VolatilityCheckerLibrary "VolatilityChecker"

Volatility is judged to be high when the range of one period is greater than the ATR of another period.

is_high(_periods, _smooth, _atr_periods, _atr_times) Return true if the volatility is high.

Parameters:

_periods : Range Period

_smooth : Smoothes the range width.

_atr_periods : ATR Period

_atr_times : Amplify the calculated ATR.

Returns: {Boolean}

is_low()

在腳本中搜尋"Volatility"

VIX and SKEW RSI Moving AveragesSKEW and VIX are both indicators of market volatility and risk, but they represent different aspects.

VIX (CBOE Volatility Index) :.

The VIX is a well-known indicator for predicting future market volatility. It is calculated primarily based on S&P 500 options premiums and indicates the degree of market instability and risk.

Typically, when the VIX is high, market participants view the future as highly uncertain and expect sharp volatility in stock prices. It is generally considered an indicator of market fear.

SKEW Index :.

The SKEW is a measure of how much market participants estimate the risk of future declines in stock prices, calculated by the CBOE (Chicago Board Options Exchange) and derived from the premium on S&P 500 options.

If the SKEW is high, market participants consider the risk of future declines in stock prices to be high. This generally indicates a "fat tail at the base" of the market and suggests that the market perceives it as very risky.

These indicators are used by market participants to indicate their concerns and expectations about future stock price volatility. In general, when the VIX is high and the SKEW is high, the market is considered volatile and risky. Conversely, when the VIX is low and the SKEW is low, the market is considered relatively stable and low risk.

Inverse Relationship between SKEW and VIX

It is often observed that there is an inverse correlation between SKEW and VIX. In general, the relationship is as follows

High VIX and low SKEW: When the VIX is high and the SKEW is low, the market is considered volatile while the risk of future stock price declines is low. This indicates that the market is exposed to sharp volatility, but market participants do not expect a major decline.

Low VIX and High SKEW: A low VIX and high SKEW indicates that the market is relatively stable, while the risk of future declines in stock prices is considered high. This indicates that the market is calm, but market participants are wary of a sharp future decline.

This inverse correlation is believed to be the result of market participants' psychology and expectations affecting the movements of the VIX and SKEW. For example, when the VIX is high, it is evident that the market is volatile, and under such circumstances, people tend to view the risk of a sharp decline in stock prices as low. Conversely, when the VIX is low, the market is considered relatively stable and the risk of future declines is likely to be higher.

SKEWVIX RSIMACROSS

In order to compare the trends of the SKEW and VIX, the 50-period moving average of the Relative Strength Index (RSI) was used for verification. the RSI is an indicator of market overheating or overcooling, and the 50-period moving average can be used to determine the medium- to long-term trend. This analysis reveals how the inverse correlation between the SKEW and the VIX relates to the long-term moving average of the RSI.

how to use

Moving Average Direction

Rising blue for VIXRSI indicates increased uncertainty in the market

Rising red for SKEWRSI indicates optimism and beyond

RSI moving average crossing

When the SKEW is dominant, market participants are considered less concerned about a black swan event (significant unexpected price volatility). This suggests that the market is stable and willing to take risks. On the other hand, when the VIX is dominant, it indicates increased market volatility. Investors are more concerned about market uncertainty and tend to take more conservative positions to avoid risk. The direction of the moving averages and the crossing of the moving averages of the two indicators can give an indication of the state of the market.

SKEW>VIX Optimistic/Goldilocks

VIX>SKEW Uncertainty/turbulence

The market can be judged as follows.

BestRegards

Expansion/Contraction Indicator (ECI) [Angel Algo]INTRODUCTION

The Expansion/Contraction Indicator (ECI) is a custom indicator designed to measure the expansion or contraction of price ranges between the open and close of each bar. It helps traders identify periods of increased or decreased volatility in the market. Since trading is most fruitful during volatile market conditions, this indicator provides valuable insights into when volatility increases, signaling the opportune moments to take action.

HOW TO USE

Expansion: When the ECI value is in the green zone, it suggests an expansion in price ranges, indicating increased volatility. This may be a potential signal for traders to expect trend movements or breakouts.

Contraction: When the ECI value falls outside the green zone, it indicates a contraction in price ranges, implying reduced volatility. This may signal potential consolidation or ranging periods in the market.

During contraction periods, it is advisable to exercise patience and await clear signals. Market cycles dictate that low-volatility contractions are often followed by high-volatility expansion periods, presenting opportunities for significant price movements.

Visualization:

Expansion Area: the area on the indicator chart filled with green. It has duller and brighter parts that indicate the level of expansion. The duller part corresponds to a low or beginning expansion.

ECI Dots: The ECI dots are plotted as circles on the chart. The dots are colored green if the ECI value is above the lower threshold, indicating an expansion. If the ECI value is below the lower threshold, the dots are colored red to indicate a contraction.

Alerts (Optional): The ECI indicator can generate alerts for expansions and contractions. By default, alerts are enabled. An expansion alert is triggered when the ECI value crosses above the upper threshold. A contraction alert is triggered when the ECI value crosses below the lower threshold.

SETTINGS

Period: determines the number of bars used to calculate the exponential moving average (EMA) of the price range. The default value is 14, but it can be set between 1 and 200. Higher values smooth out the indicator but may delay signals.

Lower Threshold: defines the level below which the ECI value indicates a contraction in price ranges, implying reduced volatility. The default value is 0.5.

CALCULATION

The indicator calculates the range between the open and close of each bar (ocRange). It then calculates the EMA of the range (emaRange) using the specified period. The ECI value is obtained by dividing the ocRange by the emaRange. Threshold Levels: The indicator includes two threshold levels for identifying expansions and contractions: a. Upper Threshold: Default value is 3.0. b. Lower Threshold: Default value is 0.5. The middle line (mL) represents the ECI value of 1.0, which indicates a neutral state, when the volatility in the market corresponds to its average value.

Simple Trend Strength & MomentumThis indicator will show a combination of Trend Strength, Volatility using an Adaptive Moving Average (AMA), and Market Momentum.

You can use this indicator to identify trends, volatility, and momentum shifts in real-time, making it an excellent tool for both trend-following and breakout strategies.

The three main features of this indicator are:

Adaptive Moving Average (AMA): Tracks the trend direction with a dynamic smoothing factor that adjusts based on market volatility. The AMA line changes color based on trend strength (green for bullish, red for bearish). I manually compute the Adaptive Moving Average (AMA) using a smoothing factor derived from the market's efficiency ratio. I have used fastLength and slowLength to control the responsiveness of the AMA.

Volatility Bands: Plots upper and lower bands around the AMA line, indicating price volatility. These bands dynamically adjust based on ATR, with a color gradient that changes intensity based on market volatility.

Momentum Circles: Positive momentum (ROC above the threshold) is shown as a green circle below the bar, while negative momentum is marked by a red circle above the bar. This makes it easy to spot momentum shifts.

The green dots in the indicator represent positive momentum. Specifically, they are displayed when the Rate of Change (ROC) of the price exceeds a predefined threshold (set as threshold in the input). This indicates that the market is experiencing upward price movement at a rate faster than the defined threshold.

How it works:

Rate of Change (ROC) measures the percentage change in price over a specified period (in this case, 14 periods).

When the ROC is greater than the set threshold (1.5 by default), a green circle (dot) is plotted below the price bar to signal that there is significant positive momentum.

This can be seen as an indicator of bullish momentum, where price is increasing at a relatively fast pace compared to previous periods.

The green dots help you spot when the price is moving upward rapidly, potentially signaling a good time to enter a long position or watch for further price action.

NOTE: It is vice versa for red dots.

Volatility_ZigZag_LibraryThis is a Pine Script library for the public indicator "Volatility ZigZag" by brettkind. For further description, please refer to the information available on the original indicator page.

Library "Volatility_ZigZag_Library"

getValues_andStyling_VolatilityZigZag_byBrettkind(hl_src, SOURCE, length, min_dev_input, stdev_fctr, ZigZag, zz_color, zz_width, zz_devline, zz_points, zz_alert_sign, ZZ_Label, ZZ_Label_clr, rev_text, zz_bars_text, pcabs_text, avg_pcabs_text, pcrel_text, avg_pcrel_text, vol_text, avg_vol_text, input_currency)

Parameters:

hl_src (bool)

SOURCE (float)

length (int)

min_dev_input (float)

stdev_fctr (float)

ZigZag (bool)

zz_color (color)

zz_width (int)

zz_devline (bool)

zz_points (bool)

zz_alert_sign (bool)

ZZ_Label (bool)

ZZ_Label_clr (color)

rev_text (bool)

zz_bars_text (bool)

pcabs_text (bool)

avg_pcabs_text (bool)

pcrel_text (bool)

avg_pcrel_text (bool)

vol_text (bool)

avg_vol_text (bool)

input_currency (string)

getStatisticTable_VolatilityZigZag_byBrettkind(x1, Y1_array, draw_tbl)

Parameters:

x1 (int)

Y1_array (array)

draw_tbl (bool)

Intraday Momentum for Volatile Stocks 29.09The strategy targets intraday momentum breakouts in volatile stocks when the broader market (Nifty) is in an uptrend. It enters long positions when stocks move significantly above their daily opening price with sufficient volume confirmation, then manages the trade using dynamic ATR-based stops and profit targets.

Entry Conditions

Price Momentum Filter: The stock must move at least 2.5% above its daily opening price, indicating strong bullish momentum. This percentage threshold is customizable and targets gap-up scenarios or strong intraday breakouts.

Volume Confirmation: Daily cumulative volume must exceed the 20-day average volume, ensuring institutional participation and genuine momentum. This prevents false breakouts on low volume.

Market Regime Filter: The Nifty index must be trading above its 50-day SMA, indicating a favorable market environment for momentum trades. This macro filter helps avoid trades during bearish market conditions.

Money Flow Index: MFI must be above 50, confirming buying pressure and positive money flow into the stock. This adds another layer of momentum confirmation.

Time Restriction: Trades are only initiated before 3:00 PM to ensure sufficient time for position management and avoid end-of-day volatility.

Exit Management

ATR Trailing Stop Loss: Uses a 3x ATR multiplier for dynamic stop-loss placement that trails higher highs, protecting profits while giving trades room to breathe. The trailing mechanism locks in gains as the stock moves favorably.

Profit Target: Set at 4x ATR above the entry price, providing a favorable risk-reward ratio based on the stock's volatility characteristics. This adaptive approach adjusts targets based on individual stock behavior.

Position Reset: Both stops and targets reset when not in a position, ensuring fresh calculations for each new trade.

Key Strengths

Volatility Adaptation: The ATR-based approach automatically adjusts risk parameters to match current market volatility levels. Higher volatility stocks get wider stops, while calmer stocks get tighter management.

Multi-Timeframe Filtering: Combines intraday price action with daily volume patterns and market regime analysis for robust signal generation.

Risk Management Focus: The strategy prioritizes capital preservation through systematic stop-loss placement and position sizing considerations.

Considerations for NSE Trading

This strategy appears well-suited for NSE intraday momentum trading, particularly for mid-cap and small-cap stocks that exhibit high volatility. The Nifty filter helps align trades with broader market sentiment, which is crucial in the Indian market context where sectoral and index movements strongly influence individual stocks.

The 2.5% threshold above open price is appropriate for volatile NSE stocks, though traders might consider adjusting this parameter based on the specific stocks being traded. The strategy's emphasis on volume confirmation is particularly valuable in the NSE environment where retail participation can create misleading price movements without institutional backin

Risk Management - Stop Loss Distance (Pips)This indicator helps traders estimate an optimal Stop Loss distance in pips based on market volatility (ATR) and a chosen risk percentage.

It does not generate buy or sell signals — it is purely a risk management visualization tool designed for educational and analytical use.

🔧 How it works

Calculates the current ATR (Average True Range) to measure market volatility.

Multiplies ATR by a user-defined factor to suggest a realistic stop-loss distance.

Displays this distance in pips, helping you understand how wide or tight your SL should be.

Optionally draws reference lines above and below the current price to visualize potential SL placement for long and short positions.

⚙️ Inputs

Account Balance (USD): Used for risk visualization.

Risk per Trade (%): Defines the percentage of account balance at risk.

ATR Period: Number of bars used to calculate volatility.

ATR Multiplier for SL: Adjusts how far the SL should be from the entry based on volatility.

Show SL Lines: Toggle visual stop-loss reference lines on or off.

📈 Display

The indicator shows:

Account balance and risk percentage.

Current ATR value.

Suggested stop-loss distance in pips.

Optional SL lines (for visualization only).

⚠️ Disclaimer

This script is for educational and analytical purposes only.

It does not provide financial advice or trade recommendations.

Use it at your own discretion and always manage risk responsibly.

Custom ATR with Paranormal Bar FilterCustom ATR with Paranormal Bar Filter

Description:

This indicator calculates a custom ATR (Average True Range) by filtering out bars with unusually large or small price ranges. It helps provide a more accurate measure of market volatility by ignoring outliers.

How it works:

True Range Calculation:

The price range for each bar is calculated.

Bars with ranges much larger or smaller than typical are excluded.

Filtered ATR:

The ATR is calculated using only the bars that pass the filter.

Current Bar Progress:

Measures how much the current bar has moved compared to the filtered ATR, based on the difference between its opening and closing prices.

Display:

A line represents the filtered ATR.

A table shows the filtered ATR, the current bar's range, and its progress relative to the ATR.

Input Settings:

ATR Period: Number of bars used to calculate the ATR.

Filter Window: Number of recent bars used to determine the typical range.

Filter Threshold: Sensitivity of the filter. A higher value allows more bars to pass.

How to Use:

Monitor Volatility:

Use the filtered ATR to understand market volatility while ignoring unusual price movements.

Track Current Bar Progress:

See how much of the ATR the current bar has completed.

Adjust Filter Settings:

Fine-tune the filter to match your trading timeframe and strategy.

This indicator is designed for traders who want to track market volatility without being misled by extreme outlier bars.

imbalances bandsThis indicator is designed to identify imbalances based on the calculation of the average of the highest and lowest prices. It forms a kind of band indicating correction points.

This indicator uses a total of 4 modified VWAPs, separated into 2 options that the user can activate or deactivate by checking or unchecking the options "Show imbalances bands VWAP 1" or "Show imbalances bands VWAP 2".

Let's talk about the first option, "Show imbalances bands VWAP 1". This displays 2 modified VWAPs on the screen, one in green and one in red, forming a kind of band that indicates possible points of imbalance in the market, signaling increased volatility between buying and selling. When the price tests the bands, it can be useful as there is a probability of a correction in the movement.

This can be particularly useful for those who trade using a scalping style, as it helps analyze when the price tests the bands. It can also be beneficial for trend traders because when the price tests one of the bands, there is a probability of a movement correction.

Now let's talk about the option "Show imbalances bands VWAP 2". It contains two modified VWAPs, one in purple and one in blue, which also form a kind of band. These bands also indicate the probability of a movement correction.

What is the difference between the Show imbalances bands VWAP 1 option and the Show imbalances bands VWAP 2 option?

The option "Show imbalances bands VWAP 2" consists of 2 modified volume-weighted moving averages that have a calculation checking the increase in volatility between the highest and lowest prices. One modified moving average is in purple, and the other modified moving average is in blue, forming a kind of two modified VWAPs.

The option "Show Imbalance Bands VWAP 1" consists of two modified moving averages using the absolute difference between the closing price and the moving average instead of the volume. This is particularly useful for assets where the volume is not a good indicator or is not available.

The option "Show Imbalance Bands VWAP 1" also has a calculation that checks for increased volatility between the highest and lowest prices. It features two modified moving averages, one in green and one in red.

This indicator can be adjusted according to the preferences and characteristics of the specific asset or market. It provides clear visual information and can be used as a complementary tool for technical analysis in trading strategies.

and Interesting period 5,20,50,80,200

Interesting imbalance setting 2.4, 3.3 ,4.2

Analysis Ideas: If you are following a trend, you can use this indicator to analyze how the price behaves around the bands. Since the imbalance bands indicate a probability of correction, it can be useful for identifying protection points or moments to be cautious, as there might be a probability of increased volatility.

Analysis Ideas2:For those trading using a scalping style, observe how the price behaves when it tests the imbalance band, as there may be a probability of increased volatility.

Please note that this indicator is designed for educational and informational purposes. Always conduct your own analysis and consider risk management strategies before making trading decisions.

Price over VolumeVersion 0.1

Price over Volume Indicator

Description

The Price over Volume indicator calculates the ratio of the closing price to the trading volume (price / volume) for the current chart's symbol and displays it as a histogram in a separate pane. A horizontal zero line is included as a reference to highlight positive and negative values or periods of undefined data (e.g., zero volume). The indicator is designed to help traders analyze the relationship between price movements and trading volume.

Insights Provided

Price-Volume Dynamics: The indicator shows how price per unit of volume fluctuates, offering insights into market efficiency and liquidity. High ratios may indicate low volume relative to price, suggesting potential volatility or thin markets, while low ratios may reflect high volume supporting price stability.

Trend and Momentum Analysis: Spikes or trends in the price-to-volume ratio can signal significant market events, such as buying/selling pressure or low liquidity periods, helping traders identify potential reversals or continuations.

Zero Line Reference: The zero line helps identify periods where the ratio is undefined (e.g., zero volume) or negative (if applicable), aiding in the interpretation of market conditions.

Volume Sensitivity: By normalizing price by volume, the indicator highlights how volume influences price movements, which is useful for assessing the strength of trends or breakouts.

How to Use

Setup: Apply the indicator to any chart with price and volume data (e.g., stocks, cryptocurrencies like BINANCE:BTCUSDT). The histogram appears in a separate pane below the main chart.

Interpretation :

High Ratios: Indicate low trading volume relative to price, potentially signaling overbought conditions or low liquidity. Use with caution in thin markets.

Low Ratios: Suggest high volume supporting price levels, indicating stronger market participation or stability.

Spikes: Watch for sudden increases in the ratio, which may precede volatility or significant price moves.

Zero Line: Periods where the histogram is absent (due to zero volume) indicate no trading activity, useful for identifying illiquid periods.

Trading Applications:

Confirmation Tool: Combine with other indicators (e.g., RSI, MACD) to confirm trend strength. A rising price-to-volume ratio with a price uptrend may indicate weakening volume support, suggesting a potential reversal.

Volume Analysis: Use alongside volume-based indicators (e.g., OBV, VWAP) to assess whether price movements are backed by sufficient volume.

Scalping/Day Trading: Monitor intraday ratio changes to identify high-impact periods with low volume, which may offer short-term trading opportunities.

Customization: Adjust the histogram color or style (e.g., change to line plot) via the Pine Editor to suit your preferences. Consider adding smoothing (e.g., moving average) for cleaner signals.

Notes

Data Requirements: Ensure the chart’s symbol has valid volume data. Symbols with no volume (e.g., some forex pairs) will result in undefined (na) values.

Limitations: The indicator is sensitive to zero-volume periods, which may cause gaps in the histogram. Use on high-liquidity symbols for best results.

Performance: Lightweight and efficient, suitable for all timeframes.

This indicator is ideal for traders seeking to understand the interplay between price and volume, offering a unique perspective on market dynamics for informed trading decisions.

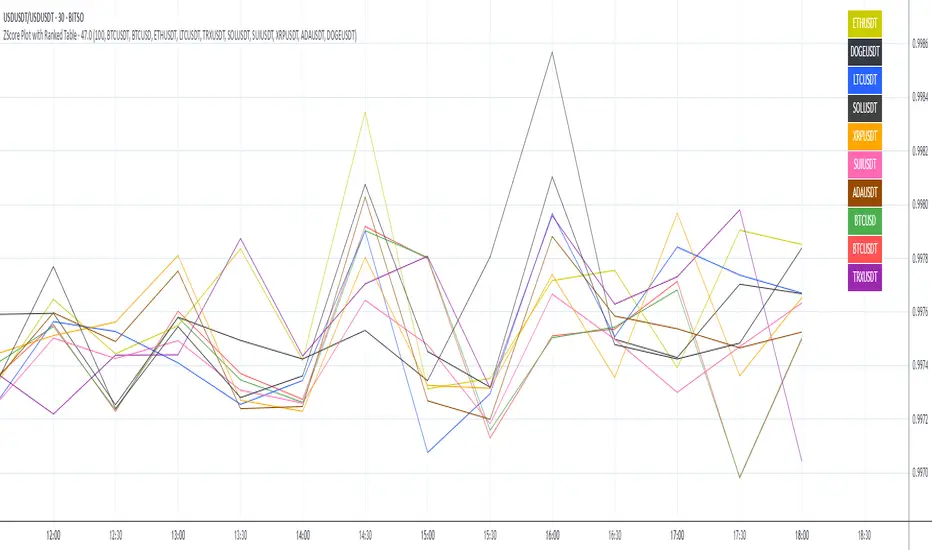

ZScore Plot with Ranked TableVersion 0.1

ZScore Plot with Ranked Table — Overview

This indicator visualizes the rolling ZScores of up to 10 crypto assets, giving traders a normalized view of log return deviations over time. It's designed for volatility analysis, anomaly detection, and clustering of asset behavior.

🎯 Purpose

• Show how each asset's performance deviates from its historical mean

• Identify potential overbought/oversold conditions across assets

• Provide a ranked leaderboard to compare asset behavior instantly

⚙️ Inputs

• Lookback: Number of bars to calculate mean and standard deviation

• Asset 1–10: Choose up to 10 symbols (e.g. BTCUSDT, ETHUSDT)

📈 Outputs

• ZScore Lines: Each asset plotted on a normalized scale (mean = 0, SD = 1)

• End-of-Line Labels: Asset names displayed at latest bar

• Leaderboard Table: Ranked list (top-right) showing:

◦ Asset name (color-matched)

◦ Final ZScore (rounded to 3 decimals)

🧠 Use Cases

• Quantitative traders seeking cross-asset momentum snapshots

• Signal engineers tracking volatility clusters

• Risk managers monitoring outliers and systemic shifts

ALT - ATR Percent Rank🔵 Description

The "ALT - ATR Percent Rank" indicator is a financial analysis tool designed to assess the volatility of an asset relative to its historical behavior, using the Average True Range (ATR) metric.

🔵 Purpose

The indicator aims to provide traders with insights into how the current volatility of an asset compares to its past levels. By evaluating the Percent Rank of the ATR, traders can determine if the current ATR value is high or low in the context of a specified historical period.

🔵 Functionality

• Asset and Timeframe Flexibility

Selectable Asset: Users can choose to apply the indicator to a different asset than the one currently displayed on the chart. This is particularly useful for comparing the volatility of multiple assets without switching charts.

Customizable Timeframe: The indicator can be set to analyze the ATR on different timeframes, regardless of the chart's current timeframe. This allows for multi-timeframe analysis without changing the view of the current chart.

• ATR Calculation

The Average True Range (ATR) is calculated over a user-defined number of bars (ATR Length). ATR is a commonly used measure of volatility that captures the degree of price movement per bar.

REF: Average True Range (ATR) Calculation

• Percent Rank Analysis

The indicator computes the Percent Rank of the current ATR value based on a specified lookback period (Percent Rank Lookback). This tells users how the current ATR compares to ATR values over the recent past, expressed as a percentile. For example, a Percent Rank of 90% indicates that the current ATR is higher than 90% of its values over the chosen lookback period, suggesting higher volatility.

• Visualization

The result is plotted as a line on a separate panel below the main trading chart, making it easy to view changes in volatility relative to historical levels.

🔵 Use Cases

• Trend Confirmation

Traders might use the indicator to confirm if a price movement is backed by significant volatility changes, which could validate the strength of a trend.

• Risk Management

Understanding when an asset is experiencing unusually high or low volatility could help in adjusting trading strategies, such as altering position sizes or setting stop-loss orders.

• Comparative Analysis

By enabling the analysis of different assets or timeframes, traders can perform comparative volatility studies, which can be essential in portfolio management or when seeking diversification opportunities.

This indicator is a valuable tool for traders who rely on volatility analysis to make informed trading decisions, providing a clear, quantifiable measure of how current market conditions compare to historical data.

Bollinger Bands with 3SD and BUY-SELL Basis*The white lines(both inner and outer ones) are from original Bollinger Bands (calculated as SMA20+SD and SMA20-SD).

*Inner lines are calculated with 2 Standard Deviation ( as classical Bollinger Bands ) and outer ones are with 3 Standard Deviation.

*3 SD calculation is important because, it is useful to investigate further the volatility.

*Classical Bollinger Bands Basis is included in calculations to obtain the bands, but the basis isn't plotted (SMA20).

*For Basis, a-13 bar EMA line is added which tells "BUY" when GREEN, and which tells "SELL" when RED.

*Generally, this code is good to further investigate the volatility especially by the help of 3SD lines. It is particularly important for crypto currencies which are generally highly volatile. On the other hand, the basis will tell BUY-SELL points and BUY-SELL points can be confirmed further, by investigating classical Bollinger Bands rules and anticipate about the volatility.

Real VIXReal VIX is showing us what we can expect from the volatility index. When Real VIX is falling, that means that market volatility will fall and there will be good uptrend.

When Real VIX is rising, that means that volatility will rise, and you can expect huge market movements

This code calculates the "Real VIX" indicator, which is a measure of market volatility. It uses data from various sources, including the High Yield Corporate Bond Index (HYG), the US Dollar Index (DXY), and various US Treasury bond yields, as well as the USDCAD currency pair.

The formula for Real VIX is complex, but it essentially calculates the difference between the current value of the VIX (a commonly used measure of market volatility) and a smoothed version of the VIX. This difference is then plotted on a chart, with green indicating that the market is less volatile than the smoothed version of the VIX suggests, and red indicating that the market is more volatile than expected.

The code also includes a warning for when the Real VIX falls below zero, which suggests that a recession may be on the horizon.

Multi-Crypto Principal Component AnalysisVersion 0.2

## 📌 Multi-Crypto Principal Component Analysis (PCA) — Indicator Summary

### 🎯 Purpose

This indicator identifies **cryptocurrency assets that are behaving differently** from the rest of the market, using a simplified approach inspired by Principal Component Analysis (PCA). It’s designed to help traders spot **cross-market divergences**, detect outliers, and improve asset selection and correlation-based strategies.

### ⚙️ How It Works

The indicator analyzes the **log returns** of up to 7 user-defined assets over a configurable lookback period (default: 100 bars). It computes the **z-score** (standardized deviation) for each asset’s return series and compares it against the average behavior of the group.

If an asset’s behavior deviates significantly (beyond a threshold of 1.5 standard deviations), it’s flagged as an **outlier**.

- Each outlier is plotted as a **colored dot horizontally spaced** above the price bar

- Up to **3 dots per bar** are shown for visual clarity

This PCA-style detection works in real time, directly on the chart, and gives you a quick overview of which assets are breaking correlation.

### 🔧 Inputs

- 🕒 **Lookback Period**: Number of bars to analyze (default: 100)

- 🔢 **Assets 1–7**: Choose any 7 crypto symbols from any exchange

- 🎨 **Colors**: Predefined per asset (e.g. BTCUSDT = red, ETHUSDT = yellow)

- 📈 **Threshold**: Internal (1.5 std dev); adjustable in code if needed

### 📊 Outputs

- 🟢 Dots above candles representing assets that are acting as outliers

- 🧠 Real-time clustering insight based on statistical deviation

- 🧭 Spatially spaced dots to avoid visual overlap when multiple outliers appear

### ⚠️ Limitations

- This is a **PCA-inspired approximation**, not true matrix-based PCA

- It does **not compute principal components or eigenvectors**

- Sensitivity may vary with asset volatility or sparse trading data

- Real PCA requires external tools like Python or R for full dimensional analysis

This tool is ideal for traders who want real-time crypto correlation insights without needing external data science platforms. It’s lightweight, fast, and highly visual — and gives you a powerful lens into market dislocations across multiple assets.

PumpC ATR Line LevelsPumpC ATR Line Levels

Overview

PumpC ATR Line Levels is a volatility-based indicator that projects potential expansion levels from the previous session’s close using the Average True Range (ATR). This tool builds upon the Previous OHLC framework created by Nephew_Sam_ by extending its session-handling logic and adding ATR-based levels, statistical tracking, and flexible visualization options.

How It Works

Calculates ATR from a user-selectable higher timeframe (default: Daily).

Projects levels above and below the previous session’s close (or current close when preview mode is enabled).

Supports up to 5 ATR multiples, each with independent toggles, colors, and labels.

Optionally displays only the most recent ATR session for clarity.

Includes a data table tracking how often ATR levels are reached or closed beyond.

Features

Configurable ATR timeframe and length (default: 21).

Default multiples: 0.30, 0.60, 0.90; optional: 1.236, 2.00.

Toggle for preview mode (using current close vs. locked prior session close).

Customizable line style, width, colors, and label placement.

Visibility filter to show only on chart TF ≤ 60 minutes.

Session statistics table with counts and percentages of level interactions.

Use Cases

Identify intraday expansion targets or stop placement zones based on volatility.

Evaluate historical tendencies of price respecting or breaking ATR bands.

Support volatility-adjusted trade planning with statistical validation.

Acknowledgment

This script was developed on top of the Previous OHLC indicator by Nephew_Sam_ , with major modifications to implement ATR-driven levels, extended statistics, and customizable table output.

Notes

This indicator does not generate buy/sell signals.

Best applied to intraday charts anchored to a higher-timeframe ATR.

Keep charts clean and avoid non-standard bar types when publishing.

RSI + ADX + ATR 18-01-25Combining RSI (Relative Strength Index), ADX (Average Directional Index), and ATR (Average True Range) creates a synergistic approach to technical analysis. This powerful trio covers momentum, trend strength, and volatility, providing comprehensive insights into market conditions. Here's a deeper exploration of their combined results:

1. Momentum Assessment with RSI

Purpose: RSI measures the speed and magnitude of recent price changes to determine overbought or oversold levels.

Benefit in Combination:

When RSI indicates overbought (above 70) or oversold (below 30) levels, it signals a potential reversal or correction.

However, these signals can be false in strongly trending markets, which is why ADX is used alongside it.

2. Trend Strength Confirmation with ADX

Purpose: ADX confirms the presence and strength of a trend.

Benefit in Combination:

If RSI shows a potential reversal but ADX indicates a strong trend (above 25), the trend is likely to continue, and RSI signals may need to be approached with caution.

Conversely, if ADX is below 20 (weak trend), RSI signals are more likely to indicate genuine reversals, as the market lacks a strong directional push.

3. Volatility Analysis with ATR

Purpose: ATR evaluates the level of price volatility.

Benefit in Combination:

High ATR values indicate volatile conditions where prices can move significantly; this helps in setting wider stop-loss levels to avoid premature exits.

Low ATR values suggest quieter markets, where tighter stop-losses and profit targets are more suitable.

FVG ATRFVG ATR — Fair Value Gap Size Measured in ATR Units

This Pine Script v6 indicator detects Fair Value Gaps and displays their size as a ratio of the Average True Range, providing traders with a normalized measurement of gap significance across different market conditions and timeframes.

Key Features

Automatic FVG Detection

The indicator identifies bullish and bearish Fair Value Gaps using the standard three-candle pattern. Bullish FVGs occur when the current low exceeds the high from two bars ago, while bearish FVGs occur when the current high falls below the low from two bars ago.

ATR Ratio Calculation

Each detected FVG is measured against the current Average True Range at the moment of detection. The ratio is displayed as a compact label next to the gap, showing values like "ATR: 0.75" or "ATR: 1.41". This normalization allows comparison of gap significance across volatile and calm market periods.

Minimal Visual Footprint

Labels are displayed directly on the chart without boxes or lines, using customizable text sizes from tiny to large. The default tiny size ensures the chart remains uncluttered while providing essential information at a glance.

Highly Customizable Display

All visual aspects are configurable through input parameters, including label position (top, middle, or bottom of gap), text size, text color, optional background, and horizontal offset from the detection candle.

Customizable Parameters

Detection Settings

Detect Bullish FVG: Enable or disable detection of bullish gaps. Default is enabled.

Detect Bearish FVG: Enable or disable detection of bearish gaps. Default is enabled.

Min Size (pips): Filter out small gaps below the specified threshold. One pip equals 10 ticks for most Forex pairs. Default is 10 pips.

ATR Calculation

ATR Period: Period length for Average True Range calculation. Default is 14, adjustable to match your trading strategy.

Label Settings

Label Position: Vertical placement of the text label relative to the FVG zone. Options are Top, Middle, or Bottom. Default is Middle.

Label Size: Text size from Tiny (smallest), Small, Normal, to Large. Default is Tiny for minimal chart clutter.

Text Color: Custom color for label text. Default is white for visibility on dark themes.

Show Background: Toggle to display labels with a colored background box or as transparent text only. Default is disabled for cleaner appearance.

Background Color: Custom color for label background when enabled. Default is semi-transparent gray.

Label Offset (bars): Horizontal distance in bars between the detection candle and the label. Set to 0 for labels directly on the candle, or increase for separation. Default is 0.

Recommended Use Cases

Multi-Timeframe Analysis

Compare FVG significance across different timeframes by observing ATR ratios. A 1.5 ATR gap on the 1-hour chart may indicate different significance than the same ratio on the daily chart.

Volatility-Adjusted Trading

Use ATR ratios to filter for only the most significant gaps. For example, only trade FVGs with ratios above 1.0 to focus on gaps larger than typical price movement.

Risk Management

Size positions based on gap magnitude relative to current volatility. Larger ATR ratios may warrant tighter stops or smaller position sizes.

Market Efficiency Analysis

Track how quickly and completely different-sized gaps get filled. Gaps with higher ATR ratios may take longer to fill or act as stronger support and resistance zones.

Technical Details

This indicator is written in Pine Script v6 and follows all recommended coding standards including strict 4-space indentation, lazy boolean evaluation, and proper type declarations. The script uses array-based storage to maintain up to 500 labels simultaneously.

The ATR ratio is calculated at the moment of FVG detection and remains fixed, never repainting. The calculation divides the FVG height (distance between gap boundaries) by the current ATR value using the specified period. Division by zero is protected with conditional logic.

Label positioning uses the xloc.bar_index and yloc.price system for precise placement. The horizontal offset parameter allows traders to adjust label spacing based on chart zoom level and personal preference. Text formatting uses str.tostring with two decimal places for clear ratio display.

Important Notes

The indicator never repaints as all FVG detections and ATR calculations are fixed upon bar confirmation. Labels persist on the chart until the maximum label count is reached, at which point the oldest labels are automatically removed by TradingView.

For optimal performance on charts with many FVGs, consider increasing the minimum pip size filter or using smaller label sizes. The tiny size option provides the smallest possible text for maximum chart clarity.

Installation and Usage

Copy the source code into the TradingView Pine Editor and add the indicator to your chart. The overlay parameter is set to true, allowing labels to display directly on price candles. Configure all parameters through the indicator settings panel to match your trading style and visual preferences.

100% Pine Script v6 indicator — No repaint — Open source

[BMAX] Averan BB(ENGLISH)

Averan is an indicator based on ADR, which shows the volatility of the market based on high-low prices on the selected timeframe. The difference between Averan and ATR is that Averan does not consider GAPs, so it basically consider the actual size of the candles.

This indicator also includes a standard deviation representation, the same as the top portion of the bollinger bands to present the variance of the volatility.

(PORTUGUÊS)

Averan é um indicador baseado no ADR, que apresenta a volatilidade do mercado baseado em máximas e mínimas do tempo gráfico escolhido. A diferença do Averan para o ATR é que o Averan não considera GAPs, portanto é basicamente calculado pelo real tamanho dos candles.

Este indicador também inclui a representação do desvio padrão, representado da mesma maneira que a banda superior do Bollinger Bands, apresentando portanto a variância da volatilidade.

VIX/VIX3M Ratio計算並顯示 CBOE:VIX 和 CBOE:VIX3M 的比率,幫助交易者評估市場的波動性。

當比率超過設定的高水平或低於低水平時,指標將顯示為紅色,提示潛在的市場異常情況。

Calculates and displays the ratio of CBOE:VIX to CBOE:VIX3M, helping traders assess market volatility.

When the ratio exceeds the set high level or falls below the low level, the indicator will be displayed in red, signaling potential market anomalies.

Bar Width Percent RankA simple script to calculate and show the current percent rank of the absolute open - close (candle bar width) over a given period.

Useful to determine the current volatility.

A higher value indicates that the current period is having a big swing.

No SurpriseNever be surprised about a sudden price move. Just a twist on B.bands, really.

Basically, how big of a price change you should expect based on recent volatility.

Check out the " Surprise " indicator to verify how surprised we were in the past.

Real Time UVXY Spike Level TrackerKey Features

Real Time All-Time Low Tracking: Continuously updates the ATL using daily timeframe data.

Multiple Spike Levels: Displays +20%, +50%, +75%, and +100% levels above the ATL.

Real-Time Spike Percentage: Shows current distance from ATL in an easy-to-read table.

Understanding the Chart Lines

Red Line (ATL): The all-time low baseline. This is your reference point for measuring volatility spikes.

Yellow Line (+20%): First level of moderate volatility increase. Minor market stress or routine volatility expansion.

Blue Line (+50%): Significant volatility event. Indicates elevated market concern or technical dislocation.

Purple Line (+75%): Major volatility spike. Typically coincides with substantial market selloffs or uncertainty.

Fuchsia Line (+100%): Extreme volatility event. Rare occurrences associated with market crashes, black swan events, or severe panic.

The Data Table Displays: Current Spike %: Real-time percentage showing how far price is above the ATL (highlighted in green)

Level Column: Each spike threshold level

Price Column: Exact price at each level for quick reference

Understanding UVXY spike levels is valuable for several reasons:

Market Timing & Entry/Exit Points UVXY typically experiences extreme spikes during market panics or crashes. Knowing historical spike levels helps you:

Identify extreme fear levels - When UVXY hits unusually high levels, it often signals peak panic and potential market bottoms

Avoid chasing volatility - Understanding what constitutes an "extreme" spike prevents buying in after the move is already exhausted Mean Reversion Trading

UVXY has a strong tendency to decay over time due to its leveraged structure and the contango in VIX futures. Spike levels matter because:

High probability reversals - When UVXY reaches extreme levels (say 2-3x normal), there's historically been a high probability of reversion

Risk/reward assessment - You can better evaluate whether a short position or volatility-selling strategy makes sense Leveraged ETF enthusiasts and volatility traders often use specific spike percentages as triggers to open short positions. For example, some traders might short when UVXY spikes 5-50%+ in a week or reaches certain percentage thresholds, betting on the inevitable decay back down