HSM TOOLS//@version=5

indicator("HSM TOOLS", overlay=true, max_lines_count=500, max_labels_count=5, max_boxes_count=500)

// General Settings Inputs

TZI = input.string (defval="UTC -4", title="Timezone Selection", options= , tooltip="Select the Timezone. ( Shifts Chart Elements )", group="Global Settings")

Timezone = TZI == "UTC -10" ? "GMT-10:00" : TZI == "UTC -7" ? "GMT-07:00" : TZI == "UTC -6" ? "GMT-06:00" : TZI == "UTC -5" ? "GMT-05:00" : TZI == "UTC -4" ? "GMT-04:00" : TZI == "UTC -3" ? "GMT-03:00" : TZI == "UTC +0" ? "GMT+00:00" : TZI == "UTC +1" ? "GMT+01:00" : TZI == "UTC +2" ? "GMT+02:00" : TZI == "UTC +3" ? "GMT+03:00" : TZI == "UTC +3:30" ? "GMT+03:30" : TZI == "UTC +4" ? "GMT+04:00" : TZI == "UTC +5" ? "GMT+05:00" : TZI == "UTC +5:30" ? "GMT+05:30" : TZI == "UTC +6" ? "GMT+06:00" : TZI == "UTC +7" ? "GMT+07:00" : TZI == "UTC +8" ? "GMT+08:00" : TZI == "UTC +9" ? "GMT+09:00" : TZI == "UTC +9:30" ? "GMT+09:30" : TZI == "UTC +10" ? "GMT+10:00" : TZI == "UTC +10:30" ? "GMT+10:30" : TZI == "UTC +11" ? "GMT+11:00" : TZI == "UTC +13" ? "GMT+13:00" : "GMT+13:45"

inputMaxInterval = input.int (31, title="Hide Indicator Above Specified Minutes", tooltip="Above 30Min, Chart Will Become Messy & Unreadable", group="Global Settings")

// Session options

ShowTSO = input.bool (true, title="Show Today's Session Only", group="Session Options", tooltip="Hide Historical Sessions")

ShowTWO = input.bool (true, title="Show Current Week's Sessions Only", group="Session Options", tooltip="Show All Sessions from the current week")

SL4W = input.bool (true, title="Show Last 4 Week Sessions", group="Session Options", tooltip="Show All Sessions from Last Four Weeks \nShould Disable Current Week Session to Work")

ShowSFill = input.bool (false, title="Show Session Highlighting", group="Session Options", tooltip="Highlights Session from Top of the Chart to Bottom")

//----------------------------------------------

// Historical Lines

ShowMOPL = input.bool (title="Midnight Historical Price Lines", defval=false, group="Historical Lines", tooltip="Shows Historical Midnight Price Lines")

MOLHist = input.bool (title="Midnight Historical Vertical Lines", defval=true, group="Historical Lines", tooltip="Shows Historical Midnight Vertical Lines")

ShowPrev = input.bool (false, title="Misc. Historical Price Lines", group="Historical Lines", tooltip="Makes Chart Cluttered, Use For Backtesting Only")

//----------------------------------------------

// Session Bool

ShowLondon = input.bool (false, "", inline="LONDON", group="Sessions", tooltip="01:00 to 05:00")

ShowNY = input.bool (false, "", inline="NY", group="Sessions", tooltip="07:00 to 10:00")

ShowLC = input.bool (false, "", inline="LC", group="Sessions", tooltip="10:00 to 12:00")

ShowPM = input.bool (false, "",inline="PM", group="Sessions", tooltip="13:00 to 16:00")

ShowAsian = input.bool (false, "",inline="ASIA2", group="Sessions", tooltip="20:00 to 00:00")

ShowFreeSesh = input.bool (false, "",inline="FREE", group="Sessions", tooltip="Custom Session")

// Session Strings

txt2 = input.string ("LONDON", title="", inline="LONDON", group="Sessions")

txt3 = input.string ("NEW YORK", title="", inline="NY", group="Sessions")

txt4 = input.string ("LDN CLOSE", title="", inline="LC", group="Sessions")

txt5 = input.string ("AFTERNOON", title="", inline="PM", group="Sessions")

txt6 = input.string ("ASIA", title="", inline="ASIA2", group="Sessions")

txt9 = input.string ("FREE SESH", title="", inline="FREE", group="Sessions")

// CBDR = input.session ('1400-2000:1234567', "", inline="CBDR", group="Sessions")

// ASIA = input.session ('2000-0000:1234567', "", inline="ASIA", group="Sessions")

// Session Times

LDNsesh = input.session ('0200-0500:1234567', "", inline="LONDON", group="Sessions")

NYsesh = input.session ('0700-1000:1234567', "", inline="NY", group="Sessions")

LCsesh = input.session ('1000-1200:1234567', "", inline="LC", group="Sessions")

PMsesh = input.session ('1300-1600:1234567', "", inline="PM", group="Sessions")

ASIA2sesh = input.session ('2000-2359:1234567', "", inline="ASIA2", group="Sessions")

FreeSesh = input.session ('0000-0000:1234567', "", inline="FREE", group="Sessions")

// Session Color

LSFC = input.color (color.new(#787b86, 90), "", inline="LONDON", group="Sessions")

NYSFC = input.color (color.new(#787b86, 90), "",inline="NY", group="Sessions")

LCSFC = input.color (color.new(#787b86, 90), "",inline="LC", group="Sessions")

PMSFC = input.color (color.new(#787b86, 90), "",inline="PM", group="Sessions")

ASFC = input.color (color.new(#787b86, 90), "",inline="ASIA2", group="Sessions")

FSFC = input.color (color.new(#787b86, 90), "",inline="FREE", group="Sessions")

//----------------------------------------------

// Vertical Line Bool

ShowMOP = input.bool (title="", defval=true, inline="MOP", group="Vertical Lines", tooltip="00:00 AM")

txt12 = input.string ("MIDNIGHT", title="", inline="MOP", group="Vertical Lines")

ShowLOP = input.bool (title="", defval=false, inline="LOP", group="Vertical Lines", tooltip="03:00 AM")

txt14 = input.string ("LONDON", title="", inline="LOP", group="Vertical Lines")

ShowNYOP = input.bool (title="", defval=true, inline="NYOP", group="Vertical Lines", tooltip="08:30 AM")

txt15 = input.string ("NEW YORK", title="", inline="NYOP", group="Vertical Lines")

ShowEOP = input.bool (title="", defval=false, inline="EOP", group="Vertical Lines", tooltip="09:30 AM")

txt16 = input.string ("EQUITIES", title="", inline="EOP", group="Vertical Lines")

// Vertical Line Color

MOPColor = input.color (color.new(#787b86, 0), "", inline="MOP", group="Vertical Lines")

LOPColor = input.color (color.rgb(0,128,128,60), "", inline="LOP", group="Vertical Lines")

NYOPColor = input.color (color.rgb(0,128,128,60), "", inline="NYOP", group="Vertical Lines")

EOPColor = input.color (color.rgb(0,128,128,60), "", inline="EOP", group="Vertical Lines")

// Vertical LineStyle

Midnight_Open_LS = input.string ("Dotted", "", options= , inline="MOP", group="Vertical Lines")

london_Open_LS = input.string ("Solid", "", options= , inline="LOP", group="Vertical Lines")

NY_Open_LS = input.string ("Solid", "", options= , inline="NYOP", group="Vertical Lines")

Equities_Open_LS = input.string ("Solid", "", options= , inline="EOP", group="Vertical Lines")

// Vertical LineWidth

Midnight_Open_LW = input.string ("1px", "", options= , inline="MOP", group="Vertical Lines")

London_Open_LW = input.string ("1px", "", options= , inline="LOP", group="Vertical Lines")

NY_Open_LW = input.string ("1px", "", options= , inline="NYOP", group="Vertical Lines")

Equities_Open_LW = input.string ("1px", "", options= , inline="EOP", group="Vertical Lines")

//----------------------------------------------

// Opening Price Bool

ShowMOPP = input.bool (title="", defval=true, inline="MOPP", group="Opening Price Lines", tooltip="00:00 AM")

txt13 = input.string ("MIDNIGHT", title="", inline="MOPP", group="Opening Price Lines")

ShowNYOPP = input.bool (title="", defval=false, inline="NYOPP", group="Opening Price Lines", tooltip="08:30 AM")

txt17 = input.string ("NEW YORK", title="", inline="NYOPP", group="Opening Price Lines")

ShowEOPP = input.bool (title="", defval=false, inline="EOPP", group="Opening Price Lines", tooltip="09:30 AM")

txt18 = input.string ("EQUITIES", title="", inline="EOPP", group="Opening Price Lines")

ShowAFTPP = input.bool (title="", defval=false, inline="AFTOPP", group="Opening Price Lines", tooltip="01:30 PM")

txt1330 = input.string ("AFTERNOON", title="", inline="AFTOPP", group="Opening Price Lines")

// Opening Price Color

MOPColP = input.color (color.new(#787b86, 0), "", inline="MOPP", group="Opening Price Lines")

NYOPColP = input.color (color.new(#787b86, 0), "", inline="NYOPP", group="Opening Price Lines")

EOPColP = input.color (color.new(#787b86, 0), "", inline="EOPP", group="Opening Price Lines")

AFTOPColP = input.color (color.new(#787b86, 0), "", inline="AFTOPP", group="Opening Price Lines")

// Opening Price LineStyle

MOPLS = input.string ("Dotted", "", options= , inline="MOPP", group="Opening Price Lines")

NYOPLS = input.string ("Dotted", "", options= , inline="NYOPP", group="Opening Price Lines")

EOPLS = input.string ("Dotted", "", options= , inline="EOPP", group="Opening Price Lines")

AFTOPLS = input.string ("Dotted", "", options= , inline="AFTOPP", group="Opening Price Lines")

// Opening Price LineWidth

i_MOPLW = input.string ("1px", "", options= , inline="MOPP", group="Opening Price Lines")

i_NYOPLW = input.string ("1px", "", options= , inline="NYOPP", group="Opening Price Lines")

i_EOPLW = input.string ("1px", "", options= , inline="EOPP", group="Opening Price Lines")

i_AFTOPLW = input.string ("1px", "", options= , inline="AFTOPP", group="Opening Price Lines")

//----------------------------------------------

// W&M Bool

ShowWeekOpen = input.bool (defval=false, title="", tooltip="Draw Weekly Open Price Line", group="HTF Opening Price Lines", inline="WO")

showMonthOpen = input.bool (defval=false, title="", tooltip="Draw Monthly Open Price Line", group="HTF Opening Price Lines", inline="MO")

// W&M String

txt19 = input.string ("WEEKLY", title="", inline="WO", group="HTF Opening Price Lines")

txt20 = input.string ("MONTHLY", title="", inline="MO", group="HTF Opening Price Lines")

// W&M Color

i_WeekOpenCol = input.color (title="", defval=color.new(#787b86, 0), group="HTF Opening Price Lines", inline="WO")

i_MonthOpenCol = input.color (title="", tooltip="", defval=color.new(#787b86, 0), group="HTF Opening Price Lines", inline="MO")

// W&M LineStyle

WOLS = input.string ("Dotted", "", options= , inline="WO", group="HTF Opening Price Lines")

MOLS = input.string ("Dotted", "", options= , inline="MO", group="HTF Opening Price Lines")

// W&M LineWidth

i_WOPLW = input.string ("1px", "", options= , inline="WO", group="HTF Opening Price Lines")

i_MONPLW = input.string ("1px", "", options= , inline="MO", group="HTF Opening Price Lines")

//----------------------------------------------

// CBDR, ASIA & FLOUT

ShowCBDR = input.bool (true, "", inline='CBDR', group="CBDR, ASIA & FLOUT")

ShowASIA = input.bool (true, "", inline='ASIA', group="CBDR, ASIA & FLOUT")

ShowFLOUT = input.bool (false, "", inline='FLOUT', group="CBDR, ASIA & FLOUT")

// Strings

txt0 = input.string ("CBDR", title="", inline="CBDR", group="CBDR, ASIA & FLOUT", tooltip="16:00 to 20:00 \nSD Increments of 1")

txt1 = input.string ("ASIA", title="", inline="ASIA", group="CBDR, ASIA & FLOUT", tooltip="20:00 to 00:00 \nSD Increments of 1")

txt7 = input.string ("FLOUT", title="", inline="FLOUT", group="CBDR, ASIA & FLOUT", tooltip="16:00 to 00:00 \nSD Increments of 0.5")

// Color

CBDRBoxCol = input.color (color.new(#787b86, 0),"", inline='CBDR', group="CBDR, ASIA & FLOUT")

ASIABoxCol = input.color (color.new(#787b86, 0), "", inline='ASIA', group="CBDR, ASIA & FLOUT")

FLOUTBoxCol = input.color (color.new(#787b86, 0),"", inline='FLOUT', group="CBDR, ASIA & FLOUT")

// Extras

box_text_cbdr = input.bool (true, "Show Text", inline="CBDR", group="CBDR, ASIA & FLOUT")

box_text_cbdr_col = input.color (color.new(color.gray, 80), "", inline="CBDR", group="CBDR, ASIA & FLOUT")

bool_cbdr_dev = input.bool (true, "SD", inline="CBDR", group="CBDR, ASIA & FLOUT")

box_text_asia = input.bool (true, "Show Text", inline="ASIA", group="CBDR, ASIA & FLOUT")

box_text_asia_col = input.color (color.new(color.gray, 80), "", inline="ASIA", group="CBDR, ASIA & FLOUT")

bool_asia_dev = input.bool (true, "SD", inline="ASIA", group="CBDR, ASIA & FLOUT")

box_text_flout = input.bool (true, "Show Text", inline="FLOUT", group="CBDR, ASIA & FLOUT")

box_text_flout_col = input.color (color.new(color.gray, 80), "", inline="FLOUT", group="CBDR, ASIA & FLOUT")

bool_flout_dev = input.bool (true, "SD", inline="FLOUT", group="CBDR, ASIA & FLOUT")

// Table

// SD Lines

ShowDevLN = input.bool (title="", defval=true, inline="DEVLN", group="Standard Deviation", tooltip="Deviation Lines")

DEVLNTXT = input.string ("SD LINES", title="", inline="DEVLN", group="Standard Deviation")

DevLNCol = input.color (color.new(#787b86, 0), "", inline="DEVLN", group="Standard Deviation")

DEVLS = input.string ("Solid", "", options= , inline="DEVLN", group="Standard Deviation")

i_DEVLW = input.string ("1px", "", options= , inline="DEVLN", group="Standard Deviation")

DEVLSS = DEVLS=="Solid" ? line.style_solid : DEVLS == "Dotted" ? line.style_dotted : line.style_dashed

DEVLW = i_DEVLW=="1px" ? 1 : i_DEVLW == "2px" ? 2 : i_DEVLW == "3px" ? 3 : i_DEVLW == "4px" ? 4 : 5

ShowDev = input.bool (false, '', inline="DEV", group="Standard Deviation")

txt8 = input.string ("SD COUNT", title="", inline="DEV", group="Standard Deviation")

SDCountCol = input.color (color.new(#787b86, 0), "", inline="DEV", group="Standard Deviation")

DevInput = input.string ("2 SD", "", options= , inline="DEV", group="Standard Deviation")

DevDirection = input.string ("Both", "", options= , inline="DEV", group="Standard Deviation", tooltip="SD Count, NULL, SD Count, SD Direction")

DevCount = DevInput == "1 SD" ? 1 : DevInput == "2 SD" ? 2 : DevInput == "3 SD" ? 3 : 4

Auto_Select = input.bool (false, "", group="Standard Deviation", inline="AUTOSD", tooltip="Auto SD Selection | Charter Content, Range Table \nMight Bug Out On Mondays" )

txtSD = input.string ("AUTO SD", "", group="Standard Deviation", inline="AUTOSD")

Tab1txtCol = input.color (color.new(#808080, 0), "", inline='AUTOSD', group="Standard Deviation")

TabOptionShow = input.string ("Show Table", "", options= , inline="AUTOSD", group="Standard Deviation")

Stats = TabOptionShow == "Show Table" ? true : false

TabOption1 = input.string ("Top Right", "", options= , inline="AUTOSD", group="Standard Deviation")

tabinp1 = TabOption1 == "Top Left" ? position.top_left : TabOption1 == "Top Center" ? position.top_center : TabOption1 == "Top Right" ? position.top_right : TabOption1 == "Middle Left" ? position.middle_left : TabOption1 == "Middle Right" ? position.middle_right : TabOption1 == "Bottom Left" ? position.bottom_left : TabOption1 == "Bottom Center" ? position.bottom_center : position.bottom_right

L_Prof = true

CellBG = color.new(#131722, 100)

//----------------------------------------------

// Day Of Week & Labels

// Label Settings Inputs

ShowLabel = input.bool (true, title="", inline="Glabel", group="Day Of Week & Labels")

txt21 = input.string ("LABEL", title="", inline="Glabel", group="Day Of Week & Labels")

LabelColor = input.color (color.rgb(0,0,0,100), "", inline="Glabel", group="Day Of Week & Labels")

LabelSizeInput = input.string ("Normal", "", options= , inline="Glabel", group="Day Of Week & Labels")

Terminusinp = input.string ("Terminus @ Current Time +1hr", "", options = , inline="Glabel", group="Day Of Week & Labels", tooltip="Select Label Size & Color & Terminus \nHistorical Price Lines needs to be toggled off for using Terminus")

ShowLabelText = input.bool (true, title="", inline="label", group="Day Of Week & Labels")

txt22 = input.string ("LABEL TEXT", title="", inline="label", group="Day Of Week & Labels")

LabelTextColor = input.color (color.new(#787b86, 0), title="", inline="label", group="Day Of Week & Labels")

LabelTextOptioninput = input.string ("Time", "", options= , inline="label", group="Day Of Week & Labels", tooltip="Choose Between Descriptive Text as Label or Time \nShow/Hide Prices on Labels")

ShowPricesBool = input.string ("Hide Prices", title="", options= , group="Day Of Week & Labels", inline="label")

ShowPrices = ShowPricesBool == "Show Prices" ? true : false

showDOW = input.bool (true, title="", inline="DOW", group="Day Of Week & Labels")

txt24 = input.string ("DAY OF WEEK", title="", inline="DOW", group="Day Of Week & Labels")

i_DOWCol = input.color (color.new(#787b86, 0), title="", inline="DOW", group="Day Of Week & Labels")

DOWTime = input.int (defval = 12, title="", inline="DOW", group="Day Of Week & Labels")

DOWLoc_inpt = input.string ("Bottom", "", options = , inline="DOW", group="Day Of Week & Labels", tooltip="DOW Color, Time Alignment, Vertical Location")

DOWLoc = DOWLoc_inpt == "Bottom" ? location.bottom : location.top

//----------------------------------------------

BIAS_M_Bool = input.bool (false, "", group="BIAS & NOTES PRECONFIG", inline="stats")

txt100 = input.string ("BIAS", title="", inline="stats", group="BIAS & NOTES PRECONFIG")

TableBG2 = color.new(#131722, 100)

Tab2txtCol = input.color (color.new(#787b86, 0), "", inline='stats', group="BIAS & NOTES PRECONFIG")

TabOption2 = input.string ("Bottom Right", "", options= , inline="stats", group="BIAS & NOTES PRECONFIG")

tabinp2 = TabOption2 == "Top Left" ? position.top_left : TabOption2 == "Top Center" ? position.top_center : TabOption2 == "Top Right" ? position.top_right : TabOption2 == "Middle Left" ? position.middle_left : TabOption2 == "Middle Right" ? position.middle_right : TabOption2 == "Bottom Left" ? position.bottom_left : TabOption2 == "Bottom Center" ? position.bottom_center : position.bottom_right

notesbool = false

NOTES_M_Bool = input.bool (true, "", group="BIAS & NOTES PRECONFIG", inline="stats2")

txt101 = input.string ("NOTES", title="", inline="stats2", group="BIAS & NOTES PRECONFIG")

Tab3txtCol = input.color (color.new(#787b86, 0), "", inline='stats2', group="BIAS & NOTES PRECONFIG")

TabOption3 = input.string ("Top Center", "", options= , inline="stats2", group="BIAS & NOTES PRECONFIG")

tabinp3 = TabOption3 == "Top Left" ? position.top_left : TabOption3 == "Top Center" ? position.top_center : TabOption3 == "Top Right" ? position.top_right : TabOption3 == "Middle Left" ? position.middle_left : TabOption3 == "Middle Right" ? position.middle_right : TabOption3 == "Bottom Left" ? position.bottom_left : TabOption3 == "Bottom Center" ? position.bottom_center : position.bottom_right

BIASbool1 = input.bool (true, '', inline="BIAS1", group="BIAS & NOTES")

txt52 = input.string ("DXY ", title="", inline="BIAS1", group="BIAS & NOTES")

BIASOption1 = input.string ("Unclear", options= , title="", inline="BIAS1", group="BIAS & NOTES")

BIASbool2 = input.bool (true, '', inline="BIAS2", group="BIAS & NOTES")

txt53 = input.string ("SPX ", title="", inline="BIAS2", group="BIAS & NOTES")

BIASOption2 = input.string ("Unclear", options= , title="", inline="BIAS2", group="BIAS & NOTES")

BIASbool3 = input.bool (true, '', inline="BIAS3", group="BIAS & NOTES")

txt54 = input.string ("DOW ", title="", inline="BIAS3", group="BIAS & NOTES")

BIASOption3 = input.string ("Unclear", options= , title="", inline="BIAS3", group="BIAS & NOTES")

BIASbool4 = input.bool (true, '', inline="BIAS4", group="BIAS & NOTES")

txt55 = input.string ("NAS ", title="", inline="BIAS4", group="BIAS & NOTES")

BIASOption4 = input.string ("Unclear", options= , title="", inline="BIAS4", group="BIAS & NOTES")

notes = input.text_area ("@hiran.invest", "Notes", group = "BIAS & NOTES")

//--------------------END OF INPUTS--------------------//

// Pre-Def

DOM = (timeframe.multiplier <= inputMaxInterval) and (timeframe.isintraday)

newDay = ta.change(dayofweek)

newWeek = ta.change(weekofyear)

newMonth = ta.change(time("M"))

transparentcol = color.rgb(255,255,255,100)

LSVLC = color.rgb(255,255,255,100)

NYSVLC = color.rgb(255,255,255,100)

PMSVLC = color.rgb(255,255,255,100)

ASVLC = color.rgb(255,255,255,100)

LSVLS = "dotted"

NYSVLS = "dotted"

PMSVLS = "dotted"

ASVLS = "dotted"

// Functions

isToday = false

if year(timenow) == year(time) and month(timenow) == month(time) and dayofmonth(timenow) == dayofmonth(time)

isToday := true

// Current Week

thisweek = year(timenow) == year(time) and weekofyear(timenow) == weekofyear(time)

LastOneWeek = year(timenow) == year(time) and weekofyear(timenow-604800000) == weekofyear(time)

LastTwoWeek = year(timenow) == year(time) and weekofyear(timenow-1209600000) == weekofyear(time)

LastThreeWeek = year(timenow) == year(time) and weekofyear(timenow-1814400000) == weekofyear(time)

LastFourWeek = year(timenow) == year(time) and weekofyear(timenow-2419200000) == weekofyear(time)

Last4Weeks = false

if thisweek == true or LastOneWeek == true or LastTwoWeek == true or LastThreeWeek == true or LastFourWeek == true

Last4Weeks := true

// Function to draw Vertical Lines

vline(Start, Color, linestyle, LineWidth) =>

line.new(x1=Start, y1=low - ta.tr, x2=Start, y2=high + ta.tr, xloc=xloc.bar_time, extend=extend.both, color=Color, style=linestyle, width=LineWidth)

// Function to convert forex pips into whole numbers

atr = ta.atr(14)

toWhole(number) =>

if syminfo.type == "forex" // This method only works on forex pairs

_return = atr < 1.0 ? (number / syminfo.mintick) / 10 : number

_return := atr >= 1.0 and atr < 100.0 and syminfo.currency == "JPY" ? _return * 100 : _return

else

number

// Function for determining the Start of a Session (taken from the Pinescript manual: www.tradingview.com )

SessionBegins(sess) =>

t = time("", sess , Timezone)

DOM and (not barstate.isfirst) and na(t ) and not na(t)

// BarIn Session

BarInSession(sess) =>

time(timeframe.period, sess, Timezone) != 0

// Label Type Logic

var SFistrue = true

if LabelTextOptioninput == "Time"

SFistrue := true

else

SFistrue := false

// Session String to int

SeshStartHour(Session) =>

math.round(str.tonumber(str.substring(Session,0,2)))

SeshStartMins(Session) =>

math.round(str.tonumber(str.substring(Session,2,4)))

SeshEndHour(Session) =>

math.round(str.tonumber(str.substring(Session,5,7)))

SeshEndMins(Session) =>

math.round(str.tonumber(str.substring(Session,7,9)))

// Time periods

CBDR = "1600-2000:1234567"

ASIA = "2000-0000:1234567"

FLOUT = "1600-0000:1234567"

midsesh = "0000-1600:1234567"

cbdrOpenTime = timestamp (Timezone, year, month, dayofmonth, SeshStartHour(CBDR), SeshStartMins(CBDR), 00)

cbdrEndTime = timestamp (Timezone, year, month, dayofmonth, SeshEndHour(CBDR), SeshEndMins(CBDR), 00)

asiaOpenTime = timestamp (Timezone, year, month, dayofmonth, SeshStartHour(ASIA), SeshStartMins(ASIA), 00)

asiaEndTime = timestamp (Timezone, year, month, dayofmonth, SeshEndHour(ASIA), SeshEndMins(ASIA), 00)+86400000

floutOpenTime = timestamp (Timezone, year, month, dayofmonth, SeshStartHour(FLOUT), SeshStartMins(FLOUT), 00)

floutEndTime = timestamp (Timezone, year, month, dayofmonth, SeshEndHour(FLOUT), SeshEndMins(FLOUT), 00)+86400000

CBDRTime = time (timeframe.period, CBDR, Timezone)

ASIATime = time (timeframe.period, ASIA, Timezone)

FLOUTTime = time (timeframe.period, FLOUT, Timezone)

LabelOnlyToday = true

// Time Periods

LondonStartTime = timestamp(Timezone, year, month, dayofmonth, SeshStartHour(LDNsesh), SeshStartMins(LDNsesh), 00)

LondonEndTime = timestamp(Timezone, year, month, dayofmonth, SeshEndHour(LDNsesh), SeshEndMins(LDNsesh), 00)

NYStartTime = timestamp(Timezone, year, month, dayofmonth, SeshStartHour(NYsesh), SeshStartMins(NYsesh), 00)

NYEndTime = timestamp(Timezone, year, month, dayofmonth, SeshEndHour(NYsesh), SeshEndMins(NYsesh), 00)

LCStartTime = timestamp(Timezone, year, month, dayofmonth, SeshStartHour(LCsesh), SeshStartMins(LCsesh), 00)

LCEndTime = timestamp(Timezone, year, month, dayofmonth, SeshEndHour(LCsesh), SeshEndMins(LCsesh), 00)

PMStartTime = timestamp(Timezone, year, month, dayofmonth, SeshStartHour(PMsesh), SeshStartMins(PMsesh), 00)

PMEndTime = timestamp(Timezone, year, month, dayofmonth, SeshEndHour(PMsesh), SeshEndMins(PMsesh), 00)

AsianStartTime = timestamp(Timezone, year, month, dayofmonth, SeshStartHour(ASIA2sesh), SeshStartMins(ASIA2sesh), 00)

AsianEndTime = timestamp(Timezone, year, month, dayofmonth, SeshEndHour(ASIA2sesh), SeshEndMins(ASIA2sesh), 00)

FreeStartTime = timestamp(Timezone, year, month, dayofmonth, SeshStartHour(FreeSesh), SeshStartMins(FreeSesh), 00)

FreeEndTime = timestamp(Timezone, year, month, dayofmonth, SeshEndHour(FreeSesh), SeshEndMins(FreeSesh), 00)

MidnightOpenTime = timestamp(Timezone, year, month, dayofmonth, 0, 0, 00)

CLEANUPTIME = timestamp(Timezone, year, month, dayofmonth, 0, 0, 00) - 16200000

LondonOpenTime = timestamp(Timezone, year, month, dayofmonth, 3, 0, 00)

NYOpenTime = timestamp(Timezone, year, month, dayofmonth, 8, 30, 00)

EquitiesOpenTime = timestamp(Timezone, year, month, dayofmonth, 9, 30, 00)

AfternoonOpenTime = timestamp(Timezone, year, month, dayofmonth, 13, 30, 00)

tMidnight = time("1", "0000-0001:1234567", Timezone)

// Cleanup - Remove old drawing objects

Cleanup(days) =>

// Delete old drawing objects

// One day is 86400000 milliseconds

removal_timestamp = (CLEANUPTIME) - (days * 86400000) // Remove every drawing object older than the start of the Today's Midnight

a_allLines = line.all

a_allLabels = label.all

a_allboxes = box.all

// Remove old lines

if array.size(a_allLines) > 0

for i = 0 to array.size(a_allLines) - 1

line_x2 = line.get_x2(array.get(a_allLines, i))

if line_x2 < (removal_timestamp)

line.delete(array.get(a_allLines, i))

// Remove old labels

if array.size(a_allLabels) > 0

for i = 0 to array.size(a_allLabels) - 1

label_x = label.get_x(array.get(a_allLabels, i))

if label_x < removal_timestamp

label.delete(array.get(a_allLabels, i))

// Remove old boxes

if array.size(a_allboxes) > 0

for i = 0 to array.size(a_allboxes) - 1

box_x = box.get_right(array.get(a_allboxes, i))

if box_x < (removal_timestamp - 86400000)

box.delete(array.get(a_allboxes, i))

// End of Cleanup function

// Terminus Function

Terminus(Terminus_Inp)=>

if Terminus_Inp == "Terminus @ Current Time"

_return = timenow

else if Terminus_Inp == "Terminus @ Current Time +15min"

_return = timenow + 900000

else if Terminus_Inp == "Terminus @ Current Time +30min"

_return = timenow + 1800000

else if Terminus_Inp == "Terminus @ Current Time +45min"

_return = timenow + 2700000

else if Terminus_Inp == "Terminus @ Current Time +1hr"

_return = timenow + 3600000

else if Terminus_Inp == "Terminus @ Current Time +2hr"

_return = timenow + 7200000

else

_return = timenow + 10800000

// Linestyle Function

MNOPLS = Midnight_Open_LS=="Solid" ? line.style_solid : Midnight_Open_LS == "Dotted" ? line.style_dotted : line.style_dashed

LNOPLS = london_Open_LS=="Solid" ? line.style_solid : london_Open_LS == "Dotted" ? line.style_dotted : line.style_dashed

NWYOPLS = NY_Open_LS=="Solid" ? line.style_solid : NY_Open_LS == "Dotted" ? line.style_dotted : line.style_dashed

EQOPLS = Equities_Open_LS=="Solid" ? line.style_solid : Equities_Open_LS == "Dotted" ? line.style_dotted : line.style_dashed

MOPLSS = MOPLS=="Solid" ? line.style_solid : MOPLS == "Dotted" ? line.style_dotted : line.style_dashed

NYOPLSS = NYOPLS=="Solid" ? line.style_solid : NYOPLS == "Dotted" ? line.style_dotted : line.style_dashed

EOPLSS = EOPLS=="Solid" ? line.style_solid : EOPLS == "Dotted" ? line.style_dotted : line.style_dashed

AFTOPLSS = AFTOPLS=="Solid" ? line.style_solid : AFTOPLS == "Dotted" ? line.style_dotted : line.style_dashed

WeekOpenLS = WOLS=="Solid" ? line.style_solid : WOLS == "Dotted" ? line.style_dotted : line.style_dashed

MonthOpenLS = MOLS=="Solid" ? line.style_solid : MOLS == "Dotted" ? line.style_dotted : line.style_dashed

// Linewidth Function

MOPLW = Midnight_Open_LW=="1px" ? 1 : Midnight_Open_LW == "2px" ? 2 : Midnight_Open_LW == "3px" ? 3 : Midnight_Open_LW == "4px" ? 4 : 5

LOPLW = London_Open_LW=="1px" ? 1 : London_Open_LW == "2px" ? 2 : London_Open_LW == "3px" ? 3 : London_Open_LW == "4px" ? 4 : 5

NYOPLW = NY_Open_LW=="1px" ? 1 : NY_Open_LW == "2px" ? 2 : NY_Open_LW == "3px" ? 3 : NY_Open_LW == "4px" ? 4 : 5

EOPLW = Equities_Open_LW=="1px" ? 1 : Equities_Open_LW == "2px" ? 2 : Equities_Open_LW == "3px" ? 3 : Equities_Open_LW == "4px" ? 4 : 5

MOPPLW = i_MOPLW=="1px" ? 1 : i_MOPLW == "2px" ? 2 : i_MOPLW == "3px" ? 3 : i_MOPLW == "4px" ? 4 : 5

NYOPPLW = i_NYOPLW=="1px" ? 1 : i_NYOPLW == "2px" ? 2 : i_NYOPLW == "3px" ? 3 : i_NYOPLW == "4px" ? 4 : 5

EOPPLW = i_EOPLW=="1px" ? 1 : i_EOPLW == "2px" ? 2 : i_EOPLW == "3px" ? 3 : i_EOPLW == "4px" ? 4 : 5

AFTOPLW = i_AFTOPLW=="1px" ? 1 : i_AFTOPLW == "2px" ? 2 : i_AFTOPLW == "3px" ? 3 : i_AFTOPLW == "4px" ? 4 : 5

WEEKOPPLW = i_WOPLW=="1px" ? 1 : i_WOPLW == "2px" ? 2 : i_WOPLW == "3px" ? 3 : i_WOPLW == "4px" ? 4 : 5

MONTHOPPLW = i_MONPLW=="1px" ? 1 : i_MONPLW == "2px" ? 2 : i_MONPLW == "3px" ? 3 : i_MONPLW == "4px" ? 4 : 5

// Label Size Function

LabelSize =LabelSizeInput=="Auto" ? size.auto : LabelSizeInput=="Tiny" ? size.tiny : LabelSizeInput=="Small" ? size.small : LabelSizeInput=="Normal" ? size.normal : LabelSizeInput=="Large" ? size.large : size.huge

// Creating Variables

var London_Start_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=LSVLC, width=1)

var London_End_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=LSVLC, width=1)

var LondonFill = linefill.new(London_Start_Vline, London_End_Vline, LSFC)

var NY_Start_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=NYSVLC, width=1)

var NY_End_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=NYSVLC, width=1)

var NYFill = linefill.new(NY_Start_Vline, NY_End_Vline, NYSFC)

var LC_Start_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=NYSVLC, width=1)

var LC_End_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=NYSVLC, width=1)

var LCFill = linefill.new(LC_Start_Vline, LC_End_Vline, LCSFC)

var PM_Start_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=PMSVLC, width=1)

var PM_End_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=PMSVLC, width=1)

var PMFill = linefill.new(PM_Start_Vline, PM_End_Vline, PMSFC)

var Asian_Start_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=ASVLC, width=1)

var Asian_End_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=ASVLC, width=1)

var AsianFill = linefill.new(Asian_Start_Vline, Asian_End_Vline, ASFC)

var Free_Start_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=ASVLC, width=1)

var Free_End_Vline = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=ASVLC, width=1)

var FreeFill = linefill.new(Free_Start_Vline, Free_End_Vline, FSFC)

var Midnight_Open = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=MOPColor, width=1)

var London_Open = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=LOPColor, width=1)

var NY_Open = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=NYOPColor, width=1)

var Equities_Open = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=EOPColor, width=1)

// When a New Day Starts, Start Drawing all lines

if newDay and dayofweek != dayofweek.sunday

// London Session

if (ShowLondon and DOM)

if ShowTSO

line.delete(London_Start_Vline )

line.delete(London_End_Vline )

linefill.delete(LondonFill )

London_Start_Vline := vline(LondonStartTime,transparentcol, line.style_solid, 1)

London_End_Vline := vline(LondonEndTime, transparentcol, line.style_solid, 1)

if ShowSFill

LondonFill := linefill.new(London_Start_Vline, London_End_Vline, LSFC)

// New York Session

if (ShowNY and DOM)

if ShowTSO

line.delete(NY_Start_Vline )

line.delete(NY_End_Vline )

linefill.delete(NYFill )

NY_Start_Vline := vline(NYStartTime, transparentcol, line.style_solid, 1)

NY_End_Vline := vline(NYEndTime, transparentcol, line.style_solid, 1)

if ShowSFill

NYFill := linefill.new(NY_Start_Vline, NY_End_Vline, NYSFC)

// London Close

if (ShowLC and DOM)

if ShowTSO

line.delete(LC_End_Vline )

linefill.delete(LCFill )

LC_Start_Vline := vline(LCStartTime, transparentcol, line.style_solid, 1)

LC_End_Vline := vline(LCEndTime, transparentcol, line.style_solid, 1)

if ShowSFill

LCFill := linefill.new(LC_Start_Vline, LC_End_Vline, LCSFC)

// PM Session

if (ShowPM and DOM)

if ShowTSO

line.delete(PM_Start_Vline )

line.delete(PM_End_Vline )

linefill.delete(PMFill )

PM_Start_Vline := vline(PMStartTime, transparentcol, line.style_solid, 1)

PM_End_Vline := vline(PMEndTime, transparentcol, line.style_solid, 1)

if ShowSFill

PMFill := linefill.new(PM_Start_Vline, PM_End_Vline, PMSFC)

// Asian Session

if (ShowAsian and DOM)

if ShowTSO

line.delete(Asian_Start_Vline )

line.delete(Asian_End_Vline )

linefill.delete(AsianFill )

Asian_Start_Vline := vline(AsianStartTime, transparentcol, line.style_solid, 1)

Asian_End_Vline := vline(AsianEndTime, transparentcol, line.style_solid, 1)

// if dayofweek == dayofweek.friday

// // line.delete(Asian_Start_Vline)

// // line.delete(Asian_End_Vline)

// Asian_Start_Vline := vline(MidnightOpenTime+244800000, transparentcol, line.style_solid, 1)

// Asian_End_Vline := vline(MidnightOpenTime+259200000, transparentcol, line.style_solid, 1)

if ShowSFill

AsianFill := linefill.new(Asian_Start_Vline, Asian_End_Vline, ASFC)

// Free Session

if (ShowFreeSesh and DOM)

if ShowTSO

line.delete(Free_Start_Vline )

line.delete(Free_End_Vline )

linefill.delete(FreeFill )

Free_Start_Vline := vline(FreeStartTime, transparentcol, line.style_solid, 1)

Free_End_Vline := vline(FreeEndTime, transparentcol, line.style_solid, 1)

if ShowSFill

FreeFill := linefill.new(Free_Start_Vline, Free_End_Vline, FSFC)

// Midnight Opening Price

if (ShowMOP and DOM)

if MOLHist == false

line.delete(Midnight_Open )

Midnight_Open := vline(MidnightOpenTime, MOPColor, MNOPLS, MOPLW)

// London Opening Price

if (ShowLOP and DOM)

if ShowTSO

line.delete(London_Open )

London_Open := vline(LondonOpenTime, LOPColor, LNOPLS, LOPLW)

// New York Opening Price

if (ShowNYOP and DOM)

if ShowTSO

line.delete(NY_Open )

NY_Open := vline(NYOpenTime, NYOPColor, NWYOPLS, NYOPLW)

// Equities Opening Price

if (ShowEOP and DOM)

if ShowTSO

line.delete(Equities_Open )

Equities_Open := vline(EquitiesOpenTime, EOPColor, EQOPLS, EOPLW)

// Variables

var label MOPLB = na

var line MOPLN = na

var label NYOPLB = na

var line NYOPLN = na

var label EOPLB = na

var line EOPLN = na

var line AFTLN = na

var label AFTLB = na

// New York Midnight Open Price line

var openMidnight = 0.0

if tMidnight

if not tMidnight

openMidnight := open

else

openMidnight := math.max(open, openMidnight)

if (ShowMOPP and (openMidnight != openMidnight ) and DOM and barstate.isconfirmed)

label.delete(MOPLB )

if ShowMOPL == false

line.delete(MOPLN )

MOPLN := line.new(x1=tMidnight, y1=openMidnight, x2=tMidnight+86400000, xloc=xloc.bar_time, y2=openMidnight, color=MOPColP, style=MOPLSS, width=MOPPLW)

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

line.set_x2(MOPLN, tMidnight+259200000)

if ShowLabel

MOPLB := label.new(x=tMidnight+86400000, y=openMidnight, xloc=xloc.bar_time, color=LabelColor, textcolor=MOPColP, style=label.style_label_left, size=LabelSize, tooltip="Midnight Opening Price")

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

label.set_x(MOPLB, tMidnight+259200000)

if ShowLabelText

if SFistrue

if ShowPrices == true

label.set_text(MOPLB, " 00:00 | " + str.tostring(open))

else

label.set_text(MOPLB, " 00:00 ")

label.set_tooltip(MOPLB, "Midnight Opening Price")

else

if ShowPrices == true

label.set_text(MOPLB, " Midnight Opening Price | " + str.tostring(open))

else

label.set_text(MOPLB, " Midnight Opening Price ")

label.set_tooltip(MOPLB, "")

label.set_textcolor(MOPLB, LabelTextColor)

label.set_size(MOPLB,LabelSize)

if time > PMEndTime and time < (MidnightOpenTime + 86400000)

line.delete(MOPLN )

if Terminusinp != "Terminus @ Next Midnight" and ShowMOPL == false

line.set_x2(MOPLN, Terminus(Terminusinp))

label.set_x(MOPLB, Terminus(Terminusinp))

// New York Opening Price Line

if (ShowNYOPP and (time == NYOpenTime) and DOM)

label.delete(NYOPLB )

if ShowPrev == false

line.delete(NYOPLN )

NYOPLN := line.new(x1=NYOpenTime, y1=open, x2=NYOpenTime+55800000, xloc=xloc.bar_time, y2=open, color=NYOPColP, style=NYOPLSS, width=NYOPPLW)

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

line.set_x2(NYOPLN, NYOpenTime+228600000)

if ShowLabel

NYOPLB := label.new(x=NYOpenTime+55800000, y=open, xloc=xloc.bar_time, color=LabelColor, textcolor=NYOPColP, style=label.style_label_left, size=LabelSize, tooltip="New York Opening Price")

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

label.set_x(NYOPLB, NYOpenTime+228600000)

if ShowLabelText

if SFistrue

if ShowPrices == true

label.set_text(NYOPLB, " 08:30 | " + str.tostring(open))

else

label.set_text(NYOPLB, " 08:30 ")

label.set_tooltip(NYOPLB, "New York Opening Price")

else

if ShowPrices == true

label.set_text(NYOPLB, " New York Opening Price | " + str.tostring(open))

else

label.set_text(NYOPLB, " New York Opening Price ")

label.set_tooltip(NYOPLB, "")

label.set_textcolor(NYOPLB, LabelTextColor)

label.set_size(NYOPLB,LabelSize)

if Terminusinp != "Terminus @ Next Midnight" and ShowPrev == false

line.set_x2(NYOPLN, Terminus(Terminusinp))

label.set_x(NYOPLB, Terminus(Terminusinp))

// Equities Opening Price Line

if (ShowEOPP and (time == EquitiesOpenTime) and DOM)

label.delete(EOPLB )

if ShowPrev == false

line.delete(EOPLN )

EOPLN := line.new(x1=EquitiesOpenTime, y1=open, x2=EquitiesOpenTime+52200000, xloc=xloc.bar_time, y2=open, color=EOPColP, style=EOPLSS, width=EOPPLW)

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

line.set_x2(EOPLN, EquitiesOpenTime+225000000)

if ShowLabel

EOPLB := label.new(x=EquitiesOpenTime+52200000, y=open, xloc=xloc.bar_time, color=LabelColor, textcolor=EOPColP, style=label.style_label_left, size=LabelSize, tooltip="Equities Opening Price")

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

label.set_x(EOPLB, EquitiesOpenTime+225000000)

if ShowLabelText

if SFistrue

if ShowPrices == true

label.set_text(EOPLB, " 09:30 | " + str.tostring(open))

else

label.set_text(EOPLB, " 09:30 ")

label.set_tooltip(EOPLB, "Equities Opening Price")

else

if ShowPrices == true

label.set_text(EOPLB, " Equities Opening Price | " + str.tostring(open))

else

label.set_text(EOPLB, " Equities Opening Price ")

label.set_tooltip(EOPLB, "")

label.set_textcolor(EOPLB, LabelTextColor)

label.set_size(EOPLB,LabelSize)

if Terminusinp != "Terminus @ Next Midnight" and ShowPrev == false

line.set_x2(EOPLN, Terminus(Terminusinp))

label.set_x(EOPLB, Terminus(Terminusinp))

// Afternoon Opening Price Line

if (ShowAFTPP and (time == AfternoonOpenTime) and DOM)

label.delete(AFTLB )

if ShowPrev == false

line.delete(AFTLN )

AFTLN := line.new(x1=AfternoonOpenTime, y1=open, x2=EquitiesOpenTime+52200000, xloc=xloc.bar_time, y2=open, color=AFTOPColP, style=AFTOPLSS, width=AFTOPLW)

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

line.set_x2(AFTLN, EquitiesOpenTime+225000000)

if ShowLabel

AFTLB := label.new(x=EquitiesOpenTime+52200000, y=open, xloc=xloc.bar_time, color=LabelColor, textcolor=AFTOPColP, style=label.style_label_left, size=LabelSize, tooltip="Equities Opening Price")

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

label.set_x(AFTLB, EquitiesOpenTime+225000000)

if ShowLabelText

if SFistrue

if ShowPrices == true

label.set_text(AFTLB, " 01:30 | " + str.tostring(open))

else

label.set_text(AFTLB, " 01:30 ")

label.set_tooltip(AFTLB, " Afternoon Opening Price")

else

if ShowPrices == true

label.set_text(AFTLB, " Afternoon Opening Price | " + str.tostring(open))

else

label.set_text(AFTLB, " Afternoon Opening Price ")

label.set_tooltip(AFTLB, "")

label.set_textcolor(AFTLB, LabelTextColor)

label.set_size(AFTLB,LabelSize)

if Terminusinp != "Terminus @ Next Midnight" and ShowPrev == false

line.set_x2(AFTLN, Terminus(Terminusinp))

label.set_x(AFTLB, Terminus(Terminusinp))

// HTF Variables

var Weekly_open = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=i_WeekOpenCol, style=WeekOpenLS, width=1)

var Weekly_openlbl = label.new(x=na, y=na, xloc=xloc.bar_time, color=LabelColor, textcolor=LabelTextColor, style=label.style_label_left, size=LabelSize)

var WeeklyOpenTime = time

var Monthly_open = line.new(x1=na, y1=na, x2=na, xloc=xloc.bar_time, y2=close, color=i_MonthOpenCol, style=MonthOpenLS, width=1)

var Monthly_openlbl = label.new(x=na, y=na, xloc=xloc.bar_time, color=LabelColor, textcolor=LabelTextColor, style=label.style_label_left, size=LabelSize)

var MonthlyOpenTime = time

// Get HTF Price levels

WeeklyOpen = request.security(syminfo.tickerid, "W", open, lookahead = barmerge.lookahead_on)

MonthlyOpen = request.security(syminfo.tickerid, "M", open, lookahead = barmerge.lookahead_on)

// Weekly Open

if newWeek

WeeklyOpenTime := time

if ShowWeekOpen and newDay and Last4Weeks

label.delete(Weekly_openlbl )

line.delete(Weekly_open )

// if ShowPrev == false

// line.delete(Weekly_open )

Weekly_open:= line.new(x1=WeeklyOpenTime-25200000, y1=WeeklyOpen, x2=EquitiesOpenTime+52200000, xloc=xloc.bar_time, y2=WeeklyOpen, color=i_WeekOpenCol, style=WeekOpenLS, width=WEEKOPPLW)

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

line.set_x2(Weekly_open, EquitiesOpenTime+225000000)

if ShowLabel

Weekly_openlbl := label.new(x=EquitiesOpenTime+52200000, y=WeeklyOpen, xloc=xloc.bar_time, color=LabelColor, textcolor=LabelTextColor, style=label.style_label_left, size=LabelSize, tooltip="Weekly Open: " + str.tostring(WeeklyOpen))

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

label.set_x(Weekly_openlbl, EquitiesOpenTime+225000000)

if ShowLabelText

if SFistrue

if ShowPrices == true

label.set_text(Weekly_openlbl," W.O. | " + str.tostring(WeeklyOpen))

else

label.set_text(Weekly_openlbl," W.O. ")

label.set_tooltip(Weekly_openlbl, " Weekly Opening Price ")

else

if ShowPrices == true

label.set_text(Weekly_openlbl," Weekly Open | " + str.tostring(WeeklyOpen))

else

label.set_text(Weekly_openlbl," Weekly Open ")

label.set_tooltip(Weekly_openlbl, "")

label.set_textcolor(Weekly_openlbl, LabelTextColor)

label.set_size(Weekly_openlbl, LabelSize)

if timeframe.multiplier > 60

line.set_x2(Weekly_open, AsianEndTime + 232000000)

label.set_x(Weekly_openlbl, AsianEndTime + 232000000)

if timeframe.period == "D"

line.set_x2(Weekly_open, AsianEndTime + 832000000)

label.set_x(Weekly_openlbl, AsianEndTime + 832000000)

if timeframe.period == "M"

line.delete(Weekly_open)

label.delete(Weekly_openlbl)

if Terminusinp != "Terminus @ Next Midnight" and DOM

line.set_x2(Weekly_open, Terminus(Terminusinp))

label.set_x(Weekly_openlbl, Terminus(Terminusinp))

// Monthly Open

if newMonth

MonthlyOpenTime := time

if showMonthOpen and newDay

line.delete(Monthly_open )

label.delete(Monthly_openlbl )

Monthly_open:= line.new(x1=MonthlyOpenTime, y1=MonthlyOpen, x2=AsianEndTime, xloc=xloc.bar_time, y2=MonthlyOpen, color=i_MonthOpenCol, style=MonthOpenLS, width=MONTHOPPLW)

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

line.set_x2(Monthly_open, EquitiesOpenTime+225000000)

if ShowLabel

Monthly_openlbl := label.new(x=AsianEndTime, y=MonthlyOpen, xloc=xloc.bar_time, color=LabelColor, textcolor=LabelTextColor, style=label.style_label_left, size=LabelSize, tooltip="Monthly Open: " + str.tostring(MonthlyOpen))

if dayofweek == dayofweek.friday and syminfo.type != "crypto"

label.set_x(Monthly_openlbl, EquitiesOpenTime+225000000)

if ShowLabelText

if SFistrue

if ShowPrices == true

label.set_text(Monthly_openlbl," M.O. | " + str.tostring(MonthlyOpen))

else

label.set_text(Monthly_openlbl," M.O. ")

label.set_tooltip(Monthly_openlbl, " Monthly Opening Price ")

else

if ShowPrices == true

label.set_text(Monthly_openlbl, " Monthly Open | " + str.tostring(MonthlyOpen))

else

label.set_text(Monthly_openlbl, " Monthly Open ")

label.set_tooltip(Monthly_openlbl, "")

label.set_textcolor(Monthly_openlbl, LabelTextColor)

label.set_size(Monthly_openlbl, LabelSize)

if timeframe.multiplier > 60

line.set_x2(Monthly_open, AsianEndTime + 232000000)

label.set_x(Monthly_openlbl, AsianEndTime + 232000000)

if timeframe.period == "D"

line.set_x2(Monthly_open, AsianEndTime + 832000000)

label.set_x(Monthly_openlbl, AsianEndTime + 832000000)

if timeframe.period == "W"

line.set_x2(Monthly_open, AsianEndTime + 2592000000)

label.set_x(Monthly_openlbl, AsianEndTime + 2592000000)

if timeframe.period == "M"

line.delete(Monthly_open)

label.delete(Monthly_openlbl)

if Terminusinp != "Terminus @ Next Midnight" and DOM

line.set_x2(Monthly_open, Terminus(Terminusinp))

label.set_x(Monthly_openlbl, Terminus(Terminusinp))

// CBDR Stuff

var float cbdr_hi = na

var float cbdr_lo = na

var float cbdr_diff = na

var box cbdrbox = na

var line cbdr_hi_line = na

var line cbdr_lo_line = na

var line dev01negline = na

var line dev02negline = na

var line dev03negline = na

var line dev04negline = na

var line dev01posline = na

var line dev02posline = na

var line dev03posline = na

var line dev04posline = na

if SessionBegins(CBDR) and DOM

cbdr_hi := high

cbdr_lo := low

cbdr_diff := cbdr_hi - cbdr_lo

if ShowTSO

box.delete(cbdrbox )

line.delete(dev01posline )

line.delete(dev01negline )

line.delete(dev02posline )

line.delete(dev02negline )

line.delete(dev03posline )

line.delete(dev03negline )

line.delete(dev04posline )

line.delete(dev04negline )

if ShowCBDR

cbdrbox := box.new(cbdrOpenTime, cbdr_hi, cbdrEndTime, cbdr_lo, color.new(CBDRBoxCol,90), 1, line.style_solid, extend.none, xloc.bar_time, color.new(CBDRBoxCol,90), txt0, size.auto, color.new(box_text_cbdr_col,80), text_wrap=text.wrap_auto)

if dayofweek == dayofweek.friday

box.set_right(cbdrbox, cbdrOpenTime+187200000)

line.set_x2(cbdr_hi_line, cbdrOpenTime+187200000)

line.set_x2(cbdr_lo_line, cbdrOpenTime+187200000)

if box_text_cbdr == false

box.set_text(cbdrbox, "")

if ShowDev and ShowCBDR and bool_cbdr_dev

for i = 1 to DevCount by 1

if i == 1

dev01posline := line.new(cbdrOpenTime, cbdr_hi + cbdr_diff * i, cbdrEndTime, cbdr_hi + cbdr_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev01negline := line.new(cbdrOpenTime, cbdr_hi - cbdr_diff * i, cbdrEndTime, cbdr_lo - cbdr_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

if dayofweek == dayofweek.friday

line.set_x2(dev01posline, cbdrOpenTime+187200000)

line.set_x2(dev01negline, cbdrOpenTime+187200000)

if i == 2

dev02posline := line.new(cbdrOpenTime, cbdr_hi + cbdr_diff * i, cbdrEndTime, cbdr_lo + cbdr_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev02negline := line.new(cbdrOpenTime, cbdr_hi - cbdr_diff * i, cbdrEndTime, cbdr_lo - cbdr_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

if dayofweek == dayofweek.friday

line.set_x2(dev02posline, cbdrOpenTime+187200000)

line.set_x2(dev02negline, cbdrOpenTime+187200000)

if i == 3

dev03posline := line.new(cbdrOpenTime, cbdr_hi + cbdr_diff * i, cbdrEndTime, cbdr_lo + cbdr_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev03negline := line.new(cbdrOpenTime, cbdr_hi - cbdr_diff * i, cbdrEndTime, cbdr_lo - cbdr_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

if dayofweek == dayofweek.friday

line.set_x2(dev03posline, cbdrOpenTime+187200000)

line.set_x2(dev03negline, cbdrOpenTime+187200000)

if i == 4

dev04posline := line.new(cbdrOpenTime, cbdr_hi + cbdr_diff * i, cbdrEndTime, cbdr_lo + cbdr_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev04negline := line.new(cbdrOpenTime, cbdr_hi - cbdr_diff * i, cbdrEndTime, cbdr_lo - cbdr_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

if dayofweek == dayofweek.friday

line.set_x2(dev04posline, cbdrOpenTime+187200000)

line.set_x2(dev04negline, cbdrOpenTime+187200000)

else if CBDRTime

cbdr_hi := math.max(high, cbdr_hi)

cbdr_lo := math.min(low, cbdr_lo)

cbdr_diff := cbdr_hi - cbdr_lo

for i = 1 to DevCount by 1

if i == 1 and ShowDev

line.set_y1(dev01posline, cbdr_hi + cbdr_diff * i)

line.set_y2(dev01posline, cbdr_hi + cbdr_diff * i)

line.set_y1(dev01negline, cbdr_lo - cbdr_diff * i)

line.set_y2(dev01negline, cbdr_lo - cbdr_diff * i)

if i == 2 and ShowDev

line.set_y1(dev02posline, cbdr_hi + cbdr_diff * i)

line.set_y2(dev02posline, cbdr_hi + cbdr_diff * i)

line.set_y1(dev02negline, cbdr_lo - cbdr_diff * i)

line.set_y2(dev02negline, cbdr_lo - cbdr_diff * i)

if i == 3 and ShowDev

line.set_y1(dev03posline, cbdr_hi + cbdr_diff * i)

line.set_y2(dev03posline, cbdr_hi + cbdr_diff * i)

line.set_y1(dev03negline, cbdr_lo - cbdr_diff * i)

line.set_y2(dev03negline, cbdr_lo - cbdr_diff * i)

if i == 4 and ShowDev

line.set_y1(dev04posline, cbdr_hi + cbdr_diff * i)

line.set_y2(dev04posline, cbdr_hi + cbdr_diff * i)

line.set_y1(dev04negline, cbdr_lo - cbdr_diff * i)

line.set_y2(dev04negline, cbdr_lo - cbdr_diff * i)

if (cbdr_hi > cbdr_hi )

if ShowCBDR

box.set_top(cbdrbox, cbdr_hi)

if (cbdr_lo < cbdr_lo )

if ShowCBDR

box.set_bottom(cbdrbox, cbdr_lo)

if DevDirection == "Upside Only"

line.delete(dev01negline)

line.delete(dev02negline)

line.delete(dev03negline)

line.delete(dev04negline)

else if DevDirection == "Downside Only"

line.delete(dev01posline)

line.delete(dev02posline)

line.delete(dev03posline)

line.delete(dev04posline)

// ASIA Stuff

var float asia_hi = na

var float asia_lo = na

var float asia_diff = na

var box asia_box = na

var line asia_hi_line = na

var line asia_lo_line = na

var line dev01negline_asia = na

var line dev02negline_asia = na

var line dev03negline_asia = na

var line dev04negline_asia = na

var line dev01posline_asia = na

var line dev02posline_asia = na

var line dev03posline_asia = na

var line dev04posline_asia = na

if SessionBegins(ASIA) and DOM

asia_hi := high

asia_lo := low

asia_diff := asia_hi - asia_lo

if ShowTSO

box.delete(asia_box )

line.delete(dev01posline_asia )

line.delete(dev01negline_asia )

line.delete(dev02posline_asia )

line.delete(dev02negline_asia )

line.delete(dev03posline_asia )

line.delete(dev03negline_asia )

line.delete(dev04posline_asia )

line.delete(dev04negline_asia )

if ShowASIA

asia_box := box.new(asiaOpenTime, asia_hi, asiaEndTime, asia_lo, color.new(ASIABoxCol,90), 1, line.style_solid, extend.none, xloc.bar_time, color.new(ASIABoxCol,90), txt1, size.auto, color.new(box_text_asia_col,80), text_wrap=text.wrap_auto)

if box_text_asia == false

box.set_text(asia_box, "")

if ShowDev and ShowASIA and bool_asia_dev

for i = 1 to DevCount by 1

if i == 1

dev01posline_asia := line.new(asiaOpenTime, asia_hi + asia_diff * i, asiaEndTime, asia_hi + asia_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev01negline_asia := line.new(asiaOpenTime, asia_hi - asia_diff * i, asiaEndTime, asia_lo - asia_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

if i == 2

dev02posline_asia := line.new(asiaOpenTime, asia_hi + asia_diff * i, asiaEndTime, asia_lo + asia_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev02negline_asia := line.new(asiaOpenTime, asia_hi - asia_diff * i, asiaEndTime, asia_lo - asia_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

if i == 3

dev03posline_asia := line.new(asiaOpenTime, asia_hi + asia_diff * i, asiaEndTime, asia_lo + asia_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev03negline_asia := line.new(asiaOpenTime, asia_hi - asia_diff * i, asiaEndTime, asia_lo - asia_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

if i == 4

dev04posline_asia := line.new(asiaOpenTime, asia_hi + asia_diff * i, asiaEndTime, asia_lo + asia_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev04negline_asia := line.new(asiaOpenTime, asia_hi - asia_diff * i, asiaEndTime, asia_lo - asia_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

else if ASIATime

asia_hi := math.max(high, asia_hi)

asia_lo := math.min(low, asia_lo)

asia_diff := asia_hi - asia_lo

for i = 1 to DevCount by 1

if i == 1 and ShowDev

line.set_y1(dev01posline_asia, asia_hi + asia_diff * i)

line.set_y2(dev01posline_asia, asia_hi + asia_diff * i)

line.set_y1(dev01negline_asia, asia_lo - asia_diff * i)

line.set_y2(dev01negline_asia, asia_lo - asia_diff * i)

if i == 2 and ShowDev

line.set_y1(dev02posline_asia, asia_hi + asia_diff * i)

line.set_y2(dev02posline_asia, asia_hi + asia_diff * i)

line.set_y1(dev02negline_asia, asia_lo - asia_diff * i)

line.set_y2(dev02negline_asia, asia_lo - asia_diff * i)

if i == 3 and ShowDev

line.set_y1(dev03posline_asia, asia_hi + asia_diff * i)

line.set_y2(dev03posline_asia, asia_hi + asia_diff * i)

line.set_y1(dev03negline_asia, asia_lo - asia_diff * i)

line.set_y2(dev03negline_asia, asia_lo - asia_diff * i)

if i == 4 and ShowDev

line.set_y1(dev04posline_asia, asia_hi + asia_diff * i)

line.set_y2(dev04posline_asia, asia_hi + asia_diff * i)

line.set_y1(dev04negline_asia, asia_lo - asia_diff * i)

line.set_y2(dev04negline_asia, asia_lo - asia_diff * i)

if (asia_hi > asia_hi )

box.set_top(asia_box, asia_hi)

if (asia_lo < asia_lo )

box.set_bottom(asia_box, asia_lo)

if DevDirection == "Upside Only"

line.delete(dev01negline_asia)

line.delete(dev02negline_asia)

line.delete(dev03negline_asia)

line.delete(dev04negline_asia)

else if DevDirection == "Downside Only"

line.delete(dev01posline_asia)

line.delete(dev02posline_asia)

line.delete(dev03posline_asia)

line.delete(dev04posline_asia)

// FLOUT Stuff

var float flout_hi = na

var float flout_lo = na

var float flout_diff = na

var box floutbox = na

var line flout_hi_line = na

var line flout_lo_line = na

var line dev01negline_flout = na

var line dev02negline_flout = na

var line dev03negline_flout = na

var line dev04negline_flout = na

var line dev01posline_flout = na

var line dev02posline_flout = na

var line dev03posline_flout = na

var line dev04posline_flout = na

if SessionBegins(FLOUT) and DOM

flout_hi := high

flout_lo := low

flout_diff := flout_hi - flout_lo

if ShowTSO

box.delete(floutbox )

line.delete(dev01posline_flout )

line.delete(dev01negline_flout )

line.delete(dev02posline_flout )

line.delete(dev02negline_flout )

line.delete(dev03posline_flout )

line.delete(dev03negline_flout )

line.delete(dev04posline_flout )

line.delete(dev04negline_flout )

if ShowFLOUT

floutbox := box.new(floutOpenTime, flout_hi, floutEndTime, flout_lo, color.new(FLOUTBoxCol,90), 1, line.style_solid, extend.none, xloc.bar_time, color.new(FLOUTBoxCol,90), txt7, size.auto, color.new(box_text_flout_col,80), text_wrap=text.wrap_auto)

if dayofweek == dayofweek.friday

box.set_right(floutbox, floutOpenTime+201600000)

line.set_x2(flout_hi_line, floutOpenTime+201600000)

line.set_x2(flout_lo_line, floutOpenTime+201600000)

if box_text_cbdr == false

box.set_text(floutbox, "")

if ShowDev and ShowFLOUT and bool_flout_dev

for i = 0.5 to DevCount by 0.5

if i == 0.5

dev01posline_flout := line.new(floutOpenTime, flout_hi + flout_diff * i, floutEndTime, flout_hi + flout_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev01negline_flout := line.new(floutOpenTime, flout_hi - flout_diff * i, floutEndTime, flout_lo - flout_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

if dayofweek == dayofweek.friday

line.set_x2(dev01posline_flout, floutOpenTime+201600000)

line.set_x2(dev01negline_flout, floutOpenTime+201600000)

if i == 1

dev02posline_flout := line.new(floutOpenTime, flout_hi + flout_diff * i, floutEndTime, flout_lo + flout_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev02negline_flout := line.new(floutOpenTime, flout_hi - flout_diff * i, floutEndTime, flout_lo - flout_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

if dayofweek == dayofweek.friday

line.set_x2(dev02posline_flout, floutOpenTime+201600000)

line.set_x2(dev02negline_flout, floutOpenTime+201600000)

if i == 1.5

dev03posline_flout := line.new(floutOpenTime, flout_hi + flout_diff * i, floutEndTime, flout_lo + flout_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev03negline_flout := line.new(floutOpenTime, flout_hi - flout_diff * i, floutEndTime, flout_lo - flout_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

if dayofweek == dayofweek.friday

line.set_x2(dev03posline_flout, floutOpenTime+201600000)

line.set_x2(dev03negline_flout, floutOpenTime+201600000)

if i == 2

dev04posline_flout := line.new(floutOpenTime, flout_hi + flout_diff * i, floutEndTime, flout_lo + flout_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

dev04negline_flout := line.new(floutOpenTime, flout_hi - flout_diff * i, floutEndTime, flout_lo - flout_diff * i, xloc=xloc.bar_time, color=DevLNCol, style=DEVLSS, width=DEVLW)

if dayofweek == dayofweek.friday

line.set_x2(dev04posline_flout, floutOpenTime+201600000)

line.set_x2(dev04negline_flout, floutOpenTime+201600000)

else if FLOUTTime

flout_hi := math.max(high, flout_hi)

flout_lo := math.min(low, flout_lo)

flout_diff := flout_hi - flout_lo

for i = 0.5 to DevCount by 0.5

if i == 0.5 and ShowDev

line.set_y1(dev01posline_flout, flout_hi + flout_diff * i)

line.set_y2(dev01posline_flout, flout_hi + flout_diff * i)

line.set_y1(dev01negline_flout, flout_lo - flout_diff * i)

line.set_y2(dev01negline_flout, flout_lo - flout_diff * i)

if i == 1 and ShowDev

line.set_y1(dev02posline_flout, flout_hi + flout_diff * i)

line.set_y2(

在腳本中搜尋"2016年黄金价格"

GBTC holdings USD market valueThis script estimates GBTC bitcoins per share, rather than hardcoding as in other scripts. Its result is an estimate of GBTC holdings USD market value.

Per share bitcoin estimates are adjusted by 2.0% / 365 per day from 2019 year end holdings. Calendar year 2019 ending bitcoins and shares were 261,192 bitcoins and 269,445,300 shares. From the 2019 Form 10-K: 'The Trust’s only ordinary recurring expense is the Sponsor’s Fee. The Sponsor’s Fee accrues daily in U.S. dollars at an annual rate of 2.0% of the Bitcoin Holdings.. The Sponsor’s Fee is payable in Bitcoins to the Sponsor monthly in arrears.'

No attempt is made to account for leap years.

Per share bitcoin estimate is converted to USD market value by multiplying by the simple average BTCUSD price at Coinbase and Bitstamp. Grayscale uses the TradeBlock XBX index, a volume weighted average of Coinbase Pro, Kraken, LMAX Digital and Bitstamp prices.

Spot checks vs archive.org captures of daily bitcoins per share and the chart on Grayscale's site:

The estimate for market close January 22 2021 is 0.00094899 bitcoins per share, the published datum on Grayscale's web site was 0.00094898. The estimate matches at 20:30 rather than at 16:00.

The estimate for December 31 2018 is 0.000988965 vs a published 0.00098895.

The estimate for December 29 2017 market value is $14.58 vs $14.65.

The estimate for December 30 2016 market value is $0.99 vs $0.98.

The estimate for January 4 2016 market value is $0.46 vs $0.45.

No estimates before 2016.

The default style is to draw a blue line with two thirds transparency outside market hours and for first/last minutes of trading, switching to daily or greater periodicity hides this.

No warranty is expressed or implied , I am not a lawyer, etc etc etc.

This is not investing advice . Always do your own due diligence .

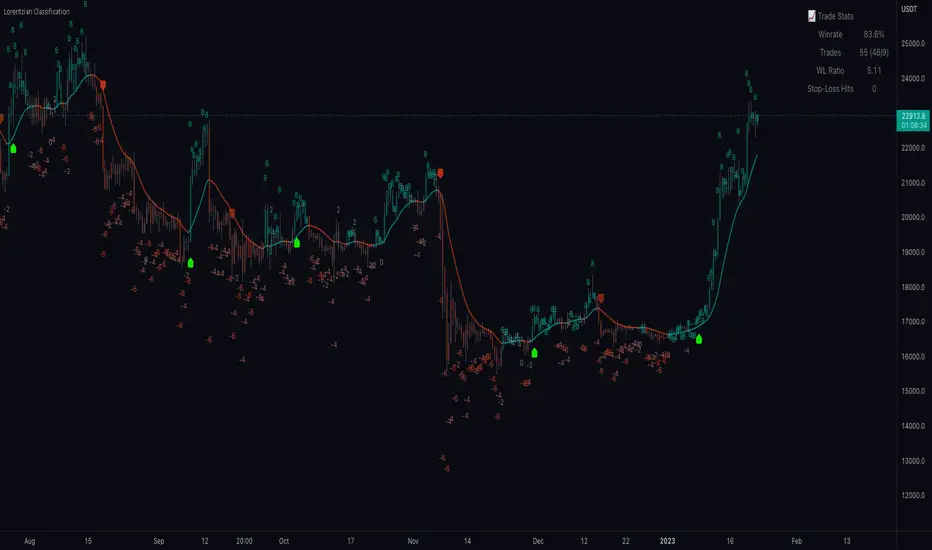

Machine Learning: Lorentzian Classification█ OVERVIEW

A Lorentzian Distance Classifier (LDC) is a Machine Learning classification algorithm capable of categorizing historical data from a multi-dimensional feature space. This indicator demonstrates how Lorentzian Classification can also be used to predict the direction of future price movements when used as the distance metric for a novel implementation of an Approximate Nearest Neighbors (ANN) algorithm.

█ BACKGROUND

In physics, Lorentzian space is perhaps best known for its role in describing the curvature of space-time in Einstein's theory of General Relativity (2). Interestingly, however, this abstract concept from theoretical physics also has tangible real-world applications in trading.

Recently, it was hypothesized that Lorentzian space was also well-suited for analyzing time-series data (4), (5). This hypothesis has been supported by several empirical studies that demonstrate that Lorentzian distance is more robust to outliers and noise than the more commonly used Euclidean distance (1), (3), (6). Furthermore, Lorentzian distance was also shown to outperform dozens of other highly regarded distance metrics, including Manhattan distance, Bhattacharyya similarity, and Cosine similarity (1), (3). Outside of Dynamic Time Warping based approaches, which are unfortunately too computationally intensive for PineScript at this time, the Lorentzian Distance metric consistently scores the highest mean accuracy over a wide variety of time series data sets (1).

Euclidean distance is commonly used as the default distance metric for NN-based search algorithms, but it may not always be the best choice when dealing with financial market data. This is because financial market data can be significantly impacted by proximity to major world events such as FOMC Meetings and Black Swan events. This event-based distortion of market data can be framed as similar to the gravitational warping caused by a massive object on the space-time continuum. For financial markets, the analogous continuum that experiences warping can be referred to as "price-time".

Below is a side-by-side comparison of how neighborhoods of similar historical points appear in three-dimensional Euclidean Space and Lorentzian Space:

This figure demonstrates how Lorentzian space can better accommodate the warping of price-time since the Lorentzian distance function compresses the Euclidean neighborhood in such a way that the new neighborhood distribution in Lorentzian space tends to cluster around each of the major feature axes in addition to the origin itself. This means that, even though some nearest neighbors will be the same regardless of the distance metric used, Lorentzian space will also allow for the consideration of historical points that would otherwise never be considered with a Euclidean distance metric.

Intuitively, the advantage inherent in the Lorentzian distance metric makes sense. For example, it is logical that the price action that occurs in the hours after Chairman Powell finishes delivering a speech would resemble at least some of the previous times when he finished delivering a speech. This may be true regardless of other factors, such as whether or not the market was overbought or oversold at the time or if the macro conditions were more bullish or bearish overall. These historical reference points are extremely valuable for predictive models, yet the Euclidean distance metric would miss these neighbors entirely, often in favor of irrelevant data points from the day before the event. By using Lorentzian distance as a metric, the ML model is instead able to consider the warping of price-time caused by the event and, ultimately, transcend the temporal bias imposed on it by the time series.

For more information on the implementation details of the Approximate Nearest Neighbors (ANN) algorithm used in this indicator, please refer to the detailed comments in the source code.

█ HOW TO USE

Below is an explanatory breakdown of the different parts of this indicator as it appears in the interface:

Below is an explanation of the different settings for this indicator:

General Settings:

Source - This has a default value of "hlc3" and is used to control the input data source.

Neighbors Count - This has a default value of 8, a minimum value of 1, a maximum value of 100, and a step of 1. It is used to control the number of neighbors to consider.

Max Bars Back - This has a default value of 2000.

Feature Count - This has a default value of 5, a minimum value of 2, and a maximum value of 5. It controls the number of features to use for ML predictions.

Color Compression - This has a default value of 1, a minimum value of 1, and a maximum value of 10. It is used to control the compression factor for adjusting the intensity of the color scale.

Show Exits - This has a default value of false. It controls whether to show the exit threshold on the chart.

Use Dynamic Exits - This has a default value of false. It is used to control whether to attempt to let profits ride by dynamically adjusting the exit threshold based on kernel regression.

Feature Engineering Settings:

Note: The Feature Engineering section is for fine-tuning the features used for ML predictions. The default values are optimized for the 4H to 12H timeframes for most charts, but they should also work reasonably well for other timeframes. By default, the model can support features that accept two parameters (Parameter A and Parameter B, respectively). Even though there are only 4 features provided by default, the same feature with different settings counts as two separate features. If the feature only accepts one parameter, then the second parameter will default to EMA-based smoothing with a default value of 1. These features represent the most effective combination I have encountered in my testing, but additional features may be added as additional options in the future.

Feature 1 - This has a default value of "RSI" and options are: "RSI", "WT", "CCI", "ADX".

Feature 2 - This has a default value of "WT" and options are: "RSI", "WT", "CCI", "ADX".

Feature 3 - This has a default value of "CCI" and options are: "RSI", "WT", "CCI", "ADX".

Feature 4 - This has a default value of "ADX" and options are: "RSI", "WT", "CCI", "ADX".

Feature 5 - This has a default value of "RSI" and options are: "RSI", "WT", "CCI", "ADX".

Filters Settings:

Use Volatility Filter - This has a default value of true. It is used to control whether to use the volatility filter.

Use Regime Filter - This has a default value of true. It is used to control whether to use the trend detection filter.

Use ADX Filter - This has a default value of false. It is used to control whether to use the ADX filter.

Regime Threshold - This has a default value of -0.1, a minimum value of -10, a maximum value of 10, and a step of 0.1. It is used to control the Regime Detection filter for detecting Trending/Ranging markets.

ADX Threshold - This has a default value of 20, a minimum value of 0, a maximum value of 100, and a step of 1. It is used to control the threshold for detecting Trending/Ranging markets.

Kernel Regression Settings:

Trade with Kernel - This has a default value of true. It is used to control whether to trade with the kernel.

Show Kernel Estimate - This has a default value of true. It is used to control whether to show the kernel estimate.

Lookback Window - This has a default value of 8 and a minimum value of 3. It is used to control the number of bars used for the estimation. Recommended range: 3-50

Relative Weighting - This has a default value of 8 and a step size of 0.25. It is used to control the relative weighting of time frames. Recommended range: 0.25-25

Start Regression at Bar - This has a default value of 25. It is used to control the bar index on which to start regression. Recommended range: 0-25

Display Settings:

Show Bar Colors - This has a default value of true. It is used to control whether to show the bar colors.

Show Bar Prediction Values - This has a default value of true. It controls whether to show the ML model's evaluation of each bar as an integer.

Use ATR Offset - This has a default value of false. It controls whether to use the ATR offset instead of the bar prediction offset.

Bar Prediction Offset - This has a default value of 0 and a minimum value of 0. It is used to control the offset of the bar predictions as a percentage from the bar high or close.

Backtesting Settings:

Show Backtest Results - This has a default value of true. It is used to control whether to display the win rate of the given configuration.

█ WORKS CITED

(1) R. Giusti and G. E. A. P. A. Batista, "An Empirical Comparison of Dissimilarity Measures for Time Series Classification," 2013 Brazilian Conference on Intelligent Systems, Oct. 2013, DOI: 10.1109/bracis.2013.22.

(2) Y. Kerimbekov, H. Ş. Bilge, and H. H. Uğurlu, "The use of Lorentzian distance metric in classification problems," Pattern Recognition Letters, vol. 84, 170–176, Dec. 2016, DOI: 10.1016/j.patrec.2016.09.006.

(3) A. Bagnall, A. Bostrom, J. Large, and J. Lines, "The Great Time Series Classification Bake Off: An Experimental Evaluation of Recently Proposed Algorithms." ResearchGate, Feb. 04, 2016.

(4) H. Ş. Bilge, Yerzhan Kerimbekov, and Hasan Hüseyin Uğurlu, "A new classification method by using Lorentzian distance metric," ResearchGate, Sep. 02, 2015.

(5) Y. Kerimbekov and H. Şakir Bilge, "Lorentzian Distance Classifier for Multiple Features," Proceedings of the 6th International Conference on Pattern Recognition Applications and Methods, 2017, DOI: 10.5220/0006197004930501.

(6) V. Surya Prasath et al., "Effects of Distance Measure Choice on KNN Classifier Performance - A Review." .

█ ACKNOWLEDGEMENTS

@veryfid - For many invaluable insights, discussions, and advice that helped to shape this project.

@capissimo - For open sourcing his interesting ideas regarding various KNN implementations in PineScript, several of which helped inspire my original undertaking of this project.

@RikkiTavi - For many invaluable physics-related conversations and for his helping me develop a mechanism for visualizing various distance algorithms in 3D using JavaScript

@jlaurel - For invaluable literature recommendations that helped me to understand the underlying subject matter of this project.

@annutara - For help in beta-testing this indicator and for sharing many helpful ideas and insights early on in its development.

@jasontaylor7 - For helping to beta-test this indicator and for many helpful conversations that helped to shape my backtesting workflow

@meddymarkusvanhala - For helping to beta-test this indicator

@dlbnext - For incredibly detailed backtesting testing of this indicator and for sharing numerous ideas on how the user experience could be improved.

[blackcat] L2 Ehlers AutoLength CCI VWAPLevel: 2

Background

John F. Ehlers introuced AutoLength CCI in Sep, 2016.

Function

In “Measuring Market Cycles” in Sep, 2016, John Ehlers described a method that he had developed to measure cycles in market data. Dr. Ehlers presented an indicator using this technique, which he referred to as an autocorrelation periodogram. He also described how this technique for determining the dominant market cycle could be used to help select the period used in other more traditional indicators such as the stochastic, the RSI, and the commodity channel index (CCI). Here, I am providing an example strategy using the concepts presented in the article with CCI and upgraded with CCI VWAP with my own idea.

Key Signal

CCIValue --> Ehlers AutoLength CCI VWAP signal

Pros and Cons

90% John F. Ehlers definition translation, even variable names are the same. This help readers who would like to use pine to read his book.

Remarks

The 87th script for Blackcat1402 John F. Ehlers Week publication.

I upgraded original Ehlers Autolength CCI to Autolength CCI VWAP

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

[blackcat] L2 Ehlers Super Passband FilterLevel: 2

Background

John F. Ehlers introuced Super Passband Filter in Jul, 2016.

Function

In “The Super Passband Filter” in Jul, 2016, John Ehlers addressed the problem of frequencies in indicators that are too low or too high. The common practice to refine frequency is to enable smart filters. However, good filters take lots of computational power. So Ehlers showed us how to use filters while keep computing power relatively low. John Ehlers described a new oscillator he’s developed to help minimize computational lag. Ehlers called this new oscillator a super passband filter. He has designed it to reject very low-frequency components and thus display as an oscillator as well as reject high-frequency components so as to minimize noise. Ehlers seeked to filter out both high and low frequencies from market data, eliminating distracting “wiggles” from the resultant signal with minimal lag effect. Trigger points for the filter are added with a root mean square (RMS) envelope over the signal line.

## Buy on the filter crossing above its -RMS line

## Short on the filter crossing below its RMS line