Index Position Size Calculator for [US30 / US100 / SP500]What it does

This tool helps you size positions consistently for index trades on US30 (Dow Jones), NAS100 (Nasdaq-100), and SP500 (S&P 500). Enter your account balance, risk %, and your planned Entry / Stop-Loss / Target and the script calculates:

• Position Size (rounded to your lot/contract step)

• Risk-to-Reward (R/R)

• Potential P/L in USD based on your inputs

• Visual Entry / SL / TP lines with green/red zones and concise labels

Supported contract styles

Choose a preset for common products (e.g., CFD $1/pt, YM/NQ/ES futures, MYM/MNQ/MES micros) or override the economics yourself. You remain in control of the two key levers:

• $/point — how many dollars you gain/lose per 1 index point per contract/lot

• Point size — how many price units equal 1 index point on your chart (often 1.0, but some brokers use 0.1 or 0.5)

Inputs

• Account Balance ($) and Risk % per trade

• Index: US30 / NAS100 / SP500

• Contract: CFD / Futures (YM, NQ, ES) / Micros (MYM, MNQ, MES)

• $/point: auto from Contract or manual override

• Point size: auto from Index or manual override

• Position size step: rounding (e.g., 1 for futures, 0.01 for CFDs)

• Entry / SL / TP: typed values (snapped to tick), with on-chart zones and labels

• Display toggles for lines and labels

How the math works

• StopPoints = |Entry − SL| ÷ PointSize

• ProfitPoints = |TP − Entry| ÷ PointSize

• Position Size = (AccountBalance × Risk%) ÷ (StopPoints × $/point)

• R/R = ProfitPoints ÷ StopPoints

• Potential P/L = PositionSize × Points × $/point

How to use (quick start)

1. Select Index and Contract.

2. Confirm $/point and Point size match your broker’s specs.

3. Enter Entry / SL / TP for the trade idea.

4. Read the Position Size, R/R, and Potential P/L in the info box.

5. Adjust for fees, spreads, and slippage as needed.

Notes & limitations

• Broker symbols can vary. Always verify $/point and Point size for your instrument before risking capital.

• The script does not place orders and does not generate trade signals; it’s a sizing/visualization tool.

• Results can differ across brokers due to pricing, spreads, minimum lot sizes, and execution rules.

• Use on the intended indices; you’ll see a reminder if you load it elsewhere.

Changelog highlights

• Pine v6, constant-safe inputs, tick-snapping, global fills (no local-scope errors).

• Robust label handling and optional minimal chart markers.

Disclaimer

This script is provided for educational purposes only and does not constitute financial advice or a recommendation to buy or sell any security or derivative. Trading involves risk, including the possible loss of principal. Always do your own research, verify contract specifications with your broker, and consider testing in a demo environment before trading live.

在腳本中搜尋"Futures"

Renko Open Range delta

Delta Renko-Style Indicator Guide (NQ Focus)

This indicator takes inspiration from the Renko Chart concept and is optimized for the RTH session (New York time zone), specifically applied to the Nasdaq futures (NQ) product.

If you’re unfamiliar with Renko charts, it may help to review their basics first, as this indicator borrows their clean, block-based perspective to simplify price interpretation.

⸻

🔧 How the Indicator Works

• At market open (9:30 AM EST), the indicator plots a horizontal open price line, referred to as 0 delta.

• From this anchor, it plots 10 incremental levels (deltas) both above and below the open, each spaced by 62.5 NQ points.

Why 62.5?

• With NQ currently trading in the 23,000–24,000 range, a 62.5-point move represents roughly 0.26% of the daily average range.

• This makes each delta step significant enough to capture movement while filtering out smaller noise.

A mini table (location adjustable) displays:

• Current delta zone

• Last touched delta level

This gives you a quick snapshot of where price sits relative to the open.

⸻

📈 How to Read the Market

• At the open, price typically oscillates between 0 and +1 / -1 delta.

• A break beyond this zone often signals stronger directional intent:

• Trending day: price can push into +2, +3, +4, +5 (or the inverse for downside).

• Range day: expect price to bounce between +1, 0, -1 deltas.

⚠️ Note: This is a visualization tool, not a trading system. Its purpose is to help you quickly recognize range vs. trend conditions.

⸻

📊 Example

• In this case, NQ reached +1 delta shortly after open.

• A retest of 0 delta followed, and price later surged to +5/+6 deltas (helped by Fed news).

⸻

🛠️ Practical Uses

This indicator can help you:

• Define profit targets

• Place hard stop levels

• Gauge whether a counter-trend trade is worth the risk

⚠️ Caution: Avoid counter-trend trades if price is aggressively pushing toward +5/+6 or -5/-6 deltas, as trend exhaustion usually hasn’t set in yet.

⸻

🔄 Adapting for ES (S&P Futures)

• On NQ, 62.5 points ≈ $1,250 per contract.

• For ES, this translates to 25 points.

• Since 1 NQ contract ≈ 2 ES contracts in dollar terms, an optimized ES delta step would be 12.5 points.

You may also experiment with different delta values (e.g., 50 or 31.25 for NQ) to align with your risk profile and trading style.

⸻

🧪 Extending Beyond NQ

You can experiment with applying this indicator to ES or even stocks, but non-futures assets may require additional calibration and testing.

⸻

✅ Bottom line: This tool provides a clean, Renko-inspired framework for quickly gauging trend vs. range conditions, setting realistic profit targets, and avoiding poor counter-trend setups.

VWAP-RSI Scalper FINAL v1Description

This script implements a robust, battle-tested intraday scalping strategy designed for prop firm challenges, funded trader programs, and serious futures scalpers.

It combines VWAP, RSI, EMA trend, and ATR-based risk management to capture high-probability mean reversion and momentum moves during the most liquid hours of the trading day.

Core Logic

RSI (Relative Strength Index):

Trades are triggered when the RSI is either oversold or overbought using a short lookback (default: 3). This ensures only the strongest intraday reversals or exhaustion moves are considered.

VWAP Filter:

Longs are only taken above VWAP, shorts only below VWAP, aligning trades with the session’s dominant bias.

EMA Filter:

Additional trend quality filter—longs require price above EMA, shorts below EMA.

Session Control:

Only trades between user-defined session hours (default: US cash session), eliminating overnight/illiquid action.

ATR-based Dynamic Stops & Targets:

Every trade uses a stop loss at 1x ATR and a take profit at 2x ATR for a positive risk/reward ratio.

Max Trades Per Day:

Prevents overtrading and controls risk exposure (default: 3).

Performance (Sample Backtest)

Profit Factor: 1.37+ (prop-firm quality)

Drawdown: <1% (very conservative risk)

Win Rate: 37–48% (RR > 1, so high edge)

Consistency: Smooth, steady equity curve over hundreds of trades.

Best For:

ES/NQ/CL/GC intraday traders

Prop firm evaluation challenges (Tradeify, Topstep, Apex, etc.)

Anyone needing robust, no-nonsense systematic edge for futures or indices.

How to Use & Tune

Apply to 3min, 5min, or 15min charts of liquid futures or indices.

Change parameters in the settings panel to suit your asset, volatility, or session hours.

Use “Strategy Tester” to validate P&L, win rate, and drawdown.

How to Optimize

Raise/lower RSI length or bands to make signals more/less frequent.

Adjust stop/target multiples for your preferred risk/reward profile.

Change session hours to match your broker or market.

Disclaimer

This is not financial advice. Use on a demo or sim account first. Results will vary by market, slippage, and execution speed. Past performance does not guarantee future results.

If you find this useful, please give it a like, follow for more strategies, and comment your results or questions!

Good luck and safe trading!

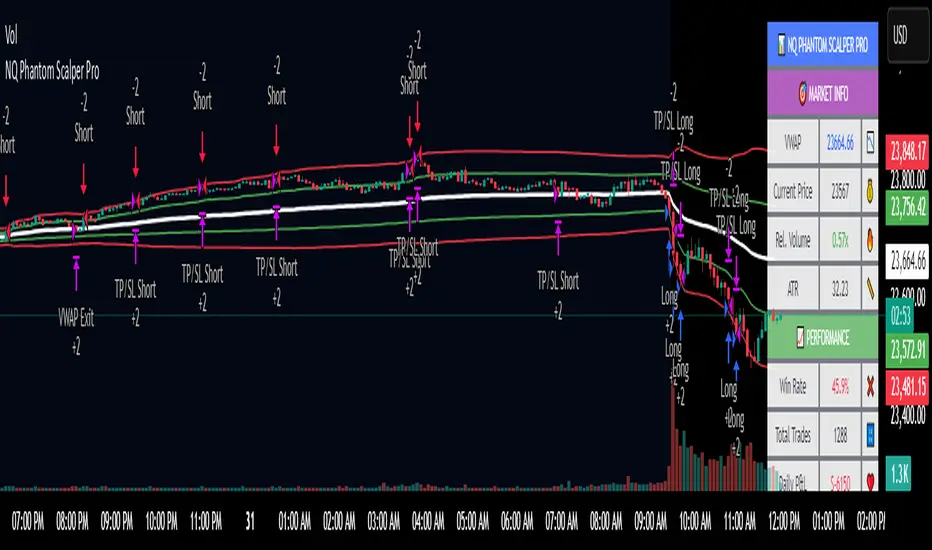

NQ Phantom Scalper Pro# 👻 NQ Phantom Scalper Pro

**Advanced VWAP Mean Reversion Strategy with Volume Confirmation**

## 🎯 Strategy Overview

The NQ Phantom Scalper Pro is a sophisticated mean reversion strategy designed specifically for Nasdaq 100 (NQ) futures scalping. This strategy combines Volume Weighted Average Price (VWAP) bands with intelligent volume spike detection to identify high-probability reversal opportunities during optimal market hours.

## 🔧 Key Features

### VWAP Band System

- **Dynamic VWAP Bands**: Automatically adjusting standard deviation bands based on intraday volatility

- **Multiple Band Levels**: Configurable Band #1 (entry trigger) and Band #2 (profit target reference)

- **Flexible Anchoring**: Choose from Session, Week, Month, Quarter, or Year-based VWAP calculations

### Volume Intelligence

- **Volume Spike Detection**: Only triggers entries when volume exceeds SMA by configurable multiplier

- **Relative Volume Display**: Real-time volume strength indicator in info panel

- **Optional Volume Filter**: Can be disabled for testing alternative setups

### Advanced Time Management

- **12-Hour Format**: User-friendly time inputs (9 AM - 4 PM default)

- **Lunch Filter**: Automatically avoids low-liquidity lunch period (12-2 PM)

- **Visual Time Zones**: Color-coded background for active/inactive periods

- **Market Hours Focus**: Optimized for peak NQ trading sessions

### Smart Risk Management

- **ATR-Based Stops**: Volatility-adjusted stop losses using Average True Range

- **Dual Exit Strategy**: VWAP mean reversion + fixed profit targets

- **Adjustable Risk-Reward**: Configurable target ratio to opposite VWAP band

- **Position Sizing**: Percentage-based equity allocation

### Optional Trend Filter

- **EMA Trend Alignment**: Optional trend filter to avoid counter-trend trades

- **Configurable Period**: Adjustable EMA length for trend determination

- **Toggle Functionality**: Enable/disable based on market conditions

## 📊 How It Works

### Entry Logic

**Long Entries**: Triggered when price touches lower VWAP band + volume spike during active hours

**Short Entries**: Triggered when price touches upper VWAP band + volume spike during active hours

### Exit Strategy

1. **VWAP Mean Reversion**: Early exit when price returns to VWAP center line

2. **Profit Target**: Fixed target based on percentage to opposite VWAP band

3. **Stop Loss**: ATR-based protective stop

### Visual Elements

- **VWAP Center Line**: Blue line showing volume-weighted fair value

- **Green Bands**: Entry trigger levels (Band #1)

- **Red Bands**: Extended levels for target reference (Band #2)

- **Orange EMA**: Trend filter line (when enabled)

- **Background Colors**: Yellow (lunch), Gray (after hours), Clear (active trading)

- **Info Panel**: Real-time metrics display

## ⚙️ Recommended Settings

### Timeframes

- **Primary**: 1-5 minute charts for scalping

- **Validation**: Test on 15-minute for swing applications

### Market Conditions

- **Best Performance**: Ranging/choppy markets with good volume

- **Trend Markets**: Enable trend filter to avoid counter-trend trades

- **High Volatility**: Increase ATR multiplier for stops

### Session Optimization

- **Pre-Market**: Generally avoided (low volume)

- **Morning Session**: 9:30 AM - 12:00 PM (high activity)

- **Lunch Period**: 12:00 PM - 2:00 PM (filtered by default)

- **Afternoon Session**: 2:00 PM - 4:00 PM (good volume)

- **After Hours**: Generally avoided (wide spreads)

## ⚠️ Risk Disclaimer

This strategy is for educational purposes only and does not constitute financial advice. Past performance does not guarantee future results. Trading futures involves substantial risk of loss and is not suitable for all investors. Users should:

- Thoroughly backtest on historical data

- Start with small position sizes

- Understand the risks of leveraged trading

- Consider transaction costs and slippage

- Never risk more than you can afford to lose

## 📈 Performance Tips

1. **Volume Threshold**: Adjust volume multiplier based on average NQ volume patterns

2. **Band Sensitivity**: Modify band multipliers for different volatility regimes

3. **Time Filters**: Customize trading hours based on your timezone and preferences

4. **Trend Alignment**: Use trend filter during strong directional markets

5. **Risk Management**: Always maintain consistent position sizing and risk parameters

**Version**: 6.0 Compatible

**Asset**: Optimized for NASDAQ 100 Futures (NQ)

**Style**: Mean Reversion Scalping

**Frequency**: High-Frequency Trading Ready

VoVix DEVMA🌌 VoVix DEVMA: A Deep Dive into Second-Order Volatility Dynamics

Welcome to VoVix+, a sophisticated trading framework that transcends traditional price analysis. This is not merely another indicator; it is a complete system designed to dissect and interpret the very fabric of market volatility. VoVix+ operates on the principle that the most powerful signals are not found in price alone, but in the behavior of volatility itself. It analyzes the rate of change, the momentum, and the structure of market volatility to identify periods of expansion and contraction, providing a unique edge in anticipating major market moves.

This document will serve as your comprehensive guide, breaking down every mathematical component, every user input, and every visual element to empower you with a profound understanding of how to harness its capabilities.

🔬 THEORETICAL FOUNDATION: THE MATHEMATICS OF MARKET DYNAMICS

VoVix+ is built upon a multi-layered mathematical engine designed to measure what we call "second-order volatility." While standard indicators analyze price, and first-order volatility indicators (like ATR) analyze the range of price, VoVix+ analyzes the dynamics of the volatility itself. This provides insight into the market's underlying state of stability or chaos.

1. The VoVix Score: Measuring Volatility Thrust

The core of the system begins with the VoVix Score. This is a normalized measure of volatility acceleration or deceleration.

Mathematical Formula:

VoVix Score = (ATR(fast) - ATR(slow)) / (StDev(ATR(fast)) + ε)

Where:

ATR(fast) is the Average True Range over a short period, representing current, immediate volatility.

ATR(slow) is the Average True Range over a longer period, representing the baseline or established volatility.

StDev(ATR(fast)) is the Standard Deviation of the fast ATR, which measures the "noisiness" or consistency of recent volatility.

ε (epsilon) is a very small number to prevent division by zero.

Market Implementation:

Positive Score (Expansion): When the fast ATR is significantly higher than the slow ATR, it indicates a rapid increase in volatility. The market is "stretching" or expanding.

Negative Score (Contraction): When the fast ATR falls below the slow ATR, it indicates a decrease in volatility. The market is "coiling" or contracting.

Normalization: By dividing by the standard deviation, we normalize the score. This turns it into a standardized measure, allowing us to compare volatility thrust across different market conditions and timeframes. A score of 2.0 in a quiet market means the same, relatively, as a score of 2.0 in a volatile market.

2. Deviation Analysis (DEV): Gauging Volatility's Own Volatility

The script then takes the analysis a step further. It calculates the standard deviation of the VoVix Score itself.

Mathematical Formula:

DEV = StDev(VoVix Score, lookback_period)

Market Implementation:

This DEV value represents the magnitude of chaos or stability in the market's volatility dynamics. A high DEV value means the volatility thrust is erratic and unpredictable. A low DEV value suggests the change in volatility is smooth and directional.

3. The DEVMA Crossover: Identifying Regime Shifts

This is the primary signal generator. We take two moving averages of the DEV value.

Mathematical Formula:

fastDEVMA = SMA(DEV, fast_period)

slowDEVMA = SMA(DEV, slow_period)

The Core Signal:

The strategy triggers on the crossover and crossunder of these two DEVMA lines. This is a profound concept: we are not looking at a moving average of price or even of volatility, but a moving average of the standard deviation of the normalized rate of change of volatility.

Bullish Crossover (fastDEVMA > slowDEVMA): This signals that the short-term measure of volatility's chaos is increasing relative to the long-term measure. This often precedes a significant market expansion and is interpreted as a bullish volatility regime.

Bearish Crossunder (fastDEVMA < slowDEVMA): This signals that the short-term measure of volatility's chaos is decreasing. The market is settling down or contracting, often leading to trending moves or range consolidation.

⚙️ INPUTS MENU: CONFIGURING YOUR ANALYSIS ENGINE

Every input has been meticulously designed to give you full control over the strategy's behavior. Understanding these settings is key to adapting VoVix+ to your specific instrument, timeframe, and trading style.

🌀 VoVix DEVMA Configuration

🧬 Deviation Lookback: This sets the lookback period for calculating the DEV value. It defines the window for measuring the stability of the VoVix Score. A shorter value makes the system highly reactive to recent changes in volatility's character, ideal for scalping. A longer value provides a smoother, more stable reading, better for identifying major, long-term regime shifts.

⚡ Fast VoVix Length: This is the lookback period for the fastDEVMA. It represents the short-term trend of volatility's chaos. A smaller number will result in a faster, more sensitive signal line that reacts quickly to market shifts.

🐌 Slow VoVix Length: This is the lookback period for the slowDEVMA. It represents the long-term, baseline trend of volatility's chaos. A larger number creates a more stable, slower-moving anchor against which the fast line is compared.

How to Optimize: The relationship between the Fast and Slow lengths is crucial. A wider gap (e.g., 20 and 60) will result in fewer, but potentially more significant, signals. A narrower gap (e.g., 25 and 40) will generate more frequent signals, suitable for more active trading styles.

🧠 Adaptive Intelligence

🧠 Enable Adaptive Features: When enabled, this activates the strategy's performance tracking module. The script will analyze the outcome of its last 50 trades to calculate a dynamic win rate.

⏰ Adaptive Time-Based Exit: If Enable Adaptive Features is on, this allows the strategy to adjust its Maximum Bars in Trade setting based on performance. It learns from the average duration of winning trades. If winning trades tend to be short, it may shorten the time exit to lock in profits. If winners tend to run, it will extend the time exit, allowing trades more room to develop. This helps prevent the strategy from cutting winning trades short or holding losing trades for too long.

⚡ Intelligent Execution

📊 Trade Quantity: A straightforward input that defines the number of contracts or shares for each trade. This is a fixed value for consistent position sizing.

🛡️ Smart Stop Loss: Enables the dynamic stop-loss mechanism.

🎯 Stop Loss ATR Multiplier: Determines the distance of the stop loss from the entry price, calculated as a multiple of the current 14-period ATR. A higher multiplier gives the trade more room to breathe but increases risk per trade. A lower multiplier creates a tighter stop, reducing risk but increasing the chance of being stopped out by normal market noise.

💰 Take Profit ATR Multiplier: Sets the take profit target, also as a multiple of the ATR. A common practice is to set this higher than the Stop Loss multiplier (e.g., a 2:1 or 3:1 reward-to-risk ratio).

🏃 Use Trailing Stop: This is a powerful feature for trend-following. When enabled, instead of a fixed stop loss, the stop will trail behind the price as the trade moves into profit, helping to lock in gains while letting winners run.

🎯 Trail Points & 📏 Trail Offset ATR Multipliers: These control the trailing stop's behavior. Trail Points defines how much profit is needed before the trail activates. Trail Offset defines how far the stop will trail behind the current price. Both are based on ATR, making them fully adaptive to market volatility.

⏰ Maximum Bars in Trade: This is a time-based stop. It forces an exit if a trade has been open for a specified number of bars, preventing positions from being held indefinitely in stagnant markets.

⏰ Session Management

These inputs allow you to confine the strategy's trading activity to specific market hours, which is crucial for day trading instruments that have defined high-volume sessions (e.g., stock market open).

🎨 Visual Effects & Dashboard

These toggles give you complete control over the on-chart visuals and the dashboard. You can disable any element to declutter your chart or focus only on the information that matters most to you.

📊 THE DASHBOARD: YOUR AT-A-GLANCE COMMAND CENTER

The dashboard centralizes all critical information into one compact, easy-to-read panel. It provides a real-time summary of the market state and strategy performance.

🎯 VOVIX ANALYSIS

Fast & Slow: Displays the current numerical values of the fastDEVMA and slowDEVMA. The color indicates their direction: green for rising, red for falling. This lets you see the underlying momentum of each line.

Regime: This is your most important environmental cue. It tells you the market's current state based on the DEVMA relationship. 🚀 EXPANSION (Green) signifies a bullish volatility regime where explosive moves are more likely. ⚛️ CONTRACTION (Purple) signifies a bearish volatility regime, where the market may be consolidating or entering a smoother trend.

Quality: Measures the strength of the last signal based on the magnitude of the DEVMA difference. An ELITE or STRONG signal indicates a high-conviction setup where the crossover had significant force.

PERFORMANCE

Win Rate & Trades: Displays the historical win rate of the strategy from the backtest, along with the total number of closed trades. This provides immediate feedback on the strategy's historical effectiveness on the current chart.

EXECUTION

Trade Qty: Shows your configured position size per trade.

Session: Indicates whether trading is currently OPEN (allowed) or CLOSED based on your session management settings.

POSITION

Position & PnL: Displays your current position (LONG, SHORT, or FLAT) and the real-time Profit or Loss of the open trade.

🧠 ADAPTIVE STATUS

Stop/Profit Mult: In this simplified version, these are placeholders. The primary adaptive feature currently modifies the time-based exit, which is reflected in how long trades are held on the chart.

🎨 THE VISUAL UNIVERSE: DECIPHERING MARKET GEOMETRY

The visuals are not mere decorations; they are geometric representations of the underlying mathematical concepts, designed to give you an intuitive feel for the market's state.

The Core Lines:

FastDEVMA (Green/Maroon Line): The primary signal line. Green when rising, indicating an increase in short-term volatility chaos. Maroon when falling.

SlowDEVMA (Aqua/Orange Line): The baseline. Aqua when rising, indicating a long-term increase in volatility chaos. Orange when falling.

🌊 Morphism Flow (Flowing Lines with Circles):

What it represents: This visualizes the momentum and strength of the fastDEVMA. The width and intensity of the "beam" are proportional to the signal strength.

Interpretation: A thick, steep, and vibrant flow indicates powerful, committed momentum in the current volatility regime. The floating '●' particles represent kinetic energy; more particles suggest stronger underlying force.

📐 Homotopy Paths (Layered Transparent Boxes):

What it represents: These layered boxes are centered between the two DEVMA lines. Their height is determined by the DEV value.

Interpretation: This visualizes the overall "volatility of volatility." Wider boxes indicate a chaotic, unpredictable market. Narrower boxes suggest a more stable, predictable environment.

🧠 Consciousness Field (The Grid):

What it represents: This grid provides a historical lookback at the DEV range.

Interpretation: It maps the recent "consciousness" or character of the market's volatility. A consistently wide grid suggests a prolonged period of chaos, while a narrowing grid can signal a transition to a more stable state.

📏 Functorial Levels (Projected Horizontal Lines):

What it represents: These lines extend from the current fastDEVMA and slowDEVMA values into the future.

Interpretation: Think of these as dynamic support and resistance levels for the volatility structure itself. A crossover becomes more significant if it breaks cleanly through a prior established level.

🌊 Flow Boxes (Spaced Out Boxes):

What it represents: These are compact visual footprints of the current regime, colored green for Expansion and red for Contraction.

Interpretation: They provide a quick, at-a-glance confirmation of the dominant volatility flow, reinforcing the background color.

Background Color:

This provides an immediate, unmistakable indication of the current volatility regime. Light Green for Expansion and Light Aqua/Blue for Contraction, allowing you to assess the market environment in a split second.

📊 BACKTESTING PERFORMANCE REVIEW & ANALYSIS

The following is a factual, transparent review of a backtest conducted using the strategy's default settings on a specific instrument and timeframe. This information is presented for educational purposes to demonstrate how the strategy's mechanics performed over a historical period. It is crucial to understand that these results are historical, apply only to the specific conditions of this test, and are not a guarantee or promise of future performance. Market conditions are dynamic and constantly change.

Test Parameters & Conditions

To ensure the backtest reflects a degree of real-world conditions, the following parameters were used. The goal is to provide a transparent baseline, not an over-optimized or unrealistic scenario.

Instrument: CME E-mini Nasdaq 100 Futures (NQ1!)

Timeframe: 5-Minute Chart

Backtesting Range: March 24, 2024, to July 09, 2024

Initial Capital: $100,000

Commission: $0.62 per contract (A realistic cost for futures trading).

Slippage: 3 ticks per trade (A conservative setting to account for potential price discrepancies between order placement and execution).

Trade Size: 1 contract per trade.

Performance Overview (Historical Data)

The test period generated 465 total trades , providing a statistically significant sample size for analysis, which is well above the recommended minimum of 100 trades for a strategy evaluation.

Profit Factor: The historical Profit Factor was 2.663 . This metric represents the gross profit divided by the gross loss. In this test, it indicates that for every dollar lost, $2.663 was gained.

Percent Profitable: Across all 465 trades, the strategy had a historical win rate of 84.09% . While a high figure, this is a historical artifact of this specific data set and settings, and should not be the sole basis for future expectations.

Risk & Trade Characteristics

Beyond the headline numbers, the following metrics provide deeper insight into the strategy's historical behavior.

Sortino Ratio (Downside Risk): The Sortino Ratio was 6.828 . Unlike the Sharpe Ratio, this metric only measures the volatility of negative returns. A higher value, such as this one, suggests that during this test period, the strategy was highly efficient at managing downside volatility and large losing trades relative to the profits it generated.

Average Trade Duration: A critical characteristic to understand is the strategy's holding period. With an average of only 2 bars per trade , this configuration operates as a very short-term, or scalping-style, system. Winning trades averaged 2 bars, while losing trades averaged 4 bars. This indicates the strategy's logic is designed to capture quick, high-probability moves and exit rapidly, either at a profit target or a stop loss.

Conclusion and Final Disclaimer

This backtest demonstrates one specific application of the VoVix+ framework. It highlights the strategy's behavior as a short-term system that, in this historical test on NQ1!, exhibited a high win rate and effective management of downside risk. Users are strongly encouraged to conduct their own backtests on different instruments, timeframes, and date ranges to understand how the strategy adapts to varying market structures. Past performance is not indicative of future results, and all trading involves significant risk.

🔧 THE DEVELOPMENT PHILOSOPHY: FROM VOLATILITY TO CLARITY

The journey to create VoVix+ began with a simple question: "What drives major market moves?" The answer is often not a change in price direction, but a fundamental shift in market volatility. Standard indicators are reactive to price. We wanted to create a system that was predictive of market state. VoVix+ was designed to go one level deeper—to analyze the behavior, character, and momentum of volatility itself.

The challenge was twofold. First, to create a robust mathematical model to quantify these abstract concepts. This led to the multi-layered analysis of ATR differentials and standard deviations. Second, to make this complex data intuitive and actionable. This drove the creation of the "Visual Universe," where abstract mathematical values are translated into geometric shapes, flows, and fields. The adaptive system was intentionally kept simple and transparent, focusing on a single, impactful parameter (time-based exits) to provide performance feedback without becoming an inscrutable "black box." The result is a tool that is both profoundly deep in its analysis and remarkably clear in its presentation.

⚠️ RISK DISCLAIMER AND BEST PRACTICES

VoVix+ is an advanced analytical tool, not a guarantee of future profits. All financial markets carry inherent risk. The backtesting results shown by the strategy are historical and do not guarantee future performance. This strategy incorporates realistic commission and slippage settings by default, but market conditions can vary. Always practice sound risk management, use position sizes appropriate for your account equity, and never risk more than you can afford to lose. It is recommended to use this strategy as part of a comprehensive trading plan. This was developed specifically for Futures

"The prevailing wisdom is that markets are always right. I take the opposite view. I assume that markets are always wrong. Even if my assumption is occasionally wrong, I use it as a working hypothesis."

— George Soros

— Dskyz, Trade with insight. Trade with anticipation.

Implied SPX from ES Implied SPX from ES Futures (ETH)

Description:

This script calculates the implied SPX index level based on real-time ES futures pricing during extended trading hours (ETH). It uses the spread between the previous day’s ES and SPX RTH closes to adjust for fair value and intraday divergence.

📈 Features:

Tracks current ES price vs. yesterday's RTH spread to estimate SPX

Useful for SPX options traders who want to monitor synthetic index levels during ETH

Ideal for assessing SPX movement when the cash market is closed

This tool is especially helpful for those trading SPX index options overnight or seeking to align SPX levels with ES futures movement.

SMT SwiftEdge PowerhouseSMT SwiftEdge Powerhouse: Precision Trading with Divergence, Liquidity Grabs, and OTE Zones

The SMT SwiftEdge Powerhouse is a powerful trading tool designed to help traders identify high-probability entry points during the most active market sessions—London and New York. By combining Smart Money Technique (SMT) Divergence, Liquidity Grabs, and Optimal Trade Entry (OTE) Zones, this script provides a unique and cohesive strategy for capturing market reversals with precision. Whether you're a scalper or a swing trader, this indicator offers clear visual signals to enhance your trading decisions on any timeframe.

What Does This Script Do?

This script integrates three key concepts to identify potential trading opportunities:

SMT Divergence:

SMT Divergence compares the price action of two correlated assets (e.g., Nasdaq and S&P 500 futures) to detect hidden market reversals. When one asset makes a higher high while the other makes a lower high (bearish divergence), or one makes a lower low while the other makes a higher low (bullish divergence), it signals a potential reversal. This technique leverages institutional "smart money" behavior to anticipate market shifts.

Liquidity Grabs:

Liquidity Grabs occur when price breaks above recent highs or below recent lows on higher timeframes (5m and 15m), often triggering stop-loss orders from retail traders. These breakouts are identified using pivot points and confirm institutional activity, setting the stage for a reversal. The script focuses on liquidity grabs during the London and New York sessions for maximum market activity.

Optimal Trade Entry (OTE) Zones:

OTE Zones are Fibonacci-based retracement areas (e.g., 61.8%) calculated after a liquidity grab. These zones highlight where price is likely to retrace before continuing in the direction of the reversal, offering a high-probability entry point. The script adjusts the width of these zones using the Average True Range (ATR) to adapt to market volatility.

By combining these components, the script identifies when institutional activity (liquidity grabs) aligns with market reversals (SMT divergence) and pinpoints precise entry points (OTE zones) during high-liquidity sessions.

Why Combine These Components?

The integration of SMT Divergence, Liquidity Grabs, and OTE Zones creates a robust trading system for several reasons:

Synergy of Institutional Signals: SMT Divergence and Liquidity Grabs both reflect "smart money" behavior—divergence shows hidden reversals, while liquidity grabs confirm institutional intent to trap retail traders. Together, they provide a strong foundation for identifying high-probability setups.

Session-Based Precision: Focusing on the London and New York sessions ensures signals occur during periods of high volatility and liquidity, increasing their reliability.

Precision Entries with OTE: After confirming a setup with divergence and liquidity grabs, OTE zones provide a clear entry area, reducing guesswork and improving trade accuracy.

Adaptability: The script works on any timeframe, with adjustable settings for signal sensitivity, session times, and Fibonacci levels, making it versatile for different trading styles.

This combination makes the script unique by aligning institutional insights with actionable entry points, tailored to the most active market hours.

How to Use the Script

Setup:

Add the script to your chart (works on any timeframe, e.g., 1m, 5m, 15m).

Configure the settings in the indicator's inputs:

Session Settings: Adjust the start/end times for London and New York sessions (default: London 8-11 UTC, New York 13-16 UTC). You can disable session restrictions if desired.

Asset Settings: Set the primary and secondary assets for SMT Divergence (default: NQ1! and ES1!). Ensure the assets are correlated.

Signal Settings: Adjust the lookback period, ATR period, and signal sensitivity (Low/Medium/High) to control the frequency of signals.

OTE Settings: Choose the Fibonacci level for OTE zones (default: 61.8%).

Visual Settings: Enable/disable OTE zones, SMT labels, and debug labels for troubleshooting.

Interpreting Signals:

Blue Circles: Indicate a liquidity grab (price breaking a 5m or 15m pivot high/low), marking the start of a potential setup.

Blue OTE Zones: Appear after a liquidity grab, showing the retracement area (e.g., 61.8% Fibonacci level) where price is likely to enter for a reversal trade. The label "OTE Trigger 5m/15m" confirms the direction (Short/Long) and session.

Green/Red Entry Boxes: Mark precise entry points when price enters the OTE zone and confirms the SMT Divergence. Green boxes indicate a long entry, red boxes a short entry.

Trading Example:

On a 1m chart, a blue circle appears when price breaks a 5m pivot high during the London session.

A blue OTE zone forms, showing a retracement area (e.g., 61.8% Fibonacci level) with the label "OTE Trigger 5m/15m (Short, London)".

Price retraces into the OTE zone, and a red "Short Entry" box appears, confirming a bearish SMT Divergence.

Enter a short trade at the red box, with a stop-loss above the OTE zone and a take-profit at the next support level.

Originality and Utility

The SMT SwiftEdge Powerhouse stands out by merging SMT Divergence, Liquidity Grabs, and OTE Zones into a single, session-focused indicator. Unlike traditional indicators that focus on one aspect of price action, this script combines institutional reversal signals with precise entry zones, tailored to the most active market hours. Its adaptability across timeframes, customizable settings, and clear visual cues make it a versatile tool for traders seeking to capitalize on smart money movements with confidence.

Tips for Best Results

Use on correlated assets like NQ1! (Nasdaq futures) and ES1! (S&P 500 futures) for accurate SMT Divergence.

Test on lower timeframes (1m, 5m) for scalping or higher timeframes (15m, 1H) for swing trading.

Adjust the "Signal Sensitivity" to "High" for more signals or "Low" for fewer, high-quality setups.

Enable "Show Debug Labels" if signals are not appearing as expected, to troubleshoot pivot points and liquidity grabs.

Rolling ATR Momentum - EnhancedATR Rolling Momentum Indicator – User Manual

---

🔍 Overview

The ATR Rolling Momentum Indicator is a dynamic volatility tool built on the Average True Range (ATR). It not only tracks increasing or decreasing momentum but also provides early warnings and confirmation signals for potential breakout moves. It’s especially powerful for futures and options traders looking to align with expanding price action.

---

📊 Core Components

✅ ATR Delta (Rolling ATR)

- Definition: Difference between current ATR and past ATR (user-defined lookback).

- Use: Tells whether volatility is expanding (positive delta) or contracting (negative delta).

- Visual: Green line for rising momentum, red for declining.

🟣 ATR Delta Slope

- Definition: Measures acceleration in momentum.

- Use: Helps identify early signs of breakout buildup.

- Visual: Purple line. Watch for slope turning up from below.

🟡 Volatility Squeeze (Yellow Dot)

- Definition: Current ATR is significantly lower than its 20-period average.

- Use: Indicates the market is coiling—possible breakout ahead.

🔼 Momentum Start (Green Triangle)

- Definition: ATR Delta slope turns from negative to positive.

- Use: Early warning to prepare for volatility expansion.

🔷 Breakout Confirmation (Blue Label Up)

- Definition: ATR Delta exceeds its high of the last 10 candles.

- Use: Confirms volatility breakout—trade opportunity if direction aligns.

🟩/🟥 Background Color

- Green Background: Momentum rising (positive ATR delta)

- Red Background: Momentum falling (negative ATR delta)

- Yellow Tint: Active squeeze zone

---

✅ How to Use It (Futures/Options Focus)

Step-by-Step:

1. Squeeze Detected (Yellow Dot) → Stay alert. Market is coiling.

2. Green Triangle Appears → Momentum is starting to rise.

3. Background Turns Green → Confirmed rising momentum.

4. Blue Label Appears → Confirmed breakout (enter trade if trend aligns).

Directional Bias:

- Use your main chart setup (price action, EMAs, trendlines, etc.) to decide direction (Call or Put, Long or Short).

- ATR Momentum only tells you how strong the move is—not which way.

---

⚙️ Inputs & Settings

- ATR Period: Default 14 (core volatility measure)

- Rolling Lookback: Used to calculate delta (default 5)

- Slope Length: Used to measure acceleration (default 3)

- Squeeze Factor: Default 0.8 — lower = more sensitive squeeze detection

- Breakout Lookback: Checks ATR delta against last X bars (default 10)

---

🧠 Pro Tips

- Works great when paired with EMA stacks, price structure, or breakout patterns.

- Avoid taking trades based only on squeeze or momentum—combine with chart confirmation.

- If background turns red after a breakout, it may be losing momentum—book partials or tighten stops.

---

🧭 Ideal For:

- Nifty/BankNifty Futures

- Option directional trades (call/put buying)

- Index scalping and momentum swing setups

---

Use this tool as your volatility compass—it won't tell you where to go, but it'll tell you when the wind is strong enough to move fast.

End of Manual

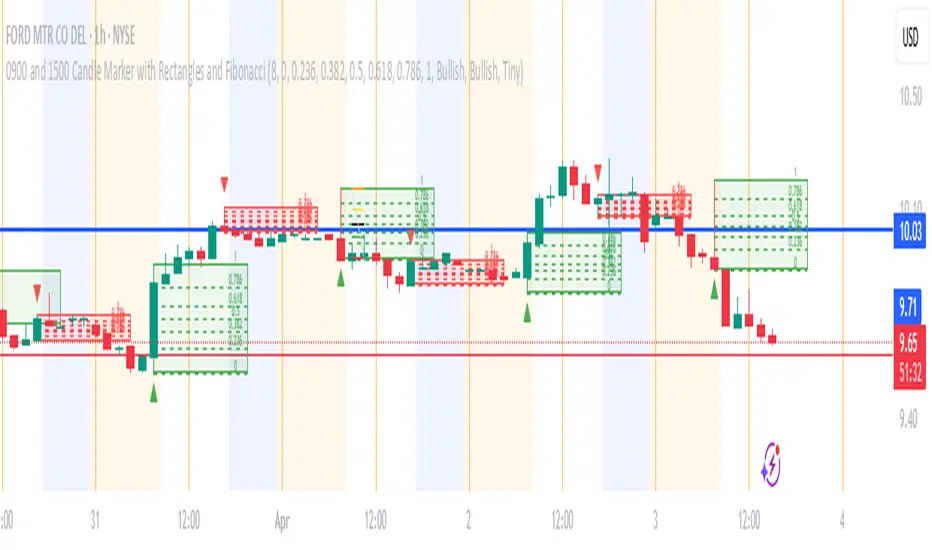

0900 and 1500 Candle Marker with Rectangles and FibonacciWelcome to the Indicator

// This tool is designed to help you analyze stock - crypto - or futures charts on TradingView by marking specific times - 9:00 AM and 3:00 PM (Eastern Time) - with colored rectangles and optional Fibonacci levels.

// It is perfect for spotting key moments in your trading day - like market opens or afternoon shifts - and understanding price ranges with simple lines and numbers.

// Whether you are new to trading or just want an easy way to visualize these times - this indicator is here to assist you.

//

// What It Does

// - Draws a green rectangle at 9:00 AM and a red rectangle at 3:00 PM on your chart - based on Eastern Time (America/New_York timezone).

// - Adds dashed lines inside these rectangles (called Fibonacci levels) to show important price points - like 0.236 or 0.618 of the rectangle’s height.

// - Places numbers on these lines (e.g. "0.5") so you can see exactly what each level represents.

// - Works on different chart types (stocks - crypto - futures) and adjusts for futures trading hours if needed.

// - Is designed to work best on timeframes of 1 hour or shorter (like 1-hour - 30-minute - 15-minute - 5-minute - or 1-minute charts) - where you can see the 9:00 AM and 3:00 PM candles clearly.

// - Lets you customize what you see through a settings menu - like hiding some lines or changing colors.

YOU MAY NOT MONETIZE

ANY PORTION OF THIS CODE.

WE ARE ALL IN THIS THING TOGETHER TO WIN.

BE A BLESSING ONTO THE WORLD AND GIVE.:)

NIFTY VWAP DistanceNIFTY Futures VWAP Distance Indicator

Track price deviation from Volume-Weighted Average Price in real-time

📈 Key Features:

Measures absolute (points) and percentage distance from VWAP

Daily session reset aligned with NSE trading hours

Dual-axis visualization with clear zero reference line

Real-time data table display for instant analysis

Typical price calculation: (H+L+C)/3 formula

Built-in safeguards against division errors

🎯 Ideal For:

Intraday traders monitoring mean reversion opportunities

Algorithmic traders needing VWAP deviation metrics

Swing traders identifying overextended price moves

Market profile analysts studying auction theory

📊 How to Use:

Apply to NIFTY Futures chart (1m-1h timeframes recommended)

Blue line = Points above/below VWAP

Red line = Percentage deviation

Positive values = Price > VWAP (bullish territory)

Negative values = Price < VWAP (bearish territory)

💡 Pro Tips:

Combine with volume profile for confirmation

Watch for >1% deviations for potential reversals

Use divergence patterns for early trend change signals

Works best with raw futures data (not continuous contracts)

🔧 Technical Specs:

Pine Script v5+

No repainting

Low latency calculations

Mobile-friendly display

"Know when price strays too far from fair value"

Ethereum COT [SAKANE]#Overview

Ethereum COT is an indicator that visualizes Ethereum futures market positions based on the Commitment of Traders (COT) report provided by the CFTC (Commodity Futures Trading Commission).

This indicator stands out from similar tools with the following features:

- **Flexible Data Switching**: Supports multiple COT report types, including "Financial," "Legacy," "OpenInterest," and "Force All."

- **Position Direction Selection**: Easily switch between long, short, and net positions. Net positions are automatically calculated.

- **Open Interest Integration**: View the overall trading volume in the market at a glance.

- **Comparison and Customization**: Toggle individual trader types (Dealer, Asset Manager, Commercials, etc.) on and off, with visually distinct color-coded graphs.

- **Force All Mode**: Simultaneously display data from different report types, enabling comprehensive market analysis.

These features make it a powerful tool for both beginners and advanced traders to deeply analyze the Ethereum futures market.

#Use Cases

1. **Analyzing Trader Sentiment**

- Compare net positions of various trader types (Dealer, Asset Manager, Commercials, etc.) to understand market sentiment.

2. **Identifying Trend Reversals**

- Detect early signs of trend reversals from sudden increases or decreases in long and short positions.

3. **Utilizing Open Interest**

- Monitor the overall trading volume represented by open interest to evaluate entry points or changes in volatility.

4. **Tracking Position Structures**

- Compare positions of leveraged funds and asset managers to analyze risk-on or risk-off environments.

#Key Features

1. **Report Type Selection**

- Financial (Financial Traders)

- Legacy (Legacy Report)

- Open Interest

- Force All (Display all data)

2. **Position Direction Selection**

- Long

- Short

- Net

3. **Visualization of Major Trader Types**

- Financial Traders: Dealer, Asset Manager, Leveraged Funds, Other Reportable

- Legacy: Commercials, Non-Commercials, Small Speculators

4. **Open Interest Visualization**

- Monitor the total open positions in the market.

5. **Flexible Customization**

- Toggle individual trader types on and off.

- Intuitive settings with tooltips for better usability.

#How to Use

1. Add the indicator to your chart and click the settings icon in the top-right corner.

2. Select the desired report type in the "Report Type" field.

3. Choose the position direction (Long/Short/Net) in the "Direction" field.

4. Toggle the visibility of trader types as needed.

#Notes

- Data is provided by the CFTC and is updated weekly. It is not real-time.

- Changes to the settings may take a few seconds to reflect.

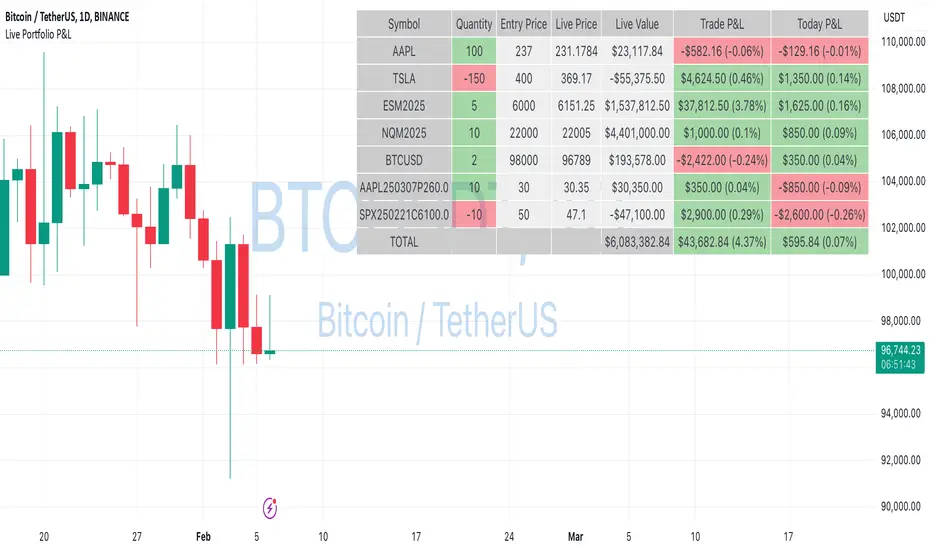

Live Portfolio P<his script calculates live P&L (Profit & Loss) for up to 40 instruments — stocks, ETFs, options, futures, and Forex pairs supported by TradingView. Instead of juggling numerous inputs, you paste your portfolio in CSV format into a single text field, and the script handles the rest. It parses each position and displays a comprehensive table showing the symbol, current price, position value, total P&L, and today’s P&L—all updated in real time.

Key Features

CSV Portfolio Input – Effortlessly import all your positions at once without filling in multiple fields. You can export the position from your broker, save it in the required format, and paste it into this script.

Supports Various Asset Classes – Works with any instrument that TradingView provides data for, including futures, options, and Forex.

Up to 40 Instruments – Track a broad and diverse set of holdings in one place.

Real-Time Updates – Get immediate feedback on live price changes, total value, and current P&L.

Today’s P&L – Monitor your daily performance to gauge short-term trends.

CSV is consumed in the following format:

Symbol (supported TradingView instruments)

Entry Price

Quantity (negative for short position)

Lot Size (for futures/options, it might not be one)

For example:

AAPL,237,100,1

TSLA,400,-150,1

ESM2025,6000,5,50

Planned Enhancements

Multi-Currency Support – Automatically convert and display your positions’ values in different currencies.

Advanced Metrics – Get deeper insights with calculations for drawdown, Sharpe ratio, and more.

Risk Management Tools – Set stop-loss and take-profit levels and receive alerts when thresholds are hit.

Option Greeks & Margin Calculations – Manage complex option strategies and track margin requirements.

Questions for You

What additional features would you like to see?

Are there any specific metrics or analytics you’d find especially valuable?

How might this script fit into your current trading workflow?

Feel free to share your thoughts and suggestions. Your feedback will help shape future updates and make this tool even more helpful for traders like you!

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

Aggregated Volume (Multi-Exchange)Indicator: Aggregated Volume (Multi-Exchange)

Overview:

The Aggregated Volume (Multi-Exchange) indicator is designed to aggregate trading volume data from multiple exchanges for a specific cryptocurrency pair. The goal is to provide a consolidated view of the total trading volume across different platforms, helping traders and analysts gauge the overall market activity for a given asset.

Features:

Multi-Exchange Support: The indicator allows you to aggregate trading volume data from various exchanges. Users can enable or disable volume data from specific exchanges (e.g., Binance, Bybit, Kucoin, etc.).

Spot and Futures Volumes: The indicator can sum the volume for spot trading and futures trading separately if desired. However, in the current version, it only sums the volume for specific pairs across multiple exchanges, without distinguishing between spot and futures volumes (though this feature can be added if necessary).

Customizable Exchange Selection: Users can select which exchanges' volume data to include in the aggregation.

Real-Time Updates: The volume data is updated in real-time as new bars are formed on the chart, providing an up-to-date picture of the trading volume.

Purpose:

The primary purpose of this indicator is to consolidate trading volume information from multiple exchanges for the same trading pair (e.g., BTC/USD). Traders can use this aggregated volume to gain a better understanding of market activity across various platforms, as well as assess the level of liquidity and interest in a particular asset.

By viewing the total aggregated volume, traders can:

Track market trends: Higher aggregated volume can signal increased market interest, making it easier to spot trends or potential breakouts.

Analyze liquidity: This indicator can help traders assess liquidity in the market, especially when using multiple exchanges.

Identify potential market manipulation: If there is a sudden spike in volume on multiple exchanges, it could signal market manipulation or an event-driven surge.

How it Works:

Volume Aggregation: The indicator collects and sums the volume data for a given symbol (e.g., BTC/USD) from different exchanges like Binance, Bybit, Kucoin, and others.

Multiple Exchanges: The volume data is aggregated from each selected exchange and plotted as a single volume value on the chart.

Real-Time Volume Plotting: The total aggregated volume is then plotted as a histogram on the chart, with the color of the bars changing depending on whether the price is rising or falling (typically green for rising prices and red for falling prices).

Inputs/Settings:

Exchange Selection: A list of checkboxes where users can choose which exchanges' volume data to include (e.g., Binance, Bybit, Kucoin, etc.).

Color Settings: Users can set the color for the histogram bars based on price direction (e.g., green for rising and red for falling).

Volume Calculation: The indicator calculates the volume for a specific cryptocurrency pair across selected exchanges in real-time.

Bitcoin COT [SAKANE]#Overview

Bitcoin COT is an indicator that visualizes Bitcoin futures market positions based on the Commitment of Traders (COT) report provided by the CFTC (Commodity Futures Trading Commission).

This indicator stands out from similar tools with the following features:

- Flexible Data Switching: Supports multiple COT report types, including "Financial," "Legacy," "OpenInterest," and "Force All."

- Position Direction Selection: Easily switch between long, short, and net positions. Net positions are automatically calculated.

- Open Interest Integration: View the overall trading volume in the market at a glance.

- Comparison and Customization: Toggle individual trader types (Dealer, Asset Manager, Commercials, etc.) on and off, with visually distinct color-coded graphs.

- Force All Mode: Simultaneously display data from different report types, enabling comprehensive market analysis.

These features make it a powerful tool for both beginners and advanced traders to deeply analyze the Bitcoin futures market.

#Use Cases

1. Analyzing Trader Sentiment

- Compare net positions of various trader types (Dealer, Asset Manager, Commercials, etc.) to understand market sentiment.

2. Identifying Trend Reversals

- Detect early signs of trend reversals from sudden increases or decreases in long and short positions.

3. Utilizing Open Interest

- Monitor the overall trading volume represented by open interest to evaluate entry points or changes in volatility.

4. Tracking Position Structures

- Compare positions of leveraged funds and asset managers to analyze risk-on or risk-off environments.

#Key Features

1. Report Type Selection

- Financial (Financial Traders)

- Legacy (Legacy Report)

- Open Interest

- Force All (Display all data)

2. Position Direction Selection

- Long

- Short

- Net

3. Visualization of Major Trader Types

- Financial Traders: Dealer, Asset Manager, Leveraged Funds, Other Reportable

- Legacy: Commercials, Non-Commercials, Small Speculators

4. Open Interest Visualization

- Monitor the total open positions in the market.

5. Flexible Customization

- Toggle individual trader types on and off.

- Intuitive settings with tooltips for better usability.

#How to Use

1. Add the indicator to your chart and click the settings icon in the top-right corner.

2. Select the desired report type in the "Report Type" field.

3. Choose the position direction (Long/Short/Net) in the "Direction" field.

4. Toggle the visibility of trader types as needed.

#Notes

- Data is provided by the CFTC and is updated weekly. It is not real-time.

- Changes to the settings may take a few seconds to reflect.

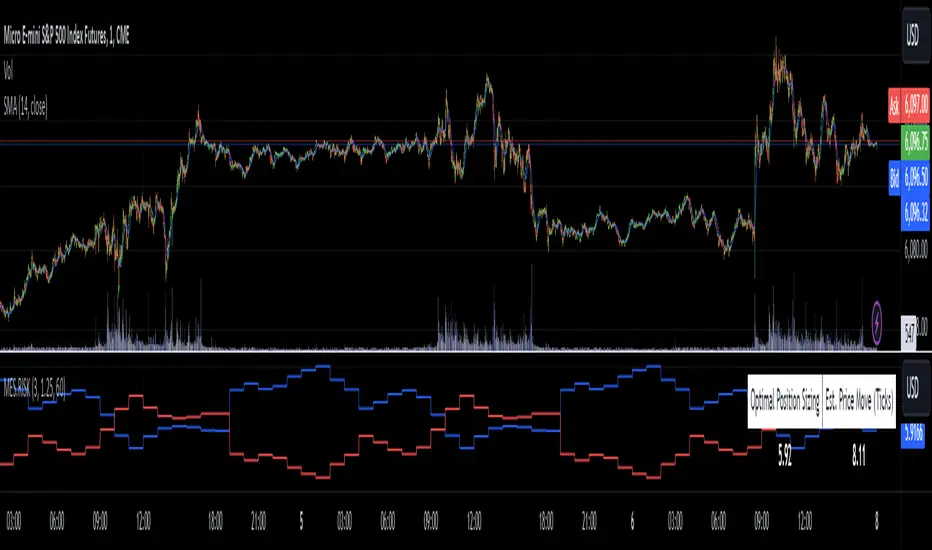

MES Position Sizing EstimatorDescription and Use:

Here is an indicator which aims to help all Micro-ES futures traders who struggle with risk management! I created this indicator designed as a general guideline to help short term traders (designed for 1 minute candles) determine how many contracts to trade on the MES for their desired profit target.

To use the indicator, simply go to MES on the 1 minute timeframe, apply the indicator, and enter your Holding Period (how long you want to have your position open for), Value Per Tick

(usually 1.25 for MES since one point is $5) and your target PnL for the trade in the inputs tab.

It will then show in a table the recommended position sizing, as well as the estimated price change for your holding period. Additionally, there are two plotted lines also showing the position sizing and estimated price change historically.

How the indicator works

On the technical level, I made calculations for this indicator using Python. I downloaded 82 days of 1 minute OHLC data from TradingView, and then ran regression (log-transformed linear regression specifically) to calculate how the average price change in MES futures scales with the amount of time a position is held for, and then ran these regressions for every hour of the day. I then copied the equations from those regressions into Pinescript, and used the assumption that:

position size = target PnL / (estimated price change for time * tick value)

Therefore, Choosing the number of contracts to trade position sizing for Micro E-mini S&P 500 Futures (MES) based on time of day, holding period, and tick value. This tool leverages historical volatility patterns and log-transformed linear regression models to provide precise recommendations tailored to your trading strategy.

If you want to check out how the regression code worked in python, it is all open source and available on my Github repository for it .

Notes:

The script assumes a log-normal distribution of price movements and is intended as an educational tool to aid in risk management.

It is not a standalone trading system and should be used in conjunction with other trading strategies and risk assessments.

Past performance is not indicative of future results, and traders should exercise caution and adjust their strategies based on personal risk tolerance.

This script is open-source and available for use and modification by the TradingView community. It aims to provide a valuable resource for traders seeking to enhance their risk management practices through data-driven insights.

Historical High/Lows Statistical Analysis(More Timeframe interval options coming in the future)

Indicator Description

The Hourly and Weekly High/Low (H/L) Analysis indicator provides a powerful tool for tracking the most frequent high and low points during different periods, specifically on an hourly basis and a weekly basis, broken down by the days of the week (DOTW). This indicator is particularly useful for traders seeking to understand historical behavior and patterns of high/low occurrences across both hourly intervals and weekly days, helping them make more informed decisions based on historical data.

With its customizable options, this indicator is versatile and applicable to a variety of trading strategies, ranging from intraday to swing trading. It is designed to meet the needs of both novice and experienced traders.

Key Features

Hourly High/Low Analysis:

Tracks and displays the frequency of hourly high and low occurrences across a user-defined date range.

Enables traders to identify which hours of the day are historically more likely to set highs or lows, offering valuable insights into intraday price action.

Customizable options for:

Hourly session start and end times.

22-hour session support for futures traders.

Hourly label formatting (e.g., 12-hour or 24-hour format).

Table position, size, and design flexibility.

Weekly High/Low Analysis by Day of the Week (DOTW):

Captures weekly high and low occurrences for each day of the week.

Allows traders to evaluate which days are most likely to produce highs or lows during the week, providing insights into weekly price movement tendencies.

Displays the aggregated counts of highs and lows for each day in a clean, customizable table format.

Options for hiding specific days (e.g., weekends) and customizing table appearance.

User-Friendly Table Display:

Both hourly and weekly data are displayed in separate tables, ensuring clarity and non-interference.

Tables can be positioned on the chart according to user preferences and are designed to be visually appealing yet highly informative.

Customizable Date Range:

Users can specify a start and end date for the analysis, allowing them to focus on specific periods of interest.

Possible Uses

Intraday Traders (Hourly Analysis):

Analyze hourly price action to determine which hours are more likely to produce highs or lows.

Identify intraday trading opportunities during statistically significant time intervals.

Use hourly insights to time entries and exits more effectively.

Swing Traders (Weekly DOTW Analysis):

Evaluate weekly price patterns by identifying which days of the week are more likely to set highs or lows.

Plan trades around days that historically exhibit strong movements or price reversals.

Futures and Forex Traders:

Use the 22-hour session feature to exclude the CME break or other session-specific gaps from analysis.

Combine hourly and DOTW insights to optimize strategies for continuous markets.

Data-Driven Trading Strategies:

Use historical high/low data to test and refine trading strategies.

Quantify market tendencies and evaluate whether observed patterns align with your strategy's assumptions.

How the Indicator Works

Hourly H/L Analysis:

The indicator calculates the highest and lowest prices for each hour in the specified date range.

Each hourly high and low occurrence is recorded and aggregated into a table, with counts displayed for all 24 hours.

Users can toggle the visibility of empty cells (hours with no high/low occurrences) and adjust the table's design to suit their preferences.

Supports both 12-hour (AM/PM) and 24-hour formats.

Weekly H/L DOTW Analysis:

The indicator tracks the highest and lowest prices for each day of the week during the user-specified date range.

Highs and lows are identified for the entire week, and the specific days when they occur are recorded.

Counts for each day are aggregated and displayed in a table, with a "Totals" column summarizing the overall occurrences.

The analysis resets weekly, ensuring accurate tracking of high/low days.

Code Breakdown:

Data Aggregation:

The script uses arrays to store counts of high/low occurrences for both hourly and weekly intervals.

Daily data is fetched using the request.security() function, ensuring consistent results regardless of the chart's timeframe.

Weekly Reset Mechanism:

Weekly high/low values are reset at the start of a new week (Monday) to ensure accurate weekly tracking.

A processing flag ensures that weekly data is counted only once at the end of the week (Sunday).

Table Visualization:

Tables are created using the table.new() function, with customizable styles and positions.

Header rows, data rows, and totals are dynamically populated based on the aggregated data.

User Inputs:

Customization options include text colors, background colors, table positioning, label formatting, and date ranges.

Code Explanation

The script is structured into two main sections:

Hourly H/L Analysis:

This section captures and aggregates high/low occurrences for each hour of the day.

The logic is session-aware, allowing users to define custom session times (e.g., 22-hour futures sessions).

Data is displayed in a clean table format with hourly labels.

Weekly H/L DOTW Analysis:

This section tracks weekly highs and lows by day of the week.

Highs and lows are identified for each week, and counts are updated only once per week to prevent duplication.

A user-friendly table displays the counts for each day of the week, along with totals.

Both sections are completely independent of each other to avoid interference. This ensures that enabling or disabling one section does not impact the functionality of the other.

Customization Options

For Hourly Analysis:

Toggle hourly table visibility.

Choose session start and end times.

Select hourly label format (12-hour or 24-hour).

Customize table appearance (colors, position, text size).

For Weekly DOTW Analysis:

Toggle DOTW table visibility.

Choose which days to include (e.g., hide weekends).

Customize table appearance (colors, position, text size).

Select values format (percentages or occurrences).

Conclusion

The Hourly and Weekly H/L Analysis indicator is a versatile tool designed to empower traders with data-driven insights into intraday and weekly market tendencies. Its highly customizable design ensures compatibility with various trading styles and instruments, making it an essential addition to any trader's toolkit.

With its focus on accuracy, clarity, and customization, this indicator adheres to TradingView's guidelines, ensuring a robust and valuable user experience.

Dynamic Spot vs Perp Spread### **Description for TradingView Publication**

---

**Dynamic Spot vs Perp Spread**

(For USDT-Spot and USDT.P-Perp)

Summary of Usefulness:

This indicator is a valuable tool for traders who want to monitor and capitalize on the relationship between spot and perpetual futures (perp) prices. When the spot price exceeds the perp price, it's often a leading signal that the perp price will follow, creating potential trading opportunities. While this behavior doesn't happen every time, divergences between spot and perp prices can frequently signal significant market movements.

What it Does:

This indicator calculates and displays the price spread (percentage difference) between the spot price and perpetual futures (perp) price of a cryptocurrency asset. It dynamically adjusts to the instrument being viewed, ensuring that spot dominance (spot price higher) is plotted above the zero line and perp dominance (perp price higher) is plotted below the zero line. Additionally, the indicator accounts for symbols with multipliers (e.g., `1000SHIBUSDT.P`) to ensure accurate calculations.

Key features include:

- Automatic symbol detection and adjustment for Spot/Perp pairs.

- Dynamic handling of price multipliers for assets with prefixes like `1000`.

- Visualization of spread with a histogram and optional smoothing using an EMA (Exponential Moving Average).

- Configurable alerts for significant spread changes and spread flips.

- No repainting: the indicator uses the `barmerge.lookahead_off` setting to ensure stable, non-repainting values.

---

### **How to Use**

1. **Add the Indicator:**

- Search for "Dynamic Spot vs Perp Spread" in the TradingView Indicators library and add it to your chart.

2. **Understand the Visualization:**

- A positive spread (green histogram) indicates that the spot price is higher than the perp price (spot dominance).

- A negative spread (red histogram) indicates that the perp price is higher than the spot price (perp dominance).

3. **Customize Settings:**

- **EMA Length:** Use the input field to smooth the spread data over a chosen number of periods.

- **Alert Threshold:** Set a threshold to receive alerts when the spread exceeds a specific percentage.

4. **Receive Alerts:**

- Enable alerts for spread flips (when dominance shifts between spot and perp) or when the spread exceeds the defined threshold.

5. **Use Case Examples:**

- **Spot vs. Perp Arbitrage:** Traders can monitor significant deviations between spot and perp prices to identify potential arbitrage opportunities.

- **Market Sentiment Analysis:** Persistent spot dominance may indicate stronger buying interest in the spot market, while perp dominance may suggest futures market speculation.

---

### **Repainting Behavior**

This indicator **does not repaint** because it uses `barmerge.lookahead_off` for all calculations, ensuring that data from the comparison symbol (spot or perp) is locked to the currently completed candle. This means the values plotted and alerts triggered are reliable and do not change retrospectively.

Repainting occurs when an indicator uses future-looking or incomplete data for calculations. By design, this indicator avoids such practices, making it suitable for live trading and analysis.

---

Universal Estimated Funding RateDescription:

This indicator calculates an estimated funding rate for perpetual futures contracts on Binance. The funding rate is derived from the premium index, reflecting the difference between the perpetual futures price and the spot market price, with an assumed constant interest rate.

Key Features:

Dynamic Symbol Detection: Automatically adapts to the base and quote currencies of the current chart, making it compatible with most Binance trading pairs that support both spot and perpetual markets.

Customizable Timeframes: Supports multiple timeframes, with a default recommendation of 4 hours to align with Binance's funding intervals.

Real-Time Data: Fetches live spot and perpetual prices to calculate the premium index and estimate funding rates in real time.

Error Handling: Displays alerts and highlights invalid data if the pair lacks spot or perpetual market information, ensuring clarity for the user.

Use Case:

This indicator is designed to help traders:

Track market sentiment through funding rates.

Identify opportunities for arbitrage or hedging between spot and perpetual markets.

Monitor trends in funding rates to complement technical analysis and refine entry/exit decisions.

How It Works:

The script dynamically identifies the spot and perpetual futures symbols for the selected chart.

It calculates the premium index as the percentage difference between the perpetual and spot prices.

Combines the premium index with an assumed interest rate (default: 0.01% per 8 hours) to estimate the funding rate.

How to Use:

Apply the indicator to any Binance trading pair chart.

Set the timeframe to align with your trading strategy (e.g., 4-hour for swing trading or 5-minute for scalping).

Observe the plotted funding rate to assess market sentiment:

Positive values indicate a long bias (longs pay shorts).

Negative values indicate a short bias (shorts pay longs).

Important Notes:

This is an estimated funding rate based on available data. For exact values, refer to Binance directly.

Funding rates are updated every 8 hours on Binance, so aligning with 4-hour charts is optimal.

Ensure both spot and perpetual data are available for the chosen pair.

This indicator is open-source and serves as a valuable tool for traders seeking deeper insights into funding dynamics on Binance. Happy trading! 🚀

COT Commercials Positions Table Der COT Commercials Opposite Positions Table for Forex ist ein umfangreicher TradingView-Indikator, der die Positionen der kommerziellen Marktteilnehmer (Commercials) im Rahmen des Commitments of Traders (COT)-Berichts darstellt. Er zeigt Long-, Short-, und Netto-Positionen sowie deren prozentuale Anteile für ausgewählte Märkte an.

Hauptmerkmale:

Datenquellenwahl: Unterstützt "Futures Only" und "Futures and Options".

Marktabdeckung: Umfasst Währungen, Rohstoffe, Indizes und Kryptowährungen.

Farbkodierung: Dynamische Farbverläufe zur Hervorhebung von Extremen bei Long-/Short-Positionen und Prozentsätzen.

Historische Daten: Zeigt Positionsdaten der letzten 10 Wochen an.

Anpassbare Tabelle: Klar strukturiert mit wichtigen Kennzahlen wie max./min. Positionen und Netto-Positionen.

Der Indikator ist besonders für Trader nützlich, die Marktstimmungen analysieren und Positionierungen großer Marktteilnehmer in ihre Handelsentscheidungen einbeziehen möchten.

Der Indikator ist hauptsächlich für Futures gedacht und funktioniert nur im 1 Woche Chart.

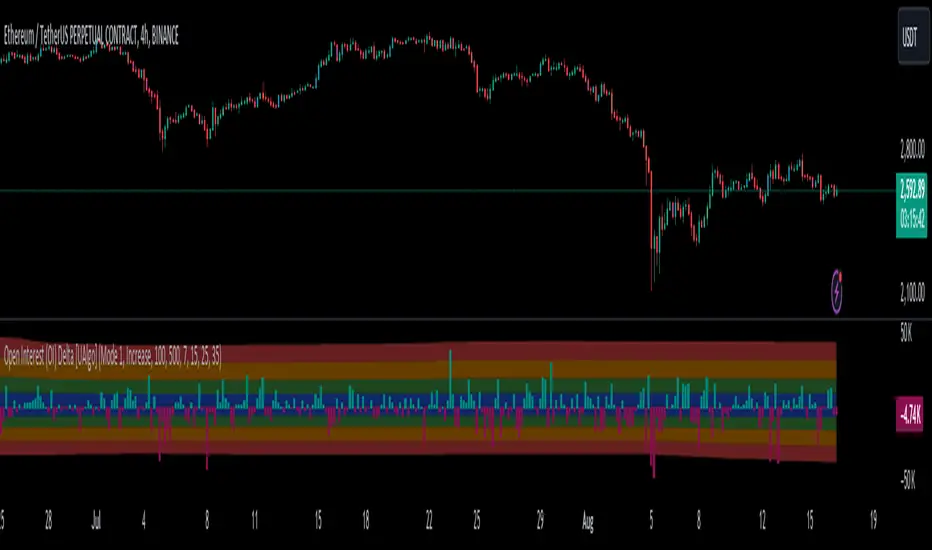

Open Interest (OI) Delta [UAlgo]The Open Interest (OI) Delta indicator is a tool designed to provide insights into the dynamics of Open Interest changes within the futures market. Open Interest (OI) refers to the total number of outstanding derivative contracts, such as options or futures, that have not been settled. The OI Delta measures the change in Open Interest over a specified period, allowing traders to assess whether new money is entering the market or existing positions are being closed.

This indicator offers two distinct display modes to visualize OI Delta, along with customizable levels that help in categorizing the magnitude of OI changes. Additionally, it provides the option to color-code the bars on the price chart based on the intensity and direction of OI Delta, making it easier for traders to interpret market sentiment and potential future price movements.

🔶 Key Features

Two Display Modes: Choose between two different modes for visualizing OI Delta, depending on your analysis preferences:

Mode 1: Displays the OI Delta directly as positive or negative values.

Mode 2: Separates positive and negative OI Delta values, displaying them as absolute values for easier comparison.

Customizable Levels: Set up to four levels of OI Delta magnitude, each with customizable thresholds and colors. These levels help categorize the OI changes into Normal, Medium, Large, and Extreme ranges, allowing for a more nuanced interpretation of market activity.

MA Length and Standard Deviation Period: Adjust the moving average length and standard deviation period for OI Delta, which smooths out the data and helps in identifying significant deviations from the norm.

Color-Coded Bar Chart: Optionally color the price bars on your chart based on the OI Delta levels, helping to visually correlate price action with changes in Open Interest.

Heatmap Display: Toggle the display of OI Delta levels on the chart, with the option to fill the areas between these levels for a more visually intuitive understanding of the data.

🔶 Interpreting Indicator

Positive vs. Negative OI Delta:

A positive OI Delta indicates that the Open Interest is increasing, suggesting that new contracts are being created, which could imply fresh capital entering the market.

A negative OI Delta suggests that Open Interest is decreasing, indicating that contracts are being closed out or settled, which might reflect profit-taking or a reduction in market interest.

Magnitude Levels:

Level 1 (Normal OI Δ): Represents typical, less significant changes in OI. If the OI Delta stays within this range, it may indicate routine market activity without any substantial shift in sentiment.

Level 2 (Medium OI Δ): Reflects a more significant change in OI, suggesting increased market interest and possibly the beginning of a new trend or phase of market participation.

Level 3 (Large OI Δ): Indicates a strong change in OI, often associated with a decisive move in the market. This could signify strong conviction among market participants, either bullish or bearish.

Level 4 (Extreme OI Δ): The highest level of OI change, often preceding major market moves. Extreme OI Δ can be a signal of potential market reversals or the final phase of a strong trend.

Color-Coded Bars:

When enabled, the color of the price bars will reflect the magnitude and direction of the OI Delta. This visual aid helps in quickly assessing the correlation between price movements and changes in market sentiment as indicated by OI.

This indicator is particularly useful for futures traders looking to gauge the strength and direction of market sentiment by analyzing changes in Open Interest. By combining this with price action, traders can gain a deeper understanding of market dynamics and make more informed trading decisions

🔶 Disclaimer

Use with Caution: This indicator is provided for educational and informational purposes only and should not be considered as financial advice. Users should exercise caution and perform their own analysis before making trading decisions based on the indicator's signals.

Not Financial Advice: The information provided by this indicator does not constitute financial advice, and the creator (UAlgo) shall not be held responsible for any trading losses incurred as a result of using this indicator.

Backtesting Recommended: Traders are encouraged to backtest the indicator thoroughly on historical data before using it in live trading to assess its performance and suitability for their trading strategies.

Risk Management: Trading involves inherent risks, and users should implement proper risk management strategies, including but not limited to stop-loss orders and position sizing, to mitigate potential losses.

No Guarantees: The accuracy and reliability of the indicator's signals cannot be guaranteed, as they are based on historical price data and past performance may not be indicative of future results.

COT Index Commercials vs large and small SpeculatorsThe COT reports for futures-only Commitments of Traders and for Futures and Options Combined Commitments of Traders are collected on Tuesdays and published every Friday at 3:30 p.m. Eastern time. The raw data is available free of charge on the Commodity Futures Trading Commission (CFTC) website.

Use it to get a better understanding on which side the smart money (producers, commercials) are trading on.