在腳本中搜尋"bear"

TMMS OscillatorThe TMMS oscillator (aka “Trading Made More Simpler”) is an indicator made of conditions based on both 2 separated Stochastic and 1 RSI.

Bullish zone is green and bearish one is red. When the histogram is grey, no signals is available at that time.

The indicator has an option to show the current trend of an Hull moving average (ascending or descending curve). When the trend is up, green dots are plotted on the zero line. When the trend is down, the dots are coloured in red.

Greetings, success with your trade!!!

Dreadblitz BarsThese bars can give you good opportunities if you know how to analyze the context.

blue=bullish

black=bearish

thumbs up

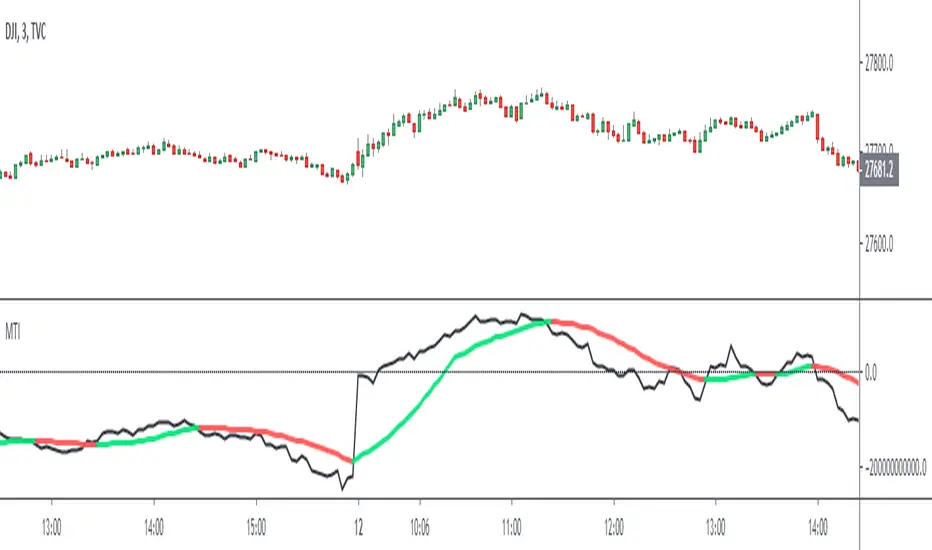

Market Thrust IndicatorThe Market Thrust indicator is a powerful measure of the stock market's internal strength or weakness. There are four components to this indicator:

1-Advancing Issues on the New York Stock Exchange (NYSE) – $ADV

2-Advancing Volume on the NYSE – $UVOL

3-Declining Issues on the NYSE – $DECL

4-Declining Volume on the NYSE – $DVOL

The formula for Market Thrust is given below:

($ADV x $UVOL)-($DECL x $DVOL)

When used for day-trading, the trend of the Market Thrust indicator is what is most important.

Rising Market Thrust Indicator: Considered a bullish sign; can act as a confirmation signal when combined with a rising stock, index ETF, or stock index future's price.

Falling Market Thrust Indicator: Considered a bearish sign; can act as a confirmation signal of a decreasing market price.

The Market Thrust indicator could be used for detecting divergences in trends. Divergences occur when:

- Price is trending higher, but the Market Thrust indicator is not moving higher or is even going down.

- Price is trending lower, however, the Market Thrust technical analysis tool is not trending lower, it is either not trending or is trending higher.

Add a fully configurable trend line over MTI.

Read more at: commodity.com

Engulfing Scanner v1This indicator helps you to quickly identify bullish and bearish engulfing patterns.

Works on currencies only (pips required).

Differential Price Counter for Bullish/Bearish BarsThis script can show the cumulative differential price of both bullish/bearish bars with the 0.1pip precision for the currencies having five decimal precision. However, can be useful for all markets.

RepulseThis indicator was originally developed by Eric Lefort, a professional trader and author from France.

It gauges and displays the bullish or bearish pressure.

Like and follow for more open source indicators!

Happy Trading!

RSI_EMA & Bearish EngulfingThis is a RSI-RSI of EMA and bearish candlestick reversal pattern formed by two candlesticks. Following an uptrend, the first candlestick is a up candlestick which is followed by a down candlestick which has a long real body that engulfs or contains the real body of the prior bar. following an uptrend, if RSI and EMA line cross then Sell and for downtrend if RSI and EMA line cross then Buy.

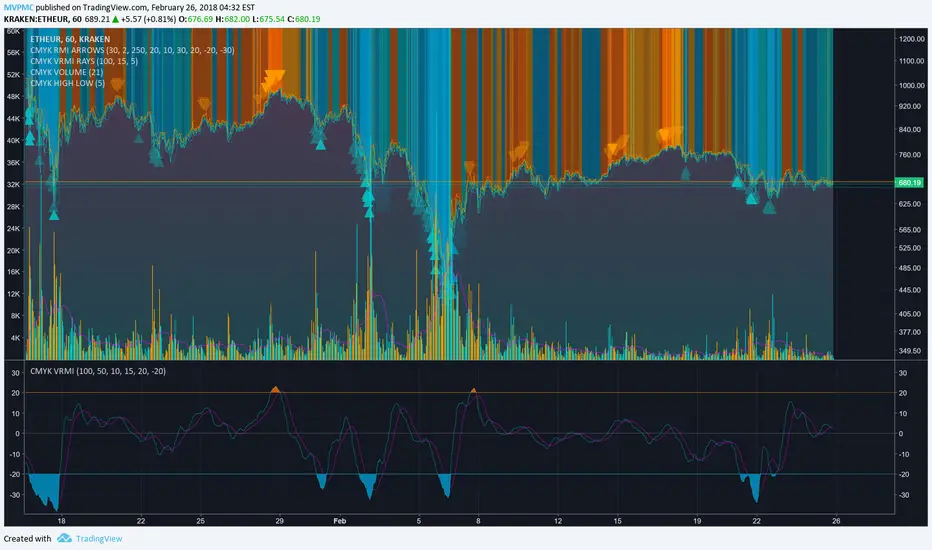

CMYK VRMI◊ Introduction

This script indicates the relative movement of price x volume.

◊ Origin

Based on 'The Relative Momentum Index' by Roger Altman : February, 1993 issue of Technical Analysis of Stocks & Commodities magazine.

While RSI counts up and down days from close to close, the Relative Momentum Index counts up and down days from the close relative to a close x number of days ago.

This results in an RSI that is smoother. The input has been changed to the change of a smoothed close multiplied by a smoothed volume.

The polarity of VRMI indicates bearish/bullish movement.

◊ Adjustments

CMYK color theme applied.

◊ Usage

VRMI indicates the force the market moves with.

◊ Future Prospects

-

◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊

CMYK VRMI RAYS ◊ Introduction

Introducing VRMI in this script, an RMI based on price movement and volume, to indicate bullish and bearish trends.

This script marks the background depending on RMI <> VRMI , VRMI polarity and large buy/sell sprees.

◊ Origin

Based on 'The Relative Momentum Index' by Roger Altman : February, 1993 issue of Technical Analysis of Stocks & Commodities magazine.

While RSI counts up and down days from close to close, the Relative Momentum Index counts up and down days from the close relative to a close x number of days ago.

This results in an RSI that is smoother.

In addition VRMI reacts quick, it is used to cut off latency from RMI, and it's polarity indicates the beginning and end of a trend.

Large buy sell sprees and detected in their proportion with an sma on the volume

◊ Adjustments

CMYK color theme applied.

◊ Usage

This indicator can be used to detect trends and mark reversals.

◊ Prospects

◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊ ◊

Super Envolvente (Bullish y Bearish)Identificador de Super-envolventes (SE), se encarga de darle un color verde a la SE alzista (Bullish) verde y rojo a la bajista (Bearish).

Bearish Trailing stopIt is a trailing SL. Works very well. Good good very good. Looks like my description needs more, so here is more random text.

Bearish signal using Point of Control (POC) with PAC by guruThis indicator code helps traders identify potential sell opportunities using several important technical indicators:

Point of Control (POC) – This is the price level where the most volume was traded over the past several days.

Previous Day's Low – This shows the lowest price reached during the previous day.

PAC (Price Action Channel) EMA – These are two moving averages (one based on the low price and one based on the close price) that help determine if the price is trending within a certain range.

Volume SMA – This is a 3-day simple moving average (SMA) of volume, which helps filter out signals based on market activity.

What the Script Does:

Point of Control (POC):

The script looks at the last 50 days (configurable) and calculates which price level had the highest trading volume.

It then plots a red line on the chart at the POC level. This is important because it helps identify areas where there was strong market interest in the past.

Volume Moving Average:

The script calculates a 3-day SMA of volume, but it excludes the current day to avoid premature signals based on today’s trading.

The volume SMA is used to ensure there’s enough market activity (with a threshold set to 25 units) before triggering a sell signal.

Price Action Channel (PAC) EMA:

The PAC consists of two exponential moving averages (EMAs):

The PAC Low EMA: This is based on the low prices over the last 34 periods (configurable).

The PAC Close EMA: This is based on the closing prices over the last 34 periods.

These EMAs help determine if the price is trending above or below certain price levels.

Sell Signal Logic: The script checks three conditions before displaying a "Sell" signal:

Price Below POC and Previous Day’s Low:

The close price must be below both the Point of Control (POC) and the previous day's low.

Volume SMA Above 25:

The 3-day volume SMA must be greater than 25. This ensures the signal only triggers when there’s enough trading volume in the market.

Today’s Low is Above PAC EMAs:

Today's low price must be above both the PAC low EMA and the PAC close EMA. This prevents sell signals when prices are already significantly below the PAC, indicating possible exhaustion in the downtrend.

If all three conditions are met, the script will display a red "Sell" label on the chart, signaling a potential selling opportunity.

No Sell Signal if Price Reverses:

If the price crosses back above the POC or the previous day's low, the script will remove the sell signal and reset for a new opportunity.

Summary of Conditions:

For the script to display a "Sell" label:

The close price must be below the Point of Control (POC) and the previous day’s low.

The 3-day volume SMA (excluding today) must be greater than 25 units.

The low price of the current day must be above both the PAC low EMA and the PAC close EMA.

If these conditions are met, a red sell label appears on the chart as a potential signal for a short (sell) trade.

Dual Super Trend IndicatorDual Super Trend Indicator

A powerful trend-following indicator designed to capture clean and reliable market moves using dual SuperTrend confirmation. Signals are generated only when both fast and slow SuperTrend align, helping traders avoid noise and focus on strong directional trends.

✔ One clear signal per trend

✔ Reduced false signals in sideways markets

✔ Automatic signal flip alerts (Long ↔ Short)

✔ Works on Intraday, Swing & Positional trading

✔ Suitable for Index, Stocks, Futures, Crypto & Forex

How to use:

Go Long when both SuperTrends turn bullish.

Go Short when both turn bearish.

Exit or trail using SuperTrend or price structure.

Built for traders who prefer simple, rule-based trend trading with clarity.

For educational purposes only. Use proper risk management.

Anchor-Point AverageAnchor-Point Average (APA) - Pine Script Indicator

Overview

The Anchor-Point Average (APA) is a unique technical indicator that calculates the average price from a user-defined starting point to the present. Unlike traditional Simple Moving Averages (SMA) that use a rolling window of fixed periods, APA uses a fixed anchor point in time, creating a cumulative average that grows with each new bar.

Key Features

Interactive Time Selection

Click-to-Select: Simply click on any bar in the chart to set your anchor point

Visual Markers: Clear labels show the start point with date/time and current average price

Flexible Analysis: Anchor to any significant event, price level, or time period

Multiple Price Types

Choose from 7 different price calculations:

Close: Standard closing price

Open: Opening price for gap analysis

High/Low: Track resistance and support levels

HL2: Midpoint price (High + Low) / 2

HLC3: Typical price (High + Low + Close) / 3

OHLC4: Average price (Open + High + Low + Close) / 4

Customizable Display

Color Settings: Customize both anchor point and current label colors

Clean Interface: Minimalist design with essential information only

Professional Labels: Display average price, sample count, and timestamps

Smart Alerts

Cross Above Alert: Notifies when price crosses above the anchor-point average

Cross Below Alert: Notifies when price drops below the anchor-point average

Visual Markers: Green triangles (bullish cross) and red triangles (bearish cross)

Why Anchor-Point Average?

Different from Traditional SMA

Traditional moving averages use a rolling window (e.g., last 20 bars), which means older data constantly drops out. APA maintains all data from your chosen anchor point, providing a true cumulative average that represents the mean price since that specific moment.

Use Cases

Long-Term Investment Analysis

Calculate average entry cost from your first purchase date

Track performance against your initial investment timing

Identify if current price is above or below your historical average

Event-Based Analysis

Anchor to product launches, earnings reports, or policy announcements

Measure price behavior after significant market events

Compare current price to post-event average levels

Support/Resistance Identification

The anchor-point average often acts as dynamic support or resistance

As more data accumulates, the line becomes increasingly stable

Price reactions to this level can signal trend continuation or reversal

Volatility Assessment

Increasing distance from anchor average indicates growing volatility

Convergence suggests consolidation or equilibrium

Track how current price deviates from long-term mean

Technical Advantages

Stability Over Time

As the sample size grows, the anchor-point average becomes progressively smoother and less sensitive to short-term volatility, providing a robust reference level.

Historical Context

Unlike moving averages that "forget" old data, APA preserves the entire price history from your chosen point, offering complete context for your analysis.

Psychological Significance

Often traders anchor mentally to specific dates or events. This indicator makes that psychological level visible and quantifiable.

How to Use

Add to Chart: Apply the indicator to any TradingView chart

Select Anchor Point: Click on the bar where you want to begin calculation

Choose Price Type: Select which price component to average (default: Close)

Customize Colors: Adjust label colors to match your chart theme

Set Alerts: Create alerts for price crossovers to stay informed

Perfect For

Long-term investors tracking cost basis

Swing traders analyzing from key pivot points

Event-driven traders measuring post-announcement trends

Anyone seeking a stable, cumulative price reference

Technical Notes

Built on Pine Script v5

Overlay indicator (plots directly on price chart)

Real-time calculation with bar-by-bar updates

Supports all timeframes and instruments

Zero repainting - calculations are final once bar closes

2 Bar Strategy + Fib EntryCustom indicator for my 2 bar strategy, bullish or bearish waring setup signal included and entry zone

Market Regime AnalyzerStatistical regime detection with forward-looking transition probabilities. Combines drift testing, variance ratios, and volume delta to classify markets into 5 regimes and quantify transition probabilities.

What Regime Are We In, and What's Likely Next?

That's the question this indicator answers with statistical rigor and forward-looking probabilities.

The Problem:

Most traders classify regimes arbitrarily: "Bull if price > 200 MA" or "Bear if RSI < 30." These rules ignore statistical significance, volume confirmation, and mean reversion patterns. The result? Late entries, false signals, and confusion when markets transition.

The Solution:

Market Regime Analyzer combines drift detection, variance ratio testing, and volume delta analysis to classify markets into 5 distinct regimes. Then it calculates the probability of transitioning to each regime based on historical patterns.

The Benefit:

Know not just where you are, but where you're likely going - with probabilities, not guesses.

The Five Market Regimes

🟢 Strong Bull (Regime 1)

- Statistically significant upward drift (t-stat > 1.96)

- Strong buying pressure (volume delta > 0.3)

- No mean reversion detected

- **Trade:** Trend-following strategies, ride the momentum

🟢 Weak Bull (Regime 2)

- Upward drift present

- BUT weak volume OR mean reversion detected

- **Trade:** Reduce position size, tighten stops, prepare for consolidation

⚪ Consolidation (Regime 3)

- No statistically significant drift

- Mixed volume signals

- Mean reversion likely present

- **Trade:** Range-trading, avoid trend-following systems

🔴 Weak Bear (Regime 4)

- Downward drift present

- BUT weak volume pressure

- **Trade:** Cautious shorts, reduce exposure, prepare for bounce

🔴 Strong Bear (Regime 5)

- Statistically significant downward drift (t-stat < -1.96)

- Strong selling pressure (volume delta < -0.3)

- No mean reversion detected

- **Trade:** Trend-following shorts, protective puts

The Statistical Framework

1. Drift Detection with T-Statistics

Instead of guessing if there's a trend, we test it statistically.

How it works:

- Calculates mean return over lookback period

- Standardizes by volatility

- Compares to significance threshold (default 1.96 = 95% confidence)

What it tells you:

- T-stat > 1.96: Statistically significant uptrend

- T-stat < -1.96: Statistically significant downtrend

- In between: No significant trend (consolidation)

Why it matters:

Only trades trends that are statistically validated, not just visually apparent.

2. Mean Reversion Testing (Variance Ratio)

Based on Lo & MacKinlay (1988) research, this detects when markets are range-bound.

How it works:

- Compares variance at different time scales

- Variance Ratio < 0.8 indicates mean reversion

What it tells you:

- Mean reversion = NO: Trends can continue

- Mean reversion = YES: Expect price to return to mean, not breakout

Why it matters:

Prevents chasing breakouts in range-bound markets.

3. Volume Delta Analysis

Total volume tells you HOW MUCH traded. Volume delta tells you WHO won.

How it works:

- Buying pressure - Selling pressure = Volume Delta

- Normalized to show relative strength

What it tells you:

- Strong positive delta (>0.3): Buyers in control

- Strong negative delta (<-0.3): Sellers in control

- Weak delta: No clear winner

Why it matters:

Price can move up on weak buying or down on weak selling. Volume delta reveals the truth.

4. Transition Probability Matrix

Historical regime changes predict future regime changes.

How it works:

- Tracks every regime transition over last 100 bars (configurable)

- Builds probability distribution for next regime

- Updates continuously

Example:

Current: Strong Bull

Historical transitions from Strong Bull:

- Stayed Strong Bull: 45%

- Became Weak Bull: 30%

- Became Consolidation: 20%

- Became Weak Bear: 4%

- Became Strong Bear: 1%

What it tells you:

Strong Bull has 75% chance of staying bullish (45% + 30%), only 5% chance of bearish turn.

Why it matters:

Adapts to your specific market's behavior patterns.

How to Use This Indicator

Strategy Adaptation

In Strong Bull/Bear Regimes:

- Use trend-following strategies

- Wider stops, let winners run

- Add to positions on pullbacks

- High confidence in directional trades

In Weak Bull/Bear Regimes:

- Reduce position sizes by 50%

- Tighter stops

- Take profits earlier

- Prepare for regime change

In Consolidation:

- Switch to range-trading strategies

- Avoid trend-following systems

- Sell resistance, buy support

- Wait for regime change before trend trades

Risk Management

Position Sizing:

- Strong regime + high continuation probability (>60%) = Normal size

- Weak regime OR high transition probability = Half size

- Consolidation = Quarter size or skip

Stop Loss Placement:

- Strong regime: Use wider stops (2x ATR)

- Weak regime: Tighter stops (1x ATR)

- Consolidation: Very tight stops (0.5x ATR)

Entry Timing

Best entries:

- Regime just changed to Strong Bull/Bear

- High probability (>50%) of staying in current regime

- No divergence signals present

- Drift and volume delta aligned

Avoid entries:

- High probability of regime change

- Divergence signals appearing

- Mean reversion detected in trending regime

- Weak volume despite price movement

Reading the Dashboard

Current Regime

Color-coded for instant recognition:

- Dark Green = Strong Bull

- Light Green = Weak Bull

- Gray = Consolidation

- Light Red = Weak Bear

- Dark Red = Strong Bear

Annualized Drift

Expected annual return based on recent trend.

- Positive = Upward bias

- Negative = Downward bias

- Near zero = No directional edge

T-Statistic

Measures statistical significance of drift.

- > 1.96 = 95% confident in uptrend

- < -1.96 = 95% confident in downtrend

- Between = Not statistically significant

Mean Reversion

- Yes = Expect price to return to mean (range-bound)

- No = Trends can continue (trending market)

Volume Pressure

Normalized volume delta strength.

- > 0.3 = Strong buying

- < -0.3 = Strong selling

- Near 0 = Balanced

Transition Probabilities

Shows most likely next regime.

- Highest probability = Most likely outcome

- Evenly distributed = High uncertainty

- Concentrated = High confidence in direction

Practical Examples

Example 1: Strong Bull with High Continuation

Dashboard shows:

Current Regime: Strong Bull

Drift: +22% annualized

T-Stat: 3.2

Mean Reversion: No

Volume Pressure: +0.45

Probabilities:

→ Strong Bull: 50%

→ Weak Bull: 25%

→ Consolidation: 20%

→ Bears: 5%

Interpretation:

- Strong uptrend (t-stat 3.2 >> 1.96)

- No mean reversion = trends can continue

- Strong buying pressure (0.45 > 0.3)

- 75% chance stays bullish (50% + 25%)

Action:

- Full position size on long setups

- Use trend-following entries

- Wider stops (2x ATR)

- High conviction trades

Example 2: Weak Bull Before Consolidation

Dashboard shows:

Current Regime: Weak Bull

Drift: +8% annualized

T-Stat: 1.2

Mean Reversion: Yes

Volume Pressure: +0.15

Probabilities:

→ Strong Bull: 10%

→ Weak Bull: 30%

→ Consolidation: 50%

→ Weak Bear: 10%

Interpretation:

- Weak drift (t-stat 1.2 < 1.96)

- Mean reversion detected = range-bound likely

- Weak volume (0.15 < 0.3)

- 50% chance of consolidation

Action:

- Reduce long positions

- Tighten stops

- Prepare for range-bound trading

- Avoid new trend trades

Example 3: Regime Transition Alert

Previous: Weak Bull

Current: Consolidation

Volume divergence signal appeared:

Price made new high, volume delta weakened

Interpretation:

- Trend exhausted

- Buyers losing control

- Regime confirmed the transition

Action:

- Exit trend-following longs

- Switch to range-trading approach

- Wait for new regime before new directional trades

Settings Guide

### Regime Detection Period (50)

Number of bars for statistical calculations.

- **30-40:** More responsive, catches changes faster, more regime switches

- **50 (default):** Balanced for daily/4H charts

- **75-100:** More stable, fewer false regime changes, slower to adapt

Transition History Depth (100)

How much history to use for probabilities.

- **50-75:** Adapts quickly to recent behavior

- **100 (default):** Balanced robustness

- **150-200:** More stable probabilities, slower to adapt

Volume Delta Period (14)

Period for volume calculations.

- **7-10:** More sensitive to volume shifts

- **14 (default):** Standard period

- **20-30:** Smoother, less noise

Significance Threshold (1.96)

T-statistic required for trend classification.

- **1.64:** 90% confidence, more trend regimes detected

- **1.96 (default):** 95% confidence, balanced

- **2.58:** 99% confidence, very conservative, mostly consolidation

Best Practices

Do:

- Wait for regime confirmation (at least 3-5 bars in new regime)

- Use probabilities to size positions appropriately

- Combine with support/resistance for entries

- Respect mean reversion signals

- Adapt strategy to current regime

Don't:

- Trade every regime change immediately

- Ignore high transition probabilities

- Use trend strategies in consolidation

- Override statistical signals with gut feel

- Trade against Strong regimes without clear setup

Timeframe Recommendations

Daily Charts:

- Default settings work well

- Most reliable regime detection

- Best for swing trading

4H Charts:

- Use default or slightly higher lookback (60-75)

- Good for active swing trading

- More regime changes than daily

1H Charts:

- Reduce lookback to 30-40

- More noise, use with caution

- Better for intraday position trading

15M and below:

- Not recommended

- Too much noise for statistical validity

- Regimes change too frequently

Combining with Other Indicators

Works Well With:

Moving Averages

- Use regime for directional bias

- MAs for specific entry/exit points

Support/Resistance

- Regime shows context

- S/R shows specific levels

- High probability at confluence

Volume Profile

- Regime shows regime

- Profile shows where volume is

- Target high-volume nodes

RSI/MACD

- Regime provides context

- Momentum shows entry timing

- Combine for higher probability

Example Combined Setup

Regime: Strong Bull

Price: Above 200 MA

Level: Pullback to support

RSI: Oversold (30)

Volume Delta: Still positive

Setup: Long entry

Reason: Trend intact, healthy pullback, buyers still present

Divergence Signals

The indicator shows volume divergence warnings:

Bearish Divergence (Red Triangle Down)

- Price makes new high

- Volume delta makes lower high

- Warning: Buyers weakening, potential reversal

Bullish Divergence (Green Triangle Up)

- Price makes new low

- Volume delta makes higher low

- Warning: Sellers weakening, potential reversal

How to use:

- Divergence in Strong regime = early warning of regime change

- Confirms when regime actually transitions

- Don't trade divergence alone, wait for regime confirmation

Limitations

This Indicator Cannot:

**Predict black swan events** - Unexpected news overrides all technical regimes

**Work in all markets** - Needs liquid markets with reliable volume data

**Guarantee profits** - Probabilities are not certainties

**Replace fundamental analysis** - Technical regimes can diverge from fundamentals

Works Best:

- Liquid markets (major indices, forex, crypto, large-cap stocks)

- Daily and 4H timeframes

- Combined with other analysis

- With proper risk management

- In normal market conditions

Common Questions

"Why did the regime stay consolidation despite strong price move?"

The indicator detected mean reversion (variance ratio < 0.8), indicating the move will likely reverse. Or the move wasn't statistically significant (t-stat < 1.96). Trust the statistics over visual appearance.

"Probabilities show 30% for each regime. What does that mean?"

High uncertainty. The market is at an inflection point. Reduce position sizes and wait for clearer regime formation.

"Can I use this for day trading?"

Not recommended on timeframes below 1H. Statistical tests need sufficient data. Better suited for swing trading.

"Why does this show Strong Bull when my momentum indicators show weakness?"

Momentum can weaken while the trend remains statistically significant. The indicator focuses on drift and volume, not momentum. Consider it a different perspective.

Technical Notes

Volume Delta Approximation

Uses OHLCV data to approximate order flow:

- Buy volume ≈ Volume on up-closes

- Sell volume ≈ Volume on down-closes

- Delta = Buy - Sell

**Note:** Real order flow (from futures or Level 2) is more precise. This approximation works well on liquid markets.

Statistical Tests

Drift T-Test:

- Null hypothesis: No drift (mean return = 0)

- Reject if |t-stat| > threshold

- Based on standard hypothesis testing

Variance Ratio:

- Compares 2-period variance to 1-period variance

- Ratio = 1 for random walk

- Ratio < 1 for mean reversion

- Threshold of 0.8 based on empirical testing

Transition Probability Implementation

Due to Pine Script v5 limitations (no native 2D arrays), the 5×5 transition matrix is stored as a flat 1D array of 25 elements:

- Position maps to index: `row × 5 + col`

- Example: Transition from Regime 2 to Regime 4 is at index `1 × 5 + 3 = 8`

- Laplace smoothing (0.1) prevents zero probabilities

- Row sums normalized to calculate probabilities

This approach is computationally efficient and maintains statistical accuracy.

No Repainting

All calculations confirmed on bar close. Regime changes appear when the bar closes, not during formation. Historical analysis is accurate.

Alert Conditions

Regime Change

- Triggers when regime transitions to any new state

- Message shows new regime number (1-5)

Bearish Divergence

- Triggers when price makes new high but volume delta doesn't confirm

Bullish Divergence

- Triggers when price makes new low but volume delta doesn't confirm

Disclaimer

FOR EDUCATIONAL PURPOSES ONLY

This indicator uses statistical methods to analyze market regimes. It does not predict the future or guarantee trading success.

Markets are probabilistic, not deterministic. A 70% probability of staying bullish means 30% chance of regime change. Always use proper risk management.

Past regime transitions do not guarantee future transitions. Market structure can change. Statistical relationships can break down.

Never risk more than you can afford to lose. Use stop losses on every trade. Test thoroughly before live trading. Consult a qualified financial advisor.

© 2026 | Open Source

Statistical rigor meets practical application

Bifurcation Zone - CAEBifurcation Zone — Cognitive Adversarial Engine (BZ-CAE)

Bifurcation Zone — CAE (BZ-CAE) is a next-generation divergence detection system enhanced by a Cognitive Adversarial Engine that evaluates both sides of every potential trade before presenting signals. Unlike traditional divergence indicators that show every price-oscillator disagreement regardless of context, BZ-CAE applies comprehensive market-state intelligence to identify only the divergences that occur in favorable conditions with genuine probability edges.

The system identifies structural bifurcation points — critical junctures where price and momentum disagree, signaling potential reversals or continuations — then validates these opportunities through five interconnected intelligence layers: Trend Conviction Scoring , Directional Momentum Alignment , Multi-Factor Exhaustion Modeling , Adversarial Validation , and Confidence Scoring . The result is a selective, context-aware signal system that filters noise and highlights high-probability setups.

This is not a "buy the arrow" indicator. It's a decision support framework that teaches you how to read market state, evaluate divergence quality, and make informed trading decisions based on quantified intelligence rather than hope.

What Sets BZ-CAE Apart: Technical Architecture

The Problem With Traditional Divergence Indicators

Most divergence indicators operate on a simple rule: if price makes a higher high and RSI makes a lower high, show a bearish signal. If price makes a lower low and RSI makes a higher low, show a bullish signal. This creates several critical problems:

Context Blindness : They show counter-trend signals in powerful trends that rarely reverse, leading to repeated losses as you fade momentum.

Signal Spam : Every minor price-oscillator disagreement generates an alert, overwhelming you with low-quality setups and creating analysis paralysis.

No Quality Ranking : All signals are treated identically. A marginal divergence in choppy conditions receives the same visual treatment as a high-conviction setup at a major exhaustion point.

Single-Sided Evaluation : They ask "Is this a good long?" without checking if the short case is overwhelmingly stronger, leading you into obvious bad trades.

Static Configuration : You manually choose RSI 14 or Stochastic 14 and hope it works, with no systematic way to validate if that's optimal for your instrument.

BZ-CAE's Solution: Cognitive Adversarial Intelligence

BZ-CAE solves these problems through an integrated five-layer intelligence architecture:

1. Trend Conviction Score (TCS) — 0 to 1 Scale

Most indicators check if ADX is above 25 to determine "trending" conditions. This binary approach misses nuance. TCS is a weighted composite metric:

Formula : 0.35 × normalize(ADX, 10, 35) + 0.35 × structural_strength + 0.30 × htf_alignment

Structural Strength : 10-bar SMA of consecutive directional bars. Captures persistence — are bulls or bears consistently winning?

HTF Alignment : Multi-timeframe EMA stacking (20/50/100/200). When all EMAs align in the same direction, you're in institutional trend territory.

Purpose : Quantifies how "locked in" the trend is. When TCS exceeds your threshold (default 0.80), the system knows to avoid counter-trend trades unless other factors override.

Interpretation :

TCS > 0.85: Very strong trend — counter-trading is extremely high risk

TCS 0.70-0.85: Strong trend — favor continuation, require exhaustion for reversals

TCS 0.50-0.70: Moderate trend — context matters, both directions viable

TCS < 0.50: Weak/choppy — reversals more viable, range-bound conditions

2. Directional Momentum Alignment (DMA) — ATR-Normalized

Formula : (EMA21 - EMA55) / ATR14

This isn't just "price above EMA" — it's a regime-aware momentum gauge. The same $100 price movement reads completely differently in high-volatility crypto versus low-volatility forex. By normalizing with ATR, DMA adapts its interpretation to current market conditions.

Purpose : Quantifies the directional "force" behind current price action. Positive = bullish push, negative = bearish push. Magnitude = strength.

Interpretation :

DMA > 0.7: Strong bullish momentum — bearish divergences risky

DMA 0.3 to 0.7: Moderate bullish bias

DMA -0.3 to 0.3: Balanced/choppy conditions

DMA -0.7 to -0.3: Moderate bearish bias

DMA < -0.7: Strong bearish momentum — bullish divergences risky

3. Multi-Factor Exhaustion Modeling — 0 to 1 Probability

Single-metric exhaustion detection (like "RSI > 80") misses complex market states. BZ-CAE aggregates five independent exhaustion signals:

Volume Spikes : Current volume versus 50-bar average

2.5x average: 0.25 weight

2.0x average: 0.15 weight

1.5x average: 0.10 weight

Divergence Present : The fact that a divergence exists contributes 0.30 weight — structural momentum disagreement is itself an exhaustion signal.

RSI Extremes : Captures oscillator climax zones

RSI > 80 or < 20: 0.25 weight

RSI > 75 or < 25: 0.15 weight

Pin Bar Detection : Identifies rejection candles (2:1 wick-to-body ratio, indicating failed breakout attempts): 0.15 weight

Extended Runs : Consecutive bars above/below EMA20 without pullback

30+ bars: 0.15 weight (market hasn't paused to consolidate)

Total exhaustion score is the sum of all applicable weights, capped at 1.0.

Purpose : Detects when strong trends become vulnerable to reversal. High exhaustion can override trend filters, allowing counter-trend trades at genuine turning points that basic indicators would miss.

Interpretation :

Exhaustion > 0.75: High probability of climax — yellow background shading alerts you visually

Exhaustion 0.50-0.75: Moderate overextension — watch for confirmation

Exhaustion < 0.50: Fresh move — trend can continue, counter-trend trades higher risk

4. Adversarial Validation — Game Theory Applied to Trading

This is BZ-CAE's signature innovation. Before approving any signal, the engine quantifies BOTH sides of the trade simultaneously:

For Bullish Divergences , it calculates:

Bull Case Score (0-1+) :

Distance below EMA20 (pullback quality): up to 0.25

Bullish EMA alignment (close > EMA20 > EMA50): 0.25

Oversold RSI (< 40): 0.25

Volume confirmation (> 1.2x average): 0.25

Bear Case Score (0-1+) :

Price below EMA50 (structural weakness): 0.30

Very oversold RSI (< 30, indicating knife-catching): 0.20

Differential = Bull Case - Bear Case

If differential < -0.10 (default threshold), the bear case is dominating — signal is BLOCKED or ANNOTATED.

For Bearish Divergences , the logic inverts (Bear Case vs Bull Case).

Purpose : Prevents trades where you're fighting obvious strength in the opposite direction. This is institutional-grade risk management — don't just evaluate your trade, evaluate the counter-trade simultaneously.

Why This Matters : You might see a bullish divergence at a local low, but if price is deeply below major support EMAs with strong bearish momentum, you're catching a falling knife. The adversarial check catches this and blocks the signal.

5. Confidence Scoring — 0 to 1 Quality Assessment

Every signal that passes initial filters receives a comprehensive quality score:

Formula :

0.30 × normalize(TCS) // Trend context

+ 0.25 × normalize(|DMA|) // Momentum magnitude

+ 0.20 × pullback_quality // Entry distance from EMA20

+ 0.15 × state_quality // ADX + alignment + structure

+ 0.10 × divergence_strength // Slope separation magnitude

+ adversarial_bonus (0-0.30) // Your side's advantage

Purpose : Ranks setup quality for filtering and position sizing decisions. You can set a minimum confidence threshold (default 0.35) to ensure only quality setups reach your chart.

Interpretation :

Confidence > 0.70: Premium setup — consider increased position size

Confidence 0.50-0.70: Good quality — standard size

Confidence 0.35-0.50: Acceptable — reduced size or skip if conservative

Confidence < 0.35: Marginal — blocked in Filtering mode, annotated in Advisory mode

CAE Operating Modes: Learning vs Enforcement

Off : Disables all CAE logic. Raw divergence pipeline only. Use for baseline comparison.

Advisory : Shows ALL signals regardless of CAE evaluation, but annotates signals that WOULD be blocked with specific warnings (e.g., "Bull: strong downtrend (TCS=0.87)" or "Adversarial bearish"). This is your learning mode — see CAE's decision logic in action without missing educational opportunities.

Filtering : Actively blocks low-quality signals. Only setups that pass all enabled gates (Trend Filter, Adversarial Validation, Confidence Gating) reach your chart. This is your live trading mode — trust the system to enforce discipline.

CAE Filter Gates: Three-Layer Protection

When CAE is enabled, signals must pass through three independent gates (each can be toggled on/off):

Gate 1: Strong Trend Filter

If TCS ≥ tcs_threshold (default 0.80)

And signal is counter-trend (bullish in downtrend or bearish in uptrend)

And exhaustion < exhaustion_required (default 0.50)

Then: BLOCK signal

Logic: Don't fade strong trends unless the move is clearly overextended

Gate 2: Adversarial Validation

Calculate both bull case and bear case scores

If opposing case dominates by more than adv_threshold (default 0.10)

Then: BLOCK signal

Logic: Avoid trades where you're fighting obvious strength in the opposite direction

Gate 3: Confidence Gating

Calculate composite confidence score (0-1)

If confidence < min_confidence (default 0.35)

Then: In Filtering mode, BLOCK signal; in Advisory mode, ANNOTATE with warning

Logic: Only take setups with minimum quality threshold

All three gates work together. A signal must pass ALL enabled gates to fire.

Visual Intelligence System

Bifurcation Zones (Supply/Demand Blocks)

When a divergence signal fires, BZ-CAE draws a semi-transparent box extending 15 bars forward from the signal pivot:

Demand Zones (Bullish) : Theme-colored box (cyan in Cyberpunk, blue in Professional, etc.) labeled "Demand" — marks where smart money likely placed buy orders as price diverged at the low.

Supply Zones (Bearish) : Theme-colored box (magenta in Cyberpunk, orange in Professional) labeled "Supply" — marks where smart money likely placed sell orders as price diverged at the high.

Theory : Divergences represent institutional disagreement with the crowd. The crowd pushed price to an extreme (new high or low), but momentum (oscillator) is waning, indicating smart money is taking the opposite side. These zones mark order placement areas that become future support/resistance.

Use Cases :

Exit targets: Take profit when price returns to opposite-side zone

Re-entry levels: If price returns to your entry zone, consider adding

Stop placement: Place stops just beyond your zone (below demand, above supply)

Auto-Cleanup : System keeps the last 20 zones to prevent chart clutter.

Adversarial Bar Coloring — Real-Time Market Debate Heatmap

Each bar is colored based on the Bull Case vs Bear Case differential:

Strong Bull Advantage (diff > 0.3): Full theme bull color (e.g., cyan)

Moderate Bull Advantage (diff > 0.1): 50% transparency bull

Neutral (diff -0.1 to 0.1): Gray/neutral theme

Moderate Bear Advantage (diff < -0.1): 50% transparency bear

Strong Bear Advantage (diff < -0.3): Full theme bear color (e.g., magenta)

This creates a real-time visual heatmap showing which side is "winning" the market debate. When bars flip from cyan to magenta (or vice versa), you're witnessing a shift in adversarial advantage — a leading indicator of potential momentum changes.

Exhaustion Shading

When exhaustion score exceeds 0.75, the chart background displays a semi-transparent yellow highlight. This immediate visual warning alerts you that the current move is at high risk of reversal, even if trend indicators remain strong.

Visual Themes — Six Aesthetic Options

Cyberpunk : Cyan/Magenta/Yellow — High contrast, neon aesthetic, excellent for dark-themed trading environments

Professional : Blue/Orange/Green — Corporate color palette, suitable for presentations and professional documentation

Ocean : Teal/Red/Cyan — Aquatic palette, calming for extended monitoring sessions

Fire : Orange/Red/Coral — Warm aggressive colors, high energy

Matrix : Green/Red/Lime — Code aesthetic, homage to classic hacker visuals

Monochrome : White/Gray — Minimal distraction, maximum focus on price action

All visual elements (signal markers, zones, bar colors, dashboard) adapt to your selected theme.

Divergence Engine — Core Detection System

What Are Divergences?

Divergences occur when price action and momentum indicators disagree, creating structural tension that often resolves in a change of direction:

Regular Divergence (Reversal Signal) :

Bearish Regular : Price makes higher high, oscillator makes lower high → Potential trend reversal down

Bullish Regular : Price makes lower low, oscillator makes higher low → Potential trend reversal up

Hidden Divergence (Continuation Signal) :

Bearish Hidden : Price makes lower high, oscillator makes higher high → Downtrend continuation

Bullish Hidden : Price makes higher low, oscillator makes lower low → Uptrend continuation

Both types can be enabled/disabled independently in settings.

Pivot Detection Methods

BZ-CAE uses symmetric pivot detection with separate lookback and lookforward periods (default 5/5):

Pivot High : Bar where high > all highs within lookback range AND high > all highs within lookforward range

Pivot Low : Bar where low < all lows within lookback range AND low < all lows within lookforward range

This ensures structural validity — the pivot must be a clear local extreme, not just a minor wiggle.

Divergence Validation Requirements

For a divergence to be confirmed, it must satisfy:

Slope Disagreement : Price slope and oscillator slope must move in opposite directions (for regular divs) or same direction with inverted highs/lows (for hidden divs)

Minimum Slope Change : |osc_slope| > min_slope_change / 100 (default 1.0) — filters weak, marginal divergences

Maximum Lookback Range : Pivots must be within max_lookback bars (default 60) — prevents ancient, irrelevant divergences

ATR-Normalized Strength : Divergence strength = min(|price_slope| × |osc_slope| × 10, 1.0) — quantifies the magnitude of disagreement in volatility context

Regular divergences receive 1.0× weight; hidden divergences receive 0.8× weight (slightly less reliable historically).

Oscillator Options — Five Professional Indicators

RSI (Relative Strength Index) : Classic overbought/oversold momentum indicator. Best for: General purpose divergence detection across all instruments.

Stochastic : Range-bound %K momentum comparing close to high-low range. Best for: Mean reversion strategies and range-bound markets.

CCI (Commodity Channel Index) : Measures deviation from statistical mean, auto-normalized to 0-100 scale. Best for: Cyclical instruments and commodities.

MFI (Money Flow Index) : Volume-weighted RSI incorporating money flow. Best for: Volume-driven markets like stocks and crypto.

Williams %R : Inverse stochastic looking back over period, auto-adjusted to 0-100. Best for: Reversal detection at extremes.

Each oscillator has adjustable length (2-200, default 14) and smoothing (1-20, default 1). You also set overbought (50-100, default 70) and oversold (0-50, default 30) thresholds.

Signal Timing Modes — Understanding Repainting

BZ-CAE offers two timing policies with complete transparency about repainting behavior:

Realtime (1-bar, peak-anchored)

How It Works :

Detects peaks 1 bar ago using pattern: high > high AND high > high

Signal prints on the NEXT bar after peak detection (bar_index)

Visual marker anchors to the actual PEAK bar (bar_index - 1, offset -1)

Signal locks in when bar CONFIRMS (closes)

Repainting Behavior :

On the FORMING bar (before close), the peak condition may change as new prices arrive

Once bar CLOSES (barstate.isconfirmed), signal is locked permanently

This is preview/early warning behavior by design

Best For :

Active monitoring and immediate alerts

Learning the system (seeing signals develop in real-time)

Responsive entry if you're watching the chart live

Confirmed (lookforward)

How It Works :

Uses Pine Script's built-in ta.pivothigh() and ta.pivotlow() functions

Requires full pivot validation period (lookback + lookforward bars)

Signal prints pivot_lookforward bars after the actual peak (default 5-bar delay)

Visual marker anchors to the actual peak bar (offset -pivot_lookforward)

No Repainting Behavior

Best For :

Backtesting and historical analysis

Conservative entries requiring full confirmation

Automated trading systems

Swing trading with larger timeframes

Tradeoff :

Delayed entry by pivot_lookforward bars (typically 5 bars)

On a 5-minute chart, this is a 25-minute delay

On a 4-hour chart, this is a 20-hour delay

Recommendation : Use Confirmed for backtesting to verify system performance honestly. Use Realtime for live monitoring only if you're actively watching the chart and understand pre-confirmation repainting behavior.

Signal Spacing System — Anti-Spam Architecture

Even after CAE filtering, raw divergences can cluster. The spacing system enforces separation:

Three Independent Filters

1. Min Bars Between ANY Signals (default 12):

Prevents rapid-fire clustering across both directions

If last signal (bull or bear) was within N bars, block new signal

Ensures breathing room between all setups

2. Min Bars Between SAME-SIDE Signals (default 24, optional enforcement):

Prevents bull-bull or bear-bear spam

Separate tracking for bullish and bearish signal timelines

Toggle enforcement on/off

3. Min ATR Distance From Last Signal (default 0, optional):

Requires price to move N × ATR from last signal location

Ensures meaningful price movement between setups

0 = disabled, 0.5-2.0 = typical range for enabled

All three filters work independently. A signal must pass ALL enabled filters to proceed.

Practical Guidance :

Scalping (1-5m) : Any 6-10, Same-side 12-20, ATR 0-0.5

Day Trading (15m-1H) : Any 12, Same-side 24, ATR 0-1.0

Swing Trading (4H-D) : Any 20-30, Same-side 40-60, ATR 1.0-2.0

Dashboard — Real-Time Control Center

The dashboard (toggleable, four corner positions, three sizes) provides comprehensive system intelligence:

Oscillator Section

Current oscillator type and value

State: OVERBOUGHT / OVERSOLD / NEUTRAL (color-coded)

Length parameter

Cognitive Engine Section

TCS (Trend Conviction Score) :

Current value with emoji state indicator

🔥 = Strong trend (>0.75)

📊 = Moderate trend (0.50-0.75)

〰️ = Weak/choppy (<0.50)

Color: Red if above threshold (trend filter active), yellow if moderate, green if weak

DMA (Directional Momentum Alignment) :

Current value with emoji direction indicator

🐂 = Bullish momentum (>0.5)

⚖️ = Balanced (-0.5 to 0.5)

🐻 = Bearish momentum (<-0.5)

Color: Green if bullish, red if bearish

Exhaustion :

Current value with emoji warning indicator

⚠️ = High exhaustion (>0.75)

🟡 = Moderate (0.50-0.75)

✓ = Low (<0.50)

Color: Red if high, yellow if moderate, green if low

Pullback :

Quality of current distance from EMA20

Values >0.6 are ideal entry zones (not too close, not too far)

Bull Case / Bear Case (if Adversarial enabled):

Current scores for both sides of the market debate

Differential with emoji indicator:

📈 = Bull advantage (>0.2)

➡️ = Balanced (-0.2 to 0.2)

📉 = Bear advantage (<-0.2)

Last Signal Metrics Section (New Feature)

When a signal fires, this section captures and displays:

Signal type (BULL or BEAR)

Bars elapsed since signal

Confidence % at time of signal

TCS value at signal time

DMA value at signal time

Purpose : Provides a historical reference for learning. You can see what the market state looked like when the last signal fired, helping you correlate outcomes with conditions.

Statistics Section

Total Signals : Lifetime count across session

Blocked Signals : Count and percentage (filter effectiveness metric)

Bull Signals : Total bullish divergences

Bear Signals : Total bearish divergences

Purpose : System health monitoring. If blocked % is very high (>60%), filters may be too strict. If very low (<10%), filters may be too loose.

Advisory Annotations

When CAE Mode = Advisory, this section displays warnings for signals that would be blocked in Filtering mode:

Examples:

"Bull spacing: wait 8 bars"

"Bear: strong uptrend (TCS=0.87)"

"Adversarial bearish"

"Low confidence 32%"

Multiple warnings can stack, separated by " | ". This teaches you CAE's decision logic transparently.

How to Use BZ-CAE — Complete Workflow

Phase 1: Initial Setup (First Session)

Apply BZ-CAE to your chart

Select your preferred Visual Theme (Cyberpunk recommended for visibility)

Set Signal Timing to "Confirmed (lookforward)" for learning

Choose your Oscillator Type (RSI recommended for general use, length 14)

Set Overbought/Oversold to 70/30 (standard)

Enable both Regular Divergence and Hidden Divergence

Set Pivot Lookback/Lookforward to 5/5 (balanced structure)

Enable CAE Intelligence

Set CAE Mode to "Advisory" (learning mode)

Enable all three CAE filters: Strong Trend Filter , Adversarial Validation , Confidence Gating

Enable Show Dashboard , position Top Right, size Normal

Enable Draw Bifurcation Zones and Adversarial Bar Coloring

Phase 2: Learning Period (Weeks 1-2)

Goal : Understand how CAE evaluates market state and filters signals.

Activities :

Watch the dashboard during signals :

Note TCS values when counter-trend signals fail — this teaches you the trend strength threshold for your instrument

Observe exhaustion patterns at actual turning points — learn when overextension truly matters

Study adversarial differential at signal times — see when opposing cases dominate

Review blocked signals (orange X-crosses):

In Advisory mode, you see everything — signals that would pass AND signals that would be blocked

Check the advisory annotations to understand why CAE would block

Track outcomes: Were the blocks correct? Did those signals fail?

Use Last Signal Metrics :

After each signal, check the dashboard capture of confidence, TCS, and DMA

Journal these values alongside trade outcomes

Identify patterns: Do confidence >0.70 signals work better? Does your instrument respect TCS >0.85?

Understand your instrument's "personality" :

Trending instruments (indices, major forex) may need TCS threshold 0.85-0.90

Choppy instruments (low-cap stocks, exotic pairs) may work best with TCS 0.70-0.75

High-volatility instruments (crypto) may need wider spacing

Low-volatility instruments may need tighter spacing

Phase 3: Calibration (Weeks 3-4)

Goal : Optimize settings for your specific instrument, timeframe, and style.

Calibration Checklist :

Min Confidence Threshold :

Review confidence distribution in your signal journal

Identify the confidence level below which signals consistently fail

Set min_confidence slightly above that level

Day trading : 0.35-0.45

Swing trading : 0.40-0.55

Scalping : 0.30-0.40

TCS Threshold :

Find the TCS level where counter-trend signals consistently get stopped out

Set tcs_threshold at or slightly below that level

Trending instruments : 0.85-0.90

Mixed instruments : 0.80-0.85

Choppy instruments : 0.75-0.80

Exhaustion Override Level :

Identify exhaustion readings that marked genuine reversals

Set exhaustion_required just below the average

Typical range : 0.45-0.55

Adversarial Threshold :

Default 0.10 works for most instruments

If you find CAE is too conservative (blocking good trades), raise to 0.15-0.20

If signals are still getting caught in opposing momentum, lower to 0.07-0.09

Spacing Parameters :

Count bars between quality signals in your journal

Set min bars ANY to ~60% of that average

Set min bars SAME-SIDE to ~120% of that average

Scalping : Any 6-10, Same 12-20

Day trading : Any 12, Same 24

Swing : Any 20-30, Same 40-60

Oscillator Selection :

Try different oscillators for 1-2 weeks each

Track win rate and average winner/loser by oscillator type

RSI : Best for general use, clear OB/OS

Stochastic : Best for range-bound, mean reversion

MFI : Best for volume-driven markets

CCI : Best for cyclical instruments

Williams %R : Best for reversal detection

Phase 4: Live Deployment

Goal : Disciplined execution with proven, calibrated system.

Settings Changes :

Switch CAE Mode from Advisory to Filtering

System now actively blocks low-quality signals

Only setups passing all gates reach your chart

Keep Signal Timing on Confirmed for conservative entries

OR switch to Realtime if you're actively monitoring and want faster entries (accept pre-confirmation repaint risk)

Use your calibrated thresholds from Phase 3

Enable high-confidence alerts: "⭐ High Confidence Bullish/Bearish" (>0.70)

Trading Discipline Rules :

Respect Blocked Signals :

If CAE blocks a trade you wanted to take, TRUST THE SYSTEM

Don't manually override — if you consistently disagree, return to Phase 2/3 calibration

The block exists because market state failed intelligence checks

Confidence-Based Position Sizing :

Confidence >0.70: Standard or increased size (e.g., 1.5-2.0% risk)

Confidence 0.50-0.70: Standard size (e.g., 1.0% risk)

Confidence 0.35-0.50: Reduced size (e.g., 0.5% risk) or skip if conservative

TCS-Based Management :

High TCS + counter-trend signal: Use tight stops, quick exits (you're fading momentum)

Low TCS + reversal signal: Use wider stops, trail aggressively (genuine reversal potential)

Exhaustion Awareness :

Exhaustion >0.75 (yellow shading): Market is overextended, reversal risk is elevated — consider early exit or tighter trailing stops even on winning trades

Exhaustion <0.30: Continuation bias — hold for larger move, wide trailing stops

Adversarial Context :

Strong differential against you (e.g., bullish signal with bear diff <-0.2): Use very tight stops, consider skipping

Strong differential with you (e.g., bullish signal with bull diff >0.2): Trail aggressively, this is your tailwind

Practical Settings by Timeframe & Style

Scalping (1-5 Minute Charts)

Objective : High frequency, tight stops, quick reversals in fast-moving markets.

Oscillator :

Type: RSI or Stochastic (fast response to quick moves)

Length: 9-11 (more responsive than standard 14)

Smoothing: 1 (no lag)

OB/OS: 65/35 (looser thresholds ensure frequent crossings in fast conditions)

Divergence :

Pivot Lookback/Lookforward: 3/3 (tight structure, catch small swings)

Max Lookback: 40-50 bars (recent structure only)

Min Slope Change: 0.8-1.0 (don't be overly strict)

CAE :

Mode: Advisory first (learn), then Filtering

Min Confidence: 0.30-0.35 (lower bar for speed, accept more signals)

TCS Threshold: 0.70-0.75 (allow more counter-trend opportunities)

Exhaustion Required: 0.45-0.50 (moderate override)

Strong Trend Filter: ON (still respect major intraday trends)

Adversarial: ON (critical for scalping protection — catches bad entries quickly)

Spacing :

Min Bars ANY: 6-10 (fast pace, many setups)

Min Bars SAME-SIDE: 12-20 (prevent clustering)

Min ATR Distance: 0 or 0.5 (loose)

Timing : Realtime (speed over precision, but understand repaint risk)

Visuals :

Signal Size: Tiny (chart clarity in busy conditions)

Show Zones: Optional (can clutter on low timeframes)

Bar Coloring: ON (helps read momentum shifts quickly)

Dashboard: Small size (corner reference, not main focus)

Key Consideration : Scalping generates noise. Even with CAE, expect lower win rate (45-55%) but aim for favorable R:R (2:1 or better). Size conservatively.

Day Trading (15-Minute to 1-Hour Charts)

Objective : Balance quality and frequency. Standard divergence trading approach.

Oscillator :

Type: RSI or MFI (proven reliability, volume confirmation with MFI)

Length: 14 (industry standard, well-studied)

Smoothing: 1-2

OB/OS: 70/30 (classic levels)

Divergence :

Pivot Lookback/Lookforward: 5/5 (balanced structure)

Max Lookback: 60 bars

Min Slope Change: 1.0 (standard strictness)

CAE :

Mode: Filtering (enforce discipline from the start after brief Advisory learning)

Min Confidence: 0.35-0.45 (quality filter without being too restrictive)

TCS Threshold: 0.80-0.85 (respect strong trends)

Exhaustion Required: 0.50 (balanced override threshold)

Strong Trend Filter: ON

Adversarial: ON

Confidence Gating: ON (all three filters active)

Spacing :

Min Bars ANY: 12 (breathing room between all setups)

Min Bars SAME-SIDE: 24 (prevent bull/bear clusters)

Min ATR Distance: 0-1.0 (optional refinement, typically 0.5-1.0)

Timing : Confirmed (1-bar delay for reliability, no repainting)

Visuals :

Signal Size: Tiny or Small

Show Zones: ON (useful reference for exits/re-entries)

Bar Coloring: ON (context awareness)

Dashboard: Normal size (full visibility)

Key Consideration : This is the "sweet spot" timeframe for BZ-CAE. Market structure is clear, CAE has sufficient data, and signal frequency is manageable. Expect 55-65% win rate with proper execution.

Swing Trading (4-Hour to Daily Charts)

Objective : Quality over quantity. High conviction only. Larger stops and targets.

Oscillator :

Type: RSI or CCI (robust on higher timeframes, smooth longer waves)

Length: 14-21 (capture larger momentum swings)

Smoothing: 1-3

OB/OS: 70/30 or 75/25 (strict extremes)

Divergence :

Pivot Lookback/Lookforward: 5/5 or 7/7 (structural purity, major swings only)

Max Lookback: 80-100 bars (broader historical context)

Min Slope Change: 1.2-1.5 (require strong, undeniable divergence)

CAE :

Mode: Filtering (strict enforcement, premium setups only)

Min Confidence: 0.40-0.55 (high bar for entry)

TCS Threshold: 0.85-0.95 (very strong trend protection — don't fade established HTF trends)

Exhaustion Required: 0.50-0.60 (higher bar for override — only extreme exhaustion justifies counter-trend)

Strong Trend Filter: ON (critical on HTF)

Adversarial: ON (avoid obvious bad trades)

Confidence Gating: ON (quality gate essential)

Spacing :

Min Bars ANY: 20-30 (substantial separation)

Min Bars SAME-SIDE: 40-60 (significant breathing room)

Min ATR Distance: 1.0-2.0 (require meaningful price movement)

Timing : Confirmed (purity over speed, zero repaint for swing accuracy)

Visuals :

Signal Size: Small or Normal (clear markers on zoomed-out view)

Show Zones: ON (important HTF levels)

Bar Coloring: ON (long-term trend awareness)

Dashboard: Normal or Large (comprehensive analysis)

Key Consideration : Swing signals are rare but powerful. Expect 2-5 signals per month per instrument. Win rate should be 60-70%+ due to stringent filtering. Position size can be larger given confidence.

Dashboard Interpretation Reference

TCS (Trend Conviction Score) States

0.00-0.50: Weak/Choppy

Emoji: 〰️

Color: Green/cyan

Meaning: No established trend. Range-bound or consolidating. Both reversal and continuation signals viable.

Action: Reversals (regular divs) are safer. Use wider profit targets (market has room to move). Consider mean reversion strategies.

0.50-0.75: Moderate Trend

Emoji: 📊

Color: Yellow/neutral

Meaning: Developing trend but not locked in. Context matters significantly.

Action: Check DMA and exhaustion. If DMA confirms trend and exhaustion is low, favor continuation (hidden divs). If exhaustion is high, reversals are viable.

0.75-0.85: Strong Trend

Emoji: 🔥

Color: Orange/warning

Meaning: Well-established trend with persistence. Counter-trend is high risk.

Action: Require exhaustion >0.50 for counter-trend entries. Favor continuation signals. Use tight stops on counter-trend attempts.

0.85-1.00: Very Strong Trend

Emoji: 🔥🔥

Color: Red/danger (if counter-trading)

Meaning: Locked-in institutional trend. Extremely high risk to fade.

Action: Avoid counter-trend unless exhaustion >0.75 (yellow shading). Focus exclusively on continuation opportunities. Momentum is king here.

DMA (Directional Momentum Alignment) Zones

-2.0 to -1.0: Strong Bearish Momentum

Emoji: 🐻🐻

Color: Dark red

Meaning: Powerful downside force. Sellers are in control.

Action: Bullish divergences are counter-momentum (high risk). Bearish divergences are with-momentum (lower risk). Size down on longs.

-0.5 to 0.5: Neutral/Balanced

Emoji: ⚖️

Color: Gray/neutral

Meaning: No strong directional bias. Choppy or consolidating.

Action: Both directions have similar probability. Focus on confidence score and adversarial differential for edge.

1.0 to 2.0: Strong Bullish Momentum

Emoji: 🐂🐂

Color: Bright green/cyan

Meaning: Powerful upside force. Buyers are in control.

Action: Bearish divergences are counter-momentum (high risk). Bullish divergences are with-momentum (lower risk). Size down on shorts.

Exhaustion States

0.00-0.50: Fresh Move

Emoji: ✓

Color: Green

Meaning: Trend is healthy, not overextended. Room to run.

Action: Counter-trend trades are premature. Favor continuation. Hold winners for larger moves. Avoid early exits.

0.50-0.75: Mature Move

Emoji: 🟡

Color: Yellow

Meaning: Move is aging. Watch for signs of climax.

Action: Tighten trailing stops on winning trades. Be ready for reversals. Don't add to positions aggressively.

0.75-0.85: High Exhaustion

Emoji: ⚠️

Color: Orange

Background: Yellow shading appears

Meaning: Move is overextended. Reversal risk elevated significantly.

Action: Counter-trend reversals are higher probability. Consider early exits on with-trend positions. Size up on reversal divergences (if CAE allows).

0.85-1.00: Critical Exhaustion

Emoji: ⚠️⚠️

Color: Red

Background: Yellow shading intensifies

Meaning: Climax conditions. Reversal imminent or underway.

Action: Aggressive reversal trades justified. Exit all with-trend positions. This is where major turns occur.

Confidence Score Tiers

0.00-0.30: Low Quality

Color: Red

Status: Blocked in Filtering mode

Action: Skip entirely. Setup lacks fundamental quality across multiple factors.

0.30-0.50: Moderate Quality

Color: Yellow/orange

Status: Marginal — passes in Filtering only if >min_confidence

Action: Reduced position size (0.5-0.75% risk). Tight stops. Conservative profit targets. Skip if you're selective.

0.50-0.70: High Quality

Color: Green/cyan

Status: Good setup across most quality factors

Action: Standard position size (1.0-1.5% risk). Normal stops and targets. This is your bread-and-butter trade.

0.70-1.00: Premium Quality

Color: Bright green/gold

Status: Exceptional setup — all factors aligned

Visual: Double confidence ring appears

Action: Consider increased position size (1.5-2.0% risk, maximum). Wider stops. Larger targets. High probability of success. These are rare — capitalize when they appear.

Adversarial Differential Interpretation

Bull Differential > 0.3 :

Visual: Strong cyan/green bar colors

Meaning: Bull case strongly dominates. Buyers have clear advantage.

Action: Bullish divergences favored (with-advantage). Bearish divergences face headwind (reduce size or skip). Momentum is bullish.

Bull Differential 0.1 to 0.3 :

Visual: Moderate cyan/green transparency

Meaning: Moderate bull advantage. Buyers have edge but not overwhelming.

Action: Both directions viable. Slight bias toward longs.

Differential -0.1 to 0.1 :

Visual: Gray/neutral bars

Meaning: Balanced debate. No clear advantage either side.

Action: Rely on other factors (confidence, TCS, exhaustion) for direction. Adversarial is neutral.

Bear Differential -0.3 to -0.1 :

Visual: Moderate red/magenta transparency

Meaning: Moderate bear advantage. Sellers have edge but not overwhelming.

Action: Both directions viable. Slight bias toward shorts.

Bear Differential < -0.3 :

Visual: Strong red/magenta bar colors

Meaning: Bear case strongly dominates. Sellers have clear advantage.

Action: Bearish divergences favored (with-advantage). Bullish divergences face headwind (reduce size or skip). Momentum is bearish.

Last Signal Metrics — Post-Trade Analysis

After a signal fires, dashboard captures:

Type : BULL or BEAR

Bars Ago : How long since signal (updates every bar)

Confidence : What was the quality score at signal time

TCS : What was trend conviction at signal time

DMA : What was momentum alignment at signal time

Use Case : Post-trade journaling and learning.

Example: "BULL signal 12 bars ago. Confidence: 68%, TCS: 0.42, DMA: -0.85"

Analysis : This was a bullish reversal (regular div) with good confidence, weak trend (TCS), but strong bearish momentum (DMA). The bet was that momentum would reverse — a counter-momentum play requiring exhaustion confirmation. Check if exhaustion was high at that time to justify the entry.

Track patterns:

Do your best trades have confidence >0.65?

Do low-TCS signals (<0.50) work better for you?

Are you more successful with-momentum (DMA aligned with signal) or counter-momentum?

Troubleshooting Guide

Problem: No Signals Appearing

Symptoms : Chart loads, dashboard shows metrics, but no divergence signals fire.

Diagnosis Checklist :

Check dashboard oscillator value : Is it crossing OB/OS levels (70/30)? If oscillator stays in 40-60 range constantly, it can't reach extremes needed for divergence detection.

Are pivots forming? : Look for local swing highs/lows on your chart. If price is in tight consolidation, pivots may not meet lookback/lookforward requirements.

Is spacing too tight? : Check "Last Signal" metrics — how many bars since last signal? If <12 and your min_bars_ANY is 12, spacing filter is blocking.

Is CAE blocking everything? : Check dashboard Statistics section — what's the blocked signal count? High blocks indicate overly strict filters.

Solutions :

Loosen OB/OS Temporarily :

Try 65/35 to verify divergence detection works

If signals appear, the issue was threshold strictness

Gradually tighten back to 67/33, then 70/30 as appropriate

Lower Min Confidence :

Try 0.25-0.30 (diagnostic level)

If signals appear, filter was too strict

Raise gradually to find sweet spot (0.35-0.45 typical)

Disable Strong Trend Filter Temporarily :

Turn off in CAE settings

If signals appear, TCS threshold was blocking everything

Re-enable and lower TCS_threshold to 0.70-0.75

Reduce Min Slope Change :

Try 0.7-0.8 (from default 1.0)

Allows weaker divergences through

Helpful on low-volatility instruments

Widen Spacing :

Set min_bars_ANY to 6-8

Set min_bars_SAME_SIDE to 12-16

Reduces time between allowed signals

Check Timing Mode :

If using Confirmed, remember there's a pivot_lookforward delay (5+ bars)

Switch to Realtime temporarily to verify system is working

Realtime has no delay but repaints

Verify Oscillator Settings :

Length 14 is standard but might not fit all instruments

Try length 9-11 for faster response

Try length 18-21 for slower, smoother response

Problem: Too Many Signals (Signal Spam)

Symptoms : Dashboard shows 50+ signals in Statistics, confidence scores mostly <0.40, signals clustering close together.

Solutions :

Raise Min Confidence :

Try 0.40-0.50 (quality filter)

Blocks bottom-tier setups

Targets top 50-60% of divergences only

Tighten OB/OS :

Use 70/30 or 75/25

Requires more extreme oscillator readings

Reduces false divergences in mid-range

Increase Min Slope Change :

Try 1.2-1.5 (from default 1.0)

Requires stronger, more obvious divergences

Filters marginal slope disagreements

Raise TCS Threshold :

Try 0.85-0.90 (from default 0.80)

Stricter trend filter blocks more counter-trend attempts

Favors only strongest trend alignment

Enable ALL CAE Gates :

Turn on Trend Filter + Adversarial + Confidence

Triple-layer protection

Blocks aggressively — expect 20-40% reduction in signals

Widen Spacing :

min_bars_ANY: 15-20 (from 12)

min_bars_SAME_SIDE: 30-40 (from 24)

Creates substantial breathing room

Switch to Confirmed Timing :

Removes realtime preview noise

Ensures full pivot validation

5-bar delay filters many false starts

Problem: Signals in Strong Trends Get Stopped Out

Symptoms : You take a bullish divergence in a downtrend (or bearish in uptrend), and it immediately fails. Dashboard showed high TCS at the time.

Analysis : This is INTENDED behavior — CAE is protecting you from low-probability counter-trend trades.

Understanding :

Check Last Signal Metrics in dashboard — what was TCS when signal fired?

If TCS was >0.85 and signal was counter-trend, CAE correctly identified it as high risk

Strong trends rarely reverse cleanly without major exhaustion

Your losses here are the system working as designed (blocking bad odds)

If You Want to Override (Not Recommended) :

Lower TCS_threshold to 0.70-0.75 (allows more counter-trend)

Lower exhaustion_required to 0.40 (easier override)

Disable Strong Trend Filter entirely (very risky)

Better Approach :

TRUST THE FILTER — it's preventing costly mistakes

Wait for exhaustion >0.75 (yellow shading) before counter-trending strong TCS

Focus on continuation signals (hidden divs) in high-TCS environments

Use Advisory mode to see what CAE is blocking and learn from outcomes

Problem: Adversarial Blocking Seems Wrong

Symptoms : You see a divergence that "looks good" visually, but CAE blocks with "Adversarial bearish/bullish" warning.

Diagnosis :

Check dashboard Bull Case and Bear Case scores at that moment

Look at Differential value

Check adversarial bar colors — was there strong coloring against your intended direction?

Understanding :

Adversarial catches "obvious" opposing momentum that's easy to miss

Example: Bullish divergence at a local low, BUT price is deeply below EMA50, bearish momentum is strong, and RSI shows knife-catching conditions

Bull Case might be 0.20 while Bear Case is 0.55

Differential = -0.35, far beyond threshold

Block is CORRECT — you'd be fighting overwhelming opposing flow

If You Disagree Consistently

Review blocked signals on chart — scroll back and check outcomes

Did those blocked signals actually work, or did they fail as adversarial predicted?

Raise adv_threshold to 0.15-0.20 (more permissive, allows closer battles)

Disable Adversarial Validation temporarily (diagnostic) to isolate its effect

Use Advisory mode to learn adversarial patterns over 50-100 signals

Remember : Adversarial is conservative BY DESIGN. It prevents "obvious" bad trades where you're fighting strong strength the other way.

Problem: Dashboard Not Showing or Incomplete

Solutions :

Toggle "Show Dashboard" to ON in settings

Try different dashboard sizes (Small/Normal/Large)

Try different positions (Top Left/Right, Bottom Left/Right) — might be off-screen

Some sections require CAE Enable = ON (Cognitive Engine section won't appear if CAE is disabled)

Statistics section requires at least 1 lifetime signal to populate

Check that visual theme is set (dashboard colors adapt to theme)

Problem: Performance Lag, Chart Freezing

Symptoms : Chart loading is slow, indicator calculations cause delays, pinch-to-zoom lags.

Diagnosis : Visual features are computationally expensive, especially adversarial bar coloring (recalculates every bar).

Solutions (In Order of Impact) :

Disable Adversarial Bar Coloring (MOST EXPENSIVE):

Turn OFF "Adversarial Bar Coloring" in settings

This is the single biggest performance drain

Immediate improvement

Reduce Vertical Lines :

Lower "Keep last N vertical lines" to 20-30

Or set to 0 to disable entirely

Moderate improvement

Disable Bifurcation Zones :

Turn OFF "Draw Bifurcation Zones"

Reduces box drawing calculations

Moderate improvement

Set Dashboard Size to Small :

Smaller dashboard = fewer cells = less rendering

Minor improvement

Use Shorter Max Lookback :

Reduce max_lookback to 40-50 (from 60+)

Fewer bars to scan for divergences

Minor improvement

Disable Exhaustion Shading :

Turn OFF "Show Market State"

Removes background coloring calculations

Minor improvement

Extreme Performance Mode :

Disable ALL visual enhancements

Keep only triangle markers

Dashboard Small or OFF

Use Minimal theme if available

Problem: Realtime Signals Repainting

Symptoms : You see a signal appear, but on next bar it disappears or moves.

Explanation :

Realtime mode detects peaks 1 bar ago: high > high AND high > high

On the FORMING bar (before close), this condition can change as new prices arrive

Example: At 10:05, high (10:04 bar) was 100, current high is 99 → peak detected

At 10:05:30, new high of 101 arrives → peak condition breaks → signal disappears

At 10:06 (bar close), final high is 101 → no peak at 10:04 anymore → signal gone permanently

This is expected behavior for realtime responsiveness. You get preview/early warning, but it's not locked until bar confirms.

Solutions :

Use Confirmed Timing :

Switch to "Confirmed (lookforward)" mode

ZERO repainting — pivot must be fully validated

5-bar delay (pivot_lookforward)

What you see in history is exactly what would have appeared live

Accept Realtime Repaint as Tradeoff :

Keep Realtime mode for speed and alerts

Understand that pre-confirmation signals may vanish

Only trade signals that CONFIRM at bar close (check barstate.isconfirmed)

Use for live monitoring, NOT for backtesting

Trade Only After Confirmation :

In Realtime mode, wait 1 full bar after signal appears before entering