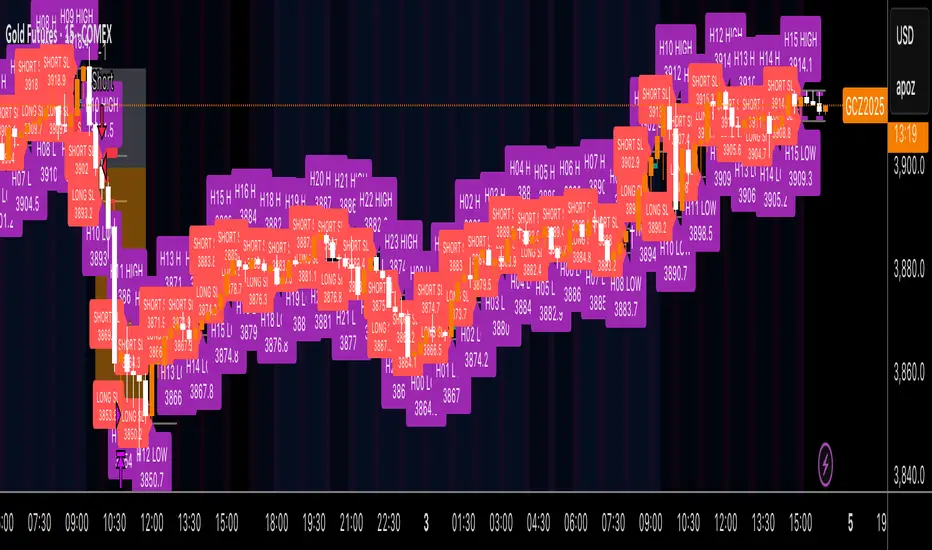

Kz GC1! ORBStrategy that trades breakouts on GC1! futures on the 5min timeframe. It also works on MGC1! for lower drawdown and to manage Apex and Top Step accounts with the lower risk.

Risk Disclaimer:

Past results as well as strategy tester reports do not indicate future performance. Guarantees do not exist in trading. By using this strategy you risk losing all your money.

Important:

It trades all days that markets are open. Set times may be seen on settings. Trades multiple times a day sometimes.

It works on the 5 and 15min timeframe only. Results are better on 5min timeframe.

The settings are optimized already for GC1! on the 5min timeframe.

How it works:

Every trading day it measures the range of the first 15min candle of pre-selected hours. As soon as price closes above or below on the 15min timeframe, it will trade the breakout targeting a set risk to reward ratio. SL on the opposite side of the range.

Settings:

Hourly Trading Hours: These are the times that worked best for this strategy. All boxes should be checked for best results. Excluded times were when it performed bad which is why those times have been left out.

ORB Formation Period: This setting determines on which timeframe candle has to close outside the opening range box in order to take a trade. It's set to 15min by default because this is what worked by far the best

Entry Type: Entries are immediate instead of waiting for a pull back to enter on a limit order.

Limit Orders: If enabled, the strategy will place a pending order x points from the current price, instead of a market order. Immediate orders are enabled by default for a better performance. Important: It doesn't actually place a limit order. The strategy will just wait for a pullback and then enter with a market order. It's more like a hidden limit order.

Limit Order Offset Points: If you have limit orders enabled, this setting determines how many points from the current price the limit order will be placed.

FVG Detection Type: How fast it detects the fair value gaps. Standard detection over immediate had better performance

Risk Type: You can chose either between Fixed USD Amount, Risk per Trade in % or Fixed Contract Size. By default it's set to fixed contract size.

Risk Amount (USD or Contracts): This setting is to set how many USD or how many contracts you want to risk per trade. Make sure to check which risk type you have selected before you choose the risk amount.

Take Profit Multiplier: This is simply the total SL size in points multiplied by x.

Example: If you put 2, you get a 2:1 Risk to Reward Ratio. By Default it's set to 2.5 because this gave the best results in backtests.

Stop Loss Padding: This is simply the buffer in points that is added to the SL for safety reasons. If you have it on 0, the SL will be at the exact price of the opposite side of the range. By default it's set to 5 because this is what delivered the best results in backtests.

Stop Loss Placement: This determines where the stop loss gets placed for the order. It has been set to ORB Range by default as this delivered the best results.

Max Trades Per Hour: This allows the user to decide how many trades are taken an hour. 1 is been set to default for best results

Visual Settings: Check boxes to show orb range, FVG's, Entry points, and trade visualization boxes.

Backtest Settings:

For the backtest the commissions were set to 1.29USD per contract and .35USD for micros which is the highest amount Tradovate charges Margin was not accounted for because typically on prop accounts you can use way more contracts than you need for the extremely low max drawdown. Margin would be important on personal accounts but even there typically it's not an issue at all especially because this strategy runs on the 15min timeframe so it won't use a lot of contracts anyways.

Why the source code is hidden:

The source code is hidden because I invested a lot of time and money into developing this strategy and optimizing it with paid 3rd party software.

Pine實用程式

KD The ScalperWe have to take the trade when all three EMAs are pointing in the same direction (no criss-cross, no up/down, sideways). All 3 EMAs should be cleanly separated from each other with strong spacing between them; they are not tangled, sideways, or messy. This is our first filter before entering the trade. Are the EMAs stacked neatly, and is the price outside of the 25 EMA? If price pulls back and closes near or below the 25 or 50 EMA and breaks the 100 EMA, we don't trade. Use the 100 EMA as a safety net and refrain from trading if the price touches or falls below the 100 EMA.

1. Confirm the trend- All 3 EMAs must align, and they must spread

2. Watch price pull back to the 25th or the 50 EMA

3. Wait for the price to bounce - And re-approach the 25 EMA

Why is this powerful?

Removes 80% of the low-probability Trades

It keeps you out of choppy markets

Avoids Reversal Traps

Anchors us to momentum

We take the entry when the price moves up again and touches the 25 EMA from below, and then when it breaks above the 25 EMA, or even better, when a lovely green bullish candle forms. A bullish candle indicates good momentum. When a bullish candle closes in green, it means the momentum has increased significantly. This is when we enter a long trade, with the stop-loss just below the 50 EMA and the profit target being 1.5 times the stop-loss.

The same rule applies to the bearish trade.

MOHStrategy Description

Uses Heikin Ashi candles to filter market noise and identify trend direction.

Entry is allowed only when strong HA candles appear (bullish without lower wick, bearish without upper wick).

Doji candles signal possible reversal.

استخدام شموع Heikin Ashi لتقليل الضوضاء وتحديد اتجاه الترند.

الدخول فقط عند ظهور شموع قوية (صاعدة بدون ذيل سفلي، هابطة بدون ذيل علوي).

شمعة الدوجي = إشارة انعكاس محتملة.

SMA Cross 5/50 with Trend Filter & Risk Management by JuggiDThe basic SMA (5/50) crossover strategy can be enhanced to improve profitability by adding filters and risk management. For example, a long entry is triggered only when the fast SMA (5) crosses above the slow SMA (50) **and** the price is above the SMA (200), ensuring trades align with the major trend. Similarly, a short entry requires the crossover confirmation plus the price staying below the SMA (200). To reduce false signals and protect capital, stop-loss and take-profit levels can be set automatically (e.g., 2% loss, 5% gain), while additional confirmation tools such as volume spikes, RSI above 50, or MACD momentum can be applied to validate stronger signals. This approach helps avoid whipsaws in sideways markets and allows trades to capture larger moves while minimizing downside risk.

Trend Following S/R Fibonacci StrategyTrend Following S/R Fibonacci Strategy

Trend Following S/R Fibonacci Strategy

Universal Webhook Connector Demo.This strategy demonstrates how to generate JSON alerts from TradingView for multiple trading platforms.

Users can select platform_name (MT5, TradeLocker, DxTrade, cTrader, etc).

Alerts are constructed in JSON format for webhook execution.

Breakout + Volume + HH/LL (Clean labels TP1-3)Breakout + Volume + HH/LL Strategy (Clean Labels)

This strategy combines breakout confirmation, volume strength, and market structure (Higher Highs / Lower Lows) to identify high-probability trade setups.

Breakout Filter: Uses a Donchian channel to detect price breakouts above resistance or below support.

Volume Confirmation: Requires volume to exceed the moving average of volume by a chosen multiplier, filtering out weak or false breakouts.

Market Structure: Long trades are only allowed if a Higher High (HH) has formed, and short trades only if a Lower Low (LL) has formed.

Trade Execution Rules:

For BUY trades: Entry at breakout, stop loss (SL) below the last pivot low, and three take profits (TP1–TP3) based on configurable risk-reward ratios.

For SELL trades: Entry at breakout, stop loss above the last pivot high, with TP1–TP3 levels set symmetrically below the entry.

Labels on Chart:

Each signal is marked with a clean label showing only:

Trade direction (BUY or SELL)

Entry price

Stop Loss

TP1, TP2, TP3

This makes the chart uncluttered while still providing all key trade information for execution or backtesting.

Long-Only Trailing Stop Loss Strategy by Ravi PrasadSimple & Eligant way to make money. As the profit % increases, the trailing stop loss follows tightly !

RSI-MACD-trade"Strategic trading strategy using RSI and MASCD

Highest returns when applied to weekly charts"

US100 Liquidity Precision StrategyScalping strategy 5-10 point sl / 17 points tp

Automatic BE

Consistent money over time

Commander Sparks | 1:1 Daily Core (Prop-Mode Overnight)Features

Trend Filter: EMA50 > EMA200 (long bias), EMA50 < EMA200 (short bias).

VWAP Filter: Only buys above VWAP, sells below VWAP.

Bollinger Band Filter: Avoids chop — enters only when price is outside BB midline in trend direction.

MACD Momentum: Entry only when MACD line crosses signal line in trend direction.

Risk Control: ATR-based stop, exactly 1:1 target, fixed full exit.

Time Filter: Trades 24/5 — including overnight & Sunday reopen.

No pyramiding — 1 trade per signal.

Entries allowed: 6:00 PM → 3:55 PM ET (1800-1555)

Auto-flat: 3:55–4:00 PM ET (so you’re flat before the 4:00 PM cutoff)

Toggle Prop Mode OFF anytime to trade 24/5 with no time limits.

RSI-Adaptive T3 [ChartPrime] — Strategy (Long Only, 1D)This trade has been successfully converted from an individual setup to a full strategy, and the results are truly outstanding. I’m currently testing this for Tesla options trading on the 1-day chart, and it appears to be working extremely well.

A special thanks to ChartPrime for creating such a beautifully designed indicator — it’s performing impressively in these tests.

If anyone would like to try it out, feel free to download and see the results for yourself. Thank you!

VWAP-RSI Scalper FINAL v1Description

This script implements a robust, battle-tested intraday scalping strategy designed for prop firm challenges, funded trader programs, and serious futures scalpers.

It combines VWAP, RSI, EMA trend, and ATR-based risk management to capture high-probability mean reversion and momentum moves during the most liquid hours of the trading day.

Core Logic

RSI (Relative Strength Index):

Trades are triggered when the RSI is either oversold or overbought using a short lookback (default: 3). This ensures only the strongest intraday reversals or exhaustion moves are considered.

VWAP Filter:

Longs are only taken above VWAP, shorts only below VWAP, aligning trades with the session’s dominant bias.

EMA Filter:

Additional trend quality filter—longs require price above EMA, shorts below EMA.

Session Control:

Only trades between user-defined session hours (default: US cash session), eliminating overnight/illiquid action.

ATR-based Dynamic Stops & Targets:

Every trade uses a stop loss at 1x ATR and a take profit at 2x ATR for a positive risk/reward ratio.

Max Trades Per Day:

Prevents overtrading and controls risk exposure (default: 3).

Performance (Sample Backtest)

Profit Factor: 1.37+ (prop-firm quality)

Drawdown: <1% (very conservative risk)

Win Rate: 37–48% (RR > 1, so high edge)

Consistency: Smooth, steady equity curve over hundreds of trades.

Best For:

ES/NQ/CL/GC intraday traders

Prop firm evaluation challenges (Tradeify, Topstep, Apex, etc.)

Anyone needing robust, no-nonsense systematic edge for futures or indices.

How to Use & Tune

Apply to 3min, 5min, or 15min charts of liquid futures or indices.

Change parameters in the settings panel to suit your asset, volatility, or session hours.

Use “Strategy Tester” to validate P&L, win rate, and drawdown.

How to Optimize

Raise/lower RSI length or bands to make signals more/less frequent.

Adjust stop/target multiples for your preferred risk/reward profile.

Change session hours to match your broker or market.

Disclaimer

This is not financial advice. Use on a demo or sim account first. Results will vary by market, slippage, and execution speed. Past performance does not guarantee future results.

If you find this useful, please give it a like, follow for more strategies, and comment your results or questions!

Good luck and safe trading!

Inascript PRO (Elliott + TP System)Inascript PRO (Elliott + TP System) is an intraday strategy for gold (XAUUSD), based on simplified Elliott Wave logic.

It features 3 Take Profits, dynamic Stop Loss, break-even logic, and session filters (London & New York).

Precise alerts include entry, TP, and SL levels.

Developed by Inaskan for clean and smart intraday trading.

Backtest [OptAlgo]This backtest script is designed to convert ideas or indicators into backtest results. The script creates buy/sell signals by comparing price sources against fixed values or other imported plots using many comparison methods. It has many features including multiple exit systems: TP/SL, custom plot-based stops and more. It supports full trading automation through webhook alerts with live signal processing.

🔢 Signal Creation System

→ Values Group : Compare price sources against fixed numerical values

→ Plots Group : Compare two different price sources/indicators against each other

→ Flexible Comparisons : 15+ comparison methods (equal, crossover, rising...)

→ Signal Types : Long, Short, Close All, Block signals, and combination signals

→ Merge Rules : Minimum condition requirements for signal activation

🔀 Advanced Signal Logic

→ Counter Signals : Choose between reversing positions or closing them

→ Signal Inversion : Flip all buy/sell signals with one toggle

→ External Signal Import : Import coded signals (1=Long, -1=Short, 0=Close)

→ Day Blocker : Enable/disable trading on specific weekdays

→ Session Control : Limit trading to specific market sessions

⚙️ Strategy Settings

→ Position Sides : All Ways, Long Only, or Short Only modes

→ Signal Control : Individual enable/disable for long and short signals

→ Counter Signal Mode : Reverse Open Position vs Close Open Position

→ Signal Reversal : Global signal inversion capability

🔰 Risk Management (Limiter Settings)

→ Leverage Control : Leverage with liquidation warnings

→ Drawdown Limit : Auto-halt strategy at specified drawdown percentage

→ Tradable Ratio : Use portion of available balance (0.01-1.0)

→ Contract Limit : Cap maximum contract size regardless of balance

🎯 TP/SL System

→ Fixed TP/SL : Set percentage-based take profit and stop loss

→ Custom Plot Stops : Use any indicator/plot as dynamic stop loss

→ ATR-Based Exits : Volatility-adjusted TP/SL using Average True Range

→ Realistic Protection : Prevents unrealistic TP/SL prices in live trading

→ Stop Modes : Instant (Sudden) vs Candle Close execution

→ ATR Stop Loss : Override fixed SL with volatility-based calculations

→ ATR Take Profit : Dynamic TP based on market volatility

→ Trailing Options : Safe, Normal, or Aggressive trailing methods

→ Calculation Modes : Normal, Volume-weighted, or Limited (with max %) options

→ Volume Integration : ATR levels adjust based on volume influx

🤖 Automation & Alerts

→ Webhook Integration : Send JSON alerts for automated execution

→ Live Signals : Real-time signal processing (every tick vs bar close)

→ Strategy Key : Unique identifier for automated systems

→ Early Entry : Send alerts X seconds before candle close

→ Fast Execution : Prevent signal lag in automated trading

🐞 Development Tools

→ Alert Plotting : Visualize signals directly on chart (disable for live alerts)

→ Professional Mode : Remove UI controls for faster calculation

→ Debug : Metrics are plotted in data window.

📊 Key Advantages

→ Multi-Condition Logic : Combine multiple indicators with flexible rules

→ Risk-First Design : Built-in drawdown and leverage protection

→ Automation Ready : Full webhook and alert system integration

⚠️ Important Warnings

→ High leverage combined with high SL may adjust to liquidation price

→ Use consistent leverage across all strategies on same trading isolated margin pair

→ Live signals require "Calculate on every tick" enabled in settings

→ Disable alert plotting when creating actual alerts to prevent latency

Test Bot: Bearish Buy / Bullish SellFor testing the connection between TradingView and your brokerage. Use with a demo account if possible.

Modular Range-Trading Strategy (V9.2)# 模块化震荡行情策略 (V9.2)

# Modular Range-Trading Strategy (V9.2)

## 策略简介 | Strategy Overview

该策略基于布林带 (Bollinger Bands)、RSI、MACD、ADX 等经典指标的组合,通过多逻辑模块化结构识别震荡区间的价格反转机会,支持多空双向操作,并在相同逻辑下允许智能加仓,适用于震荡市场的回测和研究。

This strategy combines classic indicators such as Bollinger Bands, RSI, MACD, and ADX to identify price reversal opportunities within ranging markets. It features a modular multi-logic structure, allowing both long and short trades with intelligent pyramiding under the same logic. It is designed for backtesting and research in range-bound conditions.

---

## 功能特点 | Key Features

- **多逻辑结构**:支持多套震荡逻辑(动能确认均值回归、布林带极限反转等)。

- **加仓与仓位互斥**:同逻辑下可智能加仓,不同逻辑间自动互斥,避免冲突。

- **回测可调时间范围**:可自定义回测起止时间,精准评估策略表现。

- **指标可视化**:布林带、RSI、MACD 及动态 ATR 止损线实时绘图。

- **K线收盘确认信号**:通过 `barstate.isconfirmed` 控制信号,避免未收盘的虚假信号。

- **Multi-logic structure**: Supports multiple range-trading logics (e.g., momentum-based mean reversion, Bollinger Band reversals).

- **Pyramiding with mutual exclusion**: Allows intelligent pyramiding within the same logic while preventing conflicts between different logics.

- **Adjustable backtesting range**: Customizable start and end dates for accurate performance evaluation.

- **Visual indicators**: Real-time plotting of Bollinger Bands, RSI, MACD, and dynamic ATR stop lines.

- **Close-bar confirmation**: Uses `barstate.isconfirmed` to avoid false signals before bar close.

---

## 使用说明 | Usage

1. 将该脚本添加到 TradingView 图表。

2. 在参数中设置回测时间段和指标参数。

3. 仅用于学习与策略研究,请勿直接用于实盘交易。

1. Add this script to your TradingView chart.

2. Configure backtesting dates and indicator parameters as needed.

3. For educational and research purposes only. **Not for live trading.**

---

## ⚠️ 免责声明 | Disclaimer

本策略仅供学习和研究使用,不构成任何形式的投资建议。

作者不参与任何实盘交易、资金管理或收益分成,也不保证策略盈利能力。

严禁将本脚本用于任何非法集资、私募募资或与虚拟货币相关的金融违法活动。

使用本策略即表示您自行承担所有风险与法律责任。

This strategy is for educational and research purposes only and does not constitute investment advice.

The author does not participate in live trading, asset management, or profit sharing, nor guarantee profitability.

The use of this script in illegal fundraising, private placements, or cryptocurrency-related financial activities is strictly prohibited.

By using this strategy, you accept all risks and legal responsibilities.

---

Breackout V8 MomentumBreakout V6 Strategy with Fibonacci TPs

Description

Developed by Coton, this automated trading tool is designed to identify and capitalize on breakouts from consolidation zones, supported by momentum indicators. It leverages technical indicators to detect significant price movements and enters positions with take-profits based on Fibonacci levels and a trailing stop to protect profits. Optimized for crypto trading , it operates in Scalping (1m) or Intraday (5m) modes.

Indicators Used

Volatility Bands : Identify price compression and expansion zones to detect consolidations and breakouts.

Momentum Indicators : Measure the strength and direction of price movements to confirm breakouts.

Volume Indicators : Validate breakouts with significant increases in trading activity.

Dynamic Levels : Define entry and exit points based on adaptive calculations.

Features

Breakout Detection : Identifies exits from consolidation zones with quality filters.

Fibonacci Take-Profits : Profit targets calculated using extension levels to maximize gains.

Trailing Stop : Protects profits by dynamically adjusting the stop-loss based on volatility.

Visualization : Displays consolidation zones, entry levels, stop-losses, and take-profits on the chart.

Alerts : Notifications for confirmed and ongoing breakouts with a minimum risk/reward ratio.

Table : Shows the strategy status and estimated leverage in real-time.

Input Parameters

Trading Mode: Scalping (1m) or Intraday (5m) (default: Intraday)

Fibonacci Level for TP: 1.618 (adjustable 0.5-5.0)

Minimum RR for Alerts: 1.2 (filters alerts)

Alerts

Confirmed Breakout (validated movement with quality criteria).

Ongoing Breakout (tracked with minimum risk/reward ratio, every 5 candles).

Disclaimers

Not financial advice; test in demo mode.

Past performance is not indicative of future results.

High risk in crypto trading; use proper risk management (1-2% per trade).

Commission (0.1%) may impact results; adjust for your broker.

Contact

Coton for questions or improvements.

Trading Report Generator from CSVMany people use the Trading Panel. Unfortunately, it doesn't have a Performance Report. However, TradingView has strategies, and they have a Performance Report :-D

What if we combine the first and second? It's easy!

This script is a special strategy that parses transactions in csv format from Paper Trading (and it will also work for other brokers) and “plays” them. As a result, we get a Performance Report for a specific instrument based on our real trades in Paper or another broker.

How to use it :

First, we need to get a CSV file with transactions. To do this, go to the Trading Panel and connect the desired broker. Select the History tab, then the Filled sub-tab, and configure the columns there, leaving only: Side, Qty, Fill Price, Closing Time. After that, open the Export data dialog, select History, and click Export. Open the downloaded CSV file in a regular text editor (Notepad or similar). It will contain a text like this:

Symbol,Side,Qty,Fill Price,Closing Time

FX:EURUSD,Buy,1000,1.0938700000000001,2023-04-05 14:29:23

COINBASE:ETHUSD,Sell,1,1332.05,2023-01-11 17:41:33

CME_MINI:ESH2023,Sell,1,3961.75,2023-01-11 17:30:40

CME_MINI:ESH2023,Buy,1,3956.75,2023-01-11 17:08:53

Next select all the text (Ctrl+A) and copy it to the clipboard.

Now apply the "Trading Report Generator from CSV" strategy to the chart with the desired symbol and TF, open the settings/input dialog, paste the contents of the clipboard into the single text input field of the strategy, and click Ok.

That's it.

In the Strategy Tester, we see a detailed Performance Report based on our real transactions.

P.S. The CSV file may contain transactions for different instruments, for example, you may have transactions for CRYPTO:BTCUSD and NASDAQ:AAPL. To view the report is based on CRYPTO:BTCUSD trades, simply change the symbol on the chart to CRYPTO:BTCUSD. To view the report is based on NASDAQ:AAPL trades, simply change the symbol on the chart to NASDAQ:AAPL. No changes to the strategy are required.

How it works :

At the beginning of the calculation, we parse the csv once, create trade objects (Trade) and sort them in chronological order. Next, on each bar, we check whether we have trades for the time period of the next bar. If there are, we place a limit order for each trade, with limit price == Fill Price of the trade. Here, we assume that if the trade is real, its execution price will be within the bar range, and the Pine strategy engine will execute this order at the specified limit price.

MÈGAS ALGO : MÈGAS Engine [STRATEGY]Overview

The MÈGAS Engine is an advanced algorithmic trading system that integrates a range of technical analysis tools to pinpoint high-probability opportunities in the market.

Key Features

Core Signal Generation:

-Structure Break Detection: Advanced breakout identification with adjustable

sensitivity controls

-Dual-Direction Analysis: Separate bullish and bearish signal parameters with customizable delta

thresholds and depth settings

-Dynamic Parameter Management: OverfitShield technology with pulsewave parameter cycling

to reduce overfitting risks

Filtering Alghoritm:

-Volatility Filter: Rogers-Satchell volatility estimation with RSI-based normalization to avoid

trading in unfavorable market conditions

-Volume Confirmation: Cumulative volume analysis ensuring adequate liquidity support for trade

entries

OverfitShield Method:

OverfitShield is a built-in function within the trading strategy designed to reduce overfitting bias by introducing parameter variability during execution. When the "variable" mode is activated, instead of relying on fixed values for key strategy parameters the system dynamically selects values from customizable ranges.

This approach mimics real-world market uncertainty and ensures that the strategy does not become overly dependent on a single optimal value found during backtesting — making it more robust across different market conditions and time periods.

Position Management

-Customizable Exit Set-up

The exit logic can be customized to 'CONTINUE', 'TAKE PROFIT', or 'TRAILING PROFIT' to suit

your trading approach and maximize performance.

-CONTINUE Mode:

This mode does not use predefined take profit levels. Instead, it remains in the market as long as the trend persists. By avoiding fixed exit points, this approach is often the most effective in backtesting, as it allows positions to run in favorable trends for longer periods.

-TAKE PROFIT Mode:

This mode allows you to set multiple grid-like take profit levels at different price points, effectively creating a multi-tier exit strategy. You can specify the number of profit levels you want, along with the percentage step between each level. This structured approach can be beneficial for capturing incremental profits in a trending market while allowing for more flexibility in trade management.

-TRAILING PROFIT Mode:

Similar to the Take Profit mode, this option allows you to set the trailing stop levels. The trailing stop moves with the market, ensuring that you lock in profits as the price continues to move in your favor. Once a profit level is hit, the trailing stop "follows" the price movement, adjusting dynamically to safeguard profits as the trade progresses.

3. Customizable Insight Alerts

Traders can configure personalized alert messages for every strategy action, including entries, exits, and profit targets. These alerts are fully compatible with TradingView's webhook system.

Advantages

Customization: Fully customizable exit set-up and alerts allow traders to tailor the strategy to their personal trading objectives.

How It Works — Step by Step

Step 1: Apply the Strategy

Open the chart for your selected symbol and timeframe. Add the MÈGAS Engine to the chart.

Step 2:Backtesting and Optimization

Run a full backtest and optimize the strategy parameters across the chosen trading pairs to:

Identify robust settings that perform consistently well

Avoid overfitting through validation techniques

Select the most profitable and stable configuration for live or forward testing.

Step 3: Review Results and Alerts

Check the backtest results on the chart and confirm that the custom alert messages are displaying as expected. This helps verify that everything is functioning correctly before moving forward.

Step 4: Configure Portfolio Management

Set up the exit logic based on your specific requirements. Tailor the exit strategy to match your trading approach, whether you prefer predefined take profit levels, trailing stops, or a trend-following method. This flexibility ensures the exit logic aligns with your overall strategy for optimal performance.

Open the strategy settings window. In the dedicated portfolio management section, choose your preferred capital allocation method based on your trading style and risk preferences. Once set, save the configuration as the default.

Step 5: Set Up Alerts

Click "Add Alert" on the strategy

-In the message field, use: {{strategy.order.comment}}

Under the Notifications tab:

-Enable Webhook URL

-Enter your external webhook address

-Click 'Create' to activate alerts for your strategy

Please Note:

The results and visualizations presented are derived from optimized backtesting iterations using historical and paid real-time market data sourced via TradingView. While these results are intended to demonstrate potential performance, they do not guarantee future outcomes or accuracy. Past performance is not indicative of future results, and all trading involves risk.

We strongly recommend that users review and adjust the Properties within the script settings to align with their specific account configurations and preferred trading platforms. This ensures that the strategy outputs are reflective of real-world conditions and enhances the reliability of the results obtained. Use this tool responsibly and at your own risk.

Cyber Strategy V1Сyber Strategy V1 – Indicator Testing & Strategy Execution Framework

✅ Overview

Cyber Strategy V1 is a closed-source strategy framework engineered to turn any of yours external indicator into a systematic, rule-based trading system. Designed for rigorous testing and live deployment, it combines multi-signal inputs, confirmations and automated execution paths to help traders and developers validate signal quality and manage risk with precision.

✅ Core Functionality

Multi-Source Independent Signal Inputs

Reversal Logic

Take Profit: up to 5 staggered TP levels, specified as percentage

Stop Loss: configurable via fixed percentage or dynamic SL that trails a reverse signals.

✅ Statistical Drawdown Analysis

For all profitable trades, tracks the maximum intratrade drawdown.

Computes percentile levels of profitable trades that hits minimum drawdowns to inform:

Entry buffer zones (e.g. avoid entering during transient noise)

Partial entry scaling prices.

✅ Signal Confirmation

Optional confirmation delays: hold entry until other signal section send a confirmation from another indicator.

✅ Automated Execution Integrations

Cornix Text Alerts: Generates pre-formatted alerts compatible with Cornix for semi-automated or bot trading.

Webhook Support: Emits JSON payloads on order-fill events to any endpoint, enabling full automation through third-party services or custom order-routing systems.

Important Notes

⚠️ THIS STRATEGY DOES NOT INCLUDE INDICATORS. Examples shown on screenshots use third-party tools. NO PROPRIETARY INDICATORS INCLUDED: Cyber Strategy V1 relies entirely on external signal inputs.

⚠️ All backtesting parameters are customizable; thorough backtesting under realistic slippage, fees and spread assumptions is essential before live deployment.