Bitcoin Power Law OscillatorThis is the oscillator version of the script. The main body of the script can be found here.

Understanding the Bitcoin Power Law Model

Also called the Long-Term Bitcoin Power Law Model. The Bitcoin Power Law model tries to capture and predict Bitcoin's price growth over time. It assumes that Bitcoin's price follows an exponential growth pattern, where the price increases over time according to a mathematical relationship.

By fitting a power law to historical data, the model creates a trend line that represents this growth. It then generates additional parallel lines (support and resistance lines) to show potential price boundaries, helping to visualize where Bitcoin’s price could move within certain ranges.

In simple terms, the model helps us understand Bitcoin's general growth trajectory and provides a framework to visualize how its price could behave over the long term.

The Bitcoin Power Law has the following function:

Power Law = 10^(a + b * log10(d))

Consisting of the following parameters:

a: Power Law Intercept (default: -17.668).

b: Power Law Slope (default: 5.926).

d: Number of days since a reference point(calculated by counting bars from the reference point with an offset).

Explanation of the a and b parameters:

Roughly explained, the optimal values for the a and b parameters are determined through a process of linear regression on a log-log scale (after applying a logarithmic transformation to both the x and y axes). On this log-log scale, the power law relationship becomes linear, making it possible to apply linear regression. The best fit for the regression is then evaluated using metrics like the R-squared value, residual error analysis, and visual inspection. This process can be quite complex and is beyond the scope of this post.

Applying vertical shifts to generate the other lines:

Once the initial power-law is created, additional lines are generated by applying a vertical shift. This shift is achieved by adding a specific number of days (or years in case of this script) to the d-parameter. This creates new lines perfectly parallel to the initial power law with an added vertical shift, maintaining the same slope and intercept.

In the case of this script, shifts are made by adding +365 days, +2 * 365 days, +3 * 365 days, +4 * 365 days, and +5 * 365 days, effectively introducing one to five years of shifts. This results in a total of six Power Law lines, as outlined below (From lowest to highest):

Base Power Law Line (no shift)

1-year shifted line

2-year shifted line

3-year shifted line

4-year shifted line

5-year shifted line

The six power law lines:

Bitcoin Power Law Oscillator

This publication also includes the oscillator version of the Bitcoin Power Law. This version applies a logarithmic transformation to the price, Base Power Law Line, and 5-year shifted line using the formula: log10(x) .

The log-transformed price is then normalized using min-max normalization relative to the log-transformed Base Power Law Line and 5-year shifted line with the formula:

normalized price = log(close) - log(Base Power Law Line) / log(5-year shifted line) - log(Base Power Law Line)

Finally, the normalized price was multiplied by 5 to map its value between 0 and 5, aligning with the shifted lines.

Interpretation of the Bitcoin Power Law Model:

The shifted Power Law lines provide a framework for predicting Bitcoin's future price movements based on historical trends. These lines are created by applying a vertical shift to the initial Power Law line, with each shifted line representing a future time frame (e.g., 1 year, 2 years, 3 years, etc.).

By analyzing these shifted lines, users can make predictions about minimum price levels at specific future dates. For example, the 5-year shifted line will act as the main support level for Bitcoin’s price in 5 years, meaning that Bitcoin’s price should not fall below this line, ensuring that Bitcoin will be valued at least at this level by that time. Similarly, the 2-year shifted line will serve as the support line for Bitcoin's price in 2 years, establishing that the price should not drop below this line within that time frame.

On the other hand, the 5-year shifted line also functions as an absolute resistance , meaning Bitcoin's price will not exceed this line prior to the 5-year mark. This provides a prediction that Bitcoin cannot reach certain price levels before a specific date. For example, the price of Bitcoin is unlikely to reach $100,000 before 2021, and it will not exceed this price before the 5-year shifted line becomes relevant. After 2028, however, the price is predicted to never fall below $100,000, thanks to the support established by the shifted lines.

In essence, the shifted Power Law lines offer a way to predict both the minimum price levels that Bitcoin will hit by certain dates and the earliest dates by which certain price points will be reached. These lines help frame Bitcoin's potential future price range, offering insight into long-term price behavior and providing a guide for investors and analysts. Lets examine some examples:

Example 1:

In Example 1 it can be seen that point A on the 5-year shifted line acts as major resistance . Also it can be seen that 5 years later this price level now corresponds to the Base Power Law Line and acts as a major support at point B(Note: Vertical yearly grid lines have been added for this purpose👍).

Example 2:

In Example 2, the price level at point C on the 3-year shifted line becomes a major support three years later at point D, now aligning with the Base Power Law Line.

Finally, let's explore some future price predictions, as this script provides projections on the weekly timeframe :

Example 3:

In Example 3, the Bitcoin Power Law indicates that Bitcoin's price cannot surpass approximately $808K before 2030 as can be seen at point E, while also ensuring it will be at least $224K by then (point F).

在腳本中搜尋"THE SCRIPT"

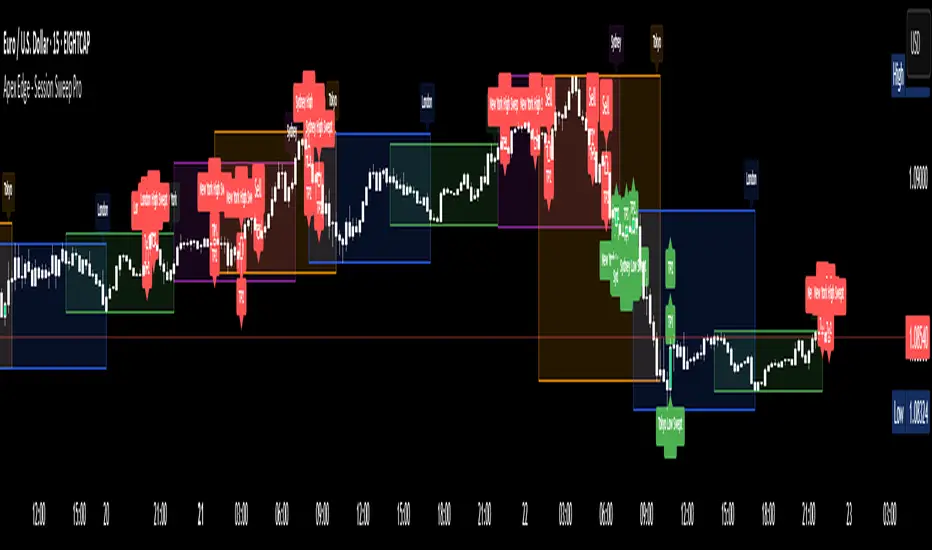

Apex Edge - Session Sweep ProApex Edge Session Sweep Pro

By Apex Edge | 2025 Edition

🔍 What is it?

The Apex Session Sweep Pro is a precision trading tool designed for identifying high-probability liquidity sweep entries during key global market sessions. It combines powerful sweep detection logic with dynamic candle colouring, session visualization, TP projections, and real-time alerts — all within a clean, performance-optimized Pine Script engine.

This is not your average session box indicator. This is Apex-grade.

⚙️ How it Works

The indicator detects session liquidity sweeps by tracking price action relative to previous session highs and lows. When a session high/low is swept (i.e., price breaches it and then closes in the opposite direction), it generates a signal:

Buy Signal → Price sweeps previous low and closes back above it

Sell Signal → Price sweeps previous high and closes back below it

Each session is boxed on the chart (Tokyo, London, New York, Sydney), color-coded, and dynamically labelled.

Upon detecting a valid sweep, the script:

Plots a small entry label (toggleable)

Projects up to 5 customizable TP levels

Coloured candles for visual trade direction

Alerts for Buy or Sell sweep signals (optional)

All elements are memory-managed and customizable to suit your trading style.

🧠 Key Features

✅ Smart Sweep Detection Logic

✅ Global Market Session Boxes (Custom Times)

✅ Toggleable Entry Labels + TP Levels

✅ Candle Colouring by Signal

✅ Manual TP input + TP toggles

✅ Real-time Alerts for Apex entries

🕒 Why Are My Sessions Offset?

Your chart’s time zone may be different from UTC. This script is UTC-based by design, so if your chart is set to UTC+1, for example, the sessions will appear one hour later. Either:

Adjust your chart to UTC or or Exchange for perfect alignment,

Or tweak the session input times manually.

🧰 Who is this for?

This tool is made for:

Intraday traders looking for sweeps into liquidity

SMC (Smart Money Concept) strategists

Forex, crypto, and indices traders

Anyone who uses session-based levels to define entries

Whether you scalp London or ride NY swings, this tool frames each session cleanly — and shows you where the traps are laid.

🚨 Disclaimer

This indicator is a technical tool, not financial advice. Use proper risk management. Past performance ≠ future results.

ICT Swiftedge# ICT SwiftEdge: Advanced Market Structure Trading System

**Overview**

ICT SwiftEdge is a powerful trading system built upon the foundation of ICTProTools' ICT Breakers, licensed under the Mozilla Public License 2.0 (mozilla.org). This script has been significantly enhanced by to combine market structure analysis with modern technical indicators and a sleek, AI-inspired statistics dashboard. The goal is to provide traders with a comprehensive tool for identifying high-probability trade setups, managing exits, and tracking performance in a visually intuitive way.

**Credits**

This script is a derivative work based on the original "ICT Breakers" by ICTProTools, used with permission under the Mozilla Public License 2.0. Significant enhancements, including RSI-MA signals, trend filtering, dynamic timeframe adjustments, dual exit strategies, and an AI-style statistics dashboard, were developed by . We express our gratitude to ICTProTools for their foundational work in market structure analysis.

**What It Does**

ICT SwiftEdge integrates multiple trading concepts to help traders identify and manage trades based on market structure and momentum:

- **Market Structure Analysis**: Identifies Break of Structure (BOS) and Market Structure Shift (MSS) patterns, which signal potential trend continuations or reversals. BOS indicates a continuation of the current trend, while MSS highlights a shift in market direction, providing key entry points.

- **RSI-MA Signals**: Generates "BUY" and "SELL" signals when BOS or MSS patterns align with the Relative Strength Index (RSI) smoothed by a Moving Average (RSI-MA). Signals are filtered to occur only when RSI-MA is above 50 (for buys) or below 50 (for sells), ensuring momentum supports the trade direction.

- **Trend Filtering**: Prevents multiple signals in the same trend, ensuring only one buy or sell signal per trend direction, reducing noise and improving trade clarity.

- **Dynamic Timeframe Adjustment**: Automatically adjusts pivot points, RSI, and MA parameters based on the selected chart timeframe (1M to 1D), optimizing performance across different market conditions.

- **Flexible Exit Strategies**: Offers two user-selectable exit methods:

- **Trailing Stop-Loss (TSL)**: Exits trades when price moves against the position by a user-defined distance (in points), locking in profits or limiting losses.

- **RSI-MA Exit**: Exits trades when RSI-MA crosses the 50 level, signaling a potential loss of momentum.

- Users can enable either or both strategies, providing flexibility to adapt to different trading styles.

- **AI-Style Statistics Dashboard**: Displays real-time trade performance metrics in a futuristic, neon-colored interface, including total trades, wins, losses, win/loss ratio, and win percentage. This helps traders evaluate the system's effectiveness without external tools.

**Why This Combination?**

The integration of these components creates a synergistic trading system:

- **BOS/MSS and RSI-MA**: Combining market structure breaks with RSI-MA ensures entries are based on both price action (structure) and momentum (RSI-MA), increasing the likelihood of high-probability trades.

- **Trend Filtering**: By limiting signals to one per trend, the system avoids overtrading and focuses on significant market moves.

- **Dynamic Adjustments**: Timeframe-specific parameters make the system versatile, suitable for scalping (1M, 5M) or swing trading (4H, 1D).

- **Dual Exit Strategies**: TSL protects profits during trending markets, while RSI-MA exits are ideal for range-bound or reversing markets, catering to diverse market conditions.

- **Statistics Dashboard**: Provides immediate feedback on trade performance, enabling data-driven decision-making without manual tracking.

This combination balances technical precision with user-friendly visuals, making it accessible to both novice and experienced traders.

**How to Use**

1. **Add to Chart**: Apply the script to any TradingView chart.

2. **Configure Settings**:

- **Chart Timeframe**: Select your chart's timeframe (1M to 1D) to optimize parameters.

- **Structure Timeframe**: Choose a timeframe for market structure analysis (leave blank for chart timeframe).

- **Exit Strategy**: Enable Trailing Stop-Loss (`useTslExit`), RSI-MA Exit (`useRsiMaExit`), or both. Adjust `tslPoints` for TSL distance.

- **Show Signals/Labels**: Toggle `showSignals` and `showExit` to display "BUY", "SELL", and "EXIT" labels.

- **Dashboard**: Enable `showDashboard` to view trade statistics. Customize colors with `dashboardBgColor` and `dashboardTextColor`.

3. **Trading**:

- Look for "BUY" or "SELL" labels to enter trades when BOS/MSS aligns with RSI-MA.

- Exit trades at "EXIT" labels based on your chosen strategy.

- Monitor the statistics dashboard to track performance (total trades, win/loss ratio, win percentage).

4. **Alerts**: Set up alerts for BOS, MSS, buy, sell, or exit signals using the provided alert conditions.

**License**

This script is licensed under the Mozilla Public License 2.0 (mozilla.org). The source code is available for review and modification under the terms of this license.

**Compliance with TradingView House Rules**

This publication adheres to TradingView's House Rules and Scripts Publication Rules. It provides a clear, self-contained description of the script's functionality, credits the original author (ICTProTools), and explains the rationale for combining indicators. The script contains no promotional content, offensive language, or proprietary restrictions beyond MPL 2.0.

**Note**

Trading involves risk, and past performance is not indicative of future results. Always backtest and validate the system on your preferred markets and timeframes before live trading.

Enjoy trading with ICT SwiftEdge, and let data-driven insights guide your decisions!

Liquidity Fracture DetectorThe Liquidity Fracture Detector is an advanced tool designed to identify micro-liquidity traps and structural fakeouts on intraday charts. These occur when the market appears to break out, only to quickly reverse — often triggered by stop hunts, inefficient fills, or manipulated order flow.

The script combines volume spikes, volatility anomalies, and price structure breaks to signal "fractures" — points where the market temporarily breaks its behavior, often followed by strong reversals or trend accelerations.

Detection logic in the script:

Volume spike greater than 2x the average (adjustable)

Volatility spike: candle range is > 1.5x the average

Extreme wicks: wick is larger than the candle body (a classic trap signal)

Structure break: price breaks previous high/low but closes back within the old range

Combine these elements → a “fracture” is marked

Visual representation:

Red background = potential bull trap (fake breakout to the upside)

Green background = potential bear trap (fake breakdown to the downside)

A label appears at each fracture: “Echo” with the number of previous hits

Ideal use cases:

Intraday trading (1m, 5m, 15m)

Crypto, indices, futures, and forex

Detecting reactive zones where the market takes a false direction

Confluence with S/R zones, order blocks, or liquidity pools

Fully customizable:

Volume and range sensitivity

Heatmap intensity

Toggle labels on/off

Note:

This script is intended to support discretionary analysis. It does not provide buy or sell signals and is not an automated strategy. Combine it with your own price action or order flow setup for optimal results.

Autofib Extensions | DTDHello trader comuunity!

I'm introducing another script that is part of my main day-trading strategy. We all know regardless of what strategy we use, we need to know what levels offer the least amount of risk to our trade entry and a great tool to anticipate how far a move might go or what level a move may retrace to are the Fibonacci Retracement and Extensions. This indicator combines both together, but with a twist.

The main elements of the script are:

1. Multiple Session High and Lows | Developing my first script led me to understand that measuring key times during each session provides understanding of the market's continuity. I have provided 3 "sessions' a user can define according to CST time where the script saves the high and low of that session window to produce the retracement and extensions from those plots. Currently, the levels are always plotted from low to high (with the 0 mark being the high) and negative values provided so the levels are consistent. You can toggle each session on or off.

2. Coloring Key Retracements / Extensions | I use a dark background for my charts so the default colors help me distinguish from other another indicator I use. Feel free to adjust the colors to your preference. I consider 3 different colors because of their significance. Retracements that you want to see continue fall back into the .50 to .618 level (this I consider the "Golden Zone"). While basic Elliott Wave Theory states a wave is completed near the 1.618 level (this I consider "Major Extensions"). Everything isn't noise, but minor levels in a larger sequence.

______________

Script Limitations

All of my scripts are made with the help of ChatGPT so there are going to be limitations. One current one that I have made progress on, but not fully is when you are viewing a timeframe where the candle doesn't start when a session window starts. On smaller timeframes like the 7-minute this is not an issue. However, on the hourly, if your session window starts at the half hour which the 3rd session default window does, the lines will not produce. I will hopefully have this rectified in the near future. I will open the script since none of this work is original in nature and I would love to see how others can create a better product. Also, this is mainly a futures trading tool. If you are using this on stocks you will find it not as useful if the session window is too wide since the script waits until the session window closes to calculate the extension values.

Cheers,

DTD

VNIndex Over 6.5% Downside Drop Indicator with TableOverview: The VNIndex 6.5% Downside Drop Indicator is a powerful tool designed to help traders and investors identify significant market drops on the VNIndex (or any other asset) based on a 6.5% downside threshold. This Pine Script® indicator automatically detects when the price of an asset drops by more than 6.5% within a single day, and visually marks those events on the chart.

Key Features:

6.5% Downside Drop Detection: Automatically calculates the daily percentage drop and identifies when the price falls by more than 6.5%.

Table Display: Displays the dates and corresponding percentage drops of all identified instances in a convenient table at the bottom right of the chart.

Markers: Red down-pointing markers are plotted above bars where the price drop exceeds the 6.5% threshold, making it easy to spot critical drop events at a glance.

Easy-to-Read Table: The table lists the date and drop percentage, updating dynamically as new drops are detected. This allows for easy tracking of significant downside moves over time.

How to Use:

Install the Script: Add this indicator to your TradingView chart.

Monitor Price Drops: The indicator will automatically detect when the price drops by over 6.5% from the previous close and display a marker on the chart and the table in the bottom right corner.

View the Table: The table displays the date and the percentage drop of each detected event, making it easy to track past significant moves.

Alerts: You can set an alert for 6.5% drops to receive notifications in real-time.

Customization Options:

The drop percentage threshold (6.5%) can be adjusted in the script to fit other market conditions or assets.

The table can be resized or styled based on user preference for better visibility.

Why Use This Indicator? This indicator is perfect for traders looking to spot large, significant price movements quickly. Large downside drops can signal potential market reversals or trading opportunities, and this tool helps you track such events effortlessly. Whether you're monitoring the VNIndex or any other asset, this indicator provides crucial insights into volatile price action, helping you make more informed decisions.

Open Source License: This indicator is open source and free to use under the Mozilla Public License 2.0. You are welcome to modify, distribute, and contribute to the project.

Contributions: Feel free to contribute improvements, fixes, or new features by creating a pull request. Let’s collaborate to make this indicator even better for the community!

Mogwai Method with RSI and EMA - BTCUSD 15mThis is a custom TradingView indicator designed for trading Bitcoin (BTCUSD) on a 15-minute timeframe. It’s based on the Mogwai Method—a mean-reversion strategy—enhanced with the Relative Strength Index (RSI) for momentum confirmation. The indicator generates buy and sell signals, visualized as green and red triangle arrows on the chart, to help identify potential entry and exit points in the volatile cryptocurrency market.

Components

Bollinger Bands (BB):

Purpose: Identifies overextended price movements, signaling potential reversions to the mean.

Parameters:

Length: 20 periods (standard for mean-reversion).

Multiplier: 2.2 (slightly wider than the default 2.0 to suit BTCUSD’s volatility).

Role:

Buy signal when price drops below the lower band (oversold).

Sell signal when price rises above the upper band (overbought).

Relative Strength Index (RSI):

Purpose: Confirms momentum to filter out false signals from Bollinger Bands.

Parameters:

Length: 14 periods (classic setting, effective for crypto).

Overbought Level: 70 (price may be overextended upward).

Oversold Level: 30 (price may be overextended downward).

Role:

Buy signal requires RSI < 30 (oversold).

Sell signal requires RSI > 70 (overbought).

Exponential Moving Averages (EMAs) (Plotted but not currently in signal logic):

Purpose: Provides trend context (included in the script for visualization, optional for signal filtering).

Parameters:

Fast EMA: 9 periods (short-term trend).

Slow EMA: 50 periods (longer-term trend).

Role: Can be re-added to filter signals (e.g., buy only when Fast EMA > Slow EMA).

Signals (Triangles):

Buy Signal: Green upward triangle below the bar when price is below the lower Bollinger Band and RSI is below 30.

Sell Signal: Red downward triangle above the bar when price is above the upper Bollinger Band and RSI is above 70.

How It Works

The indicator combines Bollinger Bands and RSI to spot mean-reversion opportunities:

Buy Condition: Price breaks below the lower Bollinger Band (indicating oversold conditions), and RSI confirms this with a reading below 30.

Sell Condition: Price breaks above the upper Bollinger Band (indicating overbought conditions), and RSI confirms this with a reading above 70.

The strategy assumes that extreme price movements in BTCUSD will often revert to the mean, especially in choppy or ranging markets.

Visual Elements

Green Upward Triangles: Appear below the candlestick to indicate a buy signal.

Red Downward Triangles: Appear above the candlestick to indicate a sell signal.

Bollinger Bands: Gray lines (upper, middle, lower) plotted for reference.

EMAs: Blue (Fast) and Orange (Slow) lines for trend visualization.

How to Use the Indicator

Setup

Open TradingView:

Log into TradingView and select a BTCUSD chart from a supported exchange (e.g., Binance, Coinbase, Bitfinex).

Set Timeframe:

Switch the chart to a 15-minute timeframe (15m).

Add the Indicator:

Open the Pine Editor (bottom panel in TradingView).

Copy and paste the script provided.

Click “Add to Chart” to apply it.

Verify Display:

You should see Bollinger Bands (gray), Fast EMA (blue), Slow EMA (orange), and buy/sell triangles when conditions are met.

Trading Guidelines

Buy Signal (Green Triangle Below Bar):

What It Means: Price is oversold, potentially ready to bounce back toward the Bollinger Band middle line.

Action:

Enter a long position (buy BTCUSD).

Set a take-profit near the middle Bollinger Band (bb_middle) or a resistance level.

Place a stop-loss 1-2% below the entry (or based on ATR, e.g., ta.atr(14) * 2).

Best Context: Works well in ranging markets; avoid during strong downtrends.

Sell Signal (Red Triangle Above Bar):

What It Means: Price is overbought, potentially ready to drop back toward the middle line.

Action:

Enter a short position (sell BTCUSD) or exit a long position.

Set a take-profit near the middle Bollinger Band or a support level.

Place a stop-loss 1-2% above the entry.

Best Context: Effective in ranging markets; avoid during strong uptrends.

Trend Filter (Optional):

To reduce false signals in trending markets, you can modify the script:

Add and ema_fast > ema_slow to the buy condition (only buy in uptrends).

Add and ema_fast < ema_slow to the sell condition (only sell in downtrends).

Check the Fast EMA (blue) vs. Slow EMA (orange) alignment visually.

Tips for BTCUSD on 15-Minute Charts

Volatility: BTCUSD can be erratic. If signals are too frequent, increase bb_mult (e.g., to 2.5) or adjust RSI levels (e.g., 75/25).

Confirmation: Use volume spikes or candlestick patterns (e.g., doji, engulfing) to confirm signals.

Time of Day: Mean-reversion works best during low-volume periods (e.g., Asian session in crypto).

Backtesting: Use TradingView’s Strategy Tester (convert to a strategy by adding entry/exit logic) to evaluate performance with historical BTCUSD data up to March 13, 2025.

Risk Management

Position Size: Risk no more than 1-2% of your account per trade.

Stop Losses: Always use stops to protect against BTCUSD’s sudden moves.

Avoid Overtrading: Wait for clear signals; don’t force trades in choppy or unclear conditions.

Example Scenario

Chart: BTCUSD, 15-minute timeframe.

Buy Signal: Price drops to $58,000, below the lower Bollinger Band, RSI at 28. A green triangle appears.

Action: Buy at $58,000, target $59,000 (middle BB), stop at $57,500.

Sell Signal: Price rises to $60,500, above the upper Bollinger Band, RSI at 72. A red triangle appears.

Action: Sell at $60,500, target $59,500 (middle BB), stop at $61,000.

This indicator is tailored for mean-reversion trading on BTCUSD. Let me know if you’d like to tweak it further (e.g., add filters, alerts, or alternative indicators)!

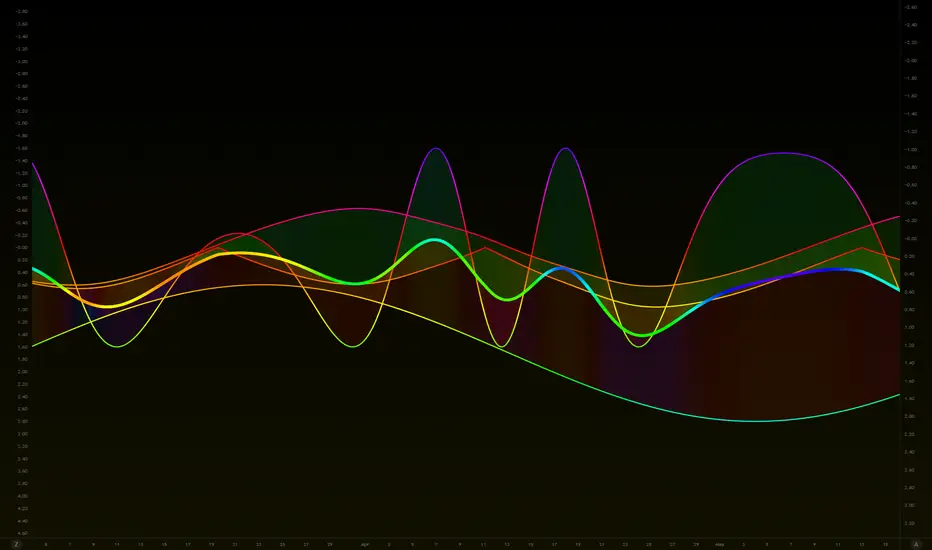

Wave Modulation Demo█ OVERVIEW

This script demonstrates Stacked Wave Modulation by visualizing four interconnected waves. Wave 1 is the base wave, influencing Wave 2's frequency, which in turn modulates Wave 3's amplitude, and finally, Wave 3 modulates Wave 4's phase. Explore the fascinating effects of wave modulation by adjusting the inputs for each wave and their modulation scales.

══════════════════════════════════════════════════

█ CONCEPTS

This script visualizes a cascade of wave modulations:

1 — Base Wave (Wave 1): This is the foundational wave. Its parameters (type, frequency, amplitude, phase, vertical shift) are directly controlled and serve as the basis for subsequent modulations.

2 — Frequency Modulation (Wave 2): Wave 2's frequency is modulated by Wave 1 . As Wave 1 oscillates, it dynamically changes the frequency of Wave 2 , creating interesting frequency variations. The Frequency Mod Scale input controls the intensity of this modulation.

3 — Amplitude Modulation (Wave 3): Building upon the cascade, Wave 3 's amplitude is modulated by Wave 2 . The peaks and troughs of Wave 2 influence the amplitude of Wave 3 , resulting in amplitude variations. The Amplitude Mod Scale input adjusts the strength of this amplitude modulation.

4 — Phase Modulation (Wave 4): Finally, Wave 4 's phase is modulated by Wave 3 . Wave 3 's oscillations shift the phase of Wave 4 , leading to phase-related distortions and dynamic wave patterns. The Phase Mod Scale input determines the extent of phase modulation.

5 — Stacked Wave (Average): The script calculates and plots the average of all four waves, providing a composite view of the combined modulation effects.

══════════════════════════════════════════════════

█ FEATURES

The script is organized into input groups for each wave, allowing for detailed customization:

1 — Wave 1: Base Wave

• Type : Select the waveform type for Wave 1 (Sine, Cosine, Triangle, Square).

• Frequency (Hz) : Sets the base frequency of Wave 1 in Hertz (cycles per second).

• Amplitude : Controls the vertical amplitude or height of Wave 1.

• Phase Shift (deg) : Adjusts the phase shift of Wave 1 in degrees, shifting the wave horizontally.

• Vertical Shift : Sets the vertical position of Wave 1 on the chart.

2 — Wave 2: Frequency Modulation

• Type : Select the waveform type for Wave 2.

• Base Frequency (Hz) : Sets the base frequency of Wave 2, before modulation.

• Amplitude : Controls the amplitude of Wave 2.

• Phase Shift (deg) : Adjusts the phase shift of Wave 2.

• Vertical Shift : Sets the vertical position of Wave 2.

• Frequency Mod Scale : Determines the degree to which Wave 1 modulates Wave 2's frequency. Higher values increase the modulation effect.

3 — Wave 3: Amplitude Modulation

• Type : Select the waveform type for Wave 3.

• Base Frequency (Hz) : Sets the base frequency of Wave 3.

• Amplitude : Controls the base amplitude of Wave 3, before modulation.

• Phase Shift (deg) : Adjusts the phase shift of Wave 3.

• Vertical Shift : Sets the vertical position of Wave 3.

• Amplitude Mod Scale : Determines the degree to which Wave 2 modulates Wave 3's amplitude. Higher values increase the modulation effect.

4 — Wave 4: Phase Modulation

• Type : Select the waveform type for Wave 4.

• Base Frequency (Hz) : Sets the base frequency of Wave 4.

• Amplitude : Controls the amplitude of Wave 4.

• Phase Shift (deg) : Sets the base phase shift of Wave 4, before modulation.

• Vertical Shift : Sets the vertical position of Wave 4.

• Phase Mod Scale : Determines the degree to which Wave 3 modulates Wave 4's phase. Higher values increase the modulation effect.

══════════════════════════════════════════════════

█ HOW TO USE

1. Add the "Stacked Wave Modulation Demo" script to your TradingView chart.

2. Explore the input settings. Each wave has its own group of customizable parameters.

3. Adjust the Type , Frequency , Amplitude , Phase Shift , and Vertical Shift for each wave to define their base characteristics.

4. Experiment with the modulation scales ( Frequency Mod Scale , Amplitude Mod Scale , Phase Mod Scale ) to control the intensity of the modulation effects between the waves.

5. Observe how the waves interact and how the modulations shape their forms and the final stacked wave (average).

══════════════════════════════════════════════════

█ NOTES

* This script utilizes the `waves` and `hsvColor` libraries. Look for other scripts on my profile.

* The frequencies are set in Hertz (cycles per second), which relate to bars on the chart. A frequency of 0.5 Hz means 0.5 cycles per bar, or 1 cycle every 2 bars.

* Adjusting the modulation scales allows you to fine-tune the visual impact of the modulation effects.

* The color of each wave plot is dynamically generated based on its value using the HSV color model for visual distinction.

* Feel free to modify and experiment with the script to create different modulation schemes or stacking methods.

Let me know if you have any other questions or would like further refinements!

Celestial Pair Spread Hello friends, after a very long time!

Today, I tried to put into code an idea that came to my mind spontaneously and suddenly.

Note :

This script is experimental and improvable.

I haven't had a chance to try it yet.

TIMEFRAME : 1D (Daily Bars)

CELESTIAL SPREAD

The spread moves in a very limited area and is consistent within itself, especially on days far from the end of the contract.

That's why there is a reassuring sky atmosphere. That's why this name was given completely improvised.

Basic logic of the script

We enter the name of the CME Futures contract we want to enter:

Ex : CL1! , ES1! , ZC1! , NQ1!

The script creates us a pair trade parity divided into secondary contracts.

Example : ES1!/ES2!

What is pair trading?

I will explain briefly here.

For users who are wondering:

www.investopedia.com

Let's get back to our topic.

Now we have created a parity that does not actually exist.

This parity is the manifestation of the relative movements of two contracts.

When the parity rises, ES1! increased,ES2! has fallen.

In the opposite case, We can say: ES1! Contract has been dropped ES2! has increased.

Pair trading is generally a trade that needs to be kept in mind from time to time.

It is a method preferred by professionals who can process very quickly.

Market risk is minimal, but since 2 contracts are purchased, more money is paid and very low percentage profits are made.

It is very expensive to do pair trading, especially with oil and its derivatives and interest security derivatives.

The contract we are considering has micros. (small-item contracts tied to the same value)

So when we switch to our broker MES1!/MES2! We will trade.

For all CME futures :

www.cmegroup.com

Anyway, let's continue:

The script created the parity showing its relationship with the next contract and plotted it as bars.

Celestial bands are just like Bollinger bands, but they consist of 3 bands based on percentage changes rather than standard deviation.

The middle band is obtained from moving averages.

The upper and lower bands are the middle band subjected to a threshold value.

The threshold value can be changed.

0.15 percent was charged for this script.

CAUTION :

As can be seen in the example below;

The most important thing is not to make any transactions when the contract switch dates are approaching.

Therefore, it is recommended to use it just below the main chart.

The blue bars in the parity are

Values that outside the upper and lower threshold values are colored blue.

For this condition

Alerts has been added.

Don't forget to add alert and edit.

MAIN PURPOSE

It is aimed to start a pair trade when such conditions come and to quickly close the trades when the parity basis reaches the value.

OTHER IMPORTANT POINTS

Other issues are broker related issues.

Difference between initial margins and maintanence margins of contracts (between 1! and 2!)

It shouldn't be too high.

The commission should not be too high.

Leverage must be high because the profit percentage is very low.

To calculate leverage you must divide your contract size by the relevant margin requirement.

Sample margin requirement table:

www.interactivebrokers.com

RISKS

It is an experimental and intellectual script,

the risk of contract price differences (maybe it will not leave a profit except for very extreme values)

I remind you of the quickness risk that comes from a two-legged trade.

Alerts definitely synchronized with an audible alert sent to a smartphone as an e-mail notification and displayed on the locked screen for quick action.

Best regards!

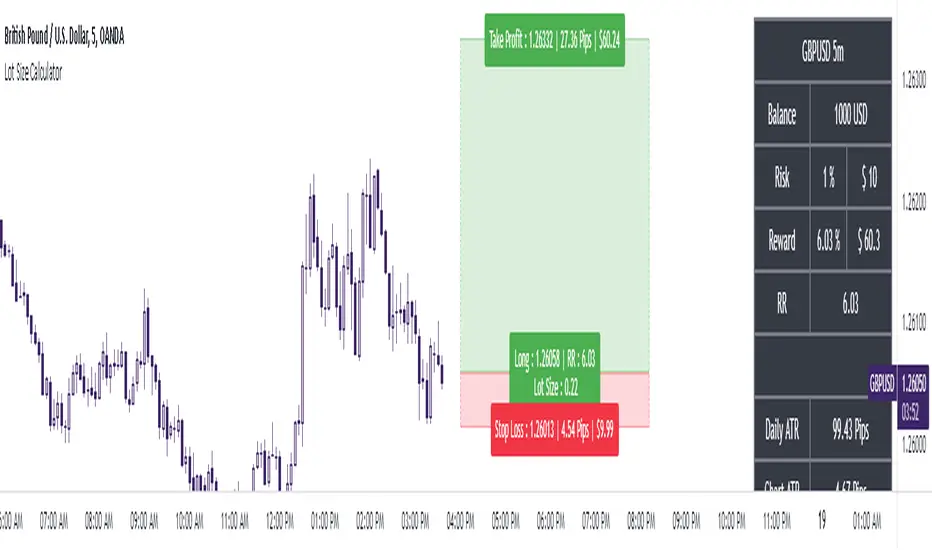

The Ultimate Lot Size Calculator Backstory

I created this Pine Script tool to calculate lot sizes with precision. While there are many lot size calculators available on TradingView, I found that most had significant flaws. I started teaching myself Pine Script over three and a half years ago with the sole purpose of building this tool. My first version was messy and lacked accuracy, so I never published it. I wanted it to be better than any other available tool, but my limited knowledge back then held me back.

Recently, I received a request to create a similar tool, as the current options still fail to deliver the precision and reliability traders need. This inspired me to revisit my original idea. With improved skills and a better understanding of Pine Script, I redesigned the tool from scratch, making it as precise, reliable, and efficient as possible.

This tool features built-in error detection to minimize mistakes and ensure accuracy in lot size calculations. I've spent more time on this project than on any other, focusing on delivering a solution that stands out on TradingView. While I plan to add more features based on user feedback, the current version is already a powerful, dependable, and easy-to-use tool for traders who value precision and efficiency in their lot size calculations.

How to use the tool ?

At first it might seem complicated, but it is quite easy to use the tool. There are two modes: auto and manual. By default, the tool is set on manual mode. When you apply the tool on the chart, it will ask you to choose the entry price, then the stop-loss price, and at last the take-profit price. Select all of them one by one. These values can be changed later.

Settings

There are various setting given for making the tool as flexible as possible. Here is the explanation for some of most important settings. Play with them and make yourself comfortable.

General settings

Auto mode : Use this mode if you want the the risk reward to be fixed and stop loss to be based on ATR. However the stop loss can be changed to be based on user input.

Manual mode : Use this mode if you want full control over entry, stop loss and take profit.

Contract Size : The tool works perfectly for all forex pairs including gold and silver but as the contract size is different for different assets it is difficult to add every single asset into the script manually so i have provided this option. In case you want to calculate lot size for a asset other then forex, gold or silver make sure to change this. Contract size = Quantity of the asset in 1 standerd lot.

Account settings

Automatic mode settings and ATR stop settings

Manual mode settings

Table and risk-reward box settings are pretty much self-explanatory i guess.

Error handling

A lot size calculator is a complex program. There are numerous points where it may fail and produce incorrect results. To make it robust and accurate, these issues must be addressed and managed properly, which practically all existing lot size calculator scripts fail to do.

Golden tip

When the symbol is changed it will display a symbol change warning as the entry, stop loss and take profit price won't change.

There are 2 ways to get fix this. Either manually enter all three values which i hate the most or remove the script from the chart and re-apply the script on chart again.

So to re-apply the indicator in most easy way follow the following instructions:

Note : If you encounter any other error then read the instruction to fix it and if it is an unknow error pleas report it to me in comments or DM.

RoGr75 - EMA 50/8 Cross With Buy/Sell Signals RoGr75 - EMA 50/8 Cross With Buy/Sell Signals

---

**Overview:**

This script is designed to generate **Buy** and **Sell** signals based on the crossover and crossunder of two Exponential Moving Averages (EMAs): **EMA 8** (green line) and **EMA 50** (blue line). The signals are plotted at a user-defined distance from the candles, ensuring clear visibility and adaptability to market volatility.

---

**Key Features:**

1. **EMA Cross Signals**:

- A **Buy Signal** is generated when the **EMA 8** crosses above the **EMA 50**.

- A **Sell Signal** is generated when the **EMA 8** crosses below the **EMA 50**.

2. **Variable Signal Distance**:

- The distance of the Buy and Sell signals from the candles is controlled by a **user-defined input** (`signal_distance`).

- The distance is calculated using the **Average True Range (ATR)** to adapt to market volatility.

3. **Customizable Parameters**:

- `signal_distance`: Adjust the distance of the signals from the candles (default: 2.0).

- ATR period: Fixed at 14 but can be modified in the script.

4. **Visual Enhancements**:

- Buy signals are displayed as green labels below the candles.

- Sell signals are displayed as red labels above the candles.

- Optional background highlighting for Buy and Sell signals.

---

**How It Works:**

- The script calculates the **EMA 8** and **EMA 50** and plots them on the chart.

- When a crossover or crossunder occurs, a label is placed at a distance determined by the formula:

- **Buy Signal Position**: `low - (signal_distance * ATR(14))`

- **Sell Signal Position**: `high + (signal_distance * ATR(14))`

- The signals are clearly visible and adapt to the volatility of the asset.

---

**Input Parameters:**

- `signal_distance` (type: input float): Controls the distance of the Buy and Sell signals from the candles. Default value is `2.0`.

---

**Usage:**

1. Add the script to your chart in TradingView.

2. Adjust the `signal_distance` input to set the desired distance of the signals from the candles.

3. Monitor the Buy and Sell signals generated by the script for potential trading opportunities.

---

**Example:**

- If `signal_distance` is set to `2.0`, the Buy signal will appear **2x ATR** below the candle's low, and the Sell signal will appear **2x ATR** above the candle's high.

---

**Customization:**

- Modify the ATR period or replace it with a fixed value for static distance.

- Adjust the colors, styles, and sizes of the labels and EMAs to suit your preferences.

---

**Ideal For:**

- Traders looking for a simple and effective EMA crossover strategy.

- Users who want customizable signal placement for better visibility.

- Those who prefer volatility-adjusted signal distances.

---

**Note:**

This script is for educational and informational purposes only. Always backtest and validate strategies before using them in live trading.

Donchian Reversal Scanner by Hitesh2603How It Works:

Bearish Side Logic:

If the price is falling with bearish candles and touching the lower Donchian Channel, the bearishCondition flag is set to true.

When a bullish candle appears afterward, the flag is reset, and the bullishReversalSquare condition becomes true.

Bullish Side Logic:

If the price is rising with bullish candles and touching the upper Donchian Channel, the bullishCondition flag is set to true.

When a bearish candle appears afterward, the flag is reset, and the bearishReversalSquare condition becomes true.

Plotting Squares:

A green square is plotted below the candle when bullishReversalSquare is true.

A red square is plotted above the candle when bearishReversalSquare is true.

Scanner Output:

The scanCondition variable is true when either bullishReversalSquare or bearishReversalSquare is true.

How to Use the Script:

On the Chart:

Add the script to your chart.

You will see squares plotted on the chart when the conditions are met:

Green squares below the candle for bullish reversals.

Red squares above the candle for bearish reversals.

In the Scanner:

Open the Scanner tab in TradingView.

Click on "Create New Scanner".

In the "Condition" field, select the script you just created.

Choose the market or watchlist you want to scan (e.g., "NYSE", "NASDAQ", or a custom watchlist).

Run the scan. The Scanner will return a list of instruments where the scanCondition is true.

Why This Works:

The scanCondition variable is now properly declared and used.

The plotchar function explicitly outputs the scanCondition variable as a plot, which the Scanner can recognize.

BTC-SPX Momentum Gauge + EMA SignalHere's an explanation of the market dynamics and signal benefits of this script:

Momentum and Sentiment Indicator:

The script uses the momentum of the S&P 500 to change the chart's background color, providing a quick visual cue of market sentiment. Green indicates potential bullish momentum in the broader market, while red suggests bearish momentum. This can help traders gauge overall market direction at a glance.

Bitcoin Trend Analysis:

By plotting the scaled TEMA of Bitcoin (BTC), traders can see how Bitcoin's trend correlates or diverges from the current asset being analyzed. Since Bitcoin is often viewed as a hedge against traditional financial systems or inflation, its trend can signal broader economic shifts or investor sentiment towards alternative investments.

Dual Trend Confirmation:

The script offers two trend lines: one for Bitcoin and one for the current ticker. When these lines move in tandem, it might indicate a strong market trend across both traditional and crypto markets. Divergence between these lines can highlight potential market anomalies or opportunities for arbitrage or hedging.

Smoothness vs. Reactivity:

The use of TEMA for Bitcoin provides a smoother signal than a simple moving average, reducing lag while still reacting to price changes. This can be particularly useful for identifying longer-term trends in Bitcoin's volatile market. The 20-period EMA for the current ticker, on the other hand, gives a quicker response to price changes in the asset you're directly trading.

Cross-Asset Correlation:

By overlaying Bitcoin's trend on another asset's chart, traders can analyze how these markets might influence each other. For instance, if Bitcoin is in an uptrend while a traditional asset is declining, it might suggest capital rotation into cryptocurrencies.

Trading Signals:

Crossovers or divergences between the TEMA of Bitcoin and the EMA of the current ticker could be used as signals for entry or exit points. For example, if the BTC TEMA crosses above the current ticker's EMA, it might suggest a shift towards crypto assets.

Risk Management:

The visual cues from the background color and moving averages can aid in risk management. For example, trading in the direction of the momentum indicated by the background color might be seen as going with the market flow, potentially reducing risk.

Macro-Economic Insights:

The relationship between Bitcoin and traditional markets can offer insights into macroeconomic conditions, particularly related to inflation, monetary policy, and investor sentiment towards fiat currencies.

Headwind and tailwind:

Currently BTC correlated trade instruments experience headwind or tailwind from the broader market. This indicator lets the user see it to help their trade decision process.

Additional Statement:

As the market realizes the dangers of the fiat that its construct is built upon and evolves and migrates into stable money, incorruptible by inflation, this indicator will reveal the external influence of that corruptible and the internal influence of the incorruptible; having diminishing returns as the rise of stable money overtakes the treasuries of the fiat construct.

MEMEQUANTMEMEQUANT

This script is a comprehensive and specialized tool designed for tracking trends and money flow within meme coins and DEX tokens. By combining various features such as trend lines, Fibonacci levels, and category-based indices, it helps traders make informed decisions in highly volatile markets.

Key Features:

1. Category-Based Indices:

• Tracks the performance of token categories like:

• AI Agent Tokens

• AI Tokens

• Animal Tokens

• Murad Picks

• Each category consists of leader tokens, which are selected based on their higher market cap and trading volume. These tokens act as benchmarks for their respective categories.

• Visualizes category indices in a line chart to identify trends and compare money flow between categories.

2. Fibonacci Correction Zones:

• Highlights key retracement levels (e.g., 60%, 70%, 80%).

• These levels are crucial for identifying potential reversal zones, commonly observed in meme coin trading patterns.

• Fully customizable to match individual trading strategies.

3. Trend Lines:

• Automatically detects major support and resistance levels.

• Separates long-term and short-term trend lines, allowing traders to focus on significant price movements.

4. Enhanced Info Table:

• Provides real-time insights, including:

• % Distance from All-Time High (ATH)

• Current Trading Volume

• 50-bar Average Volume

• Volume Change Percentage

• Displays information in an easy-to-read table on the chart.

5. Customizable Settings:

• Users can adjust transparency, colors, and ranges for Fibonacci zones, trend lines, and the table.

• Enables or disables individual features (e.g., Fibonacci, trend lines, table) based on preferences.

How It Works:

1. Tracking Money Flow Across Categories:

• The script calculates the market cap to volume ratio for each category of tokens to help identify the dominant trend.

• A higher ratio indicates greater liquidity and stability, while a lower ratio suggests higher volatility or price manipulation.

2. Identifying Retracement Patterns:

• Leverages common retracement behaviors (e.g., 70% correction levels) observed in meme coins to detect potential reversal zones.

• Combines this with trend line analysis for additional confirmation.

3. Leader Tokens as Indicators:

• Each category is represented by its leader tokens, which have historically higher liquidity and market cap. This allows the script to accurately reflect the overall trend in each category.

When to Use:

• Trend Analysis: To identify which category (e.g., AI Tokens or Animal Tokens) is leading the market.

• Reversal Zones: To spot potential support or resistance levels using Fibonacci zones.

• Money Flow: To understand how capital is moving across different token categories in real time.

Who Is This For?

This script is tailored for:

• Traders specializing in meme coins and DEX tokens.

• Those looking for an edge in trend-based trading by analyzing market cap, volume, and retracement levels.

• Anyone aiming to track money flow dynamics between different token categories.

Future Updates:

This is the initial version of the script. Future updates may include:

• Support for additional token categories and DEX data.

• More advanced pattern recognition and alerts for volume and price anomalies.

• Enhanced visualization for historical data trends.

With this tool, traders can combine money flow analysis with the 60-70% retracement strategy, turning it into a powerful assistant for navigating the fast-paced world of meme coins and DEX tokens.

This script is designed to provide meaningful insights and practical utility for traders, adhering to TradingView’s standards for originality, clarity, and user value.

Volume-MACD-RSI Integrated StrategyDescription:

This script integrates three well-known technical analysis tools—Volume, MACD, and RSI—into a single signal meant to help traders identify potential turning points under strong market conditions.

Concept Overview:

Volume Filter: We compare the current bar’s volume to a 20-period volume average and require it to exceed a specified multiplier. This ensures that signals occur only during periods of heightened market participation. The logic is that moves on low volume are less reliable, so we wait for increased activity to confirm potential trend changes.

MACD Momentum Shift:

We incorporate MACD crossovers to determine when momentum is changing direction. MACD is a popular momentum indicator that identifies shifts in trend by comparing short-term and long-term EMAs. A bullish crossover (MACD line crossing above the signal line) may suggest upward momentum is building, while a bearish crossunder can indicate momentum turning downward.

RSI Market Condition Check:

RSI helps us identify overbought or oversold conditions. By requiring that RSI be oversold on buy signals and overbought on sell signals, we attempt to pinpoint entries where price could be at an extreme. The idea is to position entries or exits at junctures where price may be due for a reversal.

How the Script Works Together:

Volume Confirmation: No signals fire unless there’s strong volume. This reduces false positives.

MACD Momentum Check: Once volume confirms market interest, MACD crossover events serve as a trigger to initiate consideration of a trade signal.

RSI Condition: Finally, RSI determines whether the market is at an extreme. This final layer helps ensure we only act on signals that have both momentum shift and a price at an extreme level, potentially increasing the reliability of signals.

Intended Use:

This script can help highlight potential reversal points or trend shifts during active market periods.

Traders can use these signals as a starting point for deeper analysis. For instance, a “BUY” arrow may prompt a trader to investigate the market context, confirm with other methods, or look for patterns that further support a long entry.

The script is best used on markets with reliable volume data, such as stocks or futures, and can be experimented with across different timeframes. Adjusting the RSI thresholds, MACD parameters, and volume multiplier can help tailor it to specific instruments or trading styles.

Chart Setup:

When adding this script to your chart, it should be the only indicator present, so you can clearly see the red “BUY” arrows and green “SELL” arrows at the candle closes where signals occur.

The chart should be kept clean and uncluttered for clarity. No other indicators are necessary since the logic is already integrated into this single script.

Coinbase Premium HeatmapCoinbase Premium Heatmap visualizes spot bitcoin premium (or discount) on Coinbase, relative to other spot markets, visualized as a heatmap overlay.

OPTIMIZED FOR CLARITY

Coinbase Premium can whipsaw quickly, with dramatic state changes over relatively brief periods, unnecessarily complicating its use (for our purposes).

To mitigate whipsaws, the script (a) averages premium/discount on an hourly basis, and (b) introduces lightweight exponential smoothing, to further simplify/clarify state.

WHY IT MATTERS

Spot Coinbase premium is a strong proxy for bullish institutional sentiment and net inflows/accumulation by western financial institutions, ETF providers, and corporations (like MicroStrategy) adding bitcoin to their treasury.

In aggregate, this holder cohort drives trend & sentiment more than any other, so it's important to know their directional bias.

HOW IT'S CALCULATED

Premium / discount calculates the spread between Coinbase spot BTC price, and spot price on Binance + Bybit. Calculation is averaged hourly, with light exponential smoothing.

HOW WE USE THE SCRIPT

When assessing optimal moments to hedge exposure (or sell spot assets) near a presumed impending cycle top, awareness of institutional sentiment is a crucial variable. This script:

(a) Filters out unnecessarily early cycle exit signals (if Coinbase premium is still present)

(b) Confirms other metrics that indicate an impending cycle top (if the neutral to bearish institutional sentiment we'd expect to see is in effect), and

(c) Visualizes state changes (from bearish to bullish & vice versa), that often make for good swing entries & exits on lower timeframes.

Market Stats Panel [Daveatt]█ Introduction

I've created a script that brings TradingView's watchlist stats panel functionality directly to your charts. This isn't just another performance indicator - it's a pixel-perfect (kidding) recreation of TradingView's native stats panel.

Important Notes

You might need to adjust manually the scaling the firs time you're using this script to display nicely all the elements.

█ Core Features

Performance Metrics

The panel displays key performance metrics (1W, 1M, 3M, 6M, YTD, 1Y) in real-time, with color-coded boxes (green for positive, red for negative) for instant performance assessment.

Display Modes

Switch seamlessly between absolute prices and percentage returns, making it easy to compare assets across different price scales.

Absolute mode

Percent mode

Historical Comparison

View year-over-year performance with color-coded lines, allowing for quick historical pattern recognition and analysis.

Data Structure Innovation

Let's talk about one of the most interesting challenges I faced. PineScript has this quirky limitation where request.security() can only return 127 tuples at most. £To work around this, I implemented a dual-request system. The first request handles indices 0-63, while the second one takes care of indices 64-127.

This approach lets us maintain extensive historical data without compromising script stability.

And here's the cool part: if you need to handle even more years of historical data, you can simply extend this pattern by adding more request.security() calls.

Each additional call can fetch another batch of monthly open prices and timestamps, following the same structure I've used.

Think of it as building with LEGO blocks - you can keep adding more pieces to extend your historical reach.

Flexible Date Range

Unlike many scripts that box you into specific timeframes, I've designed this one to be completely flexible with your date selection. You can set any start year, any end year, and the script will dynamically scale everything to match. The visual presentation automatically adjusts to whatever range you choose, ensuring your data is always displayed optimally.

█ Customization Options

Visual Settings

The panel's visual elements are highly customizable. You can adjust the panel width to perfectly fit your workspace, fine-tune the line thickness to match your preferences, and enjoy the pre-defined year color scheme that makes tracking historical performance intuitive and visually appealing.

Box Dimensions

Every aspect of the performance boxes can be tailored to your needs. Adjust their height and width, fine-tune the spacing between them, and position the entire panel exactly where you want it on your chart. The goal is to make this tool feel like it's truly yours.

█ Technical Challenges Solved

Polyline Precision

Creating precise polylines was perhaps the most demanding aspect of this project.

The challenge was ensuring accurate positioning across both time and price axes, while handling percentage mode scaling with precision.

The script constantly updates the current year's data in real-time, seamlessly integrating new information as it comes in.

Axis Management

Getting the axes right was like solving a complex puzzle. The Y-axis needed to scale dynamically whether you're viewing absolute prices or percentages.

The X-axis required careful month labeling that stays clean and readable regardless of your selected timeframe.

Everything needed to align perfectly while maintaining proper spacing in all conditions.

█ Final Notes

This tool transforms complex market data into clear, actionable insights. Whether you're day trading or analyzing long-term trends, it provides the information you need to make informed decisions. And remember, while we can't predict the future, we can certainly be better prepared for it with the right tools at hand.

A word of warning though - seeing those red numbers in a beautifully formatted panel doesn't make them any less painful! 😉

---

Happy Trading! May your charts be green and your stops be far away!

Daveatt

Rounded Grid Levels🟩 Rounded Grid Levels is a visual tool that helps traders quickly identify key psychological price levels on any chart. By dynamically adapting to the user's visible screen area, it provides consistent, easy-to-read round number grids that align with price action. The indicator offers a traditional visualization of horizontal round level grids, along with enhanced options such as tilted grids that align with market sentiment, and fan-shaped grids for alternative price interaction views. It serves purely as a visual aid, providing an adaptable way to observe rounded price levels without making predictions or generating trading signals.

⚡ OVERVIEW ⚡

The Rounded Grid Levels indicator is a visual tool designed to help traders identify and track price levels that may hold psychological significance, such as round numbers or significant milestones. These levels often serve as potential areas for price reactions, including support, resistance, or points of market interest. The indicator's gridlines are determined by user-defined settings and adjust dynamically based on the visible chart area, meaning they are influenced by the user's current zoom level and perspective. This behavior is similar to TradingView's built-in grid lines found in the chart settings canvas, which also adjust in real-time based on the visible screen, ensuring the most relevant price levels are displayed. By default, the indicator provides consistent gridlines to represent traditional round number levels, offering a straightforward view of key psychological areas. Additionally, users have access to experimental and novel configurations, such as fan-shaped layouts, which expand from a central point and adapt directionally based on user settings. This configuration can provide an alternate perspective for traders, especially useful in analyzing broader market moves and visualizing expansion relative to the current price.

Users can display the gridlines in a variety of configurations, including horizontal, neutral, auto, or fan-shaped layouts, depending on their preferred method of analysis. This flexibility allows traders to focus on different types of price action without overcrowding the visual representation of price movements.

This indicator is intended purely as a visual aid for understanding how price interacts with rounded levels over time. It does not generate predictive trading signals or recommendations but rather provides traders with a customizable framework to enhance their market analysis.

⭕ ROUND NUMBERS IN MARKET PSYCHOLOGY ⭕

Round numbers hold a significant place in financial markets, largely due to the psychological tendencies of traders and investors. These levels often represent areas of interest where human behavior, market biases, and trading strategies converge. Whether it's prices ending in 000, 500, or other recognizable values, these levels naturally attract more attention and influence decision-making.

Round numbers can act as key support or resistance levels and often become focal points in market activity. They are frequently highlighted by financial media, embedded in products like options, and serve as foundations for various trading theories. Their impact extends across different market participants and strategies, making them important focal points in both short-term and long-term market analysis.

Round numbers play an important role in guiding trader behavior and market activity. To better understand why these levels are so impactful, there are several key factors that highlight their significance in trading and price dynamics:

Psychological Impact : Humans naturally gravitate toward round numbers, such as prices ending in 000, 500, or 00. These levels tend to draw attention as traders perceive them as psychologically significant. This behavior is rooted in the cognitive bias known as "left-digit bias," where people assign greater importance to rounded, more recognizable numbers. In trading, this means that prices at these levels are more memorable and thus more likely to attract attention, creating an area where traders focus their buying or selling decisions.

Order Clustering : Traders often place buy and sell orders around these rounded levels, either manually or automatically through stop and limit orders. This clustering leads to the formation of visible support or resistance zones, as the concentrated orders tend to influence price behavior around these key levels. Market participants tend to converge their orders around these price points because of their perceived psychological importance, creating a liquidity pocket. As a result, these areas often act as barriers that the price either struggles to cross or uses as springboards for further movement.

External Influences : Financial media frequently highlights round-number milestones, amplifying market sentiment and drawing traders' attention to these levels. Additionally, algorithmic trading systems often react to round-number thresholds, which can further reinforce price movements, creating self-reinforcing reactions at these levels. As media and analysts emphasize these milestones, more traders pay attention to them, leading to increased volume and often heightened volatility at those points. This self-reinforcing cycle makes round numbers an area where price movement can either accelerate due to a breakout or stall because of clustering interest.

Option Strike Prices : Options contracts typically have strike prices set at round numbers, and as expiration approaches, these levels can influence the price of the underlying asset due to concentrated trading activity. The behavior around these levels, often called "pinning," happens because traders adjust their positions to avoid unfavorable scenarios at these key strikes. This activity tends to concentrate price movement toward these levels as traders hedge their positions, leading to increased liquidity and the potential for abrupt price reactions near option expiration dates.

Whole Number Theory : This theory suggests that whole numbers act as natural psychological barriers, where traders tend to make decisions, place orders, or expect price reactions, making these levels crucial for analysis. Whole numbers are simple to remember and are often used as informal targets for profit-taking or stop placement. This behavior leads to a natural ebb and flow around these levels, where the market finds equilibrium temporarily before deciding on a future direction. Whole numbers tend to work like magnets, drawing price to them and often creating reactions that are visible across different timeframes.

Quarters Theory : Commonly used in Forex markets, this theory focuses on quarter-point increments (e.g., 1.0000, 1.2500, 1.5000) as key levels where price often pauses or reverses. These quarter levels are treated as important psychological barriers, with price frequently interacting at these intervals. Traders use these points to gauge market strength or weakness because quarter levels divide larger round-number ranges into more manageable and meaningful segments. For example, in highly traded forex pairs like EUR/USD, traders might treat 1.2500 as a significant barrier because it represents a halfway point between 1.0000 and 1.5000, offering a balanced reference point for decision-making.

Big Round Numbers : Major round numbers, such as 100, 500, or 1000, often attract significant attention and serve as psychological thresholds. Traders anticipate strong reactions when prices approach or cross these levels. This is often because large round numbers symbolize major milestones, and price behavior around them tends to signal important market sentiment shifts. When price crosses a major level, such as a stock moving above $100 or Bitcoin crossing $50,000, it often creates a surge in trading activity as it is viewed as a validation or invalidation of market trends, drawing in momentum traders and triggering both retail and institutional responses.

By visualizing these round levels on the chart, the Rounded Grid Levels indicator helps traders identify areas where price may pause, reverse, or gain momentum. While round numbers provide useful insights, they should be used in conjunction with other technical analysis tools for a comprehensive trading strategy.

🛠️ CONFIGURATION AND SETTINGS 🛠️

The Rounded Grid Levels indicator offers a variety of configurable settings to tailor the visualization according to individual trader preferences. Below are the key settings available for customization:

Custom Settings

Rounding Step : The Rounding Step parameter sets the minimum interval between gridlines. This value determines how closely spaced the rounded levels are on the chart. For example, if the Rounding Step is set to 100, gridlines will be displayed at every 100 points (e.g., $100, $200, $300) relative to the current price level. The Rounding Step is scaled to the chart's visible area, meaning users should adjust it appropriately for different assets to ensure effective visualization. Lower values provide a more granular view, while larger values give a broader, higher-level perspective.

Major Grids : Defines the interval at which major gridlines will appear compared to minor ones. For example, if the Rounding Step is 100 and Major Grids is set to 10, major gridlines will be displayed every $1,000, while minor gridlines will be at every $100. This distinction allows traders to better visualize key psychological levels by emphasizing significant price intervals.

Direction : Users can select the gridline direction, choosing between options such as 'Up', 'Down', 'Auto', or 'Neutral'. This setting controls how the gridlines extend relative to the current price level, which can help in analyzing directional trends.

Neutral Direction : This option provides balanced gridlines both above and below the current price, allowing traders to visualize support and resistance levels symmetrically. This is useful for analyzing sideways or ranging markets without directional bias.

Up Direction : The gridlines are tilted upwards, starting from visible lows and extending toward the rounded level at the current price. By choosing Up , traders emphasize an upward sentiment, visualizing price action that aligns with rising trends. This option helps illustrate potential areas where pullbacks may occur, as well as how price might expand upwards in the current market context.

Down Direction : The gridlines are tilted downwards, starting from visible highs and extending toward the rounded level at the current price. Selecting Down allows traders to emphasize a downward sentiment, visualizing how price may expand downwards, which is particularly useful when analyzing downtrends or potential correction levels. The gridlines provide an illustrative view of how price interacts with lower levels during market declines.

Auto Direction : The gridlines automatically adjust their direction based on recent market trends. This adaptive option allows traders to visualize gridlines that dynamically change according to price action, making it suitable for evolving market conditions where the direction is uncertain. It’s useful for traders looking for an indicator that moves in sync with market shifts and doesn’t require manual adjustment.

Grid Type : Allows users to choose between 'Linear' or 'Fan' grid types. The Linear type creates evenly spaced gridlines that can be either horizontal or tilted, depending on the chosen direction setting, providing a straightforward view of price levels. The Fan type radiates lines from a central point, offering a more dynamic perspective for analyzing price expansions relative to the current price. These grid types introduce experimental visualizations influenced by chart properties, including visible highs, lows, and the current price. Regardless of the configuration, the gridlines will always end at the current bar, which represents a rounded price level, ensuring consistency in how key price areas are displayed.

Extend : This setting allows gridlines to be projected into the future, helping traders see potential levels beyond the current bar. When enabled, the behavior of the extended lines varies based on the selected grid type and direction. For Neutral and Horizontal Linear settings, the extended gridlines maintain their round-number alignment indefinitely. However, for Up , Down , or Auto directions, the angle of the extended gridlines can change dynamically based on the chart’s visible high and low or the latest price action. As a result, extended lines may not continue to align with round-number levels beyond the current bar, reflecting instead the current trend and sentiment of the market. Regardless of direction, extended gridlines remain consistently spaced and either parallel or evenly distributed, ensuring a structured visual representation.

Color Settings : Users can customize the colors for resistance, support, and minor gridlines at the current price. This helps in visually distinguishing between different grid types and their significance on the chart.

Color Options

These configuration options make the Rounded Grid Levels indicator a versatile tool for traders looking to customize their charts based on their personal trading strategies and analytical preferences.

🖼️ CHART EXAMPLES 🖼️

The following chart examples illustrate different configurations available in the Rounded Grid Levels indicator. These examples show how variations in grid type, direction, and rounding step settings impact the visualization of price levels. Traders may find that smaller rounding steps are more effective on lower time frames, where precision is key, whereas larger rounding steps help to reduce clutter and highlight key levels on higher time frames. Each image includes a caption to explain the specific configuration used, helping users better understand how to apply these settings in different market conditions.

Smaller Rounding Step (100) : With a smaller rounding step, the gridlines are spaced closely together. This setting is particularly useful for lower time frames where price action is more granular and finer details are needed. It allows traders to track price interactions at narrower levels, but on higher time frames, it may lead to clutter and exceed Pine Script's 500-line limit.

Larger Rounding Step (1000) : With a larger rounding step, the gridlines are spaced farther apart. This visualization is better suited for higher time frames or broader market overviews, allowing users to focus on major psychological levels without overloading the chart. On lower time frames, this may result in fewer actionable levels, but it helps in maintaining clarity and staying within Pine Script's line limit.

Linear Grid Type, Neutral Direction (Traditional Rounded Price Levels) : The Linear gridlines are displayed in a neutral fashion, representing traditional round-number levels with consistent spacing above and below the current price. This layout helps visualize key psychological price levels over time in a straightforward manner.

Linear Grid Type, Down Direction : The Linear gridlines are tilted downwards, remaining parallel and ending at the rounded level at the current price. This setup emphasizes downward market sentiment, allowing traders to visualize price expansion towards lower levels, which is useful when analyzing downtrends or potential correction levels.

Linear Grid Type, Down Direction : The Linear gridlines are tilted downwards, extending from the current price to lower levels. Useful for observing downtrending price movements and visualizing pullback areas during uptrends.

Linear Grid Type, Auto Direction : The Linear gridlines adjust dynamically, tilting either upwards or downwards to align with recent price trends, remaining parallel and ending at the rounded level at the current price. This configuration reflects the current market sentiment and offers traders a flexible way to observe price dynamics as they develop in real time.

Fan Grid Type, Neutral Direction : The fan-shaped gridlines radiate symmetrically from a central point, ending at the rounded level at the current price. This configuration provides an unbiased view of price action, giving traders a balanced visualization of rounded levels without directional influence.

Fan Grid Type, Up Direction : The fan-shaped gridlines originate from lower visible price points and radiate upwards, ending at the rounded level at the current price. This layout helps visualize potential price expansion to higher levels, offering insights into upward momentum while maintaining a dynamic and evolving perspective on market conditions.

Fan Grid Type, Down Direction : The fan-shaped gridlines originate from higher visible price points and radiate downwards, ending at the rounded level at the current price. This setup is particularly useful for observing potential price expansion towards lower levels, illustrating areas where the price might extend during a downtrend.

Fan Grid Type, Auto Direction : The fan-shaped gridlines dynamically adjust, originating from visible chart points based on the current market trend, and radiate outward, ending at the rounded level at the current price. This adaptive visualization offers a continuously evolving representation that aligns with changing market sentiment, helping traders assess price expansion dynamically.