BUY/SELL Timeframe ContinuityTime frame continuity refers to the alignment of price trends across multiple time frames. This means that the price movement is showing a consistent trend (either up or down) on various timeframes, like the 5-minute, 30-minute, hourly, and daily charts.

Why is it important?

Confirms Trend Strength: When multiple timeframes align, it indicates a strong and sustained trend.

Risk Management: Trading in the direction of the aligned trend can reduce risk.

This indicator checks if the current price of a selected timeframe is above or below its opening price. A buy/sell signal appears the second all bullish timeframes align (buy) or all bearish timeframes align. You can choose to paint the candles when the buy/sell conditions happen. You can select up to 10 different timeframes.

NOTE: With this indicator I prefer timeframes 15m, 30m, 1H, 4H, D, 5D, W - Together these timeframes are great for short-term trends on any stock.

在腳本中搜尋"国泰黄金ETF联接C相关行业指数的最新政策"

Multi-Symbol Scanner: Advanced EMA-RSI-Volume Strategy# Multi-Symbol Tech Stock Scanner: Advanced EMA-RSI-Volume Strategy

## Technical Analysis Methodology

This scanner implements a sophisticated multi-timeframe analysis approach combining three key technical elements:

### 1. Dual EMA System (Primary Trend Detection)

- **Long-term EMA (820 periods)**: Acts as the primary trend identifier

- Chosen specifically for tech stocks' longer-term price waves

- Helps filter out minor market noise while capturing major trend changes

- 820 periods approximately represents 3.2 years of trading days

- **Medium-term EMA (320 periods)**: Serves as trend confirmation

- Approximately 1.25 years of trading data

- Provides earlier entry signals while maintaining trend reliability

- Helps identify potential trend reversals before the major trend shift

### 2. Volume Analysis Component

The script employs a dynamic volume analysis system:

- Calculates 20-period moving average of volume as baseline

- Requires 1.5x surge above baseline for signal confirmation

- Volume surge requirement helps filter out weak moves and potential false breakouts

- Different from standard volume indicators as it uses adaptive thresholds

### 3. RSI Momentum Filter

Implements a specialized RSI configuration:

- 14-period RSI with dynamic overbought/oversold levels

- Oversold threshold: 30 (customizable)

- Overbought threshold: 70 (customizable)

- Used as a confirmation tool rather than primary signal generator

## Signal Generation Logic

### Buy Signal Requirements

1. Price must cross above 820 EMA (PRIMARY CONDITION)

2. Current price must be above 320 EMA (CONFIRMATION)

3. RSI must be above 30 but below 70 (MOMENTUM CHECK)

4. Volume must be 1.5x above 20-period average (STRENGTH VALIDATION)

### Sell Signal Requirements

1. Price must cross below 820 EMA (PRIMARY CONDITION)

2. Current price must be below 320 EMA (CONFIRMATION)

3. RSI must be above 30 but below 70 (MOMENTUM CHECK)

4. Volume must be 1.5x above 20-period average (STRENGTH VALIDATION)

## Risk Management Integration

The script automatically calculates key risk levels based on volatility:

1. **Stop Loss Calculation**:

- Default: 2% below entry for buys

- Dynamically adjusted based on price point

- Can be modified through input parameters

2. **Take Profit Targets**:

- Primary target: 6% above entry (3:1 reward-risk ratio)

- Based on historical tech stock movement patterns

- Adjustable through input parameters

## Multi-Symbol Implementation

The scanner monitors 6 symbols simultaneously using:

- Separate security calls for each data point

- Optimized data requests to prevent overload

- Individual signal processing for each symbol

- Synchronized alert generation system

## Technical Implementation Details

1. **Data Processing**:

```

- Security data requests on 10-minute timeframe

- Individual EMA calculations per symbol

- Separate volume analysis threads

- RSI calculations with standard deviation normalization

```

2. **Signal Processing**:

```

- Cross-verification of all conditions

- Time-based signal validation

- Volume surge confirmation

- Trend alignment check

```

3. **Alert System**:

```

- Bar-close confirmation required

- Multi-condition validation

- Detailed price level inclusion

- Risk parameter integration

```

## Optimization Features

1. **Memory Usage**:

- Optimized security calls

- Efficient data structure

- Reduced redundant calculations

2. **Processing Efficiency**:

- Single-pass data analysis

- Combined indicator calculations

- Streamlined alert generation

## Practical Application

The system is designed for:

1. Swing Trading (primary use)

2. Position Trading (secondary use)

3. Technical Breakout Trading

Optimal timeframes:

- Primary: 4H charts

- Secondary: Daily charts

- Verification: 1H charts

## Default Configuration

The scanner is preset to monitor key tech stocks:

- TSLA: High-volatility tech leader

- NVDA: Semiconductor sector benchmark

- AVGO: Stable tech infrastructure

- TSM: Global chip manufacturer

- META: Social media sector leader

- AMZN: E-commerce/Cloud computing leader

Each symbol can be modified through input parameters.

## Version Information

- Current Version: 1.3

- Last Updated: November 2024

- Compatibility: TradingView Pro/Pro+/Premium

## Limitations & Considerations

- Limited to 6 symbols due to TradingView security request limits

- Requires consistent market volume for optimal performance

- Best suited for liquid stocks with significant daily volume

- May need parameter adjustments during extreme market conditions

CAGR ProjectionThe CAGR Projection Indicator is a tool designed to visualize the potential growth of an asset over time based on a specified annual growth rate. This indicator overlays a projection line on the price chart, allowing traders and investors to compare actual price movements with a hypothetical growth trajectory.

One of the key features of this indicator is the ability for users to input their expected annual growth rate as a percentage. This flexibility allows for various scenarios to be modeled, from conservative estimates to more optimistic projections. Additionally, the indicator allows users to set a specific start date for the projection, enabling analysis from any chosen point in time.

The projection calculation is dynamic, adjusting for different timeframes and updating with each new bar on the chart. The indicator initializes either at the specified start date or when the first valid price is encountered. Using the initial price as a base, the indicator calculates the projected price for each subsequent bar using the compound growth formula. The calculation accounts for the specific timeframe of the chart, ensuring accurate projections regardless of whether the chart displays daily, weekly, or other intervals.

The projected growth is plotted as a blue line on the chart, providing a clear visual comparison between the actual price movement and the hypothetical growth trajectory. This visual representation makes it easy for users to quickly assess how an asset is performing relative to the expected growth rate.

This tool has several practical applications. Investors can use it to set realistic growth targets for their investments. By comparing actual price movements to the projection line, users can quickly assess if an asset is outperforming or underperforming relative to the expected growth rate. Furthermore, multiple instances of the indicator can be used with different growth rates to visualize various potential outcomes, facilitating scenario analysis.

The indicator also offers customization options, such as displaying a label showing the annual growth rate used for the projection, and the ability to adjust the color of the projection line to suit individual preferences or chart setups.

In summary, this CAGR Projection indicator serves as a valuable tool for both long-term investors and traders, offering a simple yet effective way to visualize potential growth scenarios and assess investment performance over time. It combines ease of use with powerful analytical capabilities, making it a useful addition to any trader's or investor's toolkit.

Exposure Oscillator (Cumulative 0 to ±100%)

Exposure Oscillator (Cumulative 0 to ±100%)

This Pine Script indicator plots an "Exposure Oscillator" on the chart, which tracks the cumulative market exposure from a range of technical buy and sell signals. The exposure is measured on a scale from -100% (maximum short exposure) to +100% (maximum long exposure), helping traders assess the strength of their position in the market. It provides an intuitive visual cue to aid decision-making for trend-following strategies.

Buy Signals (Increase Exposure Score by +10%)

Buy Signal 1 (Cross Above 21 EMA):

This signal is triggered when the price crosses above the 21-period Exponential Moving Average (EMA), where the current bar closes above the EMA21, and the previous bar closed below the EMA21. This indicates a potential upward price movement as the market shifts into a bullish trend.

buySignal1 = ta.crossover(close, ema21)

Buy Signal 2 (Trending Above 21 EMA):

This signal is triggered when the price closes above the 21-period EMA for each of the last 5 bars, indicating a sustained bullish trend. It confirms that the price is consistently above the EMA21 for a significant period.

buySignal2 = ta.barssince(close <= ema21) > 5

Buy Signal 3 (Living Above 21 EMA):

This signal is triggered when the price has closed above the 21-period EMA for each of the last 15 bars, demonstrating a strong, prolonged uptrend.

buySignal3 = ta.barssince(close <= ema21) > 15

Buy Signal 4 (Cross Above 50 SMA):

This signal is triggered when the price crosses above the 50-period Simple Moving Average (SMA), where the current bar closes above the 50 SMA, and the previous bar closed below it. It indicates a shift toward bullish momentum.

buySignal4 = ta.crossover(close, sma50)

Buy Signal 5 (Cross Above 200 SMA):

This signal is triggered when the price crosses above the 200-period Simple Moving Average (SMA), where the current bar closes above the 200 SMA, and the previous bar closed below it. This suggests a long-term bullish trend.

buySignal5 = ta.crossover(close, sma200)

Buy Signal 6 (Low Above 50 SMA):

This signal is true when the lowest price of the current bar is above the 50-period SMA, indicating strong bullish pressure as the price maintains itself above the moving average.

buySignal6 = low > sma50

Buy Signal 7 (Accumulation Day):

An accumulation day occurs when the closing price is in the upper half of the daily range (greater than 50%) and the volume is larger than the previous bar's volume, suggesting buying pressure and accumulation.

buySignal7 = (close - low) / (high - low) > 0.5 and volume > volume

Buy Signal 8 (Higher High):

This signal occurs when the current bar’s high exceeds the highest high of the previous 14 bars, indicating a breakout or strong upward momentum.

buySignal8 = high > ta.highest(high, 14)

Buy Signal 9 (Key Reversal Bar):

This signal is generated when the stock opens below the low of the previous bar but rallies to close above the previous bar’s high, signaling a potential reversal from bearish to bullish.

buySignal9 = open < low and close > high

Buy Signal 10 (Distribution Day Fall Off):

This signal is triggered when a distribution day (a day with high volume and a close near the low of the range) "falls off" the rolling 25-bar period, indicating the end of a bearish trend or selling pressure.

buySignal10 = ta.barssince(close < sma50 and close < sma50) > 25

Sell Signals (Decrease Exposure Score by -10%)

Sell Signal 1 (Cross Below 21 EMA):

This signal is triggered when the price crosses below the 21-period Exponential Moving Average (EMA), where the current bar closes below the EMA21, and the previous bar closed above it. It suggests that the market may be shifting from a bullish trend to a bearish trend.

sellSignal1 = ta.crossunder(close, ema21)

Sell Signal 2 (Trending Below 21 EMA):

This signal is triggered when the price closes below the 21-period EMA for each of the last 5 bars, indicating a sustained bearish trend.

sellSignal2 = ta.barssince(close >= ema21) > 5

Sell Signal 3 (Living Below 21 EMA):

This signal is triggered when the price has closed below the 21-period EMA for each of the last 15 bars, suggesting a strong downtrend.

sellSignal3 = ta.barssince(close >= ema21) > 15

Sell Signal 4 (Cross Below 50 SMA):

This signal is triggered when the price crosses below the 50-period Simple Moving Average (SMA), where the current bar closes below the 50 SMA, and the previous bar closed above it. It indicates the start of a bearish trend.

sellSignal4 = ta.crossunder(close, sma50)

Sell Signal 5 (Cross Below 200 SMA):

This signal is triggered when the price crosses below the 200-period Simple Moving Average (SMA), where the current bar closes below the 200 SMA, and the previous bar closed above it. It indicates a long-term bearish trend.

sellSignal5 = ta.crossunder(close, sma200)

Sell Signal 6 (High Below 50 SMA):

This signal is true when the highest price of the current bar is below the 50-period SMA, indicating weak bullishness or a potential bearish reversal.

sellSignal6 = high < sma50

Sell Signal 7 (Distribution Day):

A distribution day is identified when the closing range of a bar is less than 50% and the volume is larger than the previous bar's volume, suggesting that selling pressure is increasing.

sellSignal7 = (close - low) / (high - low) < 0.5 and volume > volume

Sell Signal 8 (Lower Low):

This signal occurs when the current bar's low is less than the lowest low of the previous 14 bars, indicating a breakdown or strong downward momentum.

sellSignal8 = low < ta.lowest(low, 14)

Sell Signal 9 (Downside Reversal Bar):

A downside reversal bar occurs when the stock opens above the previous bar's high but falls to close below the previous bar’s low, signaling a reversal from bullish to bearish.

sellSignal9 = open > high and close < low

Sell Signal 10 (Distribution Cluster):

This signal is triggered when a distribution day occurs three times in the rolling 7-bar period, indicating significant selling pressure.

sellSignal10 = ta.valuewhen((close < low) and volume > volume , 1, 7) >= 3

Theme Mode:

Users can select the theme mode (Auto, Dark, or Light) to match the chart's background or to manually choose a light or dark theme for the oscillator's appearance.

Exposure Score Calculation: The script calculates a cumulative exposure score based on a series of buy and sell signals.

Buy signals increase the exposure score, while sell signals decrease it. Each signal impacts the score by ±10%.

Signal Conditions: The buy and sell signals are derived from multiple conditions, including crossovers with moving averages (EMA21, SMA50, SMA200), trend behavior, and price/volume analysis.

Oscillator Visualization: The exposure score is visualized as a line on the chart, changing color based on whether the exposure is positive (long position) or negative (short position). It is limited to the range of -100% to +100%.

Position Type: The indicator also indicates the position type based on the exposure score, labeling it as "Long," "Short," or "Neutral."

Horizontal Lines: Reference lines at 0%, 100%, and -100% visually mark neutral, increasing long, and increasing short exposure levels.

Exposure Table: A table displays the current exposure level (in percentage) and position type ("Long," "Short," or "Neutral"), updated dynamically based on the oscillator’s value.

Inputs:

Theme Mode: Choose "Auto" to use the default chart theme, or manually select "Dark" or "Light."

Usage:

This oscillator is designed to help traders track market sentiment, gauge exposure levels, and manage risk. It can be used for long-term trend-following strategies or short-term trades based on moving average crossovers and volume analysis.

The oscillator operates in conjunction with the chart’s price action and provides a visual representation of the market’s current trend strength and exposure.

Important Considerations:

Risk Management: While the exposure score provides valuable insight, it should be combined with other risk management tools and analysis for optimal trading decisions.

Signal Sensitivity: The accuracy and effectiveness of the signals depend on market conditions and may require adjustments based on the user’s trading strategy or timeframe.

Disclaimer:

This script is for educational purposes only. Trading involves significant risk, and users should carefully evaluate all market conditions and apply appropriate risk management strategies before using this tool in live trading environments.

Mins Before Market Close AlertThis script will set an alert X mins before the market closes.

This is meant to be added to daily charts (calculations based off of daily bars).

This script can be useful for sending webhooks before the market closes to close open positions or to open new ones.

Simply add it to your daily chart and set up your desired alert (email, webhook, sound, etc.).

You can also change the chart marker to a different shape, color, or location to your preference.

Enjoy this simple alert!

NASI +The NASI + indicator is an advanced adaptation of the classic McClellan Oscillator, a tool widely used to gauge market breadth. It calculates the McClellan Oscillator by measuring the difference between the 19-day and 39-day EMAs of net advancing issues, which are optionally adjusted to account for the relative strength of advancing vs. declining stocks.

To enhance this analysis, NASI + applies the Relative Strength Index (RSI) to the cumulative McClellan Oscillator values, generating a unique momentum-based view of market breadth. Additionally, two extra EMAs—a 10-day and a 4-day EMA—are applied to the RSI, providing further refinement to signals for overbought and oversold conditions.

With NASI +, users benefit from:

-A deeper analysis of market momentum through cumulative breadth data.

-Enhanced sensitivity to trend shifts with the applied RSI and dual EMAs.

-Clear visual cues for overbought and oversold conditions, aiding in intuitive signal identification.

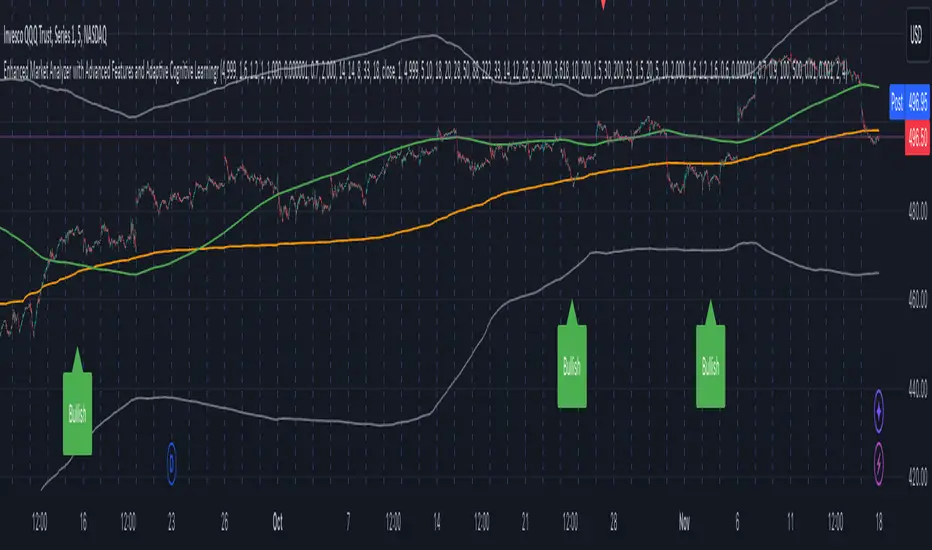

Enhanced Market Analyzer with Adaptive Cognitive LearningThe "Enhanced Market Analyzer with Advanced Features and Adaptive Cognitive Learning" is an advanced, multi-dimensional trading indicator that leverages sophisticated algorithms to analyze market trends and generate predictive trading signals. This indicator is designed to merge traditional technical analysis with modern machine learning techniques, incorporating features such as adaptive learning, Monte Carlo simulations, and probabilistic modeling. It is ideal for traders who seek deeper market insights, adaptive strategies, and reliable buy/sell signals.

Key Features:

Adaptive Cognitive Learning:

Utilizes Monte Carlo simulations, reinforcement learning, and memory feedback to adapt to changing market conditions.

Adjusts the weighting and learning rate of signals dynamically to optimize predictions based on historical and real-time data.

Hybrid Technical Indicators:

Custom RSI Calculation: An RSI that adapts its length based on recursive learning and error adjustments, making it responsive to varying market conditions.

VIDYA with CMO Smoothing: An advanced moving average that incorporates Chander Momentum Oscillator for adaptive smoothing.

Hamming Windowed VWMA: A volume-weighted moving average that applies a Hamming window for smoother calculations.

FRAMA: A fractal adaptive moving average that responds dynamically to price movements.

Advanced Statistical Analysis:

Skewness and Kurtosis: Provides insights into the distribution and potential risk of market trends.

Z-Score Calculations: Identifies extreme market conditions and adjusts trading thresholds dynamically.

Probabilistic Monte Carlo Simulation:

Runs thousands of simulations to assess potential price movements based on momentum, volatility, and volume factors.

Integrates the results into a probabilistic signal that informs trading decisions.

Feature Extraction:

Calculates a variety of market metrics, including price change, momentum, volatility, volume change, and ATR.

Normalizes and adapts these features for use in machine learning algorithms, enhancing signal accuracy.

Ensemble Learning:

Combines signals from different technical indicators, such as RSI, MACD, Bollinger Bands, Stochastic Oscillator, and statistical features.

Weights each signal based on cumulative performance and learning feedback to create a robust ensemble signal.

Recursive Memory and Feedback:

Stores and averages past RSI calculations in a memory array to provide historical context and improve future predictions.

Adaptive memory factor adjusts the influence of past data based on current market conditions.

Multi-Factor Dynamic Length Calculation:

Determines the length of moving averages based on volume, volatility, momentum, and rate of change (ROC).

Adapts to various market conditions, ensuring that the indicator is responsive to both high and low volatility environments.

Adaptive Learning Rate:

The learning rate can be adjusted based on market volatility, allowing the system to adapt its speed of learning and sensitivity to changes.

Enhances the system's ability to react to different market regimes.

Monte Carlo Simulation Engine:

Simulates thousands of random outcomes to model potential future price movements.

Weights and aggregates these simulations to produce a final probabilistic signal, providing a comprehensive risk assessment.

RSI with Dynamic Adjustments:

The initial RSI length is adjusted recursively based on calculated errors between true RSI and predicted RSI.

The adaptive RSI calculation ensures that the indicator remains effective across various market phases.

Hybrid Moving Averages:

Short-Term and Long-Term Averages: Combines FRAMA, VIDYA, and Hamming VWMA with specific weights for a unique hybrid moving average.

Weighted Gradient: Applies a color gradient to indicate trend strength and direction, improving visual clarity.

Signal Generation:

Generates buy and sell signals based on the ensemble model and multi-factor analysis.

Uses percentile-based thresholds to determine overbought and oversold conditions, factoring in historical data for context.

Optional settings to enable adaptation to volume and volatility, ensuring the indicator remains effective under different market conditions.

Monte Carlo and Learning Parameters:

Users can customize the number of Monte Carlo simulations, learning rate, memory factor, and reward decay for tailored performance.

Applications:

Scalping and Day Trading:

The fast response of the adaptive RSI and ensemble learning model makes this indicator suitable for short-term trading strategies.

Swing Trading:

The combination of long-term moving averages and probabilistic models provides reliable signals for medium-term trends.

Volatility Analysis:

The ATR, Bollinger Bands, and adaptive moving averages offer insights into market volatility, helping traders adjust their strategies accordingly.

yptestrsilibLibrary "RSIBackgroundLib"

RSI 배경색 라이브러리

rsi_background(_symbol, _timeframe)

RSI 계산 및 배경색 반환

Parameters:

_symbol (simple string) : string 심볼

_timeframe (simple string) : string 타임프레임

Returns: RSI, RSI MA, RSI MA10, 배경색

Price Move Exceed % Threshold & BE Evaluation1Handy to see history or quick back test of moves. Enter a decimal for percentage wanted and choose the time frame wanted . The occurrences of the up or down threshold are plotted in the panel as maroon or green squares and can be read as red or green text in the panel data and on the right hand scale . The last number in the panel is the average move for the chosen period.

My usage is mostly to see what % has been exceeded for break even prices of option trades. Example: in SPY a spread has a break even of 567 when the price is 570; I get the percentage of the $3 move by dividing 3/570 to get 0.0526 ; the results show as described above.

Moving AveragesWhile this "Moving Averages" indicator may not revolutionize technical analysis, it certainly offers a valuable and efficient solution for traders seeking to streamline their chart analysis process. This all-in-one tool addresses a common frustration among traders: the need to constantly search for and compare different types and lengths of moving averages.

Key Features

The indicator allows for the configuration of up to 5 moving averages simultaneously, providing a comprehensive view of price trends. Users can choose from 7 types of moving averages for each line, including SMA, EMA, WMA, VWMA, HMA, SMMA, and TMA. This variety ensures that traders can apply their preferred moving average types without the need for multiple indicators.

Each moving average can be fully customized in terms of length, color, line style, and thickness, allowing for clear visual differentiation. However, what sets this indicator apart is its "Smart Opacity" feature. When activated, this option dynamically adjusts the transparency of the moving average lines based on their direction, with ascending lines appearing more opaque and descending lines more transparent. This subtle yet effective visual cue aids in quickly identifying trend changes and potential trading signals.

Advantages

The primary benefit of this indicator lies in its convenience. By consolidating multiple moving averages into a single, customizable tool, it saves traders valuable time and reduces chart clutter. The Smart Opacity feature, while not groundbreaking, does offer an intuitive way to visualize trend strength and direction at a glance.

Moreover, the indicator's flexibility makes it suitable for various trading styles and experience levels. Whether you're a novice trader learning to interpret basic trend signals or an experienced analyst fine-tuning a complex strategy, this tool can adapt to your needs.

In conclusion, while this "Moving Averages" indicator may not be a game-changer in the world of technical analysis, it represents a thoughtful refinement of a fundamental trading tool. By focusing on user convenience and visual clarity, it offers a practical solution for traders looking to optimize their chart analysis process and make more informed trading decisions.

Dual Momentum StrategyThis Pine Script™ strategy implements the "Dual Momentum" approach developed by Gary Antonacci, as presented in his book Dual Momentum Investing: An Innovative Strategy for Higher Returns with Lower Risk (McGraw Hill Professional, 2014). Dual momentum investing combines relative momentum and absolute momentum to maximize returns while minimizing risk. Relative momentum involves selecting the asset with the highest recent performance between two options (a risky asset and a safe asset), while absolute momentum considers whether the chosen asset has a positive return over a specified lookback period.

In this strategy:

Risky Asset (SPY): Represents a stock index fund, typically more volatile but with higher potential returns.

Safe Asset (TLT): Represents a bond index fund, which generally has lower volatility and acts as a hedge during market downturns.

Monthly Momentum Calculation: The momentum for each asset is calculated based on its price change over the last 12 months. Only assets with a positive momentum (absolute momentum) are considered for investment.

Decision Rules:

Invest in the risky asset if its momentum is positive and greater than that of the safe asset.

If the risky asset’s momentum is negative or lower than the safe asset's, the strategy shifts the allocation to the safe asset.

Scientific Reference

Antonacci's work on dual momentum investing has shown the strategy's ability to outperform traditional buy-and-hold methods while reducing downside risk. This approach has been reviewed and discussed in both academic and investment publications, highlighting its strong risk-adjusted returns (Antonacci, 2014).

Reference: Antonacci, G. (2014). Dual Momentum Investing: An Innovative Strategy for Higher Returns with Lower Risk. McGraw Hill Professional.

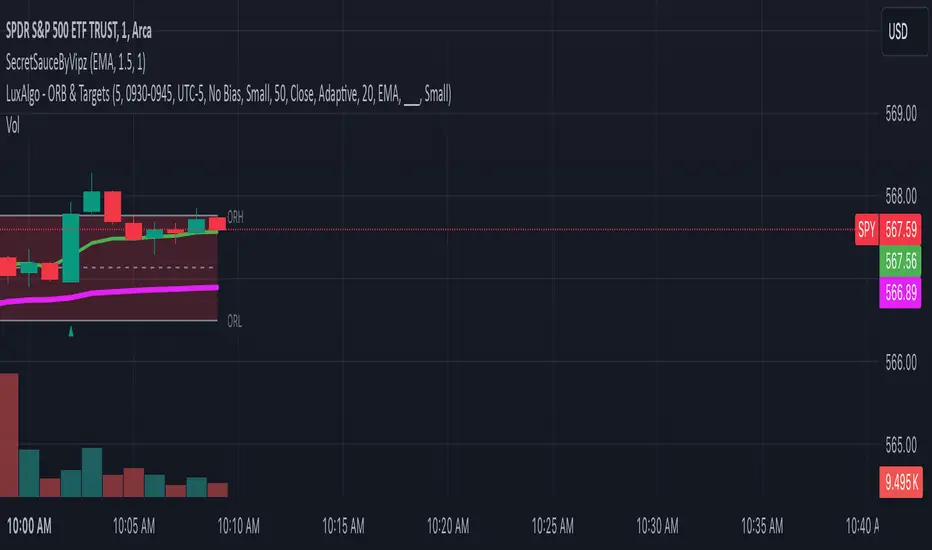

SecretSauceByVipzOverview:

SecretSauceByVipz is a sophisticated trading indicator designed to help traders identify high-probability buy and sell signals by integrating multiple technical analysis tools. By combining Exponential Moving Averages (EMAs), Average True Range (ATR) buffer zones, Volume Weighted Average Price (VWAP), and Relative Strength Index (RSI) momentum confirmation, this indicator aims to reduce false signals and enhance trading decisions.

Key Features:

Exponential Moving Averages (EMAs):

200-period EMA (Long EMA): Serves as a long-term trend indicator.

8-period EMA (Fast EMA): Captures short-term price movements.

21-period EMA (Slow EMA): Reflects medium-term price trends.

EMA Crossovers: Generates initial buy/sell signals when the fast EMA crosses over or under the slow EMA.

ATR-Based Buffer Zones:

ATR Calculation: Utilizes a 14-period ATR to measure market volatility.

Buffer Zone Multiplier: User-adjustable multiplier (default 1.0) applied to the ATR to create dynamic buffer zones around the 200 EMA.

Buffer Zones: Helps filter out false signals by requiring price to move beyond these zones for certain signals.

Volume Weighted Average Price (VWAP):

VWAP Plotting: Provides an average price weighted by volume, useful for identifying fair value areas and potential support/resistance levels.

Signal Confirmation Logic:

Confirmation Candle: Requires the next candle after a crossover to close in the signal's direction for added reliability.

Early Signals: Triggers when price crosses the 200 EMA and moves beyond the buffer zone, indicating potential early trend changes.

Strong Signals: Occur when both the price crosses the fast EMA and the fast EMA crosses the slow EMA simultaneously.

RSI Momentum Confirmation:

RSI Calculation: Uses a 14-period RSI to gauge market momentum.

Momentum Filter: Confirms signals only when RSI aligns with the trend (above 50 for bullish, below 50 for bearish signals).

Visual Aids:

EMA and VWAP Plots: Overlays the EMAs and VWAP directly on the price chart for easy visualization.

Buffer Zone Lines: Plots the upper and lower buffer zones around the 200 EMA.

Signal Labels:

Buy Signals: Displayed as green "BUY" labels below the bars.

Sell Signals: Displayed as red "SELL" labels above the bars.

How to Use:

Trend Identification:

Use the 200 EMA to determine the overall market trend.

Price above the 200 EMA suggests a bullish trend; below indicates a bearish trend.

Signal Generation:

Confirmed Signals: Wait for the confirmation candle after an EMA crossover before considering entry.

Early Signals: Consider early entries when price crosses the 200 EMA and moves beyond the buffer zone.

Strong Signals: Pay attention to strong signals where both price and EMAs are crossing over, indicating robust trend momentum.

Momentum Confirmation:

Ensure the RSI aligns with the signal direction:

Buy Signals: RSI should be above 50.

Sell Signals: RSI should be below 50.

Adjusting Sensitivity:

Modify the ATR Multiplier and Buffer Multiplier to suit different market conditions and personal trading styles.

A higher multiplier may reduce signal frequency but increase reliability.

Customization Parameters:

ATR Multiplier for Distance Filter (Default: 1.5):

Adjusts the sensitivity of the distance filter based on ATR.

Buffer Multiplier for 200 EMA (Default: 1.0):

Alters the width of the buffer zones around the 200 EMA.

Benefits:

Reduces False Signals: The combination of confirmation candles and buffer zones helps filter out noise.

Enhances Trend Detection: Multiple EMA crossovers provide insights into short-term and medium-term trends.

Incorporates Volatility and Momentum: ATR and RSI ensure signals consider market volatility and momentum.

Disclaimer:

This indicator is a tool to assist in technical analysis and should not be used as the sole basis for trading decisions. Always conduct thorough analysis and consider risk management strategies before executing trades. Past performance is not indicative of future results.

Credits:

Developed by Vipink1203.

Version:

Pine Script Version 5

The Most Powerful TQQQ EMA Crossover Trend Trading StrategyTQQQ EMA Crossover Strategy Indicator

Meta Title: TQQQ EMA Crossover Strategy - Enhance Your Trading with Effective Signals

Meta Description: Discover the TQQQ EMA Crossover Strategy, designed to optimize trading decisions with fast and slow EMA crossovers. Learn how to effectively use this powerful indicator for better trading results.

Key Features

The TQQQ EMA Crossover Strategy is a powerful trading tool that utilizes Exponential Moving Averages (EMAs) to identify potential entry and exit points in the market. Key features of this indicator include:

**Fast and Slow EMAs:** The strategy incorporates two EMAs, allowing traders to capture short-term trends while filtering out market noise.

**Entry and Exit Signals:** Automated signals for entering and exiting trades based on EMA crossovers, enhancing decision-making efficiency.

**Customizable Parameters:** Users can adjust the lengths of the EMAs, as well as take profit and stop loss multipliers, tailoring the strategy to their trading style.

**Visual Indicators:** Clear visual plots of the EMAs and exit points on the chart for easy interpretation.

How It Works

The TQQQ EMA Crossover Strategy operates by calculating two EMAs: a fast EMA (default length of 20) and a slow EMA (default length of 50). The core concept is based on the crossover of these two moving averages:

- When the fast EMA crosses above the slow EMA, it generates a *buy signal*, indicating a potential upward trend.

- Conversely, when the fast EMA crosses below the slow EMA, it produces a *sell signal*, suggesting a potential downward trend.

This method allows traders to capitalize on momentum shifts in the market, providing timely signals for trade execution.

Trading Ideas and Insights

Traders can leverage the TQQQ EMA Crossover Strategy in various market conditions. Here are some insights:

**Scalping Opportunities:** The strategy is particularly effective for scalping in volatile markets, allowing traders to make quick profits on small price movements.

**Swing Trading:** Longer-term traders can use this strategy to identify significant trend reversals and capitalize on larger price swings.

**Risk Management:** By incorporating customizable stop loss and take profit levels, traders can manage their risk effectively while maximizing potential returns.

How Multiple Indicators Work Together

While this strategy primarily relies on EMAs, it can be enhanced by integrating additional indicators such as:

- **Relative Strength Index (RSI):** To confirm overbought or oversold conditions before entering trades.

- **Volume Indicators:** To validate breakout signals, ensuring that price movements are supported by sufficient trading volume.

Combining these indicators provides a more comprehensive view of market dynamics, increasing the reliability of trade signals generated by the EMA crossover.

Unique Aspects

What sets this indicator apart is its simplicity combined with effectiveness. The reliance on EMAs allows for smoother signals compared to traditional moving averages, reducing false signals often associated with choppy price action. Additionally, the ability to customize parameters ensures that traders can adapt the strategy to fit their unique trading styles and risk tolerance.

How to Use

To effectively utilize the TQQQ EMA Crossover Strategy:

1. **Add the Indicator:** Load the script onto your TradingView chart.

2. **Set Parameters:** Adjust the fast and slow EMA lengths according to your trading preferences.

3. **Monitor Signals:** Watch for crossover points; enter trades based on buy/sell signals generated by the indicator.

4. **Implement Risk Management:** Set your stop loss and take profit levels using the provided multipliers.

Regularly review your trading performance and adjust parameters as necessary to optimize results.

Customization

The TQQQ EMA Crossover Strategy allows for extensive customization:

- **EMA Lengths:** Change the default lengths of both fast and slow EMAs to suit different time frames or market conditions.

- **Take Profit/Stop Loss Multipliers:** Adjust these values to align with your risk management strategy. For instance, increasing the take profit multiplier may yield larger gains but could also increase exposure to market fluctuations.

This flexibility makes it suitable for various trading styles, from aggressive scalpers to conservative swing traders.

Conclusion

The TQQQ EMA Crossover Strategy is an effective tool for traders seeking an edge in their trading endeavors. By utilizing fast and slow EMAs, this indicator provides clear entry and exit signals while allowing for customization to fit individual trading strategies. Whether you are a scalper looking for quick profits or a swing trader aiming for larger moves, this indicator offers valuable insights into market trends.

Incorporate it into your TradingView toolkit today and elevate your trading performance!

Bullish B's - RSI Divergence StrategyThis indicator strategy is an RSI (Relative Strength Index) divergence trading tool designed to identify high-probability entry and exit points based on trend shifts. It utilizes both regular and hidden RSI divergence patterns to spot potential reversals, with signals for both bullish and bearish conditions.

Key Features

Divergence Detection:

Bullish Divergence: Signals when RSI indicates momentum strengthening at a lower price level, suggesting a reversal to the upside.

Bearish Divergence: Signals when RSI shows weakening momentum at a higher price level, indicating a potential downside reversal.

Hidden Divergences: Looks for hidden bullish and bearish divergences, which signal trend continuation points where price action aligns with the prevailing trend.

Volume-Adjusted Entry Signals:

The strategy enters long trades when RSI shows bullish or hidden bullish divergence, indicating an upward momentum shift.

An optional volume filter ensures that only high-volume, high-conviction trades trigger a signal.

Exit Signals:

Exits long positions when RSI reaches a customizable overbought level, typically indicating a potential reversal or profit-taking opportunity.

Also closes positions if bearish divergence signals appear after a bullish setup, providing protection against trend reversals.

Trailing Stop-Loss:

Uses a trailing stop mechanism based on ATR (Average True Range) or a percentage threshold to lock in profits as the price moves in favor of the trade.

Alerts and Custom Notifications:

Integrated with TradingView alerts to notify the user when entry and exit conditions are met, supporting timely decision-making without constant monitoring.

Customizable Parameters:

Users can adjust the RSI period, pivot lookback range, overbought level, trailing stop type (ATR or percentage), and divergence range to fit their trading style.

Ideal Usage

This strategy is well-suited for trend traders and swing traders looking to capture reversals and trend continuations on medium to long timeframes. The divergence signals, paired with trailing stops and volume validation, make it adaptable for multiple asset classes, including stocks, forex, and crypto.

Summary

With its focus on RSI divergence, trailing stop-loss management, and volume filtering, this strategy aims to identify and capture trend changes with minimized risk. This allows traders to efficiently capture profitable moves and manage open positions with precision.

This Strategy BEST works with GLD!

Linear Regression Channel UltimateKey Features and Benefits

Logarithmic scale option for improved analysis of long-term trends and volatile markets

Activity-based profiling using either touch count or volume data

Customizable channel width and number of profile fills

Adjustable number of most active levels displayed

Highly configurable visual settings for optimal chart readability

Why Logarithmic Scale Matters

The logarithmic scale option is a game-changer for analyzing assets with exponential growth or high volatility. Unlike linear scales, log scales represent percentage changes consistently across the price range. This allows for:

Better visualization of long-term trends

More accurate comparison of price movements across different price levels

Improved analysis of volatile assets or markets experiencing rapid growth

How It Works

The indicator calculates a linear regression line based on the specified period

Upper and lower channel lines are drawn at a customizable distance from the regression line

The space between the channel lines is divided into a user-defined number of levels

For each level, the indicator tracks either:

- The number of times price touches the level (touch count method)

- The total volume traded when price is at the level (volume method)

The most active levels are highlighted based on this activity data

Understanding Touch Count vs Volume

Touch count method: Useful for identifying key support/resistance levels based on price action alone

Volume method: Provides insight into levels where the most trading activity occurs, potentially indicating stronger support/resistance

Practical Applications

Trend identification and strength assessment

Support and resistance level discovery

Entry and exit point optimization

Volume profile analysis for improved market structure understanding

This Linear Regression Channel indicator combines powerful statistical analysis with flexible visualization options, making it an invaluable tool for traders and analysts across various timeframes and markets. Its unique features, especially the logarithmic scale and activity profiling, provide deeper insights into market behavior and potential turning points.

VWAP it GOODWhy: Instead of having 5 individual VWAP indicators, I found it beneficial for one view with a clean display. This VWAP indicator combines the daily, weekly, monthly, quarterly and annual into one color coded view. These colors and styles can be modified by the user.

A user can turn any timeframe off, but this is how I personally like to trade since it helps me better understand potential bounce or pullback areas.

Do your own research for what is best for you.

VOLUME DIRECTION INDICATORDesigned for the 1-hour chart, this indicator shows:

Green Line: Volume when price rises, suggesting buying.

Red Line: Volume when price falls, indicating selling.

How to Use:

Watch for Crossover: When the Green Line moves above the Red, it might signal a budding uptrend.

Check Retracement: If the Green Line pulls back but stays above the Red, the uptrend could be strengthening.

Price Check: Look for a small price drop but not a reversal.

Trade Entry:

Enter at the high of the retracement candle.

Or wait for the Green Line to rise again.

For Precision: Draw a line at the retracement peak and switch to a shorter timeframe to find entry patterns above this line.

Remember: Use this with other tools for better trading decisions.

The Volume Direction Indicator provides a visual representation of market activity by assuming volume can be attributed to buying or selling based on price action within each bar. When the price closes higher than it opened, the volume for that period is considered as 'Bought Shares', plotted in green. Conversely, if the price closes lower, the volume is treated as 'Sold Shares', shown in red. This indicator resets daily to give a fresh perspective on trading activity each day.

Key Features:

Buying Pressure: Green line represents the cumulative volume during periods where the price increased.

Selling Pressure: Red line indicates the cumulative volume during price decreases.

Daily Reset: Accumulated values reset at the start of each new trading day, focusing on daily market sentiment.

Note: This indicator simplifies market dynamics by linking volume directly to price changes. It does not account for complex trading scenarios like short selling or market manipulations. Use this indicator as a tool to gauge general market direction and activity, not for precise transaction data.

Bar count with New day Markerbased on bar count, highlight the first Bar with special colour on every day.

30D Vs 90D Historical VolatilityVolatility equals risk for an underlying asset's price meaning bullish volatility is bearish for prices while bearish volatility is bullish. This compares 30-Day Historical Volatility to 90-Day Historical Volatility.

When the 30-Day crosses under the 90-day, this is typically when asset prices enter a bullish trend.

Conversely, When the 30-Day crosses above the 90-Day, this is when asset prices enter a bearish trend.

Peaks in volatility are bullish divergences while troughs are bearish divergences.

Advanced Physics Financial Indicator Each component represents a scientific theory and is applied to the price data in a way that reflects key principles from that theory.

Detailed Explanation

1. Fractal Geometry - High/Low Signal

Concept: Fractal geometry studies self-similar patterns that repeat at different scales. In markets, fractals can be used to detect recurring patterns or turning points.

Implementation: The script detects pivot highs and lows using ta.pivothigh and ta.pivotlow, representing local turning points in price. The fractalSignal is set to 1 for a pivot high, -1 for a pivot low, and 0 if there is no signal. This logic reflects the cyclical, self-similar nature of price movements.

Practical Use: This signal is useful for identifying local tops and bottoms, allowing traders to spot potential reversals or consolidation points where fractal patterns emerge.

2. Quantum Mechanics - Probabilistic Monte Carlo Simulation

Concept: Quantum mechanics introduces uncertainty and probability into systems, much like how future price movements are inherently uncertain. Monte Carlo simulations are used to model a range of possible outcomes based on random inputs.

Implementation: In this script, we simulate 100 random outcomes by generating a random number between -1 and 1 for each iteration. These random values are stored in an array, and the average of these values is calculated to represent the Quantum Signal.

Practical Use: This probabilistic signal provides a sense of randomness and uncertainty in the market, reflecting the possibility of price movement in either direction. It simulates the market’s chaotic nature by considering multiple possible outcomes and their average.

3. Thermodynamics - Efficiency Ratio Signal

Concept: Thermodynamics deals with energy efficiency and entropy in systems. The efficiency ratio in financial terms can be used to measure how efficiently the price is moving relative to volatility.

Implementation: The Efficiency Ratio is calculated as the absolute price change over n periods divided by the sum of absolute changes for each period within n. This ratio shows how much of the price movement is directional versus random, mimicking the concept of efficiency in thermodynamic systems.

Practical Use: A high efficiency ratio suggests that the market is trending smoothly (high efficiency), while a low ratio indicates choppy, non-directional movement (low efficiency, or high entropy).

4. Chaos Theory - ATR Signal

Concept: Chaos theory studies how complex systems are highly sensitive to initial conditions, leading to unpredictable behavior. In markets, chaotic price movements can often be captured through volatility indicators.

Implementation: The script uses a very long ATR period (1000) to reflect slow-moving chaos over time. The Chaos Signal is computed by measuring the deviation of the current price from its long-term average (SMA), normalized by ATR. This captures price deviations over time, hinting at chaotic market behavior.

Practical Use: The signal measures how far the price deviates from its long-term average, which can signal the degree of chaos or extreme behavior in the market. High deviations indicate chaotic or volatile conditions, while low deviations suggest stability.

5. Network Theory - Correlation with BTC

Concept: Network theory studies how different components within a system are interconnected. In markets, assets are often correlated, meaning that price movements in one asset can influence or be influenced by another.

Implementation: This indicator calculates the correlation between the asset’s price and the price of Bitcoin (BTC) over 30 periods. The Network Signal shows how connected the asset is to BTC, reflecting broader market dynamics.

Practical Use: In a highly correlated market, BTC can act as a leading indicator for other assets. A strong correlation with BTC might suggest that the asset is likely to move in line with Bitcoin, while a weak or negative correlation might indicate that the asset is moving independently.

6. String Theory - RSI & MACD Interaction

Concept: String theory attempts to unify the fundamental forces of nature into a single framework. In trading, we can view the RSI and MACD as interacting forces that provide insights into momentum and trend.

Implementation: The script calculates the RSI and MACD and combines them into a single signal. The formula for String Signal is (RSI - 50) / 100 + (MACD Line - Signal Line) / 100, normalizing both indicators to a scale where their contributions are additive. The RSI represents momentum, and MACD shows trend direction and strength.

Practical Use: This signal helps in detecting moments where momentum (RSI) and trend strength (MACD) align, giving a clearer picture of the asset's direction and overbought/oversold conditions. It unifies these two indicators to create a more holistic view of market behavior.

7. Fluid Dynamics - On-Balance Volume (OBV) Signal

Concept: Fluid dynamics studies how fluids move and flow. In markets, volume can be seen as a "flow" that drives price movement, much like how fluid dynamics describe the flow of liquids.

Implementation: The script uses the OBV (On-Balance Volume) indicator to track the cumulative flow of volume based on price changes. The signal is further normalized by its moving average to smooth out fluctuations and make it more reflective of price pressure over time.

Practical Use: The Fluid Signal shows how the flow of volume is driving price action. If the OBV rises significantly, it suggests that there is strong buying pressure, while a falling OBV indicates selling pressure. It’s analogous to how pressure builds in a fluid system.

8. Final Signal - Combining All Physics-Based Indicators

Implementation: Each of the seven physics-inspired signals is combined into a single Final Signal by averaging their values. This approach blends different market insights from various scientific domains, creating a comprehensive view of the market’s condition.

Practical Use: The final signal gives you a holistic, multi-dimensional view of the market by merging different perspectives (fractal behavior, quantum probability, efficiency, chaos, correlation, momentum/trend, and volume flow). This approach helps traders understand the market's dynamics from multiple angles, offering deeper insights than any single indicator.

9. Color Coding Based on Signal Extremes

Concept: The color of the final signal plot dynamically reflects whether the market is in an extreme state.

Implementation: The signal color is determined using percentiles. If the Final Signal is in the top 55th percentile of its range, the signal is green (bullish). If it is between the 45th and 55th percentiles, it is orange (neutral). If it falls below the 45th percentile, it is red (bearish).

Practical Use: This visual representation helps traders quickly identify the strength of the signal. Bullish conditions (green), neutral conditions (orange), and bearish conditions (red) are clearly distinguished, simplifying decision-making.

CSP Key Level Finder This script is designed for option sellers, particularly those using strategies like cash-secured puts (CSPs), to help automate the process of identifying key levels in the market. The core functionality is to calculate a specific price level where a 5% return can be achieved based on the historical volatility of the underlying asset. This level is visually plotted on a chart to guide traders in making more informed decisions without manually calculating the thresholds themselves.

The script incorporates implied volatility (IV) data to determine the volatility rank of the asset and calculates historical volatility (HV) based on price movements. These volatility measures help assess market conditions. The resulting key level is drawn as a line on the chart, along with a label that includes relevant information about volatility, making it easier for traders to evaluate potential option selling strategies.

Additionally, the script includes user input options, allowing users to control when to display the key level on the chart, offering flexibility based on individual needs. Overall, the script provides a visual aid for option sellers to streamline the process of identifying attractive entry points.

ATR PercentageThe ATR is a great indicator, but for me, it does not define the volatility of an asset I am looking at well enough. So I've adjusted it to be displayed as the usual ATR and a percentage of the closing prince (which to me tells a better story). I find this useful if I am looking through many assets and have to create a quick picture of volatility.

Indicator Definition: The script starts by defining an indicator named "ATR Percentage" that will be displayed in a separate pane (not overlayed on the price chart).

Input for ATR Period: The user can set the period for calculating the ATR through an input field.

ATR Calculation: The ta.atr function calculates the Average True Range based on the specified period.

ATR Percentage Calculation: The ATR value is converted to a percentage of the current closing price using (atrValue / close) * 100.

Plotting:

The script plots both the ATR value and its percentage on the chart.

A horizontal line at zero is added for reference.

Label Display: An optional label displays the current ATR percentage at every 10th bar to avoid cluttering the chart.

Background Color: A light blue background is added to visually separate the ATR indicator from other indicators.

VIDYA with Dynamic Length Based on ICPThis script is a Pine Script-based indicator that combines two key concepts: the Instantaneous Cycle Period (ICP) from Dr. John Ehlers and the Variable Index Dynamic Average (VIDYA). Here's an overview of how the script works:

Components:

Instantaneous Cycle Period (ICP):

This part of the indicator uses Dr. John Ehlers' approach to detect the market cycle length dynamically. It calculates the phase of price movement by computing the in-phase and quadrature components of the price detrended over a specific period.

The ICP helps adjust the smoothing length dynamically, giving a real-time estimate of the dominant cycle in price action. The script uses a phase calculation, adjusts it for cycle dynamics, and smoothes it for more reliable readings.

VIDYA (Variable Index Dynamic Average):

VIDYA is a moving average that dynamically adjusts its smoothing length based on the market conditions, in this case, using the RSI (Relative Strength Index) as a weight.

The length of VIDYA is determined by the dynamically calculated ICP, allowing it to adapt to changing market cycles.

This indicator performs several recursive layers of VIDYA smoothing (applying VIDYA multiple times) to provide a more refined result.

Key Features:

Dynamic Length: The length for the VIDYA calculation is derived from the smoothed ICP value, meaning that the smoothing adapts to the detected cycle length in real-time, making the indicator more responsive to market conditions.

Multiple VIDYA Layers: The script applies multiple layers of VIDYA smoothing (up to 5 iterations), further refining the output to smooth out market noise while maintaining responsiveness.

Plotting: The final smoothed VIDYA value and the smoothed ICP length are plotted. Additionally, overbought (70) and oversold (30) horizontal lines are provided for visual reference.

Application:

This indicator helps identify trends, smooths out price data, and adapts dynamically to market cycles. It's useful for detecting shifts in momentum and trends, and traders can use it to identify overbought or oversold conditions based on dynamically calculated thresholds.