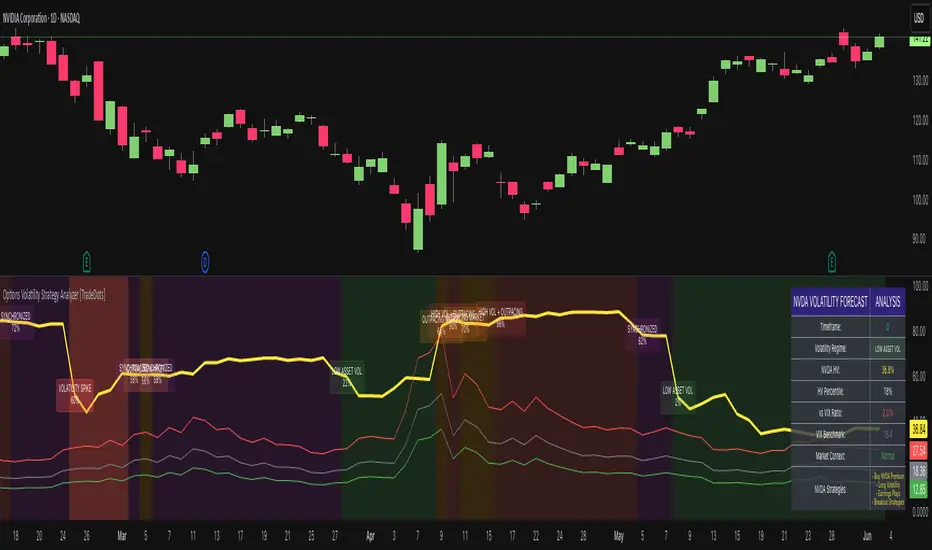

Options Volatility Strategy Analyzer [TradeDots]The Options Volatility Strategy Analyzer is a specialized tool designed to help traders assess market conditions through a detailed examination of historical volatility, market benchmarks, and percentile-based thresholds. By integrating multiple volatility metrics (including VIX and VIX9D) with color-coded regime detection, the script provides users with clear, actionable insights for selecting appropriate options strategies.

📝 HOW IT WORKS

1. Historical Volatility & Percentile Calculations

Annualized Historical Volatility (HV): The script automatically computes the asset’s historical volatility using log returns over a user-defined period. It then annualizes these values based on the chart’s timeframe, helping you understand the asset’s typical volatility profile.

Dynamic Percentile Ranks: To gauge where the current volatility level stands relative to past behavior, historical volatility values are compared against short, medium, and long lookback periods. Tracking these percentile ranks allows you to quickly see if volatility is high or low compared to historical norms.

2. Multi-Market Benchmark Comparison

VIX and VIX9D Integration: The script tracks market volatility through the VIX and VIX9D indices, comparing them to the asset’s historical volatility. This reveals whether the asset’s volatility is outpacing, lagging, or remaining in sync with broader market volatility conditions.

Market Context Analysis: A built-in term-structure check can detect market stress or relative calm by measuring how VIX compares to shorter-dated volatility (VIX9D). This helps you decide if the present environment is risk-prone or relatively stable.

3. Volatility Regime Detection

Color-Coded Background: The analyzer assigns a volatility regime (e.g., “High Asset Vol,” “Low Asset Vol,” “Outpacing Market,” etc.) based on current historical volatility percentile levels and asset vs. market ratios. A color-coded background highlights the regime, enabling traders to quickly interpret the market’s mood.

Alerts on Regime Changes & Spikes: Automated alerts warn you about any significant expansions or contractions in volatility, allowing you to react swiftly in changing conditions.

4. Strategy Forecast Table

Real-Time Strategy Suggestions: At the close of each bar, an on-chart table generates suggested options strategies (e.g., selling premium in high volatility or buying premium in low volatility). These suggestions provide a quick summary of potential tactics suited to the current regime.

Contextual Market Data: The table also displays key statistics, such as VIX levels, asset historical volatility percentile, or ratio comparisons, helping you confirm whether volatility conditions warrant more conservative or more aggressive strategies.

🛠️ HOW TO USE

1. Select Your Timeframe: The script supports multiple timeframes. For short-term trading, intraday charts often reveal faster shifts in volatility. For swing or position trading, daily or weekly charts may be more stable and produce fewer false signals.

2. Check the Volatility Regime: Observe the background color and on-chart labels to identify the current regime (e.g., “HIGH ASSET VOL,” “LOW VOL + LAGGING,” etc.).

3. Review the Forecast Table: The table suggests strategy ideas (e.g., iron condors, long straddles, ratio spreads) depending on whether volatility is elevated, subdued, or spiking. Use these as a starting point for designing trades that match your risk tolerance.

4. Combine with Additional Analysis: For optimal results, confirm signals with your broader trading plan, technical tools (moving averages, price action), and fundamental research. This script is most effective when viewed as one component in a comprehensive decision-making process.

❗️LIMITATIONS

Directional Neutrality: This indicator analyzes volatility environments but does not predict price direction (up/down). Traders must combine with directional analysis for complete strategy selection.

Late or Missed Signals: Since all calculations require a bar to close, sharp intrabar volatility moves may not appear in real-time.

False Positives in Choppy Markets: Rapid changes in percentile ranks or VIX movements can generate conflicting or premature regime shifts.

Data Sensitivity: Accuracy depends on the availability and stability of volatility data. Significant gaps or unusual market conditions may skew results.

Market Correlation Assumptions: The system assumes assets generally correlate with S&P 500 volatility patterns. May be less effective for:

Small-cap stocks with unique volatility drivers

International stocks with different market dynamics

Sector-specific events disconnected from broad market

Cryptocurrency-related assets with independent volatility patterns

RISK DISCLAIMER

Options trading involves substantial risk and is not suitable for all investors. Options strategies can result in significant losses, including the total loss of premium paid. The complexity of options strategies requires thorough understanding of the risks involved.

This indicator provides volatility analysis for educational and informational purposes only and should not be considered as investment advice. Past volatility patterns do not guarantee future performance. Market conditions can change rapidly, and volatility regimes may shift without warning.

No trading system can guarantee profits, and all trading involves the risk of loss. The indicator's regime classifications and strategy suggestions should be used as part of a comprehensive trading plan that includes proper risk management, directional analysis, and consideration of broader market conditions.

5EMA_BB_ScalpingWhat?

In this forum we have earlier published a public scanner called 5EMA BollingerBand Nifty Stock Scanner , which is getting appreciated by the community. That works on top-40 stocks of NSE as a scanner.

Whereas this time, we have come up with the similar concept as a stand-alone indicator which can be applied for any chart, for any timeframe to reap the benifit of reversal trading.

How it works?

This is essentially a reversal/divergence trading strategy, based on a widely used strategy of Power-of-Stocks 5EMA.

To know the divergence from 5-EMA we just check if the high of the candle (on closing) is below the 5-EMA. Then we check if the closing is inside the Bollinger Band (BB). That's a Buy signal. SL: low of the candle, T: middle and higher BB.

Just opposite for selling. 5-EMA low should be above 5-EMA and closing should be inside BB (lesser than BB higher level). That's a Sell signal. SL: high of the candle, T: middle and lower BB.

Along with we compare the current bar's volume with the last-20 bar VWMA (volume weighted moving average) to determine if the volume is high or low.

Present bar's volume is compared with the previous bar's volume to know if it's rising or falling.

VWAP is also determined using `ta.vwap` built-in support of TradingView.

The Bolling Band width is also notified, along with whether it is rising or falling (comparing with previous candle).

What's special?

We love this reversal trading, as it offers many benifits over trend following strategies:

Risk to Reward (RR) is superior.

It _Does Hit_ stop losses, but the stop losses are tiny.

Means, althrough the Profit Factor looks Nahh , however due to superior RR, end of day it ended up in green.

When the day is sideways, it's difficult to trade in trending strategies. This sort of volatility, reversal strategies works better.

It's always tempting to go agaist the wind. Whole world is in Put/PE and you went opposite and enter a Call/CE. And turns out profitable! That's an amazing feeling, as a trader :)

How to trade using this?

* Put any chart

* Apply this screener from Indicators (shortcut to launch indicators is just type / in your keyboard).

* It will show you the Green up arrow when buy alert comes or red down arrow when sell comes. * Also on the top right it will show the latest signal with entry, SL and target.

Disclaimer

* This piece of software does not come up with any warrantee or any rights of not changing it over the future course of time.

* We are not responsible for any trading/investment decision you are taking out of the outcome of this indicator.

ChopFlow ATR Scalp StrategyA lean, high-velocity scalp framework for NQ and other futures that blends trend clarity, volume confirmation, and adaptive exits to give you precise, actionable signals—no cluttered bands or lagging indicators.

⸻

🔍 Overview

This strategy locks onto rapid intraday moves by:

• Filtering for directional momentum with the Choppiness Index (CI)

• Confirming conviction via On-Balance Volume (OBV) against its moving average

• Automatically sizing stops and targets with a multiple of the Average True Range (ATR)

It’s designed for scalp traders who need clean, timely entries without wading through choppy noise.

⸻

⚙️ Key Features & Inputs

1. ATR Length & Multiplier

• Controls exit distances based on current volatility.

2. Choppiness Length & Threshold

• Measures trend strength; only fires when the market isn’t “stuck in the mud.”

3. OBV SMA Length

• Smoothes volume flow to confirm genuine buying or selling pressure.

4. Custom Session Hours

• Avoid overnight gaps or low-liquidity periods.

All inputs are exposed for rapid tuning to your preferred scalp cadence.

🚀 How It Works

1. Long Entry triggers when:

• CI < threshold (strong trend)

• OBV > its SMA (positive volume flow)

• You’re within the defined session

2. Short Entry mirrors the above (CI < threshold, OBV < SMA)

3. Exit uses ATR × multiplier for both stop-loss and take-profit

⸻

🎯 Usage Tips

• Start with defaults (ATR 14, multiplier 1.5; CI 14, threshold 60; OBV SMA 10).

• Monitor signal frequency, then tighten/loosen CI or OBV look-back as needed.

• Pair with a fast MA crossover or price-action trigger if you want even sharper timing.

• Backtest across different sessions (early open vs. power hours) to find your edge.

⸻

⚠️ Disclaimer

This script is provided “as-is” for educational and research purposes. Always paper-trade any new setup extensively before deploying live capital, and adjust risk parameters to your personal tolerance.

⸻

Elevate your scalp game with ChopFlow ATR—where trend, volume, and volatility converge for clear, confident entries. Happy scalping!

Option Time ValueThis TradingView script calculates and visualizes the time value of an option (Call or Put) based on its market price and intrinsic value. The time value represents the premium paid for the option above its intrinsic value, and it is a key metric for analyzing the cost of holding an option.

This script is suitable for traders analyzing options on indices or stocks, such as the NIFTY 50, and supports both Call and Put options. By dynamically extracting the strike price and option type from the input symbol, it adapts seamlessly to the selected instrument.

Key Features:

Dynamic Instrument Selection:

Users can input the underlying asset (e.g., NSE:NIFTY) and the specific option instrument (e.g., NSE:NIFTY250327C24000 for a Call or NSE:NIFTY250327P24000 for a Put).

Automatic Option Type Detection:

The script detects whether the option is a Call or a Put by parsing the input symbol for the characters "C" (Call) or "P" (Put).

Dynamic Strike Price Extraction:

The strike price is dynamically extracted from the input option symbol, eliminating the need for hardcoding and reducing user errors.

Key Metrics Plotted:

Time Value: The premium paid above the intrinsic value, plotted in blue.

Intrinsic Value: The calculated intrinsic value of the option, plotted in green.

Seamless Integration:

Designed for ease of use and integration into existing TradingView setups.

Automatically adjusts to the timeframe and pricing data of the selected instruments.

Options Cumulative Chart AnalysysThis Pine Script is a comprehensive tool designed for traders analyzing options data on TradingView. It aggregates multiple symbols to calculate and visualize cumulative performance, providing essential insights for decision-making.

Key Features:

Symbol and Strike Price Configuration:

Supports up to four configurable symbols (e.g., NIFTY options).

Allows defining buy/sell actions, quantities, and entry premiums for each symbol.

Customizable Chart Display:

Plot candlesticks and line charts for cumulative data.

Configurable Exponential Moving Averages (EMAs) for technical analysis.

Entry and price lines with customizable colors.

Timeframe Management:

Supports higher timeframe (HTF) candles.

Ensures compatibility with the current chart timeframe to maintain accuracy.

Dynamic Coloring and Visualization:

Red, green, and gray color schemes for body and wicks of candlesticks based on price movements.

Customizable positive and negative color schemes.

Table for Data Representation:

Displays an info table showing symbols, quantities, entry prices, and latest traded prices (LTP).

Adjustable table position, overlay, and styling.

Premium and Profit/Loss Calculations:

Calculates cumulative open, high, low, and close prices considering premiums and quantities.

Tracks the profit and loss dynamically based on cumulative premiums and market prices.

Alerts and Notifications:

Alerts triggered on specific conditions, such as when the profit/loss turns negative.

Modular Functions:

Functions for calculating high/low/open/close values, combining premiums, and drawing candlesticks.

Utilities for symbol management and security requests.

Custom Settings:

Includes a wide range of input options for customization:

Timeframes, EMA lengths, colors, table configurations, and more.

Error Handling:

Validates timeframe inputs to ensure compatibility and prevent runtime errors.

This script is designed for advanced traders looking for a customizable tool to analyze cumulative options data efficiently. By leveraging its modular design and visual elements, users can make informed trading decisions with a holistic view of market movements.

Rolling Straddle PremiumScript is Basically intended to provide insight's on the Rolling Straddle premium for the selected index based on the input settings.

Important thing to consider for the script to work seamlessly:

Specify the LTP in the input field (need not be very accurate)

Specify the Expiry Date for the Option Strike.

Ensure Profile matches to the chart script (Index Script)

Note: Zones marked in Blue, is the max level that indicator can track the option prices. beyond which it may fail to track, during such time consider reloading the indicator with Latest LTP .

Labels on the chart indicate that If i had shorted the Straddle, what would be my current position of that Straddle. however the rational behind shorting is only the pivot high points (not sure if this is right or wrong! )

Note On Labels: Labels are delayed basis the pivot point candles specified in the indicator settings.

EN: Entry Price (Straddle Premium) of the Strike Specified.

Cur: Current Price ( Current Straddle Premium ) of the Strike Specified.

SH: Max Straddle Premium ( Increase in Premium ) since position is active.

SL: Min Straddle Premium ( Premium Erosion ) since position is active.

Theta Shield | Flux Charts💎 GENERAL OVERVIEW

Introducing our new Theta Shield indicator! Theta is the options risk factor concerning how fast there is a decline in the value of an option over time. This indicator aims to help the trader avoid sideways market phases in the current ticker, to minimize the risk of theta decay. For more information, please check the "How Does It Work" section.

Features of the new Theta Shield Indicator :

Foresight Of Accumulation Zones

Decrease Risk Of Theta Decay

Clear "Valid" & "Non-Valid" Signals

Validness Trail

Alerts

📌 HOW DOES IT WORK ?

In options trading, theta is defined as the rate of decline in the value of an option due to the passage of time. Traders want to avoid this kind of decay in the value of an option. One of the best ways to avoid it is not holding an option contract when the market is going sideways. This indicator uses a stochastic oscillator to try to get a foresight of sideways markets, warning the trader to not hold an option contract while the price is in a range.

The indicator starts by calculating the stochastic value using close, high & low prices of the candlesticks. Then a stoch threshold & a theta length are determined depending on the option contract type defined by the user in the settings of the indicator. Each candlestick that falls above or below the stoch threshold value is counted, and a "theta valid strength" is calculated using the counted candlesticks, which has a value between -100 & 100. Here is the formula of the "theta valid strength" value :

f_lin_interpolate(float x0, float x1, float y0, float y1, float x) =>

y0 + (x - x0) * (y1 - y0) / (x1 - x0)

thetaValid = Total Candlesticks That Fall Above & Below The Threshold In Last "Theta Length" bars.

thetaValidStrength = f_lin_interpolate(0, thetaLength, -100, 100, thetaValid)

Then a trail is rendered, and "Valid" & "Non-Valid" signals are given using this freshly calculated strength value. Valid means that the indicator currently thinks that no accumulation will happen in the near future, so the option positions in the current ticker are protected from the theta decay. Non-Valid means that the indicator thinks the ticker has entered the accumulation phase, so holding any option position is not recommended, as they may be affected by the theta decay.

🚩 UNIQUENESS

This indicator offers a unique way to avoid theta decay in options trading. It uses a stochastic oscillator and thresholds to calculate a "theta strength" value, which is used for rendering validness signals and a trail. Traders can follow the valid & non-valid signals when deciding to hold their options position or not. The indicator also has an alerts feature, so you can get notified when a ticker is about to enter a range, or when it's about to get out of it.

⚙️ SETTINGS

1. General Configuration

Contract Type -> You can set the option contract type here. The indicator will adjust itself to get a better foresight depending on the contract length.

2. Style

Fill Validness -> Will render a trail based on "theta strength" value.

[1] Dynamic Support and Resistance with breakout [Dr Future]This script appears to be designed to identify and visualize dynamic support and resistance levels on a price chart, along with potential breakout signals.

Key Components & Functionality (Inferred):

Dynamic Support and Resistance: The script likely employs algorithms to calculate and plot support and resistance levels that adjust in real-time as price action evolves.

Breakout Detection: The script probably incorporates logic to recognize when the price breaks out of these dynamic support or resistance zones. This could trigger alerts or visual cues on the chart.

Dr Future's Approach: It's worth noting the " " tag, suggesting the script might be based on specific methodologies or insights associated with a trader or analyst known as "Dr Future." Without more context on their strategies, it's difficult to pinpoint the exact techniques used.

Potential Benefits:

Adaptive Levels: Dynamic support and resistance can offer a more responsive approach compared to static levels, as they account for changing market conditions.

Breakout Opportunities: Identifying breakouts can help traders spot potential entry or exit points.

Visual Clarity: Plotting these levels directly on the chart can provide a clearer picture of the current market structure and potential turning points.

Caveats:

False Signals: Like any technical tool, dynamic support and resistance can generate false signals. Breakouts might not always lead to sustained trends.

Parameter Sensitivity: The script's effectiveness likely depends on how its parameters are configured. Fine-tuning might be required to suit different markets or timeframes.

"Dr Future" Factor: The script's performance could be tied to the specific strategies of "Dr Future," which might not be universally applicable.

Important Note:

Without access to the actual code and a deeper understanding of "Dr Future's" methods, this description is based on inference and general knowledge of technical analysis.

Recommendation:

If you're considering using this script, it would be prudent to:

Backtest Thoroughly: Test the script on historical data to assess its performance and identify potential pitfalls.

Understand the Parameters: Familiarize yourself with the script's settings and how they impact the plotted levels and breakout signals.

Combine with Other Tools: Use this script in conjunction with other technical indicators and risk management strategies for a more holistic trading approach.

BetaBeta , also known as the Beta coefficient, is a measure that compares the volatility of an individual underlying or portfolio to the volatility of the entire market, typically represented by a market index like the S&P 500 or an investible product such as the SPY ETF (SPDR S&P 500 ETF Trust). A Beta value provides insight into how an asset's returns are expected to respond to market swings.

Interpretation of Beta Values

Beta = 1: The asset's volatility is in line with the market. If the market rises or falls, the asset is expected to move correspondingly.

Beta > 1: The asset is more volatile than the market. If the market rises or falls, the asset's price is expected to rise or fall more significantly.

Beta < 1 but > 0: The asset is less volatile than the market. It still moves in the same direction as the market but with less magnitude.

Beta = 0: The asset's returns are not correlated with the market's returns.

Beta < 0: The asset moves in the opposite direction to the market.

Example

A beta of 1.20 relative to the S&P 500 Index or SPY implies that if the S&P's return increases by 1%, the portfolio is expected to increase by 12.0%.

A beta of -0.10 relative to the S&P 500 Index or SPY implies that if the S&P's return increases by 1%, the portfolio is expected to decrease by 0.1%. In practical terms, this implies that the portfolio is expected to be predominantly 'market neutral' .

Calculation & Default Values

The Beta of an asset is calculated by dividing the covariance of the asset's returns with the market's returns by the variance of the market's returns over a certain period (standard period: 1 years, 250 trading days). Hint: It's noteworthy to mention that Beta can also be derived through linear regression analysis, although this technique is not employed in this Beta Indicator.

Formula: Beta = Covariance(Asset Returns, Market Returns) / Variance(Market Returns)

Reference Market: Essentially any reference market index or product can be used. The default reference is the SPY (SPDR S&P 500 ETF Trust), primarily due to its investable nature and broad representation of the market. However, it's crucial to note that Beta can also be calculated by comparing specific underlyings, such as two different stocks or commodities, instead of comparing an asset to the broader market. This flexibility allows for a more tailored analysis of volatility and correlation, depending on the user's specific trading or investment focus.

Look-back Period: The standard look-back period is typically 1-5 years (250-1250 trading days), but this can be adjusted based on the user's preference and the specifics of the trading strategy. For robust estimations, use at least 250 trading days.

Option Delta: An optional feature in the Beta Indicator is the ability to select a specific Delta value if options are written on the underlying asset with Deltas less than 1, providing an estimation of the beta-weighted delta of the position. It involves multiplying the beta of the underlying asset by the delta of the option. This addition allows for a more precise assessment of the underlying asset's correspondence with the overall market in case you are an options trader. The default Delta value is set to 1, representing scenarios where no options on the underlying asset are being analyzed. This default setting aligns with analyzing the direct relationship between the asset itself and the market, without the layer of complexity introduced by options.

Calculation: Simple or Log Returns: In the calculation of Beta, users have the option to choose between using simple returns or log returns for both the asset and the market. The default setting is 'Simple Returns'.

Advantages of Using Beta

Risk Management: Beta provides a clear metric for understanding and managing the risk of a portfolio in relation to market movements.

Portfolio Diversification: By knowing the beta of various assets, investors can create a balanced portfolio that aligns with their risk tolerance and investment goals.

Performance Benchmarking: Beta allows investors to compare an asset's risk-adjusted performance against the market or other benchmarks.

Beta-Weighted Deltas for Options Traders

For options traders, understanding the beta-weighted delta is crucial. It involves multiplying the beta of the underlying asset by the delta of the option. This provides a more nuanced view of the option's risk relative to the overall market. However, it's important to note that the delta of an option is dynamic, changing with the asset's price, time to expiration, and other factors.

Options Price CalculatorIn the team, we continue to explore and expand the boundaries of TradingView.

For now, there is not much an options trader can do with options in TradingView.

We wanted to change that and created a simple option pricer.

You can set up in parameters a set of strikes, implied volatility, and days to expiry.

The indicators will take a risk-free rate from US01Y and the underlying price from your current chart.

It will compute prices and greeks for both put and call options.

Thanks to @MUQWISHI for helping code it.

Disclaimer

Please remember that past performance may not indicate future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

Implied and Historical Volatility v4There is a famous option strategy📊 played on volatility📈. Where people go short on volatility, generally, this strategy is used before any significant event or earnings release. The basic phenomenon is that the Implied Volatility shoots up before the event and drops after the event, while the volatility of the security does not increase in most of the scenarios. 💹

I have tried to create an Indicator using which you

can analyse the historical change in Implied Volatility Vs Historic Volatility.

To get a basic idea of how the security moved during different events.

Notes:

a) Implied Volatility is calculated using the bisection method and Black 76 model option pricing model.

b) For the risk-free rate I have fetched the price of the “10-Year Indian Government Bond” price and calculated its yield to be used as our Risk-Free rate.

5MSM MAHESH 15It´s just the histogram of the MACD . (Actually it´s not a histogram, I like the Area visualisation more. But you can switch.)

5min stock market property

When I´m using the MACD , I´m just searching for a divergence between Price and the MACD-histogram. I´m not interested in the MACD-signalline or the MACD-line in any way. As you can see, The omission of them leads to better visualisation. It´s much easier to spot a divergence. On the one hand because that way the histogram scales bigger, on the other hand becauce the lines can´t overdraw the histogram.

Rules bullish Divergence: Price makes a lower low, oscillator makes higher low.

Rules bearish Divergence: Price makes a higher high, oscillator makes lower high.

Price Pivots for NASDQ 100 StocksPrice Pivots for NASDQ 100 Stocks

What is this Indicator?

• This indicator calculates the price range a Stock can move in a Day.

Advantages of this Indicator

• This is a Leading indicator, not Dynamic or Repaint.

• Helps to identify the tight range of price movement.

• Can easily identify the Options strike price.

• Develops a discipline in placing Targets.

Disadvantages of this Indicator

• The indicator is specifically made for NASDQ 100 stocks. The levels won't work for other stocks.

• The indicator shows nothing for other indexes and stocks other than above mentioned.

• The data need to be entered manually.

Who to use?

Highly beneficial for Day Traders, it can be used for Swing and Positions as well.

What timeframe to use?

• Any timeframe.

• The highlighted levels in Red and Green will not show correct levels in 1 minute timeframe.

• 5min is recommended for Day Traders.

When to use?

• Wait for proper swing to form.

• Recommended to avoid 1st 1 hour or market open, that is 9.15am to 10.15 or 10.30am.

• Within this time a proper swing will be formed.

What are the Lines?

• The concept is the price will move from one pivot to another.

• Entry and Exit can be these levels as Reversal or Retracement.

Gray Lines:

• Every lines with price labels are the Strike Prices in the Option Chain.

• Price moves from 1 Strike Price level to another.

• The dashed lines are average levels of 2 Strike Prices.

Red & Green Lines:

• The Red and Green Lines will appear only after the first 1 hour.

• The levels are calculated based on the 1st 1 hour.

• Red Lines are important Resistance levels, these are strong Bearish reversal points. It is also a breakout level, this need to be figured out from the past levels, trend, percentage change and consolidation.

• Green Lines are important Support levels, these are strong Bullish reversal points. It is also a breakdown level, this need to be figured out from the past levels, trend, percentage change and consolidation.

What are the Labels?

• First Number: Price of that level.

• Numbers in (): Percentage change and Change of price from LTP (Last Traded Price) to that Level.

How to use?

Entry:

• Enter when price is closer to the Red or Green lines.

• Enter after considering previous Swing and Trend.

• Note the 50% of previous Swing.

• Enter Short when price reverse from each level.

• If 50% of swing and the pivot level is closer it can be a good entry.

Exit:

• Use the logic of Entry, each level can be a target.

• Exit when price is closer to the Red or Green lines.

Indicator Menu

Source

• Custom: Enter the price manually after choosing the Source as Custom to show the Pivots at that price.

• LTP: Pivot is calculated based on Last Traded Price.

• Day Open: Pivot is calculated based on current day opening price.

• PD Close: Pivot is calculated based on previous day closing price.

• PD HL2: Pivot is calculated based on previous day average of High and Low.

• PD HLC3: Pivot is calculated based on previous day average of High, Low and Close.

"Time (Vertical Lines)"

• This is a marker of every 1 hour.

• Usually major price movement happen between previous day last 1 hour to today first 1 hour.

• Two swings can happen between first 2 hour of current day.

• At the end of the day last 1 hour another important movement will happen.

• Usually rest of the time won't show any interesting movement.

To the Users

• Certain symbols may show the levels as a single line. For such symbols choose a different Source or Timeframe from the indicator menu.

• Please inform if any of the Symbol's price levels don't react to the pivots , include the Symbol a well.

• Also inform if you notice any wrong values, errors or abnormal behavior in the indicator.

• Feel free to suggest or adding new features and options.

General Tips

• It is good if Stock trend is same as that of Index trend.

• Lots of indicators creates lots of confusion.

• Keep the chart simple and clean.

• Buy Low and Sell High.

• Master averages or 50%.

• Previous Swing High and Swing Low are crucial.

Important Note

• Currently the levels are in testing stage.

• Eventually the levels of certain symbols will be corrected after each update and test.