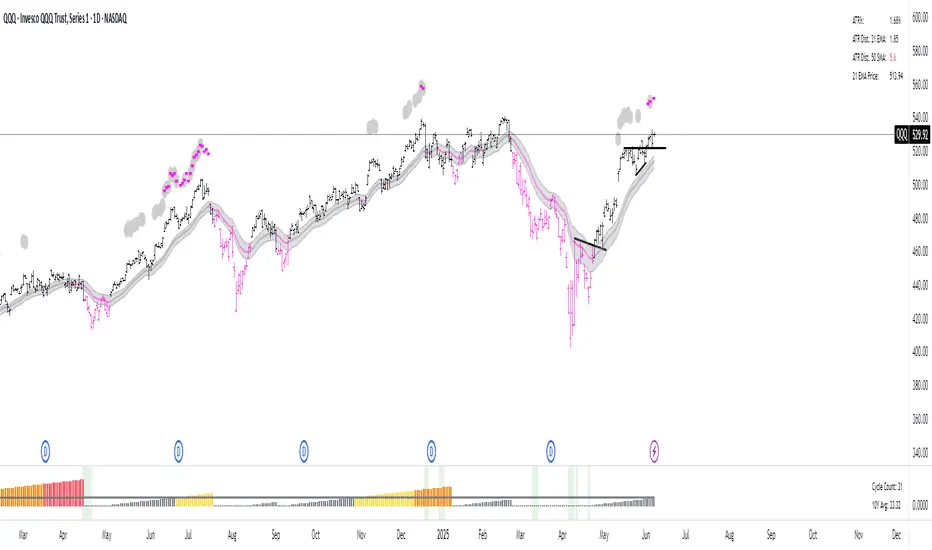

21DMA Structure Counter (EMA/SMA Option)21DMA Structure Counter (EMA/SMA Option)

Overview

The 21DMA Structure Counter is an advanced technical indicator that tracks consecutive periods where price action remains above a 21-period moving average structure. This indicator helps traders identify momentum phases and potential trend exhaustion points using statistical analysis.

Key Features

Moving Average Structure

- Configurable MA Type: Choose between EMA (Exponential Moving Average) or SMA (Simple Moving Average)

- 21-Period Default: Optimized for the widely-watched 21-period moving average

- Triple MA Structure: Tracks high, close, and low moving averages for comprehensive analysis

Statistical Analysis

- Cycle Counting: Automatically counts consecutive periods above the MA structure

- Historical Data: Maintains up to 2,500 historical cycles (approximately 10 years of daily data)

- Z-Score Calculation: Provides statistical context using mean and standard deviation

- Multiple Standard Deviation Levels: Displays +1, +2, and +3 standard deviation thresholds

Visual Indicators

Color-Coded Bars:

- Gray: Below 10-year average

- Yellow: Between average and +1 standard deviation

- Orange: Between +1 and +2 standard deviations

- Red: Between +2 and +3 standard deviations

- Fuchsia: Above +3 standard deviations (extreme readings)

Breadth Integration

- Multiple Breadth Options: NDFI, NDTH, NDTW (NASDAQ breadth indicators), or VIX

- Background Shading: Visual alerts when breadth reaches extreme levels

- High/Low Thresholds: Customizable levels for breadth analysis

- Real-time Display: Current breadth value shown in data table

Smart Reset Logic

- High Below Structure Reset: Automatically resets count when daily high falls below the lowest MA

- Flexible Hold Period: Continues counting during temporary weakness as long as structure isn't violated

- Precise Entry/Exit: Strict criteria for starting cycles, flexible for maintaining them

How to Use

Trend Identification

- Rising Counts: Indicate sustained momentum above key moving average structure

- Extreme Readings: Z-scores above +2 or +3 suggest potential trend exhaustion

- Historical Context: Compare current cycles to 10-year statistical averages

Risk Management

- Breadth Confirmation: Use breadth shading to confirm market-wide strength/weakness

- Statistical Extremes: Exercise caution when readings reach +3 standard deviations

- Reset Signals: Pay attention to structure violations for potential trend changes

Multi-Timeframe Application

- Daily Charts: Primary timeframe for swing trading and position management

- Weekly/Monthly: Longer-term trend analysis

- Intraday: Shorter-term momentum assessment (adjust MA period accordingly)

Settings

Moving Average Options

- Type: EMA or SMA selection

- Period: Default 21 (customizable)

- Reset Days: Days below structure required for reset

Visual Customization

- Standard Deviation Lines: Toggle and customize colors for +1, +2, +3 SD

- Breadth Selection: Choose from NDFI, NDTH, NDTW, or VIX

- Threshold Levels: Set custom high/low breadth thresholds

- Table Styling: Customize text colors, background, and font size

Technical Notes

- Data Retention: Maintains 2,500 historical cycles for robust statistical analysis

- Real-time Updates: Calculations update with each new bar

- Breadth Integration: Uses security() function to pull external breadth data

- Performance Optimized: Efficient array management prevents memory issues

Best Practices

1. Combine with Price Action: Use alongside support/resistance and chart patterns

2. Monitor Breadth Divergences: Watch for breadth weakness during strong readings

3. Respect Statistical Extremes: Exercise caution at +2/+3 standard deviation levels

4. Context Matters: Consider overall market environment and sector rotation

5. Risk Management: Use appropriate position sizing, especially at extreme readings

Disclaimer

This indicator is for educational and informational purposes only. It should not be used as the sole basis for trading decisions. Always combine with other forms of analysis and proper risk management techniques.

Compatible with Pine Script v6 | Optimized for daily timeframes | Best used on major indices and liquid stocks

在腳本中搜尋"同花顺软件+美国+VIX+恐慌指数+行情代码"

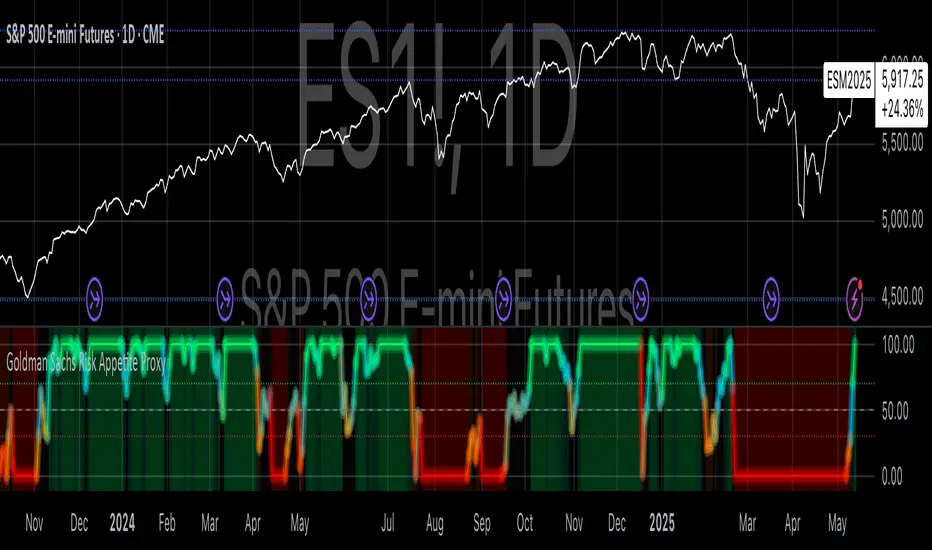

Goldman Sachs Risk Appetite ProxyRisk appetite indicators serve as barometers of market psychology, measuring investors' collective willingness to engage in risk-taking behavior. According to Mosley & Singer (2008), "cross-asset risk sentiment indicators provide valuable leading signals for market direction by capturing the underlying psychological state of market participants before it fully manifests in price action."

The GSRAI methodology aligns with modern portfolio theory, which emphasizes the importance of cross-asset correlations during different market regimes. As noted by Ang & Bekaert (2002), "asset correlations tend to increase during market stress, exhibiting asymmetric patterns that can be captured through multi-asset sentiment indicators."

Implementation Methodology

Component Selection

Our implementation follows the core framework outlined by Goldman Sachs research, focusing on four key components:

Credit Spreads (High Yield Credit Spread)

As noted by Duca et al. (2016), "credit spreads provide a market-based assessment of default risk and function as an effective barometer of economic uncertainty." Higher spreads generally indicate deteriorating risk appetite.

Volatility Measures (VIX)

Baker & Wurgler (2006) established that "implied volatility serves as a direct measure of market fear and uncertainty." The VIX, often called the "fear gauge," maintains an inverse relationship with risk appetite.

Equity/Bond Performance Ratio (SPY/IEF)

According to Connolly et al. (2005), "the relative performance of stocks versus bonds offers significant insight into market participants' risk preferences and flight-to-safety behavior."

Commodity Ratio (Oil/Gold)

Baur & McDermott (2010) demonstrated that "gold often functions as a safe haven during market turbulence, while oil typically performs better during risk-on environments, making their ratio an effective risk sentiment indicator."

Standardization Process

Each component undergoes z-score normalization to enable cross-asset comparisons, following the statistical approach advocated by Burdekin & Siklos (2012). The z-score transformation standardizes each variable by subtracting its mean and dividing by its standard deviation: Z = (X - μ) / σ

This approach allows for meaningful aggregation of different market signals regardless of their native scales or volatility characteristics.

Signal Integration

The four standardized components are equally weighted and combined to form a composite score. This democratic weighting approach is supported by Rapach et al. (2010), who found that "simple averaging often outperforms more complex weighting schemes in financial applications due to estimation error in the optimization process."

The final index is scaled to a 0-100 range, with:

Values above 70 indicating "Risk-On" market conditions

Values below 30 indicating "Risk-Off" market conditions

Values between 30-70 representing neutral risk sentiment

Limitations and Differences from Original Implementation

Proprietary Components

The original Goldman Sachs indicator incorporates additional proprietary elements not publicly disclosed. As Goldman Sachs Global Investment Research (2019) notes, "our comprehensive risk appetite framework incorporates proprietary positioning data and internal liquidity metrics that enhance predictive capability."

Technical Limitations

Pine Script v6 imposes certain constraints that prevent full replication:

Structural Limitations: Functions like plot, hline, and bgcolor must be defined in the global scope rather than conditionally, requiring workarounds for dynamic visualization.

Statistical Processing: Advanced statistical methods used in the original model, such as Kalman filtering or regime-switching models described by Ang & Timmermann (2012), cannot be fully implemented within Pine Script's constraints.

Data Availability: As noted by Kilian & Park (2009), "the quality and frequency of market data significantly impacts the effectiveness of sentiment indicators." Our implementation relies on publicly available data sources that may differ from Goldman Sachs' institutional data feeds.

Empirical Performance

While a formal backtest comparison with the original GSRAI is beyond the scope of this implementation, research by Froot & Ramadorai (2005) suggests that "publicly accessible proxies of proprietary sentiment indicators can capture a significant portion of their predictive power, particularly during major market turning points."

References

Ang, A., & Bekaert, G. (2002). "International Asset Allocation with Regime Shifts." Review of Financial Studies, 15(4), 1137-1187.

Ang, A., & Timmermann, A. (2012). "Regime Changes and Financial Markets." Annual Review of Financial Economics, 4(1), 313-337.

Baker, M., & Wurgler, J. (2006). "Investor Sentiment and the Cross-Section of Stock Returns." Journal of Finance, 61(4), 1645-1680.

Baur, D. G., & McDermott, T. K. (2010). "Is Gold a Safe Haven? International Evidence." Journal of Banking & Finance, 34(8), 1886-1898.

Burdekin, R. C., & Siklos, P. L. (2012). "Enter the Dragon: Interactions between Chinese, US and Asia-Pacific Equity Markets, 1995-2010." Pacific-Basin Finance Journal, 20(3), 521-541.

Connolly, R., Stivers, C., & Sun, L. (2005). "Stock Market Uncertainty and the Stock-Bond Return Relation." Journal of Financial and Quantitative Analysis, 40(1), 161-194.

Duca, M. L., Nicoletti, G., & Martinez, A. V. (2016). "Global Corporate Bond Issuance: What Role for US Quantitative Easing?" Journal of International Money and Finance, 60, 114-150.

Froot, K. A., & Ramadorai, T. (2005). "Currency Returns, Intrinsic Value, and Institutional-Investor Flows." Journal of Finance, 60(3), 1535-1566.

Goldman Sachs Global Investment Research (2019). "Risk Appetite Framework: A Practitioner's Guide."

Kilian, L., & Park, C. (2009). "The Impact of Oil Price Shocks on the U.S. Stock Market." International Economic Review, 50(4), 1267-1287.

Mosley, L., & Singer, D. A. (2008). "Taking Stock Seriously: Equity Market Performance, Government Policy, and Financial Globalization." International Studies Quarterly, 52(2), 405-425.

Oppenheimer, P. (2007). "A Framework for Financial Market Risk Appetite." Goldman Sachs Global Economics Paper.

Rapach, D. E., Strauss, J. K., & Zhou, G. (2010). "Out-of-Sample Equity Premium Prediction: Combination Forecasts and Links to the Real Economy." Review of Financial Studies, 23(2), 821-862.

Divergence Macro Sentiment Indicator (DMSI)The Divergence Macro Sentiment Indicator (DMSI)

Think of DMSI as your daily “mood ring” for the markets. It boils down the tug-of-war between growth assets (S&P 500, copper, oil) and safe havens (gold, VIX) into one clear histogram—so you instantly know if the bulls have broad backing or are charging ahead with one foot tied behind.

🔍 What You’re Seeing

Green bars (above zero): Risk-on conviction.

Equities and commodities are rallying while gold and volatility retreat.

Red bars (below zero): Risk-off caution.

Gold or VIX are climbing even as stocks rise—or stocks aren’t fully joined by oil/copper.

Zero line: The line in the sand between “full-steam ahead” and “proceed with care.”

📈 How to Read It

Cross-Zero Signals

Bullish trigger: DMSI flips up through zero after a red stretch → fresh long entries.

Bearish trigger: DMSI tumbles below zero from green territory → tighten stops or go defensive.

Divergence Warnings

If SPX makes new highs but DMSI is rolling over (lower green bars or red), that’s your early red flag—rallies may fizzle.

Strength Confirmation

On pullbacks, only buy dips when DMSI ≥ 0. When DMSI is deeply positive, you can be more aggressive on position size or add leverage.

💡 Trade Guidance & Use Cases

Trend Filter: Only take your S&P or sector-ETF long setups when DMSI is non-negative—avoids hollow rallies.

Macro Pair Trades:

Deep red DMSI: go long gold or gold miners (GLD, GDX).

Strong green DMSI: lean into cyclicals, industrials, even energy names.

Risk Management:

Scale out as DMSI fades into negative territory mid-trade.

Scale in or add to winners when it stays bullish.

Swing Confirmation: Overlay on any oscillator or price-pattern system—accept signals only when the macro tide is flowing in your favour.

🚀 Why It Works

Markets don’t move in a vacuum. When stocks rally but the “real-economy” metals and volatility aren’t cooperating, something’s off under the hood. DMSI catches those cross-asset cracks before price alone can—and gives you an early warning system for smarter entries, tighter risk, and bigger gains when the macro trend really kicks in.

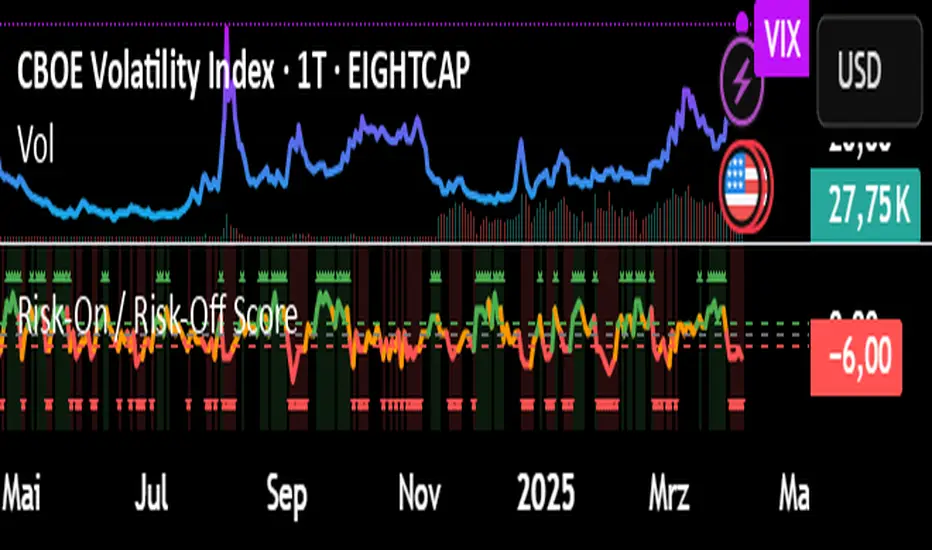

Risk-On / Risk-Off ScoreRisk-On / Risk-Off Score (Macro Sentiment Indicator)

This indicator calculates a custom Risk-On / Risk-Off Score to objectively assess the current market risk sentiment using a carefully selected basket of macroeconomic assets and intermarket relationships.

🧠 What does this indicator do?

The score is based on 14 key components grouped into three categories:

🟢 Risk-On Assets (rising = appetite for risk)

(+1 if performance over X days is positive, otherwise –1)

NASDAQ 100 (NAS100USD)

S&P 500 (SPX)

Bitcoin (BTCUSD)

Copper (HG1!)

WTI Crude Oil (CLK2025)

🔴 Risk-Off Assets (rising = flight to safety)

(–1 if performance is positive, otherwise +1)

Gold (XAUUSD)

US Treasury Bonds (TLT ETF) (TLT)

US Dollar Index (DXY)

USD/CHF

USD/JPY

US 10Y Yields (US10Y) (yields are interpreted inversely)

⚖️ Risk Spreads / Relative Indicators

(+1 if rising, –1 if falling)

Copper/Gold Ratio → HG1! / XAUUSD

NASDAQ/VIX Ratio → NAS100USD / VIX

HYG/TLT Ratio → HYG / TLT

📏 Score Calculation

Total score = sum of all components

Range: from –14 (extreme Risk-Off) to +14 (strong Risk-On)

Color-coded output:

🟢 Score > 2 = Risk-On

🟠 –2 to +2 = Neutral

🔴 Score < –2 = Risk-Off

Displayed as a line plot with background color and signal markers

🧪 Timeframe of analysis:

Default: 5 days (adjustable via input)

Calculated using Rate of Change (% change)

🧭 Use Cases:

Quickly assess macro sentiment

Filter for position sizing, hedging, or intraday bias

Especially useful for:

Swing traders

Day traders with macro filters

Volatility and options traders

📌 Note:

This is not a buy/sell signal indicator, but a contextual sentiment tool designed to help you stay aligned with overall market conditions.

Sigma Expected Movement)Okay, here's a brief description of what the final Pine Script code achieves:

Indicator Description:

This indicator calculates and plots expected price movement ranges based on the VIX index for daily, weekly, or monthly periods. It uses user-selectable VIX data (Today's Open / Previous Close) and a center price source (Today's Open / Previous Close).

Key features include:

Up to three customizable deviation levels, based on user-defined percentages of the calculated expected move.

Configurable visibility, color, opacity (default 50%), line style, and width (default 1) for each deviation level.

Optional filled area boxes between the 1st and 2nd deviation levels (enabled by default), with customizable fill color/opacity.

An optional center price line with configurable visibility (disabled by default), color, opacity, style, and width.

All drawings appear only within a user-defined time window (e.g., specific market hours).

Does not display price labels on the lines.

Optional rounding of calculated price levels.

UM Futures Dashboard with Moving Average DirectionUM Futures Dashboard with Moving Average Direction

Description :

This futures dashboard gives you quick glance of all “major” futures prices and percentage changes. The text color and trends are based on your configured moving average type and length. The dashboard will display LONG in green text when the configure MA is trending higher and SHORT in red when the configured MA is trending lower. The dashboard also includes the VIX futures roll yield and VIX futures status of Contango or Backwardation.

I have included the indicator twice on the sample chart to illustrate different table settings. I also included an 8 period WMA overlay on the price chart since this is the default of the dashboard. (The Moving Average color change is another one of my indicators titled “UM EMA SMA WMA HMA with Directional Color Change”)

Defaults and Configuration :

The default MA type is the Weighted Moving Average, (WMA) with a daily setting of 8. Choices include WMA, SMA, and EMA. The table location defaults to the upper right corner in landscape mode. It can also be set to “flip” to portrait mode. I have added the table to the chart twice to illustrate the table orientations.

Table location, orientation, timeframe, moving average type and length are user-configurable. The configured dashboard timeframe is independent of the chart timeframe. Percentage changes and Moving Averages are based on the configured dashboard timeframe.

Alerts :

Alerts can be configured on the directional change of the dashboard moving average. For example, if the daily 8 period weighted moving average begins trending higher it will turn from red to green. This color change would fire a LONG alert. A color trend change of the weighted moving average from green to red would fire a SHORT alert. Alerts are disabled by default but can be set for any or all of the futures contracts included.

Suggested Uses :

If you follow or trade futures, add this dashboard indicator to your chart layout. Configure your favorite moving average. Use this to quickly see where all the major futures are trading. This saved me from thumbing through the CNBC app on my phone.

One thing I do is to “stretch” moving average to a smaller timeframe. For example, if you like the 8 period WMA on the daily, try the 192 WMA on the hourly. ( The daily 8 period WMA is roughly a 192 WMA on an hourly chart) This can smooth out some of the violent price action and give better entries/exits.

Setup a FUTURES indicator template. I do this with the dashboard and couple other of my favorite indicators.

Suggested Settings :

Daily charts: 8 WMA

Trading Capital Management for Option SellingTrading Capital Management for Option Selling

This Pine Script indicator helps manage trading capital allocation for option selling strategies based on price percentile ranking. It provides dynamic allocation recommendations for index options (NIFTY and BANKNIFTY) and individual stock positions.

Key Features:

- Dynamic buying power (BP) allocation based on close price percentile

- Flexible index allocation between NIFTY and BANKNIFTY

- Automated calculation of recommended number of stock positions

- Risk management through position size limits

- Real-time INDIA VIX monitoring

Main Parameters:

1. Window Length: Period for percentile calculation (default: 252 days)

2. Thresholds: Low (30%) and High (70%) percentile thresholds

3. Capital Settings:

- Trading Capital: Total capital available

- Max BP% per Stock: Maximum allocation per stock position

4. Buying Power Range:

- Low Percentile BP%: Base BP usage at low percentile

- High Percentile BP%: Maximum BP usage at high percentile

5. Index Allocation:

- NIFTY/BANKNIFTY split ratio

- Minimum and maximum allocation thresholds

Display:

The indicator shows two tables:

1. Common Metrics:

- Total BP Usage with percentage

- Current INDIA VIX value

- Current Close Price Percentile

2. Capital Allocation:

- Index-wise BP allocation (NIFTY and BANKNIFTY)

- Stock allocation pool

- Recommended number of stock positions with BP per stock

Usage:

This indicator helps traders:

1. Scale positions based on market conditions using price percentile

2. Maintain balanced exposure between indices and stocks

3. Optimize capital utilization while managing risk

4. Adjust position sizing dynamically with market volatility

TradFi Fundamentals: Enhanced Macroeconomic Momentum Trading Introduction

The "Enhanced Momentum with Advanced Normalization and Smoothing" indicator is a tool that combines traditional price momentum with a broad range of macroeconomic factors. I introduced the basic version from a research paper in my last script. This one leverages not only the price action of a security but also incorporates key economic data—such as GDP, inflation, unemployment, interest rates, consumer confidence, industrial production, and market volatility (VIX)—to create a comprehensive, normalized momentum score.

Previous indicator

Explanation

In plain terms, the indicator calculates a raw momentum value based on the change in price over a defined lookback period. It then normalizes this momentum, along with several economic indicators, using a method chosen by the user (options include simple, exponential, or weighted moving averages, as well as a median absolute deviation (MAD) approach). Each normalized component is assigned a weight reflecting its relative importance, and these weighted values are summed to produce an overall momentum score.

To reduce noise, the combined momentum score can be further smoothed using a user-selected method.

Signals

For generating trade signals, the indicator offers two modes:

Zero Cross Mode: Signals occur when the smoothed momentum line crosses the zero threshold.

Zone Mode: Overbought and oversold boundaries (which are user defined) provide signals when the momentum line crosses these preset limits.

Definition of the Settings

Price Momentum Settings:

Price Momentum Lookback: The number of days used to compute the percentage change in price (default 50 days).

Normalization Period (Price Momentum): The period over which the price momentum is normalized (default 200 days).

Economic Data Settings:

Normalization Period (Economic Data): The period used to normalize all economic indicators (default 200 days).

Normalization Method: Choose among SMA, EMA, WMA, or MAD to standardize both price and economic data. If MAD is chosen, a multiplier factor is applied (default is 1.4826).

Smoothing Options:

Apply Smoothing: A toggle to enable further smoothing of the combined momentum score.

Smoothing Period & Method: Define the period and type (SMA, EMA, or WMA) used to smooth the final momentum score.

Signal Generation Settings:

Signal Mode: Select whether signals are based on a zero-line crossover or by crossing user-defined overbought/oversold (OB/OS) zones.

OB/OS Zones: Define the upper and lower boundaries (default upper zones at 1.0 and 2.0, lower zones at -1.0 and -2.0) for zone-based signals.

Weights:

Each component (price momentum, GDP, inflation, unemployment, interest rates, consumer confidence, industrial production, and VIX) has an associated weight that determines its contribution to the overall score. These can be adjusted to reflect different market views or risk preferences.

Visual Aspects

The indicator plots the smoothed combined momentum score as a continuous blue line against a dotted zero-line reference. If the Zone signal mode is selected, the indicator also displays the upper and lower OB/OS boundaries as horizontal lines (red for overbought and green for oversold). Buy and sell signals are marked by small labels ("B" for buy and "S" for sell) that appear at the bottom or top of the chart when the score crosses the defined thresholds, allowing traders to quickly identify potential entry or exit points.

Conclusion

This enhanced indicator provides traders with a robust approach to momentum trading by integrating traditional price-based signals with a suite of macroeconomic indicators. Its normalization and smoothing techniques help reduce noise and mitigate the effects of outliers, while the flexible signal generation modes offer multiple ways to interpret market conditions. Overall, this tool is designed to deliver a more nuanced perspective on market momentum.

Multiple Values TableThis Pine Script indicator, named "Multiple Values Table," provides a comprehensive view of various technical indicators in a tabular format directly on your trading chart. It allows traders to quickly assess multiple metrics without switching between different charts or panels.

Key Features:

Table Position and Size:

Users can choose the position of the table on the chart (e.g., top left, top right).

The size of the table can be adjusted (e.g., tiny, small, normal, large).

Moving Averages:

Calculates the 5-day Exponential Moving Average (5DEMA) using daily data.

Calculates the 5-week and 20-week EMAs (5WEMA and 20WEMA) using weekly data.

Indicates whether the current price is above or below these moving averages in percentage terms.

Drawdown and Williams VIX Fix:

Computes the drawdown from the 365-day high to the current close.

Calculates the Williams VIX Fix (WVF), which measures the volatility of the asset.

Shows both the current WVF and a 2% drawdown level.

Relative Strength Index (RSI):

Displays the current RSI and compares it to the RSI from 14 days ago.

Indicates whether the RSI is increasing, decreasing, or flat.

Stochastic RSI:

Computes the Stochastic RSI and compares it to the value from 14 days ago.

Indicates whether the Stochastic RSI is increasing, decreasing, or flat.

Normalized MACD (NMACD):

Calculates the Normalized MACD values.

Indicates whether the MACD is increasing, decreasing, or flat.

Awesome Oscillator (AO):

Calculates the AO on a daily timeframe.

Indicates whether the AO is increasing, decreasing, or flat.

Volume Analysis:

Displays the average volume over the last 22 days.

Shows the current day's volume as a percentage of the average volume.

Percentile Calculations:

Calculates the current percentile rank of the WVF and ATH over specified periods.

Indicates the percentile rank of the current volume percentage over the past period.

Table Display:

All these values are presented in a neatly formatted table.

The table updates dynamically with the latest data.

Example Use Cases:

Comprehensive Market Analysis: Quickly assess multiple indicators at a glance.

Trend and Momentum Analysis: Identify trends and momentum changes based on various moving averages and oscillators.

Volatility and Drawdown Monitoring: Track volatility and drawdown levels to manage risk effectively.

This script offers a powerful tool for traders who want to have a holistic view of various technical indicators in one place. It provides flexibility in customization and a user-friendly interface to enhance your trading experience.

Buy/Sell Signals for CM_Williams_Vix_FixThis script in Pine Script is designed to create an indicator that generates buy and sell signals based on the Williams VIX Fix (WVF) indicator. Here’s a brief explanation of how this script works:

Main Components:

Williams VIX Fix (WVF) – This volatility indicator is calculated using the formula:

WVF

=

(

highest(close, pd)

−

low

highest(close, pd)

)

×

100

WVF=(

highest(close, pd)

highest(close, pd)−low

)×100

where highest(close, pd) represents the highest closing price over the period pd, and low represents the lowest price over the same period.

Bollinger Bands are used to determine levels of overbought and oversold conditions. They are constructed around the moving average (SMA) of the WVF value using standard deviation (SD).

Ranges based on percentiles help identify extreme levels of WVF values to spot entry and exit points.

Buy and sell signals are generated when the WVF crosses the Bollinger Bands lines or reaches the ranges based on percentiles.

Adjustable Parameters:

LookBack Period Standard Deviation High (pd): The lookback period for calculating the highest closing price.

Bolinger Band Length (bbl): The length of the period for constructing the Bollinger Bands.

Bollinger Band Standard Devaition Up (mult): The multiplier for the standard deviation used for the upper Bollinger Band.

Look Back Period Percentile High (lb): The lookback period for calculating maximum and minimum WVF values.

Highest Percentile (ph): The percentile threshold for determining the high level.

Lowest Percentile (pl): The percentile threshold for determining the low level.

Show High Range (hp): Option to display the range based on percentiles.

Show Standard Deviation Line (sd): Option to display the standard deviation line.

Signals:

Buy Signal: Generated when the WVF crosses above the lower Bollinger Band or falls below the lower boundary of the percentile-based range.

Sell Signal: Generated when the WVF crosses below the upper Bollinger Band or rises above the upper boundary of the percentile-based range.

These signals are displayed as triangles below or above the candles respectively.

Application:

The script can be used by traders to analyze market conditions and make buying or selling decisions based on volatility and price behavior.

Hidden SMT Divergence ICT 01 [TradingFinder] HSMT SMC Technique🔵 Introduction

Hidden SMT Divergence, an advanced concept within the Smart Money Technique (SMT), identifies discrepancies between correlated assets by focusing on their closing prices.

Unlike the standard SMT Divergence, which uses high and low prices for analysis, Hidden SMT Divergence uncovers subtle signals by examining divergences based on the assets' closing values.

These divergences often highlight potential reversals or trend continuations, making this technique a valuable tool for traders aiming to anticipate market movements.

This approach applies across various markets and asset classes, including :

Commodities : CAPITALCOM:GOLD vs. CAPITALCOM:SILVER or BLACKBULL:BRENT vs. BLACKBULL:WTI .

Indices : NASDAQ:NDX vs. TVC:SPX vs. FX:US30 .

FOREX : FX:EURUSD vs. OANDA:GBPUSD vs. TVC:DXY (US Dollar Index).

Cryptocurrencies : BITSTAMP:BTCUSD vs. COINBASE:ETHUSD vs. KUCOIN:SOLUSDT vs. CRYPTOCAP:TOTAL3 .

Volatility Measures : FOREXCOM:XAUUSD vs. TVC:VIX (Volatility Index).

By identifying divergences within these asset groups, traders can gain actionable insights into potential market reversals or shifts in trend direction. Hidden SMT Divergence is particularly effective for pinpointing subtle market signals that traditional methods may overlook.

Bullish Hidden SMT Divergence : This divergence emerges when one asset forms a higher low, while the correlated asset creates a lower low in terms of their closing prices. It often signals weakening downward momentum and a potential reversal to the upside.

Bearish Hidden SMT Divergence : This occurs when one asset establishes a higher high, while the correlated asset forms a lower high based on their closing prices. It typically reflects declining upward momentum and a probable shift to the downside.

🔵 How to Use

The Hidden SMT Divergence indicator provides traders with a systematic approach to identify market reversals or trend continuations through divergences in closing prices between two correlated assets.

🟣 Bullish Hidden SMT Divergence

Bullish Hidden SMT Divergence occurs when the closing price of the primary asset forms a higher low, while the correlated asset creates a lower low. This pattern indicates weakening downward momentum and signals a potential reversal to the upside.

After identifying the divergence, confirm it using additional tools like support levels, volume trends, or indicators such as RSI and MACD. Enter a buy position as the price shows signs of reversal near support zones, ensuring proper risk management by placing a stop-loss below the support level.

Bearish Hidden SMT Divergence

Bearish Hidden SMT Divergence is identified when the closing price of the primary asset forms a higher high, while the correlated asset creates a lower high. This divergence suggests a weakening uptrend and a likely reversal to the downside.

Validate the signal by examining resistance levels, declining volume, or complementary indicators. Consider entering a sell position as the price starts declining from resistance levels, and set a stop-loss above the resistance zone to limit potential losses.

🔵 Setting

Second Symbol : Select the secondary asset to compare with the primary asset. By default, "XAUUSD" (Gold) is used, but it can be customized to any stock, cryptocurrency, or currency pair.

Divergence Fractal Periods : Defines the number of past candles considered for identifying divergences. The default value is 2, but traders can adjust it for greater precision.

Bullish Divergence Line : Displays a dashed line connecting the points of bullish divergence.

Bearish Divergence Line : Shows a similar line for bearish divergence points.

Bullish Divergence Label : Marks areas of bullish divergence with a "+SMT" label.

Bearish Divergence Label : Highlights bearish divergences with a "-SMT" label.

Chart Type : Choose between Line or Candle charts for enhanced visualization.

🔵 Conclusion

Hidden SMT Divergence offers traders a refined method for identifying market reversals by analyzing closing price discrepancies between correlated assets. Its ability to uncover subtle divergences makes it an essential tool for traders who aim to stay ahead of market trends.

By integrating this technique with other technical analysis tools and sound risk management, traders can enhance their decision-making process and capitalize on market opportunities with greater confidence.

Hidden SMT Divergence’s focus on closing prices ensures more precise signals, helping traders refine their strategies across various markets, including Forex, commodities, indices, and cryptocurrencies.

Its open-source nature allows for customization and verification, providing transparency and flexibility to suit diverse trading needs. Hidden SMT Divergence stands as a powerful addition to the arsenal of any trader seeking to unlock hidden opportunities in dynamic financial markets.

CNN Fear and Greed Index JD modified from minusminusCNN Fear and Greed Index - www.cnn.com

Modified from minusminus -

See Documentation from CNN's website

CNN's Fear and Greed index is an attempt to quantitatively score the Fear and Greed in the SPX using 7 factors:

Market Momentum- S&P 500 (SPX) and its 125-day moving average

Stock Price Strength -Net new 52-week highs and lows on the NYSE

Stock Price Breadth - McClellan Volume Summation Index

Put and Call options - 5-day average put/call ratio

Market Volatility - VIX and its 50-day moving average

Safe Haven Demand - Difference in 20-day stock and bond returns

Junk Bond Demand - Yield spread: junk bonds vs. investment grade

Each Factor has a weight input for the final calculation initially set to a weight of 1. The final calculation of the index is a weighted average of each factor.

3 Factors have separate functions for calculation : See Code for Clarity

SPX Momentum : difference between the Daily CBOE:SPX index value and it's 125 Day Simple moving average.

Stock Price Strength : Net New 52-week highs and lows on the NYSE.

Function calculates a measure of Net New 52-week highs by:

NYSE 52-week highs (INDEX:MAHN) - all new NYSE Highs (INDEX:HIGH)

measure of Net New 52-week lows by:

NYSE 52-week lows (INDEX:MALN) - all new NYSE Lows (INDEX:LOWN)

Then calculate a ratio of Net New 52-week Highs and Lows over Total Highs and Lows then takes a 5-day moving average of that ratio-See Code

Stock Price Breadth is the McClellan Volume Summation Index :

First Calculate the McClellan Oscillator

Second Calculate the Summation Index

4 Factors are Straight data requests

5 Day Simple Moving Average of the Put-Call Ratio on SPY

50 Day Simple Moving Average of the SPX VIX

Difference between 20 Day Simple Moving Average of SPX Daily Close and 20 Day Simple Moving Average of 10Y Constant Maturity US Treasury Note

Yield Spread between ICE BofA US High Yield Index and ICE BofA US Investment Grade Corporate Yield Index

The Fear and Greed Index is a weighted average of these factors - which is then normalized to scale from 0 to 100 using the past 25 values - length parameter.

3 Zones are Shaded: Red for Extreme Fear, Grey for normal jitters, Green for Extreme Greed.

Disclaimer: This is not financial advice. These are just my ideas, and I am not an investment advisor or investment professional. This code is for informational purposes only and do your own analysis before making any investment decisions. This is an attempt to replicate in spirt an index CNN publishes on their website and in no way shape or form infringes on their content, calculations or proprietary information.

From CNN: www.cnn.com

FEAR & GREED INDEX FAQs

What is the CNN Business Fear & Greed Index?

The Fear & Greed Index is a way to gauge stock market movements and whether stocks are fairly priced. The theory is based on the logic that excessive fear tends to drive down share prices, and too much greed tends to have the opposite effect.

How is Fear & Greed Calculated?

The Fear & Greed Index is a compilation of seven different indicators that measure some aspect of stock market behavior. They are market momentum, stock price strength, stock price breadth, put and call options, junk bond demand, market volatility, and safe haven demand. The index tracks how much these individual indicators deviate from their averages compared to how much they normally diverge. The index gives each indicator equal weighting in calculating a score from 0 to 100, with 100 representing maximum greediness and 0 signaling maximum fear.

How often is the Fear & Greed Index calculated?

Every component and the Index are calculated as soon as new data becomes available.

How to use Fear & Greed Index?

The Fear & Greed Index is used to gauge the mood of the market. Many investors are emotional and reactionary, and fear and greed sentiment indicators can alert investors to their own emotions and biases that can influence their decisions. When combined with fundamentals and other analytical tools, the Index can be a helpful way to assess market sentiment.

[blackcat] L1 Dynamic Volatility IndicatorThe volatility indicator (Volatility) is used to measure the magnitude and instability of price changes in financial markets or a specific asset. This thing is usually used to assess how risky the market is. The higher the volatility, the greater the fluctuation in asset prices, but brother, the risk is also relatively high! Here are some related terms and explanations:

- Historical Volatility: The actual volatility of asset prices over a certain period of time in the past. This thing is measured by calculating historical data.

- Implied Volatility: The volatility inferred from option market prices, used to measure market expectations for future price fluctuations.

- VIX Index (Volatility Index): Often referred to as the "fear index," it predicts the volatility of the US stock market within 30 days in advance. This is one of the most famous volatility indicators in global financial markets.

Volatility indicators are very important for investors and traders because they can help them understand how unstable and risky the market is, thereby making wiser investment decisions.

Today I want to introduce a volatility indicator that I have privately held for many years. It can use colors to judge sharp rises and falls! Of course, if you are smart enough, you can also predict some potential sharp rises and falls by looking at the trend!

In the financial field, volatility indicators measure the magnitude and instability of price changes in different assets. They are usually used to assess the level of market risk. The higher the volatility, the greater the fluctuation in asset prices and therefore higher risk. Historical Volatility refers to the actual volatility of asset prices over a certain period of time in the past, which can be measured by calculating historical data; while Implied Volatility is derived from option market prices and used to measure market expectations for future price fluctuations. In addition, VIX Index is commonly known as "fear index" and is used to predict volatility in the US stock market within 30 days. It is one of the most famous volatility indicators in global financial markets.

Volatility indicators are very important for investors and traders because they help them understand market uncertainty and risk, enabling them to make wiser investment decisions. The L1 Dynamic Volatility Indicator that I am introducing today is an indicator that measures volatility and can also judge sharp rises and falls through colors!

This indicator combines two technical indicators: Dynamic Volatility (DV) and ATR (Average True Range), displaying warnings about sharp rises or falls through color coding. DV has a slow but relatively smooth response, while ATR has a fast but more oscillating response. By utilizing their complementary characteristics, it is possible to construct a structure similar to MACD's fast-slow line structure. Of course, in order to achieve fast-slow lines for DV and ATR, first we need to unify their coordinate axes by normalizing them. Then whenever ATR's yellow line exceeds DV's purple line with both curves rapidly breaking through the threshold of 0.2, sharp rises or falls are imminent.

However, it is important to note that relying solely on the height and direction of these two lines is not enough to determine the direction of sharp rises or falls! Because they only judge the trend of volatility and cannot determine bull or bear markets! But it's okay, I have already considered this issue early on and added a magical gradient color band. When the color band gradually turns warm, it indicates a sharp rise; conversely, when the color band tends towards cool colors, it indicates a sharp fall! Of course, you won't see the color band in sideways consolidation areas, which avoids your involvement in unnecessary trades that would only waste your funds! This indicator is really practical and with it you can better assess market risks and opportunities!

[blackcat] L1 Larry Williams VixFix IndicatorLevel : L1

Larry Williams, had this idea to create a synthetic VIX for more than just the main stock indices. Check out the formula for Williams VixFix:

```

VIX Fix Formula = (Highest(Close, 22) – Low) / (Highest(Close, 22)) * 100

```

What does this even mean? In normal person terms, here's what it's all about:

1. Find the highest close over the last 22 days and subtract today's low (or the current bar).

2. Divide that by the highest close of the past 22 days.

3. Multiply the result by 100 to "normalize" the indicator.

Why 22 days, you ask? That's how long the normal month of trading days is.

So, you see, the formula is pretty chill. It's just a way to measure the price volatility of the last 22 trading days. It's a bit of a lagging indicator, but it gets the job done.

Here my version of this scriptcreates a custom technical indicator called "L1 Larry Williams VixFix" that measures the distance between the highest high and the lowest low of a security's price over a specified period.

The user can adjust the period length and source price used in the VixFix calculation. The period length is set to 22 by default, but can be modified by the user with the "Length" input parameter. The source price is set to "close" by default, meaning it will use the closing price of each bar to calculate the VixFix. However, the user can also choose a different type of price data, such as open, high, or low.

The VixFix is calculated as a percentage of the difference between the highest close and the lowest low over the specified period. This percentage is then multiplied by 100 to create a more readable value.

Finally, the code plots the VixFix line on the chart with a yellow color and a thickness of 2. This allows the user to easily visualize the VixFix value and incorporate it into their trading decisions.

Overall, this script provides a powerful tool for technical analysis that can help traders identify potential trend changes and market reversals.

Trend Correlation HeatmapHello everyone!

I am excited to release my trend correlation heatmap, or trend heatmap for short.

Per usual, I think its important to explain the theory before we get into the use of the indicator, so let's get into the theory!

The theory:

So what is a correlation?

Correlation is the relationship one variable has to another. Correlations are the basis of everything I do as a quantitative trader. From the correlation between the same variables (i.e. autocorrelation), the correlation between other variables (i.e. VIX and SPY, SPY High and SPY Low, DXY and ES1! close, etc.) and, as well, the correlation between price and time (time series correlation).

This may sound very familiar to you, especially if you are a user, observer or follower of my ideas and/or indicators. Ninety-five percent of my indicators are a function of one of those three things. Whether it be a time series based indicator (i.e.my time series indicator), whether it be autocorrelation (my autoregressive cloud indicator or my autocorrelation oscillator) or whether it be regressive in nature (i.e. my SPY Volume weighted close, or even my expected move which uses averages in lieu of regressive approaches but is foundational in regression principles. Or even my VIX oscillator which relies on the premise of correlations between tickers.) So correlation is extremely important to me and while its true I am more of a regression trader than anything, I would argue that I am more of a correlation trader, because correlations are the backbone of how I develop math models of stocks.

What I am trying to stress here is the importance of correlations. They really truly are foundational to any type of quantitative analysis for stocks. And as such, understanding the current relationship a stock has to time is pivotal for any meaningful analysis to be conducted.

So what is correlation to time and what does it tell us?

Correlation to time, otherwise known and commonly referred to as "Time Series", is the relationship a ticker's price has to the passing of time. It is displayed in the traditional Pearson Correlation Coefficient or R value and can be any value from -1 (strong negative relationship, i.e. a strong downtrend) to + 1 (i.e. a strong positive relationship, i.e. a strong uptrend). The higher or lower the value the stronger the up or downtrend is.

As such, correlation to time tells us two very important things. These are:

a) The direction of the stock; and

b) The strength of the trend.

Let's take a look at an example:

Above we have a chart of QQQ. We can see a trendline that seems to fit well. The questions we ask as traders are:

1. What is the likelihood QQQ breaks down from this trendline?

2. What is the likelihood QQQ continues up?

3. What is the likelihood QQQ does a false breakdown?

There are numerous mathematical approaches we can take to answer these questions. For example, 1 and 2 can be answered by use of a Cumulative Distribution Density analysis (CDDA) or even a linear or loglinear regression analysis and 3 can be answered, more or less, with a linear regression analysis and standard error ascertainment, or even just a general comparison using a data science approach (such as cosine similarity or Manhattan distance).

But, the reality is, all 3 of these questions can be visualized, at least in some way, by simply looking at the correlation to time. Let's look at this chart again, this time with the correlation heatmap applied:

If we look at the indicator we can see some pivotal things. These are:

1. We have 4, very strong uptrends that span both higher AND lower timeframes. We have a strong uptrend of 0.96 on the 5 minute, 50 candle period. We have a strong uptrend at the 300 candle lookback period on the 1 minute, we have a strong uptrend on the 100 day lookback on the daily timeframe period and we have a strong uptrend on the 5 minute on the 500 candle lookback period.

2. By comparison, we have 3 downtrends, all of which have correlations less than the 4 uptrends. All of the downtrends have a correlation above -0.8 (which we would want lower than -0.8 to be very strong), and all of the uptrends are greater than + 0.80.

3. We can also see that the uptrends are not confined to the smaller timeframes. We have multiple uptrends on multiple timeframes and both short term (50 to 100 candles) and long term (up to 500 candles).

4. The overall trend is strengthening to the upside manifested by a positive Max Change and a Positive Min change (to be discussed later more in-depth).

With this, we can see that QQQ is actually very strong and likely will continue at least some upside. If we let this play out:

We continued up, had one test and then bounced.

Now, I want to specify, this indicator is not a panacea for all trading. And in relation to the 3 questions posed, they are best answered, at least quantitatively, not only by correlation but also by the aforementioned methods (CDDA, etc.) but correlation will help you get a feel for the strength or weakness present with a stock.

What are some tangible applications of the indicator?

For me, this indicator is used in many ways. Let me outline some ways I generally apply this indicator in my day and swing trading:

1. Gauging the strength of the stock: The indictor tells you the most prevalent behavior of the stock. Are there more downtrends than uptrends present? Are the downtrends present on the larger timeframes vs uptrends on the shorter indicating a possible bullish reversal? or vice versa? Are the trends strengthening or weakening? All of these things can be visualized with the indicator.

2. Setting parameters for other indicators: If you trade EMAs or SMAs, you may have a "one size fits all" approach. However, its actually better to adjust your EMA or SMA length to the actual trend itself. Take a look at this:

This is QQQ on the 1 hour with the 200 EMA with 200 standard deviation bands added. If we look at the heatmap, we can see, yes indeed 200 has a fairly strong uptrend correlation of 0.70. But the strongest hourly uptrend is actually at 400 candles, with a correlation of 0.91. So what happens if we change the EMA length and standard deviation to 400? This:

The exact areas are circled and colour coded. You can see, the 400 offers more of a better reference point of supports and resistances as well as a better overall trend fit. And this is why I never advocate for getting married to a specific EMA. If you are an EMA 200 lover or 21 or 51, know that these are not always the best depending on the trend and situation.

Components of the indicator:

Ah okay, now for the boring stuff. Let's go over the functionality of the indicator. I tried to keep it simple, so it is pretty straight forward. If we open the menu here are our options:

We have the ability to toggle whichever timeframes we want. We also have the ability to toggle on or off the legend that displays the colour codes and the Max and Min highest change.

Max and Min highest change: The max and min highest change simply display the change in correlation over the previous 14 candles. An increasing Max change means that the Max trend is strengthening. If we see an increasing Max change and an increasing Min change (the Min correlation is moving up), this means the stock is bullish. Why? Because the min (i.e. ideally a big negative number) is going up closer to the positives. Therefore, the downtrend is weakening.

If we see both the Max and Min declining (red), that means the uptrend is weakening and downtrend is strengthening. Here are some examples:

Final Thoughts:

And that is the indicator and the theory behind the indicator.

In a nutshell, to summarize, the indicator simply tracks the correlation of a ticker to time on multiple timeframes. This will allow you to make judgements about strength, sentiment and also help you adjust which tools and timeframes you are using to perform your analyses.

As well, to make the indicator more user friendly, I tried to make the colours distinctively different. I was going to do different shades but it was a little difficult to visualize. As such, I have included a toggle-able legend with a breakdown of the colour codes!

That's it my friends, I hope you find it useful!

Safe trades and leave your questions, comments and feedback below!

Days in rangeThis script is a little widget that I made to do some homework on the VIX.

As you can see in the chart I was analyzing the 2008 market crash and the stats that followed it after until the market started to recover.

You can see that theory in my "Ideas" tab.

This is an interactive set of lines that you can use to count the the bars inside and outside of your chosen range, and the percentage outside that range.

You should initially enter the price range of your product in the menu and set some arbitrary dates that you can easily see on your chart.

Drag and drop the lines around to suit what price and the dates you are analyzing.

The table will display the bar count inside and outside of the range, the total bars, and the percentage outside that range.

I personally used this as a tool to study the overall average of the product, compared with the behavior during major market events.

It is currently my opinion that post 2020 analysis needs to take into account the behavior of any given product prior to 2020 when the

VIX was in its comfort zone. Not to say that a price valuation hasn't been set, but that the movement to that price was outside of "Normal Market Conditions,"

and the time factor to return to that value might be skewed. Other factors would need to be considered at that point pertaining to your specific product or corelating indicator.

I could see this tool being useful to Forex and commodities traders. But that isn't my field so that that for what it is. I do think it would perform best on something that is more

pegged to a price range. I personally would use it on product's, like the VIX, that I use as an indicator product. That is what it was designed for.

But I suppose it could be used for Mean price and time related analysis, maybe with a Vwap, SMA or other breakout style indicators.

Volume analysis might be pretty sporty. Possibly time patterns... the possibilities could be endless. Or... limited.

I am publishing this for my trade group so that it can be tinkered with to find other helpful ways to use it.

If anyone finds something interesting with other indicators, please drop a comment below and I could consider creating a script to integrate with this tool.

Typical Price Difference - TPD © with reversal zones and signalsv1.0 NOTE: The maths have been tested only for BTC and weekly time frame.

This is a concept that I came through after long long hours of VWAP trading and scalping.

The idea is pretty simple:

1) Typical Price is calculated by (h+l+c) / 3. If we take this price and adjust it to volume we get the VWAP value. The difference between this value and the close value, i call it " Typical Price Difference - TPD ".

2) We get the Historical Volatility as calculated by TradingView script and we add it up to TPD and divide it by two (average). This is what I call " The Source - TS ".

3) We apply the CCI formula to TS .

4) We calculate the Rate of Change (roc) of the CCI formula.

5) We apply the VIX FIX of Larry Williams (script used is from ChrisMoody - CM_Williams_Vix_Fix Finds Market Bottoms) *brilliant script!!!

How to use it:

a) When the (3) is over the TPD we have a bullish bias (green area). When it's under we have a bearish bias (red area).

b) If the (1) value goes over or under a certain value (CAUTION!!! it varies in different assets or timeframes) we get a Reversal Zone (RZ). Red/Green background.

c) If we are in a RZ and the VIX FIX gives a strong value (look for green bars in histogram) and roc (4) goes in the opposite direction, we get a reversal signal that works for the next week(s).

I applied this to BTC on a weekly time frame and after some corrections, it gives pretty good reversal zones and signals. Especially bottoms. Also look for divergences in the zones/signals.

As I said I have tested and confirmed it only on BTC/weekly. I need more time with the maths and pine to automatically adjust it to other time frames. You can play with it in different assets or time frames to find best settings by hand.

Feel free to share your thoughts or ideas on this.

P.S. I realy realy realy try to remember when or how or why I came up with the idea to combine typical price with historical volatility and CCI. I can't! It doesn't make any sense LOL

VANILLA BUY SELLThis script uses three components:-

USEFUL MA by @ALEXGROVER

SUPERTREND INDICATOR(3 supertrend with different ATR and multiplier) provided by tradingview.

VIX FEAR GAUGE by @bizkitbr

To make it easy and line free, supertrend lines have been removed but the color fill has been kept. This makes the chart clean.

For option traders, direction and momentum is everything. Hence, two need to be really clear:-

a) BUY OR SELL

b) Whether momentum exists of not

While rise is charecterised by a steady pace, a fall is charecterized by a rapid decline.

So in order to make the best use of of the charecters, a careful interpretation and backtesting has been done to enable buy sell only when vix conditions are met.

BUY SIGNAL

A buy signal is generated on following conditions:-

a)PRICE CLOSE ABOVE USEFUL MA

B)ALL THREE SUPERTRENDS ARE GREEN

C)VIXFIX IS BELOW 0.18.

SELL SIGNAL

This is generated when following is met:-

A) PRICE BELOW USEFUL MA

B)ALL THREE SUPERTRENDS ARE RED

C)VIXFIX IS ABOBE 0.18

ADDITIONALLY, A SMALL BACKGROUND COLOR CHANGE PROVIDED FOR AREAS WHERE THERE IS A BUY OR SELL.

Either labels can be used or background colours referred for seeing buy or sell.

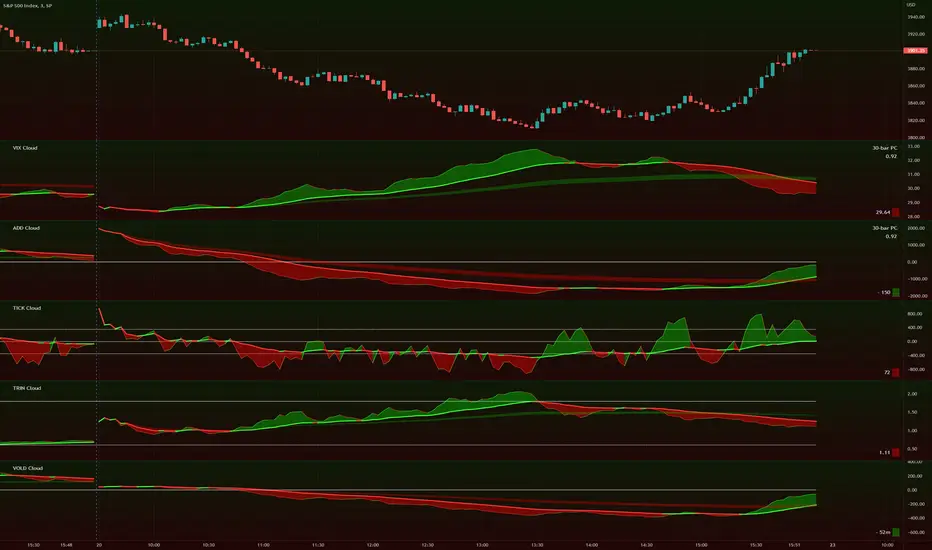

TIG's Market Internals Clouds Indicator v2.0=================================

== GENERAL INTRODUCTION

=================================

If you find market internals inform your intraday trading decisions (SPX, ES futures, SPY or more generally) this may be helpful.

Currently available internals are:

- ADD

- TICK

- TRIN

- VIX

- VOLD

Also, you can display your favorite alternative market internal (or BTC, if you want?!) by entering the relevant ticker in the 'Custom' field

=================================

== NOTES

=================================

The default EMA lengths seem to work reasonably well for 1, 2, 3-minute timeframes (except for TICK - you may wish to apply a bit more smoothing to TICK to reduce the noise)

Of course; you can add this indicator to your chart multiple times, and display a different internal each time.

The default Text Color is set as a mid-grey, which is readable in both TV color schemes. I prefer dark mode, and so I change the text color to white. You can't see the scheme setting from within a script, unfortunately, so this can't be automated.

=================================

== EXPERIMENTAL FEATURE

=================================

As a free bonus, the indicator can display the 30-bar (default) Pearson Correlation Coefficient between the internal, and price action (based on the super-fast EMA, to give a bit of smoothing). This may give a clue as to whether or not the market is aligned with what the internal is doing, or if the market (today) is not correlated with the particular internal.

Very roughly speaking:

- 0.50 means that 50% of the price action can be explained by reference to the internal. This is about the same level of correlation between VIX and Actual Move

- 0.80 suggests pretty strong correlation

I don't know why (yet) but sometimes this works, and sometimes it doesn't display a sensible figure.

=================================

== QUESTIONS AND FEEDBACK

=================================

If you have any general questions about market internals, Google is your friend.

If you have any specific queries, bug reports, feature requests or general feedback about this indicator please leave a comment below, and I'll get back to you ASAP!

Volatility Risk Premium (VRP) 1.0ENGLISH

This indicator (V-R-P) calculates the (one month) Volatility Risk Premium for S&P500 and Nasdaq-100.

V-R-P is the premium hedgers pay for over Realized Volatility for S&P500 and Nasdaq-100 index options.

The premium stems from hedgers paying to insure their portfolios, and manifests itself in the differential between the price at which options are sold (Implied Volatility) and the volatility the S&P500 and Nasdaq-100 ultimately realize (Realized Volatility).

I am using 30-day Implied Volatility (IV) and 21-day Realized Volatility (HV) as the basis for my calculation, as one month of IV is based on 30 calendaristic days and one month of HV is based on 21 trading days.

At first, the indicator appears blank and a label instructs you to choose which index you want the V-R-P to plot on the chart. Use the indicator settings (the sprocket) to choose one of the indices (or both).

Together with the V-R-P line, the indicator will show its one year moving average within a range of +/- 15% (which you can change) for benchmarking purposes. We should consider this range the “normalized” V-R-P for the actual period.

The Zero Line is also marked on the indicator.

Interpretation

When V-R-P is within the “normalized” range, … well... volatility and uncertainty, as it’s seen by the option market, is “normal”. We have a “premium” of volatility which should be considered normal.

When V-R-P is above the “normalized” range, the volatility premium is high. This means that investors are willing to pay more for options because they see an increasing uncertainty in markets.

When V-R-P is below the “normalized” range but positive (above the Zero line), the premium investors are willing to pay for risk is low, meaning they see decreasing uncertainty and risks in the market, but not by much.

When V-R-P is negative (below the Zero line), we have COMPLACENCY. This means investors see upcoming risk as being lower than what happened in the market in the recent past (within the last 30 days).

CONCEPTS:

Volatility Risk Premium

The volatility risk premium (V-R-P) is the notion that implied volatility (IV) tends to be higher than realized volatility (HV) as market participants tend to overestimate the likelihood of a significant market crash.

This overestimation may account for an increase in demand for options as protection against an equity portfolio. Basically, this heightened perception of risk may lead to a higher willingness to pay for these options to hedge a portfolio.

In other words, investors are willing to pay a premium for options to have protection against significant market crashes even if statistically the probability of these crashes is lesser or even negligible.

Therefore, the tendency of implied volatility is to be higher than realized volatility, thus V-R-P being positive.

Realized/Historical Volatility

Historical Volatility (HV) is the statistical measure of the dispersion of returns for an index over a given period of time.

Historical volatility is a well-known concept in finance, but there is confusion in how exactly it is calculated. Different sources may use slightly different historical volatility formulas.

For calculating Historical Volatility I am using the most common approach: annualized standard deviation of logarithmic returns, based on daily closing prices.

Implied Volatility

Implied Volatility (IV) is the market's forecast of a likely movement in the price of the index and it is expressed annualized, using percentages and standard deviations over a specified time horizon (usually 30 days).

IV is used to price options contracts where high implied volatility results in options with higher premiums and vice versa. Also, options supply and demand and time value are major determining factors for calculating Implied Volatility.

Implied Volatility usually increases in bearish markets and decreases when the market is bullish.

For determining S&P500 and Nasdaq-100 implied volatility I used their volatility indices: VIX and VXN (30-day IV) provided by CBOE.

Warning

Please be aware that because CBOE doesn’t provide real-time data in Tradingview, my V-R-P calculation is also delayed, so you shouldn’t use it in the first 15 minutes after the opening.

This indicator is calibrated for a daily time frame.

ESPAŇOL

Este indicador (V-R-P) calcula la Prima de Riesgo de Volatilidad (de un mes) para S&P500 y Nasdaq-100.

V-R-P es la prima que pagan los hedgers sobre la Volatilidad Realizada para las opciones de los índices S&P500 y Nasdaq-100.

La prima proviene de los hedgers que pagan para asegurar sus carteras y se manifiesta en el diferencial entre el precio al que se venden las opciones (Volatilidad Implícita) y la volatilidad que finalmente se realiza en el S&P500 y el Nasdaq-100 (Volatilidad Realizada).

Estoy utilizando la Volatilidad Implícita (IV) de 30 días y la Volatilidad Realizada (HV) de 21 días como base para mi cálculo, ya que un mes de IV se basa en 30 días calendario y un mes de HV se basa en 21 días de negociación.

Al principio, el indicador aparece en blanco y una etiqueta le indica que elija qué índice desea que el V-R-P represente en el gráfico. Use la configuración del indicador (la rueda dentada) para elegir uno de los índices (o ambos).

Junto con la línea V-R-P, el indicador mostrará su promedio móvil de un año dentro de un rango de +/- 15% (que puede cambiar) con fines de evaluación comparativa. Deberíamos considerar este rango como el V-R-P "normalizado" para el período real.

La línea Cero también está marcada en el indicador.

Interpretación

Cuando el V-R-P está dentro del rango "normalizado",... bueno... la volatilidad y la incertidumbre, como las ve el mercado de opciones, es "normal". Tenemos una “prima” de volatilidad que debería considerarse normal.

Cuando V-R-P está por encima del rango "normalizado", la prima de volatilidad es alta. Esto significa que los inversores están dispuestos a pagar más por las opciones porque ven una creciente incertidumbre en los mercados.

Cuando el V-R-P está por debajo del rango "normalizado" pero es positivo (por encima de la línea Cero), la prima que los inversores están dispuestos a pagar por el riesgo es baja, lo que significa que ven una disminución, pero no pronunciada, de la incertidumbre y los riesgos en el mercado.

Cuando V-R-P es negativo (por debajo de la línea Cero), tenemos COMPLACENCIA. Esto significa que los inversores ven el riesgo próximo como menor que lo que sucedió en el mercado en el pasado reciente (en los últimos 30 días).

CONCEPTOS:

Prima de Riesgo de Volatilidad

La Prima de Riesgo de Volatilidad (V-R-P) es la noción de que la Volatilidad Implícita (IV) tiende a ser más alta que la Volatilidad Realizada (HV) ya que los participantes del mercado tienden a sobrestimar la probabilidad de una caída significativa del mercado.

Esta sobreestimación puede explicar un aumento en la demanda de opciones como protección contra una cartera de acciones. Básicamente, esta mayor percepción de riesgo puede conducir a una mayor disposición a pagar por estas opciones para cubrir una cartera.

En otras palabras, los inversores están dispuestos a pagar una prima por las opciones para tener protección contra caídas significativas del mercado, incluso si estadísticamente la probabilidad de estas caídas es menor o insignificante.

Por lo tanto, la tendencia de la Volatilidad Implícita es de ser mayor que la Volatilidad Realizada, por lo cual el V-R-P es positivo.

Volatilidad Realizada/Histórica

La Volatilidad Histórica (HV) es la medida estadística de la dispersión de los rendimientos de un índice durante un período de tiempo determinado.

La Volatilidad Histórica es un concepto bien conocido en finanzas, pero existe confusión sobre cómo se calcula exactamente. Varias fuentes pueden usar fórmulas de Volatilidad Histórica ligeramente diferentes.

Para calcular la Volatilidad Histórica, utilicé el enfoque más común: desviación estándar anualizada de rendimientos logarítmicos, basada en los precios de cierre diarios.

Volatilidad Implícita

La Volatilidad Implícita (IV) es la previsión del mercado de un posible movimiento en el precio del índice y se expresa anualizada, utilizando porcentajes y desviaciones estándar en un horizonte de tiempo específico (generalmente 30 días).

IV se utiliza para cotizar contratos de opciones donde la alta Volatilidad Implícita da como resultado opciones con primas más altas y viceversa. Además, la oferta y la demanda de opciones y el valor temporal son factores determinantes importantes para calcular la Volatilidad Implícita.

La Volatilidad Implícita generalmente aumenta en los mercados bajistas y disminuye cuando el mercado es alcista.

Para determinar la Volatilidad Implícita de S&P500 y Nasdaq-100 utilicé sus índices de volatilidad: VIX y VXN (30 días IV) proporcionados por CBOE.

Precaución

Tenga en cuenta que debido a que CBOE no proporciona datos en tiempo real en Tradingview, mi cálculo de V-R-P también se retrasa, y por este motivo no se recomienda usar en los primeros 15 minutos desde la apertura.

Este indicador está calibrado para un marco de tiempo diario.

Implied minus Historical VolatilityJust a simple comparison of 30 day historical volatility versus 30 day implied volatility(VIX). In general, when VIX is way above realized or historical Vol, in general that is quite bullish. Backtest will be available soon.

Standard Error of the Estimate -Jon Andersen- V2Original implementation idea of bands by:

Traders issue: Stocks & Commodities V. 14:9 (375-379):

Standard Error Bands by Jon Andersen

Standard Error Bands are quite different than Bollinger's.

First, they are bands constructed around a linear regression curve.

Second, the bands are based on two standard errors above and below this regression line.

The error bands measure the standard error of the estimate around the linear regression line.

Therefore, as a price series follows the course of the regression line the bands will narrow , showing little error in the estimate. As the market gets noisy and random, the error will be greater resulting in wider bands .

Thanks to the work of @glaz & @XeL_arjona

In this version you can change the type of moving averages and the source of the bands.

Add a few studies of @dgtrd

1- ADX Colored Directional Movement Line

Directional Movement (DMI) (created by J. Welles Wilder ) consists of the Average Directional Index ( ADX ), to define whether or not there is a trend present, and Plus Directional Indicator (+D I) and Minus Directional Indicator (-D I) serve the purpose of determining trend direction

ADX Colored Directional Movement Line is custom interpretation of Directional Movement (DMI) with aim to present all 3 DMI indicator components with SINGLE line and ability to be added on top of the price chart (main chart)

How to interpret :

* triangle shapes:

▲- bullish : diplus >= diminus

▼- bearish : diplus < diminus

* colors:

green - bullish trend : adx >= strongTrend and di+ > di-

red - bearish trend : adx >= strongTrend and di+ < di-

gray - no trend : weekTrend < adx < strongTrend

yellow - week trend : adx < weekTrend

* color density:

darker : adx growing

lighter : adx falling

2- Volatility Colored Price/MA Line

Custom interpretation of the idea “Prices high above the moving average (MA) or low below it are likely to be remedied in the future by a reverse price movement”. Further details can be found under study “Price Distance to its MA by DGT”

How to interpret :

-▲ – Bullish , Price Action above Moving Average

-▼ – Bearish , Price Action below Moving Average

-Gray/Black - Low Volatility

-Green/Red – Price Action in Threshold Bands

-Dark Green/Red – Price Action Exceeds Threshold Bands

3- Volume Weighted Bar s

Volume Weighted Bars, a study of Kıvanç Özbilgiç, aims to present whether volume supports price movements. Volume Weighted Bars are calculated based on volume moving average.

How to interpret :

-Volume high above the volume moving average be displayed with red/green colors

-Average volume values will remain as they are and

-Volume low below the volume moving average will be indicated with darker colors

4- Fear & Greed index value, using technical anlysis approach calculated based on :

⮩1 - Price Momentum : Price Distance to its Moving Average

⮩2 - Strenght : Rate of Return, price movement over a period of time

⮩3 - Money Flow : Chaikin Money Flow, quantify changes in buying and selling pressure. CMF calculations is based on Accumulation/Distribution

⮩4 - Market Volatility : CBOE Volatility Index ( VIX ), the Volatility Index, or VIX , is a real-time market index that represents the market's expectation. It provides a measure of market risk and investors' sentiments

⮩5 -Safe Haven Demand: in this study GOLD demand is assumed

SPY Ninja Oscillator

SPY Ninja Oscillator correlates the true strength index exponential moving averages of SPY (green) and VIX (red) together. In doing so we can determine the start of trend shifts via SPY / VIX convergence in addition to crossover, with potential market entries and exits represented by the vertical green and red bars.

MACD and RSI have been scaled proportionally to the oscillator range ( for rsi: (rsi-50)*. 01 , and for macd: macd /3) and when overlaid and used in conjunction with the market vertical entry and exit signals, potential trend prediction becomes much more apparent.