ATR % of yesterday close with SMA (Bull/Bear colored)This script visualizes the Average True Range (ATR) as a percentage of a user-selected price point for a quick view of volatility.

ATR % values are plotted as a color-coded histogram. Bullish days (close > prior close) paint the bar green; bearish days (close < prior close) paint it red; unchanged days are gray.

Two simple moving average (SMA) overlays to reveal volatility trends.

Variables:

Histogram bars represent ATR as a % of one of:

- Previous Close (default option)

- Previous Open

- Today Close

- Today Open

Two SMA lines (default: blue for 20-period, orange for 5-period) shown on ATR % for trend/range regime tracking.

Optionally display the ATR % in continuous line (yellow)—hidden by default.

If you find it helpful, feel free to share any feedback and how you incorporate it into your trading strategy with the community!

在腳本中搜尋"Volatility"

SmartScale Envelope DCA This is a Dollar-Cost Averaging (DCA) long strategy that buys when price dips below a moving average envelope and adds to the position in a stepwise, risk-controlled way. It uses up to 8 buy-ins, applies a cooldown between entries, and exits based on either a take profit from average entry price or a stop loss. Backtest range limits trades to the last 365 days for backtest control.

All input settings can and should be adjusted to the chart, as volatility in price action varies. Simply go into the inputs settings, and start from the top and move down to get better backtest results. Moving from the top down has been proven to give the best results. Then, move to properties and set your order size, pyramiding, and so on. It may be necessary to then fine tune your adjustments a second time to dial it in.

Works well on 1 hour time frames and in volatility.

Happy Trading!

Scalping 15min: EMA + MACD + RSI + ATR-based SL/TP📈 Strategy: 15-Minute Scalping — EMA + MACD + RSI + ATR-based SL/TP

This scalping strategy is designed for 15-minute charts and combines trend-following and momentum confirmation with dynamic stop loss and take profit levels based on volatility.

🔧 Indicators Used:

EMA 50 — identifies the main trend

MACD Histogram — confirms momentum direction

RSI (14) — filters overbought/oversold conditions

ATR (14) — dynamically sets SL and TP based on market volatility

📊 Entry Conditions:

Long Entry:

Price is above EMA 50

MACD histogram is positive

RSI is above 50 but below 70

Short Entry:

Price is below EMA 50

MACD histogram is negative

RSI is below 50 but above 30

🛑 Risk Management:

Stop Loss: 1×ATR (user-configurable)

Take Profit: 2×ATR (user-configurable)

These values can be adjusted in the script inputs depending on your risk/reward preference or market conditions.

⚠️ Notes:

Strategy is optimized for scalping fast-moving pairs (e.g. crypto, forex).

Works best in trending markets.

Use backtesting and forward testing before live trading.

ATR PercentageThe ATR is a great indicator, but for me, it does not define the volatility of an asset I am looking at well enough. So I've adjusted it to be displayed as the usual ATR and a percentage of the closing prince (which to me tells a better story). I find this useful if I am looking through many assets and have to create a quick picture of volatility.

Indicator Definition: The script starts by defining an indicator named "ATR Percentage" that will be displayed in a separate pane (not overlayed on the price chart).

Input for ATR Period: The user can set the period for calculating the ATR through an input field.

ATR Calculation: The ta.atr function calculates the Average True Range based on the specified period.

ATR Percentage Calculation: The ATR value is converted to a percentage of the current closing price using (atrValue / close) * 100.

Plotting:

The script plots both the ATR value and its percentage on the chart.

A horizontal line at zero is added for reference.

Label Display: An optional label displays the current ATR percentage at every 10th bar to avoid cluttering the chart.

Background Color: A light blue background is added to visually separate the ATR indicator from other indicators.

Volatility Adjusted MomentumIt's a script that computes volatility-adjusted momentum indicators.

The problem with the momentum indicator is that it's absolute and it's hard to interpret its value. For example, if you'll change the timeframe or instrument value of Momentum will be very different.

We tried to solve that by expressing momentum in volatility. This way you can easier spot overbought/oversold values.

You can choose to use Standard Deviation or ATR for adjustments.

Thanks to @MUQWISHI for helping me code it.

Disclaimer

Please remember that past performance may not be indicative of future results.

Due to various factors, including changing market conditions, the strategy may no longer perform as well as in historical backtesting.

This post and the script don’t provide any financial advice.

ATR GainThis indicator shows the amount, in terms of a percentage, that the ATR is currently above or below the current ATR average.

This can be translated to the amount of volatility in the market compared to the current "standard" volatility.

See also "Average True Range" technical indicator

3Commas Visible DCA StrategyThis strategy consists of the following elements and can all be set by the user.

1. Entry by moving average cross.

1) Selection of moving average line.

- SMA(Simple Moving Average)

- EMA(Exponential Moving Average)

- HMA(Hull Moving Average)

2) Selection of Cross over / Cross under

2. Add Entry by DCA(Dollar Cost Averaging)

- A DCA strategy is the practice of investing into a currency at preset intervals to reduce the entry price of a position over time and mitigate volatility risk.

For example,

Base Order = 10 Dollar at Price 100%

Safety Order1 = 20 Dollar at Price 90%

Safety Order2 = 40 Dollar at Price 80%

Average Price => Price 80~90%

thereby getting a better average price for your position and greatly reducing risks from the consequences of volatility.

3. Target Price and Stop Loss.

1) Target Price : Realize profits at % set from the average unit price.

2) Stop Loss : Stop Loss % set from the last safety order.

You can easily find out what's related by changing the setting value after setting the strategy.

This strategy has the following Good characteristics.

1. It informs you of the assets required according to DCA settings.

If you are short of assets, a warning sign will appear.

2. Amount of assets invested in each long entry and long entry close.

3. Visibility of the lowest purchase price line and DCA purchase location according to DCA setting.

easily check the values set in the backtest.

I hope it will help you. Thank you.

Initial templateI have created a starting template for strategies.

It allows quick control of turning on/off long and short conditions, or disabling them entirely.

It includes trade filters for strategy equity and volatility. If there is not enough volatility it will not trade, or if the strategy equity is below the equity ema it will not trade.

It has standard stops and limits.

Simply change the long/short conditions!

BB_Keltner Firing Squeeze by RMThis script shows the Squeeze firing event, after the Bollinger Bands have been inside Keltner Channels, indicating possible short term trend of price action.

Based on Bollinger Bands & Keltner Channels scripts in the Pine scripts library.

Bollinger Bands are a type of statistical chart characterizing the prices and volatility over time of a financial instrument or commodity, using a formulaic method propounded by John Bollinger in the 1980s.

Keltner channel is a technical analysis indicator showing a central moving average line plus channel lines at a distance above and below. The indicator is named after Chester W. Keltner (1909–1998)

Squeeze is an event in the price action of a given market instrument that happens when Bollinger Bands are inside the Keltner Channels, thus indicating build up of volatility. The Firing event is the first candle not in a squeeze after the squeeze event, that releases the price action on a given direction with a given impulse that makes is last several candles. Markets are volatile and can change directions due to several reasons not accounted in this method. Use at you own discretion and evaluate your risk before proceeding.

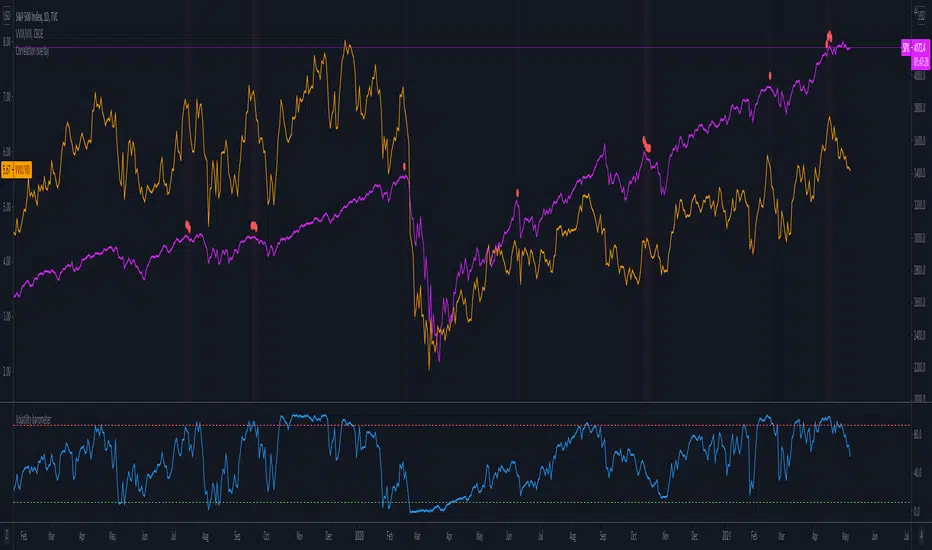

Volatility barometerIt is the indicator that analyzes the behaviour of VIX against CBOE volaility indices (VIX3M, VIX6M and VIX1Y) and VIX futures (next contract to the front one - VX!2). Because VIX is a derivate of SPX, the indicator shall be used on the SPX chart (or equivalent like SPY).

When the readings get above 90 / below 10, it means the market is overbought / oversold in terms of implied volatility. However, it does not mean it will reverse - if the price go higher along with the indicator readings then everything is fine. There is an alarming situation when the SPX is diverging - e.g. the price go higher, the readings lower. It means the SPX does not play in the same team as IVOL anymore and might reverse.

You can use it in conjunction with other implied volatility indicators for stronger signals: the Correlation overlay ( - the indicator that measures the correlation between VVIX and VIX) and VVIX/VIX ratio (it generates a signal the ratio makes 50wk high).

Difference In PriceWith the difference in price indicator, you can view price change volatility. Specifically, you can view the difference in price for a single candle segment, at any desired candlestick timeframe. This simply takes the sessions high minus the low and gives the difference. Difference in price trend lines help determine if a stock has a history of high volatility or not. This is useful for those looking to invest in stable stocks.

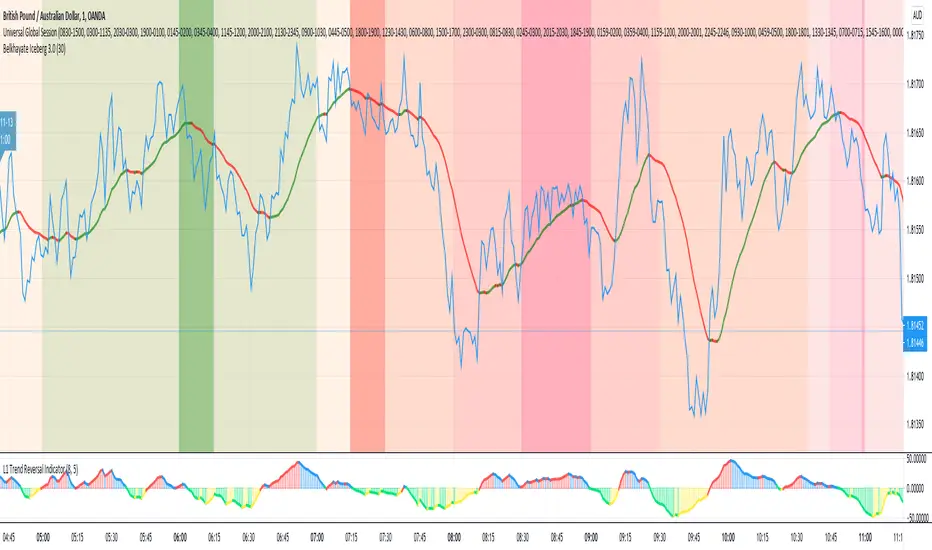

Universal Global SessionUniversal Global Session

This Script combines the world sessions of: Stocks, Forex, Bitcoin Kill Zones, strategic points, all configurable, in a single Script, to capitalize the opening and closing times of global exchanges as investment assets, becoming an Universal Global Session .

It is based on the great work of @oscarvs ( BITCOIN KILL ZONES v2 ) and the scripts of @ChrisMoody. Thank you Oscar and Chris for your excellent judgment and great work.

At the end of this writing you can find all the internet references of the extensive documentation that I present here. To maximize your benefits in the use of this Script, I recommend that you read the entire document to create an objective and practical criterion.

All the hours of the different exchanges are presented at GMT -6. In Market24hClock you can adjust it to your preferences.

After a deep investigation I have been able to show that the different world sessions reveal underlying investment cycles, where it is possible to find sustained changes in the nominal behavior of the trend before the passage from one session to another and in the natural overlaps between the sessions. These underlying movements generally occur 15 minutes before the start, close or overlap of the session, when the session properly starts and also 15 minutes after respectively. Therefore, this script is designed to highlight these particular trending behaviors. Try it, discover your own conclusions and let me know in the notes, thank you.

Foreign Exchange Market Hours

It is the schedule by which currency market participants can buy, sell, trade and speculate on currencies all over the world. It is open 24 hours a day during working days and closes on weekends, thanks to the fact that operations are carried out through a network of information systems, instead of physical exchanges that close at a certain time. It opens Monday morning at 8 am local time in Sydney —Australia— (which is equivalent to Sunday night at 7 pm, in New York City —United States—, according to Eastern Standard Time), and It closes at 5pm local time in New York City (which is equivalent to 6am Saturday morning in Sydney).

The Forex market is decentralized and driven by local sessions, where the hours of Forex trading are based on the opening range of each active country, becoming an efficient transfer mechanism for all participants. Four territories in particular stand out: Sydney, Tokyo, London and New York, where the highest volume of operations occurs when the sessions in London and New York overlap. Furthermore, Europe is complemented by major financial centers such as Paris, Frankfurt and Zurich. Each day of forex trading begins with the opening of Australia, then Asia, followed by Europe, and finally North America. As markets in one region close, another opens - or has already opened - and continues to trade in the currency market. The seven most traded currencies in the world are: the US dollar, the euro, the Japanese yen, the British pound, the Australian dollar, the Canadian dollar, and the New Zealand dollar.

Currencies are needed around the world for international trade, this means that operations are not dominated by a single exchange market, but rather involve a global network of brokers from around the world, such as banks, commercial companies, central banks, companies investment management, hedge funds, as well as retail forex brokers and global investors. Because this market operates in multiple time zones, it can be accessed at any time except during the weekend, therefore, there is continuously at least one open market and there are some hours of overlap between the closing of the market of one region and the opening of another. The international scope of currency trading means that there are always traders around the world making and satisfying demands for a particular currency.

The market involves a global network of exchanges and brokers from around the world, although time zones overlap, the generally accepted time zone for each region is as follows:

Sydney 5pm to 2am EST (10pm to 7am UTC)

London 3am to 12 noon EST (8pm to 5pm UTC)

New York 8am to 5pm EST (1pm to 10pm UTC)

Tokyo 7pm to 4am EST (12am to 9am UTC)

Trading Session

A financial asset trading session refers to a period of time that coincides with the daytime trading hours for a given location, it is a business day in the local financial market. This may vary according to the asset class and the country, therefore operators must know the hours of trading sessions for the securities and derivatives in which they are interested in trading. If investors can understand market hours and set proper targets, they will have a much greater chance of making a profit within a workable schedule.

Kill Zones

Kill zones are highly liquid events. Many different market participants often come together and perform around these events. The activity itself can be event-driven (margin calls or option exercise-related activity), portfolio management-driven (asset allocation rebalancing orders and closing buy-in), or institutionally driven (larger players needing liquidity to complete the size) or a combination of any of the three. This intense cross-current of activity at a very specific point in time often occurs near significant technical levels and the established trends emerging from these events often persist until the next Death Zone approaches or enters.

Kill Zones are evolving with time and the course of world history. Since the end of World War II, New York has slowly invaded London's place as the world center for commercial banking. So much so that during the latter part of the 20th century, New York was considered the new center of the financial universe. With the end of the cold war, that leadership appears to have shifted towards Europe and away from the United States. Furthermore, Japan has slowly lost its former dominance in the global economic landscape, while Beijing's has increased dramatically. Only time will tell how these death zones will evolve given the ever-changing political, economic, and socioeconomic influences of each region.

Financial Markets

New York

New York (NYSE Chicago, NASDAQ)

7:30 am - 2:00 pm

It is the second largest currency platform in the world, followed largely by foreign investors as it participates in 90% of all operations, where movements on the New York Stock Exchange (NYSE) can have an immediate effect (powerful) on the dollar, for example, when companies merge and acquisitions are finalized, the dollar can instantly gain or lose value.

A. Complementary Stock Exchanges

Brazil (BOVESPA - Brazilian Stock Exchange)

07:00 am - 02:55 pm

Canada (TSX - Toronto Stock Exchange)

07:30 am - 02:00 pm

New York (NYSE - New York Stock Exchange)

08:30 am - 03:00 pm

B. North American Trading Session

07:00 am - 03:00 pm

(from the beginning of the business day on NYSE and NASDAQ, until the end of the New York session)

New York, Chicago and Toronto (Canada) open the North American session. Characterized by the most aggressive trading within the markets, currency pairs show high volatility. As the US markets open, trading is still active in Europe, however trading volume generally decreases with the end of the European session and the overlap between the US and Europe.

C. Strategic Points

US main session starts in 1 hour

07:30 am

The euro tends to drop before the US session. The NYSE, CHX and TSX (Canada) trading sessions begin 1 hour after this strategic point. The North American session begins trading Forex at 07:00 am.

This constitutes the beginning of the overlap of the United States and the European market that spans from 07:00 am to 10:35 am, often called the best time to trade EUR / USD, it is the period of greatest liquidity for the main European currencies since it is where they have their widest daily ranges.

When New York opens at 07:00 am the most intense trading begins in both the US and European markets. The overlap of European and American trading sessions has 80% of the total average trading range for all currency pairs during US business hours and 70% of the total average trading range for all currency pairs during European business hours. The intersection of the US and European sessions are the most volatile overlapping hours of all.

Influential news and data for the USD are released between 07:30 am and 09:00 am and play the biggest role in the North American Session. These are the strategically most important moments of this activity period: 07:00 am, 08:00 am and 08:30 am.

The main session of operations in the United States and Canada begins

08:30 am

Start of main trading sessions in New York, Chicago and Toronto. The European session still overlaps the North American session and this is the time for large-scale unpredictable trading. The United States leads the market. It is difficult to interpret the news due to speculation. Trends develop very quickly and it is difficult to identify them, however trends (especially for the euro), which have developed during the overlap, often turn the other way when Europe exits the market.

Second hour of the US session and last hour of the European session

09:30 am

End of the European session

10:35 am

The trend of the euro will change rapidly after the end of the European session.

Last hour of the United States session

02:00 pm

Institutional clients and very large funds are very active during the first and last working hours of almost all stock exchanges, knowing this allows to better predict price movements in the opening and closing of large markets. Within the last trading hours of the secondary market session, a pullback can often be seen in the EUR / USD that continues until the opening of the Tokyo session. Generally it happens if there was an upward price movement before 04:00 pm - 05:00 pm.

End of the trade session in the United States

03:00 pm

D. Kill Zones

11:30 am - 1:30 pm

New York Kill Zone. The United States is still the world's largest economy, so by default, the New York opening carries a lot of weight and often comes with a huge injection of liquidity. In fact, most of the world's marketable assets are priced in US dollars, making political and economic activity within this region even more important. Because it is relatively late in the world's trading day, this Death Zone often sees violent price swings within its first hour, leading to the proven adage "never trust the first hour of trading in America. North.

---------------

London

London (LSE - London Stock Exchange)

02:00 am - 10:35 am

Britain dominates the currency markets around the world, and London is its main component. London, a central trading capital of the world, accounts for about 43% of world trade, many Forex trends often originate from London.

A. Complementary Stock Exchange

Dubai (DFM - Dubai Financial Market)

12:00 am - 03:50 am

Moscow (MOEX - Moscow Exchange)

12:30 am - 10:00 am

Germany (FWB - Frankfurt Stock Exchange)

01:00 am - 10:30 am

Afríca (JSE - Johannesburg Stock Exchange)

01:00 am - 09:00 am

Saudi Arabia (TADAWUL - Saudi Stock Exchange)

01:00 am - 06:00 am

Switzerland (SIX - Swiss Stock Exchange)

02:00 am - 10:30 am

B. European Trading Session

02:00 am - 11:00 am

(from the opening of the Frankfurt session to the close of the Order Book on the London Stock Exchange / Euronext)

It is a very liquid trading session, where trends are set that start during the first trading hours in Europe and generally continue until the beginning of the US session.

C. Middle East Trading Session

12:00 am - 06:00 am

(from the opening of the Dubai session to the end of the Riyadh session)

D. Strategic Points

European session begins

02:00 am

London, Frankfurt and Zurich Stock Exchange enter the market, overlap between Europe and Asia begins.

End of the Singapore and Asia sessions

03:00 am

The euro rises almost immediately or an hour after Singapore exits the market.

Middle East Oil Markets Completion Process

05:00 am

Operations are ending in the European-Asian market, at which time Dubai, Qatar and in another hour in Riyadh, which constitute the Middle East oil markets, are closing. Because oil trading is done in US dollars, and the region with the trading day coming to an end no longer needs the dollar, consequently, the euro tends to grow more frequently.

End of the Middle East trading session

06:00 am

E. Kill Zones

5:00 am - 7:00 am

London Kill Zone. Considered the center of the financial universe for more than 500 years, Europe still has a lot of influence in the banking world. Many older players use the European session to establish their positions. As such, the London Open often sees the most significant trend-setting activity on any trading day. In fact, it has been suggested that 80% of all weekly trends are set through the London Kill Zone on Tuesday.

F. Kill Zones (close)

2:00 pm - 4:00 pm

London Kill Zone (close).

---------------

Tokyo

Tokyo (JPX - Tokyo Stock Exchange)

06:00 pm - 12:00 am

It is the first Asian market to open, receiving most of the Asian trade, just ahead of Hong Kong and Singapore.

A. Complementary Stock Exchange

Singapore (SGX - Singapore Exchange)

07:00 pm - 03:00 am

Hong Kong (HKEx - Hong Kong Stock Exchange)

07:30 pm - 02:00 am

Shanghai (SSE - Shanghai Stock Exchange)

07:30 pm - 01:00 am

India (NSE - India National Stock Exchange)

09:45 pm - 04:00 am

B. Asian Trading Session

06:00 pm - 03:00 am

From the opening of the Tokyo session to the end of the Singapore session

The first major Asian market to open is Tokyo which has the largest market share and is the third largest Forex trading center in the world. Singapore opens in an hour, and then the Chinese markets: Shanghai and Hong Kong open 30 minutes later. With them, the trading volume increases and begins a large-scale operation in the Asia-Pacific region, offering more liquidity for the Asian-Pacific currencies and their crosses. When European countries open their doors, more liquidity will be offered to Asian and European crossings.

C. Strategic Points

Second hour of the Tokyo session

07:00 pm

This session also opens the Singapore market. The commercial dynamics grows in anticipation of the opening of the two largest Chinese markets in 30 minutes: Shanghai and Hong Kong, within these 30 minutes or just before the China session begins, the euro usually falls until the same moment of the opening of Shanghai and Hong Kong.

Second hour of the China session

08:30 pm

Hong Kong and Shanghai start trading and the euro usually grows for more than an hour. The EUR / USD pair mixes up as Asian exporters convert part of their earnings into both US dollars and euros.

Last hour of the Tokyo session

11:00 pm

End of the Tokyo session

12:00 am

If the euro has been actively declining up to this time, China will raise the euro after the Tokyo shutdown. Hong Kong, Shanghai and Singapore remain open and take matters into their own hands causing the growth of the euro. Asia is a huge commercial and industrial region with a large number of high-quality economic products and gigantic financial turnover, making the number of transactions on the stock exchanges huge during the Asian session. That is why traders, who entered the trade at the opening of the London session, should pay attention to their terminals when Asia exits the market.

End of the Shanghai session

01:00 am

The trade ends in Shanghai. This is the last trading hour of the Hong Kong session, during which market activity peaks.

D. Kill Zones

10:00 pm - 2:00 am

Asian Kill Zone. Considered the "Institutional" Zone, this zone represents both the launch pad for new trends as well as a recharge area for the post-American session. It is the beginning of a new day (or week) for the world and as such it makes sense that this zone often sets the tone for the remainder of the global business day. It is ideal to pay attention to the opening of Tokyo, Beijing and Sydney.

--------------

Sidney

Sydney (ASX - Australia Stock Exchange)

06:00 pm - 12:00 am

A. Complementary Stock Exchange

New Zealand (NZX - New Zealand Stock Exchange)

04:00 pm - 10:45 pm

It's where the global trading day officially begins. While it is the smallest of the megamarkets, it sees a lot of initial action when markets reopen Sunday afternoon as individual traders and financial institutions are trying to regroup after the long hiatus since Friday afternoon. On weekdays it constitutes the end of the current trading day where the change in the settlement date occurs.

B. Pacific Trading Session

04:00 pm - 12:00 am

(from the opening of the Wellington session to the end of the Sydney session)

Forex begins its business hours when Wellington (New Zealand Exchange) opens local time on Monday. Sydney (Australian Stock Exchange) opens in 2 hours. It is a session with a fairly low volatility, configuring itself as the calmest session of all. Strong movements appear when influential news is published and when the Pacific session overlaps the Asian Session.

C. Strategic Points

End of the Sydney session

12:00 am

---------------

Conclusions

The best time to trade is during overlaps in trading times between open markets. Overlaps equate to higher price ranges, creating greater opportunities.

Regarding press releases (news), it should be noted that these in the currency markets have the power to improve a normally slow trading period. When a major announcement is made regarding economic data, especially when it goes against the predicted forecast, the coin can lose or gain value in a matter of seconds. In general, the more economic growth a country produces, the more positive the economy is for international investors. Investment capital tends to flow to countries that are believed to have good growth prospects and subsequently good investment opportunities, leading to the strengthening of the country's exchange rate. Also, a country that has higher interest rates through its government bonds tends to attract investment capital as foreign investors seek high-yield opportunities. However, stable economic growth and attractive yields or interest rates are inextricably intertwined. It's important to take advantage of market overlaps and keep an eye out for press releases when setting up a trading schedule.

References:

www.investopedia.com

www.investopedia.com

www.investopedia.com

www.investopedia.com

market24hclock.com

market24hclock.com

Mean Deviation Detector - Throw Out All Other IndicatorsI set out this morning to create a script that searches out price moves that went too far too fast relative to historical pricing, given that such situations often result in the most profitable trading opportunities. I came up with the mean deviation detector. This script should be used as a means of judging how far a price is trading, in percent terms, from it's "average trading zone".

This is extremely helpful in a couple scenarios.

First, it can be used to judge a move's volatility relative to it's previous volatility. Put simply, a 5% move in the stock of Coca Cola is a lot more meaningful than a 5% move in the stock of Tesla, and the detector puts moves into historical (visual) perspective.

Second, the indicator can be used in real time as a means of determining when the chances of mean reversion are high or low. Extreme values are unsustainable and often lead to EITHER A.) price mean reversion or B.) time mean reversion. Put simply, prices either went too far and are due to fall back to a historical mean, or they need more time to digest a potentially new pricing zone.

Without getting too deep into volume profile analysis, the MDD can be a simple way of telling that a stock has moved into an "air pocket", where prices will either come back to the previous volume node (price mean reversion) or set up shop in a new, uncharted area (time mean reversion).

An extreme value doesn't always mean a trading opportunity, but it means that something interesting is happening in the stock / instrument.

I use this indicator to help me trade covered calls. Lots of high yielding weekly opportunities are stocks that have moved too far too fast, and I like to use this indicator as a means of either a.) scooping up stocks that have gotten beat up from a historical mean perspective & have likely seen the risk already "beaten" out of them, or to b.) stay away from stocks that have a very high chance of price correcting lower. In situations where I say that the risk has been "beaten" out of something, it doesn't mean that the stock won't continue to fall, it simply means that the degree and acceleration of the fall has peaked and that risk premiums in selling options will / should easily pay for continued losses. In the event that it's a price correction and not a time correction, you also increase your bat rate because you get auto-liquidated at a max profit. It's a really valuable tool in my kit.

You can also feel free to put a Keltner Chanel overlay onto the MDD to filter out noise, identify "extreme" values, and place mean reversion trades if you expect price mean reversion is likely, if you want to use this as the basis of a proper trading strategy. For a high extreme value, you could sell short term OTM call spreads, for example.

The MDD is adaptable to your own trading style & preferences.

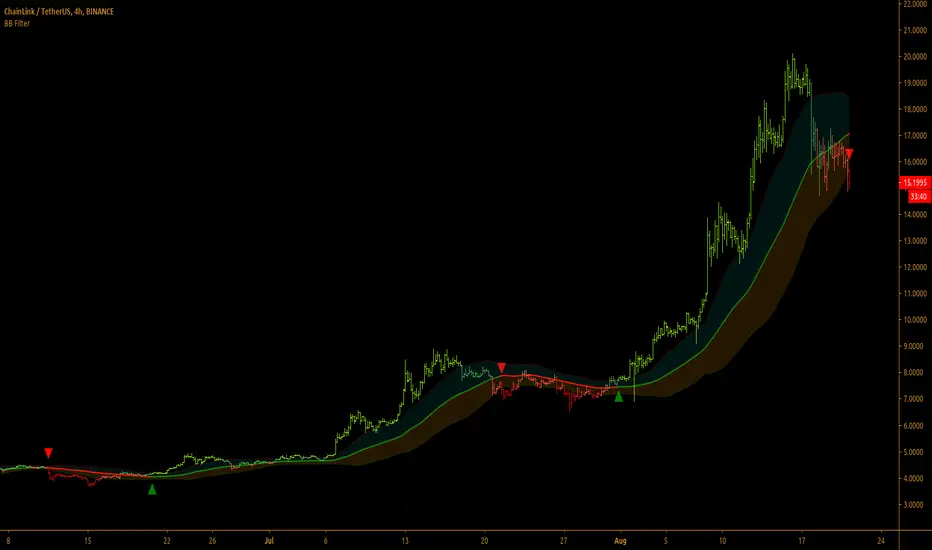

Bollinger Bands Filter

Bollinger Bands is a classic indicator that uses a simple moving average of 20 periods, along with plots of upper and lower bands that are 2 standard deviations away from the basis line. These bands help visualize price volatility and trend based on where the price is, in relation to the bands.

Bollinger Bands filter plots a long signal when price closes above the upper band and plots a short signal when price closes below the lower band. It doesn't take into account any other parameters such as Volume/RSI/ Fundamentals etc, so user must use discretion based on confirmations from another indicator or based on fundamentals.

The filter works great when the price closes above/below upper/lower bands with continuation on next bar. It is definitely useful to have this filter along with other indicators to get early glimpse of breach/fail of bands on candle close during BB squeeze or based on volatility.

This can be used on Heikin Ashi candles for spotting trends, but HA candles are not recommended for trade entries as they don't reflect true price of the asset.

This filter's default is 55 SMA and 1 standard deviation, but these can be changed from settings.

It is definitely worth reading the 22 rules of Bollinger Bands written by John Bollinger.

==================================================================

Note:

1. Alerts can be created for long and short signals using "Once per bar close".

2. The indicator doesn't repaint.

==================================================================

Trend Cloud with Buy/Sell Text [wjdtks255]Indicator Title: Trend Cloud with Buy/Sell Signal Pro

Short Description

A high-probability trend-following indicator based on Supertrend dynamics, enhanced with a Volume Filter to pinpoint explosive entries while minimizing false breakouts.

Detailed Description (Overview)

The Trend Cloud with Buy/Sell Text is designed for traders who prioritize clarity and momentum. It visualizes market trends through a "Trend Cloud" system and generates real-time BUY/SELL signals only when price action is backed by significant trading volume.

Key Technical Pillars

Dynamic Trend Cloud: Fills the area between the price and the Supertrend line, providing immediate visual feedback on trend strength and potential support/resistance zones.

Smart Volume Filter: A unique logic that compares current volume against a 20-period moving average. Labels only appear when a trend shift occurs with above-average volume, filtering out weak "fakeouts."

No-Repaint Labels: Signals are calculated and fixed at the close of the candle, ensuring that the BUY/SELL text remains permanent for reliable historical backtesting and live execution.

The Alpha Hunter Strategy (How to Trade)

1. Long Entry (Buy)

Condition: The cloud turns Aqua and a "BUY" label appears below the candle.

Confirmation: Ensure the price remains above the Aqua Trend Line.

Volume Check: The indicator automatically verifies if the volume is higher than the 20-period average before displaying the label.

Exit: Exit when a "SELL" signal appears or the price closes below the Aqua line.

2. Short Entry (Sell)

Condition: The cloud turns Red and a "SELL" label appears above the candle.

Confirmation: Price should stay below the Red Trend Line.

Exit: Exit when a "BUY" signal appears or the price closes above the Red line.

Input Parameters & Optimization

ATR Period (Default: 10): Determines the sensitivity to price volatility.

ATR Factor (Default: 3.0): Controls the distance of the trend line. Increase to 3.5 - 4.0 to reduce noise in choppy markets.

Volume Filter (Toggle): When enabled, only high-momentum signals are shown.

Recommended Usage

Best Timeframes: 15m, 1h, 4h.

Asset Classes: Highly effective for Crypto (BTC/ETH) and high-volume stocks.

QSL Upside/DownsideThe QSL Upside/Downside Indicator helps traders estimate potential gains and losses using Conditional Value at Risk (cVaR), a statistical measure that assesses both downside risk and upside potential beyond standard volatility. Instead of fixed timeframes (daily, weekly, etc.), traders can set a custom lookback period (in days) to analyze market behavior over their preferred time frame.

How It Works

The indicator calculates cVaR over the chosen period to determine how much an investment could move up or down based on past price behavior. It does this by:

• Mean Return – The average price movement over the period.

• Standard Deviation – Measures price fluctuations from the average.

• cVaR Confidence Interval (95%) – Estimates worst-case losses, meaning the downside projection reflects the worst 5% of expected losses.

• Upside Potential (Best 5%) – Instead of only considering risk, this indicator also calculates the potential upside by measuring returns in the top 5% of past price movements.

This provides a more complete view of what traders can expect—both in terms of risk and potential reward.

Key Features

✅ Custom Lookback Period – Set any number of days to analyze.

✅ cVaR Calculation (95% Confidence Interval) – Identifies extreme downside risks.

✅ Upside Potential (Best 5%) – Estimates how much an investment could rise in a best-case scenario.

✅ Clear Table Display – Quickly see projected best and worst-case portfolio values.

Understanding Probabilities: Upside & Downside Potential

Most traders focus on risk, but it’s equally important to understand potential gains. This indicator provides a probability-based view of expected market moves:

• 95% Confidence Interval (Downside cVaR) – There’s a 5% chance that losses could exceed this level.

• 95% Confidence Interval (Upside cVaR) – There’s a 5% chance that gains could be greater than this level.

• The remaining 90% of expected returns fall between these two extremes.

By knowing both potential losses and gains, traders can make more balanced, data-driven decisions rather than only focusing on worst-case scenarios.

Why Use This Indicator?

🔹 Better Risk & Reward Assessment – Understand both downside risk and upside potential.

🔹 More Realistic Market Projections – Uses probabilities instead of simple historical averages.

🔹 Flexible & Customizable – Works with any asset and any time period.

With this tool, QSL members can strategically plan trades, knowing the expected best and worst-case outcomes with a 95% probability range. 🚀

Weighted SD Bands | QuantEdgeBIntroducing Weighted SD Bands by QuantEdgeB

Overview

The Weighted SD Bands is a valuation and mean-reversion analysis tool that dynamically adjusts to price movements, helping traders identify potential overbought and oversold conditions. Built on a Weighted Moving Average (WMA), this indicator plots Standard Deviation (SD) bands around price action, highlighting extremes and potential reversal zones.

_____

Key Features

✅ Adaptive Valuation Model – Uses weighted price action to determine key valuation zones.

✅ Mean Reversion Analysis – Identifies extended deviations from fair value to spot reversal opportunities.

✅ Multi-Tier SD Bands – Provides multiple deviation levels to assess varying degrees of price stretch.

✅ Dynamic Color Coding – Highlights areas of extreme overvaluation or undervaluation.

✅ Reversal Signals – Generates Buy/Sell signals when price crosses the outer bands.

_____

How It Works

- A Weighted Moving Average (WMA) serves as the baseline (fair value).

- Standard Deviation Bands expand dynamically based on historical volatility.

- Extreme levels (±2 SD) signal potential trend exhaustion/reversal.

- Buy signals appear when price crosses below the lower 2 SD band.

- Sell signals appear when price crosses above the upper 2 SD band.

_____

Visual Representation

🔹 Gradient-filled bands help visualize price stretching beyond typical fluctuations.

🔹 Triangular markers indicate potential reversal points at extreme SD levels.

🔹 Background highlights mark high-risk valuation zones.

_____

Settings & Customization

- Lookback Length (WMA): Adjust the moving average period to control sensitivity. (default: 20)

- Source : Select the base source for the calculation. (default: close)

- SD Length: Modify the standard deviation period to fine-tune band width. (default: 30)

- Color Mode: Choose from multiple visualization themes.

_____

Who Should Use It?

📌 Mean-Reversion Traders – Spot high-probability reversal zones.

📌 Valuation-Based Investors – Identify fair value and extended price levels.

📌 Trend-Following Traders – Use SD bands to manage risk and spot potential pullbacks.

_____

Conclusion

The Weighted SD Bands indicator is a powerful tool for valuation and mean-reversion trading, providing dynamic fair value zones, extreme-level signals, and customizable SD bands to refine market timing. Whether you're trading pullbacks, rebalancing positions, or spotting reversals, this model helps you stay ahead of market inefficiencies.

🔹 Disclaimer: This tool is for educational purposes only and is not financial advice. Always conduct your own research before making investing decisions

Cumulative Price AverageThe Cumulative Price Average (CPA) indicator calculates and plots the overall average of candlestick prices, providing a smoothed representation of the market's long-term price trend. This is achieved by aggregating the averages of each candle (Open, High, Low, Close) and dynamically updating the overall average as new candles are added.

Key Features

Long-Term Price Perspective: Displays the cumulative average of all candles from the start of the chart.

Trend Visualization: Smooths out short-term price fluctuations to highlight the overall trend.

Dynamic Updates: The average adjusts with each new bar for real-time analysis.

Usage

Trend Analysis:

Identify long-term bullish or bearish trends by observing the slope of the CPA line.

Support/Resistance:

The CPA line can act as a dynamic support or resistance level for the price.

Price Comparison:

Compare the current price to the CPA to assess whether the market is overbought or oversold relative to its historical average.

This indicator is especially useful for traders seeking to incorporate a historical perspective into their analysis, providing insights into the broader market behavior beyond short-term volatility.

ATR-Based Trend Oscillator with Donchian ChannelsThis script, my Magnum Opus, combines the best elements of trend detection into a powerful ATR-based trend strength oscillator. It has been meticulously engineered to give traders a consistent edge in trend analysis across any asset, including highly volatile markets like crypto and forex. The oscillator normalizes trend strength as a percentage of ATR, smoothing out noise and allowing the oscillator to remain highly responsive while adapting to varying asset volatility.

Key Features:

ATR-Based Oscillator: Measures trend strength in relation to Average True Range, which enhances accuracy and consistency across different assets. By normalizing to ATR, the oscillator produces stable and reliable values that capture shifts in trend momentum effectively.

Dual Moving Averages for Smoothing: This script features two customizable moving averages to help confirm trend direction and strength, making it adaptable for short- and long-term analysis alike.

Donchian Channels for Strength Bounds: A Donchian Channel over the smoothed trend strength oscillator visually bounds strength levels, enabling traders to spot breakout points or reversals quickly.

Ideal for Multi-Asset Trading: The versatility of this indicator makes it a perfect choice across various asset classes, from stocks to forex and cryptocurrencies, maintaining consistency in signals and reliability.

Suggested Pairing: Use this oscillator alongside a directional indicator, such as the Vortex Indicator, to confirm trend direction. This pairing allows traders to understand not only the strength but also the direction of the trend for optimized entry and exit points.

Why This Indicator Will Elevate Your Trading: This trend strength oscillator has been refined to provide clarity and edge for any trader. By incorporating ATR-based normalization, it maintains accuracy in volatile and steady markets alike. The Donchian Channels add structure to trend strength, giving clear overbought and oversold signals, while the two moving averages ensure that lag is minimized without sacrificing accuracy.

Whether you're scalping or trend-trading, this oscillator will enhance your ability to detect and interpret trend strength, making it an essential tool in any trading arsenal.

Volume CVD and Open InterestVolume, Cumulative Delta Volume and Open Interest are great indications of strength and sentiment in the market. Until now they have required separate indicators, but this indicator can show them all.

With a clean and aesthetic plot, this indicator has the option to choose the data source:

- Volume - the total volume of transactions, buys and sells

- Up Volume - the total volume from buys only

- Down Volume - the total volume from sells only

- Up/Down Volume (Net) - the difference in the Buy Volume and Sell Volume

- Cumulative Delta - the sum of the up/down volume for the previous 14 bars

- Cumulative Delta EMA - a smoothed average of the sum of the up/down volume for the previous 14 bars, over a 14 period EMA

- Open Interest - a user defined ticker, whose value is added to the plot, while this is designed to be used with Open Interest tickers, you can actually choose any ticker you want, perhaps you want to see DXY while charting Bitcoin!

There are several customization features for the colour of the plot, with a nice gradient colouring from high to low. You can choose the lookback which defines only the highest and lowest values for the colour gradient. There is also an option for how the Open Interest value is determined, based on Close, Open or differences between previous values.

While similar, Volume and Open Interest are not the same. To me the simplest explanation is Volume shows the trades that have been executed and the buy/sell direction, while Open Interest shows the value of open trades that are yet to be completed.

Volume shows strength, sentiment and volatility.

Open Interest does not show direction, but does indicate momentum and liquidity in the market.

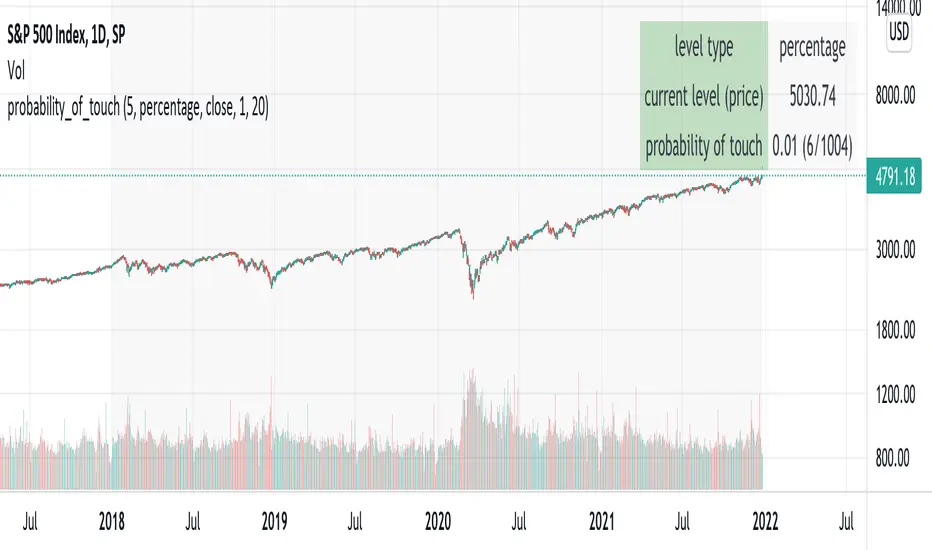

probability_of_touchBased on historical data (rather than theory), calculates the probability of a price level being "touched" within a given time frame. A "touch" means that price exceeded that level at some point. The parameters are:

- level: the "level" to be touched. it can be a number of points, percentage points, or standard deviations away from the mark price. a positive level is above the mark price, and a negative level is below the mark price.

- type: determines the meaning of the "level" parameter. "price" means price points (i.e. the numbers you see on the chart). "percentage" is expressed as a whole number, not a fraction. "stdev" means number of standard deviations, which is computed from recent realized volatlity.

- mark: the point from which the "level" is measured.

- length: the number of days within which the level must be touched.

- window: the number of days used to compute realized volatility. this parameter is only used when "type" is "stdev".

- debug: displays a fuchsia "X" over periods that touched the level. note that only a limited number of labels can be drawn.

- start: only include data after this time in the calculation.

- end: only include data before this time in the calculation.

Example: You want to know how many times Apple stock fell $1 from its closing price the next day, between 2020-02-26 and today. Use the following parameters:

level: -1

type: price

mark: close

length: 1

window:

debug:

start: 2020-02-26

end:

How does the script work? On every bar, the script looks back "length" days and sees if any day exceeded the "mark" price from "length" days ago, plus the limit. The probability is the ratio of such periods wherein price exceeded the limit to the total number of periods.

Jurik Bands//A follow up for my JMA script. This script is inspired by (and dedicated to) closure of sales (today, Oct 20 '21) of the famous Jurik Research.

...

Jurik Research, the real people who been doing real things by using the real instruments, while many others been reading books "How to become a billionaire in 2 days", watching 5687 hours videos of how to use RSI , and studying+applying machine learning to everything cuz suddenly it became trendy xD

...

In my JMA script I've said that JMA takes into account volatility. But how exactly? In fact, it's based on smth called Jurik Bands. Thing is they can be/should be used as an independent instrument. I won't lie, I've developed smth very similar myself for mean-reverting purposes, but we ain't gonna talk about this now (my stuff is much simpler, saying bye-bye to entropy).

...

The code is on purpose in Pine4, because lmao I'm not gonna call my stuff "Indicators", they don't "Indicate" anything. And it's on purpose doesn't follow any "coding conventions" made by geeks to make their stuff look more important. My conventions are simple: less code as possible and as simple as possible so we can actually do business based on these instruments.

...

Live Long And Prosper

Single Prints - Session Initial BalancesDisclaimer: Expose yourself to the knowledge of different trading methods. If you are unaware of what a Single Print is then do some research and broaden your knowledge.

This indicator has only been tested on BTCUSDT Binance pair. This indicator is meant to be used on the 30 minute timeframe to highlight Single Prints.

The calculations are base on 0000 UTC and what Single Prints are created during that day.

Single Prints

Single Prints are where prices moves to fast through an area (on a 30 minute timeframe), in the case of this indicator in $50 intervals, where the price has not yet cross back past, represented as orange lines. If you were viewing this on a Time Price Opportunity Chart (TPO) each $50 would be represented as a square with a letter in it. If price has only been through that area once, within that 24 hour period, then it is called a Single Print. If however the Single Print is on the lower wick of the candle it is called a Buying Tail and on the Upper Wick a Selling Tail.

Single Prints leave low volume nodes with liquidity gaps, these inefficient moves tend to get filled, and we can seek trading opportunities once they get filled, or we can also enter before they get filled and use these single prints as targets.

Single Prints are a sign of emotional buying or selling as very little time was spent at those levels and thus there is no value there.

The endpoints of single print sections are considered to be potential support or resistance points and or get filled (like a CME gap).

The above is only a very short summary, to understand Single Prints, Buying Tails and Selling Tails more please do your own research (DYOR).

References:

Trading Riot Volume Profile - Website

TOROS TPO Charts Explained - Youtube

Session Boxes

Session Boxes are the high and low of that markets session before the new market session opens. I used the data from the website Trading Hours for the time input.

White box – Start of day UTC 0000 to Market Close UTC 2000

Purple box – Asia Start UTC 0130 to London Start UTC 0700

Yellow box – London Start UTC 0700 to New York Start UTC 1330

Blue box – New York Start UTC 1330 to Market Close UTC 2000

Red box – Market Close UTC 2000 to End of day UTC 2359

References:

Trading Hours - Website

Initial Balance

The Initial Balance is the market range between the high and low of the first hour of trading for the market. In the case of crypto when is the Initial Balance if it is 24/7.

Context of Initial Balance:

The Initial Balance is traditionally the range of prices transacted in the first hour of trade. Many regard the Initial Balance as a significant range because, especially for the index futures which are tied to the underlying stocks, orders entered overnight or before the open are typically executed prior to the end of the first hour of trade. Some use it to understand how the rest of the day may develop, while others use it as a span of time to avoid trading altogether because of its potential volatility.

For this indicator I have coded the Initial Balance time as below:

White Box - To appear for the first hour of the day 0000 to 0100 UTC .

Purple Box - To appear for the first hour of the day 0130 to 0230 UTC .

Yellow Box - To appear for the first hour of the day 0700 to 0800 UTC .

Blue Box - To appear for the first hour of the day 1330 to 1430 UTC .

Red Box - To appear for the first hour of the day 2000 to 2100 UTC .

The diagram above shows some examples:

How price (white arrows) retraces the single prints.

How price (red arrows) uses the single prints as S/R.

References:

Not Hard Trading – Website

My Pivots Initial Balance - Website

Thanks go to:

StackOverFlow Bjorn Mistiaen

Trading View user mvs1231

Please message me if you have any feedback/questions.

I am looking at developing this indicator further in the future.