Relative Strength Volatility Adjusted Ema [CC]The Relative Strength Volatility Adjusted Exponential Moving Average was created by Vitali Apirine (Stocks and Commodities Mar 2022) and this is his final indicator of his recent Relative Strength series. I published both of the previous indicators, Relative Strength Volume Adjusted Exponential Moving Average and Relative Strength Exponential Moving Average

This indicator is particularly unique because it uses the Volatility Index (VIX) symbol as the default to determine volatility and uses this in place of the current stock's price into a typical relative strength calculation. As you can see in the chart, it follows the price much closer than the other two indicators and so of course this means that this indicator is best for choppy markets and the other two are better for trending markets. I would of course recommend to experiment with this one and see what works best for you.

I have included strong buy and sell signals in addition to normal ones so strong signals are darker in color and normal signals are lighter in color. Buy when the line turns green and sell when it turns red.

Let me know if there are any other indicators or scripts you would like to see me publish!

在腳本中搜尋"同花顺软件+美国+VIX+恐慌指数+行情代码"

Nasdaq VXN Volatility Warning IndicatorToday I am sharing with the community a volatility indicator that uses the Nasdaq VXN Volatility Index to help you or your algorithms avoid black swan events. This is a similar the indicator I published last week that uses the SP500 VIX, but this indicator uses the Nasdaq VXN and can help inform strategies on the Nasdaq index or Nasdaq derivative instruments.

Variance is most commonly used in statistics to derive standard deviation (with its square root). It does have another practical application, and that is to identify outliers in a sample of data. Variance is defined as the squared difference between a value and its mean. Calculating that squared difference means that the farther away the value is from the mean, the more the variance will grow (exponentially). This exponential difference makes outliers in the variance data more apparent.

Why does this matter?

There are assets or indices that exist in the stock market that might make us adjust our trading strategy if they are behaving in an unusual way. In some instances, we can use variance to identify that behavior and inform our strategy.

Is that really possible?

Let’s look at the relationship between VXN and the Nasdaq100 as an example. If you trade a Nasdaq index with a mean reversion strategy or algorithm, you know that they typically do best in times of volatility . These strategies essentially attempt to “call bottom” on a pullback. Their downside is that sometimes a pullback turns into a regime change, or a black swan event. The other downside is that there is no logical tight stop that actually increases their performance, so when they lose they tend to lose big.

So that begs the question, how might one quantitatively identify if this dip could turn into a regime change or black swan event?

The Nasdaq Volatility Index ( VXN ) uses options data to identify, on a large scale, what investors overall expect the market to do in the near future. The Volatility Index spikes in times of uncertainty and when investors expect the market to go down. However, during a black swan event, historically the VXN has spiked a lot harder. We can use variance here to identify if a spike in the VXN exceeds our threshold for a normal market pullback, and potentially avoid entering trades for a period of time (I.e. maybe we don’t buy that dip).

Does this actually work?

In backtesting, this cut the drawdown of my index reversion strategies in half. It also cuts out some good trades (because high investor fear isn’t always indicative of a regime change or black swan event). But, I’ll happily lose out on some good trades in exchange for half the drawdown. Lets look at some examples of periods of time that trades could have been avoided using this strategy/indicator:

Example 1 – With the Volatility Warning Indicator, the mean reversion strategy could have avoided repeatedly buying this pullback that led to this asset losing over 75% of its value:

Example 2 - June 2018 to June 2019 - With the Volatility Warning Indicator, the drawdown during this period reduces from 22% to 11%, and the overall returns increase from -8% to +3%

How do you use this indicator?

This indicator determines the variance of VXN against a long term mean. If the variance of the VXN spikes over an input threshold, the indicator goes up. The indicator will remain up for a defined period of bars/time after the variance returns below the threshold. I have included default values I’ve found to be significant for a short-term mean-reversion strategy, but your inputs might depend on your risk tolerance and strategy time-horizon. The default values are for 1hr VXN data/charts. It will pull in variance data for the VXN regardless of which chart the indicator is applied to.

Disclaimer: Open-source scripts I publish in the community are largely meant to spark ideas or be used as building blocks for part of a more robust trade management strategy. If you would like to implement a version of any script, I would recommend making significant additions/modifications to the strategy & risk management functions. If you don’t know how to program in Pine, then hire a Pine-coder. We can help!

Commitment of Traders: Financial Metrics█ OVERVIEW

This indicator displays the Commitment of Traders (COT) financial data for futures markets.

█ CONCEPTS

Commitment of Traders (COT) data is tallied by the Commodity Futures Trading Commission (CFTC) , a US federal agency that oversees the trading of derivative markets such as futures in the US. It is weekly data that provides traders with information about open interest for an asset. The CFTC oversees derivative markets traded on different exchanges, so COT data is available for assets that can be traded on CBOT, CME, NYMEX, COMEX, and ICEUS.

A detailed description of the COT report can be found on the CFTC's website .

COT data is separated into three notable reports: Legacy, Disaggregated, and Financial. This indicator presents data from the COT Financial (Traders in Financial Futures) report. The Financial report includes financial contracts, such as currencies, US Treasury securities, Eurodollars, stocks, VIX and Bloomberg commodity index. As such, the TFF data is limited to financial-related tickers. The TFF report breaks down the reportable open interest positions into four classifications: Dealer/Intermediary, Asset Manager/Institutional, Leveraged Funds, and Other Reportables.

Our other COT indicators are:

• Commitment of Traders: Legacy Metrics

• Commitment of Traders: Disaggregated Metrics

• Commitment of Traders: Total

█ HOW TO USE IT

Load the indicator on an active chart (see here if you don't know how).

By default, the indicator uses the chart's symbol to derive the COT data it displays. You can also specify a CFTC code in the "CFTC code" field of the script's inputs to display COT data from a symbol different than the chart's.

The rest of this section documents the script's input fields.

Metric

Each metric represents a different column of the Commitment of Traders report. Details are available in the explanatory notes on the CFTC's website .

Here is a summary of the metrics:

• "Open Interest" is the total of all futures and/or option contracts entered into and not yet offset by a transaction, by delivery, by exercise, etc.

The aggregate of all long open interest is equal to the aggregate of all short open interest.

• "Traders Total" is the number of all unique reportable traders, regardless of the trading direction.

• "Traders Dealer" is the number of traders classified as a "Dealer/Intermediary" reported holding any position with the specified direction.

A "producer/merchant/processor/user" is an entity typically described as the “sell side” of the market.

Though they may not predominately sell futures, they do design and sell various financial assets to clients.

They tend to have matched books or offset their risk across markets and clients.

Futures contracts are part of the pricing and balancing of risk associated with the products they sell and their activities.

• "Traders Asset Manager" is the number of traders classified as "Asset Manager/Institutional" reported holding any position with the specified direction.

These are institutional investors, including pension funds, endowments, insurance companies,

mutual funds and those portfolio/investment managers whose clients are predominantly institutional.

• "Traders Leveraged Funds" is the number of traders classified as "Leveraged Funds" reported holding any position with the specified direction.

These are typically hedge funds and various types of money managers. The traders may be engaged in managing and

conducting proprietary futures trading and trading on behalf of speculative clients.

• "Traders Other Reportable" is the number of reportable traders that are not placed in any of the three categories specified above.

The traders in this category mostly are using markets to hedge business risk, whether that risk is related to foreign exchange, equities or interest rates.

This category includes corporate treasuries, central banks, smaller banks, mortgage originators, credit unions and any other reportable traders not assigned to the other three categories.

• "Traders Total Reportable" is the number of all traders reported holding any position with the specified direction.

To determine the total number of reportable traders in a market, a trader is counted only once whether or not the trader appears in more than one category.

As a result, the sum of the numbers of traders in each separate category typically exceeds the total number of reportable traders.

• "Dealer/Asset Manager/Leveraged Funds/Total Reportable/Other Reportable Positions -- all positions held by the traders of the specified category.

• "Nonreportable Positions" is the long and short open interest derived by subtracting the total long and short reportable positions from the total open interest.

Accordingly, the number of traders involved and the commercial/non-commercial classification of each trader are unknown.

• "Concentration Gross/Net LT 4/8 TDR" is the percentage of open interest held by 4/8 of the largest traders, by gross/net positions,

without regard to whether they are classified as commercial or non-commercial. The Net position ratios are computed after offsetting each trader’s equal long and short positions.

A reportable trader with relatively large, balanced long and short positions in a single market, therefore,

may be among the four and eight largest traders in both the gross long and gross short categories, but will probably not be included among the four and eight largest traders on a net basis.

Direction

Each metric is available for a particular set of directions. Valid directions for each metric are specified with its name in the "Metric" field's dropdown menu.

COT Selection Mode

This field's value determines how the script determines which COT data to return from the chart's symbol:

- "Root" uses the root of a futures symbol ("ES" for "ESH2020").

- "Base currency" uses the base currency in a forex pair ("EUR" for "EURUSD").

- "Currency" uses the quote currency, i.e., the currency the symbol is traded in ("JPY" for "TSE:9984" or "USDJPY").

- "Auto" tries all modes, in turn.

If no COT data can be found, a runtime error is generated.

Note that if the "CTFC Code" input field contains a code, it will override this input.

Futures/Options

Specifies the type of Commitment of Traders data to display: data concerning only Futures, only Options, or both.

CTFC Code

Instead of letting the script generate the CFTC COT code from the chart and the "COT Selection Mode" input when this field is empty, you can specify an unrelated CFTC COT code here, e.g., 001602 for wheat futures.

Look first. Then leap.

[Nic] Intraday Vix LabelsPrints intraday percent change of VIX9D, VVIX, PCC, and any other arbitrary symbol on a table for quick reference.

vix_vx_regressionAn example of the linear regression library, showing the regression of VX futures on the VIX. The beta might help you weight VX futures when hedging SPX vega exposure. A VX future has point multiplier of 1000, whereas SPX options have a point multiplier of 100. Suppose the front month VX future has a beta of 0.6 and the front month SPX straddle has a vega of 8.5. Using these approximations, the VX future will underhedge the SPX straddle, since (0.6 * 1000) < (8.5 * 100). The position will have about 2.5 ($250) vega. Use the R^2 (coefficient of determination) to check how well the model fits the relationship between VX and VIX. The further from one this value, the less useful the model.

(Note that the mini, VXM futures also have a 100 point multiplier).

rv_iv_vrpThis script provides realized volatility (rv), implied volatility (iv), and volatility risk premium (vrp) information for each of CBOE's volatility indices. The individual outputs are:

- Blue/red line: the realized volatility. This is an annualized, 20-period moving average estimate of realized volatility--in other words, the variability in the instrument's actual returns. The line is blue when realized volatility is below implied volatility, red otherwise.

- Fuchsia line (opaque): the median of realized volatility. The median is based on all data between the "start" and "end" dates.

- Gray line (transparent): the implied volatility (iv). According to CBOE's volatility methodology, this is similar to a weighted average of out-of-the-money ivs for options with approximately 30 calendar days to expiration. Notice that we compare rv20 to iv30 because there are about twenty trading periods in thirty calendar days.

- Fuchsia line (transparent): the median of implied volatility.

- Lightly shaded gray background: the background between "start" and "end" is shaded a very light gray.

- Table: the table shows the current, percentile, and median values for iv, rv, and vrp. Percentile means the value is greater than "N" percent of all values for that measure.

-----

Volatility risk premium (vrp) is simply the difference between implied and realized volatility. Along with implied and realized volatility, traders interpret this measure in various ways. Some prefer to be buying options when there volatility, implied or realized, reaches absolute levels, or low risk premium, whereas others have the opposite opinion. However, all volatility traders like to look at these measures in relation to their past values, which this script assists with.

By the way, this script is similar to my "vol premia," which provides the vrp data for all of these instruments on one page. However, this script loads faster and lets you see historical data. I recommend viewing the indicator and the corresponding instrument at the same time, to see how volatility reacts to changes in the underlying price.

Augmented Dickey–Fuller (ADF) mean reversion testThe augmented Dickey-Fuller test (ADF) is a statistical test for the tendency of a price series sample to mean revert .

The current price of a mean-reverting series may tell us something about the next move (as opposed, for example, to a geometric Brownian motion). Thus, the ADF test allows us to spot market inefficiencies and potentially exploit this information in a trading strategy.

Mathematically, the mean reversion property means that the price change in the next time period is proportional to the difference between the average price and the current price. The purpose of the ADF test is to check if this proportionality constant is zero. Accordingly, the ADF test statistic is defined as the estimated proportionality constant divided by the corresponding standard error.

In this script, the ADF test is applied in a rolling window with a user-defined lookback length. The calculated values of the ADF test statistic are plotted as a time series. The more negative the test statistic, the stronger the rejection of the hypothesis that there is no mean reversion. If the calculated test statistic is less than the critical value calculated at a certain confidence level (90%, 95%, or 99%), then the hypothesis of a mean reversion is accepted (strictly speaking, the opposite hypothesis is rejected).

Input parameters:

Source - The source of the time series being tested.

Length - The number of points in the rolling lookback window. The larger sample length makes the ADF test results more reliable.

Maximum lag - The maximum lag included in the test, that defines the order of an autoregressive process being implied in the model. Generally, a non-zero lag allows taking into account the serial correlation of price changes. When dealing with price data, a good starting point is lag 0 or lag 1.

Confidence level - The probability level at which the critical value of the ADF test statistic is calculated. If the test statistic is below the critical value, it is concluded that the sample of the price series is mean-reverting. Confidence level is calculated based on MacKinnon (2010) .

Show Infobox - If True, the results calculated for the last price bar are displayed in a table on the left.

More formal background:

Formally, the ADF test is a test for a unit root in an autoregressive process. The model implemented in this script involves a non-zero constant and zero time trend. The zero lag corresponds to the simple case of the AR(1) process, while higher order autoregressive processes AR(p) can be approached by setting the maximum lag of p. The null hypothesis is that there is a unit root, with the alternative that there is no unit root. The presence of unit roots in an autoregressive time series is characteristic for a non-stationary process. Thus, if there is no unit root, the time series sample can be concluded to be stationary, i.e., manifesting the mean-reverting property.

A few more comments:

It should be noted that the ADF test tells us only about the properties of the price series now and in the past. It does not directly say whether the mean-reverting behavior will retain in the future.

The ADF test results don't directly reveal the direction of the next price move. It only tells wether or not a mean-reverting trading strategy can be potentially applicable at the given moment of time.

The ADF test is related to another statistical test, the Hurst exponent. The latter is available on TradingView as implemented by balipour , QuantNomad and DonovanWall .

The ADF test statistics is a negative number. However, it can take positive values, which usually corresponds to trending markets (even though there is no statistical test for this case).

Rigorously, the hypothesis about the mean reversion is accepted at a given confidence level when the value of the test statistic is below the critical value. However, for practical trading applications, the values which are low enough - but still a bit higher than the critical one - can be still used in making decisions.

Examples:

The VIX volatility index is known to exhibit mean reversion properties (volatility spikes tend to fade out quickly). Accordingly, the statistics of the ADF test tend to stay below the critical value of 90% for long time periods.

The opposite case is presented by BTCUSD. During the same time range, the bitcoin price showed strong momentum - the moves away from the mean did not follow by the counter-move immediately, even vice versa. This is reflected by the ADF test statistic that consistently stayed above the critical value (and even above 0). Thus, using a mean reversion strategy would likely lead to losses.

SQV CrossThis strategy is used to find tickers that do well when SPY and QQQ are up and VIX is down. This uses EMA's on the user defined resolution to define direction of each ticker. Trades are entered upon crossover. EMAs are user defined as well.

pricing_tableThis script helps you evaluate the fair value of an option. It poses the question "if I bought or sold an option under these circumstances in the past, would it have expired in the money, or worthless? What would be its expected value, at expiration, if I opened a position at N standard deviations, given the volatility forecast, with M days to expiration at the close of every previous trading day?"

The default (and only) "hv" volatility forecast is based on the assumption that today's volatility will hold for the next M days.

To use this script, only one step is mandatory. You must first select days to expiration. The script will not do anything until this value is changed from the default (-1). These should be CALENDAR days. The script will convert to these to business days for forecasting and valuation, as trading in most contracts occurs over ~250 business days per year.

Adjust any other variables as desired:

model: the volatility forecasting model

window: the number of periods for a lagged model (e.g. hv)

filter: a filter to remove forecasts from the sample

filter type: "none" (do not use the filter), "less than" (keep forecasts when filter < volatility), "greater than" (keep forecasts when filter > volatility)

filter value: a whole number percentage. see example below

discount rate: to discount the expected value to present value

precision: number of decimals in output

trim outliers: omit upper N % of (generally itm) contracts

The theoretical values are based on history. For example, suppose days to expiration is 30. On every bar, the 30 days ago N deviation forecast value is compared to the present price. If the price is above the forecast value, the contract has expired in the money; otherwise, it has expired worthless. The theoretical value is the average of every such sample. The itm probabilities are calculated the same way.

The default (and only) volatility model is a 20 period EWMA derived historical (realized) volatility. Feel free to extend the script by adding your own.

The filter parameters can be used to remove some forecasts from the sample.

Example A:

filter:

filter type: none

filter value:

Default: the filter is not used; all forecasts are included in the the sample.

Example B:

filter: model

filter type: less than

filter value: 50

If the model is "hv", this will remove all forecasts when the historical volatility is greater than fifty.

Example C:

filter: rank

filter type: greater than

filter value: 75

If the model volatility is in the top 25% of the previous year's range, the forecast will be included in the sample apart from "model" there are some common volatility indexes to choose from, such as Nasdaq (VXN), crude oil (OVX), emerging markets (VXFXI), S&P; (VIX) etc.

Refer to the middle-right table to see the current forecast value, its rank among the last 252 days, and the number of business days until

expiration.

NOTE: This script is meant for the daily chart only.

Bank Nifty DashboardThis shows a performance glance of Dow, India Vix and Major Constituents of Bank Nifty. Which will help to take quick decision.

Style settings

Normalized Change Mode: Allows the user to access a different interpretation of the indicator by showing the normalized first differences of each indicator in the dashboard instead of their sign

Dashboard Location: Location of the dashboard on the chart

Dashboard Size: Size of the dashboard on the chart

Text/Frame Color: Determines the color of the frame grid as well as the text color

Bullish Cell Color: Determines the color of cell associated with a rising indicator direction

Bearish Cell Color: Determines the color of cell associated with a decreasing indicator direction

Cell Transparency: Transparency of each cell

Usage

This will help to monitor the banks Performance on various time frames . You can change the stock list according to your usage/Index.

All showing in green indication strong momentum.

VixFixLinReg-IndicatorSame as VixFixLinearRegression strategy published earlier - but as indicator for those who want to use it as indicator.

Strategy can be found here:

Concept is simple:

Based on VixFix script by Chris Moody. VIX-Fix can sometime give early signal. Hence, apply linear regression for better estimation of market bottom. Area above 0 shows VixFix whereas the below 0 area is linear regression of VixFix. To estimate market bottom:

First wait for VixFix to turn lime

Then wait for linear regression to turn lime from green.

VixFix may no longer be lime by linear regression chages. But, that's ok.

Have also added option candle color to highlight bottom and alert condition for those who want to use it.

long_avgThis indicator helps you quickly see whether the series has a stationary

mean. For reference, view the indicator on VIX, which is thought to have a

long-term stationary mean. Best used on a monthly chart, since these won't

irritate the candle limit.

The red line traces the long-run mean of the series over time, while the blue

indicates its present value. The purple lines are one-standard deviation from

the mean.

Matrix Series and Vix Fix with VWAP CCI and QQE SignalsBased on @ChrisMoody Williams_VIX_Fix and @glaz Matrix Series .

This indicator identify potential zone of reversal according to momentum and volatility.

Includes VWAP CCI and QQE Signals.

Technical checklistNo one indicator is perfect. People always have their favorite indicators and maintain a bias on weighing them purely on psychological reasons other than mathematical. This technical checklist indicator collected 20 common indicators and custom ones to address the issue of a bias weighted decision.

Here, I apply machine learning using a simple sigmoid neuron network with one hidden layer and a single node to avoid artifacts. For the ease of data collection, the indicator matrix is first shown as a heatmap. Once an uptrend signal window is selected manually, an indicator matrix can be recorded in a binary format (i.e., 1 0 0 1 1 0, etc.).

For example, the following indicator matrix was retrieved from the MRNA chart (deciscion: first 5 rows, buying; last 5 rows, no buying):

1 1 0 0 0 1 1 1 1 1 0 1 0 0 1 1 0 1 1 1

1 1 0 0 1 1 1 0 0 0 1 0 1 1 0 1 0 1 1 1

0 0 1 1 0 1 0 0 0 1 1 1 0 0 1 0 0 1 0 0

1 1 0 0 0 1 1 1 1 1 1 0 1 0 0 1 0 1 0 0

0 0 1 1 0 1 1 1 0 1 1 1 0 1 1 1 0 1 0 0

1 1 0 0 1 0 1 0 0 0 0 1 0 0 0 1 0 0 1 1

1 1 0 0 0 0 1 0 0 0 0 1 0 0 1 1 0 1 1 1

0 0 0 0 1 0 1 0 0 1 1 0 0 0 0 0 0 1 0 0

0 0 0 0 0 0 1 0 0 0 1 0 0 1 0 0 0 1 1 1

0 0 0 0 1 0 1 0 0 0 1 0 1 0 0 0 0 1 1 1

This matrix is then used as an input to train the machine learning network. With a correlated buying decision matrix as an output:

1

1

1

1

1

0

0

0

0

0

After training, the corrected weight matrix can be applied back to the indicator. And the display mode can be changed from a heatmap into a histogram to reveal buying signals visually.

Usage:

python stock_ml.py mrna_input.txt output.txt

Weight matrix output:

1.37639407

1.67969656

1.0162141

1.3184323

-1.88888442

8.32928588

-5.35777295

3.08739916

3.06464844

0.82986227

-0.53092333

-1.95045383

4.14441698

2.99179435

-0.08379438

1.70379704

0.4173048

-1.51870972

-2.14284707

-2.08513252

Corresponding indicators to the weight matrix:

1. Breakout

2. Reversal

3. Crossover of ema20 and ema60

4. Crossover of ema20 and ema120

5. MACD golden cross

6. Long cycle (MACD crossover 0)

7. RSI not overbought

8. KD not overbought and crossover

9. OBV uptrend

10. Bullish gap

11. High volume

12. Breakout up fractal

13. Rebounce of down fractal

14. Convergence

15. Turbulence reversal

16. Low resistance

17. Bullish trend (blue zone)

18. Bearish trend (red zone)

19. VIX close above ema20

20. SPY close below ema20

PS. It is recommended not to use default settings but to train your weight matrix based on underlying and timeframe.

Fear/Greed IndexMy goal was to create something akin to the Fear & Greed Index ( money.cnn.com ) that CNN and others do.

A Fear/Greed Index can be used by any trader or investor but I believe it's best viewed with a contrarian's eye--

When the market appears to be signalling Extreme Fear, that is a good place to start buying from emotional players who want to sell no matter the price

When signalling Extreme Greed, that may be a good place to start taking profits off or getting hedged, as there may be too much exuberance in the air

Important to note and remember, however, is that there can often times be fear in the air for good reasons! I like to see this as if we dip into extreme fear and return shortly after, the fear may warrant constraint from buying, or returning back to extreme greed may be a very strong market extension

The script draws from several other tickers which I have read and personally observed to be decent macro correlations for the stock market (specifically the SP500). For the state of each of these metrics I gave a rating, good or bad, then added them together and put it into your standard Stochastic.

These macro correlations include--

The % of stocks in the SP500 above multiple Simple Moving Average lengths

VIX and its term-structure (contango, backwardation)

Treasury Bonds

Gold

Junk/High Yield Bonds

The Put/Call Ratio

The SP500 Options Skew

Advancing and Declining Issues

On some of these I opted to use a function for the Relative Momentum Index instead of RSI, as the RMI oscillates better (in my opinion). I also used a Band-Pass Filter/Double EMA for smoothing the results of the stochastic.

A LOT of these numbers were made to my own observation and discretion and can get out-dated over time. With that said, PLEASE feel free to revise, fine tune, modify this as you wish to optimize yours. And please let me know if I have made any mistakes here or something should be added.

CC - Array-meta Consolidated Interval Display (ACID)This script extends my other two Array examples (which I've also provided to you open source):

The Ticker-centric 5m,15m,45m,1h,4h,1d resolution labels using arrays:

And the more Macro VIX,GLD,TLT,QQQ,SPY,IWM 1d resolution labels using arrays:

This script aims to show how to use min/max/avg with Arrays easily. My next example after this will be exploring the usage of variance versus covariance ratios over different periodic interval resolutions. Currently, this is using the following intervals: 5m,15m,45m,1h,4h,1d. It takes these intervals, calculates the values at those resolutions and puts the absolute min and max from the 5 minute to the 1 day resolutions.

It's more of an example of the power that arrays can hold, as all this truly is right now is a min/max bound calculator. The real gem lies in the avg calculators for multiple resoltuions tied into a single label with readable data. Check out the code and let me know what you think. If you need more examples, the other two scripts I mentioned before are also open source.

Using this on intervals of less than 1D sometimes times out, the way I wrote it is memory intensive, may not work for non-pro users.

Thanks!

NONE OF THIS IS FOREWARD LOOKING STATEMENTS, THIS IS NOT A PREDECTIVE ANALYSIS TOOL. THIS IS A RESEARCH ATTEMPT AT A NOVEL INDICATOR. I am not responsible for outcomes using it.

Please use and give criticisms freely. I am experimenting with combining resolutions and comparing covariance values at different levels right now, so let me know your thoughts! The last indicator will likely not be open source, but may be depending on how complex I get.

CC - Macro Consolidated Interval Display (MCID)Ever wish you didn't have to rapidly flip between 6 different tickers to get the full picture?

Yeah, me too. Do you also wish that you kind of understood how the shift / unshift function works for arrays?

Yeah, I did too. Both of those birds are taken care of with one stone!

The Macro Consolidated Interval Display uses the new Array structure and security to display data for VIX, GLD, TLT, QQQ, SPY and IWM (at a 1D interval) SIMUTANEOUSLY! Regardless of which ticker you're looking at you can get the full picture of macro futures data without flipping around to get it.

This is my first script trying to use arrays. It basically shows the following a 1d interval:

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for VIX.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for GLD.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for TLT.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for QQQ.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for SPY.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP for IWM

To make it more or less busy, I've allowed you to toggle off any of the levels you wish. I've also chosen to leave this as open source, as it's nothing too experimental, and I hope that it can gain some traction as an Array example that the public can use! If you don't like the different values that are shown, use this source code example as a spring-board to put values that you do care about onto the labels.

If this code has helped you at all please drop me a like or some constructive criticism if you do not think it's worth a like.

Good luck and happy trading friends. This should be compatible with my CID as well:

If this gets traction, I will post something similar for a dynamic combination of tickers and intervals that you can set yourself.

CC - Consolidated Interval Display (CID)Ever wish you didn't have to rapidly flip between 6 different intervals to get the full picture?

Yeah, me too. Do you also wish that you kind of understood how the shift / unshift function works for arrays?

Yeah, I did too. Both of those birds are taken care of with one stone!

The Consolidated Interval Display uses the new Array structure and security to display data for 5m, 15m, 45m, 1h, 4h and 1d intervals SIMUTANEOUSLY! Regardless of which interval you're looking at you can get the full picture of numerical data without flipping around to get it.

This is my first script trying to use arrays. It basically shows the following for the given ticker:

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP at the 5 minute level.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP at the 15 minute level.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP at the 45 minute level.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP at the 1 hour level.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP at the 4 hour level.

ATR14, RSI7, RSI14, SMA50, SMA200 and VWAP at the 1 day level.

To make it more or less busy, I've allowed you to toggle off any of the levels you wish. I've also chosen to leave this as open source, as it's nothing too experimental, and I hope that it can gain some traction as an Array example that the public can use! If you don't like the different values that are shown, use this source code example as a spring-board to put values that you do care about onto the labels.

If this code has helped you at all please drop me a like or some constructive criticism if you do not think it's worth a like.

Good luck and happy trading friends.

If this gets traction, I will post something similar for a combination of SPY, VIX, GOLD, QQQ, IWM and TLT.

Risk RangeThis indicator creates risk ranges using implied volatility (VIX) or historical volatility, skewness ( Cboe SKEW or estimate ) and kurtosis.

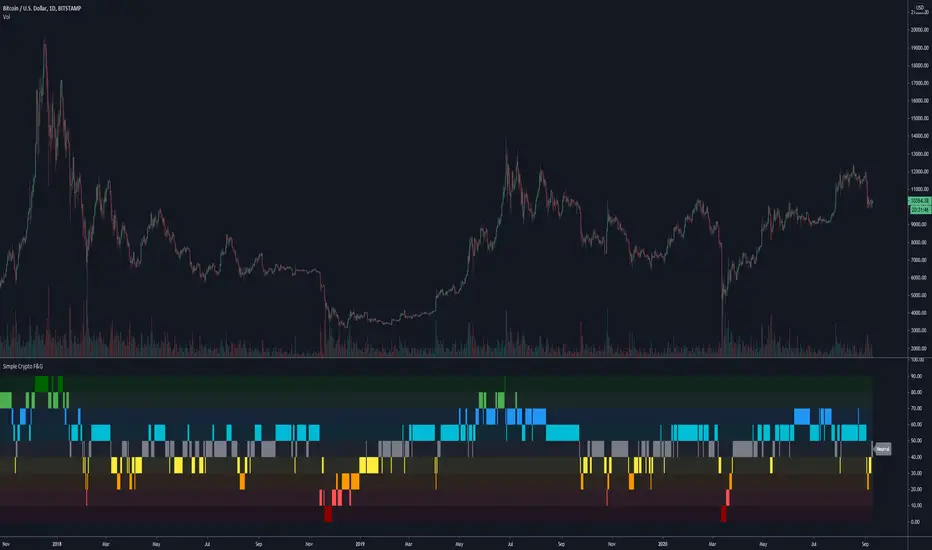

Simplified Crypto Fear & Greed DisplayA more simplified view of a Fear & Greed index.

This script has been made public because it uses Trading Psychology - Fear & Greed Index by DGT as the basis/inspiration for it.

I've re-imagined the visuals in order to display F&G data differently to the more traditional versions of the indicator floating around, as well as adapting it's calculations and reference assets for use with Crypto markets.

It's aim is to show the current status / mindset of market participants at a quick glance.

When there is a lot of fear in the market it is usually a good time to look for buying opportunities.

On the flip side you can use it to spot selling opportunities when there is too much greed / FOMO in the markets.

This indicator has the option for Traditional and Crypto markets.

The Traditional option uses the tickers VIX and GOLD as part of it's calculations, where as Crypto uses BVOL24H and BTC.D in order to base it's decisions off of more relevant data.

There are also 10 levels of smoothing so play around with that to get the desired result. Depending on the asset you are looking at, smoothing of 1 or 2 may work much better than 5+

Have a play around, customize it, use it and let me know what you think.

Carl's BOTTOM DETECTOR: Williams %R + normalized ATRThis script is based on Williams %r and normalized ATR.

When William%R indicates extreme oversold conditions

and the ATR indicates extreme volatility at the same time,

then it prints an arrow below the candle.

It is based on the concept that swing lows and market bottoms

are characterized by extreme oversold momentum and

extreme volatility.

The highest tf's like the daily, show you perfect market bottoms for btc.

If you zoom in it's still good to find swing highs and lows, if necessary

you can tweak the settings.

Next to that I added grey, red, and green vertical bands to the chart.

This is based on the VIX, the SPX volatility index.

Whenever the volatility of the S&P500 crosses above a specific level

it prints a colored background band behind the candle.

Grey means high volatility, red extreme volatility (like in the covid

crisis and 2008 crisis), and green means the same as grey, but indicates

it came after a red zone and could mean strong bullish bounce momentum.

You can tweak the thresholds for the grey/green and read areas.

Options Decay Speed for 0DTEUse only for:

SPX, 5 minutes time frame

This indicator is complementing options 0DTE strategy - selling options for SPX index in the same day as they are expiring. Output of the indicator (red or green color of the curve) indicates whether is profitable to sell options at given moment at delta and VIX specified in the parameters. Changing parameter "Candles" is not recommended.

Main thought is that options expire with certain speed (theta decay) when stock doesnt move. When stock moves in unfavorable direction slowly enough, decay speed can compensate for disadvantage coming from option delta. Intuitively there must be certain speed of stock value change (expressed in stock value per 5 minutes) that is exactly compensating theta decay. This indicator calculates those two values (details below) and shows, where theta decay is faster than stock movement in the last hour and thus favorable to sell options.

Indicator gets its result from comparing two values:

1) volatility in the form of highest high and lowest low for past 12 candles (one hour in total) divided by 12 - meaning average movement of stock expressed in

2) speed of options value decay in form of combination of theta decay and option delta. Formulas are approximation of Black-Scholes model as Pine script doesnt allow for advanced functions. Approximations are accurate to 2 decimal points from market open to one hour before market close and will not indicate green when accuracy is not sufficient. Its value is also expressed in so its mutualy comparable.

My focus was not on code elegance but on practical usability.

Written by Ondřej Škop.