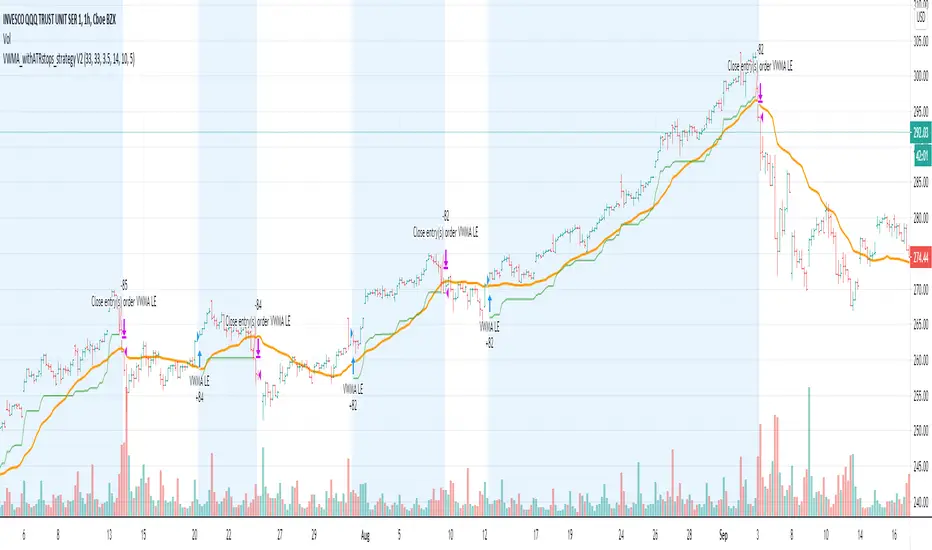

Trend #4 - ATR+EMA channelOverview:

This strategy use ATR to take-profit, Red-EMA to stop-loss, Blue-EMA channel to judgment breakout.

This strategy use commission setting is 0.05%, slippage setting is 2 ticks, you can set the appropriate value size in the properties page.

What it does:

This strategy detects when a trend is emerging and buy or sell.

How it does it:

When the price breaks through the blue EMA channel, the trend is judged to be strong in the short term, strategy generates a buy or sell order.

After buying or selling,, if the price moves in the expected direction, uses ATR to determine the appropriate spread to take profit, otherwise use red EMA for stop loss.

How to use it:

Start Date and Stop Date - This parameter adjusts the time range used by the strategy.

Stoploss - This parameter adjusts the stop loss amount after each order is placed.

Blue EMA length - This parameter adjusts the length of the channel.

Blue EMA multy - This parameter adjusts the width of the top and bottom of the channel.

ATR Period - This parameter adjusts the number of candles used by the ATR.

ATR mult - This parameter adjusts the upper and lower widths of the ATR. Lowering this parameter can improve the win rate, but not necessarily the profitability.

Red EMA length - This parameter adjusts the number of candles used by the red EMA .

Long - This switch is used to turn Long position on or off.

Short - This switch is used to turn short position on or off.

Pine Script®策略