Average Candle RangeThis indicator calculates and displays the average trading range of candles over a specified period, helping traders identify volatility patterns and potential trading opportunities.

Features:

- Customizable lookback period (1-500 bars)

- Clean visual display in a top-right table overlay

- High-precision calculation showing 10 decimal places

- Real-time updates with each new bar

How it Works:

The indicator calculates the range of each candle (High - Low) and then computes the Simple Moving Average (SMA) of these ranges over your specified lookback period. The result is displayed in an easy-to-read table overlay.

Use Cases:

- Volatility Analysis: Monitor market volatility trends

- Position Sizing: Help determine position sizes based on average price movements

- Trading Strategy Development: Use as a reference for setting stop losses and take profits

- Market Phase Identification: Help identify high vs low volatility market phases

Settings:

- Lookback Period: Default is 140 bars, adjustable from 1 to 500

Note:

The indicator displays values with 10 decimal places for high-precision analysis, particularly useful in markets with small price movements.

在腳本中搜尋"乌德勒支+VS+赫拉克勒斯"

Exponential Avg Body Size Green vs RedDescription :

This indicator calculates and plots the Exponential Moving Average (EMA) of green and red candlestick body sizes, allowing traders to easily visualize market momentum and sentiment shifts. The script includes the following features:

Customizable EMA Period: Users can set the number of candles to calculate the EMA through an input setting, with a default value of 21.

Separate Green and Red Candle Averages: Differentiates between bullish (green) and bearish (red) candlestick movements, plotting them as distinct lines.

Dynamic Range Control: Users can adjust the chart range (e.g., -50 to 50) for better visibility of the plotted lines.

Baseline for Reference: A horizontal baseline at 0 serves as a visual aid for easier interpretation.

Standalone Indicator Pane: The script is designed to display in a separate pane, preventing overlap with the price chart.

Use Case:

This indicator is ideal for traders seeking to analyze the relative strength of bullish versus bearish price movements over a specific period. The separation of green and red averages helps identify trends, potential reversals, or shifts in momentum.

Enhanced Effort vs Result Analysis V.2How to Use in Trading

A. Confirm Breakouts

Check if the Effort-Result Ratio or Z-Score spikes above the Upper Band or Z > +2:

Suggests a strong, efficient price move.

Supports breakout continuation.

B. Identify Reversal or Exhaustion

Look for Effort-Result Ratio or Z-Score dropping below the Lower Band or Z < -2:

Indicates high effort but low price movement (inefficiency).

Often signals potential trend reversal or consolidation.

C. Assess Efficiency of Trends

Use Relative Efficiency Index (REI):

REI near 1 during a trend → Confirms strength (efficient movement).

REI near 0 → Weak or inefficient movement, likely signaling exhaustion.

D. Evaluate Volume-Price Relationship

Monitor the Volume-Price Correlation:

Positive correlation (+1): Confirms price is driven by volume.

Negative correlation (-1): Indicates divergence; price moves independently of volume (potential warning signal).

3. Example Scenarios

Scenario 1: Breakout Confirmation

Effort-Result Ratio spikes above the Upper Band.

Z-Score exceeds +2.

REI approaches 1.

Volume-Price Correlation is positive (near +1).

Action: Strong breakout confirmation → Trend continuation likely.

Scenario 2: Reversal or Exhaustion

Effort-Result Ratio drops below the Lower Band.

Z-Score is below -2.

REI approaches 0.

Volume-Price Correlation weakens or turns negative.

Action: Signals trend exhaustion → Watch for reversal or consolidation.

Scenario 3: Range-Bound Market

Effort-Result Ratio stays within the Bollinger Bands.

Z-Score remains between -1 and +1.

REI fluctuates around 0.5 (neutral efficiency).

Volume-Price Correlation hovers near 0.

Action: Normal conditions → Look for breakout signals before acting.

*IMPORTANT*

There is a problem with the overlay ... How to fix some of it

The Standard Deviation bands dont work while the other variable activated so Id suggest deselecting them. The fix for this is to make sure you have the background selected and by doing this it will highlight on the chart ( you may need to increase the opacity ) when the bands ( Second standard deviation) are touched.

- Also you can use them all at once if you can but you do not need to

G&S SMT### Description of the Pine Script

This Pine Script is designed to identify **Smart Money Technique (SMT)** setups between **Gold (GC1!)** and **Silver (SI1!) Futures** on a **15-minute timeframe**. It specifically looks for divergences between the price movements of Gold and Silver over the last 4 candles and compares it with the next candle's price movement. The script provides **Bullish** and **Bearish** signals for SMT during a specified time range of **8:45 AM EST to 10:30 AM EST**.

### Key Features of the Script:

1. **Futures Symbols**:

- The script uses **Gold Futures (GC1!)** and **Silver Futures (SI1!)** on a 15-minute timeframe to monitor their price movements.

2. **Time Range Filtering**:

- The signals are only active between **8:45 AM EST and 10:30 AM EST**, ensuring that the script only signals within the most relevant trading hours for your strategy.

3. **SMT Calculation (Last 4 Candles vs Next Candle)**:

- **Gold and Silver Price Change Calculation**: The script compares the price changes of **Gold** and **Silver** over the **last 4 candles** and then compares them with the price movement of the **next candle**:

- **Bullish SMT**: Occurs when Gold shows an increase in the last 4 candles while Silver shows a decrease, and both Gold and Silver show an increase in the next candle.

- **Bearish SMT**: Occurs when Gold shows a decrease in the last 4 candles while Silver shows an increase, and both Gold and Silver show a decrease in the next candle.

4. **Bullish and Bearish Signals**:

- **Bullish SMT Signal**: The script will plot a **green** arrow below the bar when a Bullish SMT setup is identified.

- **Bearish SMT Signal**: A **red** arrow above the bar is plotted when a Bearish SMT setup is identified.

5. **Gold and Silver Difference Plot**:

- The difference between the prices of **Gold** and **Silver** is plotted as a **blue line**, giving a visual representation of the relationship between the two assets. When the difference line moves significantly, it can indicate a potential divergence or convergence in the prices of Gold and Silver.

### Script Logic Breakdown:

1. **Price Change for Last 4 Candles**:

- The script calculates the price change for Gold and Silver from the 4th-to-last candle to the last candle.

- `gold_change_last4` and `silver_change_last4` calculate these price differences.

2. **Price Change for Next Candle**:

- It then calculates the price change from the last candle to the next candle.

- `gold_change_next` and `silver_change_next` calculate these price differences.

3. **Bullish SMT Condition**:

- If Gold increased while Silver decreased in the last 4 candles, and both Gold and Silver show an increase in the next candle, it indicates a **Bullish SMT**.

4. **Bearish SMT Condition**:

- If Gold decreased while Silver increased in the last 4 candles, and both Gold and Silver show a decrease in the next candle, it indicates a **Bearish SMT**.

5. **Time Filter**:

- Signals are only plotted when the current time is between **8:45 AM EST and 10:30 AM EST** to match your preferred trading hours.

### Visualization:

- **Bullish Signals**: Plotted as **green arrows** below the bars when a Bullish SMT setup is identified.

- **Bearish Signals**: Plotted as **red arrows** above the bars when a Bearish SMT setup is identified.

- **Gold - Silver Difference**: A **blue line** is plotted to show the price difference between Gold and Silver, helping visualize any divergence.

### How It Helps:

- **Divergence Identification**: This script highlights potential divergences between Gold and Silver Futures, which can provide insights into market sentiment and smart money movements.

- **Focus on Relevant Time Frame**: By filtering signals between 8:45 AM EST and 10:30 AM EST, you are focusing on a timeframe that can be more beneficial for trading.

- **Visual Clarity**: The arrows and the price difference line provide clear signals and a visual representation of the relationship between Gold and Silver, helping you make informed trading decisions.

This script is an automated approach to detecting **SMT setups** and helping traders recognize when Gold and Silver might be signaling a bullish or bearish move based on their divergence patterns.

Tomas Ratio Strategy with Multi-Timeframe AnalysisHello,

I would like to present my new indicator I have compiled together inspired by Calmar Ratio which is a ratio that measures gains vs losers but with a little twist.

Basically the idea is that if HLC3 is above HLC3 (or previous one) it will count as a gain and it will calculate the percentage of winners in last 720 hourly bars and then apply 168 hour standard deviation to the weekly average daily gains.

The idea is that you're supposed to buy if the thick blue line goes up and not buy if it goes down (signalized by the signal line). I liked that idea a lot, but I wanted to add an option to fire open and close signals. I have also added a logic that it not open more trades in relation the purple line which shows confidence in buying.

As input I recommend only adjusting the amount of points required to fire a signal. Note that the lower amount you put, the more open trades it will allow (and vice versa)

Feel free to remove that limiter if you want to. It works without it as well, this script is meant for inexperienced eye.

I will also publish a indicator script with this limiter removed and alerts added for you to test this strategy if you so choose to.

Also, I have added that the trades will enter only if price is above 720 period EMA

Disclaimer

This strategy is for educational purposes only and should not be considered financial advice. Always backtest thoroughly and adjust parameters based on your trading style and market conditions.

Made in collaboration with ChatGPT.

RSI Divergence - Left Candles Onlyrsi

The **RSI Divergence** indicator in this script is designed to highlight **divergence** between the **Relative Strength Index (RSI)** and **price action** on a chart. Divergence can be a key signal for potential trend reversals or continuation in technical analysis.

### **Key Components of the Indicator:**

1. **RSI Calculation:**

- The **Relative Strength Index (RSI)** is calculated using a typical 14-period length, but the user can customize this input.

- RSI is a momentum oscillator that measures the speed and change of price movements, oscillating between 0 and 100. Values above 70 indicate overbought conditions, and values below 30 indicate oversold conditions.

2. **Divergence Logic:**

- **Bullish Divergence:** Occurs when the price forms a **lower low**, but the RSI forms a **higher low**. This suggests that despite price continuing to drop, momentum (RSI) is strengthening, which may indicate a potential price reversal to the upside.

- **Bearish Divergence:** Occurs when the price forms a **higher high**, but the RSI forms a **lower high**. This indicates that even though price is rising, the momentum (RSI) is weakening, which could signal a price reversal to the downside.

3. **Pivot Identification:**

- The script identifies **pivot points** (local highs and lows) on both price and RSI.

- **Bullish Divergence:** A lower price low with a higher RSI low.

- **Bearish Divergence:** A higher price high with a lower RSI high.

4. **Lookback Periods:**

- **Lookback Left (lookbackLeft):** Defines the number of bars to look back for pivot confirmation. This allows for adjusting the sensitivity of the divergence.

- The **divergence range** is constrained by two parameters:

- **Minimum range (rangeLower):** The minimum number of bars for divergence to be considered.

- **Maximum range (rangeUpper):** The maximum number of bars for divergence to be considered.

5. **Signal Generation and Plotting:**

- When a **bullish divergence** is detected, a **green label** is plotted below the bar where the divergence occurs.

- When a **bearish divergence** is detected, a **red label** is plotted above the bar.

- The script uses **`plotshape()`** to plot these labels on the chart.

6. **Alerts:**

- Alerts are configured for both **bullish** and **bearish divergences** so that you can be notified when a divergence signal occurs.

---

### **How the Indicator Works:**

- The RSI and price action are compared using **pivots**: The script checks whether the price and RSI are forming new highs or lows within the specified **lookback period**.

- If the conditions for divergence (higher/lower RSI pivot vs price pivot) are met, a signal is plotted on the chart.

- The script helps to visually identify potential reversal points and allows users to set alerts for these divergence signals.

---

### **Use Case:**

- This script is useful for traders looking to trade potential trend reversals based on **divergence** between price and RSI.

- **Bullish divergence** can indicate a **buy** opportunity, while **bearish divergence** can suggest a **sell** opportunity.

- The indicator works best in **volatile markets** and when combined with other technical analysis tools for confirmatio

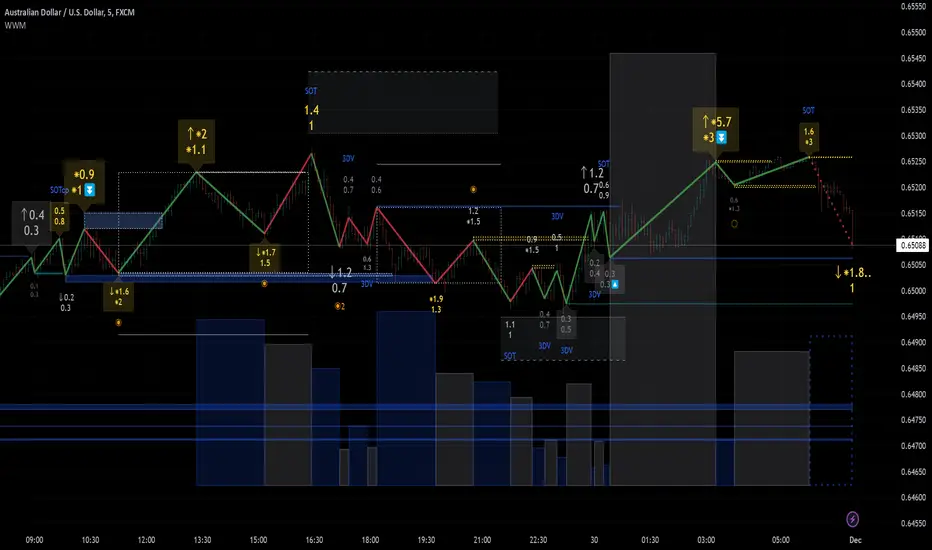

Weis Wave Max█ Overview

Weis Wave Max is the result of my weis wave study.

David Weis said,

"Trading with the Weis Wave involves changes in behavior associated with springs, upthrusts, tests of breakouts/breakdowns, and effort vs reward. The most common setup is the low-volume pullback after a bullish/bearish change in behavior."

THE STOCK MARKET UPDATE (February 24, 2013)

I inspired from his sentences and made this script.

Its Main feature is to identify the largest wave in Weis wave and advantageous trading opportunities.

█ Features

This indicator includes several features related to the Weis Wave Method.

They help you analyze which is more bullish or bearish.

Highlight Max Wave Value (single direction)

Highlight Abnormal Max Wave Value (both directions)

Support and Resistance zone

Signals and Setups

█ Usage

Weis wave indicator displays cumulative volume for each wave.

Wave volume is effective when analyzing volume from VSA (Volume Spread Analysis) perspective.

The basic idea of Weis wave is large wave volume hint trend direction. This helps identify proper entry point.

This indicator highlights max wave volume and displays the signal and then proper Risk Reward Ratio entry frame.

I defined Change in Behavior as max wave volume (single direction).

Pullback is next wave that does not exceed the starting point of CiB wave (LH sell entry, HL buy entry).

Change in Behavior Signal ○ appears when pullback is determined.

Change in Behavior Setup (Entry frame) appears when condition of Min/Max Pullback is met and follow through wave breaks end point of CiB wave.

This indicator has many other features and they can also help a user identify potential levels of trade entry and which is more bullish or bearish.

In the screenshot below we can see wave volume zones as support and resistance levels. SOT and large wave volume /delta price (yellow colored wave text frame) hint stopping action.

█ Settings

Explains the main settings.

-- General --

Wave size : Allows the User to select wave size from ① Fixed or ② ATR. ② ATR is Factor x ATR(Length).

Display : Allows the User to select how many wave text and zigzag appear.

-- Wave Type --

Wave type : Allows the User to select from Volume or Volume and Time.

Wave Volume / delta price : Displays Wave Volume / delta price.

Simplified value : Allows the User to select wave text display style from ① Divisor or ② Normalized. Normalized use SMA.

Decimal : Allows the User to select the decimal point in the Wave text.

-- Highlight Abnormal Wave --

Highlight Max Wave value (single direction) : Adds marks to the Wave text to highlight the max wave value.

Lookback : Allows the User to select how many waves search for the max wave value.

Highlight Abnormal Wave value (both directions) : Changes wave text size, color or frame color to highlight the abnormal wave value.

Lookback : Allows the User to select SMA length to decide average wave value.

Large/Small factor : Allows the User to select the threshold large wave value and small wave value. Average wave value is 1.

delta price : Highlights large delta price by large wave text size, small by small text size.

Wave Volume : Highlights large wave volume by yellow colored wave text, small by gray colored.

Wave Volume / delta price : highlights large Wave Volume / delta price by yellow colored wave text frame, small by gray colored.

-- Support and Resistance --

Single side Max Wave Volume / delta price : Draws dashed border box from end point of Max wave volume / delta price level.

Single side Max Wave Volume : Draws solid border box from start point of Max wave volume level.

Bias Wave Volume : Draws solid border box from start point of bias wave volume level.

-- Signals --

Bias (Wave Volume / delta price) : Displays Bias mark when large difference in wave volume / delta price before and after.

Ratio : Decides the threshold of become large difference.

3Decrease : Displays 3D mark when a continuous decrease in wave volume.

Shortening Of the Thrust : Displays SOT mark when a continuous decrease in delta price.

Change in Behavior and Pullback : Displays CiB mark when single side max wave volume and pullback.

-- Setups --

Change in Behavior and Pullback and Breakout : Displays entry frame when change in behavior and pullback and then breakout.

Min / Max Pullback : Decides the threshold of min / max pullback.

If you need more information, please read the indicator's tooltip.

█ Conclusion

Weis Wave is powerful interpretation of volume and its tell us potential trend change and entry point which can't find without weis wave.

It's not the holy grail, but improve your chart reading skills and help you trade rationally (at least from VSA perspective).

ADX and DI Trend meter and status table IndicatorThis ADX (Average Directional Index) and DI (Directional Indicator) indicator helps identify:

Trend Direction & Strength:

LONG: +DI above -DI with ADX > 20

SHORT: -DI above +DI with ADX > 20

RANGE: ADX < 20 indicates choppy/sideways market

Trading Signals:

Bullish: +DI crosses above -DI (green triangle)

Bearish: -DI crosses below +DI (red triangle)

ADX Strength Levels:

Strong: ADX ≥ 50

Moderate: ADX 30-49

Weak: ADX 20-29

No Trend: ADX < 20

Best Uses:

Trend confirmation before entering trades

Identifying ranging vs trending markets

Exit signal when trend weakens

Works well on multiple timeframes

Most effective in combination with other indicators

The table displays current trend direction and ADX strength in real-time

4-Frame Trend CountThis script tracks the current close vs the close from 4 time frames prior to spot a trend reversal after 9 consecutive up or down moves.

Four Supertrend By Baljit AujlaThis Pine Script is an implementation of a "Four Supertrend" indicator by Baljit Aujla. It calculates and plots four Supertrend indicators based on the Average True Range (ATR) method, allowing for different ATR periods and multipliers for each line.

Here is an explanation of the key components:

Inputs

1:- ATR Periods: Four different periods for ATR, adjustable by the user (defaults: 10, 11, 12, 13).

2:- ATR Multipliers: Four different multipliers for the ATR, adjustable by the user (defaults: 1.0, 2.0, 3.0, 4.0).

3:- Source: The data source used for calculation, default is the average of high and low prices (hl2).

4:- Change ATR Calculation Method: Option to switch between the traditional ATR and a simple moving average of true range (SMA of TR).

5:- Signal Display- Options to show buy/sell signals and highlight trends.

Logic:

The script computes four separate Supertrend lines using the ATR method for each line. For each of the four lines, it calculates an uptrend and downtrend threshold, and the trend direction changes when the close price crosses these thresholds.

For each trend line:

1. Uptrend and Downtrend Calculation: The script uses ATR-based bands above and below the price. The uptrend line is calculated by subtracting the ATR multiplied by a given multiplier from the source price, and the downtrend line is calculated by adding the ATR multiplied by a multiplier to the source price.

2. Trend Reversal Logic: The trend switches based on the price action relative to the uptrend and downtrend lines. If the price moves above the downtrend, it signals a switch to an uptrend, and vice versa for a downtrend.

3. Signal Generation: Buy signals occur when the trend changes from negative to positive (down to up), and sell signals occur when the trend changes from positive to negative (up to down).

Plots:

The script plots:

Uptrend and Downtrend Lines: These are visualized as green and red lines for each trend.

Buy/Sell Signals: Small circles are drawn on the chart when a trend change occurs (buy and sell signals).

Trend Highlighting: Background highlighting is applied to show when the market is in an uptrend (green) or downtrend (red).

Alerts:

The script has commented-out alert conditions (alertcondition), which can be enabled to send notifications when a buy or sell signal occurs, or when a trend change happens.

Enhancements:

1. Background Highlighting: This is an option to visually emphasize uptrends and downtrends by filling the background with respective colors.

2. Signal Visibility: You can toggle whether to show the buy/sell signals on the chart.

3. ATR Calculation Method: Option to change the ATR calculation method (using SMA of TR vs the default ATR).

The script is useful for identifying multi-timeframe trends with adjustable parameters and provides both signals and visual markers on the chart to aid in trading decisions.

Issues and Improvements:

The code seems to be truncated, specifically for the last Supertrend line (Line 4). To fully complete the functionality for the fourth line, the logic for up4, down4 and tread4 needs to be finished, similar to the other three lines.

Would you like help finishing the script for the fourth line or improving specific parts of it?

Relative Strength vs SPX

This indicator calculates the ratio of the current chart's price to the S&P 500 Index (SPX), providing a measure of the stock's relative strength compared to the broader market.

Key Features:

Dynamic High/Low Detection: Highlights periods when the ratio makes a new high (green) or a new low (red) based on a user-defined lookback period.

Customizable Lookback: The lookback period for detecting highs and lows can be adjusted in the settings for tailored analysis.

Visual Overlay: The ratio is plotted in a separate pane, allowing easy comparison of relative strength trends.

This tool is useful for identifying stocks outperforming or underperforming the S&P 500 over specific timeframes.

BTC vs Altcoin CorrelationThis Pine Script indicator calculates and visualizes the rolling correlation between Bitcoin (BTC) and a selected altcoin, while providing insights into the percentage of time the correlation remains above a user-defined threshold. Users can independently configure the correlation calculation period and the lookback period for measuring the percentage of time above the threshold. The correlation is displayed as a color-coded line: green when above the threshold and red otherwise, with a dashed horizontal line marking the threshold level. A dynamic table displays the current correlation value and the percentage of time spent above the threshold within the specified period, enabling quick evaluation of correlation dynamics between BTC and the chosen altcoin.

Stock vs Sector Comparison with HighlightsThis graph is meant as a support to select a stock that is expected to perform better than the sector.

The graph is based on weekly chart. So this is a medium / long term strategy.

How is expected to be used: when the stock has under performed the sector for some time, there is a natural tendence that it will catch up with the sector again. So, for example, if the color change from green to red, you should consider find another stock in the sector. If the stock looses the green color, but is not red yet, you should wait. And vice versa if you start with red. However, life is not that simple, as you can get fake signal. To mitigate this problem, you can adjust the threshold in the input setting, so just go for the signal after x weeks over/underperforming. You also need remember to select the sector in the settings, as the sector is not give automatically when you select the stock.

Below the sectors used:

Sector Name Ticker

S&P 500 (Market Index) SPY

Technology XLK

Financials XLF

Consumer Discretionary XLY

Industrials XLI

Health Care XLV

Consumer Staples XLP

Energy XLE

Utilities XLU

Communication Services XLC

Real Estate XLRE

Materials XLB

Buy vs Sell VolumeHow It Works:

BuyVol: Estimates buying volume by calculating the proportion of volume attributed to the upward price movement within each bar.

SellVol: Estimates selling volume by calculating the proportion of volume attributed to the downward price movement within each bar.

Customization:

length: You can adjust the length input parameter to change the period over which the average is calculated.

Visualization:

The buy trendline is plotted in Green and represents the average net buying vs. selling volume over the specified period.

The sell trendline is plotted in Red and represents the average net selling vs. buying volume over the specified period.

Note: This script provides an approximation and should be used in conjunction with other analysis tools to make informed trading decisions.

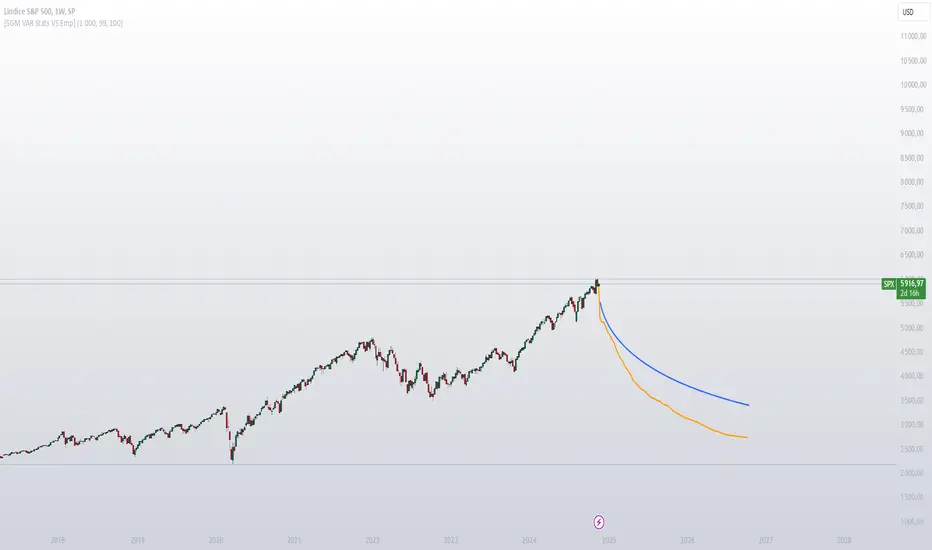

[SGM VaR Stats VS Empirical]Main Functions

Logarithmic Returns & Historical Data

Calculates logarithmic returns from closing prices.

Stores these returns in a dynamic array with a configurable maximum size.

Approximation of the Inverse Error Function

Uses an approximation of the erfinv function to calculate z-scores for given confidence levels.

Basic Statistics

Mean: Calculates the average of the data in the array.

Standard Deviation: Measures the dispersion of returns.

Median: Provides a more robust measure of central tendency for skewed distributions.

Z-Score: Converts a confidence level into a standard deviation multiplier.

Empirical vs. Statistical Projection

Empirical Projection

Based on the median of cumulative returns for each projected period.

Applies an adjustable confidence filter to exclude extreme values.

Statistical Projection

Relies on the mean and standard deviation of historical returns.

Incorporates a standard deviation multiplier for confidence-adjusted projections.

PolyLines (Graphs)

Generates projections visually through polylines:

Statistical Polyline (Blue): Based on traditional statistical methods.

Empirical Polyline (Orange): Derived from empirical data analysis.

Projection Customization

Maximum Data Size: Configurable limit for the historical data array (max_array_size).

Confidence Level: Adjustable by the user (conf_lvl), affects the width of the confidence bands.

Projection Length: Configurable number of projected periods (length_projection).

Key Steps

Capture logarithmic returns and update the historical data array.

Calculate basic statistics (mean, median, standard deviation).

Perform projections:

Empirical: Based on the median of cumulative returns.

Statistical: Based on the mean and standard deviation.

Visualization:

Compare statistical and empirical projections using polylines.

Utility

This script allows users to compare:

Traditional Statistical Projections: Based on mathematical properties of historical returns.

Empirical Projections: Relying on direct historical observations.

Divergence or convergence of these lines also highlights the presence of skewness or kurtosis in the return distribution.

Ideal for traders and financial analysts looking to assess an asset’s potential future performance using combined statistical and empirical approaches.

SPX Open vs SMA AlertThis indicator is specifically designed to identify the first market-relevant candle of the S&P 500 (SPX) after the market opens. The opening price of the trading day is compared to a customizable simple moving average (SMA) period. A visual marker and an alert are triggered when the opening price is above the SMA. Perfect for traders seeking early market trends or integrating automated trading strategies.

Features:

Market Open: The indicator uses the New York market open time (09:30 ET), accounting for time zones and daylight saving time changes.

Flexible Time Offset: Users can set a time offset to trigger alerts after the market opens.

Customizable SMA: The SMA period is adjustable, with a default value of 10.

Visual Representation: A step-line SMA is plotted directly on the chart with subtle transparency and clean markers.

Alert Functionality: Alerts are triggered when conditions are met (opening price > SMA).

Usage:

This indicator is ideal for identifying relevant trading signals early in the session.

Alerts can also serve as triggers for automated trading, e.g., in conjunction with the Trading Automation Toolbox.

Supports both intraday and daily charts.

Alarm Settings:

Select the appropriate symbol (e.g., SPX) and the alert condition "SPX Open > SMA10".

Trigger Settings:

Choose "Once Per Bar Close" to ensure the condition is evaluated at the end of each candle.

If you prefer to evaluate the condition immediately when it becomes true, choose "Once Per Minute".

Duration:

Set the alarm to "Open-ended" if you want it to remain active indefinitely.

Alternatively, set a specific expiration date for the alarm.