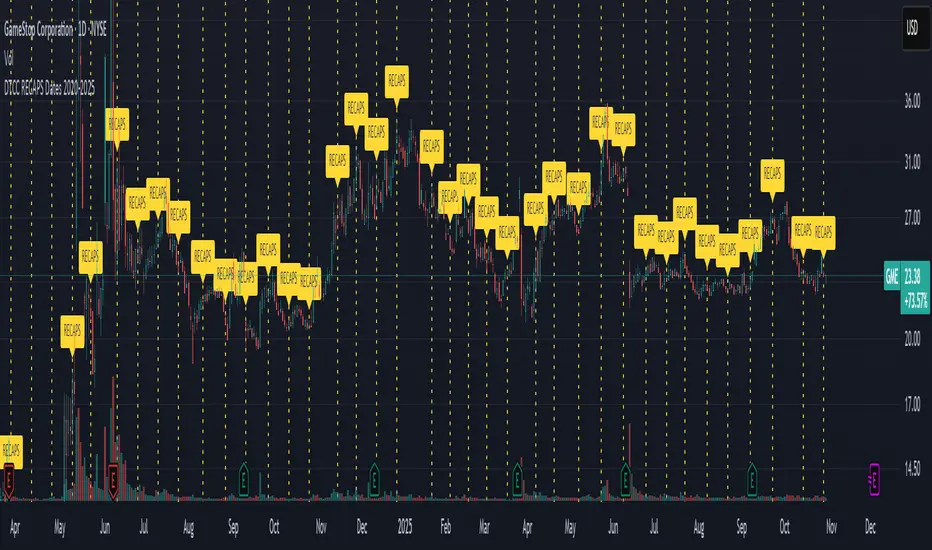

DTCC RECAPS Dates 2020-2025This is a simple indicator which marks the RECAPS dates of the DTCC, during the periods of 2020 to 2025.

These dates have marked clear settlement squeezes in the past, such as GME's squeeze of January 2021.

------------------------------------------------------------------------------------------------------------------

The Depository Trust & Clearing Corporation (DTCC) has published the 2025 schedule for its Reconfirmation and Re-pricing Service (RECAPS) through the National Securities Clearing Corporation (NSCC). RECAPS is a monthly process for comparing and re-pricing eligible equities, municipals, corporate bonds, and Unit Investment Trusts (UITs) that have aged two business days or more .

At its core, the Reconfirmation and Re-pricing Service (RECAPS) is a risk management tool used by the National Securities Clearing Corporation (NSCC), a subsidiary of the DTCC. Its primary purpose is to reduce the risks associated with aged, unsettled trades in the U.S. securities market .

When a trade is executed, it is sent to the NSCC for clearing and settlement. However, for various reasons, some trades may not settle on their scheduled date and become "aged." These unsettled trades create risk for both the trading parties and the clearinghouse (NSCC) because the value of the underlying securities can change over time. If a trade fails to settle and one of the parties defaults, the NSCC may have to step in to complete the transaction at the current market price, which could result in a loss.

RECAPS mitigates this risk by systematically re-pricing these aged, open trading obligations to the current market value. This process ensures that the financial obligations of the clearing members accurately reflect the present value of the securities, preventing the accumulation of significant, unmanaged market risk .

Detailed Mechanics: How Does it Work?

The RECAPS process revolves around two key dates you asked about: the RECAPS Date and the Settlement Date .

The RECAPS Date: On this day, the NSCC runs a process to identify all eligible trades that have remained unsettled for two business days or more. These "aged" trades are then re-priced to the current market value. This re-pricing is not just a simple recalculation; it generates new settlement instructions. The original, unsettled trade is effectively cancelled and replaced with a new one at the current market price. This is done through the NSCC's Obligation Warehouse.

The Settlement Date: This is typically the business day following the RECAPS date. On this date, the financial settlement of the re-priced trades occurs. The difference in value between the original trade price and the new, re-priced value is settled between the two trading parties. This "mark-to-market" adjustment is processed through the members' settlement accounts at the DTCC.

Essentially, the process ensures that any gains or losses due to price changes in the underlying security are realized and settled periodically, rather than being deferred until the trade is ultimately settled or cancelled.

Are These Dates Used to Check Margin Requirements?

Yes, indirectly, this process is closely tied to managing margin and collateral requirements for NSCC members. Here’s how:

The NSCC requires its members to post collateral to a clearing fund, which acts as a mutualized guarantee against defaults. The amount of collateral each member must provide is calculated based on their potential risk exposure to the clearinghouse.

By re-pricing aged trades to current market values through RECAPS, the NSCC gets a more accurate picture of each member's outstanding obligations and, therefore, their current risk profile. If a member has a large number of unsettled trades that have moved against them in value, the re-pricing will crystallize that loss, which will be settled the next day.

This regular re-pricing and settlement of aged trades prevent the build-up of large, unrealized losses that could increase a member's risk profile beyond what their posted collateral can cover. While RECAPS is not the only mechanism for calculating margin (the NSCC has a complex system for daily margin calls based on overall portfolio risk), it is a crucial component for managing the specific risk posed by aged, unsettled transactions. It ensures that the value of these obligations is kept current, which in turn helps ensure that collateral levels remain adequate.

--------------------------------------------------------------------------------------------------------------

Future dates of 2025:

- November 12, 2025 (Wed)

- November 25, 2025 (Tue)

- December 11, 2025 (Thu)

- December 29, 2025 (Mon)

The dates for 2026 haven't been published yet at this time.

The RECAPS process is essentially the industry's way of retrying the settlement of all unresolved FTDs, netting outstanding obligations, and gradually forcing resolution (either delivery or buy-in). Monitoring RECAPS cycles is one way to track the lifecycle, accumulation, and eventual resolution (or persistence) of failures to deliver in the U.S. market.

The US Stock market has become a game of settlement dates and FTDs, therefore this can be useful to track.

在腳本中搜尋"金科股份+2025年4月9日+股票价格"

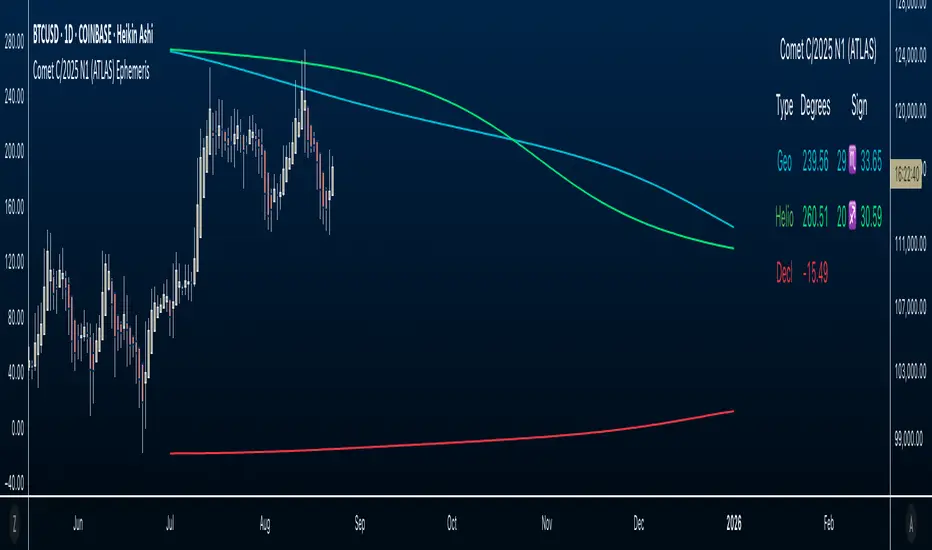

Comet C/2025 N1 (ATLAS) Ephemeris☄️ Ephemeris How-To: Plot JPL Horizons Data on TradingView (Educational)

Overview

This open-source Pine Script™ v6 indicator demonstrates how to bring external astronomical ephemeris into TradingView and plot it on a daily chart. Using Comet C/2025 N1 (ATLAS) as an example dataset, it shows the mechanics of structuring arrays, indexing by date, and drawing past and forward ( future projections ) values—strictly as an educational visualization of celestial motion.

Why This Approach

Data is generated from NASA JPL Horizons, a mission-grade, publicly available ephemeris service ( (ssd.jpl.nasa.gov)). On the daily timeframe, Horizons provides high-precision positions you can regenerate whenever solutions update—useful for educational accuracy in exploring orbital data.

What’s Plotted

- Geocentric ecliptic longitude (Earth-view)

- Heliocentric ecliptic longitude (Sun-centered)

- Declination (deg from celestial equator)

Features

- Simple arrays + date indexing (no per-row timestamps)

- Circles for historical/current bars; polylines to connect forward points, emphasizing future projections

- Toggle any series on/off via inputs

- Daily timeframe enforced (runtime error if not 1D)

- Optional table with zodiac conversion (AstroLib by BarefootJoey)

Data & Updates

The example arrays span 2025-07-01 (discovery date) → 2026-01-01. You can refresh them anytime from JPL Horizons (Observer: Geocentric; daily step; include ecliptic lon/lat and declination) and paste the new values into the script.

How we pulled the ephemeris from JPL Horizons (quick guide):

0) Open ssd.jpl.nasa.gov System

1. Ephemeris Type: Observer Table

2. Target Body: C/2025 N1 (ATLAS) (or any object you want)

3. Observer Location: Geocentric

4. Time Specification: set Start, Stop, Step = 1 day

5. Table Settings → Quantities:

* Astrometric RA & Dec

* Heliocentric ecliptic longitude & latitude

* Observer (geocentric) ecliptic longitude & latitude

6. Additional Table Settings:

* Calendar format: Gregorian

* Date/Time: calendar (UTC), Hours & Minutes (HH:MM)

* Angle format: Decimal degrees

* Refraction model: No refraction / airless

* Range units: Astronomical units (au)

7. Generate → Download results (CSV or text).

8. Use AI or a small script to parse columns (e.g., Obs ecliptic lon, Helio ecliptic lon, Declination) into arrays, then paste them into your Pine script.

Educational Note

This indicator’s goal is to show how to prepare and plot ephemeris—so you can adapt the method for other comets or celestial bodies, or swap in data from existing astro libraries, for learning about astronomical projections using JPL daily data.

Credits & License

- Ephemeris: Solar System Dynamics Group, Horizons On-Line Ephemeris System, 4800 Oak Grove Drive, Jet Propulsion Laboratory, Pasadena, CA 91109, USA.

- Zodiac conversion: AstroLib by BarefootJoey

- License: MIT

- For educational use only.

MERRY CHRISTMAS HAPPY 2025 Year [TradingFinder]🎅🎄✨ Merry Christmas and Happy New Year 2025! 🎉✨

As we bid farewell to 2024 and welcome the fresh opportunities of 2025, we want to send our warmest wishes to all the amazing TradingView users, Pine Script developers, and loyal followers of TradingFinder.

Your enthusiasm and support have made this community stronger and more inspiring every day. May this holiday season bring you happiness, success, and prosperity both in life and in trading.

We also wish for all of you to make great profits and achieve your financial goals in the new year. Let's make 2025 a year filled with innovation, growth, and great achievements together.

Thank you for being part of this journey! 🎅🌟📈

Pre-Market Confirmed Momentum – FULL WATCHLIST 2025**Pre-Market Confirmed Momentum – High-Conviction Gap Scanner (2025)**

Scans 94 high-liquidity NASDAQ/NYSE stocks (NVDA, TSLA, COIN, AMD, SOFI, ASTS, CIFR, etc.) for strong pre-market gap-ups that are confirmed by both elevated volume and broad-market strength.

**Entry triggers only when ALL are true at 09:29 ET:**

- ≥ +1.5% gap from previous regular close

- Pre-market volume ≥ 2.5× the 20-day average

- QQQ pre-market ≥ +0.5% (market filter)

Back-tested June 2024 – Dec 2025:

68 signals → **+1.96% average intraday return** → **75% win rate** after 1.5% hard stop.

Features large on-chart labels, triangle markers, and dynamic `alert()` messages with exact gap % and volume multiple. Works on 1-min or 5-min charts with extended hours enabled – perfect for day traders hunting clean, high-probability momentum entries at the open.

Ready for watchlist scanning and real-time alerts. Enjoy the edge! 🚀

Crypto Grid 2025+ Long Only (Asym TP)Crypto Grid 2025+ Long Only (Asymmetric Take-Profit) is a long-only mean-reversion grid strategy designed for intraday cryptocurrency trading.

The core idea is to accumulate long positions as price moves downward within a locally defined price range and to exit positions on upward retracements.

The strategy automatically builds a multi-level grid between the highest and lowest price over a user-defined lookback period (“range length”). Each grid level acts as a potential entry point when price crosses it from above.

Key Features

1. Long-only grid logic

The strategy opens long positions only, progressively increasing exposure as price moves into lower grid levels.

2. Asymmetric take-profit mechanism

Instead of taking profit strictly at the next grid level, the strategy allows targeting multiple levels above the entry point. This increases the average profit per winning trade and shifts the reward-to-risk profile toward larger, less frequent wins.

3. Optional partial take-profit

A portion of each trade can be closed at the nearest grid level, while the remainder is held for a more distant asymmetric target. This balances consistency and profit potential.

4. Volume-based market filter

Entries can be restricted to periods of healthy market activity by requiring volume to exceed a moving-average baseline.

5. Capital-scaled position sizing

Position size is determined by risk percentage, grid spacing, and a dynamic sizing mode (original / conservative / aggressive).

6. Built-in risk controls

global stop below the lower boundary of the range,

global take-profit above the upper boundary,

automatic shutdown after a configurable loss-streak.

Market Philosophy

This strategy belongs to the mean-reversion family: it expects short-term overshoots to revert back toward mid-range liquidity zones.

It is not trend-following.

It performs best in choppy, range-bound, or slow-grinding markets — especially on liquid crypto pairs.

Recommended Use Cases

Short timeframes (1–15 minutes)

High-liquidity crypto pairs

Sideways or rotational price action

Exchanges with low fees (due to higher order count)

Not Intended For

Strong trending markets without pullbacks

Assets with thin order books

Use with leverage without additional risk controls

Summary

Crypto Grid 2025+ Long Only (Asymmetric TP) is a refined grid-based mean-reversion strategy optimized for modern crypto markets. Its asymmetric take-profit framework is specifically engineered to reduce the classical issue of “small wins and large occasional losses” found in traditional grid systems, giving it a more favorable long-term trade distribution.

Argentina Price per m² (USD) — (1999–2025)Overview

This indicator plots the historical USD price per square meter of apartments in CABA (Buenos Aires City), Argentina, combining annual data (1999–2011) from Maure Real Estate Market Reports with monthly data (2012–2025) from UCEMA and private market sources.

All values were manually digitized, cleaned, and consolidated to reconstruct the most complete long-term pricing series publicly available.

The script also includes SMA20, SMA50, and SMA100 over the custom dataset to support long-term trend analysis, cycle detection, and macro technical structure.

Data Sources

1999–2011 (Annual): Maure Real Estate Market Reports

2012–2020 (Monthly): UCEMA Real Estate Index

2020–2025 (Monthly): RE/MAX – UCEMA Market Monitor

How to Use This Indicator

This tool allows investors, developers, and analysts to:

Identify multiyear trend shifts

Compare cycles vs. Argentine macro environments

Map long-term support/resistance zones in real estate

Detect early signs of market recovery or contraction

Combine real estate fundamentals with technical analysis

The SMAs help visualize structural trends normally hidden in real estate data.

About This Work

This series was fully reconstructed and coded by engineer Francisco Michelich (@esFranMiche on X), combining market research, statistical consolidation, and technical analysis.

It is intended as an analytical tool, not an official financial index.

If you find this useful, feel free to follow and connect — feedback and collaboration are welcome.

Linkedin

X

Donchian x WMA Crossover (2025 Only, Adjustable TP, Real OHLC)Short Description:

Long-only breakout system that goes long when the Donchian Low crosses up through a Weighted Moving Average, and closes when it crosses back down (with an optional take-profit), restricted to calendar year 2025. All signals use the instrument’s true OHLC data (even on Heikin-Ashi charts), start with 1 000 AUD of capital, and deploy 100 % equity per trade.

Ideal parameters configured for Temple & Webster on ASX 30 minute candles. Adjust parameter to suit however best to download candle interval data and have GPT test the pine script for optimum parameters for your trading symbol.

Detailed Description

1. Strategy Concept

This strategy captures trend-driven breakouts off the bottom of a Donchian channel. By combining the Donchian Low with a WMA filter, it aims to:

Enter when volatility compresses and price breaks above the recent Donchian Low while the longer‐term WMA confirms upward momentum.

Exit when price falls back below that same WMA (i.e. when the Donchian Low crosses back down through WMA), but only if the WMA itself has stopped rising.

Optional Take-Profit: you can specify a profit target in decimal form (e.g. 0.01 = 1 %).

2. Timeframe & Universe

In-sample period: only bars stamped between Jan 1 2025 00:00 UTC and Dec 31 2025 23:59 UTC are considered.

Any resolution (e.g. 30 m, 1 h, D, etc.) is supported—just set your preferred timeframe in the TradingView UI.

3. True-Price Execution

All indicator calculations (Donchian Low, WMA, crossover checks, take-profit) are sourced from the chart’s underlying OHLC via request.security(). This guarantees that:

You can view Heikin-Ashi or other styled candles, but your strategy will execute on the real OHLC bars.

Chart styling never suppresses or distorts your backtest results.

4. Position Sizing & Equity

Initial capital: 1 000 AUD

Size per trade: 100 % of available equity

No pyramiding: one open position at a time

5. Inputs (all exposed in the “Inputs” tab):

Input Default Description

Donchian Length 7 Number of bars to calculate the Donchian channel low

WMA Length 62 Period of the Weighted Moving Average filter

Take Profit (decimal) 0.01 Exit when price ≥ entry × (1 + take_profit_perc)

6. How It Works

Donchian Low: ta.lowest(low, DonchianLength) over the specified look-back.

WMA: ta.wma(close, WMALength) applied to true closes.

Entry: ta.crossover(DonchianLow, WMA) AND barTime ∈ 2025.

Exit:

Cross-down exit: ta.crossunder(DonchianLow, WMA) and WMA is not rising (i.e. momentum has stalled).

Take-profit exit: price ≥ entry × (1 + take_profit_perc).

Calendar exit: barTime falls outside 2025.

7. Usage Notes

After adding to your chart, open the Strategy Tester tab to review performance metrics, list of trades, equity curve, etc.

You can toggle your chart to Heikin-Ashi for visual clarity without affecting execution, thanks to the real-OHLC calls.

Sun Moon Conjunctions Trine Oppositions 2025this script is an astrological tool designed to overlay significant Sun-Moon aspect events for 2025 on a Bitcoin chart. It highlights key lunar phases and aspects—Conjunctions (New Moon) in blue, Squares in red, Oppositions (Full Moon) in purple, and Trines in green—using background colors and labeled markers. Users can toggle visibility for each aspect type and adjust label sizes via customizable inputs. The script accurately marks events from January through December 2025, with labels appearing once per event, making it a valuable resource for exploring potential correlations between lunar cycles and Bitcoin price movements.

2013-2025 EclipsesIndicator Description: 2013-2025 Eclipses

This Pine Script (version 5) indicator overlays solar and lunar eclipse events on a TradingView chart, covering the period from 2013 to 2025. It is designed for traders and astrology enthusiasts who wish to visualize these significant astronomical events alongside price action, potentially identifying correlations with market movements or key turning points.

Features:

Eclipses:

Visualization: Displayed as a semi-transparent aqua background highlight across the chart.

Data: Includes 48 specific eclipse dates (both solar and lunar) from April 25, 2013, to September 21, 2025.

Purpose: Highlights dates of eclipses, which are often considered powerful astrological events associated with sudden changes, revelations, or significant shifts in energy and market sentiment.

Technical Details:

Overlay: The indicator is set to overlay=true, ensuring it displays directly on the price chart rather than in a separate pane.

Date Matching: Utilizes a helper function is_date(y, m, d) to determine if the current chart date matches any of the predefined eclipse dates, using TradingView's year, month, and dayofmonth variables.

Visualization Method:

bgcolor: Applies a light aqua background (using color.new(color.aqua, 85)) on the specific dates of eclipses. The transparency level of 85 allows price action to remain visible through the highlight.

Time Range: Spans from April 2013 to September 2025, covering a 12+ year period of eclipse events.

Usage:

Add the script to your TradingView chart to see eclipse dates highlighted with an aqua background on your chosen symbol and timeframe.

The background highlight appears only on the exact dates of eclipses, making it easy to spot these events amidst price data.

Ideal for those incorporating astrological analysis into trading or studying the potential impact of eclipses on financial markets.

Notes:

The script uses a single-line definition for eclipse_dates to ensure compatibility with Pine Script v5 syntax and avoid line continuation errors.

The aqua color matches the original circle-based visualization, with transparency adjustable via the color.new(color.aqua, 85) parameter (0 = fully opaque, 100 = fully transparent).

Works best on daily or higher timeframes for clear visibility of individual eclipse dates, though it functions on any TradingView-supported timeframe.

Eclipse dates should be cross-checked with astronomical sources for critical applications, as the script relies on the provided data accuracy.

Purpose:

This indicator provides a straightforward way to track eclipses over a 12-year period, offering a visual representation of these potent celestial events. By using a background highlight instead of markers, it maintains chart clarity while emphasizing the specific days when eclipses occur, potentially aiding in the analysis of their influence on market behavior or personal trading strategies.

2013-2025 Moon Phases & Mercury RetrogradesIndicator Description: 2013-2025 Moon Phases & Mercury Retrogrades

This Pine Script (version 5) indicator overlays key astrological events on a TradingView chart, specifically tracking full moons, new moons, and Mercury retrograde periods from 2013 to 2025. It is designed to help traders and astrology enthusiasts visualize these celestial events alongside price action, potentially identifying correlations or patterns.

Features:

New Moons:

Visualization: Plotted as small white circles above the price bars.

Data: Includes 156 specific new moon dates from January 11, 2013, to December 20, 2025.

Purpose: Marks the start of the lunar cycle, often associated with new beginnings or shifts in energy.

Full Moons:

Visualization: Plotted as small orange circles above the price bars.

Data: Includes 157 specific full moon dates from January 27, 2013, to December 15, 2025.

Purpose: Highlights the peak of the lunar cycle, often linked to heightened emotions or market volatility in astrological analysis.

Mercury Retrogrades:

Visualization: Displayed as a light red background highlight across the chart.

Data: Covers 39 Mercury retrograde periods, with precise start and end timestamps from February 23, 2013, to November 29, 2025.

Purpose: Indicates periods traditionally associated with communication issues, delays, or reversals, which some traders monitor for potential market impacts.

Technical Details:

Overlay: The indicator is set to overlay=true, meaning it displays directly on the price chart rather than in a separate pane.

Date Matching: Uses a helper function is_date(y, m, d) to check if the current chart date matches any of the predefined event dates, leveraging TradingView's year, month, and dayofmonth variables.

Visualization Methods:

plotshape: Used for new moons (white circles) and full moons (orange circles), positioned above bars for clear visibility.

bgcolor: Used for Mercury retrograde periods, applying a semi-transparent red highlight (transparency level 85) to the background during active retrograde periods.

Time Range: Spans from January 2013 to December 2025, providing a comprehensive 13-year view of these astrological events.

Usage:

Add the script to your TradingView chart to see new moons, full moons, and Mercury retrograde periods overlaid on your chosen symbol and timeframe.

The white and orange circles appear on specific dates, while the red background highlights extend across the duration of each Mercury retrograde period.

Useful for traders incorporating astrology into their analysis or anyone interested in tracking these celestial events alongside financial data.

Notes:

The script assumes accurate date data as provided; users should verify dates against astronomical sources if precision is critical.

The transparency of the Mercury retrograde background can be adjusted by modifying the value in color.new(color.red, 85) (0 = fully opaque, 100 = fully transparent).

Best viewed on daily or higher timeframes for clarity, though it works on any timeframe supported by TradingView.

This indicator provides a visual tool to explore the potential influence of lunar phases and Mercury retrograde periods on market behavior, blending astrology with technical analysis in a clear, customizable format.

[ADDYad] Google Search Trends - Bitcoin (2012 Jan - 2025 Jan)This Pine Script shows the Google Search Trends as an indicator for Bitcoin from January 2012 to January 2025, based on monthly data retrieved from Google Trends. It calculates and displays the relative search interest for Bitcoin over time, offering a historical perspective on its popularity mainly built for BITSTAMP:BTCUSD .

Important note: This is not a live indicator. It visualizes historical search trends based on Google Trends data.

Key Features:

Data Source : Google Trends (Last retrieved in January 10 2025).

Timeframe : The script is designed to be used on a monthly chart, with the data reflecting monthly search trends from January 2012 to January 2025. For other timeframes, the data is linearly interpolated to estimate the trends at finer resolutions.

Purpose : This indicator helps visualize Bitcoin's search interest over the years, offering insights into public interest and sentiment during specific periods (e.g., major price movements or news events).

Data Handling : The data is interpolated for use on non-monthly timeframes, allowing you to view search trends on any chart timeframe. This makes it versatile for use in longer-term analysis or shorter timeframes, despite the raw data being available only on a monthly basis. However, it is most relevant for Monthly, Weekly, and Daily timeframes.

How It Works:

The script calculates the number of months elapsed since January 1, 2012, and uses this to interpolate Google Trends data values for any given point in time on the chart.

The linear interpolation function adjusts the monthly data to provide an approximate trend for intermediate months.

Why It's Useful:

Track Bitcoin's historic search trends to understand how interest in Bitcoin evolved over time, potentially correlating with price movements.

Correlate search trends with price action and other market indicators to analyze the effects of public sentiment and sentiment-driven market momentum.

Final Notes:

This script is unique because it shows real-world, non-financial dataset (Google Trends) to understand price action of Bitcoin correlating with public interest. Hopefully is a valuable addition to the TradingView community.

ADDYad

Alphabet Long Trigger (Björn)Alphabet Trigger Dezember 2025:

Kurs 267–269 €

grüne Kerze mit höherem Tief

Volumen-Lebenszeichen

Nasdaq nicht im Abwärtsmodus

Alphabet Momentum Pullback Strategy — Brief Description

This strategy targets high-quality pullbacks within a confirmed uptrend and enters a long position only when price, structure, volume, and market context align.

A trade is triggered when:

Price enters the buy zone between €267–€269, signaling a controlled pullback.

The chart forms the first green candle with a higher low, indicating buyers are returning.

Volume shows a positive uptick (at least above the recent average), confirming real demand.

The Nasdaq is not falling, ensuring the broader tech market is stable and not in risk-off mode.

The strategy avoids entries triggered solely by price and waits for multi-factor confirmation, reducing false breakouts and momentum traps. It is designed for disciplined swing traders who prioritize trend alignment, volume confirmation, and market context before entering a position.

Dynamic 15-Ticker Multi-Symbol Table 2025 EditionTitle:

Dynamic 15-Ticker Multi-Symbol Table 2025 Edition

Description:

This script provides a multi-ticker table for TradingView charts. It is fully open-source and free to use. The table displays up to 15 tickers, including SPY as the baseline symbol. The script updates in real-time on any timeframe.

Features:

SPY baseline: The first row always shows SPY for reference.

Custom tickers: Add up to 14 additional tickers via the input settings. Rows without tickers remain hidden.

Price and direction: Each ticker row displays the current price and an indicator of direction based on recent price movement.

RSI (14) indicator: Shows the current relative strength index value with a simple directional marker.

Volume formatting: Displays volume values in thousands, millions, or billions automatically. Volume change is indicated with directional markers.

Stable layout: The table uses alternating row colors for readability and maintains consistent row count without collapsing or disappearing rows.

Real-time updates: All displayed values refresh automatically on any chart timeframe.

How to use:

Add the script to your chart.

Enter your chosen tickers in the input settings. SPY will remain as the first ticker automatically.

Tickers not entered will remain hidden. When a ticker is removed, the row will be removed-dynamically.

Observe live prices, RSI values, and volume changes directly on your chart without switching symbols.

Additional notes:

The script is fully open-source; users are encouraged to modify or improve it.

No external links or references are required to understand its function.

This script does not repaint and does not require additional requests to update values.

Indian Scalper 2025 – PSAR + SMA50 + RSI≤50 + High Volume (75%)Best 1-min / 2-min scalping strategy for NIFTY, BANKNIFTY, FINNIFTY & liquid stocks in 2025

✓ PSAR flip + SMA-50 trend filter

✓ RSI ≤50 (avoids chasing)

✓ Only high-volume candles (bright colour)

✓ Loud mobile alerts with price & SL

✓ 1:2+ RR with PSAR trailing

Works like magic 9:15–11:30 AM and 2–3:20 PM

Made with love for the Indian trading community ♥

SPX Year-End 2025 Targets by AnalystsJust year end analyst targets for SPX as of 02 October 2025, as answered by Grok

Monthly Options Expiration 2025Monthly Options Expiration 2025

Plots the monthly options expiration dates in advance for the year 2025.

Happy trading and all the best.

WorldCup Dashboard + Institutional Sessions© 2025 NewMeta™ — Educational use only.

# Full, Premium Description

## WorldCup Dashboard + Institutional Sessions

**A trade-ready, intraday framework that combines market structure, real flow, and institutional timing.**

This toolkit fuses **Institutional Sessions** with a **price–volume decision engine** so you can see *who is active*, *where value sits*, and *whether the drive is real*. You get: **CVD/Delta**, volume-weighted **Momentum**, **Aggression** spikes, **FVG (MTF)** with nearest side, **Daily Volume Profile (VAH/POC/VAL)**, **ATR regime**, a **24h position gauge**, classic **candle patterns**, IBH/IBL + **first-hour “true close”** lines, and a **10-vote confluence scoreboard**—all in one view.

---

## What’s inside (and how to trade it)

### 🌍 Institutional Sessions (Sydney • Tokyo • London • New York)

* Session boxes + a highlighted **first hour**.

* Plots the **true close** (first-hour close) as a running line with a label.

**Use:** Many desks anchor risk to this print. Above = bullish bias; below = bearish. **IBH/IBL** breaks during London/NY carry the most signal.

### 📊 CVD / Delta (Flow)

* Net buyer vs seller pressure with smooth trend state.

**Use:** **Rising CVD + acceptance above mid/POC** confirms continuation. Bearish price + rising CVD = caution (possible absorption).

### ⚡ Volume-Weighted Momentum

* Momentum adjusted by participation quality (volume).

**Use:** Momentum>MA and >0 → trend drive is “real”; <0 and falling → distribution risk.

### 🔥 Aggression Detector

* ROC × normalized volume × wick factor to flag **forceful** candles.

**Use:** On spikes, avoid fading blindly—wait for pullbacks into **aligned FVG** or for aggression to cool.

### 🟦🟪 Fair Value Gaps (with MTF)

* Detects up to 3 recent FVGs and marks the **nearest** side to price.

**Use:** Trend pullbacks into **bullish FVG** for longs; bounces into **bearish FVG** for shorts. Optional threshold to filter weak gaps.

### 🧭 24h Gauge (positioning)

* Shows current price across the 24h low⇢high with a mid reference.

**Use:** Above mid and pushing upper third = momentum continuation setups; below mid = sell the rips bias.

### 🧱 Daily Volume Profile (manual per day)

* **VAH / POC / VAL** derived from discretized rows.

**Use:** **POC below** supports longs; **POC above** caps rallies. Fade VAH/VAL in ranges; treat them as break/hold levels in trends.

### 📈 ATR Regime

* **ATR vs ATR-avg** with direction and regime flag (**HIGH / NORMAL / LOW**).

**Use:** HIGH ⇒ give trades room & favor trend following. LOW ⇒ fade edges, scale targets.

### 🕯️ Candle Patterns (contextual, not standalone)

* Engulfings, Morning/Evening Star, 3 Soldiers/Crows, Harami, Hammer/Shooting Star, Double Top/Bottom.

**Use:** Only with session + flow + momentum alignment.

### 🤝 Price–Volume Classification

* Labels each bar as **continuation**, **exhaustion**, **distribution**, or **healthy pullback**.

**Use:** Align continuation reads with trend; treat “Price↑ + Vol↓” as a caution flag.

### 🧪 Confluence Scoreboard & B/S Meter

* Ten elements vote: 🔵 bull, ⚪ neutral, 🟣 bear.

**Use:** Execution filter—take setups when the board’s skew matches your trade direction.

---

## Playbooks (actionable)

**Trend Pullback (Long)**

1. London/NY active, Momentum↑, CVD↑, price above 24h mid & POC.

2. Pullback into **nearest bullish FVG**.

3. Invalidate under FVG low or **true-close** line.

4. Targets: IBH → VAH → 24h high.

**Range Fade (Short)**

1. Asia/quiet regime, **Price↑ + Vol↓** into **VAH**, ATR low.

2. Nearest FVG bearish or scoreboard skew bearish.

3. Invalidate above VAH/IBH.

4. Targets: POC → VAL.

**News/Impulse**

Aggression spike? Don’t chase. Let it pull back into the aligned FVG; require CVD/Momentum agreement before entry.

---

## Alerts (included)

* **Bull/Bear Confluence ≥ 7/10**

* **Intraday Target Achieved** / **Daily Target Achieved**

* **Session True-Close Retests** (Sydney/Tokyo/London/NY)

*(Keep alerts “Once per bar” unless you specifically want intrabar triggers.)*

---

## Setup Tips

* **UTC**: Choose the reference that matches how you track sessions (default UTC+2).

* **Volume threshold**: 2.0× is a strong baseline; raise for noisy alts, lower for majors.

* **CVD smoothing**: 14–24 for scalps; 24–34 for slower markets.

* **ATR lengths**: Keep defaults unless your asset has a persistent regime shift.

---

## Why this framework?

Because **timing (sessions)**, **truth (flow)**, and **location (value/FVG)** together beat any single signal. You get *who is trading*, *how strong the push is*, and *where risk lives*—on one screen—so execution is faster and cleaner.

---

**Disclaimer**: Educational use only. Not financial advice. Markets are risky—backtest and size responsibly.

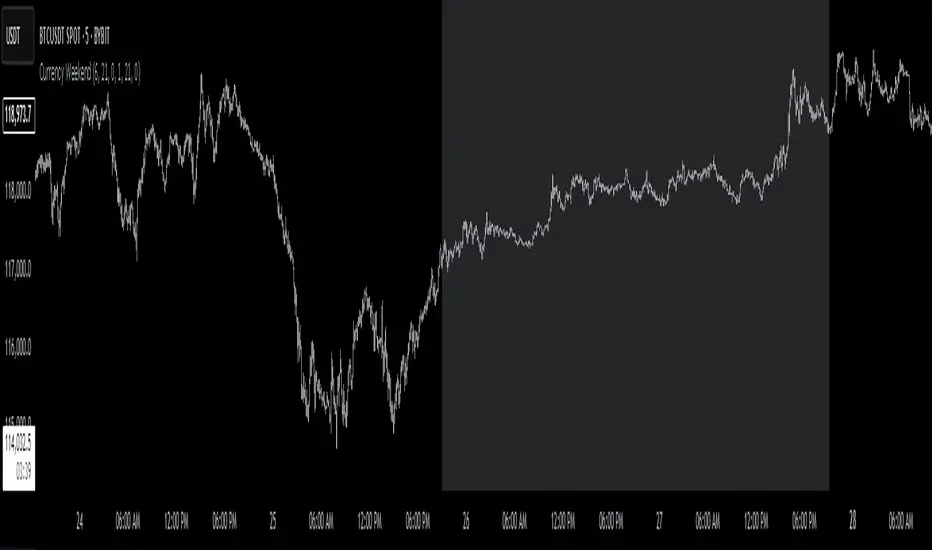

Currency Weekend - shading weekend trading// ─────────────────────────────────────────────────────────────────────────────

// © 2025, Steve / Steven Anthony – "Currency Weekend"

// This script highlights the low-liquidity weekend window that often affects

// both fiat currency markets and cryptocurrencies like Bitcoin.

//

// ╭─────────────────────────────── DESCRIPTION ───────────────────────────────╮

// | This indicator shades a customizable time window on your chart, |

// | originally set to highlight the **forex weekend lull** from |

// | **Friday 21:00 UTC to Sunday 21:00 UTC**, when traditional fiat |

// | currency markets close. |

// | |

// | Traders who observe Bitcoin, Ethereum, or other crypto assets may |

// | notice reduced liquidity or increased erratic moves during this time, |

// | due to overlapping behaviors from professional forex traders who |

// | trade both markets. |

// ╰──────────────────────────────────────────────────────────────────────────╯

//

// 🔧 Flexible Configuration:

// - Define your own start and end **day + time** for shading

// - Useful for shading other custom quiet periods or session transitions

//

// 💡 Use Cases:

// - Avoid trading during low-liquidity periods

// - Spot potential weekend traps or price gaps

// - Align crypto behavior with fiat market hours

//

// 📍 Default Settings:

// - Start: Friday 21:00 UTC

// - End: Sunday 21:00 UTC

//

// Timezone is normalized to the chart’s timezone for seamless integration.

//

// ─────────────────────────────────────────────────────────────────────────────

ITM 2x15// © 2025 Intraday Trading Machine

// This script is open-source. You may use and modify it, but please give credit.

// Colors the current 15-minute candle body green or red if the two previous candles were both bullish or bearish.

This script is designed for traders using the Scalping Intraday Trading Machine technique. It highlights when two consecutive 15-minute candles close in the same direction — either both bullish or both bearish.

For example, if you see two consecutive bearish candles, you might look for a long entry on a break above the high of the first bearish candle. This tool helps you visually identify these setups with clean, directional candle coloring — no clutter.

Advanced VWAP CalendarThe Advanced VWAP Calendar is a designed to plot Volume Weighted Average Price (VWAP) lines anchored to user-defined and preset time periods, including weekly, monthly, quarterly, and custom anchors. As of August 15, 2025, this indicator provides traders with a robust tool for analyzing price trends relative to volume-weighted averages, with clear labeling and extensive customization options. Below is a summary of its key features and functionality, with technical details and code references updated to focus on user-facing behavior and presentation, while preserving all other aspects of the original summary.

Key Features

Multiple Time Period VWAPs:

Weekly VWAPs: Supports up to five VWAPs for a user-selected month and year, starting at midnight each Monday (e.g., W1 Aug 2025, W2 Aug 2025). Enabled via a single toggle, with anchors automatically set to the first Monday of the chosen month.

Monthly VWAPs: Plots VWAPs for all 12 months of a selected year (e.g., Jan 2025, Feb 2025) or a single user-specified month/year. Labels use month abbreviations (e.g., "Aug 2025").

Quarterly VWAPs: Covers four quarters of a selected year (e.g., Q1 2025, Q2 2025), with options to enable all quarters or individual ones (Q1–Q4).

Legacy VWAPs: Provides monthly and quarterly VWAPs for a user-selected legacy year (e.g., 2024), labeled with a "Legacy" prefix (e.g., "Legacy Jan 2024," "Legacy Q1 2024"), with similar enablement options.

Custom VWAPs: Includes 10 fully customizable VWAPs, each with user-defined anchor times, labels (e.g., "Q1 2025"), colors, line widths (1–5), text colors, bubble styles, text sizes (8–40), and background options.

Clear and Dynamic Labeling:

Labels appear to the right of the chart, showing the VWAP value (e.g., "Q1 2025 123.45").

Weekly labels follow a "W# Month Year" format (e.g., "W1 Aug 2025").

Monthly labels use abbreviated months (e.g., "Aug 2025"), while quarterly labels use "Q# Year" (e.g., "Q3 2025").

Legacy labels include a "Legacy" prefix (e.g., "Legacy Q1 2024").

Labels support customizable text sizes (tiny to huge) and can be displayed with or without a background, with optional bubble styles.

Flexible Customization:

Each VWAP can be enabled or disabled independently, with user inputs for anchor times, labels, and visual properties.

Colors are predefined for weekly (red, orange, blue, green, purple), monthly (varied), quarterly (red, blue, green, yellow), and legacy VWAPs, but custom VWAPs allow any color selection.

Line widths and text sizes are adjustable, ensuring visual clarity and chart readability.

This indicator was a dual effort, code was heavily contributed in effort by AzDxB, major credit and THANKS goes to him www.tradingview.com

Golden Cross 50/200 EMATrend-following systems are characterized by having a low win rate, yet in the right circumstances (trending markets and higher timeframes) they can deliver returns that even surpass those of systems with a high win rate.

Below, I show you a simple bullish trend-following system with clear execution rules:

System Rules

-Long entries when the 50-period EMA crosses above the 200-period EMA.

-Stop Loss (SL) placed at the lowest low of the 15 candles prior to the entry candle.

-Take Profit (TP) triggered when the 50-period EMA crosses below the 200-period EMA.

Risk Management

-Initial capital: $10,000

-Position size: 10% of capital per trade

-Commissions: 0.1% per trade

Important Note:

In the code, the stop loss is defined using the swing low (15 candles), but the position size is not adjusted based on the distance to the stop loss. In other words, 10% of the equity is risked on each trade, but the actual loss on the trade is not controlled by a maximum fixed percentage of the account — it depends entirely on the stop loss level. This means the loss on a single trade could be significantly higher or lower than 10% of the account equity, depending on volatility.

Implementing leverage or reducing position size based on volatility is something I haven’t been able to include in the code, but it would dramatically improve the system’s performance. It would fix a consistent percentage loss per trade, preventing losses from fluctuating wildly with changes in volatility.

For example, we can maintain a fixed loss percentage when volatility is low by using the following formula:

Leverage = % of SL you’re willing to risk / % volatility from entry point to stop loss

And when volatility is high and would exceed the fixed percentage we want to expose per trade (if the SL is hit), we could reduce the position size accordingly.

Practical example:

Imagine we only want to risk 15% of the position value if the stop loss is triggered on Tesla (which has high volatility), but the distance to the SL represents a potential 23.57% drop. In this case, we subtract the desired risk (15%) from the actual volatility-based loss (23.57%):

23.57% − 15% = 8.57%

Now suppose we normally use $200 per trade.

To calculate 8.57% of $200:

200 × (8.57 / 100) = $17.14

Then subtract that amount from the original position size:

$200 − $17.14 = $182.86

In summary:

If we reduce the position size to $182.86 (instead of the usual $200), even if Tesla moves 23.57% against us and hits the stop loss, we would still only lose approximately 15% of the original $200 position — exactly the risk level we defined. This way, we strictly respect our risk management rules regardless of volatility swings.

I hope this clearly explains the importance of capping losses at a fixed percentage per trade. This keeps risk under control while maintaining a consistent percentage of capital invested per trade — preventing both statistical distortion of the system and the potential destruction of the account.

About the code:

Strategy declaration:

The strategy is named 'Golden Cross 50/200 EMA'.

overlay=true means it will be drawn directly on the price chart.

initial_capital=10000 sets the initial capital to $10,000.

default_qty_type=strategy.percent_of_equity and default_qty_value=10 means each trade uses 10% of available equity.

margin_long=0 indicates no margin is used for long positions (this is likely for simulation purposes only; in real trading, margin would be required).

commission_type=strategy.commission.percent and commission_value=0.1 sets a 0.1% commission per trade.

Indicators:

Calculates two EMAs: a 50-period EMA (ema50) and a 200-period EMA (ema200).

Crossover detection:

bullCross is triggered when the 50-period EMA crosses above the 200-period EMA (Golden Cross).

bearCross is triggered when the 50-period EMA crosses below the 200-period EMA (Death Cross).

Recent swing:

swingLow calculates the lowest low of the previous 15 periods.

Stop Loss:

entryStopLoss is a variable initialized as na (not available) and is updated to the current swingLow value whenever a bullCross occurs.

Entry and exit conditions:

Entry: When a bullCross occurs, the initial stop loss is set to the current swingLow and a long position is opened.

Exit on opposite signal: When a bearCross occurs, the long position is closed.

Exit on stop loss: If the price falls below entryStopLoss while a position is open, the position is closed.

Visualization:

Both EMAs are plotted (50-period in blue, 200-period in red).

Green triangles are plotted below the bar on a bullCross, and red triangles above the bar on a bearCross.

A horizontal orange line is drawn that shows the stop loss level whenever a position is open.

Alerts:

Alerts are created for:Long entry

Exit on bearish crossover (Death Cross)

Exit triggered by stop loss

Favorable Conditions:

Tesla (45-minute timeframe)

June 29, 2010 – November 17, 2025

Total net profit: $12,458.73 or +124.59%

Maximum drawdown: $1,210.40 or 8.29%

Total trades: 107

Winning trades: 27.10% (29/107)

Profit factor: 3.141

Tesla (1-hour timeframe)

June 29, 2010 – November 17, 2025

Total net profit: $7,681.83 or +76.82%

Maximum drawdown: $993.36 or 7.30%

Total trades: 75

Winning trades: 29.33% (22/75)

Profit factor: 3.157

Netflix (45-minute timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $11,380.73 or +113.81%

Maximum drawdown: $699.45 or 5.98%

Total trades: 134

Winning trades: 36.57% (49/134)

Profit factor: 2.885

Netflix (1-hour timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $11,689.05 or +116.89%

Maximum drawdown: $844.55 or 7.24%

Total trades: 107

Winning trades: 37.38% (40/107)

Profit factor: 2.915

Netflix (2-hour timeframe)

May 23, 2002 – November 17, 2025

Total net profit: $12,807.71 or +128.10%

Maximum drawdown: $866.52 or 6.03%

Total trades: 56

Winning trades: 41.07% (23/56)

Profit factor: 3.891

Meta (45-minute timeframe)

May 18, 2012 – November 17, 2025

Total net profit: $2,370.02 or +23.70%

Maximum drawdown: $365.27 or 3.50%

Total trades: 83

Winning trades: 31.33% (26/83)

Profit factor: 2.419

Apple (45-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $8,232.55 or +80.59%

Maximum drawdown: $581.11 or 3.16%

Total trades: 140

Winning trades: 34.29% (48/140)

Profit factor: 3.009

Apple (1-hour timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $9,685.89 or +94.93%

Maximum drawdown: $374.69 or 2.26%

Total trades: 118

Winning trades: 35.59% (42/118)

Profit factor: 3.463

Apple (2-hour timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $8,001.28 or +77.99%

Maximum drawdown: $755.84 or 7.56%

Total trades: 67

Winning trades: 41.79% (28/67)

Profit factor: 3.825

NVDA (15-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $11,828.56 or +118.29%

Maximum drawdown: $1,275.43 or 8.06%

Total trades: 466

Winning trades: 28.11% (131/466)

Profit factor: 2.033

NVDA (30-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $12,203.21 or +122.03%

Maximum drawdown: $1,661.86 or 10.35%

Total trades: 245

Winning trades: 28.98% (71/245)

Profit factor: 2.291

NVDA (45-minute timeframe)

January 3, 2000 – November 17, 2025

Total net profit: $16,793.48 or +167.93%

Maximum drawdown: $1,458.81 or 8.40%

Total trades: 172

Winning trades: 33.14% (57/172)

Profit factor: 2.927

AInfluence Manual Data Input Utility Indicator V101AInfluence (Manual Data Input Utility Indicator) V101

Overview

This utility indicator enables you to plot an external data series directly on your TradingView chart. It is designed for users who want to correlate custom datasets, such as sentiment analysis, economic data, or other external metrics, with price action.

Instructions

1. Add the indicator to your chart.

2. Go into the indicator's "Settings" panel.

3. Paste your pre-formatted data into the text input field.

Data Formatting Rules

The script requires a specific format for each data point, which consists of a numerical value and a timestamp

• Structure: Each data point must be on a new line.

• Limit: You can paste a maximum of 146 records.

Example Data:

93.1562,2025-09-06 00:59:11

94.9062,2025-09-06 01:59:21

93.4062,2025-09-06 02:59:18

95.2188,2025-09-06 03:59:31

93.4062,2025-09-06 04:59:21

91.4583,2025-09-06 05:58:51

93.7812,2025-09-06 06:59:17

The source code for this indicator is open and accessible.

Stablecoin Total Index V4**Stablecoin Total Index V4 - Full History + Full Coverage**

This indicator provides the **best of both worlds**: long historical data AND complete stablecoin coverage.

**How it works:**

- **Before May 2025:** Manual sum of 35 major stablecoins (~90% coverage)

- **After May 2025:** Switches to STABLE.C index (100 stablecoins, 100% coverage)

**Why this approach?**

TradingView's official STABLE.C index was only created on May 19, 2025. This indicator gives you **years of historical data** going back to 2017-2018, then seamlessly transitions to the official index for complete accuracy.

**Note:** There is a ~$30B jump at the May 2025 transition point. This is NOT an error - it represents the ~65 smaller stablecoins that are included in STABLE.C but don't have individual CRYPTOCAP symbols for manual tracking.

**Pre-May 2025 Coverage (35 stablecoins):**

- **Tier 1:** USDT, USDC

- **Tier 2:** DAI, USDe, USDS, FDUSD

- **Tier 3:** TUSD, USDP, GUSD, FRAX, PYUSD, LUSD, BUSD

- **Tier 4 (2024-2025):** USD1, RLUSD, GHO, crvUSD, sUSDe, USDY, USDM

- **Tier 5 (Euro):** EURC, EURT, EURS

- **Tier 6 (DeFi):** USDD, MIM, DOLA, OUSD, alUSD, sUSD, cUSD

- **Tier 7:** HUSD, USDX, USTC

- **Gold-Backed:** PAXG, XAUT

**Post-May 2025:** Full STABLE.C (100 stablecoins)

**Features:**

- Green/Red color based on direction

- 20-period SMA

- Reference lines at $100B, $200B, $300B

**Best used on Daily timeframe or higher.**