Credit Spread Monitor: HY & IG vs US10Y📉 Credit Spread Monitor: HY & IG vs US10Y

This indicator provides a dynamic and visual way to monitor credit spreads relative to the US Treasury benchmark. By comparing High Yield (HY) and Investment Grade (IG) corporate bond yields to the 10-Year US Treasury Yield (US10Y), it helps assess market stress, investor risk appetite, and potential macro turning points.

🔍 What It Does

-Calculates credit spreads:

HY Spread = BAMLH0A0HYM2EY − US10Y

IG Spread = BAMLC0A0CMEY − US10Y

-Detects macro risk regimes using statistical thresholds and yield curve signals:

🔴 HY Spread > +2σ → Potential financial stress

🟠 Inverted Yield Curve + HY Spread > 2% → Recession risk

🟢 HY Spread < 1.5% → Risk-on environment

-Visually highlights conditions with intuitive background colors for fast decision-making.

📊 Data Sources Explained

🔴 High Yield (HY): BAMLH0A0HYM2EY → ICE BofA US High Yield Index Effective Yield

🔵 Investment Grade (IG): BAMLC0A0CMEY → ICE BofA US Corporate Index Effective Yield

⚪ Treasury 10Y: US10Y → 10-Year US Treasury Yield

⚪ Treasury 2Y: US02Y → 2-Year US Treasury Yield (used to detect curve inversion)

✅ This Indicator Is Ideal For:

Macro traders looking to anticipate economic inflection points

Portfolio managers monitoring systemic risk or credit cycles

Fixed-income analysts tracking the cost of corporate borrowing

ETF/Asset allocators identifying shifts between risk-on and risk-off environments

🧠 Why It's Useful

This script helps visualize how tight or loose credit conditions are relative to government benchmarks. Since HY spreads typically widen before major downturns, this tool can provide early warning signals. Similarly, compressed spreads may indicate overheating or complacency in risk markets.

🛠️ Practical Use Case:

You’re managing a multi-asset portfolio. The HY spread jumps above +2σ while the yield curve remains inverted. You decide to reduce exposure to equities and high-yield bonds and rotate into cash or Treasuries as recession risk rises.

📎 Additional Notes

Sourced from FRED (Federal Reserve Economic Data) and TradingView’s bond feeds.

Designed to work best on daily resolution, using open prices to ensure consistency across series with different update timings.

This script is original, not based on built-in or public templates, and intended to offer educational, statistical, and visual insights for serious market participants.

在腳本中搜尋"N+credit最新动态"

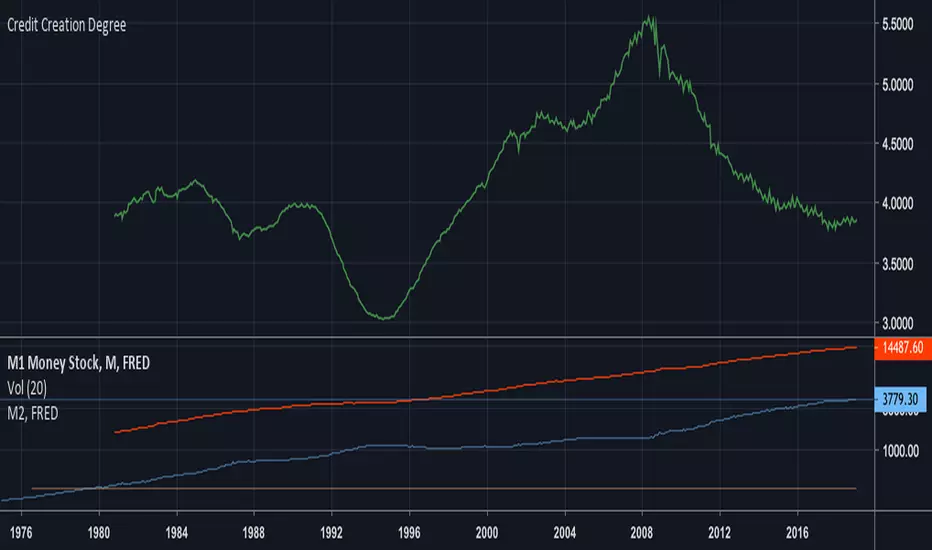

Credit Creation Degree_Debt/M1 [Xiaolai(Sean) Chen] TathaGadaReflect on my previous script "Credit Creation Degree" which is M2/M1 money stock value is the reflection of the degree of credit created which was mentioned by Ray Dalio in his 30 min video "How the Market and Economic Machines Work"

This is another option which compares the Federal Government Debt: Total domestic debt with M1 Money stock

Credit degree will finally decrease in the Long-Term Debt circle.

Credit Creation Degree_Debt/M1 [Xiaolai(Sean) Chen]Reflect on my previous script "Credit Creation Degree" which is M2/M1 money stock value is the reflection of the degree of credit created which was mentioned by Ray Dalio in his 30 min video "How the Market and Economic Machines Work"

This is another option which compares the Federal Government Debt: Total domestic debt with M1 Money stock

Credit degree will finally decrease in the Long-Term Debt circle.

Triad Macro Gauge__________________________________________________________________________________

Introduction

__________________________________________________________________________________

The Triad Macro Gauge (TMG) is designed to provide traders with a comprehensive view of the macroeconomic environment impacting financial markets. By synthesizing three critical market signals— VIX (volatility) , Credit Spreads (credit risk) , and the Stocks/Bonds Ratio (SPY/TLT) —this indicator offers a probabilistic assessment of market sentiment, helping traders identify bullish or bearish macro conditions.

Holistic Macro Analysis: Combines three distinct macroeconomic indicators for multi-dimensional insights.

Customization & Flexibility: Adjust weights, thresholds, lookback periods, and visualization styles.

Visual Clarity: Dynamic table, color-coded plots, and anomaly markers for quick interpretation.

Fully Consistent Scores: Identical values across all timeframes (4H, daily, weekly).

Actionable Signals: Clear bull/bear thresholds and volatility spike detection.

Optimized for timeframes ranging from 4 hour to 1 week , the TMG equips swing traders and long-term investors with a robust tool to navigate macroeconomic trends.

__________________________________________________________________________________

Key Indicators

__________________________________________________________________________________

VIX (CBOE:VIX): Measures market volatility (negatively weighted for bearish signals).

Credit Spreads (FRED:BAMLH0A0HYM2EY): Tracks high-yield bond spreads (negatively weighted).

Stocks/Bonds Ratio (SPY/TLT): Evaluates equity sentiment relative to treasuries (positively weighted).

__________________________________________________________________________________

Originality and Purpose

__________________________________________________________________________________

The TMG stands out by combining VIX, Credit Spreads, and SPY/TLT into a single, cohesive indicator. Its unique strength lies in its fully consistent scores across all timeframes, a critical feature for multi-timeframe analysis.

Purpose: To empower traders with a clear, actionable tool to:

Assess macro conditions

Spot market extremes

Anticipate reversals

__________________________________________________________________________________

How It Works

__________________________________________________________________________________

VIX Z-Score: Measures volatility deviations (inverted for bearish signals).

Credit Z-Score: Tracks credit spread deviations (inverted for bearish signals).

Ratio Z-Score: Assesses SPY/TLT strength (positively weighted for bullish signals).

TMG Score: Weighted composite of z-scores (bullish > +0.30, bearish < -0.30).

Anomaly Detection: Identifies extreme volatility spikes (z-score > 3.0).

All calculations are performed using daily data, ensuring that scores remain consistent across all chart timeframes.

__________________________________________________________________________________

Visualization & Interpretation

__________________________________________________________________________________

The script visualizes data through:

A dynamic table displaying TMG Score , VIX Z, Credit Z, Ratio Z, and Anomaly status, with color gradients (green for positive, red for negative, gray for neutral/N/A).

A plotted TMG Score in Area, Histogram, or Line mode , with adaptive opacity for clarity.

Bull/Bear thresholds as horizontal lines (+0.30/-0.30) to signal market conditions.

Anomaly markers (orange circles) for volatility spikes.

Crossover signals (triangles) for bull/bear threshold crossings.

The table provides an immediate snapshot of macro conditions, while the plot offers a visual trend analysis. All values are consistent across timeframes, simplifying multi-timeframe analysis.

__________________________________________________________________________________

Script Parameters

__________________________________________________________________________________

Extensive customization options:

Symbol Selection: Customize VIX, Credit Spreads, SPY, TLT symbols

Core Parameters: Adjust lookback periods, weights, smoothing

Anomaly Detection: Enable/disable with custom thresholds

Visual Style: Choose display modes and colors

__________________________________________________________________________________

Conclusion

__________________________________________________________________________________

The Triad Macro Gauge by Ox_kali is a cutting-edge tool for analyzing macroeconomic trends. By integrating VIX, Credit Spreads, and SPY/TLT, TMG provides traders with a clear, consistent, and actionable gauge of market sentiment.

Recommended for: Swing traders and long-term investors seeking to navigate macro-driven markets.

__________________________________________________________________________________

Credit & Inspiration

__________________________________________________________________________________

Special thanks to Caleb Franzen for his pioneering work on macroeconomic indicator blends – his research directly inspired the core framework of this tool.

__________________________________________________________________________________

Notes & Disclaimer

__________________________________________________________________________________

This is the initial public release (v2.5.9). Future updates may include additional features based on user feedback.

Please note that the Triad Macro Gauge is not a guarantee of future market performance and should be used with proper risk management. Past performance is not indicative of future results.

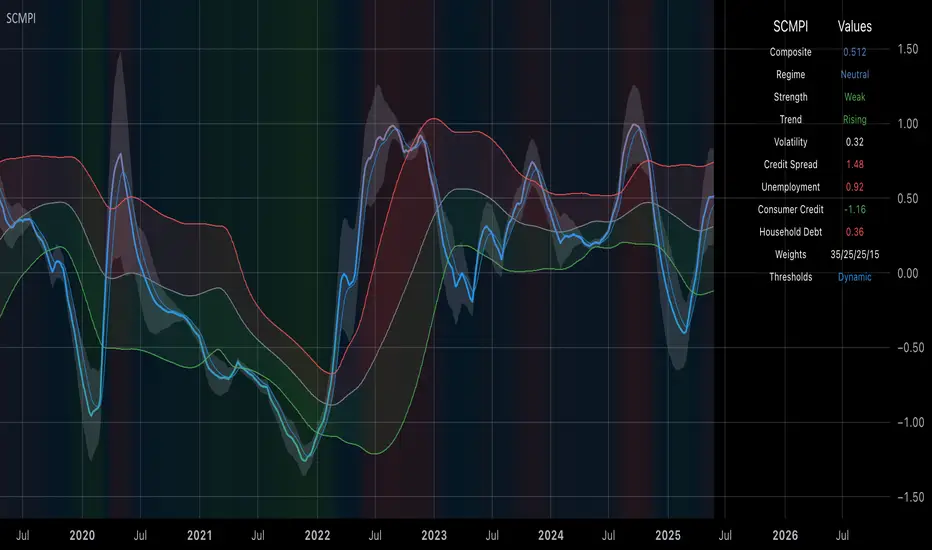

Systemic Credit Market Pressure IndexSystemic Credit Market Pressure Index (SCMPI): A Composite Indicator for Credit Cycle Analysis

The Systemic Credit Market Pressure Index (SCMPI) represents a novel composite indicator designed to quantify systemic stress within credit markets through the integration of multiple macroeconomic variables. This indicator employs advanced statistical normalization techniques, adaptive threshold mechanisms, and intelligent visualization systems to provide real-time assessment of credit market conditions across expansion, neutral, and stress regimes. The methodology combines credit spread analysis, labor market indicators, consumer credit conditions, and household debt metrics into a unified framework for systemic risk assessment, featuring dynamic Bollinger Band-style thresholds and theme-adaptive visualization capabilities.

## 1. Introduction

Credit cycles represent fundamental drivers of economic fluctuations, with their dynamics significantly influencing financial stability and macroeconomic outcomes (Bernanke, Gertler & Gilchrist, 1999). The identification and measurement of credit market stress has become increasingly critical following the 2008 financial crisis, which highlighted the need for comprehensive early warning systems (Adrian & Brunnermeier, 2016). Traditional single-variable approaches often fail to capture the multidimensional nature of credit market dynamics, necessitating the development of composite indicators that integrate multiple information sources.

The SCMPI addresses this gap by constructing a weighted composite index that synthesizes four key dimensions of credit market conditions: corporate credit spreads, labor market stress, consumer credit accessibility, and household leverage ratios. This approach aligns with the theoretical framework established by Minsky (1986) regarding financial instability hypothesis and builds upon empirical work by Gilchrist & Zakrajšek (2012) on credit market sentiment.

## 2. Theoretical Framework

### 2.1 Credit Cycle Theory

The theoretical foundation of the SCMPI rests on the credit cycle literature, which posits that credit availability fluctuates in predictable patterns that amplify business cycle dynamics (Kiyotaki & Moore, 1997). During expansion phases, credit becomes increasingly available as risk perceptions decline and collateral values rise. Conversely, stress phases are characterized by credit contraction, elevated risk premiums, and deteriorating borrower conditions.

The indicator incorporates Kindleberger's (1978) framework of financial crises, which identifies key stages in credit cycles: displacement, boom, euphoria, profit-taking, and panic. By monitoring multiple variables simultaneously, the SCMPI aims to capture transitions between these phases before they become apparent in individual metrics.

### 2.2 Systemic Risk Measurement

Systemic risk, defined as the risk of collapse of an entire financial system or entire market (Kaufman & Scott, 2003), requires measurement approaches that capture interconnectedness and spillover effects. The SCMPI follows the methodology established by Bisias et al. (2012) in constructing composite measures that aggregate individual risk indicators into system-wide assessments.

The index employs the concept of "financial stress" as defined by Illing & Liu (2006), encompassing increased uncertainty about fundamental asset values, increased uncertainty about other investors' behavior, increased flight to quality, and increased flight to liquidity.

## 3. Methodology

### 3.1 Component Variables

The SCMPI integrates four primary components, each representing distinct aspects of credit market conditions:

#### 3.1.1 Credit Spreads (BAA-10Y Treasury)

Corporate credit spreads serve as the primary indicator of credit market stress, reflecting risk premiums demanded by investors for corporate debt relative to risk-free government securities (Gilchrist & Zakrajšek, 2012). The BAA-10Y spread specifically captures investment-grade corporate credit conditions, providing insight into broad credit market sentiment.

#### 3.1.2 Unemployment Rate

Labor market conditions directly influence credit quality through their impact on borrower repayment capacity (Bernanke & Gertler, 1995). Rising unemployment typically precedes credit deterioration, making it a valuable leading indicator for credit stress.

#### 3.1.3 Consumer Credit Rates

Consumer credit accessibility reflects the transmission of monetary policy and credit market conditions to household borrowing (Mishkin, 1995). Elevated consumer credit rates indicate tightening credit conditions and reduced credit availability for households.

#### 3.1.4 Household Debt Service Ratio

Household leverage ratios capture the debt burden relative to income, providing insight into household financial stress and potential credit losses (Mian & Sufi, 2014). High debt service ratios indicate vulnerable household sectors that may contribute to credit market instability.

### 3.2 Statistical Methodology

#### 3.2.1 Z-Score Normalization

Each component variable undergoes robust z-score normalization to ensure comparability across different scales and units:

Z_i,t = (X_i,t - μ_i) / σ_i

Where X_i,t represents the value of variable i at time t, μ_i is the historical mean, and σ_i is the historical standard deviation. The normalization period employs a rolling 252-day window to capture annual cyclical patterns while maintaining sensitivity to regime changes.

#### 3.2.2 Adaptive Smoothing

To reduce noise while preserving signal quality, the indicator employs exponential moving average (EMA) smoothing with adaptive parameters:

EMA_t = α × Z_t + (1-α) × EMA_{t-1}

Where α = 2/(n+1) and n represents the smoothing period (default: 63 days).

#### 3.2.3 Weighted Aggregation

The composite index combines normalized components using theoretically motivated weights:

SCMPI_t = w_1×Z_spread,t + w_2×Z_unemployment,t + w_3×Z_consumer,t + w_4×Z_debt,t

Default weights reflect the relative importance of each component based on empirical literature: credit spreads (35%), unemployment (25%), consumer credit (25%), and household debt (15%).

### 3.3 Dynamic Threshold Mechanism

Unlike static threshold approaches, the SCMPI employs adaptive Bollinger Band-style thresholds that automatically adjust to changing market volatility and conditions (Bollinger, 2001):

Expansion Threshold = μ_SCMPI - k × σ_SCMPI

Stress Threshold = μ_SCMPI + k × σ_SCMPI

Neutral Line = μ_SCMPI

Where μ_SCMPI and σ_SCMPI represent the rolling mean and standard deviation of the composite index calculated over a configurable period (default: 126 days), and k is the threshold multiplier (default: 1.0). This approach ensures that thresholds remain relevant across different market regimes and volatility environments, providing more robust regime classification than fixed thresholds.

### 3.4 Visualization and User Interface

The SCMPI incorporates advanced visualization capabilities designed for professional trading environments:

#### 3.4.1 Adaptive Theme System

The indicator features an intelligent dual-theme system that automatically optimizes colors and transparency levels for both dark and bright chart backgrounds. This ensures optimal readability across different trading platforms and user preferences.

#### 3.4.2 Customizable Visual Elements

Users can customize all visual aspects including:

- Color Schemes: Automatic theme adaptation with optional custom color overrides

- Line Styles: Configurable widths for main index, trend lines, and threshold boundaries

- Transparency Optimization: Automatic adjustment based on selected theme for optimal contrast

- Dynamic Zones: Color-coded regime areas with adaptive transparency

#### 3.4.3 Professional Data Table

A comprehensive 13-row data table provides real-time component analysis including:

- Composite index value and regime classification

- Individual component z-scores with color-coded stress indicators

- Trend direction and signal strength assessment

- Dynamic threshold status and volatility metrics

- Component weight distribution for transparency

## 4. Regime Classification

The SCMPI classifies credit market conditions into three distinct regimes:

### 4.1 Expansion Regime (SCMPI < Expansion Threshold)

Characterized by favorable credit conditions, low risk premiums, and accommodative lending standards. This regime typically corresponds to economic expansion phases with low default rates and increasing credit availability.

### 4.2 Neutral Regime (Expansion Threshold ≤ SCMPI ≤ Stress Threshold)

Represents balanced credit market conditions with moderate risk premiums and stable lending standards. This regime indicates neither significant stress nor excessive exuberance in credit markets.

### 4.3 Stress Regime (SCMPI > Stress Threshold)

Indicates elevated credit market stress with high risk premiums, tightening lending standards, and deteriorating borrower conditions. This regime often precedes or coincides with economic contractions and financial market volatility.

## 5. Technical Implementation and Features

### 5.1 Alert System

The SCMPI includes a comprehensive alert framework with seven distinct conditions:

- Regime Transitions: Expansion, Neutral, and Stress phase entries

- Extreme Conditions: Values exceeding ±2.0 standard deviations

- Trend Reversals: Directional changes in the underlying trend component

### 5.2 Performance Optimization

The indicator employs several optimization techniques:

- Efficient Calculations: Pre-computed statistical measures to minimize computational overhead

- Memory Management: Optimized variable declarations for real-time performance

- Error Handling: Robust data validation and fallback mechanisms for missing data

## 6. Empirical Validation

### 6.1 Historical Performance

Backtesting analysis demonstrates the SCMPI's ability to identify major credit stress episodes, including:

- The 2008 Financial Crisis

- The 2020 COVID-19 pandemic market disruption

- Various regional banking crises

- European sovereign debt crisis (2010-2012)

### 6.2 Leading Indicator Properties

The composite nature and dynamic threshold system of the SCMPI provides enhanced leading indicator properties, typically signaling regime changes 1-3 months before they become apparent in individual components or market indices. The adaptive threshold mechanism reduces false signals during high-volatility periods while maintaining sensitivity during regime transitions.

## 7. Applications and Limitations

### 7.1 Applications

- Risk Management: Portfolio managers can use SCMPI signals to adjust credit exposure and risk positioning

- Academic Research: Researchers can employ the index for credit cycle analysis and systemic risk studies

- Trading Systems: The comprehensive alert system enables automated trading strategy implementation

- Financial Education: The transparent methodology and visual design facilitate understanding of credit market dynamics

### 7.2 Limitations

- Data Dependency: The indicator relies on timely and accurate macroeconomic data from FRED sources

- Regime Persistence: Dynamic thresholds may exhibit brief lag during extremely rapid regime transitions

- Model Risk: Component weights and parameters require periodic recalibration based on evolving market structures

- Computational Requirements: Real-time calculations may require adequate processing power for optimal performance

## References

Adrian, T. & Brunnermeier, M.K. (2016). CoVaR. *American Economic Review*, 106(7), 1705-1741.

Bernanke, B. & Gertler, M. (1995). Inside the black box: the credit channel of monetary policy transmission. *Journal of Economic Perspectives*, 9(4), 27-48.

Bernanke, B., Gertler, M. & Gilchrist, S. (1999). The financial accelerator in a quantitative business cycle framework. *Handbook of Macroeconomics*, 1, 1341-1393.

Bisias, D., Flood, M., Lo, A.W. & Valavanis, S. (2012). A survey of systemic risk analytics. *Annual Review of Financial Economics*, 4(1), 255-296.

Bollinger, J. (2001). *Bollinger on Bollinger Bands*. McGraw-Hill Education.

Gilchrist, S. & Zakrajšek, E. (2012). Credit spreads and business cycle fluctuations. *American Economic Review*, 102(4), 1692-1720.

Illing, M. & Liu, Y. (2006). Measuring financial stress in a developed country: An application to Canada. *Journal of Financial Stability*, 2(3), 243-265.

Kaufman, G.G. & Scott, K.E. (2003). What is systemic risk, and do bank regulators retard or contribute to it? *The Independent Review*, 7(3), 371-391.

Kindleberger, C.P. (1978). *Manias, Panics and Crashes: A History of Financial Crises*. Basic Books.

Kiyotaki, N. & Moore, J. (1997). Credit cycles. *Journal of Political Economy*, 105(2), 211-248.

Mian, A. & Sufi, A. (2014). What explains the 2007–2009 drop in employment? *Econometrica*, 82(6), 2197-2223.

Minsky, H.P. (1986). *Stabilizing an Unstable Economy*. Yale University Press.

Mishkin, F.S. (1995). Symposium on the monetary transmission mechanism. *Journal of Economic Perspectives*, 9(4), 3-10.

Equity Risk PremiumInspired by the article "2020's Best Performing Hedge Fund Warns Of 'Incredible Move' Around The Election" from ZeroHedge:

This script explores the relationship and attempts to find dislocation between equity risk (VIX) and high-yield corporate debt risk (VXHYG, The Cboe VXHYG Index is an estimate of the expected 30-day volatility of the return on iShares' High Yield Grade ETF (HYG). VXHYG is derived by applying the VIX algorithm to options on HYG).

The basic logic is (closing price of VIX / closing price of VXHYG) - 1. When equity risk is high and credit risk is low, the value of premium will be high, and vice-versa.

“'Equity volatility is almost inescapably high. Is that a good form of insurance? The payoff profiles are nothing like they were back in January. Whereas in credit, we’re almost back to where we were in January.

I find today the risk-reward profile of credit to be basically among the worst, relative to other things, I’ve seen in my career,' Weinstein said. 'A VIX at 20 used to be quite a feat. Here we are at 30, and the credit market hasn’t blinked.'

As a result of the gaping divergence between the VIX and credit spreads - the two had moved in tandem for years, but in August the two series blew out as the VIX started rising as spreads kept falling - Weinstein has pounced on the trade, betting on vol compression."

When equity risk premium is high, the market may be forming a local top.

When equity risk premium is low, the market may be forming a local bottom.

Make sure to select your current timeframe on the dropdown menu.

GX Credit Spread SignalThe GX Credit Spread Signal is an advanced indicator designed for traders who trade options strategies on the SPX index, especially using vertical credit spreads. It combines traditional technical analysis with volatility and option pricing concepts to provide relevant signals and projections on the chart.

Main features:

Trend analysis: Uses opening gap, position relative to VWAP and simple moving average (SMA 50) to indicate bullish or bearish bias right after the first 15-minute candle.

Safe range projection: Calculates a range based on the ATR (Average True Range) multiplied by a safety factor, suggesting potential strikes for credit spreads.

Quantitative estimates:

Calculates the estimated delta of options via the Black-Scholes formula approximation.

Estimated probability of expiring out of the money (OTM).

Chart visualizations: Displays projected ATR lines, previous day's levels (high, low, close) and an informative panel with strikes, delta, OTM probability, ATR and VWAP data.

Configurable alerts: Notifications for detected bullish or bearish bias, helping the trader to identify opportunities quickly.

This indicator is ideal for those who day trade with SPX options, facilitating decision-making by combining technical analysis, volatility and option probabilities in one place.

Deviation Back Tester (Great for Credit Spreads)!Error with math fixed in this one. Please use this one.

This is great for credit spreads! Lets say you wanted to know if you had sold a 15% OTM Bull Put vertical 2 months out, how often would you win? This Turns green if you would have been correct with your credit spread had it expired on that date, or red if you would've been wrong. Great for Back testing!

This could also be used for ATM debit spreads credit spreads etc. Example, how often does SPY deviate outside a 10% range relative to two months, 5% (if your doing straddles perhaps) etc.

This Can be used with any stock.

PLEASE KEEP IN MIND THAT IT TESTS DEVIATION IN BOTH DIRECTIONS. THEREFORE IT WILL HIGHLIGHT RED ON BOTH THE UPSIDE AND DOWNSIDE. WHEN BACKTESTING BE SURE TO CHECK WHETHER IT IS RED BECAUSE OF DOWNSIDE OR UPSIDE.

Xiaolai(Sean)Chen_Credit Creation DegreeM2/M1 money stock value is the reflection of the degree of credit created which was mentioned by Ray Dalio in his 30 min video "How the Market and Economic Machines Work"

Credit degree will finally decrease in the Long-Term Debt circle.

Midnight Range Standard DeviationsCredit to Lex Fx for the basic framework of this script

This indicator is designed to assist traders in identifying potential trading opportunities based on the Intraday Concurrency Technique (ICT) concepts, specifically the midnight range deviations and their relationship to Fibonacci levels. It builds upon the work of Lex-FX, whom we gratefully acknowledge for the original concept and inspiration for this indicator.

Core Concept: ICT Midnight Range

The core of this indicator revolves around the concept of the midnight range. According to ICT, the high and low formed in a specific time window (typically the first 30 minutes after midnight, New York Time) can serve as a key reference point for intraday price action. The indicator identifies this range and projects potential support and resistance levels based on deviations from this range, combined with Fibonacci ratios.

How ICT Uses Midnight Range Deviations

ICT methodology often involves looking for price to move away from the initial midnight range, then return to it, or deviate beyond it, as key areas for potential entries.

Range Identification: The indicator automatically identifies the high and low of the midnight range (00:00 - 00:30 NY Time).

Deviation Levels: The indicator calculates and displays deviation levels based on multiples of the initial midnight range. These levels are often used to identify potential areas of support and resistance, as well as potential targets for price movement. These levels can be set in the additional fib levels section, which can be configured in increments of .5 deviations all the way up to 12 deviations.

Fibonacci Confluence: ICT often emphasizes the confluence of multiple factors. This indicator adds Fibonacci levels to the midnight range deviations. This allows traders to identify areas where Fibonacci retracements or extensions align with the deviation levels, potentially creating stronger areas of support or resistance.

Looking for Sweeps: ICT often uses these levels to look for times that the high and low are swept as potential areas of liquidity, indicating the start of potential continuations.

Time-Based Analysis: The time at which price interacts with these levels can also be significant in ICT. The indicator provides options to extend the range lines to specific times (e.g., 3 hours, 6 hours, 10 hours, 12 hours, or a custom defined time) after midnight, allowing traders to focus on specific periods of the trading day.

Indicator Settings Explained:

Time Zone (TZ): Defines the time zone used for calculating the midnight range. The default is "America/New_York".

Range High Color, Range Low Color, Range Mid Color: Customize the colors of the high, low, and mid-range lines.

Range Fill Color: Sets the fill color for the area between the range high and low.

Line Style: Choose the style of the range lines (solid, dashed, dotted).

Range Line Thickness: Adjust the thickness of the range lines for better visibility.

Show Fibonacci Levels: Enable or disable the display of Fibonacci deviation levels.

Fib Up Color, Fib Down Color: Customize the colors of the Fibonacci levels above (up) and below (down) the midnight range.

Show Trendline: Enables a trendline that plots the close price, colored according to whether the price is above the high, below the low, or within the midnight range.

Show Range Lines, Show Range Labels: Toggles the visibility of the range lines and their associated labels.

Label Size: Adjust the size of the labels for better readability.

Hide Prices: Option to display only the deviation values on labels, hiding price values.

Place Fibonacci Labels on Left Side: Option to switch label position from right side to left side.

Extend Range To (Hours from Midnight): This section gives you a wide variety of options on how far you want to extend the range to, you can do 3,6,10,12, and 23 hours. Alternatively, you can select the "Use Custom Length" and set a specific time in hours.

Additional Fib Levels: This section allows the trader to set additional deviation points in increments of .5 deviations from .5 all the way up to 12 deviations

TradingView Community Guidelines Compliance:

This indicator description adheres to the TradingView community guidelines by:

Being educational: It explains the ICT methodology and how the indicator can be used in trading.

Being transparent: It clearly describes all the indicator's settings and their purpose.

Providing credit: It acknowledges Lex-FX as the original author of the concept.

Avoiding misleading claims: It does not guarantee profits or imply that the indicator is a "holy grail."

Disclaimer: Usage of this indicator and the information provided is at your own risk. The author is not responsible for any losses incurred as a result of using this indicator.

Important Considerations:

This indicator is intended for educational purposes and to assist in applying the ICT methodology.

It should not be used as a standalone trading system.

Always combine this indicator with other forms of technical analysis and risk management techniques.

Backtest thoroughly on your chosen market and timeframe before using in live trading.

Trading involves risk. Only trade with capital you can afford to lose.

Elastic Buy-Sell Volume Wighted SupertrendCredits: This uses Trading View's buy and sell volume script and the Super trend script.

Elastic Buy-Sell Volume Wighted Supertrend can be used like a traditional supertrend indicator however we do not have to arbitrarily choose a multiplier depending on the stock and time frame the code dynamically adjust the multiplier and this is described below.

The buy and sell ATR (Average True Range) play a crucial role in determining the levels for potential buy and sell signals in the market. These ATR values are calculated based on volume-weighted averages, providing insights into the strength of buying and selling pressures. By incorporating volume into the ATR calculation, the indicator can better adapt to market dynamics, as volume often reflects the intensity of price movements. Instead of using Volume as whole this uses up and down volume derived from lower time frames which is used to calculate buy and sell ATR.

The multiplier is a key factor in the Supertrend calculation, which adjusts the width of the trend bands. The multiplier in this indicator dynamically adjusts itself based on two key components: the ratio of the asset's Average True Range (ATR) to that of a broader market benchmark and the coefficient of variation (CV) of the True Range (TR). The ratio comparison provides a historical context of the asset's volatility relative to the wider market over a longer time frame, while the CV accounts for short-term fluctuations in volatility.

By comparing the asset's ATR to that of the benchmark, traders gain insights into the asset's historical volatility behavior. A higher multiplier suggests that the asset's volatility has historically exceeded that of the benchmark, indicating potentially larger price movements compared to the broader market. Conversely, a lower multiplier suggests the opposite.

The CV component measures short-term variability in the asset's volatility, ensuring that the multiplier adapts to both long-term trends and short-term fluctuations. This combined approach enables traders to make informed decisions, considering both historical volatility relative to the broader market and short-term variability. Ultimately, the dynamic multiplier enhances traders' ability to adjust their strategies effectively across various market conditions.

Overall, the use of buy and sell ATR, along with a dynamically adjusted multiplier, enhances the indicator's ability to identify trend directions and to use a dynamic stop loss level.

Whale Momentum Wave Oscillator//Credits: @Noldo - Whale Trading System @rumpypumpydumpy - ALMA Ribbons @QuantNomad - Elastic Volume Weighted Moving Average

Composite Indicator, created by taking QuantNomad's EVWMA and using that as input for a variation of rumpypumpydumpy's ALMA Ribbons. Each Ribbon had its sub ribbons summed up and then averaged. The averages were then fed through the ta.rsi and the ta.mom functions giving us our momentum waves. Signal line created from the close value being fed through the ta. ema into the ta.rsi then ta.wma then ta.mom function. Why those in that order? No reason in particular just what I stumbled upon after many variations. I then overlayed Noldo's Whale Trading System to view what "whales" were doing, giving us a good view of when capital is flowing into and out the asset which often contradicts the momentum waves prior to trend changes. Provides a nice visual for how capital is moving along with momentum. Can see when smart money is buying up a big dip or of they seem to still be waiting on the sidelines.

Fibonacci Zone Study w/Candles - R3c0nTraderCredits:

Thank you "eykpunter" for granting me permission to use "Fibonacci Zones" to create this study

What does this do? How is it different?

This study was created so it can be used with the strategy 'Fibonacci Zone DCA Strategy - R3c0nTrader' in order to generate buy/sell signals for a 3Commas bot.

I was not able to use "eykpunter's" "Fibonacci Zones" to create these signals as it was missing the code for this. To create the buy or sell signal you need to be able to create an alert for when the price moves through the Fib levels. Unfortunately, the "price" is not available to be selected when creating an alert with the original study. Hence the need to create this new study and to resolve the issue.

This study has overlay turned off by default so it will appear in a separate pane below your active chart. I did this so I can clearly view and separate the strategy from the study.

Steps Overview:

Add the study to your chart

Configure the study to match the Fib length you used in the strategy.

Create Alerts from the study to generate the buy or sell signals to 3Commas

The below steps for creating signals are just examples! Since there are numerous ways you can open or close a trade from a signal, please do your own testing. This cannot be understated.

Example of how to generate buy signals:

After adding the study, select the three dots for this study and click on "Add an alert on Fibonacci Zone Study /w Candles…"

Setup the condition to trigger the alert. If you want to initiate a buy when the price crosses over the top of the lower Fib zone (downtrend zone), then use the following:

Condition>Fibonacci Zone Study>Price High>Crossing Up>Fibonacci Zone Study>Top-Low Fib Border

Options>Once per bar

Expiration>Open-ended

Alert actions>Webhook URL (use the 3Commas webhook URL)

Alert name>Enter a name, "BUY Paper-Fib-Bot"

Message>Use the 3Commas message from the paper bot to open the trade

Example of how to generate sell signals:

After adding the study, select the three dots for this study and click on "Add an alert on Fibonacci Zone Study /w Candles…"

Setup the condition to trigger the alert. If you want to initiate a sell when the price reaches the top of the High Fib zone (uptrend zone), then try the following:

Condition>Fibonacci Zone Study>Price High>Crossing Up>Fibonacci Zone Study>Top-High Fib Border

(Note: I used "Crossing Up" but "Crossing" is another option; I just haven't tested it yet with a paper bot)

Options>Once per bar

Expiration>Open-ended

Alert actions>Webhook URL (use the 3Commas webhook URL)

Alert name>Enter a name, "SELL Paper-Fib-Bot"

Message>Use the 3Commas message from the paper bot to close the trade

Fibonacci Zone DCA Strategy - R3c0nTraderCredits:

Thank you "eykpunter" for granting me permission to use "Fibonacci Zones" to create this strategy

Thank you "junyou0424" for granting me permission to use "DCA Bot with SuperTrend Emulator" which I used for adding bot inputs, calculations, and strategy

Pre-requisites:

You can use this script without a 3Commas account and see how 3Commas DCA Bot would perform. However, I highly recommend signing up for their free account, going through their training, and testing this strategy with a paper bot. This would give you a base understanding of the settings you will see in this strategy and why you will need to know them.

What can this do?

First off, this is a Long only strategy as I wrote it with DCA in mind. It cannot be used for shorting. Shorting defeats the purpose of a DCA bot which has a goal that is Long a position not Short a position. If you want to short, there are plenty of free scripts out there that do this.

I created this script out of curiosity and I wanted to see how a strategy based on “Fibonacci” levels would work with a 3Commas DCA bot. I came across "eykpunter’s" "Fibonacci Zones" study and in TradingView and I found it to be a very interesting concept. The "Fib Zones" in his study are basically a "Donchian Channel" of 4 Fibonacci lines. These are the High @ 0.236, Center High @ 0.382, Center Low @ 0.618, and Low @ 0.764.

The Fib Zones in this strategy can be used as conditions to open a trade as well as closing a trade. There is also the option to close a trade based on a Target Take Profit (%).

Advanced Fibonacci trading is also supported by specifying additional parameters for Trade Entry and Exit.

For example, for order entry, you can increase the minimum trend strength to open an order via the "minimum ADX value" option. You can also further limit order entry by selecting the option to "Only open trades on bullish +DI" (Positive Directional Index).

Or you can play the contrarian. For example, I would look for "buying the dip" opportunities by doing the following under "Trade Entry Settings":

Set the "Min ADX value to open trade" to zero

Set the option "Open a trade when the price moves" to "1-To the bottom of Downtrend Fib zone" or "2-Higher than the top of the Downtrend Fib zone"

Uncheck option "Only open trades on bullish +DI"

Set the 'Min ADX value to open trade' to Zero

Set the 'Max +DI value to open trade' to a value between 10-20.

For Trade Exit settings, I can use a "Target Take Profit (%)" or one of the High Fib levels to close the trade.

Here's an example result when using a Contrarian-Fibonacci-Zone-DCA strategy:

Explanation of Chart lines and colors on chart

Six Options for Entering a Fibonacci Trade

Open a trade when the price moves:

1-To the bottom of Downtrend Fib zone

2-Higher than the top of the Downtrend Fib zone

3-Higher than the bottom of Ranging Fib Zone

4-Higher than the top of Ranging Fib Zone

5-Higher than the bottom of Uptrend Fib Zone

6-To the top of Uptrend Fib Zone

Three Options for Exiting a Fibonacci Trade

Take profit using:

"Target Take Profit (%)"

"High Fibonacci Border-1"

"High Fibonacci Border-2"

Ranged Volume Study - R3c0nTraderCredits:

Thank you "EvoCrypto" for granting me permission to use "Ranged Volume" to create this version of it.

What is this and What does this do?

This study shows the ranged volume, and it can be used to produce buy signals for a 3Commas bot.

What’s different about this script?

I added code so that negative volume has its own color settings and lower opacity than the positive volume.

I changed the color scheme from Yellow, Red, Green, and Black to Yellow, Red, Light Blue, and Dark Blue.

How to Use

1. On the “Inputs” tab:

a. Set your “Volume Range Length” (number of bars to look back)

b. “Heikin Ashi” – Usually I leave this enabled. Make sure this matches what you have in your strategy!

c. “Show Bar Colors” – Leave disabled. Let the Strategy script color the bars in the price chart.

d. “Show Break-Out” – Leave enabled. Highlights the volume breakout in yellow and breakdowns in red.

e. “Show Range” – Leave enabled

TTM Squeeze Pro BarsCredits:

-> John Carter creating the TTM Squeeze and TTM Squeeze Pro

-> Lazybear's original interpretation of the TTM Squeeze: Squeeze Momentum Indicator

-> Makit0's evolution of Lazybear's script to factor in the TTM Squeeze Pro upgrades - Squeeze PRO Arrows

This is my version of their collective works, with amendments primarily to the Squeeze Conditions to more accurately reflect the color coding used by the official TMM Squeeze Pro indicator.

Rather than having a separate indicator window, the TTM Squeeze Pro is now overlaid on the price bars for easier viewing.

For those unfamiliar with the TTM Squeeze, it is simply a visual way of seeing how Bollinger Bands (standard deviations from a simple moving average ) relate to Keltner Channels ( average true range bands) compared with the momentum of the price action. The concept is that as Bollinger Bands compress within Keltner Channels , price volatility decreases, giving way for a potential explosive price movement up or down.

Differences between the original TTM Squeeze and TTM Squeeze Pro:

-> Both use a 2 standard deviation Bollinger Band ;

-> The original squeeze only used a 1.5 ATR Keltner Channel; and

-> The pro version uses 1.0, 1.5 and 2.0 ATR Keltner Channels .

The pro version therefore helps differentiate between levels of squeeze (compression) as the Bollinger Bands moves through the Keltner Channels i.e. the greater the compression, the more potential for explosive moves - less compression means more squeezing.

The Histogram shows price momentum whereas the colored dots (along the zeroline) show where the Bollinger Bands are in relation to the Keltner Channels:

-> Cyan Bars = positive, increasing momentum;

-> Blue Bars = positive, decreasing momentum (indication of a reversal in price direction);

-> Red Bars = negative, increasing momentum;

-> Yellow Bars = negative, decreasing momentum (indication of a reversal in price direction);

-> Orange Dots = High Compression / large squeeze (One or both of the Bollinger Bands is inside the 1st (1.0 ATR) Keltner Channel);

-> Red Dots = Medium Squeeze (One or both of the Bollinger Bands is inside the 2nd (1.5 ATR) Keltner Channel);

-> Black Dots = Low compression / wide squeeze (One or both of the Bollinger Bands is inside the 3rd (2.0 ATR) Keltner Channels );

-> Green Dots = No Squeeze / Squeeze Fired (One or both of the Bollinger Bands is outside of the 3rd (2.0 ATR) Keltner Channel).

Ideal Scenario:

As the ticker enters the squeeze, black dots would warn of the beginning of a low compression squeeze. As the Bollinger bands continue to constrict within the Keltner Channels , red dots would highlight a medium compression. As the price action and momentum continues to compress an orange dot shows warning of high compression. As price action leaves the squeeze, the coloring would reverse e.g. orange to red to black to green. Any compression squeeze is considered fired at the first green dot that appears.

Note: This is an ideal progression of the different types of squeezes, however any type of squeeze (and color sequence) may appear at anytime, therefore the focus is primarily on the green dots after any type of compression.

Entry and Exit Guide:

-> John Carter recommends entering a position after at least 5 black dots or wait for 1st green dot ; and

-> Exit on second blue or yellow bar or, alternatively, remain in the position after confirming a continuing trend through a separate indicator.

TTM Squeeze ProCredits:

-> John Carter creating the TTM Squeeze and TTM Squeeze Pro

-> Lazybear's original interpretation of the TTM Squeeze: Squeeze Momentum Indicator

-> Makit0's evolution of Lazybear's script to factor in the TTM Squeeze Pro upgrades - Squeeze PRO Arrows

This is my version of their collective works, with amendments primarily to the Squeeze Conditions to more accurately reflect the color coding used by the official TMM Squeeze Pro indicator.

For those unfamiliar with the TTM Squeeze, it is simply a visual way of seeing how Bollinger Bands (standard deviations from a simple moving average ) relate to Keltner Channels (average true range bands) compared with the momentum of the price action. The concept is that as Bollinger Bands compress within Keltner Channels, price volatility decreases, giving way for a potential explosive price movement up or down.

Differences between the original TTM Squeeze and TTM Squeeze Pro:

-> Both use a 2 standard deviation Bollinger Band ;

-> The original squeeze only used a 1.5 ATR Keltner Channel; and

-> The pro version uses 1.0, 1.5 and 2.0 ATR Keltner Channels .

The pro version therefore helps differentiate between levels of squeeze (compression) as the Bollinger Bands moves through the Keltner Channels i.e. the greater the compression, the more potential for explosive moves - less compression means more squeezing.

The Histogram shows price momentum whereas the colored dots (along the zeroline) show where the Bollinger Bands are in relation to the Keltner Channels:

-> Cyan Bars = positive, increasing momentum;

-> Blue Bars = positive, decreasing momentum (indication of a reversal in price direction);

-> Red Bars = negative, increasing momentum;

-> Yellow Bars = negative, decreasing momentum (indication of a reversal in price direction);

-> Orange Dots = High Compression / large squeeze (One or both of the Bollinger Bands is inside the 1st (1.0 ATR) Keltner Channel);

-> Red Dots = Medium Squeeze (One or both of the Bollinger Bands is inside the 2nd (1.5 ATR) Keltner Channel);

-> Black Dots = Low compression / wide squeeze (One or both of the Bollinger Bands is inside the 3rd (2.0 ATR) Keltner Channels );

-> Green Dots = No Squeeze / Squeeze Fired (One or both of the Bollinger Bands is outside of the 3rd (2.0 ATR) Keltner Channel).

Ideal Scenario:

As the ticker enters the squeeze, black dots would warn of the beginning of a low compression squeeze. As the Bollinger bands continue to constrict within the Keltner Channels , red dots would highlight a medium compression. As the price action and momentum continues to compress an orange dot shows warning of high compression. As price action leaves the squeeze, the coloring would reverse e.g. orange to red to black to green. Any compression squeeze is considered fired at the first green dot that appears.

Note: This is an ideal progression of the different types of squeezes, however any type of squeeze (and color sequence) may appear at anytime, therefore the focus is primarily on the green dots after any type of compression.

Entry and Exit Guide:

-> John Carter recommends entering a position after at least 5 black dots or wait for 1st green dot ; and

-> Exit on second blue or yellow bar or, alternatively, remain in the position after confirming a continuing trend through a separate indicator.

Multi VWAP for Wick HunterCredit: honeybadgermakesfunnymoney for this Open Source Script

Published:

This is a tool that will allow you to visualize Wick Hunter's calcation of VWAP. Wick Hunter uses this calcuation for its Liqudations Bots.

There are four settings that you need to be configured to visualize your VWAP Band:

Long VWAP - The distance from current VWAP price, in %, that price must be UNDER when a liquidation event occurs to meet your you VWAP condition. The higher the value, the more price must move below the current VWAP price for it to enter a LONG position.

Short VWAP - The distance from current VWAP price, in %, that price must be ABOVE when a liquidation event occurs to meet your you VWAP condition. The higher the value, the more price must move above the current VWAP price for it to enter a SHORT position.

VWAP Timeframe - Select the timeframe you want the VWAP to be measured on.

VWAP Periods: Input the time period over which you want the VWAP to be measured over. For example, if you use "5" for this and "15" for VWAP Timeframe. The VWAP will be calculated based on the last five 15 minute candles.

You can play around with these settings using the indicator provide above. The indicator will print a triangle when the conditon for VWAP is met for a long for short trade. Play around with these settings. A few good timeframes that are popular are 5 minute, 15 minute, and one hour (60 minute). As far as periods, the most common settings are between 5 periods and 15 periods. In general the lower the timeframe and periods and closer VWAP will follow price.

Kirk65 UTBot Strategy FixedCredits to @HPotter for the orginal code.

Credits to @Yo_adriiiiaan for recently publishing the UT Bot study based on the original code.

Credits to @TradersAITradingPlans for making UT Bot strategy.

Strategy fixed with time period by Kirk65.

UT Bot works great with 2 hour time frame with Heikin Ashi, but riskier. Use "Once per bar" In alerts with 1.5% stoploss. If the price goes against Alerts, stoploss will save your assets. Wait until next Alert.

4 hour time frame is less risky and less profitable.

Happy trading..

Kirk65

TradersAI_UTBotCREDITS to @HPotter for the orginal code.

CREDITS to @Yo_adriiiiaan for recently publishing the UT Bot study based on the original code -

I just added some simple code to turn it into a strategy. Now, anyone can simply add the strategy to their chart to see the backtesting results!

While @Yo_adriiiiaan mentions it works best on a 4-hour timeframe or above, I am happy to share that this seems to be working on a 15-minute chart on e-mini S&P 500 Index (using the KeyValue setting at 10)! You can play around with the different settings, and may be you might discover even better settings.

Hope this helps. Btw, if any of you play with different settings and discover great settings for a specific instrument, please share them with the community here - it will be rewarded back multiple times!

[LanZhu] - MTF MAs CrossoverCredited to ChrisMoody's script ==> _CM_Ultimate_MA_MTF_V4 :)

I have modified a bit his indicator to include more MTF fast MA and slow MA crossover. I have added table to show MTF bullish and bearish status. Fast MA above Slow MA is considered Bullish and vice versa

Kindly refer to chart to see explanation of this indicator. Hopefully you guys will enjoy :)

RSI + Stochastic Alert with Advanced Doji ConfirmationCredits to Ahmed Alasfoor and Somou by Zakariya Hamad AlJulandani