Timeshifter Triple Timeframe Strategy w/ SessionsOverview

The "Enhanced Timeshifter Triple Timeframe Strategy with Session Filtering" is a sophisticated trading strategy designed for the TradingView platform. It integrates multiple technical indicators across three different timeframes and allows traders to customize their trading Sessions. This strategy is ideal for traders who wish to leverage multi-timeframe analysis and session-based trading to enhance their trading decisions.

Features

Multi-Timeframe Analysis and direction:

Higher Timeframe: Set to a daily timeframe by default, providing a broader view of market trends.

Trading Timeframe: Automatically set to the current chart timeframe, ensuring alignment with the trader's primary analysis period.

Lower Timeframe: Set to a 15-minute timeframe by default, offering a granular view for precise entry and exit points.

Indicator Selection:

RMI (Relative Momentum Index): Combines RSI and MFI to gauge market momentum.

TWAP (Time Weighted Average Price): Provides an average price over a specified period, useful for identifying trends.

TEMA (Triple Exponential Moving Average): Reduces lag and smooths price data for trend identification.

DEMA (Double Exponential Moving Average): Similar to TEMA, it reduces lag and provides a smoother trend line.

MA (Moving Average): A simple moving average for basic trend analysis.

MFI (Money Flow Index): Measures the flow of money into and out of a security, useful for identifying overbought or oversold conditions.

VWMA (Volume Weighted Moving Average): Incorporates volume data into the moving average calculation.

PSAR (Parabolic SAR): Identifies potential reversals in price movement.

Session Filtering:

London Session: Trade during the London market hours (0800-1700 GMT+1).

New York Session: Trade during the New York market hours (0800-1700 GMT-5).

Tokyo Session: Trade during the Tokyo market hours (0900-1800 GMT+9).

Users can select one or multiple sessions to align trading with specific market hours.

Trade Direction:

Long: Only long trades are permitted.

Short: Only short trades are permitted.

Both: Both long and short trades are permitted, providing flexibility based on market conditions.

ADX Confirmation:

ADX (Average Directional Index): An optional filter to confirm the strength of a trend before entering a trade.

How to Use the Script

Setup:

Add the script to your TradingView chart.

Customize the input parameters according to your trading preferences and strategy requirements.

Indicator Selection:

Choose the primary indicator you wish to use for generating trading signals from the dropdown menu.

Enable or disable the ADX confirmation based on your preference for trend strength analysis.

Session Filtering:

Select the trading sessions you wish to trade in. You can choose one or multiple Sessions based on your trading strategy and market focus.

Trade Direction:

Set your preferred trade direction (Long, Short, or Both) to align with your market outlook and risk tolerance. You can use this feature to gauge the market and understand the possible directions.

Tips for Profitable and Safe Trading:

Recommended Timeframes Combination:

LT: 1m , CT: 5m, HT: 1H

LT: 1-5m , CT: 15m, HT: 4H

LT: 5-15m , CT: 4H, HT: 1W

Backtesting:

Always backtest the strategy on historical data to understand its performance under various market conditions.

Adjust the parameters based on backtesting results to optimize the strategy for your specific trading style.

Risk Management:

Use appropriate risk management techniques, such as setting stop-loss and take-profit levels, to protect your capital.

Avoid over-leveraging and ensure that you are trading within your risk tolerance.

Market Analysis:

Combine the script with other forms of market analysis, such as fundamental analysis or market sentiment, to make well-rounded trading decisions.

Stay informed about major economic events and news that could impact market volatility and trading sessions.

Continuous Monitoring:

Regularly monitor the strategy's performance and make adjustments as necessary.

Keep an eye on the results and settings for real-time statistics and ensure that the strategy aligns with current market conditions.

Education and Practice:

Continuously educate yourself on trading strategies and market dynamics.

Practice using the strategy in a demo account before applying it to live trading to gain confidence and understanding.

在腳本中搜尋"backtest"

Anomaly Counter-Trend StrategyA mean-reversion style strategy that automatically spots unusually large price moves over a configurable lookback period and takes the opposite side, with full risk-management, commission and slippage modeling—built in Pine Script® v6.

🔎 Overview

ACTS monitors the percent-change over the past N minutes and, when that move exceeds your chosen threshold, enters a counter-trend position (short on a strong rise; long on a sharp fall). It’s ideal for markets that often “overshoot” and snap back, and can be applied on any symbol or timeframe.

⚙️ Key Features

Anomaly Detection: Detect abnormal price swings based on a user-defined % change over a lookback period.

Counter-Trend Entries: Auto-enter short on rise anomalies, long on fall anomalies (with seamless flat↔reverse transitions).

Risk Management: Configurable stop-loss and take-profit in ticks per trade.

Realistic Modeling: Simulates commissions (0.05 % default), slippage (2 ticks), and percent-of-equity sizing.

Immediate Bar-Close Execution: Orders processed on bar close for faster fills.

Visual Aids: Optional on-chart BUY/SELL triangles and background highlights during anomaly periods.

⚙️ Inputs

Input Default Description

Percentage Threshold (%) 2.00 Min % move over lookback to trigger an anomaly.

Lookback Period (Minutes) 15 Number of minutes over which to measure change.

Stop Loss (Ticks) 100 Distance from entry for stop-loss exit.

Take Profit (Ticks) 200 Distance from entry for take-profit exit.

Plot Trade Signal Shapes (on/off) true Show BUY/SELL triangles on chart.

Highlight Anomaly Background true Shade background during anomaly bars.

📊 How to Use

Add to Chart: Apply the script to any ticker & timeframe.

Tune: Adjust your percentage threshold and lookback to match each instrument’s volatility.

Review Backtest: Check built-in strategy performance (drawdown, Sharpe, etc.) under the Strategy Tester tab.

Go Live: Once optimized, link to alerts or your trade execution system.

⚠️ Disclaimer

This script is provided “as-is” for educational purposes and backtesting only. Past performance does not guarantee future results. Always backtest thoroughly, manage your own risk, and consider market conditions before live trading.

Enjoy experimenting—and may your counter-trend entries catch the next big snapback!

Supertrend + MACD CrossoverKey Elements of the Template:

Supertrend Settings:

supertrendFactor: Adjustable to control the sensitivity of the Supertrend.

supertrendATRLength: ATR length used for Supertrend calculation.

MACD Settings:

macdFastLength, macdSlowLength, macdSignalSmoothing: These settings allow you to fine-tune the MACD for better results.

Risk Management:

Stop-Loss: The stop-loss is based on the ATR (Average True Range), a volatility-based indicator.

Take-Profit: The take-profit is based on the risk-reward ratio (set to 3x by default).

Both stop-loss and take-profit are dynamic, based on ATR, which adjusts according to market volatility.

Buy and Sell Signals:

Buy Signal: Supertrend is bullish, and MACD line crosses above the Signal line.

Sell Signal: Supertrend is bearish, and MACD line crosses below the Signal line.

Visual Elements:

The Supertrend line is plotted in green (bullish) and red (bearish).

Buy and Sell signals are shown with green and red triangles on the chart.

Next Steps for Optimization:

Backtesting:

Run backtests on BTC in the 5-minute timeframe and adjust parameters (Supertrend factor, MACD settings, risk-reward ratio) to find the optimal configuration for the 60% win ratio.

Fine-Tuning Parameters:

Adjust supertrendFactor and macdFastLength to find more optimal values based on BTC's market behavior.

Tweak the risk-reward ratio to maximize profitability while maintaining a good win ratio.

Evaluate Market Conditions:

The performance of the strategy can vary based on market volatility. It may be helpful to evaluate performance in different market conditions or pair it with a filter like RSI or volume.

Let me know if you'd like further tweaks or explanations!

[TehThomas] - Displacement CandlesOverview:

This PineScript is designed to detect and visualize significant price movements, called displacements, on a trading chart. It's particularly useful for traders who want to identify potential trend changes or strong market sentiment quickly.

How the Script Works

User Input:

The script allows users to set a custom threshold for displacement detection and choose colors for bullish and bearish movements.

Displacement Detection Function:

isDisplacement(series, threshold) =>

percentage_change = math.abs(series - series ) / series * 100

percentage_change > threshold

This function calculates the percentage change between the current and previous price.

If the change exceeds the set threshold, it's considered a displacement.

Bullish and Bearish Detection:

bullish_displacement = isDisplacement(close, threshold) and close > close

bearish_displacement = isDisplacement(close, threshold) and close < close

Identifies whether the displacement is bullish (price increase) or bearish (price decrease).

Candle Coloring:

barcolor(bullish_displacement ? bullish_color : bearish_displacement ? bearish_color : na)

Changes the color of candles based on the detected displacement type.

Usefulness and Applications:

Trend Identification: Helps in quickly spotting potential trend changes or continuations.

Volatility Analysis: Provides a visual representation of market volatility.

Entry and Exit Signals: Can be used to identify potential entry or exit points for trades.

Market Sentiment: Offers insights into the strength of bullish or bearish sentiment.

Customizable Sensitivity: The adjustable threshold allows traders to fine-tune the indicator based on the asset's typical volatility.

Visual Clarity: By changing candle colors, it provides a clear, at-a-glance view of significant price movements.

Complementary Tool: Can be used alongside other technical indicators for confirmation of signals.

Multiple Timeframe Analysis: Applicable across different timeframes to suit various trading styles (day trading, swing trading, etc.).

Educational Purpose: Helps new traders understand and visualize significant price movements in the market.

Backtesting: Can be incorporated into strategy backtests to assess its effectiveness in different market conditions.

This script is particularly handy for traders who want to cut through market noise and focus on significant price movements. It's versatile enough to be used across different trading strategies and can be a valuable addition to a trader's technical analysis toolkit.

It's a very easy script and not alot to mention. If you see any improvements please let me know.

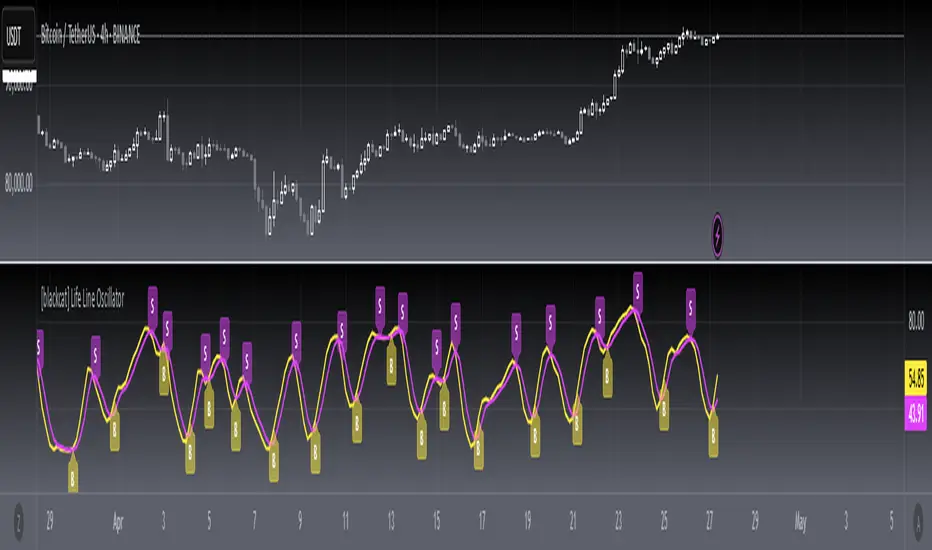

[blackcat] L1 Main life line oscillator█ OVERVIEW

The Pine Script provided is an indicator named " L1 Main life line oscillator." Its primary function is to calculate and plot two oscillators: the Main Force and the Life Line. These oscillators are derived from smoothed price data, and the script also detects and labels crossovers and crossunders between the two lines, which can be used to generate buy and sell signals.

█ FEATURES

Key Features:

• Input Parameters: Users can define the period (n) and the weight for the oscillators.

• Custom Function: A function calculate_life_line_oscillator is defined to compute the Main Force and Life Line oscillators.

• Advanced Calculations: The script uses an adaptive moving average (ALMA) and exponential moving average (EMA) to smooth the price data and calculate the oscillators.

• Crossover and Crossunder Detection: Built-in functions ta.crossover and ta.crossunder are used to identify signal points.

• Label Drawing: Custom labels are drawn on the chart to indicate buy ("B") and sell ("S") signals.

█ HOW TO USE

1 — Configure Input Parameters: Adjust the period (n) and weight to suit your trading strategy.

2 — Interpret the Oscillators: Observe the Main Force and Life Line on the chart.

3 — Act on Signals: Look for crossovers and crossunders to generate buy and sell signals. Buy signals are indicated by the label "B" and sell signals by "S".

█ LIMITATIONS

• Lag in Signals: While the use of ALMA and EMA reduces lag, some delay may still occur, especially in volatile markets.

• False Signals: Crossovers and crossunders can sometimes produce false signals, so it is advisable to use this indicator in conjunction with other tools for confirmation.

█ NOTES

Advanced Pine Script Features:

• Adaptive Moving Average (ALMA): Provides a more responsive and adaptive oscillator.

• Exponential Moving Average (EMA): Smooths the price range and Main Force values.

• Crossover and Crossunder Detection: Utilizes built-in functions for signal identification.

• Label Drawing: Enhances visual signaling with custom labels.

Optimization Techniques:

• The use of ALMA and EMA helps in reducing lag and improving the responsiveness of the oscillators.

• The custom function encapsulates complex calculations, making the main script cleaner and more maintainable.

Unique Approaches:

• The combination of ALMA and EMA to create the Main Force oscillator provides a unique smoothing method.

• The Life Line is calculated using a weighted average of the previous and current Main Force values, adding an additional layer of smoothing and responsiveness.

█ THANKS

Thank you for using the " L1 Main life line oscillator." If you have any questions or suggestions, please feel free to reach out in the comments or on the TradingView or my Discord channel.

█ EXTENDED KNOWLEDGE AND APPLICATIONS

Potential Modifications:

• Additional Indicators: Extend the script to include other technical indicators (e.g., RSI, MACD) for a more comprehensive trading signal system.

• Customizable Colors and Styles: Allow users to customize the colors and styles of the plotted lines and labels.

• Alerts: Implement alerts for crossovers and crossunders to notify users in real-time.

Application Scenarios:

• Intraday Trading: The responsiveness of the oscillators makes this script suitable for intraday trading, where quick buy and sell signals are crucial.

• Long-Term Analysis: By adjusting the period n, the script can be used for long-term trend analysis and strategic trades.

• Backtesting: The script can be modified into a strategy to backtest the performance of the oscillator-based signals against historical data.

Related Pine Script Concepts:

• Strategy Development: Understanding how to convert indicators into strategies for backtesting and live trading.

• Advanced Plotting: Exploring more advanced plotting techniques, such as using different styles and customizing plot appearances.

• Signal Validation: Techniques for validating and filtering signals to reduce false positives and improve trade accuracy.

Equilibrium Candles + Pattern [Honestcowboy]The Equilibrium Candles is a very simple trend continuation or reversal strategy depending on your settings.

How an Equilibrium Candle is created:

We calculate the equilibrium by measuring the mid point between highest and lowest point over X amount of bars back.

This now is the opening price for each bar and will be considered a green bar if price closes above equilibrium.

Bars get shaded by checking if regular candle close is higher than open etc. So you still see what the normal candles are doing.

Why are they useful?

The equilibrium is calculated the same as Baseline in Ichimoku Cloud. Which provides a point where price is very likely to retrace to. This script visualises the distance between close and equilibrium using candles. To provide a clear visual of how price relates to this equilibrium point.

This also makes it more straightforward to develop strategies based on this simple concept and makes the trader purely focus on this relationship and not think of any Ichimoku Cloud theories.

Script uses a very simple pattern to enter trades:

It will count how many candles have been one directional (above or below equilibrium)

Based on user input after X candles (7 by default) script shows we are in a trend (bg colors)

On the first pullback (candle closes on other side of equilibrium) it will look to enter a trade.

Places a stop order at the high of the candle if bullish trend or reverse if bearish trend.

If based on user input after X opposite candles (2 by default) order is not filled will cancel it and look for a new trend.

Use Reverse Logic:

There is a use reverse logic in the settings which on default is turned on. It will turn long orders into short orders making the stop orders become limit orders. It will use the normal long SL as target for the short. And TP as stop for the short. This to provide a means to reverse equity curve in case your pair is mean reverting by nature instead of trending.

ATR Calculation:

Averaged ATR, which is using ta.percentile_nearest_rank of 60% of a normal ATR (14 period) over the last 200 bars. This in simple words finds a value slightly above the mean ATR value over that period.

Big Candle Exit Logic:

Using Averaged ATR the script will check if a candle closes X times that ATR from the equilibrium point. This is then considered an overextension and all trades are closed.

This is also based on user input.

Simple trade management logic:

Checks if the user has selected to use TP and SL, or/and big candle exit.

Places a TP and SL based on averaged ATR at a multiplier based on user Input.

Closes trade if there is a Big Candle Exit or an opposite direction signal from indicator.

Script can be fully automated to MT5

There are risk settings in % and symbol settings provided at the bottom of the indicator. The script will send alert to MT5 broker trying to mimic the execution that happens on tradingview. There are always delays when using a bridge to MT5 broker and there could be errors so be mindful of that. This script sends alerts in format so they can be read by tradingview.to which is a bridge between the platforms.

Use the all alert function calls feature when setting up alerts and make sure you provide the right webhook if you want to use this approach.

There is also a simple buy and sell alert feature if you don't want to fully automate but still get alerts. These are available in the dropdown when creating an alert.

Almost every setting in this indicator has a tooltip added to it. So if any setting is not clear hover over the (?) icon on the right of the setting.

The backtest uses a 4% exposure per trade and a 10 point slippage. I did not include a commission cause I'm not personaly aware what the commissions are on most forex brokers. I'm only aware of minimal slippage to use in a backtest. Trading conditions vary per broker you use so always pay close attention to trading costs on your own broker. Use a full automation at your own risk and discretion and do proper backtesting.

TradingView.To Strategy Template (with Dyanmic Alerts)Hello traders,

If you're tired of manual trading and looking for a solid strategy template to pair with your indicators, look no further.

This Pine Script v5 strategy template is engineered for maximum customization and risk management.

Best part?

This Pine Script v5 template facilitates the dynamic construction of TradingView.TO alerts, sparing users the time and effort of mastering the TradingView.TO syntax and manually create alert commands.

This powerful tool gives much power to those who don't know how to code in Pinescript and want to automate their indicators' signals via TradingView.TO bot.

IMPORTANT NOTES

TradingView.TO is a trading bot software that forwards TradingView alerts to your brokers (examples: Binance, Oanda, Coinbase, Bybit, Metatrader 4/5, ...) for automating trading.

Many traders don't know how to create TradingView.TO dynamically-compatible alerts using the data from their TradingView scripts.

Traders using trading bots want their alerts to reflect the stop-loss/take-profit/trailing-stop/stop-loss to break options from your script and then create the orders accordingly.

This script showcases how to create TradingView.TO alerts dynamically.

TRADINGVIEW ALERTS

1) You'll have to create one alert per asset X timeframe = 1 chart.

Example: 1 alert for BTC/USDT on the 5 minutes chart, 1 alert for BTC/USDT on the 15-minute chart (assuming you want your bot to trade the BTC/USDT on the 5 and 15-minute timeframes)

2) Select the Order fills and alert() function calls condition

3) For each alert, the alert message is pre-configured with the text below

{{strategy.order.alert_message}}

Please leave it as it is.

It's a TradingView native variable that will fetch the alert text messages built by the script.

4) TradingView.TO uses webhook technology - setting a webhook URL from the alerts notifications tab is required.

KEY FEATURES

I) Modular Indicator Connection

* plug your existing indicator into the template.

* Only two lines of code are needed for full compatibility.

Step 1: Create your connector

Adapt your indicator with only 2 lines of code and then connect it to this strategy template.

To do so:

1) Find in your indicator where the conditions print the long/buy and short/sell signals.

2) Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator, whether a MACD , ZigZag, Pivots , higher-highs, lower-lows or whatever indicator with clear buy and sell conditions.

//@version=5

indicator("Supertrend", overlay = true, timeframe = "", timeframe_gaps = true)

atrPeriod = input.int(10, "ATR Length", minval = 1)

factor = input.float(3.0, "Factor", minval = 0.01, step = 0.01)

= ta.supertrend(factor, atrPeriod)

supertrend := barstate.isfirst ? na : supertrend

bodyMiddle = plot(barstate.isfirst ? na : (open + close) / 2, display = display.none)

upTrend = plot(direction < 0 ? supertrend : na, "Up Trend", color = color.green, style = plot.style_linebr)

downTrend = plot(direction < 0 ? na : supertrend, "Down Trend", color = color.red, style = plot.style_linebr)

fill(bodyMiddle, upTrend, color.new(color.green, 90), fillgaps = false)

fill(bodyMiddle, downTrend, color.new(color.red, 90), fillgaps = false)

buy = ta.crossunder(direction, 0)

sell = ta.crossunder(direction, 0)

//////// CONNECTOR SECTION ////////

Signal = buy ? 1 : sell ? -1 : 0

plot(Signal, title = "Signal", display = display.data_window)

//////// CONNECTOR SECTION ////////

Important Notes

🔥 The Strategy Template expects the value to be exactly 1 for the bullish signal and -1 for the bearish signal

Now, you can connect your indicator to the Strategy Template using the method below or that one.

Step 2: Connect the connector

1) Add your updated indicator to a TradingView chart

2) Add the Strategy Template as well to the SAME chart

3) Open the Strategy Template settings, and in the Data Source field, select your 🔌Connector🔌 (which comes from your indicator)

Note it doesn’t have to be named 🔌Connector🔌 - you can name it as you want - however, I recommend an explicit name you can easily remember.

From then, you should start seeing the signals and plenty of other stuff on your chart.

🔥 Note that whenever you update your indicator values, the strategy statistics and visuals on your chart will update in real-time

II) BOT Risk Management:

- Max Drawdown:

Mode: Select whether the max drawdown is calculated in percentage (%) or USD.

Value: If the max drawdown reaches this specified value, set a value to halt the bot.

- Max Consecutive Days:

Use Max Consecutive Days BOT Halt: Enable/Disable halting the bot if the max consecutive losing days value is reached.

- Max Consecutive Days: Set the maximum number of consecutive losing days allowed before halting the bot.

- Max Losing Streak:

Use Max Losing Streak: Enable/Disable a feature to prevent the bot from taking too many losses in a row.

- Max Losing Streak Length: Set the maximum length of a losing streak allowed.

Margin Call:

- Use Margin Call: Enable/Disable a feature to exit when a specified percentage away from a margin call to prevent it.

Margin Call (%): Set the percentage value to trigger this feature.

- Close BOT Total Loss:

Use Close BOT Total Loss: Enable/Disable a feature to close all trades and halt the bot if the total loss is reached.

- Total Loss ($): Set the total loss value in USD to trigger this feature.

Intraday BOT Risk Management:

- Intraday Losses:

Use Intraday Losses BOT Halt: Enable/Disable halting the bot on reaching specified intraday losses.

Mode: Select whether the intraday loss is calculated in percentage (%) or USD.

- Max Intraday Losses (%): Set the value for maximum intraday losses.

Limit Intraday Trades:

- Use Limit Intraday Trades: Enable/Disable a feature to limit the number of intraday trades.

- Max Intraday Trades: Set the maximum number of intraday trades allowed.

Restart Intraday EA:

III) Order Types and Position Sizing

- Choose between market or limit orders.

- Set your position size directly in the template.

Please use the position size from the “Inputs” and not the “Properties” tab.

I know it's redundant. - the template needs this value from the "Inputs" tab to build the alerts, and the Backtester needs it from the "Properties" tab.

IV) Advanced Take-Profit and Stop-Loss Options

- Choose to set your SL/TP in either USD or percentages.

- Option for multiple take-profit levels and trailing stop losses.

- Move your stop loss to break even +/- offset in USD for “risk-free” trades.

V) Miscellaneous:

Retry order openings if they fail.

Order Types:

Select and specify order type and price settings.

Position Size:

Define the type and size of positions.

Leverage:

Leverage settings, including margin type and hedge mode.

Session:

Limit trades to specific sessions.

Dates:

Limit trades to a specific date range.

Trades Direction:

Direction: Specify the market direction for opening positions.

VI) Logger

The TradingView.TO commands are logged in the TradingView logger.

You'll find more information about it in this TradingView blog post .

WHY YOU MIGHT NEED THIS TEMPLATE

1) Transform your indicator into a TradingView.TO trading bot more easily than before

Connect your indicator to the template

Create your alerts

Set your EA settings

2) Save Time

Auto-generated alert messages for TradingView.TO.

I tested them all and checked with the support team what could/couldn’t be done.

3) Be in Control

Manage your trading risks with advanced features.

4) Customizable

Fits various trading styles and asset classes.

REQUIREMENTS

* Make sure you have your TradingView.TO account

* If there is any issue with the template, ask me in the comments section - I’ll answer quickly.

BACKTEST RESULTS FROM THIS POST

1) I connected this strategy template to a dummy Supertrend script.

I could have selected any other indicator or concept for this script post.

I wanted to share an example of how you can quickly upgrade your strategy, making it compatible with TradingView.TO.

2) The backtest results aren't relevant for this educational script publication.

I used realistic backtesting data but didn't look too much into optimizing the results, as this isn't the point of why I'm publishing this script.

This strategy is a template to be connected to any indicator - the sky is the limit. :)

3) This template is made to take 1 trade per direction at any given time.

Pyramiding is set to 1 on TradingView.

The strategy default settings are:

* Initial Capital: 100000 USD

* Position Size: 1%

* Commission Percent: 0.075%

* Slippage: 1 tick

* No margin/leverage used

ProfitView Strategy TemplateHello traders,

This script took me a full week of coding/testing, sweat, and tears - and I’m too nice as I’m giving it for free to the community.

If you're tired of manual trading and looking for a solid strategy template to pair with your indicators, look no further.

This Pine Script v5 strategy template is engineered for maximum customization and risk management.

Best part?

This Pine Script v5 template facilitates the dynamic construction of ProfitView alerts, sparing users the time and effort of mastering the ProfitView syntax and manually creating alert commands.

This powerful tool gives much power to those who don't know how to code in Pinescript and want to automate their indicators' signals via the ProfitView Chrome extension.

IMPORTANT NOTES

ProfitView is a trading bot software that forwards TradingView alerts to your brokers (examples: Binance, Oanda, Coinbase, Bybit, etc.) for automating trading.

Many traders don't know how to dynamically create ProfitView-compatible alerts using the data from their TradingView scripts.

Traders using trading bots want their alerts to reflect the stop-loss/take-profit/trailing-stop/stop-loss to break options from your script and then create the orders accordingly.

This script showcases how to create ProfitView alerts dynamically.

TRADINGVIEW ALERTS

1) You'll have to create one alert per asset X timeframe = 1 chart.

Example: 1 alert for EUR/USD on the 5 minutes chart, 1 alert for EUR/USD on the 15-minute chart (assuming you want your bot to trade the EUR/USD on the 5 and 15-minute timeframes)

2) Select the Order fills and alert() function calls condition

3) For each alert, the alert message is pre-configured with the text below

{{strategy.order.alert_message}}

Please leave it as it is.

It's a TradingView native variable that will fetch the alert text messages built by the script.

4) ProfitView doesn't use webhook technology, so setting a webhook URL from the alerts notifications tab is unnecessary.

KEY FEATURES

I) Modular Indicator Connection

* plug your existing indicator into the template.

* Only two lines of code are needed for full compatibility.

Step 1: Create your connector

Adapt your indicator with only 2 lines of code and then connect it to this strategy template.

To do so:

1) Find in your indicator where the conditions print the long/buy and short/sell signals.

2) Create an additional plot as below

I'm giving an example with a Two moving averages cross.

Please replicate the same methodology for your indicator, whether a MACD , ZigZag, Pivots , higher-highs, lower-lows or whatever indicator with clear buy and sell conditions.

//@version=5

indicator("Supertrend", overlay = true, timeframe = "", timeframe_gaps = true)

atrPeriod = input.int(10, "ATR Length", minval = 1)

factor = input.float(3.0, "Factor", minval = 0.01, step = 0.01)

= ta.supertrend(factor, atrPeriod)

supertrend := barstate.isfirst ? na : supertrend

bodyMiddle = plot(barstate.isfirst ? na : (open + close) / 2, display = display.none)

upTrend = plot(direction < 0 ? supertrend : na, "Up Trend", color = color.green, style = plot.style_linebr)

downTrend = plot(direction < 0 ? na : supertrend, "Down Trend", color = color.red, style = plot.style_linebr)

fill(bodyMiddle, upTrend, color.new(color.green, 90), fillgaps = false)

fill(bodyMiddle, downTrend, color.new(color.red, 90), fillgaps = false)

buy = ta.crossunder(direction, 0)

sell = ta.crossunder(direction, 0)

//////// CONNECTOR SECTION ////////

Signal = buy ? 1 : sell ? -1 : 0

plot(Signal, title = "Signal", display = display.data_window)

//////// CONNECTOR SECTION ////////

Important Notes

🔥 The Strategy Template expects the value to be exactly 1 for the bullish signal and -1 for the bearish signal

Now, you can connect your indicator to the Strategy Template using the method below or that one.

Step 2: Connect the connector

1) Add your updated indicator to a TradingView chart

2) Add the Strategy Template as well to the SAME chart

3) Open the Strategy Template settings, and in the Data Source field, select your 🔌Connector🔌 (which comes from your indicator)

Note it doesn’t have to be named 🔌Connector🔌 - you can name it as you want - however, I recommend an explicit name you can easily remember.

From then, you should start seeing the signals and plenty of other stuff on your chart.

🔥 Note that whenever you update your indicator values, the strategy statistics and visuals on your chart will update in real-time

II) BOT Risk Management:

- Max Drawdown:

Mode: Select whether the max drawdown is calculated in percentage (%) or USD.

Value: If the max drawdown reaches this specified value, set a value to halt the bot.

- Max Consecutive Days:

Use Max Consecutive Days BOT Halt: Enable/Disable halting the bot if the max consecutive losing days value is reached.

- Max Consecutive Days: Set the maximum number of consecutive losing days allowed before halting the bot.

- Max Losing Streak:

Use Max Losing Streak: Enable/Disable a feature to prevent the bot from taking too many losses in a row.

- Max Losing Streak Length: Set the maximum length of a losing streak allowed.

Margin Call:

- Use Margin Call: Enable/Disable a feature to exit when a specified percentage away from a margin call to prevent it.

Margin Call (%): Set the percentage value to trigger this feature.

- Close BOT Total Loss:

Use Close BOT Total Loss: Enable/Disable a feature to close all trades and halt the bot if the total loss is reached.

- Total Loss ($): Set the total loss value in USD to trigger this feature.

Intraday BOT Risk Management:

- Intraday Losses:

Use Intraday Losses BOT Halt: Enable/Disable halting the bot on reaching specified intraday losses.

Mode: Select whether the intraday loss is calculated in percentage (%) or USD.

- Max Intraday Losses (%): Set the value for maximum intraday losses.

Limit Intraday Trades:

- Use Limit Intraday Trades: Enable/Disable a feature to limit the number of intraday trades.

- Max Intraday Trades: Set the maximum number of intraday trades allowed.

Restart Intraday EA:

- Use Restart Intraday EA: Enable/Disable a feature to restart the bot at the first bar of the next day if it has been stopped with an intraday risk management safeguard.

III) Order Types and Position Sizing

- Choose between market, limit, or stop orders.

- Set your position size directly in the template.

Please use the position size from the “Inputs” and not the “Properties” tab.

I know it's redundant. - the template needs this value from the "Inputs" tab to build the alerts, and the Backtester needs it from the "Properties" tab.

IV) Advanced Take-Profit and Stop-Loss Options

- Choose to set your SL/TP in either pips or percentages.

- Option for multiple take-profit levels and trailing stop losses.

- Move your stop loss to break even +/- offset in pips for “risk-free” trades.

V) Miscellaneous

Retry order openings if they fail.

Order Types:

Select and specify order type and price settings.

Position Size:

Define the type and size of positions.

Leverage:

Leverage settings, including margin type and hedge mode.

Session:

Limit trades to specific sessions.

Dates:

Limit trades to a specific date range.

Trades Direction:

Direction: Specify the market direction for opening positions.

VI) Notifications (Telegram/Discord/Email/IFTTT/Twilio/SMS)

Customize notifications sent to Telegram, Discord, Email, IFTTT, Twilio, and ProfitView Logger.

VII) Logger

The ProfitView commands are logged in the TradingView logger.

You'll find more information about it in this TradingView blog post .

WHY YOU MIGHT NEED THIS TEMPLATE

1) Transform your indicator into a ProfitView trading bot more easily than before

Connect your indicator to the template

Create your alerts

Set your EA settings

2) Save Time

Auto-generated alert messages for ProfitView.

I tested them all and checked with the support team what could/couldn’t be done.

3) Be in Control

Manage your trading risks with advanced features.

4) Customizable

Fits various trading styles and asset classes.

REQUIREMENTS

* Make sure you have your ProfitView account and do the settings correctly in your Chrome extension. If you don't know how to do it, read the documentation + ask for help in the ProfitView Discord support channel.

* If there is any issue with the template, ask me in the comments section - I’ll answer quickly.

BACKTEST RESULTS FROM THIS POST

1) I connected this strategy template to a dummy Supertrend script.

I could have selected any other indicator or concept for this script post.

I wanted to share an example of how you can quickly upgrade your strategy, making it compatible with ProfitView.

2) The backtest results aren't relevant for this educational script publication.

I used realistic backtesting data but didn't look too much into optimizing the results, as this isn't the point of why I'm publishing this script.

This strategy is a template to be connected to any indicator - the sky is the limit. :)

3) This template is made to take 1 trade per direction at any given time.

Pyramiding is set to 1 on TradingView.

The strategy default settings are:

* Initial Capital: 100000 USD

* Position Size: 1%

* Commission Percent: 0.075%

* Slippage: 1 tick

* No margin/leverage used

Best regards,

Dave

EMA bands + leledc + bollinger bands trend following strategy v2The basics:

In its simplest form, this strategy is a positional trend following strategy which enters long when price breaks out above "middle" EMA bands and closes or flips short when price breaks down below "middle" EMA bands. The top and bottom of the middle EMA bands are calculated from the EMA of candle highs and lows, respectively.

The idea is that entering trades on breakouts of the high EMAs and low EMAs rather than the typical EMA based on candle closes gives a bit more confirmation of trend strength and minimizes getting chopped up. To further reduce getting chopped up, the strategy defaults to close on crossing the opposite EMA band (ie. long on break above high EMA middle band and close below low EMA middle band).

This strategy works on all markets on all timeframes, but as a trend following strategy it works best on markets prone to trending such as crypto and tech stocks. On lower timeframes, longer EMAs tend to work best (I've found good results on EMA lengths even has high up to 1000), while 4H charts and above tend to work better with EMA lengths 21 and below.

As an added filter to confirm the trend, a second EMA can be used. Inputting a slower EMA filter can ensure trades are entered in accordance with longer term trends, inputting a faster EMA filter can act as confirmation of breakout strength.

Bar coloring can be enabled to quickly visually identify a trend's direction for confluence with other indicators or strategies.

The goods:

Waiting for the trend to flip before closing a trade (especially when a longer base EMA is used) often leaves money on the table. This script combines a number of ways to identify when a trend is exhausted for backtesting the best early exits.

"Delayed bars inside middle bands" - When a number of candle's in a row open and close between the middle EMA bands, it could be a sign the trend is weak, or that the breakout was not the start of a new trend. Selecting this will close out positions after a number of bars has passed

"Leledc bars" - Originally introduced by glaz, this is a price action indicator that highlights a candle after a number of bars in a row close the same direction and result in greatest high/low over a period. It often triggers when a strong trend has paused before further continuation, or it marks the end of a trend. To mitigate closing on false Leledc signals, this strategy has two options: 1. Introducing requirement for increased volume on the Leledc bars can help filter out Leledc signals that happen mid trend. 2. Closing after a number of Leledc bars appear after position opens. These two options work great in isolation but don't perform well together in my testing.

"Bollinger Bands exhaustion bars" - These bars are highlighted when price closes back inside the Bollinger Bands and RSI is within specified overbought/sold zones. The idea is that a trend is overextended when price trades beyond the Bollinger Bands. When price closes back inside the bands it's likely due for mean reversion back to the base EMA in which this strategy will ideally re-enter a position. Since the added RSI requirements often make this indicator too strict to trigger a large enough sample size to backtest, I've found it best to use "non-standard" settings for both the bands and the RSI as seen in the default settings.

"Buy/Sell zones" - Similar to the idea behind using Bollinger Bands exhaustion bars as a closing signal. Instead of calculating off of standard deviations, the Buy/Sell zones are calculated off multiples of the middle EMA bands. When trading beyond these zones and subsequently failing back inside, price may be due for mean reversion back to the base EMA. No RSI filter is used for Buy/Sell zones.

If any early close conditions are selected, it's often worth enabling trade re-entry on "middle EMA band bounce". Instead of waiting for a candle to close back inside the middle EMA bands, this feature will re-enter position on only a wick back into the middle bands as will sometimes happen when the trend is strong.

Any and all of the early close conditions can be combined. Experimenting with these, I've found can result in less net profit but higher win-rates and sharpe ratios as less time is spent in trades.

The deadly:

The trend is your friend. But wouldn't it be nice to catch the trends early? In ranging markets (or when using slower base EMAs in this strategy), waiting for confirmation of a breakout of the EMA bands at best will cause you to miss half the move, at worst will result in getting consistently chopped up. Enabling "counter-trend" trades on this strategy will allow the strategy to enter positions on the opposite side of the EMA bands on either a Leledc bar or Bollinger Bands exhaustion bar. There is a filter requiring either a high/low (for Leledc) or open (for BB bars) outside the selected inner or outer Buy/Sell zone. There are also a number of different close conditions for the counter-trend trades to experiment with and backtest.

There are two ways I've found best to use counter-trend trades

1. Mean reverting scalp trades when a trend is clearly overextended. Selecting from the first 5 counter-trend closing conditions on the dropdown list will usually close the trades out quickly, with less profit but less risk.

2. Trying to catch trends early. Selecting any of the close conditions below the first 5 can cause the strategy to behave as if it's entering into a new trend (from the wrong side).

This feature can be deadly effective in profiting from every move price makes, or deadly to the strategy's PnL if not set correctly. Since counter-trend trades open opposite the middle bands, a stop-loss is recommended to reduce risk. If stop-losses for counter-trend trades are disabled, the strategy will hold a position open often until liquidation in a trending market if th trade is offsides. Note that using a slower base EMA makes counter-trend stop-losses even more necessary as it can reduce the effectiveness of the Buy/Sell zone filter for opening the trades as price can spend a long time trending outside the zones. If faster EMAs (34 and below) are used with "Inner" Buy/Zone filter selected, the first few closing conditions will often trigger almost immediately closing the trade at a loss.

The niche:

I've added a feature to default into longs or shorts. Enabling these with other features (aside from the basic long/short on EMA middle band breakout) tends to break the strategy one way or another. Enabling default long works to simulate trying to acquire more of the asset rather than the base currency. Enabling default short can have positive results for those high FDV, high inflation coins that go down-only for months at a time. Otherwise, I use default short as a hedge for coins that I hold and stake spot. I gain the utility and APR of staking while reducing the risk of holding the underlying asset by maintaining a net neutral position *most* of the time.

Disclaimer:

This script is intended for experimenting and backtesting different strategies around EMA bands. Use this script for your live trading at your own risk. I am a rookie coder, as such there may be errors in the code that cause the strategy to behave not as intended. As far as I can tell it doesn't repaint, but I cannot guarantee that it does not. That being said if there's any question, improvements, or errors you've found, drop a comment below!

RSI Chebyshev Pro with Goldilocks Fractals - NR [NPR21]RSI Chebyshev Pro with Goldilocks Fractals - Non-Repaint

CHART INFORMATION

Instrument: /MNQ (Micro E-mini Nasdaq-100 Futures)

Timeframe: 2-minute

Indicator: RSI Chebyshev Pro with Goldilocks Fractals - NR

THE PROBLEM

Standard RSI is too choppy and noisy – it whipsaws all over the place in volatile markets like futures, giving false oversold/overbought signals that burn you on entries. I was sick of missing real reversals or getting stopped out on fakeouts. I wanted something smoother that still catches the big momentum shifts without lagging too much, plus actual market structure to make it more reliable for quick trades.

WHAT MAKES THIS UNIQUE

Unlike basic RSI indicators that use simple moving average smoothing, this combines several advanced techniques that aren't commonly found together:

1. Chebyshev Type I Filtering - Signal processing mathematics (not basic EMAs) that kills noise while keeping real swings sharp. Most RSI smoothing just blurs everything - this keeps responsiveness without the chop.

2. MAMA Adaptive Period - The moving average adapts to actual market cycles using the MESA algorithm, not fixed periods that lag in changing conditions.

3. RSI Pivot Fractals - These aren't price fractals slapped onto RSI. The fractals detect pivots directly on RSI values at extreme levels, with signals appearing back at the exact pivot bar (not current bar), showing you where the actual reversal happened.

4. True Non-Repainting Implementation - Signals appear delayed BUT locked at the historical pivot location forever. What you see in backtests is exactly what appeared live - no vanishing signals, no shifting.

5. All-in-One Integration - Instead of running 3-4 separate indicators (RSI + fractals + patterns + smoothing), everything works together in a single, optimized calculation with confluence built in.

This isn't just RSI with some Williams Fractals thrown on top - it's a complete rethink of how to identify high-probability RSI reversals using signal processing and adaptive algorithms.

ORIGIN & ENHANCEMENTS

Original Source: ChartPrime RSI Chebyshev indicator

Converted & Enhanced by: NPR21

What I Added:

✅ Converted to Pine Script v6 - Made this available to TradingView traders

✅ Goldilocks Fractals - RSI alone doesn't tell you about price structure. These fractals nail those "just right" pivot points where highs/lows confirm. I kept seeing RSI extremes that reversed hard when they lined up with fractals - this was the missing piece for confluence.

✅ 100% Non-Repainting - I've been burned by repainters. You'd backtest something, looks amazing, then live it vanishes or shifts. Lost real money on that. This is rock-solid: signals show delayed but once they're there, they're locked forever. Makes backtesting trustworthy.

✅ Candlestick Patterns - Engulfing, Morning Star, Evening Star detection for confluence

✅ Customizable Visuals - BUY/SELL labels, multiple display styles, full color/size control

✅ Complete Alert System - Get notified on all signal types

HOW IT WORKS

Chebyshev Filtering:

Like putting noise-canceling on your RSI – smooths out jittery ups and downs from random price spikes without flattening into useless lag. It's signal processing math that keeps important swings sharp while killing BS noise. Way better than simple EMA smoothing that blurs everything.

The Components:

Ultra-Smooth RSI - Chebyshev Type I filtering + adaptive MAMA algorithm

Goldilocks Fractals - Pivot detection confirmed after N bars (default 5)

Pattern Recognition - Detects Engulfing, Morning/Evening Star patterns

Visual Styles - Candle Trend (hollow green/solid red) or traditional candles

SIGNAL DELAY vs REPAINTING

✅ THIS HAS SIGNAL DELAY (GOOD) - NOT REPAINTING (BAD)

Signal Delay:

Signals appear after N bars (default 5 bar delay)

Once visible, NEVER disappears or moves

Perfect for backtesting - 100% reliable

What you see in history is what you'd see live

Why the Delay:

To confirm a pivot, we need to see price didn't go lower/higher in the next N bars. This confirmation makes signals reliable. The delay is the price for trustworthy signals.

Want faster? Drop Fractal Periods to 2-3 (more signals, less confirmation).

HOW I TRADE IT

My /MNQ Scalping (1-3 min charts):

LONG: BUY label appears (down fractal + maybe morning star/engulfing) → Check RSI crossing up from oversold (<30) → Confirm with volume → Long with stop below fractal low → Target 1-2R

SHORT: SELL label (up fractal + maybe evening star) → RSI from overbought → Short with stop above

Filter: Only longs in uptrends (watch the MA). Exit partials if momentum fades.

Best Timeframes: 1-5 min for futures scalping. Works on 15 min for swings but for pure scalping, stay under 5 min in high-vol sessions.

SETTINGS I USE

Standard Setup:

Length: 24, Smoothing: 3

Auto MA: ON, Multiplier: 1-2

Fractal Periods: 5 (good confirmation)

Choppy Days:

Smoothing to 5

Aggressive:

Fractal Periods to 3

Pro Tip: Pair with volume or price EMA. Love when fractal BUY + engulfing bull align. Use Candle Trend style. Test on demo first.

KEY SETTINGS

RSI: Length (24), Smoothing (3), Auto MA, Style (Candle/Candle Trend)

Fractals: Periods (5 = more reliable, 3 = faster/riskier), Label colors/sizes, Offsets

Alerts: All signals fire only on confirmed, non-repainting events

DISCLAIMERS

⚠️ Tool, not a complete system - use proper risk management

⚠️ Signals have delay for reliability - not for instant entries

⚠️ Best with price action, volume, other analysis

⚠️ Test on demo before live trading

Questions? Comment below!

NPR21

RSI Chebyshev Pro with Goldilocks Fractals - NR [NPR21]RSI Chebyshev Pro with Goldilocks Fractals - Non-Repaint

----------------------------------------------------------------------------------------------------------------------

CHART INFORMATION

Instrument: /MNQ (Micro E-mini Nasdaq-100 Futures)

Timeframe: 2-minute

Indicator: RSI Chebyshev Pro with Goldilocks Fractals - NR

----------------------------------------------------------------------------------------------------------------------

THE PROBLEM

Standard RSI is too choppy and noisy – it whipsaws all over the place in volatile markets like futures, giving false oversold/overbought signals that burn you on entries. I was sick of missing real reversals or getting stopped out on fakeouts. I wanted something smoother that still catches the big momentum shifts without lagging too much, plus actual market structure to make it more reliable for quick trades.

WHAT MAKES THIS UNIQUE

Unlike basic RSI indicators that use simple moving average smoothing, this combines several advanced techniques that aren't commonly found together:

1. Chebyshev Type I Filtering - Signal processing mathematics (not basic EMAs) that kills noise while keeping real swings sharp. Most RSI smoothing just blurs everything - this keeps responsiveness without the chop.

2. MAMA Adaptive Period - The moving average adapts to actual market cycles using the MESA algorithm, not fixed periods that lag in changing conditions.

3. RSI Pivot Fractals - These aren't price fractals slapped onto RSI. The fractals detect pivots directly on RSI values at extreme levels, with signals appearing back at the exact pivot bar (not current bar), showing you where the actual reversal happened.

4. True Non-Repainting Implementation - Signals appear delayed BUT locked at the historical pivot location forever. What you see in backtests is exactly what appeared live - no vanishing signals, no shifting.

5. All-in-One Integration - Instead of running 3-4 separate indicators (RSI + fractals + patterns + smoothing), everything works together in a single, optimized calculation with confluence built in.

This isn't just RSI with some Williams Fractals thrown on top - it's a complete rethink of how to identify high-probability RSI reversals using signal processing and adaptive algorithms.

ORIGIN & ENHANCEMENTS

Original Source: ChartPrime RSI Chebyshev indicator

Converted & Enhanced by: NPR21

What I Added:

✅ Converted to Pine Script v6 - Made this available to TradingView traders

✅ Goldilocks Fractals - RSI alone doesn't tell you about price structure. These fractals nail those "just right" pivot points where highs/lows confirm. I kept seeing RSI extremes that reversed hard when they lined up with fractals - this was the missing piece for confluence.

✅ 100% Non-Repainting - I've been burned by repainters. You'd backtest something, looks amazing, then live it vanishes or shifts. Lost real money on that. This is rock-solid: signals show delayed but once they're there, they're locked forever. Makes backtesting trustworthy.

✅ Candlestick Patterns - Engulfing, Morning Star, Evening Star detection for confluence

✅ Customizable Visuals - BUY/SELL labels, multiple display styles, full color/size control

✅ Complete Alert System - Get notified on all signal types

HOW IT WORKS

Chebyshev Filtering:

Like putting noise-canceling on your RSI – smooths out jittery ups and downs from random price spikes without flattening into useless lag. It's signal processing math that keeps important swings sharp while killing BS noise. Way better than simple EMA smoothing that blurs everything.

The Components:

Ultra-Smooth RSI - Chebyshev Type I filtering + adaptive MAMA algorithm

Goldilocks Fractals - Pivot detection confirmed after N bars (default 5)

Pattern Recognition - Detects Engulfing, Morning/Evening Star patterns

Visual Styles - Candle Trend (hollow green/solid red) or traditional candles

SIGNAL DELAY vs REPAINTING

✅ THIS HAS SIGNAL DELAY (GOOD) - NOT REPAINTING (BAD)

Signal Delay:

Signals appear after N bars (default 5 bar delay)

Once visible, NEVER disappears or moves

Perfect for backtesting - 100% reliable

What you see in history is what you'd see live

Why the Delay:

To confirm a pivot, we need to see price didn't go lower/higher in the next N bars. This confirmation makes signals reliable. The delay is the price for trustworthy signals.

Want faster? Drop Fractal Periods to 2-3 (more signals, less confirmation).

HOW I TRADE IT

My /MNQ Scalping (1-3 min charts):

LONG: BUY label appears (down fractal + maybe morning star/engulfing) → Check RSI crossing up from oversold (<30) → Confirm with volume → Long with stop below fractal low → Target 1-2R

SHORT: SELL label (up fractal + maybe evening star) → RSI from overbought → Short with stop above

Filter: Only longs in uptrends (watch the MA). Exit partials if momentum fades.

Best Timeframes: 1-5 min for futures scalping. Works on 15 min for swings but for pure scalping, stay under 5 min in high-vol sessions.

SETTINGS I USE

Standard Setup:

Length: 24, Smoothing: 3

Auto MA: ON, Multiplier: 1-2

Fractal Periods: 5 (good confirmation)

Choppy Days:

Smoothing to 5

Aggressive:

Fractal Periods to 3

Pro Tip: Pair with volume or price EMA. Love when fractal BUY + engulfing bull align. Use Candle Trend style. Test on demo first.

KEY SETTINGS

RSI: Length (24), Smoothing (3), Auto MA, Style (Candle/Candle Trend)

Fractals: Periods (5 = more reliable, 3 = faster/riskier), Label colors/sizes, Offsets

Alerts: All signals fire only on confirmed, non-repainting events

DISCLAIMERS

⚠️ Tool, not a complete system - use proper risk management

⚠️ Signals have delay for reliability - not for instant entries

⚠️ Best with price action, volume, other analysis

⚠️ Test on demo before live trading

Questions? Comment below!

NPR21

RSI Chebyshev Pro with Goldilocks Fractals - NR [NPR21]RSI Chebyshev Pro with Goldilocks Fractals - Non-Repaint

==================================================================================

**CHART INFORMATION**

The example chart shown displays:

- Instrument: /MNQ (Micro E-mini Nasdaq-100 Futures)

- Timeframe: 2-minute

- Indicator: RSI Chebyshev Pro with Goldilocks Fractals - NR

==================================================================================

═════════════════════════════════════════════════════════════

THE PROBLEM

Standard RSI is too choppy and noisy – it whipsaws all over the place in volatile markets like futures, giving false oversold/overbought signals that burn you on entries. I was sick of missing real reversals or getting stopped out on fakeouts. I wanted something smoother that still catches the big momentum shifts without lagging too much, plus actual market structure to make it more reliable for quick trades.

═════════════════════════════════════════════════════════════

WHAT MAKES THIS UNIQUE

Unlike basic RSI indicators that use simple moving average smoothing, this combines several advanced techniques that aren't commonly found together:

1. Chebyshev Type I Filtering - Signal processing mathematics (not basic EMAs) that kills noise while keeping real swings sharp. Most RSI smoothing just blurs everything - this keeps responsiveness without the chop.

2. MAMA Adaptive Period - The moving average adapts to actual market cycles using the MESA algorithm, not fixed periods that lag in changing conditions.

3. RSI Pivot Fractals - These aren't price fractals slapped onto RSI. The fractals detect pivots directly on RSI values at extreme levels, with signals appearing back at the exact pivot bar (not current bar), showing you where the actual reversal happened.

4. True Non-Repainting Implementation - Signals appear delayed BUT locked at the historical pivot location forever. What you see in backtests is exactly what appeared live - no vanishing signals, no shifting.

5. All-in-One Integration - Instead of running 3-4 separate indicators (RSI + fractals + patterns + smoothing), everything works together in a single, optimized calculation with confluence built in.

This isn't just RSI with some Williams Fractals thrown on top - it's a complete rethink of how to identify high-probability RSI reversals using signal processing and adaptive algorithms.

═════════════════════════════════════════════════════════════

ORIGIN & ENHANCEMENTS

Original Source: ChartPrime RSI Chebyshev indicator

Converted & Enhanced by: NPR21

What I Added:

✅ Converted to Pine Script v6 - Made this available to TradingView traders

✅ Goldilocks Fractals - RSI alone doesn't tell you about price structure. These fractals nail those "just right" pivot points where highs/lows confirm. I kept seeing RSI extremes that reversed hard when they lined up with fractals - this was the missing piece for confluence.

✅ 100% Non-Repainting - I've been burned by repainters. You'd backtest something, looks amazing, then live it vanishes or shifts. Lost real money on that. This is rock-solid: signals show delayed but once they're there, they're locked forever. Makes backtesting trustworthy.

✅ Candlestick Patterns - Engulfing, Morning Star, Evening Star detection for confluence

✅ Customizable Visuals - BUY/SELL labels, multiple display styles, full color/size control

✅ Complete Alert System - Get notified on all signal types

═════════════════════════════════════════════════════════════

HOW IT WORKS

Chebyshev Filtering:

Like putting noise-canceling on your RSI – smooths out jittery ups and downs from random price spikes without flattening into useless lag. It's signal processing math that keeps important swings sharp while killing BS noise. Way better than simple EMA smoothing that blurs everything.

The Components:

Ultra-Smooth RSI - Chebyshev Type I filtering + adaptive MAMA algorithm

Goldilocks Fractals - Pivot detection confirmed after N bars (default 5)

Pattern Recognition - Detects Engulfing, Morning/Evening Star patterns

Visual Styles - Candle Trend (hollow green/solid red) or traditional candles

═════════════════════════════════════════════════════════════

SIGNAL DELAY vs REPAINTING

✅ THIS HAS SIGNAL DELAY (GOOD) - NOT REPAINTING (BAD)

Signal Delay:

Signals appear after N bars (default 5 bar delay)

Once visible, NEVER disappears or moves

Perfect for backtesting - 100% reliable

What you see in history is what you'd see live

Why the Delay:

To confirm a pivot, we need to see price didn't go lower/higher in the next N bars. This confirmation makes signals reliable. The delay is the price for trustworthy signals.

Want faster? Drop Fractal Periods to 2-3 (more signals, less confirmation).

════════════════════════════════════════════════════════════

HOW I TRADE IT

My /MNQ Scalping (1-3 min charts):

LONG: BUY label appears (down fractal + maybe morning star/engulfing) → Check RSI crossing up from oversold (<30) → Confirm with volume → Long with stop below fractal low → Target 1-2R

SHORT: SELL label (up fractal + maybe evening star) → RSI from overbought → Short with stop above

Filter: Only longs in uptrends (watch the MA). Exit partials if momentum fades.

Best Timeframes: 1-5 min for futures scalping. Works on 15 min for swings but for pure scalping, stay under 5 min in high-vol sessions.

═════════════════════════════════════════════════════════════

SETTINGS I USE

Standard Setup:

Length: 24, Smoothing: 3

Auto MA: ON, Multiplier: 1-2

Fractal Periods: 5 (good confirmation)

Choppy Days: Smoothing to 5

Aggressive: Fractal Periods to 3

Pro Tip: Pair with volume or price EMA. Love when fractal BUY + engulfing bull align. Use Candle Trend style. Test on demo first.

═════════════════════════════════════════════════════════════

KEY SETTINGS

RSI: Length (24), Smoothing (3), Auto MA, Style (Candle/Candle Trend)

Fractals: Periods (5 = more reliable, 3 = faster/riskier), Label colors/sizes, Offsets

Alerts: All signals fire only on confirmed, non-repainting events

═════════════════════════════════════════════════════════════

DISCLAIMERS

⚠️ Tool, not a complete system - use proper risk management

⚠️ Signals have delay for reliability - not for instant entries

⚠️ Best with price action, volume, other analysis

⚠️ Test on demo before live trading

═════════════════════════════════════════════════════════════

Questions? Comment below!

NPR21

PA SystemPA System

短简介 Short Description(放在最上面)

中文:

PA System 是一套以 AL Brooks 价格行为为核心的策略(Strategy),将 结构(HH/HL/LH/LL)→ 回调(H1/L1)→ 二次入场(H2/L2 微平台突破) 串成完整可回测流程,并可选叠加 BoS/CHoCH 结构突破过滤 与 Liquidity Sweep(扫流动性)确认。内置风险管理:定风险仓位、部分止盈、保本、移动止损、时间止损、冷却期。

English:

PA System is an AL Brooks–inspired Price Action strategy that chains Market Structure (HH/HL/LH/LL) → Pullback (H1/L1) → Second Entry (H2/L2 via Micro Range Breakout) into a complete backtestable workflow, with optional BoS/CHoCH structure-break filtering and Liquidity Sweep confirmation. Built-in risk management includes risk-based sizing, partial exits, breakeven, trailing stops, time stop, and cooldown.

⸻

1) 核心理念 Core Idea

中文:

这不是“指标堆叠”,而是一条清晰的价格行为决策链:

结构确认 → 回调出现 → 小平台突破(二次入场)→ 风控出场。

策略把 Brooks 常见的“二次入场”思路程序化,同时用可选的结构突破与扫流动性模块提升信号质量、减少震荡误入。

English:

This is not an “indicator soup.” It’s a clear price-action decision chain:

Confirmed structure → Pullback → Micro-range breakout (second entry) → Risk-managed exits.

The system programmatically implements the Brooks-style “second entry” concept, and optionally adds structure-break and liquidity-sweep context to reduce chop and improve trade quality.

⸻

2) 主要模块 Main Modules

A. 结构识别 Market Structure (HH/HL/LH/LL)

中文:

使用 pivot 摆动点确认结构,标记 HH/HL/LH/LL,并可显示最近一组摆动水平线,方便对照结构位置。

English:

Uses confirmed pivot swings to label HH/HL/LH/LL and optionally plots the most recent swing levels for clean structure context.

B. 状态机 Market Regime (State Machine + “Always In”)

中文:

基于趋势K强度、EMA关系与波动范围,识别市场环境(Breakout/Channel/Range)以及 Always-In 方向,用于过滤不合适的交易环境。

English:

A lightweight regime engine detects Breakout/Channel/Range and an “Always In” directional bias using momentum and EMA/range context to avoid low-quality conditions.

C. 二次入场 Second Entry Engine (H1→H2 / L1→L2)

中文:

• H1/L1:回调到结构附近并出现反转迹象

• H2/L2:在 H1/L1 后等待最小 bars,然后触发 Micro Range Breakout(小平台突破)并要求信号K收盘强度达标

这一段是策略的“主发动机”。

English:

• H1/L1: Pullback into structure with reversal intent

• H2/L2: After a minimum wait, triggers on Micro Range Breakout plus a configurable close-strength filter

This is the main “entry engine.”

D. 可选过滤器 Optional Filters (Quality Boost)

BoS/CHoCH(结构突破过滤)

中文: 可识别 BoS / CHoCH,并可要求“入场前最近 N bars 必须有同向 break”。

English: Detects BoS/CHoCH and can require a recent same-direction break within N bars.

Liquidity Sweeps(扫流动性确认)

中文: 画出 pivot 高/低的流动性水平线,检测“刺破后收回”的 sweep,并可要求入场前出现同向 sweep。

English: Tracks pivot-based liquidity levels, confirms sweeps (pierce-and-reclaim), and can require a recent sweep before entry.

E. FVG 可视化 FVG Visualization

中文: 提供 FVG 区域盒子与管理模式(仅保留未回补 / 仅保留最近N),主要用于区域理解与复盘,不作为强制入场条件(可自行扩展)。

English: Displays FVG boxes with retention modes (unfilled-only or last-N). Primarily for context/analysis; not required for entries (you can extend it as a filter/target).

⸻

3) 风险管理 Risk Management (Built-In)

中文:

• 定风险仓位:按账户权益百分比计算仓位

• SL/TP:基于结构 + ATR 缓冲,且限制最大止损 ATR 倍

• 部分止盈:到达指定 R 后减仓

• 保本:到达指定 R 后推到 BE

• 移动止损:到达指定 R 后开始跟随

• 时间止损:持仓太久不动则退出

• 冷却期:出场后等待 N bars 再允许新单

English:

• Risk-based sizing: position size from equity risk %

• SL/TP: structure + ATR buffer with max ATR risk cap

• Partial exits at an R threshold

• Breakeven at an R threshold

• Trailing stop activation at an R threshold

• Time stop to reduce chop damage

• Cooldown after exit to avoid rapid re-entries

⸻

4) 推荐使用方式 Recommended Usage

中文:

• 推荐从 5m / 15m / 1H 开始测试

• 想更稳:开启 EMA Filter + Break Filter + Sweep Filter,并提高 Close Strength

• 想更多信号:关闭 Break/Sweep 过滤或降低 Swing Length / Close Strength

• 回测时务必设置合理的手续费与滑点,尤其是期货/指数

English:

• Start testing on 5m / 15m / 1H

• For higher quality: enable EMA Filter + Break Filter + Sweep Filter and increase Close Strength

• For more signals: disable Break/Sweep filters or reduce Swing Length / Close Strength

• Use realistic commissions/slippage in backtests (especially for futures/indices)

⸻

5) 重要说明 Notes

中文:

结构 pivot 需要右侧确认 bars,因此结构点存在天然滞后(确认后不会再变)。策略逻辑尽量避免不必要的对象堆叠,并对数组/对象做了稳定管理,适合长期运行与复盘。

English:

Pivot-based structure requires right-side confirmation (inherent lag; once confirmed it won’t change). The script is designed for stability and resource-safe object management, suitable for long sessions and review.

⸻

免责声明 Disclaimer(建议原样保留)

中文:

本脚本仅用于教育与研究目的,不构成任何投资建议。策略回测结果受市场条件、手续费、滑点、交易时段、数据质量等影响显著。使用者需自行验证并承担全部风险。过往表现不代表未来结果。

English:

This script is for educational and research purposes only and does not constitute financial advice. Backtest results are highly sensitive to market conditions, fees, slippage, session settings, and data quality. Use at your own risk. Past performance is not indicative of future results.

MLExtensionsLibrary "MLExtensions"

A set of extension methods for a novel implementation of a Approximate Nearest Neighbors (ANN) algorithm in Lorentzian space.

normalizeDeriv(src, quadraticMeanLength)

Returns the smoothed hyperbolic tangent of the input series.

Parameters:

src (float) : The input series (i.e., the first-order derivative for price).

quadraticMeanLength (int) : The length of the quadratic mean (RMS).

Returns: nDeriv The normalized derivative of the input series.

normalize(src, min, max)

Rescales a source value with an unbounded range to a target range.

Parameters:

src (float) : The input series

min (float) : The minimum value of the unbounded range

max (float) : The maximum value of the unbounded range

Returns: The normalized series

rescale(src, oldMin, oldMax, newMin, newMax)

Rescales a source value with a bounded range to anther bounded range

Parameters:

src (float) : The input series

oldMin (float) : The minimum value of the range to rescale from

oldMax (float) : The maximum value of the range to rescale from

newMin (float) : The minimum value of the range to rescale to

newMax (float) : The maximum value of the range to rescale to

Returns: The rescaled series

getColorShades(color)

Creates an array of colors with varying shades of the input color

Parameters:

color (color) : The color to create shades of

Returns: An array of colors with varying shades of the input color

getPredictionColor(prediction, neighborsCount, shadesArr)

Determines the color shade based on prediction percentile

Parameters:

prediction (float) : Value of the prediction

neighborsCount (int) : The number of neighbors used in a nearest neighbors classification

shadesArr (array) : An array of colors with varying shades of the input color

Returns: shade Color shade based on prediction percentile

color_green(prediction)

Assigns varying shades of the color green based on the KNN classification

Parameters:

prediction (float) : Value (int|float) of the prediction

Returns: color

color_red(prediction)

Assigns varying shades of the color red based on the KNN classification

Parameters:

prediction (float) : Value of the prediction

Returns: color

tanh(src)

Returns the the hyperbolic tangent of the input series. The sigmoid-like hyperbolic tangent function is used to compress the input to a value between -1 and 1.

Parameters:

src (float) : The input series (i.e., the normalized derivative).

Returns: tanh The hyperbolic tangent of the input series.

dualPoleFilter(src, lookback)

Returns the smoothed hyperbolic tangent of the input series.

Parameters:

src (float) : The input series (i.e., the hyperbolic tangent).

lookback (int) : The lookback window for the smoothing.

Returns: filter The smoothed hyperbolic tangent of the input series.

tanhTransform(src, smoothingFrequency, quadraticMeanLength)

Returns the tanh transform of the input series.

Parameters:

src (float) : The input series (i.e., the result of the tanh calculation).

smoothingFrequency (int)

quadraticMeanLength (int)

Returns: signal The smoothed hyperbolic tangent transform of the input series.

n_rsi(src, n1, n2)

Returns the normalized RSI ideal for use in ML algorithms.

Parameters:

src (float) : The input series (i.e., the result of the RSI calculation).

n1 (simple int) : The length of the RSI.

n2 (simple int) : The smoothing length of the RSI.

Returns: signal The normalized RSI.

n_cci(src, n1, n2)

Returns the normalized CCI ideal for use in ML algorithms.

Parameters:

src (float) : The input series (i.e., the result of the CCI calculation).

n1 (simple int) : The length of the CCI.

n2 (simple int) : The smoothing length of the CCI.

Returns: signal The normalized CCI.

n_wt(src, n1, n2)

Returns the normalized WaveTrend Classic series ideal for use in ML algorithms.

Parameters:

src (float) : The input series (i.e., the result of the WaveTrend Classic calculation).

n1 (simple int)

n2 (simple int)

Returns: signal The normalized WaveTrend Classic series.

n_adx(highSrc, lowSrc, closeSrc, n1)

Returns the normalized ADX ideal for use in ML algorithms.

Parameters:

highSrc (float) : The input series for the high price.

lowSrc (float) : The input series for the low price.

closeSrc (float) : The input series for the close price.

n1 (simple int) : The length of the ADX.

regime_filter(src, threshold, useRegimeFilter)

Parameters:

src (float)

threshold (float)

useRegimeFilter (bool)

filter_adx(src, length, adxThreshold, useAdxFilter)

filter_adx

Parameters:

src (float) : The source series.

length (simple int) : The length of the ADX.

adxThreshold (int) : The ADX threshold.

useAdxFilter (bool) : Whether to use the ADX filter.

Returns: The ADX.

filter_volatility(minLength, maxLength, useVolatilityFilter)

filter_volatility

Parameters:

minLength (simple int) : The minimum length of the ATR.

maxLength (simple int) : The maximum length of the ATR.

useVolatilityFilter (bool) : Whether to use the volatility filter.

Returns: Boolean indicating whether or not to let the signal pass through the filter.

backtest(high, low, open, startLongTrade, endLongTrade, startShortTrade, endShortTrade, isEarlySignalFlip, maxBarsBackIndex, thisBarIndex, src, useWorstCase)

Performs a basic backtest using the specified parameters and conditions.

Parameters:

high (float) : The input series for the high price.

low (float) : The input series for the low price.

open (float) : The input series for the open price.

startLongTrade (bool) : The series of conditions that indicate the start of a long trade.

endLongTrade (bool) : The series of conditions that indicate the end of a long trade.

startShortTrade (bool) : The series of conditions that indicate the start of a short trade.

endShortTrade (bool) : The series of conditions that indicate the end of a short trade.

isEarlySignalFlip (bool) : Whether or not the signal flip is early.

maxBarsBackIndex (int) : The maximum number of bars to go back in the backtest.

thisBarIndex (int) : The current bar index.

src (float) : The source series.

useWorstCase (bool) : Whether to use the worst case scenario for the backtest.

Returns: A tuple containing backtest values

init_table()

init_table()

Returns: tbl The backtest results.

update_table(tbl, tradeStatsHeader, totalTrades, totalWins, totalLosses, winLossRatio, winrate, earlySignalFlips)

update_table(tbl, tradeStats)

Parameters:

tbl (table) : The backtest results table.

tradeStatsHeader (string) : The trade stats header.

totalTrades (float) : The total number of trades.

totalWins (float) : The total number of wins.

totalLosses (float) : The total number of losses.

winLossRatio (float) : The win loss ratio.

winrate (float) : The winrate.

earlySignalFlips (float) : The total number of early signal flips.

Returns: Updated backtest results table.

VMDM - Volume, Momentum & Divergence Master [BullByte]VMDM - Volume, Momentum and Divergence Master

Educational Multi-Layer Market Structure Analysis System

Multi-factor divergence engine that scores RSI momentum, volume pressure, and institutional footprints into one non-repainting confluence rating (0-100).

WHAT THIS INDICATOR IS