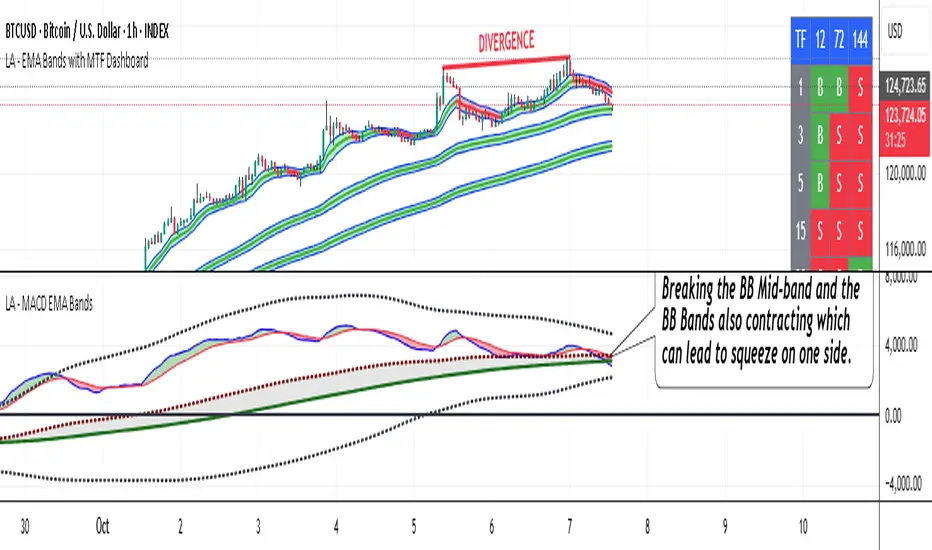

LA - MACD EMA BandsOverview of the "LA - MACD EMA Bands" Indicator

For Better view, use this indicator along with "LA - EMA Bands with MTF Dashboard"

The "LA - MACD EMA Bands" is a custom technical indicator written in Pine Script v6 for TradingView. It builds on the traditional Moving Average Convergence Divergence (MACD) oscillator by incorporating additional smoothing via Exponential Moving Averages (EMAs) and Bollinger Bands (BB) applied directly to the MACD line. This creates a multi-layered momentum and volatility tool displayed in a separate pane below the price chart (not overlaid on the price itself).

The indicator allows for customization, such as selecting a different timeframe (for multi-timeframe analysis) and adjusting period lengths. It fetches data from the specified timeframe using request.security with lookahead enabled to avoid repainting issues. The core idea is to provide insights into momentum trends, crossovers, and volatility expansions/contractions in the MACD's behavior, making it suitable for identifying potential trend reversals, continuations, or ranging markets.

Unlike a standard MACD, which focuses primarily on momentum via a single line, signal line, and histogram, this version emphasizes longer-term smoothing and volatility boundaries. It uses visual fills between lines to highlight bullish/bearish conditions, aiding quick interpretation. Below, I'll break down each component, its calculation, visual representation, and practical uses.

Detailed Breakdown of Each Component and Its Uses

MACD Line (Blue Line, Labeled 'MACD Line')

Calculation: This is the core MACD value, computed as the difference between a fast EMA (default length 12) and a slow EMA (default length 144) of the input source (default: close price). The EMAs are calculated on data from the selected timeframe.

Visuals: Plotted as a solid blue line.

Uses:

Measures momentum: When above zero, it indicates bullish momentum (prices rising faster in the short term); below zero, bearish momentum.

Trend identification: Rising MACD suggests strengthening uptrends; falling suggests downtrends.

Divergence spotting: Compare with price action—e.g., if price makes higher highs but MACD makes lower highs, it signals potential bearish reversal (and vice versa for bullish divergence).

In trading: Often used for entry/exit signals when crossing the zero line or other lines in the indicator.

MACD EMA (Red Line, Labeled 'MACD EMA')

Calculation: A 12-period EMA applied to the MACD Line itself.

Visuals: Plotted as a solid red line.

Uses:

Acts as a signal line for the MACD, smoothing out short-term noise.

Crossover signals: When the MACD Line crosses above the MACD EMA, it can signal a bullish buy opportunity; crossing below suggests a bearish sell.

Trend confirmation: Helps filter false signals in choppy markets by requiring confirmation from this slower-moving average.

In trading: Useful for momentum-based strategies, like entering trades on crossovers in alignment with the overall trend.

Fill Between MACD Line and MACD EMA (Green/Red Shaded Area, Titled 'MACD Fill')

Calculation: The area between the MACD Line and MACD EMA is filled with color based on their relative positions.

Color Logic: Green (with 57% transparency) if MACD Line > MACD EMA (bullish); red if MACD Line < MACD EMA (bearish).

Visuals: Semi-transparent fill for easy visibility without overwhelming the lines.

Uses:

Quick visual cue for momentum shifts: Green areas highlight bullish phases; red for bearish.

Enhances readability: Makes crossovers more apparent at a glance, especially in fast-moving markets.

In trading: Can be used to time entries/exits or as a filter (e.g., only take long trades in green zones).

Bollinger Bands on MACD (BB Upper: Black Dotted, BB Basis: Maroon Dotted, BB Lower: Black Dotted)

Calculation: Bollinger Bands applied to the MACD Line.

BB Basis: 144-period EMA of the MACD Line.

BB Standard Deviation: 144-period stdev of the MACD Line.

BB Upper: BB Basis + (2.0 * BB Stdev)

BB Lower: BB Basis - (2.0 * BB Stdev)

Visuals: Upper and lower bands as black dotted lines; basis as maroon dotted

Uses:

Volatility measurement: Bands expand during high momentum volatility (strong trends) and contract during low volatility (ranging or consolidation).

Mean reversion: When MACD Line touches or exceeds the upper band, it may signal overbought conditions (potential sell); lower band for oversold (potential buy).

Squeeze detection: Narrow bands (squeeze) often precede big moves—watch for breakouts.

In trading: Combines momentum with volatility; e.g., a MACD Line breakout above the upper band could confirm a strong uptrend.

BB Basis EMA (Green Line, Labeled 'BB Basis EMA')

Calculation: A 72-period EMA applied to the BB Basis (which is already a 144-period EMA of the MACD Line).

Visuals: Solid green line.

Uses:

Further smoothing: Provides a longer-term view of the MACD's average behavior, reducing noise from the BB Basis.

Trend direction: Acts as a baseline for the BB system—above it suggests bullish bias in momentum volatility; below, bearish.

Crossover with BB Basis: Can signal shifts in volatility trends (e.g., BB Basis crossing above BB Basis EMA indicates increasing bullish volatility).

In trading: Useful for confirming longer-term trends or as a filter for BB-based signals.

Fill Between BB Basis and BB Basis EMA (Gray Shaded Area, Titled 'BB Basis Fill')

Calculation: The area between BB Basis and BB Basis EMA is filled.

Color Logic: Currently set to a constant semi-transparent gray regardless of position.

Visuals: Semi-transparent gray fill.

Uses:

Highlights divergence: Shows when the shorter-term BB Basis deviates from its longer-term EMA, indicating potential volatility shifts.

Visual aid for crossovers: Makes it easier to spot when BB Basis crosses its EMA.

In trading: Could be used to identify overextensions in volatility (e.g., wide gray areas might signal impending mean reversion).

Zero Line (Black Horizontal Line)

Calculation: A simple horizontal line at y=0.

Visuals: Solid black line.

Uses:

Reference point: Divides bullish (above) from bearish (below) territory for all MACD-related lines.

In trading: Crossovers of the zero line by the MACD Line or BB Basis can signal major trend changes.

How It Differs from a Normal MACD

A standard MACD (e.g., the built-in TradingView MACD with defaults 12/26/9) consists of:

MACD Line: EMA(12) - EMA(26).

Signal Line: EMA(MACD Line, 9).

Histogram: MACD Line - Signal Line (bars showing convergence/divergence).

Key differences in "LA - MACD EMA Bands":

Periods: Uses a much longer slow EMA (144 vs. 26), making it more sensitive to long-term trends but less reactive to short-term price action. The MACD EMA is 12 periods (vs. 9), further emphasizing smoothing.

No Histogram: Replaces the histogram with fills and bands for visual emphasis on crossovers and volatility.

Added Bollinger Bands: Applies BB directly to the MACD Line (with a long 144-period basis), introducing volatility analysis absent in standard MACD. This helps detect "squeezes" or expansions in momentum.

Additional EMA Layer: The BB Basis EMA (72-period) adds a secondary smoothing level to the BB system, providing a hierarchical view of momentum (short-term MACD → mid-term BB → long-term EMA).

Multi-Timeframe Support: Built-in option for higher timeframes, unlike basic MACD.

Focus: Standard MACD is purely momentum-focused; this version integrates volatility (via BB) and multi-layer smoothing, making it better for trend-following in volatile markets but potentially overwhelming for beginners.

Overall, this indicator transforms the MACD from a simple oscillator into a comprehensive momentum-volatility hybrid, reducing false signals in trending markets but introducing lag.

Overall Pros and Cons

Pros:

Enhanced Visualization: Fills and bands make trends, crossovers, and volatility easier to spot without needing multiple indicators.

Reduced Noise: Longer periods (144, 72) smooth out whipsaws, ideal for swing or position trading in trending assets like stocks or forex.

Volatility Integration: BB adds a dimension not in standard MACD, helping identify breakouts or consolidations.

Customizable: Inputs for timeframes and lengths allow adaptation to different assets/timeframes.

Multi-Layered Insights: Combines short-term signals (MACD crossovers) with long-term confirmation (BB EMA), improving signal reliability.

Cons:

Lagging Nature: Long periods (e.g., 144) delay signals, missing early entries in fast markets or leading to late exits.

Complexity: Multiple lines and fills can clutter the pane, requiring experience to interpret; beginners might misread it.

Potential Overfitting: Custom periods (12/144/12/144/72) may work well on historical data but underperform in live trading without backtesting.

No Built-in Alerts/Signals: Relies on visual interpretation; users must manually set alerts for crossovers.

Resource Intensive: On lower timeframes or with lookahead, it might slow chart loading on Trading View.

This indicator shines in strategies combining momentum and volatility, like trend-following with BB squeezes, but test it on your assets (e.g., via backtesting) to ensure it fits your style.

For Better view, use this indicator along with "LA - EMA Bands with MTF Dashboard"

在腳本中搜尋"12月4号是什么星座"

Swing Guardrail — 30-sec Midterm Check (EBITDA Margin & EV/EBITDWhat it does

Before a short-term swing entry, this indicator right-sizes positions by a quick midterm (3–12m) durability screen using two fundamentals:

EBITDA Margin (TTM) → earning power / operational resilience

EV/EBITDA (TTM) → price tag vs earning capacity (payback feel)

A high-contrast table (top-right) shows both metrics and a verdict:

PASS — both meet thresholds → normal size

HALF — only one meets → reduce size

FAIL — neither meets → avoid

Why check “midterm” for a short-term trade?

Short swings still face earnings/news gaps, failed breakouts, and regime shifts. Names with weak margins or stretched valuation tend to break faster and deeper. A 30-sec durability check helps you:

Filter fragile setups (avoid expensive + weakening names)

Stabilize drawdowns (size down when quality/price don’t align)

Keep timing unchanged while improving risk-adjusted returns

Inputs (defaults)

Min EBITDA Margin % (TTM): 8%

Max EV/EBITDA (TTM): 12

Dark chart? High-contrast colors

How to use with a swing system

Get your entry from price/volume (e.g., Ichimoku cloud break, Kijun reclaim, Tenkan>Kijun; or your A/B/C rules).

Run this check only to set size (not timing).

Optional alerts: Once per bar close for PASS / HALF / FAIL.

Size mapping & event guard

PASS → 100% of your planned size

HALF → ~50% size / tighter stops

FAIL → watchlist only

If earnings < ~10 JP business days, drop one tier; ≤3 days → avoid.

Sector guides (tweak as needed)

Software/Internet: Margin ≥ 15%, EV/EBITDA ≤ 18

Industrials/Consumer: Margin ≥ 8%, EV/EBITDA ≤ 12

Retail: Margin ≥ 5–7%, EV/EBITDA ≤ 10–12

Edge cases / substitutions

Banks/Insurers/REITs or net-cash/negative EBITDA: EV/EBITDA may mislead → consider Net Debt/EBITDA or sector metrics (CET1/LTV/DSCR).

Sparse data / fresh listings: numbers may be NA until updates.

Notes & limitations

Data via request.financial() (TTM/most-recent). Some tickers/regions can show NA until fundamentals refresh.

This is a risk-screen / sizing tool, not a buy/sell signal.

Disclaimer

Educational use only. Not investment advice.

日本語

タイトル

スイング用ガードレール―中期“壊れにくさ”30秒チェック(EBITDAマージン & EV/EBITDA, TTM)

概要

短期スイングのエントリー前に、中期(3〜12か月)の耐久性を2指標で素早く確認し、ポジションサイズを決めるためのツールです。

EBITDAマージン(TTM):事業の稼ぐ力・体力

EV/EBITDA(TTM):その体力に対する“値札”(回収年数の感覚)

右上の高コントラスト表に数値と判定を表示:

PASS:両方クリア → 通常サイズ

HALF:片方のみ → サイズ半分

FAIL:両方NG → 見送り

なぜ短期でも“中期”を確認?

短期でも決算・ニュースのギャップ、ブレイク失敗、地合い転換は起きます。マージンが弱い/割高すぎる銘柄は崩れやすく、戻りも鈍い傾向。30秒の耐久性チェックで

脆いセットアップを回避

ドローダウンを平準化(サイズで吸収)

タイミングは変えずに、リスク調整後リターンの改善を狙えます。

入力(既定)

最低EBITDAマージン:8%

最大EV/EBITDA:12

黒背景向け:高コントラスト表示

使い方(スイング手法と併用)

まずは価格シグナル(一目の雲上抜け/基準線回復/転換線>基準線、またはA/B/Cルール)。

本インジの判定でサイズのみ決定(エントリーのタイミングは出しません)。

任意でバー確定アラート(PASS/HALF/FAIL)を設定。

サイズ目安 & イベント抑制

PASS:計画サイズ100%

HALF:約50%(ストップもタイトに)

FAIL:見送り

決算まで≦10営業日なら1段階サイズダウン、≦3営業日は原則見送り。

セクター目安(調整推奨)

ソフト/ネット:マージン 15%以上、EV/EBITDA 18以下

工業/一般消費:マージン 8%以上、EV/EBITDA 12以下

小売:マージン 5〜7%以上、EV/EBITDA 10〜12以下

例外・代替

銀行・保険・REIT/ネットキャッシュ・EBITDAマイナス:EV/EBITDAは適さない場合 → Net Debt/EBITDAやCET1/LTV/DSCR等で補助。

新規上場・データ薄:更新までNAのことあり。

注意

データは request.financial() を使用。更新前はNAの可能性。

本ツールはリスク確認/サイズ調整用で、売買シグナルではありません。

免責

情報提供のみ。投資判断は自己責任で。

FUMO 200 MagnetWhat it does

FUMO Magnet measures how far price has stretched away from its long-term “magnet” — a blended EMA/SMA moving average (200 by default).

It plots a logarithmic deviation (optionally normalized) as an oscillator around zero.

Above 0** → price is above the magnet (stretched up)

Below 0** → price is below the magnet (stretched down)

Guide levels** highlight potential overbought/oversold zones

---

Why log deviation?

Log returns make extremes comparable across cycles and compress exponential trends — especially useful for BTC and other crypto assets.

Normalization modes further adjust the scale, keeping the oscillator readable on any chart.

---

Inputs

**Base**

* Source (default: Close)

* Base Length (default: 200 EMA/SMA)

* EMA vs SMA weight (%) — 0% = pure SMA, 100% = pure EMA, 50% = blended

* EMA smoothing of deviation — acts as a noise filter

**Normalization**

* None (Log Deviation) — raw log stretch in % terms

* Z-score — deviation in standard deviations (σ)

* Robust Z (MAD) — deviation vs median absolute deviation, resistant to outliers

* Tanh squash — smooth nonlinear squash of extremes for compact scale

* Normalization window (for Z / MAD)

* Tanh scale (lower = stronger squash)

* Clamp after normalization — hard cap at ±X

**Levels**

* Guide levels (Upper / Lower) — visual thresholds (default ±12)

* Zero line toggle

---

### How to read it

* **Trend bias**: sustained time above 0 = uptrend, below 0 = downtrend

* **Stretch / mean reversion**: the farther from 0, the higher the reversion risk

* **Cross-checks**: combine with structure (HH/HL, LH/LL), volume, or momentum (RSI, MACD)

---

### Recommended settings by timeframe

**Long-term (1D / 1W)**

* Normalization: None (Log Deviation)

* Base Length: 200

* EMA vs SMA weight: 50% (adjust 35–65% for faster/slower magnet)

* Deviation smoothing: 20 (10–30 range)

* Guide levels: ±12 to ±20

* Use case: cycle extremes, portfolio rebalancing, trim/add logic

**Swing (4H – 1D)**

* Normalization: Z-score

* Window: 200 (100–250)

* Smoothing: 14–20

* Guide levels: ±2σ to ±3σ

* Use case: stretched conditions across regimes; ±3σ is rare, often mean-reverts

**Intraday / Active swing (1H – 4H)**

* Normalization: Robust Z (MAD)

* Window: 200 (150 for faster response)

* Smoothing: 10–16

* Guide levels: ±3 to ±4 (robust units)

* Use case: handles spikes better than σ, fewer false overbought/oversold signals

**Scalping / Universal readability (15m – 1H)**

* Normalization: Tanh squash

* Tanh scale: 6–10 (start with 8)

* Smoothing: 8–12

* Guide levels: ±8 to ±12

* Use case: compact panel across assets and timeframes; not % or σ, but visually consistent

---

### Optional

* Clamp: enable ±20 (or ±25) for strict bounded range (useful for public charts)

---

### Quick setups

**BTC Daily (“cycle view”)**

* Normalization: None

* Blend: 50%

* Smooth: 20

* Levels: ±12–15

**BTC 4H (“swing”)**

* Normalization: Z-score

* Window: 200

* Smooth: 16

* Levels: ±2.5σ to ±3σ

**Alts 1H (“volatile”)**

* Normalization: Robust Z (MAD)

* Window: 200

* Smooth: 12

* Levels: ±3.5 to ±4.5

**Mixed assets 15m (“compact panel”)**

* Normalization: Tanh squash

* Scale: 8

* Smooth: 10

* Levels: ±8–12

* Clamp: ±20

Meta-LR ForecastThis indicator builds a forward-looking projection from the current bar by combining twelve time-compressed “mini forecasts.” Each forecast is a linear-regression-based outlook whose contribution is adaptively scaled by trend strength (via ADX) and normalized to each timeframe’s own volatility (via that timeframe’s ATR). The result is a 12-segment polyline that starts at the current price and extends one bar at a time into the future (1× through 12× the chart’s timeframe). Alongside the plotted path, the script computes two summary measures:

* Per-TF Bias% — a directional efficiency × R² score for each micro-forecast, expressed as a percent.

* Meta Bias% — the same score, but applied to the final, accumulated 12-step path. It summarizes how coherent and directional the combined projection is.

This tool is an indicator, not a strategy. It does not place orders. Nothing here is trade advice; it is a visual, quantitative framework to help you assess directional bias and trend context across a ladder of timeframe multiples.

The core engine fits a simple least-squares line on a normalized price series for each small forecast horizon and extrapolates one bar forward. That “trend” forecast is paired with its mirror, an “anti-trend” forecast, constructed around the current normalized price. The model then blends between these two wings according to current trend strength as measured by ADX.

ADX is transformed into a weight (w) in using an adaptive band centered on the rolling mean (μ) with width derived from the standard deviation (σ) of ADX over a configurable lookback. When ADX is deeply below the lower band, the weight approaches -1, favoring anti-trend behavior. Inside the flat band, the weight is near zero, producing neutral behavior. Clearly above the upper band, the weight approaches +1, favoring a trend-following stance. The transitions between these regions are linear so the regime shift is smooth rather than abrupt.

You can shape how quickly the model commits to either wing using two exponents. One exponent controls how aggressively positive weights lean into the trend forecast; the other controls how aggressively negative weights lean into the anti-trend forecast. Raising these exponents makes the response more gradual; lowering them makes the shift more decisive. An optional switch can force full anti-trend behavior when ADX registers a deep-low condition far below the lower tail, if you prefer a categorical stance in very flat markets.

A key design choice is volatility normalization. Every micro-forecast is computed in ATR units of its own timeframe. The script fetches that timeframe’s ATR inside each security call and converts normalized outputs back to price with that exact ATR. This avoids scaling higher-timeframe effects by the chart ATR or by square-root time approximations. Using “ATR-true” for each timeframe keeps the cross-timeframe accumulation consistent and dimensionally correct.

Bias% is defined as directional efficiency multiplied by R², expressed as a percent. Directional efficiency captures how much net progress occurred relative to the total path length; R² captures how well the path aligns with a straight line. If price meanders without net progress, efficiency drops; if the variation is well-explained by a line, R² rises. Multiplying the two penalizes choppy, low-signal paths and rewards sustained, coherent motion.

The forward path is built by converting each per-timeframe Bias% into a small ATR-sized delta, then cumulatively adding those deltas to form a 12-step projection. This produces a polyline anchored at the current close and stepping forward one bar per timeframe multiple. Segment color flips by slope, allowing a quick read of the path’s direction and inflection.

Inputs you can tune include:

* Max Regression Length. Upper bound for each micro-forecast’s regression window. Larger values smooth the trend estimate at the cost of responsiveness; smaller values react faster but can add noise.

* Price Source. The price series analyzed (for example, close or typical price).

* ADX Length. Period used for the DMI/ADX calculation.

* ATR Length (normalization). Window used for ATR; this is applied per timeframe inside each security call.

* Band Lookback (for μ, σ). Lookback used to compute the adaptive ADX band statistics. Larger values stabilize the band; smaller values react more quickly.

* Flat half-width (σ). Width of the neutral band on both sides of μ. Wider flats spend more time neutral; narrower flats switch regimes more readily.

* Tail width beyond flat (σ). Distance from the flat band edge to the extreme trend/anti-trend zone. Larger tails create a longer ramp; smaller tails reach extremes sooner.

* Polyline Width. Visual thickness of the plotted segments.

* Negative Wing Aggression (anti-trend). Exponent shaping for negative weights; higher values soften the tilt into mean reversion.

* Positive Wing Aggression (trend). Exponent shaping for positive weights; lower values make trend commitment stronger and sooner.

* Force FULL Anti-Trend at Deep-Low ADX. Optional hard switch for extremely low ADX conditions.

On the chart you will see:

* A 12-segment forward polyline starting from the current close to bar\_index + 1 … +12, with green segments for up-steps and red for down-steps.

* A small label at the latest bar showing Meta Bias% when available, or “n/a” when insufficient data exists.

Interpreting the readouts:

* Trend-following contexts are characterized by ADX above the adaptive upper band, pushing w toward +1. The blended forecast leans toward the regression extrapolation. A strongly positive Meta Bias% in this environment suggests directional alignment across the ladder of timeframes.

* Mean-reversion contexts occur when ADX is well below the lower tail, pushing w toward -1 (or forcing anti-trend if enabled). After a sharp advance, a negative Meta Bias% may indicate the model projects pullback tendencies.

* Neutral contexts occur when ADX sits inside the flat band; w is near zero, the blended forecast remains close to current price, and Meta Bias% tends to hover near zero.

These are analytical cues, not rules. Always corroborate with your broader process, including market structure, time-of-day behavior, liquidity conditions, and risk limits.

Practical usage patterns include:

* Momentum confirmation. Combine a rising Meta Bias% with higher-timeframe structure (such as higher highs and higher lows) to validate continuation setups. Treat the 12th step’s distance as a coarse sense of potential room rather than as a target.

* Fade filtering. If you prefer fading extremes, require ADX to be near or below the lower ramp before acting on counter-moves, and avoid fades when ADX is decisively above the upper band.

* Position planning. Because per-step deltas are ATR-scaled, the path’s vertical extent can be mentally mapped to typical noise for the instrument, informing stop distance choices. The script itself does not compute orders or size.

* Multi-timeframe alignment. Each step corresponds to a clean multiple of your chart timeframe, so the polyline visualizes how successively larger windows bias price, all referenced to the current bar.

House-rules and repainting disclosures:

* Indicator, not strategy. The script does not execute, manage, or suggest orders. It displays computed paths and bias scores for analysis only.

* No performance claims. Past behavior of any measure, including Meta Bias%, does not guarantee future results. There are no assurances of profitability.

* Higher-timeframe updates. Values obtained via security for higher-timeframe series can update intrabar until the higher-timeframe bar closes. The forward path and Meta Bias% may change during formation of a higher-timeframe candle. If you need confirmed higher-timeframe inputs, consider reading the prior higher-timeframe value or acting only after the higher-timeframe close.

* Data sufficiency. The model requires enough history to compute ATR, ADX statistics, and regression windows. On very young charts or illiquid symbols, parts of the readout can be unavailable until sufficient data accumulates.

* Volatility regimes. ATR normalization helps compare across timeframes, but unusual volatility regimes can make the path look deceptively flat or exaggerated. Judge the vertical scale relative to your instrument’s typical ATR.

Tuning tips:

* Stability versus responsiveness. Increase Max Regression Length to steady the micro-forecasts but accept slower response. If you lower it, consider slightly increasing Band Lookback so regime boundaries are not too jumpy.

* Regime bands. Widen the flat half-width to spend more time neutral, which can reduce over-trading tendencies in chop. Shrink the tail width if you want the model to commit to extremes sooner, at the cost of more false swings.

* Wing shaping. If anti-trend behavior feels too abrupt at low ADX, raise the negative wing exponent. If you want trend bias to kick in more decisively at high ADX, lower the positive wing exponent. Small changes have large effects.

* Forced anti-trend. Enable the deep-low option only if you explicitly want a categorical “markets are flat, fade moves” policy. Many users prefer leaving it off to keep regime decisions continuous.

Troubleshooting:

* Nothing plots or the label shows “n/a.” Ensure the chart has enough history for the ADX band statistics, ATR, and the regression windows. Exotic or illiquid symbols with missing data may starve the higher-timeframe computations. Try a more liquid market or a higher timeframe.

* Path flickers or shifts during the bar. This is expected when any higher-timeframe input is still forming. Wait for the higher-timeframe close for fully confirmed behavior, or modify the code to read prior values from the higher timeframe.

* Polyline looks too flat or too steep. Check the chart’s vertical scale and recent ATR regime. Adjust Max Regression Length, the wing exponents, or the band widths to suit the instrument.

Integration ideas for manual workflows:

* Confluence checklist. Use Meta Bias% as one of several independent checks, alongside structure, session context, and event risk. Act only when multiple cues align.

* Stop and target thinking. Because deltas are ATR-scaled at each timeframe, benchmark your proposed stops and targets against the forward steps’ magnitude. Stops that are much tighter than the prevailing ATR often sit inside normal noise.

* Session context. Consider session hours and microstructure. The same ADX value can imply different tradeability in different sessions, particularly in index futures and FX.

This indicator deliberately avoids:

* Fixed thresholds for buy or sell decisions. Markets vary and fixed numbers invite overfitting. Decide what constitutes “high enough” Meta Bias% for your market and timeframe.

* Automatic risk sizing. Proper sizing depends on account parameters, instrument specifications, and personal risk tolerance. Keep that decision in your risk plan, not in a visual bias tool.

* Claims of edge. These measures summarize path geometry and trend context; they do not ensure a tradable edge on their own.

Summary of how to think about the output:

* The script builds a 12-step forward path by stacking linear-regression micro-forecasts across increasing multiples of the chart timeframe.

* Each micro-forecast is blended between trend and anti-trend using an adaptive ADX band with separate aggression controls for positive and negative regimes.

* All computations are done in ATR-true units for each timeframe before reconversion to price, ensuring dimensional consistency when accumulating steps.

* Bias% (per-timeframe and Meta) condenses directional efficiency and trend fidelity into a compact score.

* The output is designed to serve as an analytical overlay that helps assess whether conditions look trend-friendly, fade-friendly, or neutral, while acknowledging higher-timeframe update behavior and avoiding prescriptive trade rules.

Use this tool as one component within a disciplined process that includes independent confirmation, event awareness, and robust risk management.

CDC ActionZone BF for ETHUSD-1D © PRoSkYNeT-EE

Based on improvements from "Kitti-Playbook Action Zone V.4.2.0.3 for Stock Market"

Based on improvements from "CDC Action Zone V3 2020 by piriya33"

Based on Triple MACD crossover between 9/15, 21/28, 15/28 for filter error signal (noise) from CDC ActionZone V3

MACDs generated from the execution of millions of times in the "Brute Force Algorithm" to backtest data from the past 5 years. ( 2017-08-21 to 2022-08-01 )

Released 2022-08-01

***** The indicator is used in the ETHUSD 1 Day period ONLY *****

Recommended Stop Loss : -4 % (execute stop Loss after candlestick has been closed)

Backtest Result ( Start $100 )

Winrate 63 % (Win:12, Loss:7, Total:19)

Live Days 1,806 days

B : Buy

S : Sell

SL : Stop Loss

2022-07-19 07 - 1,542 : B 6.971 ETH

2022-04-13 07 - 3,118 : S 8.98 % $10,750 12,7,19 63 %

2022-03-20 07 - 2,861 : B 3.448 ETH

2021-12-03 07 - 4,216 : SL -8.94 % $9,864 11,7,18 61 %

2021-11-30 07 - 4,630 : B 2.340 ETH

2021-11-18 07 - 3,997 : S 13.71 % $10,832 11,6,17 65 %

2021-10-05 07 - 3,515 : B 2.710 ETH

2021-09-20 07 - 2,977 : S 29.38 % $9,526 10,6,16 63 %

2021-07-28 07 - 2,301 : B 3.200 ETH

2021-05-20 07 - 2,769 : S 50.49 % $7,363 9,6,15 60 %

2021-03-30 07 - 1,840 : B 2.659 ETH

2021-03-22 07 - 1,681 : SL -8.29 % $4,893 8,6,14 57 %

2021-03-08 07 - 1,833 : B 2.911 ETH

2021-02-26 07 - 1,445 : S 279.27 % $5,335 8,5,13 62 %

2020-10-13 07 - 381 : B 3.692 ETH

2020-09-05 07 - 335 : S 38.43 % $1,407 7,5,12 58 %

2020-07-06 07 - 242 : B 4.199 ETH

2020-06-27 07 - 221 : S 28.49 % $1,016 6,5,11 55 %

2020-04-16 07 - 172 : B 4.598 ETH

2020-02-29 07 - 217 : S 47.62 % $791 5,5,10 50 %

2020-01-12 07 - 147 : B 3.644 ETH

2019-11-18 07 - 178 : S -2.73 % $536 4,5,9 44 %

2019-11-01 07 - 183 : B 3.010 ETH

2019-09-23 07 - 201 : SL -4.29 % $551 4,4,8 50 %

2019-09-18 07 - 210 : B 2.740 ETH

2019-07-12 07 - 275 : S 63.69 % $575 4,3,7 57 %

2019-05-03 07 - 168 : B 2.093 ETH

2019-04-28 07 - 158 : S 29.51 % $352 3,3,6 50 %

2019-02-15 07 - 122 : B 2.225 ETH

2019-01-10 07 - 125 : SL -6.02 % $271 2,3,5 40 %

2018-12-29 07 - 133 : B 2.172 ETH

2018-05-22 07 - 641 : S 5.95 % $289 2,2,4 50 %

2018-04-21 07 - 605 : B 0.451 ETH

2018-02-02 07 - 922 : S 197.42 % $273 1,2,3 33 %

2017-11-11 07 - 310 : B 0.296 ETH

2017-10-09 07 - 297 : SL -4.50 % $92 0,2,2 0 %

2017-10-07 07 - 311 : B 0.309 ETH

2017-08-22 07 - 310 : SL -4.02 % $96 0,1,1 0 %

2017-08-21 07 - 323 : B 0.310 ETH

Bar Balance [LucF]Bar Balance extracts the number of up, down and neutral intrabars contained in each chart bar, revealing information on the strength of price movement. It can display stacked columns representing raw up/down/neutral intrabar counts, or an up/down balance line which can be calculated and visualized in many different ways.

WARNING: This is an analysis tool that works on historical bars only. It does not show any realtime information, and thus cannot be used to issue alerts or for automated trading. When realtime bars elapse, the indicator will require a browser refresh, a change to its Inputs or to the chart's timeframe/symbol to recalculate and display information on those elapsed bars. Once a trader understands this, the indicator can be used advantageously to make discretionary trading decisions.

Traders used to work with my Delta Volume Columns Pro will feel right at home in this indicator's Inputs . It has lots of options, allowing it to be used in many different ways. If you value the bar balance information this indicator mines, I hope you will find the time required to master the use of Bar Balance well worth the investment.

█ OVERVIEW

The indicator has two modes: Columns and Line .

Columns

• In Columns mode you can display stacked Up/Down/Neutral columns.

• The "Up" section represents the count of intrabars where `close > open`, "Down" where `close < open` and "Neutral" where `close = open`.

• The Up section always appears above the centerline, the Down section below. The Neutral section overlaps the centerline, split halfway above and below it.

The Up and Down sections start where the Neutral section ends, when there is one.

• The Up and Down sections can be colored independently using 7 different methods.

• The signal line plotted in Line mode can also be displayed in Columns mode.

Line

• Displays a single balance line using a zero centerline.

• A variable number of independent methods can be used to calculate the line (6), determine its color (5), and color the fill (5).

You can thus evaluate the state of 3 different components with this single line.

• A "Divergence Levels" feature will use the line to automatically draw expanding levels on divergence events.

Features available in both modes

• The color of all components can be selected from 15 base colors, with 16 gradient levels used for each base color in the indicator's gradients.

• A zero line can show a 6-state aggregate value of the three main volume balance modes.

• The background can be colored using any of 5 different methods.

• Chart bars can be colored using 5 different methods.

• Divergence and large neutral count ratio events can be shown in either Columns or Line mode, calculated in one of 4 different methods.

• Markers on 6 different conditions can be displayed.

█ CONCEPTS

Intrabar inspection

Intrabar inspection means the indicator looks at lower timeframe bars ( intrabars ) making up a given chart bar to gather its information. If your chart is on a 1-hour timeframe and the intrabar resolution determined by the indicator is 5 minutes, then 12 intrabars will be analyzed for each chart bar and the count of up/down/neutral intrabars among those will be tallied.

Bar Balances and calculation methods

The indicator uses a variety of methods to evaluate bar balance and to derive other calculations from them:

1. Balance on Bar : Uses the relative importance of instant Up and Down counts on the bar.

2. Balance Averages : Uses the difference between the EMAs of Up and Down counts.

3. Balance Momentum : Starts by calculating, separately for both Up and Down counts, the difference between the same EMAs used in Balance Averages and an SMA of double the period used for the EMAs. These differences are then aggregated and finally, a bounded momentum of that aggregate is calculated using RSI.

4. Markers Bias : It sums the bull/bear occurrences of the four previous markers over a user-defined period (the default is 14).

5. Combined Balances : This is the aggregate of the instant bull/bear bias of the three main bar balances.

6. Dual Up/Down Averages : This is a display mode showing the EMA calculated for each of the Up and Down counts.

Interpretation of neutral intrabars

What do neutral intrabars mean? When price does not change during a bar, it can be because there is simply no interest in the market, or because of a perfect balance between buyers and sellers. The latter being more improbable, Bar Balance assumes that neutral bars reveal a lack of interest, which entails uncertainty. That is the reason why the option is provided to interpret ratios of neutral intrabars greater than 50% as divergences. It is also the rationale behind the option to dampen signal lines on the inverse ratio of neutral intrabars, so that zero intrabars do not affect the signal, and progressively larger proportions of neutral intrabars will reduce the signal's amplitude, as the balance calcs using the up/down counts lose significance. The impact of the dampening will vary with markets. Weaker markets such as cryptos will often contain greater numbers of neutral intrabars, so dampening the Line in that sector will have a greater impact than in more liquid markets.

█ FEATURES

1 — Columns

• While the size of the Up/Down columns always represents their respective importance on the bar, their coloring mode is independent. The default setup uses a standard coloring mode where the Up/Down columns over/under the zero line are always in the bull/bear color with a higher intensity for the winning side. Six other coloring modes allow you to pack more information in the columns. When choosing to color the top columns using a bull/bear gradient on Balance Averages, for example, you will end up with bull/bear colored tops. In order for the color of the bottom columns to continue to show the instant bar balance, you can then choose the "Up/Down Ratio on Bar — Dual Solid Colors" coloring mode to make those bars the color of the winning side for that bar.

• Line mode shows only the line, but Columns mode allows displaying the line along with it. If the scale of the line is different than that of the scale of the columns, the line will often appear flat. Traders may find even a flat line useful as its bull/bear colors will be easily distinguishable.

2 — Line

• The default setup for Line mode uses a calculation on "Balance Momentum", with a fill on the longer-term "Balance Averages" and a line color based on the "Markers Bias". With the background set on "Line vs Divergence Levels" and the zero line on the hard-coded "Combined Bar Balances", you have access to five distinct sources of information at a glance, to which you can add divergences, divergences levels and chart bar coloring. This provides powerful potential in displaying bar balance information.

• When no columns are displayed, Line mode can show the full scale of whichever line you choose to calculate because the columns' scale no longer interferes with the line's scale.

• Note that when "Balance on Bar" is selected, the Neutral count is also displayed as a ratio of the balance line. This is the only instance where the Neutral count is displayed in Line mode.

• The "Dual Up/Down Averages" is an exception as it displays two lines: one average for the Up counts and another for the Down counts. This mode will be most useful when Columns are also displayed, as it provides a reference for the top and bottom columns.

3 — Zero Line

The zero line can be colored using two methods, both based on the Combined Balances, i.e., the aggregate of the instant bull/bear bias of the three main bar balances.

• In "Six-state Dual Color Gradient" mode, a dot appears on every bar. Its color reflects the bull/bear state of the Combined Balances, and the dot's brightness reflects the tally of balance biases.

• In "Dual Solid Colors (All Bull/All Bear Only)" a dot only appears when all three balances are either bullish or bearish. The resulting pattern is identical to that of Marker 1.

4 — Divergences

• Divergences are displayed as a small circle at the top of the scale. Four different types of divergence events can be detected. Divergences occur whenever the bull/bear bias of the method used diverges with the bar's price direction.

• An option allows you to include in divergence events instances where the count of neutral intrabars exceeds 50% of the total intrabar count.

• The divergence levels are dynamic levels that automatically build from the line's values on divergence events. On consecutive divergences, the levels will expand, creating a channel. This implementation of the divergence levels corresponds to my view that divergences indicate anomalies, hesitations, points of uncertainty if you will. It excludes any association of a pre-determined bullish/bearish bias to divergences. Accordingly, the levels merely take note of divergence events and mark those points in time with levels. Traders then have a reference point from which they can evaluate further movement. The bull/bear/neutral colors used to plot the levels are also congruent with this view in that they are determined by price's position relative to the levels, which is how I think divergences can be put to the most effective use.

5 — Background

• The background can show a bull/bear gradient on four different calculations. You can adjust its brightness to make its visual importance proportional to how you use it in your analysis.

6 — Chart bars

• Chart bars can be colored using five different methods.

• You have the option of emptying the body of bars where volume does not increase, as does my TLD indicator, the idea behind this being that movement on bars where volume does not increase is less relevant.

7 — Intrabar Resolution

You can choose between three modes. Two of them are automatic and one is manual:

a) Fast, Longer history, Auto-Steps (~12 intrabars) : Optimized for speed and deeper history. Uses an average minimum of 12 intrabars.

b) More Precise, Shorter History Auto-Steps (~24 intrabars) : Uses finer intrabar resolution. It is slower and provides less history. Uses an average minimum of 24 intrabars.

c) Fixed : Uses the fixed resolution of your choice.

Auto-Steps calculations vary for 24/7 and conventional markets in order to achieve the proper target of minimum intrabars.

You can choose to view the intrabar resolution currently used to calculate delta volume. It is the default.

The proper selection of the intrabar resolution is important. It must achieve maximal granularity to produce precise results while not unduly slowing down calculations, or worse, causing runtime errors.

8 — Markers

Six markers are available:

1. Combined Balances Agreement : All three Bar Balances are either bullish or bearish.

2. Up or Down % Agrees With Bar : An up marker will appear when the percentage of up intrabars in an up chart bar is greater than the specified percentage. Conditions mirror to down bars.

3. Divergence confirmations By Price : One of the four types of balance calculations can be used to detect divergences with price. Confirmations occur when the bar following the divergence confirms the balance bias. Note that the divergence events used here do not include neutral intrabar events.

4. Balance Transitions : Bull/bear transitions of the selected balance.

5. Markers Bias Transitions : Bull/bear transitions of the Markers Bias.

6. Divergence Confirmations By Line : Marks points where the line first breaches a divergence level.

Markers appear when the condition is detected, without delay. Since nothing is plotted in realtime, markers do not appear on the realtime bar.

9 — Settings

• Two modes can be selected to dampen the line on the ratio of neutral intrabars.

• A distinct weight can be attributed to the count of the latter half of intrabars, on the assumption that later intrabars may be more important in determining the outcome of chart bars.

• Allows control over the periods of the different moving averages used in calculations.

• The default periods used for the various calculations define the following hierarchy from slow to fast:

Balance Averages: 50,

Balance Momentum: 20,

Dual Up/Down Averages: 20,

Marker Bias: 10.

█ LIMITATIONS

• This script uses a special characteristic of the `security()` function allowing the inspection of intrabars—which is not officially supported by TradingView.

• The method used does not work on the realtime bar—only on historical bars.

• The indicator only works on some chart resolutions: 3, 5, 10, 15 and 30 minutes, 1, 2, 4, 6, and 12 hours, 1 day, 1 week and 1 month. The script’s code can be modified to run on other resolutions, but chart resolutions must be divisible by the lower resolution used for intrabars and the stepping mechanism could require adaptation.

• When using the "Line vs Divergence Levels — Dual Color Gradient" color mode to fill the line, background or chart bars, keep in mind that a line calculation mode must be defined for it to work, as it determines gradients on the movement of the line relative to divergence levels. If the line is hidden, it will not work.

• When the difference between the chart’s resolution and the intrabar resolution is too great, runtime errors will occur. The Auto-Steps selection mechanisms should avoid this.

• Alerts do not work reliably when `security()` is used at intrabar resolutions. Accordingly, no alerts are configured in the indicator.

• The color model used in the indicator provides for fancy visuals that come at a price; when you change values in Inputs , it can take 20 seconds for the changes to materialize. Luckily, once your color setup is complete, the color model does not have a large performance impact, as in normal operation the `security()` calls will become the most important factor in determining response time. Also, once in a while a runtime error will occur when you change inputs. Just making another change will usually bring the indicator back up.

█ RAMBLINGS

Is this thing useful?

I'll let you decide. Bar Balance acts somewhat like an X-Ray on bars. The intrabars it analyzes are no secret; one can simply change the chart's resolution to see the same intrabars the indicator uses. What the indicator brings to traders is the precise count of up/down/neutral intrabars and, more importantly, the calculations it derives from them to present the information in a way that can make it easier to use in trading decisions.

How reliable is Bar Balance information?

By the same token that an up bar does not guarantee that more up bars will follow, future price movements cannot be inferred from the mere count of up/down/neutral intrabars. Price movement during any chart bar for which, let's say, 12 intrabars are analyzed, could be due to only one of those intrabars. One can thus easily see how only relying on bar balance information could be very misleading. The rationale behind Bar Balance is that when the information mined for multiple chart bars is aggregated, it can provide insight into the history behind chart bars, and thus some bias as to the strength of movements. An up chart bar where 11/12 intrabars are also up is assumed to be stronger than the same up bar where only 2/12 intrabars are up. This logic is not bulletproof, and sometimes Bar Balance will stray. Also, keep in mind that balance lines do not represent price momentum as RSI would. Bar Balance calculations have no idea where price is. Their perspective, like that of any historian, is very limited, constrained that it is to the narrow universe of up/down/neutral intrabar counts. You will thus see instances where price is moving up while Balance Momentum, for example, is moving down. When Bar Balance performs as intended, this indicates that the rally is weakening, which does necessarily imply that price will reverse. Occasionally, price will merrily continue to advance on weakening strength.

Divergences

Most of the divergence detection methods used here rely on a difference between the bias of a calculation involving a multi-bar average and a given bar's price direction. When using "Bar Balance on Bar" however, only the bar's balance and price movement are used. This is the default mode.

As usual, divergences are points of interest because they reveal imbalances, which may or may not become turning points. I do not share the overwhelming enthusiasm traders have for the purported ability of bullish/bearish divergences to indicate imminent reversals.

Superfluity

In "The Bed of Procrustes", Nassim Nicholas Taleb writes: To bankrupt a fool, give him information . Bar Balance can display lots of information. While learning to use a new indicator inevitably requires an adaptation period where we put it through its paces and try out all its options, once you have become used to Bar Balance and decide to adopt it, rigorously eliminate the components you don't use and configure the remaining ones so their visual prominence reflects their relative importance in your analysis. I tried to provide flexible options for traders to control this indicator's visuals for that exact reason—not for window dressing.

█ NOTES

For traders

• To avoid misleading traders who don't read script descriptions, the indicator shows nothing in the realtime bar.

• The Data Window shows key values for the indicator.

• All gradients used in this indicator determine their brightness intensities using advances/declines in the signal—not their relative position in a fixed scale.

• Note that because of the way gradients are optimized internally, changing their brightness will sometimes require bringing down the value a few steps before you see an impact.

• Because this indicator does not use volume, it will work on all markets.

For coders

• For those interested in gradients, this script uses an advanced version of the Advance/Decline gradient function from the PineCoders Color Gradient (16 colors) Framework . It allows more precise control over the range, steps and min/max values of the gradients.

• I use the PineCoders Coding Conventions for Pine to write my scripts.

• I used functions modified from the PineCoders MTF Selection Framework for the selection of timeframes.

█ THANKS TO:

— alexgrover who helped me think through the dampening method used to attenuate signal lines on high ratios of neutral intrabars.

— A guy called Kuan who commented on a Backtest Rookies presentation of their Volume Profile indicator . The technique I use to inspect intrabars is derived from Kuan's code.

— theheirophant , my partner in the exploration of the sometimes weird abysses of `security()`’s behavior at intrabar resolutions.

— midtownsk8rguy , my brilliant companion in mining the depths of Pine graphics. He is also the co-author of the PineCoders Color Gradient Frameworks .

Monthly Color Marker V4

## 📊 Monthly Color Marker - Historical Month Highlighting

### Overview

A unique indicator that allows rapid identification of all monthly candles from a specific month across multiple years. The indicator marks candles with different colors based on their direction (bullish/bearish), enabling quick analysis of seasonal patterns and cyclical behavior of stocks or assets.

### 🎯 Purpose

- **Identify Seasonal Patterns (Seasonality)** - Discover recurring trends in specific months

- **Quick Historical Analysis** - Visual representation of monthly performance over the years

- **Direction Recognition** - Instant understanding of whether a month tends to be bullish or bearish

- **Seasonal Trading Planning** - Build strategies based on cyclical patterns

### ⚙️ Adjustable Parameters

1. **Month to Mark (1-12)**

- Select the desired month for analysis

- 1 = January, 2 = February... 12 = December

- Default: 11 (November)

2. **Years Back (1-50)**

- Determines how many years back to scan

- Recommended: 10-25 years for statistically reliable data

- Default: 25 years

3. **Bullish Candle Color**

- Color for marking bullish candles (close > open)

- Default: Green

- Customizable to your personal color scheme

4. **Bearish Candle Color**

- Color for marking bearish candles (close < open)

- Default: Red

- Customizable to your personal color scheme

5. **Show Current Year**

- Whether to include the current month in the marking

- Useful when the month hasn't finished yet

- Default: Yes

### 📈 How to Use the Indicator

#### Step 1: Adding to Chart

1. Switch to **Monthly timeframe** - Required!

2. Add the indicator to your chart

3. Select the month you want to analyze

#### Step 2: Initial Analysis

- **Count green vs red candles** - What's the ratio?

- **Look for patterns** - Are there years where the month always rises/falls?

- **Identify outliers** - Years where behavior was different

#### Step 3: Making Decisions

- **Mostly green** → Statistically, the month tends to rise

- **Mostly red** → Statistically, the month tends to fall

- **Mixed** → No clear seasonal pattern

### 💡 Usage Examples

**Example 1: "Santa Claus Rally"**

- Select month 12 (December)

- Check if there are mostly green candles

- If yes, this confirms the well-known year-end rally effect

**Example 2: "September Effect"**

- Select month 9 (September)

- Historically, September is considered a weak month

- Do the data support this for this stock?

**Example 3: Quarterly Earnings**

- Identify which month earnings are released

- Check the historical response

- Plan entry/exit accordingly

### 🔍 Combining with Other Indicators

This indicator works excellently with:

- **Historical Monthly Levels** (the first indicator) - Identify nearby price levels

- **Volume Profile** - Check volume during those months

- **RSI/MACD** - Identify momentum strength in specific months

### ⚠️ Important Notes

1. **Must use Monthly timeframe!** The indicator won't work correctly on other timeframes

2. **Statistical Sample** - More years = more reliable analysis

3. **Not a Guarantee** - Past performance doesn't guarantee future results, use additional analysis

4. **Adjust Colors** - If hard to see, change colors in settings

### 🎨 Tips for Optimal Experience

- **Zoom Out** - See more years at a glance

- **Clean Chart** - Remove unnecessary indicators for clear analysis

- **Compare Stocks** - Check multiple stocks for the same month

- **Document Findings** - Take screenshots and save insights for future reference

### 📊 Recommended Statistics

After identifying an interesting month:

- Calculate success rate (green / total candles)

- Check average volatility

- Identify outlier years and investigate what happened

- Plan entry/exit strategy

### 🚀 Who Is This Indicator For?

✅ **Swing Traders** - Plan medium-term trades

✅ **Seasonal Investors** - Exploit cyclical patterns

✅ **Technical Analysts** - Understand historical behavior

✅ **Portfolio Managers** - Time entries and exits

---

### 📝 Summary

The Monthly Color Marker indicator is a powerful and easy-to-use tool for identifying seasonal patterns. The combination of clear visualization with flexible parameters makes it an essential tool for any trader seeking a statistical edge in the market.

**Recommendation:** Start with 25 years back, analyze 2-3 key months, and build a data-driven strategy.

---

**Version:** 4.0

**Compatibility:** Pine Script v5

**Timeframe:** Monthly only

**Author:** 954

## 📊 Monthly Color Marker - סימון חודשים היסטוריים

### תיאור כללי

אינדיקטור ייחודי המאפשר לזהות במהירות את כל הנרות החודשיים מחודש ספציפי לאורך השנים. האינדיקטור מסמן את הנרות בצבעים שונים בהתאם לכיוון התנועה (עלייה/ירידה), ומאפשר ניתוח מהיר של דפוסים עונתיים והתנהגות מחזורית של המניה או הנכס.

### 🎯 מטרת האינדיקטור

- **זיהוי דפוסים עונתיים (Seasonality)** - מציאת מגמות חוזרות בחודשים מסוימים

- **ניתוח היסטורי מהיר** - ראייה ויזואלית של ביצועי החודש לאורך השנים

- **זיהוי כיווניות** - הבנה מיידית האם החודש נוטה להיות שורי או דובי

- **תכנון מסחר עונתי** - בניית אסטרטגיות מבוססות מחזוריות

### ⚙️ פרמטרים מתכווננים

1. **חודש לסימון (1-12)**

- בחירת החודש הרצוי לניתוח

- 1 = ינואר, 2 = פברואר... 12 = דצמבר

- ברירת מחדל: 11 (נובמבר)

2. **שנים אחורה (1-50)**

- קובע כמה שנים אחורה לסרוק

- מומלץ: 10-25 שנים לקבלת תמונה סטטיסטית מהימנה

- ברירת מחדל: 25 שנים

3. **צבע נר עולה**

- צבע לסימון נרות שורים (close > open)

- ברירת מחדל: ירוק

- ניתן להתאים לסכמת הצבעים האישית

4. **צבע נר יורד**

- צבע לסימון נרות דוביים (close < open)

- ברירת מחדל: אדום

- ניתן להתאים לסכמת הצבעים האישית

5. **צבע את השנה הנוכחית**

- האם לכלול את החודש הנוכחי בסימון

- שימושי כאשר החודש טרם הסתיים

- ברירת מחדל: כן

### 📈 איך להשתמש באינדיקטור

#### שלב 1: הוספה לגרף

1. עבור לטיימפריים **חודשי (Monthly)** - חובה!

2. הוסף את האינדיקטור לגרף

3. בחר את החודש שאתה רוצה לנתח

#### שלב 2: ניתוח ראשוני

- **ספור נרות ירוקים מול אדומים** - מה היחס?

- **חפש דפוסים** - האם יש שנים שבהן החודש תמיד עולה/יורד?

- **זהה חריגים** - שנים שבהן ההתנהגות הייתה שונה

#### שלב 3: קבלת החלטות

- **רוב ירוקים** → סטטיסטית החודש נוטה לעלות

- **רוב אדומים** → סטטיסטית החודש נוטה לרדת

- **מעורב** → אין דפוס עונתי ברור

### 💡 דוגמאות שימוש

**דוגמה 1: "Santa Claus Rally"**

- בחר חודש 12 (דצמבר)

- בדוק אם יש רוב נרות ירוקים

- אם כן, זה מאשר את האפקט הידוע של עליות בסוף השנה

**דוגמה 2: "September Effect"**

- בחר חודש 9 (ספטמבר)

- היסטורית, ספטמבר נחשב לחודש חלש

- האם הנתונים תומכים בכך במניה זו?

**דוגמה 3: דיווחים רבעוניים**

- זהה בחודש אילו נפרסמים דיווחים

- בדוק את התגובה ההיסטורית

- תכנן כניסה/יציאה בהתאם

### 🔍 שילוב עם אינדיקטורים אחרים

האינדיקטור עובד מצוין בשילוב עם:

- **Historical Monthly Levels** (האינדיקטור הראשון) - זיהוי רמות מחיר קרובות

- **Volume Profile** - בדיקת ווליום באותם חודשים

- **RSI/MACD** - זיהוי כוח המומנטום בחודשים ספציפיים

### ⚠️ הערות חשובות

1. **חובה להשתמש בטיימפריים חודשי!** האינדיקטור לא יעבוד נכון בטיימפריים אחרים

2. **מדגם סטטיסטי** - ככל שיש יותר שנים, הניתוח מהימן יותר

3. **לא ערובה** - עבר לא מבטיח עתיד, השתמש בניתוח נוסף

4. **התאם צבעים** - אם קשה לראות, שנה את הצבעים בהגדרות

### 🎨 טיפים לחוויית שימוש מיטבית

- **זום אאוט** - ראה יותר שנים במבט אחד

- **נקה גרף** - הסר אינדיקטורים מיותרים לניתוח ברור

- **השווה מניות** - בדוק מספר מניות לאותו חודש

- **תעד ממצאים** - צלם מסך ושמור תובנות לעתיד

### 📊 סטטיסטיקה מומלצת

לאחר שזיהית חודש מעניין:

- חשב אחוז הצלחה (ירוקים / כל הנרות)

- בדוק תנודתיות ממוצעת

- זהה שנים חריגות ובדוק מה קרה אז

- תכנן אסטרטגיית כניסה/יציאה

### 🚀 למי מתאים האינדיקטור?

✅ **סווינג טריידרים** - תכנון עסקאות לטווח בינוני

✅ **משקיעים עונתיים** - ניצול דפוסים מחזוריים

✅ **אנליסטים טכניים** - הבנת התנהגות היסטורית

✅ **מנהלי תיקים** - תזמון כניסות ויציאות

---

### 📝 סיכום

אינדיקטור Monthly Color Marker הוא כלי חזק וקל לשימוש לזיהוי דפוסים עונתיים. השילוב של ויזואליזציה ברורה עם פרמטרים גמישים הופך אותו לכלי חיוני לכל טריידר המחפש יתרון סטטיסטי בשוק.

**המלצה:** התחל עם 25 שנים אחורה, נתח 2-3 חודשים מרכזיים, ובנה אסטרטגיה מבוססת נתונים.

---

**גרסה:** 4.0

**תאימות:** Pine Script v5

**טיימפריים:** חודשי בלבד

**מחבר:** [954

---

Markov Chain [3D] | FractalystWhat exactly is a Markov Chain?

This indicator uses a Markov Chain model to analyze, quantify, and visualize the transitions between market regimes (Bull, Bear, Neutral) on your chart. It dynamically detects these regimes in real-time, calculates transition probabilities, and displays them as animated 3D spheres and arrows, giving traders intuitive insight into current and future market conditions.

How does a Markov Chain work, and how should I read this spheres-and-arrows diagram?

Think of three weather modes: Sunny, Rainy, Cloudy.

Each sphere is one mode. The loop on a sphere means “stay the same next step” (e.g., Sunny again tomorrow).

The arrows leaving a sphere show where things usually go next if they change (e.g., Sunny moving to Cloudy).

Some paths matter more than others. A more prominent loop means the current mode tends to persist. A more prominent outgoing arrow means a change to that destination is the usual next step.

Direction isn’t symmetric: moving Sunny→Cloudy can behave differently than Cloudy→Sunny.

Now relabel the spheres to markets: Bull, Bear, Neutral.

Spheres: market regimes (uptrend, downtrend, range).

Self‑loop: tendency for the current regime to continue on the next bar.

Arrows: the most common next regime if a switch happens.

How to read: Start at the sphere that matches current bar state. If the loop stands out, expect continuation. If one outgoing path stands out, that switch is the typical next step. Opposite directions can differ (Bear→Neutral doesn’t have to match Neutral→Bear).

What states and transitions are shown?

The three market states visualized are:

Bullish (Bull): Upward or strong-market regime.

Bearish (Bear): Downward or weak-market regime.

Neutral: Sideways or range-bound regime.

Bidirectional animated arrows and probability labels show how likely the market is to move from one regime to another (e.g., Bull → Bear or Neutral → Bull).

How does the regime detection system work?

You can use either built-in price returns (based on adaptive Z-score normalization) or supply three custom indicators (such as volume, oscillators, etc.).

Values are statistically normalized (Z-scored) over a configurable lookback period.

The normalized outputs are classified into Bull, Bear, or Neutral zones.

If using three indicators, their regime signals are averaged and smoothed for robustness.

How are transition probabilities calculated?

On every confirmed bar, the algorithm tracks the sequence of detected market states, then builds a rolling window of transitions.

The code maintains a transition count matrix for all regime pairs (e.g., Bull → Bear).

Transition probabilities are extracted for each possible state change using Laplace smoothing for numerical stability, and frequently updated in real-time.

What is unique about the visualization?

3D animated spheres represent each regime and change visually when active.

Animated, bidirectional arrows reveal transition probabilities and allow you to see both dominant and less likely regime flows.

Particles (moving dots) animate along the arrows, enhancing the perception of regime flow direction and speed.

All elements dynamically update with each new price bar, providing a live market map in an intuitive, engaging format.

Can I use custom indicators for regime classification?

Yes! Enable the "Custom Indicators" switch and select any three chart series as inputs. These will be normalized and combined (each with equal weight), broadening the regime classification beyond just price-based movement.

What does the “Lookback Period” control?

Lookback Period (default: 100) sets how much historical data builds the probability matrix. Shorter periods adapt faster to regime changes but may be noisier. Longer periods are more stable but slower to adapt.

How is this different from a Hidden Markov Model (HMM)?

It sets the window for both regime detection and probability calculations. Lower values make the system more reactive, but potentially noisier. Higher values smooth estimates and make the system more robust.

How is this Markov Chain different from a Hidden Markov Model (HMM)?

Markov Chain (as here): All market regimes (Bull, Bear, Neutral) are directly observable on the chart. The transition matrix is built from actual detected regimes, keeping the model simple and interpretable.

Hidden Markov Model: The actual regimes are unobservable ("hidden") and must be inferred from market output or indicator "emissions" using statistical learning algorithms. HMMs are more complex, can capture more subtle structure, but are harder to visualize and require additional machine learning steps for training.

A standard Markov Chain models transitions between observable states using a simple transition matrix, while a Hidden Markov Model assumes the true states are hidden (latent) and must be inferred from observable “emissions” like price or volume data. In practical terms, a Markov Chain is transparent and easier to implement and interpret; an HMM is more expressive but requires statistical inference to estimate hidden states from data.

Markov Chain: states are observable; you directly count or estimate transition probabilities between visible states. This makes it simpler, faster, and easier to validate and tune.

HMM: states are hidden; you only observe emissions generated by those latent states. Learning involves machine learning/statistical algorithms (commonly Baum–Welch/EM for training and Viterbi for decoding) to infer both the transition dynamics and the most likely hidden state sequence from data.

How does the indicator avoid “repainting” or look-ahead bias?

All regime changes and matrix updates happen only on confirmed (closed) bars, so no future data is leaked, ensuring reliable real-time operation.

Are there practical tuning tips?

Tune the Lookback Period for your asset/timeframe: shorter for fast markets, longer for stability.

Use custom indicators if your asset has unique regime drivers.

Watch for rapid changes in transition probabilities as early warning of a possible regime shift.

Who is this indicator for?

Quants and quantitative researchers exploring probabilistic market modeling, especially those interested in regime-switching dynamics and Markov models.

Programmers and system developers who need a probabilistic regime filter for systematic and algorithmic backtesting:

The Markov Chain indicator is ideally suited for programmatic integration via its bias output (1 = Bull, 0 = Neutral, -1 = Bear).

Although the visualization is engaging, the core output is designed for automated, rules-based workflows—not for discretionary/manual trading decisions.

Developers can connect the indicator’s output directly to their Pine Script logic (using input.source()), allowing rapid and robust backtesting of regime-based strategies.

It acts as a plug-and-play regime filter: simply plug the bias output into your entry/exit logic, and you have a scientifically robust, probabilistically-derived signal for filtering, timing, position sizing, or risk regimes.

The MC's output is intentionally "trinary" (1/0/-1), focusing on clear regime states for unambiguous decision-making in code. If you require nuanced, multi-probability or soft-label state vectors, consider expanding the indicator or stacking it with a probability-weighted logic layer in your scripting.

Because it avoids subjectivity, this approach is optimal for systematic quants, algo developers building backtested, repeatable strategies based on probabilistic regime analysis.

What's the mathematical foundation behind this?

The mathematical foundation behind this Markov Chain indicator—and probabilistic regime detection in finance—draws from two principal models: the (standard) Markov Chain and the Hidden Markov Model (HMM).

How to use this indicator programmatically?

The Markov Chain indicator automatically exports a bias value (+1 for Bullish, -1 for Bearish, 0 for Neutral) as a plot visible in the Data Window. This allows you to integrate its regime signal into your own scripts and strategies for backtesting, automation, or live trading.

Step-by-Step Integration with Pine Script (input.source)

Add the Markov Chain indicator to your chart.

This must be done first, since your custom script will "pull" the bias signal from the indicator's plot.

In your strategy, create an input using input.source()

Example:

//@version=5

strategy("MC Bias Strategy Example")

mcBias = input.source(close, "MC Bias Source")

After saving, go to your script’s settings. For the “MC Bias Source” input, select the plot/output of the Markov Chain indicator (typically its bias plot).

Use the bias in your trading logic

Example (long only on Bull, flat otherwise):

if mcBias == 1

strategy.entry("Long", strategy.long)

else

strategy.close("Long")

For more advanced workflows, combine mcBias with additional filters or trailing stops.

How does this work behind-the-scenes?

TradingView’s input.source() lets you use any plot from another indicator as a real-time, “live” data feed in your own script (source).

The selected bias signal is available to your Pine code as a variable, enabling logical decisions based on regime (trend-following, mean-reversion, etc.).

This enables powerful strategy modularity : decouple regime detection from entry/exit logic, allowing fast experimentation without rewriting core signal code.

Integrating 45+ Indicators with Your Markov Chain — How & Why

The Enhanced Custom Indicators Export script exports a massive suite of over 45 technical indicators—ranging from classic momentum (RSI, MACD, Stochastic, etc.) to trend, volume, volatility, and oscillator tools—all pre-calculated, centered/scaled, and available as plots.

// Enhanced Custom Indicators Export - 45 Technical Indicators

// Comprehensive technical analysis suite for advanced market regime detection

//@version=6

indicator('Enhanced Custom Indicators Export | Fractalyst', shorttitle='Enhanced CI Export', overlay=false, scale=scale.right, max_labels_count=500, max_lines_count=500)

// |----- Input Parameters -----| //

momentum_group = "Momentum Indicators"

trend_group = "Trend Indicators"

volume_group = "Volume Indicators"

volatility_group = "Volatility Indicators"

oscillator_group = "Oscillator Indicators"

display_group = "Display Settings"

// Common lengths

length_14 = input.int(14, "Standard Length (14)", minval=1, maxval=100, group=momentum_group)

length_20 = input.int(20, "Medium Length (20)", minval=1, maxval=200, group=trend_group)

length_50 = input.int(50, "Long Length (50)", minval=1, maxval=200, group=trend_group)

// Display options

show_table = input.bool(true, "Show Values Table", group=display_group)

table_size = input.string("Small", "Table Size", options= , group=display_group)

// |----- MOMENTUM INDICATORS (15 indicators) -----| //

// 1. RSI (Relative Strength Index)

rsi_14 = ta.rsi(close, length_14)

rsi_centered = rsi_14 - 50

// 2. Stochastic Oscillator

stoch_k = ta.stoch(close, high, low, length_14)

stoch_d = ta.sma(stoch_k, 3)

stoch_centered = stoch_k - 50

// 3. Williams %R

williams_r = ta.stoch(close, high, low, length_14) - 100

// 4. MACD (Moving Average Convergence Divergence)

= ta.macd(close, 12, 26, 9)

// 5. Momentum (Rate of Change)

momentum = ta.mom(close, length_14)

momentum_pct = (momentum / close ) * 100

// 6. Rate of Change (ROC)

roc = ta.roc(close, length_14)

// 7. Commodity Channel Index (CCI)

cci = ta.cci(close, length_20)

// 8. Money Flow Index (MFI)

mfi = ta.mfi(close, length_14)

mfi_centered = mfi - 50

// 9. Awesome Oscillator (AO)

ao = ta.sma(hl2, 5) - ta.sma(hl2, 34)

// 10. Accelerator Oscillator (AC)

ac = ao - ta.sma(ao, 5)

// 11. Chande Momentum Oscillator (CMO)

cmo = ta.cmo(close, length_14)

// 12. Detrended Price Oscillator (DPO)

dpo = close - ta.sma(close, length_20)

// 13. Price Oscillator (PPO)

ppo = ta.sma(close, 12) - ta.sma(close, 26)

ppo_pct = (ppo / ta.sma(close, 26)) * 100

// 14. TRIX

trix_ema1 = ta.ema(close, length_14)

trix_ema2 = ta.ema(trix_ema1, length_14)

trix_ema3 = ta.ema(trix_ema2, length_14)

trix = ta.roc(trix_ema3, 1) * 10000

// 15. Klinger Oscillator

klinger = ta.ema(volume * (high + low + close) / 3, 34) - ta.ema(volume * (high + low + close) / 3, 55)

// 16. Fisher Transform

fisher_hl2 = 0.5 * (hl2 - ta.lowest(hl2, 10)) / (ta.highest(hl2, 10) - ta.lowest(hl2, 10)) - 0.25

fisher = 0.5 * math.log((1 + fisher_hl2) / (1 - fisher_hl2))

// 17. Stochastic RSI

stoch_rsi = ta.stoch(rsi_14, rsi_14, rsi_14, length_14)

stoch_rsi_centered = stoch_rsi - 50

// 18. Relative Vigor Index (RVI)

rvi_num = ta.swma(close - open)

rvi_den = ta.swma(high - low)

rvi = rvi_den != 0 ? rvi_num / rvi_den : 0

// 19. Balance of Power (BOP)

bop = (close - open) / (high - low)

// |----- TREND INDICATORS (10 indicators) -----| //

// 20. Simple Moving Average Momentum

sma_20 = ta.sma(close, length_20)

sma_momentum = ((close - sma_20) / sma_20) * 100

// 21. Exponential Moving Average Momentum

ema_20 = ta.ema(close, length_20)

ema_momentum = ((close - ema_20) / ema_20) * 100

// 22. Parabolic SAR

sar = ta.sar(0.02, 0.02, 0.2)

sar_trend = close > sar ? 1 : -1

// 23. Linear Regression Slope

lr_slope = ta.linreg(close, length_20, 0) - ta.linreg(close, length_20, 1)

// 24. Moving Average Convergence (MAC)

mac = ta.sma(close, 10) - ta.sma(close, 30)

// 25. Trend Intensity Index (TII)

tii_sum = 0.0

for i = 1 to length_20

tii_sum += close > close ? 1 : 0

tii = (tii_sum / length_20) * 100

// 26. Ichimoku Cloud Components

ichimoku_tenkan = (ta.highest(high, 9) + ta.lowest(low, 9)) / 2

ichimoku_kijun = (ta.highest(high, 26) + ta.lowest(low, 26)) / 2

ichimoku_signal = ichimoku_tenkan > ichimoku_kijun ? 1 : -1

// 27. MESA Adaptive Moving Average (MAMA)

mama_alpha = 2.0 / (length_20 + 1)

mama = ta.ema(close, length_20)

mama_momentum = ((close - mama) / mama) * 100

// 28. Zero Lag Exponential Moving Average (ZLEMA)

zlema_lag = math.round((length_20 - 1) / 2)

zlema_data = close + (close - close )

zlema = ta.ema(zlema_data, length_20)

zlema_momentum = ((close - zlema) / zlema) * 100

// |----- VOLUME INDICATORS (6 indicators) -----| //

// 29. On-Balance Volume (OBV)

obv = ta.obv

// 30. Volume Rate of Change (VROC)

vroc = ta.roc(volume, length_14)

// 31. Price Volume Trend (PVT)

pvt = ta.pvt

// 32. Negative Volume Index (NVI)

nvi = 0.0

nvi := volume < volume ? nvi + ((close - close ) / close ) * nvi : nvi

// 33. Positive Volume Index (PVI)

pvi = 0.0

pvi := volume > volume ? pvi + ((close - close ) / close ) * pvi : pvi

// 34. Volume Oscillator

vol_osc = ta.sma(volume, 5) - ta.sma(volume, 10)

// 35. Ease of Movement (EOM)

eom_distance = high - low

eom_box_height = volume / 1000000

eom = eom_box_height != 0 ? eom_distance / eom_box_height : 0

eom_sma = ta.sma(eom, length_14)

// 36. Force Index

force_index = volume * (close - close )

force_index_sma = ta.sma(force_index, length_14)

// |----- VOLATILITY INDICATORS (10 indicators) -----| //

// 37. Average True Range (ATR)

atr = ta.atr(length_14)

atr_pct = (atr / close) * 100

// 38. Bollinger Bands Position

bb_basis = ta.sma(close, length_20)

bb_dev = 2.0 * ta.stdev(close, length_20)

bb_upper = bb_basis + bb_dev

bb_lower = bb_basis - bb_dev

bb_position = bb_dev != 0 ? (close - bb_basis) / bb_dev : 0

bb_width = bb_dev != 0 ? (bb_upper - bb_lower) / bb_basis * 100 : 0

// 39. Keltner Channels Position

kc_basis = ta.ema(close, length_20)

kc_range = ta.ema(ta.tr, length_20)

kc_upper = kc_basis + (2.0 * kc_range)

kc_lower = kc_basis - (2.0 * kc_range)

kc_position = kc_range != 0 ? (close - kc_basis) / kc_range : 0

// 40. Donchian Channels Position

dc_upper = ta.highest(high, length_20)

dc_lower = ta.lowest(low, length_20)

dc_basis = (dc_upper + dc_lower) / 2

dc_position = (dc_upper - dc_lower) != 0 ? (close - dc_basis) / (dc_upper - dc_lower) : 0

// 41. Standard Deviation

std_dev = ta.stdev(close, length_20)

std_dev_pct = (std_dev / close) * 100

// 42. Relative Volatility Index (RVI)

rvi_up = ta.stdev(close > close ? close : 0, length_14)

rvi_down = ta.stdev(close < close ? close : 0, length_14)

rvi_total = rvi_up + rvi_down

rvi_volatility = rvi_total != 0 ? (rvi_up / rvi_total) * 100 : 50

// 43. Historical Volatility

hv_returns = math.log(close / close )

hv = ta.stdev(hv_returns, length_20) * math.sqrt(252) * 100

// 44. Garman-Klass Volatility

gk_vol = math.log(high/low) * math.log(high/low) - (2*math.log(2)-1) * math.log(close/open) * math.log(close/open)

gk_volatility = math.sqrt(ta.sma(gk_vol, length_20)) * 100

// 45. Parkinson Volatility

park_vol = math.log(high/low) * math.log(high/low)

parkinson = math.sqrt(ta.sma(park_vol, length_20) / (4 * math.log(2))) * 100

// 46. Rogers-Satchell Volatility

rs_vol = math.log(high/close) * math.log(high/open) + math.log(low/close) * math.log(low/open)

rogers_satchell = math.sqrt(ta.sma(rs_vol, length_20)) * 100

// |----- OSCILLATOR INDICATORS (5 indicators) -----| //

// 47. Elder Ray Index

elder_bull = high - ta.ema(close, 13)

elder_bear = low - ta.ema(close, 13)

elder_power = elder_bull + elder_bear

// 48. Schaff Trend Cycle (STC)

stc_macd = ta.ema(close, 23) - ta.ema(close, 50)

stc_k = ta.stoch(stc_macd, stc_macd, stc_macd, 10)

stc_d = ta.ema(stc_k, 3)

stc = ta.stoch(stc_d, stc_d, stc_d, 10)

// 49. Coppock Curve

coppock_roc1 = ta.roc(close, 14)

coppock_roc2 = ta.roc(close, 11)

coppock = ta.wma(coppock_roc1 + coppock_roc2, 10)

// 50. Know Sure Thing (KST)

kst_roc1 = ta.roc(close, 10)

kst_roc2 = ta.roc(close, 15)

kst_roc3 = ta.roc(close, 20)