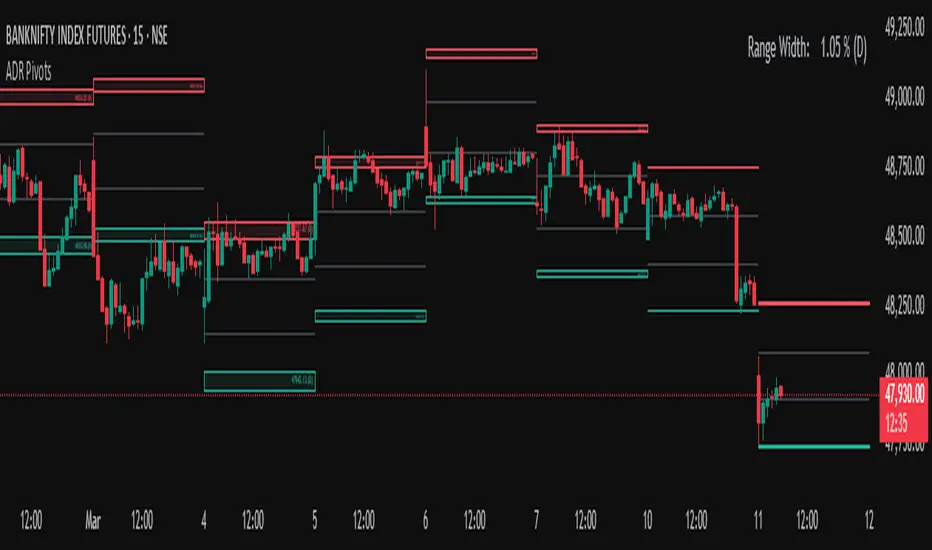

Average Daily Range (ADR) (Multi Timeframe, Multi Period)Average Daily Range (ADR)

(Multi Timeframe, Multi Period, Extended Levels)

Tips

• Narrow Zones are an indication of breakouts. It can be a very tight range as well.

• Wider Zones can be Sideways or Volatile.

What is this Indicator?

• This is Average Daily Range (ADR) Zones or Pivots.

• This have Multi Timeframe, Multi Period (Up to 3 Levels) and Extended Target Levels.

Advantages of this Indicator

• This is a Leading indicator, not Dynamic or Repaint.

• Helps to identify the reversal points.

• The levels are more accurate and not like the old formulas.

• Can practically follow the Buy Low and Sell High principle.

• Helps to keep minimum Stop Loss.

Who to use?

• Highly beneficial for Day Traders

• It can be used for Swing and Positions as well.

What timeframe to use?

• Any timeframe.

When to use?

• Any market conditions.

How to use?

Entry

• Long entry when the Price reach at or closer to the Green Support zone.

• Long entry when the Price retrace to the Red Resistance zone.

• Short entry when the Price reach at or closer to the Red Resistance zone.

• Short entry when the Price retrace to the Green Support zone.

• Long or Short at the Pivot line.

Exit

• Use past ADR levels as targets.

• Or use the Target levels in the indicator for breakouts.

• Use the Pivot line as target.

• Use Support or Resistance Zones as targets in reversal method.

What are the Lines?

Gray Line:

• It the day Open or can be considered as Pivot.

Red & Green ADR Zones:

• Red Zone is Resistance.

• Green Zone is Support.

• Mostly price can reverse from this Zones.

• Multiple Red and Green Lines forms a Zone.

• These lines are average levels of past days which helps to figure out the maximum and minimum price range that can be moved in that day.

• The default number of days are 5, 7 and 14. This can be customized.

Red & Green Target Lines:

• These are Target levels.

What are the Labels?

• First Number: Price of that level.

• Numbers in (): Percentage change and Change of price from LTP (Last Traded Price) to that Level.

General Tips

• It is good if Stock trend is same as that of the Index trend.

• Lots of indicators creates lots of confusion.

• Keep the chart simple and clean.

• Buy Low and Sell High.

• Master averages or 50%.

在腳本中搜尋"accumulation"

Volume Risk Avoidance IndicatorPrice Pattern Analysis is the core of trading. But price patterns often fails.

VRAI (Volume Risk Avoidance Indicator) shows Volume Pressure, so that you can avoid volume-based risks.

For example, never short when you see green (buying pressure). Never long when you see red (selling pressure).

You still need to pick good price patterns, because the crossover of volume pressure is not reliable.

Enjoy!

Break of structure indicatorThis indicator allows you to set a range of price which you want to get an alert about if price breaks that structure.

Whale Hunter [Gu5]Indicator to show a big change (Whale) in the same candle

The candles change color, until the Momentum returns to zero

After the movement of a whale, the market is usually on range, and there may be false entries

The default values (2.618% and 20 lenght), are optimized for BTCUSD 15m

---

Spanish

Este indicador muestrar un gran cambio porcentual (ballena) en la misma vela

Las velas cambian de color, hasta que el Momentum vuelve a cero

Luego de el movimiento de una ballena, el mercado suele quedar en lateral, y puede haber falsas entradas

Los valores por defecto (2.618% y 20 lenght), están optimizados para BTCUSD 15m

Volume Ticks - Increasing Volume Bar Count [LucF]Volume Ticks is a zero-lag market sentiment indicator. It works by providing a cumulative count of increasing volume columns.

A one count is added for each increasing volume column where close>open, and one is subtracted on an increasing volume column if close

IO_EMA_Delta_OscillatorThis is a EMA Delta Oscillator: An attempt to show ranging markets based on the slope of the EMA.

Green = Bullish Market

Blue = Ranging Market

Red = Bearish Market

The EMA Slope is normalized to make it work like an oscillator with values between 0 and 1.

Bar colors show the oscillator colors, bar borders show the actual candle colors.

- Invsto

(sarangab)

XBT Volatility Weighted Bottom Finder. [For Daily Charts]An update to:

Made it into and indicator.

v. 0.0.1

DESIGNED FOR DAILY CHARTS

Weis Wave ChartThis indicator is based on the Weis Wave described by David H. Weis in his book Trades About to Happen: A Modern Adaptation of the Wyckoff Method, more info how to use this indicator can be found in this video . The Weis Wave is an adaptation of Richard D. Wyckoff’s method Wave Charts. It works in all time periods and can be applied to all asset types.

Unlike other implementations I found here on TradingView, this implementation make use of a Renko-like zig zag pattern, very similar to how it is described in David H. Weis' book. The settings for the zig zag pattern are very similar to the standard Renko settings here on TradingView, in the "Renko Assignment Method" you either chose "ATR" or "Traditional" (read more about it here ). The ATR length or the brick size is then entered in the textbox "Value". You can also chose another setting in the "Renko Assignment Method" drop down named "Part of Price" which calculate the brick size from the current close and divide it by the value in the text box "Value". It is also possible to chose if the zig zag pattern shall use the high/low, the open/close or just the close as the most extreme values in its calculation, you select this in the drop down "Price Source".

TradingView's pine script does currently not support to print non-static text on the chart, so it is not possible at this point to write out the volume on the zig zag chart. It is also not possible to have both an overlay and separate chart pane in the same indicator, therefor this indicator is split up in two.

You can find the volume indicator here:

Weis Wave VolumeThis indicator is based on the Weis Wave described by David H. Weis in his book Trades About to Happen: A Modern Adaptation of the Wyckoff Method, more info how to use this indicator can also be found in this video . The Weis Wave is an adaptation of Richard D. Wyckoff’s method Wave Charts. It works in all time periods and can be applied to all asset types. For assets that do not support volume Weis propose in his book to use the true range instead, so if you want to use this indicator for assets that do not support volume, make sure to enable the checkbox "Use True Range instead of Volume".

Unlike other implementations I found here on Trading, this implementation make use of a Renko-like zig zag pattern, very similar to how it is described in David H. Weis' book. The settings for the zig zag pattern are very similar to the standard Renko settings here on TradingView, in the "Renko Assignment Method" you either chose "ATR" or "Traditional" (read more about it here ). The ATR length or the brick size is then entered in the textbox "Value". You can also chose another setting in the "Renko Assignment Method" drop down named "Part of Price" which calculate the brick size from the current close and divide it by the value in the text box "Value". It is also possible to chose if the zig zag pattern shall use the high/low, the open/close or just the close as the most extreme values in its calculation, you select this in the drop down "Price Source". If you want the price to oscillate around a zero value, enable the "Oscillating" checkbox.

TradingView's pine script does currently not support to print non-static text on the chart, so it is not possible at this point to write out the volume on the zig zag chart. It is also not possible to have both an overlay and separate chart pane in the same indicator, therefor this indicator is split up in two.

You can find the zig zag indicator here:

Indicator: Weis Wave Volume [LazyBear]This indicator takes market volume and organizes it into wave charts, clearly highlighting inflection points and regions of supply/demand.

Try tuning this for your instrument (Forex not supported) by adjusting the "Trend Detection Length". This "clubs together" minor waves. If you like an oscillator-kind-of display, enable "ShowDistributionBelowZero" option.

Note: This indicator is a port of a clone of WeisVolumePlugin available for another platform. I don't know how close this is to the original Weis, if any has access to it, do let me know how this compares. Thanks.

More info:

weisonwyckoff.com

Complete list of my indicators:

Bitcoin Macro Trend IndicatorBitcoin Macro Trend Indicator: A Multi-Timeframe Confirmation System for Strategic Positioning

Introduction

The Bitcoin Macro Trend Indicator is a comprehensive technical analysis tool designed for cryptocurrency traders and investors seeking to navigate Bitcoin's volatile cycles. It integrates multiple exponential moving averages (EMAs) and MACD variations into a unified system that identifies long-term accumulation zones, bull market tops, and strategic re-entry points. This document outlines the logical foundation of this integration, explains the synergistic operation of its components, and provides practical guidance for its application.

Rationale for Multi-Indicator Integration

Bitcoin's market behavior exhibits distinct cyclical patterns characterized by extended accumulation periods, parabolic advances, and sharp corrections. Single indicators often generate false signals during volatile conditions. This system employs a layered confirmation approach where:

Ultra-long-term EMAs establish the primary trend context

Medium-term EMA crossovers identify trend transitions

Multiple MACD configurations detect momentum shifts across different time horizons

This multi-timeframe methodology reduces noise and increases signal reliability by requiring convergence across independent but complementary technical elements.

Component Synergy and Operational Mechanism

1. EMA Framework: The Trend Foundation

700-period EMA: Serves as the primary trend baseline. Prices below this line suggest long-term undervaluation (accumulation territory), while sustained positions above indicate established bull markets.

18/63-period EMA Pair: Functions as the core trend transition system. The golden cross (18 above 63) confirms bullish momentum, while the death cross signals potential trend exhaustion.

12/52-period EMA Pair: Specialized for identifying renewed momentum after corrections within ongoing trends, reducing premature re-entry during false recoveries.

12-period EMA (Auxiliary): Provides early warning of short-term trend deterioration that may precede larger corrections.

2. MACD Ensemble: Momentum Verification

Bottom MACD (168/364/6): With exceptionally slow parameters, this configuration filters out short-term noise to identify genuine long-term momentum shifts characteristic of market bottoms.

Top MACD (63/133/1): Optimized for detecting momentum divergence at potential market tops, where traditional MACD settings often lag.

Local Top Warning MACD (30/65/4): Balanced to capture intermediate-term momentum deterioration that frequently precedes significant pullbacks.

Early Bull MACD (9/19/6): Sensitive to initial momentum surges following accumulation periods, providing early confirmation of trend initiation.

3. Signal Hierarchy and Progressive Confirmation

The indicator employs a cascading confirmation logic:

Stage 1 (Accumulation): Requires both long-term MACD improvement AND price position below the 700-period EMA. Strong accumulation signals add Early Bull MACD confirmation.

Stage 2 (Warning): Local top warnings activate only when multiple conditions align: medium-term trend remains bullish, ultra-long-term trend confirms strength, AND specialized MACDs show momentum deterioration.

Stage 3 (Re-entry): Requires both EMA crossover confirmation AND momentum recovery in the warning MACD, reducing false continuation signals.

Stage 4 (Top Confirmation): The most stringent criteria, demanding convergence across long-term, medium-term, and momentum indicators before signaling major trend reversal.

Practical Application and Interpretation

Signal Classification System

Accumulation Zones (Green): Areas where long-term indicators suggest undervaluation. These represent strategic buying opportunities for patient investors.

Strong Accumulation Signals (Dark Green): Enhanced accumulation zones with additional momentum confirmation, suggesting higher-probability entry points.

Local Top Warnings (Orange/Red): Progressive warnings of increasing risk, with red zones indicating conditions historically associated with more severe corrections.

Re-entry Opportunities (Blue): Post-correction zones where momentum recovery aligns with trend resumption signals.

Bull Market Termination (Purple): Signals suggesting completion of major advance cycles, prompting defensive positioning.

Top Confirmation (Dark Red): High-confidence reversal signals with multi-timeframe confirmation.

Usage Guidelines

Timeframe Recommendation: Designed primarily for daily and weekly charts where macroeconomic trends are most evident.

Position Sizing: Accumulation signals support gradual position building, while warning signals suggest reducing exposure rather than immediate liquidation.

Corroboration: Although self-contained, the indicator performs best when combined with volume analysis and fundamental considerations.

Historical Validation: Users should review signal performance across multiple market cycles to understand characteristic behaviors.

Limitations and Considerations

No technical indicator predicts market movements with absolute certainty. This tool provides probabilistic assessments based on historical patterns.

Extraordinary market events or fundamental shifts may override technical signals.

The indicator's parameters, while optimized for Bitcoin's historical behavior, may require adjustment for unprecedented market conditions.

Signals should be interpreted in context of overall market structure and trader/investor time horizon.

Originality and Differentiation

This system represents a novel synthesis of established technical concepts through:

Parameter Optimization: Specific EMA and MACD periods calibrated to Bitcoin's characteristic volatility and cycle duration.

Conditional Layering: Unlike single-criterion systems, signals require convergence across independent technical dimensions.

Progressive Warning System: Multi-stage alerts that distinguish between routine corrections and potential trend reversals.

Macro-Micro Integration: Simultaneous analysis of ultra-long-term trends and short-term momentum shifts.

Empirical Foundation

The indicator's design incorporates observations from Bitcoin's market behavior since 2010, particularly:

The tendency for major bottoms to form during extended periods below long-term moving averages

Characteristic momentum patterns preceding significant tops

The predictive value of specific EMA relationships during different market phases

Historical performance of multi-timeframe confirmation versus single indicators

Conclusion

The Bitcoin Macro Trend Indicator provides a structured framework for identifying high-probability turning points in Bitcoin's market cycles. By integrating multiple technical perspectives into a confirmation hierarchy, it reduces reaction to market noise while maintaining sensitivity to genuine trend changes. Users should employ this tool as part of a comprehensive trading plan that includes risk management protocols and consideration of external market factors. The system's greatest utility emerges when understood not as a predictive oracle but as a systematic method for identifying favorable risk-reward scenarios based on multi-timeframe technical convergence.

VSA Trading SystemMaster Reference Guide

📚 TABLE OF CONTENTS

PART 1: Core VSA Framework & Philosophy

PART 2: Volume Analysis Deep Dive

PART 3: Key VSA Setups (Complete)

PART 4: Wyckoff Accumulation & Distribution

PART 5: Multi-Timeframe Analysis

PART 6: Candle & Spread Analysis

PART 7: Entry, Stop Loss & Take Profit Rules

PART 8: Position Sizing & Risk Management

PART 9: Complete Trade Checklists

PART 10: Common Mistakes & Quick Reference

PART 11: Trade Journal Template

PART 1: CORE VSA FRAMEWORK & PHILOSOPHY

The Foundation Principle

╔════════════════════════════════════════════════════════════════╗

║ VSA FOUNDATION PRINCIPLE ║

╠════════════════════════════════════════════════════════════════╣

║ ║

║ "Smart Money leaves footprints in VOLUME" ║

║ ║

║ • Institutions cannot hide their activity ║

║ • Large orders create volume anomalies ║

║ • Price can lie, but volume confirms truth ║

║ • Volume is the FUEL, Price is the VEHICLE ║

║ • No fuel = No real move ║

║ ║

╚════════════════════════════════════════════════════════════════╝

The Golden Rule: Effort vs. Result

┌─────────────────────────────────────────────────────────────┐

│ HARMONY = TREND CONTINUATION │

│ ANOMALY = TREND REVERSAL │

└─────────────────────────────────────────────────────────────┘

Volume-Price Harmony Matrix

Price Action Volume Signal Interpretation

Rising ↑ Rising ↑ ✅ STRONG BULLISH Healthy uptrend, buyers in control

Rising ↑ Falling ↓ ⚠️ WEAK BULLISH Fuel running out, reversal near

Falling ↓ Rising ↑ ✅ STRONG BEARISH Aggressive selling, downtrend healthy

Falling ↓ Falling ↓ ⚠️ WEAK BEARISH Sellers exhausted, bottom forming

Effort vs. Result Complete Matrix

╔══════════════════════════════════════════════════════════════════╗

║ EFFORT VS RESULT MATRIX ║

╠═══════════════╦══════════════════╦════════════════════════════════╣

║ EFFORT ║ RESULT ║ INTERPRETATION ║

║ (Volume) ║ (Price Move) ║ ║

╠═══════════════╬══════════════════╬════════════════════════════════╣

║ ║ ║ ║

║ HIGH Volume ║ WIDE Spread ║ ✅ Normal - Trend healthy ║

║ ║ ║ ║

╠═══════════════╬══════════════════╬════════════════════════════════╣

║ ║ ║ ║

║ HIGH Volume ║ NARROW Spread ║ ⚠️ Absorption - Reversal soon ║

║ ║ ║ ║

╠═══════════════╬══════════════════╬════════════════════════════════╣

║ ║ ║ ║

║ LOW Volume ║ WIDE Spread ║ ⚠️ Fake move - Will reverse ║

║ ║ ║ ║

╠═══════════════╬══════════════════╬════════════════════════════════╣

║ ║ ║ ║

║ LOW Volume ║ NARROW Spread ║ 😐 No interest - Wait ║

║ ║ ║ ║

╚═══════════════╩══════════════════╩════════════════════════════════╝

PART 2: VOLUME ANALYSIS DEEP DIVE

Volume Classification (Compare to 20-period MA):

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

ULTRA HIGH ▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓ (>200% of 20-period average)

→ Major institutional activity

→ Potential climax or absorption

HIGH ▓▓▓▓▓▓▓▓▓▓▓▓ (150-200% of average)

→ Significant interest

→ Breakout/breakdown confirmation

ABOVE AVERAGE ▓▓▓▓▓▓▓▓▓ (100-150% of average)

→ Healthy trend participation

→ Normal directional moves

AVERAGE ▓▓▓▓▓▓ (80-120% of average)

→ Baseline activity

→ Consolidation periods

LOW ▓▓▓ (50-80% of average)

→ Lack of interest

→ Test bars, pullbacks

ULTRA LOW ▓ (<50% of average)

→ No participation

→ Holiday/pre-news quiet

Volume Bar Colors & Meanings

┌─────────────────────────────────────────────────────────────┐

│ VOLUME BAR ANALYSIS │

├─────────────────────────────────────────────────────────────┤

│ │

│ GREEN Volume Bar (Buying Volume Dominant) │

│ ▓▓▓▓▓▓▓▓▓ │

│ + Green Candle = Healthy Buying │

│ + Red Candle = Possible Accumulation (watch for reversal) │

│ │

├─────────────────────────────────────────────────────────────┤

│ │

│ RED Volume Bar (Selling Volume Dominant) │

│ ░░░░░░░░░ │

│ + Red Candle = Healthy Selling │

│ + Green Candle = Possible Distribution (watch for drop) │

│ │

└─────────────────────────────────────────────────────────────┘

Volume Context Analysis

┌─────────────────────────────────────────────────────────────────┐

│ CONTEXT IS EVERYTHING │

├─────────────────────────────────────────────────────────────────┤

│ │

│ Same high volume candle means DIFFERENT things: │

│ │

│ AT SUPPORT: AT RESISTANCE: │

│ ┌─────────────┐ ┌─────────────┐ │

│ │ High Volume │ │ High Volume │ │

│ │ Small Body │ │ Small Body │ │

│ │ = BUYING │ │ = SELLING │ │

│ │ (Bullish) │ │ (Bearish) │ │

│ └─────────────┘ └─────────────┘ │

│ │

│ IN UPTREND: IN DOWNTREND: │

│ ┌─────────────┐ ┌─────────────┐ │

│ │ High Volume │ │ High Volume │ │

│ │ Small Body │ │ Small Body │ │

│ │ = Potential │ │ = Potential │ │

│ │ TOP │ │ BOTTOM │ │

│ └─────────────┘ └─────────────┘ │

│ │

└─────────────────────────────────────────────────────────────────┘

Volume Spike Interpretation

SCENARIO 1: Volume Spike at Support

─────────────────────────────────────

│

↓ ← Price drops to support

═════════════ Support Line

▼

▓▓▓▓▓▓▓▓▓▓▓▓ ← ULTRA HIGH Volume

→ INTERPRETATION: Absorption/Accumulation

→ ACTION: Prepare for LONG entry after confirmation

─────────────────────────────────────

SCENARIO 2: Volume Spike at Resistance

─────────────────────────────────────

▓▓▓▓▓▓▓▓▓▓▓▓ ← ULTRA HIGH Volume

▲

═════════════ Resistance Line

↑ ← Price rises to resistance

│

→ INTERPRETATION: Churning/Distribution

→ ACTION: Prepare for SHORT entry OR exit longs

─────────────────────────────────────

SCENARIO 3: Volume Spike on Breakout

─────────────────────────────────────

↗ ← Price breaks out

═════════════════════════════ Resistance

│

▓▓▓▓▓▓▓▓▓ ← HIGH Volume on breakout

→ INTERPRETATION: Valid Breakout

→ ACTION: ENTER in breakout direction

─────────────────────────────────────

SCENARIO 4: Low Volume on Breakout

─────────────────────────────────────

↗ ← Price breaks out

═════════════════════════════ Resistance

│

▓▓ ← LOW Volume on breakout

→ INTERPRETATION: FAKE Breakout

→ ACTION: DO NOT ENTER, wait for failure

─────────────────────────────────────

Recommended Volume Indicators

ESSENTIAL INDICATORS:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

1. STANDARD VOLUME

└─ Basic but essential

└─ Color-coded by candle direction

2. VOLUME MOVING AVERAGE (20-period)

└─ Shows average volume

└─ Helps identify "high" vs "low" volume

└─ CRITICAL: Only consider signals where Volume > 1.5x MA

└─ Ultra High = Volume > 2x MA

3. VOLUME WEIGHTED AVERAGE PRICE (VWAP)

└─ Intraday fair value

└─ Institutional reference point

OPTIONAL BUT USEFUL:

━━━━━━━━━━━━━━━━━━━━━

• On-Balance Volume (OBV) - Cumulative flow, good for divergences

• Accumulation/Distribution Line - Money flow direction

• Volume Profile - Price levels with most volume

• Money Flow Index - Volume-weighted RSI

PART 3: KEY VSA SETUPS (COMPLETE)

Setup 1: Test No Supply (Bullish)

VISUAL:

Prior Uptrend

↗

↗

↗

↗

↗

↗ ┌───┐

↗ │ R │ ← Small RED candle (Test)

↗ └───┘

↗ │

↗ │ LOW VOLUME

↗ │

↗ ══════╧══════

COMPLETE CHECKLIST:

□ Existing uptrend (HH + HL pattern)

□ Small pullback candle (red/bearish)

□ Volume BELOW average (ideally <70% of 20-MA)

□ Volume LESS than previous 2 bars

□ Spread (range) is NARROW

□ Candle closes near its high (upper half)

□ Doesn't break previous swing low

□ Wicks are small (no heavy selling)

ENTRY TRIGGER:

→ Next candle closes green above test candle high

→ Volume on entry candle is average or above

STOP LOSS:

→ Below the test candle low

→ OR below the previous swing low

WHY IT WORKS:

Smart money "tests" to see if sellers remain.

Low volume = No sellers left = Safe to push higher

Setup 2: Test No Demand (Bearish)

VISUAL:

┌───┐

│ G │ ← Small GREEN candle (Test)

└───┘

│ LOW VOLUME

↗ │

↗ ══════════╧══════

↗ ↘

↗ ↘

↘

↘ Downtrend continues

COMPLETE CHECKLIST:

□ UP bar (close > open) - Green candle

□ Volume LESS than previous 2 bars

□ Volume BELOW average (ideally <70% of 20-MA)

□ Spread (range) is NARROW

□ Close in MIDDLE or LOW of bar

□ Located at resistance OR after uptrend

□ Price struggling to make new highs

ENTRY TRIGGER:

→ Next candle closes red below test candle low

STOP LOSS:

→ Above the test candle high

WHY IT WORKS:

Buyers tried but professionals not interested.

Low volume = No demand = Prepare for drop

Setup 3: Spring (Bull Trap Reversal)

VISUAL:

Support Line

═══════════════════════════════

↓↗ ← Spring (false breakdown + quick recovery)

Spring

(Bear Trap)

Price Chart:

════════════════════ Support

↓

↓ ← Break below support

▼

SPRING ← Ultra low point

↗

↗ ← Quick recovery above support

════════════════════

↗

↗ ← Uptrend begins

Volume Pattern:

On Spring: ▓▓▓ (Can be high or low)

On Test: ▓ (Must be LOW)

On Breakout: ▓▓▓▓▓▓▓ (High)

CHECKLIST:

□ Price dipped below support (Spring)

□ Quickly reversed back above support

□ Pullback test shows LOW VOLUME

□ Test candle doesn't break spring low

ENTRY:

→ Enter LONG on low volume test after spring

→ OR enter when price closes above spring high

STOP LOSS:

→ Below the spring low

Setup 4: Upthrust (Bear Trap Reversal)

VISUAL:

↑ False breakout above resistance

═══════════════════════════════ Resistance

↗↓ ← Upthrust (break above + fail)

Upthrust

(Bull Trap)

Price Chart:

↗

↗ ← Price rises

════════════════════ Resistance

↗

UPTHRUST ← Ultra high point (false break)

↓

↓ ← Quick rejection below resistance

════════════════════

↓

↘ ← Downtrend begins

Volume Pattern:

On Upthrust: ▓▓▓▓▓ (Often high - sucking in buyers)

On Test: ▓ (Must be LOW)

On Breakdown: ▓▓▓▓▓▓▓ (High)

CHECKLIST:

□ Price broke ABOVE resistance

□ Quickly FAILED and fell back below

□ Pullback test (rally) shows LOW VOLUME

□ Test candle doesn't break upthrust high

ENTRY:

→ Enter SHORT on low volume test after upthrust

→ OR enter when price closes below upthrust low

STOP LOSS:

→ Above the upthrust high

Setup 5: Absorption (Churning)

BEARISH ABSORPTION (Distribution at Top):

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Price: ──────────────── Resistance

│ ▲ │

│ █ │ ← Small GREEN body

│ ▼ │ (buyers trying to push up)

─────┴───┴─────

Volume: ▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓ ← MASSIVE (>200% average)

COMPLETE CHECKLIST:

□ Small/Medium GREEN candle

□ Volume > 2x average

□ Close in MIDDLE or LOWER half of candle

□ Located at resistance OR after extended uptrend

□ Price NOT making significant new highs despite volume

INTERPRETATION:

• Price tries to go up

• Huge volume BUT small price movement

• Where did all that buying go?

• Answer: Institutions ABSORBED it by selling

CONFIRMATION:

□ Next candle should be RED

RESULT: Expect price drop

═══════════════════════════════════════════════════

BULLISH ABSORPTION (Accumulation at Bottom):

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

│ ▼ │

│ █ │ ← Small RED body

│ ▲ │ (sellers trying to push down)

─────┴───┴─────

Price: ──────────────── Support

Volume: ▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓ ← MASSIVE (>200% average)

COMPLETE CHECKLIST:

□ Small/Medium RED candle

□ Volume > 2x average

□ Close in MIDDLE or UPPER half of candle

□ Located at support OR after extended downtrend

□ Price NOT making significant new lows despite volume

INTERPRETATION:

• Price tries to go down

• Huge volume BUT small price movement

• Where did all that selling go?

• Answer: Institutions ABSORBED it by buying

CONFIRMATION:

□ Next candle should be GREEN

RESULT: Expect price rise

Setup 6: Climactic Action

BUYING CLIMAX (Marks the TOP):

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

▲

/│\ ← WIDEST candle in uptrend

/ │ \ + Close near HIGH

/ │ \

/ │ \

▓▓▓▓▓▓▓▓▓▓▓▓▓ ← HIGHEST volume in uptrend

CHARACTERISTICS:

□ Widest spread (range) in the trend

□ Highest volume in the trend

□ Usually closes near the high

□ Euphoria/FOMO buying

□ Professionals SELLING to public

→ Signals END of Uptrend

→ Distribution phase begins

→ DO NOT BUY - Wait for short setup

═══════════════════════════════════════════

SELLING CLIMAX (Marks the BOTTOM):

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

\ │ /

\ │ /

\ │ /

\│/ ← WIDEST candle in downtrend

▼ + Often closes OFF the lows

▓▓▓▓▓▓▓▓▓▓▓▓▓ ← HIGHEST volume in downtrend

CHARACTERISTICS:

□ Widest spread (range) in the trend

□ Highest volume in the trend

□ Often closes in middle or upper half (key difference!)

□ Panic selling

□ Professionals BUYING from public

→ Signals END of Downtrend

→ Accumulation phase begins

→ DO NOT SELL - Wait for long setup after TEST

Setup 7: Stopping Volume

STOPPING VOLUME (Bottom Formation):

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Price falling...

↓

↓

↓

┌───────────┐

│ ███████ │ ← Wide spread DOWN bar

│ ███████ │ BUT closes OFF the lows

│ │ │ (Close in UPPER half - KEY!)

└─────│─────┘

│

▓▓▓▓▓▓▓▓▓▓▓▓▓▓ ← ULTRA HIGH volume

CHECKLIST:

□ Downtrend in progress

□ Wide spread (large range) candle

□ Ultra high volume (>200% of average)

□ Closes in UPPER HALF of the bar (critical!)

□ May have long lower wick

INTERPRETATION:

→ Professionals absorbing all selling

→ Supply being removed from market

NEXT STEPS:

→ Expect sideways consolidation

→ Wait for LOW VOLUME TEST before entry

→ Do NOT enter immediately - wait for confirmation

Setup 8: Breakout Confirmation

VALID BREAKOUT: FAKE BREAKOUT:

─────────────── ───────────────

│ ↑ HIGH VOLUME │ ↑ LOW VOLUME

─────│───────── ─────│─────────

│ │

▓▓▓▓▓▓▓▓▓ (Volume >150% avg) ▓▓▓ (Volume <100% avg)

✅ ENTER TRADE ❌ DO NOT ENTER

(Wait for failure/retest)

VALID BREAKOUT CHECKLIST:

□ Price closes ABOVE resistance (for long) or BELOW support (for short)

□ Volume > 150% of 20-period average

□ Candle closes near the extreme (high for long, low for short)

□ Preferably preceded by low volume consolidation

□ Higher timeframes support the direction

ENTRY:

→ Enter on close of breakout candle

→ OR enter on low volume retest of breakout level

STOP LOSS:

→ Below breakout level (for longs)

→ Above breakout level (for shorts)

PART 4: WYCKOFF ACCUMULATION & DISTRIBUTION

WYCKOFF ACCUMULATION

Price:

│

│ PS SC

│ ↘ ↓

│ ↘ ↓ AR

│ ↘ ↓ ↗

│ ↘ ↓ ↗ ST

│ ↓↗──────────┐ LPS

│ PHASE A │ PHASE B │ ↘ ↗ SOS

│ │ │ ↘ ↗ ↗

│ │ │ ↓ ↗

│ │ │ SPRING↗

│ │ PHASE C│ │↗ PHASE D

│ │ │ ↗

└────────────┴─────────┴────┴──────────→

PHASE DEFINITIONS:

━━━━━━━━━━━━━━━━━━

PHASE A - Stopping the Downtrend:

PS = Preliminary Support (first buying appears)

SC = Selling Climax (panic selling absorbed - HIGH volume)

AR = Automatic Rally (dead cat bounce)

ST = Secondary Test (retest of SC lows - lower volume than SC)

PHASE B - Building the Cause:

→ Sideways accumulation

→ Volume generally decreasing

→ Multiple tests of support and resistance

→ "Backing up to the creek" patterns

PHASE C - The Test:

SPRING = False breakdown below support (bear trap)

→ Can be high or low volume

→ Key: Quick recovery above support

TEST = Low volume retest after spring (CRITICAL ENTRY POINT)

PHASE D - Markup Begins:

SOS = Sign of Strength (strong rally with high volume)

LPS = Last Point of Support (final low volume pullback)

→ This is the LAST safe entry before markup

PHASE E - Markup (Not shown):

→ Strong uptrend with increasing volume

→ Higher highs and higher lows

VOLUME PATTERN:

━━━━━━━━━━━━━━━

▓▓▓▓▓▓ ▓▓ ▓▓ ▓▓▓▓▓

(High) (Lower) (Low on) (High on

at SC during Spring SOS)

Phase B Test

Key Accumulation Entry Point

ENTRY CHECKLIST - THE SPRING + TEST:

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

□ Phase A complete (SC and AR visible)

□ Phase B complete (sideways range established)

□ Spring occurred (price dipped below support)

□ Price quickly recovered above support

□ Test pullback has LOW VOLUME (critical!)

□ Test doesn't break spring low

ENTRY TRIGGER:

→ Enter LONG after low volume test

→ OR enter on break above spring high with volume

STOP LOSS:

→ Below spring low

TARGET:

→ Measure the range (support to resistance)

→ Project that distance above resistance

Wyckoff Distribution Schematic--

WYCKOFF DISTRIBUTION

Price:

│ PSY

│ ↗ BC

│ ↗ ↗ ↘

│ PHASE D ↗ ↗ ↘ UTAD

│ ↘ ↗ ↗ ↘ ↗↘

│ ↘ ↗ ↗────────↘↗ ↘

│ ↘ ↗ │ PHASE B │ ↘ SOW

│ ↘ ↗ │ │ ↘

│ ↘ │ PHASE C │ ↘

│ LPSY │ │ ↘

│ │ │ ↘

└────────────────┴─────────┴─────────→

PHASE DEFINITIONS:

━━━━━━━━━━━━━━━━━━

PHASE A - Stopping the Uptrend:

PSY = Preliminary Supply (first selling appears)

BC = Buying Climax (euphoric buying absorbed - HIGH volume)

AR = Automatic Reaction (first drop)

ST = Secondary Test (retest of BC highs - lower volume than BC)

PHASE B - Building the Cause:

→ Sideways distribution

→ Volume patterns show supply entering on rallies

→ Multiple tests of support and resistance

PHASE C - The Test:

UTAD = Upthrust After Distribution (false breakout above resistance)

→ Bull trap

→ Often high volume (sucking in late buyers)

TEST = Low volume retest after upthrust (ENTRY POINT FOR SHORTS)

PHASE D - Markdown Begins:

SOW = Sign of Weakness (strong drop with high volume)

LPSY = Last Point of Supply (final low volume rally)

→ This is the LAST safe short entry before markdown

PHASE E - Markdown (Not shown):

→ Strong downtrend with increasing volume

→ Lower highs and lower lows

PART 5: MULTI-TIMEFRAME ANALYSIS

The 4-Step Alignment Process

╔════════════════════════════════════════════════════════════════╗

║ 4-HOUR CHART (MACRO VIEW) ║

╠════════════════════════════════════════════════════════════════╣

║ ║

║ PURPOSE: Determine the PRIMARY trend direction ║

║ ║

║ ANALYZE: ║

║ □ Overall trend (Uptrend/Downtrend/Range) ║

║ □ Major support/resistance levels ║

║ □ Volume trend (increasing/decreasing with price) ║

║ □ Any divergences forming (Price↑ Volume↓ = warning) ║

║ □ Look for Accumulation/Distribution phases ║

║ ║

║ SIGNALS TO NOTE: ║

║ • Climax volume at extremes ║

║ • Trend line breaks ║

║ • Higher timeframe absorption patterns ║

║ ║

║ RULE: Only trade in the direction of 4H trend ║

║ ║

╚════════════════════════════════════════════════════════════════╝

↓ ALIGNED?

╔════════════════════════════════════════════════════════════════╗

║ 1-HOUR CHART (STRUCTURE) ║

╠════════════════════════════════════════════════════════════════╣

║ ║

║ PURPOSE: Confirm trend and identify key levels ║

║ ║

║ ANALYZE: ║

║ □ Trend alignment with 4H ║

║ □ Key swing highs and lows ║

║ □ Support/resistance zones ║

║ □ Moving average positions (if used) ║

║ □ Current Wyckoff phase ║

║ □ Volume pattern on recent moves ║

║ ║

║ SIGNALS TO NOTE: ║

║ • Structure breaks (BOS - Break of Structure) ║

║ • Change of character (CHoCH) ║

║ • Volume spikes at key levels ║

║ ║

║ RULE: Structure must support trade direction ║

║ ║

╚════════════════════════════════════════════════════════════════╝

↓ ALIGNED?

╔════════════════════════════════════════════════════════════════╗

║ 30-MIN CHART (SETUP) ║

╠════════════════════════════════════════════════════════════════╣

║ ║

║ PURPOSE: Identify specific trade setups ║

║ ║

║ ANALYZE: ║

║ □ Pullback/rally quality ║

║ □ Is pullback volume DECREASING? (Required for entry) ║

║ □ Approach to key levels ║

║ □ VSA patterns forming ║

║ □ Price action quality ║

║ ║

║ SIGNALS TO NOTE: ║

║ • Test patterns (No Supply/No Demand) ║

║ • Absorption at levels ║

║ • Volume drying up on counter-moves ║

║ ║

║ RULE: Wait for low volume pullback before entry ║

║ ║

╚════════════════════════════════════════════════════════════════╝

↓ ALIGNED?

╔════════════════════════════════════════════════════════════════╗

║ 15-MIN CHART (ENTRY TRIGGER) ║

╠════════════════════════════════════════════════════════════════╣

║ ║

║ PURPOSE: Precise entry timing ║

║ ║

║ ANALYZE: ║

║ □ Entry trigger candle forming ║

║ □ Volume on trigger candle ║

║ □ Exact stop loss placement ║

║ □ Immediate support/resistance ║

║ ║

║ ENTRY TRIGGERS (Need one): ║

║ • Test No Supply / Test No Demand ║

║ • Spring/Upthrust + Test ║

║ • Absorption + Confirmation candle ║

║ • Breakout with High Volume ║

║ ║

║ CRITICAL RULE: Wait for candle CLOSE before entering ║

║ ║

╚════════════════════════════════════════════════════════════════╝

↓ ALL ALIGNED?

═══════════════════════════

✅ EXECUTE TRADE

═══════════════════════════

PART 6: CANDLE & SPREAD ANALYSIS

Candle Close Position Analysis

WHERE DOES THE CANDLE CLOSE?

Strong Bullish: Neutral: Bearish:

┌─────────┐ ┌─────────┐ ┌─────────┐

│ ████████│ ← Close │ │ │ │ │

│ ████████│ at TOP │ │ │ ← Close │ │ │

│ ████████│ (Upper │ ████ │ MIDDLE │ │ │

│ │ │ third) │ ████ │ │ ████████│ ← Close

│ │ │ │ │ │ │ ████████│ BOTTOM

└─────────┘ └─────────┘ └─────────┘

✅ Buyers won ⚠️ Struggle ❌ Sellers won

decisively (indecision) decisively

APPLICATION RULES:

━━━━━━━━━━━━━━━━━━

□ Close in UPPER 1/3 + High Volume = Strong Buying

□ Close in LOWER 1/3 + High Volume = Strong Selling

□ Close in MIDDLE + High Volume = Battle (Wait for clarity)

FOR ABSORPTION SIGNALS:

□ Bearish Absorption: Green candle closes in MIDDLE or LOWER half

□ Bullish Absorption: Red candle closes in MIDDLE or UPPER half

Spread (Range) Analysis-

SPREAD = High - Low of Candle

┌──────────────────────────────────────────────────────────────┐

│ SPREAD ANALYSIS │

├──────────────────────────────────────────────────────────────┤

│ │

│ WIDE SPREAD + HIGH VOLUME: │

│ ┌─────────────────────┐ │

│ │ │ │ │

│ │ ███████████ │ → HEALTHY momentum │

│ │ ███████████ │ → Trend continuation │

│ │ │ │ → Strong commitment │

│ └─────────────────────┘ │

│ ▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓▓ │

│ │

├──────────────────────────────────────────────────────────────┤

│ │

│ NARROW SPREAD + HIGH VOLUME: │

│ ┌───────────┐ │

│ │ ████ │ ← Small body │

│ │ ████ │ │

│ └───────────┘ → ABSORPTION warning! │

│ ▓▓▓▓▓▓▓▓▓▓▓▓ → Effort with no result │

│ → Expect reversal │

│ │

├──────────────────────────────────────────────────────────────┤

│ │

│ WIDE SPREAD + LOW VOLUME: │

│ ┌─────────────────────┐ │

│ │ │ │ │

│ │ ███████████ │ → FAKE MOVE warning! │

│ │ ███████████ │ → No commitment │

│ │ │ │ → Will likely reverse │

│ └─────────────────────┘ │

│ ▓▓▓ │

│ │

├──────────────────────────────────────────────────────────────┤

│ │

│ NARROW SPREAD + LOW VOLUME: │

│ ┌───────────┐ │

│ │ ████ │ → No interest │

│ │ ████ │ → Consolidation │

│ └───────────┘ → WAIT for signal │

│ ▓▓ │

│ │

└──────────────────────────────────────────────────────────────┘

PART 7: ENTRY, STOP LOSS & TAKE PROFIT RULES

╔═══════════════════════════════════════════════════════════════╗

║ LONG ENTRY CRITERIA ║

╠═══════════════════════════════════════════════════════════════╣

║ ║

║ MULTI-TIMEFRAME CHECK: ║

║ ──────────────────── ║

║ □ 4H: Uptrend + Rising Volume (or no bearish divergence) ║

║ □ 1H: Uptrend + Price holding above support ║

║ □ 30M: Pullback with DECREASING volume ║

║ □ 15M: Entry trigger present ║

║ ║

║ VOLUME CONFIRMATION: ║

║ ─────────────────── ║

║ □ Pullback candles have LOW volume ║

║ □ No bearish absorption at highs ║

║ □ Prior trend showed harmony (price↑ + volume↑) ║

║ □ Volume compared to 20-MA (signal volume significant?) ║

║ ║

║ CANDLE CONFIRMATION: ║

║ ─────────────────── ║

║ □ Entry candle closes in upper half ║

║ □ No abnormally wide spread with low volume (fake move) ║

║ □ Test candle had appropriate close position ║

║ ║

║ ENTRY TRIGGERS (Any One): ║

║ ──────────────────────── ║

║ ○ Test No Supply confirmed (low vol red, next green) ║

║ ○ Spring + Low Volume Test ║

║ ○ Breakout with High Volume (>150% of average) ║

║ ○ Bullish Absorption at support + green confirmation ║

║ ○ Stopping volume + Test ║

║ ║

║ WAIT FOR CANDLE CLOSE BEFORE ENTERING! ║

║ ║

╚═══════════════════════════════════════════════════════════════╝

Short Entry Criteria-

╔═══════════════════════════════════════════════════════════════╗

║ SHORT ENTRY CRITERIA ║

╠═══════════════════════════════════════════════════════════════╣

║ ║

║ MULTI-TIMEFRAME CHECK: ║

║ ──────────────────── ║

║ □ 4H: Downtrend OR Bearish Divergence (price↑ volume↓) ║

║ □ 1H: Lower Highs forming OR at resistance ║

║ □ 30M: Rally with DECREASING volume ║

║ □ 15M: Entry trigger present ║

║ ║

║ VOLUME CONFIRMATION: ║

║ ─────────────────── ║

║ □ Rally candles have LOW volume ║

║ □ No bullish absorption at lows ║

║ □ Bearish Absorption visible at resistance ║

║ □ Anomaly present (price↑ but volume↓) ║

║ ║

║ CANDLE CONFIRMATION: ║

║ ─────────────────── ║

║ □ Entry candle closes in lower half ║

║ □ No abnormally wide spread with low volume (fake move) ║

║ □ Test candle had appropriate close position ║

║ ║

║ ENTRY TRIGGERS (Any One): ║

║ ──────────────────────── ║

║ ○ Test No Demand confirmed (low vol green, next red) ║

║ ○ Upthrust + Low Volume Test ║

║ ○ Sign of Weakness (SOW) - Big red + High Volume ║

║ ○ Breakdown with High Volume (>150% of average) ║

║ ○ Bearish Absorption at resistance + red confirmation ║

║ ║

║ WAIT FOR CANDLE CLOSE BEFORE ENTERING! ║

║ ║

╚═══════════════════════════════════════════════════════════════╝

Stop Loss Placement Rules-

╔════════════════════════════════════════════════════════════╗

║ STOP LOSS PLACEMENT RULES ║

╠════════════════════════════════════════════════════════════╣

║ ║

║ FOR LONG TRADES: ║

║ ───────────────── ║

║ Option A: Below the TEST candle low ║

║ Option B: Below the Spring low (if Spring setup) ║

║ Option C: Below support zone + ATR buffer ║

║ ║

║ BUFFER FORMULA: ║

║ SL = Support Level - (0.5 × ATR of entry timeframe) ║

║ ║

║ VISUAL: ║

║ ─────────────────────────────── Support/Demand Zone ║

║ ← Entry Point ║

║ ║

║ ─────────────────────────────── SL: Below Support ║

║ │← 1-2% below zone OR below spring low ║

║ ║

╠════════════════════════════════════════════════════════════╣

║ ║

║ FOR SHORT TRADES: ║

║ ────────────────── ║

║ Option A: Above the TEST candle high ║

║ Option B: Above the Upthrust high (if Upthrust setup) ║

║ Option C: Above resistance zone + ATR buffer ║

║ ║

║ BUFFER FORMULA: ║

║ SL = Resistance Level + (0.5 × ATR of entry timeframe) ║

║ ║

║ VISUAL: ║

║ │← SL: Above resistance/recent high ║

║ ─────────────────────────────── Resistance Zone ║

║ ← Entry Point (Short) ║

║ ║

╚════════════════════════════════════════════════════════════╝

Take Profit Rules-

╔════════════════════════════════════════════════════════════╗

║ TAKE PROFIT RULES ║

╠════════════════════════════════════════════════════════════╣

║ ║

║ MINIMUM RISK:REWARD = 1:2 ║

║ ║

║ TP LEVELS (Based on Structure): ║

║ ──────────────────────────── ║

║ TP1: First resistance/support level = Aim for 1R ║

║ TP2: Second resistance/support level = Aim for 2R ║

║ TP3: Major level OR measured move = Aim for 3R+ ║

║ ║

║ SCALING OUT METHOD: ║

║ ───────────────────── ║

║ □ TP1 (33-40%): Close first portion at 1R ║

║ → Move SL to breakeven after TP1 hit ║

║ ║

║ □ TP2 (33-40%): Close second portion at 2R ║

║ → Trail SL to 1R profit level ║

║ ║

║ □ TP3 (20-34%): Close final portion at 3R or trail ║

║ → Use trailing stop below each new swing ║

║ ║

║ TRAILING STOP METHOD: ║

║ ────────────────────────────── ║

║ Longs: Trail SL below each new Higher Low ║

║ Shorts: Trail SL above each new Lower High ║

║ ║

║ VISUAL (Long Trade): ║

║ ║

║ TP3 ─────────────── (Major Resistance: 3R) ║

║ ║

║ TP2 ─────────────── (Next Resistance: 2R) ║

║ ║

║ TP1 ─────────────── (First Resistance: 1R) ║

║ ║

║ ENTRY ────────────── ║

║ ║

║ SL ───────────────── ║

║ ║

╠════════════════════════════════════════════════════════════╣

║ ║

║ EXIT ON VSA WEAKNESS SIGNALS: ║

║ ───────────────────────────── ║

║ Exit immediately if you see: ║

║ □ Climactic volume against your position ║

║ □ Absorption candle against your position ║

║ □ Break of structure on entry timeframe ║

║ □ Test No Demand (if long) or Test No Supply (if short) ║

║ ║

╚════════════════════════════════════════════════════════════╝

PART 8: POSITION SIZING & RISK MANAGEMENT

Position Size Calculator-

╔════════════════════════════════════════════════════════════════╗

║ POSITION SIZE CALCULATOR ║

╠════════════════════════════════════════════════════════════════╣

║ ║

║ STEP 1: Define Account Risk ║

║ ───────────────────────────── ║

║ Account Size: $__________ ║

║ Risk Per Trade: ____% (Recommended: 1-2%) ║

║ Dollar Risk: $__________ (Account × Risk%) ║

║ ║

║ STEP 2: Define Trade Risk ║

║ ──────────────────────── ║

║ Entry Price: $__________ ║

║ Stop Loss: $__________ ║

║ Risk Per Unit: $__________ (Entry - SL, absolute value) ║

║ ║

║ STEP 3: Calculate Position ║

║ ───────────────────────── ║

║ ║

║ Dollar Risk ║

║ Position Size = ───────────────── ║

║ Risk Per Unit ║

║ ║

║ ═══════════════════════════════════════════════════════════ ║

║ EXAMPLE: ║

║ ═══════════════════════════════════════════════════════════ ║

║ ║

║ Account: $10,000 ║

║ Risk: 1% = $100 ║

║ Entry: $50.00 ║

║ Stop Loss: $48.00 ║

║ Risk Per Share: $2.00 ║

║ ║

║ Position Size = $100 ÷ $2.00 = 50 shares ║

║ ║

╚════════════════════════════════════════════════════════════════╝

Risk Management Rules-

╔════════════════════════════════════════════════════════════╗

║ RISK MANAGEMENT RULES ║

╠════════════════════════════════════════════════════════════╣

║ ║

║ CAPITAL PROTECTION: ║

║ ─────────────────── ║

║ □ Never risk more than 1-2% per trade ║

║ □ Maximum 3 trades open at same time ║

║ □ Maximum 5% total portfolio risk at any time ║

║ □ Reduce size by 50% after 2 consecutive losses ║

║ □ Stop trading after 3 consecutive losses (review) ║

║ ║

║ CORRELATION AWARENESS: ║

║ ────────────────────── ║

║ □ Don't take same-direction trades in correlated pairs ║

║ □ Treat correlated positions as single larger position ║

║ ║

║ DRAWDOWN RULES: ║

║ ─────────────── ║

║ □ 5% daily drawdown = Stop trading for the day ║

║ □ 10% weekly drawdown = Review and reduce size ║

║ □ 20% monthly drawdown = Pause and full strategy review ║

║ ║

╚════════════════════════════════════════════════════════════╝

Position Scaling Strategy-

ENTRY SCALING (Building Position):

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

┌─────────────────────────────────────┐

│ │

│ Initial Entry: 50% of position │

│ First Add: 25% of position │

│ Second Add: 25% of position │

│ │

│ Add ONLY when: │

│ • Price moves in your favor │

│ • Volume confirms the move │

│ • Move SL to breakeven first │

│ • New VSA confirmation present │

│ │

└─────────────────────────────────────┘

EXIT SCALING (Taking Profits):

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

┌─────────────────────────────────────┐

│ │

│ TP1 (1R): Close 40% of position │

│ → Move SL to breakeven │

│ │

│ TP2 (2R): Close 40% of position │

│ → Trail SL to 1R │

│ │

│ TP3 (3R+): Close remaining 20% │

│ → Trail or let run │

│ │

└─────────────────────────────────────┘

PART 9: COMPLETE TRADE CHECKLISTS

Pre-Trade Validation Checklist-

╔════════════════════════════════════════════════════════════════════╗

║ COMPLETE VSA TRADE CHECKLIST ║

╠════════════════════════════════════════════════════════════════════╣

║ ║

║ TRADE TYPE: □ LONG □ SHORT ║

║ DATE: ___________ PAIR/ASSET: ___________ ║

║ ║

║ ═══════════════════════════════════════════════════════════════ ║

║ SECTION A: MULTI-TIMEFRAME ALIGNMENT (Must have 4/4) ║

║ ═══════════════════════════════════════════════════════════════ ║

║ ║

║ 4H CHART: ║

║ □ Trend aligned with trade direction ║

║ □ Volume confirms trend (harmony) ║

║ □ No major resistance/support blocking immediately ║

║ □ No bearish/bullish divergence against trade ║

║ ║

║ 1H CHART: ║

║ □ Trend aligned with trade direction ║

║ □ Structure intact (HH/HL for long, LH/LL for short) ║

║ □ Key level identified and respected ║

║ □ Wyckoff phase supports trade ║

║ ║

║ 30M CHART: ║

║ □ Trend aligned with trade direction ║

║ □ Pullback/Rally has DECREASING volume (LOW volume) ║

║ □ Near support zone (long) or resistance zone (short) ║

║ □ VSA setup forming ║

║ ║

║ 15M CHART: ║

║ □ Entry signal clearly present ║

║ □ Volume confirming the signal ║

║ □ Candle close position supports trade ║

║ □ Waiting for candle CLOSE before entry ║

║ ║

║ ═══════════════════════════════════════════════════════════════ ║

║ SECTION B: VOLUME ANALYSIS (Must have 4/4) ║

║ ═══════════════════════════════════════════════════════════════ ║

║ ║

║ □ Volume compared to 20-MA (is signal volume significant?) ║

║ □ Volume and Price in Harmony OR Clear reversal signal ║

║ □ Pullback/Rally has LOW volume (below average) ║

║ □ No absorption signals against trade direction ║

║ ║

║ ═══════════════════════════════════════════════════════════════ ║

║ SECTION C: CANDLE/SPREAD ANALYSIS (Must have 3/3) ║

║ ═══════════════════════════════════════════════════════════════ ║

║ ║

║ □ Spread (range) appropriate for the signal ║

║ □ Close position supports trade direction ║

║ □ No wide spread + low volume moves (fake move warning) ║

║ ║

║ ═══════════════════════════════════════════════════════════════ ║

║ SECTION D: ENTRY SIGNAL (Must have 1 confirmed) ║

║ ═══════════════════════════════════════════════════════════════ ║

║ ║

║ □ Test No Supply / Test No Demand ║

║ □ Spring / Upthrust + Low Volume Test ║

║ □ Absorption at key level + Confirmation candle ║

║ □ Breakout with High Volume (>150% average) ║

║ □ Stopping Volume + Test ║

║ ║

║ ═══════════════════════════════════════════════════════════════ ║

║ SECTION E: RISK MANAGEMENT (Must have 5/5) ║

║ ═══════════════════════════════════════════════════════════════ ║

║ ║

║ □ Risk ≤ 1-2% of account ║

║ □ Risk:Reward ≥ 1:2 ║

║ □ Stop Loss placed at logical structure level ║

║ □ Position size calculated correctly ║

║ □ Not during major news event (checked economic calendar) ║

║ ║

║ Entry Price: _______________ ║

║ Stop Loss: _______________ ║

║ Risk Per Unit: _______________ ║

║ Position Size: _______________ ║

║ TP1 (1R): _______________ ║

║ TP2 (2R): _______________ ║

║ TP3 (3R): _______________ ║

║ ║

║ ═══════════════════════════════════════════════════════════════ ║

║ SECTION F: FINAL CONFIRMATION ║

║ ═══════════════════════════════════════════════════════════════ ║

║ ║

║ □ Wait for candle CLOSE (don't enter mid-candle) ║

║ □ Check spread/slippage acceptable ║

║ □ Trade noted in journal before entering ║

║ ║

║ ════════════════════════════════════════════════════════════ ║

║ MINIMUM REQUIREMENTS: ║

║ • Section A: 4/4 timeframes aligned ║

║ • Section B: 4/4 volume checks passed ║

║ • Section C: 3/3 candle checks passed ║

║ • Section D: 1+ entry signal confirmed ║

║ • Section E: 5/5 risk checks passed ║

║ • Section F: All final checks done ║

║ ║

║ TOTAL: 17+ checks must be YES to execute ║

║ ════════════════════════════════════════════════════════════ ║

║ ║

║ ════════════════════════════ ║

║ ✅ EXECUTE TRADE ║

║ ════════════════════════════ ║

║ ║

╚════════════════════════════════════════════════════════════════════╝

Quick Decision Flowchart-

┌─────────────────┐

│ POTENTIAL │

│ TRADE SPOTTED │

└────────┬────────┘

│

▼

┌──────────────────────────┐

│ Is 4H trend in your │

│ trade direction? │

└──────────────┬───────────┘

│ │

YES NO

│ │

▼ ▼

┌──────────────┐ ┌─────────────┐

│ Check 1H │ │ NO TRADE │

│ alignment │ │ ─────── │

└──────┬───────┘ └─────────────┘

│

ALIGNED?

│ │

YES NO → NO TRADE

│

▼

┌───────────────────┐

│ Is 30M showing │

│ LOW VOLUME │

│ pullback/rally? │

└─────────┬─────────┘

│

YES │ NO

│ │

│ ▼

│ ┌────────────┐

│ │ WAIT │

│ │ for setup │

│ └────────────┘

│

▼

┌───────────────────┐

│ VSA Signal on │

│ 15M Chart? │

│ (Candle CLOSED?) │

└─────────┬─────────┘

│

YES │ NO → WAIT

│

▼

┌───────────────────┐

│ R:R at least 1:2? │

└─────────┬─────────┘

│

YES │ NO → NO TRADE

│

▼

┌───────────────────┐

│ Risk ≤ 2% of │

│ account? │

└─────────┬─────────┘

│

YES │ NO → REDUCE SIZE

│

▼

┌───────────────────┐

│ Major news │

│ within 30 min? │

└─────────┬─────────┘

│

NO │ YES → WAIT

│

▼

╔═════════════════════╗

║ EXECUTE TRADE ║

║ ═══════════════ ║

║ • Set Entry ║

║ • Set Stop Loss ║

║ • Set Targets ║

║ • Log in Journal ║

╚═════════════════════╝

PART 10: COMMON MISTAKES & QUICK REFERENCE

Top 10 VSA Mistakes to Avoid-

╔════════════════════════════════════════════════════════════╗

║ TOP 10 VSA MISTAKES ║

╠════════════════════════════════════════════════════════════╣

║ ║

║ 1. ❌ Analyzing volume in ISOLATION ║

║ ✅ Always combine volume + price + location + context ║

║ ║

║ 2. ❌ Entering on HIGH volume pullback ║

║ ✅ Only enter on LOW volume pullback (Test) ║

║ ║

║ 3. ❌ Ignoring the CLOSE position of candle ║

║ ✅ Where it closes matters as much as volume ║

║ ║

║ 4. ❌ Trading VSA signals against higher TF trend ║

║ ✅ Always align with 4H/1H direction first ║

║ ║

║ 5. ❌ Chasing breakouts without volume confirmation ║

║ ✅ Wait for high volume OR don't enter ║

║ ║

║ 6. ❌ Entering during NEWS events ║

║ ✅ Volume is distorted during news - wait 30min ║

║ ║

║ 7. ❌ Misreading climax volume as continuation ║

║ ✅ Recognize climax = potential reversal ║

║ ║

║ 8. ❌ Not waiting for TEST confirmation ║

║ ✅ Wait for Spring/Upthrust to be TESTED (low volume) ║

║ ║

║ 9. ❌ Ignoring spread (candle range) ║

║ ✅ Wide spread + Low volume = FAKE MOVE warning ║

║ ║

║ 10. ❌ Not using relative volume ║

║ ✅ Compare to 20-period volume MA ║

║ ║

╚════════════════════════════════════════════════════════════╝

Critical Rules - Never Break These-

╔═══════════════════════════════════════════════════════════════╗

║ NEVER BREAK THESE RULES ║

╠═══════════════════════════════════════════════════════════════╣

║ ║

║ 1. NEVER enter without volume confirmation ║

║ ║

║ 2. NEVER trade against the higher timeframe trend ║

║ ║

║ 3. NEVER chase breakouts with low volume ║

║ ║

║ 4. ALWAYS wait for the TEST after accumulation/distribution ║

║ ║

║ 5. ALWAYS use stop loss - no exceptions ║

║ ║

║ 6. ALWAYS confirm 4H → 1H → 30M → 15M alignment ║

║ ║

║ 7. ALWAYS wait for candle CLOSE before entering ║

║ ║

║ 8. When Volume and Price DIVERGE → Expect REVERSAL ║

║ ║

║ 9. High Volume + Small Candle = Smart Money Activity ║

║ ║

║ 10. Low Volume on Pullback = Healthy Trend (entry zone) ║

║ ║

║ 11. High Volume on Pullback = Warning Sign (don't enter) ║

║ ║

║ 12. NEVER risk more than 2% on any single trade ║

║ ║

╚═══════════════════════════════════════════════════════════════╝

PART 11: TRADE JOURNAL TEMPLATE

Trade Journal Entry--

╔════════════════════════════════════════════════════════════════════╗

║ TRADE JOURNAL ║

╠════════════════════════════════════════════════════════════════════╣

║ ║

║ TRADE #: _____ DATE: ___________ TIME: ___________ ║

║ ║

║ PAIR/ASSET: _______________ DIRECTION: □ LONG □ SHORT ║

║ ║

║ ═══════════════════════════════════════════════════════════════ ║

║ PRE-TRADE ANALYSIS ║

║ ═══════════════════════════════════════════════════════════════ ║

║ ║

║ TIMEFRAME ALIGNMENT: ║

║ 4H: _____________________________________________ ║

║ 1H: _____________________________________________ ║

║ 30M: ____________________________________________ ║

║ 15M: ____________________________________________ ║

║ ║

║ VSA SETUP TYPE: ________________________________ ║

║ ║

║ VOLUME OBSERVATION: ____________________________ ║

║ _________________________________________________ ║

║ ║

║ CANDLE/SPREAD NOTES: ___________________________ ║

║ _________________________________________________ ║

║ ║

║ ═══════════════════════════════════════════════════════════════ ║

║ TRADE PARAMETERS ║

║ ═══════════════════════════════════════════════════════════════ ║

║ ║

║ Entry Price: _______________ ║

║ Stop Loss: _______________ ║

║ Position Size: _______________ ║

║ Risk Amount: $_____________ (____% of account) ║

║ ║

║ TP1: _______________ (1R) ║

║ TP2: _______________ (2R) ║

║ TP3: _______________ (3R) ║

║ ║

║ ═══════════════════════════════════════════════════════════════ ║

║ POST-TRADE ANALYSIS ║

║ ═══════════════════════════════════════════════════════════════ ║

║ ║

║ RESULT: □ WIN □ LOSS □ BREAKEVEN ║

║ ║

║ Exit Price: _______________ ║

║ P&L: $_____________ (____R) ║

║ ║

║ WHAT WENT WELL: ║

║ _________________________________________________ ║

║ _________________________________________________ ║

║ ║

║ WHAT COULD IMPROVE: ║

║ _________________________________________________ ║

║ _________________________________________________ ║

║ ║

║ DID I FOLLOW MY RULES? □ YES □ NO ║

║ If NO, which rule was broken? _____________________ ║

║ ║

║ SCREENSHOT SAVED: □ YES ║

║ ║

║ LESSONS LEARNED: ║

║ _________________________________________________ ║

║ _________________________________________________ ║

║ _________________________________________________ ║

║ ║

╚════════════════════════════════════════════════════════════════════╝

Weekly Review Template-

╔════════════════════════════════════════════════════════════════════╗

║ WEEKLY REVIEW ║

╠════════════════════════════════════════════════════════════════════╣

║ ║

║ WEEK OF: _______________ ║

║ ║

║ STATISTICS: ║

║ ─────────── ║

║ Total Trades: _____ ║

║ Wins: _____ (____%) ║

║ Losses: _____ (____%) ║

║ Breakeven: _____ ║

║ Total R Gained/Lost: _____R ║

║ P&L: $_____ ║

║ ║

║ BEST TRADE THIS WEEK: ║

║ Setup: ______________ R Gained: _____R ║

║ Why it worked: ____________________________________ ║

║ ║

║ WORST TRADE THIS WEEK: ║

║ Setup: ______________ R Lost: _____R ║

║ Why it failed: ____________________________________ ║

║ ║

║ RULES FOLLOWED: _____% ║

║ RULES BROKEN: _____% ║

║ ║

║ PATTERNS NOTICED: ║

║ _________________________________________________ ║

║ _________________________________________________ ║

║ ║

║ GOALS FOR NEXT WEEK: ║

║ 1. _______________________________________________ ║

║ 2. _______________________________________________ ║

║ 3. _______________________________________________ ║

║ ║

╚════════════════════════════════════════════════════════════════════╝

FINAL SUMMARY

╔════════════════════════════════════════════════════════════════╗

║ THE VSA TRADING PROCESS ║

╠════════════════════════════════════════════════════════════════╣

║ ║

║ 1. SCAN for volume anomalies on charts ║

║ ║

║ 2. IDENTIFY the pattern (Test, Absorption, Spring, etc.) ║

║ ║

║ 3. CONFIRM across multiple timeframes (4H → 1H → 30M → 15M) ║

║ ║

║ 4. ANALYZE candle close position and spread ║

║ ║

║ 5. WAIT for trigger (don't anticipate, react to confirmation) ║

║ ║

║ 6. CALCULATE position size based on stop distance ║

║ ║

║ 7. EXECUTE with predefined entry, stop, and targets ║

║

Smart Money Flow Signals [QuantAlgo]🟢 Overview

The Smart Money Flow Signals indicator synthesizes significant volume-price dynamics through multi-component analysis to identify potential accumulation and distribution phases driven by substantial market participants. It combines Money Flow Index momentum, Chaikin Money Flow accumulation patterns, volume-weighted price momentum, and buying/selling pressure metrics into a unified composite oscillator that quantifies periods of concentrated capital movement, helping traders and investors identify conditions where significant volume participants may be actively positioning across multiple market conditions and timeframes.

🟢 How It Works

The indicator's core methodology lies in its weighted composite approach, where multiple volume-price components are calculated sequentially and then integrated to create a comprehensive significant flow activity signal.

First, the Money Flow Index (MFI) is calculated to measure buying and selling pressure by incorporating volume into price momentum analysis:

raw_money_flow = source * volume

positive_flow = source >= source ? raw_money_flow : 0

negative_flow = source < source ? raw_money_flow : 0

positive_money_flow = math.sum(positive_flow, mfi_period)

negative_money_flow = math.sum(negative_flow, mfi_period)

money_flow_index = 100 - 100 / (1 + positive_money_flow / negative_money_flow)

This creates an RSI-style momentum indicator that tracks whether money (price × volume) is flowing into or out of the asset, with values ranging from 0 to 100 where readings above 50 suggest buying pressure dominance.

Then, Chaikin Money Flow (CMF) is computed to evaluate accumulation and distribution by analyzing where prices close within each bar's range, weighted by volume:

money_flow_multiplier = high != low ? (close - low - (high - close)) / (high - low) : 0

money_flow_volume = money_flow_multiplier * volume

volume_sma = ta.sma(volume, trend_period)

chaikin_money_flow = volume_sma != 0 ? ta.sma(money_flow_volume, trend_period) / volume_sma : 0

Positive CMF values indicate accumulation (closes near the high of the range), while negative values indicate distribution (closes near the low of the range), with volume weighting emphasizing periods of significant participation.

Next, Volume Analysis is performed to quantify current volume intensity relative to historical averages:

volume_average = ta.sma(volume, trend_period)

volume_strength = volume_average != 0 ? volume / volume_average : 1

volume_weight = math.log(volume_strength + 1)

The logarithmic transformation creates a volume weight that amplifies signals during high-volume periods while preventing extreme volume spikes from overwhelming the composite calculation.

Following this, Buy/Sell Pressure is quantified by comparing cumulative volume during bullish versus bearish candles:

buying_pressure = math.sum(volume * (close >= open ? 1 : 0), trend_period)

selling_pressure = math.sum(volume * (close < open ? 1 : 0), trend_period)

pressure_ratio = (buying_pressure - selling_pressure) / (buying_pressure + selling_pressure) * 100

This creates a directional pressure ratio that reveals whether significant participants are predominantly buying or selling, expressed as a percentage between -100 (all selling) and +100 (all buying).

Then, Volume-Weighted Momentum is calculated through an exponential smoothing channel that adjusts price deviation based on volume intensity:

exponential_smooth_average = ta.ema(source, momentum_channel_period)

deviation = ta.ema(math.abs(source - exponential_smooth_average), momentum_channel_period)

channel_index = deviation != 0 ? (source - exponential_smooth_average) / (0.015 * deviation) * (1 + volume_weight * 0.5) : 0

This channel index measures how far price has deviated from its exponential average relative to typical deviation, with the volume weight multiplier (1 + volume_weight * 0.5) amplifying the signal when significant volume accompanies the price movement.

Finally, the Composite Wave is constructed by combining all components with specific weighting to create the final oscillator:

momentum_wave = ta.ema(channel_index, trend_period)

money_flow_wave = (money_flow_index - 50) * 1.2

chaikin_flow_wave = chaikin_money_flow * 100

composite_wave = momentum_wave * 0.5 + chaikin_flow_wave * 0.3 + money_flow_wave * 0.2

smoothed_wave = ta.sma(composite_wave, signal_smoothing)

This creates a multi-dimensional volume flow oscillator that combines price-volume momentum, accumulation-distribution patterns, and buying-selling pressure into a single signal, providing traders with probabilistic insights into periods of concentrated market activity and directional bias based on weighted component convergence.

🟢 Signal Interpretation

▶ Positive Values (Above Zero, Green): Composite money flow above equilibrium indicating net accumulation pressure, positive buying volume dominance, and bullish volume-price alignment = Favorable conditions for long positions, significant capital flowing into the asset = Buy/hold opportunities

▶ Negative Values (Below Zero, Red): Composite money flow below equilibrium indicating net distribution pressure, negative selling volume dominance, and bearish volume-price alignment = Unfavorable conditions for long positions, significant capital flowing out of the asset = Sell/short opportunities

▶ Extreme Overbought Zone: Excessive bullish money flow indicating potential accumulation exhaustion, where buying pressure may have reached unsustainable levels with elevated reversal risk = Caution on new longs, potential distribution phase beginning, profit-taking zone for existing positions

▶ Extreme Oversold Zone: Excessive bearish money flow indicating potential distribution exhaustion, where selling pressure may have reached unsustainable levels with elevated reversal risk = Caution on new shorts, potential accumulation phase beginning, buying opportunity zone for contrarian entries

▶ Smoothed Trend Line (White) Alignment: When the smoothed trend line confirms the composite wave direction, it validates the underlying volume-price trend and filters false signals caused by short-term noise

▶ Volume Intensity Correlation: Gradient intensity (color saturation) reflects combined wave strength, volume participation, and directional alignment, where darker/more saturated colors indicate stronger concentrated activity and higher-probability directional moves

🟢 Features

▶ Preconfigured Presets: Three optimized parameter configurations accommodate different trading styles, timeframes, and market analysis approaches.

1. "Default" provides balanced volume flow measurement suitable for swing trading on 4-hour and daily charts, offering moderate responsiveness to money flow shifts with standard RSI-equivalent MFI period and moderate smoothing for most market conditions.

2. "Fast Response" delivers heightened sensitivity optimized for active intraday trading and scalping on 1-minute to 1-hour charts, using compressed calculation periods across all components and minimal smoothing to capture rapid volume flow changes and quick trend shifts as they develop, ideal for early entry/exit opportunities with acceptance of increased signal frequency during consolidation.

3. "Smooth Trend" offers conservative extreme identification ideal for position trading and long-term analysis on daily to weekly charts, employing extended periods across all money flow components with substantial smoothing to filter short-term noise and isolate only strong, sustained accumulation and distribution phases driven by significant volume participants.

▶ Built-in Alerts: Seven alert conditions enable comprehensive automated monitoring of significant money flow transitions and extreme market states.

1. "Bullish Flow" triggers when the composite wave crosses above zero, signaling the shift from distribution to accumulation and concentrated buying activity beginning.

2. "Bearish Flow" activates when the composite wave crosses below zero, signaling the shift from accumulation to distribution and concentrated selling activity starting.

3. "Any Flow Direction Change" provides a combined notification for either bullish or bearish crossover regardless of direction, useful for general money flow momentum shifts.

4. "Extreme Overbought" alerts when the composite wave reaches or exceeds the overbought threshold (default +60), indicating excessive buying pressure and potential exhaustion.

5. "Extreme Oversold" notifies when the composite wave reaches or falls below the oversold threshold (default -60), indicating excessive selling pressure and potential capitulation.

6. "Overbought Reversal" triggers specifically when the wave crosses back down through the overbought level after being extended, signaling the beginning of distribution from extreme levels.

7. "Oversold Reversal" activates when the wave crosses back up through the oversold level after being extended, signaling the beginning of accumulation from extreme levels.

▶ Color Customization: Six visual themes (Classic, Aqua, Cosmic, Ember, Neon, plus Custom) accommodate different chart backgrounds and visual preferences, ensuring optimal contrast and immediate identification of bullish versus bearish volume flow conditions across various devices and screen sizes. Optional bar coloring provides instant visual context of current significant volume activity intensity and direction without switching between the price pane and indicator pane, enabling traders and investors to immediately assess volume-price positioning dynamics while analyzing price action.

Adaptive Market Wave TheoryAdaptive Market Wave Theory

🌊 CORE INNOVATION: PROBABILISTIC PHASE DETECTION WITH MULTI-AGENT CONSENSUS

Adaptive Market Wave Theory (AMWT) represents a fundamental paradigm shift in how traders approach market phase identification. Rather than counting waves subjectively or drawing static breakout levels, AMWT treats the market as a hidden state machine —using Hidden Markov Models, multi-agent consensus systems, and reinforcement learning algorithms to quantify what traditional methods leave to interpretation.

The Wave Analysis Problem:

Traditional wave counting methodologies (Elliott Wave, harmonic patterns, ABC corrections) share fatal weaknesses that AMWT directly addresses:

1. Non-Falsifiability : Invalid wave counts can always be "recounted" or "adjusted." If your Wave 3 fails, it becomes "Wave 3 of a larger degree" or "actually Wave C." There's no objective failure condition.

2. Observer Bias : Two expert wave analysts examining the same chart routinely reach different conclusions. This isn't a feature—it's a fundamental methodology flaw.

3. No Confidence Measure : Traditional analysis says "This IS Wave 3." But with what probability? 51%? 95%? The binary nature prevents proper position sizing and risk management.

4. Static Rules : Fixed Fibonacci ratios and wave guidelines cannot adapt to changing market regimes. What worked in 2019 may fail in 2024.

5. No Accountability : Wave methodologies rarely track their own performance. There's no feedback loop to improve.

The AMWT Solution:

AMWT addresses each limitation through rigorous mathematical frameworks borrowed from speech recognition, machine learning, and reinforcement learning:

• Non-Falsifiability → Hard Invalidation : Wave hypotheses die permanently when price violates calculated invalidation levels. No recounting allowed.

• Observer Bias → Multi-Agent Consensus : Three independent analytical agents must agree. Single-methodology bias is eliminated.

• No Confidence → Probabilistic States : Every market state has a calculated probability from Hidden Markov Model inference. "72% probability of impulse state" replaces "This is Wave 3."

• Static Rules → Adaptive Learning : Thompson Sampling multi-armed bandits learn which agents perform best in current conditions. The system adapts in real-time.

• No Accountability → Performance Tracking : Comprehensive statistics track every signal's outcome. The system knows its own performance.

The Core Insight:

"Traditional wave analysis asks 'What count is this?' AMWT asks 'What is the probability we are in an impulsive state, with what confidence, confirmed by how many independent methodologies, and anchored to what liquidity event?'"

🔬 THEORETICAL FOUNDATION: HIDDEN MARKOV MODELS

Why Hidden Markov Models?

Markets exist in hidden states that we cannot directly observe—only their effects on price are visible. When the market is in an "impulse up" state, we see rising prices, expanding volume, and trending indicators. But we don't observe the state itself—we infer it from observables.

This is precisely the problem Hidden Markov Models (HMMs) solve. Originally developed for speech recognition (inferring words from sound waves), HMMs excel at estimating hidden states from noisy observations.

HMM Components:

1. Hidden States (S) : The unobservable market conditions

2. Observations (O) : What we can measure (price, volume, indicators)

3. Transition Matrix (A) : Probability of moving between states

4. Emission Matrix (B) : Probability of observations given each state