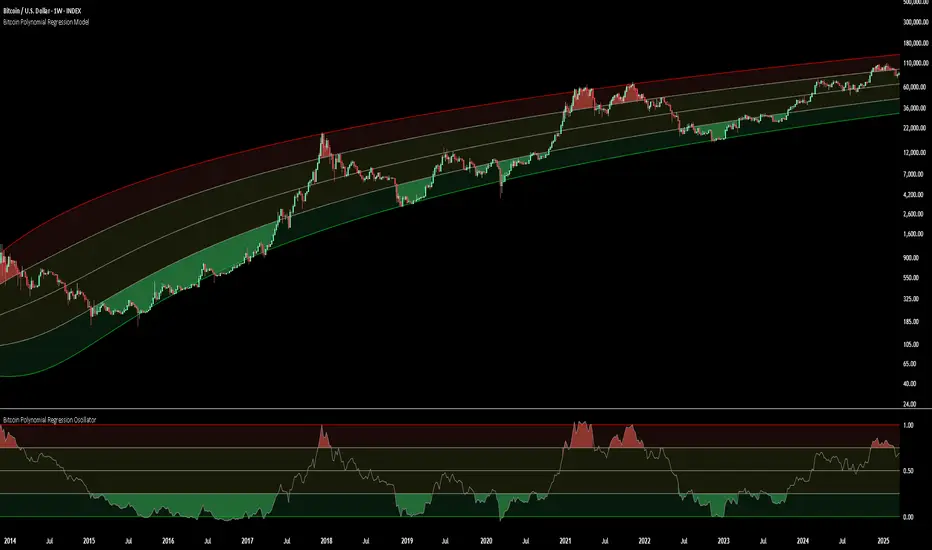

Bitcoin Polynomial Regression ModelThis is the main version of the script. Click here for the Oscillator part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines. The Oscillator version can be found here.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

在腳本中搜尋"2024年5月2日+深交所+股票成交额+新浪财经"

Bitcoin Polynomial Regression OscillatorThis is the oscillator version of the script. Click here for the other part of the script.

💡Why this model was created:

One of the key issues with most existing models, including our own Bitcoin Log Growth Curve Model , is that they often fail to realistically account for diminishing returns. As a result, they may present overly optimistic bull cycle targets (hence, we introduced alternative settings in our previous Bitcoin Log Growth Curve Model).

This new model however, has been built from the ground up with a primary focus on incorporating the principle of diminishing returns. It directly responds to this concept, which has been briefly explored here .

📉The theory of diminishing returns:

This theory suggests that as each four-year market cycle unfolds, volatility gradually decreases, leading to more tempered price movements. It also implies that the price increase from one cycle peak to the next will decrease over time as the asset matures. The same pattern applies to cycle lows and the relationship between tops and bottoms. In essence, these price movements are interconnected and should generally follow a consistent pattern. We believe this model provides a more realistic outlook on bull and bear market cycles.

To better understand this theory, the relationships between cycle tops and bottoms are outlined below:https://www.tradingview.com/x/7Hldzsf2/

🔧Creation of the model:

For those interested in how this model was created, the process is explained here. Otherwise, feel free to skip this section.

This model is based on two separate cubic polynomial regression lines. One for the top price trend and another for the bottom. Both follow the general cubic polynomial function:

ax^3 +bx^2 + cx + d.

In this equation, x represents the weekly bar index minus an offset, while a, b, c, and d are determined through polynomial regression analysis. The input (x, y) values used for the polynomial regression analysis are as follows:

Top regression line (x, y) values:

113, 18.6

240, 1004

451, 19128

655, 65502

Bottom regression line (x, y) values:

103, 2.5

267, 211

471, 3193

676, 16255

The values above correspond to historical Bitcoin cycle tops and bottoms, where x is the weekly bar index and y is the weekly closing price of Bitcoin. The best fit is determined using metrics such as R-squared values, residual error analysis, and visual inspection. While the exact details of this evaluation are beyond the scope of this post, the following optimal parameters were found:

Top regression line parameter values:

a: 0.000202798

b: 0.0872922

c: -30.88805

d: 1827.14113

Bottom regression line parameter values:

a: 0.000138314

b: -0.0768236

c: 13.90555

d: -765.8892

📊Polynomial Regression Oscillator:

This publication also includes the oscillator version of the this model which is displayed at the bottom of the screen. The oscillator applies a logarithmic transformation to the price and the regression lines using the formula log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed top and bottom regression line with the formula:

normalized price = log(close) - log(bottom regression line) / log(top regression line) - log(bottom regression line)

This transformation results in a price value between 0 and 1 between both the regression lines.

🔍Interpretation of the Model:

In general, the red area represents a caution zone, as historically, the price has often been near its cycle market top within this range. On the other hand, the green area is considered an area of opportunity, as historically, it has corresponded to the market bottom.

The top regression line serves as a signal for the absolute market cycle peak, while the bottom regression line indicates the absolute market cycle bottom.

Additionally, this model provides a predicted range for Bitcoin's future price movements, which can be used to make extrapolated predictions. We will explore this further below.

🔮Future Predictions:

Finally, let's discuss what this model actually predicts for the potential upcoming market cycle top and the corresponding market cycle bottom. In our previous post here , a cycle interval analysis was performed to predict a likely time window for the next cycle top and bottom:

In the image, it is predicted that the next top-to-top cycle interval will be 208 weeks, which translates to November 3rd, 2025. It is also predicted that the bottom-to-top cycle interval will be 152 weeks, which corresponds to October 13th, 2025. On the macro level, these two dates align quite well. For our prediction, we take the average of these two dates: October 24th 2025. This will be our target date for the bull cycle top.

Now, let's do the same for the upcoming cycle bottom. The bottom-to-bottom cycle interval is predicted to be 205 weeks, which translates to October 19th, 2026, and the top-to-bottom cycle interval is predicted to be 259 weeks, which corresponds to October 26th, 2026. We then take the average of these two dates, predicting a bear cycle bottom date target of October 19th, 2026.

Now that we have our predicted top and bottom cycle date targets, we can simply reference these two dates to our model, giving us the Bitcoin top price prediction in the range of 152,000 in Q4 2025 and a subsequent bottom price prediction in the range of 46,500 in Q4 2026.

For those interested in understanding what this specifically means for the predicted diminishing return top and bottom cycle values, the image below displays these predicted values. The new values are highlighted in yellow:

And of course, keep in mind that these targets are just rough estimates. While we've done our best to estimate these targets through a data-driven approach, markets will always remain unpredictable in nature. What are your targets? Feel free to share them in the comment section below.

[COG]S&P 500 Weekly Seasonality ProjectionS&P 500 Weekly Seasonality Projection

This indicator visualizes S&P 500 seasonality patterns based on historical weekly performance data. It projects price movements for up to 26 weeks ahead, highlighting key seasonal periods that have historically affected market performance.

Key Features:

Projects price movements based on historical S&P 500 weekly seasonality patterns (2005-2024)

Highlights six key seasonal periods: Jan-Feb Momentum, March Lows, April-May Strength, Summer Strength, September Dip, and Year-End Rally

Customizable forecast length from 1-26 weeks with quick timeframe selection buttons

Optional moving average smoothing for more gradual projections

Detailed statistics table showing projected price and percentage change

Seasonality mini-map showing the full annual pattern with current position

Customizable colors and visual elements

How to Use:

Apply to S&P 500 index or related instruments (daily timeframe or higher recommended)

Set your desired forecast length (1-26 weeks)

Monitor highlighted seasonal zones that have historically shown consistent patterns

Use the projection line as a general guideline for potential price movement

Settings:

Forecast length: Configure from 1-26 weeks or use quick select buttons (1M, 3M, 6M, 1Y)

Visual options: Customize colors, backgrounds, label sizes, and table position

Display options: Toggle statistics table, period highlights, labels, and mini-map

This indicator is designed as a visual guide to help identify potential seasonal tendencies in the S&P 500. Historical patterns are not guarantees of future performance, but understanding these seasonal biases can provide valuable context for your trading decisions.

Note: For optimal visualization, use on Daily timeframe or higher. Intraday timeframes will display a warning message.

Bitcoin Halving DatesBitcoin Halving Dates Indicator

This custom indicator automatically marks Bitcoin's key halving events by drawing vertical lines on your chart. It highlights the historical halving dates (2012, 2016, 2020) and includes an estimated date for the upcoming halving in 2024, making it easy to visualize significant supply events that can influence market trends.

Features:

Automated Markings: Displays vertical lines on the first bar of each halving day.

Customizable: Easily adjust halving dates and styling options to suit your analysis.

Built for Traders: Enhance your technical analysis by keeping track of pivotal market events.

Use this indicator to gain a visual edge by integrating critical Bitcoin halving events into your trading strategy. Happy Trading!

MM Labelled AVWAPTradingView provides a tool to show anchored VWAP plots on your screen, but there is no way to label the plots to add additional context to the level. Instead, users are forced to use the plot style (color, line style, line thickness, etc) to indicate what the plots are for and then they have to remember that meaning when looking at different charts. It also means that for key market-wide moments, users will need to add the plot for every symbol.

Now, for the first time on TradingView, you can create anchored VWAP plots with labels on them so you can understand the meaning behind the key moments you care about and don't need to remember what they mean by using styles like color or thickness. You can use this indicator to track key moments like the 2022 market bottom, or the Aug 9, 2024 "Carry Trade Unwind" bottom. The labelled AVWAP plots are visible on every chart by default. If you have an AVWAP moment that is only relevant to a small number of symbols, you can configure the indicator to only appear on those symbols.

TEMA OBOS Strategy PakunTEMA OBOS Strategy

Overview

This strategy combines a trend-following approach using the Triple Exponential Moving Average (TEMA) with Overbought/Oversold (OBOS) indicator filtering.

By utilizing TEMA crossovers to determine trend direction and OBOS as a filter, it aims to improve entry precision.

This strategy can be applied to markets such as Forex, Stocks, and Crypto, and is particularly designed for mid-term timeframes (5-minute to 1-hour charts).

Strategy Objectives

Identify trend direction using TEMA

Use OBOS to filter out overbought/oversold conditions

Implement ATR-based dynamic risk management

Key Features

1. Trend Analysis Using TEMA

Uses crossover of short-term EMA (ema3) and long-term EMA (ema4) to determine entries.

ema4 acts as the primary trend filter.

2. Overbought/Oversold (OBOS) Filtering

Long Entry Condition: up > down (bullish trend confirmed)

Short Entry Condition: up < down (bearish trend confirmed)

Reduces unnecessary trades by filtering extreme market conditions.

3. ATR-Based Take Profit (TP) & Stop Loss (SL)

Adjustable ATR multiplier for TP/SL

Default settings:

TP = ATR × 5

SL = ATR × 2

Fully customizable risk parameters.

4. Customizable Parameters

TEMA Length (for trend calculation)

OBOS Length (for overbought/oversold detection)

Take Profit Multiplier

Stop Loss Multiplier

EMA Display (Enable/Disable TEMA lines)

Bar Color Change (Enable/Disable candle coloring)

Trading Rules

Long Entry (Buy Entry)

ema3 crosses above ema4 (Golden Cross)

OBOS indicator confirms up > down (bullish trend)

Execute a buy position

Short Entry (Sell Entry)

ema3 crosses below ema4 (Death Cross)

OBOS indicator confirms up < down (bearish trend)

Execute a sell position

Take Profit (TP)

Entry Price + (ATR × TP Multiplier) (Default: 5)

Stop Loss (SL)

Entry Price - (ATR × SL Multiplier) (Default: 2)

TP/SL settings are fully customizable to fine-tune risk management.

Risk Management Parameters

This strategy emphasizes proper position sizing and risk control to balance risk and return.

Trading Parameters & Considerations

Initial Account Balance: $7,000 (adjustable)

Base Currency: USD

Order Size: 10,000 USD

Pyramiding: 1

Trading Fees: $0.94 per trade

Long Position Margin: 50%

Short Position Margin: 50%

Total Trades (M5 Timeframe): 128

Deep Test Results (2024/11/01 - 2025/02/24)BTCUSD-5M

Total P&L:+1638.20USD

Max equity drawdown:694.78USD

Total trades:128

Profitable trades:44.53

Profit factor:1.45

These settings aim to protect capital while maintaining a balanced risk-reward approach.

Visual Support

TEMA Lines (Three EMAs)

Trend direction is indicated by color changes (Blue/Orange)

ema3 (short-term) and ema4 (long-term) crossover signals potential entries

OBOS Histogram

Green → Strong buying pressure

Red → Strong selling pressure

Blue → Possible trend reversal

Entry & Exit Markers

Blue Arrow → Long Entry Signal

Red Arrow → Short Entry Signal

Take Profit / Stop Loss levels displayed

Strategy Improvements & Uniqueness

This strategy is based on indicators developed by "l_lonthoff" and "jdmonto0", but has been significantly optimized for better entry accuracy, visual clarity, and risk management.

Enhanced Trend Identification with TEMA

Detects early trend reversals using ema3 & ema4 crossover

Reduces market noise for a smoother trend-following approach

Improved OBOS Filtering

Prevents excessive trading

Reduces unnecessary risk exposure

Dynamic Risk Management with ATR-Based TP/SL

Not a fixed value → TP/SL adjusts to market volatility

Fully customizable ATR multiplier settings

(Default: TP = ATR × 5, SL = ATR × 2)

Summary

The TEMA + OBOS Strategy is a simple yet powerful trading method that integrates trend analysis and oscillators.

TEMA for trend identification

OBOS for noise reduction & overbought/oversold filtering

ATR-based TP/SL settings for dynamic risk management

Before using this strategy, ensure thorough backtesting and demo trading to fine-tune parameters according to your trading style.

[GYTS] FiltersToolkit LibraryFiltersToolkit Library

🌸 Part of GoemonYae Trading System (GYTS) 🌸

🌸 --------- 1. INTRODUCTION --------- 🌸

💮 What Does This Library Contain?

This library is a curated collection of high-performance digital signal processing (DSP) filters and auxiliary functions designed specifically for financial time series analysis. It includes a shortlist of our favourite and best performing filters — each rigorously tested and selected for their responsiveness, minimal lag and robustness in diverse market conditions. These tools form an integral part of the GoemonYae Trading System (GYTS), chosen for their unique characteristics in handling market data.

The library contains two main categories:

1. Smoothing filters (low-pass filters and moving averages) for e.g. denoising, trend following

2. Detrending tools (high-pass and band-pass filters, known as "oscillators") for e.g. mean reversion

This collection is finely tuned for practical trading applications and is therefore not meant to be exhaustive. However, will continue to expand as we discover and validate new filtering techniques. I welcome collaboration and suggestions for novel approaches.

🌸 ——— 2. ADDED VALUE ——— 🌸

💮 Unified syntax and comprehensive documentation

The FiltersToolkit Library brings together a wide array of valuable filters under a unified, intuitive syntax. Each function is thoroughly documented, with clear explanations and academic sources that underline the mathematical rigour behind the methods. This level of documentation not only facilitates integration into trading strategies but also helps underlying the underlying concepts and rationale.

💮 Optimised performance and readability

The code prioritizes computational efficiency while maintaining readability. Key optimizations include:

- Minimizing redundant calculations in recursive filters

- Smart coefficient caching

- Efficient state management

- Vectorized operations where applicable

💮 Enhanced functionality and flexibility

Some filters in this library introduce extended functionality beyond the original publications. For instance, the MESA Adaptive Moving Average (MAMA) and Ehlers’ Combined Bandpass Filter incorporate multiple variations found in the literature, thereby providing traders with flexible tools that can be fine-tuned to different market conditions.

🌸 ——— 3. THE FILTERS ——— 🌸

💮 Hilbert Transform Function

This function implements the Hilbert Transform as utilised by John Ehlers. It converts a real-valued time series into its analytic signal, enabling the extraction of instantaneous phase and frequency information—an essential step in adaptive filtering.

Source: John Ehlers - "Rocket Science for Traders" (2001), "TASC 2001 V. 19:9", "Cybernetic Analysis for Stocks and Futures" (2004)

💮 Homodyne Discriminator

By leveraging the Hilbert Transform, this function computes the dominant cycle period through a Homodyne Discriminator. It extracts the in-phase and quadrature components of the signal, facilitating a robust estimation of the underlying cycle characteristics.

Source: John Ehlers - "Rocket Science for Traders" (2001), "TASC 2001 V. 19:9", "Cybernetic Analysis for Stocks and Futures" (2004)

💮 MESA Adaptive Moving Average (MAMA)

An advanced dual-stage adaptive moving average, this function outputs both the MAMA and its companion FAMA. It combines adaptive alpha computation with elements from Kaufman’s Adaptive Moving Average (KAMA) to provide a responsive and reliable trend indicator.

Source: John Ehlers - "Rocket Science for Traders" (2001), "TASC 2001 V. 19:9", "Cybernetic Analysis for Stocks and Futures" (2004)

💮 BiQuad Filters

A family of second-order recursive filters offering exceptional control over frequency response:

- High-pass filter for detrending

- Low-pass filter for smooth trend following

- Band-pass filter for cycle isolation

The quality factor (Q) parameter allows fine-tuning of the resonance characteristics, making these filters highly adaptable to different market conditions.

Source: Robert Bristow-Johnson's Audio EQ Cookbook, implemented by @The_Peaceful_Lizard

💮 Relative Vigor Index (RVI)

This filter evaluates the strength of a trend by comparing the closing price to the trading range. Operating similarly to a band-pass filter, the RVI provides insights into market momentum and potential reversals.

Source: John Ehlers – “Cybernetic Analysis for Stocks and Futures” (2004)

💮 Cyber Cycle

The Cyber Cycle filter emphasises market cycles by smoothing out noise and highlighting the dominant cyclical behaviour. It is particularly useful for detecting trend reversals and cyclical patterns in the price data.

Source: John Ehlers – “Cybernetic Analysis for Stocks and Futures” (2004)

💮 Butterworth High Pass Filter

Inspired by the classical Butterworth design, this filter achieves a maximally flat magnitude response in the passband while effectively removing low-frequency trends. Its design minimises phase distortion, which is vital for accurate signal interpretation.

Source: John Ehlers – “Cybernetic Analysis for Stocks and Futures” (2004)

💮 2-Pole SuperSmoother

Employing a two-pole design, the SuperSmoother filter reduces high-frequency noise with minimal lag. It is engineered to preserve trend integrity while offering a smooth output even in noisy market conditions.

Source: John Ehlers – “Cybernetic Analysis for Stocks and Futures” (2004)

💮 3-Pole SuperSmoother

An extension of the 2-pole design, the 3-pole SuperSmoother further attenuates high-frequency noise. Its additional pole delivers enhanced smoothing at the cost of slightly increased lag.

Source: John Ehlers – “Cybernetic Analysis for Stocks and Futures” (2004)

💮 Adaptive Directional Volatility Moving Average (ADXVma)

This adaptive moving average adjusts its smoothing factor based on directional volatility. By combining true range and directional movement measurements, it remains exceptionally flat during ranging markets and responsive during directional moves.

Source: Various implementations across platforms, unified and optimized

💮 Ehlers Combined Bandpass Filter with Automated Gain Control (AGC)

This sophisticated filter merges a highpass pre-processing stage with a bandpass filter. An integrated Automated Gain Control normalises the output to a consistent range, while offering both regular and truncated recursive formulations to manage lag.

Source: John F. Ehlers – “Truncated Indicators” (2020), “Cycle Analytics for Traders” (2013)

💮 Voss Predictive Filter

A forward-looking filter that predicts future values of a band-limited signal in real time. By utilising multiple time-delayed feedback terms, it provides anticipatory coupling and delivers a short-term predictive signal.

Source: John Ehlers - "A Peek Into The Future" (TASC 2019-08)

💮 Adaptive Autonomous Recursive Moving Average (A2RMA)

This filter dynamically adjusts its smoothing through an adaptive mechanism based on an efficiency ratio and a dynamic threshold. A double application of an adaptive moving average ensures both responsiveness and stability in volatile and ranging markets alike. Very flat response when properly tuned.

Source: @alexgrover (2019)

💮 Ultimate Smoother (2-Pole)

The Ultimate Smoother filter is engineered to achieve near-zero lag in its passband by subtracting a high-pass response from an all-pass response. This creates a filter that maintains signal fidelity at low frequencies while effectively filtering higher frequencies at the expense of slight overshooting.

Source: John Ehlers - TASC 2024-04 "The Ultimate Smoother"

Note: This library is actively maintained and enhanced. Suggestions for additional filters or improvements are welcome through the usual channels. The source code contains a list of tested filters that did not make it into the curated collection.

Best Buffett Ratio w/ Std-Dev Offset + Conditional PlotSummary:

This script provides a visually clear way to track the so-called “Buffett Ratio,”

a popular market valuation gauge which compares the total US stock market cap

to the country’s GDP. In addition, it plots a “hardcoded” long-term trend line,

along with fixed standard-deviation bands (in log space), and uses background colors

to signal potentially overvalued or undervalued zones.

What Is the Buffett Ratio?

Often credited to Warren Buffett, the Buffett Ratio (or Buffett Indicator) measures:

(Total US Stock Market Capitalization) / (US GDP)

• A higher ratio typically means equities are more expensive relative to the size of the economy.

• A lower ratio suggests equities may be more attractively valued compared to GDP.

Historically, the ratio has tended to drift upward over many decades,

as the US economy and stock markets grow, but it still oscillates around some trend over time.

How to Use

1) Add to Chart:

- In TradingView, simply apply the indicator (it internally fetches CRSPTM1 & GDP data).

2) Tweak Inputs:

- Log Offset for 1σ: Adjust how wide the ±1σ/±2σ bands appear around the trend.

- Anchor Points: Edit startYear , endYear , startRatio , endRatio

if you want a different slope or different “fair value” anchors.

3) Interpretation:

- If the indicator is above +2σ (red line) , it’s historically “very expensive,”

often leading to lower future returns over the long term.

- If it’s below –2σ (green line) , it’s historically “deep undervaluation,”

often pointing to better future returns over time.

- The intermediate zones show degrees of mild over- or undervaluation.

How This Script Works

1) Buffett Ratio Calculation:

- The script requests data from TradingView’s built-in CRSPTM1 index (total US market cap).

- It also requests US GDP data via request.economic("US", "GDP") .

- If GDP data is missing, the ratio becomes na on that bar.

2) Hardcoded Trend Line:

- Rather than a rolling average, the script uses two “anchors” (e.g. 1950 → 0.30 ratio, 2024 → 1.25 ratio)

and solves for a single log-growth rate to produce a steady upward slope.

3) Fixed Standard Deviations in Log Space:

- The script takes the log of the trend line, then applies a fixed offset for ±1σ and ±2σ,

creating proportional bands that do not “expand/contract” from a rolling window.

4) Conditional Plotting:

- The script only begins plotting once the Buffett Ratio actually has data (around 2011).

5) Color-Coded Zones:

- Above +2σ: red background (historically very expensive)

- Between +1σ and +2σ: yellow background (moderately expensive)

- Between –1σ and +1σ: no background color (around normal)

- Between –2σ and –1σ: aqua background (moderately undervalued)

- Below –2σ: green background (historically deep undervaluation)

Final Notes

• Data Limitations: US GDP data and CRSPTM1 only go back so far, so this starts around 2011.

• Long-Term vs. Short-Term: Best viewed on monthly/quarterly charts and interpreted over years.

• Tuning: If you believe structural changes have shifted the ratio’s fair slope,

adjust the code’s anchors or log offsets.

Enjoy, and use responsibly!

Ehlers Maclaurin Ultimate Smoother [CT]Ehlers Maclaurin Ultimate Smoother

Introduction

The Ehlers Maclaurin Ultimate Smoother is an innovative enhancement of the classic Ehlers SuperSmoother. By leveraging advanced Maclaurin series approximations, this indicator offers superior market analysis and signal generation.

The indicator combines Ehlers' Ultimate Smoother with Maclaurin series approximations to create a more efficient and accurate smoothing mechanism:

Input price data passes through the initial smoothing phase

Maclaurin series approximates trigonometric functions

Enhanced high-pass filter removes market noise

Final smoothing phase produces the output signal

Why the Maclaurin Approach?

The Maclaurin series is a special form of the Taylor series, centered around 0. It provides an efficient way to approximate complex functions using polynomial terms. In this indicator, we use the Maclaurin approach to improve the sine and cosine functions, resulting in:

Faster Calculations: By using polynomial approximations, we significantly reduce computational complexity.

Improved Stability: The approximation provides a more stable numerical basis for calculations.

Preservation of Precision: Despite the approximation, we maintain the precision needed for price smoothing.

Calculations

The indicator employs several key mathematical components:

Maclaurin Series Approximation:

sin(x) ≈ x - x³/3! + x⁵/5! - x⁷/7! + x⁹/9!

cos(x) ≈ 1 - x²/2! + x⁴/4! - x⁶/6! + x⁸/8!

Smoothing Algorithm:

Uses exponential smoothing with optimized coefficients

Implements high-pass filtering for noise reduction

Applies dynamic weighting based on market conditions

Mathematical Foundation

Utilizes Maclaurin series for trigonometric approximation

Implements Ehlers' smoothing principles

Incorporates advanced filtering techniques

Technical Advantages

Signal Processing:

Lag Reduction: Faster signal detection with less delay.

Noise Filtration: Effective elimination of high-frequency noise.

Precision Enhancement: Preservation of critical price movements.

Adaptive Processing: Dynamic response to market volatility.

Visual Enhancements:

Smart color intensity mapping.

Real-time visualization of trend strength.

Adaptive opacity based on movement significance.

Implementation

Core Configuration:

Plot Type: Choose between the original and the Maclaurin enhanced version.

Length: Default set to 30, optimal for daily timeframes.

hpLength: Default set to 10 for enhanced noise reduction.

Advanced Parameters:

The indicator offers advanced control with:

Dual processing modes (Original/Maclaurin).

Dynamic color intensity system.

Customizable smoothing parameters.

Professional Analysis Tools:

Accurate trend reversal identification.

Advanced support/resistance detection.

Superior performance in volatile markets.

Technical Specifications

Maclaurin Series Implementation:

The indicator employs a 5-term Maclaurin series approximation for both sine and cosine, ensuring efficient and accurate computation.

Performance Metrics

Improved processing efficiency.

Reduced memory utilization.

Increased signal accuracy.

Licensing & Attribution

© 2024 Mupsje aka CasaTropical

Professional Credits

Original Ultimate and SuperSmoother concept: John F. Ehlers

Maclaurin enhancement: Casa Tropical (CT)

www.mathsisfun.com

SW monthly Gann Days**Script Description:**

The script you are looking at is based on the work of W.D. Gann, a famous trader and market analyst in the early 20th century, known for his use of geometry, astrology, and numerology in market analysis. Gann believed that certain days in the market had significant importance, and he observed that markets often exhibited significant price moves around specific dates. These dates were typically associated with cyclical patterns in price movements, and Gann referred to these as "Gann Days."

In this script, we have focused on highlighting certain days of the month that Gann believed to have an influence on market behavior. The specific days in question are the **6th to 7th**, **9th to 10th**, **14th to 15th**, **19th to 20th**, **23rd to 24th**, and **29th to 31st** of each month. These ranges are based on Gann’s theory that there are recurring time cycles in the market that cause turning points or critical price movements to occur around certain days of the month.

### **Why Gann Used These Days:**

1. **Mathematical and Astrological Cycles:**

Gann believed that markets were influenced by natural cycles, and that certain dates (or combinations of dates) played a critical role in the price movements. These specific days are part of his broader theory of "time cycles" where the market would often change direction, reverse, or exhibit significant volatility on particular days. Gann's research was based on both mathematical principles and astrological observations, leading him to assign importance to these days.

2. **Gann's Universal Timing Theory:**

According to Gann, financial markets operate in a universe governed by geometric and astrological principles. These cycles repeat themselves over time, and specific days in a given month correspond to key turning points within these repeating cycles. Gann found that the 6th to 7th, 9th to 10th, 14th to 15th, 19th to 20th, 23rd to 24th, and 29th to 31st often marked significant changes in the market, making them particularly important for traders to watch.

3. **Market Psychology and Sentiment:**

These specific days likely correspond to key moments where market participants tend to react in predictable ways, influenced by past market behavior on similar dates. For example, news events or scheduled economic reports might fall within these time windows, causing the market to respond in a particular way. Gann's method involves using these cyclical patterns to predict turning points in market prices, enabling traders to anticipate when the market might make a reversal or face a significant shift in direction.

4. **Turning Points:**

Gann believed that markets often reversed or encountered critical points around specific dates. This is why he considered certain days more important than others. By identifying and focusing on these days, traders can better anticipate the market’s movement and make more informed trading decisions.

5. **Numerology:**

Gann also utilized numerology in his trading system, believing that numbers, and particularly certain key numbers, had significance in predicting market movements. The days selected in this script may correspond to numerological patterns that Gann identified in his analysis of the markets, such as recurring numbers in his astrological and geometric systems.

### **Purpose of the Script:**

This script highlights these "Gann Days" within a trading chart for 2024 and 2025. The color-coding or background highlighting is intended to draw attention to these dates, so traders can observe the potential for significant market movements during these times. By identifying these specific dates, traders following Gann's theories may gain insights into possible turning points, corrections, or key price movements based on the market's historical behavior around these days.

Overall, Gann’s use of specific days was based on his deep belief in the cyclical nature of the market and his attempt to tie those cycles to the natural laws of time, geometry, and astrology. By focusing on these dates, Gann aimed to give traders an edge in predicting significant market events and price shifts.

Follow Through Day (FTD) + Sweep [TrendX_]The Follow Through Day (FTD) + Sweep indicator is a Trend-following tool mixing William O'Neil's original FTD concept and Liquidity concept. This indicator helps you identify potential subsequent bullish trends with greater precision by combining volume analysis, price action, and liquidity concepts.

💎 FEATURES

Follow Through Day Candle (FTD Candle)

The FTD, pioneered by William O'Neil, serves as a reliable signal for identifying the beginning of new bull markets. It's particularly valuable because it combines multiple market factors - price action, volume, and timing - to confirm genuine market reversals rather than temporary bounces.

The power of the FTD lies in its ability to distinguish between ordinary market fluctuations and significant trend changes. By requiring specific criteria to be met across multiple sessions, it helps filter out false signals and identifies high-probability reversal points where institutional investors are likely beginning to accumulate positions.

Sweep Area

The Sweep area feature enhances the traditional FTD concept by incorporating modern liquidity analysis. This overlay identifies zones where large market participants are likely to trigger stop losses before continuing the trend. These areas often represent optimal entry points for traders looking to join the new uptrend with reduced risk.

🔎 BREAKDOWN

FTD Candle

The FTD formation process occurs in two distinct phases: Setup and Completion.

Setup Phase

Strong Market Decline

The market must first experience a significant downtrend

This selling pressure helps clear out weak hands and creates oversold conditions

The decline creates the potential energy for a powerful reversal

First Recovery Session

Marks the initial sign of buying pressure emerging

Often characterized by a strong reversal candle

Represents the first indication that selling pressure may be exhausting

Recovery Confirmation

The second and third days must maintain prices above the new pivot low

This consolidation period helps confirm the validity of the initial bounce

Shows that sellers are no longer in control of price action

Completion Phase:

Supply Test Session

Low volume indicates diminishing selling pressure

Price remains above the pivot low

Creates the foundation for institutional buyers to begin accumulating

Breakout Day

Price increase exceeds average profit of bullish candles

Volume increases by at least 15% compared to previous session

Shows strong institutional commitment to the new uptrend

Timing Window

Must occur between the 4th and 8th candle after First Recovery Session

This specific timing helps confirm the sustainability of the reversal

Based on O'Neil's research of historical market bottoms

FTD Sweep

The Post-FTD Phase introduces the Sweep concept, which is crucial for understanding how large market participants operate. This feature leverages the liquidity concept because institutional traders often need to trigger stop losses to accumulate larger positions at better prices. This helps:

Create liquidity pools for large position entries

Shake out weak hands before continuing the trend

Test the strength of the new trend by absorbing selling pressure

⚙️ USAGE

Sweep + TP & SL Strategy

Example: BTCUSDT (1D) - Replay back to 9th November 2024

After an FTD candle forms, traders can adopt a systematic approach to enhance their trading strategy. First, they should determine the swing range and convert the post-FTD zone into concrete stop loss and take profit levels, which are based on the price action during the FTD formation. Next, traders should wait for a sweep formation, as this indicates that institutional players are accumulating positions. A quick price rejection from the sweep level should be observed before executing an entry.

The reasoning behind this strategy is rooted in market microstructure. By waiting for the sweep, traders position themselves alongside institutional players who need to build large positions without causing adverse price movement. The sweep creates the liquidity they need, and the subsequent move often represents the true trend continuation.

DISCLAIMER

This indicator is not financial advice, it can only help traders make better decisions. There are many factors and uncertainties that can affect the outcome of any endeavor, and no one can guarantee or predict with certainty what will occur. Therefore, one should always exercise caution and judgment when making decisions based on past performance.

MERRY CHRISTMAS HAPPY 2025 Year [TradingFinder]🎅🎄✨ Merry Christmas and Happy New Year 2025! 🎉✨

As we bid farewell to 2024 and welcome the fresh opportunities of 2025, we want to send our warmest wishes to all the amazing TradingView users, Pine Script developers, and loyal followers of TradingFinder.

Your enthusiasm and support have made this community stronger and more inspiring every day. May this holiday season bring you happiness, success, and prosperity both in life and in trading.

We also wish for all of you to make great profits and achieve your financial goals in the new year. Let's make 2025 a year filled with innovation, growth, and great achievements together.

Thank you for being part of this journey! 🎅🌟📈

Bitcoin Logarithmic Regression BandsOverview

This indicator displays logarithmic regression bands for Bitcoin. Logarithmic regression is a statistical method used to model data where growth slows down over time. I initially created these bands in 2019 using a spreadsheet, and later coded them in TradingView in 2021. Over time, the bands proved effective at capturing Bitcoin's bull market peaks and bear market lows. In 2024, I decided to share this indicator because I believe these logarithmic regression bands offer the best fit for the Bitcoin chart.

How It Works

The logarithmic regression lines are fitted to the Bitcoin (BTCUSD) chart using two key factors: the 'a' factor (slope) and the 'b' factor (intercept). The two lines in the upper and lower bands share the same 'a' factor, but I adjust the 'b' factor by 0.2 to more accurately capture the bull market peaks and bear market lows. The formula for logaritmic regression is 10^((a * ln) - b).

How to Use the Logarithmic Regression Bands

1. Lower Band (Support Band):

The two lines in the lower band create a potential support area for Bitcoin’s price. Historically, Bitcoin’s price has always found its lows within this band during past market cycles. When the price is within the lower band, it suggests that Bitcoin is undervalued and could be set for a rebound.

2. Upper Band (Resistance Band):

The two lines in the upper band create a potential resistance area for Bitcoin’s price. Bitcoin has consistently reached its highs in this band during previous market cycles. If the price is within the upper band, it indicates that Bitcoin is overvalued, and a potential price correction may be imminent.

Use Cases

- Price Bottoming:

Bitcoin tends to bottom out at the lower band before entering a prolonged bull market or a period of sideways movement.

- Price Topping:

In reverse, Bitcoin tends to top out at the upper band before entering a bear market phase.

- Profitable Strategy:

Buying at the lower band and selling at the upper band can be a profitable trading strategy, as these bands often indicate key price levels for Bitcoin’s market cycles.

Line Break Chart StrategyHello All!

We should not pass this year without a gift!

My last publication in 2024 is Complete Line Break Chart Strategy with many features!

What is Line Break Chart?

" Line Break is a Japanese chart style that disregards time intervals and only focuses on price movements, similar to the Kagi and Renko chart styles. Line Break charts form a series of up and down bars (referred to as lines). Up lines represent rising prices, and down lines represent falling prices. New confirmed lines only form on the chart when closing prices break the range covered by previous lines. Users can control the number of past lines used in the calculation via the "Number of Lines" input in the chart settings. The typical "Number of Lines" setting is 3, meaning the chart forms a new up line when the closing price is above the high prices of the last three lines, and it forms a new down line when the closing price is below the past three lines' low prices. If the current price is higher, it is an up line and if it is lower, it is a down line. If the current closing price is the same or the move in the opposite direction is not large enough to warrant a reversal, l then no new line is draw n" by Tradingview. You can find it here

Now let's start examining the features of the indicator:

By using Line break reversals it shows trend on the main chart. You can create alert .

Moreover, you can decide which trade should be taken by using Risk Management in the indicator. You can set the " Maximum Risk " and then if the risk is more than you set then the trade is not taken. When trend changed it checks the distance between reversal level and open price and compare it with the Maximum Risk

Breakout:

It can find breakouts and shows on the chart. You can create alert for breakouts

It can show breakouts on the main chart:

Flip-Flops:

Upon looking at set of price break charts, the trader will notice that there are instances when uptrend blocks is followed by one reversal block, and then by a reversal to a series of uptrend blocks. The opposite is also possible: a series of downtrend blocks is followed by one reversal box and then by an immediate reversal to downtrend. This price action is called a " Flip-Flop ". This structure usually produces trend continuation signal. when we see this then we better use Buy/Sell stop order. lets see this on the chart:

Temporal Sequence Table:

Sequence frequency shows the frequency distribution of the number of sequential highs and the number of sequential lows that have been generated. This is quite important to the trader who is seeking to join a trend or put on a trade when the price break reverses into a new trend direction. For example, if the pattern over the past year has been that there never were more than nine consecutive high closes, it would make sense not to enter a position late into the sequence of new high closes.

also you can see market structure. I have tried to formalize it and show it under the table. so you can understand if it's choppy market.

"Number of Lines" has very important role. While using low time frames such seconds/minutes time frame you may want to choose higher number of lines such 5,6. ( this may minimize the risk of a whipsaw )

Gaps feature:

You can set Gaps on/off. if Gaps on then you can see how long it takes for each box

Reversal and Continuation Probability:

The script calculated Reversal level and Continuation probability of the trend by using Sequence frequency.

It also shows unconfirmed box and current closing price level:

Last but not least it has Overlay option for all items, and can show all items in the main chart!

P.S. I added alerts :)

Wish you all a happy new year!

Enjoy!

Merry Christmas Tree🎄 Merry Christmas 2024 🎅

May your holidays sparkle with joy and laughter, and may the year ahead be full of blessings and success. Wishing you and your loved ones peace, love, and happiness this Christmas and always! 🌟🎁

BKLevelsThis displays levels from a text input, levels from certain times on the previous day, and high/low/close from previous day. The levels are drawn for the date in the first line of the text input. Newlines are required between each level

Example text input:

2024-12-17

SPY,606,5,1,Lower Hvol Range,FIRM

SPY,611,1,1,Last 20K CBlock,FIRM

SPY,600,2,1,Last 20K PBlock,FIRM

SPX,6085,1,1,HvolC,FIRM

SPX,6080,2,1,HvolP,FIRM

SPX,6095,3,1,Upper PDVR,FIRM

SPX,6060,3,1,Lower PDVR,FIRM

For each line, the format is ,,,,,

For color, there are 9 possible user- configurable colors- so you can input numbers 1 through 9

For line style, the possible inputs are:

"FIRM" -> solid line

"SHORT_DASH" -> dotted line

"MEDIUM_DASH" -> dashed line

"LONG_DASH" -> dashed line

Options Series - Anchored VWAP Ribbon➤ AVWAP On different chart symbols:

⭐ Overview and Key Features:

Anchored VWAP Calculation:

The script implements the Anchored Volume Weighted Average Price (AVWAP), a tool used by professional traders to identify key price levels weighted by volume, starting from a specific timestamp (anchor point).

Bullish and Bearish Analysis:

It determines the dominance of bullish or bearish momentum based on the relationship between the close price and AVWAP levels across multiple time points.

Dynamic Visualization:

The background of the chart changes color based on overall bullish or bearish sentiment, making it easier to interpret market trends.

Multi-Time Anchors:

By defining multiple anchor points (e.g., 09:15, 09:20), the script calculates a series of AVWAP values for fine-grained intraday analysis.

Customizable Inputs:

Users can select the source price (e.g., hlc3), date, and time for AVWAP calculation.

⭐ How It Works and Functionality:

AVWAP Logic:

Uses the timestamp() function to establish a reference (anchor point).

Calculates the cumulative weighted price (price * volume) and cumulative volume from this anchor point.

The ratio of these sums gives the AVWAP, which updates dynamically with new bars.

Bullish and Bearish Signals:

Binary flags (1 or 0) are set for each time point depending on whether the closing price is above or below the AVWAP for that time.

Aggregates these flags into AVWAP_bull and AVWAP_bear to represent the overall market sentiment.

Decision Logic:

Determines final market conditions (bullish or bearish dominance) based on aggregated scores.

Visual feedback (background and bar colors) is applied accordingly.

⭐ Visualizations and User Experience:

Background Colors:

Green or red background highlights the overall sentiment (bullish or bearish), providing a quick market overview.

Bar Coloring:

Bars are color-coded based on bullish, bearish, or neutral conditions, making it easier to identify trends directly on the chart.

AVWAP Levels:

The calculated AVWAP values are plotted as colored lines for each anchor point, giving precise intraday levels of significance.

Bright colors (fluorescent green/red) are used for additional clarity when the close price is above or below these levels.

🎨 Settings and Customization:

Anchor Point:

Fully customizable anchor points allow users to set specific dates and times (e.g., 09:15 on December 13, 2024) for AVWAP calculations.

Source Price:

Users can choose from hlc3, close, or any other price source to calculate the AVWAP, tailoring the indicator to their strategy.

Visual Appearance:

The transparency, colors, and line styles are adjustable, enabling users to customize the chart to match their trading preferences.

Dynamic Signals:

The script accommodates numerous AVWAP levels, providing flexibility for scalpers and swing traders alike.

⭐ Uniqueness of the Concept:

Precise Intraday Analysis:

Unlike static VWAP, this script allows anchoring to specific times during the day, offering granular insights into market behavior.

Cumulative Sentiment Approach:

Aggregates signals across multiple time intervals, providing a comprehensive view of intraday momentum rather than a single-point reference.

Blending AVWAP with Visual Feedback:

Combines traditional AVWAP calculations with visually impactful features like background shading and bar coloring to enhance decision-making.

Scalability:

Supports adding multiple additional anchor points and customization for broader applicability in different market conditions.

🚀 Conclusion:

The Anchored VWAP Ribbon script is a powerful tool for traders seeking to analyze price behavior relative to volume-weighted levels anchored at specific times. It provides a visually intuitive way to assess intraday market sentiment, combining traditional technical indicators with customizable visualization features. The script’s flexibility makes it suitable for a variety of trading styles, from scalping to swing trading, while its unique cumulative sentiment logic sets it apart from conventional VWAP tools.

5x Volume indicator - Day Trading5x Volume Screener - Day Trading

Version: 6.0

Description:

This indicator is designed to identify significant volume spikes in crypto and stock markets,

specifically targeting instances where volume exceeds 5x the average of a 10-period Simple Moving Average (SMA) as the baseline.

Perfect for day traders and momentum traders looking for high-volume breakout opportunities.

Key Features:

Tracks real-time volume compared to 5-period moving average

Visual alerts through green histogram bars for 5x volume spikes

Dynamic volume ratio display showing exact multiple of average volume

Clear threshold line for quick reference

Optional labels showing precise volume ratios

Benefits:

Instantly spot unusual volume activity

Identify potential breakout opportunities

Validate price movements with volume confirmation

Perfect for day trading and scalping

Works across multiple timeframes

Best Used For:

Day trading setups

Breakout trading

Volume confirmation

Momentum trading

Market reversal identification

Created by: CigarSavant

Last Updated: December 2024

Employee Portfolio Generator [By MUQWISHI]▋ INTRODUCTION :

The “Employee Portfolio Generator” simplifies the process of building a long-term investment portfolio tailored for employees seeking to build wealth through investments rather than traditional bank savings. The tool empowers employees to set up recurring deposits at customizable intervals, enabling to make additional purchases in a list of preferred holdings, with the ability to define the purchasing investment weight for each security. The tool serves as a comprehensive solution for tracking portfolio performance, conducting research, and analyzing specific aspects of portfolio investments. The output includes an index value, a table of holdings, and chart plots, providing a deeper understanding of the portfolio's historical movements.

_______________________

▋ OVERVIEW:

● Scenario (The chart above can be taken as an example) :

Let say, in 2010, a newly employed individual committed to saving $1,000 each month. Rather than relying on a traditional savings account, chose to invest the majority of monthly savings in stable well-established stocks. Allocating 30% of monthly saving to AMEX:SPY and another 30% to NASDAQ:QQQ , recognizing these as reliable options for steady growth. Additionally, there was an admired toward innovative business models of NASDAQ:AAPL , NASDAQ:MSFT , NASDAQ:AMZN , and NASDAQ:EBAY , leading to invest 10% in each of those companies. By the end of 2024, after 15 years, the total monthly deposits amounted to $179,000, which would have been the result of traditional saving alone. However, by sticking into long term invest, the value of the portfolio assets grew, reaching nearly $900,000.

_______________________

▋ OUTPUTS:

The table can be displayed in three formats:

1. Portfolio Index Title: displays the index name at the top, and at the bottom, it shows the index value, along with the chart timeframe, e.g., daily change in points and percentage.

2. Specifications: displays the essential information on portfolio performance, including the investment date range, total deposits, free cash, returns, and assets.

3. Holdings: a list of the holding securities inside a table that contains the ticker, last price, entry price, return percentage of the portfolio's total deposits, and latest weighted percentage of the portfolio. Additionally, a tooltip appears when the user passes the cursor over a ticker's cell, showing brief information about the company, such as the company's name, exchange market, country, sector, and industry.

4. Indication of New Deposit: An indication of a new deposit added to the portfolio for additional purchasing.

5. Chart: The portfolio's historical movements can be visualized in a plot, displayed as a bar chart, candlestick chart, or line chart, depending on the preferred format, as shown below.

_______________________

▋ INDICATOR SETTINGS:

Section(1): Table Settings

(1) Naming the index.

(2) Table location on the chart and cell size.

(3) Sorting Holdings Table. By securities’ {Return(%) Portfolio, Weight(%) Portfolio, or Ticker Alphabetical} order.

(4) Choose the type of index: {Assets, Return, or Return (%)}, and the plot type for the portfolio index: {Candle, Bar, or Line}.

(5) Positive/Negative colors.

(6) Table Colors (Title, Cell, and Text).

(7) To show/hide any of selected indicator’s components.

Section(2): Recurring Deposit Settings

(1) From DateTime of starting the investment.

(2) To DateTime of ending the investment

(3) The amount of recurring deposit into portfolio and currency.

(4) The frequency of recurring deposits into the portfolio {Weekly, 2-Weeks, Monthly, Quarterly, Yearly}

(5) The Depositing Model:

● Fixed: The amount for recurring deposits remains constant throughout the entire investment period.

● Increased %: The recurring deposit amount increases at the selected frequency and percentage throughout the entire investment period.

(5B) If the user selects “ Depositing Model: Increased % ”, specify the growth model (linear or exponential) and define the rate of increase.

Section(3): Portfolio Holdings

(1) Enable a ticker in the investment portfolio.

(2) The selected deposit frequency weight for a ticker. For example, if the monthly deposit is $1,000 and the selected weight for XYZ stock is 30%, $300 will be used to purchase shares of XYZ stock.

(3) Select up to 6 tickers that the investor is interested in for long-term investment.

Please let me know if you have any questions

Ticker Tape with Multiple Inputs# Ticker Tape

A customizable multi-symbol price tracker that displays real-time price information in a scrolling ticker format, similar to financial news tickers.

This indicator is inspired from Tradingciew's default tickertape indicator with changes in the way inputs are given.

### Overview

This indicator allows you to monitor up to 15 different symbols simultaneously across any supported exchanges on TradingView. It displays essential price information including current price, price change, and percentage change in an easy-to-read format at the bottom of your chart.

### Features

• Monitor up to 15 different symbols simultaneously

• Support for any exchange available on TradingView

• Real-time price updates

• Color-coded price changes (green for increase, red for decrease)

• Smooth scrolling animation (can be disabled)

• Customizable scroll speed and position offset

### Input Parameters

#### Ticker Tape Controls

• Running: Enable/disable the scrolling animation

• Offset: Adjust the starting position of the ticker tape

#### Symbol Settings

• Exchange (1-15): Enter the exchange name (e.g., NSE, BINANCE, NYSE)

• Symbol (1-15): Enter the symbol name (e.g., BANKNIFTY, RELIANCE, BTCUSDT)

### Display Format

For each symbol, the ticker shows:

1. Symbol Name

2. Current Price

3. Price Change (Absolute and Percentage)

### Example Usage

Input Settings:

Exchange 1: NSE

Symbol 1: BANKNIFTY

Exchange 2: NSE

Symbol 2: RELIANCE

The ticker tape will display:

`NIFTY BANK 46750.00 +350.45 (0.75%) | RELIANCE 2456.85 -12.40 (-0.50%) |`

### Use Cases

1. Multi-Market Monitoring: Track different markets simultaneously without switching between charts

2. Portfolio Tracking: Monitor all your positions in real-time

### Tips for Best Use

1. Group related symbols together for easier monitoring

2. Use the offset parameter to position important symbols in your preferred viewing area

3. Disable scrolling if you prefer a static display

4. Leave exchange field empty for default exchange symbols

### Notes

• Price updates occur in real-time during market hours

• Color coding helps quickly identify price direction

• The indicator adapts to any chart timeframe

• Empty input pairs are automatically skipped

### Performance Considerations

The indicator is optimized for efficiency, but monitoring too many high-frequency symbols might impact chart performance. It's recommended to use only the symbols you actively need to monitor.

Version: 2.0 Stock_Cloud

Last Updated: December 2024

Kalman Filter Oscillator v4The Kalman Filter Oscillator v4 is an advanced tool designed to help traders and investors identify trends more effectively while reducing the impact of market noise. As the latest iteration in its development, this version integrates improvements that make it more adaptive and precise, catering to the challenges of today’s financial markets.

This indicator operates on the principle of the Kalman filter, a well-regarded mathematical approach used for estimating the state of a dynamic system. By filtering out random fluctuations, it smooths price data to provide clearer insights into underlying trends. Unlike traditional methods such as moving averages, which often lag and can miss rapid shifts, the Kalman Filter Oscillator is reactive in real time, making it particularly suited for dynamic markets.

Version v4 builds on earlier versions by offering a refined combination of short-term and long-term trend analysis. Through adjustable parameters, traders can balance sensitivity to immediate price changes with a broader perspective of the market direction. Additionally, the oscillator incorporates a unique feature that tracks a price’s position relative to its recent highs and lows, which enhances its ability to pinpoint potential turning points or key market conditions.

The indicator’s value lies in its adaptability and practicality. Traders can use it to confirm trends, identify overbought or oversold conditions, or smooth out erratic price movements, reducing the likelihood of false signals. By presenting information in a clear and actionable format, it allows users to make better-informed decisions with greater confidence.

As of late 2024, the Kalman Filter Oscillator v4 represents a sophisticated yet user-friendly advancement in trend analysis. While not a one-size-fits-all solution, it serves as a valuable component in a trader’s toolkit, complementing other strategies and enhancing overall market understanding.

Alans Date Range CalculatorOverview

Setting a date range for backtesting enables you to evaluate your trading strategy under various market conditions. Traders can test a strategy’s performance during specific periods, such as economic downturns, bull markets, or periods of high volatility. This helps assess the trading strategy’s robustness and adaptability across different scenarios.

Specifying years of data instead of just inputting specific start and end dates offers several advantages:

1. **Consistency**: Using a fixed number of years ensures that the testing period is consistent across different strategies or iterations. This makes it easier to compare performance metrics and draw meaningful conclusions.

2. **Flexibility**: Specifying years allows for automatic adjustment of the start date based on the current date or selected end date. This is particularly useful when new data becomes available or when testing on different assets with varying historical data lengths.

3. **Efficiency**: It simplifies updating and retesting strategies. Instead of recalculating specific start dates each time, traders can quickly adjust the number of years to process, making it easier to test strategies over different timeframes.

4. **Comprehensive Analysis**: Broader timeframes defined by years help you evaluate how your strategy performs over multiple market cycles, providing insights into long-term viability and potential weaknesses.

Defining a date range by specifying years allows for more thorough and systematic backtesting, helping traders develop more reliable and effective trading systems.

Alan's Date Range Calculator: A TradingView Pine Script Indicator

Purpose

This Pine Script indicator calculates and displays a date range for backtesting trading strategies. It allows users to specify the number of years to analyze and an end date, then calculates the corresponding start date. Most importantly, users can copy the inputs and function into their own strategies to quickly add a time span feature for backtesting.

Key Features

User-defined input for the number of years to analyze

Customizable end date with a calendar input

Automatic calculation of the start date

Visual display of both start and end dates on the chart

How It Works

User Inputs

Years of Data to Process: An integer input allowing users to specify the number of years for analysis (default: 20, range: 1-100)

End Date: A calendar input for selecting the end date of the analysis period (default: December 31, 2024)

Date Calculation

The script uses a custom function calcStartDate() to determine the start date. It subtracts the specified number of years from the end date's year and sets the start date to January 1st of that year.

Visual Output

The indicator displays two labels on the chart:

Start Date Label: Shows the calculated start date

End Date Label: Displays the user-specified end date

Both labels are positioned horizontally at the bottom of the chart, with the end date label to the right of the start date label.

Applications

This indicator is particularly useful for traders who want to:

Define specific date ranges for backtesting strategies

Quickly visualize the time span of their analysis

Ensure consistent testing periods across different strategies or assets

Customization

Users can easily adjust the analysis period by changing the number of years or selecting a different end date. This flexibility allows for testing strategies across various market conditions and time frames.

MACD, ADX & RSI -> for altcoins# MACD + ADX + RSI Combined Indicator

## Overview

This advanced technical analysis tool combines three powerful indicators (MACD, ADX, and RSI) into a single view, providing a comprehensive analysis of trend, momentum, and divergence signals. The indicator is designed to help traders identify potential trading opportunities by analyzing multiple aspects of price action simultaneously.

## Components

### 1. MACD (Moving Average Convergence Divergence)

- **Purpose**: Identifies trend direction and momentum

- **Components**:

- Fast EMA (default: 12 periods)

- Slow EMA (default: 26 periods)

- Signal Line (default: 9 periods)

- Histogram showing the difference between MACD and Signal line

- **Visual**:

- Blue line: MACD line

- Orange line: Signal line

- Green/Red histogram: MACD histogram

- **Interpretation**:

- Histogram color changes indicate potential trend shifts

- Crossovers between MACD and Signal lines suggest entry/exit points

### 2. ADX (Average Directional Index)

- **Purpose**: Measures trend strength and direction

- **Components**:

- ADX line (default threshold: 20)

- DI+ (Positive Directional Indicator)

- DI- (Negative Directional Indicator)

- **Visual**:

- Navy blue line: ADX

- Green line: DI+

- Red line: DI-

- **Interpretation**:

- ADX > 20 indicates a strong trend

- DI+ crossing above DI- suggests bullish momentum

- DI- crossing above DI+ suggests bearish momentum

### 3. RSI (Relative Strength Index)

- **Purpose**: Identifies overbought/oversold conditions and divergences

- **Components**:

- RSI line (default: 14 periods)

- Divergence detection

- **Visual**:

- Purple line: RSI

- Horizontal lines at 70 (overbought) and 30 (oversold)

- Divergence labels ("Bull" and "Bear")

- **Interpretation**:

- RSI > 70: Potentially overbought

- RSI < 30: Potentially oversold

- Bullish/Bearish divergences indicate potential trend reversals

## Alert System

The indicator includes several automated alerts:

1. **MACD Alerts**:

- Rising to falling histogram transitions

- Falling to rising histogram transitions

2. **RSI Divergence Alerts**:

- Bullish divergence formations

- Bearish divergence formations

3. **ADX Trend Alerts**:

- Strong trend development (ADX crossing threshold)

- DI+ crossing above DI- (bullish)

- DI- crossing above DI+ (bearish)

## Settings Customization

All components can be fine-tuned through the settings panel:

### MACD Settings

- Fast Length

- Slow Length

- Signal Smoothing

- Source

- MA Type options (SMA/EMA)

### ADX Settings

- Length

- Threshold level

### RSI Settings

- RSI Length

- Source

- Divergence calculation toggle

## Usage Guidelines

### Entry Signals

Strong entry signals typically occur when multiple components align:

1. MACD histogram color change

2. ADX showing strong trend (>20)

3. RSI showing divergence or leaving oversold/overbought zones

### Exit Signals

Consider exits when:

1. MACD crosses signal line in opposite direction

2. ADX shows weakening trend

3. RSI reaches extreme levels with divergence

### Risk Management

- Use the indicator as part of a complete trading strategy

- Combine with price action and support/resistance levels

- Consider multiple timeframe analysis for confirmation

- Don't rely solely on any single component

## Technical Notes

- Built for TradingView using Pine Script v5

- Compatible with all timeframes

- Optimized for real-time calculation

- Includes proper error handling and NA value management

- Memory-efficient calculations for smooth performance

## Installation

1. Copy the provided Pine Script code

2. Open TradingView Chart

3. Create New Indicator -> Pine Editor

4. Paste the code and click "Add to Chart"

5. Adjust settings as needed through the indicator settings panel

## Version Information

- Version: 2.0

- Last Updated: November 2024

- Platform: TradingView

- Language: Pine Script v5