[blackcat] L1 Dynamic Volatility IndicatorThe volatility indicator (Volatility) is used to measure the magnitude and instability of price changes in financial markets or a specific asset. This thing is usually used to assess how risky the market is. The higher the volatility, the greater the fluctuation in asset prices, but brother, the risk is also relatively high! Here are some related terms and explanations:

- Historical Volatility: The actual volatility of asset prices over a certain period of time in the past. This thing is measured by calculating historical data.

- Implied Volatility: The volatility inferred from option market prices, used to measure market expectations for future price fluctuations.

- VIX Index (Volatility Index): Often referred to as the "fear index," it predicts the volatility of the US stock market within 30 days in advance. This is one of the most famous volatility indicators in global financial markets.

Volatility indicators are very important for investors and traders because they can help them understand how unstable and risky the market is, thereby making wiser investment decisions.

Today I want to introduce a volatility indicator that I have privately held for many years. It can use colors to judge sharp rises and falls! Of course, if you are smart enough, you can also predict some potential sharp rises and falls by looking at the trend!

In the financial field, volatility indicators measure the magnitude and instability of price changes in different assets. They are usually used to assess the level of market risk. The higher the volatility, the greater the fluctuation in asset prices and therefore higher risk. Historical Volatility refers to the actual volatility of asset prices over a certain period of time in the past, which can be measured by calculating historical data; while Implied Volatility is derived from option market prices and used to measure market expectations for future price fluctuations. In addition, VIX Index is commonly known as "fear index" and is used to predict volatility in the US stock market within 30 days. It is one of the most famous volatility indicators in global financial markets.

Volatility indicators are very important for investors and traders because they help them understand market uncertainty and risk, enabling them to make wiser investment decisions. The L1 Dynamic Volatility Indicator that I am introducing today is an indicator that measures volatility and can also judge sharp rises and falls through colors!

This indicator combines two technical indicators: Dynamic Volatility (DV) and ATR (Average True Range), displaying warnings about sharp rises or falls through color coding. DV has a slow but relatively smooth response, while ATR has a fast but more oscillating response. By utilizing their complementary characteristics, it is possible to construct a structure similar to MACD's fast-slow line structure. Of course, in order to achieve fast-slow lines for DV and ATR, first we need to unify their coordinate axes by normalizing them. Then whenever ATR's yellow line exceeds DV's purple line with both curves rapidly breaking through the threshold of 0.2, sharp rises or falls are imminent.

However, it is important to note that relying solely on the height and direction of these two lines is not enough to determine the direction of sharp rises or falls! Because they only judge the trend of volatility and cannot determine bull or bear markets! But it's okay, I have already considered this issue early on and added a magical gradient color band. When the color band gradually turns warm, it indicates a sharp rise; conversely, when the color band tends towards cool colors, it indicates a sharp fall! Of course, you won't see the color band in sideways consolidation areas, which avoids your involvement in unnecessary trades that would only waste your funds! This indicator is really practical and with it you can better assess market risks and opportunities!

在腳本中搜尋"Volatility"

Smoothed Volatility Bands [CC]The Smoothed Volatility Bands were created by Sylvain Vervoort (Stocks and Commodities Sep 2020 pg 19) and this is a heavily customized version of regular Bollinger Bands that take volatility into account. Feel free to change the moving average since Vervoort recommended trying that out. Buy when the indicator line turns green and sell when it turns red.

Let me know if there are any other indicators you want me to publish!

Fear Volatility Gate [by Oberlunar]The Fear Volatility Gate by Oberlunar is a filter designed to enhance operational prudence by leveraging volatility-based risk indices. Its architecture is grounded in the empirical observation that sudden shifts in implied volatility often precede instability across financial markets. By dynamically interpreting signals from globally recognized "fear indices", such as the VIX, the indicator aims to identify periods of elevated systemic uncertainty and, accordingly, restrict or flag potential trade entries.

The rationale behind the Fear Volatility Gate is rooted in the understanding that implied volatility represents a forward-looking estimate of market risk. When volatility indices rise sharply, it reflects increased demand for options and a broader perception of uncertainty. In such contexts, price movements can become less predictable, more erratic, and often decoupled from technical structures. Rather than relying on price alone, this filter provides an external perspective—derived from derivative markets—on whether current conditions justify caution.

The indicator operates in two primary modes: single-source and composite . In the single-source configuration, a user-defined volatility index is monitored individually. In composite mode, the filter can synthesize input from multiple indices simultaneously, offering a more comprehensive macro-risk assessment. The filtering logic is adaptable, allowing signals to be combined using inclusive (ANY), strict (ALL), or majority consensus logic. This allows the trader to tailor sensitivity based on the operational context or asset class.

The indices available for selection cover a broad spectrum of market sectors. In the equity domain, the filter supports the CBOE Volatility Index ( CBOE:VIX VIX) for the S&P 500, the Nasdaq-100 Volatility Index ( CBOE:VXN VXN), the Russell 2000 Volatility Index ( CBOEFTSE:RVX RVX), and the Dow Jones Volatility Index ( CBOE:VXD VXD). For commodities, it integrates the Crude Oil Volatility Index ( CBOE:OVX ), the Gold Volatility Index ( CBOE:GVZ ), and the Silver Volatility Index ( CBOE:VXSLV ). From the fixed income perspective, it includes the ICE Bank of America MOVE Index ( OKX:MOVEUSD ), the Volatility Index for the TLT ETF ( CBOE:VXTLT VXTLT), and the 5-Year Treasury Yield Index ( CBOE:FVX.P FVX). Within the cryptocurrency space, it incorporates the Bitcoin Volmex Implied Volatility Index ( VOLMEX:BVIV BVIV), the Ethereum Volmex Implied Volatility Index ( VOLMEX:EVIV EVIV), the Deribit Bitcoin Volatility Index ( DERIBIT:DVOL DVOL), and the Deribit Ethereum Volatility Index ( DERIBIT:ETHDVOL ETHDVOL). Additionally, the user may define a custom instrument for specialized tracking.

To determine whether market conditions are considered high-risk, the indicator supports three modes of evaluation.

The moving average cross mode compares a fast Hull Moving Average to a slower one, triggering a signal when short-term volatility exceeds long-term expectations.

The Z-score mode standardizes current volatility relative to historical mean and standard deviation, identifying significant deviations that may indicate abnormal market stress.

The percentile mode ranks the current value against a historical distribution, providing a relative perspective particularly useful when dealing with non-normal or skewed distributions.

When at least one selected index meets the condition defined by the chosen mode, and if the filtering logic confirms it, the indicator can mark the trading environment as “blocked”. This status is visually highlighted through background color changes and symbolic markers on the chart. An optional tabular interface provides detailed diagnostics, including raw values, fast-slow MA comparison, Z-scores, percentile levels, and binary risk status for each active index.

The Fear Volatility Gate is not a predictive tool in itself but rather a dynamic constraint layer that reinforces discipline under conditions of macro instability. It is particularly valuable when trading systems are exposed to highly leveraged or short-duration strategies, where market noise and sentiment can temporarily override structural price behavior. By synchronizing trading signals with volatility regimes, the filter promotes a more cautious, informed approach to decision-making.

This approach does not assume that all volatility spikes are harmful or that market corrections are imminent. Rather, it acknowledges that periods of elevated implied volatility statistically coincide with increased execution risk, slippage, and spread widening, all of which may erode the profitability of even the most technically accurate setups.

Therefore, the Fear Volatility Gate acts as a protective mechanism.

Oberlunar 👁️⭐

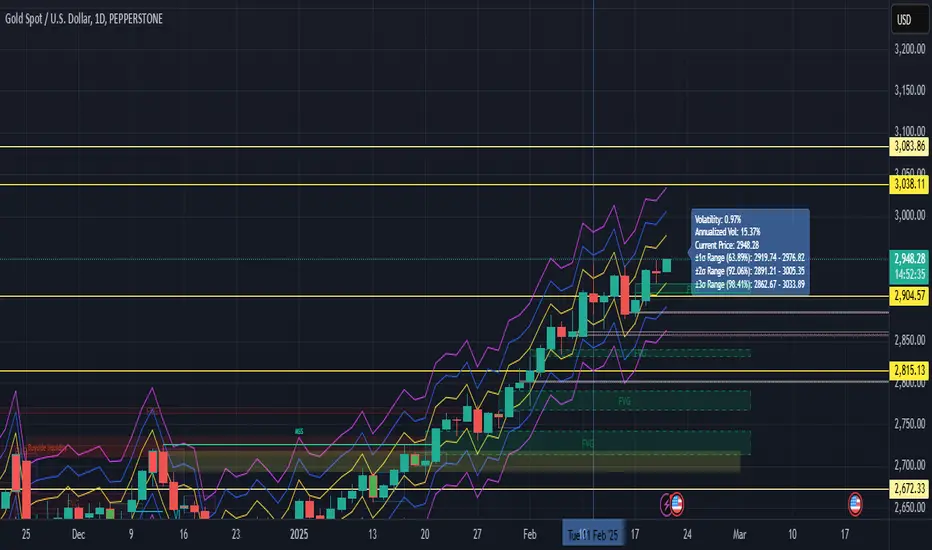

Volatility with Sigma BandsOverview

The Volatility Analysis with Sigma Bands indicator is a powerful and flexible tool designed for traders who want to gain deeper insights into market price fluctuations. It calculates historical volatility within a user-defined time range and displays ±1σ, ±2σ, and ±3σ standard deviation bands, helping traders identify potential support, resistance levels, and extreme price behaviors.

Key Features

Multiple Volatility Band Displays:

±1σ Range (Yellow line): Covers approximately 68% of price fluctuations.

±2σ Range (Blue line): Covers approximately 95% of price fluctuations.

±3σ Range (Fuchsia line): Covers approximately 99% of price fluctuations.

Dynamic Probability Mode:

Toggle between standard normal distribution probabilities (68.2%, 95.4%, 99.7%) and actual historical probability calculations, allowing for more accurate analysis tailored to varying market conditions.

Highly Customizable Label Display:

The label shows:

Real-time volatility

Annualized volatility

Current price

Price ranges for each σ level

Users can adjust the label’s position and horizontal offset to prevent it from overlapping key price areas.

Real-Time Calculation & Visualization:

The indicator updates in real-time based on the selected time range and current market data, making it suitable for day trading, swing trading, and long-term trend analysis.

Use Cases

Risk Management:

Understand the distribution probabilities of price within different standard deviation bands to set more effective stop-loss and take-profit levels.

Trend Confirmation:

Determine trend strength or spot potential reversals by observing whether the price breaks above or below ±1σ or ±2σ ranges.

Market Sentiment Analysis:

Price movement beyond the ±3σ range often indicates extreme market sentiment, providing potential reversal opportunities.

Backtesting and Historical Analysis:

Utilize the customizable time range feature to backtest volatility during various periods, providing valuable insights for strategy refinement.

The Volatility Analysis with Sigma Bands indicator is an essential tool for traders seeking to understand market volatility patterns. Whether you're a day trader looking for precise entry and exit points or a long-term investor analyzing market behavior, this indicator provides deep insights into volatility dynamics, helping you make more confident trading decisions.

Rolling Volatility Indicator

Description :

The Rolling Volatility indicator calculates the volatility of an asset's price movements over a specified period. It measures the degree of variation in the price series over time, providing insights into the market's potential for price fluctuations.

This indicator utilizes a rolling window approach, computing the volatility by analyzing the logarithmic returns of the asset's price. The user-defined length parameter determines the timeframe for the volatility calculation.

How to Use :

Adjust the "Length" parameter to set the rolling window period for volatility calculation.

Ajust "trading_days" for the sampling period, this is the total number of trading days (usually 252 days for stocks and 365 for crypto)

Higher values for the length parameter will result in a smoother, longer-term view of volatility, while lower values will provide a more reactive, shorter-term perspective.

Volatility levels can assist in identifying periods of increased market activity or potential price changes. Higher volatility may suggest increased risk and potential opportunities, while lower volatility might indicate periods of reduced market activity.

Key Features :

Customizable length parameter for adjusting the calculation period and trading days such that it can also be applied to stock market or any markets.

Visual representation of volatility with a plotted line on the chart.

The Rolling Volatility indicator can be a valuable tool for traders and analysts seeking insights into market volatility trends, aiding in decision-making processes and risk management strategies.

[blackcat] L1 Volatility Quality Index (VQI)The Volatility Quality Index (VQI) is an indicator used to measure the quality of market volatility. Volatility refers to the extent of price changes in the market. VQI helps traders assess market stability and risk levels by analyzing price volatility. This introduction may be a bit abstract, so let me help you understand it with a comparative metaphor if you're not immersed in various technical indicators.

Imagine you are playing a jump rope game, and you notice that sometimes the rope moves fast and other times it moves slowly. This is volatility, which describes the speed of the rope. VQI is like an instrument specifically designed to measure rope speed. It observes the movement of the rope and provides a numerical value indicating how fast or slow it is moving. This value can help you determine both the stability of the rope and your difficulty level in jumping over it. With this information, you know when to start jumping and when to wait while skipping rope.

In trading, VQI works similarly. It observes market price volatility and provides a numerical value indicating market stability and risk levels for traders. If VQI has a high value, it means there is significant market volatility with relatively higher risks involved. Conversely, if VQI has a low value, it indicates lower market volatility with relatively lower risks involved as well. The calculation involves dividing the range by values obtained from calculating Average True Range (ATR) multiplied by a factor/multiple.

The purpose of VQI is to assist traders in evaluating the quality of market volatility so they can develop better trading strategies accordingly.

Therefore, VQI helps traders understand the quality of market volatility for better strategy formulation and risk management—just like adjusting your jumping style based on rope speed during jump-rope games; traders can adjust their trading decisions based on VQI values.

The calculation of VQI indicator depends on given period length and multiple factors: Period length is used to calculate Average True Range (ATR), while the multiple factor adjusts the range of volatility. By dividing the range by values and multiplying it with a multiple, VQI numerical value can be obtained.

VQI indicator is typically presented in the form of a histogram on price charts. Higher VQI values indicate better quality of market volatility, while lower values suggest poorer quality of volatility. Traders can use VQI values to assess the strength and reliability of market volatility, enabling them to make wiser trading decisions.

It should be noted that VQI is just an auxiliary indicator; traders should consider other technical indicators and market conditions comprehensively when making decisions. Additionally, parameter settings for VQI can also be adjusted and optimized based on individual trading preferences and market characteristics.

(MVD) Meta-Volatility Divergence (DAFE) Meta-Volatility Divergence (MVD)

Reveal the Hidden Tension in Volatility.

The Meta-Volatility Divergence (MVD) indicator is a next-generation tool designed to expose the disagreement between multiple volatility measures—helping you spot when the market’s “volatility engines” are out of sync, and a regime shift or volatility event may be brewing.

What Makes MVD Unique?

Multi-Source Volatility Analysis:

Unlike traditional volatility indicators that rely on a single measure, MVD fuses four distinct volatility signals:

ATR (Average True Range): Captures the average range of price movement.

Stdev (Standard Deviation): Measures the dispersion of closing prices.

Range: The average difference between high and low.

VoVix: A proprietary “volatility of volatility” metric, quantifying the difference between fast and slow ATR, normalized by ATR’s own volatility.

Divergence Engine:

The core MVD line (yellow) represents the mean absolute deviation (MAD) of these volatility measures from their average. When the line is flat, all volatility measures are in agreement. When the line rises, it means the market’s volatility signals are diverging—often a precursor to regime shifts, volatility expansions, or hidden stress.

Dynamic Z-Score Normalization:

The MVD line is normalized as a Z-score, so you can easily spot when current divergence is rare or extreme compared to recent history.

Visual Clarity:

Yellow center line: Tracks the real-time divergence of volatility measures.

Green dashed thresholds: Mark the ±2.00 Z-score levels, highlighting when divergence is unusually high and action may be warranted.

Dashboard: Toggleable panel shows all key metrics (ATR, Stdev, VoVix, MVD Z) and your custom branding.

Compact Info Label : For mobile or minimalist users, a single-line summary keeps you informed without clutter.

What Makes The MVD line move?

- The MVD line rises when the included volatility measures (ATR, Stdev, Range, VoVix) are moving in different directions or at different magnitudes. For example, if ATR is rising but Stdev is falling, the line will move up, signaling disagreement.

- The line falls or flattens when all volatility measures are in sync, indicating a consensus in the market’s volatility regime.

- VoVix adds a unique dimension, making the indicator especially sensitive to sudden changes in volatility structure that most tools miss.

Inputs & Settings

ATR Length: Sets the lookback for ATR calculation. Shorter = more sensitive, longer = smoother.

Stdev Length: Sets the lookback for standard deviation. Adjust for your asset’s volatility.

Range Length: Sets the lookback for the average high-low range.

MVD Lookback: Controls the window for Z-score normalization. Higher values = more historical context, lower = more responsive.

Show Dashboard: Toggle the full dashboard panel on/off.

Show Compact Info Label: Toggle the mobile-friendly info line on/off.

Tip:

Adjust these settings to match your asset’s volatility and your trading timeframe. There is no “one size fits all”—tuning is key to extracting the most value from MVD.

How to make MVD work for you:

Threshold Crosses: When the MVD line crosses above or below the green dashed thresholds (±2.00), it signals that volatility measures are diverging more than usual. This is a heads-up that a volatility event, regime shift, or hidden market stress may be developing.

Not a Buy/Sell Signal: A threshold cross is not a direct buy or sell signal. It is an indication that the market’s volatility structure is changing. Use it as a filter, confirmation, or alert in combination with your own strategy and risk management.

Dashboard & Info Line: Use the dashboard for a full view of all metrics, or the info label for a quick glance—especially useful on mobile.

Chart: MNQ! on 5min frames

ATR: 14

StDev L: 11

Range L: 13

MDV LB: 13

Important Note

MVD is a market structure and volatility regime tool.

It is designed to alert you to potential changes in market conditions, not to provide direct trade entries or exits. Always combine with your own analysis and risk management.

Meta-Volatility Divergence:

See the market’s hidden tension. Anticipate the next wave.

For educational purposes only. Not financial advice. Always use proper risk management.

Use with discipline. Trade your edge.

— Dskyz, for DAFE Trading Systems

Dynamic Volatility Differential Model (DVDM)The Dynamic Volatility Differential Model (DVDM) is a quantitative trading strategy designed to exploit the spread between implied volatility (IV) and historical (realized) volatility (HV). This strategy identifies trading opportunities by dynamically adjusting thresholds based on the standard deviation of the volatility spread. The DVDM is versatile and applicable across various markets, including equity indices, commodities, and derivatives such as the FDAX (DAX Futures).

Key Components of the DVDM:

1. Implied Volatility (IV):

The IV is derived from options markets and reflects the market’s expectation of future price volatility. For instance, the strategy uses volatility indices such as the VIX (S&P 500), VXN (Nasdaq 100), or RVX (Russell 2000), depending on the target market. These indices serve as proxies for market sentiment and risk perception (Whaley, 2000).

2. Historical Volatility (HV):

The HV is computed from the log returns of the underlying asset’s price. It represents the actual volatility observed in the market over a defined lookback period, adjusted to annualized levels using a multiplier of \sqrt{252} for daily data (Hull, 2012).

3. Volatility Spread:

The difference between IV and HV forms the volatility spread, which is a measure of divergence between market expectations and actual market behavior.

4. Dynamic Thresholds:

Unlike static thresholds, the DVDM employs dynamic thresholds derived from the standard deviation of the volatility spread. The thresholds are scaled by a user-defined multiplier, ensuring adaptability to market conditions and volatility regimes (Christoffersen & Jacobs, 2004).

Trading Logic:

1. Long Entry:

A long position is initiated when the volatility spread exceeds the upper dynamic threshold, signaling that implied volatility is significantly higher than realized volatility. This condition suggests potential mean reversion, as markets may correct inflated risk premiums.

2. Short Entry:

A short position is initiated when the volatility spread falls below the lower dynamic threshold, indicating that implied volatility is significantly undervalued relative to realized volatility. This signals the possibility of increased market uncertainty.

3. Exit Conditions:

Positions are closed when the volatility spread crosses the zero line, signifying a normalization of the divergence.

Advantages of the DVDM:

1. Adaptability:

Dynamic thresholds allow the strategy to adjust to changing market conditions, making it suitable for both low-volatility and high-volatility environments.

2. Quantitative Precision:

The use of standard deviation-based thresholds enhances statistical reliability and reduces subjectivity in decision-making.

3. Market Versatility:

The strategy’s reliance on volatility metrics makes it universally applicable across asset classes and markets, ensuring robust performance.

Scientific Relevance:

The strategy builds on empirical research into the predictive power of implied volatility over realized volatility (Poon & Granger, 2003). By leveraging the divergence between these measures, the DVDM aligns with findings that IV often overestimates future volatility, creating opportunities for mean-reversion trades. Furthermore, the inclusion of dynamic thresholds aligns with risk management best practices by adapting to volatility clustering, a well-documented phenomenon in financial markets (Engle, 1982).

References:

1. Christoffersen, P., & Jacobs, K. (2004). The importance of the volatility risk premium for volatility forecasting. Journal of Financial and Quantitative Analysis, 39(2), 375-397.

2. Engle, R. F. (1982). Autoregressive conditional heteroskedasticity with estimates of the variance of United Kingdom inflation. Econometrica, 50(4), 987-1007.

3. Hull, J. C. (2012). Options, Futures, and Other Derivatives. Pearson Education.

4. Poon, S. H., & Granger, C. W. J. (2003). Forecasting volatility in financial markets: A review. Journal of Economic Literature, 41(2), 478-539.

5. Whaley, R. E. (2000). The investor fear gauge. Journal of Portfolio Management, 26(3), 12-17.

This strategy leverages quantitative techniques and statistical rigor to provide a systematic approach to volatility trading, making it a valuable tool for professional traders and quantitative analysts.

Uptrick: Volatility Reversion BandsUptrick: Volatility Reversion Bands is an indicator designed to help traders identify potential reversal points in the market by combining volatility and momentum analysis within one comprehensive framework. It calculates dynamic bands around a simple moving average and issues signals when price interacts with these bands. Below is a fully expanded description, structured in multiple sections, detailing originality, usefulness, uniqueness, and the purpose behind blending standard deviation-based and ATR-based concepts. All references to code have been removed to focus on the written explanation only.

Section 1: Overview

Uptrick: Volatility Reversion Bands centers on a moving average around which various bands are constructed. These bands respond to changes in price volatility and can help gauge potential overbought or oversold conditions. Signals occur when the price moves beyond certain thresholds, which may imply a reversal or significant momentum shift.

Section 2: Originality, Usefulness, Uniqness, Purpose

This indicator merges two distinct volatility measurements—Bollinger Bands and ATR—into one cohesive system. Bollinger Bands use standard deviation around a moving average, offering a baseline for what is statistically “normal” price movement relative to a recent mean. When price hovers near the upper band, it may indicate overbought conditions, whereas price near the lower band suggests oversold conditions. This straightforward construction often proves invaluable in moderate-volatility settings, as it pinpoints likely turning points and gauges a market’s typical trading range.

Yet Bollinger Bands alone can falter in conditions marked by abrupt volatility spikes or sudden gaps that deviate from recent norms. Intraday news, earnings releases, or macroeconomic data can alter market behavior so swiftly that standard-deviation bands do not keep pace. This is where ATR (Average True Range) adds an important layer. ATR tracks recent highs, lows, and potential gaps to produce a dynamic gauge of how much price is truly moving from bar to bar. In quieter times, ATR contracts, reflecting subdued market activity. In fast-moving markets, ATR expands, exposing heightened volatility on each new bar.

By overlaying Bollinger Bands and ATR-based calculations, the indicator achieves a broader situational awareness. Bollinger Bands excel at highlighting relative overbought or oversold areas tied to an established average. ATR simultaneously scales up or down based on real-time market swings, signaling whether conditions are calm or turbulent. When combined, this means a price that barely crosses the Bollinger Band but also triggers a high ATR-based threshold is likely experiencing a volatility surge that goes beyond typical market fluctuations. Conversely, a price breach of a Bollinger Band when ATR remains low may still warrant attention, but not necessarily the same urgency as in a high-volatility regime.

The resulting synergy offers balanced, context-rich signals. In a strong trend, the ATR layer helps confirm whether an apparent price breakout really has momentum or if it is just a temporary spike. In a range-bound market, standard deviation-based Bollinger Bands define normal price extremes, while ATR-based extensions highlight whether a breakout attempt has genuine force behind it. Traders gain clarity on when a move is both statistically unusual and accompanied by real volatility expansion, thus carrying a higher probability of a directional follow-through or eventual reversion.

Practical advantages emerge across timeframes. Scalpers in fast-paced markets appreciate how ATR-based thresholds update rapidly, revealing if a sudden price push is routine or exceptional. Swing traders can rely on both indicators to filter out false signals in stable conditions or identify truly notable moves. By calibrating to changes in volatility, the merged system adapts naturally whether the market is trending, ranging, or transitioning between these phases.

In summary, combining Bollinger Bands (for a static sense of standard-deviation-based overbought/oversold zones) with ATR (for a dynamic read on current volatility) yields an adaptive, intuitive indicator. Traders can better distinguish fleeting noise from meaningful expansions, enabling more informed entries, exits, and risk management. Instead of relying on a single yardstick for all market conditions, this fusion provides a layered perspective, encouraging traders to interpret price moves in the broader context of changing volatility.

Section 3: Why Bollinger Bands and ATR are combined

Bollinger Bands provide a static snapshot of volatility by computing a standard deviation range above and below a central average. ATR, on the other hand, adapts in real time to expansions or contractions in market volatility. When combined, these measures offset each other’s limitations: Bollinger Bands add structure (overbought and oversold references), and ATR ensures responsiveness to rapid price shifts. This synergy helps reduce noisy signals, particularly during sudden market turbulence or extended consolidations.

Section 4: User Inputs

Traders can adjust several parameters to suit their preferences and strategies. These typically include:

1. Lookback length for calculating the moving average and standard deviation.

2. Multipliers to control the width of Bollinger Bands.

3. An ATR multiplier to set the distance for additional reversal bands.

4. An option to display weaker signals when the price merely approaches but does not cross the outer bands.

Section 5: Main Calculations

At the core of this indicator are four important steps:

1. Calculate a basis using a simple moving average.

2. Derive Bollinger Bands by adding and subtracting a product of the standard deviation and a user-defined multiplier.

3. Compute ATR over the same lookback period and multiply it by the selected factor.

4. Combine ATR-based distance with the Bollinger Bands to set the outer reversal bands, which serve as stronger signal thresholds.

Section 6: Signal Generation

The script interprets meaningful reversal points when the price:

1. Crosses below the lower outer band, potentially highlighting oversold conditions where a bullish reversal may occur.

2. Crosses above the upper outer band, potentially indicating overbought conditions where a bearish reversal may develop.

Section 7: Visualization

The indicator provides visual clarity through labeled signals and color-coded references:

1. Distinct colors for upper and lower reversal bands.

2. Markers that appear above or below bars to denote possible buying or selling signals.

3. A gradient bar color scheme indicating a bar’s position between the lower and upper bands, helping traders quickly see if the price is near either extreme.

Section 8: Weak Signals (Optional)

For those preferring early cues, the script can highlight areas where the price nears the outer bands. When weak signals are enabled:

1. Bars closer to the upper reversal zone receive a subtle marker suggesting a less robust, yet still noteworthy, potential selling area.

2. Bars closer to the lower reversal zone receive a subtle marker suggesting a less robust, yet still noteworthy, potential buying area.

Section 9: Simplicity, Effectiveness, and Lower Timeframes

Although combining standard deviation and ATR involves sophisticated volatility concepts, this indicator is visually straightforward. Reversal bands and gradient-colored bars make it easy to see at a glance when price approaches or crosses a threshold. Day traders operating on lower timeframes benefit from such clarity because it helps filter out minor fluctuations and focus on more meaningful signals.

Section 10: Adaptability across Market Phases

Because both the standard deviation (for Bollinger Bands) and ATR adapt to changing volatility, the indicator naturally adjusts to various environments:

1. Trending: The additional ATR-based outer bands help distinguish between temporary pullbacks and deeper reversals.

2. Ranging: Bollinger Bands often remain narrower, identifying smaller reversals, while the outer ATR bands remain relatively close to the main bands.

Section 11: Reduced Noise in High-Volatility Scenarios

By factoring ATR into the band calculations, the script widens or narrows the thresholds during rapid market fluctuations. This reduces the amount of false triggers typically found in indicators that rely solely on fixed calculations, preventing overreactions to abrupt but short-lived price spikes.

Section 12: Incorporation with Other Technical Tools

Many traders combine this indicator with oscillators such as RSI, MACD, or Stochastic, as well as volume metrics. Overbought or oversold signals in momentum oscillators can provide additional confirmation when price reaches the outer bands, while volume spikes may reinforce the significance of a breakout or potential reversal.

Section 13: Risk Management Considerations

All trading strategies carry risk. This indicator, like any tool, can and does produce losing trades if price unexpectedly reverses again or if broader market conditions shift rapidly. Prudent traders employ protective measures:

1. Stop-loss orders or trailing stops.

2. Position sizing that accounts for market volatility.

3. Diversification across different asset classes when possible.

Section 14: Overbought and Oversold Identification

Standard Bollinger Bands highlight regions where price might be overextended relative to its recent average. The extended ATR-based reversal bands serve as secondary lines of defense, identifying moments when price truly stretches beyond typical volatility bounds.

Section 15: Parameter Customization for Different Needs

Users can tailor the script to their unique preferences:

1. Shorter lookback settings yield faster signals but risk more noise.

2. Higher multipliers spread the bands further apart, filtering out small moves but generating fewer signals.

3. Longer lookback periods smooth out market noise, often leading to more stable but less frequent trading cues.

Section 16: Examples of Different Trading Styles

1. Day Traders: Often reduce the length to capture quick price swings.

2. Swing Traders: May use moderate lengths such as 20 to 50 bars.

3. Position Traders: Might opt for significantly longer settings to detect macro-level reversals.

Section 17: Performance Limitations and Reality Check

No technical indicator is free from false signals. Sudden fundamental news events, extreme sentiment changes, or low-liquidity conditions can render signals less reliable. Backtesting and forward-testing remain essential steps to gauge whether the indicator aligns well with a trader’s timeframe, risk tolerance, and instrument of choice.

Section 18: Merging Volatility and Momentum

A critical uniqueness of this indicator lies in how it merges Bollinger Bands (standard deviation-based) with ATR (pure volatility measure). Bollinger Bands provide a relative measure of price extremes, while ATR dynamically reacts to market expansions and contractions. Together, they offer an enhanced perspective on potential market turns, ideally reducing random noise and highlighting moments where price has traveled beyond typical bounds.

Section 19: Purpose of this Merger

The fundamental purpose behind blending standard deviation measures with real-time volatility data is to accommodate different market behaviors. Static standard deviation alone can underreact or overreact in abnormally volatile conditions. ATR alone lacks a baseline reference to normality. By merging them, the indicator aims to provide:

1. A versatile dynamic range for both typical and extreme moves.

2. A filter against frequent whipsaws, especially in choppy environments.

3. A visual framework that novices and experts can interpret rapidly.

Section 20: Summary and Practical Tips

Uptrick: Volatility Reversion Bands offers a powerful tool for traders looking to combine volatility-based signals with momentum-derived reversals. It emphasizes clarity through color-coded bars, defined reversal zones, and optional weak signal markers. While potentially useful across all major timeframes, it demands ongoing risk management, realistic expectations, and careful study of how signals behave under different market conditions. No indicator serves as a crystal ball, so integrating this script into an overall strategy—possibly alongside volume data, fundamentals, or momentum oscillators—often yields the best results.

Disclaimer and Educational Use

This script is intended for educational and informational purposes. It does not constitute financial advice, nor does it guarantee trading success. Sudden economic events, low-liquidity times, and unexpected market behaviors can all undermine technical signals. Traders should use proper testing procedures (backtesting and forward-testing) and maintain disciplined risk management measures.

Volatility Stop with Vwap StrategyFirst the credits goes to @TradingView for their release of the volatility stop mtf indicator.

I have took it, and inside I have added a weekly vwap for a better trend direction and at the same time I have added a dynamic risk managment which is calculated from the distance between the volatility line to the close of the candle.

The rules for entry are simple:

For long:We enter when our close of the candle is above the volatility stop line and at the same time the close of the candle is above weekly vwap

For short we enter when our close of the candle is below the volatility stop line and at the same time the close of the candle is below weekly vwap.

We exit when we either have a reverse signal than the one we enterred, or based on the TP/SL which is calculated with the distance from vwap to the close of the candle.

If you have any questions please let me know !

Volatility Signaling 50SMAOverview of the Script:

The script implements a volatility signaling indicator using a 50-period Simple Moving Average (SMA). It incorporates Bollinger Bands and the Average True Range (ATR) to dynamically adjust the SMA's color based on volatility conditions. Here's a detailed breakdown:

Components of the Script:

1. Inputs:

The script allows the user to customize key parameters for flexibility:

Bollinger Bands Length (length): Determines the period for calculating the Bollinger Bands.

Source (src): The price data to use, defaulting to the closing price.

Standard Deviation Multiplier (mult): Scales the Bollinger Bands' width.

ATR Length (atrLength): Sets the period for calculating the ATR.

The 50-period SMA length (smaLength) is fixed at 50.

2. Bollinger Bands Calculation:

Basis: Calculated as the SMA of the selected price source over the specified length.

Upper and Lower Bands: Determined by adding/subtracting a scaled standard deviation (dev) from the basis.

3. ATR Calculation:

Computes the Average True Range over the user-defined atrLength.

4. Volatility-Based Conditions:

The script establishes thresholds for Bollinger Band width relative to ATR:

Yellow Condition: When the band width (upper - lower) is less than 1.25 times the ATR.

Orange Condition: When the band width is less than 1.5 times the ATR.

Red Condition: When the band width is less than 1.75 times the ATR.

5. Dynamic SMA Coloring:

The 50-period SMA is colored based on the above conditions:

Yellow: Indicates relatively low volatility.

Orange: Indicates moderate volatility.

Red: Indicates higher volatility.

White: Default color when no conditions are met.

6. Plotting the 50-Period SMA:

The script plots the SMA (sma50) with a dynamically assigned color, enabling visual analysis of market conditions.

Use Case:

This script is ideal for traders seeking to assess market volatility and identify changes using Bollinger Bands and ATR. The colored SMA provides an intuitive way to gauge market dynamics directly on the chart.

Example Visualization:

Yellow SMA: The market is in a low-volatility phase.

Orange SMA: Volatility is picking up but remains moderate.

Red SMA: Higher volatility, potentially signaling significant market activity.

White SMA: Neutral/default state.

Volatility Stop MTFThis is a multi-timeframe version of our Volatility Stop , an ATR-based trend detector that can be used as a stop.

► Timeframe selection

The higher timeframe can be selected using 3 different ways:

• By steps (60 min., 1D, 3D, 1W, 1M, 1Y).

• As a multiple of the current chart's resolution, which can be fractional, so 3.5 will work.

• Fixed.

Note that you can also use this indicator without the higher timeframe functionality. It will then behave as our normal Volatility Stop would.

► Stop breaches

Two modes of stop-breaching logic can be selected.

• In the default, Early Breach mode, the stop is considered breached when a bar at the chart's current resolution breaches the higher timeframe stop.

• You may also choose to calculate breaches on the higher timeframe information only.

Choosing the Early Breach mode has the advantage of generating faster exits. It will create a state of limbo where the stop has been breached but the Volatility Stop trend has not yet reversed. The impact of detecting earlier exits to minimize losses comes, as is usually the case, at the cost of a compromise: if the stop is breached early in a long trend, the indicator will then spend most of that trend in limbo. Sizeable portions of a trend can thus be missed.

A few options are provided when you use Early Breach mode:

• A red triangle can identify early breaches (default).

• You can color bars or the background to identify limbo states.

When in limbo, the color used to plot the indicator's line or shapes will always be darker.

► Alerts

Five pre-defined alerts are supplied:

• #1: On any trend change.

• #2: On changes into an uptrend.

• #3: On changes into a downtrend.

• #4: Only on breaches of the uptrend by the chart's bars (Early Breach mode). Will not trigger on a trend change.

• #5: Only on breaches of the downtrend by the chart's bars (Early Breach mode). Will not trigger on a trend change.

As usual, alerts should be configured to trigger Once Per Bar Close . When creating alerts, you will see a warning to the effect that potentially repainting code is used, even if the indicator's default non-repainting mode is active. The warning is normal.

► Other features

• You can color bars using the indicator's up/down state. When bars are colored, up bars are more brightly colored.

• The HTF line is non-repainting by default, but you can allow it to repaint.

• You can confirm the higher timeframe used by displaying it at a selectable distance from the last bar on the chart.

• Choice of 2 color themes.

• Choice of display as a line, circles, diamonds or arrows. The line can be used with the other shapes. If no line is required, set its thickness to zero.

Enjoy!

Look first. Then leap.

Volatility StopThis is a new version of the classic Volatility Stop originally published in 2014 by admin and written in Pine v1. While the code has evolved, its logic is identical. It is an ATR-based trend detector that can also be used as a stop. It belongs to the same family of indicators as:

• Charles Le Beau's Chandelier Exit ,

• Olivier Seban's Super Trend , and

• Sylvain Vervoort's Average True Range Trailing Stop .

Unlike the Chandelier Exit , Volatility Stop will not move against the trend.

This new version is written in Pine v4. The indicator can be used as a chart overlay, like the original. The calculations have been functionalized for easier reuse, so it is now easier to lift the logic out of the script and use it in others.

Features

• Choice of 2 color themes.

• Choice of display as a line, circles, diamonds or arrows. The line can be used with the other shapes. If no line is required, set its thickness to zero.

• Same default of length=20 and ATR factor=2 used in the original Volatility Stop.

• 3 alerts: on any trend change, or on changes into up or downtrends only. Alerts should be configured to trigger Once Per Bar Close .

Original version:

Look first. Then leap.

Volatility Quality [Alpha Extract]The Alpha-Extract Volatility Quality (AVQ) Indicator provides traders with deep insights into market volatility by measuring the directional strength of price movements. This sophisticated momentum-based tool helps identify overbought and oversold conditions, offering actionable buy and sell signals based on volatility trends and standard deviation bands.

🔶 CALCULATION

The indicator processes volatility quality data through a series of analytical steps:

Bar Range Calculation: Measures true range (TR) to capture price volatility.

Directional Weighting: Applies directional bias (positive for bullish candles, negative for bearish) to the true range.

VQI Computation: Uses an exponential moving average (EMA) of weighted volatility to derive the Volatility Quality Index (VQI).

vqiRaw = ta.ema(weightedVol, vqiLen)

Smoothing: Applies an additional EMA to smooth the VQI for clearer signals.

Normalization: Optionally normalizes VQI to a -100/+100 scale based on historical highs and lows.

Standard Deviation Bands: Calculates three upper and lower bands using standard deviation multipliers for volatility thresholds.

vqiStdev = ta.stdev(vqiSmoothed, vqiLen)

upperBand1 = vqiSmoothed + (vqiStdev * stdevMultiplier1)

upperBand2 = vqiSmoothed + (vqiStdev * stdevMultiplier2)

upperBand3 = vqiSmoothed + (vqiStdev * stdevMultiplier3)

lowerBand1 = vqiSmoothed - (vqiStdev * stdevMultiplier1)

lowerBand2 = vqiSmoothed - (vqiStdev * stdevMultiplier2)

lowerBand3 = vqiSmoothed - (vqiStdev * stdevMultiplier3)

Signal Generation: Produces overbought/oversold signals when VQI reaches extreme levels (±200 in normalized mode).

Formula:

Bar Range = True Range (TR)

Weighted Volatility = Bar Range × (Close > Open ? 1 : Close < Open ? -1 : 0)

VQI Raw = EMA(Weighted Volatility, VQI Length)

VQI Smoothed = EMA(VQI Raw, Smoothing Length)

VQI Normalized = ((VQI Smoothed - Lowest VQI) / (Highest VQI - Lowest VQI) - 0.5) × 200

Upper Band N = VQI Smoothed + (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

Lower Band N = VQI Smoothed - (StdDev(VQI Smoothed, VQI Length) × Multiplier N)

🔶 DETAILS

Visual Features:

VQI Plot: Displays VQI as a line or histogram (lime for positive, red for negative).

Standard Deviation Bands: Plots three upper and lower bands (teal for upper, grayscale for lower) to indicate volatility thresholds.

Reference Levels: Horizontal lines at 0 (neutral), +100, and -100 (in normalized mode) for context.

Zone Highlighting: Overbought (⋎ above bars) and oversold (⋏ below bars) signals for extreme VQI levels (±200 in normalized mode).

Candle Coloring: Optional candle overlay colored by VQI direction (lime for positive, red for negative).

Interpretation:

VQI ≥ 200 (Normalized): Overbought condition, strong sell signal.

VQI 100–200: High volatility, potential selling opportunity.

VQI 0–100: Neutral bullish momentum.

VQI 0 to -100: Neutral bearish momentum.

VQI -100 to -200: High volatility, strong bearish momentum.

VQI ≤ -200 (Normalized): Oversold condition, strong buy signal.

🔶 EXAMPLES

Overbought Signal Detection: When VQI exceeds 200 (normalized), the indicator flags potential market tops with a red ⋎ symbol.

Example: During strong uptrends, VQI reaching 200 has historically preceded corrections, allowing traders to secure profits.

Oversold Signal Detection: When VQI falls below -200 (normalized), a lime ⋏ symbol highlights potential buying opportunities.

Example: In bearish markets, VQI dropping below -200 has marked reversal points for profitable long entries.

Volatility Trend Tracking: The VQI plot and bands help traders visualize shifts in market momentum.

Example: A rising VQI crossing above zero with widening bands indicates strengthening bullish momentum, guiding traders to hold or enter long positions.

Dynamic Support/Resistance: Standard deviation bands act as dynamic volatility thresholds during price movements.

Example: Price reversals often occur near the third standard deviation bands, providing reliable entry/exit points during volatile periods.

🔶 SETTINGS

Customization Options:

VQI Length: Adjust the EMA period for VQI calculation (default: 14, range: 1–50).

Smoothing Length: Set the EMA period for smoothing (default: 5, range: 1–50).

Standard Deviation Multipliers: Customize multipliers for bands (defaults: 1.0, 2.0, 3.0).

Normalization: Toggle normalization to -100/+100 scale and adjust lookback period (default: 200, min: 50).

Display Style: Switch between line or histogram plot for VQI.

Candle Overlay: Enable/disable VQI-colored candles (lime for positive, red for negative).

The Alpha-Extract Volatility Quality Indicator empowers traders with a robust tool to navigate market volatility. By combining directional price range analysis with smoothed volatility metrics, it identifies overbought and oversold conditions, offering clear buy and sell signals. The customizable standard deviation bands and optional normalization provide precise context for market conditions, enabling traders to make informed decisions across various market cycles.

T3 Volatility Quality Index (VQI) w/ DSL & Pips Filtering [Loxx]T3 Volatility Quality Index (VQI) w/ DSL & Pips Filtering is a VQI indicator that uses T3 smoothing and discontinued signal lines to determine breakouts and breakdowns. This also allows filtering by pips.***

What is the Volatility Quality Index ( VQI )?

The idea behind the volatility quality index is to point out the difference between bad and good volatility in order to identify better trade opportunities in the market. This forex indicator works using the True Range algorithm in combination with the open, close, high and low prices.

What are DSL Discontinued Signal Line?

A lot of indicators are using signal lines in order to determine the trend (or some desired state of the indicator) easier. The idea of the signal line is easy : comparing the value to it's smoothed (slightly lagging) state, the idea of current momentum/state is made.

Discontinued signal line is inheriting that simple signal line idea and it is extending it : instead of having one signal line, more lines depending on the current value of the indicator.

"Signal" line is calculated the following way :

When a certain level is crossed into the desired direction, the EMA of that value is calculated for the desired signal line

When that level is crossed into the opposite direction, the previous "signal" line value is simply "inherited" and it becomes a kind of a level

This way it becomes a combination of signal lines and levels that are trying to combine both the good from both methods.

In simple terms, DSL uses the concept of a signal line and betters it by inheriting the previous signal line's value & makes it a level.

What is the T3 moving average?

Better Moving Averages Tim Tillson

November 1, 1998

Tim Tillson is a software project manager at Hewlett-Packard, with degrees in Mathematics and Computer Science. He has privately traded options and equities for 15 years.

Introduction

"Digital filtering includes the process of smoothing, predicting, differentiating, integrating, separation of signals, and removal of noise from a signal. Thus many people who do such things are actually using digital filters without realizing that they are; being unacquainted with the theory, they neither understand what they have done nor the possibilities of what they might have done."

This quote from R. W. Hamming applies to the vast majority of indicators in technical analysis . Moving averages, be they simple, weighted, or exponential, are lowpass filters; low frequency components in the signal pass through with little attenuation, while high frequencies are severely reduced.

"Oscillator" type indicators (such as MACD , Momentum, Relative Strength Index ) are another type of digital filter called a differentiator.

Tushar Chande has observed that many popular oscillators are highly correlated, which is sensible because they are trying to measure the rate of change of the underlying time series, i.e., are trying to be the first and second derivatives we all learned about in Calculus.

We use moving averages (lowpass filters) in technical analysis to remove the random noise from a time series, to discern the underlying trend or to determine prices at which we will take action. A perfect moving average would have two attributes:

It would be smooth, not sensitive to random noise in the underlying time series. Another way of saying this is that its derivative would not spuriously alternate between positive and negative values.

It would not lag behind the time series it is computed from. Lag, of course, produces late buy or sell signals that kill profits.

The only way one can compute a perfect moving average is to have knowledge of the future, and if we had that, we would buy one lottery ticket a week rather than trade!

Having said this, we can still improve on the conventional simple, weighted, or exponential moving averages. Here's how:

Two Interesting Moving Averages

We will examine two benchmark moving averages based on Linear Regression analysis.

In both cases, a Linear Regression line of length n is fitted to price data.

I call the first moving average ILRS, which stands for Integral of Linear Regression Slope. One simply integrates the slope of a linear regression line as it is successively fitted in a moving window of length n across the data, with the constant of integration being a simple moving average of the first n points. Put another way, the derivative of ILRS is the linear regression slope. Note that ILRS is not the same as a SMA ( simple moving average ) of length n, which is actually the midpoint of the linear regression line as it moves across the data.

We can measure the lag of moving averages with respect to a linear trend by computing how they behave when the input is a line with unit slope. Both SMA (n) and ILRS(n) have lag of n/2, but ILRS is much smoother than SMA .

Our second benchmark moving average is well known, called EPMA or End Point Moving Average. It is the endpoint of the linear regression line of length n as it is fitted across the data. EPMA hugs the data more closely than a simple or exponential moving average of the same length. The price we pay for this is that it is much noisier (less smooth) than ILRS, and it also has the annoying property that it overshoots the data when linear trends are present.

However, EPMA has a lag of 0 with respect to linear input! This makes sense because a linear regression line will fit linear input perfectly, and the endpoint of the LR line will be on the input line.

These two moving averages frame the tradeoffs that we are facing. On one extreme we have ILRS, which is very smooth and has considerable phase lag. EPMA has 0 phase lag, but is too noisy and overshoots. We would like to construct a better moving average which is as smooth as ILRS, but runs closer to where EPMA lies, without the overshoot.

A easy way to attempt this is to split the difference, i.e. use (ILRS(n)+EPMA(n))/2. This will give us a moving average (call it IE /2) which runs in between the two, has phase lag of n/4 but still inherits considerable noise from EPMA. IE /2 is inspirational, however. Can we build something that is comparable, but smoother? Figure 1 shows ILRS, EPMA, and IE /2.

Filter Techniques

Any thoughtful student of filter theory (or resolute experimenter) will have noticed that you can improve the smoothness of a filter by running it through itself multiple times, at the cost of increasing phase lag.

There is a complementary technique (called twicing by J.W. Tukey) which can be used to improve phase lag. If L stands for the operation of running data through a low pass filter, then twicing can be described by:

L' = L(time series) + L(time series - L(time series))

That is, we add a moving average of the difference between the input and the moving average to the moving average. This is algebraically equivalent to:

2L-L(L)

This is the Double Exponential Moving Average or DEMA , popularized by Patrick Mulloy in TASAC (January/February 1994).

In our taxonomy, DEMA has some phase lag (although it exponentially approaches 0) and is somewhat noisy, comparable to IE /2 indicator.

We will use these two techniques to construct our better moving average, after we explore the first one a little more closely.

Fixing Overshoot

An n-day EMA has smoothing constant alpha=2/(n+1) and a lag of (n-1)/2.

Thus EMA (3) has lag 1, and EMA (11) has lag 5. Figure 2 shows that, if I am willing to incur 5 days of lag, I get a smoother moving average if I run EMA (3) through itself 5 times than if I just take EMA (11) once.

This suggests that if EPMA and DEMA have 0 or low lag, why not run fast versions (eg DEMA (3)) through themselves many times to achieve a smooth result? The problem is that multiple runs though these filters increase their tendency to overshoot the data, giving an unusable result. This is because the amplitude response of DEMA and EPMA is greater than 1 at certain frequencies, giving a gain of much greater than 1 at these frequencies when run though themselves multiple times. Figure 3 shows DEMA (7) and EPMA(7) run through themselves 3 times. DEMA^3 has serious overshoot, and EPMA^3 is terrible.

The solution to the overshoot problem is to recall what we are doing with twicing:

DEMA (n) = EMA (n) + EMA (time series - EMA (n))

The second term is adding, in effect, a smooth version of the derivative to the EMA to achieve DEMA . The derivative term determines how hot the moving average's response to linear trends will be. We need to simply turn down the volume to achieve our basic building block:

EMA (n) + EMA (time series - EMA (n))*.7;

This is algebraically the same as:

EMA (n)*1.7-EMA( EMA (n))*.7;

I have chosen .7 as my volume factor, but the general formula (which I call "Generalized Dema") is:

GD (n,v) = EMA (n)*(1+v)-EMA( EMA (n))*v,

Where v ranges between 0 and 1. When v=0, GD is just an EMA , and when v=1, GD is DEMA . In between, GD is a cooler DEMA . By using a value for v less than 1 (I like .7), we cure the multiple DEMA overshoot problem, at the cost of accepting some additional phase delay. Now we can run GD through itself multiple times to define a new, smoother moving average T3 that does not overshoot the data:

T3(n) = GD ( GD ( GD (n)))

In filter theory parlance, T3 is a six-pole non-linear Kalman filter. Kalman filters are ones which use the error (in this case (time series - EMA (n)) to correct themselves. In Technical Analysis , these are called Adaptive Moving Averages; they track the time series more aggressively when it is making large moves.

Included

Signals

Alerts

Related indicators

Zero-line Volatility Quality Index (VQI)

Volatility Quality Index w/ Pips Filtering

Variety Moving Average Waddah Attar Explosion (WAE)

***This indicator is tuned to Forex. If you want to make it useful for other tickers, you must change the pip filtering value to match the asset. This means that for BTC, for example, you likely need to use a value of 10,000 or more for pips filter.

Volatility Cloud (SAR)Inspired by the Volatility Index from Wilder

Apply the SAR point to highs, lows ans medians and create a cloud of volatility

Candle Percent Volatility by AllenlkThis indicator gives you the percentage movement of each candle. Measurements are taken between the candle High point and Low point, and also between the Open and Close and calculated in percent %. From there it smooths out the data with a moving average. This gives you an idea of how much volatility is within each candle given the time resolution of the chart.

I like to use this information as a way to turn off a strategy, or select a proper time resolution for a strategy. If each candle has less than 2.5% Volatility most strategies will typically buy and sell rapidly at prices that are too close together, potentially losing money. During those times it seems best to either temporarily turn off the strategy, change the time resolution or switch to another strategy.

Multi Fib Volatility StopA 7-band overlapping Fibonacci volatility stop. Select the start and multiplier and 6 increasing fibonacci bands will be overlayed to suggest areas of high probability buy/ sell opportunities.

Volatility Based Momentum (VBM)The Volatility Based Momentum (VBM) indicator is a variation on the rate-of-change (ROC) indicator. Instead of expressing momentum in a percentage gain or loss, VBM normalizes momentum using the historical volatility of the underlying security.

The VBM indicator offers numerous benefits to traders who orient their trading around volatility. For these traders, VBM expresses momentum in a normalized, universally applicable ‘multiples of volatility’ (MoV) unit. Given the universal applicability of MoV, VBM is especially suited to traders whose trading incorporates numerous timeframes, different types of securities (e.g., stocks, Forex pairs), or the frequent comparison of momentum between multiple securities.

The calculation for a volatility based momentum (VBM) indicator is very similar to ROC, but divides by the security’s historical volatility instead. The average true range indicator (ATR) is used to compute historical volatility.

VBM(n,v) = (Close - Close n periods ago) / ATR(v periods)

For example, on a daily chart, VBM(22,65) calculates how many MoV price has increased or decreased over the last 22 trading days (approximately one calendar month). The second parameter is the number of periods to use with the ATR indicator to normalize the momentum in terms of volatility.

For more details, there is an article further describing VBM and its applicability versus ROC.

[RS]Function Volatility Stop V0Function for Volatility Stop:

added some tweeks so it can be used on any series as in example a rsi.

VDUB Bands - MTF WMA+ATR Volatility Lanes (6 Alerts)VDUB Bands draws volatility-scaled “trend lanes” around a Weighted Moving Average (WMA) using ATR (or a WMA of True Range). It can display up to four tiers (L1–L4), with higher tiers sourced from higher timeframes to show local structure → higher-timeframe structure on a single chart.

────────────────────────────────────────

1. What it does (plain English)

────────────────────────────────────────

Think of each tier as a lane system around the trend:

• Inner rails = “normal volatility lane” around the WMA

• Outer rails = “extension / extreme zone” for that tier

• Higher tiers (L3/L4) show bigger structure

• Lower tiers (L1/L2) show active lane behavior

Typical interpretation:

• Price inside inner rails → normal variance around the trend lane

• Between inner and outer → stretched, but not extreme

• Outside outer rails → extended vs that tier’s volatility band

────────────────────────────────────────

2) Why it’s useful (and why it’s not a mashup)

────────────────────────────────────────

This is not a bundle of unrelated indicators. Everything serves one cohesive purpose:

• Visualize trend + volatility lanes across multiple time horizons

• Keep rails consistent and readable (levels, fills, outlines)

• Optional multi-timeframe aggregation for structure context

• A compact 6-alert set to catch key transitions without alert spam

────────────────────────────────────────

3) What you see on the chart

────────────────────────────────────────

For each level (L1–L4), you can show:

• Upper/Lower Inner rails

• Upper/Lower Outer rails

• Optional center fill (between outer rails) = operating range

• Optional MA line per tier (off by default to reduce clutter)

• Base WMA line (L1 MA) if enabled

Suggested workflow:

• Start with L1 + L2 only

• Add L3/L4 once you like the structure view

• Use Dynamic Opacity if the chart feels crowded

────────────────────────────────────────

4) How it works (transparent formula)

────────────────────────────────────────

For each tier:

• MA = WMA(source, baseLen × levelMultiplier)

• ATR_like = Wilder ATR (default)

OR WMA(TrueRange, atrLen × levelMultiplier)

Inner rails:

• upperInner = MA + ATR_like × innerMult

• lowerInner = MA - ATR_like × innerMult

Outer rails:

• upperOuter = MA + ATR_like × outerMult

• lowerOuter = MA - ATR_like × outerMult

Tier behavior:

• L1 uses the chart timeframe

• L2–L4 can use user-selected HTFs (defaults: 4H / D / W)

or optional auto-selection

────────────────────────────────────────

5) Multi-timeframe behavior + interpolation

────────────────────────────────────────

• L2–L4 use request.security() with lookahead OFF (no future data).

• HTF bands naturally “step” when the HTF candle confirms.

• Interpolate HTF Bands (optional): visually blends from the prior confirmed HTF value to the current confirmed HTF value to reduce stepping. This is display smoothing, not prediction.

Repaint note:

• If Live Interp (Repaints) is enabled, the HTF lines can update intrabar and may repaint. Keep it OFF for strict non-repainting behavior.

────────────────────────────────────────

6) Auto-select L2/L3/L4 (optional)

────────────────────────────────────────

Two modes:

A) Ladder (deterministic)

• Picks “bigger” timeframes relative to the chart (simple and fast).

B) Score (data-driven)

• Tests candidate timeframes and scores them using:

• Coverage: % of closes inside the OUTER band over Score Lookback

• Width: average outer-band width as a fraction of MA

• Targets: Target Coverage + Target Width

• Weights: Coverage Weight + Width Weight

Performance notes:

• Score mode is heavier (many candidates).

• “Lock auto-select after first pick” is recommended to reduce load and avoid platform limits.

────────────────────────────────────────

7) Alerts (6 total, aggregated across L1–L4)

────────────────────────────────────────

Alerts trigger if ANY tier meets the condition:

• Cross ABOVE an OUTER band

• Cross BELOW an OUTER band

• Cross ABOVE an INNER band

• Cross BELOW an INNER band

• Price is OUTSIDE ABOVE an OUTER band

• Price is OUTSIDE BELOW an OUTER band

These are intentionally aggregated to keep the alert count small while catching meaningful transitions.

────────────────────────────────────────

8) Limitations & transparency

────────────────────────────────────────

• Indicator only (not a strategy). No performance claims.

• MTF values update when the higher timeframe candle confirms.

• Interpolation is visual smoothing; it does not forecast.

• Non-standard chart types (Heikin Ashi/Renko/etc) may behave differently from standard candles.

• If you enable repainting options, signals/levels may change intrabar.

────────────────────────────────────────

9) Credits/reuse disclosure

────────────────────────────────────────

• Conceptual inspiration: VDUB and the community “VDUB_BINARY_PRO_3_V2” idea of WMA ± TR/ATR × multipliers.

• This version is a reimplementation + extension, adding:

o Multi-tier architecture (L1–L4)

o Higher-timeframe sourcing + optional interpolation

o Optional scoring-based timeframe selection

o Dynamic opacity + streamlined plotting

o Aggregated 6-alert set

No code was copied directly from the older script; this is a rewritten implementation with additional features and different structure.

www.tradingview.com

Volatility Regime NavigatorA guide to understanding VIX, VVIX, VIX9D, VVIX/VIX, and the Composite Risk Score

1. Purpose of the Indicator

This dashboard summarizes short-term market volatility conditions using four core volatility metrics.

It produces:

• Individual readings

• A combined Regime classification

• A Composite Risk Score (0–100)

• A simplified Risk Bucket (Bullish → Stress)

Use this to evaluate market fragility, drift potential, tail-risk, and overall risk-on/off conditions.

This is especially useful for intraday ES/NQ trading, expected-move context, and understanding when breakouts or fades have edge.

2. The Four Core Volatility Inputs

(1) VIX — Baseline Equity Volatility

• < 16: Complacent (easy drift-up, but watch for fragility)

• 16–22: Healthy, normal volatility → ideal trading conditions

• > 22: Stress rising

• > 26: Tail-risk / risk-off environment

(2) VIX9D — Short-Term Event Vol

Measures 9-day implied volatility. Reacts to immediate news/events.

• < 14: Strongly bullish (drift regime)

• 14–17: Bullish to neutral

• 17–20: Event risk building

• > 20: Short-term stress / caution

(3) VVIX — Volatility of VIX (fragility index)

Tracks volatility of volatility.

• < 100: “Bullish, Bullish” — very low fragility

• 100–120: Normal

• 120–140: Fragile

• > 140: Stress, hedging pressure

(4) VVIX/VIX Ratio — Microstructure Risk-On/Risk-Off

One of the most sensitive indicators of market confidence.

• 5.0–6.5: Strongest “normal/bullish” zone

• < 5.0: Bottom-stalking / fear regime

• > 6.5: Complacency → vulnerable to reversals

• > 7.5: Fragile / top-risk

3. Composite Risk Score (0–100)

The dashboard converts all four inputs into a single score.

Score Interpretation

• 80–100 → Bullish - Drift regime. Shallow pullbacks. Upside favored.

• 60–79 → Normal - Healthy tape. Balanced two-way trading.

• 40–59 → Fragile - Choppy, failed breakouts, thinner liquidity.

• 20–39 → Risk-Off - Downside tails active. Favor fades and defensive behavior.

• < 20 → Stress - Crisis or event-driven tape. Avoid longs.

Score updates every bar.

4. Regime Label

Independent of the composite score, the script provides a Regime classification based on combinations of VIX + VVIX/VIX:

• Bullish+ → Buying is easy, tape lifts passively

• Normal → Cleanest and most tradable conditions

• Complacent → Top-risk; be careful chasing upside

• Mixed → Signals conflict; chop potential

• Bottom Stalk → High VIX, low VVIX/VIX (capitulation signatures)

A trailing “+” or “*” indicates additional bullish or caution overlays from VIX9D/VVIX.

5. How to Use the Dashboard in Trading

When Bullish (Score ≥ 80):

• Expect drift-up behavior

• Downside limited unless catalyst hits

• Structure favors breakouts and trend continuation

• Mean reversion trades have lower expectancy

When Normal (Score 60–79):

• The “playbook regime”

• Breakouts and mean reversion both valid

• Best overall trading environment

When Fragile (Score 40–59):

• Expect chop

• Breakouts fail

• Take quicker profits

• Avoid overleveraged directional bets

When Risk-Off (20–39):

• Favor fades of strength

• Downside tails activate

• Trend-following short setups gain edge

• Respect volatility bands

When Stress (<20):

• Avoid long exposure

• Do not chase dips

• Expect violent, news-sensitive behavior

• Position sizing becomes critical

6. Quick Summary

• VIX = weather

• VIX9D = short-term storm radar

• VVIX = foundation stability

• VVIX/VIX = confidence vs fragility

• Composite Score = overall regime health

• Risk Bucket = simple “what do I do?” label

This dashboard gives traders a high-confidence, low-noise view of equity volatility conditions in real time.