ICT TIME ELEMENTS [KaninFX]## Overview

The ICT Time Elements indicator is a comprehensive trading tool designed to visualize the most critical market sessions and timeframes according to Inner Circle Trader (ICT) methodology. This indicator helps traders identify high-probability trading opportunities by highlighting key market sessions, killzones, and liquidity periods throughout the trading day.

## Key Features

### 🕐 Complete ICT Time Framework

- **Asian Range**: 8:00 PM - 12:00 AM (NY Time) - Evening consolidation period

- **London Killzone**: 2:00 AM - 5:00 AM (NY Time) - European market opening liquidity

- **NY Killzone**: 7:00 AM - 10:00 AM (NY Time) - US market opening with high volatility

- **Silver Bullet Sessions**:

- London Silver Bullet: 3:00 AM - 4:00 AM

- AM Silver Bullet: 10:00 AM - 11:00 AM

- PM Silver Bullet: 2:00 PM - 3:00 PM

- **Lunch Hours**: 5:00 AM - 7:00 AM & 12:00 PM - 1:00 PM (Lower volatility periods)

- **News Embargo**: 8:30 AM - 9:30 AM (High impact news release window)

- **20-Minute Macros**: :50 to :10 minutes of each hour (Short-term reversal periods)

- **True Day Close**: 4:00 PM - 4:30 PM (Official market close)

### 🎨 Visual Customization

- **Multiple Themes**: Dark, Light, and Custom color schemes

- **Adjustable Opacity**: Control zone transparency (0-100%)

- **Font Customization**: Tiny, Small, Normal, Large text sizes

- **Custom Colors**: Personalize each zone with your preferred colors

- **Professional Display**: Clean histogram visualization with zone labels

### 🌍 Multi-Timezone Support

Built-in support for major trading centers:

- America/New_York (Default)

- America/Chicago

- America/Los_Angeles

- Europe/London

- Asia/Tokyo

- Asia/Shanghai

- Australia/Sydney

### 📊 Smart Information Display

- **Real-time Zone Detection**: Automatically identifies current active session

- **Zone Labels**: Clear labeling at the center of each time period

- **Current Zone Indicator**: Arrow pointer showing the active session

- **Comprehensive Info Table**: Quick reference for all time zones and their schedules

- **Flexible Table Positioning**: Place info table in any corner of your chart

### ⚡ Performance Optimized

- **Memory Management**: Automatic cleanup of old labels to maintain performance

- **Efficient Processing**: Optimized time calculations for smooth operation

- **Resource Control**: Limited label generation to prevent system overload

## How It Works

The indicator continuously monitors the current time against predefined ICT session schedules. When price action enters a recognized time zone, the indicator:

1. **Highlights the Period**: Colors the histogram bar according to the active session

2. **Labels the Zone**: Places descriptive text identifying the current market condition

3. **Updates Info Table**: Shows current session status and complete schedule

4. **Tracks Macro Periods**: Identifies 20-minute reversal windows within major sessions

### Special Features

- **Macro Detection**: Automatically identifies when current time falls within a 20-minute macro period

- **Session Overlap Handling**: Properly manages overlapping time zones with priority logic

- **Dynamic Color Adjustment**: Theme-aware color selection for optimal visibility

## Best Use Cases

### For ICT Traders

- Identify optimal entry times during killzone sessions

- Recognize silver bullet opportunities for quick scalps

- Avoid trading during lunch hour consolidations

- Prepare for news embargo volatility

### For Session Traders

- Track major market session transitions

- Plan trading strategy around high-liquidity periods

- Understand global market flow and timing

### For Swing Traders

- Identify macro trend continuation points

- Time position entries during optimal sessions

- Understand market structure changes across sessions

## Installation & Setup

1. Add the indicator to your TradingView chart

2. Select your preferred timezone from the dropdown

3. Choose theme (Dark/Light) or customize colors

4. Adjust font size and table position to your preference

5. Enable/disable features as needed for your trading style

## Pro Tips

- **Combine with Price Action**: Use time zones alongside support/resistance levels

- **Focus on Killzones**: Highest probability setups occur during London and NY killzones

- **Watch Silver Bullets**: These 1-hour windows often provide excellent reversal opportunities

- **Respect Lunch Hours**: Lower volatility periods - consider smaller position sizes

- **News Embargo Awareness**: Prepare for potential whipsaws during 8:30-9:30 AM

## Conclusion

The ICT Time Elements indicator transforms complex ICT timing concepts into an easy-to-read visual tool. Whether you're a beginner learning ICT methodology or an experienced trader looking to optimize your timing, this indicator provides the essential market session awareness needed for successful trading.

*Compatible with all TradingView plans and timeframes. Works best on 1-minute to 1-hour charts for optimal session visualization.*

在腳本中搜尋"A股+股票筛选器+10元以下"

Bear Market Probability Model# Bear Market Probability Model: A Multi-Factor Risk Assessment Framework

The Bear Market Probability Model represents a comprehensive quantitative framework for assessing systemic market risk through the integration of 13 distinct risk factors across four analytical categories: macroeconomic indicators, technical analysis factors, market sentiment measures, and market breadth metrics. This indicator synthesizes established financial research methodologies to provide real-time probabilistic assessments of impending bear market conditions, offering institutional-grade risk management capabilities to retail and professional traders alike.

## Theoretical Foundation

### Historical Context of Bear Market Prediction

Bear market prediction has been a central focus of financial research since the seminal work of Dow (1901) and the subsequent development of technical analysis theory. The challenge of predicting market downturns gained renewed academic attention following the market crashes of 1929, 1987, 2000, and 2008, leading to the development of sophisticated multi-factor models.

Fama and French (1989) demonstrated that certain financial variables possess predictive power for stock returns, particularly during market stress periods. Their three-factor model laid the groundwork for multi-dimensional risk assessment, which this indicator extends through the incorporation of real-time market microstructure data.

### Methodological Framework

The model employs a weighted composite scoring methodology based on the theoretical framework established by Campbell and Shiller (1998) for market valuation assessment, extended through the incorporation of high-frequency sentiment and technical indicators as proposed by Baker and Wurgler (2006) in their seminal work on investor sentiment.

The mathematical foundation follows the general form:

Bear Market Probability = Σ(Wi × Ci) / ΣWi × 100

Where:

- Wi = Category weight (i = 1,2,3,4)

- Ci = Normalized category score

- Categories: Macroeconomic, Technical, Sentiment, Breadth

## Component Analysis

### 1. Macroeconomic Risk Factors

#### Yield Curve Analysis

The inclusion of yield curve inversion as a primary predictor follows extensive research by Estrella and Mishkin (1998), who demonstrated that the term spread between 3-month and 10-year Treasury securities has historically preceded all major recessions since 1969. The model incorporates both the 2Y-10Y and 3M-10Y spreads to capture different aspects of monetary policy expectations.

Implementation:

- 2Y-10Y Spread: Captures market expectations of monetary policy trajectory

- 3M-10Y Spread: Traditional recession predictor with 12-18 month lead time

Scientific Basis: Harvey (1988) and subsequent research by Ang, Piazzesi, and Wei (2006) established the theoretical foundation linking yield curve inversions to economic contractions through the expectations hypothesis of the term structure.

#### Credit Risk Premium Assessment

High-yield credit spreads serve as a real-time gauge of systemic risk, following the methodology established by Gilchrist and Zakrajšek (2012) in their excess bond premium research. The model incorporates the ICE BofA High Yield Master II Option-Adjusted Spread as a proxy for credit market stress.

Threshold Calibration:

- Normal conditions: < 350 basis points

- Elevated risk: 350-500 basis points

- Severe stress: > 500 basis points

#### Currency and Commodity Stress Indicators

The US Dollar Index (DXY) momentum serves as a risk-off indicator, while the Gold-to-Oil ratio captures commodity market stress dynamics. This approach follows the methodology of Akram (2009) and Beckmann, Berger, and Czudaj (2015) in analyzing commodity-currency relationships during market stress.

### 2. Technical Analysis Factors

#### Multi-Timeframe Moving Average Analysis

The technical component incorporates the well-established moving average convergence methodology, drawing from the work of Brock, Lakonishok, and LeBaron (1992), who provided empirical evidence for the profitability of technical trading rules.

Implementation:

- Price relative to 50-day and 200-day simple moving averages

- Moving average convergence/divergence analysis

- Multi-timeframe MACD assessment (daily and weekly)

#### Momentum and Volatility Analysis

The model integrates Relative Strength Index (RSI) analysis following Wilder's (1978) original methodology, combined with maximum drawdown analysis based on the work of Magdon-Ismail and Atiya (2004) on optimal drawdown measurement.

### 3. Market Sentiment Factors

#### Volatility Index Analysis

The VIX component follows the established research of Whaley (2009) and subsequent work by Bekaert and Hoerova (2014) on VIX as a predictor of market stress. The model incorporates both absolute VIX levels and relative VIX spikes compared to the 20-day moving average.

Calibration:

- Low volatility: VIX < 20

- Elevated concern: VIX 20-25

- High fear: VIX > 25

- Panic conditions: VIX > 30

#### Put-Call Ratio Analysis

Options flow analysis through put-call ratios provides insight into sophisticated investor positioning, following the methodology established by Pan and Poteshman (2006) in their analysis of informed trading in options markets.

### 4. Market Breadth Factors

#### Advance-Decline Analysis

Market breadth assessment follows the classic work of Fosback (1976) and subsequent research by Brown and Cliff (2004) on market breadth as a predictor of future returns.

Components:

- Daily advance-decline ratio

- Advance-decline line momentum

- McClellan Oscillator (Ema19 - Ema39 of A-D difference)

#### New Highs-New Lows Analysis

The new highs-new lows ratio serves as a market leadership indicator, based on the research of Zweig (1986) and validated in academic literature by Zarowin (1990).

## Dynamic Threshold Methodology

The model incorporates adaptive thresholds based on rolling volatility and trend analysis, following the methodology established by Pagan and Sossounov (2003) for business cycle dating. This approach allows the model to adjust sensitivity based on prevailing market conditions.

Dynamic Threshold Calculation:

- Warning Level: Base threshold ± (Volatility × 1.0)

- Danger Level: Base threshold ± (Volatility × 1.5)

- Bounds: ±10-20 points from base threshold

## Professional Implementation

### Institutional Usage Patterns

Professional risk managers typically employ multi-factor bear market models in several contexts:

#### 1. Portfolio Risk Management

- Tactical Asset Allocation: Reducing equity exposure when probability exceeds 60-70%

- Hedging Strategies: Implementing protective puts or VIX calls when warning thresholds are breached

- Sector Rotation: Shifting from growth to defensive sectors during elevated risk periods

#### 2. Risk Budgeting

- Value-at-Risk Adjustment: Incorporating bear market probability into VaR calculations

- Stress Testing: Using probability levels to calibrate stress test scenarios

- Capital Requirements: Adjusting regulatory capital based on systemic risk assessment

#### 3. Client Communication

- Risk Reporting: Quantifying market risk for client presentations

- Investment Committee Decisions: Providing objective risk metrics for strategic decisions

- Performance Attribution: Explaining defensive positioning during market stress

### Implementation Framework

Professional traders typically implement such models through:

#### Signal Hierarchy:

1. Probability < 30%: Normal risk positioning

2. Probability 30-50%: Increased hedging, reduced leverage

3. Probability 50-70%: Defensive positioning, cash building

4. Probability > 70%: Maximum defensive posture, short exposure consideration

#### Risk Management Integration:

- Position Sizing: Inverse relationship between probability and position size

- Stop-Loss Adjustment: Tighter stops during elevated risk periods

- Correlation Monitoring: Increased attention to cross-asset correlations

## Strengths and Advantages

### 1. Comprehensive Coverage

The model's primary strength lies in its multi-dimensional approach, avoiding the single-factor bias that has historically plagued market timing models. By incorporating macroeconomic, technical, sentiment, and breadth factors, the model provides robust risk assessment across different market regimes.

### 2. Dynamic Adaptability

The adaptive threshold mechanism allows the model to adjust sensitivity based on prevailing volatility conditions, reducing false signals during low-volatility periods and maintaining sensitivity during high-volatility regimes.

### 3. Real-Time Processing

Unlike traditional academic models that rely on monthly or quarterly data, this indicator processes daily market data, providing timely risk assessment for active portfolio management.

### 4. Transparency and Interpretability

The component-based structure allows users to understand which factors are driving risk assessment, enabling informed decision-making about model signals.

### 5. Historical Validation

Each component has been validated in academic literature, providing theoretical foundation for the model's predictive power.

## Limitations and Weaknesses

### 1. Data Dependencies

The model's effectiveness depends heavily on the availability and quality of real-time economic data. Federal Reserve Economic Data (FRED) updates may have lags that could impact model responsiveness during rapidly evolving market conditions.

### 2. Regime Change Sensitivity

Like most quantitative models, the indicator may struggle during unprecedented market conditions or structural regime changes where historical relationships break down (Taleb, 2007).

### 3. False Signal Risk

Multi-factor models inherently face the challenge of balancing sensitivity with specificity. The model may generate false positive signals during normal market volatility periods.

### 4. Currency and Geographic Bias

The model focuses primarily on US market indicators, potentially limiting its effectiveness for global portfolio management or non-USD denominated assets.

### 5. Correlation Breakdown

During extreme market stress, correlations between risk factors may increase dramatically, reducing the model's diversification benefits (Forbes and Rigobon, 2002).

## References

Akram, Q. F. (2009). Commodity prices, interest rates and the dollar. Energy Economics, 31(6), 838-851.

Ang, A., Piazzesi, M., & Wei, M. (2006). What does the yield curve tell us about GDP growth? Journal of Econometrics, 131(1-2), 359-403.

Baker, M., & Wurgler, J. (2006). Investor sentiment and the cross‐section of stock returns. The Journal of Finance, 61(4), 1645-1680.

Baker, S. R., Bloom, N., & Davis, S. J. (2016). Measuring economic policy uncertainty. The Quarterly Journal of Economics, 131(4), 1593-1636.

Barber, B. M., & Odean, T. (2001). Boys will be boys: Gender, overconfidence, and common stock investment. The Quarterly Journal of Economics, 116(1), 261-292.

Beckmann, J., Berger, T., & Czudaj, R. (2015). Does gold act as a hedge or a safe haven for stocks? A smooth transition approach. Economic Modelling, 48, 16-24.

Bekaert, G., & Hoerova, M. (2014). The VIX, the variance premium and stock market volatility. Journal of Econometrics, 183(2), 181-192.

Brock, W., Lakonishok, J., & LeBaron, B. (1992). Simple technical trading rules and the stochastic properties of stock returns. The Journal of Finance, 47(5), 1731-1764.

Brown, G. W., & Cliff, M. T. (2004). Investor sentiment and the near-term stock market. Journal of Empirical Finance, 11(1), 1-27.

Campbell, J. Y., & Shiller, R. J. (1998). Valuation ratios and the long-run stock market outlook. The Journal of Portfolio Management, 24(2), 11-26.

Dow, C. H. (1901). Scientific stock speculation. The Magazine of Wall Street.

Estrella, A., & Mishkin, F. S. (1998). Predicting US recessions: Financial variables as leading indicators. Review of Economics and Statistics, 80(1), 45-61.

Fama, E. F., & French, K. R. (1989). Business conditions and expected returns on stocks and bonds. Journal of Financial Economics, 25(1), 23-49.

Forbes, K. J., & Rigobon, R. (2002). No contagion, only interdependence: measuring stock market comovements. The Journal of Finance, 57(5), 2223-2261.

Fosback, N. G. (1976). Stock market logic: A sophisticated approach to profits on Wall Street. The Institute for Econometric Research.

Gilchrist, S., & Zakrajšek, E. (2012). Credit spreads and business cycle fluctuations. American Economic Review, 102(4), 1692-1720.

Harvey, C. R. (1988). The real term structure and consumption growth. Journal of Financial Economics, 22(2), 305-333.

Kahneman, D., & Tversky, A. (1979). Prospect theory: An analysis of decision under risk. Econometrica, 47(2), 263-291.

Magdon-Ismail, M., & Atiya, A. F. (2004). Maximum drawdown. Risk, 17(10), 99-102.

Nickerson, R. S. (1998). Confirmation bias: A ubiquitous phenomenon in many guises. Review of General Psychology, 2(2), 175-220.

Pagan, A. R., & Sossounov, K. A. (2003). A simple framework for analysing bull and bear markets. Journal of Applied Econometrics, 18(1), 23-46.

Pan, J., & Poteshman, A. M. (2006). The information in option volume for future stock prices. The Review of Financial Studies, 19(3), 871-908.

Taleb, N. N. (2007). The black swan: The impact of the highly improbable. Random House.

Whaley, R. E. (2009). Understanding the VIX. The Journal of Portfolio Management, 35(3), 98-105.

Wilder, J. W. (1978). New concepts in technical trading systems. Trend Research.

Zarowin, P. (1990). Size, seasonality, and stock market overreaction. Journal of Financial and Quantitative Analysis, 25(1), 113-125.

Zweig, M. E. (1986). Winning on Wall Street. Warner Books.

Impulse Profile Zones [BigBeluga]🔵 OVERVIEW

Impulse Profile Zones is a volume-based tool designed to highlight high-impact candles and visualize hidden liquidity zones inside them using microstructure data. It’s ideal for identifying volume concentration and potential reaction points during impulsive market moves.

Whenever a candle exceeds a specified size threshold, this indicator captures its structure and overlays a detailed intrabar volume profile (from a 10x lower timeframe), allowing traders to analyze the distribution of interest within powerful market impulses.

🔵 CONCEPTS

Filters candles that exceed a user-defined threshold by size.

For qualifying candles, retrieves lower timeframe price and volume data.

Divides the candle’s body into 10 volume bins and calculates the volume per zone. Highlights the bin with the highest volume as the Point of Control (POC) .

Each POC line extends forward until a new impulse is detected.

🔵 FEATURES

Impulse Candle Detection:

Triggers only when a candle’s body size is larger than the defined threshold.

Lower Timeframe Profiling:

Aggregates 10-bin volume data from a lower timeframe (typically 1/10 of current TF).

Volume Distribution Bars:

Each bin displays a stylized bar using unicode block characters (e.g., ▇▇▇, ▇▇ or ▇--).

The bar size reflects the relative volume intensity.

POC Zone Mapping:

The bin with the highest volume is marked with a bold horizontal line.

Its value is labeled and extended until the next valid impulse.

🔵 HOW TO USE

Use large candle profiles to assess which price levels inside a move were most actively traded.

Watch the POC line as a magnet for future price interaction (support/resistance or reaction).

Combine with market structure or order block indicators to identify confluence levels.

Adjust the “Filter Large Candles” input to detect more or fewer events based on volatility.

🔵 CONCLUSION

Impulse Profile Zones is a hybrid microstructure tool that bridges lower timeframe volume with higher timeframe impulse candles. By revealing where most of the volume occurred inside large moves, traders gain a deeper view into hidden liquidity, enabling smarter trade entries and more confident profit-taking zones.

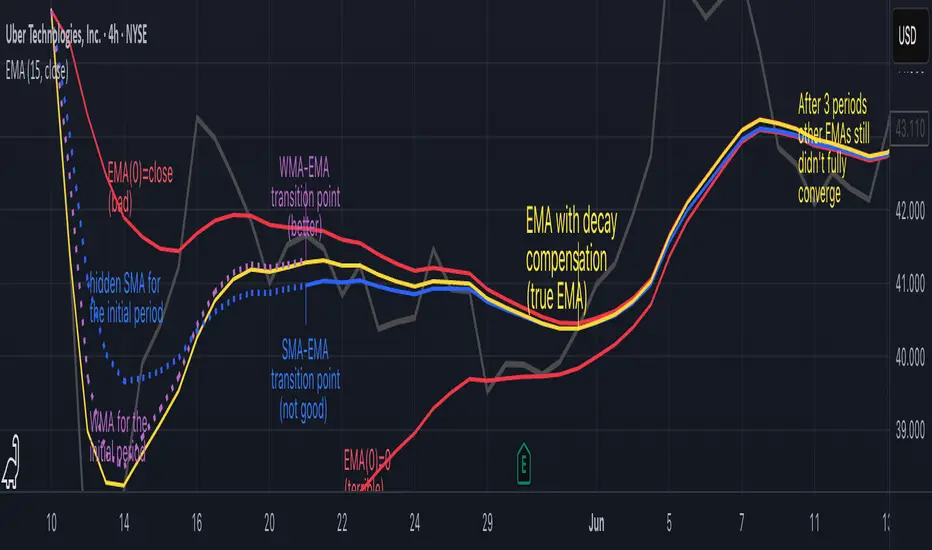

Why EMA Isn't What You Think It IsMany new traders adopt the Exponential Moving Average (EMA) believing it's simply a "better Simple Moving Average (SMA)". This common misconception leads to fundamental misunderstandings about how EMA works and when to use it.

EMA and SMA differ at their core. SMA use a window of finite number of data points, giving equal weight to each data point in the calculation period. This makes SMA a Finite Impulse Response (FIR) filter in signal processing terms. Remember that FIR means that "all that we need is the 'period' number of data points" to calculate the filter value. Anything beyond the given period is not relevant to FIR filters – much like how a security camera with 14-day storage automatically overwrites older footage, making last month's activity completely invisible regardless of how important it might have been.

EMA, however, is an Infinite Impulse Response (IIR) filter. It uses ALL historical data, with each past price having a diminishing - but never zero - influence on the calculated value. This creates an EMA response that extends infinitely into the past—not just for the last N periods. IIR filters cannot be precise if we give them only a 'period' number of data to work on - they will be off-target significantly due to lack of context, like trying to understand Game of Thrones by watching only the final season and wondering why everyone's so upset about that dragon lady going full pyromaniac.

If we only consider a number of data points equal to the EMA's period, we are capturing no more than 86.5% of the total weight of the EMA calculation. Relying on he period window alone (the warm-up period) will provide only 1 - (1 / e^2) weights, which is approximately 1−0.1353 = 0.8647 = 86.5%. That's like claiming you've read a book when you've skipped the first few chapters – technically, you got most of it, but you probably miss some crucial early context.

▶️ What is period in EMA used for?

What does a period parameter really mean for EMA? When we select a 15-period EMA, we're not selecting a window of 15 data points as with an SMA. Instead, we are using that number to calculate a decay factor (α) that determines how quickly older data loses influence in EMA result. Every trader knows EMA calculation: α = 1 / (1+period) – or at least every trader claims to know this while secretly checking the formula when they need it.

Thinking in terms of "period" seriously restricts EMA. The α parameter can be - should be! - any value between 0.0 and 1.0, offering infinite tuning possibilities of the indicator. When we limit ourselves to whole-number periods that we use in FIR indicators, we can only access a small subset of possible IIR calculations – it's like having access to the entire RGB color spectrum with 16.7 million possible colors but stubbornly sticking to the 8 basic crayons in a child's first art set because the coloring book only mentioned those by name.

For example:

Period 10 → alpha = 0.1818

Period 11 → alpha = 0.1667

What about wanting an alpha of 0.17, which might yield superior returns in your strategy that uses EMA? No whole-number period can provide this! Direct α parameterization offers more precision, much like how an analog tuner lets you find the perfect radio frequency while digital presets force you to choose only from predetermined stations, potentially missing the clearest signal sitting right between channels.

Sidenote: the choice of α = 1 / (1+period) is just a convention from 1970s, probably started by J. Welles Wilder, who popularized the use of the 14-day EMA. It was designed to create an approximate equivalence between EMA and SMA over the same number of periods, even thought SMA needs a period window (as it is FIR filter) and EMA doesn't. In reality, the decay factor α in EMA should be allowed any valye between 0.0 and 1.0, not just some discrete values derived from an integer-based period! Algorithmic systems should find the best α decay for EMA directly, allowing the system to fine-tune at will and not through conversion of integer period to float α decay – though this might put a few traditionalist traders into early retirement. Well, to prevent that, most traditionalist implementations of EMA only use period and no alpha at all. Heaven forbid we disturb people who print their charts on paper, draw trendlines with rulers, and insist the market "feels different" since computers do algotrading!

▶️ Calculating EMAs Efficiently

The standard textbook formula for EMA is:

EMA = CurrentPrice × alpha + PreviousEMA × (1 - alpha)

But did you know that a more efficient version exists, once you apply a tiny bit of high school algebra:

EMA = alpha × (CurrentPrice - PreviousEMA) + PreviousEMA

The first one requires three operations: 2 multiplications + 1 addition. The second one also requires three ops: 1 multiplication + 1 addition + 1 subtraction.

That's pathetic, you say? Not worth implementing? In most computational models, multiplications cost much more than additions/subtractions – much like how ordering dessert costs more than asking for a water refill at restaurants.

Relative CPU cost of float operations :

Addition/Subtraction: ~1 cycle

Multiplication: ~5 cycles (depending on precision and architecture)

Now you see the difference? 2 * 5 + 1 = 11 against 5 + 1 + 1 = 7. That is ≈ 36.36% efficiency gain just by swapping formulas around! And making your high school math teacher proud enough to finally put your test on the refrigerator.

▶️ The Warmup Problem: how to start the EMA sequence right

How do we calculate the first EMA value when there's no previous EMA available? Let's see some possible options used throughout the history:

Start with zero : EMA(0) = 0. This creates stupidly large distortion until enough bars pass for the horrible effect to diminish – like starting a trading account with zero balance but backdating a year of missed trades, then watching your balance struggle to climb out of a phantom debt for months.

Start with first price : EMA(0) = first price. This is better than starting with zero, but still causes initial distortion that will be extra-bad if the first price is an outlier – like forming your entire opinion of a stock based solely on its IPO day price, then wondering why your model is tanking for weeks afterward.

Use SMA for warmup : This is the tradition from the pencil-and-paper era of technical analysis – when calculators were luxury items and "algorithmic trading" meant your broker had neat handwriting. We first calculate an SMA over the initial period, then kickstart the EMA with this average value. It's widely used due to tradition, not merit, creating a mathematical Frankenstein that uses an FIR filter (SMA) during the initial period before abruptly switching to an IIR filter (EMA). This methodology is so aesthetically offensive (abrupt kink on the transition from SMA to EMA) that charting platforms hide these early values entirely, pretending EMA simply doesn't exist until the warmup period passes – the technical analysis equivalent of sweeping dust under the rug.

Use WMA for warmup : This one was never popular because it is harder to calculate with a pencil - compared to using simple SMA for warmup. Weighted Moving Average provides a much better approximation of a starting value as its linear descending profile is much closer to the EMA's decay profile.

These methods all share one problem: they produce inaccurate initial values that traders often hide or discard, much like how hedge funds conveniently report awesome performance "since strategy inception" only after their disastrous first quarter has been surgically removed from the track record.

▶️ A Better Way to start EMA: Decaying compensation

Think of it this way: An ideal EMA uses an infinite history of prices, but we only have data starting from a specific point. This creates a problem - our EMA starts with an incorrect assumption that all previous prices were all zero, all close, or all average – like trying to write someone's biography but only having information about their life since last Tuesday.

But there is a better way. It requires more than high school math comprehension and is more computationally intensive, but is mathematically correct and numerically stable. This approach involves compensating calculated EMA values for the "phantom data" that would have existed before our first price point.

Here's how phantom data compensation works:

We start our normal EMA calculation:

EMA_today = EMA_yesterday + α × (Price_today - EMA_yesterday)

But we add a correction factor that adjusts for the missing history:

Correction = 1 at the start

Correction = Correction × (1-α) after each calculation

We then apply this correction:

True_EMA = Raw_EMA / (1-Correction)

This correction factor starts at 1 (full compensation effect) and gets exponentially smaller with each new price bar. After enough data points, the correction becomes so small (i.e., below 0.0000000001) that we can stop applying it as it is no longer relevant.

Let's see how this works in practice:

For the first price bar:

Raw_EMA = 0

Correction = 1

True_EMA = Price (since 0 ÷ (1-1) is undefined, we use the first price)

For the second price bar:

Raw_EMA = α × (Price_2 - 0) + 0 = α × Price_2

Correction = 1 × (1-α) = (1-α)

True_EMA = α × Price_2 ÷ (1-(1-α)) = Price_2

For the third price bar:

Raw_EMA updates using the standard formula

Correction = (1-α) × (1-α) = (1-α)²

True_EMA = Raw_EMA ÷ (1-(1-α)²)

With each new price, the correction factor shrinks exponentially. After about -log₁₀(1e-10)/log₁₀(1-α) bars, the correction becomes negligible, and our EMA calculation matches what we would get if we had infinite historical data.

This approach provides accurate EMA values from the very first calculation. There's no need to use SMA for warmup or discard early values before output converges - EMA is mathematically correct from first value, ready to party without the awkward warmup phase.

Here is Pine Script 6 implementation of EMA that can take alpha parameter directly (or period if desired), returns valid values from the start, is resilient to dirty input values, uses decaying compensator instead of SMA, and uses the least amount of computational cycles possible.

// Enhanced EMA function with proper initialization and efficient calculation

ema(series float source, simple int period=0, simple float alpha=0)=>

// Input validation - one of alpha or period must be provided

if alpha<=0 and period<=0

runtime.error("Alpha or period must be provided")

// Calculate alpha from period if alpha not directly specified

float a = alpha > 0 ? alpha : 2.0 / math.max(period, 1)

// Initialize variables for EMA calculation

var float ema = na // Stores raw EMA value

var float result = na // Stores final corrected EMA

var float e = 1.0 // Decay compensation factor

var bool warmup = true // Flag for warmup phase

if not na(source)

if na(ema)

// First value case - initialize EMA to zero

// (we'll correct this immediately with the compensation)

ema := 0

result := source

else

// Standard EMA calculation (optimized formula)

ema := a * (source - ema) + ema

if warmup

// During warmup phase, apply decay compensation

e *= (1-a) // Update decay factor

float c = 1.0 / (1.0 - e) // Calculate correction multiplier

result := c * ema // Apply correction

// Stop warmup phase when correction becomes negligible

if e <= 1e-10

warmup := false

else

// After warmup, EMA operates without correction

result := ema

result // Return the properly compensated EMA value

▶️ CONCLUSION

EMA isn't just a "better SMA"—it is a fundamentally different tool, like how a submarine differs from a sailboat – both float, but the similarities end there. EMA responds to inputs differently, weighs historical data differently, and requires different initialization techniques.

By understanding these differences, traders can make more informed decisions about when and how to use EMA in trading strategies. And as EMA is embedded in so many other complex and compound indicators and strategies, if system uses tainted and inferior EMA calculatiomn, it is doing a disservice to all derivative indicators too – like building a skyscraper on a foundation of Jell-O.

The next time you add an EMA to your chart, remember: you're not just looking at a "faster moving average." You're using an INFINITE IMPULSE RESPONSE filter that carries the echo of all previous price actions, properly weighted to help make better trading decisions.

EMA done right might significantly improve the quality of all signals, strategies, and trades that rely on EMA somewhere deep in its algorithmic bowels – proving once again that math skills are indeed useful after high school, no matter what your guidance counselor told you.

Silver Bullet 5 minutes Box - By KaVeHThis indicator plots high-low range boxes based on selected intraday time windows on the 5-minute chart. It's inspired by the "Silver Bullet" trading concept, highlighting key liquidity grabs and volatility pockets at predefined times. It helps traders visually identify potential smart money trading windows during the New York session and other time anchors.

⚠️ This script only works on the 5-minute chart.

📦 Main Features:

⏰ Customizable Time Boxes:

Define up to 4 separate time windows per day:

3:00 AM – 3:05 AM (New York time) (Box 1)

10:00 AM – 10:05 AM (New York time) (Box 2)

2:00 PM – 2:05 PM (New York time) (Box 3)

8:00 PM – 8:05 PM (New York time) (Box 4)

🎨 Color and Visibility Control:

Each box can be independently toggled and colored for visual distinction.

🕔 New York Time Based:

All timestamps are automatically adjusted to New York Time, aligning with institutional market behavior.

📉 Post-Box Projection:

After each time window closes, a box extends forward 6 hours (72 bars on a 5-minute chart) to highlight the range.

💡 Use Case:

These boxes are best used to:

Detect liquidity sweeps.

Mark potential entry or exit zones.

Track price behavior after specific time-based events.

For example, the 10 AM box is often used to identify setups just after the NYSE open and into the first hour of volatility.

⚠️ TradingView Compliance Notes:

This script is original and does not replicate or resell premium/paid indicators.

All logic is coded from scratch by kaveh_mirmousavi, using public concepts from ICT/Smart Money Trading.

Fully complies with the Mozilla Public License 2.0.

Does not include financial advice or signals — for educational use only.

✅ How to Use:

Apply to a 5-minute chart.

Adjust the desired time boxes in the input panel.

Watch for price action within and after the boxes.

Enjoy and feel free to share feedback or ideas for improvement!

pymath█ OVERVIEW

This library ➕ enhances Pine Script's built-in types (`float`, `int`, `array`, `array`) with mathematical methods, mirroring 🪞 many functions from Python's `math` module. Import this library to overload or add to built-in capabilities, enabling calls like `myFloat.sin()` or `myIntArray.gcd()`.

█ CONCEPTS

This library wraps Pine's built-in `math.*` functions and implements others where necessary, expanding the mathematical toolkit available within Pine Script. It provides a more object-oriented approach to mathematical operations on core data types.

█ HOW TO USE

• Import the library: i mport kaigouthro/pymath/1

• Call methods directly on variables: myFloat.sin() , myIntArray.gcd()

• For raw integer literals, you MUST use parentheses: `(1234).factorial()`.

█ FEATURES

• **Infinity Handling:** Includes `isinf()` and `isfinite()` for robust checks. Uses `POS_INF_PROXY` to represent infinity.

• **Comprehensive Math Functions:** Implements a wide range of methods, including trigonometric, logarithmic, hyperbolic, and array operations.

• **Object-Oriented Approach:** Allows direct method calls on `int`, `float`, and arrays for cleaner code.

• **Improved Accuracy:** Some functions (e.g., `remainder()`) offer improved accuracy compared to default Pine behavior.

• **Helper Functions:** Internal helper functions optimize calculations and handle edge cases.

█ NOTES

This library improves upon Pine Script's built-in `math` functions by adding new ones and refining existing implementations. It handles edge cases such as infinity, NaN, and zero values, enhancing the reliability of your Pine scripts. For Speed, it wraps and uses built-ins, as thy are fastest.

█ EXAMPLES

//@version=6

indicator("My Indicator")

// Import the library

import kaigouthro/pymath/1

// Create some Vars

float myFloat = 3.14159

int myInt = 10

array myIntArray = array.from(1, 2, 3, 4, 5)

// Now you can...

plot( myFloat.sin() ) // Use sin() method on a float, using built in wrapper

plot( (myInt).factorial() ) // Factorial of an integer (note parentheses)

plot( myIntArray.gcd() ) // GCD of an integer array

method isinf(self)

isinf: Checks if this float is positive or negative infinity using a proxy value.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) value to check.

Returns: (bool) `true` if the absolute value of `self` is greater than or equal to the infinity proxy, `false` otherwise.

method isfinite(self)

isfinite: Checks if this float is finite (not NaN and not infinity).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The value to check.

Returns: (bool) `true` if `self` is not `na` and not infinity (as defined by `isinf()`), `false` otherwise.

method fmod(self, divisor)

fmod: Returns the C-library style floating-point remainder of `self / divisor` (result has the sign of `self`).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Dividend `x`.

divisor (float) : (float) Divisor `y`. Cannot be zero or `na`.

Returns: (float) The remainder `x - n*y` where n is `trunc(x/y)`, or `na` if divisor is 0, `na`, or inputs are infinite in a way that prevents calculation.

method factorial(self)

factorial: Calculates the factorial of this non-negative integer.

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) The integer `n`. Must be non-negative.

Returns: (float) `n!` as a float, or `na` if `n` is negative or overflow occurs (based on `isinf`).

method isqrt(self)

isqrt: Calculates the integer square root of this non-negative integer (floor of the exact square root).

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) The non-negative integer `n`.

Returns: (int) The greatest integer `a` such that a² <= n, or `na` if `n` is negative.

method comb(self, k)

comb: Calculates the number of ways to choose `k` items from `self` items without repetition and without order (Binomial Coefficient).

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) Total number of items `n`. Must be non-negative.

k (int) : (int) Number of items to choose. Must be non-negative.

Returns: (float) The binomial coefficient nCk, or `na` if inputs are invalid (n<0 or k<0), `k > n`, or overflow occurs.

method perm(self, k)

perm: Calculates the number of ways to choose `k` items from `self` items without repetition and with order (Permutations).

Namespace types: series int, simple int, input int, const int

Parameters:

self (int) : (int) Total number of items `n`. Must be non-negative.

k (simple int) : (simple int = na) Number of items to choose. Must be non-negative. Defaults to `n` if `na`.

Returns: (float) The number of permutations nPk, or `na` if inputs are invalid (n<0 or k<0), `k > n`, or overflow occurs.

method log2(self)

log2: Returns the base-2 logarithm of this float. Input must be positive. Wraps `math.log(self) / math.log(2.0)`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be positive.

Returns: (float) The base-2 logarithm, or `na` if input <= 0.

method trunc(self)

trunc: Returns this float with the fractional part removed (truncates towards zero).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The integer part, or `na` if input is `na` or infinite.

method abs(self)

abs: Returns the absolute value of this float. Wraps `math.abs()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The absolute value, or `na` if input is `na`.

method acos(self)

acos: Returns the arccosine of this float, in radians. Wraps `math.acos()`. Input must be between -1 and 1.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be between -1 and 1.

Returns: (float) Angle in radians , or `na` if input is outside or `na`.

method asin(self)

asin: Returns the arcsine of this float, in radians. Wraps `math.asin()`. Input must be between -1 and 1.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be between -1 and 1.

Returns: (float) Angle in radians , or `na` if input is outside or `na`.

method atan(self)

atan: Returns the arctangent of this float, in radians. Wraps `math.atan()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) Angle in radians , or `na` if input is `na`.

method ceil(self)

ceil: Returns the ceiling of this float (smallest integer >= self). Wraps `math.ceil()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The ceiling value, or `na` if input is `na` or infinite.

method cos(self)

cos: Returns the cosine of this float (angle in radians). Wraps `math.cos()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The cosine, or `na` if input is `na`.

method degrees(self)

degrees: Converts this float from radians to degrees. Wraps `math.todegrees()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The angle in degrees, or `na` if input is `na`.

method exp(self)

exp: Returns e raised to the power of this float. Wraps `math.exp()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The exponent.

Returns: (float) `e**self`, or `na` if input is `na`.

method floor(self)

floor: Returns the floor of this float (largest integer <= self). Wraps `math.floor()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The floor value, or `na` if input is `na` or infinite.

method log(self)

log: Returns the natural logarithm (base e) of this float. Wraps `math.log()`. Input must be positive.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be positive.

Returns: (float) The natural logarithm, or `na` if input <= 0 or `na`.

method log10(self)

log10: Returns the base-10 logarithm of this float. Wraps `math.log10()`. Input must be positive.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be positive.

Returns: (float) The base-10 logarithm, or `na` if input <= 0 or `na`.

method pow(self, exponent)

pow: Returns this float raised to the power of `exponent`. Wraps `math.pow()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The base.

exponent (float) : (float) The exponent.

Returns: (float) `self**exponent`, or `na` if inputs are `na` or lead to undefined results.

method radians(self)

radians: Converts this float from degrees to radians. Wraps `math.toradians()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in degrees.

Returns: (float) The angle in radians, or `na` if input is `na`.

method round(self)

round: Returns the nearest integer to this float. Wraps `math.round()`. Ties are rounded away from zero.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) The rounded integer, or `na` if input is `na` or infinite.

method sign(self)

sign: Returns the sign of this float (-1, 0, or 1). Wraps `math.sign()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (int) -1 if negative, 0 if zero, 1 if positive, `na` if input is `na`.

method sin(self)

sin: Returns the sine of this float (angle in radians). Wraps `math.sin()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The sine, or `na` if input is `na`.

method sqrt(self)

sqrt: Returns the square root of this float. Wraps `math.sqrt()`. Input must be non-negative.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be non-negative.

Returns: (float) The square root, or `na` if input < 0 or `na`.

method tan(self)

tan: Returns the tangent of this float (angle in radians). Wraps `math.tan()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The angle in radians.

Returns: (float) The tangent, or `na` if input is `na`.

method acosh(self)

acosh: Returns the inverse hyperbolic cosine of this float. Input must be >= 1.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be >= 1.

Returns: (float) The inverse hyperbolic cosine, or `na` if input < 1 or `na`.

method asinh(self)

asinh: Returns the inverse hyperbolic sine of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The inverse hyperbolic sine, or `na` if input is `na`.

method atanh(self)

atanh: Returns the inverse hyperbolic tangent of this float. Input must be between -1 and 1 (exclusive).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number. Must be between -1 and 1 (exclusive).

Returns: (float) The inverse hyperbolic tangent, or `na` if input is outside (-1, 1) or `na`.

method cosh(self)

cosh: Returns the hyperbolic cosine of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The hyperbolic cosine, or `na` if input is `na`.

method sinh(self)

sinh: Returns the hyperbolic sine of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The hyperbolic sine, or `na` if input is `na`.

method tanh(self)

tanh: Returns the hyperbolic tangent of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The input number.

Returns: (float) The hyperbolic tangent, or `na` if input is `na`.

method atan2(self, dx)

atan2: Returns the angle in radians between the positive x-axis and the point (dx, self). Wraps `math.atan2()`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The y-coordinate `y`.

dx (float) : (float) The x-coordinate `x`.

Returns: (float) The angle in radians , result of `math.atan2(self, dx)`. Returns `na` if inputs are `na`. Note: `math.atan2(0, 0)` returns 0 in Pine.

Optimization: Use built-in math.atan2()

method cbrt(self)

cbrt: Returns the cube root of this float.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The value to find the cube root of.

Returns: (float) The real cube root. Handles negative inputs correctly, or `na` if input is `na`.

method exp2(self)

exp2: Returns 2 raised to the power of this float. Calculated as `2.0.pow(self)`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The exponent.

Returns: (float) `2**self`, or `na` if input is `na` or results in non-finite value.

method expm1(self)

expm1: Returns `e**self - 1`. Calculated as `self.exp() - 1.0`. May offer better precision for small `self` in some environments, but Pine provides no guarantee over `self.exp() - 1.0`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The exponent.

Returns: (float) `e**self - 1`, or `na` if input is `na` or `self.exp()` is `na`.

method log1p(self)

log1p: Returns the natural logarithm of (1 + self). Calculated as `(1.0 + self).log()`. Pine provides no specific precision guarantee for self near zero.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Value to add to 1. `1 + self` must be positive.

Returns: (float) Natural log of `1 + self`, or `na` if input is `na` or `1 + self <= 0`.

method modf(self)

modf: Returns the fractional and integer parts of this float as a tuple ` `. Both parts have the sign of `self`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The number `x` to split.

Returns: ( ) A tuple containing ` `, or ` ` if `x` is `na` or non-finite.

method remainder(self, divisor)

remainder: Returns the IEEE 754 style remainder of `self` with respect to `divisor`. Result `r` satisfies `abs(r) <= 0.5 * abs(divisor)`. Uses round-half-to-even.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Dividend `x`.

divisor (float) : (float) Divisor `y`. Cannot be zero or `na`.

Returns: (float) The IEEE 754 remainder, or `na` if divisor is 0, `na`, or inputs are non-finite in a way that prevents calculation.

method copysign(self, signSource)

copysign: Returns a float with the magnitude (absolute value) of `self` but the sign of `signSource`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Value providing the magnitude `x`.

signSource (float) : (float) Value providing the sign `y`.

Returns: (float) `abs(x)` with the sign of `y`, or `na` if either input is `na`.

method frexp(self)

frexp: Returns the mantissa (m) and exponent (e) of this float `x` as ` `, such that `x = m * 2^e` and `0.5 <= abs(m) < 1` (unless `x` is 0).

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) The number `x` to decompose.

Returns: ( ) A tuple ` `, or ` ` if `x` is 0, or ` ` if `x` is non-finite or `na`.

method isclose(self, other, rel_tol, abs_tol)

isclose: Checks if this float `a` and `other` float `b` are close within relative and absolute tolerances.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) First value `a`.

other (float) : (float) Second value `b`.

rel_tol (simple float) : (simple float = 1e-9) Relative tolerance. Must be non-negative and less than 1.0.

abs_tol (simple float) : (simple float = 0.0) Absolute tolerance. Must be non-negative.

Returns: (bool) `true` if `abs(a - b) <= max(rel_tol * max(abs(a), abs(b)), abs_tol)`. Handles `na`/`inf` appropriately. Returns `na` if tolerances are invalid.

method ldexp(self, exponent)

ldexp: Returns `self * (2**exponent)`. Inverse of `frexp`.

Namespace types: series float, simple float, input float, const float

Parameters:

self (float) : (float) Mantissa part `x`.

exponent (int) : (int) Exponent part `i`.

Returns: (float) The result of `x * pow(2, i)`, or `na` if inputs are `na` or result is non-finite.

method gcd(self)

gcd: Calculates the Greatest Common Divisor (GCD) of all integers in this array.

Namespace types: array

Parameters:

self (array) : (array) An array of integers.

Returns: (int) The largest positive integer that divides all non-zero elements, 0 if all elements are 0 or array is empty. Returns `na` if any element is `na`.

method lcm(self)

lcm: Calculates the Least Common Multiple (LCM) of all integers in this array.

Namespace types: array

Parameters:

self (array) : (array) An array of integers.

Returns: (int) The smallest positive integer that is a multiple of all non-zero elements, 0 if any element is 0, 1 if array is empty. Returns `na` on potential overflow or if any element is `na`.

method dist(self, other)

dist: Returns the Euclidean distance between this point `p` and another point `q` (given as arrays of coordinates).

Namespace types: array

Parameters:

self (array) : (array) Coordinates of the first point `p`.

other (array) : (array) Coordinates of the second point `q`. Must have the same size as `p`.

Returns: (float) The Euclidean distance, or `na` if arrays have different sizes, are empty, or contain `na`/non-finite values.

method fsum(self)

fsum: Returns an accurate floating-point sum of values in this array. Uses built-in `array.sum()`. Note: Pine Script does not guarantee the same level of precision tracking as Python's `math.fsum`.

Namespace types: array

Parameters:

self (array) : (array) The array of floats to sum.

Returns: (float) The sum of the array elements. Returns 0.0 for an empty array. Returns `na` if any element is `na`.

method hypot(self)

hypot: Returns the Euclidean norm (distance from origin) for this point given by coordinates in the array. `sqrt(sum(x*x for x in coordinates))`.

Namespace types: array

Parameters:

self (array) : (array) Array of coordinates defining the point.

Returns: (float) The Euclidean norm, or 0.0 if the array is empty. Returns `na` if any element is `na` or non-finite.

method prod(self, start)

prod: Calculates the product of all elements in this array.

Namespace types: array

Parameters:

self (array) : (array) The array of values to multiply.

start (simple float) : (simple float = 1.0) The starting value for the product (returned if the array is empty).

Returns: (float) The product of array elements * start. Returns `na` if any element is `na`.

method sumprod(self, other)

sumprod: Returns the sum of products of values from this array `p` and another array `q` (dot product).

Namespace types: array

Parameters:

self (array) : (array) First array of values `p`.

other (array) : (array) Second array of values `q`. Must have the same size as `p`.

Returns: (float) The sum of `p * q ` for all i, or `na` if arrays have different sizes or contain `na`/non-finite values. Returns 0.0 for empty arrays.

Average Daily LiquidityIt is important to have sufficient daily trading value (liquidity) to ensure you can easily enter and, importantly, exit the trade. This indicator allows you to see if the traded value of a stock is adequate. The default average is 10 periods and it is common to average the daily traded value as both price and volume can have spikes causing trading errors. Some investors use a 5 period for a week, 10 period for 2 weeks, 20 or 21 period for 4 weeks/month and 65 periods for a quarter. You need to ascertain your buying amount such as $10000 and then have the average daily trading value be your comfortable moving average more such as average liquidity is more than 10 x MA(close x volume) or $100000 in this example. The value is extremely important for small and micro cap stocks you may wish to purchase.

ETF Builder & Backtest System [TradeDots]Create, analyze, and monitor your own custom “ETF-like” portfolio directly on TradingView. This script merges up to 10 different assets with user-defined weightings into a single composite chart, allowing you to see how your personalized portfolio would have performed historically. It is an original tool designed to help traders and investors quickly gauge risk and return profiles without leaving the TradingView platform.

📝 HOW IT WORKS

1. Custom Portfolio Construction

Multiple Assets : Combine up to 10 different stocks, ETFs, cryptocurrencies, or other symbols.

User-Defined Weights : Allocate each asset a percentage weight (e.g., 15% in AAPL, 10% in MSFT, etc.).

Single Composite Value : The script calculates a weighted “ETF-style” price, effectively simulating a merged portfolio curve on your chart.

2. Performance Tracking & Return Analysis

Automatic History Capture : The indicator records each asset’s starting price when it first appears in your chosen date range.

Rolling Updates : As time progresses, all asset prices are continually evaluated and the portfolio value is updated in real time.

Buy & Hold Returns : See how each asset—and the overall portfolio—performed from the “start” date to the most recent bar.

Annualized Return : Automatically calculates CAGR (Compound Annual Growth Rate) to help visualize performance over varying timescales.

3. Table & Visual Output

Performance Table : A comprehensive table displays individual asset returns, annualized returns, and portfolio totals.

Normalized Chart Plot : The composite ETF value is scaled to 100 at the start date, making it easy to compare relative growth or decline.

Optional Time Filter : You can define a specific date range (Start/End Dates) to focus on a particular period or to limit historical data.

⚙️ KEY FEATURES

1. Flexible Asset Selection

Choose any symbols from multiple asset classes. The script will only run calculations when data is available—no need to worry about missing quotes.

2. Dynamic Table Reporting

Start Price for each asset

Percentage Weight in the portfolio

Total Return (%) and Annualized Return (%)

3. Simple Backtesting Logic

This script takes a straightforward Buy & Hold perspective. Once the start date is reached, the portfolio remains static until the end date, so you can quickly assess hypothetical growth.

4. Plot Customization

Toggle the main “ETF” plot on/off.

Alter the visual style for tables and text.

Adjust the time filter to limit or extend your performance measurement window.

🚀 HOW TO USE IT

1. Add the Script

Search for “ETF Builder & Backtest System ” in the Indicators & Strategies tab or manually add it to your chart after saving it in your Pine Editor.

2. Configure Inputs

Enable Time Filter : Choose whether to restrict the analysis to a particular date range.

Start & End Date : Define the period you want to measure performance over (e.g., from 2019-12-31 to 2025-01-01).

Assets & Weights : Enter each symbol and specify a percentage weight (up to 10 assets).

Display Options : Pick where you want the Table to appear and choose background/text colors.

3. Interpret the Table & Plots

Asset Rows : Each asset’s ticker, weighting, start price, and performance metrics.

ETF Total Row : Summarizes total weighting, composite starting value, and overall returns.

Normalized Plot : Tracks growth/decline of the combined portfolio, starting at 100 on the chart.

4. Refine Your Strategy

Compare how different weights or a new mix of assets would have performed over the same period.

Assess if certain assets contribute disproportionately to your returns or volatility.

Use the results to guide allocations in your real trading or paper trading accounts.

❗️LIMITATIONS

1. Buy & Hold Only

This script does not handle rebalancing or partial divestments. Once the portfolio starts, weights remain fixed throughout the chosen timeframe.

2. No Reinvestment Tracking

Dividends or other distributions are not factored into performance.

3. Data Availability

If historical data for a particular asset is unavailable on TradingView, related results may display as “N/A.”

4. Market Regimes & Volatility

Past performance does not guarantee similar future behavior. Markets can change rapidly, which may render historical backtests less predictive over time.

⚠️ RISK DISCLAIMER

Trading and investing carry significant risk and can result in financial loss. The “ETF Builder & Backtest System ” is provided for informational and educational purposes only. It does not constitute financial advice.

Always conduct your own research.

Use proper risk management and position sizing.

Past performance does not guarantee future results.

This script is an original creation by TradeDots, published under the Mozilla Public License 2.0.

Use this indicator as part of a broader trading or investment approach—consider fundamental and technical factors, overall market context, and personal risk tolerance. No trading tool can assure profits; exercise caution and responsibility in all financial decisions.

Compression Patterns (w/ Trend + Proximity Filter)🧠 Description:

This indicator identifies high-probability price compression patterns within trending environments — a setup prized by experienced swing and day traders alike. It combines the classic NR4, NR7, 2-Bar NR, 3-Bar NR, and Inside Day formations with a powerful trend filter and proximity logic to deliver clear, focused signals.

🔍 What's Inside:

▪️ Compression Patterns

The core of this tool lies in the logic of price compression. These patterns signal the market taking a breath — volatility contracts, volume dries up, and price coils like a spring.

When this happens in the right context, the next move is often explosive.

NR4 / NR7: Narrowest range in 4 or 7 bars — excellent for spotting the quiet before the storm.

2-Bar NR / 3-Bar NR: These identify the tightest consecutive 2 or 3-day ranges over the past 20 days — contextually rare and powerful.

Inside Day: A simple but highly effective consolidation pattern, especially when it clusters around key moving averages.

▪️ Trend Filter (EMA Stack)

You could say this is where most indicators fall apart — no context.

This one doesn’t make that mistake.

Signals only fire when the 10 EMA > 20 EMA > 50 EMA, and price is above the 20 EMA. That’s a strong, established uptrend — the only environment where breakouts are statistically favourable.

Why?

Because trend following works.

It may not give you fixed daily returns, but it’s the only strategy with theoretically infinite profit potential. You risk little, trade less, and position yourself for rare but massive moves. That’s the edge.

▪️ Proximity Filter (1 ATR to EMA)

We’ve added another layer of discipline. Signals only fire when price is:

Within 1 ATR of the 10 EMA (if price is above it), or

Within 1 ATR of the 20 EMA (if price is below the 10 EMA)

This ensures you’re not chasing. You’re waiting for tight, controlled pullbacks into dynamic support — exactly where institutions add size, not exit.

⚙️ Fully Customisable:

Toggle visibility of each pattern

Custom colours and transparency for label & background

Adjustable ATR length and multiplier

Change label text if needed (useful for translations or tweaks)

🎯 Ideal Use Case:

Swing trading off the daily chart

Day trading with VWAP/MACD filters (in alternate versions)

Supplementing price action strategies

🔚 Final Word:

This isn’t an “everything scanner.”

It’s a discerning sniper scope for traders who wait patiently for clean trends, tight consolidations, and perfect proximity — then strike.

SMC Entry Signals MTF v2📘 User Guide for the SMC Entry Signals MTF v2 Indicator

🎯 Purpose of the Indicator

This indicator is designed to identify reversal entry points based on Smart Money Concepts (SMC) and candlestick confirmation. It’s especially useful for traders who use:

Imbalance zones, order blocks, breaker blocks

Liquidity grabs

Multi-timeframe confirmation (MTF)

📈 How to Use the Signals on the Chart

✅ LONG Signal (green triangle below the candle):

Conditions:

Price is in a discount zone (below the FIB 50% level)

A bullish engulfing candle appears

A bullish Order Block (OB) or Breaker Block is detected

There’s an upward imbalance

A bullish OB is confirmed on the higher timeframe

➡️ How to act:

Consider entering long on the current or next candle.

Place your stop-loss below the OB or the nearest swing low.

Take profit at the nearest liquidity zone or premium area (above FIB 50%).

🔻 SHORT Signal (red triangle above the candle):

Conditions:

Price is in a premium zone (above FIB 50%)

A bearish engulfing candle appears

A bearish OB or Breaker Block is detected

There’s a downward imbalance

A bearish OB is confirmed on the higher timeframe

➡️ How to act:

Consider short entry after the signal.

Place your stop-loss above the OB or swing high.

Target the discount zone or the next liquidity pocket.

⚙️ Recommended Settings by Trading Style

Trading Style Suggested Settings Notes

Intraday (1–15m) fibLookback = 20–50, obLookback = 5–10, htf_tf = 1H/4H Fast signals. Use Discount/Premium + Engulfing.

Swing/Position (1H–1D) fibLookback = 50–100, obLookback = 10–20, htf_tf = 1D/1W Higher trust in MTF confirmation. Ideal with fundamentals.

Scalping (1m) fibLookback = 10–20, obLookback = 3–5, htf_tf = 15m/1H Remove Breaker and MTF for quick reaction trades.

🧠 Best Practices for Traders

Trend Filtering:

Use EMAs or volume to confirm the current trend.

Take longs only in uptrends, shorts in downtrends.

Liquidity Zones:

Use this indicator after liquidity grabs.

OBs and Breakers often appear right after stop hunts.

Combine with Manual Zones:

This works best when paired with manually drawn OBs and key levels.

Backtest the Signals:

Use Bar Replay mode on TradingView to test past signals.

🧪 Example Trade Setup

Example on BTCUSDT 15m:

Price drops into the discount zone.

A green triangle appears (bullish engulfing + OB + imbalance + HTF OB).

You enter long, stop below the OB, target the premium zone.

🎯 This type of setup often gives a risk/reward ratio of 1:2 or better — profitable even with a 40% win rate.

⏰ Alerts & Automation

Enable alerts:

"SMC Long Entry" — fires when a long signal appears.

"SMC Short Entry" — fires when a short signal appears.

You can integrate this with bots via webhook, like:

TradingConnector, 3Commas, Alertatron, etc.

✅ What This Indicator Gives You

High-probability entries using SMC logic

Customizable filters for entry logic

Multi-timeframe confirmation for stronger setups

Suitable for both intraday and swing trading

Options Volume [theUltimator5]📊 Option Volume — Multi-Strike Option Flow Visualizer

The Option Volume indicator tracks and visualizes volume activity for up to 10 custom option strike symbols on any ticker. It supports both individual strike analysis and a combined cumulative volume mode, providing an intuitive view of option flow across your selected strikes.

🔧 Features:

Dynamic Strike Control: Select up to 10 strikes and customize each with ticker, expiration date (YYMMDD), and option type (Call or Put).

Volume Display Modes:

🔹 Individual: Shows a separate volume bar for each strike.

🔸 Cumulative: Combines all selected strike volumes into a single bar, colored green for Calls and red for Puts.

Customizable Table Display:

Toggle the option symbol table on/off.

Position the table in any corner of the chart.

Table cell colors match plotted bars in Individual mode, or turn red/green in Cumulative mode based on option type.

Smart Volume Filtering: Only shows volume bars on the bar where volume updates (i.e., no carryover from stale bars).

Input Efficiency: All strike prices are automatically rounded to the nearest 0.5 increment for standardized symbol formatting.

⚙️ How to Use:

Select the ticker you want to analyze.

Input the expiration date and option type (C or P).

Define strike prices (up to 10).

Toggle between Individual or Cumulative volume display.

Adjust the number of visible strikes and table position as needed.

This tool is ideal for traders looking to monitor strike-level option volume behavior, spot flow anomalies, or keep track of high-interest strike activity in real-time.

The indicator currently doesn't support multiple expiration dates or a combination of calls/puts. If you want to view multiple expirations or a both calls and puts at the same time, simply add the indicator multiple times.

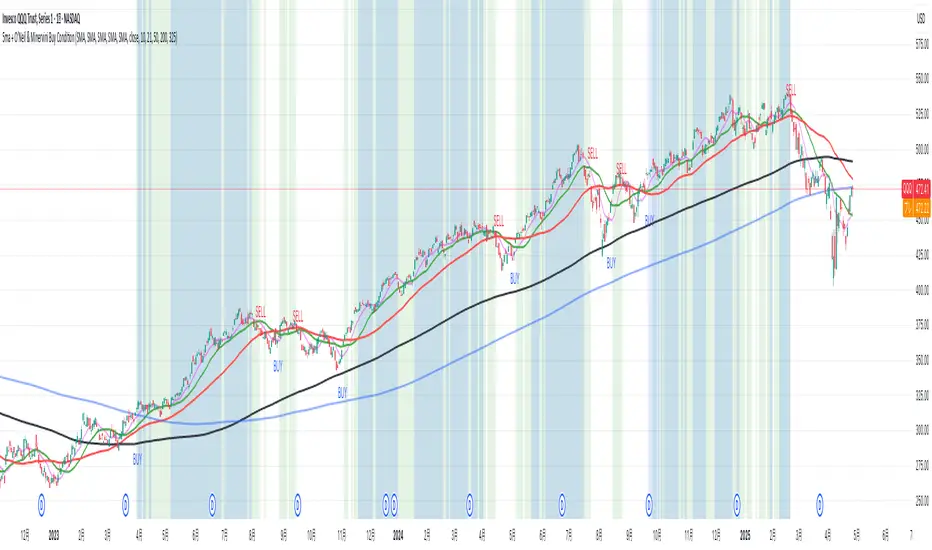

5ma + O’Neil & Minervini Buy ConditionIndicator Overview

5ma + O’Neil & Minervini Buy Condition is an original TradingView indicator that extends beyond a simple collection of standard moving averages by offering:

- Five Fully Independent Lines : Each of MA1–MA5 can be configured as SMA, EMA, WMA, or VWMA with its own period and data source. This level of customization unlocks unique combinations no existing script provides.

- Synergy of Multiple Timeframes : Default settings (10, 21, 50, 200, 325) reflect ultra‑short, short, medium, long, and volume‑weighted long‑term perspectives. The layered structure functions as a multi‑filter, sharpening entry signals and trend confirmation beyond any single MA.

- Integrated Buy Conditions : Built‑in O’Neil and Minervini buy filters use fixed SMA‑based rules (50 & 200 SMA rising within 15% of 52‑week high; 10 > 21 > 50 SMA rising within high/low thresholds), plus a combined condition highlighting when both methods align.

- Clean Visualization & Style Controls : Background coloring for each buy condition appears only in the Style tab under clearly named parameters (O’Neil Buy Condition, Minervini Buy Condition, Both Conditions). MA lines support transparent default colors and customizable line width for optimal readability without clutter.

Calculation & Logic

SMA: (P₁ + P₂ + … + Pₙ) ÷ N

EMA: α = 2 ÷ (N + 1)

EMA_today = (Price_today – EMA_yesterday) × α + EMA_yesterday

WMA: (P₁×N + P₂×(N–1) + … + Pₙ×1) ÷

VWMA: Σ(Pᵢ×Vᵢ) ÷ Σ(Vᵢ) for i = 1…N

```

Buy Condition Logic

- O’Neil: Price > 50 SMA & 200 SMA (both rising) **and** within 15% of the 52‑week high.

- Minervini : 10 SMA > 21 SMA > 50 SMA (both short‑term SMAs rising) **and** within 25% of the 52‑week high **and** at least 25% above the 52‑week low.

- Combined : Both O’Neil and Minervini conditions true.

Usage Examples

1. Short‑Mid Cross : Observe MA1/MA2 crossover while MA3/MA4 confirm trend strength.

2. Volume‑Weighted Long‑Term : Use VWMA as MA5 to filter institutional‑strength pullbacks.

3. Multi‑Filter Entry : Look for purple background (Both Conditions) on daily chart as high‑confidence entry.

Why It’s Unique

- Not a Mash‑Up : Though built on standard MA formulas, the customizable layering and built‑in buy filters create a novel multi‑dimensional analysis tool.

- Trader‑Friendly : Detailed comments in the code explain parameter choices, calculation methods, and practical entry scenarios so that even Pine novices can understand the underlying mechanics.

- Publication‑Ready : Description and code demonstrate originality, add clear value, and comply with house‑rule requirements by explaining why and how components interact, not just listing features.

- Combined Custom MA & Buy Conditions : By integrating customizable moving averages with built-in buy filters, users can easily recognize O’Neil and Minervini recommended setups.

[blackcat] L3 Dark Horse OscillatorOVERVIEW

The L3 Dark Horse Oscillator is a sophisticated technical indicator meticulously crafted to offer traders deep insights into market momentum. By leveraging advanced calculations involving Relative Strength Value (RSV) and proprietary oscillatory techniques, this script provides clear and actionable signals for identifying potential buying and selling opportunities. Its distinctive feature—a vibrant gradient color scheme—enhances readability and makes it easier to visualize trends and reversals on the chart 📈↗️.

FEATURES

Advanced Calculation Methods: Utilizes complex algorithms to compute the Relative Strength Value (RSV) over specific periods, providing a nuanced view of price movements.

Default Period: 27 bars for initial RSV calculation.

Additional Period: 36 bars for extended RSV analysis.

Dual-Oscillator Components:

Component A: Derived using multiple layers of Simple Moving Averages (SMAs) applied to the RSV, offering a smoothed representation of short-term momentum.

Component B: Employs a unique averaging method tailored to capture medium-term trends effectively.

Dynamic Gradient Color Scheme: Enhances visualization through a spectrum of colors that change dynamically based on the calculated values, making trend identification intuitive and engaging 🌈.

Customizable Horizontal Reference Lines: Key levels are marked at 0, 10, 50, and 90 to serve as benchmarks for assessing the oscillator's readings, helping traders make informed decisions quickly.

Comprehensive Visual Representation: Combines the strengths of both components into a single, gradient-colored candlestick plot, providing a holistic view of market sentiment and momentum shifts 📊.

HOW TO USE

Adding the Indicator: Start by adding the L3 Dark Horse Oscillator to your TradingView chart via the indicators menu. This will overlay the necessary plots directly onto your price chart.

Interpreting the Components: Familiarize yourself with the two primary components represented by yellow and fuchsia lines. These lines indicate the underlying momentum derived from the RSV calculations.

Monitoring Momentum Shifts: Pay close attention to the gradient-colored candlesticks, which reflect the combined strength of both components. Notice how these candles transition through various shades, signaling changes in market dynamics.

Utilizing Reference Levels: Leverage the horizontal lines at 0, 10, 50, and 90 as critical thresholds. For instance, values above 50 might suggest bullish conditions, while those below could hint at bearish tendencies.