Advanced Volume Analytics and Distribution IndicatorThe Advanced Volume Analytics and Distribution Indicator is a sophisticated tool designed for financial analysts and traders who seek in-depth insights into market volume dynamics. This Pine Script-based indicator is a comprehensive solution, offering a rich set of features that analyze volume data using various statistical methods and theories. It's tailored for those who require a deeper understanding of market movements and volume distribution.

Key Features:

Volume Distribution Analysis: Utilizes standard deviation and mean calculations to analyze the distribution of trading volume. Employs z-scores to measure the standard deviations of volume from its mean, offering insights into volume anomalies.

Bell Curve Modeling: Constructs a bell curve (normal distribution) based on volume data, enabling users to visualize and assess the distribution of volume in a standard statistical format.

Provides a z-score based bell curve, offering a normalized view of volume deviations.

Exponential Smoothing: Applies exponential smoothing to volume data, giving more weight to recent observations. This feature is crucial for analyzing trending behaviors in volume data.

Stress Metric Calculation: Introduces a unique 'stress' metric, calculated using a custom formula. This metric is designed to evaluate the volatility or variability in the volume data over a specified period.

Central Limit Theorem (CLT) Mean Estimation: Implements CLT for estimating the mean of volume data. The CLT states that the distribution of sample means approximates a normal distribution as the sample size becomes larger.

Variance Point Estimation: Calculates the variance of volume data, providing insights into its variability and consistency over time.

Chi-Squared Test (Commented): Although not active in the initial release, the script includes a framework for a Chi-Squared Test to compare observed and expected volume frequencies, offering potential for future statistical comparisons.

Percentile Calculations and Convolution: Performs percentile calculations on volume data and employs convolution to these percentiles, enabling a more nuanced analysis of volume distribution.

Customizability: Users can input various parameters like anchor period, degrees of freedom, and smoothing preferences, making the tool adaptable to different analysis needs.

Visualization and Plotting: Features multiple plots for easy visualization of volume metrics, including stress, bell curves, point estimators, and smoothed data.

Theoretical Foundations:

This indicator is grounded in established statistical theories and methods, including the Central Limit Theorem, Chi-Squared Test (for future implementations), and convolution techniques. These foundations ensure that the indicator not only provides practical insights but also maintains a high standard of statistical rigor.

Intended Users:

This indicator is ideal for technical analysts, traders, and financial professionals who require a deep and statistically sound understanding of market volume behavior.

Release Notes:

This tool is designed a theoretical test of established statistical models and requires familiarity with Pine Script for customization. Future updates may include activation and expansion of the Chi-Squared Test functionality and additional statistical modules based on user feedback. It should be noted that it is advisable to use a logarithmic-inverted scale; when combined, these scales can provide a unique perspective that neither could offer alone. This combination might be particularly useful in highlighting exponential growth or decay trends, or in cases where the most significant data points are in the lower range of the dataset.

Notes of Stress Calculations:

The "stress metric" in the script is a custom-designed feature intended to measure the level of variability or volatility in the volume data over a given time period. This metric is calculated using a novel approach with concepts similar to those used in the field of engineering , particularly in stress analysis and finite element analysis (FEA).

Segmentation of Time Frame:

The script divides the given time frame (timeFrame) into smaller segments based on a specified number of units (units). This segmentation essentially breaks down the entire period into smaller, more manageable intervals for analysis. For each segment, the script calculates a 'stress' value. This involves iterating through each segment and performing calculations based on the source data (src), the default src is the volume data.

Calculation per Segment:

For each segment, the script identifies two points: the starting point (x1) and the ending point (x2). It then retrieves the corresponding values of the source data at these points (y1 and y2).

It calculates the difference in the x-axis (delta_x, the length of the segment) and the difference in the y-axis (delta_y, the change in volume over that segment).

Stress Calculation:

The script then calculates the 'stress' for each segment as the ratio of delta_y to delta_x. This ratio gives a measure of how much the volume has changed per unit of time within each segment. The stress values for each segment are then summed up to provide a cumulative measure of stress over the entire time frame.

The stress metric is essentially a measure of the volatility or variability in volume data. High stress values indicate larger changes in volume over shorter periods, suggesting more volatile market conditions. For traders and analysts, understanding the level of volatility is crucial. It can inform decision-making processes, risk management strategies, and provide insights into market sentiment. By comparing stress levels across different time frames or different securities, analysts can gain insights into relative market dynamics.

在腳本中搜尋"curve"

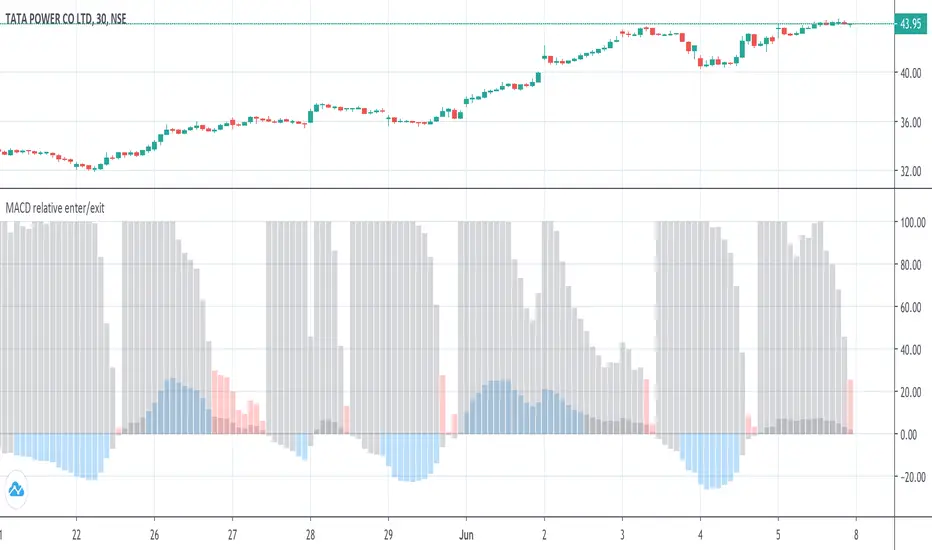

MACD histogram relative open/closePrelude

This script makes it easy to capture MACD Histogram open/close for automated trading.

There seems to be no "magic" value for MACD Histogram that always works as a cut-off for trade entry/exit, because of the variation in market price over time.

The idea behind this script is to replicate the view of the MACD graph we (humans) see on the screen, in mathematics, so the computer can approximately detect when the curve is opening/closing.

Math

The maths for this is composed of 2 sections -

1. Entry -

i. To trigger entry, we normalize the Histogram value by first determining the lowest and highest values on the MACD curves (MACD, Signal & Hist).

ii. The lowest and highest values are taken over the "Frame of reference" which is a hyperparameter.

iii. Once the frame of reference is determined, the entry cutoff param can be defined with respect to the values from (i) (10% by default)

2. Exit

To trigger an exit, a trader searches for the point where the Histogram starts to drop "steeply".

To convert the notion of "steep" into mathematics -

i. Take the max histogram value reached since last MACD curve flip

ii. Define the cutoff with reference to the value from (i) (30% by default)

Plots

Gray - Dead region

Blue - Histogram opening

Red - Histogram is closing

Notes

A good value for the frame of reference can be estimated by looking at the timescale of the graph you generally work with during manual trading.

For me, that turned out to be ~2.5 hours. (as shown in the above graph)

For a 3-minute ticker, frame of reference = 2.5 * 60 / 3 = 50

Which is the default given in this script.

Ultimately, it is up to you to do grid search and find these hyperparams for the stock and ticker size you're working with.

Also, this script only serves the purpose of detecting the Histogram curve opening/closing.

You may want to add further checks to perform proper trading using MACD.

Dynamic Flow Ribbon [Adaptive]The Dynamic Flow Ribbon is a next-generation trend-following tool designed to solve the two biggest problems traders face: Lag and Noise .

Unlike traditional Moving Averages (SMA/EMA) that are often too slow to catch reversals or too sensitive to chop, this indicator utilizes Rational Quadratic Kernel Smoothing . This advanced mathematical approach creates a "Flow Ribbon" that hugs price action tightly during trends while remaining silky smooth, filtering out the random noise that leads to false signals.

This is not just a crossover indicator; it is a complete Market Regime Detector . It automatically identifies when the market is trending and when it is ranging, helping you stay out of dangerous "chop" zones.

Why Use This?

Zero-Lag Smoothing: Experience the responsiveness of a fast EMA with the smoothness of a slow SMA.

Chop Filter: The ribbon automatically turns Gray when volatility (ADX) drops, signaling you to sit on your hands and preserve capital.

Visual Clarity: No messy lines. Just a clean, glowing ribbon that tells you the trend direction instantly.

How It Works

The indicator calculates two dynamic curves:

Fast Flow Line: Tracks immediate price action using a tight kernel window.

Base Flow Line: A slower, weighted baseline that acts as the trend anchor.

The Ribbon: The space between these lines forms the "Ribbon."

Green (Bullish): Fast Flow > Base Flow. The trend is Up.

Red (Bearish): Fast Flow < Base Flow. The trend is Down.

Gray (Flat): Volatility is too low (ADX < Threshold). The market is sideways.

How to Trade

This tool is best used for Trend Continuation and Reversal Catching .

The Entry: Wait for a Crossover Signal (Small Circle).

Buy when the Ribbon flips Green.

Sell when the Ribbon flips Red.

The Filter: If the Ribbon is Gray , ignore all signals. This prevents you from getting whipsawed in a ranging market.

The Exit: You can ride the trend until the Ribbon flips color, or use your own support/resistance targets.

Settings

Bandwidth (Smoothness): Adjusts the sensitivity of the kernel. Higher values = smoother ribbon (better for swing trading). Lower values = faster reaction (better for scalping).

Trend Filter: Toggle the ADX-based chop filter on/off.

Visuals: Fully customizable colors to match your chart aesthetic.

Pro Tip: Combine for Maximum Accuracy

While the Dynamic Flow Ribbon is excellent for Trend Direction, it does not plot Support & Resistance levels.

For the ultimate trading setup, I highly recommend pairing this with my AIO Pivot Master

or any other pivot indicator, which you can easily find on TradingView.

Use Dynamic Flow to determine the Direction .

Use AIO Pivot Master to find your Entry and Exit targets .

Disclaimer

For Educational and Informational Purposes Only

This indicator is provided for educational and informational purposes only and DOES NOT constitute financial, investment, or trading advice. It does not predict future market movements with certainty.

Risk Warning

Trading in financial markets (Stocks, Crypto, Futures, Forex, etc.) involves a high degree of risk and may not be suitable for all investors. You could lose some or all of your initial investment. Past performance of any trading system or methodology is not necessarily indicative of future results.

No Liability

The author of this script assumes no responsibility or liability for any errors or omissions in the content of this indicator, or for any trading losses or damages incurred as a result of using this tool. Users are solely responsible for their own trading decisions and should always use proper risk management. By using this script, you acknowledge and agree to these terms.

Ultimate RSI [captainua]Ultimate RSI

Overview

This indicator combines multiple RSI calculations with volume analysis, divergence detection, and trend filtering to provide a comprehensive RSI-based trading system. The script calculates RSI using three different periods (6, 14, 24) and applies various smoothing methods to reduce noise while maintaining responsiveness. The combination of these features creates a multi-layered confirmation system that reduces false signals by requiring alignment across multiple indicators and timeframes.

The script includes optimized configuration presets for instant setup: Scalping, Day Trading, Swing Trading, and Position Trading. Simply select a preset to instantly configure all settings for your trading style, or use Custom mode for full manual control. All settings include automatic input validation to prevent configuration errors and ensure optimal performance.

Configuration Presets

The script includes preset configurations optimized for different trading styles, allowing you to instantly configure the indicator for your preferred trading approach. Simply select a preset from the "Configuration Preset" dropdown menu:

- Scalping: Optimized for fast-paced trading with shorter RSI periods (4, 7, 9) and minimal smoothing. Noise reduction is automatically disabled, and momentum confirmation is disabled to allow faster signal generation. Designed for quick entries and exits in volatile markets.

- Day Trading: Balanced configuration for intraday trading with moderate RSI periods (6, 9, 14) and light smoothing. Momentum confirmation is enabled for better signal quality. Ideal for day trading strategies requiring timely but accurate signals.

- Swing Trading: Configured for medium-term positions with standard RSI periods (14, 14, 21) and moderate smoothing. Provides smoother signals suitable for swing trading timeframes. All noise reduction features remain active.

- Position Trading: Optimized for longer-term trades with extended RSI periods (24, 21, 28) and heavier smoothing. Filters are configured for highest-quality signals. Best for position traders holding trades over multiple days or weeks.

- Custom: Full manual control over all settings. All input parameters are available for complete customization. This is the default mode and maintains full backward compatibility with previous versions.

When a preset is selected, it automatically adjusts RSI periods, smoothing lengths, and filter settings to match the trading style. The preset configurations ensure optimal settings are applied instantly, eliminating the need for manual configuration. All settings can still be manually overridden if needed, providing flexibility while maintaining ease of use.

Input Validation and Error Prevention

The script includes comprehensive input validation to prevent configuration errors:

- Cross-Input Validation: Smoothing lengths are automatically validated to ensure they are always less than their corresponding RSI period length. If you set a smoothing length greater than or equal to the RSI length, the script automatically adjusts it to (RSI Length - 1). This prevents logical errors and ensures valid configurations.

- Input Range Validation: All numeric inputs have minimum and maximum value constraints enforced by TradingView's input system, preventing invalid parameter values.

- Smart Defaults: Preset configurations use validated default values that are tested and optimized for each trading style. When switching between presets, all related settings are automatically updated to maintain consistency.

Core Calculations

Multi-Period RSI:

The script calculates RSI using the standard Wilder's RSI formula: RSI = 100 - (100 / (1 + RS)), where RS = Average Gain / Average Loss over the specified period. Three separate RSI calculations run simultaneously:

- RSI(6): Uses 6-period lookback for high sensitivity to recent price changes, useful for scalping and early signal detection

- RSI(14): Standard 14-period RSI for balanced analysis, the most commonly used RSI period

- RSI(24): Longer 24-period RSI for trend confirmation, provides smoother signals with less noise

Each RSI can be smoothed using EMA, SMA, RMA (Wilder's smoothing), WMA, or Zero-Lag smoothing. Zero-Lag smoothing uses the formula: ZL-RSI = RSI + (RSI - RSI ) to reduce lag while maintaining signal quality. You can apply individual smoothing lengths to each RSI period, or use global smoothing where all three RSIs share the same smoothing length.

Dynamic Overbought/Oversold Thresholds:

Static thresholds (default 70/30) are adjusted based on market volatility using ATR. The formula: Dynamic OB = Base OB + (ATR × Volatility Multiplier × Base Percentage / 100), Dynamic OS = Base OS - (ATR × Volatility Multiplier × Base Percentage / 100). This adapts to volatile markets where traditional 70/30 levels may be too restrictive. During high volatility, the dynamic thresholds widen, and during low volatility, they narrow. The thresholds are clamped between 0-100 to remain within RSI bounds. The ATR is cached for performance optimization, updating on confirmed bars and real-time bars.

Adaptive RSI Calculation:

An adaptive RSI adjusts the standard RSI(14) based on current volatility relative to average volatility. The calculation: Adaptive Factor = (Current ATR / SMA of ATR over 20 periods) × Volatility Multiplier. If SMA of ATR is zero (edge case), the adaptive factor defaults to 0. The adaptive RSI = Base RSI × (1 + Adaptive Factor), clamped to 0-100. This makes the indicator more responsive during high volatility periods when traditional RSI may lag. The adaptive RSI is used for signal generation (buy/sell signals) but is not plotted on the chart.

Overbought/Oversold Fill Zones:

The script provides visual fill zones between the RSI line and the threshold lines when RSI is in overbought or oversold territory. The fill logic uses inclusive conditions: fills are shown when RSI is currently in the zone OR was in the zone on the previous bar. This ensures complete coverage of entry and exit boundaries. A minimum gap of 0.1 RSI points is maintained between the RSI plot and threshold line to ensure reliable polygon rendering in TradingView. The fill uses invisible plots at the threshold levels and the RSI value, with the fill color applied between them. You can select which RSI (6, 14, or 24) to use for the fill zones.

Divergence Detection

Regular Divergence:

Bullish divergence: Price makes a lower low (current low < lowest low from previous lookback period) while RSI makes a higher low (current RSI > lowest RSI from previous lookback period). Bearish divergence: Price makes a higher high (current high > highest high from previous lookback period) while RSI makes a lower high (current RSI < highest RSI from previous lookback period). The script compares current price/RSI values to the lowest/highest values from the previous lookback period using ta.lowest() and ta.highest() functions with index to reference the previous period's extreme.

Pivot-Based Divergence:

An enhanced divergence detection method that uses actual pivot points instead of simple lowest/highest comparisons. This provides more accurate divergence detection by identifying significant pivot lows/highs in both price and RSI. The pivot-based method uses a tolerance-based approach with configurable constants: 1% tolerance for price comparisons (priceTolerancePercent = 0.01) and 1.0 RSI point absolute tolerance for RSI comparisons (pivotTolerance = 1.0). Minimum divergence threshold is 1.0 RSI point (minDivergenceThreshold = 1.0). It looks for two recent pivot points and compares them: for bullish divergence, price makes a lower low (at least 1% lower) while RSI makes a higher low (at least 1.0 point higher). This method reduces false divergences by requiring actual pivot points rather than just any low/high within a period. When enabled, pivot-based divergence replaces the traditional method for more accurate signal generation.

Strong Divergence:

Regular divergence is confirmed by an engulfing candle pattern. Bullish engulfing requires: (1) Previous candle is bearish (close < open ), (2) Current candle is bullish (close > open), (3) Current close > previous open, (4) Current open < previous close. Bearish engulfing is the inverse: previous bullish, current bearish, current close < previous open, current open > previous close. Strong divergence signals are marked with visual indicators (🐂 for bullish, 🐻 for bearish) and have separate alert conditions.

Hidden Divergence:

Continuation patterns that signal trend continuation rather than reversal. Bullish hidden divergence: Price makes a higher low (current low > lowest low from previous period) but RSI makes a lower low (current RSI < lowest RSI from previous period). Bearish hidden divergence: Price makes a lower high (current high < highest high from previous period) but RSI makes a higher high (current RSI > highest RSI from previous period). These patterns indicate the trend is likely to continue in the current direction.

Volume Confirmation System

Volume threshold filtering requires current volume to exceed the volume SMA multiplied by the threshold factor. The formula: Volume Confirmed = Volume > (Volume SMA × Threshold). If the threshold is set to 0.1 or lower, volume confirmation is effectively disabled (always returns true). This allows you to use the indicator without volume filtering if desired.

Volume Climax is detected when volume exceeds: Volume SMA + (Volume StdDev × Multiplier). This indicates potential capitulation moments where extreme volume accompanies price movements. Volume Dry-Up is detected when volume falls below: Volume SMA - (Volume StdDev × Multiplier), indicating low participation periods that may produce unreliable signals. The volume SMA is cached for performance, updating on confirmed and real-time bars.

Multi-RSI Synergy

The script generates signals when multiple RSI periods align in overbought or oversold zones. This creates a confirmation system that reduces false signals. In "ALL" mode, all three RSIs (6, 14, 24) must be simultaneously above the overbought threshold OR all three must be below the oversold threshold. In "2-of-3" mode, any two of the three RSIs must align in the same direction. The script counts how many RSIs are in each zone: twoOfThreeOB = ((rsi6OB ? 1 : 0) + (rsi14OB ? 1 : 0) + (rsi24OB ? 1 : 0)) >= 2.

Synergy signals require: (1) Multi-RSI alignment (ALL or 2-of-3), (2) Volume confirmation, (3) Reset condition satisfied (enough bars since last synergy signal), (4) Additional filters passed (RSI50, Trend, ADX, Volume Dry-Up avoidance). Separate reset conditions track buy and sell signals independently. The reset condition uses ta.barssince() to count bars since the last trigger, returning true if the condition never occurred (allowing first signal) or if enough bars have passed.

Regression Forecasting

The script uses historical RSI values to forecast future RSI direction using four methods. The forecast horizon is configurable (1-50 bars ahead). Historical data is collected into an array, and regression coefficients are calculated based on the selected method.

Linear Regression: Calculates the least-squares fit line (y = mx + b) through the last N RSI values. The calculation: meanX = sumX / horizon, meanY = sumY / horizon, denominator = sumX² - horizon × meanX², m = (sumXY - horizon × meanX × meanY) / denominator, b = meanY - m × meanX. The forecast projects this line forward: forecast = b + m × i for i = 1 to horizon.

Polynomial Regression: Fits a quadratic curve (y = ax² + bx + c) to capture non-linear trends. The system of equations is solved using Cramer's rule with a 3×3 determinant. If the determinant is too small (< 0.0001), the system falls back to linear regression. Coefficients are calculated by solving: n×c + sumX×b + sumX²×a = sumY, sumX×c + sumX²×b + sumX³×a = sumXY, sumX²×c + sumX³×b + sumX⁴×a = sumX²Y. Note: Due to the O(n³) computational complexity of polynomial regression, the forecast horizon is automatically limited to a maximum of 20 bars when using polynomial regression to maintain optimal performance. If you set a horizon greater than 20 bars with polynomial regression, it will be automatically capped at 20 bars.

Exponential Smoothing: Applies exponential smoothing with adaptive alpha = 2/(horizon+1). The smoothing iterates from oldest to newest value: smoothed = alpha × series + (1 - alpha) × smoothed. Trend is calculated by comparing current smoothed value to an earlier smoothed value (at 60% of horizon): trend = (smoothed - earlierSmoothed) / (horizon - earlierIdx). Forecast: forecast = base + trend × i.

Moving Average: Uses the difference between short MA (horizon/2) and long MA (horizon) to estimate trend direction. Trend = (maShort - maLong) / (longLen - shortLen). Forecast: forecast = maShort + trend × i.

Confidence bands are calculated using RMSE (Root Mean Squared Error) of historical forecast accuracy. The error calculation compares historical values with forecast values: RMSE = sqrt(sumSquaredError / count). If insufficient data exists, it falls back to calculating standard deviation of recent RSI values. Confidence bands = forecast ± (RMSE × confidenceLevel). All forecast values and confidence bands are clamped to 0-100 to remain within RSI bounds. The regression functions include comprehensive safety checks: horizon validation (must not exceed array size), empty array handling, edge case handling for horizon=1 scenarios, division-by-zero protection, and bounds checking for all array access operations to prevent runtime errors.

Strong Top/Bottom Detection

Strong buy signals require three conditions: (1) RSI is at its lowest point within the bottom period: rsiVal <= ta.lowest(rsiVal, bottomPeriod), (2) RSI is below the oversold threshold minus a buffer: rsiVal < (oversoldThreshold - rsiTopBottomBuffer), where rsiTopBottomBuffer = 2.0 RSI points, (3) The absolute difference between current RSI and the lowest RSI exceeds the threshold value: abs(rsiVal - ta.lowest(rsiVal, bottomPeriod)) > threshold. This indicates a bounce from extreme levels with sufficient distance from the absolute low.

Strong sell signals use the inverse logic: RSI at highest point, above overbought threshold + rsiTopBottomBuffer (2.0 RSI points), and difference from highest exceeds threshold. Both signals also require: volume confirmation, reset condition satisfied (separate reset for buy vs sell), and all additional filters passed (RSI50, Trend, ADX, Volume Dry-Up avoidance).

The reset condition uses separate logic for buy and sell: resetCondBuy checks bars since isRSIAtBottom, resetCondSell checks bars since isRSIAtTop. This ensures buy signals reset based on bottom conditions and sell signals reset based on top conditions, preventing incorrect signal blocking.

Filtering System

RSI(50) Filter: Only allows buy signals when RSI(14) > 50 (bullish momentum) and sell signals when RSI(14) < 50 (bearish momentum). This filter ensures you're buying in uptrends and selling in downtrends from a momentum perspective. The filter is optional and can be disabled. Recommended to enable for noise reduction.

Trend Filter: Uses a long-term EMA (default 200) to determine trend direction. Buy signals require price above EMA, sell signals require price below EMA. The EMA slope is calculated as: emaSlope = ema - ema . Optional EMA slope filter additionally requires the EMA to be rising (slope > 0) for buy signals or falling (slope < 0) for sell signals. This provides stronger trend confirmation by requiring both price position and EMA direction.

ADX Filter: Uses the Directional Movement Index (calculated via ta.dmi()) to measure trend strength. Signals only fire when ADX exceeds the threshold (default 20), indicating a strong trend rather than choppy markets. The ADX calculation uses separate length and smoothing parameters. This filter helps avoid signals during sideways/consolidation periods.

Volume Dry-Up Avoidance: Prevents signals during periods of extremely low volume relative to average. If volume dry-up is detected and the filter is enabled, signals are blocked. This helps avoid unreliable signals that occur during low participation periods.

RSI Momentum Confirmation: Requires RSI to be accelerating in the signal direction before confirming signals. For buy signals, RSI must be consistently rising (recovering from oversold) over the lookback period. For sell signals, RSI must be consistently falling (declining from overbought) over the lookback period. The momentum check verifies that all consecutive changes are in the correct direction AND the cumulative change is significant. This filter ensures signals only fire when RSI momentum aligns with the signal direction, reducing false signals from weak momentum.

Multi-Timeframe Confirmation: Requires higher timeframe RSI to align with the signal direction. For buy signals, current RSI must be below the higher timeframe RSI by at least the confirmation threshold. For sell signals, current RSI must be above the higher timeframe RSI by at least the confirmation threshold. This ensures signals align with the larger trend context, reducing counter-trend trades. The higher timeframe RSI is fetched using request.security() from the selected timeframe.

All filters use the pattern: filterResult = not filterEnabled OR conditionMet. This means if a filter is disabled, it always passes (returns true). Filters can be combined, and all must pass for a signal to fire.

RSI Centerline and Period Crossovers

RSI(50) Centerline Crossovers: Detects when the selected RSI source crosses above or below the 50 centerline. Bullish crossover: ta.crossover(rsiSource, 50), bearish crossover: ta.crossunder(rsiSource, 50). You can select which RSI (6, 14, or 24) to use for these crossovers. These signals indicate momentum shifts from bearish to bullish (above 50) or bullish to bearish (below 50).

RSI Period Crossovers: Detects when different RSI periods cross each other. Available pairs: RSI(6) × RSI(14), RSI(14) × RSI(24), or RSI(6) × RSI(24). Bullish crossover: fast RSI crosses above slow RSI (ta.crossover(rsiFast, rsiSlow)), indicating momentum acceleration. Bearish crossover: fast RSI crosses below slow RSI (ta.crossunder(rsiFast, rsiSlow)), indicating momentum deceleration. These crossovers can signal shifts in momentum before price moves.

StochRSI Calculation

Stochastic RSI applies the Stochastic oscillator formula to RSI values instead of price. The calculation: %K = ((RSI - Lowest RSI) / (Highest RSI - Lowest RSI)) × 100, where the lookback is the StochRSI length. If the range is zero, %K defaults to 50.0. %K is then smoothed using SMA with the %K smoothing length. %D is calculated as SMA of smoothed %K with the %D smoothing length. All values are clamped to 0-100. You can select which RSI (6, 14, or 24) to use as the source for StochRSI calculation.

RSI Bollinger Bands

Bollinger Bands are applied to RSI(14) instead of price. The calculation: Basis = SMA(RSI(14), BB Period), StdDev = stdev(RSI(14), BB Period), Upper = Basis + (StdDev × Deviation Multiplier), Lower = Basis - (StdDev × Deviation Multiplier). This creates dynamic zones around RSI that adapt to RSI volatility. When RSI touches or exceeds the bands, it indicates extreme conditions relative to recent RSI behavior.

Noise Reduction System

The script includes a comprehensive noise reduction system to filter false signals and improve accuracy. When enabled, signals must pass multiple quality checks:

Signal Strength Requirement: RSI must be at least X points away from the centerline (50). For buy signals, RSI must be at least X points below 50. For sell signals, RSI must be at least X points above 50. This ensures signals only trigger when RSI is significantly in oversold/overbought territory, not just near neutral.

Extreme Zone Requirement: RSI must be deep in the OB/OS zone. For buy signals, RSI must be at least X points below the oversold threshold. For sell signals, RSI must be at least X points above the overbought threshold. This ensures signals only fire in extreme conditions where reversals are more likely.

Consecutive Bar Confirmation: The signal condition must persist for N consecutive bars before triggering. This reduces false signals from single-bar spikes or noise. The confirmation checks that the signal condition was true for all bars in the lookback period.

Zone Persistence (Optional): Requires RSI to remain in the OB/OS zone for N consecutive bars, not just touch it. This ensures RSI is truly in an extreme state rather than just briefly touching the threshold. When enabled, this provides stricter filtering for higher-quality signals.

RSI Slope Confirmation (Optional): Requires RSI to be moving in the expected signal direction. For buy signals, RSI should be rising (recovering from oversold). For sell signals, RSI should be falling (declining from overbought). This ensures momentum is aligned with the signal direction. The slope is calculated by comparing current RSI to RSI N bars ago.

All noise reduction filters can be enabled/disabled independently, allowing you to customize the balance between signal frequency and accuracy. The default settings provide a good balance, but you can adjust them based on your trading style and market conditions.

Alert System

The script includes separate alert conditions for each signal type: buy/sell (adaptive RSI crossovers), divergence (regular, strong, hidden), crossovers (RSI50 centerline, RSI period crossovers), synergy signals, and trend breaks. Each alert type has its own alertcondition() declaration with a unique title and message.

An optional cooldown system prevents alert spam by requiring a minimum number of bars between alerts of the same type. The cooldown check: canAlert = na(lastAlertBar) OR (bar_index - lastAlertBar >= cooldownBars). If the last alert bar is na (first alert), it always allows the alert. Each alert type maintains its own lastAlertBar variable, so cooldowns are independent per signal type. The default cooldown is 10 bars, which is recommended for noise reduction.

Higher Timeframe RSI

The script can display RSI from a higher timeframe using request.security(). This allows you to see the RSI context from a larger timeframe (e.g., daily RSI on an hourly chart). The higher timeframe RSI uses RSI(14) calculation from the selected timeframe. This provides context for the current timeframe's RSI position relative to the larger trend.

RSI Pivot Trendlines

The script can draw trendlines connecting pivot highs and lows on RSI(6). This feature helps visualize RSI trends and identify potential trend breaks.

Pivot Detection: Pivots are detected using a configurable period. The script can require pivots to have minimum strength (RSI points difference from surrounding bars) to filter out weak pivots. Lower minPivotStrength values detect more pivots (more trendlines), while higher values detect only stronger pivots (fewer but more significant trendlines). Pivot confirmation is optional: when enabled, the script waits N bars to confirm the pivot remains the extreme, reducing repainting. Pivot confirmation functions (f_confirmPivotLow and f_confirmPivotHigh) are always called on every bar for consistency, as recommended by TradingView. When pivot bars are not available (na), safe default values are used, and the results are then used conditionally based on confirmation settings. This ensures consistent calculations and prevents calculation inconsistencies.

Trendline Drawing: Uptrend lines connect confirmed pivot lows (green), and downtrend lines connect confirmed pivot highs (red). By default, only the most recent trendline is shown (old trendlines are deleted when new pivots are confirmed). This keeps the chart clean and uncluttered. If "Keep Historical Trendlines" is enabled, the script preserves up to N historical trendlines (configurable via "Max Trendlines to Keep", default 5). When historical trendlines are enabled, old trendlines are saved to arrays instead of being deleted, allowing you to see multiple trendlines simultaneously for better trend analysis. The arrays are automatically limited to prevent memory accumulation.

Trend Break Detection: Signals are generated when RSI breaks above or below trendlines. Uptrend breaks (RSI crosses below uptrend line) generate buy signals. Downtrend breaks (RSI crosses above downtrend line) generate sell signals. Optional trend break confirmation requires the break to persist for N bars and optionally include volume confirmation. Trendline angle filtering can exclude flat/weak trendlines from generating signals (minTrendlineAngle > 0 filters out weak/flat trendlines).

How Components Work Together

The combination of multiple RSI periods provides confirmation across different timeframes, reducing false signals. RSI(6) catches early moves, RSI(14) provides balanced signals, and RSI(24) confirms longer-term trends. When all three align (synergy), it indicates strong consensus across timeframes.

Volume confirmation ensures signals occur with sufficient market participation, filtering out low-volume false breakouts. Volume climax detection identifies potential reversal points, while volume dry-up avoidance prevents signals during unreliable low-volume periods.

Trend filters align signals with the overall market direction. The EMA filter ensures you're trading with the trend, and the EMA slope filter adds an additional layer by requiring the trend to be strengthening (rising EMA for buys, falling EMA for sells).

ADX filter ensures signals only fire during strong trends, avoiding choppy/consolidation periods. RSI(50) filter ensures momentum alignment with the trade direction.

Momentum confirmation requires RSI to be accelerating in the signal direction, ensuring signals only fire when momentum is aligned. Multi-timeframe confirmation ensures signals align with higher timeframe trends, reducing counter-trend trades.

Divergence detection identifies potential reversals before they occur, providing early warning signals. Pivot-based divergence provides more accurate detection by using actual pivot points. Hidden divergence identifies continuation patterns, useful for trend-following strategies.

The noise reduction system combines multiple filters (signal strength, extreme zone, consecutive bars, zone persistence, RSI slope) to significantly reduce false signals. These filters work together to ensure only high-quality signals are generated.

The synergy system requires alignment across all RSI periods for highest-quality signals, significantly reducing false positives. Regression forecasting provides forward-looking context, helping anticipate potential RSI direction changes.

Pivot trendlines provide visual trend analysis and can generate signals when RSI breaks trendlines, indicating potential reversals or continuations.

Reset conditions prevent signal spam by requiring a minimum number of bars between signals. Separate reset conditions for buy and sell signals ensure proper signal management.

Usage Instructions

Configuration Presets (Recommended): The script includes optimized preset configurations for instant setup. Simply select your trading style from the "Configuration Preset" dropdown:

- Scalping Preset: RSI(4, 7, 9) with minimal smoothing. Noise reduction disabled, momentum confirmation disabled for fastest signals.

- Day Trading Preset: RSI(6, 9, 14) with light smoothing. Momentum confirmation enabled for better signal quality.

- Swing Trading Preset: RSI(14, 14, 21) with moderate smoothing. Balanced configuration for medium-term trades.

- Position Trading Preset: RSI(24, 21, 28) with heavier smoothing. Optimized for longer-term positions with all filters active.

- Custom Mode: Full manual control over all settings. Default behavior matches previous script versions.

Presets automatically configure RSI periods, smoothing lengths, and filter settings. You can still manually adjust any setting after selecting a preset if needed.

Getting Started: The easiest way to get started is to select a configuration preset matching your trading style (Scalping, Day Trading, Swing Trading, or Position Trading) from the "Configuration Preset" dropdown. This instantly configures all settings for optimal performance. Alternatively, use "Custom" mode for full manual control. The default configuration (Custom mode) shows RSI(6), RSI(14), and RSI(24) with their default smoothing. Overbought/oversold fill zones are enabled by default.

Customizing RSI Periods: Adjust the RSI lengths (6, 14, 24) based on your trading timeframe. Shorter periods (6) for scalping, standard (14) for day trading, longer (24) for swing trading. You can disable any RSI period you don't need.

Smoothing Selection: Choose smoothing method based on your needs. EMA provides balanced smoothing, RMA (Wilder's) is traditional, Zero-Lag reduces lag but may increase noise. Adjust smoothing lengths individually or use global smoothing for consistency. Note: Smoothing lengths are automatically validated to ensure they are always less than the corresponding RSI period length. If you set smoothing >= RSI length, it will be auto-adjusted to prevent invalid configurations.

Dynamic OB/OS: The dynamic thresholds automatically adapt to volatility. Adjust the volatility multiplier and base percentage to fine-tune sensitivity. Higher values create wider thresholds in volatile markets.

Volume Confirmation: Set volume threshold to 1.2 (default) for standard confirmation, higher for stricter filtering, or 0.1 to disable volume filtering entirely.

Multi-RSI Synergy: Use "ALL" mode for highest-quality signals (all 3 RSIs must align), or "2-of-3" mode for more frequent signals. Adjust the reset period to control signal frequency.

Filters: Enable filters gradually to find your preferred balance. Start with volume confirmation, then add trend filter, then ADX for strongest confirmation. RSI(50) filter is useful for momentum-based strategies and is recommended for noise reduction. Momentum confirmation and multi-timeframe confirmation add additional layers of accuracy but may reduce signal frequency.

Noise Reduction: The noise reduction system is enabled by default with balanced settings. Adjust minSignalStrength (default 3.0) to control how far RSI must be from centerline. Increase requireConsecutiveBars (default 1) to require signals to persist longer. Enable requireZonePersistence and requireRsiSlope for stricter filtering (higher quality but fewer signals). Start with defaults and adjust based on your needs.

Divergence: Enable divergence detection and adjust lookback periods. Strong divergence (with engulfing confirmation) provides higher-quality signals. Hidden divergence is useful for trend-following strategies. Enable pivot-based divergence for more accurate detection using actual pivot points instead of simple lowest/highest comparisons. Pivot-based divergence uses tolerance-based matching (1% for price, 1.0 RSI point for RSI) for better accuracy.

Forecasting: Enable regression forecasting to see potential RSI direction. Linear regression is simplest, polynomial captures curves, exponential smoothing adapts to trends. Adjust horizon based on your trading timeframe. Confidence bands show forecast uncertainty - wider bands indicate less reliable forecasts.

Pivot Trendlines: Enable pivot trendlines to visualize RSI trends and identify trend breaks. Adjust pivot detection period (default 5) - higher values detect fewer but stronger pivots. Enable pivot confirmation (default ON) to reduce repainting. Set minPivotStrength (default 1.0) to filter weak pivots - lower values detect more pivots (more trendlines), higher values detect only stronger pivots (fewer trendlines). Enable "Keep Historical Trendlines" to preserve multiple trendlines instead of just the most recent one. Set "Max Trendlines to Keep" (default 5) to control how many historical trendlines are preserved. Enable trend break confirmation for more reliable break signals. Adjust minTrendlineAngle (default 0.0) to filter flat trendlines - set to 0.1-0.5 to exclude weak trendlines.

Alerts: Set up alerts for your preferred signal types. Enable cooldown to prevent alert spam. Each signal type has its own alert condition, so you can be selective about which signals trigger alerts.

Visual Elements and Signal Markers

The script uses various visual markers to indicate signals and conditions:

- "sBottom" label (green): Strong bottom signal - RSI at extreme low with strong buy conditions

- "sTop" label (red): Strong top signal - RSI at extreme high with strong sell conditions

- "SyBuy" label (lime): Multi-RSI synergy buy signal - all RSIs aligned oversold

- "SySell" label (red): Multi-RSI synergy sell signal - all RSIs aligned overbought

- 🐂 emoji (green): Strong bullish divergence detected

- 🐻 emoji (red): Strong bearish divergence detected

- 🔆 emoji: Weak divergence signals (if enabled)

- "H-Bull" label: Hidden bullish divergence

- "H-Bear" label: Hidden bearish divergence

- ⚡ marker (top of pane): Volume climax detected (extreme volume) - positioned at top for visibility

- 💧 marker (top of pane): Volume dry-up detected (very low volume) - positioned at top for visibility

- ↑ triangle (lime): Uptrend break signal - RSI breaks below uptrend line

- ↓ triangle (red): Downtrend break signal - RSI breaks above downtrend line

- Triangle up (lime): RSI(50) bullish crossover

- Triangle down (red): RSI(50) bearish crossover

- Circle markers: RSI period crossovers

All markers are positioned at the RSI value where the signal occurs, using location.absolute for precise placement.

Signal Priority and Interpretation

Signals are generated independently and can occur simultaneously. Higher-priority signals generally indicate stronger setups:

1. Multi-RSI Synergy signals (SyBuy/SySell) - Highest priority: Requires alignment across all RSI periods plus volume and filter confirmation. These are the most reliable signals.

2. Strong Top/Bottom signals (sTop/sBottom) - High priority: Indicates extreme RSI levels with strong bounce conditions. Requires volume confirmation and all filters.

3. Divergence signals - Medium-High priority: Strong divergence (with engulfing) is more reliable than regular divergence. Hidden divergence indicates continuation rather than reversal.

4. Adaptive RSI crossovers - Medium priority: Buy when adaptive RSI crosses below dynamic oversold, sell when it crosses above dynamic overbought. These use volatility-adjusted RSI for more accurate signals.

5. RSI(50) centerline crossovers - Medium priority: Momentum shift signals. Less reliable alone but useful when combined with other confirmations.

6. RSI period crossovers - Lower priority: Early momentum shift indicators. Can provide early warning but may produce false signals in choppy markets.

Best practice: Wait for multiple confirmations. For example, a synergy signal combined with divergence and volume climax provides the strongest setup.

Chart Requirements

For proper script functionality and compliance with TradingView requirements, ensure your chart displays:

- Symbol name: The trading pair or instrument name should be visible

- Timeframe: The chart timeframe should be clearly displayed

- Script name: "Ultimate RSI " should be visible in the indicator title

These elements help traders understand what they're viewing and ensure proper script identification. The script automatically includes this information in the indicator title and chart labels.

Performance Considerations

The script is optimized for performance:

- ATR and Volume SMA are cached using var variables, updating only on confirmed and real-time bars to reduce redundant calculations

- Forecast line arrays are dynamically managed: lines are reused when possible, and unused lines are deleted to prevent memory accumulation

- Calculations use efficient Pine Script functions (ta.rsi, ta.ema, etc.) which are optimized by TradingView

- Array operations are minimized where possible, with direct calculations preferred

- Polynomial regression automatically caps the forecast horizon at 20 bars (POLYNOMIAL_MAX_HORIZON constant) to prevent performance degradation, as polynomial regression has O(n³) complexity. This safeguard ensures optimal performance even with large horizon settings

- Pivot detection includes edge case handling to ensure reliable calculations even on early bars with limited historical data. Regression forecasting functions include comprehensive safety checks: horizon validation (must not exceed array size), empty array handling, edge case handling for horizon=1 scenarios, and division-by-zero protection in all mathematical operations

The script should perform well on all timeframes. On very long historical data, forecast lines may accumulate if the horizon is large; consider reducing the forecast horizon if you experience performance issues. The polynomial regression performance safeguard automatically prevents performance issues for that specific regression type.

Known Limitations and Considerations

- Forecast lines are forward-looking projections and should not be used as definitive predictions. They provide context but are not guaranteed to be accurate.

- Dynamic OB/OS thresholds can exceed 100 or go below 0 in extreme volatility scenarios, but are clamped to 0-100 range. This means in very volatile markets, the dynamic thresholds may not widen as much as the raw calculation suggests.

- Volume confirmation requires sufficient historical volume data. On new instruments or very short timeframes, volume calculations may be less reliable.

- Higher timeframe RSI uses request.security() which may have slight delays on some data feeds.

- Regression forecasting requires at least N bars of history (where N = forecast horizon) before it can generate forecasts. Early bars will not show forecast lines.

- StochRSI calculation requires the selected RSI source to have sufficient history. Very short RSI periods on new charts may produce less reliable StochRSI values initially.

Practical Use Cases

The indicator can be configured for different trading styles and timeframes:

Swing Trading: Select the "Swing Trading" preset for instant optimal configuration. This preset uses RSI periods (14, 14, 21) with moderate smoothing. Alternatively, manually configure: Use RSI(24) with Multi-RSI Synergy in "ALL" mode, combined with trend filter (EMA 200) and ADX filter. This configuration provides high-probability setups with strong confirmation across multiple RSI periods.

Day Trading: Select the "Day Trading" preset for instant optimal configuration. This preset uses RSI periods (6, 9, 14) with light smoothing and momentum confirmation enabled. Alternatively, manually configure: Use RSI(6) with Zero-Lag smoothing for fast signal detection. Enable volume confirmation with threshold 1.2-1.5 for reliable entries. Combine with RSI(50) filter to ensure momentum alignment. Strong top/bottom signals work well for day trading reversals.

Trend Following: Enable trend filter (EMA) and EMA slope filter for strong trend confirmation. Use RSI(14) or RSI(24) with ADX filter to avoid choppy markets. Hidden divergence signals are useful for trend continuation entries.

Reversal Trading: Focus on divergence detection (regular and strong) combined with strong top/bottom signals. Enable volume climax detection to identify capitulation moments. Use RSI(6) for early reversal signals, confirmed by RSI(14) and RSI(24).

Forecasting and Planning: Enable regression forecasting with polynomial or exponential smoothing methods. Use forecast horizon of 10-20 bars for swing trading, 5-10 bars for day trading. Confidence bands help assess forecast reliability.

Multi-Timeframe Analysis: Enable higher timeframe RSI to see context from larger timeframes. For example, use daily RSI on hourly charts to understand the larger trend context. This helps avoid counter-trend trades.

Scalping: Select the "Scalping" preset for instant optimal configuration. This preset uses RSI periods (4, 7, 9) with minimal smoothing, disables noise reduction, and disables momentum confirmation for faster signals. Alternatively, manually configure: Use RSI(6) with minimal smoothing (or Zero-Lag) for ultra-fast signals. Disable most filters except volume confirmation. Use RSI period crossovers (RSI(6) × RSI(14)) for early momentum shifts. Set volume threshold to 1.0-1.2 for less restrictive filtering.

Position Trading: Select the "Position Trading" preset for instant optimal configuration. This preset uses extended RSI periods (24, 21, 28) with heavier smoothing, optimized for longer-term trades. Alternatively, manually configure: Use RSI(24) with all filters enabled (Trend, ADX, RSI(50), Volume Dry-Up avoidance). Multi-RSI Synergy in "ALL" mode provides highest-quality signals.

Practical Tips and Best Practices

Getting Started: The fastest way to get started is to select a configuration preset that matches your trading style. Simply choose "Scalping", "Day Trading", "Swing Trading", or "Position Trading" from the "Configuration Preset" dropdown to instantly configure all settings optimally. For advanced users, use "Custom" mode for full manual control. The default configuration (Custom mode) is balanced and works well across different markets. After observing behavior, customize settings to match your trading style.

Reducing Repainting: All signals are based on confirmed bars, minimizing repainting. The script uses confirmed bar data for all calculations to ensure backtesting accuracy.

Signal Quality: Multi-RSI Synergy signals in "ALL" mode provide the highest-quality signals because they require alignment across all three RSI periods. These signals have lower frequency but higher reliability. For more frequent signals, use "2-of-3" mode. The noise reduction system further improves signal quality by requiring multiple confirmations (signal strength, extreme zone, consecutive bars, optional zone persistence and RSI slope). Adjust noise reduction settings to balance signal frequency vs. accuracy.

Filter Combinations: Start with volume confirmation, then add trend filter for trend alignment, then ADX filter for trend strength. Combining all three filters significantly reduces false signals but also reduces signal frequency. Find your balance based on your risk tolerance.

Volume Filtering: Set volume threshold to 0.1 or lower to effectively disable volume filtering if you trade instruments with unreliable volume data or want to test without volume confirmation. Standard confirmation uses 1.2-1.5 threshold.

RSI Period Selection: RSI(6) is most sensitive and best for scalping or early signal detection. RSI(14) provides balanced signals suitable for day trading. RSI(24) is smoother and better for swing trading and trend confirmation. You can disable any RSI period you don't need to reduce visual clutter.

Smoothing Methods: EMA provides balanced smoothing with moderate lag. RMA (Wilder's smoothing) is traditional and works well for RSI. Zero-Lag reduces lag but may increase noise. WMA gives more weight to recent values. Choose based on your preference for responsiveness vs. smoothness.

Forecasting: Linear regression is simplest and works well for trending markets. Polynomial regression captures curves and works better in ranging markets. Exponential smoothing adapts to trends. Moving average method is most conservative. Use confidence bands to assess forecast reliability.

Divergence: Strong divergence (with engulfing confirmation) is more reliable than regular divergence. Hidden divergence indicates continuation rather than reversal, useful for trend-following strategies. Pivot-based divergence provides more accurate detection by using actual pivot points instead of simple lowest/highest comparisons. Adjust lookback periods based on your timeframe: shorter for day trading, longer for swing trading. Pivot divergence period (default 5) controls the sensitivity of pivot detection.

Dynamic Thresholds: Dynamic OB/OS thresholds automatically adapt to volatility. In volatile markets, thresholds widen; in calm markets, they narrow. Adjust the volatility multiplier and base percentage to fine-tune sensitivity. Higher values create wider thresholds in volatile markets.

Alert Management: Enable alert cooldown (default 10 bars, recommended) to prevent alert spam. Each alert type has its own cooldown, so you can set different cooldowns for different signal types. For example, use shorter cooldown for synergy signals (high quality) and longer cooldown for crossovers (more frequent). The cooldown system works independently for each signal type, preventing spam while allowing different signal types to fire when appropriate.

Technical Specifications

- Pine Script Version: v6

- Indicator Type: Non-overlay (displays in separate panel below price chart)

- Repainting Behavior: Minimal - all signals are based on confirmed bars, ensuring accurate backtesting results

- Performance: Optimized with caching for ATR and volume calculations. Forecast arrays are dynamically managed to prevent memory accumulation.

- Compatibility: Works on all timeframes (1 minute to 1 month) and all instruments (stocks, forex, crypto, futures, etc.)

- Edge Case Handling: All calculations include safety checks for division by zero, NA values, and boundary conditions. Reset conditions and alert cooldowns handle edge cases where conditions never occurred or values are NA.

- Reset Logic: Separate reset conditions for buy signals (based on bottom conditions) and sell signals (based on top conditions) ensure logical correctness.

- Input Parameters: 60+ customizable parameters organized into logical groups for easy configuration. Configuration presets available for instant setup (Scalping, Day Trading, Swing Trading, Position Trading, Custom).

- Noise Reduction: Comprehensive noise reduction system with multiple filters (signal strength, extreme zone, consecutive bars, zone persistence, RSI slope) to reduce false signals.

- Pivot-Based Divergence: Enhanced divergence detection using actual pivot points for improved accuracy.

- Momentum Confirmation: RSI momentum filter ensures signals only fire when RSI is accelerating in the signal direction.

- Multi-Timeframe Confirmation: Optional higher timeframe RSI alignment for trend confirmation.

- Enhanced Pivot Trendlines: Trendline drawing with strength requirements, confirmation, and trend break detection.

Technical Notes

- All RSI values are clamped to 0-100 range to ensure valid oscillator values

- ATR and Volume SMA are cached for performance, updating on confirmed and real-time bars

- Reset conditions handle edge cases: if a condition never occurred, reset returns true (allows first signal)

- Alert cooldown handles na values: if no previous alert, cooldown allows the alert

- Forecast arrays are dynamically sized based on horizon, with unused lines cleaned up

- Fill logic uses a minimum gap (0.1) to ensure reliable polygon rendering in TradingView

- All calculations include safety checks for division by zero and boundary conditions. Regression functions validate that horizon doesn't exceed array size, and all array access operations include bounds checking to prevent out-of-bounds errors

- The script uses separate reset conditions for buy signals (based on bottom conditions) and sell signals (based on top conditions) for logical correctness

- Background coloring uses a fallback system: dynamic color takes priority, then RSI(6) heatmap, then monotone if both are disabled

- Noise reduction filters are applied after accuracy filters, providing multiple layers of signal quality control

- Pivot trendlines use strength requirements to filter weak pivots, reducing noise in trendline drawing. Historical trendlines are stored in arrays and automatically limited to prevent memory accumulation when "Keep Historical Trendlines" is enabled

- Volume climax and dry-up markers are positioned at the top of the pane for better visibility

- All calculations are optimized with conditional execution - features only calculate when enabled (performance optimization)

- Input Validation: Automatic cross-input validation ensures smoothing lengths are always less than RSI period lengths, preventing configuration errors

- Configuration Presets: Four optimized preset configurations (Scalping, Day Trading, Swing Trading, Position Trading) for instant setup, plus Custom mode for full manual control

- Constants Management: Magic numbers extracted to documented constants for improved maintainability and easier tuning (pivot tolerance, divergence thresholds, fill gap, etc.)

- TradingView Function Consistency: All TradingView functions (ta.crossover, ta.crossunder, ta.atr, ta.lowest, ta.highest, ta.lowestbars, ta.highestbars, etc.) and custom functions that depend on historical results (f_consecutiveBarConfirmation, f_rsiSlopeConfirmation, f_rsiZonePersistence, f_applyAllFilters, f_rsiMomentum, f_forecast, f_confirmPivotLow, f_confirmPivotHigh) are called on every bar for consistency, as recommended by TradingView. Results are then used conditionally when needed. This ensures consistent calculations and prevents calculation inconsistencies.

ChronoFlow## ChronoFlow Sentinel

ChronoFlow Sentinel is a regime console that blends normalized fast/mid/slow regression slopes, phases them against a dual-speed EMA spread, and grades alignment so you instantly know whether the time stack is trending, rotating, or fighting itself.

HOW IT WORKS

Multi-Timeframe Slopes – Linear regression slopes are fetched via request.security() for your chosen fast, mid, and slow frames.

Normalized Weighting – User weights are rescaled so the composite chrono score is always on a consistent scale, regardless of configuration.

Phase Differential – The indicator subtracts a slow EMA from a fast EMA to detect whether price impulse confirms the slope mix.

Alignment Score – Signs of the three slopes are compared to compute a 0-1 alignment metric; backgrounds and alerts use this to signal confidence vs. chop.

Diagnostics Console – A bottom-right table streams each slope, the blended score, and which timeframe currently dominates.

HOW TO USE IT

Trend Qualification : Only push multi-contract positions when chrono score is positive, phase is positive, and alignment stays above your alert threshold (default 0.66).

Chop Defense : When alignment dips and conflict markers appear, immediately switch into mean-reversion tactics or sit flat.

Swing + Intraday Bridge : Pair ChronoFlow with other structure tools; require both aligned backgrounds and price confirmation before committing to swing entries.

CRYPTOCAP:SOL | CRYPTOCAP:XRP side by side view with ChronoFlow

VISUAL FEATURES

Optional flow curves: Enable Plot Raw Flows to audit each timeframe's slope when troubleshooting a signal.

Background intensity: Opacity auto-adjusts with alignment, so weak trends look faded while strong regimes glow vividly.

Signal/Conflict toggles: Long/short and chop markers are opt-in, keeping the panel pristine until you need annotations.

Conflict alerts: Built-in alert condition fires whenever alignment falls below your threshold, warning execution layers to scale down risk.

PARAMETERS

Fast Frame (default: 30): Fast timeframe for regression slope calculation.

Mid Frame (default: 120): Mid timeframe for regression slope calculation.

Slow Frame (default: D): Slow timeframe for regression slope calculation.

Fast Regression (default: 21): Regression length for fast timeframe.

Mid Regression (default: 34): Regression length for mid timeframe.

Slow Regression (default: 55): Regression length for slow timeframe.

Phase Length (default: 13): EMA period for phase differential calculation.

Fast Weight (default: 0.45): Influence of the fast timeframe in the composite score.

Mid Weight (default: 0.35): Influence of the mid timeframe in the composite score.

Slow Weight (default: 0.20): Influence of the slow timeframe in the composite score.

Plot Raw Flows (default: disabled): Enable to audit each timeframe's slope when troubleshooting.

Show Signal Labels (default: disabled): Toggle long/short signal markers.

Show Conflict Labels (default: disabled): Toggle conflict/chop markers.

Conflict Alert Level (default: 0.66): Set the alignment threshold that should trigger reduced size or flat positioning.

ALERTS

The indicator includes three alert conditions:

ChronoFlow Bullish: Detected a bullish regime shift

ChronoFlow Bearish: Detected a bearish regime shift

ChronoFlow Conflict: Flagged a low-alignment regime

LIMITATIONS

This indicator requires access to multiple timeframes via request.security() , which may consume additional resources. The alignment score is a simplified metric—real market conditions are more complex than a 0-1 scale can capture. The phase differential calculation assumes EMA spreads are meaningful proxies for momentum, which may not hold in all market regimes. Users should test parameter combinations on their specific instruments and timeframes, as default values are optimized for typical index futures trading.

---

Static K-means Clustering | InvestorUnknownStatic K-Means Clustering is a machine-learning-driven market regime classifier designed for traders who want a data-driven structure instead of subjective indicators or manually drawn zones.

This script performs offline (static) K-means training on your chosen historical window. Using four engineered features:

RSI (Momentum)

CCI (Price deviation / Mean reversion)

CMF (Money flow / Strength)

MACD Histogram (Trend acceleration)

It groups past market conditions into K distinct clusters (regimes). After training, every new bar is assigned to the nearest cluster via Euclidean distance in 4-dimensional standardized feature space.

This allows you to create models like:

Regime-based long/short filters

Volatility phase detectors

Trend vs. chop separation

Mean-reversion vs. breakout classification

Volume-enhanced money-flow regime shifts

Full machine-learning trading systems based solely on regimes

Note:

This script is not a universal ML strategy out of the box.

The user must engineer the feature set to match their trading style and target market.

K-means is a tool, not a ready made system, this script provides the framework.

Core Idea

K-means clustering takes raw, unlabeled market observations and attempts to discover structure by grouping similar bars together.

// STEP 1 — DATA POINTS ON A COORDINATE PLANE

// We start with raw, unlabeled data scattered in 2D space (x/y).

// At this point, nothing is grouped—these are just observations.

// K-means will try to discover structure by grouping nearby points.

//

// y ↑

// |

// 12 | •

// | •

// 10 | •

// | •

// 8 | • •

// |

// 6 | •

// |

// 4 | •

// |

// 2 |______________________________________________→ x

// 2 4 6 8 10 12 14

//

//

//

// STEP 2 — RANDOMLY PLACE INITIAL CENTROIDS

// The algorithm begins by placing K centroids at random positions.

// These centroids act as the temporary “representatives” of clusters.

// Their starting positions heavily influence the first assignment step.

//

// y ↑

// |

// 12 | •

// | •

// 10 | • C2 ×

// | •

// 8 | • •

// |

// 6 | C1 × •

// |

// 4 | •

// |

// 2 |______________________________________________→ x

// 2 4 6 8 10 12 14

//

//

//

// STEP 3 — ASSIGN POINTS TO NEAREST CENTROID

// Each point is compared to all centroids.

// Using simple Euclidean distance, each point joins the cluster

// of the centroid it is closest to.

// This creates a temporary grouping of the data.

//

// (Coloring concept shown using labels)

//

// - Points closer to C1 → Cluster 1

// - Points closer to C2 → Cluster 2

//

// y ↑

// |

// 12 | 2

// | 1

// 10 | 1 C2 ×

// | 2

// 8 | 1 2

// |

// 6 | C1 × 2

// |

// 4 | 1

// |

// 2 |______________________________________________→ x

// 2 4 6 8 10 12 14

//

// (1 = assigned to Cluster 1, 2 = assigned to Cluster 2)

// At this stage, clusters are formed purely by distance.

Your chosen historical window becomes the static training dataset , and after fitting, the centroids never change again.

This makes the model:

Predictable

Repeatable

Consistent across backtests

Fast for live use (no recalculation of centroids every bar)

Static Training Window

You select a period with:

Training Start

Training End

Only bars inside this range are used to fit the K-means model. This window defines:

the market regime examples

the statistical distributions (means/std) for each feature

how the centroids will be positioned post-trainin

Bars before training = fully transparent

Training bars = gray

Post-training bars = full colored regimes

Feature Engineering (4D Input Vector)

Every bar during training becomes a 4-dimensional point:

This combination balances: momentum, volatility, mean-reversion, trend acceleration giving the algorithm a richer "market fingerprint" per bar.

Standardization

To prevent any feature from dominating due to scale differences (e.g., CMF near zero vs CCI ±200), all features are standardized:

standardize(value, mean, std) =>

(value - mean) / std

Centroid Initialization

Centroids start at diverse coordinates using various curves:

linear

sinusoidal

sign-preserving quadratic

tanh compression

init_centroids() =>

// Spread centroids across using different shapes per feature

for c = 0 to k_clusters - 1

frac = k_clusters == 1 ? 0.0 : c / (k_clusters - 1.0) // 0 → 1

v = frac * 2 - 1 // -1 → +1

array.set(cent_rsi, c, v) // linear

array.set(cent_cci, c, math.sin(v)) // sinusoidal

array.set(cent_cmf, c, v * v * (v < 0 ? -1 : 1)) // quadratic sign-preserving

array.set(cent_mac, c, tanh(v)) // compressed

This makes initial cluster spread “random” even though true randomness is hardly achieved in pinescript.

K-Means Iterative Refinement

The algorithm repeats these steps:

(A) Assignment Step, Each bar is assigned to the nearest centroid via Euclidean distance in 4D:

distance = sqrt(dx² + dy² + dz² + dw²)

(B) Update Step, Centroids update to the mean of points assigned to them. This repeats iterations times (configurable).

LIVE REGIME CLASSIFICATION

After training, each new bar is:

Standardized using the training mean/std

Compared to all centroids

Assigned to the nearest cluster

Bar color updates based on cluster

No re-training occurs. This ensures:

No lookahead bias

Clean historical testing

Stable regimes over time

CLUSTER BEHAVIOR & TRADING LOGIC

Clusters (0, 1, 2, 3…) hold no inherent meaning. The user defines what each cluster does.

Example of custom actions:

Cluster 0 → Cash

Cluster 1 → Long

Cluster 2 → Short

Cluster 3+ → Cash (noise regime)

This flexibility means:

One trader might have cluster 0 as consolidation.

Another might repurpose it as a breakout-loading zone.

A third might ignore 3 clusters entirely.

Example on ETHUSD

Important Note:

Any change of parameters or chart timeframe or ticker can cause the “order” of clusters to change

The script does NOT assume any cluster equals any actionable bias, user decides.

PERFORMANCE METRICS & ROC TABLE

The indicator computes average 1-bar ROC for each cluster in:

Training set

Test (live) set

This helps measure:

Cluster profitability consistency

Regime forward predictability

Whether a regime is noise, trend, or reversion-biased

EQUITY SIMULATION & FEES

Designed for close-to-close realistic backtesting.

Position = cluster of previous bar

Fees applied only on regime switches. Meaning:

Staying long → no fee

Switching long→short → fee applied

Switching any→cash → fee applied

Fee input is percentage, but script already converts internally.

Disclaimers

⚠️ This indicator uses machine-learning but does not predict the future. It classifies similarity to past regimes, nothing more.

⚠️ Backtest results are not indicative of future performance.

⚠️ Clusters have no inherent “bullish” or “bearish” meaning. You must interpret them based on your testing and your own feature engineering.

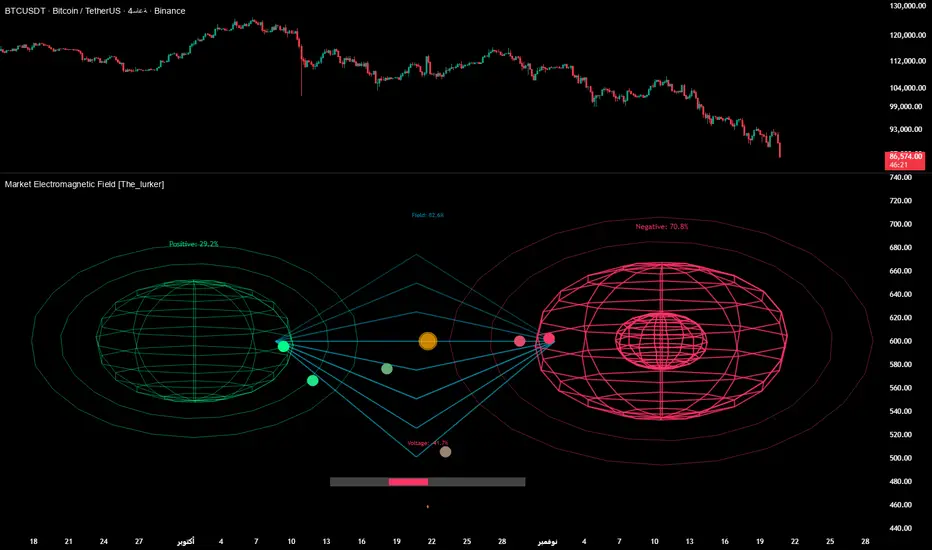

Market Electromagnetic Field [The_lurker]Market Electromagnetic Field

An innovative analytical indicator that presents a completely new model for understanding market dynamics, inspired by the laws of electromagnetic physics — but it's not a rhetorical metaphor, rather a complete mathematical system.

Unlike traditional indicators that focus on price or momentum, this indicator portrays the market as a closed physical system, where:

⚡ Candles = Electric charges (positive at bullish close, negative at bearish)

⚡ Buyers and Sellers = Two opposing poles where pressure accumulates

⚡ Market tension = Voltage difference between the poles

⚡ Price breakout = Electrical discharge after sufficient energy accumulation

█ Core Concept

Markets don't move randomly, but follow a clear physical cycle:

Accumulation → Tension → Discharge → Stabilization → New Accumulation

When charges accumulate (through strong candles with high volume) and exceed a certain "electrical capacitance" threshold, the indicator issues a "⚡ DISCHARGE IMMINENT" alert — meaning a price explosion is imminent, giving the trader an opportunity to enter before the move begins.

█ Competitive Advantage

- Predictive forecasting (not confirmatory after the event)

- Smart multi-layer filtering reduces false signals

- Animated 3D visual representation makes reading price conditions instant and intuitive — without need for number analysis

█ Theoretical Physical Foundation

The indicator doesn't use physical terms for decoration, but applies mathematical laws with precise market adjustments:

⚡ Coulomb's Law

Physics: F = k × (q₁ × q₂) / r²

Market: Field Intensity = 4 × norm_positive × norm_negative

Peaks at equilibrium (0.5 × 0.5 × 4 = 1.0), and decreases at dominance — because conflict increases at parity.

⚡ Ohm's Law

Physics: V = I × R

Market: Voltage = norm_positive − norm_negative

Measures balance of power:

- +1 = Absolute buying dominance

- −1 = Absolute selling dominance

- 0 = Balance

⚡ Capacitance

Physics: C = Q / V

Market: Capacitance = |Voltage| × Field Intensity

Represents stored energy ready for discharge — increases with bias combined with high interaction.

⚡ Electrical Discharge

Physics: Occurs when exceeding insulation threshold

Market: Discharge Probability = min(Capacitance / Discharge Threshold, 1.0)

When ≥ 0.9: "⚡ DISCHARGE IMMINENT"

📌 Key Note:

Maximum capacitance doesn't occur at absolute dominance (where field intensity = 0), nor at perfect balance (where voltage = 0), but at moderate bias (±30–50%) with high interaction (field intensity > 25%) — i.e., in moments of "pressure before breakout".

█ Detailed Calculation Mechanism

⚡ Phase 1: Candle Polarity

polarity = (close − open) / (high − low)

- +1.0: Complete bullish candle (Bullish Marubozu)

- −1.0: Complete bearish candle (Bearish Marubozu)

- 0.0: Doji (no decision)

- Intermediate values: Represent the ratio of candle body to its range — reducing the effect of long-shadow candles

⚡ Phase 2: Volume Weight

vol_weight = volume / SMA(volume, lookback)

A candle with 150% of average volume = 1.5x stronger charge

⚡ Phase 3: Adaptive Factor

adaptive_factor = ATR(lookback) / SMA(ATR, lookback × 2)

- In volatile markets: Increases sensitivity

- In quiet markets: Reduces noise

- Always recommended to keep it enabled

⚡ Phase 4–6: Charge Accumulation and Normalization

Charges are summed over lookback candles, then ratios are normalized:

norm_positive = positive_charge / total_charge

norm_negative = negative_charge / total_charge

So that: norm_positive + norm_negative = 1 — for easier comparison

⚡ Phase 7: Field Calculations

voltage = norm_positive − norm_negative

field_intensity = 4 × norm_positive × norm_negative × field_sensitivity

capacitance = |voltage| × field_intensity

discharge_prob = min(capacitance / discharge_threshold, 1.0)

█ Settings

⚡ Electromagnetic Model

Lookback Period

- Default: 20

- Range: 5–100

- Recommendations:

- Scalping: 10–15

- Day Trading: 20

- Swing: 30–50

- Investing: 50–100

Discharge Threshold

- Default: 0.7

- Range: 0.3–0.95

- Recommendations:

- Speed + Noise: 0.5–0.6

- Balance: 0.7

- High Accuracy: 0.8–0.95

Field Sensitivity

- Default: 1.0

- Range: 0.5–2.0

- Recommendations:

- Amplify Conflict: 1.2–1.5

- Natural: 1.0

- Calm: 0.5–0.8

Adaptive Mode

- Default: Enabled

- Always keep it enabled

🔬 Dynamic Filters

All enabled filters must pass for discharge signal to appear.

Volume Filter

- Condition: volume > SMA(volume) × vol_multiplier

- Function: Excludes "weak" candles not supported by volume

- Recommendation: Enabled (especially for stocks and forex)

Volatility Filter

- Condition: STDEV > SMA(STDEV) × 0.5

- Function: Ignores sideways stagnation periods

- Recommendation: Always enabled

Trend Filter

- Condition: Voltage alignment with fast/slow EMA

- Function: Reduces counter-trend signals

- Recommendation: Enabled for swing/investing only