Advanced Multi-Timeframe Trend & Signal System═══════════════════════════════════════════════════════════════

ADVANCED MULTI-TIMEFRAME TREND & SIGNAL SYSTEM v1.0

═══════════════════════════════════════════════════════════════

Created by: Zakaria Safri

License: Mozilla Public License 2.0

A comprehensive technical analysis tool designed for traders seeking

multi-dimensional market insights. This indicator combines proven

technical analysis methods with modern visualization techniques.

═══════════════════════════════════════════════════════════════

KEY FEATURES

═══════════════════════════════════════════════════════════════

✓ SUPERTREND SIGNAL GENERATION

- Customizable sensitivity settings

- Clear long/short entry signals

- Automatic trend direction detection

- ATR-based dynamic calculations

✓ MULTI-TIMEFRAME DASHBOARD

- Real-time trend analysis across 6 timeframes

- Synchronized trend confirmation

- Customizable table position and size

- Current: 1M, 5M, 15M, 1H, 1D coverage

✓ QQE REVERSAL DETECTION

- Quantitative Qualitative Estimation algorithm

- Early reversal signal identification

- Adjustable RSI and smoothing parameters

- Confirmation-based plotting

✓ DYNAMIC SUPPORT & RESISTANCE

- Pivot-based level calculation

- Quick and standard pivot detection

- Color-coded zones (8 levels)

- Automatic level updates

✓ MOMENTUM BREAKOUT SIGNALS

- Ichimoku-inspired calculations

- Bullish and bearish breakout detection

- Visual zone highlighting

- Trend confirmation filters

✓ RISK MANAGEMENT SYSTEM

- ATR-based stop loss calculation

- Multiple take profit targets (TP1, TP2, TP3)

- Customizable risk-to-reward ratios

- Dynamic price level tracking

- Hit detection markers

✓ VOLATILITY BANDS

- Keltner Channel implementation

- Multiple band layers (3 levels)

- EMA-based calculations

- Adaptive to market conditions

✓ TREND CLOUD VISUALIZATION

- Dual moving average cloud

- Clear trend direction indication

- Customizable color scheme

- Trend bar coloring

═══════════════════════════════════════════════════════════════

HOW TO USE

═══════════════════════════════════════════════════════════════

SETUP:

1. Add indicator to your chart

2. Configure sensitivity in Core Signals section

3. Enable desired features (signals, reversals, breakouts)

4. Set up risk management levels if trading

5. Position MTF dashboard to preference

SIGNAL INTERPRETATION:

• LONG Signal: Price crosses above Supertrend

• SHORT Signal: Price crosses below Supertrend

• REV (Reversal): QQE indicates potential trend change

• Diamond Breakouts: Momentum shift confirmation

• T1/T2/T3: Take profit level hits

MULTI-TIMEFRAME ANALYSIS:

• Green (BULL): Higher timeframe supports uptrend

• Red (BEAR): Higher timeframe supports downtrend

• Use for trend alignment and confirmation

• Best results when multiple timeframes align

RISK MANAGEMENT:

• Enable Stop Loss for automatic SL calculation

• Activate TP levels based on trading style

• Adjust Risk-to-Reward ratio (1:1 to 1:10)

• Monitor hit detection circles for exits

═══════════════════════════════════════════════════════════════

TECHNICAL SPECIFICATIONS

═══════════════════════════════════════════════════════════════

CALCULATIONS:

• Supertrend: ATR-based with customizable multiplier

• QQE: Modified RSI with Wilders smoothing

• Keltner Channels: EMA basis with ATR bands

• Pivots: Standard left/right bar methodology

• Support/Resistance: Multi-level pivot analysis

PARAMETERS:

• Supertrend Sensitivity: 0.5 to 10.0 (default: 2.0)

• RSI Period: 5 to 50 (default: 14)

• QQE Multiplier: 1.0 to 10.0 (default: 4.238)

• Risk-to-Reward: 1 to 10 (default: 4)

TIMEFRAMES:

Compatible with all timeframes. MTF dashboard displays:

• 1 Minute (1M)

• 5 Minutes (5M)

• 15 Minutes (15M)

• 1 Hour (1H)

• 1 Day (1D)

• Current chart timeframe

═══════════════════════════════════════════════════════════════

CUSTOMIZATION OPTIONS

═══════════════════════════════════════════════════════════════

VISUAL:

• Professional color scheme (Cyan/Orange)

• Adjustable table position (9 positions)

• Table size options (tiny/small/normal/large)

• Transparent zone highlighting

• Clean, modern label design

TOGGLES:

• Enable/disable any feature independently

• Show/hide signals, reversals, breakouts

• Toggle S/R levels and zones

• Control trend cloud and bands

• Master trend line optional

ALERTS:

The indicator provides visual signals that can be used with

TradingView's alert system by setting alerts on the indicator.

═══════════════════════════════════════════════════════════════

BEST PRACTICES

═══════════════════════════════════════════════════════════════

✓ Combine signals for higher probability setups

✓ Use MTF dashboard for trend confirmation

✓ Respect S/R levels for entry/exit planning

✓ Monitor QQE reversals at key price levels

✓ Adjust sensitivity based on asset volatility

✓ Test on demo/paper trading first

✓ Use proper risk management always

═══════════════════════════════════════════════════════════════

IMPORTANT DISCLAIMER

═══════════════════════════════════════════════════════════════

This indicator is a technical analysis tool and does NOT:

• Guarantee profitable trades

• Provide financial advice

• Predict future price movements with certainty

• Replace proper risk management

• Substitute for personal due diligence

Past performance does not indicate future results. All trading

involves risk. Users should:

- Understand the indicator's logic

- Test thoroughly before live trading

- Use appropriate position sizing

- Never risk more than they can afford to lose

- Consult financial advisors if needed

═══════════════════════════════════════════════════════════════

CODING STANDARDS

═══════════════════════════════════════════════════════════════

This indicator follows PineCoders Coding Conventions:

✓ Proper variable naming (prefixes: i_, f_, c_)

✓ Clear function documentation

✓ Organized code structure

✓ Type declarations

✓ Efficient calculations

✓ No repainting (confirmed signals)

✓ Proper use of request.security

═══════════════════════════════════════════════════════════════

SUPPORT & UPDATES

═══════════════════════════════════════════════════════════════

Version: 1.0

Author: Zakaria Safri

License: MPL 2.0

Last Updated: 2024

For questions, feedback, or suggestions, please comment below.

═══════════════════════════════════════════════════════════════

#trading #signals #supertrend #multiTimeframe #QQE #reversals

#supportResistance #riskManagement #trendAnalysis #momentum

在腳本中搜尋"a股板块+沪深两市+股价不超过10元的股票+技术形态好"

Choppiness Index | CipherDecodedThe Choppiness Index is a multi-timeframe regime indicator that measures whether price action is trending or consolidating.

This recreation was inspired by the Choppiness Index chart from Checkonchain, with full credit to their team for the idea.

🔹 How It Works

CI = 100 * log10( SUM(ATR(1), n) / (highest(high, n) – lowest(low, n)) ) / log10(n)

Where:

n – lookback length (e.g. 14 days / 10 weeks / 10 months)

ATR(1) – true-range of each bar

SUM(ATR(1), n) – total true-range over n bars

highest(high, n) and lowest(low, n) – price range over n bars

Low values → strong trend

High values → sideways consolidation

Below is a simplified function used in the script for computing CI on any timeframe:

f_ci(_n) =>

_tr = ta.tr(true)

_sum = math.sum(_tr, _n)

_hh = ta.highest(high, _n)

_ll = ta.lowest(low, _n)

_rng = _hh - _ll

_rng > 0 ? 100 * math.log10(_sum / _rng) / math.log10(_n) : na

Consolidation Threshold — 50.0

Trend Threshold — 38.2

When Weekly CI < Trend Threshold, a trending zone (yellow) appears.

When Weekly CI > Consolidation Threshold, a consolidation zone (purple) appears.

Users can toggle either background independently.

🔹 Example Background Logic

bgcolor(isTrend and Trend ? color.new(#f3e459, 50) : na, title = "Trending", force_overlay = true)

bgcolor(isConsol and Cons ? color.new(#974aa5, 50) : na, title = "Consolidation", force_overlay = true)

🔹 Usage Tips

Observe the Weekly CI for regime context.

Combine with price structure or trend filters for signal confirmation.

Low CI values (< 38) indicate strong trend activity — the market may soon consolidate to reset.

High CI values (> 60) reflect sideways or range-bound conditions — the market is recharging before a potential new trend.

🔹 Disclaimer

This indicator is provided for educational purposes.

No trading outcomes are guaranteed.

This tool does not guarantee market turns or performance; it should be used as part of a broader system.

Use responsibly and perform your own testing.

🔹 Credits

Concept origin — Checkonchain Choppiness Index

Asia Session 2h (8PM–10PM EST, Today Only)This indicator automatically highlights the first 2 hours of the Asia trading session (8:00 PM – 10:00 PM EST) with a transparent teal box. It updates daily and only displays the current day’s session for a clean chart appearance.

Features:

Marks the Asia session open range (8–10 PM EST).

Automatically adjusts each day.

Works on any timeframe.

No clutter — only shows today’s box.

Ideal for traders who want to track Tokyo/Asia session volatility or identify key breakout zones before the London open.

Multi-Timeframe EMA Trend Dashboard with Volume and RSI Filters═══════════════════════════════════════════════════════════

MULTI-TIMEFRAME EMA TREND DASHBOARD

═══════════════════════════════════════════════════════════

OVERVIEW

This indicator provides a comprehensive view of trend direction across multiple timeframes using the classic EMA 20/50 crossover methodology, enhanced with volume confirmation and RSI filtering. It aggregates trend information from six timeframes into a single dashboard for efficient market analysis.

The indicator is designed for educational purposes and to assist traders in identifying potential trend alignments across different time horizons.

═══════════════════════════════════════════════════════════

FEATURES

═══════════════════════════════════════════════════════════

MULTI-TIMEFRAME ANALYSIS

• Monitors 6 timeframes simultaneously: 1m, 5m, 15m, 1H, 4H, 1D

• Each timeframe analyzed independently using request.security()

• Non-repainting implementation with proper lookahead settings

• Calculates overall trend strength as percentage of bullish timeframes

EMA CROSSOVER SYSTEM

• Fast EMA (default: 20) and Slow EMA (default: 50)

• Bullish: Fast EMA > Slow EMA

• Bearish: Fast EMA < Slow EMA

• Neutral: Fast EMA = Slow EMA (rare condition)

• Visual EMA plots with optional fill area

VOLUME CONFIRMATION

• Optional volume filter for crossover signals

• Compares current volume against moving average (default: 20-period SMA)

• Categorizes volume as: High (>1.5x average), Normal (>average), Low (70), oversold (<30), and neutral zones

• Used in quality score calculation

• Optional display toggle

SUPPORT & RESISTANCE DETECTION

• Automatic detection using highest/lowest over lookback period (default: 50 bars)

• Plots resistance (red), support (green), and mid-level (gray)

• Step-line style for clear visualization

• Optional display toggle

QUALITY SCORING SYSTEM

• Rates trade setups from 1-5 stars

• Considers: MTF alignment, volume confirmation, RSI positioning

• 5 stars: 4+ timeframes aligned + volume confirmed + RSI 50-70

• 4 stars: 4+ timeframes aligned + volume confirmed

• 3 stars: 3+ timeframes aligned

• 2 stars: Exactly 3 timeframes aligned

• 1 star: Other conditions

VISUAL DASHBOARD

• Clean table display (position customizable)

• Color-coded trend indicators (green/red/yellow)

• Extended statistics panel (toggleable)

• Shows: Trends, Strength, Quality, RSI, Volume, Price Distance

═══════════════════════════════════════════════════════════

TECHNICAL SPECIFICATIONS

═══════════════════════════════════════════════════════════

CALCULATIONS

Trend Determination per Timeframe:

• request.security() fetches EMA values with gaps=off, lookahead=off

• Compares Fast EMA vs Slow EMA

• Returns: 1 (bullish), -1 (bearish), 0 (neutral)

Trend Strength:

• Counts number of bullish timeframes

• Formula: (bullish_count / 6) × 100

• Range: 0% (all bearish) to 100% (all bullish)

Price Distance from EMA:

• Formula: ((close - EMA) / EMA) × 100

• Positive: Price above EMA

• Negative: Price below EMA

• Warning when absolute distance > 5%

ANTI-REPAINTING MEASURES

• All request.security() calls use lookahead=barmerge.lookahead_off

• Dashboard updates only on barstate.islast

• Historical bars remain unchanged

• Crossover signals finalize on bar close

═══════════════════════════════════════════════════════════

USAGE GUIDE

═══════════════════════════════════════════════════════════

INTERPRETING THE DASHBOARD

Timeframe Rows:

• Each row shows individual timeframe trend status

• Look for alignment (multiple timeframes same direction)

• Higher timeframes generally more significant

Strength Indicator:

• >66.67%: Strong bullish (4+ timeframes bullish)

• 33.33-66.67%: Mixed/choppy conditions

• <33.33%: Strong bearish (4+ timeframes bearish)

Quality Score:

• Higher stars = better confluence of factors

• 5-star setups have strongest multi-factor confirmation

• Lower scores may indicate weaker or conflicting signals

SUGGESTED APPLICATIONS

Trend Confirmation:

• Check if multiple timeframes confirm current chart trend

• Higher agreement = stronger trend confidence

• Use for position sizing decisions

Entry Timing:

• Wait for EMA crossover on chart timeframe

• Confirm with higher timeframe alignment

• Volume above average preferred

• RSI not in extreme zones

Divergence Detection:

• When lower timeframes diverge from higher

• May indicate trend exhaustion or reversal

• Requires additional confirmation

CUSTOMIZATION

EMA Settings:

• Adjust Fast/Slow lengths for different sensitivities

• Shorter periods = more responsive, more signals

• Longer periods = smoother, fewer signals

• Common alternatives: 10/30, 12/26, 50/200

Volume Filter:

• Enable for higher-quality signals (fewer false positives)

• Disable in always-liquid markets or for more signals

• Adjust MA length based on typical volume patterns

Display Options:

• Toggle EMAs, S/R levels, extended stats as needed

• Choose dashboard position to avoid chart overlap

• Adjust colors for visibility preferences

═══════════════════════════════════════════════════════════

ALERTS

═══════════════════════════════════════════════════════════

AVAILABLE ALERT CONDITIONS

1. Bullish EMA Cross (Volume Confirmed)

2. Bearish EMA Cross (Volume Confirmed)

3. Strong Bullish Alignment (4+ timeframes)

4. Strong Bearish Alignment (4+ timeframes)

5. Trend Strength Increasing (>16.67% jump)

6. Trend Strength Decreasing (>16.67% drop)

7. Excellent Trade Setup (5-star rating)

Alert messages use standard placeholders:

• {{ticker}} - Symbol name

• {{close}} - Current close price

• {{time}} - Bar timestamp

═══════════════════════════════════════════════════════════

LIMITATIONS & CONSIDERATIONS

═══════════════════════════════════════════════════════════

KNOWN LIMITATIONS

• Lower timeframe data may not be available on all symbols

• 1-minute data typically limited to recent history

• request.security() subject to TradingView data limits

• Dashboard requires screen space (may overlap on small screens)

• More complex calculations may affect load time on slower devices

NOT SUITABLE FOR

• Highly volatile/illiquid instruments (many false signals)

• News-driven markets during announcements

• Automated trading without additional filters

• Markets where EMA strategies don't perform well

DOES NOT PROVIDE

• Exact entry/exit prices

• Stop-loss or take-profit levels

• Position sizing recommendations

• Guaranteed profit signals

• Market predictions

═══════════════════════════════════════════════════════════

BEST PRACTICES

═══════════════════════════════════════════════════════════

RECOMMENDED USAGE

✓ Combine with price action analysis

✓ Use appropriate risk management

✓ Backtest on historical data before live use

✓ Adjust settings for specific market characteristics

✓ Wait for higher-quality setups in important trades

✓ Consider overall market context and fundamentals

NOT RECOMMENDED

✗ Using as standalone trading system without confirmation

✗ Trading every signal without discretion

✗ Ignoring risk management principles

✗ Trading without understanding the methodology

✗ Applying to unsuitable markets/timeframes

═══════════════════════════════════════════════════════════

EDUCATIONAL BACKGROUND

═══════════════════════════════════════════════════════════

EMA CROSSOVER STRATEGY

The Exponential Moving Average crossover is a classical trend-following technique:

• Golden Cross: Fast EMA crosses above Slow EMA (bullish signal)

• Death Cross: Fast EMA crosses below Slow EMA (bearish signal)

• Widely used since the 1970s in various markets

• More responsive than SMA due to exponential weighting

MULTI-TIMEFRAME ANALYSIS

Analyzing multiple timeframes helps traders:

• Identify alignment between short and long-term trends

• Reduce false signals from single-timeframe noise

• Understand market context across different horizons

• Make informed decisions about trade duration

VOLUME ANALYSIS

Volume confirmation adds reliability:

• High volume suggests institutional participation

• Low volume signals may indicate false breakouts

• Volume precedes price in many market theories

• Helps distinguish genuine moves from noise

═══════════════════════════════════════════════════════════

TECHNICAL IMPLEMENTATION

═══════════════════════════════════════════════════════════

CODE STRUCTURE

• Organized in clear sections with proper commenting

• Uses explicit type declarations (int, float, bool, color, string)

• Constants defined at top (BULLISH=1, BEARISH=-1, etc.)

• Functions documented with @function, @param, @returns

• Follows PineCoders naming conventions (camelCase variables)

PERFORMANCE OPTIMIZATION

• var keyword for table (created once, not every bar)

• Calculations cached where possible

• Dashboard updates only on last bar

• Minimal redundant security() calls

SECURITY IMPLEMENTATION

• Proper gaps and lookahead parameters

• No future data leakage

• Signals finalize on bar close

• Historical bars remain static

═══════════════════════════════════════════════════════════

VERSION INFORMATION

═══════════════════════════════════════════════════════════

Current Version: 2.0

Pine Script Version: 5

Last Updated: 2024

Developed by: Zakaria Safri

═══════════════════════════════════════════════════════════

SETTINGS REFERENCE

═══════════════════════════════════════════════════════════

EMA SETTINGS

• Fast EMA Length: 1-500 (default: 20)

• Slow EMA Length: 1-500 (default: 50)

VOLUME & MOMENTUM

• Use Volume Confirmation: true/false (default: true)

• Volume MA Length: 1-500 (default: 20)

• Show RSI Levels: true/false (default: true)

• RSI Length: 1-500 (default: 14)

PRICE ACTION FEATURES

• Show Price Distance: true/false (default: true)

• Show Key Levels: true/false (default: true)

• S/R Lookback Period: 10-500 (default: 50)

DISPLAY SETTINGS

• Show EMAs on Chart: true/false (default: true)

• Fast EMA Color: customizable (default: cyan)

• Slow EMA Color: customizable (default: orange)

• EMA Line Width: 1-5 (default: 2)

• Show Fill Between EMAs: true/false (default: true)

• Show Crossover Signals: true/false (default: true)

DASHBOARD SETTINGS

• Position: Top Left/Right, Bottom Left/Right

• Show Extended Statistics: true/false (default: true)

ALERT SETTINGS

• Alert on Multi-TF Alignment: true/false (default: true)

• Alert on Trend Strength Change: true/false (default: true)

═══════════════════════════════════════════════════════════

RISK DISCLAIMER

═══════════════════════════════════════════════════════════

This indicator is provided for educational and informational purposes only. It should not be considered financial advice or a recommendation to buy or sell any security.

IMPORTANT NOTICES:

• Past performance does not indicate future results

• All trading involves risk of capital loss

• No indicator guarantees profitable trades

• Always conduct independent research and analysis

• Use proper risk management and position sizing

• Consult a qualified financial advisor before trading

• The developer assumes no liability for trading losses

By using this indicator, you acknowledge that you understand these risks and accept full responsibility for your trading decisions.

═══════════════════════════════════════════════════════════

SUPPORT & CONTRIBUTIONS

═══════════════════════════════════════════════════════════

FEEDBACK WELCOME

• Constructive comments appreciated

• Bug reports help improve the indicator

• Feature suggestions considered for future versions

• Share your experience to help other users

OPEN SOURCE

This code is published as open source for the TradingView community to:

• Learn from the implementation

• Modify for personal use

• Understand multi-timeframe analysis techniques

If you find this indicator useful, please consider:

• Leaving a thoughtful review

• Sharing with other traders who might benefit

• Following for future updates and releases

═══════════════════════════════════════════════════════════

ADDITIONAL RESOURCES

═══════════════════════════════════════════════════════════

RECOMMENDED READING

• TradingView Pine Script documentation

• PineCoders community resources

• Technical analysis textbooks on moving averages

• Multi-timeframe trading strategy guides

• Risk management principles

RELATED CONCEPTS

• Trend following strategies

• Moving average convergence/divergence

• Multiple timeframe analysis

• Volume-price relationships

• Momentum indicators

═══════════════════════════════════════════════════════════

Thank you for using this indicator. Trade responsibly and continue learning!

═══════════════════════════════════════════════════════════

Adaptive Trend 1m ### Overview

The "Adaptive Trend Impulse Parallel SL/TP 1m Realistic" strategy is a sophisticated trading system designed specifically for high-volatility markets like cryptocurrencies on 1-minute timeframes. It combines trend-following with momentum filters and adaptive parameters to dynamically adjust to market conditions, ensuring more reliable entries and risk management. This strategy uses SuperTrend for primary trend detection, enhanced by MACD, RSI, Bollinger Bands, and optional volume spikes. It incorporates parallel stop-loss (SL) and multiple take-profit (TP) levels based on ATR, with options for breakeven and trailing stops after the first TP. Optimized for realistic backtesting on short timeframes, it avoids over-optimization by adapting indicators to market speed and efficiency.

### Principles of Operation

The strategy operates on the principle of adaptive impulse trading, where entry signals are generated only when multiple conditions align to confirm a strong trend reversal or continuation:

1. **Trend Detection (SuperTrend)**: The core signal comes from an adaptive SuperTrend indicator. It calculates upper and lower bands using ATR (Average True Range) with dynamic periods and multipliers. A buy signal occurs when the price crosses above the lower band (from a downtrend), and a sell signal when it crosses below the upper band (from an uptrend). Adaptation is based on Rate of Change (ROC) to measure market speed, shortening periods in fast markets for quicker responses.

2. **Momentum and Trend Filters**:

- **MACD**: Uses adaptive fast and slow lengths. In "Trend Filter" mode (default when "Use MACD Cross" is false), it checks if the MACD line is above/below the signal for long/short. In cross mode, it requires a crossover/crossunder.

- **RSI**: Adaptive period RSI must be above 50 for longs and below 50 for shorts, confirming overbought/oversold conditions dynamically.

- **Bollinger Bands (BB)**: Depending on the mode ("Midline" by default), it requires the price to be above/below the BB midline for longs/shorts, or a breakout in "Breakout" mode. Deviation adapts to market efficiency.

- **Volume Spike Filter** (optional): Entries require volume to exceed an adaptive multiple of its SMA, signaling strong impulse.

3. **Volatility Filter**: Entries are only allowed if current ATR percentage exceeds a historical minimum (adaptive), preventing trades in low-volatility ranges.

4. **Risk Management (Parallel SL/TP)**:

- **Stop-Loss**: Set at an adaptive ATR multiple below/above entry for long/short.

- **Take-Profits**: Three levels at adaptive ATR multiples, with partial position closures (e.g., 51% at TP1, 25% at TP2, remainder at TP3).

- **Post-TP1 Features**: Optional breakeven moves SL to entry after TP1. Trailing SL uses BB midline as a dynamic trail.

- All levels are calculated per trade using the ATR at entry, making them "realistic" for 1m charts by widening SL and tightening initial TPs.

The strategy enters long on buy signals with all filters met, and short on sell signals. It uses pyramid margin (100% long/short) for full position sizing.

Adaptation is driven by:

- **Market Speed (normSpeed)**: Based on ROC, tightens multipliers in volatile periods.

- **Efficiency Ratio (ER)**: Measures trend strength, adjusting periods for trending vs. ranging markets.

This ensures the strategy "adapts" without manual tweaks, reducing false signals in varying conditions.

### Main Advantages

- **Adaptability**: Unlike static strategies, parameters dynamically adjust to market volatility and trend strength, improving performance across ranging and trending phases without over-optimization.

- **Realistic Risk Management for 1m**: Wider SL and tiered TPs prevent premature stops in noisy short-term charts, while partial profits lock in gains early. Breakeven/trailing options protect profits in extended moves.

- **Multi-Filter Confirmation**: Combines trend, momentum, and volume for high-probability entries, reducing whipsaws. The volatility filter avoids flat markets.

- **Debug Visualization**: Built-in plots for signals, levels, and component checks (when "Show Debug" is enabled) help users verify logic on charts.

- **Efficiency**: Low computational load, suitable for real-time trading on TradingView with alerts.

Backtesting shows robust results on volatile assets, with a focus on sustainable risk (e.g., SL at 3x ATR avoids excessive drawdowns).

### Uniqueness

What sets this strategy apart is its **fully adaptive framework** integrating multiple indicators with real-time market metrics (ROC for speed, ER for efficiency). Most trend strategies use fixed parameters, leading to poor adaptation; here, every key input (periods, multipliers, deviations) scales dynamically within bounds, creating a "self-tuning" system. The "parallel SL/TP with 1m realism" adds custom handling for micro-timeframes: tightened initial TPs for quick wins and adaptive min-ATR filter to skip low-vol bars. Unlike generic mashups, it justifies the combination—SuperTrend for trend, MACD/RSI/BB for impulse confirmation, volume for conviction—working synergistically to capture "trend impulses" while filtering noise. The post-TP1 breakeven/trailing tied to BB adds a unique profit-locking mechanism not common in open-source scripts.

### Recommended Settings

These settings are optimized and recommended for trading ASTER/USDT on Bybit, with 1-minute chart, x10 leverage, and cross margin mode. They provide a balanced risk-reward for this volatile pair:

- **Base Inputs**:

- Base ATR Period: 10

- Base SuperTrend ATR Multiplier: 2.5

- Base MACD Fast: 8

- Base MACD Slow: 17

- Base MACD Signal: 6

- Base RSI Period: 9

- Base Bollinger Period: 12

- Bollinger Deviation: 1.8

- Base Volume SMA Period: 19

- Base Volume Spike Multiplier: 1.8

- Adaptation Window: 54

- ROC Length: 10

- **TP/SL Settings**:

- Use Stop Loss: True

- Base SL Multiplier (ATR): 3

- Use Take Profits: True

- Base TP1 Multiplier (ATR): 5.5

- Base TP2 Multiplier (ATR): 10.5

- Base TP3 Multiplier (ATR): 19

- TP1 % Position: 51

- TP2 % Position: 25

- Breakeven after TP1: False

- Trailing SL after TP1: False

- Base Min ATR Filter: 0.001

- Use Volume Spike Filter: True

- BB Condition: Midline

- Use MACD Cross (false=Trend Filter): True

- Show Debug: True

For backtesting, use initial capital of 30 USD, base currency USDT, order size 100 USDT, pyramiding 1, commission 0.1%, slippage 0 ticks, long/short margin 0%.

Always backtest on your platform and use risk management—risk no more than 1-2% per trade. This is not financial advice; trade at your own risk.

WorldCup Dashboard + Institutional Sessions© 2025 NewMeta™ — Educational use only.

# Full, Premium Description

## WorldCup Dashboard + Institutional Sessions

**A trade-ready, intraday framework that combines market structure, real flow, and institutional timing.**

This toolkit fuses **Institutional Sessions** with a **price–volume decision engine** so you can see *who is active*, *where value sits*, and *whether the drive is real*. You get: **CVD/Delta**, volume-weighted **Momentum**, **Aggression** spikes, **FVG (MTF)** with nearest side, **Daily Volume Profile (VAH/POC/VAL)**, **ATR regime**, a **24h position gauge**, classic **candle patterns**, IBH/IBL + **first-hour “true close”** lines, and a **10-vote confluence scoreboard**—all in one view.

---

## What’s inside (and how to trade it)

### 🌍 Institutional Sessions (Sydney • Tokyo • London • New York)

* Session boxes + a highlighted **first hour**.

* Plots the **true close** (first-hour close) as a running line with a label.

**Use:** Many desks anchor risk to this print. Above = bullish bias; below = bearish. **IBH/IBL** breaks during London/NY carry the most signal.

### 📊 CVD / Delta (Flow)

* Net buyer vs seller pressure with smooth trend state.

**Use:** **Rising CVD + acceptance above mid/POC** confirms continuation. Bearish price + rising CVD = caution (possible absorption).

### ⚡ Volume-Weighted Momentum

* Momentum adjusted by participation quality (volume).

**Use:** Momentum>MA and >0 → trend drive is “real”; <0 and falling → distribution risk.

### 🔥 Aggression Detector

* ROC × normalized volume × wick factor to flag **forceful** candles.

**Use:** On spikes, avoid fading blindly—wait for pullbacks into **aligned FVG** or for aggression to cool.

### 🟦🟪 Fair Value Gaps (with MTF)

* Detects up to 3 recent FVGs and marks the **nearest** side to price.

**Use:** Trend pullbacks into **bullish FVG** for longs; bounces into **bearish FVG** for shorts. Optional threshold to filter weak gaps.

### 🧭 24h Gauge (positioning)

* Shows current price across the 24h low⇢high with a mid reference.

**Use:** Above mid and pushing upper third = momentum continuation setups; below mid = sell the rips bias.

### 🧱 Daily Volume Profile (manual per day)

* **VAH / POC / VAL** derived from discretized rows.

**Use:** **POC below** supports longs; **POC above** caps rallies. Fade VAH/VAL in ranges; treat them as break/hold levels in trends.

### 📈 ATR Regime

* **ATR vs ATR-avg** with direction and regime flag (**HIGH / NORMAL / LOW**).

**Use:** HIGH ⇒ give trades room & favor trend following. LOW ⇒ fade edges, scale targets.

### 🕯️ Candle Patterns (contextual, not standalone)

* Engulfings, Morning/Evening Star, 3 Soldiers/Crows, Harami, Hammer/Shooting Star, Double Top/Bottom.

**Use:** Only with session + flow + momentum alignment.

### 🤝 Price–Volume Classification

* Labels each bar as **continuation**, **exhaustion**, **distribution**, or **healthy pullback**.

**Use:** Align continuation reads with trend; treat “Price↑ + Vol↓” as a caution flag.

### 🧪 Confluence Scoreboard & B/S Meter

* Ten elements vote: 🔵 bull, ⚪ neutral, 🟣 bear.

**Use:** Execution filter—take setups when the board’s skew matches your trade direction.

---

## Playbooks (actionable)

**Trend Pullback (Long)**

1. London/NY active, Momentum↑, CVD↑, price above 24h mid & POC.

2. Pullback into **nearest bullish FVG**.

3. Invalidate under FVG low or **true-close** line.

4. Targets: IBH → VAH → 24h high.

**Range Fade (Short)**

1. Asia/quiet regime, **Price↑ + Vol↓** into **VAH**, ATR low.

2. Nearest FVG bearish or scoreboard skew bearish.

3. Invalidate above VAH/IBH.

4. Targets: POC → VAL.

**News/Impulse**

Aggression spike? Don’t chase. Let it pull back into the aligned FVG; require CVD/Momentum agreement before entry.

---

## Alerts (included)

* **Bull/Bear Confluence ≥ 7/10**

* **Intraday Target Achieved** / **Daily Target Achieved**

* **Session True-Close Retests** (Sydney/Tokyo/London/NY)

*(Keep alerts “Once per bar” unless you specifically want intrabar triggers.)*

---

## Setup Tips

* **UTC**: Choose the reference that matches how you track sessions (default UTC+2).

* **Volume threshold**: 2.0× is a strong baseline; raise for noisy alts, lower for majors.

* **CVD smoothing**: 14–24 for scalps; 24–34 for slower markets.

* **ATR lengths**: Keep defaults unless your asset has a persistent regime shift.

---

## Why this framework?

Because **timing (sessions)**, **truth (flow)**, and **location (value/FVG)** together beat any single signal. You get *who is trading*, *how strong the push is*, and *where risk lives*—on one screen—so execution is faster and cleaner.

---

**Disclaimer**: Educational use only. Not financial advice. Markets are risky—backtest and size responsibly.

Hyper SAR Reactor Trend StrategyHyperSAR Reactor Adaptive PSAR Strategy

Summary

Adaptive Parabolic SAR strategy for liquid stocks, ETFs, futures, and crypto across intraday to daily timeframes. It acts only when an adaptive trail flips and confirmation gates agree. Originality comes from a logistic boost of the SAR acceleration using drift versus ATR, plus ATR hysteresis, inertia on the trail, and a bear-only gate for shorts. Add to a clean chart and run on bar close for conservative alerts.

Scope and intent

• Markets: large cap equities and ETFs, index futures, major FX, liquid crypto

• Timeframes: one minute to daily

• Default demo: BTC on 60 minute

• Purpose: faster yet calmer PSAR that resists chop and improves short discipline

• Limits: this is a strategy that places simulated orders on standard candles

Originality and usefulness

• Novel fusion: PSAR AF is boosted by a logistic function of normalized drift, trail is monotone with inertia, entries use ATR buffers and optional cooldown, shorts are allowed only in a bear bias

• Addresses false flips in low volatility and weak downtrends

• All controls are exposed in Inputs for testability

• Yardstick: ATR normalizes drift so settings port across symbols

• Open source. No links. No solicitation

Method overview

Components

• Adaptive AF: base step plus boost factor times logistic strength

• Trail inertia: one sided blend that keeps the SAR monotone

• Flip hysteresis: price must clear SAR by a buffer times ATR

• Volatility gate: ATR over its mean must exceed a ratio

• Bear bias for shorts: price below EMA of length 91 with negative slope window 54

• Cooldown bars optional after any entry

• Visual SAR smoothing is cosmetic and does not drive orders

Fusion rule

Entry requires the internal flip plus all enabled gates. No weighted scores.

Signal rule

• Long when trend flips up and close is above SAR plus buffer times ATR and gates pass

• Short when trend flips down and close is below SAR minus buffer times ATR and gates pass

• Exit uses SAR as stop and optional ATR take profit per side

Inputs with guidance

Reactor Engine

• Start AF 0.02. Lower slows new trends. Higher reacts quicker

• Max AF 1. Typical 0.2 to 1. Caps acceleration

• Base step 0.04. Typical 0.01 to 0.08. Raises speed in trends

• Strength window 18. Typical 10 to 40. Drift estimation window

• ATR length 16. Typical 10 to 30. Volatility unit

• Strength gain 4.5. Typical 2 to 6. Steepness of logistic

• Strength center 0.45. Typical 0.3 to 0.8. Midpoint of logistic

• Boost factor 0.03. Typical 0.01 to 0.08. Adds to step when strength rises

• AF smoothing 0.50. Typical 0.2 to 0.7. Adds inertia to AF growth

• Trail smoothing 0.35. Typical 0.15 to 0.45. Adds inertia to the trail

• Allow Long, Allow Short toggles

Trade Filters

• Flip confirm buffer ATR 0.50. Typical 0.2 to 0.8. Raise to cut flips

• Cooldown bars after entry 0. Typical 0 to 8. Blocks re entry for N bars

• Vol gate length 30 and Vol gate ratio 1. Raise ratio to trade only in active regimes

• Gate shorts by bear regime ON. Bear bias window 54 and Bias MA length 91 tune strictness

Risk

• TP long ATR 1.0. Set to zero to disable

• TP short ATR 0.0. Set to 0.8 to 1.2 for quicker shorts

Usage recipes

Intraday trend focus

Confirm buffer 0.35 to 0.5. Cooldown 2 to 4. Vol gate ratio 1.1. Shorts gated by bear regime.

Intraday mean reversion focus

Confirm buffer 0.6 to 0.8. Cooldown 4 to 6. Lower boost factor. Leave shorts gated.

Swing continuation

Strength window 24 to 34. ATR length 20 to 30. Confirm buffer 0.4 to 0.6. Use daily or four hour charts.

Properties visible in this publication

Initial capital 10000. Base currency USD. Order size Percent of equity 3. Pyramiding 0. Commission 0.05 percent. Slippage 5 ticks. Process orders on close OFF. Bar magnifier OFF. Recalculate after order filled OFF. Calc on every tick OFF. No security calls.

Realism and responsible publication

No performance claims. Past results never guarantee future outcomes. Shapes can move while a bar forms and settle on close. Strategies execute only on standard candles.

Honest limitations and failure modes

High impact events and thin books can void assumptions. Gap heavy symbols may prefer longer ATR. Very quiet regimes can reduce contrast and invite false flips.

Open source reuse and credits

Public domain building blocks used: PSAR concept and ATR. Implementation and fusion are original. No borrowed code from other authors.

Strategy notice

Orders are simulated on standard candles. No lookahead.

Entries and exits

Long: flip up plus ATR buffer and all gates true

Short: flip down plus ATR buffer and gates true with bear bias when enabled

Exit: SAR stop per side, optional ATR take profit, optional cooldown after entry

Tie handling: stop first if both stop and target could fill in one bar

Previous TPOIndicator Summary

This Pine Script indicator, "Previous TPO," is designed to calculate and display five key price levels from the previous trading day's market activity. It uses a 30-minute TPO (Time Price Opportunity) profile, which is a method of organizing price by time to find areas of high and low activity.

The five levels it plots on the current day are:

1. Previous Value Area High (VAH)

2. Previous Value Area Low (VAL)

3. Previous Point of Control (POC)

4. Previous Initial Balance High (IBH)

5. Previous Initial Balance Low (IBL)

The script is built to be efficient, running its main calculation only once at the beginning of each new day. It also includes an automatic line management system to delete old lines, preventing the "Too many lines" error and keeping the chart clean.

How the Code Works

1. Data Collection: At the start of a new day (00:00), the script looks back at the chart's history. It uses request.security to access 30-minute bar data.

2. Collector Loop: It then loops backward, bar by bar, to find and store 48 unique 30-minute High/Low data points, which represents the full 24-hour range of the previous day.

3. TPO Profile: With this 30-minute data, it builds a TPO profile. It divides the previous day's price range into small bins (price levels) and counts how many 30-minute periods "touched" each price bin.

4. Level Calculation:

o POC: It finds the price bin with the highest TPO count (the most traded price) and sets it as the Point of Control.

o VAH/VAL: It starts at the POC and expands outward, adding the next-most-traded price bins until 70% (or the user-defined percentage) of the day's TPOs are included. The highest and lowest prices of this range are the Value Area High and Value Area Low.

o IBH/IBL: It identifies the high and low of the first hour (the first two 30-minute bars) of the previous day to set the Initial Balance High and Initial Balance Low.

5. Drawing: The script draws these five levels as horizontal lines across the current trading day, providing a constant reference.

6. Line Management: It keeps track of all lines in an array. When the total number of lines exceeds the user's limit (e.g., 50 days * 5 lines = 250), it automatically deletes the oldest lines from the chart.

Usefulness for Trading

This indicator provides a powerful framework for intraday traders by contextualizing the current day's price action against the previous day's "auction."

• Key Support/Resistance: The VAH, VAL, and POC act as significant support and resistance lev-els. Price reacting at these levels can signal mean reversion, while acceptance beyond them can signal a trend or expansion day.

• Value Area as Context: Trading inside the previous day's value area (between VAH and VAL) is often seen as "balanced" or "range-bound" trading. Trading outside of it is "unbalanced" or "trending."

• POC as a "Magnet": The POC, being the area of highest volume/time, often acts as a "magnet" or "center of gravity" for price.

• Opening Range: The Initial Balance (IB) levels show the opening range. A breakout from this range is often a key signal for the day's initial direction.

• 80% Rule: The script contains (currently commented-out) setup logic for the "80% Rule." This is a specific Market Profile strategy where:

1. The market opens inside the previous day's Value Area.

2. The Initial Balance fails to extend outside the VA (e.g., in a short setup, the IB high stays below the VAH).

3. This setup suggests an 80% probability that the price will rotate and test the other side of the Value Area (e.g., test the VAL).

Publication and restrictions

This script is published under the Mozilla Public Licence 2.0 (MPL 2.0) and is therefore suitable for publi-cation as an open source indicator on TradingView.

Timeframe limitation: The indicator is designed for intraday timeframes. Timeframes below 10 minutes do not work and lead to an error. Recommended time frame 30 minutes.

It will not work correctly on:

Time frame under 10 minutes: The data collection loop (max_bars_to_check = 3000) is not large enough to collect the bars required for a full day on a 5-minute chart or smaller.

High time frames (e.g. 1H, 4H, Daily): The script's logic is based on a chart timeframe 30-minute data that it requests. If higher time frames are selected, the script works but the zones are no longer correct or become irrelevant.

Aurum DCX AVE Gold and Silver StrategySummary in one paragraph

Aurum DCX AVE is a volatility break strategy for gold and silver on intraday and swing timeframes. It aligns a new Directional Convexity Index with an Adaptive Volatility Envelope and an optional USD/DXY bias so trades appear only when direction quality and expansion agree. It is original because it fuses three pieces rarely combined in one model for metals: a convexity aware trend strength score, a percentile based envelope that widens with regime heat, and an intermarket DXY filter.

Scope and intent

• Markets. Gold and silver futures or spot, other liquid commodities, major indices

• Timeframes. Five minutes to one day. Defaults to 30min for swing pace

• Default demo used in this publication. TVC:GOLD on 30m

• Purpose. Enter confirmed volatility breaks while muting chop using regime heat and USD bias

• Limits. This is a strategy. Orders are simulated on standard candles only

Originality and usefulness

• Unique fusion. DCX combines DI strength with path efficiency and curvature. AVE blends ATR with a high TR percentile and widens with DCX heat. DXY adds an intermarket bias

• Failure mode addressed. False starts inside compression and unconfirmed breakouts during USD swings

• Testability. Each component has a named input. Entry names L and S are visible in the list of trades

• Portable yardstick. Weekly ATR for stops and R multiples for targets

• Open source. Method and implementation are disclosed for community review

Method overview in plain language

You score direction quality with DCX, size an adaptive envelope with a blend of ATR and a high TR percentile, and only allow breaks that clear the band while DCX is above a heat threshold in the same direction. An optional DXY filter favors long when USD weakens and short when USD strengthens. Orders are bracketed with a Weekly ATR stop and an R multiple target, with optional trailing to the envelope.

Base measures

• Range basis. True Range and ATR over user windows. A high TR percentile captures expansion tails used by AVE

• Return basis. Not required

Components

• Directional Convexity Index DCX. Measures directional strength with DX, multiplies by path efficiency, blends a curvature term from acceleration, scales to 0 to 100, and uses a rise window

• Adaptive Volatility Envelope AVE. Midline ALMA or HMA or EMA plus bands sized by a blend of ATR and a high TR percentile. The blend weight follows volatility of volatility. Band width widens with DCX heat

• DXY Bias optional. Daily EMA trend of DXY. Long bias when USD weakens. Short bias when USD strengthens

• Risk block. Initial stop equals Weekly ATR times a multiplier. Target equals an R multiple of the initial risk. Optional trailing to AVE band

Fusion rule

• All gates must pass. DCX above threshold and rising. Directional lead agrees. Price breaks the AVE band in the same direction. DXY bias agrees when enabled

Signal rule

• Long. Close above AVE upper and DCX above threshold and DCX rising and plus DI leads and DXY bias is bearish

• Short. Close below AVE lower and DCX above threshold and DCX falling and minus DI leads and DXY bias is bullish

• Exit and flip. Bracket exit at stop or target. Optional trailing to AVE band

Inputs with guidance

Setup

• Symbol. Default TVC:GOLD (Correlation Asset for internal logic)

• Signal timeframe. Blank follows the chart

• Confirm timeframe. Default 1 day used by the bias block

Directional Convexity Index

• DCX window. Typical 10 to 21. Higher filters more. Lower reacts earlier

• DCX rise bars. Typical 3 to 6. Higher demands continuation

• DCX entry threshold. Typical 15 to 35. Higher avoids soft moves

• Efficiency floor. Typical 0.02 to 0.06. Stability in quiet tape

• Convexity weight 0..1. Typical 0.25 to 0.50. Higher gives curvature more influence

Adaptive Volatility Envelope

• AVE window. Typical 24 to 48. Higher smooths more

• Midline type. ALMA or HMA or EMA per preference

• TR percentile 0..100. Typical 75 to 90. Higher favors only strong expansions

• Vol of vol reference. Typical 0.05 to 0.30. Controls how much the percentile term weighs against ATR

• Base envelope mult. Typical 1.4 to 2.2. Width of bands

• Regime adapt 0..1. Typical 0.6 to 0.95. How much DCX heat widens or narrows the bands

Intermarket Bias

• Use DXY bias. Default ON

• DXY timeframe. Default 1 day

• DXY trend window. Typical 10 to 50

Risk

• Risk percent per trade. Reporting field. Keep live risk near one to two percent

• Weekly ATR. Default 14. Basis for stops

• Stop ATR weekly mult. Typical 1.5 to 3.0

• Take profit R multiple. Typical 1.5 to 3.0

• Trail with AVE band. Optional. OFF by default

Properties visible in this publication

• Initial capital. 20000

• Base currency. USD

• request.security lookahead off everywhere

• Commission. 0.03 percent

• Slippage. 5 ticks

• Default order size method percent of equity with value 3% of the total capital available

• Pyramiding 0

• Process orders on close ON

• Bar magnifier ON

• Recalculate after order is filled OFF

• Calc on every tick OFF

Realism and responsible publication

• No performance claims. Past results never guarantee future outcomes

• Shapes can move while a bar forms and settle on close

• Strategies use standard candles for signals and orders only

Honest limitations and failure modes

• Economic releases and thin liquidity can break assumptions behind the expansion logic

• Gap heavy symbols may prefer a longer ATR window

• Very quiet regimes can reduce signal contrast. Consider higher DCX thresholds or wider bands

• Session time follows the exchange of the chart and can change symbol to symbol

• Symbol sensitivity is expected. Use the gates and length inputs to find stable settings

Open source reuse and credits

• None

Mode

Public open source. Source is visible and free to reuse within TradingView House Rules

Legal

Education and research only. Not investment advice. You are responsible for your decisions. Test on historical data and in simulation before any live use. Use realistic costs.

Realtime RenkoI've been working on real-time renko for a while as a coding challenge. The interesting problem here is building renko bricks that form based on incoming tick data rather than waiting for bar closes. Every tick that comes through gets processed immediately, and when price moves enough to complete a brick, that brick closes and a new one opens right then. It's just neat because you can run it and it updates as you'd expect with renko, forming bricks based purely on price movement happening in real time rather than waiting for arbitrary time intervals to pass.

The three brick sizing methods give you flexibility in how you define "enough movement" to form a new brick. Traditional renko uses a fixed price range, so if you set it to 10 ticks, every brick represents exactly 10 ticks of movement. This works well for instruments with stable tick sizes and predictable volatility. ATR-based sizing calculates the average true range once at startup using a weighted average across all historical bars, then divides that by your brick value input. If you want bricks that are one full ATR in size, you'd use a brick value of 1. If you want half-ATR bricks, use 2. This inverted relationship exists because the calculation is ATR divided by your input, which lets you work with multiples and fractions intuitively. Percentage-based sizing makes each brick a fixed percentage move from the previous brick's close, which automatically scales with price level and works well for instruments that move proportionally rather than in absolute tick increments.

The best part about this implementation is how it uses varip for state management. When you first load the indicator, there's no history at all. Everything starts fresh from the moment you add it to your chart because varip variables only exist in real-time. This means you're watching actual renko bricks form from real tick data as it arrives. The indicator builds its own internal history as it runs, storing up to 250 completed bricks in memory, but that history only exists for the current session. Refresh the page or reload the indicator and it starts over from scratch.

The visual implementation uses boxes for brick bodies and lines for wicks, drawn at offset bar indices to create the appearance of a continuous renko chart in the indicator pane. Each brick occupies two bar index positions horizontally, which spaces them out and makes the chart readable. The current brick updates in real time as new ticks arrive, with its high, low, and close values adjusting continuously until it reaches the threshold to close and become finalized. Once a brick closes, it gets pushed into the history array and a new brick opens at the closing level of the previous one.

What makes this especially useful for debugging and analysis are the hover tooltips on each brick. Clicking on any brick brings up information showing when it opened with millisecond precision, how long it took to form from open to close, its internal bar index within the renko sequence, and the brick size being used. That time delta measurement is particularly valuable because it reveals the pace of price movement. A brick that forms in five seconds indicates very different market conditions than one that takes three minutes, even though both bricks represent the same amount of price movement. You can spot acceleration and deceleration in trend development by watching how quickly consecutive bricks form.

The pine logs that generate when bricks close serve as breadcrumbs back to the main chart. Every time a brick finalizes, the indicator writes a log entry with the same information shown in the tooltip. You can click that log entry and TradingView jumps your main chart to the exact timestamp when that brick closed. This lets you correlate renko brick formation with what was happening on the time-based chart, which is critical for understanding context. A brick that closed during a major news announcement or at a key support level tells a different story than one that closed during quiet drift, and the logs make it trivial to investigate those situations.

The internal bar indexing system maintains a separate count from the chart's bar_index, giving each renko brick its own sequential number starting from when the indicator begins running. This makes it easy to reference specific bricks in your analysis or when discussing patterns with others. The internal index increments only when a brick closes, so it's a pure measure of how many bricks have formed regardless of how much chart time has passed. You can match these indices between the visual bricks and the log entries, which helps when you're trying to track down the details of a specific brick that caught your attention.

Brick overshoot handling ensures that when price blows through the threshold level instead of just barely touching it, the brick closes at the threshold and the excess movement carries over to the next brick. This prevents gaps in the renko sequence and maintains the integrity of the brick sizing. If price shoots up through your bullish threshold and keeps going, the current brick closes at exactly the threshold level and the new brick opens there with the overshoot already baked into its initial high. Without this logic, you'd get renko bricks with irregular sizes whenever price moved aggressively, which would undermine the whole point of using fixed-range bricks.

The timezone setting lets you adjust timestamps to your local time or whatever reference you prefer, which matters when you're analyzing logs or comparing brick formation times across different sessions. The time delta formatter converts raw milliseconds into human-readable strings showing days, hours, minutes, and seconds with fractional precision. This makes it immediately clear whether a brick took 12.3 seconds or 2 minutes and 15 seconds to form, without having to parse millisecond values mentally.

This is the script version that will eventually be integrated into my real-time candles library. The library version had an issue with tooltips not displaying correctly, which this implementation fixes by using a different approach to label creation and positioning. Running it as a standalone indicator also gives you more control over the visual settings and makes it easier to experiment with different brick sizing methods without affecting other tools that might be using the library version.

What this really demonstrates is that real-time indicators in Pine Script require thinking about state management and tick processing differently than historical indicators. Most indicator code assumes bars are immutable once closed, so you can reference `close ` and know that value will never change. Real-time renko throws that assumption out because the current brick is constantly mutating with every tick until it closes. Using varip for state variables and carefully tracking what belongs to finalized bricks versus the developing brick makes it possible to maintain consistency while still updating smoothly in real-time. The fact that there's no historical reconstruction and everything starts fresh when you load it is actually a feature, not a limitation, because you're seeing genuine real-time brick formation rather than some approximation of what might have happened in the past.

HTF Candles with PVSRA Volume Coloring (PCS Series)This indicator displays higher timeframe (HTF) candles using a PVSRA-inspired color model that blends price and volume strength, allowing traders to visualize higher-timeframe activity directly on lower-timeframe charts without switching screens.

OVERVIEW

This script visualizes higher-timeframe (HTF) candles directly on lower-timeframe charts using a custom PVSRA (Price, Volume & Support/Resistance Analysis) color model.

Unlike standard HTF indicators, it aggregates real-time OHLC and volume data bar-by-bar and dynamically draws synthetic HTF candles that update as the higher-timeframe bar evolves.

This allows traders to interpret momentum, trend continuation, and volume pressure from broader market structures without switching charts.

INTEGRATION LOGIC

This script merges higher-timeframe candle projection with PVSRA volume analysis to provide a single, multi-timeframe momentum view.

The HTF structure reveals directional context, while PVSRA coloring exposes the underlying strength of buying and selling pressure.

By combining both, traders can see when a higher-timeframe candle is building with strong or weak volume, enabling more informed intraday decisions than either tool could offer alone.

HOW IT WORKS

Aggregates price data : Groups lower-timeframe bars to calculate higher-timeframe Open, High, Low, Close, and total Volume.

Applies PVSRA logic : Compares each HTF candle’s volume to the average of the last 10 bars:

• >200% of average = strong activity

• >150% of average = moderate activity

• ≤150% = normal activity

Assigns colors :

• Green/Blue = bullish high-volume

• Red/Fuchsia = bearish high-volume

• White/Gray = neutral or low-volume moves

Draws dynamic outlines : Outlines update live while the current HTF candle is forming.

Supports symbol override : Calculations can use another instrument for correlation analysis.

This multi-timeframe aggregation avoids repainting issues in request.security() and ensures accurate real-time HTF representation.

FEATURES

Dual HTF Display : Visualize two higher timeframes simultaneously (e.g., 4H and 1D).

Dynamic PVSRA Coloring : Volume-weighted candle colors reveal bullish or bearish dominance.

Customizable Layout : Adjust candle width, spacing, offset, and color schemes.

Candle Outlines : Highlight the forming HTF candle to monitor developing structure.

Symbol Override : Display HTF candles from another instrument for cross-analysis.

SETTINGS

HTF 1 & HTF 2 : enable/disable, set timeframes, choose label colors, show/hide outlines.

Number of Candles : choose how many HTF candles to plot (1–10).

Offset Position : distance to the right of the current price where HTF candles begin.

Spacing & Width : adjust separation and scaling of candle groups.

Show Wicks/Borders : toggle wick and border visibility.

PVSRA Colors : enable or disable volume-based coloring.

Symbol Override : use a secondary ticker for HTF data if desired.

USAGE TIPS

Set the indicator’s visual order to “Bring to front.”

Always choose HTFs higher than your active chart timeframe.

Use PVSRA colors to identify strong momentum and potential reversals.

Adjust candle spacing and width for your chart layout.

Outlines are not shown on chart timeframes below 5 minutes.

TRADING STRATEGY

Strategy Overview : Combine HTF structure and PVSRA volume signals to

• Identify zones of high institutional activity and potential reversals.

• Wait for confirmation through consolidation or a pullback to key levels.

• Trade in alignment with dominant higher-timeframe structure rather than chasing volatility.

Setup :

• Chart timeframe: lower (5m, 15m, 1H)

• HTF 1: 4H or 1D

• HTF 2: 1D or 1W

• PVSRA Colors: enabled

• Outlines: enabled

Entry Concept :

High-volume candles (green or red) often indicate market-maker activity , such zones often reflect liquidity absorption by larger players and are not necessarily ideal entry points.

Wait for the next consolidation or pullback toward a support or resistance level before acting.

Bullish scenario :

• After a high-volume or rejection candle near a low, price consolidates and forms a higher low.

• Enter long only when structure confirms strength above support.

Bearish scenario :

• After a high-volume or rejection candle near a top, price consolidates and forms a lower high.

• Enter short once resistance holds and momentum weakens.

Exit Guidelines :

• Exit when next HTF candle shifts in color or momentum fades.

• Exit if price structure breaks opposite to your trade direction.

• Always use stop-loss and take-profit levels.

Additional Tips :

• Never enter directly on strong green/red high-volume candles, these are usually areas of institutional absorption.

• Wait for market structure confirmation and volume normalization.

• Combine with RSI, moving averages, or support/resistance for timing.

• Avoid trading when HTF candles are mixed or low-volume (unclear bias).

• Outlines hidden below 5m charts.

Risk Management :

• Use stop-loss and take-profit on all positions.

• Limit risk to 1–2% per trade.

• Adjust position size for volatility.

FINAL NOTES

This script helps traders synchronize lower-timeframe execution with higher-timeframe momentum and volume dynamics.

Test it on demo before live use, and adjust settings to fit your trading style.

DISCLAIMER

This script is for educational purposes only and does not constitute financial advice.

SUPPORT & UPDATES

Future improvements may include alert conditions and additional visualization modes. Feedback is welcome in the comments section.

CREDITS & LICENSE

Created by @seoco — open source for community learning.

Licensed under Mozilla Public License 2.0 .

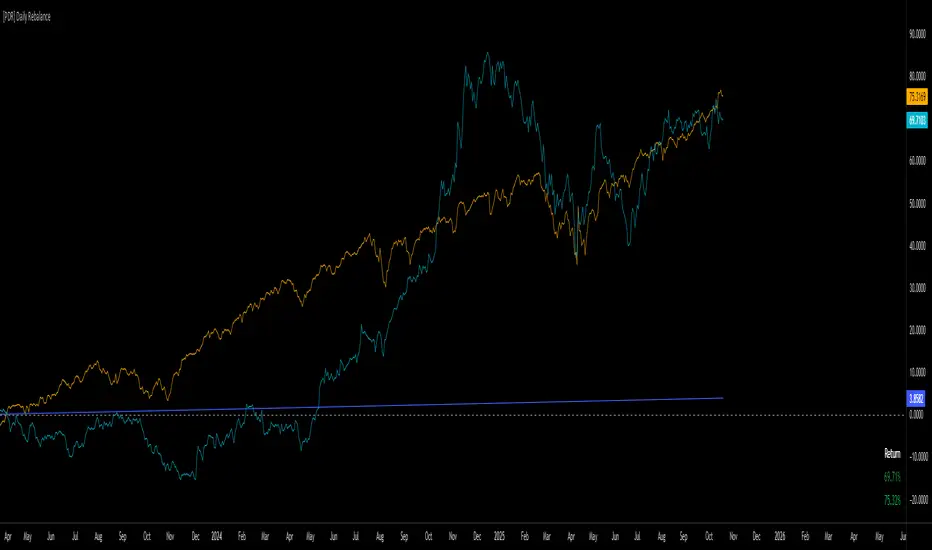

[PDR] Daily Rebalance█ OVERVIEW

This indicator is a powerful portfolio backtesting tool designed to simulate the performance of a static-weight, daily rebalancing strategy. It allows you to define a portfolio of up to 10 assets, set their target weights, and track its cumulative return against a user-defined benchmark and a risk-free rate.

The core of the script is its daily rebalancing logic, which calculates and logs every trade needed to bring the portfolio back to its target allocations at the close of each day. This provides a transparent and detailed view of how a static portfolio would have performed historically, including the impact of trading costs.

█ KEY FEATURES

Daily Rebalancing: Simulates a portfolio that is rebalanced at the close of every day to maintain target asset allocations.

Customizable Portfolio: Configure up to 10 different assets with specific weights. If all weights are left at 0, the script automatically creates an equal-weight portfolio from the selected assets.

Performance Comparison: Plots the portfolio's equity curve against a user-defined benchmark (e.g., SET:SET50 ) and a risk-free return, allowing for easy relative performance analysis.

Realistic Simulation: Accounts for trading costs like broker commission and minimum lot sizes for more accurate and grounded backtesting results.

Detailed Performance Metrics: An on-chart table displays real-time statistics, including Current Drawdown, Max Drawdown, and Total Return for both your portfolio and the benchmark.

Trade-by-Trade Logs: For full transparency, every rebalancing trade (BUY/SELL), including shares, price, notional value, and fees, is logged in the Pine Logs panel.

█ HOW TO USE

**Apply to a Daily Chart:** This script is designed to work exclusively on the daily ( 1D ) timeframe. Applying it to any other timeframe will result in a runtime error.

**Configure Settings:** Open the indicator's settings. Set your `Initial Capital`, `Start Time`, and the `Benchmark` symbol you wish to compare against.

**Define Your Assets:** In the 'Assets' group, check the box to enable each asset you want to include, select the symbol, and define its target `Weight (%)`.

**Set Trading Costs:** Adjust the `Broker Commission (%)` and `Minimal Buyable Lot` to match your expected trading conditions.

**Analyze the Results:** The performance curves are plotted in the indicator pane below your main chart. The key metrics table is displayed on the bottom-right of your chart.

**View Rebalancing Trades:** This is a crucial step for understanding the simulation. To see the detailed daily trades, you **must** open the **Pine Logs**. You can find this panel at the bottom of your TradingView window, next to the "Pine Editor" and "Strategy Tester" tabs. The logs provide a complete breakdown of every rebalancing action.

█ DISCLAIMER

This is a backtesting and simulation tool, not a trading signal generator. Its purpose is for research and performance analysis. Past performance is not indicative of future results. Always conduct your own research before making any investment decisions.

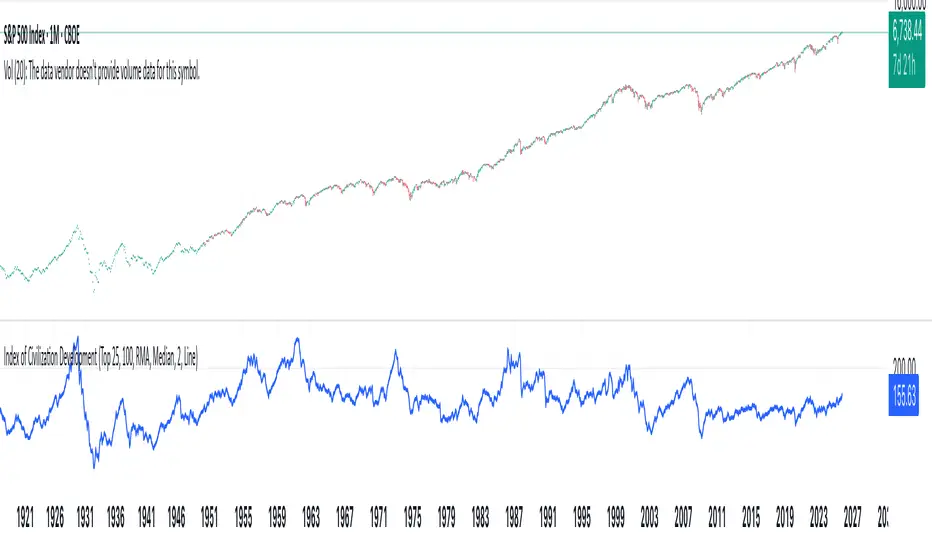

Index of Civilization DevelopmentIndex of Civilization Development Indicator

This Pine Script (version 6) creates a custom technical indicator for TradingView, titled Index of Civilization Development. It generates a composite index by averaging normalized stock market performances from a selection of global country indices. The normalization is relative to each index's 100-period simple moving average (SMA), scaled to a percentage (100% baseline). This allows for a comparable "development" or performance metric across diverse markets, potentially highlighting trends in global economic or "civilizational" progress based on equity markets.The indicator plots as a single line in a separate pane (non-overlay) and is designed to handle up to 40 symbols to respect TradingView's request.security() call limits.Key FeaturesComposite Index Calculation: Fetches the previous bar's close (close ) and its 100-period SMA for each selected symbol.

Normalizes each: (close / SMA(100)) * 100.

Averages the valid normalizations (ignores invalid/NA data) to produce a single "Index (%)" value.

Symbol Selection Modes:Top N Countries: Selects from a predefined list of the top 50 global stock indices (by market cap/importance, e.g., SPX for USA, SHCOMP for China). Options: Top 5, 15, 25, or 50.

Democratic Countries: ~38 symbols from democracies (e.g., SPX, NI225, NIFTY; based on democracy indices ≥6/10, including flawed/parliamentary systems).

Dictatorships: ~12 symbols from authoritarian/hybrid regimes (e.g., SHCOMP, TASI, IMOEX; scores <6/10).

Customization:Line color (default: blue).

Line width (1-5, default: 2).

Line style: Solid line (default), Stepline, or Circles.

Data Handling:Uses request.security() with lookahead enabled for real-time accuracy, gaps off, and invalid symbol ignoring.

Runs calculations on every bar, with max_bars_back=2000 for historical depth.

Arrays are populated only on the first bar (barstate.isfirst) for efficiency.

Predefined Symbol Lists (Examples)Top 50: SPX (USA), SHCOMP (China), NI225 (Japan), ..., BAX (Bahrain).

Democratic: Focuses on free-market democracies like USA, Japan, UK, Canada, EU nations, Australia, etc.

Dictatorships: Authoritarian markets like China, Saudi Arabia, Russia, Turkey, etc.

Usage TipsAdd to any chart (e.g., daily/weekly timeframe) to view the composite line.

Ideal for macro analysis: Compare democratic vs. authoritarian performance, or track "top world" equity health.

Potential Limitations: Relies on TradingView's symbol availability; some exotic indices (e.g., KWSEIDX) may fail if not supported. The 40-symbol cap prevents errors.

Interpretation: Values >100 indicate above-trend performance; <100 suggest underperformance relative to recent averages.

This script blends financial data with geopolitical categorization for a unique "civilization index" perspective on global markets. For modifications, ensure symbol tickers match TradingView's format.

ICT First Presented FVG with Volume Imbalance [1st P. FVG + VI]The indicator identifies and highlights the first presented Fair Value Gap (FVG) occurringthe morning (09:30–10:00) and afternoon (13:30–14:00) session's first 30 minutes. It includes an optional feature to extend FVG zones when a volume imbalance (V.I.) is detected, providing additional context for areas of potential price inefficiency. This powerful combination helps traders identify significant market structure gaps that often act as support/resistance zones and potential price targets.

What is an FVG?

A Fair Value Gap, often abbreviated as FVG, is a price range on a chart where there is an inefficiency or imbalance in trading. This typically happens when price moves rapidly in one direction, leaving a gap between the wicks or bodies of three consecutive candles. For example, in a bullish move, if the low of the third candle is higher than the high of the first candle, the space between them is the FVG.

What is a Volume Imbalance?

A volume imbalance is a smaller, more precise inefficiency within price action, often visible as a "crack" or thin area in the price delivery. It represents a spot where the volume traded was not balanced between buyers and sellers, often seen as a thin wick or a gap between candle bodies.

FVG + Volume Imbalance:

When you have a fair value gap that contains a volume imbalance, it becomes a more significant area of interest. ICT teaches that you should not ignore a volume imbalance if it’s part of an FVG. In fact, you should use the volume imbalance in conjunction with the FVG to define your trading range more accurately

📊 Volume Imbalance Integration

Toggle Option: Enable/disable volume imbalance detection based on preference

Extended Boundaries: When enabled, FVG boundaries expand to include volume imbalance zones

Accurate Gap Sizing: Total gap calculation includes volume imbalance extensions

Multi-Scenario Support: Handles volume imbalances at start, end, or both sides of FVG formations

📈 Multiple Display Modes

Current Day: Shows only today's FVGs for clean chart analysis

Current Week: Displays all weekly FVGs for broader context

Forward Extension: Extends FVG boxes and CE, Upper/Lower Quadrant lines into the future

📊 Visualization

Bullish FVGs appear in semi-transparent blue or purple zones (depending on session).

Bearish FVGs appear in red or orange zones.

Optional dotted lines mark the CE (midpoint) of each FVG for additional reference.

Quadrant Division: Additional 25%/75% lines for large FVGs (configurable minimum gap size)

🎯 Smart Filtering

First Presentation Only: Only displays the initial FVG in each session, avoiding clutter

Minimum Gap Size: Configurable tick-based thresholds for AM and PM sessions

Core FVG Validation: Ensures only valid Fair Value Gaps are displayed

⚙️ Configuration Options

Display Settings

Show Mode: Current Day or Current Week view

Forward Extension: 1-500 bars projection

Day Labels: Toggle weekday labels in weekly mode

Text Color: Customizable label colors

Volume Imbalance Settings

Include Volume Imbalance: Master toggle for enhanced boundary calculation

Automatic Detection: Identifies imbalance scenarios without additional input

Session-Specific Settings

AM Session (09:30-10:00):

Enable/disable AM FVG detection

Customizable bullish/bearish colors

CE line visibility and coloring

Minimum gap size in ticks

PM Session (13:30-14:00):

Enable/disable PM FVG detection

Customizable bullish/bearish colors

CE line visibility and coloring

Minimum gap size in ticks

Quadrant Settings

Enable/Disable: Toggle quadrant line display

Minimum Gap: Tick threshold for quadrant activation

Line Style: Dotted, dashed, or solid

Color: Customizable quadrant line color

How It Works

FVG Boundary Calculation

Traditional FVG: High to Low (bullish) or Low to High (bearish)

Enhanced FVG: Extended boundaries to include volume imbalance zones when enabled

Total Gap Size: Calculated including any volume imbalance extensions

Volume Imbalance Detection

The indicator identifies volume imbalances by detecting bars where:

Bullish Imbalance: Current bar's body is completely above previous bar's body

Bearish Imbalance: Current bar's body is completely below previous bar's body

⚠️ Disclaimer

This script is a technical visualization tool only.

It does not provide financial advice, signals, or predictions. Always perform independent analysis and manage risk appropriately before making trading decisions.

多周期趋势动量面板加强版(Multi-Timeframe Trend Momentum Panel - User Guide)多周期趋势动量面板(Multi-Timeframe Trend Momentum Panel - User Guide)(english explanation follows.)

📖 指标功能详解 (精简版):

🎯 核心功能:

1. 多周期趋势分析 同时监控8个时间周期(1m/5m/15m/1H/4H/D/W/M)

2. 4维度投票系统 MA趋势+RSI动量+MACD+布林带综合判断

3. 全球交易时段 可视化亚洲/伦敦/纽约交易时间

4. 趋势强度评分 0100%量化市场力量

5. 智能警报 强势多空信号自动推送

________________________________________

📚 重要名词解释:

🔵 趋势状态 (MA均线分析):

名词 含义 信号强度

强势多头 快MA远高于慢MA(差值≥0.35%) ⭐⭐⭐⭐⭐ 做多

多头倾向 快MA略高于慢MA(差值<0.35%) ⭐⭐⭐ 谨慎做多

震荡 快慢MA缠绕,无明确方向 ⚠️ 观望

空头倾向 快MA略低于慢MA ⭐⭐⭐ 谨慎做空

强势空头 快MA远低于慢MA ⭐⭐⭐⭐⭐ 做空

简单理解: 快MA就像短跑运动员(反应快),慢MA是长跑运动员(稳定)。短跑远超长跑=强势多头,反之=强势空头。

________________________________________

🟠 动量状态 (RSI力度分析):

名词 含义 操作建议

动量上攻↗ RSI>60且快速上升 强烈买入信号

动量高位 RSI>60但上升变慢 警惕回调,可减仓

动量中性 RSI在4060之间,平稳 等待方向明确

动量低位 RSI<40但下跌变慢 警惕反弹,可止盈

动量下压↘ RSI<40且快速下降 强烈卖出信号

简单理解: RSI就像汽车速度表。"动量上攻"=油门踩到底加速,"动量高位"=已经很快但不再加速了。

________________________________________

🟣 辅助信号:

MACD:

• MACD多头 = 柱状图>0 = 买方力量强

• MACD空头 = 柱状图<0 = 卖方力量强

布林带(BB):

• BB超买 = 价格在布林带上轨附近 = 可能回调

• BB超卖 = 价格在布林带下轨附近 = 可能反弹

• BB中轨 = 价格在中间位置 = 平衡状态

________________________________________

💡 快速上手 3步看懂面板:

第1步: 看"综合结论标签" (K线上方)

• 绿色"多头占优" → 可以做多

• 红色"空头占优" → 可以做空

• 橙色"震荡/均衡" → 观望

第2步: 看"票数 多/空" (面板最下方)

• 多头票数远大于空头 (差距>2) → 趋势强

• 票数接近 (差距<1) → 震荡市

第3步: 看"趋势强度" (综合标签中)

• 强度>70% → 强势趋势,可重仓

• 强度5070% → 中等趋势,正常仓位

• 强度<50% → 弱势,轻仓或观望

________________________________________

🎨 时段背景色含义:

• 紫色背景 = 亚洲时段 (东京交易时间) 波动较小

• 橙色背景 = 伦敦时段 (欧洲交易时间) 波动增大

• 蓝色背景 = 纽约凌晨 美盘准备阶段

• 红色背景 = 纽约关键5分钟 (09:3009:35) ⚠️ 最重要! 市场最活跃,趋势易形成

• 绿色背景 = 纽约上午后段 延续早盘趋势

交易建议: 重点关注红色关键时段,这5分钟往往决定全天方向!

________________________________________

⚙️ 三大市场推荐设置

🥇 黄金: Hull MA 12/EMA 34, 阈值0.250.35%

₿ 比特币: EMA 21/EMA 55, 阈值0.801.20%

💎 以太坊: TEMA 21/EMA 55, 阈值0.600.80%

参数优化建议

黄金 (XAUUSD)

快速MA: Hull MA 12 (超灵敏捕捉黄金快速波动)

慢速MA: EMA 34 (斐波那契数列)

RSI周期: 9 (加快反应)

强趋势阈值: 0.25%