Indicators Combination Framework v3 IND [DTU]Hello All,

This script is a framework to analyze and see the results by combine selected indicators for (long, short, longexit, shortexit) conditions.

I was designed this for beginners and users to facilitate to see effects of the technical indicators combinations on the chart WITH NO CODE

You can improve your strategies according the results of this system by connecting the framework to a strategy framework/template such as Pinecoder, Benson, daveatt or custom.

This is enhanced version of my previous indicator "Indicators & Conditions Test Framework "

Currently there are 93 indicators (23 newly added) connected over library. You can also import an External Indicator or add Custom indicator (In the source)

It is possible to change it from Indicator to strategy (simple one) by just remarking strategy parts in the source code and see real time profit of your combinations

Feel free to change or use it in your source

Special thanks goes to Pine wizards: Trading view (built-in Indicators), @Rodrigo, @midtownsk8rguy, @Lazybear, @Daveatt and others for their open source codes and contributions

SIMPLE USAGE

1. SETTING: Show Alerts= True (To see your entries and Exists)

2. Define your Indicators (ex: INDICATOR1: ema(close,14), INDICATOR2: ema(close,21), INDICATOR3: ema(close,200)

3. Define Your Combinations for long & Short Conditions

a. For Long: (INDICATOR1 crossover INDICATOR2) AND (INDICATOR3 < close)

b. For Short: (INDICATOR1 crossunder INDICATOR2) AND (INDICATOR3 > close)

4. Select Strategy/template (Import strategy to chart) that you export your signals from the list

5. Analyze the best profit by changing Indicators values

SOME INDICATORS DETAILS

Each Indicator includes:

- Factorization : Converting the selected indicator to Double, triple Quadruple such as EMA to DEMA, TEMA QEMA

- Log : Simple or log10 can be used for calculation on function entries

- Plot Type : You can overlay the indicator on the chart (such ema) or you can use stochastic/Percentrank approach to display in the variable hlines range

- Extended Parametes : You can use default parameters or you can use extended (P1,P2) parameters regarding to indicator type and your choice

- Color : You can define indicator color and line properties

- Smooth : you can enable swma smooth

- indicators : you can select one of the 93 function like ema(),rsi().. to define your indicator

- Source : you can select from already defined indicators (IND1-4), External Indicator (EXT), Custom Indicator (CUST), and other sources (close, open...)

CONDITION DETAILS

- There are are 4 type of conditions, long entry, short entry, long exit, short exit.

- Each condition are built up from 4 combinations that joined with "AND" & "OR" operators

- You can see the results by enabling show alerts check box

- If you only wants to enter long entry and long exit, just fill these conditions

- If "close on opposite" checkbox selected on settings, long entry will be closed on short entry and vice versa

COMBINATIONS DETAILS

- There are 4 combinations that joined with "AND" & "OR" operators for each condition

- combinations are built up from compare 1st entry with 2nd one by using operator

- 1st and 2nd entries includes already defined indicators (IND1-5), External Indicator (EXT), Custom Indicator (CUST), and other sources (close, open...)

- Operators are comparison values such as >,<, crossover,...

- 2nd entry include "VALUE" parameter that will use to compare 1st indicator with value area

- If 2nd indicator selected different than "VALUE", value are will mean previous value of the selection. (ex: value area= 2, 2nd entry=close, means close )

- Selecting "NONE" for the 1st entry will disable calculation of current and following combinations

JOINS DETAILS

- Each combination will join wiht the following one with the JOIN (AND, OR) operator (if the following one is not equal "NONE")

CUSTOM INDICATOR

- Custom Indicator defines harcoded in the source code.

- You can call it with "CUST" in the Indicator definition source or combination entries source

- You can change or implement your custom indicator by updating the source code

EXTERNAL INDICATOR

- You can import an external indicator by selecting it from the ext source.

- External Indicator should be already imported to the chart and it have an plot function to output its signal

EXPORTING SIGNAL

- You can export your result to an already defined strategy template such as Pine coders, Benson, Daveatt Strategy templates

- Or you can define your custom export for other future strategy templates

ALERTS

- By enabling show alerts checkbox, you can see long entry exits on the bottom, and short entry exits aon the top of the chart

ADDITIONAL INFO

- You can see all off the inputs descriptions in the tooltips. (You can also see the previous version for details)

- Availability to set start, end dates

- Minimize repainting by using security function options (Secure, Semi Secure, Repaint)

- Availability of use timeframes

-

Version 3 INDICATORS LIST (More to be added):

▼▼▼ OVERLAY INDICATORS ▼▼▼

alma(src,len,offset=0.85,sigma=6).-------Arnaud Legoux Moving Average

ama(src,len,fast=14,slow=100).-----------Adjusted Moving Average

accdist().-------------------------------Accumulation/distribution index.

cma(src,len).----------------------------Corrective Moving average

dema(src,len).---------------------------Double EMA (Same as EMA with 2 factor)

ema(src,len).----------------------------Exponential Moving Average

gmma(src,len).---------------------------Geometric Mean Moving Average

highest(src,len).------------------------Highest value for a given number of bars back.

hl2ma(src,len).--------------------------higest lowest moving average

hma(src,len).----------------------------Hull Moving Average.

lagAdapt(src,len,perclen=5,fperc=50).----Ehlers Adaptive Laguerre filter

lagAdaptV(src,len,perclen=5,fperc=50).---Ehlers Adaptive Laguerre filter variation

laguerre(src,len).-----------------------Ehlers Laguerre filter

lesrcp(src,len).-------------------------lowest exponential esrcpanding moving line

lexp(src,len).---------------------------lowest exponential expanding moving line

linreg(src,len,loffset=1).---------------Linear regression

lowest(src,len).-------------------------Lovest value for a given number of bars back.

mcginley(src, len.-----------------------McGinley Dynamic adjusts for market speed shifts, which sets it apart from other moving averages, in addition to providing clear moving average lines

percntl(src,len).------------------------percentile nearest rank. Calculates percentile using method of Nearest Rank.

percntli(src,len).-----------------------percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

previous(src,len).-----------------------Previous n (len) value of the source

pivothigh(src,BarsLeft=len,BarsRight=2).-Previous pivot high. src=src, BarsLeft=len, BarsRight=p1=2

pivotlow(src,BarsLeft=len,BarsRight=2).--Previous pivot low. src=src, BarsLeft=len, BarsRight=p1=2

rema(src,len).---------------------------Range EMA (REMA)

rma(src,len).----------------------------Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sar(start=len, inc=0.02, max=0.02).------Parabolic SAR (parabolic stop and reverse) is a method to find potential reversals in the market price direction of traded goods.start=len, inc=p1, max=p2. ex: sar(0.02, 0.02, 0.02)

sma(src,len).----------------------------Smoothed Moving Average

smma(src,len).---------------------------Smoothed Moving Average

super2(src,len).-------------------------Ehlers super smoother, 2 pole

super3(src,len).-------------------------Ehlers super smoother, 3 pole

supertrend(src,len,period=3).------------Supertrend indicator

swma(src,len).---------------------------Sine-Weighted Moving Average

tema(src,len).---------------------------Triple EMA (Same as EMA with 3 factor)

tma(src,len).----------------------------Triangular Moving Average

vida(src,len).---------------------------Variable Index Dynamic Average

vwma(src,len).---------------------------Volume Weigted Moving Average

volstop(src,len,atrfactor=2).------------Volatility Stop is a technical indicator that is used by traders to help place effective stop-losses. atrfactor=p1

wma(src,len).----------------------------Weigted Moving Average

vwap(src_).------------------------------Volume Weighted Average Price (VWAP) is used to measure the average price weighted by volume

▼▼▼ NON OVERLAY INDICATORS ▼▼

adx(dilen=len, adxlen=14, adxtype=0).----adx. The Average Directional Index (ADX) is a used to determine the strength of a trend. len=>dilen, p1=adxlen (default=14), p2=adxtype 0:ADX, 1:+DI, 2:-DI (def:0)

angle(src,len).--------------------------angle of the series (Use its Input as another indicator output)

aroon(len,dir=0).------------------------aroon indicator. Aroons major function is to identify new trends as they happen.p1 = dir: 0=mid (default), 1=upper, 2=lower

atr(src,len).----------------------------average true range. RMA of true range.

awesome(fast=len=5,slow=34,type=0).------Awesome Oscilator is an indicator used to measure market momentum. defaults : fast=len= 5, p1=slow=34, p2=type: 0=Awesome, 1=difference

bbr(src,len,mult=1).---------------------bollinger %%

bbw(src,len,mult=2).---------------------Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci(src,len).----------------------------commodity channel index

cctbbo(src,len).-------------------------CCT Bollinger Band Oscilator

change(src,len).-------------------------A.K.A. Momentum. Difference between current value and previous, source - source . is most commonly referred to as a rate and measures the acceleration of the price and/or volume of a security

cmf(len=20).-----------------------------Chaikin Money Flow Indicator used to measure Money Flow Volume over a set period of time. Default use is len=20

cmo(src,len).----------------------------Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog(src,len).----------------------------The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

copcurve(src,len).-----------------------Coppock Curve. was originally developed by Edwin Sedge Coppock (Barrons Magazine, October 1962).

correl(src,len).-------------------------Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count(src,len).--------------------------green avg - red avg

cti(src,len).----------------------------Ehler s Correlation Trend Indicator by

dev(src,len).----------------------------ta.dev() Measure of difference between the series and its ta.sma

dpo(len).--------------------------------Detrended Price OScilator is used to remove trend from price.

efi(len).--------------------------------Elders Force Index (EFI) measures the power behind a price movement using price and volume.

eom(len=14,div=10000).-------------------Ease of Movement.It is designed to measure the relationship between price and volume.p1 = div: 10000= (default)

falling(src,len).------------------------ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

fisher(len).-----------------------------Fisher Transform is a technical indicator that converts price to Gaussian normal distribution and signals when prices move significantly by referencing recent price data

histvol(len).----------------------------Historical volatility is a statistical measure used to analyze the general dispersion of security or market index returns for a specified period of time.

kcr(src,len,mult=2).---------------------Keltner Channels Range

kcw(src,len,mult=2).---------------------ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

klinger(type=len).-----------------------Klinger oscillator aims to identify money flow’s long-term trend. type=len: 0:Oscilator 1:signal

macd(src,len).---------------------------MACD (Moving Average Convergence/Divergence)

mfi(src,len).----------------------------Money Flow Index s a tool used for measuring buying and selling pressure

msi(len=10).-----------------------------Mass Index (def=10) is used to examine the differences between high and low stock prices over a specific period of time

nvi().-----------------------------------Negative Volume Index

obv().-----------------------------------On Balance Volume

pvi().-----------------------------------Positive Volume Index

pvt().-----------------------------------Price Volume Trend

ranges(src,upper=len, lower=-5).---------ranges of the source. src=src, upper=len, v1:lower=upper . returns: -1 source=upper otherwise 0

rising(src,len).-------------------------ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc(src,len).----------------------------Rate of Change

rsi(src,len).----------------------------Relative strength Index

rvi(src,len).----------------------------The Relative Volatility Index (RVI) is calculated much like the RSI, although it uses high and low price standard deviation instead of the RSI’s method of absolute change in price.

smi_osc(src,len,fast=5, slow=34).--------smi Oscillator

smi_sig(src,len,fast=5, slow=34).--------smi Signal

stc(src,len,fast=23,slow=50).------------Schaff Trend Cycle (STC) detects up and down trends long before the MACD. Code imported from

stdev(src,len).--------------------------Standart deviation

trix(src,len) .--------------------------the rate of change of a triple exponentially smoothed moving average.

tsi(src,len).----------------------------The True Strength Index indicator is a momentum oscillator designed to detect, confirm or visualize the strength of a trend.

ultimateOsc(len.-------------------------Ultimate Oscillator indicator (UO) indicator is a technical analysis tool used to measure momentum across three varying timeframes

variance(src,len).-----------------------ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta.sma), and it informally measures how far a set of numbers are spread out from their mean.

willprc(src,len).------------------------Williams %R

wad().-----------------------------------Williams Accumulation/Distribution.

wvad().----------------------------------Williams Variable Accumulation/Distribution.

HISTORY

v3.01

ADD: 23 new indicators added to indicators list from the library. Current Total number of Indicators are 93. (to be continued to adding)

ADD: 2 more Parameters (P1,P2) for indicator calculation added. Par:(Use Defaults) uses only indicator(Source, Length) with library's default parameters. Par:(Use Extra Parameters P1,P2) use indicator(Source,Length,p1,p2) with additional parameters if indicator needs.

ADD: log calculation (simple, log10) option added on indicator function entries

ADD: New Output Signals added for compatibility on exporting condition signals to different Strategy templates.

ADD: Alerts Added according to conditions results

UPD: Indicator source inputs now display with indicators descriptions

UPD: Most off the source code rearranged and some functions moved to the new library. Now system work like a little bit frontend/backend

UPD: Performance improvement made on factorization and other source code

UPD: Input GUI rearranged

UPD: Tooltips corrected

REM: Extended indicators removed

UPD: IND1-IND4 added to indicator data source. Now it is possible to create new indicators with the previously defined indicators value. ex: IND1=ema(close,14) and IND2=rsi(IND1,20) means IND2=rsi(ema(close,14),20)

UPD: Custom Indicator (CUST) added to indicator data source and Combination Indicator source.

UPD: Volume added to indicator data source and Combination Indicator source.

REM: Custom indicators removed and only one custom indicator left

REM: Plot Type "Org. Range (-1,1)" removed

UPD: angle, rising, falling type operators moved to indicator library

在腳本中搜尋"curve"

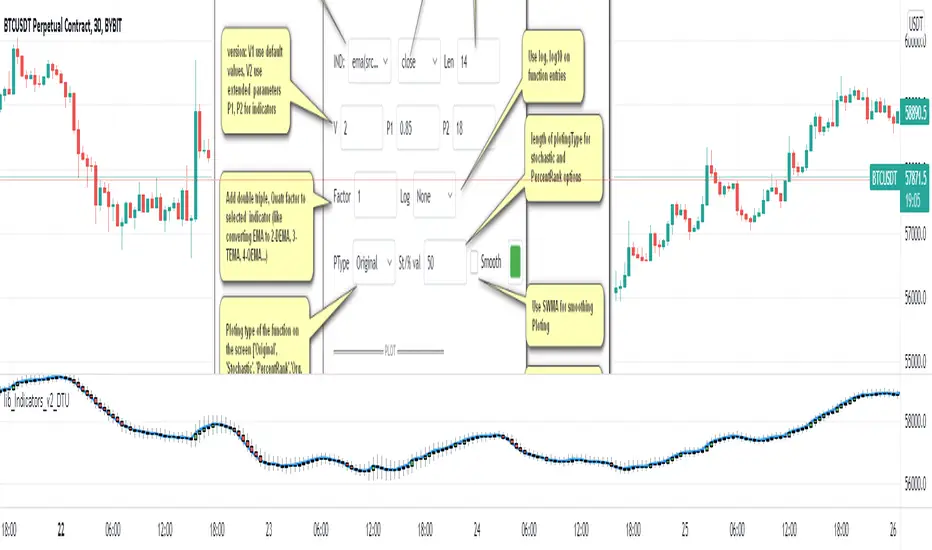

Indicator Functions with Factor and HeikinAshiHello all,

This indicator returns below selected indicators values with entered parameters.

Also you can add factorization, functions candles, function HeikinAshi and more to the plot.

VERSION:

Version 1: returns series only source and Length with already defined default values

Version 2: returns series with source, Length, p1 and p2 parameters according to the indicator definition (ex: )

PARAMETERS p1 p2

for defining multi arguments (See indicators list) indicator input value usable with verison=V2 selected.. ex: for alma( src , len ,offset=0.85,sigma=6), set source=source, len=length, p1=0.85 an p2=6

FACTOR:

Add double triple, Quadruple factors to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

1-Original

2-Double

3-Triple

4-Quadruple

LOG

Log: Use log, log10 on function entries

PLOTTING:

PType: Plotting type of the function on the screen

Original :use original values

Org. Range (-1,1): usable for indicators between range -1 and 1

Stochastic: Convert indicator values by using stochastic calculation between -1 & 1. (use AT/% length to better view)

PercentRank: Convert indicator values by using Percent Rank calculation between -1 & 1. (use AT/% length to better view)

ST/%: length for plotting Type for stochastic and Percent Rank options

Smooth: Use SWMA for smoothing the function

DISPLAY TYPES

Plot Candles: Display the selected indicator as candle by implementing values

Plot Ind: Display result of indicator with selected source

HeikinAshi: Display Selected indicator candles with Heikin Ashi calculation

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma( src , len ,offset=0.85,sigma=6)', // Arnaud Legoux Moving Average

ama = 'ama( src , len ,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', // Accumulation/distribution index.

cma = 'cma( src , len )', //Corrective Moving average

dema = 'dema( src , len )', // Double EMA (Same as EMA with 2 factor)

ema = 'ema( src , len )', // Exponential Moving Average

gmma = 'gmma( src , len )', //Geometric Mean Moving Average

hghst = 'highest( src , len )', //Highest value for a given number of bars back.

hl2ma = 'hl2ma( src , len )', //higest lowest moving average

hma = 'hma( src , len )', // Hull Moving Average .

lgAdt = 'lagAdapt( src , len ,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV( src , len ,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre( src , len )', //Ehler's Laguerre filter

lsrcp = 'lesrcp( src , len )', //lowest exponential esrcpanding moving line

lexp = 'lexp( src , len )', //lowest exponential expanding moving line

linrg = 'linreg( src , len ,loffset=1)', // Linear regression

lowst = 'lowest( src , len )', //Lovest value for a given number of bars back.

pcnl = 'percntl( src , len )', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli( src , len )', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema( src , len )', //Range EMA (REMA)

rma = 'rma( src , len )', //Moving average used in RSI . It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma( src , len )', // Smoothed Moving Average

smma = 'smma( src , len )', // Smoothed Moving Average

supr2 = 'super2( src , len )', //Ehler's super smoother, 2 pole

supr3 = 'super3( src , len )', //Ehler's super smoother, 3 pole

strnd = 'supertrend( src , len ,period=3)', //Supertrend indicator

swma = 'swma( src , len )', //Sine-Weighted Moving Average

tema = 'tema( src , len )', // Triple EMA (Same as EMA with 3 factor)

tma = 'tma( src , len )', //Triangular Moving Average

vida = 'vida( src , len )', // Variable Index Dynamic Average

vwma = 'vwma( src , len )', // Volume Weigted Moving Average

wma = 'wma( src , len )', //Weigted Moving Average

angle = 'angle( src , len )', //angle of the series (Use its Input as another indicator output)

atr = 'atr( src , len )', // average true range . RMA of true range.

bbr = 'bbr( src , len ,mult=1)', // bollinger %%

bbw = 'bbw( src , len ,mult=2)', // Bollinger Bands Width . The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci( src , len )', // commodity channel index

cctbb = 'cctbbo( src , len )', // CCT Bollinger Band Oscilator

chng = 'change( src , len )', //Difference between current value and previous, source - source.

cmo = 'cmo( src , len )', // Chande Momentum Oscillator . Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog( src , len )', //The cog (center of gravity ) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve( src , len )', // Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl( src , len )', // Correlation coefficient . Describes the degree to which two series tend to deviate from their ta. sma values.

count = 'count( src , len )', //green avg - red avg

dev = 'dev( src , len )', //ta.dev() Measure of difference between the series and it's ta. sma

fall = 'falling( src , len )', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr( src , len ,mult=2)', // Keltner Channels Range

kcw = 'kcw( src , len ,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd( src , len )', // macd

mfi = 'mfi( src , len )', // Money Flow Index

nvi = 'nvi()', // Negative Volume Index

obv = 'obv()', // On Balance Volume

pvi = 'pvi()', // Positive Volume Index

pvt = 'pvt()', // Price Volume Trend

rise = 'rising( src , len )', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc( src , len )', // Rate of Change

rsi = 'rsi( src , len )', // Relative strength Index

smosc = 'smi_osc( src , len ,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig( src , len ,fast=5, slow=34)', //smi Signal

stdev = 'stdev( src , len )', //Standart deviation

trix = 'trix( src , len )' , //the rate of change of a triple exponentially smoothed moving average .

tsi = 'tsi( src , len )', //True Strength Index

vari = 'variance( src , len )', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta. sma ), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc( src , len )', // Williams %R

wad = 'wad()', // Williams Accumulation/Distribution .

wvad = 'wvad()' //Williams Variable Accumulation/Distribution

I will update the indicator list when I will update the library

Thanks to tradingview, @RodrigoKazuma for their open source indicators

lib_Indicators_v2_DTULibrary "lib_Indicators_v2_DTU"

This library functions returns included Moving averages, indicators with factorization, functions candles, function heikinashi and more.

Created it to feed as backend of my indicator/strategy "Indicators & Combinations Framework Advanced v2 " that will be released ASAP.

This is replacement of my previous indicator (lib_indicators_DT)

I will add an indicator example which will use this indicator named as "lib_indicators_v2_DTU example" to help the usage of this library

Additionally library will be updated with more indicators in the future

NOTES:

Indicator functions returns only one series :-(

plotcandle function returns candle series

INDICATOR LIST:

hide = 'DONT DISPLAY', //Dont display & calculate the indicator. (For my framework usage)

alma = 'alma(src,len,offset=0.85,sigma=6)', //Arnaud Legoux Moving Average

ama = 'ama(src,len,fast=14,slow=100)', //Adjusted Moving Average

acdst = 'accdist()', //Accumulation/distribution index.

cma = 'cma(src,len)', //Corrective Moving average

dema = 'dema(src,len)', //Double EMA (Same as EMA with 2 factor)

ema = 'ema(src,len)', //Exponential Moving Average

gmma = 'gmma(src,len)', //Geometric Mean Moving Average

hghst = 'highest(src,len)', //Highest value for a given number of bars back.

hl2ma = 'hl2ma(src,len)', //higest lowest moving average

hma = 'hma(src,len)', //Hull Moving Average.

lgAdt = 'lagAdapt(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter

lgAdV = 'lagAdaptV(src,len,perclen=5,fperc=50)', //Ehler's Adaptive Laguerre filter variation

lguer = 'laguerre(src,len)', //Ehler's Laguerre filter

lsrcp = 'lesrcp(src,len)', //lowest exponential esrcpanding moving line

lexp = 'lexp(src,len)', //lowest exponential expanding moving line

linrg = 'linreg(src,len,loffset=1)', //Linear regression

lowst = 'lowest(src,len)', //Lovest value for a given number of bars back.

pcnl = 'percntl(src,len)', //percentile nearest rank. Calculates percentile using method of Nearest Rank.

pcnli = 'percntli(src,len)', //percentile linear interpolation. Calculates percentile using method of linear interpolation between the two nearest ranks.

rema = 'rema(src,len)', //Range EMA (REMA)

rma = 'rma(src,len)', //Moving average used in RSI. It is the exponentially weighted moving average with alpha = 1 / length.

sma = 'sma(src,len)', //Smoothed Moving Average

smma = 'smma(src,len)', //Smoothed Moving Average

supr2 = 'super2(src,len)', //Ehler's super smoother, 2 pole

supr3 = 'super3(src,len)', //Ehler's super smoother, 3 pole

strnd = 'supertrend(src,len,period=3)', //Supertrend indicator

swma = 'swma(src,len)', //Sine-Weighted Moving Average

tema = 'tema(src,len)', //Triple EMA (Same as EMA with 3 factor)

tma = 'tma(src,len)', //Triangular Moving Average

vida = 'vida(src,len)', //Variable Index Dynamic Average

vwma = 'vwma(src,len)', //Volume Weigted Moving Average

wma = 'wma(src,len)', //Weigted Moving Average

angle = 'angle(src,len)', //angle of the series (Use its Input as another indicator output)

atr = 'atr(src,len)', //average true range. RMA of true range.

bbr = 'bbr(src,len,mult=1)', //bollinger %%

bbw = 'bbw(src,len,mult=2)', //Bollinger Bands Width. The Bollinger Band Width is the difference between the upper and the lower Bollinger Bands divided by the middle band.

cci = 'cci(src,len)', //commodity channel index

cctbb = 'cctbbo(src,len)', //CCT Bollinger Band Oscilator

chng = 'change(src,len)', //Difference between current value and previous, source - source .

cmo = 'cmo(src,len)', //Chande Momentum Oscillator. Calculates the difference between the sum of recent gains and the sum of recent losses and then divides the result by the sum of all price movement over the same period.

cog = 'cog(src,len)', //The cog (center of gravity) is an indicator based on statistics and the Fibonacci golden ratio.

cpcrv = 'copcurve(src,len)', //Coppock Curve. was originally developed by Edwin "Sedge" Coppock (Barron's Magazine, October 1962).

corrl = 'correl(src,len)', //Correlation coefficient. Describes the degree to which two series tend to deviate from their ta.sma values.

count = 'count(src,len)', //green avg - red avg

dev = 'dev(src,len)', //ta.dev() Measure of difference between the series and it's ta.sma

fall = 'falling(src,len)', //ta.falling() Test if the `source` series is now falling for `length` bars long. (Use its Input as another indicator output)

kcr = 'kcr(src,len,mult=2)', //Keltner Channels Range

kcw = 'kcw(src,len,mult=2)', //ta.kcw(). Keltner Channels Width. The Keltner Channels Width is the difference between the upper and the lower Keltner Channels divided by the middle channel.

macd = 'macd(src,len)', //macd

mfi = 'mfi(src,len)', //Money Flow Index

nvi = 'nvi()', //Negative Volume Index

obv = 'obv()', //On Balance Volume

pvi = 'pvi()', //Positive Volume Index

pvt = 'pvt()', //Price Volume Trend

rise = 'rising(src,len)', //ta.rising() Test if the `source` series is now rising for `length` bars long. (Use its Input as another indicator output)

roc = 'roc(src,len)', //Rate of Change

rsi = 'rsi(src,len)', //Relative strength Index

smosc = 'smi_osc(src,len,fast=5, slow=34)', //smi Oscillator

smsig = 'smi_sig(src,len,fast=5, slow=34)', //smi Signal

stdev = 'stdev(src,len)', //Standart deviation

trix = 'trix(src,len)' , //the rate of change of a triple exponentially smoothed moving average.

tsi = 'tsi(src,len)', //True Strength Index

vari = 'variance(src,len)', //ta.variance(). Variance is the expectation of the squared deviation of a series from its mean (ta.sma), and it informally measures how far a set of numbers are spread out from their mean.

wilpc = 'willprc(src,len)', //Williams %R

wad = 'wad()', //Williams Accumulation/Distribution.

wvad = 'wvad()' //Williams Variable Accumulation/Distribution.

}

f_func(string, float, simple, float, float, float, simple) f_func Return selected indicator value with different parameters. New version. Use extra parameters for available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

Returns: float Return calculated indicator value

fn_heikin(float, float, float, float) fn_heikin Return given src data (open, high,low,close) as heikin ashi candle values

Parameters:

float : o_ open value

float : h_ high value

float : l_ low value

float : c_ close value

Returns: float heikin ashi open, high,low,close vlues that will be used with plotcandle

fn_plotFunction(float, string, simple, bool) fn_plotFunction Return input src data with different plotting options

Parameters:

float : src_ indicator src_data or any other series.....

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

Returns: float

fn_funcPlotV2(string, float, simple, float, float, float, simple, string, simple, bool, bool) fn_funcPlotV2 Return selected indicator value with different parameters. New version. Use extra parameters fora available indicators

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 extra parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 extra parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 extra parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return calculated indicator value

fn_factor(string, float, simple, float, float, float, simple, simple, string, simple, bool, bool) fn_factor Return selected indicator's factorization with given arguments

Parameters:

string : FuncType_ indicator from the indicator list

float : src_data_ close, open, high, low,hl2, hlc3, ohlc4 or any

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

simple : int fact_ Add double triple, Quatr factor to selected indicator (like converting EMA to 2-DEMA, 3-TEMA, 4-QEMA...)

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

Returns: float Return result of the function

fn_plotCandles(string, simple, float, float, float, simple, string, simple, bool, bool, bool) fn_plotCandles Return selected indicator's candle values with different parameters also heikinashi is available

Parameters:

string : FuncType_ indicator from the indicator list

simple : int length_ indicator length

float : p1 parameter-1. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p2 parameter-2. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

float : p3 parameter-3. active on Version 2 for defining multi arguments indicator input value. ex: lagAdapt(src_, length_,LAPercLen_=p1,FPerc_=p2)

simple : int version_ indicator version for backward compatibility. V1:dont use extra parameters p1,p2,p3 and use default values. V2: use extra parameters for available indicators

string : plotingType Ploting type of the function on the screen

simple : int stochlen_ length for plotingType for stochastic and PercentRank options

bool : plotSWMA Use SWMA for smoothing Ploting

bool : log_ Use log on function entries

bool : plotheikin_ Use Heikin Ashi on Plot

Returns: float

REAL MARKET RATESBased on near and long term eurodollar yield curve. Attempts to indicate, through a spread median, how major players may position themselves in the near future.

Standard Error of the Estimate -Jon Andersen- V2Original implementation idea of bands by:

Traders issue: Stocks & Commodities V. 14:9 (375-379):

Standard Error Bands by Jon Andersen

Standard Error Bands are quite different than Bollinger's.

First, they are bands constructed around a linear regression curve.

Second, the bands are based on two standard errors above and below this regression line.

The error bands measure the standard error of the estimate around the linear regression line.

Therefore, as a price series follows the course of the regression line the bands will narrow , showing little error in the estimate. As the market gets noisy and random, the error will be greater resulting in wider bands .

Thanks to the work of @glaz & @XeL_arjona

In this version you can change the type of moving averages and the source of the bands.

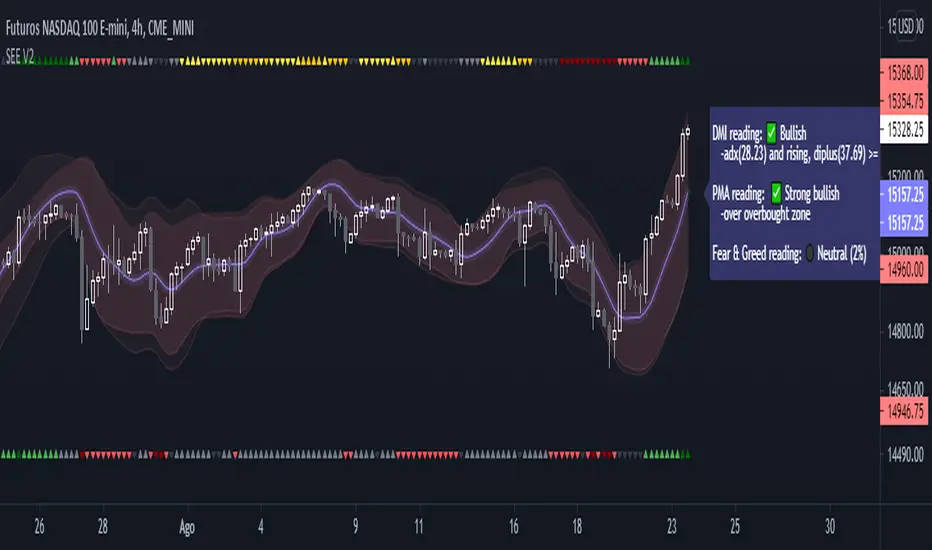

Add a few studies of @dgtrd

1- ADX Colored Directional Movement Line

Directional Movement (DMI) (created by J. Welles Wilder ) consists of the Average Directional Index ( ADX ), to define whether or not there is a trend present, and Plus Directional Indicator (+D I) and Minus Directional Indicator (-D I) serve the purpose of determining trend direction

ADX Colored Directional Movement Line is custom interpretation of Directional Movement (DMI) with aim to present all 3 DMI indicator components with SINGLE line and ability to be added on top of the price chart (main chart)

How to interpret :

* triangle shapes:

▲- bullish : diplus >= diminus

▼- bearish : diplus < diminus

* colors:

green - bullish trend : adx >= strongTrend and di+ > di-

red - bearish trend : adx >= strongTrend and di+ < di-

gray - no trend : weekTrend < adx < strongTrend

yellow - week trend : adx < weekTrend

* color density:

darker : adx growing

lighter : adx falling

2- Volatility Colored Price/MA Line

Custom interpretation of the idea “Prices high above the moving average (MA) or low below it are likely to be remedied in the future by a reverse price movement”. Further details can be found under study “Price Distance to its MA by DGT”

How to interpret :

-▲ – Bullish , Price Action above Moving Average

-▼ – Bearish , Price Action below Moving Average

-Gray/Black - Low Volatility

-Green/Red – Price Action in Threshold Bands

-Dark Green/Red – Price Action Exceeds Threshold Bands

3- Volume Weighted Bar s

Volume Weighted Bars, a study of Kıvanç Özbilgiç, aims to present whether volume supports price movements. Volume Weighted Bars are calculated based on volume moving average.

How to interpret :

-Volume high above the volume moving average be displayed with red/green colors

-Average volume values will remain as they are and

-Volume low below the volume moving average will be indicated with darker colors

4- Fear & Greed index value, using technical anlysis approach calculated based on :

⮩1 - Price Momentum : Price Distance to its Moving Average

⮩2 - Strenght : Rate of Return, price movement over a period of time

⮩3 - Money Flow : Chaikin Money Flow, quantify changes in buying and selling pressure. CMF calculations is based on Accumulation/Distribution

⮩4 - Market Volatility : CBOE Volatility Index ( VIX ), the Volatility Index, or VIX , is a real-time market index that represents the market's expectation. It provides a measure of market risk and investors' sentiments

⮩5 -Safe Haven Demand: in this study GOLD demand is assumed

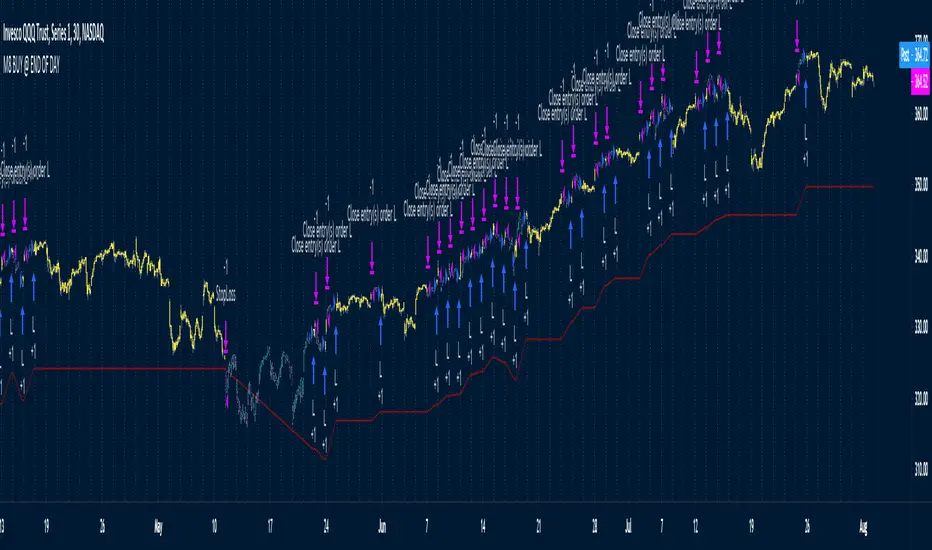

M8 BUY @ END OF DAYI've read a couple of times at a couple of different places that most of the move in the market happens after hours, meaning during non-standard trading hours.

After-market and pre-market hours and have seen data presented showing that systems which bought just before end normal market hours and sold the next morning had really amazing resutls.

But when testing those I found the results to be quite poor compared to the pretty graphs I saw, and after much tweaking and trying different ideas I gave up on the idea until I recently decided to try a new position management system.

The System

Buys at the end of the trading day before the close

Sells the next morning at the open IF THE CLOSE OF THE CURRENT BAR IS HIGHER THAN THE ENTRY PRICE

When the current price is not higher, the system will keep the position open until it EITHER gets stops out or closes on profit <<< this is WHY it has the high win %

The system has a high win ratio because it will keep that one position open until it either reaches profit or stops out

This "system" of waiting, and keeping the trade open, actually turned out to be a fantastic way to kind of put the complete trading strategy in a kind of limbo mode. It either waits for market failure or for a profit.

I don't really care about win % at all, almost always high win % ratio systems are just nonsense. What I look for is a PF -- profit factor of 1.5 or above, and a relatively smooth equity curve. -- This has both.

The Stop Loss setting is set @ .95, meaning a 5% stop loss. The Red Line on the chart is the stop loss line.

There is no set profit target -- it simply takes what the market gives.

Non-Repainting System

This does use a 200D Simple Moving Average as a filter. Like a Green Light / Red Light traffic light, the system will only trade long when the price is above its 200 Moving average.

Here is the code: "F1 = close > sma(security(syminfo.tickerid, "D", close ), MarketFilterLen) // HIGH OF OLD DATA -- SO NO REPAINTING"

I use "close ", so that's data from two days ago, it's fixed, confirmed, non-repainting data from the higher timeframe.

-- I would only suggest using this on direction tickers like SPY, QQQ, SSO, TQQQ, market sectors with additional filters in place.

{Gunzo} Trend Sniper (WMA with coefficient)Trend Sniper is a trend-following indicator that sticks closer to the trend than others moving averages as it is using an upgraded weighted moving average implementation.

OVERVIEW :

It is typical to use a moving average indicator (SMA, EMA, WMA or TMA) to identify the trend of an asset. Standard moving averages indicators smooth the price and doesn’t stick very closely to the actual price, showing potential lagging information.

CALCULATION :

In order to have a trendline that sticks to the price, we are going to use a weighted moving average as it puts more weight on recent candles and less on past candles. The weight is usually calculated using the distance from current candle to the other candles used in the calculation. We have the following formula for the standard calculation as implemented in TradingView :

WMA_standard = (Price1 * Weight1 + …… + PriceN * WeightN)) / (Weight1 + …… + WeightN)

This “Trend Sniper” indicator uses an additional coefficient to alter even more the weight of each candle.

WMA_with_coefficient = (Price1 * (Weight1 - Coefficient) + …… + PriceN * (WeightN - Coefficient)) / ((Weight1 - Coefficient) + …… + (WeightN - Coefficient))

SETTINGS :

MA source : Source used for moving average calculation (ex : “close”)

MA length : Length of the moving average. Higher values will give a smoother line, lower values will give a more reactive line.

Use extra smoothing : Enable/disable usage of a EMA to extra smooth the line curve. If activated the indicator may be lagging, but it will also avoid many false buy/sell signals.

MA extra smoothing length : Length of the moving average of the extra smoothing.

Change candle colors : Enable/disable painting the candles of the chart with the colors of the weighted moving average.

Display buy/sell signals : Display buy/sell signals (circles) when the moving average is changing direction

VISUALIZATIONS :

This indicator has 3 possible visualizations :

Moving Average line : the line represents the weighted moving average that is following the price of the asset, when the line goes up we are in a uptrend (green line) when the line goes down we are in a downtrend (red line).

Candle coloring : the color of the moving average line can be applied to the candles of the chart for better readability.

Signals : Buy/Sell signals can be displayed at the bottom of the chart

USAGE :

This indicator can help analyze the trend directional changes :

First of all, if the moving average line is under the price (or above the price), then we can assume that the uptrend is strong (or downtrend is strong).

If the current candle crosses the moving average line, it is the first sign that the trend is weakening and possibly starting to revert.

If the weighted moving average is changing direction, then the trend change is confirmed and the color of the line changes

LV Cop&RMA w HeikinA buy signal is generated when the indicator turns upwards from previous indicator level.

A sell signal is generated when the indicator turns downwards from previous indicator level.

The indicator is trend-following, and based on averages, so by its nature it doesn't pick a bottom, but rather shows when a rally has started.

It is designed for daily period use.

Frequent buy/sell signals can occur on low and high levels.

It is designed with the mentality of Coppock curve. Rma is used instead of Wma and Heikin-Ashi closing price is used instead of standard closing price.

[blackcat] L2 Ehlers RSI with NETLevel: 2

Background

John F. Ehlers introuced RSI with Noise Elimination Technology (NET) in Dec, 2020.

Function

Many indicators produce more or less noisy output, resulting in false or delayed signals. Dr. Ehlers proposed “Noise Elimination Technology,” in Dec, 2020. He introduces using a Kendall correlation to reduce indicator noise and provide better clarification of the indicator direction. This approach attempts to reduce noise without using smoothing filters, which tend to introduce indicator lag and therefore, delayed decisions. With this script, I use his “MyRSI” indicator, which he introduced in his May 2018 article in S&C, by adding some Tradingview pine v4 code for the noise elimination technology. The indicator plots the MyRSI value as well as the value after applying NET to MyRSI. This de-noising technology uses the Kendall correlation of the indicator with a rising slope. Compared with a lowpass filter, this method does not delay the signals.

The technology appears to work well in this example for removing the noise. But note that the NET function is not meant as a replacement of a lowpass or smoothing filter; its output is always in the -1 to +1 range, so it can be used for de-noising oscillators, but not, for instance, to generate a smoothed version of the price curve.

Key Signal

NET --> Ehlers RSI with NET fast line

Trigger --> Ehlers RSI with NET slow line

Pros and Cons

100% John F. Ehlers definition translation, even variable names are the same. This help readers who would like to use pine to read his book.

Remarks

The 99th script for Blackcat1402 John F. Ehlers Week publication.

Readme

In real life, I am a prolific inventor. I have successfully applied for more than 60 international and regional patents in the past 12 years. But in the past two years or so, I have tried to transfer my creativity to the development of trading strategies. Tradingview is the ideal platform for me. I am selecting and contributing some of the hundreds of scripts to publish in Tradingview community. Welcome everyone to interact with me to discuss these interesting pine scripts.

The scripts posted are categorized into 5 levels according to my efforts or manhours put into these works.

Level 1 : interesting script snippets or distinctive improvement from classic indicators or strategy. Level 1 scripts can usually appear in more complex indicators as a function module or element.

Level 2 : composite indicator/strategy. By selecting or combining several independent or dependent functions or sub indicators in proper way, the composite script exhibits a resonance phenomenon which can filter out noise or fake trading signal to enhance trading confidence level.

Level 3 : comprehensive indicator/strategy. They are simple trading systems based on my strategies. They are commonly containing several or all of entry signal, close signal, stop loss, take profit, re-entry, risk management, and position sizing techniques. Even some interesting fundamental and mass psychological aspects are incorporated.

Level 4 : script snippets or functions that do not disclose source code. Interesting element that can reveal market laws and work as raw material for indicators and strategies. If you find Level 1~2 scripts are helpful, Level 4 is a private version that took me far more efforts to develop.

Level 5 : indicator/strategy that do not disclose source code. private version of Level 3 script with my accumulated script processing skills or a large number of custom functions. I had a private function library built in past two years. Level 5 scripts use many of them to achieve private trading strategy.

Combo Backtest 123 Reversal & Kase Dev Stops This is combo strategies for get a cumulative signal.

First strategy

This System was created from the Book "How I Tripled My Money In The

Futures Market" by Ulf Jensen, Page 183. This is reverse type of strategies.

The strategy buys at market, if close price is higher than the previous close

during 2 days and the meaning of 9-days Stochastic Slow Oscillator is lower than 50.

The strategy sells at market, if close price is lower than the previous close price

during 2 days and the meaning of 9-days Stochastic Fast Oscillator is higher than 50.

Second strategy

The Kase Dev Stops system finds the optimal statistical balance between letting profits run,

while cutting losses. Kase DevStop seeks an ideal stop level by accounting for volatility (risk),

the variance in volatility (the change in volatility from bar to bar), and volatility skew

(the propensity for volatility to occasionally spike incorrectly).

Kase Dev Stops are set at points at which there is an increasing probability of reversal against

the trend being statistically significant based on the log normal shape of the range curve.

Setting stops will help you take as much risk as necessary to stay in a good position, but not more.

You can change long to short in the Input Settings

Please, use it only for learning or paper trading. Do not for real trading.

WARNING:

- For purpose educate only

- This script to change bars colors.

Cycle Swing MomentumAdaptive Ultra-Smooth Momentum indicator

The Cycle-Swing-Indicator "CSI" provides an optimized "momentum" oscillator based on the current dominant cycle by looking at the swing of the dominant cycle instead of the raw source momentum. Offering the following improvements:

Smoothness

Zero delay

Sharpness at turning points

Robust and adaptable to market conditions

Accurate deviation detection

The following common problems with standard indicators are solved by this indicator:

First, normal indicators introduce a lot of false signals due to their noisy signal line. Second, to compensate for the noise, one would normally try to add some smoothing. But this only results in adding more delay to the indicator, which makes it almost useless. Third, standard indicators require a length adjustment to derive reliable signals. However, you never know how to set the right length.

All three problems described above are solved by the developed adaptive cyclic algorithm.

The above chart shows current Bitcoin 4h data from the last days as of writing with the proposed signal reading for this indicator. The standard momentum indicator is included for comparison.

HOW TO USE

The indicator works without any parameter and can be applied to any chart and any time-frame. It will adapt automatically to the Dominant Cycle and use the dominant cycle of the source data to derive the ultra smooth momentum curve. Adaptive upper/lower bands are included and highlight areas with extreme readings. Automatic divergence detection can be turned off/on.

HOW TO READ

The indicator can be used like any oscillator. In addition, it provides adaptive high and low bands.

* Look for turns above the upper/lower bands

* Look for divergences between source and signals line

Further reading/Original source:

The indicator uses the dominant cycle to optimize signal, smoothing and cyclic memory. To get more in-depth information on the Cycle Swing Indicator, please read Chapter 10 "Cycle Swing Indicator: Trading the swing of the dominant cycle" of the book "Decoding the Hidden Market Rhythm, Part 1" available at your favorite book store.

Related ideas:

Please also check the cyclic RSI indicator which also uses cyclic information to improve the signal.

Bitcoin M2 supply adjusted priceThis script plots bitcoin candles adjusted by M2 supply (blue line), helping the trader to obtain insight of new support/resistance levels adjusted by M2 supply.

Note: As it was not possible to make the price adjust automatically by the last M2 value (pinescript limitation, I guess), the input parameter "M2Last" must be updated manually observing the last M2 value in blue curve.

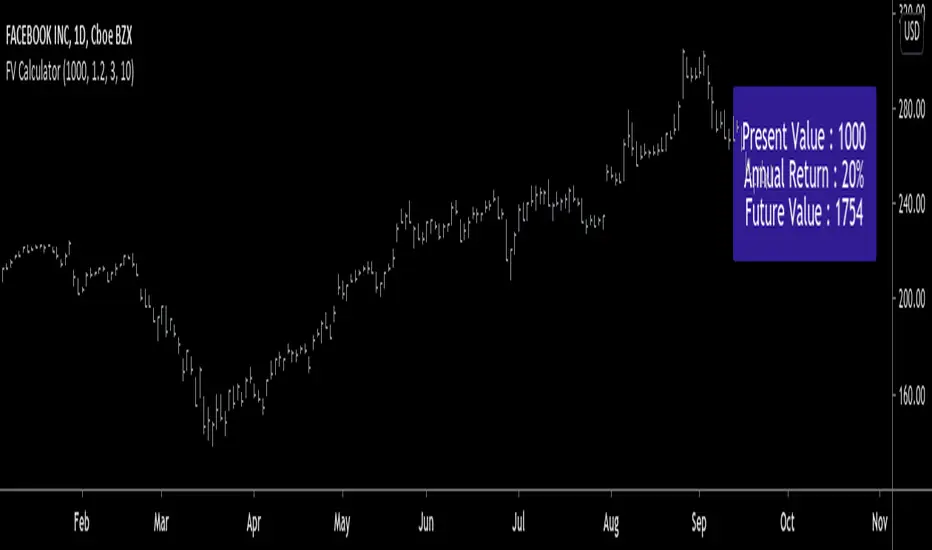

Future Value: Compound Interest with Regular Deposits [racer8]This isn't no ordinary FV equation, this one takes into account regular deposits. I had to derive this equation myself.

This calculator calculates future value based on the following inputs:

- Present value

- Yearly return

- Yearly deposit

- years

Application: Can be used to determine you're future value of your equity curve.

C = c*m^n + a*m*{(m^(n-1)-1)/(m-1)}

C = Future value

c = present value

m = yearly return multiplier

n = years

a = yearly deposit amount

Enjoy :)

Ichimoku Cloud using Tilson T3 SmoothingThe standard Ichimoku Cloud is derived from Donchian Channels and is based on the range of the data set. However the channels are choppy and may not always be easy to read. By using moving averages, similar leading spans can be generated with a smoother outline. The T3 averages further smooths out the curve.

BTC Contango IndexInspired by a Twitter post by Byzantine General:

This is a script that shows the contango between spot and futures prices of Bitcoin to identify overbought and oversold conditions. Contango and backwardation are terms used to define the structure of the forward curve. When a market is in contango, the forward price of a futures contract is higher than the spot price. Conversely, when a market is in backwardation, the forward price of the futures contract is lower than the spot price.

The aggregate prices on top exchanges are taken and then averaged to obtain a Spot Average and a Futures Average. The script then plots (Futures Average/Spot Average) - 1 to illustrate the percent difference (contango) between spot and futures prices of Bitcoin.

When in contango, Bitcoin may be overbought.

When in backwardation, Bitcoin may be oversold.

XBT % ContangoSimilar to my other indicators, but measures XBTUSD Contango in terms of percent.

Also, built it so you could change the values that give the red and green signals. Default values are 0% or less (backwardation) indicates green. However, i found that a 0.5% setting worked will finding local bottoms for current contract of XBTH20 (March 2020). The upper value default is at 5%, and signals red when the next contract reaches over 5%.

My assumption is as BTC increases in value over time, measuring contango in terms of percent will be a better measure of the XBT futures curve.

Leverage Strategy and a few words on risk/opportunityHello traders,

I started this script as a joke for someone... finally appears it could be used for educational content

Let's talk about leverage and margin call

Margin Call

A margin call is the broker's demand that an investor deposit additional money or securities so that the account is brought up to the minimum value, known as the maintenance margin.

A margin call usually means that one or more of the securities held in the margin account has decreased in value below a certain point.

Leverage

A leverage is a system which allows the trader to open positions much larger than his own capital. ... “Leverage” usually refers to the ratio between the position value and the investment needed,

Strat

The strategy simulates long/short positions on a 4h high/low breakout based on the chart candle close.

The panel below shows the strategy equity curve. Activating the margin call option will show when the account would be margin called giving the settings

Casino

I'm not doing any financial recommendation here.

I made this strategy so that people include more risk management metrics into their strategy.

From the code, we see it's fairly easy to calculate a leveraged position size and a margin call flag - when that flag is hit, the system stops trading.

I simplified things to the extreme here but my point is that the leverage is a double-edge sword gift.

Assuming we always take the same position sizing, increasing the leverage speed up how fast a margin could be ..... called. (bad joke? feel free to tell me). Not saying it will, saying it introduces more risk by design.

Then one could say "I'll just turn off that stupid margin call option". And that's when someone starts backtesting with unrealistic market conditions.

Finally...

When I backtest I always assume the worst in every scenario possible (because I'm French), I always try to minimize the risk first (also because I'm French), keeping as close from 0 as possible (French again)

Then I add the "opportunity" component, looking to catch the maximum of opportunity while keeping the risk low.

It's like a Rubix cube puzzle - decreasing the risk is one side of the equation but whenever I try to catch more opportunity... my risks increases.

Then I update my risk... and now the opportunity decreases... (#wut #wen #simple)

Completely removing the risk from a trading strategy isn't something I wouldn't dare doing.

Trading involves risk. Being obsessed by decreasing the risk is what I do BEST :)

Dave

Kase Dev Stops Backtest The Kase Dev Stops system finds the optimal statistical balance between letting profits run,

while cutting losses. Kase DevStop seeks an ideal stop level by accounting for volatility (risk),

the variance in volatility (the change in volatility from bar to bar), and volatility skew

(the propensity for volatility to occasionally spike incorrectly).

Kase Dev Stops are set at points at which there is an increasing probability of reversal against

the trend being statistically significant based on the log normal shape of the range curve.

Setting stops will help you take as much risk as necessary to stay in a good position, but not more.

WARNING:

- For purpose educate only

- This script to change bars colors.

Kase Dev Stops Strategy The Kase Dev Stops system finds the optimal statistical balance between letting profits run,

while cutting losses. Kase DevStop seeks an ideal stop level by accounting for volatility (risk),

the variance in volatility (the change in volatility from bar to bar), and volatility skew

(the propensity for volatility to occasionally spike incorrectly).

Kase Dev Stops are set at points at which there is an increasing probability of reversal against

the trend being statistically significant based on the log normal shape of the range curve.

Setting stops will help you take as much risk as necessary to stay in a good position, but not more.

WARNING:

- For purpose educate only

- This script to change bars colors.

Kase Dev Stops The Kase Dev Stops system finds the optimal statistical balance between letting profits run,

while cutting losses. Kase DevStop seeks an ideal stop level by accounting for volatility (risk),

the variance in volatility (the change in volatility from bar to bar), and volatility skew

(the propensity for volatility to occasionally spike incorrectly).

Kase Dev Stops are set at points at which there is an increasing probability of reversal against

the trend being statistically significant based on the log normal shape of the range curve.

Setting stops will help you take as much risk as necessary to stay in a good position, but not more.

Lucid SARI wrote this script after having listened to Hyperwave with Sawcruhteez and Tyler Jenks of Lucid Investments Strategies LLC on July 3, 2019. They felt that the existing built-in Parabolic SAR indicator was not doing its calculations properly, and they hoped that someone might help them correct this. So I tried my hand at it, learning Pine Script as I went. I worked on it through the early morning hours and finished it by 4 am on July 4, 2019. I've added a few bits of code since, adding the rule regarding the SAR not advancing beyond the high (low) of the prior two candles during an uptrend (downtrend), but the core script is as it was.

This code is open source under the MIT license. If you have any improvements or corrections to suggest, please send me a pull request via the github repository github.com

For more details on the initial script, see

Sawcruhteez from Lucid Investment Strategies wrote the following description of the Parabolic SAR, where the quotes are from Section II of J. Welles Wilder, Jr.'s book New Concepts in Technical Trading Systems (1978)

--------------------------------------------------------------------------------------------------------------------------

Parabolic SAR

"The Parabolic Time / Price System derives its name from the fact that when charted, the

pattern formed by the stops resembles a parabola, or if you will, a French Curve. The system

allows room for the market to react for the first few days after a trade is initiated and then the

stop begins to move up more rapidly. The stop is not only a function of price but also a function

of time .

"The stop never backs up. It moves an incremental amount each day, only in the direction which

the trade has been initiated."

"The stop is also a function of price because the distance the stop moves up is relative to the

favorable distance the price has moved... specifically, the most favorable price reached since the

trade was initiated."

A. The calculation for a bullish Parabolic SAR is:

Tomorrow’s SAR = Today’s SAR + AF(EP - Today’s SAR)

"Acceleration Factor (AF) is one of a progression of numbers beginning at 0.02 and ending at

0.20. The AF is increased by 0.02 each period that a new high is made" (if long) or new low is

made (if short).

EP is the "Extreme Price Point for the trade made so far. If Long , EP is the extreme high price for

the trade; if Short , EP is the extreme low price for the trade.”

Most websites will provide the above calculation for the Parabolic SAR but almost all of them

leave out this crucial detail:

B. "Never move the SAR into the previous day’s range or today’s range

"1. If Long , never move the SAR for tomorrow above the previous day’s low or

today’s low . If the SAR is calculated to be above the previous day’s low or

today’s low, then use the lower low between today and the previous day as

the new SAR. Make the next days calculations based upon this SAR.

"2. If Short , never move the SAR for tomorrow below the previous day’s high or

today’s high . If the SAR is calculated to be below the previous days’ high or

today’s high, then use the higher high between today and the previous day

as the new SAR. Make the next days calculations based upon this SAR."

When a Bullish SAR is broken then it gets placed at the SIP (significant point) of the prior trend.

In otherwords it is placed above the current candle and at the price that was the SIP.

The inverse is true for the first Bullish SAR.

"This system is a true reversal system; that is, every stop point is also a reverse point." If breaking

through a bearish SAR (one above price) that simultaneously signals to close a short and go

long.

DSL Synthetic MomentumThis indicator combines 5 running moving averages of different periods, calculate their momentum and synthesize the result into 1 single curve.

Dynamic levels made of the discontinued signal lines function are added to create pseudo overbought and oversold levels.

Rolling Skew (Returns) - Beasley SavageSkewness is a term in statistics used to describe asymmetry from the normal distribution in a set of statistical data. Skewness can come in the form of negative skewness or positive skewness, depending on whether data points are skewed to the left and negative, or to the right and positive of the data average. A dataset that shows this characteristic differs from a normal bell curve.