Shadow Corp 90min Boxes90-min cycle boxes, marks 90min session highs and lows with color coded boxes.Pine Script®指標由BlackRabbitFX提供28

Intraday Time Cycle Levels (Labels + Alerts + Colors)Jag japp detta spelet fram och tbx. Tack för ert förtoende.Pine Script®指標由Andreipip提供1121

SCPEM - Socionomic Crypto Peak Model (0-85 Scale)SCPEM Indicator Overview The SCPEM (Socionomic Crypto Peak Evaluation Model) indicator is a TradingView tool designed to approximate cycle peaks in cryptocurrency markets using socionomic theory, which links market behavior to collective social mood. It generates a score from 0-85 (where 85 signals extreme euphoria and high reversal risk) and plots it as a blue line on the chart for visual backtesting and real-time analysis. #### How It Works The indicator uses technical proxies to estimate social mood factors, as Pine Script cannot fetch external data like sentiment indices or social media directly. It calculates a weighted composite score on each bar: - Proxies derive from price, volume, and volatility data. - The raw sum of factor scores (max ~28) is normalized to 0-85. - The score updates historically for backtesting, showing mood progression over time. - Alerts trigger if the score exceeds 60, indicating high peak probability. Users can adjust inputs (e.g., lengths for RSI or pivots) to fine-tune for different assets or timeframes. Metrics Used (Technical Proxies) Crypto-Specific Sentiment Approximated by RSI (overbought levels indicate greed). Social Media Euphoria Based on volume relative to its SMA (spikes suggest herding/FOMO). Broader Social Mood Proxies Derived from ATR volatility (high values signal uncertain/mixed mood). Search and Cultural Interest Proxied by OBV trend (rising accumulation implies growing interest). Socionomic Wildcard Uses Bollinger Band width (expansion for positive mood, contraction for negative). Elliott Wave Position Counts recent price pivots (more swings indicate later wave stages and exhaustion).Pine Script®指標由gtvsteve提供8

Simplified STH-MVRV + Z-ScoreSimplified Short Term Holder MVRV (STH-MVRV) + Z-Score Indicator Description: This indicator visualizes the Short Term Holder Market Value to Realized Value ratio (STH-MVRV) and its normalized Z-Score, providing insight into Bitcoin’s market cycle phases and potential overbought or oversold conditions. How it works: The STH-MVRV ratio compares the market value of coins held by short-term holders to their realized value, helping to identify periods of profit-taking or accumulation by these holders. The indicator calculates three versions: STH-MVRV (MVRV): Ratio of current MVRV to its 155-day SMA. STH-MVRV (Price): Ratio of BTC price to its 155-day SMA. STH-MVRV (AVG): Average of the above two ratios. You can select which ratio to display via the input dropdown. Threshold Lines: Adjustable upper and lower threshold lines mark significant levels where market sentiment might shift. The indicator also plots a baseline at 1.0 as a reference. Z-Score Explanation: The Z-Score is a normalized value scaled between -3 and +3, calculated relative to the chosen threshold levels. When the ratio hits the upper threshold, the Z-Score approaches +2, indicating potential overbought conditions. Conversely, reaching the lower threshold corresponds to a Z-Score near -2, signaling potential oversold conditions. This Z-Score is shown in a clear table in the top right corner of the chart for easy monitoring. Data Sources: MVRV data is fetched from the BTC_MVRV dataset. Price data is sourced from the BTC/USD index. Usage: Use this indicator to assess short-term holder market behavior and to help identify buying or selling opportunities based on extremes indicated by the Z-Score. Combining this tool with other analysis can improve timing decisions in Bitcoin trading.Pine Script®指標由simonweisser_business提供44

Katik Cycle 56 DaysThis script plots vertical dotted lines on the chart every 56 trading days, starting from the first bar. It calculates intervals based on the bar_index and draws the lines for both historical and future dates by projecting the lines forward. The lines are extended across the entire chart height using extend=extend.both, ensuring visibility regardless of chart zoom level. You can customize the interval length using the input box. Note: Use this only for 1D (Day) candle so that you can find the changes in the trend...Pine Script®指標由Katik143提供8

It Screams When Crypto BottomsGet ready to ride the crypto rollercoaster with your new favourite tool for catching Bitcoin at its juiciest, most oversold moments. This isn’t just another boring indicator — it screams when it’s time to load your bags and get ready for the ride back up! Expect it to scream just once or twice per cycle at the very bottom, so you know exactly when the party starts! Why You'll Love It: Crypto-Exclusive Magic: It does not really matter what chart you are on; this indicator only bothers about the original and realised market cap of BTC. We all know the rest will follow. Big Picture Focus: Designed for daily. No noisy intraday drama — just pure, clear signals. Screaming Alerts: When the signal hits, it’s like a neon sign screaming, “Crypto Bottomed!" Think of this indicator as your backstage pass to the crypto world’s most dramatic moments. It’s not subtle — it’s bold, loud, and ready to help you time the market like a pro. P.S.: Use it only on a daily chart. Don’t even try it on shorter timeframes — it won’t scream, and you’ll miss the show! 🙀Pine Script®指標由AlexFuch提供44

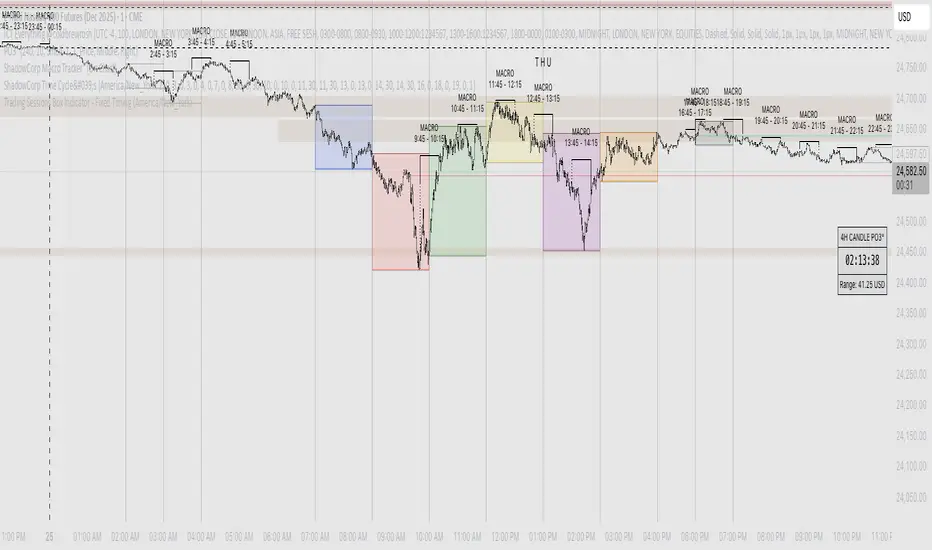

AMDX Time ZoneThis script is base on the theory of @traderdaye, on the TimeZone AMDX Accumulation Manipulation Distribution X reversal / continuation OR AMDX It show you the box on intraday Timeframe: Q1: 18.00 - 19.30 | Q2: 19.30 - 21.00 | Q3: 21.00 - 22.30 | Q4: 22.30 - 00.00 (90min Cycles of the Asian Session) Q1: 00.00 - 01.30 | Q2: 01.30 - 03.00 | Q3: 03.00 - 04.30 | Q4: 04.30 - 06.00 (90min Cycles of the London Session) Q1: 06.00 - 07.30 | Q2: 07.30 - 09.00 | Q3: 09.00 - 10.30 | Q4: 10.30 - 12.00 (90min Cycles of the NY Session) Q1: 12.00 - 13.30 | Q2: 13.30 - 15.00 | Q3: 15.00 - 16.30 | Q4: 16.30 - 18.00 (90min Cycles of the PM Session) You can extend this theory to the day => to the week => to the month Thanks LuxAlgo for the base, Hope you enjoy it Pine Script®指標由roamin129提供55739

OPEX & VIX Expiry Markers (Past, Present, Future)Expiry Date Indicator for Options & Index Traders Track Key Expiration Dates Automatically For traders focused on options, indices, and expiration-based strategies, staying aware of key expiration dates is essential. This TradingView indicator automatically plots OPEX, VIX Expiry, and Quarterly Expirations on your charts—helping you plan trades more effectively without manual tracking. Features: ✔ OPEX Expiration Markers – Highlights the third Friday of each month, when equity and index options expire. ✔ VIX Expiration Tracking – Marks Wednesday VIX expirations, useful for volatility-based trades. ✔ Quarterly Expiration Highlights – Identifies major market expiration cycles for better trade management. ✔ Live Countdown to Next OPEX – Displays how many days remain until the next expiration. ✔ Works on Any Timeframe – Past, present, and future expiration dates update dynamically. ✔ Customizable Settings – Enable or disable specific features based on your trading style. Ideal for Traders Who Use: 📈 SPX / SPY / NDX / VIX Options Strategies 📅 Iron Condors, Credit Spreads, and Expiration-Based Trades This tool helps traders stay ahead of expiration cycles, ensuring they never miss an important date. Simple, effective, and built for seamless integration into your trading workflow. This keeps it professional and to the point without overhyping it. Let me know if you'd like any further refinements! 🚀Pine Script®指標由similarTruffle37447提供1151

SOL Hedge | 8500 TargetHigh efficiency and risk control. This script provides a structured framework for high-frequency execution while maintaining strict boundaries on losses and overtrading. ### Core Advantages **1. Strict Risk Management** The strategy enforces a fixed 1:3 risk-to-reward ratio. By automating the exit points immediately upon entry, it eliminates "hope-trading" or moving stop losses manually, ensuring that a single win covers the cost of three losses. **2. Overtrading Prevention** The daily trade limit (set to 100) acts as a mechanical circuit breaker. This protects the account from catastrophic "revenge trading" by hard-locking the script once the quota is reached, regardless of market conditions. **3. Execution Speed** Because the logic is purely mechanical and lacks heavy indicator processing, it is extremely lightweight. This minimizes calculation lag, allowing for rapid entry and exit cycles that are difficult to perform manually at high volumes. **4. Visual and Operational Clarity** The UI is streamlined for focus. The color-coded background provides instant confirmation of the current bias, and the simplified input panel allows for quick adjustments to pip targets without digging into the code. **5. Instrument Versatility** The pip-calculation logic is dynamic. It automatically detects the decimal precision of the asset (Forex vs. Yen pairs), making it portable across different markets without needing manual code rewrites for price formatting. **In short:** The script excels at enforcing discipline through hardcoded limits and a healthy reward-to-risk ratio. It removes emotional bias and provides a scalable framework for high-volume trading.Pine Script®策略由oxaam479提供6

ICT IPDA LookbackThis description is tailored for the TradingView community, using the specific terminology associated with Michael Huddleston's (ICT) Interbank Price Delivery Algorithm (IPDA). 📜 TradingView Indicator Description ICT IPDA Lookback Engine (20-40-60 Day Cycles) Overview This indicator automates the IPDA Data Range lookback periods as taught by Michael J. Huddleston (ICT). In the Interbank Price Delivery Algorithm, time is the primary filter. The algorithm references specific lookback windows—20, 40, and 60 trading days—to seek liquidity and rebalance inefficiencies. Instead of manually counting bars every morning, this tool plots precise vertical anchors to help you identify the Institutional Order Flow and the "Draw on Liquidity" (DOL) within the current dealing range. 🛠️ Key Features Rolling Lookback Anchors: Automatically plots red vertical lines at the 20, 40, and 60-day intervals. Time-Based Accuracy: Calculated using calendar-adjusted trading days to ensure the lines land on the correct institutional data points, regardless of weekends or holidays. Multi-Asset Support: Works seamlessly across Forex, Futures, Indices, and Commodities. Real-Time Movement: The lines shift dynamically with the current candle, maintaining the exact IPDA window as the algorithm processes new data. 💡 How to Use (ICT IPDA Logic) Define the Context: Look back at the 20-day range (Short-term), 40-day range (Intermediate-term), and 60-day range (Long-term). Identify PD Arrays: Use these vertical lines to anchor your search for Old Highs/Lows, Fair Value Gaps (FVG), and Order Blocks (OB) within those specific windows. Determine Premium vs. Discount: Check where the current price sits relative to the Highs and Lows of these three ranges to establish your Daily Bias. Quarterly Shifts: Monitor how price reacts as it reaches the extremity of the 60-day lookback, often signaling a potential "Quarterly Shift" in institutional direction. 📖 Technical Details Indicator Type: Overlay Calculations: Uses timenow and millisecond conversion for precise "Calendar Day" placement. Best Timeframes: Designed for the Daily (1D) chart but can be used on lower timeframes (H4, H1, M15) to visualize the higher-timeframe data ranges while scalping.Pine Script®指標由jellylungs提供8

Bitcoin Cycles Halvins/Tops/Bottoms By CrBeThis Script shows you the actual Bitcoin tops and bottoms dates.Pine Script®指標由crs1993提供49

Time CyclesA new version because the previous didn't work, only for my own entertainmentPine Script®指標由DanielMarcell提供141

Timeframe Quadrants | InvrsROBINHOODTimeframe Quadrant Visualizer Summary This indicator is a powerful visualization tool designed to help traders analyze price action by dividing various timeframes into four distinct, color-coded quadrants. By breaking down periods from a full year to a single minute, it offers a unique perspective on market cycles and intraday patterns. The script includes fully customizable colors and display styles, allowing you to tailor the visual output to your specific charting needs. Key Features Multiple Timeframe Divisions: Choose to divide a Year, Month, Week, Day, Hour, or Minute into four parts. Customizable Quadrant Logic: Year: Divided into calendar quarters (Jan-Mar, Apr-Jun, Jul-Sep, Oct-Dec). Month: Divided into four approximate weeks (Days 1-7, 8-14, 15-21, 22-end). Week: Divided into four 42-hour blocks, starting from Sunday at 00:00. Day: Divided into four 6-hour blocks. Hour: Divided into four 15-minute blocks. Minute: Divided into four 15-second blocks. Flexible Display Options: Visualize the quadrants as either a full Background Color overlay or a Bar Overlay that colors the price bars directly. Timeframe Separators: A vertical line is automatically drawn at the beginning of each selected timeframe (e.g., at the start of each new day when "Day" is selected), making it easy to see where each period begins. Full Color Customization: All four quadrant colors are user-definable, along with a global transparency setting to ensure the indicator complements your chart without obscuring price action. Timezone-Aware: All calculations are performed based on a user-selected timezone from a dropdown menu, ensuring accuracy and consistency across different markets and trading sessions. As an added option, there is a manual input if the timezone is not available. How to Use Add to Chart: Add the "Timeframe Quadrants" indicator to your chart. Open Settings: Hover over the indicator's name on your chart and click the Settings (gear) icon. Configure the Indicator: Timeframe: Select the primary time period you want to divide (e.g., "Day", "Week", "Hour"). Display Method: Choose whether you want the quadrants to appear as a Background Color or a Bar Overlay. Timezone: Select the desired timezone from the dropdown menu. This is crucial for aligning the quadrants with specific market sessions (e.g., "America/New_York" for the NYSE session). Quadrant Colors: Customize the color for each of the four quadrants. Transparency %: Adjust the transparency of the colors to your preference. Underlying Concepts This script operates by using Pine Script's built-in time and date variables. It identifies the current bar's position within the user-selected timeframe (timeframe_choice) and assigns it to one of four quadrants based on pre-defined logic. For example, when "Day" is selected, it uses the hour() function to determine which 6-hour block the current bar falls into. The vertical separator lines are generated by detecting a change in the relevant time unit (e.g., ta.change(dayofmonth)), which marks the first bar of a new period. Disclaimer: This tool is intended for visual analysis and pattern recognition. It does not generate buy or sell signals and should be used in conjunction with your own trading strategy and risk management. Past performance is not indicative of future results.Pine Script®指標由InvrsROBINHOOD提供17

Day of Week Highlighter# 📅 Day of Week Highlighter - Global Market Edition **Enhanced visual trading tool that highlights each day of the week with customizable colors across all major global financial market timezones.** ## 🌍 Global Market Coverage This indicator supports **27 major financial market timezones**, including: - **Asia-Pacific**: Tokyo, Sydney, Hong Kong, Singapore, Shanghai, Seoul, Mumbai, Dubai, Auckland (New Zealand) - **Europe**: London, Frankfurt, Zurich, Paris, Amsterdam, Moscow, Istanbul - **Americas**: New York, Chicago, Toronto, São Paulo, Buenos Aires - **Plus UTC and other key financial centers** ## ✨ Key Features ### 🎨 **Fully Customizable Colors** - Individual color picker for each day of the week - Transparent overlays that don't obstruct price action - Professional color scheme defaults ### 🌐 **Comprehensive Timezone Support** - 27 major global financial market timezones - Automatic daylight saving time adjustments - Perfect for multi-market analysis and global trading ### ⚙️ **Flexible Display Options** - Toggle individual days on/off - Optional day name labels with size control - Clean, professional appearance ### 📊 **Trading Applications** - **Market Session Analysis**: Identify trading patterns by day of week - **Multi-Market Coordination**: Track different markets in their local time - **Pattern Recognition**: Spot day-specific market behaviors - **Risk Management**: Avoid trading on historically volatile days ## 🔧 How to Use 1. **Add to Chart**: Apply the indicator to any timeframe 2. **Select Timezone**: Choose your preferred market timezone from the dropdown 3. **Customize Colors**: Set unique colors for each day in the settings panel 4. **Enable/Disable Days**: Toggle specific days on or off as needed 5. **Optional Labels**: Show day names with customizable label sizes ## 💡 Pro Tips - Use different color intensities to highlight your preferred trading days - Combine with other session indicators for comprehensive market timing - Perfect for swing traders who want to identify weekly patterns - Ideal for international traders managing multiple market sessions ## 🎯 Perfect For - Day traders tracking intraday patterns - Swing traders analyzing weekly cycles - International traders managing multiple markets - Anyone wanting better visual organization of their charts **Works on all timeframes and instruments. Set it once, trade with confidence!** --- *Compatible with Pine Script v6 | No repainting | Lightweight performance*Pine Script®指標由Vandalistt提供7

MoonBoys BTC Production Cost Daily═════════════════════════════════════════════════════════════ MoonBoys BTC PRODUCTION COST DAILY ═════════════════════════════════════════════════════════════ Track Bitcoin's real-time production cost using comprehensive electricity consumption data and mining economics to identify macro support/resistance zones. ═══ OVERVIEW ═══ This indicator calculates Bitcoin's actual cost of production by combining Cambridge Bitcoin Electricity Consumption Index (CBECI) data with electricity pricing models across different mining eras. It reveals where miners are profitable or underwater, providing crucial macro-level support zones that have historically acted as psychological and economic floors. Perfect for: • Identifying long-term accumulation zones • Understanding miner profitability and capitulation risk • Spotting macro support levels during bear markets • Gauging healthy vs. overheated price levels • Planning dollar-cost averaging strategies ═══ KEY FEATURES ═══ 📊 COMPREHENSIVE HISTORICAL DATA └─ 378 data points spanning 2011-2026 └─ Complete CBECI electricity consumption dataset └─ Verified accuracy: all dates and values cross-checked └─ Updates every ~14 days with new CBECI releases ⚡ ELECTRICITY COST MODELING └─ Pre-June 2019: $0.05/kWh (Early mining era) └─ Pre-April 2021: $0.04/kWh (China dominance period) └─ Post-May 2021: $0.05/kWh (China exodus, Western migration) └─ Post-April 2024: $0.05/kWh (Post-4th halving era) └─ Fully customizable for scenario analysis 🎯 DUAL COST CURVES └─ Red line: Pure electricity cost per BTC └─ Purple line: Total production cost (electricity + operations) └─ Green line: Miner price (spot + transaction fee revenue) └─ Pink fill: Zones where miners are losing money 📈 AUTOMATIC HALVING ADJUSTMENTS └─ Integrates all Bitcoin halvings (2012, 2016, 2020, 2024) └─ Block reward automatically adjusts: 50 → 25 → 12.5 → 6.25 → 3.125 └─ Accurate per-day BTC production calculations 💰 PROFIT MARGIN TRACKING └─ Annual profit margin labels (optional) └─ Shows miner profitability percentage └─ Appears on chart at electricity cost level └─ Calculated using 365-day moving average ═══ HOW TO READ IT ═══ ┌─────────────────────────────────────────────────────────┐ │ INDICATOR │ MEANING │ ├─────────────────────────────────────────────────────────┤ │ 🟢 Green Line │ Miner Price (BTC price + fee revenue)│ │ (above purple) │ → Miners profitable, healthy market │ ├─────────────────────────────────────────────────────────┤ │ 🟢 Green Line │ Price below production cost │ │ (below purple) │ → Miner capitulation zone │ │ │ → Strong historical buy signal │ ├─────────────────────────────────────────────────────────┤ │ 🔴 Red Line │ Pure electricity cost per BTC │ │ │ → Absolute minimum mining cost │ ├─────────────────────────────────────────────────────────┤ │ 🟣 Purple Line │ Total production cost │ │ │ → Break-even for miners (60% elec) │ ├─────────────────────────────────────────────────────────┤ │ 🌸 Pink Fill │ Below-cost territory │ │ │ → Miners selling at a loss │ │ │ → Historical accumulation zone │ └─────────────────────────────────────────────────────────┘ ═══ TRADING APPLICATIONS ═══ 🐻 BEAR MARKET BOTTOMS → Price touching or breaking below production cost = high probability bottom → Extended periods below cost = miner capitulation → Historical bottoms: Nov 2011, Jan 2015, Dec 2018, Nov 2022 → Strongest buy signal in macro Bitcoin investing 📈 BULL MARKET HEALTH CHECKS → Distance above production cost = market heat level → 100-200% above cost = healthy bull market → 500%+ above cost = euphoric/bubble territory → Use as take-profit reference points 💎 ACCUMULATION STRATEGY → DCA when price approaches production cost → Increase buy size when price drops below cost → Maximum allocation when 10-20% below cost → Layer entry as margin shows negative percentages ⚖️ SUPPORT/RESISTANCE ZONES → Production cost acts as macro support in downtrends → Often becomes resistance after prolonged bear markets → Price reclaiming cost = bullish structural shift → Failed reclaims = continued weakness 🔄 HALVING CYCLE ANALYSIS → Cost doubles after each halving (supply cut) → Price typically consolidates near new cost basis → Historic pattern: break above cost = new bull cycle → Track 6-12 months post-halving for trend confirmation ═══ SETTINGS GUIDE ═══ ⚡ ELECTRICITY COST ASSUMPTIONS (USD/kWh) ├─ Pre-June 2019 (0.05): Early mining era, hobby miners ├─ Pre-China Exodus 2021 (0.04): Cheap Chinese hydropower ├─ Post-May 2021 (0.05): Western migration, higher costs └─ Post-April 2024 (0.05): Current era post-4th halving 💡 Adjust these for "what if" scenarios or local costs 💰 ELECTRICITY PERCENTAGE (Default: 60%) └─ Electricity as % of total mining costs └─ Remaining 40% = hardware, labor, rent, maintenance └─ Lower % = higher total cost (more conservative) └─ Typical range: 50-70% 🎨 VISUAL TOGGLES ├─ Plot BTC Miner Price: Show/hide green line │ └─ Includes transaction fee revenue per BTC ├─ Plot Production Cost Curves: Show/hide red & purple lines └─ Plot Annual Profit Margin Labels: Show/hide margin % └─ Appears annually (Jan 1st) and on last bar ═══ HOW IT WORKS ═══ 1. ELECTRICITY CONSUMPTION DATA • Cambridge Bitcoin Electricity Consumption Index (CBECI) • Actual network-wide energy usage in TWh (terawatt-hours) • Updated bi-weekly with real hash rate data • 378 historical data points (Aug 2011 - Jan 2026) 2. COST CALCULATION FORMULA Electricity Cost per BTC = (TWh per year / 365.25 days) × (10^9 to convert to kWh) / (BTC mined per day) × (Electricity price per kWh) Total Cost per BTC = Electricity Cost / (Electricity % of total costs) 3. BTC MINED PER DAY Blocks per day (144) × Block reward • 2009-2012: 50 BTC/block = 7,200 BTC/day • 2012-2016: 25 BTC/block = 3,600 BTC/day • 2016-2020: 12.5 BTC/block = 1,800 BTC/day • 2020-2024: 6.25 BTC/block = 900 BTC/day • 2024+: 3.125 BTC/block = 450 BTC/day 4. MINER PRICE METRIC Spot close price + (Transaction fees per day / BTC mined per day) • Currently simplified with fees = 0 • Shows true revenue per BTC for miners 5. PROFIT MARGIN CALCULATION ((Miner Price / Total Cost) - 1) × 100 • Smoothed with 365-day SMA • Shows sustainable annual profitability ═══ BEST PRACTICES ═══ ✅ DO: • Use on DAILY timeframe for accuracy (designed for daily data) • Combine with on-chain metrics (SOPR, MVRV, Puell Multiple) • Layer with traditional TA for entry/exit timing • Understand this is AVERAGE global cost (varies by miner) • Use as macro filter, not short-term trading signal • Check profit margins during capitulation events ❌ DON'T: • Use as sole indicator for short-term trades • Ignore that efficient miners have much lower costs • Forget that cost is constantly rising (hash rate + difficulty) • Assume price can't go below cost (it can temporarily) • Trade based only on cost - liquidity events can wick lower • Expect instant reversals at cost levels ═══ HISTORICAL PERFORMANCE ═══ Major Bitcoin bottoms near/below production cost: 📅 November 2011 Price: ~$2 | Cost: ~$5 → 60% below cost, -95% drawdown → Bottom signal ✓ 📅 January 2015 Price: ~$150 | Cost: ~$180 → 17% below cost, -85% drawdown → Bottom signal ✓ 📅 December 2018 Price: ~$3,200 | Cost: ~$3,500 → 9% below cost, -84% drawdown → Bottom signal ✓ 📅 November 2022 Price: ~$15,500 | Cost: ~$17,000 → 9% below cost, -77% drawdown → Bottom signal ✓ Pattern: When price trades below production cost, accumulation zone. ═══ TECHNICAL NOTES ═══ • Built with Pine Script v5 • Data source: Cambridge Centre for Alternative Finance (CBECI) Updated Quaterly by Request • All dates/values verified against official CSV dataset • Electricity price adjusts based on major mining regime shifts • Uses series variables for proper historical calculation • Forward-fills data between CBECI update periods • Accounts for all 4 halvings in BTC history ═══ DATA PERIODS EXPLAINED ═══ 🏭 PRE-JUNE 2019 ($0.05/kWh) Early mining era, distributed hobby miners, average global cost 🇨🇳 JUNE 2019 - APRIL 2021 ($0.04/kWh) China dominance period, cheap hydropower in Sichuan/Yunnan 🌍 MAY 2021 - APRIL 2024 ($0.05/kWh) China ban, Western migration, renewable energy transition 🔮 POST-APRIL 2024 ($0.05/kWh) 4th halving, institutional mining, current era ═══ UNDERSTANDING MINING ECONOMICS ═══ ⚡ ELECTRICITY = 60% OF COST (Default) └─ Largest variable expense for miners └─ Directly tied to hash rate and difficulty 🔧 OTHER COSTS = 40% ├─ ASIC hardware (depreciation) ├─ Facility rent and cooling ├─ Labor and maintenance ├─ Internet and infrastructure └─ Insurance and legal 💰 REVENUE SOURCES ├─ Block subsidy (newly minted BTC) └─ Transaction fees (variable, usually 2-10% of revenue) 📉 MINER BEHAVIOR • Profitable: Accumulate BTC, expand operations • Break-even: Hold BTC, maintain operations • Unprofitable: Forced selling, potential capitulation ═══ ADVANCED USE CASES ═══ 🔬 SCENARIO ANALYSIS → Adjust electricity costs to model different regions → US miners: $0.05-0.07/kWh → Nordic miners: $0.02-0.04/kWh → Middle East: $0.01-0.03/kWh 📊 COMBINE WITH ON-CHAIN DATA → Miner Net Position Change (selling pressure) → Hash Ribbons (miner capitulation indicator) → Difficulty Ribbon (hash rate compression) → Puell Multiple (miner revenue extremes) 🎯 MULTI-TIMEFRAME CONFLUENCE → Weekly chart: macro trend and cost support → Daily chart: precise entry/exit near cost → 4H chart: short-term reactions at cost levels 🌐 CORRELATION TRADING → Miner stocks (MARA, RIOT, CLSK) vs BTC cost → When BTC < cost, miner stocks typically -30-50% → Energy prices (oil, nat gas) affect mining costs ═══ LIMITATIONS & CONSIDERATIONS ═══ ⚠️ AVERAGE COST, NOT ACTUAL • Large miners with PPAs have costs as low as $0.02-0.03/kWh • Inefficient miners may have costs 2-3x the average • This shows network-wide average for reference ⚠️ ELECTRICITY PRICE ASSUMPTIONS • Static periods vs. dynamic energy markets • Renewable energy % growing = lower average cost over time • Geographic distribution matters (Texas vs. Kazakhstan) ⚠️ DOESN'T INCLUDE • ASIC efficiency improvements (more hash/watt) • Stranded energy and flare gas mining • Government subsidies or penalties • Seasonal variations (wet/dry seasons) ⚠️ LAGGING INDICATOR • CBECI data updates every ~14 days • Historical data, not forward-looking • Cost always rises, but at variable rate ═══ DISCLAIMER ═══ This indicator visualizes Bitcoin's estimated global average production cost based on publicly available electricity consumption data and modeled pricing assumptions. It does NOT: • Guarantee future price movements or bottoms • Account for individual miner profitability variations • Include all operational costs (simplified to electricity %) • Predict miner capitulation or selling pressure • Constitute financial advice or buy/sell signals Production cost is A REFERENCE POINT, not a hard floor. Price can and has traded below cost during extreme capitulation events. Market liquidity, macro conditions, and sentiment often override cost-basis logic in the short term. Always conduct your own research and use proper risk management. 📚 EDUCATIONAL USE ONLY | NOT FINANCIAL ADVICE ═══ RESOURCES ═══ Cambridge Bitcoin Electricity Consumption Index (CBECI) → ccaf.io Bitcoin Mining Economics → insights.braiins.com Block Reward Halving Schedule → www.bitcoinblockhalf.com Difficulty & Hash Rate Charts → www.blockchain.com Understanding ASIC Mining → academy.binance.com Mining Profitability Calculator → www.coinwarz.com On-Chain Miner Metrics → cryptoquant.com Energy & Mining Data → hashrateindex.com ═══════════════════════════════════════════════════════════ Built for the Bitcoin community 🚀 Because understanding the cost of production is fundamental analysis 💎 ═══════════════════════════════════════════════════════════Pine Script®指標由VickzinBK提供1

Goertzel Browser [Loxx]As the financial markets become increasingly complex and data-driven, traders and analysts must leverage powerful tools to gain insights and make informed decisions. One such tool is the Goertzel Browser indicator, a sophisticated technical analysis indicator that helps identify cyclical patterns in financial data. This powerful tool is capable of detecting cyclical patterns in financial data, helping traders to make better predictions and optimize their trading strategies. With its unique combination of mathematical algorithms and advanced charting capabilities, this indicator has the potential to revolutionize the way we approach financial modeling and trading. █ Brief Overview of the Goertzel Browser The Goertzel Browser is a sophisticated technical analysis tool that utilizes the Goertzel algorithm to analyze and visualize cyclical components within a financial time series. By identifying these cycles and their characteristics, the indicator aims to provide valuable insights into the market's underlying price movements, which could potentially be used for making informed trading decisions. The primary purpose of this indicator is to: 1. Detect and analyze the dominant cycles present in the price data. 2. Reconstruct and visualize the composite wave based on the detected cycles. 3. Project the composite wave into the future, providing a potential roadmap for upcoming price movements. To achieve this, the indicator performs several tasks: 1. Detrending the price data: The indicator preprocesses the price data using various detrending techniques, such as Hodrick-Prescott filters, zero-lag moving averages, and linear regression, to remove the underlying trend and focus on the cyclical components. 2. Applying the Goertzel algorithm: The indicator applies the Goertzel algorithm to the detrended price data, identifying the dominant cycles and their characteristics, such as amplitude, phase, and cycle strength. 3. Constructing the composite wave: The indicator reconstructs the composite wave by combining the detected cycles, either by using a user-defined list of cycles or by selecting the top N cycles based on their amplitude or cycle strength. 4. Visualizing the composite wave: The indicator plots the composite wave, using solid lines for the past and dotted lines for the future projections. The color of the lines indicates whether the wave is increasing or decreasing. 5. Displaying cycle information: The indicator provides a table that displays detailed information about the detected cycles, including their rank, period, Bartel's test results, amplitude, and phase. This indicator is a powerful tool that employs the Goertzel algorithm to analyze and visualize the cyclical components within a financial time series. By providing insights into the underlying price movements and their potential future trajectory, the indicator aims to assist traders in making more informed decisions. █ What is the Goertzel Algorithm? The Goertzel algorithm, named after Gerald Goertzel, is a digital signal processing technique that is used to efficiently compute individual terms of the Discrete Fourier Transform (DFT). It was first introduced in 1958, and since then, it has found various applications in the fields of engineering, mathematics, and physics. The Goertzel algorithm is primarily used to detect specific frequency components within a digital signal, making it particularly useful in applications where only a few frequency components are of interest. The algorithm is computationally efficient, as it requires fewer calculations than the Fast Fourier Transform (FFT) when detecting a small number of frequency components. This efficiency makes the Goertzel algorithm a popular choice in applications such as: 1. Telecommunications: The Goertzel algorithm is used for decoding Dual-Tone Multi-Frequency (DTMF) signals, which are the tones generated when pressing buttons on a telephone keypad. By identifying specific frequency components, the algorithm can accurately determine which button has been pressed. 2. Audio processing: The algorithm can be used to detect specific pitches or harmonics in an audio signal, making it useful in applications like pitch detection and tuning musical instruments. 3. Vibration analysis: In the field of mechanical engineering, the Goertzel algorithm can be applied to analyze vibrations in rotating machinery, helping to identify faulty components or signs of wear. 4. Power system analysis: The algorithm can be used to measure harmonic content in power systems, allowing engineers to assess power quality and detect potential issues. The Goertzel algorithm is used in these applications because it offers several advantages over other methods, such as the FFT: 1. Computational efficiency: The Goertzel algorithm requires fewer calculations when detecting a small number of frequency components, making it more computationally efficient than the FFT in these cases. 2. Real-time analysis: The algorithm can be implemented in a streaming fashion, allowing for real-time analysis of signals, which is crucial in applications like telecommunications and audio processing. 3. Memory efficiency: The Goertzel algorithm requires less memory than the FFT, as it only computes the frequency components of interest. 4. Precision: The algorithm is less susceptible to numerical errors compared to the FFT, ensuring more accurate results in applications where precision is essential. The Goertzel algorithm is an efficient digital signal processing technique that is primarily used to detect specific frequency components within a signal. Its computational efficiency, real-time capabilities, and precision make it an attractive choice for various applications, including telecommunications, audio processing, vibration analysis, and power system analysis. The algorithm has been widely adopted since its introduction in 1958 and continues to be an essential tool in the fields of engineering, mathematics, and physics. █ Goertzel Algorithm in Quantitative Finance: In-Depth Analysis and Applications The Goertzel algorithm, initially designed for signal processing in telecommunications, has gained significant traction in the financial industry due to its efficient frequency detection capabilities. In quantitative finance, the Goertzel algorithm has been utilized for uncovering hidden market cycles, developing data-driven trading strategies, and optimizing risk management. This section delves deeper into the applications of the Goertzel algorithm in finance, particularly within the context of quantitative trading and analysis. Unveiling Hidden Market Cycles: Market cycles are prevalent in financial markets and arise from various factors, such as economic conditions, investor psychology, and market participant behavior. The Goertzel algorithm's ability to detect and isolate specific frequencies in price data helps trader analysts identify hidden market cycles that may otherwise go unnoticed. By examining the amplitude, phase, and periodicity of each cycle, traders can better understand the underlying market structure and dynamics, enabling them to develop more informed and effective trading strategies. Developing Quantitative Trading Strategies: The Goertzel algorithm's versatility allows traders to incorporate its insights into a wide range of trading strategies. By identifying the dominant market cycles in a financial instrument's price data, traders can create data-driven strategies that capitalize on the cyclical nature of markets. For instance, a trader may develop a mean-reversion strategy that takes advantage of the identified cycles. By establishing positions when the price deviates from the predicted cycle, the trader can profit from the subsequent reversion to the cycle's mean. Similarly, a momentum-based strategy could be designed to exploit the persistence of a dominant cycle by entering positions that align with the cycle's direction. Enhancing Risk Management: The Goertzel algorithm plays a vital role in risk management for quantitative strategies. By analyzing the cyclical components of a financial instrument's price data, traders can gain insights into the potential risks associated with their trading strategies. By monitoring the amplitude and phase of dominant cycles, a trader can detect changes in market dynamics that may pose risks to their positions. For example, a sudden increase in amplitude may indicate heightened volatility, prompting the trader to adjust position sizing or employ hedging techniques to protect their portfolio. Additionally, changes in phase alignment could signal a potential shift in market sentiment, necessitating adjustments to the trading strategy. Expanding Quantitative Toolkits: Traders can augment the Goertzel algorithm's insights by combining it with other quantitative techniques, creating a more comprehensive and sophisticated analysis framework. For example, machine learning algorithms, such as neural networks or support vector machines, could be trained on features extracted from the Goertzel algorithm to predict future price movements more accurately. Furthermore, the Goertzel algorithm can be integrated with other technical analysis tools, such as moving averages or oscillators, to enhance their effectiveness. By applying these tools to the identified cycles, traders can generate more robust and reliable trading signals. The Goertzel algorithm offers invaluable benefits to quantitative finance practitioners by uncovering hidden market cycles, aiding in the development of data-driven trading strategies, and improving risk management. By leveraging the insights provided by the Goertzel algorithm and integrating it with other quantitative techniques, traders can gain a deeper understanding of market dynamics and devise more effective trading strategies. █ Indicator Inputs src: This is the source data for the analysis, typically the closing price of the financial instrument. detrendornot: This input determines the method used for detrending the source data. Detrending is the process of removing the underlying trend from the data to focus on the cyclical components. The available options are: hpsmthdt: Detrend using Hodrick-Prescott filter centered moving average. zlagsmthdt: Detrend using zero-lag moving average centered moving average. logZlagRegression: Detrend using logarithmic zero-lag linear regression. hpsmth: Detrend using Hodrick-Prescott filter. zlagsmth: Detrend using zero-lag moving average. DT_HPper1 and DT_HPper2: These inputs define the period range for the Hodrick-Prescott filter centered moving average when detrendornot is set to hpsmthdt. DT_ZLper1 and DT_ZLper2: These inputs define the period range for the zero-lag moving average centered moving average when detrendornot is set to zlagsmthdt. DT_RegZLsmoothPer: This input defines the period for the zero-lag moving average used in logarithmic zero-lag linear regression when detrendornot is set to logZlagRegression. HPsmoothPer: This input defines the period for the Hodrick-Prescott filter when detrendornot is set to hpsmth. ZLMAsmoothPer: This input defines the period for the zero-lag moving average when detrendornot is set to zlagsmth. MaxPer: This input sets the maximum period for the Goertzel algorithm to search for cycles. squaredAmp: This boolean input determines whether the amplitude should be squared in the Goertzel algorithm. useAddition: This boolean input determines whether the Goertzel algorithm should use addition for combining the cycles. useCosine: This boolean input determines whether the Goertzel algorithm should use cosine waves instead of sine waves. UseCycleStrength: This boolean input determines whether the Goertzel algorithm should compute the cycle strength, which is a normalized measure of the cycle's amplitude. WindowSizePast and WindowSizeFuture: These inputs define the window size for past and future projections of the composite wave. FilterBartels: This boolean input determines whether Bartel's test should be applied to filter out non-significant cycles. BartNoCycles: This input sets the number of cycles to be used in Bartel's test. BartSmoothPer: This input sets the period for the moving average used in Bartel's test. BartSigLimit: This input sets the significance limit for Bartel's test, below which cycles are considered insignificant. SortBartels: This boolean input determines whether the cycles should be sorted by their Bartel's test results. UseCycleList: This boolean input determines whether a user-defined list of cycles should be used for constructing the composite wave. If set to false, the top N cycles will be used. Cycle1, Cycle2, Cycle3, Cycle4, and Cycle5: These inputs define the user-defined list of cycles when 'UseCycleList' is set to true. If using a user-defined list, each of these inputs represents the period of a specific cycle to include in the composite wave. StartAtCycle: This input determines the starting index for selecting the top N cycles when UseCycleList is set to false. This allows you to skip a certain number of cycles from the top before selecting the desired number of cycles. UseTopCycles: This input sets the number of top cycles to use for constructing the composite wave when UseCycleList is set to false. The cycles are ranked based on their amplitudes or cycle strengths, depending on the UseCycleStrength input. SubtractNoise: This boolean input determines whether to subtract the noise (remaining cycles) from the composite wave. If set to true, the composite wave will only include the top N cycles specified by UseTopCycles. █ Exploring Auxiliary Functions The following functions demonstrate advanced techniques for analyzing financial markets, including zero-lag moving averages, Bartels probability, detrending, and Hodrick-Prescott filtering. This section examines each function in detail, explaining their purpose, methodology, and applications in finance. We will examine how each function contributes to the overall performance and effectiveness of the indicator and how they work together to create a powerful analytical tool. Zero-Lag Moving Average: The zero-lag moving average function is designed to minimize the lag typically associated with moving averages. This is achieved through a two-step weighted linear regression process that emphasizes more recent data points. The function calculates a linearly weighted moving average (LWMA) on the input data and then applies another LWMA on the result. By doing this, the function creates a moving average that closely follows the price action, reducing the lag and improving the responsiveness of the indicator. The zero-lag moving average function is used in the indicator to provide a responsive, low-lag smoothing of the input data. This function helps reduce the noise and fluctuations in the data, making it easier to identify and analyze underlying trends and patterns. By minimizing the lag associated with traditional moving averages, this function allows the indicator to react more quickly to changes in market conditions, providing timely signals and improving the overall effectiveness of the indicator. Bartels Probability: The Bartels probability function calculates the probability of a given cycle being significant in a time series. It uses a mathematical test called the Bartels test to assess the significance of cycles detected in the data. The function calculates coefficients for each detected cycle and computes an average amplitude and an expected amplitude. By comparing these values, the Bartels probability is derived, indicating the likelihood of a cycle's significance. This information can help in identifying and analyzing dominant cycles in financial markets. The Bartels probability function is incorporated into the indicator to assess the significance of detected cycles in the input data. By calculating the Bartels probability for each cycle, the indicator can prioritize the most significant cycles and focus on the market dynamics that are most relevant to the current trading environment. This function enhances the indicator's ability to identify dominant market cycles, improving its predictive power and aiding in the development of effective trading strategies. Detrend Logarithmic Zero-Lag Regression: The detrend logarithmic zero-lag regression function is used for detrending data while minimizing lag. It combines a zero-lag moving average with a linear regression detrending method. The function first calculates the zero-lag moving average of the logarithm of input data and then applies a linear regression to remove the trend. By detrending the data, the function isolates the cyclical components, making it easier to analyze and interpret the underlying market dynamics. The detrend logarithmic zero-lag regression function is used in the indicator to isolate the cyclical components of the input data. By detrending the data, the function enables the indicator to focus on the cyclical movements in the market, making it easier to analyze and interpret market dynamics. This function is essential for identifying cyclical patterns and understanding the interactions between different market cycles, which can inform trading decisions and enhance overall market understanding. Bartels Cycle Significance Test: The Bartels cycle significance test is a function that combines the Bartels probability function and the detrend logarithmic zero-lag regression function to assess the significance of detected cycles. The function calculates the Bartels probability for each cycle and stores the results in an array. By analyzing the probability values, traders and analysts can identify the most significant cycles in the data, which can be used to develop trading strategies and improve market understanding. The Bartels cycle significance test function is integrated into the indicator to provide a comprehensive analysis of the significance of detected cycles. By combining the Bartels probability function and the detrend logarithmic zero-lag regression function, this test evaluates the significance of each cycle and stores the results in an array. The indicator can then use this information to prioritize the most significant cycles and focus on the most relevant market dynamics. This function enhances the indicator's ability to identify and analyze dominant market cycles, providing valuable insights for trading and market analysis. Hodrick-Prescott Filter: The Hodrick-Prescott filter is a popular technique used to separate the trend and cyclical components of a time series. The function applies a smoothing parameter to the input data and calculates a smoothed series using a two-sided filter. This smoothed series represents the trend component, which can be subtracted from the original data to obtain the cyclical component. The Hodrick-Prescott filter is commonly used in economics and finance to analyze economic data and financial market trends. The Hodrick-Prescott filter is incorporated into the indicator to separate the trend and cyclical components of the input data. By applying the filter to the data, the indicator can isolate the trend component, which can be used to analyze long-term market trends and inform trading decisions. Additionally, the cyclical component can be used to identify shorter-term market dynamics and provide insights into potential trading opportunities. The inclusion of the Hodrick-Prescott filter adds another layer of analysis to the indicator, making it more versatile and comprehensive. Detrending Options: Detrend Centered Moving Average: The detrend centered moving average function provides different detrending methods, including the Hodrick-Prescott filter and the zero-lag moving average, based on the selected detrending method. The function calculates two sets of smoothed values using the chosen method and subtracts one set from the other to obtain a detrended series. By offering multiple detrending options, this function allows traders and analysts to select the most appropriate method for their specific needs and preferences. The detrend centered moving average function is integrated into the indicator to provide users with multiple detrending options, including the Hodrick-Prescott filter and the zero-lag moving average. By offering multiple detrending methods, the indicator allows users to customize the analysis to their specific needs and preferences, enhancing the indicator's overall utility and adaptability. This function ensures that the indicator can cater to a wide range of trading styles and objectives, making it a valuable tool for a diverse group of market participants. The auxiliary functions functions discussed in this section demonstrate the power and versatility of mathematical techniques in analyzing financial markets. By understanding and implementing these functions, traders and analysts can gain valuable insights into market dynamics, improve their trading strategies, and make more informed decisions. The combination of zero-lag moving averages, Bartels probability, detrending methods, and the Hodrick-Prescott filter provides a comprehensive toolkit for analyzing and interpreting financial data. The integration of advanced functions in a financial indicator creates a powerful and versatile analytical tool that can provide valuable insights into financial markets. By combining the zero-lag moving average, █ In-Depth Analysis of the Goertzel Browser Code The Goertzel Browser code is an implementation of the Goertzel Algorithm, an efficient technique to perform spectral analysis on a signal. The code is designed to detect and analyze dominant cycles within a given financial market data set. This section will provide an extremely detailed explanation of the code, its structure, functions, and intended purpose. Function signature and input parameters: The Goertzel Browser function accepts numerous input parameters for customization, including source data (src), the current bar (forBar), sample size (samplesize), period (per), squared amplitude flag (squaredAmp), addition flag (useAddition), cosine flag (useCosine), cycle strength flag (UseCycleStrength), past and future window sizes (WindowSizePast, WindowSizeFuture), Bartels filter flag (FilterBartels), Bartels-related parameters (BartNoCycles, BartSmoothPer, BartSigLimit), sorting flag (SortBartels), and output buffers (goeWorkPast, goeWorkFuture, cyclebuffer, amplitudebuffer, phasebuffer, cycleBartelsBuffer). Initializing variables and arrays: The code initializes several float arrays (goeWork1, goeWork2, goeWork3, goeWork4) with the same length as twice the period (2 * per). These arrays store intermediate results during the execution of the algorithm. Preprocessing input data: The input data (src) undergoes preprocessing to remove linear trends. This step enhances the algorithm's ability to focus on cyclical components in the data. The linear trend is calculated by finding the slope between the first and last values of the input data within the sample. Iterative calculation of Goertzel coefficients: The core of the Goertzel Browser algorithm lies in the iterative calculation of Goertzel coefficients for each frequency bin. These coefficients represent the spectral content of the input data at different frequencies. The code iterates through the range of frequencies, calculating the Goertzel coefficients using a nested loop structure. Cycle strength computation: The code calculates the cycle strength based on the Goertzel coefficients. This is an optional step, controlled by the UseCycleStrength flag. The cycle strength provides information on the relative influence of each cycle on the data per bar, considering both amplitude and cycle length. The algorithm computes the cycle strength either by squaring the amplitude (controlled by squaredAmp flag) or using the actual amplitude values. Phase calculation: The Goertzel Browser code computes the phase of each cycle, which represents the position of the cycle within the input data. The phase is calculated using the arctangent function (math.atan) based on the ratio of the imaginary and real components of the Goertzel coefficients. Peak detection and cycle extraction: The algorithm performs peak detection on the computed amplitudes or cycle strengths to identify dominant cycles. It stores the detected cycles in the cyclebuffer array, along with their corresponding amplitudes and phases in the amplitudebuffer and phasebuffer arrays, respectively. Sorting cycles by amplitude or cycle strength: The code sorts the detected cycles based on their amplitude or cycle strength in descending order. This allows the algorithm to prioritize cycles with the most significant impact on the input data. Bartels cycle significance test: If the FilterBartels flag is set, the code performs a Bartels cycle significance test on the detected cycles. This test determines the statistical significance of each cycle and filters out the insignificant cycles. The significant cycles are stored in the cycleBartelsBuffer array. If the SortBartels flag is set, the code sorts the significant cycles based on their Bartels significance values. Waveform calculation: The Goertzel Browser code calculates the waveform of the significant cycles for both past and future time windows. The past and future windows are defined by the WindowSizePast and WindowSizeFuture parameters, respectively. The algorithm uses either cosine or sine functions (controlled by the useCosine flag) to calculate the waveforms for each cycle. The useAddition flag determines whether the waveforms should be added or subtracted. Storing waveforms in matrices: The calculated waveforms for each cycle are stored in two matrices - goeWorkPast and goeWorkFuture. These matrices hold the waveforms for the past and future time windows, respectively. Each row in the matrices represents a time window position, and each column corresponds to a cycle. Returning the number of cycles: The Goertzel Browser function returns the total number of detected cycles (number_of_cycles) after processing the input data. This information can be used to further analyze the results or to visualize the detected cycles. The Goertzel Browser code is a comprehensive implementation of the Goertzel Algorithm, specifically designed for detecting and analyzing dominant cycles within financial market data. The code offers a high level of customization, allowing users to fine-tune the algorithm based on their specific needs. The Goertzel Browser's combination of preprocessing, iterative calculations, cycle extraction, sorting, significance testing, and waveform calculation makes it a powerful tool for understanding cyclical components in financial data. █ Generating and Visualizing Composite Waveform The indicator calculates and visualizes the composite waveform for both past and future time windows based on the detected cycles. Here's a detailed explanation of this process: Updating WindowSizePast and WindowSizeFuture: The WindowSizePast and WindowSizeFuture are updated to ensure they are at least twice the MaxPer (maximum period). Initializing matrices and arrays: Two matrices, goeWorkPast and goeWorkFuture, are initialized to store the Goertzel results for past and future time windows. Multiple arrays are also initialized to store cycle, amplitude, phase, and Bartels information. Preparing the source data (srcVal) array: The source data is copied into an array, srcVal, and detrended using one of the selected methods (hpsmthdt, zlagsmthdt, logZlagRegression, hpsmth, or zlagsmth). Goertzel function call: The Goertzel function is called to analyze the detrended source data and extract cycle information. The output, number_of_cycles, contains the number of detected cycles. Initializing arrays for past and future waveforms: Three arrays, epgoertzel, goertzel, and goertzelFuture, are initialized to store the endpoint Goertzel, non-endpoint Goertzel, and future Goertzel projections, respectively. Calculating composite waveform for past bars (goertzel array): The past composite waveform is calculated by summing the selected cycles (either from the user-defined cycle list or the top cycles) and optionally subtracting the noise component. Calculating composite waveform for future bars (goertzelFuture array): The future composite waveform is calculated in a similar way as the past composite waveform. Drawing past composite waveform (pvlines): The past composite waveform is drawn on the chart using solid lines. The color of the lines is determined by the direction of the waveform (green for upward, red for downward). Drawing future composite waveform (fvlines): The future composite waveform is drawn on the chart using dotted lines. The color of the lines is determined by the direction of the waveform (fuchsia for upward, yellow for downward). Displaying cycle information in a table (table3): A table is created to display the cycle information, including the rank, period, Bartel value, amplitude (or cycle strength), and phase of each detected cycle. Filling the table with cycle information: The indicator iterates through the detected cycles and retrieves the relevant information (period, amplitude, phase, and Bartel value) from the corresponding arrays. It then fills the table with this information, displaying the values up to six decimal places. To summarize, this indicator generates a composite waveform based on the detected cycles in the financial data. It calculates the composite waveforms for both past and future time windows and visualizes them on the chart using colored lines. Additionally, it displays detailed cycle information in a table, including the rank, period, Bartel value, amplitude (or cycle strength), and phase of each detected cycle. █ Enhancing the Goertzel Algorithm-Based Script for Financial Modeling and Trading The Goertzel algorithm-based script for detecting dominant cycles in financial data is a powerful tool for financial modeling and trading. It provides valuable insights into the past behavior of these cycles and potential future impact. However, as with any algorithm, there is always room for improvement. This section discusses potential enhancements to the existing script to make it even more robust and versatile for financial modeling, general trading, advanced trading, and high-frequency finance trading. Enhancements for Financial Modeling Data preprocessing: One way to improve the script's performance for financial modeling is to introduce more advanced data preprocessing techniques. This could include removing outliers, handling missing data, and normalizing the data to ensure consistent and accurate results. Additional detrending and smoothing methods: Incorporating more sophisticated detrending and smoothing techniques, such as wavelet transform or empirical mode decomposition, can help improve the script's ability to accurately identify cycles and trends in the data. Machine learning integration: Integrating machine learning techniques, such as artificial neural networks or support vector machines, can help enhance the script's predictive capabilities, leading to more accurate financial models. Enhancements for General and Advanced Trading Customizable indicator integration: Allowing users to integrate their own technical indicators can help improve the script's effectiveness for both general and advanced trading. By enabling the combination of the dominant cycle information with other technical analysis tools, traders can develop more comprehensive trading strategies. Risk management and position sizing: Incorporating risk management and position sizing functionality into the script can help traders better manage their trades and control potential losses. This can be achieved by calculating the optimal position size based on the user's risk tolerance and account size. Multi-timeframe analysis: Enhancing the script to perform multi-timeframe analysis can provide traders with a more holistic view of market trends and cycles. By identifying dominant cycles on different timeframes, traders can gain insights into the potential confluence of cycles and make better-informed trading decisions. Enhancements for High-Frequency Finance Trading Algorithm optimization: To ensure the script's suitability for high-frequency finance trading, optimizing the algorithm for faster execution is crucial. This can be achieved by employing efficient data structures and refining the calculation methods to minimize computational complexity. Real-time data streaming: Integrating real-time data streaming capabilities into the script can help high-frequency traders react to market changes more quickly. By continuously updating the cycle information based on real-time market data, traders can adapt their strategies accordingly and capitalize on short-term market fluctuations. Order execution and trade management: To fully leverage the script's capabilities for high-frequency trading, implementing functionality for automated order execution and trade management is essential. This can include features such as stop-loss and take-profit orders, trailing stops, and automated trade exit strategies. While the existing Goertzel algorithm-based script is a valuable tool for detecting dominant cycles in financial data, there are several potential enhancements that can make it even more powerful for financial modeling, general trading, advanced trading, and high-frequency finance trading. By incorporating these improvements, the script can become a more versatile and effective tool for traders and financial analysts alike. █ Understanding the Limitations of the Goertzel Algorithm While the Goertzel algorithm-based script for detecting dominant cycles in financial data provides valuable insights, it is important to be aware of its limitations and drawbacks. Some of the key drawbacks of this indicator are: Lagging nature: As with many other technical indicators, the Goertzel algorithm-based script can suffer from lagging effects, meaning that it may not immediately react to real-time market changes. This lag can lead to late entries and exits, potentially resulting in reduced profitability or increased losses. Parameter sensitivity: The performance of the script can be sensitive to the chosen parameters, such as the detrending methods, smoothing techniques, and cycle detection settings. Improper parameter selection may lead to inaccurate cycle detection or increased false signals, which can negatively impact trading performance. Complexity: The Goertzel algorithm itself is relatively complex, making it difficult for novice traders or those unfamiliar with the concept of cycle analysis to fully understand and effectively utilize the script. This complexity can also make it challenging to optimize the script for specific trading styles or market conditions. Overfitting risk: As with any data-driven approach, there is a risk of overfitting when using the Goertzel algorithm-based script. Overfitting occurs when a model becomes too specific to the historical data it was trained on, leading to poor performance on new, unseen data. This can result in misleading signals and reduced trading performance. No guarantee of future performance: While the script can provide insights into past cycles and potential future trends, it is important to remember that past performance does not guarantee future results. Market conditions can change, and relying solely on the script's predictions without considering other factors may lead to poor trading decisions. Limited applicability: The Goertzel algorithm-based script may not be suitable for all markets, trading styles, or timeframes. Its effectiveness in detecting cycles may be limited in certain market conditions, such as during periods of extreme volatility or low liquidity. While the Goertzel algorithm-based script offers valuable insights into dominant cycles in financial data, it is essential to consider its drawbacks and limitations when incorporating it into a trading strategy. Traders should always use the script in conjunction with other technical and fundamental analysis tools, as well as proper risk management, to make well-informed trading decisions. █ Interpreting Results The Goertzel Browser indicator can be interpreted by analyzing the plotted lines and the table presented alongside them. The indicator plots two lines: past and future composite waves. The past composite wave represents the composite wave of the past price data, and the future composite wave represents the projected composite wave for the next period. The past composite wave line displays a solid line, with green indicating a bullish trend and red indicating a bearish trend. On the other hand, the future composite wave line is a dotted line with fuchsia indicating a bullish trend and yellow indicating a bearish trend. The table presented alongside the indicator shows the top cycles with their corresponding rank, period, Bartels, amplitude or cycle strength, and phase. The amplitude is a measure of the strength of the cycle, while the phase is the position of the cycle within the data series. Interpreting the Goertzel Browser indicator involves identifying the trend of the past and future composite wave lines and matching them with the corresponding bullish or bearish color. Additionally, traders can identify the top cycles with the highest amplitude or cycle strength and utilize them in conjunction with other technical indicators and fundamental analysis for trading decisions. This indicator is considered a repainting indicator because the value of the indicator is calculated based on the past price data. As new price data becomes available, the indicator's value is recalculated, potentially causing the indicator's past values to change. This can create a false impression of the indicator's performance, as it may appear to have provided a profitable trading signal in the past when, in fact, that signal did not exist at the time. The Goertzel indicator is also non-endpointed, meaning that it is not calculated up to the current bar or candle. Instead, it uses a fixed amount of historical data to calculate its values, which can make it difficult to use for real-time trading decisions. For example, if the indicator uses 100 bars of historical data to make its calculations, it cannot provide a signal until the current bar has closed and become part of the historical data. This can result in missed trading opportunities or delayed signals. █ Conclusion The Goertzel Browser indicator is a powerful tool for identifying and analyzing cyclical patterns in financial markets. Its ability to detect multiple cycles of varying frequencies and strengths make it a valuable addition to any trader's technical analysis toolkit. However, it is important to keep in mind that the Goertzel Browser indicator should be used in conjunction with other technical analysis tools and fundamental analysis to achieve the best results. With continued refinement and development, the Goertzel Browser indicator has the potential to become a highly effective tool for financial modeling, general trading, advanced trading, and high-frequency finance trading. Its accuracy and versatility make it a promising candidate for further research and development. █ Footnotes What is the Bartels Test for Cycle Significance? The Bartels Cycle Significance Test is a statistical method that determines whether the peaks and troughs of a time series are statistically significant. The test is named after its inventor, George Bartels, who developed it in the mid-20th century. The Bartels test is designed to analyze the cyclical components of a time series, which can help traders and analysts identify trends and cycles in financial markets. The test calculates a Bartels statistic, which measures the degree of non-randomness or autocorrelation in the time series. The Bartels statistic is calculated by first splitting the time series into two halves and calculating the range of the peaks and troughs in each half. The test then compares these ranges using a t-test, which measures the significance of the difference between the two ranges. If the Bartels statistic is greater than a critical value, it indicates that the peaks and troughs in the time series are non-random and that there is a significant cyclical component to the data. Conversely, if the Bartels statistic is less than the critical value, it suggests that the peaks and troughs are random and that there is no significant cyclical component. The Bartels Cycle Significance Test is particularly useful in financial analysis because it can help traders and analysts identify significant cycles in asset prices, which can in turn inform investment decisions. However, it is important to note that the test is not perfect and can produce false signals in certain situations, particularly in noisy or volatile markets. Therefore, it is always recommended to use the test in conjunction with other technical and fundamental indicators to confirm trends and cycles. Deep-dive into the Hodrick-Prescott Fitler The Hodrick-Prescott (HP) filter is a statistical tool used in economics and finance to separate a time series into two components: a trend component and a cyclical component. It is a powerful tool for identifying long-term trends in economic and financial data and is widely used by economists, central banks, and financial institutions around the world. The HP filter was first introduced in the 1990s by economists Robert Hodrick and Edward Prescott. It is a simple, two-parameter filter that separates a time series into a trend component and a cyclical component. The trend component represents the long-term behavior of the data, while the cyclical component captures the shorter-term fluctuations around the trend. The HP filter works by minimizing the following objective function: Minimize: (Sum of Squared Deviations) + λ (Sum of Squared Second Differences) Where: The first term represents the deviation of the data from the trend. The second term represents the smoothness of the trend. λ is a smoothing parameter that determines the degree of smoothness of the trend. The smoothing parameter λ is typically set to a value between 100 and 1600, depending on the frequency of the data. Higher values of λ lead to a smoother trend, while lower values lead to a more volatile trend. The HP filter has several advantages over other smoothing techniques. It is a non-parametric method, meaning that it does not make any assumptions about the underlying distribution of the data. It also allows for easy comparison of trends across different time series and can be used with data of any frequency. However, the HP filter also has some limitations. It assumes that the trend is a smooth function, which may not be the case in some situations. It can also be sensitive to changes in the smoothing parameter λ, which may result in different trends for the same data. Additionally, the filter may produce unrealistic trends for very short time series. Despite these limitations, the HP filter remains a valuable tool for analyzing economic and financial data. It is widely used by central banks and financial institutions to monitor long-term trends in the economy, and it can be used to identify turning points in the business cycle. The filter can also be used to analyze asset prices, exchange rates, and other financial variables. The Hodrick-Prescott filter is a powerful tool for analyzing economic and financial data. It separates a time series into a trend component and a cyclical component, allowing for easy identification of long-term trends and turning points in the business cycle. While it has some limitations, it remains a valuable tool for economists, central banks, and financial institutions around the world.Pine Script®指標由loxx提供1111323