Bias AnalyzerName: Bias Analyzer

Category: Market Analyzer

Timeframe: 1H and 1D, depending on the Analysis type.

Technical Analysis: Usually when we think about a Trading System we start from an idea. This idea comes normally from observation and the study of the market.

Have we ever observed a market - for example Bitcoin - and thought that it increases at the start of a USA session? Great, this is a well-known category of Trading System and the purpose of the Bias Analyzer is to study these phenomena.

There are different types of Trading System that we can classify considering the market in-efficiency that we use to our advantage. In this case we make the Bias. Literally "inclination" or "presupposition" or precisely "tendency" of the price to go up or down in a temporal way.

The characteristics of the Bias depend on how much the Bias is persistent on the market since the analysed period. therefore we can consider:

Hourly Bias : analysing the hourly behaviours during the week. Trades normally last from a few hours to a few days.

Seasonal Bias : analysing the behaviour of the weeks in the monthly or annual context, evaluating the seasons.

Suggested usage: The possibilities of the tool are infinite, these are some scenarios of use:

Development of Intraday Trading Systems based on Hourly Bias with possible filters for specific days of the week.

Development of a Multi-day Trading System based on daily Bias with monthly analysis.

To identify the best day to execute our investment through Dollar Cost Average with a bit of healthy buy the dip

Main features:

Hourly Summary organized in Week

The cells contain the sum of the various price deltas for the single hour. The transparency indicates the frequency in which the candles close positive or negative. This information is available both in a synthetic way, as in the first column "Sum", and for each day of the week.

Hourly Details organized in different entry/exit

Shows the cumulative data of the various deltas, considering the purchase and the sale at certain times. In the rows are represented the buying hours and in the columns the selling hours.

Daily Summary organized in Months

The cells contain the summation of the various price deltas for the single day.

Hourly Details organized in different entry/exit

Allows to visualise the detailed analysis table, choosing to do it for all the months or for a specific month and shows the cumulative data of the various deltas, considering the purchase and the sale in certain days.

Configuration: You can configure the tool easily and completely.

Analysis

Calculate from Close to Open : this is the core of the whole analysis where the "Price Delta" to be calculated is defined. At this moment there is the possibility to calculate the distance between opening and closing.

Calculate in Percent or Cash : this allows to calculate the Price Delta in Percent or in Cash.

Analysis on 1H Timeframe

Show Hourly Summary on : allows to visualise the summary analysis table of the week. The cells contain the sum of the various price deltas for the single hour. The transparency indicates the frequency in which the candles close positive or negative. This information is available both in a synthetic way, as in the first column "Sum", and for each day of the week. At the bottom left there is also data which allows us to understand how many candles are being analysed. At the bottom of each day it is possible to visualise the cumulative data of the day. The position of the table is customizable.

Show Hourly Details of on : allows to visualise the detailed analysis table, choosing to do it for all days or for a specific day, and shows the cumulative data of the various deltas, considering the purchase and the sale at certain times. In the rows are represented the buying hours and in the columns the selling hours. For example, going to the table "All Days" we can see in the cell of row 13 and in column 22 the cumulative data of a possible buy on 13 and a sell at the end of 22. To facilitate the research of the values there is a configurable transparency system.

Analysis on 1D Timeframe

Show Daily Summary on : allows to visualise the summary analysis table of the month. The cells contain the summation of the various price deltas for the single day: The first row is the summation of all days of the month for all months in the analysis period, while the other rows represent the analysis for the various days of the individual months.

Show Daily Details of on : allows to visualise the detailed analysis table, choosing to do it for all the months or for a specific month and shows the cumulative data of the various deltas, considering the purchase and the sale in certain days. In the rows are represented the buying days and in the columns the selling days. For example, going to the table "All Months" we can see in the cell at row 1 and at column 3 the cumulative of a possible purchase on the 1st and the sale on the 3rd. To facilitate the research of the values, there is a configurable transparency system.

Table Layout

Size : allows to define the size of the text in the table.

Precision : it is possible to define the decimal precision of the calculations presented in the tables.

Transparency Factor : allows the application of a multiplication factor when the table calculates the transparency of detail tables.

Colours : allows to specify the colours of Profit, Loss and Neutral, besides to adapt a style coherent with the Dark Mode or Light Mode of Trading View

Volatility Filter

It is possible to directly apply a filter to the time series on which the delta is calculated. The volatility filter uses the ATR - an indicator that allows you to calculate the volatility in a given period. Briefly: the higher the ATR value, the higher the volatility. Therefore the filter works by comparing the volatility on two periods and indicates compression or expansion.

Backtest Dates

In order to facilitate the identification of in-sample and out-of-sample data, as well as the degradation of a given behaviour, it is possible to specify a period in which to do the analysis.

在腳本中搜尋"Table"

Uptrick: Price Memory TrendIntroduction

Uptrick: Price Memory Trend is a custom indicator designed to detect directional shifts and volatility changes using a non-traditional price memory approach. Unlike moving average systems, it builds a dynamic memory of price that adapts gradually over time, allowing it to detect significant deviations and trend transitions with reduced noise.

Overview

This script identifies trend changes by comparing the current price to a memory-based baseline. When price deviates significantly from this memory base, it triggers a trend regime shift—either bullish or bearish. Adaptive deviation bands are calculated using absolute deviation from the memory base, not ATR or standard deviation, which allows the indicator to capture volatility uniquely. Visual components include color-coded candles, labeled signals, optional bands, and a live status table summarizing current trend metrics.

Originality

The indicator’s core innovation lies in its use of a decaying memory function to track trend direction, replacing moving averages with a price memory that responds only to significant deviations. This method avoids lag typically associated with smoothing techniques, enabling timely trend detection. Furthermore, deviation is measured directly in price terms, rather than through volatility surrogates like ATR or Bollinger Bands, resulting in a more raw and responsive depiction of price behavior.

Inputs

Core Engine

Memory Strength: Sets how strongly the memory responds to price changes. Higher values make the memory base more reactive.

Memory Decay: Controls how much past memory is retained. Lower values weight new prices more heavily.

Deviation Length: Length of the EMA used to smooth absolute price deviation. A longer setting results in smoother bands.

Band Multiplier: Expands or contracts the dynamic bands. Higher values widen the bands, reducing sensitivity.

Customization

Color Palette: Selects one of six predefined color schemes for bull and bear visuals.

Show Bands: Enables or disables the display of deviation bands.

Look: Chooses between 'Bands', 'Trail', or 'Intense' styles, affecting how bands and fills are drawn.

Bands

Trail

Intense

Show Info Table: Toggles display of the real-time trend and volatility status panel.

Table Position: Determines which corner of the chart the info panel appears in.

Text Size: Adjusts font size used within the info table.

Features

Trend Detection

Bullish Shift: Triggered when price crosses above the upper band, entering a new bullish regime.

Bearish Shift: Triggered when price crosses below the lower band, entering a new bearish regime.

Trend state is persistent and updated only on confirmed transitions, avoiding repeated entries in the same direction.

Candle Coloring

Candles are dynamically recolored based on current trend direction: bull, bear, or neutral.

Signal Labels

Visual labels marked "Up" or "Down" are placed on the chart when a regime shift occurs, helping to mark turning points.

Deviation Bands

Dynamic upper and lower bands are drawn based on smoothed absolute deviation from the memory base.

Additional outer bands based on ATR may be drawn to highlight zone intensity when the 'Intense' or 'Trail' styles are selected.

Bands visually indicate overextension and help frame price context relative to memory.

Alerts

Built-in alert conditions trigger on bullish or bearish trend shifts, useful for automation or notifications.

Info Table

The optional info table displays:

Current trend direction

Band state (calm, hot, or cool)

Price stretch from base

Trend age in bars

Confidence level based on deviation

Memory slope and acceleration

Band width and compression state

Reversion risk based on stretch level

Info Table:

Trade Example:

Logic

Price Memory

A recursive formula updates a memory variable based on the current price.

The memory adjusts only when the price deviates meaningfully from its previous value.

The formula uses a combination of delta-weighting and exponential decay:

> memory := previous_memory + delta × memory_strength

> memory := memory × memory_decay + price × (1 - memory_decay)

This produces a smooth, adaptive base that responds gradually to directional price moves.

Deviation and Bands

Absolute deviation between price and the memory base is calculated and smoothed using an EMA.

The upper and lower bands are then calculated as:

> Upper Band = memory base + (smoothed deviation × band multiplier)

> Lower Band = memory base - (smoothed deviation × band multiplier)

ATR-based extensions can optionally be drawn around these bands for added visual structure.

Trend Logic

Bullish and bearish states are tracked using crossovers and crossunders of price against the upper and lower bands.

The indicator maintains a persistent trend state variable that updates only when a confirmed regime change occurs.

This prevents multiple signals within the same trend direction (non-pyramiding behavior).

Stretch and Band Analysis

Stretch is measured as the deviation of price from memory, normalized by smoothed deviation.

Band width is tracked over time and used to detect compression or expansion.

Band position is calculated to identify where price sits between the upper and lower bands.

Info Table Metrics

Memory Slope and Acceleration: Show first and second derivative of the memory base to capture trend speed and change.

Confidence Level: Based on stretch intensity, indicating trend strength.

Reversion Risk: Inferred from how extended price is beyond the band.

Compression: Evaluated by comparing current band width to its recent average.

Summary

Uptrick: Price Memory Trend provides an alternative framework for trend identification by replacing traditional smoothing with adaptive memory logic. It measures price deviation without reliance on ATR or standard deviation, instead focusing on distance from a reactive baseline. With regime-based trend tracking, customizable visuals, and a detailed status table, it supports both discretionary and system-driven trading styles.

Disclaimer

This script is for informational and educational purposes only. It does not provide financial advice or guarantees. Trading involves risk, and past performance is not indicative of future results. Always perform your own research before making trading decisions.

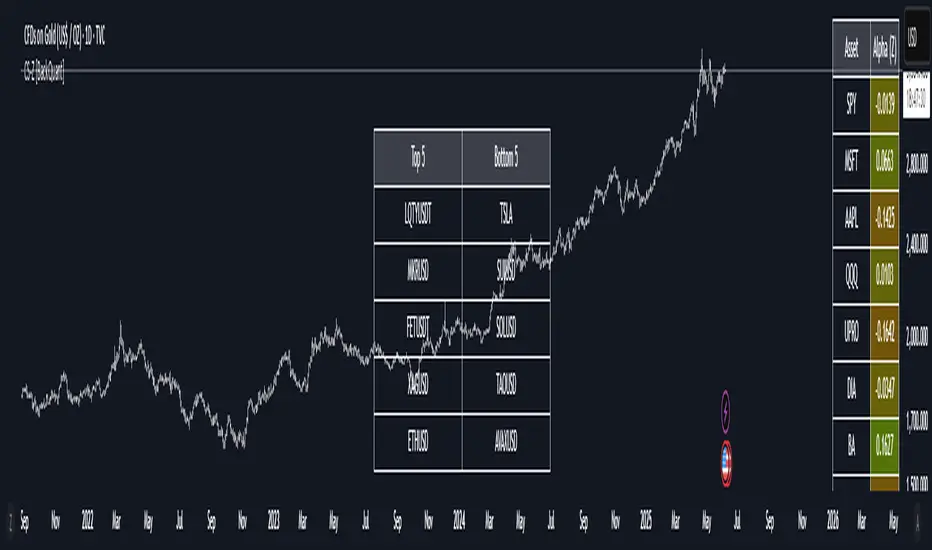

40 Ticker Cross-Sectional Z-Scores [BackQuant]40 Ticker Cross-Sectional Z-Scores

BackQuant’s 40 Ticker Cross-Sectional Z-Scores is a powerful portfolio management strategy that analyzes the relative performance of up to 40 different assets, comparing them on a cross-sectional basis to identify the top and bottom performers. This indicator computes Z-scores for each asset based on their log returns and evaluates them relative to the mean and standard deviation over a rolling window. The Z-scores represent how far an asset's return deviates from the average, and these values are used to rank the assets, allowing for dynamic asset allocation based on performance.

By focusing on the strongest-performing assets and avoiding the weakest, this strategy aims to enhance returns while managing risk. Additionally, by adjusting for standard deviations, the system offers a risk-adjusted method of ranking assets, making it suitable for traders who want to dynamically allocate capital based on performance metrics rather than just price movements.

Key Features

1. Cross-Sectional Z-Score Calculation:

The system calculates Z-scores for 40 different assets, evaluating their log returns against the mean and standard deviation over a rolling window. This enables users to assess the relative performance of each asset dynamically, highlighting which assets are performing better or worse compared to their historical norms. The Z-score is a useful statistical tool for identifying outliers in asset performance.

2. Asset Ranking and Allocation:

The system ranks assets based on their Z-scores and allocates capital to the top performers. It identifies the top and bottom assets, and traders can allocate capital to the top-performing assets, ensuring that their portfolio is aligned with the best performers. Conversely, the bottom assets are removed from the portfolio, reducing exposure to underperforming assets.

3. Rolling Window for Mean and Standard Deviation Calculations:

The Z-scores are calculated based on rolling means and standard deviations, making the system adaptive to changing market conditions. This rolling calculation window allows the strategy to adjust to recent performance trends and minimize the impact of outdated data.

4. Mean and Standard Deviation Visualization:

The script provides real-time visualizations of the mean (x̄) and standard deviation (σ) of asset returns, helping traders quickly identify trends and volatility in their portfolio. These visual indicators are useful for understanding the current market environment and making more informed allocation decisions.

5. Top & Bottom Performer Tables:

The system generates tables that display the top and bottom performers, ranked by their Z-scores. Traders can quickly see which assets are outperforming and underperforming. These tables provide clear and actionable insights, helping traders make informed decisions about which assets to include in their portfolio.

6. Customizable Parameters:

The strategy allows traders to customize several key parameters, including:

Rolling Calculation Window: Set the window size for the rolling mean and standard deviation calculations.

Top & Bottom Tickers: Choose how many of the top and bottom assets to display and allocate capital to.

Table Orientation: Select between vertical or horizontal table formats to suit the user’s preference.

7. Forward Test & Out-of-Sample Testing:

The system includes out-of-sample forward tests, ensuring that the strategy is evaluated based on real-time performance, not just historical data. This forward testing approach helps validate the robustness of the strategy in dynamic market conditions.

8. Visual Feedback and Alerts:

The system provides visual feedback on the current asset rankings and allocations, with dynamic labels and plots on the chart. Additionally, users receive alerts when allocations change, keeping them informed of important adjustments.

9. Risk Management via Z-Scores and Std Dev:

The system’s approach to asset selection is based on Z-scores, which normalize performance relative to the historical mean. By incorporating standard deviation, it accounts for the volatility and risk associated with each asset. This allows for more precise risk management and portfolio construction.

10. Note on Mean Reversion Strategy:

If you take the inverse of the signals provided by this indicator, the strategy can be used for mean-reversion rather than trend-following. This would involve buying the underperforming assets and selling the outperforming ones. However, it's important to note that this approach does not work well with highly correlated assets, as the relationship between the assets could result in the same directional movement, undermining the effectiveness of the mean-reversion strategy.

References

www.uts.edu.au

onlinelibrary.wiley.com

www.cmegroup.com

Final Thoughts

The 40 Ticker Cross-Sectional Z-Scores strategy offers a data-driven approach to portfolio management, dynamically allocating capital based on the relative performance of assets. By using Z-scores and standard deviations, this strategy ensures that capital is directed to the strongest performers while avoiding weaker assets, ultimately improving the risk-adjusted returns of the portfolio. Whether you’re focused on trend-following or looking to explore mean-reversion strategies, this flexible system can be tailored to suit your investment goals.

Volume pressure by GSK-VIZAG-AP-INDIA🔍 Volume Pressure by GSK-VIZAG-AP-INDIA

🧠 Overview

“Volume Pressure” is a multi-timeframe, real-time table-based volume analysis tool designed to give traders a clear and immediate view of buying and selling pressure across custom-selected timeframes. By breaking down buy volume, sell volume, total volume, and their percentages, this indicator helps traders identify demand/supply imbalances and volume momentum in the market.

🎯 Purpose / Trading Use Case

This indicator is ideal for intraday and short-term traders who want to:

Spot aggressive buying or selling activity

Track volume dynamics across multiple timeframes *1 min time frame will give best results*

Use volume pressure as a confirming tool alongside price action or trend-based systems

It helps determine when large buying/selling activity is occurring and whether such behavior is consistent across timeframes—a strong signal of institutional interest or volume-driven trend shifts.

🧩 Key Features & Logic

Real-Time Table Display: A clean, dynamic table showing:

Buy Volume

Sell Volume

Total Volume

Buy % of total volume

Sell % of total volume

Multi-Time frame Analysis: Supports 8 user-selectable custom time frames from 1 to 240 minutes, giving flexibility to analyze volume pressure at various granularities.

Color-Coded Volume Bias:

Green for dominant Buy pressure

Red for dominant Sell pressure

Yellow for Neutral

Intensity-based blinking for extreme values (over 70%)

Dynamic Data Calculation:

Uses volume * (close > open) logic to estimate buy vs sell volumes bar-by-bar, then aggregates by timeframe.

⚙️ User Inputs & Settings

Timeframe Selectors (TF1 to TF8): Choose any 8 timeframes you want to monitor volume pressure across.

Text & Color Settings:

Customize text colors for Buy, Sell, Total volumes

Choose Buy/Sell bias colors

Enable/disable blinking for visual emphasis on extremes

Table Appearance:

Set header color, metric background, and text size

Table positioning: top-right, bottom-right, etc.

Blinking Highlight Toggle: Enable this to visually highlight when Buy/Sell % exceeds 70%—a sign of strong pressure.

📊 Visual Elements Explained

The table has 6 rows and 10 columns:

Row 0: Headers for Today and TF1 to TF8

Rows 1–3: Absolute values (Buy Vol, Sell Vol, Total Vol)

Rows 4–5: Relative percentages (Buy %, Sell %), with dynamic background color

First column shows the metric names (e.g., “Buy Vol”)

Cells blink using alternate background colors if volume pressure crosses thresholds

💡 How to Use It Effectively

Use Buy/Sell % rows to confirm potential breakout trades or identify volume exhaustion zones

Look for multi-timeframe confluence: If 5 or more TFs show >70% Buy pressure, buyers are in control

Combine with price action (e.g., breakouts, reversals) to increase conviction

Suitable for equities, indices, futures, crypto, especially on lower timeframes (1m to 15m)

🏆 What Makes It Unique

Table-based MTF Volume Pressure Display: Most indicators only show volume as bars or histograms; this script summarizes and color-codes volume bias across timeframes in a tabular format.

Customization-friendly: Full control over colors, themes, and timeframes

Blinking Alerts: Rare visual feature to capture user attention during extreme pressure

Designed with performance and readability in mind—even for fast-paced scalping environments.

🚨 Alerts / Extras

While this script doesn’t include TradingView alert functions directly, the visual blinking serves as a strong real-time alert mechanism.

Future versions may include built-in alert conditions for buy/sell bias thresholds.

🔬 Technical Concepts Used

Volume Dissection using close > open logic (to estimate buyer vs seller pressure)

Simple aggregation of volume over custom timeframes

Table plotting using Pine Script table.new, table.cell

Dynamic color logic for bias identification

Custom blinking logic using na(bar_index % 2 == 0 ? colorA : colorB)

⚠️ Disclaimer

This indicator is a tool for analysis, not financial advice. Always backtest and validate strategies before using any indicator for live trading. Past performance is not indicative of future results. Use at your own risk and apply proper risk management.

✍️ Author & Signature

Indicator Name: Volume Pressure

Author: GSK-VIZAG-AP-INDIA

TradingView Username: prowelltraders

Relative Performance SuiteOverview

The Relative Performance Suite (RPS) is a versatile and comprehensive indicator designed to evaluate an asset's performance relative to a benchmark. By offering multiple methods to measure performance, including Relative Performance, Alpha, and Price Ratio, this tool helps traders and investors assess asset strength, resilience, and overall behavior in different market conditions.

Key Features:

✅ Multiple Performance Measures:

Choose from various relative performance calculations, including:

Relative Performance:

Measures how much an asset has outperformed or underperformed its benchmark over a given period.

Relative Performance (Proportional):

A proportional version of relative performance,

factoring in scaling effects.

Relative Performance (MA Based):

Uses moving averages to smooth performance fluctuations.

Alpha:

A measure of an asset’s performance relative to what would be expected based on its beta and the benchmark’s return. It represents the excess return above the risk-free rate after adjusting for market risk.

Price Ratio:

Compares asset prices directly to determine relative value over time.

✅ Customizable Moving Averages:

Apply different moving average types (SMA, EMA, SMMA, WMA, VWMA) to smooth price inputs and refine calculations.

✅ Beta Calculation:

Includes a Beta measure used in Alpha calculation, which users can toggle the visibility of helping users understand an asset's sensitivity to market movements.

✅ Risk-Free Rate Adjustment:

Incorporate risk-free rates (e.g., US Treasury yields, Fed Funds Rate) for a more accurate calculation of Alpha.

✅ Logarithmic Returns Option:

Users can switch between standard returns and log returns for more refined performance analysis.

✅ Dynamic Color Coding:

Identify outperformance or underperformance with intuitive color coding.

Option to color bars based on relative strength, making chart analysis easier.

✅ Customizable Tables for Data Display:

Overview table summarizing key metrics.

Explanation table offering insights into how values are derived.

How to Use:

Select a Benchmark: Choose a comparison symbol (e.g., TOTAL or SPX ).

Pick a Performance Metric: Use different modes to analyze relative performance.

Customize Calculation Methods: Adjust moving averages, timeframes, and log returns based on preference.

Interpret the Colors & Tables: Utilize the dynamic coloring and tables to quickly assess market conditions.

Ideal For:

Traders looking to compare individual asset performance against an index or benchmark.

Investors analyzing Alpha & Beta to understand risk-adjusted returns.

Market analysts who want a visually intuitive and data-rich performance tracking tool.

This indicator provides a powerful and flexible way to track relative asset strength, helping users make more informed trading decisions.

ATR Price Range Prediction V.2### ATR Price Range Prediction V.2

This script calculates the expected high and low prices for the current day based on the Average True Range (ATR) and displays the proportion of days where the daily range (high - low) is greater than or equal to the ATR. Additionally, the script provides an option to adjust the size of the text displayed in the top-right corner of the chart.

#### How It Works

1. **ATR Calculation**: The script calculates the ATR for a specified period (`atrPeriod`). ATR is a measure of volatility that represents the average range between the high and low prices over a specified number of periods.

2. **Expected High and Low Calculation**:

- **Expected High**: Calculated by adding the ATR value to the low price of the current day.

- **Expected Low**: Calculated by subtracting the ATR value from the high price of the current day.

3. **Proportion Calculation**: The script calculates the proportion of days where the daily range (high - low) is greater than or equal to the ATR value. This proportion is updated in real-time as new data comes in.

4. **Table Display**: Instead of displaying labels on each candle, the script shows the expected high, expected low, and the calculated proportion in a table located at the top-right corner of the chart. The size of the text in this table can be adjusted using the `Table Size` input.

5. **Color Coding**: The script changes the color of the bars to yellow if the daily range is greater than or equal to the ATR value, making it easy to identify these bars visually.

#### How to Use

- **ATR Period (`atrPeriod`)**: Adjust the period for the ATR calculation using the input parameter. The default value is 14.

- **Table Size (`tableSizeOption`)**: Choose the size of the text displayed in the table. Options include `tiny`, `small`, `normal`, `large`, and `huge`.

- **Expected High and Low**: Use the green and red lines to identify potential target prices or stop-loss levels for your trades. The green line represents the expected high, and the red line represents the expected low.

- **Proportion**: The table in the top-right corner of the chart shows the proportion of days where the daily range is greater than or equal to the ATR value. This can provide insight into the volatility of the asset.

- **Color Coding**: Yellow bars indicate days where the daily range is greater than or equal to the ATR value.

---

### ภาษาไทย

### ATR คาดการณ์ราคาสูงสุดและต่ำสุด พร้อมสัดส่วน

สคริปต์นี้คำนวณราคาสูงสุดและต่ำสุดที่คาดการณ์สำหรับวันปัจจุบันโดยอิงจากค่าเฉลี่ยช่วงที่แท้จริง (ATR) และแสดงสัดส่วนของวันที่ช่วงราคาต่อวัน (สูง - ต่ำ) มากกว่าหรือเท่ากับค่า ATR นอกจากนี้ยังมีตัวเลือกในการปรับขนาดข้อความที่แสดงในกล่องข้อความมุมขวาบนของกราฟ

#### วิธีการทำงาน

1. **การคำนวณ ATR**: สคริปต์คำนวณค่า ATR สำหรับช่วงเวลาที่กำหนด (`atrPeriod`) ATR เป็นมาตรวัดความผันผวนที่แสดงช่วงเฉลี่ยระหว่างราคาสูงสุดและต่ำสุดในช่วงเวลาที่กำหนด

2. **การคำนวณราคาสูงสุดและต่ำสุดที่คาดการณ์**:

- **ราคาสูงสุดที่คาดการณ์**: คำนวณโดยการบวกค่า ATR กับราคาต่ำสุดของวันปัจจุบัน

- **ราคาต่ำสุดที่คาดการณ์**: คำนวณโดยการลบค่า ATR จากราคาสูงสุดของวันปัจจุบัน

3. **การคำนวณสัดส่วน**: สคริปต์คำนวณสัดส่วนของวันที่ช่วงราคาต่อวัน (สูง - ต่ำ) มากกว่าหรือเท่ากับค่า ATR สัดส่วนนี้จะอัปเดตแบบเรียลไทม์เมื่อมีข้อมูลใหม่เข้ามา

4. **การแสดงผลในตาราง**: แทนที่จะแสดงป้ายกำกับบนแท่งเทียนแต่ละแท่ง สคริปต์จะแสดงราคาสูงสุดที่คาดการณ์ ราคาต่ำสุดที่คาดการณ์ และสัดส่วนที่คำนวณในตารางที่มุมขวาบนของกราฟ โดยสามารถปรับขนาดข้อความในตารางได้

5. **การใช้สี**: สคริปต์จะเปลี่ยนสีของแท่งเทียนเป็นสีเหลืองหากช่วงราคาต่อวันมากกว่าหรือเท่ากับค่า ATR ทำให้สามารถระบุแท่งเทียนเหล่านี้ได้ง่ายขึ้น

#### วิธีการใช้งาน

- **ATR Period (`atrPeriod`)**: ปรับช่วงเวลาสำหรับการคำนวณ ATR โดยใช้พารามิเตอร์การป้อนค่า ค่าเริ่มต้นคือ 14

- **Table Size (`tableSizeOption`)**: เลือกขนาดข้อความที่แสดงในตาราง ตัวเลือกได้แก่ `tiny`, `small`, `normal`, `large`, และ `huge`

- **ราคาสูงสุดและต่ำสุดที่คาดการณ์**: ใช้เส้นสีเขียวและสีแดงเพื่อระบุราคาที่เป็นเป้าหมายหรือระดับการหยุดขาดทุนสำหรับการซื้อขายของคุณ เส้นสีเขียวแสดงถึงราคาสูงสุดที่คาดการณ์และเส้นสีแดงแสดงถึงราคาต่ำสุดที่คาดการณ์

- **สัดส่วน**: ตารางที่มุมขวาบนของกราฟแสดงสัดส่วนของวันที่ช่วงราคาต่อวันมากกว่าหรือเท่ากับค่า ATR ซึ่งสามารถให้ข้อมูลเชิงลึกเกี่ยวกับความผันผวนของสินทรัพย์

- **การใช้สี**: แท่งเทียนสีเหลืองบ่งบอกถึงวันที่ช่วงราคาต่อวันมากกว่าหรือเท่ากับค่า ATR

_____

Volume Profile Histogram [SS]I usually (and by usually, I mean the past year xD) release a significant indicator as my Christmas gift to the community on Christmas Eve. Last year, it was the Z-Score buy and sell signal; this year, it's something a little more conventional. So here is this year’s gift—hope you like it! 🎁

Seems like everyone has their take on Volume Profiles (aka SVP or VSP). I decided to create one, and in true Steversteves fashion, you can expect to find all the goodies that come with most of my stuff, including a volume profile presented in a bell-curve/histogram style (chart above) and statistical frequency tables showing the cases by ranges:

And it wouldn't be a true Steversteves indicator without some kind of ATR thing:

So, what does it do?

At the end of the day, it is a form of an SVP indicator. However, it is meant to operate on a larger scale, sorting volume in a traditional bell-curve style. In addition to displaying volume, it breaks down buying vs. selling volume. Selling volume is classified as such when the open is greater than close, while buying is when close is greater than open. This breakdown allows you to see the distribution, by price range, of where selling and buying occur.

This permits the indicator to provide 2 Points of Control (POCs). A POC is defined as an area of high volume activity. Because buying and selling volumes are broken down into two, we can identify areas with high selling and areas with high buying. Sometimes they coincide, sometimes they differ.

If we look at SQQQ, for example:

We can see that the bearish point of control is one point below the bullish POC. This is interesting because it essentially shows where people may be "panic selling" or setting their stop-outs. If SQQQ drops below 18.8, then it's likely to trigger panic selling, as indicated by the histogram.

Conversely, we can observe that traders tend to position long between $18 and $24. The POC is noted in the stats table and also displayed on the chart. Bullish POC is shown in purple, bearish in yellow. These, of course, can be toggled off.

The Frequency Table:

The frequency table shows how many observations were obtained in each price range. The histogram illustrates the cumulative volume traded, while the frequency simply counts how many cases occurred over the lookback period.

ATR Range Analytics by Volume:

The indicator also has the ability to display range analytics by volume. When you toggle on the range analytics by volume option, a range chart will appear:

www.tradingview.com

The range chart goes from the minimum recorded volume to the maximum recorded volume in the period, showing the average range and direction associated with this volume. This is crucial to pay attention to because not all stocks behave the same way.

For example, in the chart above (AMD), we can see that low volume produces a general bearish bias, and high volume produces a general bullish bias. However, if we look at the range analytics for SPY:

Low volume has the inverse effect. Low volume is associated with a more bullish bias, and high volume indicates a more bearish bias. In the ATR chart, the threshold volume to transition from bullish bias to bearish bias is approximately > 78,607,268 traded shares.

The Stats Table:

The stats table can be toggled on or off. It simply displays the POCs and the time range for the VSP. The default time range is 1 trading year (252 days), assuming you are on the daily timeframe. However, you can use this on any timeframe.

The percentages displayed in the histogram is the cumulative percent of buying and selling volume independently. So when you see the percentage on the selling histogram, its the percent of cumulative selling only. Same for the buying.

And that's the indicator! I hope you enjoy it. Let me know your thoughts. I hope you all have safe holidays, a Merry Christmas for you North Americans, and a Happy Christmas for you UKers, and whatever else you celebrate/care about and do! Safe trades, everyone, and enjoy your holidays! 🎁🎄🎄🎄⭐⭐⭐ 🕎 🕎 🕎

High/Low of week: Stats & Day of Week tendencies// Purpose:

-To show High of Week (HoW) day and Low of week (LoW) day frequencies/percentages for an asset.

-To further analyze Day of Week (DoW) tendencies based on averaged data from all various custom weeks. Giving a more reliable measure of DoW tendencies ('Meta Averages').

-To backtest day-of-week tendencies: across all asset history or across custom user input periods (i.e. consolidation vs trending periods).

-Education: to see how how data from a 'hard-defined-week' may be misleading when seeking statistical evidence of DoW tendencies.

// Notes & Tips:

-Only designed for use on DAILY timeframe.

-Verification table is to make sure HoW / LoW DAY (referencing previous finished week) is printing correctly and therefore the stats table is populating correctly.

-Generally, leaving Timezone input set to "America/New_York" is best, regardless of your asset or your chart timezone. But if misaligned by 1 day =>> tweak this timezone input to correct

-If you want to use manual backtesting period (e.g. for testing consolidation periods vs trending periods): toggle these settings on, then click the indicator display line three dots >> 'Reset Points' to quickly set start & end dates.

// On custom week start days:

-For assets like BTC which trade 7 days a week, this is quite simple. Pick custom start day, use verification table to check all is well. See the start week day & time in said verification table.

-For traditional assets like S&P which trade only 5 days a week and suffer from occasional Holidays, this is a bit more complicated. If the custom start day input is a bank holiday, its custom 'week' will be discounted from the data set. E.g.1: if you choose 'use custom start day' and set it to Monday, then bank holiday Monday weeks will be discounted from the data set. E.g.2: If you choose 'use custom start day' and set it to Thursday, then the Holiday Thursday custom week (e.g Thanksgiving Thursday >> following Weds) would be discounted from the data set.

// On 'Meta Averages':

-The idea is to try and mitigate out the 'continuation bias' that comes from having a fixed week start/end time: i.e. sometimes a market is trending through the week start/end time, so the start/end day stats are over-weighted if one is trying to tease out typical weekly profile tendencies or typical DoW tendencies. You'll notice this if you compare the stats with various custom start days ('bookend' start/end days are always more heavily weighted). I wanted to try to mitigate out this 'bias' by cycling through all the possible new week start/end days and taking an average of the results. i.e. on BTC/USD the 'meta average' for Tuesday would be the average of the Tuesday HoW frequencies from the set of all 7 possible custom weeks(Mon-Sun, Tues-Mon, Weds-Tues, etc etc).

// User Inputs:

~Week Start:

-use custom week start day (default toggled OFF); Choose custom week start day

-show Meta Averages (default toggled ON)

~Verification Table:

-show table, show new week lines, number of new week lines to show

-table formatting options (position, color, size)

-timezone (only for tweaking if printed DoW is misaligned by 1 day)

~Statistics Table:

-show table, table formatting options (position, color, size)

~Manual Backtesting:

-Use start date (default toggled OFF), choose start date, choose vline color

-Use end date (defautl toggled OFF), choose end date, choose vline color

// Demo charts:

NQ1! (Nasdaq), Full History, Traditional week (Mon>>Friday) stats. And Meta Averages. Annotations in purple:

NQ1! (Nasdaq), Full History, Custom week (custom start day = Wednesday). And Meta Averages. Annotations in purple:

Plan Limit TimerA Pine Script library that helps developers monitor script execution time against TradingView's plan-specific timeout limits. Displays a visual debug table with runtime metrics, percentage of limit consumed, and color-coded status warnings.

WHAT THIS LIBRARY DOES

TradingView enforces different script timeout limits based on subscription tier:

• Basic : 20 seconds

• Essential / Plus / Premium : 40 seconds

• Ultimate : 100 seconds

This library measures your script's total execution time and displays it relative to these limits, helping you optimize indicators for users on different plans.

THE DEBUG TABLE

When enabled, a table appears on your chart showing:

• Plan : The selected TradingView subscription tier

• Limit : Maximum allowed execution time for that plan

• Runtime : Measured script execution time

• Per Bar : Average time spent per bar

• Bars : Number of bars processed

• % Used : Percentage of timeout limit consumed (color-coded)

• Status : OK (green), WARNING (yellow), DANGER (orange), or EXCEEDED (red)

HOW IT WORKS

The library captures a timestamp at the start of your script using timenow, then calculates the elapsed time at the end. It compares this against the selected plan's timeout limit to determine percentage used and status.

Technical Note : Pine Script's timenow variable has approximately 1-second precision. Scripts that execute in under 1 second may display 0ms. This is a platform limitation, not a library issue. For detailed per-function profiling, use TradingView's built-in Pine Profiler (More → Profiler mode in the Editor).

EXPORTED FUNCTIONS

startTimer()

Call at the very beginning of your script. Returns a timestamp.

getStats(startTime, plan)

Calculates timing statistics. Returns a TimingStats object with all metrics.

showTimingTable(stats, plan, tablePosition, showOnlyOnLast)

Renders the debug table on the chart.

debugTiming(startTime, plan, tablePosition)

Convenience function combining getStats() and showTimingTable() in one call.

isApproachingLimit(stats, threshold)

Returns true if execution time has reached the specified percentage of the limit.

getRemainingMs(stats)

Returns milliseconds remaining before timeout.

formatSummary(stats)

Returns a compact single-line string for labels or tooltips.

addTimingLabel(stats, barIdx, price, labelStyle, textSize)

Creates a color-coded chart label displaying timing statistics. Useful for visual debugging without the full table. Returns the label object for further customization.

EXPORTED CONSTANTS

• LIMIT_BASIC = 20

• LIMIT_ESSENTIAL = 40

• LIMIT_PLUS = 40

• LIMIT_PREMIUM = 40

• LIMIT_ULTIMATE = 100

EXPORTED TYPE: TimingStats

Object containing:

• totalTimeMs (float): Total execution time in milliseconds

• timePerBarMs (float): Average time per bar

• barsTimed (int): Number of bars measured

• barsSkipped (int): Bars excluded from measurement

• planLimitMs (int): Plan timeout in milliseconds

• percentUsed (float): Percentage of limit consumed

• status (string): "OK", "WARNING", "DANGER", or "EXCEEDED"

HOW TO USE IN YOUR INDICATOR

//@version=6

indicator("My Indicator", overlay = true)

import YourUsername/PlanLimitTimer/1 as timer

// User selects their TradingView plan

planInput = input.string("basic", "Your Plan", options = )

// START TIMING - must be first

startTime = timer.startTimer()

// Your indicator calculations here

sma20 = ta.sma(close, 20)

rsi14 = ta.rsi(close, 14)

plot(sma20)

// END TIMING - must be last

timer.debugTiming(startTime, planInput)

ADVANCED USAGE EXAMPLE

//@version=6

indicator("Advanced Example", overlay = true)

import YourUsername/PlanLimitTimer/1 as timer

planInput = input.string("basic", "Plan", options = )

startTime = timer.startTimer()

// Your calculations...

sma = ta.sma(close, 200)

plot(sma)

// Get stats for programmatic use

stats = timer.getStats(startTime, planInput)

// Option 1: Use addTimingLabel for a quick visual indicator

if barstate.islast

timer.addTimingLabel(stats, bar_index, high)

// Option 2: Show custom warning label if approaching limit

if timer.isApproachingLimit(stats, 70.0) and barstate.islast

label.new(bar_index, low, "Warning: " + timer.formatSummary(stats),

color = color.orange, textcolor = color.white, style = label.style_label_up)

// Display the debug table

timer.showTimingTable(stats, planInput, position.bottom_right)

IMPORTANT LIMITATIONS

1. Precision : Timing precision is approximately 1 second due to timenow behavior. Fast scripts show 0ms.

2. Variability : Results vary based on TradingView server load. The same script may show different times across runs.

3. Total Time Only : This library measures total script execution time, not individual function timing. For per-function analysis, use the Pine Profiler in the Editor.

4. Historical Bars : On historical bars, timenow reflects when the script loaded, not individual bar processing times.

USE CASES

• Optimization Debugging : See how close your script is to timeout limits

• Multi-Plan Support : Help users select appropriate settings for their subscription tier

• Performance Regression : Detect when changes increase execution time

• Documentation : Show users the performance characteristics of your indicator

Hour/Day/Month Optimizer [CHE] Hour/Day/Month Optimizer — Bucketed seasonality ranking for hours, weekdays, and months with additive or compounded returns, win rate, simple Sharpe proxy, and trade counts

Summary

This indicator profiles time-of-day, day-of-week, and month-of-year behavior by assigning every bar to a bucket and accumulating its return into that bucket. It reports per-bucket score (additive or compounded), win rate, a dispersion-aware return proxy, and trade counts, then ranks buckets and highlights the current one if it is best or worst. A compact on-chart table shows the top buckets or the full ranking; a last-bar label summarizes best and worst. Optional hour filtering and UTC shifting let you align buckets with your trading session rather than exchange time.

Motivation: Why this design?

Traders often see repetitive timing effects but struggle to separate genuine seasonality from noise. Static averages are easily distorted by sample size, compounding, or volatility spikes. The core idea here is simple, explicit bucket aggregation with user-controlled accumulation (sum or compound) and transparent quality metrics (win rate, a dispersion-aware proxy, and counts). The result is a practical, legible seasonality surface that can be used for scheduling and filtering rather than prediction.

What’s different vs. standard approaches?

Reference baseline: Simple heatmaps or average-return tables that ignore compounding, dispersion, or sample size.

Architecture differences:

Dual aggregation modes: additive sum of bar returns or compounded factor.

Per-bucket win rate and trade count to expose sample support.

A simple dispersion-aware return proxy to penalize unstable averages.

UTC offset and optional custom hour window.

Deterministic, closed-bar rendering via a lightweight on-chart table.

Practical effect: You see not only which buckets look strong but also whether the observation is supported by enough bars and whether stability is acceptable. The background tint and last-bar label give immediate context for the current bucket.

How it works (technical)

Each bar is assigned to a bucket based on the selected dimension (hour one to twenty-four, weekday one to seven, or month one to twelve) after applying the UTC shift. An optional hour filter can exclude bars outside a chosen window. For each bucket the script accumulates either the sum of simple returns or the compounded product of bar factors. It also counts bars and wins, where a win is any bar with a non-negative return. From these, it derives:

Score: additive total or compounded total minus the neutral baseline.

Win rate: wins as a percentage of bars in the bucket.

Dispersion-aware proxy (“Sharpe” column): a crude ratio that rises when average return improves and falls when variability increases.

Buckets are sorted by a user-selected key (score, win rate, dispersion proxy, or trade count). The current bar’s bucket is tinted if it matches the global best or worst. At the last bar, a table is drawn with headers, an optional info row, and either the top three or all rows, using zebra backgrounds and color-coding (lime for best, red for worst). Rendering is last-bar only; no higher-timeframe data is requested, and no future data is referenced.

Parameter Guide

UTC Offset (hours) — Shifts bucket assignment relative to exchange time. Default: zero. Tip: Align to your local or desk session.

Use Custom Hours — Enables a local session window. Default: off. Trade-off: Reduces noise outside your active hours but lowers sample size.

Start / End — Inclusive hour window one to twenty-four. Defaults: eight to seventeen. Tip: Widen if rankings look unstable.

Aggregation — “Additive” sums bar returns; “Multiplicative” compounds them. Default: Additive. Tip: Use compounded for long-horizon bias checks.

Dimension — Bucket by Hour, Day, or Month. Default: Hour. Tip: Start Hour for intraday planning; switch to Day or Month for scheduling.

Show — “Top Three” or “All”. Default: Top Three. Trade-off: Clarity vs. completeness.

Sort By — Score, Win Rate, Sharpe, or Trades. Default: Score. Tip: Use Trades to surface stable buckets; use Win Rate for skew awareness.

X / Y — Table anchor. Defaults: right / top. Tip: Move away from price clusters.

Text — Table text size. Default: normal.

Light Mode — Light palette for bright charts. Default: off.

Show Parameters Row — Info header with dimension and span. Default: on.

Highlight Current Bucket if Best/Worst — Background tint when current bucket matches extremes. Default: on.

Best/Worst Barcolor — Tint colors. Defaults: lime / red.

Mark Best/Worst on Last Bar — Summary label on the last bar. Default: on.

Reading & Interpretation

Score column: Higher suggests stronger cumulative behavior for the chosen aggregation. Compounded mode emphasizes persistence; additive mode treats all bars equally.

Win Rate: Stability signal; very high with very low trades is unreliable.

“Sharpe” column: A quick stability proxy; use it to down-rank buckets that look good on score but fluctuate heavily.

Trades: Sample size. Prefer buckets with adequate counts for your timeframe and asset.

Tinting: If the current bucket is globally best, expect a lime background; if worst, red. This is context, not a trade signal.

Practical Workflows & Combinations

Trend following: Use Hour or Day to avoid initiating trades during historically weak buckets; require structure confirmation such as higher highs and higher lows, plus a momentum or volatility filter.

Mean reversion: Prefer buckets with moderate scores but acceptable win rate and dispersion proxy; combine with deviation bands or volume normalization.

Exits/Stops: Tighten exits during historically weak buckets; relax slightly during strong ones, but keep absolute risk controls independent of the table.

Multi-asset/Multi-TF: Start with Hour on liquid intraday assets; for swing, use Day. On monthly seasonality, require larger lookbacks to avoid overfitting.

Behavior, Constraints & Performance

Repaint/confirmation: Calculations use completed bars only; table and label are drawn on the last bar and can update intrabar until close.

security()/HTF: None used; repaint risk limited to normal live-bar updates.

Resources: Arrays per dimension, light loops for metric building and sorting, `max_bars_back` two thousand, and capped label/table counts.

Known limits: Sensitive to sample size and regime shifts; ignores costs and slippage; bar-based wins can mislead on assets with frequent gaps; compounded mode can over-weight streaks.

Sensible Defaults & Quick Tuning

Start: Hour dimension, Additive, Top Three, Sort by Score, default session window off.

Too many flips: Switch to Sort by Trades or raise sample by widening hours or timeframe.

Too sluggish/over-smoothed: Switch to Additive (if on compounded) or shorten your chart timeframe while keeping the same dimension.

Overfit risk: Prefer “All” view to verify that top buckets are not isolated with tiny counts; use Day or Month only with long histories.

What this indicator is—and isn’t

This is a seasonality and scheduling layer that ranks time buckets using transparent arithmetic and simple stability checks. It is not a predictive model, not a complete trading system, and it does not manage risk. Use it to plan when to engage, then rely on structure, confirmation, and independent risk management for entries and exits.

Disclaimer

The content provided, including all code and materials, is strictly for educational and informational purposes only. It is not intended as, and should not be interpreted as, financial advice, a recommendation to buy or sell any financial instrument, or an offer of any financial product or service. All strategies, tools, and examples discussed are provided for illustrative purposes to demonstrate coding techniques and the functionality of Pine Script within a trading context.

Any results from strategies or tools provided are hypothetical, and past performance is not indicative of future results. Trading and investing involve high risk, including the potential loss of principal, and may not be suitable for all individuals. Before making any trading decisions, please consult with a qualified financial professional to understand the risks involved.

By using this script, you acknowledge and agree that any trading decisions are made solely at your discretion and risk.

Do not use this indicator on Heikin-Ashi, Renko, Kagi, Point-and-Figure, or Range charts, as these chart types can produce unrealistic results for signal markers and alerts.

Best regards and happy trading

Chervolino

Aggressive Predictor+ (Last Bar, Vol, Wick)# Aggressive Predictor+ Pine Script Indicator

**Version:** Based on the script incorporating Last Bar analysis, Volume Confirmation, and Wick Rejection.

## Overview

This TradingView Pine Script indicator aims to predict the likely directional bias of the **next** candle based on an aggressive analysis of the **last closed candle's** price action, volume, and wick characteristics relative to recent market volatility (ATR).

It is designed to be **highly reactive** to the most recent bar's information. The prediction is visualized directly on the chart through shapes, a projected line, a text label, and an information table.

**Please Note:** Predicting the next candle is inherently speculative. This indicator provides a probability assessment based on its specific logic and should be used as a supplementary tool within a broader trading strategy, not as a standalone signal. Its performance heavily depends on market conditions and the chosen settings.

## Core Logic Explained

The indicator follows these steps for each new bar, looking back at the **last closed bar** (` `):

1. **Calculate Recent Volatility:** Determines the Average True Range (ATR) over the specified `ATR Lookback Period` (`atr_len`). This provides context for how volatile the market has been recently.

2. **Analyze Last Bar's Body:** Calculates the price change from open to close (`close - open `) of the last completed bar.

3. **Compare Body to Volatility:** Compares the absolute size of the last bar's body to the calculated ATR (`prev_atr`) multiplied by a sensitivity threshold (`threshold_atr_mult`).

* If the body size (positive) exceeds the threshold, the initial prediction is "Upward".

* If the body size (negative) exceeds the negative threshold, the initial prediction is "Downward".

* Otherwise, the initial prediction is "Neutral".

4. **Check Volume Confirmation:** Compares the volume of the last bar (`volume `) to its recent average volume (`ta.sma(volume, vol_avg_len) `). If the volume is significantly higher (based on `vol_confirm_mult`), it adds context ("High Vol") to directional predictions.

5. **Check for Wick Rejection:** Analyzes the wicks of the last bar.

* If the initial prediction was "Upward" but there was a large upper wick (relative to the body size, defined by `wick_rejection_mult`), it indicates potential selling pressure rejecting higher prices. The prediction is **overridden to "Neutral"**.

* If the initial prediction was "Downward" but there was a large lower wick, it indicates potential buying pressure supporting lower prices. The prediction is **overridden to "Neutral"**.

6. **Determine Final Prediction:** The final state ("Upward", "Downward", or "Neutral") is determined after considering potential wick rejection overrides. Context about volume or wick rejection is added to the display text.

## Visual Elements

* **Prediction Shapes:**

* Green Up Triangle: Below the bar for an "Upward" prediction (without wick rejection).

* Red Down Triangle: Above the bar for a "Downward" prediction (without wick rejection).

* Gray Diamond: Above/Below the bar if a directional move was predicted but then neutralized due to Wick Rejection.

* **Prediction Line:**

* Extends forward from the current bar's close for `line_length` bars (Default: 20).

* Color indicates the final predicted state (Green: Upward, Red: Downward, Gray: Neutral).

* Style is solid for directional predictions, dotted for Neutral.

* The *slope/magnitude* of the line is based on recent volatility (ATR) and the `projection_mult` setting, representing a *potential* magnitude if the predicted direction holds, scaled by recent volatility. **This is purely a visual projection, not a precise price forecast.**

* **Prediction Label:**

* Appears at the end of the Prediction Line.

* Displays the final prediction state (e.g., "Upward (High Vol)", "Neutral (Wick Rej)").

* Shows the raw price change of the last bar's body and its size relative to ATR (e.g., "Last Body: 1.50 (120.5% ATR)").

* Tooltip provides more detailed calculation info.

* **Info Table:**

* Displays the prediction state, color-coded.

* Shows details about the last bar's body size relative to ATR.

* Dynamically positioned near the latest bar (offsets configurable).

## Configuration Settings (Inputs)

These settings allow you to customize the indicator's behavior and appearance. Access them by clicking the "Settings" gear icon on the indicator name on your chart.

### Price Action & ATR

* **`ATR Lookback Period` (`atr_len`):**

* *Default:* 14

* *Purpose:* Number of bars used to calculate the Average True Range (ATR), which measures recent volatility.

* **`Body Threshold (ATR Multiplier)` (`threshold_atr_mult`):**

* *Default:* 0.5

* *Purpose:* Key setting for **aggression**. The last bar's body size (`close - open`) must be greater than `ATR * this_multiplier` to be initially classified as "Upward" or "Downward".

* *Effect:* **Lower values** make the indicator **more aggressive** (easier to predict direction). Higher values require a stronger price move relative to volatility and result in more "Neutral" predictions.

### Volume Confirmation

* **`Volume Avg Lookback` (`vol_avg_len`):**

* *Default:* 20

* *Purpose:* Number of bars used to calculate the simple moving average of volume.

* **`Volume Confirmation Multiplier` (`vol_confirm_mult`):**

* *Default:* 1.5

* *Purpose:* Volume on the last bar is considered "High" if it's greater than `Average Volume * this_multiplier`.

* *Effect:* Primarily adds context "(High Vol)" or "(Low Vol)" to the display text for directional predictions. Doesn't change the core prediction state itself.

### Wick Rejection

* **`Wick Rejection Multiplier` (`wick_rejection_mult`):**

* *Default:* 1.0

* *Purpose:* If an opposing wick (upper wick on an up-candle, lower wick on a down-candle) is larger than `body size * this_multiplier`, the directional prediction is overridden to "Neutral".

* *Effect:* Higher values require a much larger opposing wick to cause a rejection override. Lower values make wick rejection more likely.

### Projection Settings

* **`Projection Multiplier (ATR based)` (`projection_mult`):**

* *Default:* 1.0

* *Purpose:* Scales the projected *magnitude* of the prediction line. The projected price change shown by the line is `+/- ATR * this_multiplier`.

* *Effect:* Adjusts how far up or down the prediction line visually slopes. Does not affect the predicted direction.

* **`Prediction Line Length (Bars)` (`line_length`):**

* *Default:* 20

* *Purpose:* Controls how many bars forward the **visual** prediction line extends.

* *Effect:* Purely visual length adjustment.

### Visuals

* **`Upward Color` (`bullish_color`):** Color for Upward predictions.

* **`Downward Color` (`bearish_color`):** Color for Downward predictions.

* **`Neutral Color` (`neutral_color`):** Color for Neutral predictions (including Wick Rejections).

* **`Show Prediction Shapes` (`show_shapes`):** Toggle visibility of the triangles/diamonds on the chart.

* **`Show Prediction Line` (`show_line`):** Toggle visibility of the projected line.

* **`Show Prediction Label` (`show_label`):** Toggle visibility of the text label at the end of the line.

* **`Show Info Table` (`show_table`):** Toggle visibility of the information table.

### Table Positioning

* **`Table X Offset (Bars)` (`table_x_offset`):**

* *Default:* 3

* *Purpose:* How many bars to the right of the current bar the info table should appear.

* **`Table Y Offset (ATR Multiplier)` (`table_y_offset_atr`):**

* *Default:* 0.5

* *Purpose:* How far above the high of the last bar the info table should appear, measured in multiples of ATR.

## How to Use

1. Open the Pine Editor in TradingView.

2. Paste the complete script code.

3. Click "Add to Chart".

4. Adjust the input settings (especially `threshold_atr_mult`) to tune the indicator's aggressiveness and visual preferences.

5. Observe the prediction elements alongside your other analysis methods.

## Disclaimer

**This indicator is for informational and educational purposes only. It does not constitute financial advice or a recommendation to buy or sell any asset.** Trading financial markets involves significant risk, and you could lose money. Predictions about future price movements are inherently uncertain. The performance of this indicator depends heavily on market conditions and the settings used. Always perform your own due diligence and consider multiple factors before making any trading decisions. Use this indicator at your own risk.

Risk RewardThe Risk Reward indicator, developed by OmegaTools, is a versatile technical tool designed to help traders visualize and evaluate potential reward and risk levels in their trades. By comparing recent price action against moving averages and volatility deviations, it calculates a range-weighted assessment of upside reward and downside risk. It provides a clear, color-coded visual representation of these potential ranges, along with critical support and resistance levels to aid in trade decision-making. This indicator is ideal for traders seeking to optimize their risk-reward ratio and make informed trade management decisions.

Features

Reward and Risk Visualization: Provides a histogram showing the relative potential of upside reward versus downside risk based on current price action.

Dynamic Support and Resistance Levels: Calculates and plots key price levels based on extreme of historical volatility, helping traders to identify important price zones.

Trade Size Customization: Users can adjust the trade size, and the indicator will calculate and display the estimated risk and reward in monetary terms based on the contract value.

Adaptive Volatility Extensions: Automatically adjusts extension lines based on volume, helping traders anticipate future price ranges and potential breakouts or breakdowns.

Customizable Visuals: Allows users to personalize the color scheme for bullish and bearish scenarios, making the chart more intuitive and user-friendly.

User Guide

Trade Size (size): Adjust the trade size in units (default is 1). This parameter impacts the risk and reward calculation shown in the summary table.

Length (lnt): Set the length for the exponential moving average (EMA) and the highest/lowest price calculations. This length determines the sensitivity of the indicator.

Different Visual (down): A boolean input to adjust the method for calculating downside risk. When set to true, it uses a different visual scheme.

Bullish Color (upc): Customize the color of the bullish (upside) histogram and support levels.

Bearish Color (dnc): Customize the color of the bearish (downside) histogram and resistance levels.

Plots

First Probability: Displays a histogram representing the higher value between reward and risk. It is colored according to whether the upside or downside is greater, providing a clear signal for potential trade direction.

Second Probability: A secondary histogram plot that visualizes the lower value between reward and risk, offering an additional perspective on the trade’s risk-reward balance.

Low Level/High Level: Displays dynamic support and resistance levels based on historical price data and volatility deviations.

Extension Lines: Visualize potential future price levels using volatility-adjusted projections. These lines help traders anticipate where price could move based on current conditions.

On-Chart Labels and Risk-Reward Table:

Risk and Reward Calculations: The indicator calculates the monetary value of downside risk and upside reward based on the provided trade size, volatility measures, and price movements.

Risk/Reward Table: Displayed directly on the chart, showing the downside risk and upside reward in easy-to-understand numerical values. This helps traders quickly assess the feasibility of a trade.

How It Works:

Moving Average Comparison: The indicator first calculates the 21-period (default) exponential moving average (EMA). It then compares the current price against this moving average to determine whether the market is in a bullish or bearish phase.

Deviation Calculation: It calculates the average deviation between the price and the EMA for both bullish and bearish movements, which is used to establish dynamic support and resistance levels.

Risk-Reward Calculation: Based on the highest and lowest price levels over the set period and the calculated deviations, it determines the potential upside reward and downside risk. The reward is calculated as the distance between the current price and the upper resistance levels, while the risk is determined as the distance to the lower support levels.

Visual Representation

The indicator plots histograms representing the relative magnitude of potential reward and risk.

Support and resistance levels are dynamically plotted on the chart using circles and lines, helping traders easily spot key areas of interest.

Extension lines are drawn to visualize potential future price levels based on current volatility.

Risk/Reward Table: This feature displays the calculated monetary risk and reward based on the trade size. It updates dynamically with price changes, offering a constant reference point for traders to evaluate their trade setup.

Practical Application

Identify Entry Points: Use the dynamic support and resistance levels to identify ideal trade entry points. The histogram helps determine whether the potential reward justifies the risk.

Risk Management: The calculated downside risk provides traders with an objective view of where to place stop-loss levels, while the upside reward aids in setting profit targets.

Trade Execution: By visually assessing whether reward outweighs risk, traders can make more informed decisions on trade execution, with the risk-reward ratio clearly displayed on the chart.

Best Practices:

Use Alongside Other Indicators: While this indicator offers a powerful standalone tool for assessing risk and reward, it works best when combined with other trend or momentum indicators for confirmation.

Adjust Inputs Based on Market Conditions: Adjust the length and trade size inputs depending on the asset being traded and the time horizon, as different assets may require different sensitivity settings.

Scoopy StacksWaffle Around Multiple

(Open, High, Low, Close) Stacks On

Pre/Post Market & (Daily, Weekly,

Monthly, Yearly) Sessions With

Meticulous Columns, Rows, Tooltips,

Colors, Custom Ideas, and Alerts.

Sessions Use Two Step Incremental Values

Default Value: (1) Shows Two Previous

(O, H, L, C); Increasing Value Swaps

Sessions With Next Two Stacks.

⬛️ KEY WORDS:

🟢 Crossover | 🔴 Crossunder

📗 High | 📕 Low

📔 Open | 📓 Close

🥇 First Idea | 🥈 Second Idea

🥉 Third Idea | 🎖️ Fourth Idea

🟥 ALERTS:

Default Option: (Per Bar)

Alerts Once Conditions Are Met

(Bar Close) Alerts When Bar Closes

Default Option: (Reg)

Alerts During Regular Market

Trading Hours, (0930-1600)

(Ext) Alerts During Extended

Market Hours, (1600-0930)

(24/7) Alerts All Day

Optional Preferences:

Regular Alerts - Stocks

Extended Alerts - Futures

24/7 Alerts - Crypto

🟧 STACKS:

Default Value: (1)

Incremental Stack Value, Increasing Value

Swaps Sessions With the Next Two Stacks

(✓) Swap Stacks?

Pre/Post Market High/Lows,

1-2 Day High/Lows, 1-2 Week High/Lows,

1-2 Month High/Lows, 1-2 Year High/Lows

( ) Swap Stacks?

Pre/Post Market Open/Close,

1-2 Day Open/Close, 1-2 Week Open/Close,

1-2 Month Open/Close, 1-2 Year Open/Close

🟨 EXAMPLES:

Default Stack:

🟢 | 📗 Pre Market High (PRE) | 4600.00

🔴 | 📕 Post Market Low (POST) | 420.00

Optional: (Open)

🟢 | 📔 Post Market Open (POST) | 4400.00

Optional: (Close)

🔴 | 📓 Pre Market Close (PRE) | 430.00

Default Stack Value: (1)

🔴 | 📗 1 Day High (1DH) | 460.00

Next Stack Value: (3)

🟢 | 📕 4 Day Low (4DL) | 420.00

Optional: (Open)

🔴 | 📔 2 Day Open (2DO) | 440.00

Optional: (Close)

🟢 | 📓 3 Day Close (3DC) | 430.00

Default Stack Value: (5)

🟢 | 📗 5 Week High (5WH) | 460.00

Next Stack Value: (7)

🔴 | 📕 8 Week Low (8WL) | 420.00

Optional: (Open)

🔴 | 📔 7 Week Open (7WO) | 4400.00

Optional: (Close)

🟢 | 📓 6 Week Close (6WC) | 430.00

Default Stack Value: (9)

🔴 | 📗 9 Month High (9MH) | 460.00

Next Stack Value: (11)

🟢 | 📕 12 Month Low (12ML) | 420.00

Optional: (Open)

🟢 | 📔 11 Month Open (11MO) | 4400.00

Optional: (Close)

🔴 | 📓 10 Month Close (10MC) | 430.00

Default Stack Value: (13)

🟢 | 📗 13 Year High (13YH) | 460.00

Next Stack Value: (15)

🟢 | 📕 16 Year Low (16YL) | 420.00

Optional: (Open)

🔴 | 📔 15 Year Open (15YO) | 4400.00

Optional: (Close)

🔴 | 📓 14 Year Close (14YC) | 430.00

🟩 TABLES:

Default Value: (1)

Moves Table Up, Down, Left, or Right

Based on Second Default Value

First Default Value: (Top Right)

Sets Table Placement, Middle Center

Allows Table To Move In All Directions

Second Default Value: (Default)

Fixed Table Position, Switching Values

Moves Direction of the Table

🟦 IDEAS:

(✓) Show Ideas?

Shows Four Ideas With Custom Texts

and Values; Ideas Are Based Around

Post-It Note Reminders with Alerts

Suggestions For Text Ideas:

Take Profit, Stop Loss, Trim, Hold,

Long, Short, Bounce Spot, Retest,

Chop, Support, Resistance, Buy, Sell

🟪 EXAMPLES:

Default Value: (5)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥇)

Shown On First Table Cell and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥇 | 5.00

Default Value: (10)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥈)

Shown On Second Table Cell and

Message Appearing On Alerts

Alert Shows: 🔴 | 🥈 | 10.00

Default Value: (50)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🥉)

Shown On Third Table Cell and

Message Appearing On Alerts

Alert Shows: 🟢 | 🥉 | 50.00

Default Value: (100)

Shows the Custom Table Value For

Sorted Table Positions and Alerts

Default Text: (🎖️)

Shown On Fourth Table Cell and

Message Appearing On Alerts

Alert Shows: 🔴 | 🎖️ | 100.00

⬛️ REFERENCES:

Pre-market Highs & Lows on regular

trading hours (RTH) chart

By Twingall

Previous Day Week Highs & Lows

By Sbtnc

Screener for 40+ instruments

By QuantNomad

Daily Weekly Monthly Yearly Opens

By Meliksah55

DataChartLibrary "DataChart"

Library to plot scatterplot or heatmaps for your own set of data samples

draw(this)

draw contents of the chart object

Parameters:

this : Chart object

Returns: current chart object

init(this)

Initialize Chart object.

Parameters:

this : Chart object to be initialized

Returns: current chart object

addSample(this, sample, trigger)

Add sample data to chart using Sample object

Parameters:

this : Chart object

sample : Sample object containing sample x and y values to be plotted

trigger : Samples are added to chart only if trigger is set to true. Default value is true

Returns: current chart object

addSample(this, x, y, trigger)

Add sample data to chart using x and y values

Parameters:

this : Chart object

x : x value of sample data

y : y value of sample data

trigger : Samples are added to chart only if trigger is set to true. Default value is true

Returns: current chart object

addPriceSample(this, priceSampleData, config)

Add price sample data - special type of sample designed to measure price displacements of events

Parameters:

this : Chart object

priceSampleData : PriceSampleData object containing event driven displacement data of x and y

config : PriceSampleConfig object containing configurations for deriving x and y from priceSampleData

Returns: current chart object

Sample

Sample data for chart

Fields:

xValue : x value of the sample data

yValue : y value of the sample data

ChartProperties

Properties of plotting chart

Fields:

title : Title of the chart

suffix : Suffix for values. It can be used to reference 10X or 4% etc. Used only if format is not format.percent

matrixSize : size of the matrix used for plotting

chartType : Can be either scatterplot or heatmap. Default is scatterplot

outliersStart : Indicates the percentile of data to filter out from the starting point to get rid of outliers

outliersEnd : Indicates the percentile of data to filter out from the ending point to get rid of outliers.

backgroundColor

plotColor : color of plots on the chart. Default is color.yellow. Only used for scatterplot type

heatmapColor : color of heatmaps on the chart. Default is color.red. Only used for heatmap type

borderColor : border color of the chart table. Default is color.yellow.

plotSize : size of scatter plots. Default is size.large

format : data representation format in tooltips. Use mintick.percent if measuring any data in terms of percent. Else, use format.mintick

showCounters : display counters which shows totals on each quadrants. These are single cell tables at the corners displaying number of occurences on each quadrant.

showTitle : display title at the top center. Uses the title string set in the properties

counterBackground : background color of counter table cells. Default is color.teal

counterTextColor : text color of counter table cells. Default is color.white

counterTextSize : size of counter table cells. Default is size.large

titleBackground : background color of chart title. Default is color.maroon

titleTextColor : text color of the chart title. Default is color.white

titleTextSize : text size of the title cell. Default is size.large

addOutliersToBorder : If set, instead of removing the outliers, it will be added to the border cells.

useCommonScale : Use common scale for both x and y. If not selected, different scales are calculated based on range of x and y values from samples. Default is set to false.

plotchar : scatter plot character. Default is set to ascii bullet.

ChartDrawing

Chart drawing objects collection

Fields:

properties : ChartProperties object which determines the type and characteristics of chart being plotted

titleTable : table containing title of the chart.

mainTable : table containing plots or heatmaps.

quadrantTables : Array of tables containing counters of all 4 quandrants

Chart

Chart type which contains all the information of chart being plotted

Fields:

properties : ChartProperties object which determines the type and characteristics of chart being plotted

samples : Array of Sample objects collected over period of time for plotting on chart.

displacements : Array containing displacement values. Both x and y values

displacementX : Array containing only X displacement values.

displacementY : Array containing only Y displacement values.

drawing : ChartDrawing object which contains all the drawing elements

PriceSampleConfig

Configs used for adding specific type of samples called PriceSamples

Fields:

duration : impact duration for which price displacement samples are calculated.

useAtrReference : Default is true. If set to true, price is measured in terms of Atr. Else is measured in terms of percentage of price.

atrLength : atrLength to be used for measuring the price based on ATR. Used only if useAtrReference is set to true.

PriceSampleData

Special type of sample called price sample. Can be used instead of basic Sample type

Fields:

trigger : consider sample only if trigger is set to true. Default is true.

source : Price source. Default is close

highSource : High price source. Default is high

lowSource : Low price source. Default is low

tr : True range value. Default is ta.tr

trend_vol_stopThe description below is copied from the script's comments. Because TradingView does not allow me to edit this description, please refer to the script's comments section, as well as the release notes, for the most up-to-date information.

----------

Usage:

The inputs define the trend and the volatility stop.

Trend:

The trend is defined by a moving average crossover. When the short

(or fast) moving average is above the long (slow) moving average, the

trend is up. Otherwise, the trend is down. The inputs are:

long: the number of periods in the long/slow moving average.

short: the number of periods in the short/fast moving average.

The slow moving average is shown in various colors (see explanation