Fibonacci Exponential Moving Averages ( EMA )Here you can have 4 EMA on one indicator. The inputs are for 8, 13, 21 and 55 previous open&close which are from Fibonacci sequence.

How to : To use the script, click on "Add to Favourite Scripts", then load the script from Indicators on the Chart.

在腳本中搜尋"Exponential"

Fibonacci Exponential Moving Averages ( EMA )

Have 8, 13, 21 and 55 EMA on one indicator ! enjoy :)

R.N

Difference of Exponentially Weighted AveragesImplementation of Difference of Exponentially Weighted Averages in Pine Script. It can generate a line that adjust to the overall trend of a graphic. The lines that are generated in a new plot are the the Difference of Exponentially Weighted Averages (blue) and it binarization over the previous values.

Exponentially Weighted Averages

This technique is used for generating smoother lines that adjust to a graphic. In finances, it is used to predict the overall trend of a graphic. The function that defines the EWA is the one bellow:

Vt = β V(t-1) + (1 - β) θt

Where:

β: Hyper-parameter that we have to adjust.

V(t-1): Value calculated for the previous element of the graphic.

θt: Current element of the graphic.

The calculus of differences consist in subtract to each value the previous values.

Kalman Exponentialy Weighted Moving Average | MisinkoMasterThe Kalman Exponentialy Weighted Moving Average is a technical analysis tool providing users with more responsive and smoother signals, providing crystal-clear signals and giving investors valuable insights on market trends, however it could be used in many cases.

A deeper dive into the indicator:

When going through my creation of strategies, I had stumbled on an indicator called "EWMA", which worked decently, but it was far too simple in my opinion so I decided to combine the EMA & WMA, but with a little more complexity, and it has worked .

I began by learning how both MAs work, I already knew how WMA works, but EMA I did not.

After learning both I found out they were quite simple in principle and that there was a way to combine them in such way that you would get really good signals, however it was way too noisy.

While it could avoid major dumps that were not avoided by most indicators, it would lose that edge because of being too noisy.

After testing out many conditions, combinations & more, the best working one was this one:

WMA > KEWMA = long

WMA < KEWMA = short

I will explain this later, but this gave fast signals, and while it still was noisy it was better then before.

To smooth it out, I started testing price filters => Gaussian Filter and many more were tested out, but they either slowed it down to the point it was no longer of much use, or did not smooth it at all.

After testing the Kalman filter on this thing, I was shocked.

It was just right and made the indicator a lot better, smoothed it and kept most of the responsivness it had.

Now to the big question: "How is it calculated?"

Now first it needs to calculate the Kalman source, which smooths the source which will be used.

After that, we calculate the Weighted Moving Average for " n " period on the Kalman source.

Now that we have our WMA values, we need to calculate " a ".

a is calculated in the following formula:

a = 2/(1+ n )

where n is the user defined length

Now for the last part:

KEWMA = WMAyesterday * (1-a) + WMAtoday * a

This creates a very accurate and reactive indicator, that can prove useful in many uses, beyond those I will and did talk about.

For the trend logic as mentioned before:

Long = WMA > KEWMA

Short = WMA < KEWMA

This worked best, but you might find better ways of using it.

I think that is all I have to say about it, I left it open source so you can all code it in your strategies and play around with it.

Enjoy Gs!

Hybrid Adaptive Double Exponential Smoothing🙏🏻 This is HADES (Hybrid Adaptive Double Exponential Smoothing) : fully data-driven & adaptive exponential smoothing method, that gains all the necessary info directly from data in the most natural way and needs no subjective parameters & no optimizations. It gets applied to data itself -> to fit residuals & one-point forecast errors, all at O(1) algo complexity. I designed it for streaming high-frequency univariate time series data, such as medical sensor readings, orderbook data, tick charts, requests generated by a backend, etc.

The HADES method is:

fit & forecast = a + b * (1 / alpha + T - 1)

T = 0 provides in-sample fit for the current datum, and T + n provides forecast for n datapoints.

y = input time series

a = y, if no previous data exists

b = 0, if no previous data exists

otherwise:

a = alpha * y + (1 - alpha) * a

b = alpha * (a - a ) + (1 - alpha) * b

alpha = 1 / sqrt(len * 4)

len = min(ceil(exp(1 / sig)), available data)

sig = sqrt(Absolute net change in y / Sum of absolute changes in y)

For the start datapoint when both numerator and denominator are zeros, we define 0 / 0 = 1

...

The same set of operations gets applied to the data first, then to resulting fit absolute residuals to build prediction interval, and finally to absolute forecasting errors (from one-point ahead forecast) to build forecasting interval:

prediction interval = data fit +- resoduals fit * k

forecasting interval = data opf +- errors fit * k

where k = multiplier regulating intervals width, and opf = one-point forecasts calculated at each time t

...

How-to:

0) Apply to your data where it makes sense, eg. tick data;

1) Use power transform to compensate for multiplicative behavior in case it's there;

2) If you have complete data or only the data you need, like the full history of adjusted close prices: go to the next step; otherwise, guided by your goal & analysis, adjust the 'start index' setting so the calculations will start from this point;

3) Use prediction interval to detect significant deviations from the process core & make decisions according to your strategy;

4) Use one-point forecast for nowcasting;

5) Use forecasting intervals to ~ understand where the next datapoints will emerge, given the data-generating process will stay the same & lack structural breaks.

I advise k = 1 or 1.5 or 4 depending on your goal, but 1 is the most natural one.

...

Why exponential smoothing at all? Why the double one? Why adaptive? Why not Holt's method?

1) It's O(1) algo complexity & recursive nature allows it to be applied in an online fashion to high-frequency streaming data; otherwise, it makes more sense to use other methods;

2) Double exponential smoothing ensures we are taking trends into account; also, in order to model more complex time series patterns such as seasonality, we need detrended data, and this method can be used to do it;

3) The goal of adaptivity is to eliminate the window size question, in cases where it doesn't make sense to use cumulative moving typical value;

4) Holt's method creates a certain interaction between level and trend components, so its results lack symmetry and similarity with other non-recursive methods such as quantile regression or linear regression. Instead, I decided to base my work on the original double exponential smoothing method published by Rob Brown in 1956, here's the original source , it's really hard to find it online. This cool dude is considered the one who've dropped exponential smoothing to open access for the first time🤘🏻

R&D; log & explanations

If you wanna read this, you gotta know, you're taking a great responsability for this long journey, and it gonna be one hell of a trip hehe

Machine learning, apprentissage automatique, машинное обучение, digital signal processing, statistical learning, data mining, deep learning, etc., etc., etc.: all these are just artificial categories created by the local population of this wonderful world, but what really separates entities globally in the Universe is solution complexity / algorithmic complexity.

In order to get the game a lil better, it's gonna be useful to read the HTES script description first. Secondly, let me guide you through the whole R&D; process.

To discover (not to invent) the fundamental universal principle of what exponential smoothing really IS, it required the review of the whole concept, understanding that many things don't add up and don't make much sense in currently available mainstream info, and building it all from the beginning while avoiding these very basic logical & implementation flaws.

Given a complete time t, and yet, always growing time series population that can't be logically separated into subpopulations, the very first question is, 'What amount of data do we need to utilize at time t?'. Two answers: 1 and all. You can't really gain much info from 1 datum, so go for the second answer: we need the whole dataset.

So, given the sequential & incremental nature of time series, the very first and basic thing we can do on the whole dataset is to calculate a cumulative , such as cumulative moving mean or cumulative moving median.

Now we need to extend this logic to exponential smoothing, which doesn't use dataset length info directly, but all cool it can be done via a formula that quantifies the relationship between alpha (smoothing parameter) and length. The popular formulas used in mainstream are:

alpha = 1 / length

alpha = 2 / (length + 1)

The funny part starts when you realize that Cumulative Exponential Moving Averages with these 2 alpha formulas Exactly match Cumulative Moving Average and Cumulative (Linearly) Weighted Moving Average, and the same logic goes on:

alpha = 3 / (length + 1.5) , matches Cumulative Weighted Moving Average with quadratic weights, and

alpha = 4 / (length + 2) , matches Cumulative Weighted Moving Average with cubic weghts, and so on...

It all just cries in your shoulder that we need to discover another, native length->alpha formula that leverages the recursive nature of exponential smoothing, because otherwise, it doesn't make sense to use it at all, since the usual CMA and CMWA can be computed incrementally at O(1) algo complexity just as exponential smoothing.

From now on I will not mention 'cumulative' or 'linearly weighted / weighted' anymore, it's gonna be implied all the time unless stated otherwise.

What we can do is to approach the thing logically and model the response with a little help from synthetic data, a sine wave would suffice. Then we can think of relationships: Based on algo complexity from lower to higher, we have this sequence: exponential smoothing @ O(1) -> parametric statistics (mean) @ O(n) -> non-parametric statistics (50th percentile / median) @ O(n log n). Based on Initial response from slow to fast: mean -> median Based on convergence with the real expected value from slow to fast: mean (infinitely approaches it) -> median (gets it quite fast).

Based on these inputs, we need to discover such a length->alpha formula so the resulting fit will have the slowest initial response out of all 3, and have the slowest convergence with expected value out of all 3. In order to do it, we need to have some non-linear transformer in our formula (like a square root) and a couple of factors to modify the response the way we need. I ended up with this formula to meet all our requirements:

alpha = sqrt(1 / length * 2) / 2

which simplifies to:

alpha = 1 / sqrt(len * 8)

^^ as you can see on the screenshot; where the red line is median, the blue line is the mean, and the purple line is exponential smoothing with the formulas you've just seen, we've met all the requirements.

Now we just have to do the same procedure to discover the length->alpha formula but for double exponential smoothing, which models trends as well, not just level as in single exponential smoothing. For this comparison, we need to use linear regression and quantile regression instead of the mean and median.

Quantile regression requires a non-closed form solution to be solved that you can't really implement in Pine Script, but that's ok, so I made the tests using Python & sklearn:

paste.pics

^^ on this screenshot, you can see the same relationship as on the previous screenshot, but now between the responses of quantile regression & linear regression.

I followed the same logic as before for designing alpha for double exponential smoothing (also considered the initial overshoots, but that's a little detail), and ended up with this formula:

alpha = sqrt(1 / length) / 2

which simplifies to:

alpha = 1 / sqrt(len * 4)

Btw, given the pattern you see in the resulting formulas for single and double exponential smoothing, if you ever want to do triple (not Holt & Winters) exponential smoothing, you'll need len * 2 , and just len * 1 for quadruple exponential smoothing. I hope that based on this sequence, you see the hint that Maybe 4 rounds is enough.

Now since we've dealt with the length->alpha formula, we can deal with the adaptivity part.

Logically, it doesn't make sense to use a slower-than-O(1) method to generate input for an O(1) method, so it must be something universal and minimalistic: something that will help us measure consistency in our data, yet something far away from statistics and close enough to topology.

There's one perfect entity that can help us, this is fractal efficiency. The way I define fractal efficiency can be checked at the very beginning of the post, what matters is that I add a square root to the formula that is not typically added.

As explained in the description of my metric QSFS , one of the reasons for SQRT-transformed values of fractal efficiency applied in moving window mode is because they start to closely resemble normal distribution, yet with support of (0, 1). Data with this interesting property (normally distributed yet with finite support) can be modeled with the beta distribution.

Another reason is, in infinitely expanding window mode, fractal efficiency of every time series that exhibits randomness tends to infinitely approach zero, sqrt-transform kind of partially neutralizes this effect.

Yet another reason is, the square root might better reflect the dimensional inefficiency or degree of fractal complexity, since it could balance the influence of extreme deviations from the net paths.

And finally, fractals exhibit power-law scaling -> measures like length, area, or volume scale in a non-linear way. Adding a square root acknowledges this intrinsic property, while connecting our metric with the nature of fractals.

---

I suspect that, given analogies and connections with other topics in geometry, topology, fractals and most importantly positive test results of the metric, it might be that the sqrt transform is the fundamental part of fractal efficiency that should be applied by default.

Now the last part of the ballet is to convert our fractal efficiency to length value. The part about inverse proportionality is obvious: high fractal efficiency aka high consistency -> lower window size, to utilize only the last data that contain brand new information that seems to be highly reliable since we have consistency in the first place.

The non-obvious part is now we need to neutralize the side effect created by previous sqrt transform: our length values are too low, and exponentiation is the perfect candidate to fix it since translating fractal efficiency into window sizes requires something non-linear to reflect the fractal dynamics. More importantly, using exp() was the last piece that let the metric shine, any other transformations & formulas alike I've tried always had some weird results on certain data.

That exp() in the len formula was the last piece that made it all work both on synthetic and on real data.

^^ a standalone script calculating optimal dynamic window size

Omg, THAT took time to write. Comment and/or text me if you need

...

"Versace Pip-Boy, I'm a young gun coming up with no bankroll" 👻

∞

Brown's Exponential Smoothing Tool (BEST)Brown's Exponential Smoothing Tool (BEST) is a script for technical analysis in financial markets. It is designed to smooth out price fluctuations and identify trends in a given time series data.

The script begins by defining the "BEST" indicator, which will be overlaid on top of the chart. The user can then specify the source of the data (e.g. close price) and set the values for the smoothing factor (alpha) and the style of exponential smoothing (BES, DBES, or TBES).

The script then defines three functions for calculating the exponential smoothing: "bes", "tbes", and "dbes". The "bes" function applies a single iteration of exponential smoothing to the input data, using the specified alpha value. The "tbes" function applies three iterations of exponential smoothing, using the triple exponential moving average (TEMA) formula to smooth out the data even further. The "dbes" function applies two iterations of exponential smoothing, using the double exponential moving average (DEMA) formula to smooth out the data.

Finally, the script defines a "ma" function, which returns the exponential smoothing result based on the style selected by the user. The script plots the result of the "ma" function on the chart, using the color orange.

In summary, Brown's Exponential Smoothing Tool is a script for smoothing out financial time series data and identifying trends. It allows the user to choose from three different styles of exponential smoothing, each of which has its own strengths and weaknesses. By applying exponential smoothing to financial data, traders and analysts can better understand the underlying trends and make more informed decisions.

ChartRage - ELMAELMA - Exponential Logarithmic Moving Average

This is a new kind of moving average that is using exponential normalization of a logarithmic formula. The exponential function is used to average the weight on the moving average while the logarithmic function is used to calculate the overall price effect.

Features and Settings:

◻️ Following rate of change instead of absolute levels

◻️ Choose input source of the data

◻️ Real time signals through price interaction

◻️ Change ELMA length

◻️ Change the exponential decay rate

◻️ Customize base color and signal color

Equation of the ELMA:

This formula calculates a weighted average of the logarithm of prices, where more recent prices have a higher weight. The result is then exponentiated to return the ELMA value. This approach emphasizes the relative changes in price, making the ELMA sensitive to the % rate of change rather than absolute price levels. The decay rate can be adjusted in the settings.

Comparison EMA vs ELMA:

In this image we see the differences to the Exponential Moving Average.

Price Interaction and earlier Signals:

In this image we have added the bars, so we can see that the ELMA provides different signals of resistance and support zones and highlights them, by changing to the color yellow, when prices interact with the ELMA.

Strategy by trading Support and Resistance Zones:

The ELMA helps to evaluate trends and find entry points in bullish market conditions, and exit points in bearish conditions. When prices drop below the ELMA in a bull market, it is considered a buying signal. Conversely, in a bear market, it serves as an exit signal when prices trade above the ELMA.

Volatile Markets:

The ELMA works on all timeframes and markets. In this example we used the default value for Bitcoin. The ELMA clearly shows support and resistance zones. Depending on the asset, the length and the decay rate should be adjusted to provide the best results.

Real Time Signals:

Signals occur not after a candle closes but when price interacts with the ELMA level, providing real time signals by shifting color. (default = yellow)

Disclaimer* All analyses, charts, scripts, strategies, ideas, or indicators developed by us are provided for informational and educational purposes only. We do not guarantee any future results based on the use of these tools or past data. Users should trade at their own risk.

This work is licensed under Attribution-NonCommercial-ShareAlike 4.0 International

creativecommons.org

Multi Time Frame Exponential Moving Average and dasboardThis Pine script, titled "Multi Time Frame Exponential Moving Average (MTF EMA)," provides an innovative approach for traders who wish to track trends across multiple timeframes without having to switch between different charts. It combines two main features: an indicator displaying exponential moving averages (EMA) on five different time periods, as well as a compact dashboard that synthesizes this information on a single chart window.

The originality of this script lies in its ability to provide a comprehensive analysis of EMA trends across different time intervals, allowing traders to quickly and clearly understand the market dynamics without having to navigate between multiple charts. Rather than switching from one chart to another to observe trends on different time scales, traders can now consult a single dashboard to obtain all the necessary information.

The script uses exponential moving averages (EMA) to identify trends over five time periods: 5 minutes, 15 minutes, 1 hour, 4 hours, and 1 day. The values of the EMAs are calculated based on the closing prices of candles. Bullish or bearish trends are indicated by upward or downward arrows respectively, making it easy to interpret the information on the dashboard.

To use this script, traders can simply add it to their chart on the TradingView platform. They can customize the parameters of the exponential moving averages according to their preferences and choose between a dark or light theme for the dashboard. Then, they can observe trends on different time scales directly on the dashboard, enabling them to make informed trading decisions.

In summary, this script offers a practical and innovative solution for tracking trends across multiple timeframes, combining the efficiency of exponential moving averages with the convenience of a dashboard centralized on a single chart. This allows traders to save time and stay informed about market movements effectively and efficiently.

Triple Brown's Exponential Smoothing (TBES)This script is a PineScript implementation of the Triple Exponential Moving Average (TEMA) indicator, which is a trend-following indicator used in technical analysis. The TEMA attempts to reduce the lag present in other moving averages by using a triple exponential smoothing technique.

The script begins by declaring the function "indicator" with the name "TBES", and setting the "overlay" parameter to "true" to display the indicator on top of the price chart. It also defines an input parameter called "Source" which is the source data for the TEMA calculation (usually the closing price of a financial asset). It also defines an input parameter called "Alpha" which is a smoothing factor that controls the weighting of the TEMA calculation.

The script then defines the "bes" function, which stands for "Brown's Exponential Smoothing". This function takes in the source data and the alpha smoothing factor as input, and applies the double exponential smoothing calculation to produce a smoothed version of the source data.

The "tbes" function is then defined, which stands for "Triple Brown's Exponential Smoothing" and calculates the TEMA. It does this by first applying the "bes" function to the source data, then applying it again to the output of the first "bes" calculation, and then applying it a third time to the output of the second "bes" calculation. The final TEMA value is then calculated as the sum of three times the difference between the output of the first "bes" calculation and the output of the second "bes" calculation, and the output of the third "bes" calculation.

Finally, the script plots the TEMA value on the chart in green color by calling the "plot" function and passing it the output of the "tbes" function, along with a string label for the indicator.

Advanced Exponential Smoothing Indicator (AESI) [AstrideUnicorn]The Advanced Exponential Smoothing Indicator (AESI) provides a smoothed representation of price data using the exponential smoothing technique. It helps traders identify the overall trend and potential reversal points in the market.

SETTINGS

Length: The number of periods used for the calculation of the exponential moving average (EMA). Higher values provide a smoother result but may lag behind price movements.

Alpha: The smoothing factor that determines the weight of the recent price data in the smoothing calculation. Higher values give more weight to recent data, resulting in a more responsive indicator.

Cloud Mode: Determines whether to display a cloud between the AESI line and the EMA line. When enabled, the cloud represents bullish (green) and bearish (red) market conditions.

HOW TO USE

The AESI indicator consists of a single line that represents the advanced exponential smoothing of the price data. It aims to provide a smoother version of the price series, reducing noise and revealing the underlying trend.

Bullish Condition: When the AESI line is above the EMA line, it indicates a bullish market condition. Traders may consider looking for buying opportunities or holding onto existing long positions.

Bearish Condition: When the AESI line is below the EMA line, it suggests a bearish market condition. Traders may consider looking for selling opportunities or holding onto existing short positions.

Optional Cloud Mode:

Enabling the cloud mode allows you to visualize bullish and bearish market conditions more clearly. The cloud appears between the AESI line and the EMA line, providing a visual representation of the prevailing market sentiment.

Bullish Cloud: When the AESI line is above the EMA line, the cloud is green, indicating a potential bullish market condition.

Bearish Cloud: When the AESI line is below the EMA line, the cloud is red, indicating a potential bearish market condition.

Note: The AESI indicator is most effective when used in conjunction with other technical analysis tools and indicators to confirm trading signals and make informed trading decisions.

Adjusting the Parameters:

You can adjust the Length and Alpha parameters to find the best ones for different timeframes and market conditions. Experimenting with different parameter values can help you find the optimal settings for your trading strategy.

It is recommended to backtest the AESI indicator on historical price data and evaluate its performance before using it in live trading. Remember that no indicator can guarantee profitable trades, and it is important to use risk management techniques and exercise caution when making trading decisions.

[blackcat] L1 Vitali Apirine Exponential Deviation BandsLevel 1

Background

Vitali Apirine’s articles in the July issues on 2019,“Exponential Deviation Bands”

Function

In “Exponential Deviation Bands” in this issue, author Vitali Apirine introduces a price band indicator based on exponential deviation rather than the more traditional standard deviation, such as is used in the well-known Bollinger Bands. As compared to standard deviation bands, the author’s exponential deviation bands apply more weight to recent data and generate fewer breakouts. Apirine describes using the bands as a tool to assist in identifying trends.

Remarks

Feedbacks are appreciated.

6 Moving Averages with MTF v1.0This indicator is a collection of 6 different period Moving Averages. It has support for different time-frame resolution for all of them individually.

Also, it has 11 different type of Moving Average calculation functions:

1. Simple Moving Average (SMA)

2. Exponential Moving Average (EMA)

3. Weighted Moving Average (WMA)

4. Volume Weighted Moving Average (VWMA)

5. Smoothed Moving Average (SMMA)

6. Double Exponential Moving Average (DEMA)

7. Triple Exponential Moving Average (TEMA)

8. Hull WMA Moving Average (HullMA)

9. Triangular Moving Average (TMA)

10. Super Smoother Moving Average (SSMA)

11. Zero Lag Exponential Moving Average (ZEMA)

Note: The Moving Average calculation function is adapted from @JustUncleL

Happy trading 😉

Thank you.

Hull-Exponential Moving Average (HEMA)The Hull Exponential Moving Average (HEMA) is an experimental technical indicator that uses a sequence of Exponential Moving Averages (EMAs) with the same logic as HMA - except with EMAs and not WMAs. It aims to create a responsive yet smooth trend indicator than HMA.

HEMA applies a multi-stage EMA process. Initial EMAs are calculated using alphas derived from logarithmic relationships and the input period. Their outputs are then combined in a de-lagging step, which itself uses a logarithmically derived ratio. A final EMA smoothing pass is then applied to this de-lagged series. This creates a moving average that responds quickly to genuine price changes while maintaining effective noise filtering. The specific alpha calculations and the de-lagging formula contribute to its balance between responsiveness and smoothness.

▶️ **Core Concepts**

Logarithmically-derived alphas: Alpha values for the three EMA stages are derived using natural logarithms and specific formulas related to the input period **N**.

Three-stage EMA process: The calculation involves:

An initial EMA (using **αS**) on the source data.

A second EMA (using **αF**) also on the source data.

A de-lagging step that combines the outputs of the first two EMAs using a specific ratio **r**.

A final EMA (using **αFin**) applied to the de-lagged series.

Specific de-lagging formula: Utilizes a constant ratio **r = ln(2.0) / (1.0 + ln(2.0))** to combine the outputs of the first two EMAs, aiming to reduce lag.

Optimized final smoothing: The alpha for the final EMA (**αFin**) is calculated based on the square root of the period **N**.

Warmup compensation: The internal EMA calculations include a warmup mechanism to provide more accurate values from the initial bars. This involves tracking decay factors (**eS**, **eF**, **eFin**) and applying a compensation factor **1.0 / (1.0 - e_decay)** during the warmup period. A shared warmup duration is determined by the smallest alpha among the three stages.

HEMA achieves its characteristics through this multi-stage EMA process, where the specific alpha calculations and the de-lagging step are key to its responsiveness and smoothness.

▶️ **Common Settings and Parameters**

Period (**N**): Default: 10 | Base lookback period for all alpha calculations | When to Adjust: Increase for longer-term trends and more smoothness, decrease for shorter-term signals and more responsiveness

Source: Default: Close | Data point used for calculation | When to Adjust: Change to HL2, HLC3, or OHLC4 for different price representations

Pro Tip: The HEMA's behavior is sensitive to the **Period** setting due to the non-linear relationships in its alpha calculations. Experiment with values around your typical MA periods. Small changes in **N** can have a noticeable impact, especially for smaller **N** values.

▶️ **Calculation and Mathematical Foundation**

Simplified explanation:

HEMA calculates its value through a sequence of three Exponential Moving Averages (EMAs) with specially derived smoothing factors (alphas).

Two initial EMAs are calculated from the source price, using alphas **αS** and **αF**.

The outputs of these two EMAs are combined into a "de-lagged" series.

This de-lagged series is then smoothed by a third EMA, using alpha **αFin**, to produce the final HEMA value.

All internal EMAs use a warmup compensation mechanism for improved accuracy on early bars.

Technical formula (let **N** be the input period):

1. Alpha for the first EMA (slow component related):

αS = 3.0 / (2.0 * N - 1.0)

2. Lambda for **αS** (intermediate value):

λS = -ln(1.0 - αS)

Note: **αS** must be less than 1, which implies 2N-1 > 3 or N > 2 for **λS** to be well-defined without NaN from ln of non-positive number. The code uses nz() for robustness but the formula implies this constraint.

3. De-lagging ratio **r**:

r = ln(2.0) / (1.0 + ln(2.0))

(This is a constant, approximately 0.409365)

4. Alpha for the second EMA (fast component related):

αF = 1.0 - exp(-λS / r)

5. Alpha for the final EMA smoothing:

αFin = 2.0 / (sqrt(N) / 2.0 + 1.0)

6. Applying the stages:

**OutputS = EMA_internal(source, αS, eS_state, emaS_state)**

**OutputF = EMA_internal(source, αF, eF_state, emaF_state)**

8. Calculate the de-lagged series:

DeLag = (OutputF / (1.0 - r)) - (r * OutputS / (1.0 - r))

9. Calculate the final HEMA:

HEMA = EMA_internal(DeLag, αFin, eFin_state, emaFin_state)

🔍 Technical Note: The HEMA implementation uses a shared warmup period controlled by **aMin** (the minimum of **αS**, **αF**, **αFin**). During this period, each internal EMA stage still tracks its own decay factor (**eS**, **eF**, **eFin**) to apply the correct compensation. The **nz()** function is used in the code to handle potential NaN values from alpha calculations if **N** is very small (e.g., **N=1** would make **αS=3**, **1-αS = -2**, **ln(-2)** is NaN).

▶️ **Interpretation Details**

HEMA provides several key insights for traders:

When price crosses above HEMA, it often signals the beginning of an uptrend

When price crosses below HEMA, it often signals the beginning of a downtrend

The slope of HEMA provides insight into trend strength and momentum

HEMA creates smooth dynamic support and resistance levels during trends

Multiple HEMA lines with different periods can identify potential reversal zones

HEMA is particularly effective for trend following strategies where both responsiveness and noise reduction are important. It provides earlier signals than traditional EMAs while exhibiting less whipsaw than standard HMA in choppy market conditions. The indicator excels at identifying the underlying trend direction while filtering out minor price fluctuations.

▶️ **Limitations and Considerations**

Experimental nature: As an experimental indicator, HEMA may behave differently from established HMA in certain market conditions

Lag characteristics: While designed to reduce lag, HEMA may exhibit slightly more lag than HMA in some scenarios due to the long tail of EMA

Mathematical complexity: The multi-stage calculation with specialized alpha parameters makes the behavior less intuitive to understand

Parameter sensitivity: Performance can vary significantly with different period settings

Complementary tools: Works best when combined with volume analysis or momentum indicators for confirmation

▶️ **References**

Hull, A. (2005). "Hull Moving Average," Technical Analysis of Stocks & Commodities .

RetryClaude can make mistakes. Please double-check responses.

Multiple Exponential Moving AveragesThe "Multiple Exponential Moving Averages" indicator is a custom technical analysis tool created for TradingView. It combines five different Exponential Moving Averages (EMAs) into a single indicator. Each EMA has a user-defined length, and they are plotted on the chart with different colors to differentiate them.

Exponential Moving Averages are commonly used in technical analysis to smooth out price data and identify trends. They give more weight to recent price data, making them more responsive to recent price changes than Simple Moving Averages (SMAs). By combining multiple EMAs with different lengths, TradingView users will no longer have to worry that they will run out of slots when wanting to add new indicators to their chart.

Triple Exponential Hull Moving Average THMAThis pine script calculates the triple exponential Hull moving average (THMA) of a given data series. The THMA is a type of moving average that is calculated using the exponential moving average (EMA) of the data. In this script, the ema() function is used to calculate the EMA of the data three times, with different lengths for each calculation. The resulting value is the THMA of the data. The script also plots the THMA on a chart, using a green color for upward trends and a red color for downward trends. The length of the moving average and the alpha parameter used in the EMA calculation can be specified by the user as input parameters.

A trader may use this pine script to help identify trends in the stock market. By plotting the triple exponential Hull moving average (THMA) of the data on a chart, the trader can quickly see whether the market is trending up or down, and how strong the trend is. This can help the trader make informed decisions about when to buy and sell stocks. Additionally, the script allows the user to customize the length of the moving average and the alpha parameter used in the EMA calculation, which can be useful for analyzing different time frames and making more accurate predictions.

Cumulative Weighted Triple Exponential Moving Average (CWTEMA)This Pine Script code defines an indicator called "CWTEMA" that plots a custom weighted triple exponential moving average (TEMA) on a chart. The indicator takes two inputs: a source series (usually the close price of a security) and a length parameter that specifies the number of periods over which the moving average is calculated.

The code first defines a tema() function, which calculates the TEMA for a given series of data and a given length. The function uses the ta.ema() function from the ta library to compute the exponential moving average of the source data, and then applies the triple exponential moving average formula to calculate the TEMA.

The wma() function is then defined, which calculates the weighted moving average of a given series of data using a set of weights. This function computes the weighted sum of the source data using the given weights, then divides this sum by the sum of the weights to calculate the weighted moving average.

Finally, the cweema() function is defined, which calculates the custom weighted TEMA. This function first computes the weights for each value in the moving average using the given length parameter, then calls the wma() and tema() functions to calculate the weighted moving average using the TEMA values. The cweema() function is then plotted on the chart.

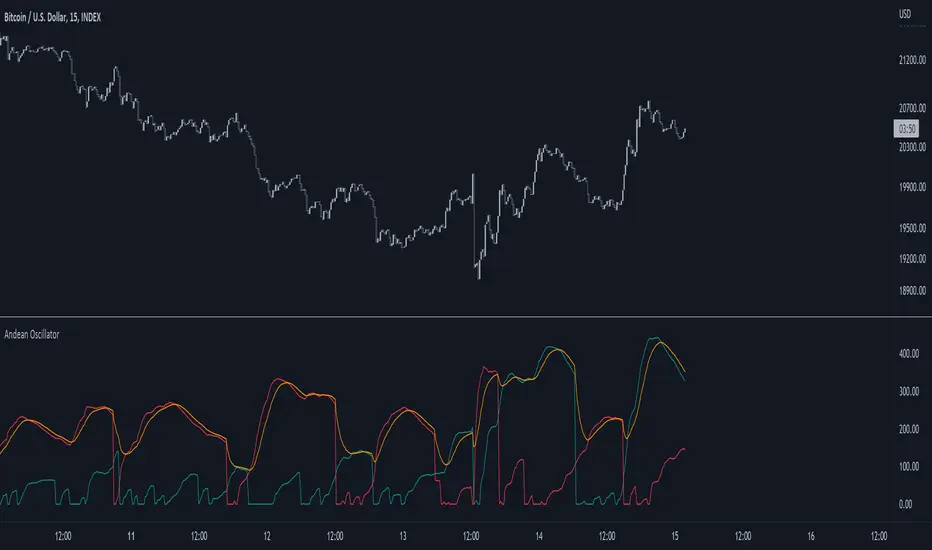

Andean OscillatorThe following script is an original creation originally posted on the blog section of the broker Alpaca.

The proposed indicator aims to measure the degree of variations of individual up-trends and down-trends in the price, thus allowing to highlight the direction and amplitude of a current trend.

Settings

Length : Determines the significance of the trends degree of variations measured by the indicator.

Signal Length : Moving average period of the signal line.

Usage

The Andean Oscillator can return multiple information to the user, with its core interpretation revolving around the bull and bear components.

A rising bull component (in green) indicates the presence of bullish price variations while a rising bear component (in red) indicates the presence of bearish price variations.

When the bull component is over the bear component market is up-trending, and the user can expect new higher highs. When the bear component is over the bull component market is down-trending, and the user can expect new lower lows.

The signal line (in orange) allows a more developed interpretation of the indicator and can be used in several ways.

It is possible to use it to filter out potential false signals given by the crosses between the bullish and bearish components. As such the user might want to enter a position once the bullish or bearish component crosses over the signal line instead.

Details

Measuring the degree of variations of trends in the price by their direction (up-trend/down-trend) can be done in several way.

The approach taken by the proposed indicator makes use of exponential envelopes and the naive computation of standard deviation.

First, exponential envelopes are obtained from both the regular prices and squared prices, thus giving two upper extremities, and two lower extremities.

The bullish component is obtained by first subtracting the upper extremity of the squared prices with the squared upper extremity of regular prices, the square root is then applied to this result.

The bearish component is obtained in the same way, but makes use of the lower extremities of the exponential envelopes.

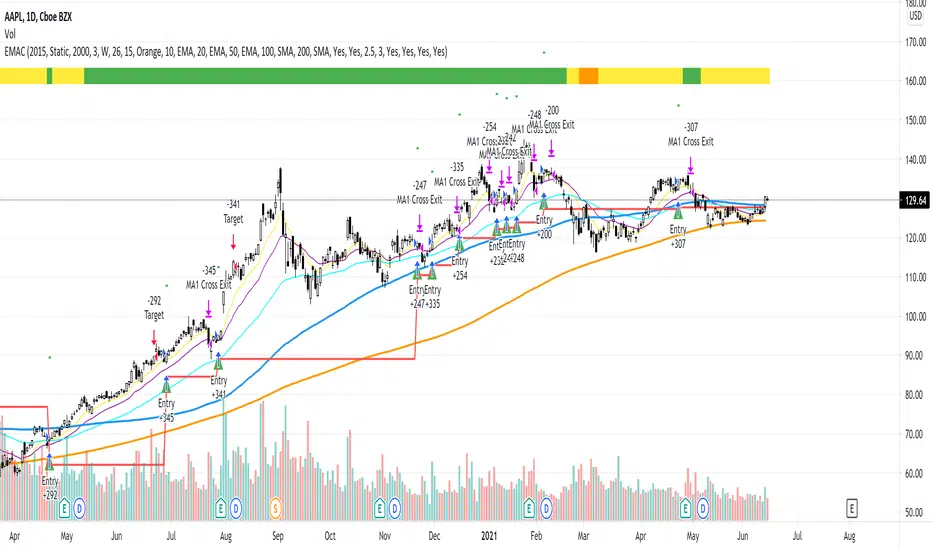

EMAC - Exponential Moving Average Cross - StudyEMAC - Exponential Moving Average Cross - Study

This is the short Study version of EMAC that has been optimized for TradersPost alerts only

For the original full Strategy version with many editable inputs please see EMAC - Exponential Moving Average Cross

For the full Strategy version with the best currently known optimized inputs (average best settings across 26 tickers) please see EMAC - Exponential Moving Average Cross - Optimized

EMAC - Exponential Moving Average Cross - OptimizedEMAC - Exponential Moving Average Cross - Optimized

This is the full Strategy version with the best currently known optimized inputs with the average best settings across the following 26 tickers:

QQQ

TQQQ

SPY

SPXL

AAPL

AMZN

TSLA

BYND

CRWD

DDOG

ESTC

FSLY

MDB

NVDA

PINS

PTON

ROKU

SHOP

SQ

TDOC

TWLO

APPS

CHWY

DKNG

ETSY

FVRR

For the short Study version of EMAC that has been optimized for TradersPost alerts only please see EMAC - Exponential Moving Average Cross - Study

For the original full Strategy version with many editable inputs please see EMAC - Exponential Moving Average Cross

EMAC - Exponential Moving Average CrossEMAC - Exponential Moving Average Cross

This strategy is based in part on original 10ema Basic Swing Trade Strategy by Matt Delong: www.tradingview.com

Link to original 10ema Basic Swing Trade Strategy:

This is the Original EMAC - Exponential Moving Average Cross strategy built as a class for reallifetrading dot com and so has all the default settings and has not been optimized. I would not recommend using this strategy with the default settings and is for educational purposes only. For the fully optimized version please come back around the same time tomorrow 6/16/21 for the EMAC - Exponential Moving Average Cross - Optimized

If you have any questions feel free to reach out to me with a comment and I will try to get back to you quickly with a reply.

Zero Lag Exponential Moving Average (ZLEMA) The Zero lag exponential moving average (ZLEMA) indicator was created

by John Ehlers and Ric Way.

As is the case with the Double exponential moving average (DEMA) and

the Triple exponential moving average (TEMA) and as indicated by the

name, the aim is to eliminate the inherent lag associated to all trend

following indicators which average a price over time.

Kalman Exponential SuperTrendThe Kalman Exponential SuperTrend is a new, smoother & superior version of the famous "SuperTrend". Using Kalman smoothing, a concept from the EMA (Exponential Moving Average), this script leverages the best out of each and combines it into a single indicator.

How does it work?

First, we need to calculate the Kalman smoothed source. This is a kind of complex calculation, so you need to study it if you want to know how it works precisely. It smooths the source of the SuperTrend, which helps us smooth the SuperTrend.

Then, we calculate "a" where:

n = user defined ATR length

a = 2/(n+1)

Now we calculate the ATR over "n" period. Classical calculation, nothing changed here.

Now we calculate the SuperTrend using the Kalman smoothed source & ATR where:

kalman = kalman smoothed source

ATR = Average True Range

m = Factor chosen by user.

Upper Band = kalman + ATR * m

Lower Band = kalman - ATR * m

Now we just smooth it a bit further using the "a" and a concept from the EMA.

u1 = Upper Band a bar ago

l1 = Lower Band a bar ago

u = Upper Band

l = Lower Band

Upper = u1 * (1-a) + u * a

Lower = l1 * (1-a) + u * a

When the classical (not Kalman) source crosses above the Upper, it indicates an uptrend. When it crosses below the Lower, it indicates a downtrend.

Methodology & Concepts

When I took a look at the classical SuperTrend => It was just far too slow, and if I made it faster it was noisy as hell. So I decided I would try to make up for it.

I tried the gaussian, bilateral filter, but then I tried kalman and that worked the best, so I added it. Now it was still too noisy and unconsistent, so I revisited my knowledge of concepts and picked the one from the EMA, and it kinda solved it.

In the core of the indicator, all it does is combine them in a really simple way, but if you go more deeply you see how it fits the puzzlé really well.

It is not about trying out random things´=> but about seeking what it is missing and trying to lessen its bad side.

That is the entire point of this indicator => Offer a unique approach to the SuperTrend type, that lessen the bad sides of it.

I also added different plotting types, this is so everyone can find their favorite

Enjoy Gs!

Thanks @BackQuant for making a open source Kalman code <3

Volume Exponential Moving Averages (EMA)

Description:

This script is a simple script that plots a desired exponential moving average of buy and sell volume as a line chart with a tunable smoothing factor. There is a highlight on the plot area of either green or red to denote if the EMA of buy volume or sell volume is of a higher value. This indicator uses basic math of exponential averages and calculates volume using the formulas: "buy volume" = the product of total volume and the "closing price" minus the "low price" divided by "high price" minus the "low price" for a specific candle. Conversely, "sell volume" = the product of "total volume" and the "high price" minus the "close price" divided by "high price" minus the "low price" for a specific candle.

Utility:

This indicator is an effective way to gauge the acceleration/ deceleration of buyers and sellers in the market and can be used in combination with market structure and important levels to understand if buyers or sellers are taking over at any given time.

How to use this indicator:

There are two settings for this indicator:

1. The Length of the EMA: The length of the EMA can be adjusted based on your preference for a running number of candles' data. If you are interested to know short term changes in volume (e.g. over the past few candles at a major level) you can adjust this setting lower (~3-9 length). Conversely, if you are interested in volume trends over a greater number of candles you can increase this to your liking.

Personal preference : Because I am a short term daytrader/ scalper, I keep this setting at 6 length to see immediate changes in the acceleration or deceleration of buyers/ sellers.

2. The Smoothing Factor: The smoothing factor can be adjusted to further tune the size of trend you are interested in with 1 = No smoothing of the EMA line. Smoothing of the EMA line increases as the value for smoothing increases, resulting in a less volatile, more smooth EMA line. However, the more smooth the line, the less sensitive the EMA will be to immediate changes in volume pace. The less smoothing factor is applied, the more volatile data will be, resulting in quicker observation of shorter term trends. Again the same rules apply as the EMA length as these are similar in function: If you are interested to know short term changes in volume (e.g. over the past few candles at a major level) you can adjust this setting lower (~2-6). Conversely, if you are interested in volume trends over a greater number of candles you can increase this to your liking.

Personal preference : Because I am a short term daytrader/ scalper, I keep this setting at 2-4 smoothing factor to see immediate changes in the acceleration or deceleration of buyers/ sellers.

You should, of course, play with these settings to your exact preferences based on your trading style.

Tips for using this indicator:

General Use:

When the buy volume EMA is moving up, buyers are increasing the pace of buying and when the buy volume EMA is moving down, buyers are decreasing the pace of buying. Conversely, when the sell volume EMA is moving up, sellers are increasing the pace of selling and when the sell volume EMA is moving down, sellers are decreasing the pace of selling. The overall movement of the stock is relative to the combination of these rates. e.g. If both buyers and sellers are increasing at the same rate (EMAs slopes are roughly equal) there will be not a large change in price. If the slope of the buy volume EMA is greater than the slope of sell volume EMA, the price should move up. Conversely, if the slope of the sell volume EMA is greater than the slope of buy volume EMA, the price should move down.

Predicting pullbacks, reversals, and continuations:

This indicator allows you to see if buyers or sellers are increasing their pace, even if the stock price is in consolidation. This allows you to predict if out of the consolidation buyers or sellers are likely to win based on the momentum of the volume in consolidation. e.g. If price is in consolidation after an uptrend and the buy volume EMA starts to decrease, this could be a sign that buyers are running out of steam at this price level. Another example, If at a major support the buy volume EMA begins to trend up then buyers are accelerating the pace of buying at this level.

EMA crosses: There is something to be said about the point at which the buy volume EMA and sell volume EMA cross. This signifies that at this moment there is a shift in which the acceleration of one party outpaces that of the other and can result in increased speed of the movement of the stock price.

Considerations

Because volume changes constantly, this indicator is best to identify short term changes in volume that could impact price movements. It is not guaranteed to continue just because buyers or sellers have had a change in pace. Therefore it is advised to use this indicator in combination with significant price levels such as pivot points, or price levels from volume profile tools to identify the price zones where significant volume changes are likely to impact price movements. It is also advised to continue to monitor the changes in pace in buyers and sellers using this volume EMA indicator to determine if a change in pace is short lived or if it will continue for a longer duration.

Examples of use:

Bullish Reversal:

Bearish Continuation:

Bearish EMA Crossover: (Settings: Length 6, Smoothing factor 3)

Bullish EMA Crossover: (Settings: Length 6, Smoothing factor 4)