Hurst Exponent - Detrended Fluctuation AnalysisIn stochastic processes, chaos theory and time series analysis, detrended fluctuation analysis (DFA) is a method for determining the statistical self-affinity of a signal. It is useful for analyzing time series that appear to be long-memory processes and noise.

█ OVERVIEW

We have introduced the concept of Hurst Exponent in our previous open indicator Hurst Exponent (Simple). It is an indicator that measures market state from autocorrelation. However, we apply a more advanced and accurate way to calculate Hurst Exponent rather than simple approximation. Therefore, we recommend using this version of Hurst Exponent over our previous publication going forward. The method we used here is called detrended fluctuation analysis. (For folks that are not interested in the math behind the calculation, feel free to skip to "features" and "how to use" section. However, it is recommended that you read it all to gain a better understanding of the mathematical reasoning).

█ Detrend Fluctuation Analysis

Detrended Fluctuation Analysis was first introduced by by Peng, C.K. (Original Paper) in order to measure the long-range power-law correlations in DNA sequences . DFA measures the scaling-behavior of the second moment-fluctuations, the scaling exponent is a generalization of Hurst exponent.

The traditional way of measuring Hurst exponent is the rescaled range method. However DFA provides the following benefits over the traditional rescaled range method (RS) method:

• Can be applied to non-stationary time series. While asset returns are generally stationary, DFA can measure Hurst more accurately in the instances where they are non-stationary.

• According the the asymptotic distribution value of DFA and RS, the latter usually overestimates Hurst exponent (even after Anis- Llyod correction) resulting in the expected value of RS Hurst being close to 0.54, instead of the 0.5 that it should be. Therefore it's harder to determine the autocorrelation based on the expected value. The expected value is significantly closer to 0.5 making that threshold much more useful, using the DFA method on the Hurst Exponent (HE).

• Lastly, DFA requires lower sample size relative to the RS method. While the RS method generally requires thousands of observations to reduce the variance of HE, DFA only needs a sample size greater than a hundred to accomplish the above mentioned.

█ Calculation

DFA is a modified root-mean-squares (RMS) analysis of a random walk. In short, DFA computes the RMS error of linear fits over progressively larger bins (non-overlapped “boxes” of similar size) of an integrated time series.

Our signal time series is the log returns. First we subtract the mean from the log return to calculate the demeaned returns. Then, we calculate the cumulative sum of demeaned returns resulting in the cumulative sum being mean centered and we can use the DFA method on this. The subtraction of the mean eliminates the “global trend” of the signal. The advantage of applying scaling analysis to the signal profile instead of the signal, allows the original signal to be non-stationary when needed. (For example, this process converts an i.i.d. white noise process into a random walk.)

We slice the cumulative sum into windows of equal space and run linear regression on each window to measure the linear trend. After we conduct each linear regression. We detrend the series by deducting the linear regression line from the cumulative sum in each windows. The fluctuation is the difference between cumulative sum and regression.

We use different windows sizes on the same cumulative sum series. The window sizes scales are log spaced. Eg: powers of 2, 2,4,8,16... This is where the scale free measurements come in, how we measure the fractal nature and self similarity of the time series, as well as how the well smaller scale represent the larger scale.

As the window size decreases, we uses more regression lines to measure the trend. Therefore, the fitness of regression should be better with smaller fluctuation. It allows one to zoom into the “picture” to see the details. The linear regression is like rulers. If you use more rulers to measure the smaller scale details you will get a more precise measurement.

The exponent we are measuring here is to determine the relationship between the window size and fitness of regression (the rate of change). The more complex the time series are the more it will depend on decreasing window sizes (using more linear regression lines to measure). The less complex or the more trend in the time series, it will depend less. The fitness is calculated by the average of root mean square errors (RMS) of regression from each window.

Root mean Square error is calculated by square root of the sum of the difference between cumulative sum and regression. The following chart displays average RMS of different window sizes. As the chart shows, values for smaller window sizes shows more details due to higher complexity of measurements.

The last step is to measure the exponent. In order to measure the power law exponent. We measure the slope on the log-log plot chart. The x axis is the log of the size of windows, the y axis is the log of the average RMS. We run a linear regression through the plotted points. The slope of regression is the exponent. It's easy to see the relationship between RMS and window size on the chart. Larger RMS equals less fitness of the regression. We know the RMS will increase (fitness will decrease) as we increases window size (use less regressions to measure), we focus on the rate of RMS increasing (how fast) as window size increases.

If the slope is < 0.5, It means the rate of of increase in RMS is small when window size increases. Therefore the fit is much better when it's measured by a large number of linear regression lines. So the series is more complex. (Mean reversion, negative autocorrelation).

If the slope is > 0.5, It means the rate of increase in RMS is larger when window sizes increases. Therefore even when window size is large, the larger trend can be measured well by a small number of regression lines. Therefore the series has a trend with positive autocorrelation.

If the slope = 0.5, It means the series follows a random walk.

█ FEATURES

• Sample Size is the lookback period for calculation. Even though DFA requires a lower sample size than RS, a sample size larger > 50 is recommended for accurate measurement.

• When a larger sample size is used (for example = 1000 lookback length), the loading speed may be slower due to a longer calculation. Date Range is used to limit numbers of historical calculation bars. When loading speed is too slow, change the data range "all" into numbers of weeks/days/hours to reduce loading time. (Credit to allanster)

• “show filter” option applies a smoothing moving average to smooth the exponent.

• Log scale is my work around for dynamic log space scaling. Traditionally the smallest log space for bars is power of 2. It requires at least 10 points for an accurate regression, resulting in the minimum lookback to be 1024. I made some changes to round the fractional log space into integer bars requiring the said log space to be less than 2.

• For a more accurate calculation a larger "Base Scale" and "Max Scale" should be selected. However, when the sample size is small, a larger value would cause issues. Therefore, a general rule to be followed is: A larger "Base Scale" and "Max Scale" should be selected for a larger the sample size. It is recommended for the user to try and choose a larger scale if increasing the value doesn't cause issues.

The following chart shows the change in value using various scales. As shown, sometimes increasing the value makes the value itself messy and overshoot.

When using the lowest scale (4,2), the value seems stable. When we increase the scale to (8,2), the value is still alright. However, when we increase it to (8,4), it begins to look messy. And when we increase it to (16,4), it starts overshooting. Therefore, (8,2) seems to be optimal for our use.

█ How to Use

Similar to Hurst Exponent (Simple). 0.5 is a level for determine long term memory.

• In the efficient market hypothesis, market follows a random walk and Hurst exponent should be 0.5. When Hurst Exponent is significantly different from 0.5, the market is inefficient.

• When Hurst Exponent is > 0.5. Positive Autocorrelation. Market is Trending. Positive returns tend to be followed by positive returns and vice versa.

• Hurst Exponent is < 0.5. Negative Autocorrelation. Market is Mean reverting. Positive returns trends to follow by negative return and vice versa.

However, we can't really tell if the Hurst exponent value is generated by random chance by only looking at the 0.5 level. Even if we measure a pure random walk, the Hurst Exponent will never be exactly 0.5, it will be close like 0.506 but not equal to 0.5. That's why we need a level to tell us if Hurst Exponent is significant.

So we also computed the 95% confidence interval according to Monte Carlo simulation. The confidence level adjusts itself by sample size. When Hurst Exponent is above the top or below the bottom confidence level, the value of Hurst exponent has statistical significance. The efficient market hypothesis is rejected and market has significant inefficiency.

The state of market is painted in different color as the following chart shows. The users can also tell the state from the table displayed on the right.

An important point is that Hurst Value only represents the market state according to the past value measurement. Which means it only tells you the market state now and in the past. If Hurst Exponent on sample size 100 shows significant trend, it means according to the past 100 bars, the market is trending significantly. It doesn't mean the market will continue to trend. It's not forecasting market state in the future.

However, this is also another way to use it. The market is not always random and it is not always inefficient, the state switches around from time to time. But there's one pattern, when the market stays inefficient for too long, the market participants see this and will try to take advantage of it. Therefore, the inefficiency will be traded away. That's why Hurst exponent won't stay in significant trend or mean reversion too long. When it's significant the market participants see that as well and the market adjusts itself back to normal.

The Hurst Exponent can be used as a mean reverting oscillator itself. In a liquid market, the value tends to return back inside the confidence interval after significant moves(In smaller markets, it could stay inefficient for a long time). So when Hurst Exponent shows significant values, the market has just entered significant trend or mean reversion state. However, when it stays outside of confidence interval for too long, it would suggest the market might be closer to the end of trend or mean reversion instead.

Larger sample size makes the Hurst Exponent Statistics more reliable. Therefore, if the user want to know if long term memory exist in general on the selected ticker, they can use a large sample size and maximize the log scale. Eg: 1024 sample size, scale (16,4).

Following Chart is Bitcoin on Daily timeframe with 1024 lookback. It suggests the market for bitcoin tends to have long term memory in general. It generally has significant trend and is more inefficient at it's early stage.

在腳本中搜尋"hurst"

Hurst Exponent Trend filterHello Traders !!

Hurst Exponent Trend filter utalises the Hurst Exponent and VAWMA (one of my other unique indicators - check my script publishings to use) to categorise the market and decide whether its Trending, H > 0.5, In random Geometric Brownian Motion (GBM) H = 0.5 or Mean reverting (Contrarian), H < 0.5, When Trending a Trend following indicator -The VAWMA- is color highlighted, By doing so, theoreticaly price noise is eleimnated leaving statsitcaly true zones of price action Trend.

What is The Hurst Exponent ?

Developed by The Hydrologist Edwin Harlod Hurst, The Hurst Exponent measures auto correlation in time series sets, Its first applicartions were in the natural world, e.g. in measureing the volume of water in a river.

Although since then it has had applications in Finance, this may be largly due to autocorrelation functions being usefull tools in univaritae time series anaylyis.

The Hurst Exponent (H) aims to segment the market into three differnet states, Trending (H > 0.5), Random Geometric Brownian Motion (H = 0.5) and Mean Reverting / Contrarian (H < 0.5). In my interpritation this can be used as a trend filter that iliminates market noise, which may be achived by only focusing on trending zones.

How to Interprit the Indicator :

Focusing on the Above image, When H > 0.5 A trend is presnet, to decide the directional bias, both VAWMA`s position is checked, given the fast VAWMA > slow VAWMA and the current close > the fast VAWMA a bulish bias is present, signafied by a vibrant green fill between the fast VAWMA and price action. note the exact opposite logic for a bearish bias and H > 0.5 (signafied by a vibrant red fill). .

I will continue to update this Trading Indicator.

PS : Thats given I can hopfully remmember

Happy Trading !!

Hurst Momentum Oscillator | AlphaNattHurst Momentum Oscillator | AlphaNatt

An adaptive oscillator that combines the Hurst Exponent - which identifies whether markets are trending or mean-reverting - with momentum analysis to create signals that automatically adjust to market regime.

"The Hurst Exponent reveals a hidden truth: markets aren't always trending. This oscillator knows when to ride momentum and when to fade it."

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📐 THE MATHEMATICS

Hurst Exponent (H):

Measures the long-term memory of time series:

H > 0.5: Trending (persistent) behavior

H = 0.5: Random walk

H < 0.5: Mean-reverting behavior

Originally developed for analyzing Nile river flooding patterns, now used in:

Fractal market analysis

Network traffic prediction

Climate modeling

Financial markets

The Innovation:

This oscillator multiplies momentum by the Hurst coefficient:

When trending (H > 0.5): Momentum is amplified

When mean-reverting (H < 0.5): Momentum is reduced

Result: Adaptive signals based on market regime

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

💎 KEY ADVANTAGES

Regime Adaptive: Automatically adjusts to trending vs ranging markets

False Signal Reduction: Reduces momentum signals in mean-reverting markets

Trend Amplification: Stronger signals when trends are persistent

Mathematical Edge: Based on fractal dimension analysis

No Repainting: All calculations on historical data

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

📊 TRADING SIGNALS

Visual Interpretation:

Cyan zones: Bullish momentum in trending market

Magenta zones: Bearish momentum or mean reversion

Background tint: Blue = trending, Pink = mean-reverting

Gradient intensity: Signal strength

Trading Strategies:

1. Trend Following:

Trade momentum signals when background is blue (trending)

2. Mean Reversion:

Fade extreme readings when background is pink

3. Regime Transition:

Watch for background color changes as early warning

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

🎯 OPTIMAL USAGE

Best Conditions:

Strong trending markets (crypto bull runs)

Clear ranging markets (forex sessions)

Regime transitions

Multi-timeframe analysis

Market Applications:

Crypto: Excellent for identifying trend persistence

Forex: Detects when pairs are ranging

Stocks: Identifies momentum stocks

Commodities: Catches persistent trends

━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━━

Developed by AlphaNatt | Fractal Market Analysis

Version: 1.0

Classification: Adaptive Regime Oscillator

Not financial advice. Always DYOR.

Hurst Exponent SmoothedDescription:

The Hurst Exponent Smoothed indicator provides a dynamic analysis of market behavior by calculating the Hurst Exponent over a specified lookback period. This tool is especially useful for identifying whether a market is trending or mean-reverting.

Key Features:

Lookback Period: Set to 90 by default, this parameter controls how many periods the indicator considers for its calculations. Adjusting this value allows you to fine-tune the sensitivity of the indicator to recent price action.

Market Analysis: The Hurst Exponent gives insights into the nature of price movement:

A value near 0.5 suggests a random walk, indicating that the market is unpredictable.

Values above 0.5 indicate a trending market where price movements exhibit persistence, suggesting that the current trend may continue.

Values below 0.5 point to a mean-reverting market, where price movements tend to reverse, making it a potential signal for contrarian trading strategies.

Usage:

Trend Following: When the Hurst Exponent is consistently above 0.5, it may indicate a strong trend. Traders can use this information to align with the current market direction.

Mean Reversion: If the Hurst Exponent falls below 0.5, it could signal that the market is more likely to revert to the mean, offering opportunities for mean-reversion strategies.

Visuals:

The indicator displays a smooth line oscillating between values, giving traders a clear visual cue for the current market condition.

The script is optimized for various timeframes, as demonstrated on the BTCUSD pair on a 270-minute chart. Traders can adapt the lookback period based on their trading style and the specific asset being analyzed.

Open Source: This script is open-source and free to use. Feel free to customize and adapt it to your needs!

Hurst Dual-Channel + ECDF Early Reentry (Single Trigger)Hello,

This indicator can be useful during ranging market phases, especially on short timeframes such as 5 minutes, within a statistically contrarian approach.

It combines two quantitative methodologies:

– Hurst-type adaptive channels, which measure short- and medium-term price deviations using the ATR (Average True Range);

– an Empirical Cumulative Distribution Function (ECDF), which locates the current price between its recent extremes (0 corresponding to the lower bound, 1 to the upper bound).

The goal is to identify relative overbought and oversold zones, where the price exceeds the channels and then begins to revert toward its statistical mean.

The indicator does not issue trading recommendations: it merely highlights specific statistical conditions for research and analytical purposes.

The “BUY” and “SELL” labels indicate such technical configurations:

– ECDF < 0.2 with price returning above the lower channels → bullish reentry.

– ECDF > 0.9 with price returning below the upper channels → bearish reentry.

The parameters (channel periods, ECDF window, smoothing) allow you to fine-tune the sensitivity of the analysis according to instrument volatility or chosen timeframe.

🟩 Buy Signal (BUY)

A buy signal is triggered when a strong downside deviation pushes the price below both channels, followed by a gradual reentry inside the bands.

More precisely:

– The low is below both channels (low < scb and low < mcb).

– The ECDF crosses back above 0.19 (exit from oversold).

– Both events occur within the last six bars.

– The price moves back above the lower channel (high > scb).

– No previous long signal is active.

This configuration represents a statistical reentry to the mean after an excessive drop.

🟥 Sell Signal (SELL)

Conversely, a sell signal appears when a strong upside deviation pushes the price above both channels, followed by a pullback below them:

– The high exceeds both channels (high > sct and high > mct).

– The ECDF crosses below 0.9 (exit from overbought).

– Both events occur within the last six bars.

– The price falls back below the upper channel (low < sct).

– No previous short signal is active.

This reflects a bearish reentry following a statistical overextension.

⚙️ Operating Logic

Each signal is triggered only once per cycle thanks to the variables triggered_long and triggered_short, preventing duplicates until a new extreme occurs.

The tool is designed for visual analysis and pattern research, not for automated execution.

🔍 ECDF Principle and Calculation

The ECDF is a non-parametric measure of a value’s position within its recent distribution:

ECDF(X)=number of values ≤XNECDF(X) = \frac{\text{number of values } \le X}{N}ECDF(X)=Nnumber of values ≤X

It expresses the empirical proportion of observations below the current value.

Example:

If, among the last 100 observations, 85 are below the current price, then

ECDF=0.85ECDF = 0.85ECDF=0.85

→ The price is at the 85th percentile, statistically high relative to recent history.

Strengths: robust, model-free, well-suited to asymmetric or non-normal market regimes.

Limitations: it does not measure amplitude and depends on the selected window size.

🌊 Intuitive Analogy: The River and the Gauge

Imagine a river with a depth gauge:

– The Z-Score tells you how many meters above the average level the water currently stands.

– The ECDF tells you in how many past cases the water level was lower than it is now.

The Z-Score assumes the river always follows the same symmetrical pattern.

The ECDF simply observes reality — adapting naturally, even when the current becomes unpredictable.

Final note:

This indicator is designed for visual and statistical exploration of price behavior.

The signals represent statistical states, not trade instructions.

Entering long or short positions based on them is entirely at your own discretion and risk.

HURST Channel StrategyBased on the work TJS / Trading Zoom / Svoboda

Strategy based on Hurst channel with loss averaging when an open position is below 0.5 channel range.

How it works:

1. opens the long position when the close price crosses over the lower band (from bottom to top)

2. opens additional position (double in size) when average position price is lower than average channel value (0.5)

3. closes the position when the close price crosses over the higher band (from top to bottom)

Works the best on :

- volatile and continuous instruments (futures)

- on timeframes above 15 minutes

- uptrends or consolidations

- downtrends require more capital to open double positions

Prometheus Analytics Hurst ExponentThis indicator uses market data to calculate the Hurst Exponent so traders can have knowledge of the long memory of the asset.

Users can control the lookback length for the H value (Hurst Exponent), lookback length for the SMA (Simple Moving Average) of the Hurst Exponent, to show either, and what to calculate the H value and SMA on.

Hurst Exponent:

The Hurst Exponent is a value between 0 and 1 with 0.5 as a midline.

An H value(Hurst Exponent) above 0.5 indicates a trending market, and a market that should have larger, longer moves.

An H value below 0.5 indicates a mean reverting market, and a market that should have smaller, shorter moves.

An H value of0.5 indicates a random walk. This would mean the price would follow a Brownian Motion model and future prices would be independent from past prices.

Just because the H value is above 0.5 does not indicate that there should be an UP trend, just as a value below 0.5 does not indicate a DOWN trend. It indicates that there should be a trend, up or down.

Scenarios:

An intuitive way to use the Hurst Exponent is as an asset is trending in whatever direction, as the H value crosses below 0.5 it indicates a reversal. It indicates that what was happening before isn’t impacting what is happening now as much.

Steps explained from picture:

Step 1: Strong uptrend is identified with the asset moving up aggressively with H above 0.5.

Step 2: The H value crosses below 0.5 and prices stay elevated.

Step 3: Price reverts back down as the H value stays below 0.5

Just because the H value is above 0.5 doesn’t mean the asset has to be uptrending. In this example we see the asset fall as the H value is above 0.5. Not only that, but every time it crosses below 0.5, the asset takes a breather on the way down

Step 1: As the H value crosses above 0.5, we can expect trends to appear in the asset.

Step 2: After the trend switches to down, we only see a breather and some chop after the H value crosses back below 0.5.

Step 3: Once The H value crosses back over we see the downtrend continue and new lows be made.

Step 4: We see it once again, simply the area of chop is bigger. We don’t see a higher high, breaking the overall downtrend, but once the H value crosses over again the downturn continues and we see a lower low.

It may occur when no strong trend is made in either direction. The H value above 0.5 does indeed sometimes correlate with an uptrend sometimes.

Step 1: After the strong downtrend we see a break below 0.5 with some consolidation.

Step 2: No clear big move on the asset or H value.

Step 3: H value above 0.5 leads to a break of highs and a new uptrend.

Users have the option to decide what to calculate the H value on. Close is the default, or dollar return per bar are the options. Dollar return per bar and offer an H value that may give a better indication of when price moves will be small and sporadic.

Using dollar move per bar.

Step 1: H value cross above 0.5, we see large candles and fast moves.

Step 2: H value crosses below 0.5, the candles immediately following are shorter. The big red candles come right before the cross back above.

Step 3: H value cross back above 0.5, after some chop, large move down.

Similar story

Step 1: H value above 0.5, big trends either direction

Step 2: After the H value crosses below, the moves are short and choppy.

Settings:

Options to show or remove either the H value or it’s SMA.

Options to adjust the period uses, default is (32, 16)

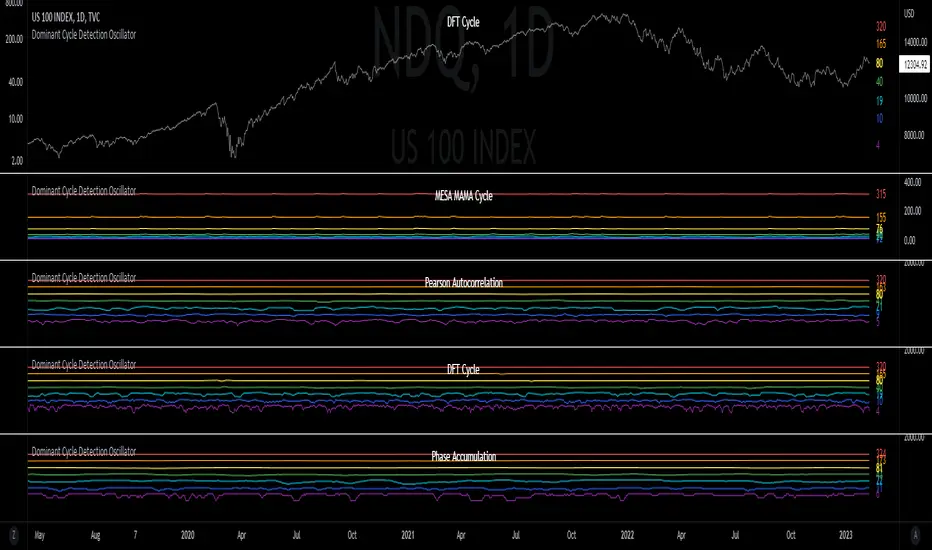

Dominant Cycle Detection OscillatorThis is a Dominant Cycle Detection Oscillator that searches multiple ranges of wavelengths within a spectrum. Choose one of 4 different dominant cycle detection methods (MESA MAMA cycle, Pearson Autocorrelation, Discreet Fourier Transform, and Phase Accumulation) to determine the most dominant cycles and see the historical results. Straight lines can indicate a steady dominant cycle; while Wavy lines might indicate a varying dominant cycle length. The steadier the cycle, the easier it may be to predict future events in that cycle (keep the log scale in mind when considering steadiness). The presence of evenly divisible (or harmonic) cycle lengths may also indicate stronger cycles; for example, 19, 38, and 76 dominant lengths for the 2x, 4x, and 8x cycles. Practically, a trader can use these cycle outputs as the default settings for other Hurst/cycle indicators. For example, if you see dominant cycle oscillator outputs of 38 & 76 for the 4x and 8x cycle respectively, you might want to test/use defaults of 38 & 76 for the 4x & 8x lengths in the bandpass, diamond/semi-circle notation, moving average & envelope, and FLD instead of the defaults 40 & 80 for a more fine-tuned analysis.

Muting the oscillator's historical lines and overlaying the indicator on the chart can visually cue a trader to the cycle lengths without taking up extra panes. The DFT Cycle lengths with muted historical lines have been overlayed on the chart in the photo.

The y-axis scale for this indicator's pane (just the oscillator pane, not the chart) most likely needs to be changed to logarithmic to look normal, but it depends on the search ranges in your settings. There are instructions in the settings. In the photo, the MESA MAMA scale is set to regular (not logarithmic) which demonstrates how difficult it can be to read if not changed.

In the Spectral Analysis chapter of Hurst's book Profit Magic, he recommended doing a Fourier analysis across a spectrum of frequencies. Hurst acknowledged there were many ways to do this analysis but recommended the method described by Lanczos. Currently in this indicator, the closest thing to the method described by Lanczos is the DFT Discreet Fourier Transform method.

Shoutout to @lastguru for the dominant cycle library referenced in this code. He mentioned that he may add more methods in the future.

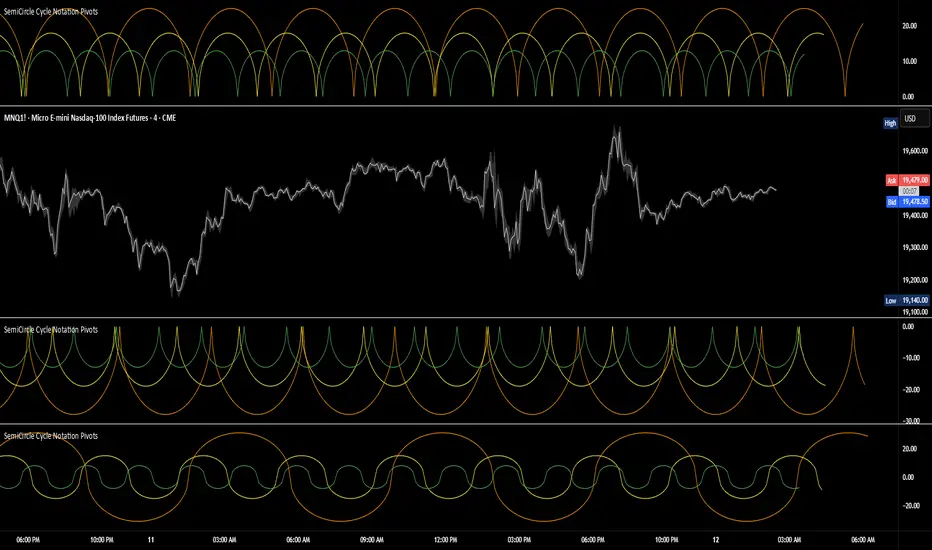

SemiCircle Cycle Notation PivotsFor decades, traders have sought to decode the rhythm of the markets through cycle theory. From the groundbreaking work of HM Gartley in the 1930s to modern-day cycle trading tools on TradingView, the concept remains the same: markets move in repeating waves with larger cycles influencing smaller ones in a fractal-like structure, and understanding their timing gives traders an edge to better anticipate future price movements🔮.

Traditional cycle analysis has always been manual, requiring traders to painstakingly plot semicircles, diamonds, or sine waves to estimate pivot points and time reversals. Drawing tools like semicircle & sine wave projections exist on TradingView, but they lack automation—forcing traders to adjust cycle lengths by eye, often leading to inconsistencies.

This is where SemiCircle Cycle Notation Pivots indicator comes in. Semicircle cycle chart notation appears to have evolved as a practical visualization tool among cycle theorists rather than being pioneered by a single individual; some key influences include HM Gartley, WD Gann, JM Hurst, Walter Bressert, and RayTomes. Built upon LonesomeTheBlue's foundational ZigZag Waves indicator , this indicator takes cycle visualization to the next level by dynamically detecting price pivots and then automatically plotting semicircles based on real-time cycle length calculations & expected rhythm of price action over time.

Key Features:

Automated Cycle Detection: The indicator identifies pivot points based on your preference—highs, lows, or both—and plots semicircle waves that correspond to Hurst's cycle notation.

Customizable Cycle Lengths: Tailor the analysis to your trading strategy with adjustable cycle lengths, defaulting to 10, 20, and 40 bars, allowing for flexibility across various timeframes and assets.

Dynamic Wave Scaling: The semicircle waves adapt to different price structures, ensuring that the visualization remains proportional to the detected cycle lengths and aiding in the identification of potential reversal points.

Automated Cycle Detection: Dynamically identifies price pivot points and automatically adjusts offsets based on real-time cycle length calculations, ensuring precise semicircle wave alignment with market structure.

Color-Coded Cycle Tiers: Each cycle tier is distinctly color-coded, enabling quick differentiation and a clearer understanding of nested market cycles.

Local Hurst Slope [Dynamic Regime]1. HOW THE INDICATOR WORKS (Math → Market Edge)Step

Math

Market Intuition

1. Log-Returns

r_t = log(P_t / P_{t-1})

Removes scale, makes series stationary

2. R/S per τ

R = max(cum_dev) - min(cum_dev)

S = stdev(segment)

Measures memory strength over window τ

3. H(τ) = log(R/S) / log(τ)

Di Matteo (2007)

H > 0.5 → Trend memory

H < 0.5 → Mean-reversion

4. Slope = dH/d(log τ)

Linear regression of H vs log(τ)

Slope > 0.12 → Trend accelerating

Slope < -0.08 → Reversion emerging

LEADING EDGE: The slope changes 3–20 bars BEFORE price confirms

→ You enter before the crowd, exit before the trap

Slope > +0.12 + Strong Trend = Bullish = Long

Slope +0.05 to +0.12 = Weak Trend = Cautious = Hold/Trail

Slope -0.05 to +0.05 = Random = No Edge

Slope-0.08 to -0.05 = Weak Reversion = Bearish setup = Prepare Short

Slope < -0.08 = Strong Reversion = Bearish= Short

PRO TIPS

Only trade in direction of 200-day SMA

Filters false signals

Avoid trading 3 days before/after earnings

Volatility kills edge

Use on ETFs (SPY, QQQ)

Cleaner than single stocks

Combine with RSI(14)

RSI < 30 + Hurst short = nuclear reversal

Stealthy Hurst ExponentThis is my attempt at Hurst Exponent indicator.

Above 0.5 is supposed to indicate a trend is present.

Below 0.5 is noise.

0.5 is supposed to be Brownian Motion or regular market noise.

If you have corrections to the code you want to share, please post it.

I'm not an expert in math or coding, so this shouldn't be copied / ported.

This code didn't work very well as a filter, but you may have a fix or other use.

Bridge Bands ATR (Overlay) ShaneHurst-Adaptive Volatility Bands

A fractal-inspired evolution of Bollinger and Keltner bands that adapts dynamically to both volatility and trend persistence.

This indicator estimates the Hurst exponent (H) — a measure of market memory — and adjusts a standard volatility band to lean in the direction of the prevailing trend.

When H > 0.5, markets exhibit persistence (trending behavior); the bands shift in the trend’s direction.

When H < 0.5, markets are mean-reverting; the bands flatten and recent extremes become potential fade zones.

Band width scales with recent volatility (σ), expanding in turbulent conditions and contracting during calm periods.

Key Features:

Adaptive offset using the Hurst exponent

Volatility-sensitive width for dynamic market regimes

EMA baseline with directional bias

Clear visual separation between trending and choppy phases

Inspired by Benoit Mandelbrot’s The Misbehavior of Markets and H.E. Hurst’s original work on long-term memory in time series.

Use it to identify regime shifts, trend-following entries, and volatility-adjusted stop levels.

Credit for this script goes to a number of people including Steve B, MichaalAngle, doc and joecat808. 500 day DEMA (double EMA) can be used as a longer term momentum line.

Tensor Market Analysis Engine (TMAE)# Tensor Market Analysis Engine (TMAE)

## Advanced Multi-Dimensional Mathematical Analysis System

*Where Quantum Mathematics Meets Market Structure*

---

## 🎓 THEORETICAL FOUNDATION

The Tensor Market Analysis Engine represents a revolutionary synthesis of three cutting-edge mathematical frameworks that have never before been combined for comprehensive market analysis. This indicator transcends traditional technical analysis by implementing advanced mathematical concepts from quantum mechanics, information theory, and fractal geometry.

### 🌊 Multi-Dimensional Volatility with Jump Detection

**Hawkes Process Implementation:**

The TMAE employs a sophisticated Hawkes process approximation for detecting self-exciting market jumps. Unlike traditional volatility measures that treat price movements as independent events, the Hawkes process recognizes that market shocks cluster and exhibit memory effects.

**Mathematical Foundation:**

```

Intensity λ(t) = μ + Σ α(t - Tᵢ)

```

Where market jumps at times Tᵢ increase the probability of future jumps through the decay function α, controlled by the Hawkes Decay parameter (0.5-0.99).

**Mahalanobis Distance Calculation:**

The engine calculates volatility jumps using multi-dimensional Mahalanobis distance across up to 5 volatility dimensions:

- **Dimension 1:** Price volatility (standard deviation of returns)

- **Dimension 2:** Volume volatility (normalized volume fluctuations)

- **Dimension 3:** Range volatility (high-low spread variations)

- **Dimension 4:** Correlation volatility (price-volume relationship changes)

- **Dimension 5:** Microstructure volatility (intrabar positioning analysis)

This creates a volatility state vector that captures market behavior impossible to detect with traditional single-dimensional approaches.

### 📐 Hurst Exponent Regime Detection

**Fractal Market Hypothesis Integration:**

The TMAE implements advanced Rescaled Range (R/S) analysis to calculate the Hurst exponent in real-time, providing dynamic regime classification:

- **H > 0.6:** Trending (persistent) markets - momentum strategies optimal

- **H < 0.4:** Mean-reverting (anti-persistent) markets - contrarian strategies optimal

- **H ≈ 0.5:** Random walk markets - breakout strategies preferred

**Adaptive R/S Analysis:**

Unlike static implementations, the TMAE uses adaptive windowing that adjusts to market conditions:

```

H = log(R/S) / log(n)

```

Where R is the range of cumulative deviations and S is the standard deviation over period n.

**Dynamic Regime Classification:**

The system employs hysteresis to prevent regime flipping, requiring sustained Hurst values before regime changes are confirmed. This prevents false signals during transitional periods.

### 🔄 Transfer Entropy Analysis

**Information Flow Quantification:**

Transfer entropy measures the directional flow of information between price and volume, revealing lead-lag relationships that indicate future price movements:

```

TE(X→Y) = Σ p(yₜ₊₁, yₜ, xₜ) log

```

**Causality Detection:**

- **Volume → Price:** Indicates accumulation/distribution phases

- **Price → Volume:** Suggests retail participation or momentum chasing

- **Balanced Flow:** Market equilibrium or transition periods

The system analyzes multiple lag periods (2-20 bars) to capture both immediate and structural information flows.

---

## 🔧 COMPREHENSIVE INPUT SYSTEM

### Core Parameters Group

**Primary Analysis Window (10-100, Default: 50)**

The fundamental lookback period affecting all calculations. Optimization by timeframe:

- **1-5 minute charts:** 20-30 (rapid adaptation to micro-movements)

- **15 minute-1 hour:** 30-50 (balanced responsiveness and stability)

- **4 hour-daily:** 50-100 (smooth signals, reduced noise)

- **Asset-specific:** Cryptocurrency 20-35, Stocks 35-50, Forex 40-60

**Signal Sensitivity (0.1-2.0, Default: 0.7)**

Master control affecting all threshold calculations:

- **Conservative (0.3-0.6):** High-quality signals only, fewer false positives

- **Balanced (0.7-1.0):** Optimal risk-reward ratio for most trading styles

- **Aggressive (1.1-2.0):** Maximum signal frequency, requires careful filtering

**Signal Generation Mode:**

- **Aggressive:** Any component signals (highest frequency)

- **Confluence:** 2+ components agree (balanced approach)

- **Conservative:** All 3 components align (highest quality)

### Volatility Jump Detection Group

**Volatility Dimensions (2-5, Default: 3)**

Determines the mathematical space complexity:

- **2D:** Price + Volume volatility (suitable for clean markets)

- **3D:** + Range volatility (optimal for most conditions)

- **4D:** + Correlation volatility (advanced multi-asset analysis)

- **5D:** + Microstructure volatility (maximum sensitivity)

**Jump Detection Threshold (1.5-4.0σ, Default: 3.0σ)**

Standard deviations required for volatility jump classification:

- **Cryptocurrency:** 2.0-2.5σ (naturally volatile)

- **Stock Indices:** 2.5-3.0σ (moderate volatility)

- **Forex Major Pairs:** 3.0-3.5σ (typically stable)

- **Commodities:** 2.0-3.0σ (varies by commodity)

**Jump Clustering Decay (0.5-0.99, Default: 0.85)**

Hawkes process memory parameter:

- **0.5-0.7:** Fast decay (jumps treated as independent)

- **0.8-0.9:** Moderate clustering (realistic market behavior)

- **0.95-0.99:** Strong clustering (crisis/event-driven markets)

### Hurst Exponent Analysis Group

**Calculation Method Options:**

- **Classic R/S:** Original Rescaled Range (fast, simple)

- **Adaptive R/S:** Dynamic windowing (recommended for trading)

- **DFA:** Detrended Fluctuation Analysis (best for noisy data)

**Trending Threshold (0.55-0.8, Default: 0.60)**

Hurst value defining persistent market behavior:

- **0.55-0.60:** Weak trend persistence

- **0.65-0.70:** Clear trending behavior

- **0.75-0.80:** Strong momentum regimes

**Mean Reversion Threshold (0.2-0.45, Default: 0.40)**

Hurst value defining anti-persistent behavior:

- **0.35-0.45:** Weak mean reversion

- **0.25-0.35:** Clear ranging behavior

- **0.15-0.25:** Strong reversion tendency

### Transfer Entropy Parameters Group

**Information Flow Analysis:**

- **Price-Volume:** Classic flow analysis for accumulation/distribution

- **Price-Volatility:** Risk flow analysis for sentiment shifts

- **Multi-Timeframe:** Cross-timeframe causality detection

**Maximum Lag (2-20, Default: 5)**

Causality detection window:

- **2-5 bars:** Immediate causality (scalping)

- **5-10 bars:** Short-term flow (day trading)

- **10-20 bars:** Structural flow (swing trading)

**Significance Threshold (0.05-0.3, Default: 0.15)**

Minimum entropy for signal generation:

- **0.05-0.10:** Detect subtle information flows

- **0.10-0.20:** Clear causality only

- **0.20-0.30:** Very strong flows only

---

## 🎨 ADVANCED VISUAL SYSTEM

### Tensor Volatility Field Visualization

**Five-Layer Resonance Bands:**

The tensor field creates dynamic support/resistance zones that expand and contract based on mathematical field strength:

- **Core Layer (Purple):** Primary tensor field with highest intensity

- **Layer 2 (Neutral):** Secondary mathematical resonance

- **Layer 3 (Info Blue):** Tertiary harmonic frequencies

- **Layer 4 (Warning Gold):** Outer field boundaries

- **Layer 5 (Success Green):** Maximum field extension

**Field Strength Calculation:**

```

Field Strength = min(3.0, Mahalanobis Distance × Tensor Intensity)

```

The field amplitude adjusts to ATR and mathematical distance, creating dynamic zones that respond to market volatility.

**Radiation Line Network:**

During active tensor states, the system projects directional radiation lines showing field energy distribution:

- **8 Directional Rays:** Complete angular coverage

- **Tapering Segments:** Progressive transparency for natural visual flow

- **Pulse Effects:** Enhanced visualization during volatility jumps

### Dimensional Portal System

**Portal Mathematics:**

Dimensional portals visualize regime transitions using category theory principles:

- **Green Portals (◉):** Trending regime detection (appear below price for support)

- **Red Portals (◎):** Mean-reverting regime (appear above price for resistance)

- **Yellow Portals (○):** Random walk regime (neutral positioning)

**Tensor Trail Effects:**

Each portal generates 8 trailing particles showing mathematical momentum:

- **Large Particles (●):** Strong mathematical signal

- **Medium Particles (◦):** Moderate signal strength

- **Small Particles (·):** Weak signal continuation

- **Micro Particles (˙):** Signal dissipation

### Information Flow Streams

**Particle Stream Visualization:**

Transfer entropy creates flowing particle streams indicating information direction:

- **Upward Streams:** Volume leading price (accumulation phases)

- **Downward Streams:** Price leading volume (distribution phases)

- **Stream Density:** Proportional to information flow strength

**15-Particle Evolution:**

Each stream contains 15 particles with progressive sizing and transparency, creating natural flow visualization that makes information transfer immediately apparent.

### Fractal Matrix Grid System

**Multi-Timeframe Fractal Levels:**

The system calculates and displays fractal highs/lows across five Fibonacci periods:

- **8-Period:** Short-term fractal structure

- **13-Period:** Intermediate-term patterns

- **21-Period:** Primary swing levels

- **34-Period:** Major structural levels

- **55-Period:** Long-term fractal boundaries

**Triple-Layer Visualization:**

Each fractal level uses three-layer rendering:

- **Shadow Layer:** Widest, darkest foundation (width 5)

- **Glow Layer:** Medium white core line (width 3)

- **Tensor Layer:** Dotted mathematical overlay (width 1)

**Intelligent Labeling System:**

Smart spacing prevents label overlap using ATR-based minimum distances. Labels include:

- **Fractal Period:** Time-based identification

- **Topological Class:** Mathematical complexity rating (0, I, II, III)

- **Price Level:** Exact fractal price

- **Mahalanobis Distance:** Current mathematical field strength

- **Hurst Exponent:** Current regime classification

- **Anomaly Indicators:** Visual strength representations (○ ◐ ● ⚡)

### Wick Pressure Analysis

**Rejection Level Mathematics:**

The system analyzes candle wick patterns to project future pressure zones:

- **Upper Wick Analysis:** Identifies selling pressure and resistance zones

- **Lower Wick Analysis:** Identifies buying pressure and support zones

- **Pressure Projection:** Extends lines forward based on mathematical probability

**Multi-Layer Glow Effects:**

Wick pressure lines use progressive transparency (1-8 layers) creating natural glow effects that make pressure zones immediately visible without cluttering the chart.

### Enhanced Regime Background

**Dynamic Intensity Mapping:**

Background colors reflect mathematical regime strength:

- **Deep Transparency (98% alpha):** Subtle regime indication

- **Pulse Intensity:** Based on regime strength calculation

- **Color Coding:** Green (trending), Red (mean-reverting), Neutral (random)

**Smoothing Integration:**

Regime changes incorporate 10-bar smoothing to prevent background flicker while maintaining responsiveness to genuine regime shifts.

### Color Scheme System

**Six Professional Themes:**

- **Dark (Default):** Professional trading environment optimization

- **Light:** High ambient light conditions

- **Classic:** Traditional technical analysis appearance

- **Neon:** High-contrast visibility for active trading

- **Neutral:** Minimal distraction focus

- **Bright:** Maximum visibility for complex setups

Each theme maintains mathematical accuracy while optimizing visual clarity for different trading environments and personal preferences.

---

## 📊 INSTITUTIONAL-GRADE DASHBOARD

### Tensor Field Status Section

**Field Strength Display:**

Real-time Mahalanobis distance calculation with dynamic emoji indicators:

- **⚡ (Lightning):** Extreme field strength (>1.5× threshold)

- **● (Solid Circle):** Strong field activity (>1.0× threshold)

- **○ (Open Circle):** Normal field state

**Signal Quality Rating:**

Democratic algorithm assessment:

- **ELITE:** All 3 components aligned (highest probability)

- **STRONG:** 2 components aligned (good probability)

- **GOOD:** 1 component active (moderate probability)

- **WEAK:** No clear component signals

**Threshold and Anomaly Monitoring:**

- **Threshold Display:** Current mathematical threshold setting

- **Anomaly Level (0-100%):** Combined volatility and volume spike measurement

- **>70%:** High anomaly (red warning)

- **30-70%:** Moderate anomaly (orange caution)

- **<30%:** Normal conditions (green confirmation)

### Tensor State Analysis Section

**Mathematical State Classification:**

- **↑ BULL (Tensor State +1):** Trending regime with bullish bias

- **↓ BEAR (Tensor State -1):** Mean-reverting regime with bearish bias

- **◈ SUPER (Tensor State 0):** Random walk regime (neutral)

**Visual State Gauge:**

Five-circle progression showing tensor field polarity:

- **🟢🟢🟢⚪⚪:** Strong bullish mathematical alignment

- **⚪⚪🟡⚪⚪:** Neutral/transitional state

- **⚪⚪🔴🔴🔴:** Strong bearish mathematical alignment

**Trend Direction and Phase Analysis:**

- **📈 BULL / 📉 BEAR / ➡️ NEUTRAL:** Primary trend classification

- **🌪️ CHAOS:** Extreme information flow (>2.0 flow strength)

- **⚡ ACTIVE:** Strong information flow (1.0-2.0 flow strength)

- **😴 CALM:** Low information flow (<1.0 flow strength)

### Trading Signals Section

**Real-Time Signal Status:**

- **🟢 ACTIVE / ⚪ INACTIVE:** Long signal availability

- **🔴 ACTIVE / ⚪ INACTIVE:** Short signal availability

- **Components (X/3):** Active algorithmic components

- **Mode Display:** Current signal generation mode

**Signal Strength Visualization:**

Color-coded component count:

- **Green:** 3/3 components (maximum confidence)

- **Aqua:** 2/3 components (good confidence)

- **Orange:** 1/3 components (moderate confidence)

- **Gray:** 0/3 components (no signals)

### Performance Metrics Section

**Win Rate Monitoring:**

Estimated win rates based on signal quality with emoji indicators:

- **🔥 (Fire):** ≥60% estimated win rate

- **👍 (Thumbs Up):** 45-59% estimated win rate

- **⚠️ (Warning):** <45% estimated win rate

**Mathematical Metrics:**

- **Hurst Exponent:** Real-time fractal dimension (0.000-1.000)

- **Information Flow:** Volume/price leading indicators

- **📊 VOL:** Volume leading price (accumulation/distribution)

- **💰 PRICE:** Price leading volume (momentum/speculation)

- **➖ NONE:** Balanced information flow

- **Volatility Classification:**

- **🔥 HIGH:** Above 1.5× jump threshold

- **📊 NORM:** Normal volatility range

- **😴 LOW:** Below 0.5× jump threshold

### Market Structure Section (Large Dashboard)

**Regime Classification:**

- **📈 TREND:** Hurst >0.6, momentum strategies optimal

- **🔄 REVERT:** Hurst <0.4, contrarian strategies optimal

- **🎲 RANDOM:** Hurst ≈0.5, breakout strategies preferred

**Mathematical Field Analysis:**

- **Dimensions:** Current volatility space complexity (2D-5D)

- **Hawkes λ (Lambda):** Self-exciting jump intensity (0.00-1.00)

- **Jump Status:** 🚨 JUMP (active) / ✅ NORM (normal)

### Settings Summary Section (Large Dashboard)

**Active Configuration Display:**

- **Sensitivity:** Current master sensitivity setting

- **Lookback:** Primary analysis window

- **Theme:** Active color scheme

- **Method:** Hurst calculation method (Classic R/S, Adaptive R/S, DFA)

**Dashboard Sizing Options:**

- **Small:** Essential metrics only (mobile/small screens)

- **Normal:** Balanced information density (standard desktop)

- **Large:** Maximum detail (multi-monitor setups)

**Position Options:**

- **Top Right:** Standard placement (avoids price action)

- **Top Left:** Wide chart optimization

- **Bottom Right:** Recent price focus (scalping)

- **Bottom Left:** Maximum price visibility (swing trading)

---

## 🎯 SIGNAL GENERATION LOGIC

### Multi-Component Convergence System

**Component Signal Architecture:**

The TMAE generates signals through sophisticated component analysis rather than simple threshold crossing:

**Volatility Component:**

- **Jump Detection:** Mahalanobis distance threshold breach

- **Hawkes Intensity:** Self-exciting process activation (>0.2)

- **Multi-dimensional:** Considers all volatility dimensions simultaneously

**Hurst Regime Component:**

- **Trending Markets:** Price above SMA-20 with positive momentum

- **Mean-Reverting Markets:** Price at Bollinger Band extremes

- **Random Markets:** Bollinger squeeze breakouts with directional confirmation

**Transfer Entropy Component:**

- **Volume Leadership:** Information flow from volume to price

- **Volume Spike:** Volume 110%+ above 20-period average

- **Flow Significance:** Above entropy threshold with directional bias

### Democratic Signal Weighting

**Signal Mode Implementation:**

- **Aggressive Mode:** Any single component triggers signal

- **Confluence Mode:** Minimum 2 components must agree

- **Conservative Mode:** All 3 components must align

**Momentum Confirmation:**

All signals require momentum confirmation:

- **Long Signals:** RSI >50 AND price >EMA-9

- **Short Signals:** RSI <50 AND price 0.6):**

- **Increase Sensitivity:** Catch momentum continuation

- **Lower Mean Reversion Threshold:** Avoid counter-trend signals

- **Emphasize Volume Leadership:** Institutional accumulation/distribution

- **Tensor Field Focus:** Use expansion for trend continuation

- **Signal Mode:** Aggressive or Confluence for trend following

**Range-Bound Markets (Hurst <0.4):**

- **Decrease Sensitivity:** Avoid false breakouts

- **Lower Trending Threshold:** Quick regime recognition

- **Focus on Price Leadership:** Retail sentiment extremes

- **Fractal Grid Emphasis:** Support/resistance trading

- **Signal Mode:** Conservative for high-probability reversals

**Volatile Markets (High Jump Frequency):**

- **Increase Hawkes Decay:** Recognize event clustering

- **Higher Jump Threshold:** Avoid noise signals

- **Maximum Dimensions:** Capture full volatility complexity

- **Reduce Position Sizing:** Risk management adaptation

- **Enhanced Visuals:** Maximum information for rapid decisions

**Low Volatility Markets (Low Jump Frequency):**

- **Decrease Jump Threshold:** Capture subtle movements

- **Lower Hawkes Decay:** Treat moves as independent

- **Reduce Dimensions:** Simplify analysis

- **Increase Position Sizing:** Capitalize on compressed volatility

- **Minimal Visuals:** Reduce distraction in quiet markets

---

## 🚀 ADVANCED TRADING STRATEGIES

### The Mathematical Convergence Method

**Entry Protocol:**

1. **Fractal Grid Approach:** Monitor price approaching significant fractal levels

2. **Tensor Field Confirmation:** Verify field expansion supporting direction

3. **Portal Signal:** Wait for dimensional portal appearance

4. **ELITE/STRONG Quality:** Only trade highest quality mathematical signals

5. **Component Consensus:** Confirm 2+ components agree in Confluence mode

**Example Implementation:**

- Price approaching 21-period fractal high

- Tensor field expanding upward (bullish mathematical alignment)

- Green portal appears below price (trending regime confirmation)

- ELITE quality signal with 3/3 components active

- Enter long position with stop below fractal level

**Risk Management:**

- **Stop Placement:** Below/above fractal level that generated signal

- **Position Sizing:** Based on Mahalanobis distance (higher distance = smaller size)

- **Profit Targets:** Next fractal level or tensor field resistance

### The Regime Transition Strategy

**Regime Change Detection:**

1. **Monitor Hurst Exponent:** Watch for persistent moves above/below thresholds

2. **Portal Color Change:** Regime transitions show different portal colors

3. **Background Intensity:** Increasing regime background intensity

4. **Mathematical Confirmation:** Wait for regime confirmation (hysteresis)

**Trading Implementation:**

- **Trending Transitions:** Trade momentum breakouts, follow trend

- **Mean Reversion Transitions:** Trade range boundaries, fade extremes

- **Random Transitions:** Trade breakouts with tight stops

**Advanced Techniques:**

- **Multi-Timeframe:** Confirm regime on higher timeframe

- **Early Entry:** Enter on regime transition rather than confirmation

- **Regime Strength:** Larger positions during strong regime signals

### The Information Flow Momentum Strategy

**Flow Detection Protocol:**

1. **Monitor Transfer Entropy:** Watch for significant information flow shifts

2. **Volume Leadership:** Strong edge when volume leads price

3. **Flow Acceleration:** Increasing flow strength indicates momentum

4. **Directional Confirmation:** Ensure flow aligns with intended trade direction

**Entry Signals:**

- **Volume → Price Flow:** Enter during accumulation/distribution phases

- **Price → Volume Flow:** Enter on momentum confirmation breaks

- **Flow Reversal:** Counter-trend entries when flow reverses

**Optimization:**

- **Scalping:** Use immediate flow detection (2-5 bar lag)

- **Swing Trading:** Use structural flow (10-20 bar lag)

- **Multi-Asset:** Compare flow between correlated assets

### The Tensor Field Expansion Strategy

**Field Mathematics:**

The tensor field expansion indicates mathematical pressure building in market structure:

**Expansion Phases:**

1. **Compression:** Field contracts, volatility decreases

2. **Tension Building:** Mathematical pressure accumulates

3. **Expansion:** Field expands rapidly with directional movement

4. **Resolution:** Field stabilizes at new equilibrium

**Trading Applications:**

- **Compression Trading:** Prepare for breakout during field contraction

- **Expansion Following:** Trade direction of field expansion

- **Reversion Trading:** Fade extreme field expansion

- **Multi-Dimensional:** Consider all field layers for confirmation

### The Hawkes Process Event Strategy

**Self-Exciting Jump Trading:**

Understanding that market shocks cluster and create follow-on opportunities:

**Jump Sequence Analysis:**

1. **Initial Jump:** First volatility jump detected

2. **Clustering Phase:** Hawkes intensity remains elevated

3. **Follow-On Opportunities:** Additional jumps more likely

4. **Decay Period:** Intensity gradually decreases

**Implementation:**

- **Jump Confirmation:** Wait for mathematical jump confirmation

- **Direction Assessment:** Use other components for direction

- **Clustering Trades:** Trade subsequent moves during high intensity

- **Decay Exit:** Exit positions as Hawkes intensity decays

### The Fractal Confluence System

**Multi-Timeframe Fractal Analysis:**

Combining fractal levels across different periods for high-probability zones:

**Confluence Zones:**

- **Double Confluence:** 2 fractal levels align

- **Triple Confluence:** 3+ fractal levels cluster

- **Mathematical Confirmation:** Tensor field supports the level

- **Information Flow:** Transfer entropy confirms direction

**Trading Protocol:**

1. **Identify Confluence:** Find 2+ fractal levels within 1 ATR

2. **Mathematical Support:** Verify tensor field alignment

3. **Signal Quality:** Wait for STRONG or ELITE signal

4. **Risk Definition:** Use fractal level for stop placement

5. **Profit Targeting:** Next major fractal confluence zone

---

## ⚠️ COMPREHENSIVE RISK MANAGEMENT

### Mathematical Position Sizing

**Mahalanobis Distance Integration:**

Position size should inversely correlate with mathematical field strength:

```

Position Size = Base Size × (Threshold / Mahalanobis Distance)

```

**Risk Scaling Matrix:**

- **Low Field Strength (<2.0):** Standard position sizing

- **Moderate Field Strength (2.0-3.0):** 75% position sizing

- **High Field Strength (3.0-4.0):** 50% position sizing

- **Extreme Field Strength (>4.0):** 25% position sizing or no trade

### Signal Quality Risk Adjustment

**Quality-Based Position Sizing:**

- **ELITE Signals:** 100% of planned position size

- **STRONG Signals:** 75% of planned position size

- **GOOD Signals:** 50% of planned position size

- **WEAK Signals:** No position or paper trading only

**Component Agreement Scaling:**

- **3/3 Components:** Full position size

- **2/3 Components:** 75% position size

- **1/3 Components:** 50% position size or skip trade

### Regime-Adaptive Risk Management

**Trending Market Risk:**

- **Wider Stops:** Allow for trend continuation

- **Trend Following:** Trade with regime direction

- **Higher Position Size:** Trend probability advantage

- **Momentum Stops:** Trail stops based on momentum indicators

**Mean-Reverting Market Risk:**

- **Tighter Stops:** Quick exits on trend continuation

- **Contrarian Positioning:** Trade against extremes

- **Smaller Position Size:** Higher reversal failure rate

- **Level-Based Stops:** Use fractal levels for stops

**Random Market Risk:**

- **Breakout Focus:** Trade only clear breakouts

- **Tight Initial Stops:** Quick exit if breakout fails

- **Reduced Frequency:** Skip marginal setups

- **Range-Based Targets:** Profit targets at range boundaries

### Volatility-Adaptive Risk Controls

**High Volatility Periods:**

- **Reduced Position Size:** Account for wider price swings

- **Wider Stops:** Avoid noise-based exits

- **Lower Frequency:** Skip marginal setups

- **Faster Exits:** Take profits more quickly

**Low Volatility Periods:**

- **Standard Position Size:** Normal risk parameters

- **Tighter Stops:** Take advantage of compressed ranges

- **Higher Frequency:** Trade more setups

- **Extended Targets:** Allow for compressed volatility expansion

### Multi-Timeframe Risk Alignment

**Higher Timeframe Trend:**

- **With Trend:** Standard or increased position size

- **Against Trend:** Reduced position size or skip

- **Neutral Trend:** Standard position size with tight management

**Risk Hierarchy:**

1. **Primary:** Current timeframe signal quality

2. **Secondary:** Higher timeframe trend alignment

3. **Tertiary:** Mathematical field strength

4. **Quaternary:** Market regime classification

---

## 📚 EDUCATIONAL VALUE AND MATHEMATICAL CONCEPTS

### Advanced Mathematical Concepts

**Tensor Analysis in Markets:**

The TMAE introduces traders to tensor analysis, a branch of mathematics typically reserved for physics and advanced engineering. Tensors provide a framework for understanding multi-dimensional market relationships that scalar and vector analysis cannot capture.

**Information Theory Applications:**

Transfer entropy implementation teaches traders about information flow in markets, a concept from information theory that quantifies directional causality between variables. This provides intuition about market microstructure and participant behavior.

**Fractal Geometry in Trading:**

The Hurst exponent calculation exposes traders to fractal geometry concepts, helping understand that markets exhibit self-similar patterns across multiple timeframes. This mathematical insight transforms how traders view market structure.

**Stochastic Process Theory:**

The Hawkes process implementation introduces concepts from stochastic process theory, specifically self-exciting point processes. This provides mathematical framework for understanding why market events cluster and exhibit memory effects.

### Learning Progressive Complexity

**Beginner Mathematical Concepts:**

- **Volatility Dimensions:** Understanding multi-dimensional analysis

- **Regime Classification:** Learning market personality types

- **Signal Democracy:** Algorithmic consensus building

- **Visual Mathematics:** Interpreting mathematical concepts visually

**Intermediate Mathematical Applications:**

- **Mahalanobis Distance:** Statistical distance in multi-dimensional space

- **Rescaled Range Analysis:** Fractal dimension measurement

- **Information Entropy:** Quantifying uncertainty and causality

- **Field Theory:** Understanding mathematical fields in market context

**Advanced Mathematical Integration:**

- **Tensor Field Dynamics:** Multi-dimensional market force analysis

- **Stochastic Self-Excitation:** Event clustering and memory effects

- **Categorical Composition:** Mathematical signal combination theory

- **Topological Market Analysis:** Understanding market shape and connectivity

### Practical Mathematical Intuition

**Developing Market Mathematics Intuition:**

The TMAE serves as a bridge between abstract mathematical concepts and practical trading applications. Traders develop intuitive understanding of:

- **How markets exhibit mathematical structure beneath apparent randomness**

- **Why multi-dimensional analysis reveals patterns invisible to single-variable approaches**

- **How information flows through markets in measurable, predictable ways**

- **Why mathematical models provide probabilistic edges rather than certainties**

---

## 🔬 IMPLEMENTATION AND OPTIMIZATION

### Getting Started Protocol

**Phase 1: Observation (Week 1)**

1. **Apply with defaults:** Use standard settings on your primary trading timeframe

2. **Study visual elements:** Learn to interpret tensor fields, portals, and streams

3. **Monitor dashboard:** Observe how metrics change with market conditions

4. **No trading:** Focus entirely on pattern recognition and understanding

**Phase 2: Pattern Recognition (Week 2-3)**

1. **Identify signal patterns:** Note what market conditions produce different signal qualities

2. **Regime correlation:** Observe how Hurst regimes affect signal performance

3. **Visual confirmation:** Learn to read tensor field expansion and portal signals

4. **Component analysis:** Understand which components drive signals in different markets

**Phase 3: Parameter Optimization (Week 4-5)**

1. **Asset-specific tuning:** Adjust parameters for your specific trading instrument

2. **Timeframe optimization:** Fine-tune for your preferred trading timeframe

3. **Sensitivity adjustment:** Balance signal frequency with quality

4. **Visual customization:** Optimize colors and intensity for your trading environment

**Phase 4: Live Implementation (Week 6+)**

1. **Paper trading:** Test signals with hypothetical trades

2. **Small position sizing:** Begin with minimal risk during learning phase

3. **Performance tracking:** Monitor actual vs. expected signal performance

4. **Continuous optimization:** Refine settings based on real performance data

### Performance Monitoring System

**Signal Quality Tracking:**

- **ELITE Signal Win Rate:** Track highest quality signals separately

- **Component Performance:** Monitor which components provide best signals

- **Regime Performance:** Analyze performance across different market regimes

- **Timeframe Analysis:** Compare performance across different session times

**Mathematical Metric Correlation:**

- **Field Strength vs. Performance:** Higher field strength should correlate with better performance

- **Component Agreement vs. Win Rate:** More component agreement should improve win rates

- **Regime Alignment vs. Success:** Trading with mathematical regime should outperform

### Continuous Optimization Process

**Monthly Review Protocol:**

1. **Performance Analysis:** Review win rates, profit factors, and maximum drawdown

2. **Parameter Assessment:** Evaluate if current settings remain optimal

3. **Market Adaptation:** Adjust for changes in market character or volatility

4. **Component Weighting:** Consider if certain components should receive more/less emphasis

**Quarterly Deep Analysis:**

1. **Mathematical Model Validation:** Verify that mathematical relationships remain valid

2. **Regime Distribution:** Analyze time spent in different market regimes

3. **Signal Evolution:** Track how signal characteristics change over time

4. **Correlation Analysis:** Monitor correlations between different mathematical components

---

## 🌟 UNIQUE INNOVATIONS AND CONTRIBUTIONS

### Revolutionary Mathematical Integration

**First-Ever Implementations:**

1. **Multi-Dimensional Volatility Tensor:** First indicator to implement true tensor analysis for market volatility

2. **Real-Time Hawkes Process:** First trading implementation of self-exciting point processes

3. **Transfer Entropy Trading Signals:** First practical application of information theory for trade generation

4. **Democratic Component Voting:** First algorithmic consensus system for signal generation

5. **Fractal-Projected Signal Quality:** First system to predict signal quality at future price levels

### Advanced Visualization Innovations

**Mathematical Visualization Breakthroughs:**

- **Tensor Field Radiation:** Visual representation of mathematical field energy

- **Dimensional Portal System:** Category theory visualization for regime transitions

- **Information Flow Streams:** Real-time visual display of market information transfer

- **Multi-Layer Fractal Grid:** Intelligent spacing and projection system

- **Regime Intensity Mapping:** Dynamic background showing mathematical regime strength

### Practical Trading Innovations

**Trading System Advances:**

- **Quality-Weighted Signal Generation:** Signals rated by mathematical confidence

- **Regime-Adaptive Strategy Selection:** Automatic strategy optimization based on market personality

- **Anti-Spam Signal Protection:** Mathematical prevention of signal clustering

- **Component Performance Tracking:** Real-time monitoring of algorithmic component success

- **Field-Strength Position Sizing:** Mathematical volatility integration for risk management

---

## ⚖️ RESPONSIBLE USAGE AND LIMITATIONS

### Mathematical Model Limitations

**Understanding Model Boundaries:**

While the TMAE implements sophisticated mathematical concepts, traders must understand fundamental limitations:

- **Markets Are Not Purely Mathematical:** Human psychology, news events, and fundamental factors create unpredictable elements

- **Past Performance Limitations:** Mathematical relationships that worked historically may not persist indefinitely

- **Model Risk:** Complex models can fail during unprecedented market conditions

- **Overfitting Potential:** Highly optimized parameters may not generalize to future market conditions

### Proper Implementation Guidelines

**Risk Management Requirements:**

- **Never Risk More Than 2% Per Trade:** Regardless of signal quality

- **Diversification Mandatory:** Don't rely solely on mathematical signals

- **Position Sizing Discipline:** Use mathematical field strength for sizing, not confidence

- **Stop Loss Non-Negotiable:** Every trade must have predefined risk parameters

**Realistic Expectations:**

- **Mathematical Edge, Not Certainty:** The indicator provides probabilistic advantages, not guaranteed outcomes

- **Learning Curve Required:** Complex mathematical concepts require time to master

- **Market Adaptation Necessary:** Parameters must evolve with changing market conditions

- **Continuous Education Important:** Understanding underlying mathematics improves application

### Ethical Trading Considerations

**Market Impact Awareness:**

- **Information Asymmetry:** Advanced mathematical analysis may provide advantages over other market participants

- **Position Size Responsibility:** Large positions based on mathematical signals can impact market structure

- **Sharing Knowledge:** Consider educational contributions to trading community

- **Fair Market Participation:** Use mathematical advantages responsibly within market framework

### Professional Development Path

**Skill Development Sequence:**

1. **Basic Mathematical Literacy:** Understand fundamental concepts before advanced application

2. **Risk Management Mastery:** Develop disciplined risk control before relying on complex signals

3. **Market Psychology Understanding:** Combine mathematical analysis with behavioral market insights

4. **Continuous Learning:** Stay updated on mathematical finance developments and market evolution

---

## 🔮 CONCLUSION

The Tensor Market Analysis Engine represents a quantum leap forward in technical analysis, successfully bridging the gap between advanced pure mathematics and practical trading applications. By integrating multi-dimensional volatility analysis, fractal market theory, and information flow dynamics, the TMAE reveals market structure invisible to conventional analysis while maintaining visual clarity and practical usability.

### Mathematical Innovation Legacy

This indicator establishes new paradigms in technical analysis:

- **Tensor analysis for market volatility understanding**

- **Stochastic self-excitation for event clustering prediction**

- **Information theory for causality-based trade generation**

- **Democratic algorithmic consensus for signal quality enhancement**

- **Mathematical field visualization for intuitive market understanding**

### Practical Trading Revolution

Beyond mathematical innovation, the TMAE transforms practical trading:

- **Quality-rated signals replace binary buy/sell decisions**

- **Regime-adaptive strategies automatically optimize for market personality**

- **Multi-dimensional risk management integrates mathematical volatility measures**

- **Visual mathematical concepts make complex analysis immediately interpretable**

- **Educational value creates lasting improvement in trading understanding**

### Future-Proof Design

The mathematical foundations ensure lasting relevance:

- **Universal mathematical principles transcend market evolution**

- **Multi-dimensional analysis adapts to new market structures**

- **Regime detection automatically adjusts to changing market personalities**

- **Component democracy allows for future algorithmic additions**

- **Mathematical visualization scales with increasing market complexity**

### Commitment to Excellence

The TMAE represents more than an indicator—it embodies a philosophy of bringing rigorous mathematical analysis to trading while maintaining practical utility and visual elegance. Every component, from the multi-dimensional tensor fields to the democratic signal generation, reflects a commitment to mathematical accuracy, trading practicality, and educational value.

### Trading with Mathematical Precision

In an era where markets grow increasingly complex and computational, the TMAE provides traders with mathematical tools previously available only to institutional quantitative research teams. Yet unlike academic mathematical models, the TMAE translates complex concepts into intuitive visual representations and practical trading signals.

By combining the mathematical rigor of tensor analysis, the statistical power of multi-dimensional volatility modeling, and the information-theoretic insights of transfer entropy, traders gain unprecedented insight into market structure and dynamics.

### Final Perspective

Markets, like nature, exhibit profound mathematical beauty beneath apparent chaos. The Tensor Market Analysis Engine serves as a mathematical lens that reveals this hidden order, transforming how traders perceive and interact with market structure.

Through mathematical precision, visual elegance, and practical utility, the TMAE empowers traders to see beyond the noise and trade with the confidence that comes from understanding the mathematical principles governing market behavior.

Trade with mathematical insight. Trade with the power of tensors. Trade with the TMAE.

*"In mathematics, you don't understand things. You just get used to them." - John von Neumann*

*With the TMAE, mathematical market understanding becomes not just possible, but intuitive.*

— Dskyz, Trade with insight. Trade with anticipation.

Mandelbrot-Fibonacci Cascade Vortex (MFCV)Mandelbrot-Fibonacci Cascade Vortex (MFCV) - Where Chaos Theory Meets Sacred Geometry

A Revolutionary Synthesis of Fractal Mathematics and Golden Ratio Dynamics

What began as an exploration into Benoit Mandelbrot's fractal market hypothesis and the mysterious appearance of Fibonacci sequences in nature has culminated in a groundbreaking indicator that reveals the hidden mathematical structure underlying market movements. This indicator represents months of research into chaos theory, fractal geometry, and the golden ratio's manifestation in financial markets.

The Theoretical Foundation

Mandelbrot's Fractal Market Hypothesis Traditional efficient market theory assumes normal distributions and random walks. Mandelbrot proved markets are fractal - self-similar patterns repeating across all timeframes with power-law distributions. The MFCV implements this through:

Hurst Exponent Calculation: H = log(R/S) / log(n/2)

Where:

R = Range of cumulative deviations

S = Standard deviation

n = Period length

This measures market memory:

H > 0.5: Trending (persistent) behavior

H = 0.5: Random walk

H < 0.5: Mean-reverting (anti-persistent) behavior

Fractal Dimension: D = 2 - H

This quantifies market complexity, where higher dimensions indicate more chaotic behavior.

Fibonacci Vortex Theory Markets don't move linearly - they spiral. The MFCV reveals these spirals using Fibonacci sequences:

Vortex Calculation: Vortex(n) = Price + sin(bar_index × φ / Fn) × ATR(Fn) × Volume_Factor

Where:

φ = 0.618 (golden ratio)

Fn = Fibonacci number (8, 13, 21, 34, 55)

Volume_Factor = 1 + (Volume/SMA(Volume,50) - 1) × 0.5

This creates oscillating spirals that contract and expand with market energy.

The Volatility Cascade System