Volume Exponential Moving Averages (EMA)

Description:

This script is a simple script that plots a desired exponential moving average of buy and sell volume as a line chart with a tunable smoothing factor. There is a highlight on the plot area of either green or red to denote if the EMA of buy volume or sell volume is of a higher value. This indicator uses basic math of exponential averages and calculates volume using the formulas: "buy volume" = the product of total volume and the "closing price" minus the "low price" divided by "high price" minus the "low price" for a specific candle. Conversely, "sell volume" = the product of "total volume" and the "high price" minus the "close price" divided by "high price" minus the "low price" for a specific candle.

Utility:

This indicator is an effective way to gauge the acceleration/ deceleration of buyers and sellers in the market and can be used in combination with market structure and important levels to understand if buyers or sellers are taking over at any given time.

How to use this indicator:

There are two settings for this indicator:

1. The Length of the EMA: The length of the EMA can be adjusted based on your preference for a running number of candles' data. If you are interested to know short term changes in volume (e.g. over the past few candles at a major level) you can adjust this setting lower (~3-9 length). Conversely, if you are interested in volume trends over a greater number of candles you can increase this to your liking.

Personal preference : Because I am a short term daytrader/ scalper, I keep this setting at 6 length to see immediate changes in the acceleration or deceleration of buyers/ sellers.

2. The Smoothing Factor: The smoothing factor can be adjusted to further tune the size of trend you are interested in with 1 = No smoothing of the EMA line. Smoothing of the EMA line increases as the value for smoothing increases, resulting in a less volatile, more smooth EMA line. However, the more smooth the line, the less sensitive the EMA will be to immediate changes in volume pace. The less smoothing factor is applied, the more volatile data will be, resulting in quicker observation of shorter term trends. Again the same rules apply as the EMA length as these are similar in function: If you are interested to know short term changes in volume (e.g. over the past few candles at a major level) you can adjust this setting lower (~2-6). Conversely, if you are interested in volume trends over a greater number of candles you can increase this to your liking.

Personal preference : Because I am a short term daytrader/ scalper, I keep this setting at 2-4 smoothing factor to see immediate changes in the acceleration or deceleration of buyers/ sellers.

You should, of course, play with these settings to your exact preferences based on your trading style.

Tips for using this indicator:

General Use:

When the buy volume EMA is moving up, buyers are increasing the pace of buying and when the buy volume EMA is moving down, buyers are decreasing the pace of buying. Conversely, when the sell volume EMA is moving up, sellers are increasing the pace of selling and when the sell volume EMA is moving down, sellers are decreasing the pace of selling. The overall movement of the stock is relative to the combination of these rates. e.g. If both buyers and sellers are increasing at the same rate (EMAs slopes are roughly equal) there will be not a large change in price. If the slope of the buy volume EMA is greater than the slope of sell volume EMA, the price should move up. Conversely, if the slope of the sell volume EMA is greater than the slope of buy volume EMA, the price should move down.

Predicting pullbacks, reversals, and continuations:

This indicator allows you to see if buyers or sellers are increasing their pace, even if the stock price is in consolidation. This allows you to predict if out of the consolidation buyers or sellers are likely to win based on the momentum of the volume in consolidation. e.g. If price is in consolidation after an uptrend and the buy volume EMA starts to decrease, this could be a sign that buyers are running out of steam at this price level. Another example, If at a major support the buy volume EMA begins to trend up then buyers are accelerating the pace of buying at this level.

EMA crosses: There is something to be said about the point at which the buy volume EMA and sell volume EMA cross. This signifies that at this moment there is a shift in which the acceleration of one party outpaces that of the other and can result in increased speed of the movement of the stock price.

Considerations

Because volume changes constantly, this indicator is best to identify short term changes in volume that could impact price movements. It is not guaranteed to continue just because buyers or sellers have had a change in pace. Therefore it is advised to use this indicator in combination with significant price levels such as pivot points, or price levels from volume profile tools to identify the price zones where significant volume changes are likely to impact price movements. It is also advised to continue to monitor the changes in pace in buyers and sellers using this volume EMA indicator to determine if a change in pace is short lived or if it will continue for a longer duration.

Examples of use:

Bullish Reversal:

Bearish Continuation:

Bearish EMA Crossover: (Settings: Length 6, Smoothing factor 3)

Bullish EMA Crossover: (Settings: Length 6, Smoothing factor 4)

在腳本中搜尋"国泰黄金ETF联接C相关行业指数的最新政策"

Multiple Symbol Trend Screener [Pineify]Multiple Symbol Trend Screener Pineify – Ultimate Multi-Indicator Scanner for TradingView

Empower your trading with deep market insights across multiple symbols using this feature-rich Pine Script screener. The Multiple Symbol Trend Screener Pineify enables traders to monitor and compare trends, reversals, and consolidations in real-time across the biggest equity symbols on TradingView, through a synergistic blend of popular technical indicators.

Key Features

Monitor up to 15 symbols and their trends simultaneously

Integrates 7 professional-grade indicators: MA Distance, Aroon, Parabolic SAR (PSAR), ADX, Supertrend, Keltner Channel, and BBTrend

Color-coded table display for instant visual assessment

Customizable lookback periods, indicator types, and calculation methods

SEO optimized for multi-symbol trend detection, screener, and advanced TradingView indicator

How It Works

This indicator leverages TradingView’s Pine Script v6 and request.security() to process multiple symbols across selected timeframes. Data populates a dynamic table, updating each cell based on the calculated value of every underlying indicator. MA Distance highlights deviation from moving averages; Aroon flags emerging trend strength; PSAR marks potential trend reversals; ADX assesses trend momentum; Supertrend detects bullish/bearish phases; Keltner Channel and BBTrend offer volatility and power insights.

Set up your preferred symbols and timeframes

Each indicator runs its calculation per symbol using its parameter group

All results are displayed in a table for a comprehensive dashboard view

Trading Ideas and Insights

Traders can use this screener for cross-market comparison, directional bias, entry/exit filtering, and comprehensive trend evaluation. The screener is excellent for swing trading, day trading, and portfolio tracking. It enables confirmation across multiple frameworks — for example, spotting momentum with ADX before confirming direction with Supertrend and PSAR.

Identify correlated movements or divergences across selected assets

Spot synchronized trend changes for basket trading ideas

Filter symbols by volatility, strength, or trend status for precise trade selection

How Multiple Indicators Work Together

The screener’s edge lies in its intelligent correlation of popular indicators. MA Distance measures the proximity to chosen moving averages, ideal for spotting overbought/oversold conditions. Aroon reveals the strength of new price trends, PSAR indicates reversal signals, and ADX quantifies the momentum of these trends. Supertrend provides a directional phase, while Keltner Channel & BBTrend analyze volatility shifts and band compressions. This amalgamation allows for a robust, multi-dimensional market snapshot, capturing details missed by single-indicator tools.

By displaying all key metrics side-by-side, the screener enables holistic decision-making, revealing confluence zones and contradiction areas across multiple tickers and timeframes.

Unique Aspects

Original implementation combining seven independent trend and momentum indicators for each symbol

Rich customization for symbols, timeframes, and all indicator parameters

Intuitive color-coding for quick reading of bullish/bearish/neutral signals

Comprehensive dashboard for instant actionable insights

How to Use

Load the indicator onto your TradingView chart

Go to the script’s settings and input your preferred symbols and relevant timeframes

Set your desired parameters for each indicator group: Moving Average type, Aroon length, PSAR values, ADX smoothing, etc.

Observe the results in the top-right table, then use it to filter candidates and validate trade setups

The screener is suitable for all timeframes and asset classes available on TradingView. Make sure your chart’s timeframe matches the one used in the scanner for optimal accuracy.

Customization

Choose up to 15 symbols to monitor in a single dashboard

Customize lookback periods, indicator types, colors, and display settings

Configure alerting options and thresholds for advanced trade automation

Conclusion

The Multiple Symbol Trend Screener Pineify sets a new standard for multi-asset screening on TradingView. By elegantly merging seven proven technical indicators, the screener delivers powerful trend detection, reversal analysis, and volatility monitoring — all in one dashboard. Take your trading to new heights with in-depth, customizable market surveillance.

ShockDrop Alerts v1⚡ ShockDrop Alerts — Rapid Drop & Drawdown Detector

ShockDrop Alerts helps you react instantly to sudden market shocks.

It tracks both fast price drops and intraday drawdowns, plotting clean visual arrows and sending alerts when volatility spikes — so you can respond before small dips turn into major moves.

⚙️ How It Works

• Fast Drop (FAST) – detects sharp declines (e.g. 2 % in 4 minutes) using 1-minute data across any timeframe.

• Drawdown (DD) – triggers when price trades a set percentage below the day’s session high (e.g. 2 %).

Each alert type has its own independent cooldown timer and can be toggled on or off.

🎯 What You’ll See

• FAST → 🔴 red arrow above the bar (rapid drop detection)

• DD → 🟠 orange arrow below the bar (intraday drawdown)

These appear only when your defined conditions are met. Connect them to TradingView alerts for instant popup, email, mobile, or webhook notifications.

🧭 Key Features

• Detects high-velocity price shocks in real time

• Separate cooldowns for FAST and DD triggers

• Extended-hours toggle to include pre/post-market data

• Clean, clutter-free visuals — only actionable arrows

• Uses 1-minute precision data, works on any symbol or timeframe

• Supports server-side alerts (TradingView Pro +)

📬 Why Traders Use It

• Get early warnings during flash crashes or liquidity spikes

• Automate risk-based exits when markets accelerate downward

• Track SPY, QQQ, crypto, or futures for rapid reversals

• Stay alert to high-impact news events — such as surprise policy comments, earnings releases, or market-moving presidential posts — that can cause sudden volatility

Requires TradingView Pro + for continuous server-side alerting.

NYSE FOMO Indicator (Up/Down Volume Ratio)This script plots the NYSE Sentiment Gauge, based on the daily Up/Down Volume Ratio (UVOL ÷ DVOL).

It measures crowd emotion in the overall market:

• ≥ 3 = Red: FOMO, extreme buying.

• 2–3 = Yellow: Cautious optimism.

• 0.5–2 = Grey: Neutral zone.

• 0.33–0.5 = Green: Emerging fear.

• ≤ 0.33 = Bright Green: Panic selling, potential bottom.

The line color and chart background change according to these zones, visually showing shifts in market sentiment.

Swing Data - SimplifiedThe swing data indicator by jfsrev but simplified. Thank you jfsrev for your work!

Larry Williams Oops StrategyThis strategy is a modern take on Larry Williams’ classic Oops setup. It trades intraday while referencing daily bars to detect opening gaps and align entries with the prior day’s direction. Risk is managed with day-based stops, and—unlike the original—all positions are closed at the end of the session (or at the last bar’s close), not at a fixed profit target or the first profitable open.

Entry Rules

Long setup (bullish reversion): Today opens below yesterday’s low (down gap) and yesterday’s candle was bearish. Place a buy stop at yesterday’s low + Filter (ticks).

Short setup (bearish reversion): Today opens above yesterday’s high (up gap) and yesterday’s candle was bullish. Place a sell stop at yesterday’s high − Filter (ticks).

Longs are only taken on down-gap days; shorts only on up-gap days.

Protective Stop

If long, stop loss trails the current day’s low.

If short, stop loss trails the current day’s high.

Exit Logic

Positions are force-closed at the end of the session (in the last bar), ensuring no overnight exposure. There is no take-profit; only stop loss or end-of-day flat.

Notes

This strategy is designed for intraday charts (minutes/seconds) using daily data for gaps and prior-day direction.

Longs/shorts can be enabled or disabled independently.

Larry Williams Bonus Track PatternThis strategy trades the day immediately following an Inside Day, under specific directional and timing conditions. It is designed for daily-based setups but executed on intraday charts to ensure orders are placed exactly at the open of the following day, rather than at the daily bar close.

Entry Conditions

Only trades on Monday, Thursday, or Friday.

The previous day must be an Inside Day (its high is lower than the prior high and its low is higher than the prior low).

The bar before the Inside Day must be bullish (close > open).

On the following day (t):

The daily open must be below both the Inside Day’s high and the highest high of the two days before that.

A buy stop is placed at the highest high of the three previous days (Inside Day and the two days before it).

If the new day’s open is already above that level (gap up), the strategy enters long immediately at the open.

Exit Rules

Stop Loss: Fixed, defined in points or percentage (user input).

FPO (First Profitable Open): the position is closed at the first daily open after the entry day where the open price is above the average entry price (the first profitable open).

Notes

The script must be applied on an intraday timeframe (e.g., 15-minute or 1-hour) so that the strategy can:

Detect the Inside Day pattern using daily data (request.security).

Execute orders in real time at the next day’s open.

Running it directly on the daily timeframe will delay executions by one bar due to Pine Script’s evaluation model.

Larry Williams - Smash Day (SL/TP in %)This strategy implements Larry Williams’ “Smash Day” reversal concept on any symbol and timeframe (daily is the classic). A Smash Day is a bar that closes beyond a recent extreme and then potentially reverses on the next session.

TwinPulse Q Lead SPY x QQQ Intermarket Pulse 1HTwinPulse Q Lead is a concise one hour indicator for SPY and QQQ that converts three sources of market information into a single pulse line, a mode readout with BUY SELL WAIT, and compact alerts. It blends intermarket leadership between QQQ and SPY, intraday flow from the slope of session VWAP, and where the current price sits inside the regular trading hours range. The three components are normalized, fused, compressed to a stable range, and smoothed for clear thresholds. The aim is a readable intraday regime signal that helps you decide when to participate and when to stand aside.

The script is built with Pine v6, uses request security with lookahead off, and does not repaint. It is an indicator, not a strategy. It does not contain any solicitation, links, or outside references. The description is self contained and explains both logic and use so that any trader can understand the design without reading code.

What makes this original and useful

Intermarket leadership is measured directly from QQQ and SPY on your working timeframe using a Z score of the return spread. When growth is leading value heavy large caps, leadership turns positive. When it lags, leadership turns negative. This gives a real time read of the Nasdaq versus S and P tug of war that most day traders watch informally.

Intraday flow is taken from the slope of the session VWAP. A linear regression of VWAP over a short window captures whether value is rising or falling inside the day. Dividing by ATR normalizes slope by typical movement so that the signal is comparable across weeks.

Session position places price inside the current regular hours high to low. It answers whether the day is trading in the top half, the bottom half, or the middle. This is a simple but powerful context filter for breakouts and fades.

The three components are fused into one pulse, compressed with either hyperbolic tangent or softsign to keep values bounded, and then smoothed by a short EMA. This yields a stable range with a zero line so the eye can read shifts quickly.

The panel shows a human readable mode with reasons and a strength score. Traders who do not want to read lines can rely on a simple state and a compact justification that explains why the state is set.

This is not a mashup that simply overlays unrelated indicators. Each component was chosen to answer a distinct question that is common to SPY and QQQ intraday decision making. Leadership answers who is in charge, flow answers whether value inside the session is building or leaking, and position answers if price is pressing the extremes or circling the middle. The pulse ties the three together and prevents any single component from dominating.

How the calculations work

Leadership. Compute a short rate of change for SPY and QQQ. Subtract SPY from QQQ to get spread returns, then compute a rolling Z score over a longer window. Positive values mean QQQ is leading. Negative values mean SPY is leading.

Flow. Compute session VWAP on the active symbol. Regress VWAP over a short window to obtain a slope estimate. Divide by ATR to scale slope by current volatility so that a small rise on a quiet day is not treated the same as a small rise on a wild day.

Position. Track the highest high and lowest low since the start of regular hours. Place the current close inside that range on a zero to one scale, then recenter to a minus one to plus one scale. Positive means the top half of the day, negative means the bottom half.

Fusion. Multiply each component by a weight so users can emphasize or de emphasize leadership, flow, or position. Sum to a raw pulse.

Compression. Pass the raw pulse through a bounded function. Hyperbolic tangent is smooth and has natural saturation near the extremes. Softsign is faster and behaves like a smoother version of sign near zero. Compression avoids unbounded excursions and makes thresholds meaningful across days.

Smoothing. Apply a short EMA to the compressed pulse to reduce noise. This creates the main line called TwinPulse in the plot.

Thresholds. You can use static symmetric levels or adaptive levels. The adaptive option computes a mean and a standard deviation of the smoothed pulse over a user window, then sets upper and lower thresholds as mean plus or minus sigma times standard deviation. This allows thresholds to adjust across regimes. Static levels are still available for traders who want repeatable levels.

Events and mode. A long event fires when the smoothed pulse crosses the upper threshold with positive flow and any optional filters agree. A short event fires on the symmetric condition. The mode reads the current state rather than fire and forget. It returns BUY when the smoothed pulse is above the upper threshold with positive flow, SELL when the smoothed pulse is below the lower threshold with negative flow, otherwise WAIT. A cooldown controls how often events can fire so alerts do not spam during choppy periods.

Inputs and default values

The script ships with defaults chosen for SPY and QQQ on one hour charts.

Symbols. SPY and QQQ by default. You can switch to any pair. Many users may test IWM versus SPY for small cap reads.

Regular hours selector. On by default. This restricts the position factor to New York regular hours. Turn it off if you prefer full session behavior.

ROC length is three bars. Z score length is fifty bars. VWAP slope window is ten bars. ATR length is fourteen bars. Pulse smoothing length is three bars.

Compression mode. Choose hyperbolic tangent or softsign. Hyperbolic tangent is default.

Weights. Leadership and flow are one by default. Position is set to zero point seven to give a modest influence to where price sits inside the day.

Thresholds. Adaptive thresholds are on by default with a lookback of one hundred bars and a sigma width of zero point eight. Static levels at plus or minus zero point six are ready if you disable adaptive mode.

Filters. ADX filter is off by default. If you enable it, the script requires ADX above a user minimum before it will signal. Higher time frame confirmation is off by default. When enabled it compares the smoothed pulse on the confirm timeframe to zero and requires alignment for longs or shorts.

Cooldown. Three bars by default so that alerts do not trigger too frequently.

UI. Bar coloring is on by default. The panel is on by default and sits at the top right.

All request security calls use lookahead off and will not request future data. All persistent state variables are assigned in a way that prevents repainting. The indicator does not use non standard chart types in its logic.

How to use the indicator

Load a one hour chart of SPY or QQQ. Keep a clean chart so that the script output is easy to read.

Turn on regular hours if you want the session position to reflect the cash session. This is recommended for SPY and QQQ.

Watch the panel. Mode reads BUY or SELL or WAIT. The strength value is a simple vote based score that ranges from zero to one hundred. It counts leadership, flow, ADX if enabled, and higher time frame confirmation if enabled. You can use strength to filter weak states.

Consider action only when mode is BUY or SELL and the signal has not just fired on the last bar. The triangles mark where an event fired. Alerts use the same logic as the events. WAIT means stand aside.

To slow the system, enable ADX and set a higher minimum or enable higher time frame confirmation. To speed it up, disable the filters, disable adaptive thresholds, or tighten the sigma width.

When publishing, use a clean chart with only this indicator. Show the symbol and timeframe clearly and make sure the plot legend is visible. If you add drawings on the chart, only include ones that help readers understand the output.

Publication notes and compliance

This description is written in English. The title uses ASCII and only uses capital letters for common abbreviations. The script is original and explains how and why the components work together. There are no links or promotional material. The script does not claim performance. It does not use lookahead. The panel and alerts exist to help a human read and act with discipline. The indicator can be published as open source or as protected. If you choose protected, the description still allows readers to understand how the logic works without access to the code.

If you later convert the logic into a strategy for publication, use realistic commission and slippage, risk no more than a small share of equity per trade, and choose a dataset that yields a large enough sample. Explain any deviations from these default recommendations in your strategy description. Do not publish results from non standard chart types since they can mislead readers on signal timing.

Limitations and risks

Intermarket leadership is a relative measure. There are hours when both SPY and QQQ fall while leadership remains positive. Treat leadership as a context, not a stand alone trigger.

VWAP slope is a path measure inside the session. It can flip several times on a choppy day. That is why the script uses a short smoothing and an optional cooldown. Use ADX or higher time frame confirmation to avoid the worst chop.

Session position assumes a meaningful regular hours range. On half days or around openings with gaps the position factor can be less informative. If this bothers you, reduce the weight of position or turn it off.

Compression and smoothing introduce lag by design. The goal is stability and clarity. If you want earlier but noisier signals, reduce smoothing and weights, and use static thresholds.

No indicator guarantees future results. TwinPulse Q Lead is a decision aid. It should be combined with your risk rules, position size policy, and a clear exit plan. Past behavior is not a promise for the future.

Frequently asked questions

What symbols are supported. Any symbol can be used as the chart symbol. Leadership uses the two user symbols which default to SPY and QQQ. Many traders may try IWM versus SPY or DIA versus SPY.

Can I change the timeframe. Yes, but the design target is one hour. On very short timeframes the VWAP slope becomes very sensitive and you should consider stronger filters.

Does the script repaint. No. It uses request security with lookahead off and the panel updates on the last bar only. Events are based on bar close conditions unless you attach alerts on any alert function call which will still respect the logic without looking into the future.

How are the strength numbers built. The strength score is the share of aligned votes across leadership, flow, ADX if enabled, and higher time frame confirmation if enabled. A value near one hundred means many filters agree. A value near fifty means partial alignment. It is not a probability or an accuracy number.

Can I use non standard chart types. You can view the indicator on them but do not publish signals from non standard chart types because that can mislead readers about timing. Use classic candles or bars when you publish and when you test.

Why do I sometimes see BUY but the price is not moving. A BUY mode requires pulse above the upper threshold and positive flow. It does not require higher highs immediately. Treat BUY as a permission to look for entries using your own execution rules.

EMA 9/20 Crossover AlertThis EMA 9/20 Crossover Alert indicator is a technical tool used on price charts to detect and notify traders when the short-term 9-period Exponential Moving Average (EMA) crosses above or below the longer-term 20-period EMA. This crossover often signals potential shifts in market momentum, signaling possible buy or sell opportunities. The indicator visually plots both EMAs on the chart and creates alert conditions so traders can be promptly informed of these crossover events, aiding in timely decision-making without needing to constantly watch the chart. It is widely used in momentum and trend-following trading strategies to identify trend reversals or continuations

Zay Gwet AlertEMA 9, VWAP and ORB 15 minutes alert in Burmese. When the market across the EMA 9 will give alert to buy or sell. And when the market across the VWAP and ORB 15 will alert as well. Especially for Burmese community as it is in Burmese language.

Multi Brownian Forecast📊 Multi Brownian Forecast (Time-Adaptive, Probabilistic)

This indicator uses a sophisticated Geometric Brownian Motion (GBM) Monte Carlo simulation to project future price paths. It adapts to any chart timeframe and provides quantitative, multi-period probability signals.

---

🧠 Core Mathematical Methodology

The model relies on GBM, which is a continuous-time stochastic process that models asset prices.

1. Historical Analysis (Drift & Volatility):

* The script first calculates Logarithmic Returns over a user-defined Historical Lookback (Hours) .

* Drift ($\mu$): Computed as the average of the log returns.

* Volatility ($\sigma$): Computed as the standard deviation of the log returns.

* These values are then time-adapted to an hourly step, compensating for the chart's current timeframe (e.g., 5-minute, 1-hour).

2. Monte Carlo Simulation:

* It runs a specified Number of Simulations (e.g., 1000).

* For each simulation, the price is stepped forward hourly using the GBM formula, which incorporates the calculated drift and a random shock drawn from a normal distribution (generated via the Box-Muller transform ).

---

✨ Key Features

Probabilistic Quartile Forecast: Plots a dynamic "cone" of probability on the chart. It shows key price percentiles (Q1, Q2/Median, Q3, and Q4/Outer Bound) at the forecast's expiration, visualizing the expected range of price outcomes based on the simulations.

Multi-Period Probability Signals: This is the core signal feature. Users can define multiple, independent forecast periods (e.g., 4h, 16h, 48h) in a comma-separated list.

* For each period, a Probability Up and Probability Down is calculated based on hitting a custom Target Price Change (%) (e.g., 2%) at a certain confidence level given a simulation over the historical backlook.

* The probabilities are displayed in a chart table. The cell text turns white if the calculated probability exceeds the user-defined Signal Confidence (%) .

Conditional Fibonacci Retracement: Optionally displays a Fibonacci Retracement on the chart. This feature is only activated when one of the multi-period signals reaches its minimum confidence threshold, providing a contextual technical level when a probabilistic edge is found.

Magic Volume - Projected [MW]Magic Volume – Projected

This lower-pane volume tool estimates the full-bar volume before the bar closes by measuring the current bar’s elapsed time and the rate of incoming volume. It then contrasts that “expected volume” against typical activity and recent momentum to spotlight potential burst conditions (breakout/acceleration), color-codes the live volume stream, and annotates when the projected surge is likely bullish or bearish based on bar structure and recent highs/lows.

Settings

Projected / Expected Volume

Moving Average: EMA length used for volume baseline comparisons. (Default: 14)

Minimum Volume: Hard floor the bar’s raw volume must exceed to qualify as notable. (Default: 10,000)

Consecutive Volume Above 14 EMA: Count required for “sustained” high-volume context. (Default: 3)

Stochastic Volume Burst

Stochastic Length: Window for the Stochastic calculation on volume. (Default: 8)

Smoothing: Smoothing applied to Stochastic volume and its signal. (Default: 3)

Stochastic Volume Breakout Threshold: Level above which Stochastic volume is considered a breakout. (Default: 20)

Volume Bar Increase Amount: Multiplier the current bar’s volume must exceed vs. prior bar to be considered a “burst.” (Default: 1.618)

Plotted Items

Expected Volume (columns): Magenta columns projecting the full-bar volume from intrabar rate. Turns lime when a high expected-volume condition aligns with bullish bar structure; turns red under analogous bearish conditions.

Actual Volume (columns): Live volume columns, color-coded by state:

• Blue = baseline;

• Orange = “burst” (volume rising fast above prior × factor and above baseline);

• Yellow = “burst at breakout” (burst + Stochastic volume breakout);

• Light Blue = Stochastic breakout only.

Volume EMA (line): Yellow EMA for baseline comparison (default 14).

Calculations

Compute elapsed time in the current bar (ms → seconds) and convert the current bar’s accumulated volume into a rate (volume per second).

Project full-bar Expected Volume = (volume so far / seconds elapsed) × bar-seconds.

Compute Volume EMA (default 14) for baseline; derive Stochastic(volume, length) and smoothed signal for momentum.

Define “Burst” conditions:

• Volume > prior volume × Volume Bar Increase Amount;

• Volume > Minimum Volume;

• Volume > Volume EMA;

• Stochastic(volume) rising and/or above threshold.

Classify “Burst at Breakout” when Burst aligns with Stochastic crossover above the Breakout Threshold.

Classify Bullish/Bearish Expected Volume: if Expected Volume is ≥ 1.618 × prior bar volume and prior volume > Volume EMA, then:

• Bullish if bar is green with a rising low;

• Bearish if bar is red with a falling high.

Color-map actual volume columns by state; overlay Expected Volume columns (magenta) and paint conditional overlays (lime/red) when directional context is detected.

How to Use

Spot the Surge Early

When Expected Volume spikes well above typical (and especially above ~1.618× the prior bar) before the bar closes, it often precedes a volatile move. Use this to prepare entries with tight, structure-based risk (e.g., just beyond the current bar’s wick) and asymmetric targets.

Confirm with Momentum

Yellow/orange volume columns indicate burst/breakout behavior in the live tape. When this aligns with a lime (bullish) or red (bearish) Expected Volume column, the probability of follow-through improves—particularly if aligned with prevailing trend or key levels.

Context Matters

Combine with your preferred S/R or structure tools (e.g., order blocks, channels, VWAP) to avoid chasing into obvious supply/demand. The projected surge can mark both continuations and sharp reversals depending on location and broader context.

Alerts

High Expected Volume – Bullish: When projected volume surges and the price action meets bullish conditions (green body with rising low).

High Expected Volume – Bearish: When projected volume surges and the price action meets bearish conditions (red body with falling high).

Other Usage Notes and Limitations

Projected volume depends on intrabar pace; abrupt pauses/flushes can change the projection quickly, especially on very small timeframes.

Minimum Volume and EMA baselines help filter thin markets; adjust upward on illiquid symbols to reduce noise.

A rising projection does not pick direction on its own—directional coloring (lime/red) requires price-action confirmation; otherwise treat magenta projections as “heads-up” only.

As with any single indicator, use within a broader plan (risk management, structure, confluence) to mitigate false positives and improve selectivity.

Inputs (Quick Reference)

Moving Average (int, default 14)

Stochastic Length (int, default 8)

Smoothing (int, default 3)

Stochastic Volume Breakout Threshold (int, default 20)

Volume Bar Increase Amount (float, default 1.618)

Minimum Volume (int, default 10,000)

Consecutive Volume Above 14 EMA (int, default 3)

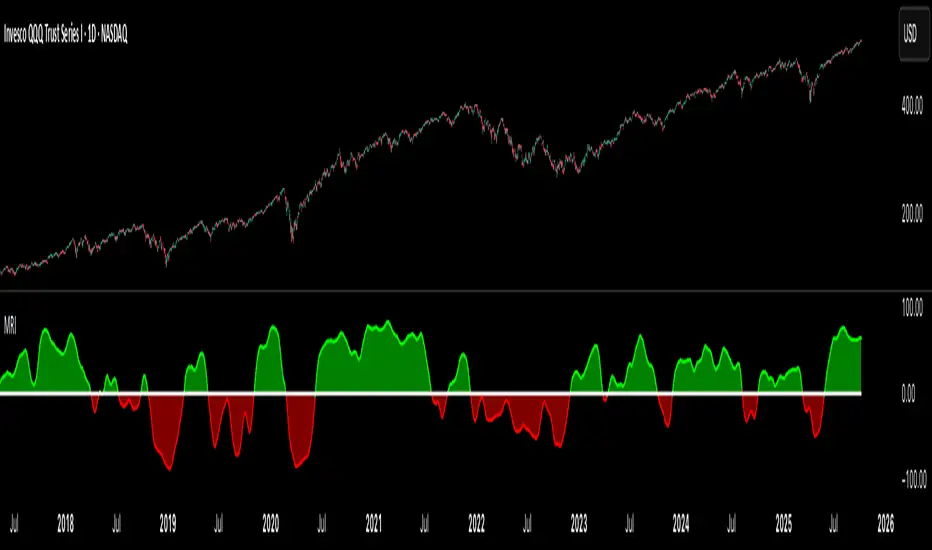

Market Regime IndexThe Market Regime Index is a top-down macro regime nowcasting tool that offers a consolidated view of the market’s risk appetite. It tracks 32 of the world’s most influential markets across asset classes to determine investor sentiment by applying trend-following signals to each independent asset. It features adjustable parameters and a built-in alert system that notifies investors when conditions transition between Risk-On and Risk-Off regimes. The selected markets are grouped into equities (7), fixed income (9), currencies (7), commodities (5), and derivatives (4):

Equities = S&P 500 E-mini Index Futures, Nasdaq-100 E-mini Index Futures, Russell 2000 E-mini Index Futures, STOXX Europe 600 Index Futures, Nikkei 225 Index Futures, MSCI Emerging Markets Index Futures, and S&P 500 High Beta (SPHB)/Low Beta (SPLV) Ratio.

Fixed Income = US 10Y Treasury Yield, US 2Y Treasury Yield, US 10Y-02Y Yield Spread, German 10Y Bund Yield, UK 10Y Gilt Yield, US 10Y Breakeven Inflation Rate, US 10Y TIPS Yield, US High Yield Option-Adjusted Spread, and US Corporate Option-Adjusted Spread.

Currencies = US Dollar Index (DXY), Australian Dollar/US Dollar, Euro/US Dollar, Chinese Yuan/US Dollar, Pound Sterling/US Dollar, Japanese Yen/US Dollar, and Bitcoin/US Dollar.

Commodities = ICE Brent Crude Oil Futures, COMEX Gold Futures, COMEX Silver Futures, COMEX Copper Futures, and S&P Goldman Sachs Commodity Index (GSCI) Futures.

Derivatives = CBOE S&P 500 Volatility Index (VIX), ICE US Bond Market Volatility Index (MOVE), CBOE 3M Implied Correlation Index, and CBOE VIX Volatility Index (VVIX)/VIX.

All assets are directionally aligned with their historical correlation to the S&P 500. Each asset contributes equally based on its individual bullish or bearish signal. The overall market regime is calculated as the difference between the number of Risk-On and Risk-Off signals divided by the total number of assets, displayed as the percentage of markets confirming each regime. Green indicates Risk-On and occurs when the number of Risk-On signals exceeds Risk-Off signals, while red indicates Risk-Off and occurs when the number of Risk-Off signals exceeds Risk-On signals.

Bullish Signal = (Fast MA – Slow MA) > (ATR × ATR Margin)

Bearish Signal = (Fast MA – Slow MA) < –(ATR × ATR Margin)

Market Regime = (Risk-On signals – Risk-Off signals) ÷ Total assets

This indicator is designed with flexibility in mind, allowing users to include or exclude individual assets that contribute to the market regime and adjust the input parameters used for trend signal detection. These parameters apply to each independent asset, and the overall regime signal is smoothed by the signal length to reduce noise and enhance reliability. Investors can position according to the prevailing market regime by selecting factors that have historically outperformed under each regime environment to minimise downside risk and maximise upside potential:

Risk-On Equity Factors = High Beta > Cyclicals > Low Volatility > Defensives.

Risk-Off Equity Factors = Defensives > Low Volatility > Cyclicals > High Beta.

Risk-On Fixed Income Factors = High Yield > Investment Grade > Treasuries.

Risk-Off Fixed Income Factors = Treasuries > Investment Grade > High Yield.

Risk-On Commodity Factors = Industrial Metals > Energy > Agriculture > Gold.

Risk-Off Commodity Factors = Gold > Agriculture > Energy > Industrial Metals.

Risk-On Currency Factors = Cryptocurrencies > Foreign Currencies > US Dollar.

Risk-Off Currency Factors = US Dollar > Foreign Currencies > Cryptocurrencies.

In summary, the Market Regime Index is a comprehensive macro risk-management tool that identifies the current market regime and helps investors align portfolio risk with the market’s underlying risk appetite. Its intuitive, color-coded design makes it an indispensable resource for investors seeking to navigate shifting market conditions and enhance risk-adjusted performance by selecting factors that have historically outperformed. While it has proven historically valuable, asset-specific characteristics and correlations evolve over time as market dynamics change.

HTF & PD/PM LevelsTired of mapping your own levels every morning? Look no further! This script automatically maps out and updates HTF & PD/PM Levels along with ATH. I personally use these as confirmation zones with EMA & VWAP, RSI, and Volume... but alone, these levels mark major support and resistances.

What are they?

🏰 HTF Levels — “Big Grown-Up Lines”

HTF = Higher Time Frame

Think of your price chart like a big map. HTF levels are the important lines from bigger chunks of time:

>Daily (yesterday’s close, high, low)

>Weekly (this week’s open, high, low, close)

>Monthly (this month’s open/close)

Why they matter:

These are like big walls and floors that price often bounces off or stops at. Big traders (institutions) watch them because they show where a lot of buying or selling happened before.

⏰ PD & PM Levels — “Yesterday & Morning Clues”

PD = Previous Day

>PDH = Previous Day’s High

>PDL = Previous Day’s Low

>PDC = Previous Day’s Close

PM = Pre-Market

>PMH = Pre-Market High

>PML = Pre-Market Low

>ATH = All-Time High

Why they matter:

These tell you where price moved when most regular traders weren’t awake yet (pre-market) and where it ended up yesterday. Price often revisits or reacts to these spots.

⚡ How Options Traders Use Them

Support & Resistance:

If price is near an HTF or PD/PM level, it might stop and turn around there (like a ball hitting a wall) or it might use it as a launchpad to the next level if it breaks.

Entry & Exit Spots:

Traders might buy calls (bet price goes up) if it breaks above an important level, or puts (bet price goes down) if it breaks below.

Risk Management:

These levels give clear spots to set stops and targets — “If price breaks this level, I’m out.”

Super Simple Picture:

HTF = big important levels from days, weeks, months.

PD/PM = yesterday’s and morning’s clues where price already moved.

Traders use them to guess where price might bounce or break to plan option trades safely.

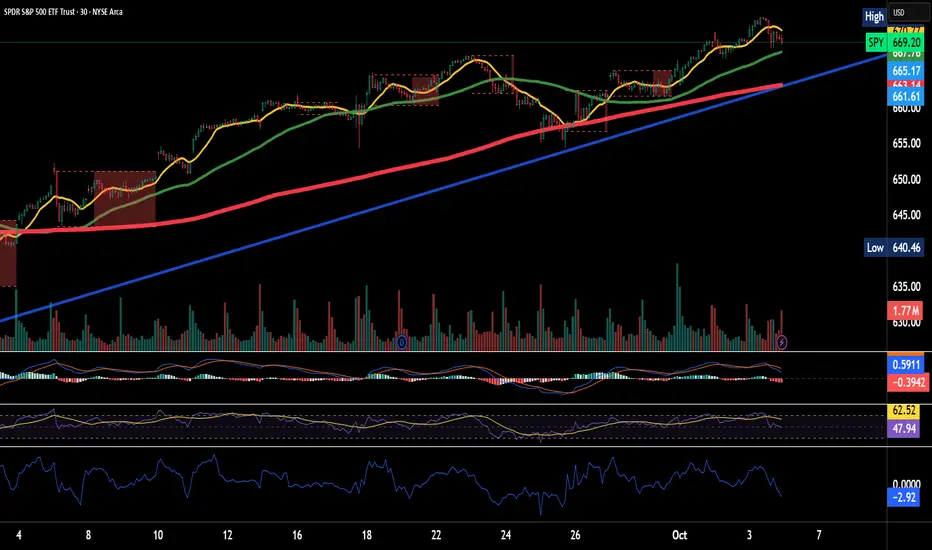

Overnight Z/VolRatio SignalThis indicator highlights overnight setups where both volatility expansion and prior-day range deviation suggest directional opportunity at the RTH open.

It calculates:

• Overnight Z-Score (Z_long): how far the overnight session’s range tilts from the 20-day overnight mean, standardized by its standard deviation.

• VolRatio: ratio of the current RTH session volume to the 20-day average, a proxy for participation and conviction.

Signal Logic (LONG bias)

A long-bias condition triggers when:

• Z_long ≥ 0.40 (overnight tilt strongly positive)

• VolRatio ≥ 1.30 (above-average RTH volume)

• Optional filters: R1/R4 region alignment, YDH/YDL proximity, and other context flags.

Visuals mark qualifying days with colored labels and session highlights.

It is intended as a context signal — not an auto-trading system — for SPY/SPX/ES or correlated large-cap indices.

Usage Notes

• Works best when applied to daily or intraday 5m chart with extended hours enabled.

• Typical exit: ~150 minutes after 09:30 ET.

• Fridays are optionally excluded to avoid expiration-related distortions.

bar count plot only for far lookbackPurpose:

TradingView limits the number of text/label objects (≈500), which causes traditional bar-count indicators to stop showing numbers when you scroll far back in history.

This plots-only version bypasses that limitation entirely, allowing you to view bar numbers anywhere on the chart, even thousands of bars back.

How It Works:

Displays each bar’s in-day sequence number (1–78 by default) under the candles.

Counts restart automatically at the start of each trading day.

Uses a dual-channel “digit plot” system (tens + ones) instead of labels—extremely light on performance and unlimited in lookback.

The digits are drawn every N bars (default = 3) to keep the view uncluttered.

Key Parameters:

Show every Nth bar: Controls how often numbers appear (1 = every bar, 3 = every 3 bars, etc.).

Notes:

Digits are plotted directly via plotshape()—no labels—so they remain visible even 5 000 + bars back.

Alignment may vary slightly depending on chart zoom; this version is intended mainly for deep historical review rather than precise near-term alignment.

Trend CandlesThis shows candlesticks that only follow the trend. So it will make it easier to know where the trend is going.

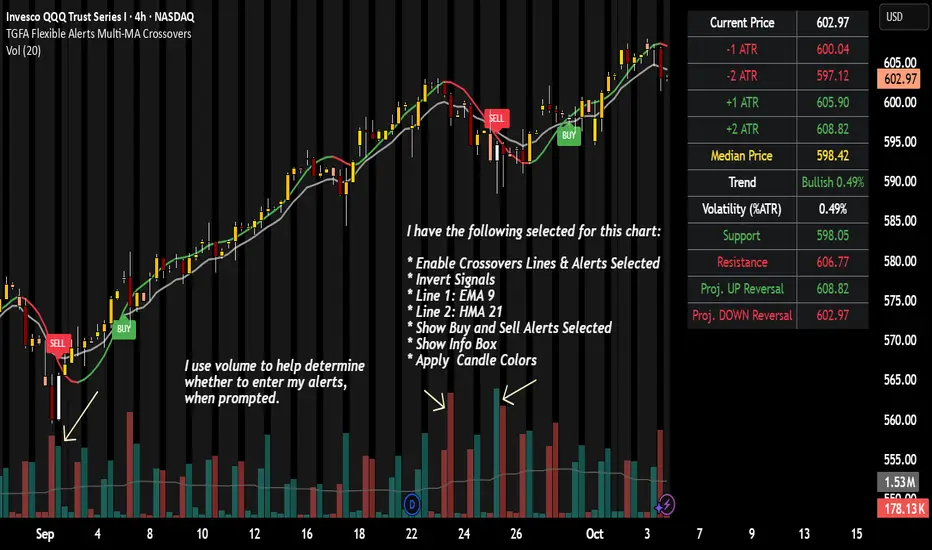

TGFA Flexible Alerts Multi-MA CrossoversTGFA Flexible Alerts, Multi-MA Crossovers

Description

Flexible MA crossovers with BUY/SELL alerts, customizable candle colors, and an info box for ATR/volatility insights. Supports EMA/SMA/HMA/VWAP on any chart.

Overview

TGFA Flexible Alerts is a versatile Pine Script indicator for traders seeking customizable moving average (MA) crossovers, visual signals, and quick-reference metrics. It overlays crossover lines (e.g., fast EMA over slow SMA), generates BUY/SELL labels and alerts, colors candles based on themes, and includes an optional info box with ATR bands, support/resistance, and trend projections. Built for any symbol and timeframe (optimized for 1H intraday), it auto-detects Heikin Ashi charts and handles mixed MA types like responsive HMA with lagging EMAs. All logic uses built-in TA functions for reliability—no repainting on confirmed bars.

Key Features

MA Crossover Engine: Configurable lines (EMA, SMA, HMA, VWAP) with dynamic colors (HMA tints green/red based on slope). Enable/disable via inputs.

Invert Signals Toggle: Flips BUY/SELL logic for mixed MA setups (e.g., HMA as fast line over EMA).

Reasoning: Traditional crossovers assume a fast line (low lag) crossing above a slow line (high lag) for buys. HMA's hull design makes it ultra-responsive, so it may "lead" too aggressively—causing premature signals. Inverting aligns it with user intuition (e.g., HMA dipping below then recovering signals strength), reducing false positives in trending markets. Test on your pairs!

Visual Alerts: BUY/SELL labels at crossover price (with optional price display and offset adjustment).

Single MA Overlays: Independent plots for EMA/SMA/HMA/VWAP (length 0 to hide).

Info Box: Real-time table with current price, ±1/2 ATR bands, median price (over lookback), trend (SMA50 slope), volatility % (ATR normalized), support/resistance (recent highs/lows), and reversal projections (tied to SMA50 pivot for up/down bias).

Candle Coloring: 20+ themes (dark/light canvases) for bull/bear/reversal/low-volume bars—e.g., Emerald Blaze greens uptrends, dims on low vol. Toggle off for no changes.

Chart Source Flexibility: Auto-switches to Heikin Ashi if detected; manual override for Regular/HA.

Alerts fire on crossovers/crossunders (custom messages with ticker/interval). Open-source for forking.

How to Use

Add to Chart: Search in TradingView's public library, apply to any symbol (e.g., stocks, forex). Best on 1H for intraday, but works on daily/weekly too.

Setup Crossovers: Choose Line 1/2 types/lengths (e.g., HMA 9 over SMA 20). Enable "Invert Signals" if using HMA—prevents lag mismatches in volatile assets.

Alerts & Labels: Toggle labels for visuals; set TradingView alerts on "Buy"/"Sell" conditions. Use offset for crowded charts.

Info Box Insights: Enable for quick scans—e.g., enter long near support if trend is bullish and price > median. Adjust ATR length (default 14) for sensitivity.

Candle Themes: Pick a scheme (e.g., Neon Pulse for dark mode); it overrides bar colors without altering data.

Customization Tip: For HMA-heavy setups, invert + short lengths (5-9) catch turns early; pair with volume filter in alerts.

Limitations & Disclaimers - Designed for overlay on price charts; may overlap in tight ranges—adjust transparency via styles.

HMA can repaint intra-bar; signals confirm on close. Not back tested for all assets—validate with strategy tester.

Info box projections use SMA(50) as a trend pivot (same for up/down as reference); customize via code for advanced calcs. Candle colors are cosmetic only.

This is an analysis tool, not advice. Trading involves risk; combine with fundamentals/news. Past performance isn't indicative of future results. No liability for losses.

I'm still a newbie, so feedback encouraged!

Thank you!!

ThisGirl

Tunç ŞatıroğluTunç Şatıroğlu's Technical Analysis Suite

Description:

This comprehensive Pine Script indicator, inspired by the technical analysis teachings of Tunç Şatıroğlu, integrates six powerful TradingView indicators into a single, user-friendly suite for robust trend, momentum, and divergence analysis. Each component has been carefully selected and enhanced by beytun to improve functionality, performance, and visual clarity, aligning with Şatıroğlu's approach to technical analysis. The default configuration is meticulously set to match the exact settings of the individual indicators as used by Tunç Şatıroğlu in his training, ensuring authenticity and ease of use for followers of his methodology. Whether you're a beginner or an experienced trader, this suite provides a versatile toolkit for analyzing markets across multiple timeframes.

Included Indicators:

1. WaveTrend with Crosses (by LazyBear, modified): A momentum oscillator that identifies overbought/oversold conditions and trend reversals with clear buy/sell signals via crosses and bar color highlights.

2. Kaufman Adaptive Moving Average (KAMA) (by HPotter, modified): A dynamic moving average that adapts to market volatility, offering a smoother trend-following signal.

3. SuperTrend (by Alex Orekhov, modified): A trend-following indicator that plots dynamic support/resistance levels with buy/sell signals and optional wicks for enhanced accuracy.

4. Nadaraya-Watson Envelope (by LuxAlgo, modified): A non-linear envelope that highlights potential reversals with customizable repainting options for smoother outputs.

5. Divergence for Many Indicators v4 (by LonesomeTheBlue, modified): Detects regular and hidden divergences across multiple indicators (MACD, RSI, Stochastic, CCI, Momentum, OBV, VWMA, CMF, MFI, and more) for early reversal signals.

6. Ichimoku Cloud (TradingView built-in, modified): A multi-faceted indicator for trend direction, support/resistance, and momentum, with enhanced visuals for the Kumo Cloud.

Key Features:

- Authentic Default Settings : Pre-configured to mirror the exact parameters used by Tunç Şatıroğlu for each indicator, ensuring alignment with his proven technical analysis approach.

- Customizable Settings : Enable/disable individual indicators and fine-tune parameters to suit your trading style while retaining the option to revert to Şatıroğlu’s defaults.

- Enhanced User Experience : Modifications improve visual clarity, performance, and usability, with options like repainting smoothing for Nadaraya-Watson and adjustable Ichimoku projection periods.

- Multi-Timeframe Analysis : Combines trend-following, momentum, and divergence tools for a holistic view of market dynamics.

- Alert Conditions : Built-in alerts for SuperTrend direction changes, buy/sell signals, and divergence detections to keep you informed.

- Visual Clarity : Overlays (KAMA, SuperTrend, Nadaraya-Watson, Ichimoku) and pane-based indicators (WaveTrend, Divergences) are clearly distinguished, with customizable colors and styles.

Notes:

- The Nadaraya-Watson Envelope and Ichimoku Cloud may repaint in their default modes. Use the "Repainting Smoothing" option for Nadaraya-Watson or adjust Ichimoku settings to mitigate repainting if preferred.

- Published under the MIT License, with components licensed under GPL-3.0 (SuperTrend), CC BY-NC-SA 4.0 (Nadaraya-Watson), MPL 2.0 (Divergence), and TradingView's terms (Ichimoku Cloud).

Usage:

Add this indicator to your TradingView chart to leverage Tunç Şatıroğlu’s exact indicator configurations out of the box. Customize settings as needed to align with your strategy, and use the combined signals to identify trends, reversals, and divergences. Ideal for traders following Şatıroğlu’s methodologies or anyone seeking a powerful, all-in-one technical analysis tool.

Credits:

Original authors: LazyBear, HPotter, Alex Orekhov, LuxAlgo, LonesomeTheBlue, and TradingView.

Modifications and integration by beytun .

License:

Published under the MIT License, incorporating code under GPL-3.0, CC BY-NC-SA 4.0, MPL 2.0, and TradingView’s terms where applicable.

Advantage RSI PredictorThe Relative Strength Index (RSI) is a widely used momentum oscillator that measures the speed and change of price movements, typically on a scale from 0 to 100, to identify overbought (above 70) or oversold (below 30) conditions. However, its reliance on historical data limits its ability to predict future price movements. To overcome this, an advanced indicator—termed the Advanced RSI Predictor (ARP)—can be developed to provide predictive bands for RSI levels, enhancing its forecasting potential.The ARP leverages machine learning techniques, such as Long Short-Term Memory (LSTM) networks, combined with traditional RSI calculations to forecast future RSI values and establish confidence intervals or bands. These bands represent a range within which the RSI is likely to fluctuate over a specified period, offering traders a probabilistic perspective on momentum shifts. The indicator starts with the standard RSI computation, using a 14-period lookback as a foundation, but enriches this by incorporating additional inputs like moving averages, volatility measures (e.g., Bollinger Bands width), and trading volume. These features are processed through an LSTM model trained on historical price and RSI data to predict future RSI trajectories.The output includes upper and lower predictive bands, typically set at a 95% confidence level, surrounding a central forecasted RSI line. For example, if the current RSI is 45, the ARP might project a band from 40 to 50 over the next five days, indicating potential momentum stability or a range for overbought/oversold thresholds. The bands adapt dynamically to market conditions—narrowing during stable trends and widening during volatile periods—using real-time data updates. This adaptability allows traders to anticipate breakouts or reversals before they manifest on the price chart.Validation can be strengthened through backtesting against historical data, ensuring the ARP’s bands align with significant market turns. This indicator proves especially valuable in trending markets, where traditional RSI levels (e.g., 70 or 30) may falter, offering a sophisticated tool for informed trading or investment decisions.

Brownian Motion Probabilistic Forecasting (Time Adaptive)Probabilistic Price Forecast Indicator

Overview

The Probabilistic Price Forecast is an advanced technical analysis tool designed for the TradingView platform. Instead of predicting a single future price, this indicator uses a Monte Carlo simulation to model thousands of potential future price paths, generating a cone of possibilities and calculating the probability of specific outcomes.

This allows traders to move beyond simple price targets and ask more sophisticated questions, such as: "What is the probability that this stock will increase by 5% over the next 24 hours?"

Core Concept: Geometric Brownian Motion

The indicator's forecasting model is built on the principles of Geometric Brownian Motion (GBM) , a widely accepted mathematical model for describing the random movements of financial asset prices. The core idea is that the next price step is a function of the asset's historical trend (drift), its volatility, and a random "shock."

The formula used to project each price step in the simulation is:

next_price = current_price * exp( (μ - (σ²/2))Δt + σZ√(Δt) )

Where:

μ (mu) represents the drift , which is the average historical return.

σ (sigma) represents the volatility , measured by the standard deviation of historical returns.

Z is a random variable from a standard normal distribution, representing the random "shock" or new information affecting the price.

Δt (delta t) is the time step for each projection.

How It Works

The indicator performs a comprehensive analysis on the most recent bar of the chart:

**Historical Analysis**: It first analyzes a user-defined historical period (e.g., the last 240 hours of price data) to calculate the asset's historical drift (μ) and volatility (σ) from its logarithmic returns.

**Monte Carlo Simulation**: It then runs thousands of simulations (e.g., 2000) of future price paths over a specified forecast period (e.g., the next 24 hours). Each path is unique due to the random shock (Z) applied at every step.

**Probability Distribution**: After all simulations are complete, it collects the final price of each path and sorts them to build a probability distribution of potential outcomes.

**Visualization and Signaling**: Finally, it visualizes this distribution on the chart and generates signals based on the user's criteria.

Key Features & Configuration

The indicator is highly configurable, allowing you to tailor its analysis to your specific needs.

Time-Adaptive Periods

The lookback and forecast periods are defined in hours , not bars. The script automatically converts these hour-based inputs into the correct number of bars based on the chart's current timeframe, ensuring the analysis remains consistent across different chart resolutions.

Forecast Quartiles

You can visualize the forecast as a "cone of probability" on the chart. The indicator draws lines and a shaded area representing the price levels for different quartiles (percentiles) of the simulation results. By default, this shows the range between the 25th and 95th percentiles.

Independent Bullish and Bearish Signals

The indicator allows you to set independent criteria for bullish and bearish signals, providing greater flexibility. You can configure:

A bullish signal for an X% confidence of a Y% price increase.

A bearish signal for a W% confidence of a Z% price decrease.

For example, you can set it to alert you for a 90% chance of a 2% drop, while simultaneously looking for a 60% chance of a 10% rally.

How to Interpret the Indicator

The Forecast Cone : The blue shaded area on the chart represents the probable range of future prices. The width of the cone indicates the expected volatility; a wider cone means higher uncertainty. The price labels on the right side of the cone show the calculated percentile levels at the end of the forecast period.

Green Signal Label : A green "UP signal" label appears when the probability of the price increasing by your target percentage exceeds your defined confidence level.

Red Signal Label : A red "DOWN signal" label appears when the probability of the price decreasing by your target percentage exceeds your confidence level.

This tool provides a statistical edge for understanding future possibilities but should be used in conjunction with other analysis techniques.

VWAP / ORB / VP & POCThis is an all-in-one technical analysis tool designed to give you a comprehensive view of the market on a single chart. It combines three powerful indicators—VWAP, Opening Range, and Volume Profile—to help you identify key price levels, understand intraday trends, and spot areas of high liquidity.

What It Does

The indicator plots three distinct components on your chart:

Volume-Weighted Average Price (VWAP): A benchmark that shows the average price a security has traded at throughout the day, based on both price and volume. It's often used by institutional traders to gauge whether they are getting a good price. The script also plots standard deviation or percentage-based bands around the VWAP line, which can act as dynamic support and resistance.

Opening Range Breakout (ORB): A tool that highlights the high and low of the initial trading period of a session (e.g., the first 15 minutes). The script draws lines for the opening price, range high, and range low for the rest of the session. It also colors the chart with zones to visually separate price action above, below, and within this critical opening range.

Volume Profile (VP): A powerful study that shows trading activity over a set number of bars at specific price levels. Unlike traditional volume that is plotted over time, this is plotted on the price axis. It helps you instantly see where the most and least trading has occurred, identifying significant levels like the Point of Control (POC)—the single price with the most volume—and the Value Area (VA), where the majority of trading took place.

How to Use It for Trading

The real strength of this indicator comes from finding confluence, where two or more of its components signal the same key level.

Identifying Support & Resistance: The POC, VWAP bands, Opening Range high/low, and session open price are all powerful levels to watch. When price approaches one of these levels, you can anticipate a potential reaction (a bounce or a breakout).

Gauging Intraday Trend: A simple rule of thumb is to consider the intraday trend bullish when the price is trading above the VWAP and bearish when it is trading below the VWAP.

Finding High-Value Zones: The Volume Profile’s Value Area (VA) shows you where the market has accepted a price. Trading within the VA is considered "fair value," while prices outside of it are "unfair." Reversals often happen when the price tries to re-enter the Value Area from the outside.

Settings:

Here’s a breakdown of all the settings you can change to customize the indicator to your liking.

Volume Profile Settings:

Number of Bars: How many of the most recent bars to use for the calculation. A higher number gives a broader profile.

Row Size: The number of price levels (rows) in the profile. Higher numbers give a more detailed, granular view.

Value Area Volume %: The percentage of total volume to include in the Value Area (standard is 70%).

Horizontal Offset: Moves the Volume Profile further to the right to avoid overlapping with recent price action.

Colors & Styles: Customize the colors for the POC line, Value Area, and the up/down volume bars.

VWAP Settings:

Anchor Period: Resets the VWAP calculation at the start of a new Session, Week, Month, Year, etc. You can even anchor it to corporate events like Earnings or Splits.

Source: The price source used in the calculation (default is hlc3, the average of the high, low, and close).

Bands Calculation Mode:

Standard Deviation: The bands are based on statistical volatility.

Percentage: The bands are a fixed percentage away from the VWAP line.

Bands Multiplier: Sets the distance of the bands from the VWAP. You can enable and configure up to three sets of bands.

ORB Settings (Opening Range)

Opening Range Timeframe: The duration of the opening range (e.g., 15 for 15 minutes, 60 for the first hour).

Market Session & Time Zone: Crucial for ensuring the range is calculated at the correct time for the asset you're trading.

Line & Zone Styles: Full customization for the colors, thickness, and style (Solid, Dashed, Dotted) of the High, Low, and Opening Price lines, as well as the background colors for the zones above, below, and within the range.