Gross and Net LTF Volume + Trailing Percentile Sessions CVOL Hi Traders !

Gross volume, net lower time frame (LTF) volume and trailing session percentile Cumulative session volume:

The code calculates and plots the following volume indicators:

Volume (Gross Volume): The total volume for the current bar.

Net lower time frame volume: The difference between the buy and sell volumes of the lower time frame.

Cumulative daily session volume: The cumulative sum of the volume for the current day.

Percentile Cumulative daily session volume: The percentile of the cumulative daily session volume (calculated on a rolling basis).

The above indicators may be plotted exclusively or exclusively.

Why is Volume important:

Volume is the number of shares or contracts traded (of a financial asset) during a given time period (timeframe). It is a crucial indicator in technical analysis and quantitative trading, as volume helps in identifying

Price Confirmation: Volume confirms price movements by indicating the level of interest and participation in the market. When prices move significantly, accompanied by strong volume, it suggests that the movement is likely to be sustained. Conversely, if prices move without significant volume, it suggests that the movement may be temporary or lacking conviction.

Trend Strength: Volume can help identify the strength and direction of a trend. During an uptrend, increasing volume alongside price increases indicates that the upward momentum is gaining traction. Conversely, decreasing volume during an uptrend suggests that the upward momentum may be weakening.

Reversal Points: Sharp volume spikes in the opposite direction of the prevailing trend can signal a potential reversal point. This is because large volume indicates a significant shift in trader sentiment, suggesting that the trend may be changing direction.

Liquidity: High volume indicates that a security is liquid, meaning that it can be easily bought and sold without significant price impact. Liquidity is important for traders who want to execute large orders without significantly affecting the market price.

For example, suppose we want to identify positive price confirmation and positive trend strength, in this case we may use the CVOL (with trailing percentile).

The above image showcases price expansion conditional on high positive volume (increasing CVOL), The price expansion also exhibits Volume confluences (the colored bars).

Positive Confluence: Increase in positive total volume and an increase in positive lower time frame volume in relative and absolute terms.

Negative Confluence : Increase in negative total volume and an increase in negative lower time frame volume in relative and absolute terms.

Also note how the percentile color does not change, this means that the new volume bars are > than the highest percentile (80%) of volume values from the beginning of the session.

在腳本中搜尋"liquidity"

NetLiquidityLibraryMacFLibrary "NetLiquidityLibraryMacF"

The Net Liquidity Library provides daily values for net liquidity. Net liquidity is measured as Fed Balance Sheet - Treasury General Account - Reverse Repo. Time series for each individual component included too.

get_net_liquidity(component)

Gets the Net Liquidity time series for the last 250 trading days. Dates that are not present are represented as na.

Parameters:

component (simple string) : The component of the Net Liquidity function to return. Possible values: 'fed', 'tga', and 'rrp'. (`Net Liquidity` is returned if no argument is supplied).

Returns: The Net Liquidity time series or a component of the Net Liquidity function.

Bitcoin Relative Macro StrengthBTC Relative Macro Strength

Overview

The BTC Relative Macro Strength indicator measures Bitcoin's price strength relative to the global macro environment. By tracking deviations from the macro trend, it identifies potentially overvalued and undervalued market phases.

The global macro trend is derived by multiplying the ISM PMI (a widely-used proxy for the business cycle) by a simplified measure of global liquidity.

Calculations

Global Liquidity = Fed Balance Sheet − Reverse Repo − Treasury General Account + U.S. M2 + China M2

Global Macro Trend = ISM PMI × Global Liquidity

Understanding the Global Macro Trend

The global macro trend plot combines the ebb and flow of global liquidity with the cyclical patterns of the business cycle. The resulting composite exhibits strong directional correlation with Bitcoin—or more precisely, Bitcoin appears to move in lockstep with liquidity conditions and business cycle phases.

This relationship has strengthened notably since COVID, likely because Bitcoin's growing market capitalization has increased its exposure to macro forces.

The takeaway is that Bitcoin is acutely sensitive to growth in the money supply (it trends with liquidity expansion) and oscillates with the phases of the business cycle.

Indicator Components

📊 Histogram: BTC/Macro Change

Displays the rolling percentage change of Bitcoin's price relative to the global macro trend.

High values: Bitcoin is outpacing macro conditions (potentially overvalued)

Low values: Bitcoin is underperforming macro conditions (potentially undervalued)

Color scheme:

🟢 Green = Positive deviation

🔴 Red = Negative deviation

📈 Macro Slope Line

Plots the scaled percentage change of the global macro trend itself.

Color scheme:

🔵 Teal = BULLISH (slope positive and rising)

⚪ Gray = NEUTRAL (slope and trend disagree)

🟣 Pink = BEARISH (slope negative and falling)

FieldDescription

BTC/Macro Change : Percentage change of Bitcoin's price vs. the Global Macro Trend (default: 21-bar average)

Macro Trend : Composite assessment combining slope direction and trend momentum. Reads BULLISH when both align upward, BEARISH when both align downward, NEUTRAL when they disagree

Macro Slope : The global macro trend's average slope expressed as a percentage

BTC Valuation : Relative valuation category based on BTC/Macro deviation (Extreme Premium → Extreme Discount)

BTC Price : Current Bitcoin price

How to Use

This indicator is primarily useful for identifying market phases where Bitcoin's price has diverged from the global macro trend.

Identify extremes : Look for periods when the histogram reaches elevated positive or negative levels

Assess valuation : Use the BTC Valuation reading to gauge relative over/undervaluation

Confirm with trend : Check whether macro conditions support or contradict the current price level

Mean reversion : Consider that significant deviations from trend historically tend to revert

Note: This indicator identifies relative valuation based on macro conditions—it does not predict price direction or timing.

Settings

Lookback Period - 21 bars - Number of bars for calculating rolling averages

Macro Slope Scale - 3.0 - Multiplier for macro slope line visibility

Market Structure ICT Screener [TradingFinder] BoS ChoCh🔵 Introduction

Market Structure is the foundation of every Smart Money and ICT based trading model. It describes how price moves through a sequence of highs and lows, forming clear phases of expansion, retracement and reversal. Understanding this structure allows traders to read institutional order flow and align their positions with the true direction of liquidity.

Two of the most critical components in Market Structure are the Break of Structure (BOS) and Change of Character (CHOCH). A BOS represents trend continuation, confirming strength within the current direction. In contrast, CHOCH also known as a Market Structure Shift (MSS) signals the first sign of a trend reversal or liquidity shift where order flow begins to change from bullish to bearish or vice versa.

Because the market is fractal, structure can exist at multiple levels known as Major (External) and Minor (Internal). Major structure defines the overall trend on higher timeframes while minor or internal structure reveals short term swings and early reversals within that larger move.

🔵 How to Use

Understanding Market Structure starts with identifying how price interacts with previous swing highs and swing lows. Every trend in the market, whether bullish or bearish, is built from a sequence of impulsive and corrective moves. Impulsive legs show strong displacement in the direction of liquidity flow, while corrective legs represent temporary pullbacks as the market rebalances before the next expansion. Recognizing these sequences is essential for reading the story of price and anticipating what may happen next.

A Break of Structure (BOS) occurs when price decisively moves beyond a previous structural point by breaking above the last high in an uptrend or falling below the last low in a downtrend. This event confirms that the current trend remains intact and that liquidity has been successfully taken from one side of the market. A BOS acts as confirmation of continuation and reflects strength within the existing directional bias.

A Change of Character (CHOCH) appears when price violates structure in the opposite direction of the prevailing trend. This is the first signal that market sentiment and order flow may be shifting. For example, during a downtrend if price breaks above a previous high, it indicates that sellers are losing control and a potential bullish reversal may be developing. In an uptrend, when price drops below a recent low, it suggests a possible bearish transition.

Because the market is fractal, structure exists across multiple layers. Major structure reflects the dominant movement visible on higher timeframes and defines the broader directional bias. Minor or internal structure represents smaller swings within that move and helps identify early transitions before they appear on the higher timeframe. When internal and external structures align, they offer a high probability signal for trend continuation or reversal.

By observing BOS and CHOCH across both internal and external structures, traders can clearly visualize when the market is expanding, contracting or preparing to shift direction. This structured understanding of price movement forms the foundation for precise trend analysis and high quality decision making in any Smart Money or ICT based trading approach.

🔵 Settings

🟣 Display Settings

Table on Chart : Allows users to choose the position of the signal dashboard either directly on the chart or below it, depending on their layout preference.

Number of Symbols : Enables users to control how many symbols are displayed in the screener table, from 10 to 20, adjustable in increments of 2 symbols for flexible screening depth.

Table Mode : This setting offers two layout styles for the signal table :

Basic : Mode displays symbols in a single column, using more vertical space.

Extended : Mode arranges symbols in pairs side-by-side, optimizing screen space with a more compact view.

Table Size : Lets you adjust the table’s visual size with options such as: auto, tiny, small, normal, large, huge.

Table Position : Sets the screen location of the table. Choose from 9 possible positions, combining vertical (top, middle, bottom) and horizontal (left, center, right) alignments.

🟣 Symbol Settings

Each of the 20 symbol slots comes with a full set of customizable parameters :

Symbol : Define or select the asset (e.g., XAUUSD, BTCUSD, EURUSD, etc.).

Timeframe : Set your desired timeframe for each symbol (e.g., 15, 60, 240, 1D).

Pivot Period : Set the length used to detect swing highs and lows. Shorter values increase sensitivity, longer ones focus on major structures.

🔵 Conclusion

Mastering Market Structure and understanding the relationship between BOS and CHOCH allows traders to see the market with greater clarity and confidence. These two elements reveal how liquidity moves through different phases of expansion and retracement and how institutional order flow shifts between accumulation and distribution.

By analyzing both internal and external structures, traders can align short term and long term perspectives and anticipate where price is most likely to react. The ability to read these structural shifts helps identify continuation points, reversals and areas where liquidity is engineered or collected.

Incorporating Market Structure into a consistent trading process transforms the way a trader views the chart. Instead of reacting to random movements, each swing, break and shift becomes part of a logical framework that reflects the true behavior of the market. Understanding BOS and CHOCH is not just a concept but a complete language of price that guides every professional decision in Smart Money and ICT based trading.

Dual-Frame Momentum OscillatorDual-Frame Momentum Oscillator (DFMO)

This is not just another oscillator. This is a confluence engine, built for the discerning trader who reads the story of price action and needs an objective tool to confirm the climax.

The Dual-Frame Momentum Oscillator was designed to solve a specific problem: how to differentiate a genuine, sustainable breakout from an exhaustive liquidity grab. It provides a visual confirmation for high-probability reversal and scalp setups by measuring momentum across two distinct time frames simultaneously.

This tool is for the trader who understands that indicators should not dictate trades, but rather confirm a well-defined thesis based on market structure, volume, and liquidity.

The Core Concept: Context Meets Trigger

The DFMO fuses a slow, methodical Stochastic with a hyper-sensitive RSI to give you a complete picture of momentum.

The Context (Slow Stochastic %K - default 40,4,4): This acts as your long-term momentum gauge. It tells you if the underlying trend is healthy or nearing exhaustion. A high reading suggests the market is overextended and vulnerable, while a low reading suggests the opposite.

The Trigger (Fast RSI - default 3): This is your immediate impulse reader. It measures the velocity and intensity of the current price thrust, making it incredibly sensitive to exhaustive moves, spikes, and bounces.

By themselves, they are useful. Together, they are formidable.

The Confluence Engine: Your Visual Edge

The true power of the DFMO lies in its "Confluence Engine." The indicator's background highlights in real-time when both oscillators are in agreement, visually flagging moments of maximum opportunity.

Bearish Confluence Zone (Red): The background turns red only when the Stochastic is overbought AND the RSI is overbought. This is your signal that the broader trend is exhausted and the current buying impulse has reached a climax. It is the ideal confirmation for a short entry following a liquidity sweep above a key high.

Bullish Confluence Zone (Green): The background turns green only when the Stochastic is oversold AND the RSI is oversold. This signals that the downtrend is tired and the immediate selling pressure is exhaustive, providing high-probability confirmation for a long entry at a key support level.

When these zones appear, the indicator is telling you that both the context and the trigger are aligned. This removes ambiguity and allows for decisive, confident execution.

Practical Application: The Liquidity Sweep

Imagine you're stalking a short on a futures contract like MCL or MES. You've marked the high of the day (HOD) as a key resistance level where liquidity is resting. You see a sharp, vertical impulse move that breaks the HOD, clearing out the stops.

Is this a real breakout, or is it a manipulation move—a classic liquidity grab?

You glance down at the DFMO. The moment price swept the high, the background flashed red. That's your objective confirmation. The slow Stoch was already overbought, and the fast RSI spiking confirmed the exhaustive, terminal nature of that price thrust. You now have the confidence to enter your short scalp, knowing you are aligned with the probable direction of the market's next move.

This is how you move from "feeling" the market to systematically executing a high-probability edge. This is how you aspire for greatness.

Add the Dual-Frame Momentum Oscillator to your toolkit and transform your ability to time entries with surgical precision.

Candle Range DetectorCandle Range Detector

// Pine Script v6

// Detects candle-based ranges, mitigations, and sweeps with advanced logic

Overview

This indicator automatically detects price ranges based on candle containment, then tracks when those ranges are mitigated (broken) and when a sweep occurs. It is designed for traders who want to identify liquidity events and range breaks with precision.

How It Works

- Range Detection: A range is formed when a candle is fully contained within the previous candle (its high is lower and its low is higher). This marks a potential area of price balance or liquidity.

- Mitigation: A range is considered mitigated when price closes beyond its extension levels (configurable by normal or Fibonacci logic). This signals that the range has been invalidated or "taken out" by price action.

- Sweep Detection: After mitigation, the script watches for a sweep event: a candle that both trades through the range extreme and closes decisively beyond the log-mid of the candle itself. This is a strong sign of a liquidity grab or stop run.

- Alerts & Visuals: You can enable alerts and on-chart labels for sweeps. Only the most recent mitigated range can be swept, and each range can only be swept once.

- Timeframe Sensitivity: On weekly or monthly charts, a candle can both mitigate and sweep a range on the same bar. On lower timeframes, only one event can occur per bar.

Why It Works

- Candle containment is a robust way to identify natural price ranges and liquidity pools, as it reflects where price is consolidating or being absorbed.

- Mitigation marks the moment when a range is no longer defended, often leading to new directional moves.

- Sweeps are powerful signals of stop hunts or liquidity grabs, especially when confirmed by a close beyond the log-mid of the candle, indicating strong intent.

Visual Explanation

Tip: Use this tool to spot high-probability reversal or continuation zones, and to get alerted to key liquidity events in real time.

SiCInside Sweep Close (ISC):

This concept captures a specific price action behavior and can help refine trading strategies for better precision. Here's a detailed explanation:

Inside:

The closing price of the candle stays within the range of the previous candle.

This indicates a containment of price action, suggesting indecision or preparation for a significant move.

Sweep:

The wick of the candle takes out (or "sweeps") the low (or high) of the previous candle.

This sweep can trigger stop-losses of retail traders or activate pending orders, often used by smart money strategies.

Close:

The candle ultimately closes inside the range of the previous candle.

This close signifies that the sweep was a liquidity grab rather than a genuine breakout, providing an actionable trading signal.

How ISC Can Be Used in Trading:

Liquidity Grab Recognition:

ISC can indicate when liquidity is swept from the market, making it an ideal entry point for traders anticipating a reversal or continuation.

Smart Money Concept (SMC) Synergy:

If you follow SMC principles, ISC aligns with key concepts like liquidity sweeps, order blocks, and mitigation zones.

Risk Management:

By identifying the ISC setup, you can place tighter stop-loss levels just outside the sweep, optimizing risk-reward ratios.

Entry Signals:

When you spot an ISC, you can enter trades at the close of the candle, anticipating a move in the direction opposite to the sweep.

Example of ISC in Action:

Imagine a bearish candle:

The wick sweeps the low of the previous candle, possibly triggering stop-losses.

However, the close stays inside the previous candle’s range.

This setup might indicate a reversal, where price moves upward after grabbing liquidity.

Why This Name Works:

It’s concise, professional, and directly linked to the trading action you’re describing.

The short form, ISC, is easy to remember and discuss within trading circles or while teaching others.

It ties into widely known concepts like smart money, price action, and liquidity sweeps, making it relatable yet unique.

Does this align with how you envision using the concept? Let me know if you’d like more refinements or visual examples!

Sessions Lite [TradingFinder] New York, London, Asia, NYSE Forex🔵 Introduction

A trading session is one of the basic concepts in the financial market that refers to specific time periods. In fact, a session means hours during the day and night, during which traders in a certain part of the world conduct their transactions.

Although the "Forex" and "CFDs" market is open 24 hours a day and it is possible to trade in it, but in some hours the activity in this market decreases so much that many traders prefer not to trade and only watch the market. On the other hand, there are specific times when the market is very busy and dynamic, and many traders tend to trade during these hours of the day and night.

Trading sessions are usually divided into three main categories, which are "Asian", "European" and "North American" sessions. These trading sessions are also called the "Tokyo", "London" and "New York" sessions, respectively. But they also categorized these sessions in more detailed ways such as "Sydney session", "Shanghai session" or "NYSE session".

🔵 Tokyo trading session (Asian session)

After the weekend that happens on Saturday and Sunday, the Forex market starts with the Asian session. In this continent, most of the transactions are done in the Tokyo session, and for this reason, it is usually called the Asian session or the Tokyo session. However, other countries such as Australia, China and Singapore also do a lot of trading in this session.

The Tokyo session has a lower volume of transactions compared to the London and New York sessions, and therefore the liquidity is lower. In this session, most of the Forex currency pairs move in a price range. For this reason, different people use the ups and downs with the trading strategy in the range and get profit.

The low liquidity of the Tokyo session means that trading spreads are also higher during these hours. Besides, most of the transactions of this session are done in the early hours and at the same time as the planned news release.

In the Tokyo or Asia session, the best currency pairs to trade are the "Japanese yen", the "Australian dollar", and the "New Zealand dollar".

"Nikkei" index is also a good option for trading. If you trade in the Tokyo session, you should also be aware of the release of economic news and data from Australian, New Zealand and Japanese financial institutions.

🔵 London trading session (European session)

After the Asian session, it is time for the European session. In this period of time, transactions are very large and many European markets are involved. However, the European session is usually known as the London session.

Because of its specific time zone, London is not only known as the Forex trading center in Europe, but it is also known as the Forex trading center in the world. The London session overlaps with two other major trading sessions in the world, Asia and America. This means that most of the Forex transactions are done in this session. According to the latest statistics, 32% of Forex transactions are related to the London session, which shows that about a third of the activity performed in Forex takes place during this period.

This will increase the volume of Forex transactions and increase liquidity. An event that causes the spread of transactions to decrease. Of course, high liquidity also leads to greater volatility, which is desirable for many traders.

In the European session, the pound and euro currencies and the "DAX", "FTSE100", and "CAC40" indices are known as the best tradable assets. Also, traders of this session should pay attention to the news and data published by the "European Central Bank" and the "Bank of England". The news of countries like Germany, France and Italy are also very important.

🔵 American trading session (New York session)

When the New York session begins, several hours have passed since the end of the Tokyo session, but the European session is in the middle. In this session, they usually affect the financial activities carried out in America, but they also affect other countries such as Canada, Mexico and several South American countries.

The "US dollar" and stock indices such as "S&P", "Dow Jones" and "Nasdaq" are the most important assets that are traded in this session.

The early hours of the American session have a lot of liquidity and volatility due to the overlap with the European session, but with the end of the European session, the activity in the American session also decreases.

You can trade all major Forex currency pairs in the New York trading session. In this session, the "Federal Reserve", as the most important central bank in the world, is the institution that you should pay attention to its news and data.

The trading session indicator is an analytical tool in the financial markets that is used to display and analyze specific trading periods during a day. These indicators are generally useful for determining support and resistance levels during any trading session and for detecting different trading patterns.

For example, usually these indicators display the open and close price levels, the highest and lowest prices during a trading session. Also, you may notice various price patterns such as price channels, price phase phases and market trend changes during different trading sessions using these indicators.

🔵 cause of construction

In particular, the session light indicator version is designed and built for those traders who use many different tools on their chart at the same time. These traders can include "Volume Traders", "ICT traders", "Day Traders" and... These individuals can use "Session Lite" without disturbing the display of their other trading tools such as "Order Blocks", "Liquidity", "Zigzag", "FVG" etc.

But in general, there are several reasons for making tools like trading session indicators in financial markets, some of which include the following :

1. Analysis of specific time frames : Some traders and investors like to consider specific time frames for price analysis and review. For example, analyzing price changes during each trading session can help analyze trading patterns and identify trading opportunities.

2. Recognize different price patterns : Different price patterns may be observed during trading sessions. Trading session indicators can help to make better trading decisions by analyzing these patterns and their strengths and weaknesses.

3. Identifying Support and Resistance Levels : These tools may help to identify support and resistance levels during any trading session which can be helpful in deciding whether to enter or exit the market.

🔵 How to use

The Session Lite indicator displays 8 sessions by default. Asia session, Sydney session, Tokyo session, Shanghai session, Europe session, London session, New York session and New York Stock Exchange (NYSE) session are the sessions that are displayed.

You can activate or deactivate the display of each session by using the tick button next to the name of each session.

Two gray vertical dashes are also displayed by default, which indicate the beginning of the European session and the New York session. This feature is available for all sessions, but it is enabled by default only for these two sessions, and you can activate it for the rest of the session. You can enable or disable the display of this line by using the Start Session tick key.

Likewise, the information table is displayed by default, which includes the open or closed information of each session and the start and end times of each session. These timings are based on the UTC time zone.

Accordingly, the schedule of trading sessions is as follows :

Asia session from 23:00 to 06:00

Sydney session from 23:00 to 05:00

Tokyo session from 00:00 to 00:06

Shanghai session from 01:30 to 06:57

European session from 07:00 to 16:30

London session from 08:00 to 16:30

New York session from 13:00 to 22:00

New York Stock Exchange (NYSE) session from 14:30 to T 22:00

Important note : the beginning of the European session coincides with the opening of the Frankfurt market.

🔵 Settings

• In the settings section, there are customization capabilities according to the type of use of each user. The settings related to showing or not showing the box of each session, the start indicator of each session, setting the start and end time of the session and choosing the desired color to display each session are among the things that can be set from this section.

• At the end of the settings, you will see the "Info Table" option; By disabling this option, the "sessions" clock table displayed on the upper right side will be disabled.

Mars Signals - Ultimate Institutional Suite v3.0(Joker)Comprehensive Trading Manual

Mars Signals – Ultimate Institutional Suite v3.0 (Joker)

## Chapter 1 – Philosophy & System Architecture

This script is not a simple “buy/sell” indicator.

Mars Signals – UIS v3.0 (Joker) is designed as an institutional-style analytical assistant that layers several methodologies into a single, coherent framework.

The system is built on four core pillars:

1. Smart Money Concepts (SMC)

- Detection of Order Blocks (professional demand/supply zones).

- Detection of Fair Value Gaps (FVGs) (price imbalances).

2. Smart DCA Strategy

- Combination of RSI and Bollinger Bands

- Identifies statistically discounted zones for scaling into spot positions or exiting shorts.

3. Volume Profile (Visible Range Simulation)

- Distribution of volume by price, not by time.

- Identification of POC (Point of Control) and high-/low-volume areas.

4. Wyckoff Helper – Spring

- Detection of bear traps, liquidity grabs, and sharp bullish reversals.

All four pillars feed into a Confluence Engine (Scoring System).

The final output is presented in the Dashboard, with a clear, human-readable signal:

- STRONG LONG 🚀

- WEAK LONG ↗

- NEUTRAL / WAIT

- WEAK SHORT ↘

- STRONG SHORT 🩸

This allows the trader to see *how many* and *which* layers of the system support a bullish or bearish bias at any given time.

## Chapter 2 – Settings Overview

### 2.1 General & Dashboard Group

- Show Dashboard Panel (`show_dash`)

Turns the dashboard table in the corner of the chart ON/OFF.

- Show Signal Recommendation (`show_rec`)

- If enabled, the textual signal (STRONG LONG, WEAK SHORT, etc.) is displayed.

- If disabled, you only see feature status (ON/OFF) and the current price.

- Dashboard Position (`dash_pos`)

Determines where the dashboard appears on the chart:

- `Top Right`

- `Bottom Right`

- `Top Left`

### 2.2 Smart Money (SMC) Group

- Enable SMC Strategy (`show_smc`)

Globally enables or disables the Order Block and FVG logic.

- Order Block Pivot Lookback (`ob_period`)

Main parameter for detecting key pivot highs/lows (swing points).

- Default value: 5

- Concept:

A bar is considered a pivot low if its low is lower than the lows of the previous 5 and the next 5 bars.

Similarly, a pivot high has a high higher than the previous 5 and the next 5 bars.

These pivots are used as anchors for Order Blocks.

- Increasing `ob_period`:

- Fewer levels.

- But levels tend to be more significant and reliable.

- In highly volatile markets (major news, war events, FOMC, etc.),

using values 7–10 is recommended to filter out weak levels.

- Show Fair Value Gaps (`show_fvg`)

Enables/disables the drawing of FVG zones (imbalances).

- Bullish OB Color (`c_ob_bull`)

- Color of Bullish Order Blocks (Demand Zones).

- Default: semi-transparent green (transparency ≈ 80).

- Bearish OB Color (`c_ob_bear`)

- Color of Bearish Order Blocks (Supply Zones).

- Default: semi-transparent red.

- Bullish FVG Color (`c_fvg_bull`)

- Color of Bullish FVG (upward imbalance), typically yellow.

- Bearish FVG Color (`c_fvg_bear`)

- Color of Bearish FVG (downward imbalance), typically purple.

### 2.3 Smart DCA Strategy Group

- Enable DCA Zones (`show_dca`)

Enables the Smart DCA logic and visual labels.

- RSI Length (`rsi_len`)

Lookback period for RSI (default: 14).

- Shorter → more sensitive, more noise.

- Longer → fewer signals, higher reliability.

- Bollinger Bands Length (`bb_len`)

Moving average period for Bollinger Bands (default: 20).

- BB Multiplier (`bb_mult`)

Standard deviation multiplier for Bollinger Bands (default: 2.0).

- For extremely volatile markets, values like 2.5–3.0 can be used so that only extreme deviations trigger a DCA signal.

### 2.4 Volume Profile (Visible Range Sim) Group

- Show Volume Profile (`show_vp`)

Enables the simulated Volume Profile bars on the right side of the chart.

- Volume Lookback Bars (`vp_lookback`)

Number of bars used to compute the Volume Profile (default: 150).

- Higher values → broader historical context, heavier computation.

- Row Count (`vp_rows`)

Number of vertical price segments (rows) to divide the total price range into (default: 30).

- Width (%) (`vp_width`)

Relative width of each volume bar as a percentage.

In the code, bar widths are scaled relative to the row with the maximum volume.

> Technical note: Volume Profile calculations are executed only on the last bar (`barstate.islast`) to keep the script performant even on higher timeframes.

### 2.5 Wyckoff Helper Group

- Show Wyckoff Events (`show_wyc`)

Enables detection and plotting of Wyckoff Spring events.

- Volume MA Length (`vol_ma_len`)

Length of the moving average on volume.

A bar is considered to have Ultra Volume if its volume is more than 2× the volume MA.

## Chapter 3 – Smart Money Strategy (Order Blocks & FVG)

### 3.1 What Is an Order Block?

An Order Block (OB) represents the footprint of large institutional orders:

- Bullish Order Block (Demand Zone)

The last selling region (bearish candle/cluster) before a strong upward move.

- Bearish Order Block (Supply Zone)

The last buying region (bullish candle/cluster) before a strong downward move.

Institutions and large players place heavy orders in these regions. Typical price behavior:

- Price moves away from the zone.

- Later returns to the same zone to fill unfilled orders.

- Then continues the larger trend.

In the script:

- If `pl` (pivot low) forms → a Bullish OB is created.

- If `ph` (pivot high) forms → a Bearish OB is created.

The box is drawn:

- From `bar_index ` to `bar_index`.

- Between `low ` and `high `.

- `extend=extend.right` extends the OB into the future, so it acts as a dynamic support/resistance zone.

- Only the last 4 OB boxes are kept to avoid clutter.

### 3.2 Order Block Color Guide

- Semi-transparent Green (`c_ob_bull`)

- Represents a Bullish Order Block (Demand Zone).

- Interpretation: a price region with a high probability of bullish reaction.

- Semi-transparent Red (`c_ob_bear`)

- Represents a Bearish Order Block (Supply Zone).

- Interpretation: a price region with a high probability of bearish reaction.

Overlap (Multiple OBs in the Same Area)

When two or more Order Blocks overlap:

- The shared area appears visually denser/stronger.

- This suggests higher order density.

- Such zones can be treated as high-priority levels for entries, exits, and stop-loss placement.

### 3.3 Demand/Supply Logic in the Scoring Engine

is_in_demand = low <= ta.lowest(low, 20)

is_in_supply = high >= ta.highest(high, 20)

- If current price is near the lowest lows of the last 20 bars, it is considered in a Demand Zone → positive impact on score.

- If current price is near the highest highs of the last 20 bars, it is considered in a Supply Zone → negative impact on score.

This logic complements Order Blocks and helps the Dashboard distinguish whether:

- Market is currently in a statistically cheap (long-friendly) area, or

- In a statistically expensive (short-friendly) area.

### 3.4 Fair Value Gaps (FVG)

#### Concept

When the market moves aggressively:

- Some price levels are skipped and never traded.

- A gap between wicks/shadows of consecutive candles appears.

- These regions are called Fair Value Gaps (FVGs) or Imbalances.

The market generally “dislikes” imbalance and often:

- Returns to these zones in the future.

- Fills the gap (rebalance).

- Then resumes its dominant direction.

#### Implementation in the Code

Bullish FVG (Yellow)

fvg_bull_cond = show_smc and show_fvg and low > high and close > high

if fvg_bull_cond

box.new(bar_index , high , bar_index, low, ...)

Core condition:

`low > high ` → the current low is above the high of two bars ago; the space between them is an untraded gap.

Bearish FVG (Purple)

fvg_bear_cond = show_smc and show_fvg and high < low and close < low

if fvg_bear_cond

box.new(bar_index , low , bar_index, high, ...)

Core condition:

`high < low ` → the current high is below the low of two bars ago; again a price gap exists.

#### FVG Color Guide

- Transparent Yellow (`c_fvg_bull`) – Bullish FVG

Often acts like a magnet for price:

- Price tends to retrace into this zone,

- Fill the imbalance,

- And then continue higher.

- Transparent Purple (`c_fvg_bear`) – Bearish FVG

Price tends to:

- Retrace upward into the purple area,

- Fill the imbalance,

- And then resume downward movement.

#### Trading with FVGs

- FVGs are *not* standalone entry signals.

They are best used as:

- Targets (take-profit zones), or

- Reaction areas where you expect a pause or reversal.

Examples:

- If you are long, a bearish FVG above is often an excellent take-profit zone.

- If you are short, a bullish FVG below is often a good cover/exit zone.

### 3.5 Core SMC Trading Templates

#### Reversal Long

1. Price trades down into a green Order Block (Demand Zone).

2. A bullish confirmation candle (Close > Open) forms inside or just above the OB.

3. If this zone is close to or aligned with a bullish FVG (yellow), the signal is reinforced.

4. Entry:

- At the close of the confirmation candle, or

- Using a limit order near the upper boundary of the OB.

5. Stop-loss:

- Slightly below the OB.

- If the OB is broken decisively and price consolidates below it, the zone loses validity.

6. Targets:

- The next FVG,

- Or the next red Order Block (Supply Zone) above.

#### Reversal Short

The mirror scenario:

- Price rallies into a red Order Block (Supply).

- A bearish confirmation candle forms (Close < Open).

- FVG/premium structure above can act as a confluence.

- Stop-loss goes above the OB.

- Targets: lower FVGs or subsequent green OBs below.

## Chapter 4 – Smart DCA Strategy (RSI + Bollinger Bands)

### 4.1 Smart DCA Concept

- Classic DCA = buying at fixed time intervals regardless of price.

- Smart DCA = scaling in only when:

- Price is statistically cheaper than usual, and

- The market is in a clear oversold condition.

Code logic:

rsi_val = ta.rsi(close, rsi_len)

= ta.bb(close, bb_len, bb_mult)

dca_buy = show_dca and rsi_val < 30 and close < bb_lower

dca_sell = show_dca and rsi_val > 70 and close > bb_upper

Conditions:

- DCA Buy – Smart Scale-In Zone

- RSI < 30 → oversold.

- Close < lower Bollinger Band → price has broken below its typical volatility envelope.

- DCA Sell – Overbought/Distribution Zone

- RSI > 70 → overbought.

- Close > upper Bollinger Band → price is extended far above the mean.

### 4.2 Visual Representation on the Chart

- Green “DCA” Label Below Candle

- Shape: `labelup`.

- Color: lime background, white text.

- Meaning: statistically attractive level for laddered spot entries or short exits.

- Red “SELL” Label Above Candle

- Warning that the market is in an extended, overbought condition.

- Suitable for profit-taking on longs or considering short entries (with proper confluence and risk management).

- Light Green Background (`bgcolor`)

- When `dca_buy` is true, the candle background turns very light green (high transparency).

- This helps visually identify DCA Zones across the chart at a glance.

### 4.3 Practical Use in Trading

#### Spot Trading

Used to build a better average entry price:

- Every time a DCA label appears, allocate a fixed portion of capital (e.g., 2–5%).

- Combining DCA signals with:

- Green OBs (Demand Zones), and/or

- The Volume Profile POC

makes the zone structurally more important.

#### Futures Trading

- Longs

- Use DCA Buy signals as low-risk zones for opening or adding to longs when:

- Price is inside a green OB, or

- The Dashboard already leans LONG.

- Shorts

- Use DCA Sell signals as:

- Exit zones for longs, or

- Areas to initiate shorts with stops above structural highs.

## Chapter 5 – Volume Profile (Visible Range Simulation)

### 5.1 Concept

Traditional volume (histogram under the chart) shows volume over time.

Volume Profile shows volume by price level:

- At which prices has the highest trading activity occurred?

- Where did buyers and sellers agree the most (High Volume Nodes – HVNs)?

- Where did price move quickly due to low participation (Low Volume Nodes – LVNs)?

### 5.2 Implementation in the Script

Executed only when `show_vp` is enabled and on the last bar:

1. The last `vp_lookback` bars (default 150) are processed.

2. The minimum low and maximum high over this window define the price range.

3. This price range is divided into `vp_rows` segments (e.g., 30 rows).

4. For each row:

- All bars are scanned.

- If the mid-price `(high + low ) / 2` falls inside a row, that bar’s volume is added to the row total.

5. The row with the greatest volume is stored as `max_vol_idx` (the POC row).

6. For each row, a volume box is drawn on the right side of the chart.

### 5.3 Color Scheme

- Semi-transparent Orange

- The row with the maximum volume – the Point of Control (POC).

- Represents the strongest support/resistance level from a volume perspective.

- Semi-transparent Blue

- Other volume rows.

- The taller the bar → the higher the volume → the stronger the interest at that price band.

### 5.4 Trading Applications

- If price is above POC and retraces back into it:

→ POC often acts as support, suitable for long setups.

- If price is below POC and rallies into it:

→ POC often acts as resistance, suitable for short setups or profit-taking.

HVNs (Tall Blue Bars)

- Represent areas of equilibrium where the market has spent time and traded heavily.

- Price tends to consolidate here before choosing a direction.

LVNs (Short or Nearly Empty Bars)

- Represent low participation zones.

- Price often moves quickly through these areas – useful for targeting fast moves.

## Chapter 6 – Wyckoff Helper – Spring

### 6.1 Spring Concept

In the Wyckoff framework:

- A Spring is a false break of support.

- The market briefly trades below a well-defined support level, triggers stop losses,

then sharply reverses upward as institutional buyers absorb liquidity.

This movement:

- Clears out weak hands (retail sellers).

- Provides large players with liquidity to enter long positions.

- Often initiates a new uptrend.

### 6.2 Code Logic

Conditions for a Spring:

1. The current low is lower than the lowest low of the previous 50 bars

→ apparent break of a long-standing support.

2. The bar closes bullish (Close > Open)

→ the breakdown was rejected.

3. Volume is significantly elevated:

→ `volume > 2 × volume_MA` (Ultra Volume).

When all conditions are met and `show_wyc` is enabled:

- A pink diamond is plotted below the bar,

- With the label “Spring” – one of the strongest long signals in this system.

### 6.3 Trading Use

- After a valid Spring, markets frequently enter a meaningful bullish phase.

- The highest quality setups occur when:

- The Spring forms inside a green Order Block, and

- Near or on the Volume Profile POC.

Entries:

- At the close of the Spring bar, or

- On the first pullback into the mid-range of the Spring candle.

Stop-loss:

- Slightly below the Spring’s lowest point (wick low plus a small buffer).

## Chapter 7 – Confluence Engine & Dashboard

### 7.1 Scoring Logic

For each bar, the script:

1. Resets `score` to 0.

2. Adjusts the score based on different signals.

SMC Contribution

if show_smc

if is_in_demand

score += 1

if is_in_supply

score -= 1

- Being in Demand → `+1`

- Being in Supply → `-1`

DCA Contribution

if show_dca

if dca_buy

score += 2

if dca_sell

score -= 2

- DCA Buy → `+2` (strong, statistically driven long signal)

- DCA Sell → `-2`

Wyckoff Spring Contribution

if show_wyc

if wyc_spring

score += 2

- Spring → `+2` (entry of strong money)

### 7.2 Mapping Score to Dashboard Signal

- score ≥ 2 → STRONG LONG 🚀

Multiple bullish conditions aligned.

- score = 1 → WEAK LONG ↗

Some bullish bias, but only one layer clearly positive.

- score = 0 → NEUTRAL / WAIT

Rough balance between buying and selling forces; staying flat is usually preferable.

- score = -1 → WEAK SHORT ↘

Mild bearish bias, suited for cautious or short-term plays.

- score ≤ -2 → STRONG SHORT 🩸

Convergence of several bearish signals.

### 7.3 Dashboard Structure

The dashboard is a two-column table:

- Row 0

- Column 0: `"Mars Signals"` – black background, white text.

- Column 1: `"UIS v3.0"` – black background, yellow text.

- Row 1

- Column 0: `"Price:"` (light grey background).

- Column 1: current closing price (`close`) with a semi-transparent blue background.

- Row 2

- Column 0: `"SMC:"`

- Column 1:

- `"ON"` (green) if `show_smc = true`

- `"OFF"` (grey) otherwise.

- Row 3

- Column 0: `"DCA:"`

- Column 1:

- `"ON"` (green) if `show_dca = true`

- `"OFF"` (grey) otherwise.

- Row 4

- Column 0: `"Signal:"`

- Column 1: signal text (`status_txt`) with background color `status_col`

(green, red, teal, maroon, etc.)

- If `show_rec = false`, these cells are cleared.

## Chapter 8 – Visual Legend (Colors, Shapes & Actions)

For quick reading inside TradingView, the visual elements are described line by line instead of a table.

Chart Element: Green Box

Color / Shape: Transparent green rectangle

Core Meaning: Bullish Order Block (Demand Zone)

Suggested Trader Response: Look for longs, Smart DCA adds, closing or reducing shorts.

Chart Element: Red Box

Color / Shape: Transparent red rectangle

Core Meaning: Bearish Order Block (Supply Zone)

Suggested Trader Response: Look for shorts, or take profit on existing longs.

Chart Element: Yellow Area

Color / Shape: Transparent yellow zone

Core Meaning: Bullish FVG / upside imbalance

Suggested Trader Response: Short take-profit zone or expected rebalance area.

Chart Element: Purple Area

Color / Shape: Transparent purple zone

Core Meaning: Bearish FVG / downside imbalance

Suggested Trader Response: Long take-profit zone or temporary supply region.

Chart Element: Green "DCA" Label

Color / Shape: Green label with white text, plotted below the candle

Core Meaning: Smart ladder-in buy zone, DCA buy opportunity

Suggested Trader Response: Spot DCA entry, partial short exit.

Chart Element: Red "SELL" Label

Color / Shape: Red label with white text, plotted above the candle

Core Meaning: Overbought / distribution zone

Suggested Trader Response: Take profit on longs, consider initiating shorts.

Chart Element: Light Green Background (bgcolor)

Color / Shape: Very transparent light-green background behind bars

Core Meaning: Active DCA Buy zone

Suggested Trader Response: Treat as a discount zone on the chart.

Chart Element: Orange Bar on Right

Color / Shape: Transparent orange horizontal bar in the volume profile

Core Meaning: POC – price with highest traded volume

Suggested Trader Response: Strong support or resistance; key reference level.

Chart Element: Blue Bars on Right

Color / Shape: Transparent blue horizontal bars in the volume profile

Core Meaning: Other volume levels, showing high-volume and low-volume nodes

Suggested Trader Response: Use to identify balance zones (HVN) and fast-move corridors (LVN).

Chart Element: Pink "Spring" Diamond

Color / Shape: Pink diamond with white text below the candle

Core Meaning: Wyckoff Spring – liquidity grab and potential major bullish reversal

Suggested Trader Response: One of the strongest long signals in the suite; look for high-quality long setups with tight risk.

Chart Element: STRONG LONG in Dashboard

Color / Shape: Green background, white text in the Signal row

Core Meaning: Multiple bullish layers in confluence

Suggested Trader Response: Consider initiating or increasing longs with strict risk management.

Chart Element: STRONG SHORT in Dashboard

Color / Shape: Red background, white text in the Signal row

Core Meaning: Multiple bearish layers in confluence

Suggested Trader Response: Consider initiating or increasing shorts with a logical, well-placed stop.

## Chapter 9 – Timeframe-Based Trading Playbook

### 9.1 Timeframe Selection

- Scalping

- Timeframes: 1M, 5M, 15M

- Objective: fast intraday moves (minutes to a few hours).

- Recommendation: focus on SMC + Wyckoff.

Smart DCA on very low timeframes may introduce excessive noise.

- Day Trading

- Timeframes: 15M, 1H, 4H

- Provides a good balance between signal quality and frequency.

- Recommendation: use the full stack – SMC + DCA + Volume Profile + Wyckoff + Dashboard.

- Swing Trading & Position Investing

- Timeframes: Daily, Weekly

- Emphasis on Smart DCA + Volume Profile.

- SMC and Wyckoff are used mainly to fine-tune swing entries within larger trends.

### 9.2 Scenario A – Scalping Long

Example: 5-Minute Chart

1. Price is declining into a green OB (Bullish Demand).

2. A candle with a long lower wick and bullish close (Pin Bar / Rejection) forms inside the OB.

3. A Spring diamond appears below the same candle → very strong confluence.

4. The Dashboard shows at least WEAK LONG ↗, ideally STRONG LONG 🚀.

5. Entry:

- On the close of the confirmation candle, or

- On the first pullback into the mid-range of that candle.

6. Stop-loss:

- Slightly below the OB.

7. Targets:

- Nearby bearish FVG above, and/or

- The next red OB.

### 9.3 Scenario B – Day-Trading Short

Recommended Timeframes: 1H or 4H

1. The market completes a strong impulsive move upward.

2. Price enters a red Order Block (Supply).

3. In the same zone, a purple FVG appears or remains unfilled.

4. On a lower timeframe (e.g., 15M), RSI enters overbought territory and a DCA Sell signal appears.

5. The main timeframe Dashboard (1H) shows WEAK SHORT ↘ or STRONG SHORT 🩸.

Trade Plan

- Open a short near the upper boundary of the red OB.

- Place the stop above the OB or above the last swing high.

- Targets:

- A yellow FVG lower on the chart, and/or

- The next green OB (Demand) below.

### 9.4 Scenario C – Swing / Investment with Smart DCA

Timeframes: Daily / Weekly

1. On the daily or weekly chart, each time a green “DCA” label appears:

- Allocate a fixed fraction of your capital (e.g., 3–5%) to that asset.

2. Check whether this DCA zone aligns with the orange POC of the Volume Profile:

- If yes → the quality of the entry zone is significantly higher.

3. If the DCA signal sits inside a daily green OB, the probability of a medium-term bottom increases.

4. Always build the position laddered, never all-in at a single price.

Exits for investors:

- Near weekly red OBs or large purple FVG zones.

- Ideally via partial profit-taking rather than closing 100% at once.

### 9.5 Case Study 1 – BTCUSDT (15-Minute)

- Context: Price has sold off down towards 65,000 USD.

- A green OB had previously formed at that level.

- Near the lower boundary of this OB, a partially filled yellow FVG is present.

- As price returns to this region, a Spring appears.

- The Dashboard shifts from NEUTRAL / WAIT to WEAK LONG ↗.

Plan

- Enter a long near the OB low.

- Place stop below the Spring low.

- First target: a purple FVG around 66,200.

- Second (optional) target: the first red OB above that level.

### 9.6 Case Study 2 – Meme Coin (PEPE – 4H)

- After a strong pump, price enters a corrective phase.

- On the 4H chart, RSI drops below 30; price breaks below the lower Bollinger Band → a DCA label prints.

- The Volume Profile shows the POC at approximately the same level.

- The Dashboard displays STRONG LONG 🚀.

Plan

- Execute laddered buys in the combined DCA + POC zone.

- Place a protective stop below the last significant swing low.

- Target: an expected 20–30% upside move towards the next red OB or purple FVG.

## Chapter 10 – Risk Management, Psychology & Advanced Tuning

### 10.1 Risk Management

No signal, regardless of its strength, replaces risk control.

Recommendations:

- In futures, do not expose more than 1–3% of account equity to risk per trade.

- Adjust leverage to the volatility of the instrument (lower leverage for highly volatile altcoins).

- Place stop-losses in zones where the idea is clearly invalidated:

- Below/above the relevant Order Block or Spring, not randomly in the middle of the structure.

### 10.2 Market-Specific Parameter Tuning

- Calmer Markets (e.g., major FX pairs)

- `ob_period`: 3–5.

- `bb_mult`: 2.0 is usually sufficient.

- Highly Volatile Markets (Crypto, news-driven assets)

- `ob_period`: 7–10 to highlight only the most robust OBs.

- `bb_mult`: 2.5–3.0 so that only extreme deviations trigger DCA.

- `vol_ma_len`: increase (e.g., to ~30) so that Spring triggers only on truly exceptional

volume spikes.

### 10.3 Trading Psychology

- STRONG LONG 🚀 does not mean “risk-free”.

It means the probability of a successful long, given the model’s logic, is higher than average.

- Treat Mars Signals as a confirmation and context system, not a full replacement for your own decision-making.

- Example of disciplined thinking:

- The Dashboard prints STRONG LONG,

- But price is simultaneously testing a multi-month macro resistance or a major negative news event is imminent,

- In such cases, trade smaller, widen stops appropriately, or skip the trade.

## Chapter 11 – Technical Notes & FAQ

### 11.1 Does the Script Repaint?

- Order Blocks and Springs are based on completed pivot structures and confirmed candles.

- Until a pivot is confirmed, an OB does not exist; after confirmation, behavior is stable under classic SMC assumptions.

- The script is designed to be structurally consistent rather than repainting signals arbitrarily.

### 11.2 Computational Load of Volume Profile

- On the last bar, the script processes up to `vp_lookback` bars × `vp_rows` rows.

- On very low timeframes with heavy zooming, this can become demanding.

- If you experience performance issues:

- Reduce `vp_lookback` or `vp_rows`, or

- Temporarily disable Volume Profile (`show_vp = false`).

### 11.3 Multi-Timeframe Behavior

- This version of the script is not internally multi-timeframe.

All logic (OB, DCA, Spring, Volume Profile) is computed on the active timeframe only.

- Practical workflow:

- Analyze overall structure and key zones on higher timeframes (4H / Daily).

- Use lower timeframes (15M / 1H) with the same tool for timing entries and exits.

## Conclusion

Mars Signals – Ultimate Institutional Suite v3.0 (Joker) is a multi-layer trading framework that unifies:

- Price structure (Order Blocks & FVG),

- Statistical behavior (Smart DCA via RSI + Bollinger),

- Volume distribution by price (Volume Profile with POC, HVN, LVN),

- Liquidity events (Wyckoff Spring),

into a single, coherent system driven by a transparent Confluence Scoring Engine.

The final output is presented in clear, actionable language:

> STRONG LONG / WEAK LONG / NEUTRAL / WEAK SHORT / STRONG SHORT

The system is designed to support professional decision-making, not to replace it.

Used together with strict risk management and disciplined execution,

Mars Signals – UIS v3.0 (Joker) can serve as a central reference manual and operational guide

for your trading workflow, from scalping to swing and investment positioning.

Volume Spikes + Daily VWAP SD BandsVolume Spikes + Daily VWAP SD Bands

This indicator combines volume spike detection to help traders identify potential absorption zones with daily VWAP and standard deviation bands , key price levels, continuation opportunities, and possible institutional bias.

Features:

Volume Spike Detection

Highlights candles with unusually high volume relative to a configurable SMA.

Optional filters:

Local highs/lows only (Only Use Valid Highs & Lows)

Candle shapes: Hammer / Shooter only

Candle color match: bullish spikes on green, bearish on red

Plots small circles above/below bars for bullish and bearish volume spikes.

Alerts available for both bullish and bearish spikes.

Interpretation: Volume spikes at local highs/lows can indicate absorption, where one side absorbs aggressive buying/selling pressure.

Daily VWAP

Calculates volume-weighted average price (VWAP) for the current day.

Optionally shows previous day’s VWAP for reference.

Plot lines are customizable with optional circles on lines for visual clarity.

Labels on the last bar show exact VWAP values.

Institutional Bias Insight: Price above both current and previous VWAPs may indicate bullish positioning; price below both VWAPs may indicate bearish positioning. Many professional traders consider this a clue to institutional bias, but it’s not guaranteed. Always confirm with volume, delta, or orderflow analysis.

Standard Deviation Bands

Optional x1 and x2 SD bands around the daily VWAP.

Visual fill between bands shows price volatility zones.

Can be used to identify potential support/resistance or absorption zones.

Use Case: Price bounces off first SD band may indicate continuation signals, especially when volume spikes occur at those levels.

Customizable Visuals

Colors for bullish and bearish volume spikes

VWAP and SD band colors and thickness

Optional circles and filled bands for better readability

Alerts

Bullish / Bearish Volume Spikes

Supports TradingView alert system for automated notifications

Advanced Use Cases:

Combine with Cumulative Delta or Orderflow tools to confirm true absorption zones.

Identify high-volume rejection candles signaling possible trend continuation.

Use VWAP positioning relative to price to assess potential institutional bias, keeping in mind it is probabilistic, not guaranteed.

Visualize intraday VWAP levels and volatility with SD bands for better trade timing.

Settings: Fully customizable, including volume multiplier, SMA length, session filter, candle shape, color options, and VWAP/SD display preferences.

MarketStructureLibMarketStructure Library

This library extends the "MarketStructure" library by mickes () under the Mozilla Public License 2.0, credited to mickes. It provides functions for detecting and visualizing market structure, including Break of Structure (BOS), Change of Character (CHoCH), Equal High/Low (EQH/EQL), and liquidity zones, with enhancements for improved accuracy and customization.

Functionality

Market Structure Detection: Identifies internal (orderflow) and swing market structures using pivot points, with support for BOS, CHoCH, and EQH/EQL.

Volatility Filter: Only confirms pivots when the ATR exceeds a user-defined threshold, reducing false signals in low-volatility markets.

Trend Strength Metric: Calculates a trend strength score based on pivot frequency and volatility, stored in the Structure type for use in scripts.

Customizable Visualizations: Allows users to configure line styles and colors for BOS and CHoCH, and label sizes for pivots, BOS, CHoCH, and liquidity.

Liquidity Zones: Visualizes liquidity levels with confirmation bars and lookback periods.

Methodology

Pivot Detection: Uses ta.pivothigh and ta.pivotlow with a volatility filter (ATR multiplier) to confirm significant pivots.

Trend Strength: Computes a score as pivotCount / LeftLength * (currentATR / ATR), reflecting trend reliability based on pivot frequency and market volatility.

BOS/CHoCH Logic: Detects BOS when price breaks a pivot in the trend direction, and CHoCH when price reverses against the trend, with labels for "MSF" or "MSF+" based on pivot patterns.

EQH/EQL Zones: Creates boxes around equal highs/lows within an ATR-based threshold, with optional extension.

Visualization: Draws lines and labels for BOS, CHoCH, and liquidity, with user-defined styles, colors, and sizes.

Usage

Integration: Import into Pine Script indicators (e.g., import Fenomentn/MarketStructure/1) to analyze market structure.

Configuration: Set pivot lengths, volatility threshold, label sizes, and visualization styles via script inputs.

Alerts: Enable alerts for BOS, CHoCH, and EQH/EQL events, triggered on bar close to avoid repainting.

Best Practices: Use on forex or crypto charts (1m to 12h timeframes) for optimal results. Adjust the volatility threshold for different market conditions.

Originality

This library builds on mickes’ framework by adding:

A volatility-based pivot filter to enhance signal accuracy.

A trend strength metric for assessing trend reliability.

Dynamic label sizing and customizable visualization styles for better usability. No additional open-source code was reused beyond mickes’ library, credited under MPL 2.0.

Developed by Fenomentn. Published under Mozilla Public License 2.0.

Currency Futures StatisticsThe "Currency Futures Statistics" indicator provides comprehensive insights into the performance and characteristics of various currency futures. This indicator is crucial for portfolio management as it combines multiple metrics that are instrumental in evaluating currency futures' risk and return profiles.

Metrics Included:

Historical Volatility:

Definition: Historical volatility measures the standard deviation of returns over a specified period, scaled to an annual basis.

Importance: High volatility indicates greater price fluctuations, which translates to higher risk. Investors and portfolio managers use volatility to gauge the stability of a currency future and to make informed decisions about risk management and position sizing (Hull, J. C. (2017). Options, Futures, and Other Derivatives).

Open Interest:

Definition: Open interest represents the total number of outstanding futures contracts that are held by market participants.

Importance: High open interest often signifies liquidity in the market, meaning that entering and exiting positions is less likely to impact the price significantly. It also reflects market sentiment and the degree of participation in the futures market (Black, F., & Scholes, M. (1973). The Pricing of Options and Corporate Liabilities).

Year-over-Year (YoY) Performance:

Definition: YoY performance calculates the percentage change in the futures contract's price compared to the same week from the previous year.

Importance: This metric provides insight into the long-term trend and relative performance of a currency future. Positive YoY performance suggests strengthening trends, while negative values indicate weakening trends (Fama, E. F. (1991). Efficient Capital Markets: II).

200-Day Simple Moving Average (SMA) Position:

Definition: This metric indicates whether the current price of the currency future is above or below its 200-day simple moving average.

Importance: The 200-day SMA is a widely used trend indicator. If the price is above the SMA, it suggests a bullish trend, while being below indicates a bearish trend. This information is vital for trend-following strategies and can help in making buy or sell decisions (Bollinger, J. (2001). Bollinger on Bollinger Bands).

Why These Metrics are Important for Portfolio Management:

Risk Assessment: Historical volatility and open interest provide essential information for assessing the risk associated with currency futures. Understanding the volatility helps in estimating potential price swings, which is crucial for managing risk and setting appropriate stop-loss levels.

Liquidity and Market Participation: Open interest is a critical indicator of market liquidity. Higher open interest usually means tighter bid-ask spreads and better liquidity, which facilitates smoother trading and better execution of trades.

Trend Analysis: YoY performance and the SMA position help in analyzing long-term trends. This analysis is crucial for making strategic investment decisions and adjusting the portfolio based on changing market conditions.

Informed Decision-Making: Combining these metrics allows for a holistic view of the currency futures market. This comprehensive view helps in making informed decisions, balancing risks and returns, and optimizing the portfolio to align with investment goals.

In summary, the "Currency Futures Statistics" indicator equips investors and portfolio managers with valuable data points that are essential for effective risk management, liquidity assessment, trend analysis, and overall portfolio optimization.

VAMSI ADVANCE Entry HelperThe "VAMSI Entry Helper" indicator is designed to assist traders in identifying potential entry points in the market by analyzing price equilibrium and liquidity equilibrium using a combination of Relative Strength Index (RSI) and moving averages. Here’s a detailed description of its components and functionality:

Components of the Indicator:

RSI (Relative Strength Index):

RSI Length: This parameter (rsiLengthInput) controls the period over which the RSI is calculated. It is set to 50 by default, but you can adjust it as needed.

RSI Source: The source of the price data for calculating the RSI, which is the closing price by default.

Moving Average (MA):

MA Type: You can choose between Simple Moving Average (SMA) and Exponential Moving Average (EMA) for smoothing the RSI values.

MA Length: This parameter (maLengthInput) controls the period over which the moving average of the RSI is calculated. It is set to 60 by default.

Functionality:

RSI Calculation:

The script calculates the RSI based on the selected source and length. RSI is a momentum oscillator that measures the speed and change of price movements and oscillates between 0 and 100.

The RSI calculation involves computing the average gains and losses over the specified period (rsiLengthInput), and then applying the RSI formula.

Moving Average of RSI:

After calculating the RSI, the indicator computes a moving average of the RSI values using the specified type (SMA or EMA) and length (maLengthInput). This smoothed RSI helps in identifying the equilibrium of liquidity.

Plots:

RSI Plot: The RSI values are plotted on the chart with a purple line (#4B0082), providing a visual representation of price equilibrium.

MA Plot: The moving average of the RSI is plotted with a black line, showing the smoothed trend of the RSI.

Middle Band: A horizontal line at the 50 level is plotted as a reference point, indicating the midpoint of the RSI scale. This can help in identifying overbought and oversold conditions.

Use Case:

Price Equilibrium: The RSI plot helps traders identify when the price is relatively strong or weak. RSI values above 70 may indicate an overbought condition, while values below 30 may indicate an oversold condition.

Liquidity Equilibrium: The moving average of the RSI provides a smoothed view of the RSI, helping traders see the overall trend of liquidity equilibrium.

Example Usage:

Entry Points: Traders might look for entry points when the RSI crosses above or below its moving average, indicating potential changes in momentum.

Overbought/Oversold Conditions: Traders can use the RSI values along with the middle band (50) to identify overbought (RSI > 70) and oversold (RSI < 30) conditions.

Customization:

RSI Length: Adjustable to fit different trading strategies and timeframes.

Source: You can change the source data for the RSI calculation (e.g., close, open, high, low).

MA Type and Length: You can choose between SMA and EMA and adjust the period to better fit your trading style.

This indicator provides a comprehensive tool for traders to analyze price and liquidity equilibrium, helping them make informed decisions about entry points in the market.

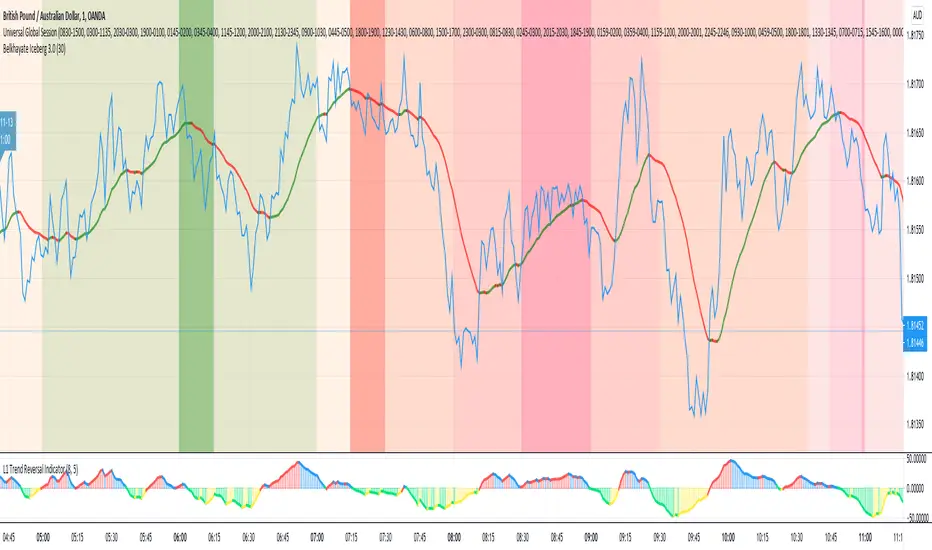

Universal Global SessionUniversal Global Session

This Script combines the world sessions of: Stocks, Forex, Bitcoin Kill Zones, strategic points, all configurable, in a single Script, to capitalize the opening and closing times of global exchanges as investment assets, becoming an Universal Global Session .

It is based on the great work of @oscarvs ( BITCOIN KILL ZONES v2 ) and the scripts of @ChrisMoody. Thank you Oscar and Chris for your excellent judgment and great work.

At the end of this writing you can find all the internet references of the extensive documentation that I present here. To maximize your benefits in the use of this Script, I recommend that you read the entire document to create an objective and practical criterion.

All the hours of the different exchanges are presented at GMT -6. In Market24hClock you can adjust it to your preferences.

After a deep investigation I have been able to show that the different world sessions reveal underlying investment cycles, where it is possible to find sustained changes in the nominal behavior of the trend before the passage from one session to another and in the natural overlaps between the sessions. These underlying movements generally occur 15 minutes before the start, close or overlap of the session, when the session properly starts and also 15 minutes after respectively. Therefore, this script is designed to highlight these particular trending behaviors. Try it, discover your own conclusions and let me know in the notes, thank you.

Foreign Exchange Market Hours

It is the schedule by which currency market participants can buy, sell, trade and speculate on currencies all over the world. It is open 24 hours a day during working days and closes on weekends, thanks to the fact that operations are carried out through a network of information systems, instead of physical exchanges that close at a certain time. It opens Monday morning at 8 am local time in Sydney —Australia— (which is equivalent to Sunday night at 7 pm, in New York City —United States—, according to Eastern Standard Time), and It closes at 5pm local time in New York City (which is equivalent to 6am Saturday morning in Sydney).

The Forex market is decentralized and driven by local sessions, where the hours of Forex trading are based on the opening range of each active country, becoming an efficient transfer mechanism for all participants. Four territories in particular stand out: Sydney, Tokyo, London and New York, where the highest volume of operations occurs when the sessions in London and New York overlap. Furthermore, Europe is complemented by major financial centers such as Paris, Frankfurt and Zurich. Each day of forex trading begins with the opening of Australia, then Asia, followed by Europe, and finally North America. As markets in one region close, another opens - or has already opened - and continues to trade in the currency market. The seven most traded currencies in the world are: the US dollar, the euro, the Japanese yen, the British pound, the Australian dollar, the Canadian dollar, and the New Zealand dollar.

Currencies are needed around the world for international trade, this means that operations are not dominated by a single exchange market, but rather involve a global network of brokers from around the world, such as banks, commercial companies, central banks, companies investment management, hedge funds, as well as retail forex brokers and global investors. Because this market operates in multiple time zones, it can be accessed at any time except during the weekend, therefore, there is continuously at least one open market and there are some hours of overlap between the closing of the market of one region and the opening of another. The international scope of currency trading means that there are always traders around the world making and satisfying demands for a particular currency.

The market involves a global network of exchanges and brokers from around the world, although time zones overlap, the generally accepted time zone for each region is as follows:

Sydney 5pm to 2am EST (10pm to 7am UTC)

London 3am to 12 noon EST (8pm to 5pm UTC)

New York 8am to 5pm EST (1pm to 10pm UTC)

Tokyo 7pm to 4am EST (12am to 9am UTC)

Trading Session

A financial asset trading session refers to a period of time that coincides with the daytime trading hours for a given location, it is a business day in the local financial market. This may vary according to the asset class and the country, therefore operators must know the hours of trading sessions for the securities and derivatives in which they are interested in trading. If investors can understand market hours and set proper targets, they will have a much greater chance of making a profit within a workable schedule.

Kill Zones

Kill zones are highly liquid events. Many different market participants often come together and perform around these events. The activity itself can be event-driven (margin calls or option exercise-related activity), portfolio management-driven (asset allocation rebalancing orders and closing buy-in), or institutionally driven (larger players needing liquidity to complete the size) or a combination of any of the three. This intense cross-current of activity at a very specific point in time often occurs near significant technical levels and the established trends emerging from these events often persist until the next Death Zone approaches or enters.

Kill Zones are evolving with time and the course of world history. Since the end of World War II, New York has slowly invaded London's place as the world center for commercial banking. So much so that during the latter part of the 20th century, New York was considered the new center of the financial universe. With the end of the cold war, that leadership appears to have shifted towards Europe and away from the United States. Furthermore, Japan has slowly lost its former dominance in the global economic landscape, while Beijing's has increased dramatically. Only time will tell how these death zones will evolve given the ever-changing political, economic, and socioeconomic influences of each region.

Financial Markets

New York

New York (NYSE Chicago, NASDAQ)

7:30 am - 2:00 pm

It is the second largest currency platform in the world, followed largely by foreign investors as it participates in 90% of all operations, where movements on the New York Stock Exchange (NYSE) can have an immediate effect (powerful) on the dollar, for example, when companies merge and acquisitions are finalized, the dollar can instantly gain or lose value.

A. Complementary Stock Exchanges

Brazil (BOVESPA - Brazilian Stock Exchange)

07:00 am - 02:55 pm

Canada (TSX - Toronto Stock Exchange)

07:30 am - 02:00 pm

New York (NYSE - New York Stock Exchange)

08:30 am - 03:00 pm

B. North American Trading Session

07:00 am - 03:00 pm

(from the beginning of the business day on NYSE and NASDAQ, until the end of the New York session)