Dynamic Horizontal Lines

Gann levels (squares of 9) have multiple levels. Adding lines at all these levels would add too much noise on the chart.

This indicator adds horizontal lines as per the Gann levels (Squares of 9) closest to the days close.

The current indicator add horizontal lines at the Gann level closest to the days close. It also adds 4 lines above & below the closest Gann level

I have considered Gann levels from 1 to 10000. You can append the Gann levels based on your requirements.

在腳本中搜尋"涨幅大于1000的股票"

DF: Horizontal Levels and Colors for NYSE TICK Chart

DF: Horizontal Levels and Colors for NYSE TICK Chart

This is intended to be added very specifically to your NYSE TICK chart.

This script creates a custom indicator designed to enhance the visual analysis

of market breadth through the NYSE TICK data. It features:

1. **Horizontal Levels**:

- **1300 and -1300**: Gray lines indicating extreme bullish and bearish conditions.

- **1000 and -1000**: Light red and green lines representing significant support and resistance zones.

- **850 and -850**: Customizable blue lines that can be adjusted according to user preferences.

**Zero Line**: A solid white line marking the neutral point, drawn prominently for quick reference.

2. **Color Fills**:

- Red fill between 1000 and 1300 to highlight extreme bullish sentiment.

- Green fill between -1000 and -1300 to signify extreme bearish sentiment.

3. **Exponential Moving Average (EMA)**:

- Calculated based on user-defined length (default set to 8).

- The EMA line's color dynamically adjusts based on its slope:

- White when trending upwards.

- Magenta when trending downwards, providing quick visual cues of market momentum.

Overall, this script serves as a powerful tool for traders seeking to visualize market trends, support and resistance levels, and market breadth through the NYSE TICK data, enhancing their decision-making process in trading.

Moving Average Crossover Swing StrategyMoving Average Crossover Swing Strategy

**Overview:**

The basic concept of this strategy is to generate a signal when a faster/shorter length moving average crosses over (for Longs) or crosses under (for Shorts) a medium/longer length moving average. All of which are customizable. This strategy can work on any timeframe, however the daily is the timeframe used for the default settings and screenshots, as it was designed to be a multi-day swing strategy. Once a signal has been confirmed with a candle close, based on user options, the strategy will enter the trade on the open of the next candle.

The crossover strategy is nothing new to trading, but what can make this strategy unique and helpful, is the addition of further confirmation points, ATR based stop loss and take profit targets, optional early exit criteria, customizable to your needs and style, and just about everything visual can be toggled on/off. This strategy is based on a Trend (MA) indicator and a Momentum (MACD) indicator. While a Volume-based indicator is not shown here, one could consider using their favorite from that category to further compliment the signal idea.

It should be noted that depending on the time frame, direction(s) chosen, the signal options, confirmation options, and exit options selected, that a ticker may not produce more than 100 trades on the back test. Depending on your style and frequency, one could consider adjusting options and/or testing multiple tickers. It should also be noted that this strategy simply tests the underlying stock prices, not options contracts. And of course, testing this strategy against historical data does not assume that the same results will occur in future price action.

Shoutout given to Ripster's Clouds Indicator as pieces of that code were taken and modified to create both the Cloud visualization effects, and the Moving Average Pair Plots that are implemented in this strategy.

BASIC DEFAULTS

All can be changed as normal

Initial capital = 10,000

Order Sizing = 25% of equity (use the "Inputs" tab to modify this)

Pyramiding = 0

Commission = 0.65 USD per order

Price Verification = 1 tick

Slippage = 1 tick

RISK MANAGMENT

You will notice two different percentage options and ATR multipliers. This strategy will adjust position sizing by not exceeding either one of those % values based on the ATR (Average True Range) of the symbol and the multipliers selected, should the stock hit the stop loss price.

For Example, lets assume these values are true:

Account size = $10,000,

Max Risk = 1% of account size

Max Position Size = 25% of the account size

Stock Price = 23.45

ATR = 3.5

ATR Stop Loss Multiplier = 1.4

Then the formulas would be:

ACCT_SIZE * MaxRisk_% = 10000 * .01 = $100 (MaxCashRisk)

-----

MaxCashRisk / (ATR * ATR_SL_MULTIPLIER) = 100 / (3.5 * 1.4) = 20.4 Shares based on Max Cash Risk

-----

(ACCT_SIZE * MaxEquity_%) / STOCK_PRICE = (10000 * .25) / 23.45 = 106.61 Shares based on Max Equity Allocation

The minimum value of each of those options is then used, which in this case would be to purchase 20 shares so as not to exceed the max dollar risk should the stock reach the stop loss target. Likewise, if the ATR were to be much lower, say 0.48 cents, and all else the same, then the strategy would purchase the 106 shares based on Max Equity Allocation because the Max Cash Risk would require 149.25 shares.

MOVING AVERAGE OPTIONS

Select between and change the length & type of up to 5 pairs (10 total) of moving averages

The "Show Cloud-x" option will display a fill color between the "a" and "b" pairs

All moving averages lines can be toggled on/off in the "Style" tab, as well as adjusting their colors.

Visualization features do not affect calculations, meaning you could have all or nothing on the chart and the strategy will still produce results

SIGNAL CHOICES

Choose the fast/shorter length MA and the medium/longer length MA to determine the entry signal

CONFIRMATION OPTIONS

Both of these have customizable values and can be toggled on/off

A candle close over a slower/much longer length moving average

An additional cross-over (cross-under for Shorts) on the MACD indicator using default MACD values. While the MACD indicator is not necessary to have on the chart, it can help to add that for visualization. The calculations will perform whether the indicator is on the chart or not.

EARLY EXIT CRITERIA

Both can be toggled on/off with customizable values

MA Cross Exit will exit the trade early if the select moving averages cross-under (for longs) or cross-over (for shorts), indicating a potential reversal.

Max Bars in Trades will act as a last-resort exit by simply calculating the amount of full bars the trade has been open, and exiting on the opening of the next bar. For example: the default value is 8 bars, so after 8 full bars in the trade, if no other exit has been triggered (Stop Loss, Take Profit, or MA Cross(if enabled)), then the trade will exit at the opening of the 9th bar.

Finally, there is a table displaying the amount of trades taken for each side, and the amount & percent of both early exits. This table can be turned off in the "Style" tab

ADDITIONAL PLOTS

MACD (Moving Average Convergence/Divergence):

- The MACD is an optional confirmation indicator for this strategy.

- Plotting the indicator is not necessary for the strategy to work, but it can be helpful to visually see the status and position of the MACD if this feature is enabled in the strategy

- This helps to identify if there is also momentum behind the entry signal

Anchored Monte Carlo Shuffled Projection [LuxAlgo]The Anchored Monte Carlo Shuffled Projection tool randomly simulates future price points based on historical bar movements made before a user-anchored point in time.

By anchoring our data and projections to a single point in time, users can better understand and reflect on how the price played out while taking into consideration our random simulations.

🔶 USAGE

After selecting the indicator to apply to the chart, you will be prompted to "Set the Anchor Point". Do so by clicking on the desired location on your chart, only time is used as the anchor point.

Note: To select a new anchor point when applied to the chart, click on the 'More' dropdown next to the indicator status bar (○○○), then select "Reset points...".

Alternate Method: You are also able to click and drag the vertical line that displays on the anchor point bar when the indicator is highlighted.

By randomly simulating bar movements, a range is developed of potential price action which could be utilized to locate future price development as well as potential support/resistance levels.

Performing numerous simulations and taking the average at each step will converge toward the result highlighted by the "Average Line", and can point out where the price might develop, assuming the trend and amount of volatility persist.

Current closing price + Sum of changes in the calculation window

This constraint will cause the simulations always to display an endpoint consistent with the current lookback's slope.

While this may be helpful to some traders, this indicator includes an option to produce a less biased range, as seen below:

🔶 DETAILS

The Anchored Monte Carlo Shuffled Projection tool creates simulations based on prices within a user-set lookback window originating at the specified anchor point. Simulations are done as follows:

Collect each bar's price changes in the user-set window.

Randomize the order of each change in the window.

Project the cumulative sum of the shuffled changes from the current closing price.

Collect data on each point along the way.

This is the process for the Default calculation; for the 'Randomize Direction' calculation, when added onto the front for every other change, the value is inverted, creating the randomized endpoints for each simulation.

The script contains each simulation's data for that bar, with a maximum of 1000 simulations.

To get a glimpse behind the scenes, each simulation (up to 99) can be viewed using the 'Visualize Simulations' Options, as seen below.

Because the script holds the full simulation data, the script can also calculate this data, such as standard deviations.

In this script the Standard deviation lines are the average of all standard deviations across the vertical data groups, this provides a singular value that can be displayed a distance away from the simulation center line.

🔶 SETTINGS

Lookback: Sets the number of Bars to include in calculations.

Simulation Count: Sets the number of randomized simulations to calculate. (Max 1000)

Randomize Direction: See Details Above. Creates a more 'Normalized' Distribution

Visualize Simulations: See Details Above. Turns on Visualizations, and colors are randomly generated. Visualized max does not cap the calculated max. If 1000 simulations are used, the data will be from 1000 simulations, however, only the last 99 simulations will be visualized.

🔹 Standard Deviations

Standard Deviation Multiplier: Sets the multiplier to use for the Standard Deviation distance away from the center line.

🔹 Style

Extend Lines: Extends the Simulated Value Lines into the future for further reference and analysis.

Monte Carlo Shuffled Projection [LuxAlgo]The Monte Carlo Shuffled Projection tool randomly simulates future price points based on historical bar movements made within a user-selected window.

The tool shows potential paths price might take in the future, as well as highlighting potential support/resistance levels.

Note that simulations and their resulting elements are subject to slight changes over time.

🔶 USAGE

By randomly simulating bar movements, a range is developed of potential price action which could be utilized to locate future price development as well as potential support/resistance levels.

Performing a large number of simulations and taking the average at each step will converge toward the result highlighted by the "Average Line", and can point out where the price might develop assuming the trend and amount of volatility persist.

Current closing price + Sum of changes in the calculation window)

This constraint will cause the simulations to always display an endpoint consistent with the current lookback's slope.

While this may be helpful to some traders, this indicator includes an option to produce a less biased range as seen below:

🔶 DETAILS

The Monte Carlo Shuffled Projection tool creates simulations based on the most recent prices within a user-set window. Simulations are done as follows:

Collect each bar's price changes in the user-set window.

Randomize the order of each change in the window.

Project the cumulative sum of the shuffled changes from the current closing price.

Collect data on each point along the way.

This is the process for the Default calculation, for the 'Randomize Direction' calculation, when added onto the front for every other change, the value is inverted, creating the randomized endpoints for each simulation.

The script contains each simulation's data for that bar with a maximum of 1000 simulations.

To get a glimpse behind the scenes each simulation (up to 99) can be viewed using the 'Visualize Simulations' Options as seen below.

Because the script holds the full simulation data, the script can also do calculations on this data, such as calculating standard deviations.

In this script the Standard deviation lines are the average of all standard deviations across the vertical data groups, this provides a singular value that can be displayed a distance away from the simulation center line.

🔶 SETTINGS

Color and Toggle Options are Provided throughout.

Lookback: Sets the number of Bars to include in calculations.

Simulation Count: Sets the number of randomized simulations to calculate. (Max 1000)

Randomize Direction: See Details Above. Creates a more 'Normalized' Distribution

Visualize Simulations: See Details Above. Turns on Visualizations, and colors are randomly generated. Visualized max does not cap the calculated max. If 1000 simulations are used, the data will be from 1000 simulations, however only the last 99 simulations will be visualized.

Standard Deviation Multiplier: Sets the multiplier to use for the Standard Deviation distance away from the center line.

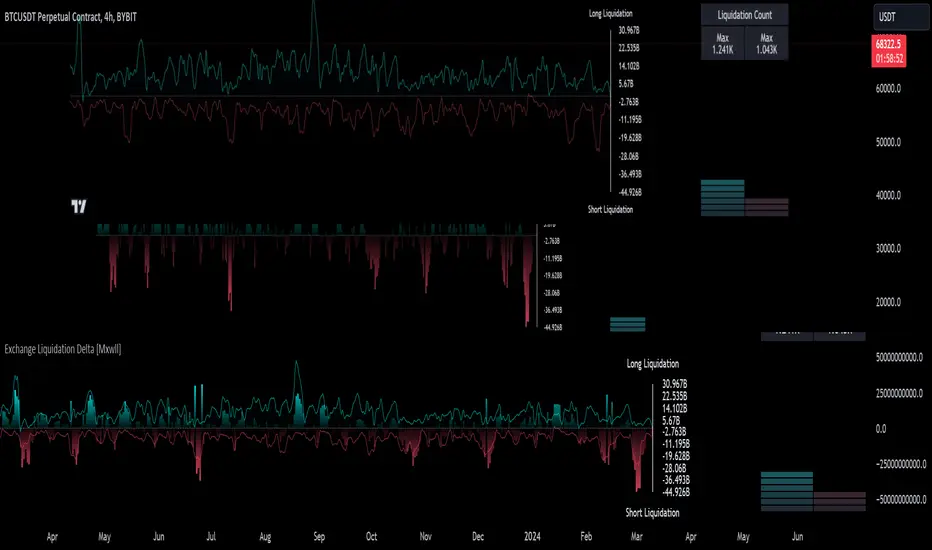

Genuine Liquidation Delta [Mxwll] - No EstimatesTHANK YOU TradingView for allowing us to upload custom data!!!

As a result, Mxwll Capital is providing an indicator that shows REAL liquidation delta for over 100 cryptocurrencies sourced directly from a popular crypto exchange!

Features

Crypto exchange sourced liquidation delta

Crypto exchange sourced long liquidation daily count

Crypto exchange sourced short liquidation daily count

All provided data extends back 2 years!!

Various aesthetic components to illustrate data

Liquidation delta data (sourced from a popular exchange) is provided for:

1000shib

aave

ada

algo

alice

arb

audio

alpha

ankr

ape

apt

atom

avax

axs

bal

band

bat

bch

bel

blz

blur

bnb

bnx

btc

chr

chz

comp

coti

crv

ctk

dash

defi

doge

dot

dydx

edu

egld

enj

ens

eos

etc

eth

fil

flm

ftm

fxs

gala

gmx

grt

hbar

hnt

icx

id

inj

iost

iota

joe

kava

knc

ksm

ldo

lina

link

lit

lrc

ltc

mana

mask

matic

mkr

near

neo

ocean

omg

one

ont

op

people

qtum

reef

ren

rndr

rose

rlc

rsr

rune

rvn

sand

sfp

skl

snx

sol

stmx

storj

sui

sushi

sxp

theta

tomo

trb

trx

unfi

uni

vet

waves

xem

xlm

xmr

xrp

xtz

yfi

zec

zen

zil

zrx

How-To

The image above shows the indicator with default settings.

The image above shows the start point of our data!

Over 2-years of data, allowing for plentiful analysis!

The image above explains the primary plot.

Filled blue columns reflect liquidation delta exceeding the long side. When the liquidation delta plot is aqua and exceeds 0 to the upside, longs were liquidated more than shorts for the

day.

Filled red columns reflect liquidation delta exceeding the short side. When the liquidation delta plot is red and exceeds 0 to the downside, shorts were liquidated more than longs for the day.

The image above explains the solid line (polyline) plot and its intentions!

Filled, solid, blue line reflects the total number of long liquidation events for the period.

Filled, solid, red line reflects the total number of short liquidation events for the period.

Keep in mind that the total number of liquidation events is normalized to plot alongside the total liquidation delta for the day. So, there aren't "millions" of liquidation events taking place, the total liquidation count for the long and short side is simply normalized to fit atop total liquidation delta.

The image above explains the liquidation count meter the indicator provides!

The left (blue columns) reflect the intensity of long liquidation events for the day. The right (red columns) reflect the intensity of short liquidation events for the day.

The "Max" numbers at the top show the maximum number of long liquidation events, or short liquidation events, for their respective columns.

Therefore, if the number of long liquidation events were "1.241k", as stated for this cryptocurrency in the table, the blue meter would be full. Similar logic applies to the red meter.

Once more, THANK YOU @TradingView and @PineCoders for allowing us to upload custom data! This project wouldn't be possible without it!

Psychological levels (Bank levels) PsychoLevels v3 - TartigradiaPsychological levels (Bank levels) plots the closest "round" price levels above and below current price, based on neuroscience research of how humans intuitively calculate in logarithms.

Psychological levels, also called bank levels, are "round" price numbers, by truncating after the nth leftmost digits, around which price often experience resistance or support, because traders and investors tend to set orders around these round numbers.

The calculation done here is fully automatic and dynamic, contrary to other similar scripts, this one uses a mathematical calculation that extracts the 1, 2 or 3 leftmost digits and calculate the previous and next level by incrementing/decrementing these digits. This means it works for any symbol under any price range.

This approach is based on neuroscience research, which found that human brains intuitively approximate numbers on a logarithmic scale, adults and children alike, and similarly to macaques, for more info see Numerical Cognition , Weber-Fechner Law , Zipf law .

For example, if price is at 0.0421, the next major price level is 0.05 and medium one is 0.043. For another asset currently priced at 19354, the next and previous major price levels are 20000 and 10000 respectively, and the next/previous medium levels are 20000 and 19000, and the next/previous weak levels are 19400 and 19300.

IMPORTANT: Please enable "Scale price chart only" in the chart's scale's options, as otherwise major levels may make the chart's scale very small and hard to read.

How it works

At any time, there are 3 levels of strength (1 leftmost digit, 2 leftmost digits, 3 leftmost digits) represented by different sizes, and 3 directional levels for each of these strengths (level above, level below, and half-level) represented by different colors and positions, around current price.

Indeed, contrary to other similar price levels scripts, we do not plot ALL price levels at all times, because otherwise the chart becomes wayyy too cluttered, and also it's highly processing intensive to plot so many lines. So we here use a dynamical approach: we plot only the relevant levels, the closest ones according to current price.

Hence, when a level disappears, it does not mean that it does not exist anymore, but simply that we are not drawing it right now because it is not pertinent for the current price movement (ie, too far away).

Breakouts can be detected in two different ways depending on if SMA is set to a value higher than 1 or not: if SMA == 1, then there is no smoothing, so the levels adapt instantaneously to the current price, so to detect breakout, you should refer to the levels at the previous tick and whether they were broken by current tick's price; if SMA > 1, then there is some smoothing, and so the levels will stay in-place even if there is a breakout, so it's easier to spot breakouts without having to look at the previous ticks, but on the other hand you won't see the new levels for the new price range until after a few more ticks for the smoothing window to adapt. Hence, by default, smoothing is disabled, so that you can see the currently pertinent levels at all time, even right after or during a breakout.

By default, the strong above level is in green, strong below level is in red, medium above level is in blue, medium below level is in yellow, and weak levels aren't displayed but can be. Half levels are also displayed, in a darker color. Strong levels are increments of the first leftmost digit (eg, 10000 to 20000), medium levels are increments of the second leftmost digit (eg, 19000 to 20000), and weak levels of the third leftmost digit (eg, 19100 to 19200). Instead of plotting all the psychological levels all at once as a grid, which makes the chart unintelligible, here the levels adapt dynamically around the current price, so that they show the above/below/half levels relatively to the current price.

Indeed, "half-levels" are also displayed (eg, medium level can also display 19500 instead of only 19000 or 20000). This was made because otherwise the gap between two levels was too big, especially for the strongest levels (eg, there was no major level between 20000 and 30000, but with a half-step we also get a half-level at 25000, and empirically price tends to respect these half levels - I also tried quarter levels but empirically the results were not good). In addition to this hard-coded half-level, you can also create more subdivisions (eg, quarter levels) by setting the simple moving average to a value higher than 1.

The script can be made to run on the daily timeframe whatever the current chart's timeframe is, to reduce the variability in levels, to make it less noisy than intraday price movement. But by default, the chart resolution is used, because I empirically found that the levels found with this indicator work on all time resolutions quite well.

The step can be adjusted to increase the gap between levels, eg, if you want to display one every 2 levels then input step = 2 (eg, 22000, 24000, 26000, etc), or if you want to display quarter levels, input 0.25 (eg, 22000, 22250, 22500, etc). The default values should fit most use cases and cover most psychological levels.

How to read

Focust first on bigger dotted levels, they are stronger and more likely to cause a rebound or a major event or price to stay at this level.

Remember that it's not enough to just look at levels, the context is important, because levels have various effects depending on current price movement: if price is above a level, the level is a support on which price can rebound; if price is below a level, the level is a resistance on which price can rebound (or break); and finally sometimes price also stays hovering around a level for some time.

Levels closer to 9 are less weaker, and levels closer to 0 are stronger, according to Zipf law. This is now reflected since v3 in the transparency, levels that are closer to 9 will be more transparent.

The switch in color for the same level illustrates how a level switches from being a support to a resistance and inversely. Eg, if a major level turns from green to red, then it changed from being a resistance (above) to a support (below).

As is well known in trading, longer standing levels are stronger. This indicator provides a direct illustration: in practice, the number of consecutive dots on the same line influences the strength of the level: the longer the chain of dots, the more you can expect this price level to be significant. The length does not mean the level will necessarily hold, but that other traders are likely to monitor if it holds, and if not then price will break down. Hence, longer levels are good spots to place stop losses, or to enter trades depending on your strategy. In general, a single dot is not enough to consider a level significant, but 2 or more is a good enough level, and 10+ is a strong level. Intuitively, this makes sense, and is what pro traders do: the longer a level is tested, the stronger it is. This indicator can visually represent this intuition and allows to use it as a more systematic trading signal.

Motivation

I initially made the first version of the PsychoLevels indicator mainly to train with PineScript, but I found it surprisingly accurate to define levels that are respected by price movements. So I guess it can be useful for new traders and experienced traders alike, as it's easy to forget that psychological levels can often be as strong if not stronger than technical levels. It can also be used to quickly screen other minor assets for trading opportunities. For example, a hybrid strategy would be to manually define levels on BTCUSD but using this script to automatically define levels in crypto altcoins and quickly screen them for a trade opportunity that can be greater than with BTCUSD but with the same trend.

Personally, although initially I did not believe an automated tool would work well for this purpose, I could now empirically verify that it is quite reliable for the purpose of detecting levels, and so I use it all the time to find the levels automatically and help me monitor them like a hawk, so that I only have to draw uber major levels, the ones that last between cycles and that are hard to autodetect, but otherwise all daily/weekly levels are usually covered. However, trendlines must still be drawn manually or with another indicator (but note that up to now I have found none that worked well enough), as PsychoLevels only draws levels (ie, horizontal lines, not oblique ones!).

Differences with the previous version PsychoLevels v2

price levels now have a transparency according to their importance for the human brain: numbers closer to 9 are weaker, and numbers closer to 0 are stronger and represent a major psychological threshold (eg, that's why prices marked as $9.99 sell better than $10.00). This option can be disabled to get the exact same behavior as v2.

modularized and typed code

PsychoLevels v2 can be found here:

Psychological levels (Bank levels) PsychoLevels v2 - TartigradiaPsychological levels (Bank levels) plots "round" price levels above and below current price, by truncating after the nth leftmost digits, based on neuroscience research of how humans intuitively calculate in logarithms.

Psychological levels, also called bank levels, are "round" price numbers around which price often experience resistance or support, because traders and investors tend to set orders around these round numbers.

Calculation here is fully automatic and dynamic, contrary to other similar scripts, this one uses a mathematical calculation that extracts the 1, 2 or 3 leftmost digits and calculate the previous and next level by incrementing/decrementing these digits. This means it works for any symbol under any price range.

This approach is based on neuroscience research, which found that human brains intuitively approximate numbers on a logarithmic scale, adults and children alike, and similarly to macaques, for more info see Numerical Cognition , Weber-Fechner Law , Zipf law.

For example, if price is at 0.0421, the next major price level is 0.05 and medium one is 0.043. For another asset currently priced at 19354, the next and previous major price levels are 20000 and 10000 respectively, and the next/previous medium levels are 20000 and 19000, and the next/previous weak levels are 19400 and 19300.

Usage:

* By default, strong upper level is in green, strong lower level is in red, medium upper level is in blue, medium lower level is in yellow, and weak levels aren't displayed but can be. Half levels are also displayed, in a darker color. Strong levels are increments of the first leftmost digit (eg, 10000 to 20000), medium levels are increments of the second leftmost digit (eg, 19000 to 20000), and weak levels of the third leftmost digit (eg, 19100 to 19200). Instead of plotting all the psychological levels all at once as a grid, which makes the chart unintelligible, here the levels adapt dynamically around the current price, so that they show the upper/lower levels relatively to the current price.

* A simple moving average is implemented, so that "half-levels" are also displayed when relevant (eg, medium level can also display 19500 instead of only 19000 or 20000). This can be disabled by setting smoothing to 1.

* By default, the script runs on the daily timeframe, whatever the current chart's timeframe is. This is to reduce the variability in levels, to make it less noisy than intraday price movement, but this can be changed in the settings.

* The step can be adjusted to increase the gap between levels, eg, if you want to display one every 2 levels then input step = 2 (eg, 22000, 24000, 26000, etc), or if you want to display quarter levels, input 0.25 (eg, 22000, 22250, 22500, etc). The default values should fit most use cases and cover most psychological levels.

I made this script mainly to train with PineScript, but I found it surprisingly accurate to define levels that are respected by price movements. So I guess it can be useful for new traders and experienced traders alike, as it's easy to forget that psychological levels can often be as strong if not stronger than technical levels. It can also be used to quickly screen other minor assets for trading opportunities. For example, a hybrid strategy would be to manually define levels on BTCUSD but using this script to automatically define levels in crypto altcoins and quickly screen them for a trade opportunity that can be greater than with BTCUSD but with the same trend.

Changes compared to v1:

* Deduplicated redundant calculations and hence faster script.

* Added half-step levels, which allows to more easily see breakouts (because the levels are still on-screen).

* All steps are now configuration on the GUI.

* Revamped color scheme.

* And major reasons to post as a separate v2 script rather than updating: because we can't update the original description nor screenshot. I have now read more about the House Rules and saw other scriptmakers, so I am trying to write better descriptions like wizards do, by explaining not only how the script works but what the underlying financial concept is to a neophyte audience.

Psychological levels (Bank levels) by tartigradiaPsychological levels (Bank levels) plots the price levels by truncating after the nth leftmost digits, as it appears the humain brain tends to intuitively calculate in log/zipf.

Contrary to other similar scripts, this one uses a mathematical calculation that extracts the 1, 2 or 3 leftmost digits and calculate the previous and next level by incrementing/decrementing these digits. This means it works for any asset at any price range.

For example, if price is at 0.0421, the next major price level is 0.05 and medium one is 0.043. For another asset currently priced at 19354, the next and previous major price levels are 20000 and 10000 respectively, and the next/previous medium levels are 20000 and 19000, and the next/previous weak levels are 19400 and 19300.

By default, strong upper level is in green, strong lower level is in red, medium upper level is in blue, medium lower level is in yellow, and weak levels aren't displayed but can be. Strong levels are increments of the first leftmost digit (eg, 10000 to 20000), medium levels are increments of the second leftmost digit (eg, 19000 to 20000), and weak levels of the third leftmost digit (eg, 19100 to 19200). Instead of plotting all the psychological levels all at once as a grid, which makes the chart unintelligible, here the levels adapt dynamically around the current price, so that they show the upper/lower levels relatively to the current price.

A simple moving average is implemented, so that "half-levels" are also displayed when relevant (eg, medium level can also display 19500 instead of only 19000 or 20000). This can be disabled by setting smoothing to 1.

I made this script mainly to train with PineScript, but I guess it can be useful for new traders, as it's easy to forget that psychological levels can often be as strong if not stronger than technical levels.

Realtime FootprintThe purpose of this script is to gain a better understanding of the order flow by the footprint. To that end, i have added unusual features in addition to the standard features.

I use "Real Time 5D Profile by LucF" main engine to create basic footprint(profile type) and added some popular features and my favorites.

This script can only be used in realtime, because tradingview doesn't provide historical Bid/Ask date.

Bid/Ask date used this script are up/down ticks.

This script can only be used by time based chart (1m, 5m , 60m and daily etc)

This script use many labels and these are limited max 500, so you can't display many bars.

If you want to display foot print bars longer, turn off the unused sub-display function.

Default setting is footprint is 25 labels, IB count is 1, COT high and Ratio high is 1, COT low and Ratio low is 1 and Delta Box Ratio Volume is 1 , total 29.

plus UA , IB stripes , ladder fading mark use several labels.

///////// General Setting ///////////

Resets on Volume / Range bar

: If you want to use simple time based Resets on, please set Total Volume is 0.

Your timeframe is always the first condition. So if you set Total Volume is 1000, both conditions(Volume >= 1000 and your timeframe start next bar) must be met. (that is, new footprint bar doesn't start at when total volume = exactly 1000).

Ticks per row and Maximum row of Bar

: 1 is minimum size(tick). "Maximum row of Bar" decide the number of rows used in one footprint. 1 row is created from 1 label, so you need to reduce this number to display many footprints (Max label is 500).

Volume Filter and For Calculation and Display

: "Volume Filter" decide minimum size of using volume for this script.

"For Calculation and Display" is used to convert volume to an integer.

This script only use integer to make profile look better (I contained Bid number and Ask number in one row( one label) to saving labels. This require to make no difference in width by the number of digits and this script corresponds integers from 0 to 3 digits).

ex) Symbol average volume size is from 0.0001 to 0.001. You decide only use Volume >= 0.0005 by "Volume Filter".

Next, you convert volume to integer, by setting "For Calculation and Display" is 1000 (0.0005 * 1000 = 5).

If 0.00052 → 5.2 → 5, 0.00058 → 5.8 → 6 (Decimal numbers are rounded off)

This integer is used to all calculation in this script.

//////// Main Display ///////

Footprint, Total, Row Delta, Diagonal Delta and Profile

: "Footprint" display Ask and Bid per row. "Total" display Ask + Bid per row.

"Row Delta" display Ask - Bid per row. "Diagonal Delta" display Ask(row N) - Bid(row N -1) per row.

Profile display Total Volume(Ask + Bid) per row by using Block. Profile Block coloring are decided by Row Delta value(default: positive Row Delta (Ask > Bid) is greenish colors and negative Row Delta (Ask < Bid) is reddish colors.)

Volume per Profile Block, Row Imbalance Ratio and Delta Bull/Bear/Neutral Colors

: "Volume per Profile Block" decide one block contain how many total volume.

ex) When you set 20, Total volume 70 display 3 block.

The maximum number of blocks that can be used per low is 20.

So if you set 20, Total volume 400 is 20 blocks. total volume 800 is 20 blocks too.

"Row Imbalance Ratio" decide block coloring. The row imbalance is that the difference between Ask and Bid (row delta) is large.

default is x3, x2 and x1. The larger the difference, the brighter the color.

ex) Ask 30 Bid 10 is light green. Ask 20 Bid 10 is green. Ask 11 Bid 10 is dark green.

Ask 0 Bid 1 is light red. Ask 1 Bid 2 is red. ask 30 Bid 59 is dark green.

Ask 10 Bid 10 is neutral color(gray)

profile coloring is reflected same row's other elements(Ask, Bid, Total and Delta) too.

It's because one label can only use one text color.

/////// Sub Display ///////

Delta, total and Commitment of Traders

: "Delta" is total Ask - total Bid in one footprint bar. Total is total Ask + total Bid in one footprint bar.

"Commitment of traders" is variation of "Delta". COT High is reset to 0 when current highest is touched. COT Low is opposite.

Basic concept of Delta is to compare price with Delta. Ordinary, when price move up, delta is positive. Price move down is negative delta.

This is because market orders move price and market orders are counted by Delta (although this description is not exactly correct).

But, sometimes prices do not move even though many market orders are putting pressure on price , or conversely, price move strongly without many market orders.

This is key point. Big player absorb market orders by iceberg order(Subdivide large orders and pretend to be small limit orders.

Small limit orders look weak in the order book, but they are added each time you fill, so they are more powerful than they look.), so price don't move.

On the other hand, when the price is moving easily, smart players may be aiming to attract and counterattack to a better price for them.

It's more of a sport than science, and there's always no right response. Pay attention to the relationship between price, volume and delta.

ex) If COT Low is large negative value, it means many sell market orders is coming, but iceberg order is absorbing their attack at limit order.

you should not do buy entry, only this clue. but this is one of the hints.

"Delta, Box Ratio and Total texts is contained same label and its color are "Delta" coloring. Positive Delta is Delta Bull color(green),Negative Delta is Delta Bear Color

and Delta = 0 is Neutral Color(gray). When Delta direction and price direction are opposite is Delta Divergence Color(yellow).

I didn't add the cumulative volume delta because I prefer to display the CVD line on the price chart rather than the number.

Box Ratio , Box Ratio Divisor and Heavy Box Ratio Ratio

: This is not ordinary footprint features, but I like this concept so I added.

Box Ratio by Richard W. Arms is simple but useful tool. calculation is "total volume (one bar) divided by Bar range (highest - lowest)."

When Bull and bear are fighting fiercely this number become large, and then important price move happen.

I made average BR from something like 5 SMA and if current BR exceeds average BR x (Heavy Box Ratio Ratio), BR box mark will be filled.

Box Ratio Divisor is used to good looking display(BR multiplied by Box Ratio Divisor is rounded off and displayed as an integer)

Diagonal Imbalance Count , D IB Mark and D IB Stripes

: Diagonal Imbalance is defined by "Diagonal Imbalance Ratio".

ex) You set 2. When Ask(row N) 30 Bid(row N -1)10, it's 30 > 10*2, so positive Diagonal Imbalance.

When Ask(row N) 4 Bid(row N -1)9, it's 4*2 < 9, so negative Diagonal Imbalance.

This calculation does not use equals to avoid Ask(row N) 0 Bid(row N -1)0 became Diagonal Imbalance.

Ask(row N) 0 Bid(row N -1)0, it's 0 = 0*2, not Diagonal Imbalance. Ask(row N) 10 Bid(row N -1)5, it's 10 = 5*2, not Diagonal Imbalance.

"D IB Mark" emphasize Ask or Bid number which is dominant side(Winner of Diagonal Imbalance calculation), by under line.

"Diagonal Imbalance Count" compare Ask side D IB Mark to Bid side D IB Mark in one footprint.

Coloring depend on which is more aggressive side (it has many IB Mark) and When Aggressive direction and price direction are opposite is Delta Divergence Color(yellow).

"D IB Stripes" is a function that further emphasizes with an arrow Mark, when a DIB mark is added on the same side for three consecutive row. Three consecutive arrow is added at third row.

Unfinished Auction, Ratio Bounds and Ladder fading Mark

: "Unfinished Auction" emphasize highest or lowest row which has both Ask and Bid, by Delta Divergence Color(yellow) XXXXXX mark.

Unfinished Auction sometimes has magnet effect, price may touch and breakout at UA side in the future.

This concept is famous as profit taking target than entry decision.

But, I'm interested in the case that Big player make fake breakout at UA side and trapped retail traders, and then do reversal with retail traders stop-loss hunt.

Anyway, it's not stand alone signal.

"Ratio Bounds" gauge decrease of pressure at extreme price. Ratio Bounds High is number which second highest ask is divided by highest ask.

Ratio Bounds Low is number which second lowest bid is divided by lowest bid. The larger the number, the less momentum the price has.

ex)first footprint bar has Ratio Bounds Low 2, second footprint bar has RBL 4, third footprint bar has RBL 20.

This indicates that the bear's power is gradually diminishing.

"Ladder fading mark" emphasizes the decrease of the value in 3 consecutive row at extreme price. I added two type Marks.

Ask/Bid type(triangle Mark) is Ask/Bid values are decreasing of three consecutive row at extreme price.

Row Imbalance type(Diamond Mark) are row Imbalance values are decreasing of three consecutive row at extreme price.

ex)Third lowest Bid 40, second lowest Bid 10 and lowest Bid 5 have triangle up Mark. That is bear's power is gradually diminishing.

(This Mark only check Bid value at lowest price and Ask value at highest price).

Third highest row delta + 60, second highest row delta + 5, highest delta - 20 have diamond Mark. That is Bull's power is gradually diminishing.

Sub display use Delta colors at bottom of Sub display section.

////// Candle & POC /////////

candle and POC

: Ordinary, "POC" Point of Control is row of largest total volume, but this script'POC is volume weighted average.

This is because the regular POC was visually displayed by the profile ,and I was influenced LucF's ideas.

POC coloring is decided in relation to the previous POC. When current POC is higher than previous POC, color is UP Bar Color(green).

In the opposite case, Down Bar color is used.

POC Divergence Color is used when Current POC is up but current bar close is lower than open (Down price Bar),or in the opposite case.

POC coloring has option also highlight background by Delta Divergence Color(yellow). but bg color is displayed at your time frame current price bar not current footprint bar.

The basic explanation is over.

I add some image to promote understanding basic ideas.

Indicators Combination Framework v3 IND [DTU]Hello All,

This script is a framework to analyze and see the results by combine selected indicators for (long, short, longexit, shortexit) conditions.

I was designed this for beginners and users to facilitate to see effects of the technical indicators combinations on the chart WITH NO CODE

You can improve your strategies according the results of this system by connecting the framework to a strategy framework/template such as Pinecoder, Benson, daveatt or custom.

This is enhanced version of my previous indicator "Indicators & Conditions Test Framework "

Currently there are 93 indicators (23 newly added) connected over library. You can also import an External Indicator or add Custom indicator (In the source)

It is possible to change it from Indicator to strategy (simple one) by just remarking strategy parts in the source code and see real time profit of your combinations

Feel free to change or use it in your source

Special thanks goes to Pine wizards: Trading view (built-in Indicators), @Rodrigo, @midtownsk8rguy, @Lazybear, @Daveatt and others for their open source codes and contributions

SIMPLE USAGE

1. SETTING: Show Alerts= True (To see your entries and Exists)

2. Define your Indicators (ex: INDICATOR1: ema(close,14), INDICATOR2: ema(close,21), INDICATOR3: ema(close,200)

3. Define Your Combinations for long & Short Conditions

a. For Long: (INDICATOR1 crossover INDICATOR2) AND (INDICATOR3 < close)

b. For Short: (INDICATOR1 crossunder INDICATOR2) AND (INDICATOR3 > close)

4. Select Strategy/template (Import strategy to chart) that you export your signals from the list

5. Analyze the best profit by changing Indicators values

SOME INDICATORS DETAILS

Each Indicator includes:

- Factorization : Converting the selected indicator to Double, triple Quadruple such as EMA to DEMA, TEMA QEMA

- Log : Simple or log10 can be used for calculation on function entries

- Plot Type : You can overlay the indicator on the chart (such ema) or you can use stochastic/Percentrank approach to display in the variable hlines range

- Extended Parametes : You can use default parameters or you can use extended (P1,P2) parameters regarding to indicator type and your choice

- Color : You can define indicator color and line properties

- Smooth : you can enable swma smooth

- indicators : you can select one of the 93 function like ema(),rsi().. to define your indicator

- Source : you can select from already defined indicators (IND1-4), External Indicator (EXT), Custom Indicator (CUST), and other sources (close, open...)

CONDITION DETAILS

- There are are 4 type of conditions, long entry, short entry, long exit, short exit.

- Each condition are built up from 4 combinations that joined with "AND" & "OR" operators

- You can see the results by enabling show alerts check box

- If you only wants to enter long entry and long exit, just fill these conditions

- If "close on opposite" checkbox selected on settings, long entry will be closed on short entry and vice versa

COMBINATIONS DETAILS

- There are 4 combinations that joined with "AND" & "OR" operators for each condition

- combinations are built up from compare 1st entry with 2nd one by using operator

- 1st and 2nd entries includes already defined indicators (IND1-5), External Indicator (EXT), Custom Indicator (CUST), and other sources (close, open...)

- Operators are comparison values such as >,<, crossover,...

- 2nd entry include "VALUE" parameter that will use to compare 1st indicator with value area

- If 2nd indicator selected different than "VALUE", value are will mean previous value of the selection. (ex: value area= 2, 2nd entry=close, means close )

- Selecting "NONE" for the 1st entry will disable calculation of current and following combinations

JOINS DETAILS

- Each combination will join wiht the following one with the JOIN (AND, OR) operator (if the following one is not equal "NONE")

CUSTOM INDICATOR

- Custom Indicator defines harcoded in the source code.

- You can call it with "CUST" in the Indicator definition source or combination entries source

- You can change or implement your custom indicator by updating the source code

EXTERNAL INDICATOR

- You can import an external indicator by selecting it from the ext source.

- External Indicator should be already imported to the chart and it have an plot function to output its signal

EXPORTING SIGNAL

- You can export your result to an already defined strategy template such as Pine coders, Benson, Daveatt Strategy templates

- Or you can define your custom export for other future strategy templates

ALERTS

- By enabling show alerts checkbox, you can see long entry exits on the bottom, and short entry exits aon the top of the chart

ADDITIONAL INFO

- You can see all off the inputs descriptions in the tooltips. (You can also see the previous version for details)

- Availability to set start, end dates

- Minimize repainting by using security function options (Secure, Semi Secure, Repaint)

- Availability of use timeframes

-

Version 3 INDICATORS LIST (More to be added):

▼▼▼ OVERLAY INDICATORS ▼▼▼

alma(src,len,offset=0.85,sigma=6).-------Arnaud Legoux Moving Average

ama(src,len,fast=14,slow=100).-----------Adjusted Moving Average

accdist().-------------------------------Accumulation/distribution index.

cma(src,len).----------------------------Corrective Moving average

dema(src,len).---------------------------Double EMA (Same as EMA with 2 factor)

ema(src,len).----------------------------Exponential Moving Average

gmma(src,len).---------------------------Geometric Mean Moving Average

highest(src,len).------------------------Highest value for a given number of bars back.

hl2ma(src,len).--------------------------higest lowest moving average

hma(src,len).----------------------------Hull Moving Average.

lagAdapt(src,len,perclen=5,fperc=50).----Ehlers Adaptive Laguerre filter

lagAdaptV(src,len,perclen=5,fperc=50).---Ehlers Adaptive Laguerre filter variation

laguerre(src,len).-----------------------Ehlers Laguerre filter

lesrcp(src,len).-------------------------lowest exponential esrcpanding moving line

lexp(src,len).---------------------------lowest exponential expanding moving line

linreg(src,len,loffset=1).---------------Linear regression

lowest(src,len).-------------------------Lovest value for a given number of bars back.

mcginley(src, len.-----------------------McGinley Dynamic adjusts for market speed shifts, which sets it apart from other moving averages, in addition to providing clear moving average lines

percntl(src,len).------------------------percentile nearest rank. Calculates percentile using method of Nearest Rank.

percntli(src,len).-----------------------percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

previous(src,len).-----------------------Previous n (len) value of the source

pivothigh(src,BarsLeft=len,BarsRight=2).-Previous pivot high. src=src, BarsLeft=len, BarsRight=p1=2

pivotlow(src,BarsLeft=len,BarsRight=2).--Previous pivot low. src=src, BarsLeft=len, BarsRight=p1=2

rema(src,len).---------------------------Range EMA (REMA)

rma(src,len).----------------------------Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sar(start=len, inc=0.02, max=0.02).------Parabolic SAR (parabolic stop and reverse) is a method to find potential reversals in the market price direction of traded goods.start=len, inc=p1, max=p2. ex: sar(0.02, 0.02, 0.02)

sma(src,len).----------------------------Smoothed Moving Average

smma(src,len).---------------------------Smoothed Moving Average

super2(src,len).-------------------------Ehlers super smoother, 2 pole

super3(src,len).-------------------------Ehlers super smoother, 3 pole

supertrend(src,len,period=3).------------Supertrend indicator

swma(src,len).---------------------------Sine-Weighted Moving Average

tema(src,len).---------------------------Triple EMA (Same as EMA with 3 factor)

tma(src,len).----------------------------Triangular Moving Average

vida(src,len).---------------------------Variable Index Dynamic Average

vwma(src,len).---------------------------Volume Weigted Moving Average

volstop(src,len,atrfactor=2).------------Volatility Stop is a technical indicator that is used by traders to help place effective stop-losses. atrfactor=p1

wma(src,len).----------------------------Weigted Moving Average

vwap(src_).------------------------------Volume Weighted Average Price (VWAP) is used to measure the average price weighted by volume

▼▼▼ NON OVERLAY INDICATORS ▼▼

adx(dilen=len, adxlen=14, adxtype=0).----adx. The Average Directional Index (ADX) is a used to determine the strength of a trend. len=>dilen, p1=adxlen (default=14), p2=adxtype 0:ADX, 1:+DI, 2:-DI (def:0)

angle(src,len).--------------------------angle of the series (Use its Input as another indicator output)

aroon(len,dir=0).------------------------aroon indicator. Aroons major function is to identify new trends as they happen.p1 = dir: 0=mid (default), 1=upper, 2=lower

atr(src,len).----------------------------average true range. RMA of true range.

awesome(fast=len=5,slow=34,type=0).------Awesome Oscilator is an indicator used to measure market momentum. defaults : fast=len= 5, p1=slow=34, p2=type: 0=Awesome, 1=difference

bbr(src,len,mult=1).---------------------bollinger %%

bbw(src,len,mult=2).---------------------Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci(src,len).----------------------------commodity channel index

cctbbo(src,len).-------------------------CCT Bollinger Band Oscilator

change(src,len).-------------------------A.K.A. Momentum. Difference between current value and previous, source - source . is most commonly referred to as a rate and measures the acceleration of the price and/or volume of a security

cmf(len=20).-----------------------------Chaikin Money Flow Indicator used to measure Money Flow Volume over a set period of time. Default use is len=20

cmo(src,len).----------------------------Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog(src,len).----------------------------The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

copcurve(src,len).-----------------------Coppock Curve. was originally developed by Edwin Sedge Coppock (Barrons Magazine, October 1962).

correl(src,len).-------------------------Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count(src,len).--------------------------green avg - red avg

cti(src,len).----------------------------Ehler s Correlation Trend Indicator by

dev(src,len).----------------------------ta.dev() Measure of difference between the series and its ta.sma

dpo(len).--------------------------------Detrended Price OScilator is used to remove trend from price.

efi(len).--------------------------------Elders Force Index (EFI) measures the power behind a price movement using price and volume.

eom(len=14,div=10000).-------------------Ease of Movement.It is designed to measure the relationship between price and volume.p1 = div: 10000= (default)

falling(src,len).------------------------ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

fisher(len).-----------------------------Fisher Transform is a technical indicator that converts price to Gaussian normal distribution and signals when prices move significantly by referencing recent price data

histvol(len).----------------------------Historical volatility is a statistical measure used to analyze the general dispersion of security or market index returns for a specified period of time.

kcr(src,len,mult=2).---------------------Keltner Channels Range

kcw(src,len,mult=2).---------------------ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

klinger(type=len).-----------------------Klinger oscillator aims to identify money flow’s long-term trend. type=len: 0:Oscilator 1:signal

macd(src,len).---------------------------MACD (Moving Average Convergence/Divergence)

mfi(src,len).----------------------------Money Flow Index s a tool used for measuring buying and selling pressure

msi(len=10).-----------------------------Mass Index (def=10) is used to examine the differences between high and low stock prices over a specific period of time

nvi().-----------------------------------Negative Volume Index

obv().-----------------------------------On Balance Volume

pvi().-----------------------------------Positive Volume Index

pvt().-----------------------------------Price Volume Trend

ranges(src,upper=len, lower=-5).---------ranges of the source. src=src, upper=len, v1:lower=upper . returns: -1 source=upper otherwise 0

rising(src,len).-------------------------ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc(src,len).----------------------------Rate of Change

rsi(src,len).----------------------------Relative strength Index

rvi(src,len).----------------------------The Relative Volatility Index (RVI) is calculated much like the RSI, although it uses high and low price standard deviation instead of the RSI’s method of absolute change in price.

smi_osc(src,len,fast=5, slow=34).--------smi Oscillator

smi_sig(src,len,fast=5, slow=34).--------smi Signal

stc(src,len,fast=23,slow=50).------------Schaff Trend Cycle (STC) detects up and down trends long before the MACD. Code imported from

stdev(src,len).--------------------------Standart deviation

trix(src,len) .--------------------------the rate of change of a triple exponentially smoothed moving average.

tsi(src,len).----------------------------The True Strength Index indicator is a momentum oscillator designed to detect, confirm or visualize the strength of a trend.

ultimateOsc(len.-------------------------Ultimate Oscillator indicator (UO) indicator is a technical analysis tool used to measure momentum across three varying timeframes

variance(src,len).-----------------------ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta.sma), and it informally measures how far a set of numbers are spread out from their mean.

willprc(src,len).------------------------Williams %R

wad().-----------------------------------Williams Accumulation/Distribution.

wvad().----------------------------------Williams Variable Accumulation/Distribution.

HISTORY

v3.01

ADD: 23 new indicators added to indicators list from the library. Current Total number of Indicators are 93. (to be continued to adding)

ADD: 2 more Parameters (P1,P2) for indicator calculation added. Par:(Use Defaults) uses only indicator(Source, Length) with library's default parameters. Par:(Use Extra Parameters P1,P2) use indicator(Source,Length,p1,p2) with additional parameters if indicator needs.

ADD: log calculation (simple, log10) option added on indicator function entries

ADD: New Output Signals added for compatibility on exporting condition signals to different Strategy templates.

ADD: Alerts Added according to conditions results

UPD: Indicator source inputs now display with indicators descriptions

UPD: Most off the source code rearranged and some functions moved to the new library. Now system work like a little bit frontend/backend

UPD: Performance improvement made on factorization and other source code

UPD: Input GUI rearranged

UPD: Tooltips corrected

REM: Extended indicators removed

UPD: IND1-IND4 added to indicator data source. Now it is possible to create new indicators with the previously defined indicators value. ex: IND1=ema(close,14) and IND2=rsi(IND1,20) means IND2=rsi(ema(close,14),20)

UPD: Custom Indicator (CUST) added to indicator data source and Combination Indicator source.

UPD: Volume added to indicator data source and Combination Indicator source.

REM: Custom indicators removed and only one custom indicator left

REM: Plot Type "Org. Range (-1,1)" removed

UPD: angle, rising, falling type operators moved to indicator library

Indicators & Conditions Test Framework [DTU]Hello All,

This script is a framework to build strategies by combining indicators and conditions (long, short, exits). You are able to analyze your strategies in realtime by changing the input parameters related to indicators, conditions and their combinations.

OVERVIEW

With this Study/Strategy framework, you will be able to create strategy conditions, display them on the chart, and test them using existing indicators as well as external and custom indicators that you can add.

The main purpose of the Framework is to choose your indicators to be used in the conditions and test your strategy by producing your "Long, short, Exit long, Exit short" combinations.

Although may be, it can be a bit difficult and complicated at first start, but you can understand the logic on its use in a very short time.

Notes:

I removed external links off descriptive images and video to be comply with Trading view violation House Rules

Since I am new in the community and still trying to understand the pine script language I can make errors and violations on my script. Please Inform me on any issue that I made..

HOW TO

STEP 1: SETTINGS ______________________________________________________________________________________________________

SOURCE, TIMEFRAME, SECURITY

Select the Source, timeframe and Secure type that your indicators will use.

Here, the Secure entry consists of 3 parts and the f_security function is used to determine it.

a)Secure

This option is defined as reducing repaint in tradingview calculations as much as possible. The following function is used.

request.security(_symbol, _res, _src , lookahead=barmerge.lookahead_on)

b)Semi Secure

While this option can reduce repaint in tradingview calculations as much as possible, it is less secure. The following function is used.

request.security(_symbol, _res, _src )

c)Repaint

This option turns on the repaint feature. The following function is used.

request.security(_symbol, _res, _src ) : na

Ind Source:

You can the source that indicators will use their own calculations

Ext Source:

You can import external Indicator sources from here . It appears on condition/combination area as "EXT".

To export the External indicator plot it with a title. It will be visible in source dropdown input

PERIOD , ALERTS...

Period:

Determine your strategy testing period by selecting start and end date/time

(!!! According to your tradingview subscription, it takes the last 5000, 10000.. bars.

The extra bar option may cause problems such as not appearing in the calculations or errors).

Plot Alerts:

Plot condition result as alerts arrows on the chart's bottom for "LONG" and the top for "SHORT" entries, exits

Close on opposite:

When selected, a long entry gets closed when a short entry opens and vice versa

Show Profit:

It appears if script is in strategy mode (not in study) this can display current or open profit for better reanalyzing your strategy entry exit points. (Currently under development)

PLOT TYPE OPERATIONS

This option has 4 entries

a) Mult

Sets the multiplier for the selected Plot Type (stochastic, Percentrank, Org Range (-1,1) ) except for "Original" in the range (-1,1).

EXAMPLE: When 1000 is selected, the indicator in the range of (-1,1) will appear in the range of (-1000, 1000) on the screen.

b) Shift

It determines the shift that will appear on the screen for the selected Plot Type (stochastic, Percentrank,Org Range (-1,1) ) in the range (-1,1) other than "Original".

EXAMPLE: When Shift:35000 and mult:1000 are selected, the indicator will appear in the range (34000, 36000) on the screen.

c) Smooth

This option (only for Stochastic & PercentRank) allows to smooth the indicator to be displayed.

Here, tradinview ta.swma function is used.

b) hline

Adjusts the horizontal lines to appear on the screen according to the mult factor for the range (-1,1)

The lines represent the values (-1, -05, 0, 05, 1)

STEP 2: INDICATORS ______________________________________________________________________________________________________

You need to choose indicators that you can use in strategy conditions.

Here, the indicators come from the dturkuler/lib_Indicators_DT open script library defined in the code

In addition, you can add the indicators that you will create in the area defined in the code to this list..

You can also import external indicators and test them with other variables on the system..

You can choose a maximum of 5 indicators that you can use in total. (can be increased in new versions)

Indicators are categorized in 3 main sections

Indicator Selection:

You can select your indicators from this area

a)Moving Averages

These are indicators such as EMA, SMA that you can show on the stock. They come from the library.

These indicators are fed from Settings/source. Only the length value can be used as a parameter.

In addition, line colors can be changed..

As of now, there are 28 indicators in the library in total and 5 indicators are left as future use for this field for now.

b)Other Indicators

These are different indicators from the stock value such as RSI, COG. They come from the library. These indicators are fed from Settings/source.

Only the length value can be used as a parameter. In addition, line colors can be changed.

As of now, there are 24 indicators in the library in total and 5 indicators are left as a future use for this field for now.

c)Custom Indicators

These indicators are the ones you can create by programming yourself in the source code..

The area at the bottom of the settings screen is reserved for the parameters of this type of indicators.

Indicator Length:

You can update your selected indicator length value from here. (Not: it doesn't work for custom indicators since they have their parameter on cust. Ind. input screen )

Indicator Plot Type:

Next to the indicators, there is an input selection field about how they will be displayed on the screen.

a)Original

The indicator is displayed on the screen with its current values. It is an ideal solution for displaying moving average indicators such as (EMA, SMA) over current stock.

Since the values of indicators such as (RSI, COB) are low (-100,100 : -1.1), they appear at the bottom of the screen and make analysis difficult.

For this reason, other options may be more suitable for these.

b)Stochastic

The indicator is displayed on the screen with stochastic calculation in the range of -1.1.

It uses the stochastic(50) calculation method to spread indicators such as (RSI, COB) over the range (-1,1).

Indicators in this selection can be fixed and monitored under stock on the screen with the parameters under the Plot Type section.

You can see the original values of the relevant indicator on the Data Window screen.

(!!! Do not use the values on the chart in your condition calculations. Instead, get the values from Data Window)

c)PercentRank

The indicator is displayed on the screen with stochastic calculation in the range of -1.1. .

Since the values of indicators such as (RSI, COB) are low (-100,100 : -1.1), they appear at the bottom of the screen and make analysis difficult.

Indicators in this selection can be fixed and monitored under stock on the screen with the parameters under the Plot Type section.

You can see the original values of the relevant indicator on the Data Window screen

((!!! Do not use the values on the chart in your condition calculations. Instead, get the values from Data Window)

d)Org Range (-1,1)

If your indicator is in the range of -1.1, your indicator will be displayed on the screen with its original calculation in the range of -1.1.

Indicators in this selection can be fixed and monitored under stock on the screen with the parameters under the Plot Type section.

You can see the original values of the relevant indicator on the Data Window screen.

(!!! Do not use the values on the chart in your fitness calculations. Instead, get the values from Data Window)

STEP 2 NOTES:

STEP 3: CONDITIONS ______________________________________________________________________________________________________

After choosing the indicators you will use in the conditions, you move on to the "CONDITIONS" section.

There are 4 conditions type here.

• LONG ENTRY CONDITION

• SHORT ENTRY CONDITION

• LONG CLOSE CONDITION

• SHORT CLOSE CONDITION

The use of each condition is the same.

There are 3 combinations you can use in each condition. (can be increased in new versions)

a)COMBINATIONS

There are 3 combinations you can use in each condition. (can be increased in new versions)

Each combination are build from 4 parts

1)1st Indicator

If set to "NONE" this combination will not be used on calculations. You can select

IND1-5: from indicators (See above),

EXT: value from externally imported indicator

Stock built-in values: close, open...

2)Operator

Selected Operator compares 1st Indicator with the 2nd one. You can select different operators such as

crossover, crossunder, cross,>,<,=....

3)2nd Indicator

This indicator will be compared with the 1st one via selected Operator. You can select

IND1-5: from indicators (See above),

VALUE: a float value defined in the combinations value parameter

EXT: value from externally imported indicator

Stock builtin values: close,open...

4)Value

When the 2nd indicator field is "VALUE", value area compares the entered value.

ex: 1st indicator="open", op=">", 2nd indicator="VALUE", value=3000.12 means is(close>3000.12)

In other conditions, it compares the previous values of the indicator.

ex: 1st indicator="open", op=">" 2nd indicator is "close" and value is 2 means is(open>close )

EXAMPLES:

indicator 1= "IND1", Operator=">", indicator 2= "IND2" => is(IND1>IND2)

indicator 1= "IND1", Operator=">", indicator 2= "VALUE", "0.1" => is(IND1>0.9)

indicator 1= "IND2", Operator="crossover", indicator 2= "IND1" => is(IND2 crossover IND1) : like a=ta.crossover(IND2, IND1)

indicator 1= "IND1", Operator="<", indicator 2= "close" => is(IND1>close)

indicator 1= "IND1", Operator="<", indicator 2= "EXT" => is(IND1>EXT) , EXT mean external imported indicator that define on settings section

indicator 1= "IND1", Operator="<", indicator 2= "IND1", Value="1" => is (IND1>IND1 )

b)JOIN COMBINATIONS

Each combination in Condition is compared with the next one via JOIN operator

The join operator can be selected as AND or OR.

Examples:

1st combination= is(IND1>0.9) true

2nd combination= is(IND2 crossover IND1) false

1st combination "AND" 2ndcombination" => false (is(IND1>0.9) AND is(IND2 crossover IND1))

1st combination "OR" 2nd combination" => true (is(IND1>0.9) OR is(IND2 crossover IND1))

STEP 3 NOTES:

When the 2nd indicator field is "VALUE", value area compares the entered value. In other conditions, it compares the previous values of the indicator.

In cases where "VALUE" is not selected, integer values must be entered in this field. (float should not be entered. ie 1, 2 should be entered)

!!!If the 1st indicator is "NONE" in the combination, that combination is cancelled.

Each combination returns true/false, allowing the selected value to be compared with another value

Example: EMA(21)>EMA(50) returns true under all conditions or (EMA(21) crossover EMA(50)) returns true when passed.

You can use , Value of 5 indicators (IND1-IND5) or (VALUE) that you have defined in combinations or import indicator (EXT) or stock values (close, open, high...) in your calculations.

combination Compares the 1st indicator with 2nd indicator via the operator.

STEP 4: CUSTOM INDICATORS ______________________________________________________________________________________________________

There is an area in the code for designing Custom Indicators.

Here you can design your own indicators and use them in the framework.

You can also create unlimited parameters for your indicators in the SETTINGS custom indicator field.

For now, only 3 Custom indicators have been defined.

Examples are entered in the code for custom indicators.

STEP 4 NOTES:

Including / updating custom to the code is explained in the source code

• LIMITATIONS:

!!! According to your tradingview subscription, it takes the last 5000, 10000.. bars. More bar options may cause problems such as not appearing in the calculations or errors.

• RAMBLINGS:

• NOTES [ /i]

This Script can be used as an indicator if the last strategy parts in the code are commented out and converted to the initial strategy study.

It was originally prepared for my use with my own strategy framework and has export functions accordingly.

When integrated to my own strategy framework it brings many more features over strategy definition of trades.

• TODO [ /i]

TODO: Add tooltips to the settings screen

TODO: Add double triple, Quatr factor for all indicators (convert any indicator to factor2-4 facotr. ex: EMA to DEMA, TEMA, QEMA...)

TODO: Add factorized Fibo avg range indicator (good for trend definition and entry exit points)

TODO: Add bands to the indicator and conditions

TODO: Add debug window for exporting indicator's parameters

TODO: Add isRising(value) isFalling(value), is...(value) .... to combinations (they can be used as custom indicator also

TODO: Reassess condition entry screen for user friendly GUI

TODO: Increase # conditions from 3 to 4

TODO: Reassess strategy entries, exit and close (should be improved)

TODO: Add Alerts, Condiional alerts for indicator (study) part

TODO: Create export function v3 for Pinecoders Indicator framework

• THANKS:

For Pine script format docs RicardoSantos .

For Pine script coding standards Pinecoders .

For moving average script used on library s RodrigoKazuma .

taLibrary "ta"

█ OVERVIEW

This library holds technical analysis functions calculating values for which no Pine built-in exists.

Look first. Then leap.

█ FUNCTIONS

cagr(entryTime, entryPrice, exitTime, exitPrice)

It calculates the "Compound Annual Growth Rate" between two points in time. The CAGR is a notional, annualized growth rate that assumes all profits are reinvested. It only takes into account the prices of the two end points — not drawdowns, so it does not calculate risk. It can be used as a yardstick to compare the performance of two instruments. Because it annualizes values, the function requires a minimum of one day between the two end points (annualizing returns over smaller periods of times doesn't produce very meaningful figures).

Parameters:

entryTime : The starting timestamp.

entryPrice : The starting point's price.

exitTime : The ending timestamp.

exitPrice : The ending point's price.

Returns: CAGR in % (50 is 50%). Returns `na` if there is not >=1D between `entryTime` and `exitTime`, or until the two time points have not been reached by the script.

█ v2, Mar. 8, 2022

Added functions `allTimeHigh()` and `allTimeLow()` to find the highest or lowest value of a source from the first historical bar to the current bar. These functions will not look ahead; they will only return new highs/lows on the bar where they occur.

allTimeHigh(src)

Tracks the highest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `high`.

Returns: (float) The highest value tracked.

allTimeLow(src)

Tracks the lowest value of `src` from the first historical bar to the current bar.

Parameters:

src : (series int/float) Series to track. Optional. The default is `low`.

Returns: (float) The lowest value tracked.

█ v3, Sept. 27, 2022

This version includes the following new functions:

aroon(length)

Calculates the values of the Aroon indicator.

Parameters:

length (simple int) : (simple int) Number of bars (length).

Returns: ( [float, float ]) A tuple of the Aroon-Up and Aroon-Down values.

coppock(source, longLength, shortLength, smoothLength)

Calculates the value of the Coppock Curve indicator.

Parameters:

source (float) : (series int/float) Series of values to process.

longLength (simple int) : (simple int) Number of bars for the fast ROC value (length).

shortLength (simple int) : (simple int) Number of bars for the slow ROC value (length).

smoothLength (simple int) : (simple int) Number of bars for the weigted moving average value (length).

Returns: (float) The oscillator value.

dema(source, length)

Calculates the value of the Double Exponential Moving Average (DEMA).

Parameters:

source (float) : (series int/float) Series of values to process.