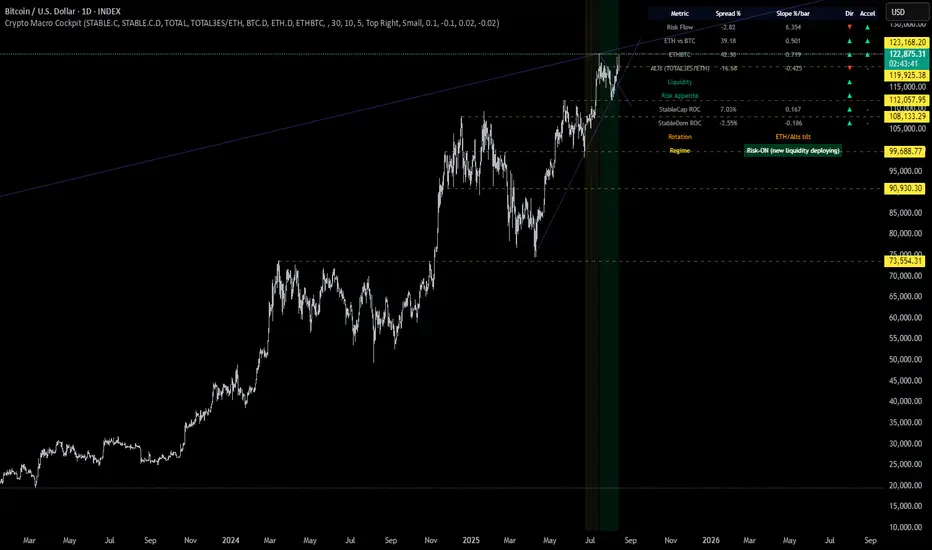

Crypto Macro CockpitCrypto Macro Cockpit — Institutional Liquidity Regime Detection

🔍 Overview

This script introduces a modern macro framework for crypto market regime detection, leveraging newly added stablecoin market data on TradingView. It’s designed to guide traders through the evolving institutional era of crypto — where liquidity, not just price, is king.

🌐 Why This Matters

Historically, traditional proxies like M2 money supply or bond yields were referenced to infer macro liquidity shifts. But with the regulatory green light and institutional embrace of stablecoins, on-chain fiat liquidity is now directly observable.

Stablecoins = The new M2 for crypto.

This script utilizes real-time data from:

📊 CRYPTOCAP:STABLE.C (Total Stablecoin Market Cap)

📊 CRYPTOCAP:STABLE.C.D (Stablecoin Dominance)

to assess dry powder, risk appetite, and macro regime transitions.

📋 How to Read the Crypto Macro Cockpit

This dashboard updates every few bars and is organized into four actionable segments:

1️⃣ Macro Spreads

Metric --> Interpretation

Risk Flow --> Measures capital flow between stablecoins and total crypto market cap. → Green = risk deploying.

ETH vs BTC --> Shift in dominance between ETH and BTC → rotation gauge.

ETHBTC --> Price ratio movement → confirms leadership tilt.

ALTs (TOTAL3ES) --> Momentum in altcoin market, excluding BTC/ETH/stables → key for alt season timing.

2️⃣ Liquidity & Risk Appetite

Metric --> Interpretation

Liquidity --> Directional change in stablecoin cap → more stables = more dry powder.

Risk Appetite --> Inverse of stablecoin dominance → falling dominance = capital rotating into risk.

3️⃣ Stablecoin Context

Metric --> Interpretation

StableCap ROC --> Growth rate of stablecoin market cap → proxy for fiat inflows.

StableDom ROC --> Change in stablecoin dominance → reflects market caution or aggression.

4️⃣ Composite Labels

Label --> Interpretation

Rotation --> Sector tilt (BTC-led vs ETH/Alts)

Regime --> Synthesized macro environment → "Risk-ON", "Caution", "Waiting", or "Risk-OFF"

Background Color --> Optional tint reflecting regime for quick glance validation

All metrics are evaluated with directional arrows (▲/▼/•) and acceleration overlays, using user-defined thresholds scaled by timeframe for precision.

🔔 Built-in Alerts

Predefined, non-repainting alerts include:

Regime transitions

Sector rotations

Confirmed ETH/ALT rotations

Stablecoin market cap spikes

Risk Flow acceleration

You can use these alerts for discretionary trading or automated system triggers.

⚠️ Disclaimer

This script is for educational and informational purposes only. It does not constitute financial advice. Trading cryptocurrencies involves risk, and past performance does not guarantee future results. Always do your own research and manage risk responsibly.

✅ Ready to Use

No configuration needed — just load the script

Works on all timeframes (optimized for 1D)

Thresholds and smoothing are customizable

Table positioning and sizing is user-controlled

If you find this helpful, feel free to ⭐️ favorite or leave feedback. Questions welcome in the comments.

Let’s trade with macro awareness in this new era.

在腳本中搜尋"liquidity"

Fibs Has Lied 🌟 Fibs Has Lied - Indicator Overview 🌟

Designed for indices like US30, NQ, and SPX, this indicator highlights setups where price interacts with key EMA levels during specific trading sessions (default: 6:30–11:30 AM EST).

🌟 Key Features & Levels 🌟

🔹EMA Crossover Setups

The indicator uses the 100-period and 200-period EMAs to identify bullish and bearish setups:

- Bullish Setup: Triggers when the 100 EMA crosses above the 200 EMA, followed by two consecutive candles opening above the 100 EMA, with the low within a specified point distance (e.g., 20 points for US30).

- Bearish Setup: Triggers when the 100 EMA crosses below the 200 EMA, followed by two consecutive candles opening below the 100 EMA, with the high within the point distance.

- Signals are marked with green (buy) or red (sell) triangles and text, ensuring you don’t miss a setup. 📈

🔹 Reset Conditions for Re-Entries

After an initial setup, the indicator watches for “reset” opportunities:

- Buy Reset: If price moves below the 200 EMA after a bullish crossover, then returns with two consecutive candles where lows are above the 100 EMA (within point distance), a new buy signal is plotted.

- Sell Reset: If price moves above the 200 EMA after a bearish crossover, then returns with two consecutive candles where highs are below the 100 EMA (within point distance), a new sell signal is plotted.

This feature captures additional entries after liquidity grabs or fakeouts, aligning with ICT’s manipulation concepts. 🔄

🔹 Session-Based Filtering

Focus your trades during high-liquidity windows! The default session (6:30–11:30 AM EST, New York timezone) targets the London/NY overlap, where price often seeks liquidity or sets up for reversals. Toggle the time filter off for 24/7 signals if desired. 🕒

🔹Symbol-Specific Point Distance

Customizable entry zones based on your chosen index:

- US30: 20 points from the 100 EMA.

- NQ: 3 points from the 100 EMA.

- SPX: 2.5 points from the 100 EMA.

This ensures setups are tailored to the volatility of your market, maximizing relevance. 🎯

🔹 Market Structure Markers (Optional)

Visualize swing points with pivot-based labels:

- HH (Higher High): Signals uptrend continuation.

- HL (Higher Low): Indicates potential bullish support.

- LH (Lower High): Suggests weakening uptrend or reversal.

- LL (Lower Low): Points to downtrend continuation.

- Toggle these on/off to keep your chart clean while analyzing trend direction. 📊

🔹 EMA Visualization

Optionally plot the 100 EMA (blue) and 200 EMA (red) to see key levels where price reacts. These act as dynamic support/resistance, perfect for spotting liquidity pools or ICT’s Power of 3 setups. ⚖️

🌟 Customization Options 🌟

- Symbol Selection: Choose US30, NQ, or SPX to adjust point distance for entries.

- Time Filter: Enable/disable the 6:30–11:30 AM EST session to focus on high-liquidity periods.

- EMA Display: Toggle 100/200 EMAs on/off to reduce chart clutter.

- Market Structure: Show/hide HH/HL/LH/LL labels for cleaner analysis.

- Signal Markers: Green (buy) and red (sell) triangles with text are auto-plotted for easy identification.

🌟 Usage Tips 🌟

- Best Timeframes: Use on 3m for intraday scalping and 30m for swing trades.

- Combine with ICT Tools: Pair with order blocks, fair value gaps, or kill zones for stronger setups.

- Focus on Session: The default 6:30–11:30 AM EST session captures London/NY volatility—perfect for liquidity-driven moves.

- Avoid Overcrowding: Disable market structure or EMAs if you only want setup signals.

Multi-Timeframe SFP + SMTImportant: Please Read First

This indicator is not a "one size fits all" solution. It is a professional and complex tool that requires you to learn how to use it, in addition to backtesting different settings to discover what works best for your specific trading style and the assets you trade. The default settings provided are my personal preferences for trading higher-timeframe setups, but you are encouraged to experiment and find your own optimal configuration.

Please note that while this initial version is solid, it may still contain small errors or bugs. I will be actively working on improving the indicator over time. Also, be aware that the script is not written for maximum efficiency and may be resource-intensive, but this should not pose a problem for most users.

The source code for this indicator is open. If you truly want to understand precisely how all the logic works, you can copy and paste the code into an AI assistant like Gemini or ChatGPT and ask it to explain any part of the script to you.

Author's Preferred Settings (Guideline)

As a starting point, here are the settings I personally use for my trading:

SFP Timeframe: 4-Hour (Strength: 5-5)

Max Lookback: 35 Bars

Raid Expiration: 1 Bar

SFP Lines Limit: 1

SMT Timeframe 1: 30-Minute (Strength: 2-2) with 3-Minute LTF Detection.

SMT Timeframe 2: 15-Minute (Strength: 3-3) with 3-Minute LTF Detection.

SMT Timeframe 3: 1-Hour (Strength: 1-1) with 3-Minute LTF Detection.

SMT Timeframe 4: 15-Minute (Strength: 1-1) with 3-Minute LTF Detection.

Multi-Timeframe SMT: An Overview

This indicator is a powerful tool designed to identify high-probability trading setups by combining two key institutional concepts: Swing Failure Patterns (SFP) on a higher timeframe and Smart Money Technique (SMT) divergences on a lower timeframe. A key feature is the ability to configure and run up to four independent SMT analyses simultaneously, allowing you to monitor for divergences across multiple timeframes (e.g., 15m, 1H, 4H) from a single indicator.

Its primary purpose is to generate automated signals through TradingView's alert system. By setting up alerts, the script runs server-side, monitoring the market for you. When a setup presents itself, it will send a push notification to your device, allowing you to personally evaluate the trade without being tied to your screen.

The Strategy: HTF Liquidity Sweeps into LTF SMT

The core strategy is built on a classic institutional trading model:

Wait for a liquidity sweep on a significant high timeframe (e.g., 4-hour, Daily).

Once liquidity is taken, look for a confirmation of a shift in market structure on a lower timeframe.

This indicator uses an SMT divergence as that confirmation signal, indicating that smart money may be stepping in to reverse the price.

How It Works: The Two-Step Process

The indicator's logic follows a precise two-step process to generate a signal:

Step 1: The Swing Failure Pattern (SFP)

First, the indicator identifies a high-timeframe liquidity sweep. This is configured in the "Swing Failure Pattern (SFP) Timeframe" settings.

It looks for a candle that wicks above a previous high (or below a previous low) but then closes back within the range of that pivot. This action is known as a "raid" or a "swing failure," suggesting the move failed to find genuine momentum.

Step 2: The SMT Divergence

The moment a valid SFP is confirmed, the indicator's multiple SMT engines activate.

Each engine begins monitoring the specific SMT timeframe you have configured (e.g., "SMT Timeframe 1," "SMT Timeframe 2," etc.) for a Smart Money Technique (SMT) divergence.

An SMT divergence occurs when two closely correlated assets fail to move in sync. For example, after a raid on a high, Asset A makes a new high, but Asset B fails to do so. This disagreement suggests weakness and a potential reversal.

When the script finds this divergence, it plots the SMT line and triggers an alert.

The Power of Alerts

The true strength of this indicator lies in its alert capabilities. You can create alerts for both unconfirmed and confirmed SMTs.

Enable Alerts LTF Detection: These alerts trigger when an unconfirmed, potential SMT is spotted on the lower "LTF Detection" timeframe. While not yet confirmed, these early alerts can notify you of a potential move before it fully happens, allowing you to be ahead of the curve and find the best possible trade entries.

Enable Alerts Confirmed SMT: These alerts trigger only when a permanent, confirmed SMT line is plotted on your chosen SMT timeframe. These signals are more reliable but occur later than the early detection alerts.

Key Concepts Explained

What is Pivot Strength?

Pivot Strength determines how significant a high or low needs to be to qualify as a valid structural point. A setting of 5-5, for example, means that for a candle's high to be considered a valid pivot high, its high must be higher than the highs of the 5 candles to its left and the 5 candles to its right.

Higher Strength (e.g., 5-5, 8-8): Creates fewer, but more significant, pivots. This is ideal for identifying major structural highs and lows on higher timeframes.

Lower Strength (e.g., 2-2, 3-3): Creates more pivots, making it suitable for identifying the smaller shifts in momentum on lower timeframes.

Raid Expiration & Validity

An SFP signal is not valid forever. The "Raid Expiration" setting determines how many SFP timeframe bars can pass after a raid before that signal is considered "stale" and can no longer be used to validate an SMT. This ensures your SMT divergences are always in response to recent liquidity sweeps.

Why You Must Be on the Right Chart Timeframe to See SMT Lines

Pine Script™ has a fundamental rule: an indicator running on a chart can only "see" the bars of that chart's timeframe or higher.

When the SMT logic is set to the 15-minute timeframe, it calculates its pivots based on 15-minute data. To accurately plot lines connecting these pivots, you must be on a 15-minute chart or lower (e.g., 5-minute, 1-minute).

If you are on a higher timeframe chart, like the 1-hour, the 15-minute bars do not exist on that chart, so the indicator has no bars to draw the lines on.

This is precisely why the alert system is so powerful. You can set your alert to run on the 15-minute timeframe, and TradingView's servers will monitor that timeframe for you, sending a notification regardless of what chart you are currently viewing.

Mig Trade Model - Kill Zones

Key features:

Liquidity Hunt Detection: Spots aggressive moves that "hunt" stops beyond recent swing highs/lows.

Consolidation Filter: Requires 1-3 small-range candles after a hunt before confirming with a strong candle.

Bias Application: Uses daily open/close to auto-detect bias or allows manual override.

Kill Zone Restriction: Limits signals to London (default: 7-10 AM UTC) and NY (default: 12-3 PM UTC) sessions for better relevance in active markets.

This strategy is inspired by smart money concepts (SMC) and ICT (Inner Circle Trader) methodologies, aiming to capture venom-like "stings" in price action where liquidity is grabbed before reversals.

How It Works

ATR Calculation: Uses a user-defined ATR length (default: 14) to measure volatility, which scales candle body and range thresholds.

Bias Determination:

Auto: Compares daily close to open (bullish if close > open).

Manual: User selects "Bullish" or "Bearish."

Strong Candles:

Bullish: Green candle with body > 2x ATR (configurable).

Bearish: Red candle with body > 2x ATR.

Small Range Candles:

Candles where high-low < 0.5x ATR (configurable).

Liquidity Hunt:

Bullish Hunt: Strong bearish candle making a new low below the past swing low (default: 10 bars).

Bearish Hunt: Strong bullish candle making a new high above the past swing high.

Signal Generation:

After a hunt, counts 1-3 small-range candles.

Confirms with a strong candle in the opposite direction (e.g., strong bullish after bearish hunt).

Resets if >3 small candles or an opposing strong candle appears.

Kill Zone Filter:

Checks if the current bar's time (in UTC) falls within London or NY Kill Zones.

Only allows final "Buy" (bullish entry) or "Sell" (bearish entry) if bias matches and in Kill Zone.

Plots:

Yellow circle (below): Bullish liquidity hunt.

Orange circle (above): Bearish liquidity hunt.

Blue diamond (below): Raw bullish signal.

Purple diamond (above): Raw bearish signal.

Green triangle up ("Buy"): Filtered bullish entry.

Red triangle down ("Sell"): Filtered bearish entry.

Inputs

Bias: "Auto" (default), "Bullish", or "Bearish" – Controls signal direction based on daily trend.

ATR Length: 14 (default) – Period for ATR calculation.

Swing Length for Liquidity Hunt: 10 (default) – Bars to look back for swing highs/lows.

Strong Candle Body Multiplier (x ATR): 2.0 (default) – Threshold for strong candle bodies.

Small Range Multiplier (x ATR): 0.5 (default) – Threshold for small-range candles.

London Kill Zone Start/End Hour (UTC): 7/10 (default) – Customize London session hours.

NY Kill Zone Start/End Hour (UTC): 12/15 (default) – Customize New York session hours.

Usage Tips

Timeframe: Best on lower timeframes (e.g., 5-15 min) for intraday trading, especially forex pairs like EURUSD or GBPUSD.

Timezone Adjustment: Inputs are in UTC. If your chart is in a different timezone (e.g., EST = UTC-5), adjust hours accordingly (e.g., London: 2-5 AM EST → 7-10 UTC).

Risk Management: Use with stop-loss (e.g., beyond the hunt low/high) and take-profit based on ATR multiples. Not financial advice—backtest thoroughly.

Customization: Tweak multipliers for different assets; higher for volatile cryptos, lower for stocks.

Limitations: Relies on historical data; may generate false signals in ranging markets. Combine with other indicators like volume or support/resistance.

This indicator is for educational purposes. Always use discretion and proper risk management in live trading. If you find it useful, feel free to share feedback or suggestions!

FEDFUNDS Rate Divergence Oscillator [BackQuant]FEDFUNDS Rate Divergence Oscillator

1. Concept and Rationale

The United States Federal Funds Rate is the anchor around which global dollar liquidity and risk-free yield expectations revolve. When the Fed hikes, borrowing costs rise, liquidity tightens and most risk assets encounter head-winds. When it cuts, liquidity expands, speculative appetite often recovers. Bitcoin, a 24-hour permissionless asset sometimes described as “digital gold with venture-capital-like convexity,” is particularly sensitive to macro-liquidity swings.

The FED Divergence Oscillator quantifies the behavioural gap between short-term monetary policy (proxied by the effective Fed Funds Rate) and Bitcoin’s own percentage price change. By converting each series into identical rate-of-change units, subtracting them, then optionally smoothing the result, the script produces a single bounded-yet-dynamic line that tells you, at a glance, whether Bitcoin is outperforming or underperforming the policy backdrop—and by how much.

2. Data Pipeline

• Fed Funds Rate – Pulled directly from the FRED database via the ticker “FRED:FEDFUNDS,” sampled at daily frequency to synchronise with crypto closes.

• Bitcoin Price – By default the script forces a daily timeframe so that both series share time alignment, although you can disable that and plot the oscillator on intraday charts if you prefer.

• User Source Flexibility – The BTC series is not hard-wired; you can select any exchange-specific symbol or even swap BTC for another crypto or risk asset whose interaction with the Fed rate you wish to study.

3. Math under the Hood

(1) Rate of Change (ROC) – Both the Fed rate and BTC close are converted to percent return over a user-chosen lookback (default 30 bars). This means a cut from 5.25 percent to 5.00 percent feeds in as –4.76 percent, while a climb from 25 000 to 30 000 USD in BTC over the same window converts to +20 percent.

(2) Divergence Construction – The script subtracts the Fed ROC from the BTC ROC. Positive values show BTC appreciating faster than policy is tightening (or falling slower than the rate is cutting); negative values show the opposite.

(3) Optional Smoothing – Macro series are noisy. Toggle “Apply Smoothing” to calm the line with your preferred moving-average flavour: SMA, EMA, DEMA, TEMA, RMA, WMA or Hull. The default EMA-25 removes day-to-day whips while keeping turning points alive.

(4) Dynamic Colour Mapping – Rather than using a single hue, the oscillator line employs a gradient where deep greens represent strong bullish divergence and dark reds flag sharp bearish divergence. This heat-map approach lets you gauge intensity without squinting at numbers.

(5) Threshold Grid – Five horizontal guides create a structured regime map:

• Lower Extreme (–50 pct) and Upper Extreme (+50 pct) identify panic capitulations and euphoria blow-offs.

• Oversold (–20 pct) and Overbought (+20 pct) act as early warning alarms.

• Zero Line demarcates neutral alignment.

4. Chart Furniture and User Interface

• Oscillator fill with a secondary DEMA-30 “shader” offers depth perception: fat ribbons often precede high-volatility macro shifts.

• Optional bar-colouring paints candles green when the oscillator is above zero and red below, handy for visual correlation.

• Background tints when the line breaches extreme zones, making macro inflection weeks pop out in the replay bar.

• Everything—line width, thresholds, colours—can be customised so the indicator blends into any template.

5. Interpretation Guide

Macro Liquidity Pulse

• When the oscillator spends weeks above +20 while the Fed is still raising rates, Bitcoin is signalling liquidity tolerance or an anticipatory pivot view. That condition often marks the embryonic phase of major bull cycles (e.g., March 2020 rebound).

• Sustained prints below –20 while the Fed is already dovish indicate risk aversion or idiosyncratic crypto stress—think exchange scandals or broad flight to safety.

Regime Transition Signals

• Bullish cross through zero after a long sub-zero stint shows Bitcoin regaining upward escape velocity versus policy.

• Bearish cross under zero during a hiking cycle tells you monetary tightening has finally started to bite.

Momentum Exhaustion and Mean-Reversion

• Touches of +50 (or –50) come rarely; they are statistically stretched events. Fade strategies either taking profits or hedging have historically enjoyed positive expectancy.

• Inside-bar candlestick patterns or lower-timeframe bearish engulfings simultaneously with an extreme overbought print make high-probability short scalp setups, especially near weekly resistance. The same logic mirrors for oversold.

Pair Trading / Relative Value

• Combine the oscillator with spreads like BTC versus Nasdaq 100. When both the FED Divergence oscillator and the BTC–NDQ relative-strength line roll south together, the cross-asset confirmation amplifies conviction in a mean-reversion short.

• Swap BTC for miners, altcoins or high-beta equities to test who is the divergence leader.

Event-Driven Tactics

• FOMC days: plot the oscillator on an hourly chart (disable ‘Force Daily TF’). Watch for micro-structural spikes that resolve in the first hour after the statement; rapid flips across zero can front-run post-FOMC swings.

• CPI and NFP prints: extremes reached into the release often mean positioning is one-sided. A reversion toward neutral in the first 24 hours is common.

6. Alerts Suite

Pre-bundled conditions let you automate workflows:

• Bullish / Bearish zero crosses – queue spot or futures entries.

• Standard OB / OS – notify for first contact with actionable zones.

• Extreme OB / OS – prime time to review hedges, take profits or build contrarian swing positions.

7. Parameter Playground

• Shorten ROC Lookback to 14 for tactical traders; lengthen to 90 for macro investors.

• Raise extreme thresholds (for example ±80) when plotting on altcoins that exhibit higher volatility than BTC.

• Try HMA smoothing for responsive yet smooth curves on intraday charts.

• Colour-blind users can easily swap bull and bear palette selections for preferred contrasts.

8. Limitations and Best Practices

• The Fed Funds series is step-wise; it only changes on meeting days. Rapid BTC oscillations in between may dominate the calculation. Keep that perspective when interpreting very high-frequency signals.

• Divergence does not equal causation. Crypto-native catalysts (ETF approvals, hack headlines) can overwhelm macro links temporarily.

• Use in conjunction with classical confirmation tools—order-flow footprints, market-profile ledges, or simple price action to avoid “pure-indicator” traps.

9. Final Thoughts

The FEDFUNDS Rate Divergence Oscillator distills an entire macro narrative monetary policy versus risk sentiment into a single colourful heartbeat. It will not magically predict every pivot, yet it excels at framing market context, spotting stretches and timing regime changes. Treat it as a strategic compass rather than a tactical sniper scope, combine it with sound risk management and multi-factor confirmation, and you will possess a robust edge anchored in the world’s most influential interest-rate benchmark.

Trade consciously, stay adaptive, and let the policy-price tension guide your roadmap.

Midnight 30min High/LowMidnight 30min High/Low — Overnight Liquidity Range Tracker

Capture the Overnight Session: A Strategic Level Identification Tool from Professional Trading Methodology

This indicator captures the high and low prices during the critical 30-minute midnight session (12:00-12:30 AM EST) and projects these levels forward as key support and resistance zones. These overnight ranges often contain significant liquidity and serve as crucial reference points for intraday price action, representing areas where institutional activity may have established important levels.

🔍 What This Script Does:

Identifies Critical Overnight Session Levels

- Automatically detects the 12:00-12:30 AM EST session window

- Captures the highest and lowest prices during this 30-minute period

- Projects these levels forward for multiple trading days

Creates Dynamic Support/Resistance Zones

- Extends midnight high/low levels as horizontal lines with customizable projection periods

- Fills the area between high and low to create a visual trading range

- Updates automatically each trading day with new overnight levels

Provides Clear Visual Reference Points

- Optional session start markers (●) highlight when the midnight session begins

- Color-coded lines distinguish between high and low levels

- Transparent fill area creates an easy-to-identify trading zone

Real-Time Level Tracking

- Updates levels in real-time during the active midnight session

- Maintains historical levels for reference and backtesting

- Compatible with data window for precise level values

⚙️ Customization Options:

Extend Days (1-30):** Control how many days forward the levels are projected (default: 5 days)

High Line Color:** Customize the midnight high line color (default: blue)

Low Line Color:** Customize the midnight low line color (default: orange)

Fill Color:** Adjust the transparency and color of the range area (default: light aqua, 80% transparency)

Show Session Markers:** Toggle yellow session start indicators on/off (default: enabled)

💡 How to Use:

Deploy on lower timeframes (1m-15m) for precise level identification and reaction monitoring**

Watch for key price interactions:

- Rejection at midnight high levels (potential resistance)

- Bounce from midnight low levels (potential support)

- Range-bound trading between the high and low levels

Combine with liquidity concepts:

- Monitor for stop hunts above/below these levels

- Look for false breakouts that snap back into the range

- Use as confluence with other ICT concepts like FVGs and Order Blocks

Strategic Applications:

- Range trading between midnight levels

- Breakout confirmation when price closes decisively outside the range

- Support/resistance validation for entry and exit planning

🔗 Combine With These Tools for Complete Market Structure Analysis:

✅ First FVG — Opening Range Fair Value Gap Detector.

✅ ICT Turtle Soup (Liquidity Reversal)— Spot stop hunts and false breakout scenarios

✅ ICT Macro Zones (Grey Box Version)- It tracks real-time highs and lows for each Silver Bullet session

✅ ICT SMC Liquidity Grabs and OBs- Liquidity Grabs, Order Block Zones, and Fibonacci OTE Levels, allowing traders to identify institutional entry models with clean, rule-based visual signals.

Together, these tools create a comprehensive Smart Money Concepts (SMC) framework — helping traders identify, anticipate, and capitalize on institutional-level price movements with precision and confidence during critical overnight sessions.

PRO SMC DASHBOARDPRO SMC DASHBOARD - PRO LEVEL

Advanced Supply & Demand / SMC dashboard for scalping and intraday:

Multi-Timeframe Trend: Visualizes trend direction for M1, M5, M15, H1, H4.

HTF Supply/Demand: Shows closest high time frame (HTF) supply/demand zone and distance (in pips).

Smart “Flip” & Liquidity Signals: Flip and Liquidity Sweep arrows/signals are shown only when truly significant:

Near HTF Supply/Demand zone

And confirmed by volume spike or high confluence score

Momentum & Bias: Real-time momentum (RSI M1), H1 bias and fakeout detection.

Confluence Score: Objective score (out of 7) for trade confidence.

Volume Spike, Divergence, BOS: Includes volume spikes, RSI divergence (M1), and Break of Structure (BOS) for both M15 & H1.

Ultra-clean chart: Only valid signals/alerts shown; no spam or visual clutter.

Full dashboard with all signals and context, always visible bottom-right.

Best used for:

Forex, Gold/Silver, US indices, and crypto

Scalping/intraday with fast, clear decisions based on multi-factor SMC logic

Usage:

Add to your chart, monitor the dashboard for valid setups, and trade only when multiple factors align for high-probability entries.

How to Use the PRO SMC DASHBOARD

1. Add the Script to Your Chart:

Apply the indicator to your favorite Forex, Gold, crypto, or indices chart (best on M1, M5, or M15 for entries).

2. Read the Dashboard (Bottom Right):

The dashboard shows real-time information from multiple timeframes and key SMC filters, including:

Trend (M1, M5, M15, H1, H4):

Arrows show up (↑) or down (↓) trend for each timeframe, based on EMA.

Momentum (RSI M1):

Shows “Strong Up,” “Strong Down,” or “Neutral” plus the current RSI value.

RSI (H1):

Higher timeframe momentum confirmation.

ATR State:

Indicates current volatility (High, Normal, Low).

Session:

Detects if the market is in London, NY, or Asia session (based on UTC).

HTF S/D Zone:

Shows the nearest high timeframe Supply or Demand zone, its timeframe (M15, H1, H4), and exact pip distance.

Fakeout (last 3):

Detects recent false breakouts—if there are multiple fakeouts, potential for reversal is higher.

FVG (Fair Value Gap):

Indicates direction and distance to the nearest FVG (Above/Below).

Bias:

“Strong Buy,” “Strong Sell,” or “Neutral”—multi-timeframe, momentum, and volatility filtered.

Inducement:

Alerts for possible “stop hunt” or liquidity grab before reversal.

BOS (Break of Structure):

Recent or live breaks of market structure (for both M15 & H1).

Liquidity Sweep:

Shows if price just swept a key high/low and then reversed (often key reversal point).

Confluence Score (0-7):

Higher score means more factors align—look for 5+ for strong setups.

Volume Spike:

“YES” appears if the current volume is significantly above average—big players are active!

RSI Divergence:

Bullish or bearish divergence on M1—signals early reversal risk.

Momentum Flip:

“UP” or “DN” appears if RSI M1 crosses the 50 line, confirmed by location and other filters.

Chart Signals (Arrows & Markers):

Flip arrows (up/down) and Liquidity markers only appear when price is at/near a key Supply/Demand zone and confirmed by either a volume spike or strong confluence.

No signal spam:

If you see an arrow or LIQ tag, it’s a truly significant moment!

Suggested Trading Workflow:

Scan the Dashboard:

Is the multi-timeframe trend aligned?

Are you near a major Supply or Demand zone?

Is the Confluence Score high (5 or more)?

Check for Signals:

Is there a Flip or LIQ marker near a Supply/Demand zone?

Is volume spiking or a fakeout just occurred?

Look for Reversal or Continuation:

If there’s a Flip at Demand (with high confluence), consider a long setup.

If there’s a LIQ sweep + flip + volume at Supply, consider a short.

Manage Risk:

Don’t chase every signal.

Confirm with your entry criteria and preferred session timing.

Pro Tips:

Highest confidence trades:

When dashboard signals and chart arrows/markers agree, especially with high confluence and volume spike.

Adapt pip distance filter:

Dashboard is tuned for FX and gold; for other assets, adjust pip-size filter if needed.

Use alerts (if enabled):

Set up custom TradingView alerts for “Flip” or “Liquidity” signals for auto-notifications.

Designed to help you make professional, objective decisions—without chart clutter or second-guessing!

CandelaCharts - HTF Sweeps📝 Overview

This indicator lets you overlay a higher timeframe (HTF) onto your current chart, giving you a clearer view of broader market movements without switching timeframes.

This indicator also detects liquidity sweeps and plots them on both the higher timeframe (HTF) and the current lower timeframe (LTF), helping traders clearly spot potential reversal points. It adds LTF dividers for better structure clarity, making it easier to align with HTF shifts and refine entry timing with greater precision.

📦 Features

This indicator identifies price sweeps and their invalidations, helping traders spot potential liquidity grabs and failed breakout attempts.

Overlay a configurable higher timeframe (HTF) on the current chart

Detects and plots liquidity sweeps on both HTF and LTF

Adds lower timeframe (LTF) dividers for improved structure clarity

Ideal for ICT-style top-down analysis and precision entries without switching charts

⚙️ Settings

Customize the indicator to suit your strategy. Alert options are also available, so you can stay informed when key market events are triggered.

Timeframes: Select the higher timeframe (HTF) to overlay on your current chart.

HTF Coloring: Customize the color scheme for HTF candles.

HTF Offset: Space of HTF Candles and current chart.

HTF Size: Adjust the size of HTF candles.

HTF Labels: Toggle labels for HTF.

LTF H/L Line: Show or hide high/low lines from the lower timeframe.

LTF O/C Line: Display open/close lines from the lower timeframe.

Sweep: Enable detection and plotting of liquidity sweeps.

I-sweep: Toggle invalidated sweep detection.

Alerts: Enable Sweep Formation or Invalidation alerts

⚡️ Showcase

See the indicator applied in live market scenarios, illustrating how sweep detections and invalidations unfold on various charts.

HTF Candles

HTF Sweeps

LTF Sweeps

Invalidated Sweeps

🚨 Alerts

This indicator includes built-in alert functionality to keep you informed of key market events in real time. It supports the following customizable alerts on TradingView:

Sweep Detection: Notifies you when a price sweep is detected—either a liquidity sweep above recent highs or below recent lows. This can be a strong signal of potential reversals or liquidity grabs by larger market participants.

Sweep Invalidation: Alerts you when a previously detected sweep becomes invalidated due to price action moving beyond a defined threshold. This helps traders stay adaptive and avoid acting on outdated signals.

These alerts are fully integrated with TradingView’s native alert system, so you can receive notifications via app, email, or pop-up—ensuring you're always up to date, even when you're away from the chart.

⚠️ Disclaimer

Trading involves significant risk, and many participants may incur losses. The content on this site is not intended as financial advice and should not be interpreted as such. Decisions to buy, sell, hold, or trade securities, commodities, or other financial instruments carry inherent risks and are best made with guidance from qualified financial professionals. Past performance is not indicative of future results.

[Mustang Algo] Channel Strategy# Mustang Algo Channel Strategy - Universal Market Sentiment Oscillator

## 🎯 ORIGINAL CONCEPT

This strategy employs a unique market sentiment oscillator that works on ALL financial assets. It uses Bitcoin supply dynamics combined with stablecoin market capitalization as a macro sentiment indicator to generate universal timing signals across stocks, forex, commodities, indices, and cryptocurrencies.

## 🌐 UNIVERSAL APPLICATION

- **Any Asset Class:** Stocks, Forex, Commodities, Indices, Crypto, Bonds

- **Market-Wide Timing:** BTC/Stablecoin ratio serves as a global risk sentiment gauge

- **Cross-Market Signals:** Trade any instrument using macro liquidity conditions

- **Ecosystem Approach:** One oscillator for all financial markets

## 🧮 METHODOLOGY

**Core Calculation:** BTC Supply / (Combined Stablecoin Market Cap / BTC Price)

- **Data Sources:** DAI + USDT + USDC market capitalizations

- **Signal Generation:** RSI(14) applied to the ratio, double-smoothed with WMA

- **Timing Logic:** Crossover signals filtered by overbought/oversold zones

- **Multi-Timeframe:** Configurable timeframe analysis (default: Daily)

## 📈 TRADING STRATEGY

**LONG Entries:** Bullish crossover when market sentiment is oversold (<48)

**SHORT Entries:** Bearish crossover when market sentiment is overbought (>55)

**Universal Timing:** These macro signals apply to trading any financial instrument

## ⚙️ FLEXIBLE RISK MANAGEMENT

**Three SL/TP Calculation Modes:**

- **Percentage Mode:** Traditional % based (4% SL, 12% TP default)

- **Ticks Mode:** Precise tick-based calculation (50/150 ticks default)

- **Pips Mode:** Forex-style pip calculation (50/150 pips default)

**Realistic Parameters:**

- Commission: 0.1% (adjustable for different asset classes)

- Slippage: 2 ticks

- Position sizing: 10% of equity (conservative)

- No pyramiding (single position management)

## 📊 KEY ADVANTAGES

✅ **Universal Application:** One strategy for all asset classes

✅ **Macro Foundation:** Based on global liquidity and risk sentiment

✅ **False Signal Filtering:** Overbought/oversold zones reduce noise

✅ **Flexible Risk Management:** Multiple SL/TP calculation methods

✅ **No Lookahead Bias:** Clean backtesting with realistic results

✅ **Cross-Market Correlation:** Captures broad market risk cycles

## 🎛️ CONFIGURATION GUIDE

1. **Asset Selection:** Apply to stocks, forex, commodities, indices, crypto

2. **Timeframe Setup:** Daily recommended for swing trading

3. **Sentiment Bounds:** Adjust 48/55 levels based on market volatility

4. **Risk Management:** Choose appropriate SL/TP mode for your asset class

5. **Direction Filter:** Select Long Only, Short Only, or Both

## 📋 BACKTESTING STANDARDS

**Compliant with TradingView Guidelines:**

- ✅ Realistic commission structure (0.1% default)

- ✅ Appropriate slippage modeling (2 ticks)

- ✅ Conservative position sizing (10% equity)

- ✅ Sustainable risk ratios (1:3 SL/TP)

- ✅ No lookahead bias (proper historical simulation)

- ✅ Sufficient sample size potential (100+ trades possible)

## 🔬 ORIGINAL RESEARCH

This strategy introduces a revolutionary approach to financial markets by treating the BTC/Stablecoin ratio as a global risk sentiment gauge. Unlike traditional indicators that analyze individual asset price action, this oscillator captures macro liquidity flows that affect ALL financial markets - from stocks to forex to commodities.

## 🎯 MARKET APPLICATIONS

**Stocks & Indices:** Risk-on/risk-off sentiment timing

**Forex:** Global liquidity flow analysis for major pairs

**Commodities:** Risk appetite for inflation hedges

**Bonds:** Flight-to-safety vs. risk-seeking behavior

**Crypto:** Native application with direct correlation

## ⚠️ RISK DISCLOSURE

- Designed for intermediate to long-term trading across all timeframes

- Market sentiment can remain extreme longer than expected

- Always use appropriate position sizing for your specific asset class

- Adjust commission and slippage settings for different markets

- Past performance does not guarantee future results

## 🚀 INNOVATION SUMMARY

**What makes this strategy unique:**

- First to use BTC/Stablecoin ratio as universal market sentiment indicator

- Applies macro-economic principles to technical analysis across all assets

- Single oscillator provides timing signals for entire financial ecosystem

- Bridges traditional finance with digital asset insights

- Combines fundamental liquidity analysis with technical precision

Sniper SweepsPurpose

Detect when price sweeps above recent highs (buy-side liquidity) or below recent lows (sell-side liquidity), but closes back inside the range. This is often interpreted as a stop-hunt or liquidity grab by institutional traders.

Core Concepts

Liquidity Sweep: When price briefly breaks a recent swing high/low (potentially triggering stop losses), but then closes back within the previous range.

Buy-side Sweep: Price breaks a previous high, but closes below it.

Sell-side Sweep: Price breaks a previous low, but closes above it.

Summary

This indicator is useful for:

Identifying potential stop-hunts or liquidity grabs.

Recognizing SMC trade setups around swept highs/lows.

Getting alerted when significant liquidity levels are manipulated.

CRT Finder (WanHakimFX)📈 Liquidity Grab Indicator with MTF Confluence & Alerts

🔍 Overview:

The Liquidity Grab Indicator is designed to detect precise moments when price sweeps liquidity — either by wicking below recent lows (bullish LQH) or above recent highs (bearish LQL) — followed by a clear rejection. It combines this logic with multi-timeframe confirmation and trend filters, making it a powerful tool for identifying high-probability reversal setups.

⚙️ How It Works:

✅ Liquidity Sweep Logic (LQH / LQL)

Bullish (LQH):

Current candle wicks below the previous low

Closes above the previous candle body

Confirms potential bullish reversal

Bearish (LQL):

Current candle wicks above the previous high

Closes below the previous candle body

Confirms potential bearish reversal

✅ Additional Conditions:

Must occur during London or New York sessions.

Requires trend confluence:

LQH = Price must be above SMMA 60/100/200

LQL = Price must be below SMMA 60/100/200

🧠 Multi-Timeframe Confluence:

The indicator scans for LQH/LQL sweeps across:

Daily

4H

1H

30M

15M

If a sweep occurs on any of these timeframes, an alert is triggered and a triangle marker appears on the chart for real-time visual confluence.

📊 Visual Features:

Green/Red labels for active timeframe sweeps.

Dotted wick lines to show liquidity zones from the previous candle.

Colored triangle markers for MTF sweep alerts.

🛠 Strategy Usage:

This indicator is best used as a trigger tool in a confluence-based strategy:

Use higher-timeframe MTF LQH/LQL markers for directional bias.

Wait for matching sweep on your entry timeframe (e.g., M1/M5).

Enter on confirmation candle or break of structure.

Target imbalances, FVGs, or previous highs/lows.

Risk-managed entries using sweep candle's high/low as stop.

📢 Alerts:

✅ Bullish Sweep (LQH) on any timeframe

✅ Bearish Sweep (LQL) on any timeframe

Equal High/Low (EQH/EQL) [AlgoAlpha]OVERVIEW

This script detects and visualizes Equal High (EQH) and Equal Low (EQL) zones—key liquidity areas where price has previously stalled or reversed. These levels often attract institutional interest due to the liquidity buildup around them. The indicator is built to highlight such zones using dynamic thresholding, overbought/oversold RSI filtering, and adaptive mitigation logic to manage zone relevance over time.

CONCEPTS

Equal Highs/Lows are price points where the market has repeatedly failed to break past a certain high or low, hinting at areas where stop orders and pending interest may be concentrated. These areas are often prime targets for liquidity grabs or reversals. By combining this with RSI filtering, the script avoids false signals during neutral conditions and instead focuses on zones where market pressure is more directional.

FEATURES

Detection Logic: The script identifies EQH and EQL zones by comparing the similarity between recent highs or lows with a dynamic volatility threshold. The `tolerance` input allows users to control how strict this comparison is.

RSI Filtering: If enabled, it only creates zones when RSI is significantly overbought or oversold (based on the `state_thresh` input). This helps ensure zones form only in meaningful market conditions.

Zone Display: Bullish (EQL) zones are shown in grey, while bearish (EQH) zones are in blue. Two horizontal lines mark the zone using wick and body extremes, and a filled area visualizes the zone between them.

Zone Management: Zones automatically extend with price until they’re invalidated. You can choose whether a zone is removed based on wick or body sweeps and whether it requires one or two candle confirmations. Zones also expire after a customizable number of bars.

Alerts: Four alert conditions are built in—when a new EQH/EQL is formed and when one is mitigated—making it easy to integrate into alert-based workflows.

USAGE

Equal highs/lows can be used as liquidity markers, either as entry points or as take-profit targets.

This tool is ideal for liquidity-based strategies and helps traders map out possible reversal or sweep zones that often precede aggressive moves.

Time-Based Fair Value Gaps (FVG) with Inversions (iFVG)Overview

The Time-Based Fair Value Gaps (FVG) with Inversions (iFVG) (ICT/SMT) indicator is a specialized tool designed for traders using Inner Circle Trader (ICT) methodologies. Inspired by LuxAlgo's Fair Value Gap indicator, this script introduces significant enhancements by integrating ICT principles, focusing on precise time-based FVG detection, inversion tracking, and retest signals tailored for institutional trading strategies. Unlike LuxAlgo’s general FVG approach, this indicator filters FVGs within customizable 10-minute windows aligned with ICT’s macro timeframes and incorporates ICT-specific concepts like mitigation, liquidity grabs, and session-based gap prioritization.

This tool is optimized for 1–5 minute charts, though probably best for 1 minute charts, identifying bullish and bearish FVGs, tracking their mitigation into inverted FVGs (iFVGs) as key support/resistance zones, and generating retest signals with customizable “Close” or “Wick” confirmation. Features like ATR-based filtering, optional FVG labels, mitigation removal, and session-specific FVG detection (e.g., first FVG in AM/PM sessions) make it a powerful tool for ICT traders.

Originality and Improvements

While inspired by LuxAlgo’s FVG indicator (credit to LuxAlgo for their foundational work), this script significantly extends the original concept by:

1. Time-Based FVG Detection: Unlike LuxAlgo’s continuous FVG identification, this script filters FVGs within user-defined 10-minute windows each hour (:00–:10, :10–:20, etc.), aligning with ICT’s emphasis on specific periods of institutional activity, such as hourly opens/closes or kill zones (e.g., New York 7:00–11:00 AM EST). This ensures FVGs are relevant to high-probability ICT setups.

2. Session-Specific First FVG Option: A unique feature allows traders to display only the first FVG in ICT-defined AM (9:30–10:00 AM EST) or PM (1:30–2:00 PM EST) sessions, reflecting ICT’s focus on initial market imbalances during key liquidity events.

3. ICT-Driven Mitigation and Inversion Logic: The script tracks FVG mitigation (when price closes through a gap) and converts mitigated FVGs into iFVGs, which serve as ICT-style support/resistance zones. This aligns with ICT’s view that mitigated gaps become critical reversal points, unlike LuxAlgo’s simpler gap display.

4. Customizable Retest Signals: Retest signals for iFVGs are configurable for “Close” (conservative, requiring candle body confirmation) or “Wick” (faster, using highs/lows), catering to ICT traders’ need for precise entry timing during liquidity grabs or Judas swings.

5. ATR Filtering and Mitigation Removal: An optional ATR filter ensures only significant FVGs are displayed, reducing noise, while mitigation removal declutters the chart by removing filled gaps, aligning with ICT’s principle that mitigated gaps lose relevance unless inverted.

6. Timezone and Timeframe Safeguards: A timezone offset setting aligns FVG detection with EST for ICT’s New York-centric strategies, and a timeframe warning alerts users to avoid ≥1-hour charts, ensuring accuracy in time-based filtering.

These enhancements make the script a distinct tool that builds on LuxAlgo’s foundation while offering ICT traders a tailored, high-precision solution.

How It Works

FVG Detection

FVGs are identified when a candle’s low is higher than the high of two candles prior (bullish FVG) or a candle’s high is lower than the low of two candles prior (bearish FVG). Detection is restricted to:

• User-selected 10-minute windows (e.g., :00–:10, :50–:60) to capture ICT-relevant periods like hourly transitions.

• AM/PM session first FVGs (if enabled), focusing on 9:30–10:00 AM or 1:30–2:00 PM EST for key market opens.

An optional ATR filter (default: 0.25× ATR) ensures only gaps larger than the threshold are displayed, prioritizing significant imbalances.

Mitigation and Inversion

When price closes through an FVG (e.g., below a bullish FVG’s bottom), the FVG is mitigated and becomes an iFVG, plotted as a support/resistance zone. iFVGs are critical in ICT for identifying reversal points where institutional orders accumulate.

Retest Signals

The script generates signals when price retests an iFVG:

• Close: Triggers when the candle body confirms the retest (conservative, lower noise).

• Wick: Triggers when the candle’s high/low touches the iFVG (faster, higher sensitivity). Signals are visualized with triangular markers (▲ for bullish, ▼ for bearish) and can trigger alerts.

Visualization

• FVGs: Displayed as colored boxes (green for bullish, red for bearish) with optional “Bull FVG”/“Bear FVG” labels.

• iFVGs: Shown as extended boxes with dashed midlines, limited to the user-defined number of recent zones (default: 5).

• Mitigation Removal: Mitigated FVGs/iFVGs are removed (if enabled) to keep the chart clean.

How to Use

Recommended Settings

• Timeframe: Use 1–5 minute charts for precision, avoiding ≥1-hour timeframes (a warning label appears if misconfigured).

• Time Windows: Enable :00–:10 and :50–:60 for hourly open/close FVGs, or use the “Show only 1st presented FVG” option for AM/PM session focus.

• ATR Filter: Keep enabled (multiplier 0.25–0.5) for significant gaps; disable on 1-minute charts for more FVGs during volatility.

• Signal Preference: Use “Close” for conservative entries, “Wick” for aggressive setups.

• Timezone Offset: Set to -5 for EST (or -4 for EDT) to align with ICT’s New York session.

Trading Strategy

1. Macro Timeframes: Focus on New York (7:00–11:00 AM EST) or London (2:00–5:00 AM EST) kill zones for high institutional activity.

2. FVG Entries: Trade bullish FVGs as support in uptrends or bearish FVGs as resistance in downtrends, especially in :00–:10 or :50–:60 windows.

3. iFVG Retests: Enter on retest signals (▲/▼) during liquidity grabs or Judas swings, using “Close” for confirmation or “Wick” for speed.

4. Session FVGs: Use the “Show only 1st presented FVG” option to target the first gap in AM/PM sessions, often tied to ICT’s market maker algorithms.

5. Risk Management: Combine with ICT concepts like order blocks or breaker blocks for confluence, and set stops beyond FVG/iFVG boundaries.

Alerts

Set alerts for:

• “Bullish FVG Detected”/“Bearish FVG Detected”: New FVGs in selected windows.

• “Bullish Signal”/“Bearish Signal”: iFVG retest confirmations.

Settings Description

• Show Last (1–100, default: 5): Number of recent iFVGs to display. Lower values reduce clutter.

• Show only 1st presented FVG : Limits FVGs to the first in 9:30–10:00 AM or 1:30–2:00 PM EST sessions (overrides time window checkboxes).

• Time Window Checkboxes: Enable/disable FVG detection in 10-minute windows (:00–:10, :10–:20, etc.). All enabled by default.

• Signal Preference: “Close” (default) or “Wick” for iFVG retest signals.

• Use ATR Filter: Enables ATR-based size filtering (default: true).

• ATR Multiplier (0–∞, default: 0.25): Sets FVG size threshold (higher values = larger gaps).

• Remove Mitigated FVGs: Removes filled FVGs/iFVGs (default: true).

• Show FVG Labels: Displays “Bull FVG”/“Bear FVG” labels (default: true).

• Timezone Offset (-12 to 12, default: -5): Aligns time windows with EST.

• Colors: Customize bullish (green), bearish (red), and midline (gray) colors.

Why Use This Indicator?

This indicator empowers ICT traders with a tool that goes beyond generic FVG detection, offering precise, time-filtered gaps and inversion tracking aligned with institutional trading principles. By focusing on ICT’s macro timeframes, session-specific imbalances, and customizable signal logic, it provides a clear edge for scalping, swing trading, or reversal setups in high-liquidity markets.

SMC Entry Signals MTF v2📘 User Guide for the SMC Entry Signals MTF v2 Indicator

🎯 Purpose of the Indicator

This indicator is designed to identify reversal entry points based on Smart Money Concepts (SMC) and candlestick confirmation. It’s especially useful for traders who use:

Imbalance zones, order blocks, breaker blocks

Liquidity grabs

Multi-timeframe confirmation (MTF)

📈 How to Use the Signals on the Chart

✅ LONG Signal (green triangle below the candle):

Conditions:

Price is in a discount zone (below the FIB 50% level)

A bullish engulfing candle appears

A bullish Order Block (OB) or Breaker Block is detected

There’s an upward imbalance

A bullish OB is confirmed on the higher timeframe

➡️ How to act:

Consider entering long on the current or next candle.

Place your stop-loss below the OB or the nearest swing low.

Take profit at the nearest liquidity zone or premium area (above FIB 50%).

🔻 SHORT Signal (red triangle above the candle):

Conditions:

Price is in a premium zone (above FIB 50%)

A bearish engulfing candle appears

A bearish OB or Breaker Block is detected

There’s a downward imbalance

A bearish OB is confirmed on the higher timeframe

➡️ How to act:

Consider short entry after the signal.

Place your stop-loss above the OB or swing high.

Target the discount zone or the next liquidity pocket.

⚙️ Recommended Settings by Trading Style

Trading Style Suggested Settings Notes

Intraday (1–15m) fibLookback = 20–50, obLookback = 5–10, htf_tf = 1H/4H Fast signals. Use Discount/Premium + Engulfing.

Swing/Position (1H–1D) fibLookback = 50–100, obLookback = 10–20, htf_tf = 1D/1W Higher trust in MTF confirmation. Ideal with fundamentals.

Scalping (1m) fibLookback = 10–20, obLookback = 3–5, htf_tf = 15m/1H Remove Breaker and MTF for quick reaction trades.

🧠 Best Practices for Traders

Trend Filtering:

Use EMAs or volume to confirm the current trend.

Take longs only in uptrends, shorts in downtrends.

Liquidity Zones:

Use this indicator after liquidity grabs.

OBs and Breakers often appear right after stop hunts.

Combine with Manual Zones:

This works best when paired with manually drawn OBs and key levels.

Backtest the Signals:

Use Bar Replay mode on TradingView to test past signals.

🧪 Example Trade Setup

Example on BTCUSDT 15m:

Price drops into the discount zone.

A green triangle appears (bullish engulfing + OB + imbalance + HTF OB).

You enter long, stop below the OB, target the premium zone.

🎯 This type of setup often gives a risk/reward ratio of 1:2 or better — profitable even with a 40% win rate.

⏰ Alerts & Automation

Enable alerts:

"SMC Long Entry" — fires when a long signal appears.

"SMC Short Entry" — fires when a short signal appears.

You can integrate this with bots via webhook, like:

TradingConnector, 3Commas, Alertatron, etc.

✅ What This Indicator Gives You

High-probability entries using SMC logic

Customizable filters for entry logic

Multi-timeframe confirmation for stronger setups

Suitable for both intraday and swing trading

PRO SMC Full Suite BY Mashrur“PRO SMC Full Suite BY Mashrur”

A Pine Script (v5) indicator for TradingView, focused on Smart Money Concepts (SMC). It overlays on price charts and provides visual tools for identifying key institutional trading behaviors.

🎯 Purpose

This script is designed to help traders analyze and trade using SMC principles by automatically detecting:

Order Blocks (OBs)

Fair Value Gaps (FVGs)

Breaks of Structure (BoS)

Liquidity Sweeps (Buy/Sell Side Liquidity Grabs)

Mitigation Entries

⚙️ Inputs / Settings

Show Fair Value Gaps: Toggle FVGs on/off

Higher Timeframe (HTF): Choose HTF for OB analysis

Use HTF OBs: Switch between current TF OBs and HTF OBs

Show Order Blocks: Toggle OBs on/off

Show OB Mitigation Entries: Toggle mitigation entry signals on/off

🧠 Core Logic Overview

🔹 1. Swing Points Detection

Identifies swing highs/lows using a 3-bar pattern (pivot-based structure).

🔹 2. Break of Structure (BoS)

A bullish BoS happens when price closes above the last swing high.

A bearish BoS occurs when price closes below the last swing low.

🔹 3. Order Block Detection

Upon BoS, the script marks the previous candle as the Order Block.

Uses either:

Current TF OBs (based on price action)

HTF OBs (based on candle body direction)

🔹 4. Mitigation Entry Logic

A mitigation occurs when price returns to the OB and reacts with confirmation:

Bullish: price dips into OB and closes above

Bearish: price wicks into OB and closes below

Plots entry markers for these mitigations.

🔹 5. Liquidity Sweeps

Detects equal highs/lows (liquidity zones)

Marks Buy SL when price dips below an equal low then closes above

Marks Sell SL when price breaks above an equal high then closes below

🔹 6. Fair Value Gaps (FVGs)

FVG Up: Gap between candle 3 and candle 1 (low > high )

FVG Down: Gap between candle 3 and candle 1 (high < low )

Plots highlighted boxes on these gaps

📊 Visual Elements

Boxes: For OB zones and FVGs

Shapes:

Labels: OB Buy/Sell entries

Triangles: Buy SL / Sell SL liquidity sweeps

Lines: Equal Highs and Lows

🔔 Alerts

Built-in alerts to notify when:

OB entries are confirmed

Liquidity sweeps happen

Helps in automation or active monitoring

✅ Ideal For

Traders using SMC, ICT concepts, Wyckoff, or institutional trading models

Anyone wanting to automate detection of structural elements on their chart

Akkerman IMB + Targets IndicatorAkkerman IMB + Targets Indicator

The Akkerman IMB + Targets Indicator is a powerful tool for traders who use the Smart Money Concept (SMC) methodology for intraday trading. This indicator combines several key elements of technical analysis, such as IMB (Imbalance) zones, liquidity zones, and intraday targets, to help traders identify significant levels on the chart for potential entry and exit points.

Main Features of the Indicator:

IMB (Imbalance) Zones:

The indicator detects IMB zones (imbalances) on the chart, which are often significant for the market because these zones can signal unsupported price moves where the market may either retrace or continue the move.

Green box — indicates a bullish IMB, where the price moves downward but does not reach the previous "low" level.

Red box — indicates a bearish IMB, where the price moves upward but does not reach the previous "high" level.

Liquidity Zones:

The indicator automatically identifies liquidity zones, which are critical levels for potential retracements or breakouts. These zones are determined by equal highs and lows on the chart (where the price has made similar highs or lows).

Triangles or lines highlight levels where significant buy or sell orders might be gathered.

Intraday Target Lines:

The indicator generates targets for intraday trading based on support and resistance levels over the last 10 periods.

These target lines on the chart indicate potential entry or exit points based on the lowest and highest prices over the past 10 bars, which represent key points for trading within the current session.

Indicator Settings:

Show IMB: Toggle to show or hide IMB zones on the chart.

Show Liquidity Zones: Toggle to show or hide liquidity zones on the chart.

Show Targets (Intraday): Toggle to show or hide intraday target lines.

Max Targets (maxTargets): Set the maximum number of targets to display on the chart.

How to Use:

IMB Zones help identify potential retracement or breakout zones on the market. These zones are a critical part of Smart Money analysis, as markets often retrace to these areas after significant price moves.

Liquidity Zones provide clues about where large orders may be gathered, which could lead to a retracement or breakout.

Intraday Targets assist in identifying important levels for entering or exiting trades within the current session to take advantage of short-term price movements.

Important Notes:

This indicator works best on the 1-hour timeframe (H1) for more accurate and stable signals.

For maximum effectiveness, it is recommended to combine this indicator with other technical indicators and analysis methods.

HL2 Moving Average with BandsThis indicator is designed to assist traders in identifying potential trade entries and exits for S&P 500 (ES) and Nasdaq-100 (NQ) futures. It calculates a Simple Moving Average (SMA) based on the HL2 value (average of high and low prices) of the current candle over a user-defined lookback period (default: 200 periods). The indicator plots this SMA as a blue line, providing a smoothed reference for price trends.

Additionally, it includes upper and lower bands calculated as a percentage (default: 0.5%) above and below the SMA, plotted as green and red lines, respectively. These bands act as dynamic thresholds to identify overbought or oversold conditions. The indicator generates trade signals based on price action relative to these bands:

Long Entry: A green upward triangle is plotted below the candle when the close crosses above the upper band, signaling a potential buy.

Close Long: A red square is plotted above the candle when the close crosses back below the upper band, indicating an exit for the long position.

Short Entry: A red downward triangle is plotted above the candle when the close crosses below the lower band, signaling a potential sell.

Close Short: A green square is plotted below the candle when the close crosses back above the lower band, indicating an exit for the short position.

The script is customizable, allowing users to adjust the SMA length and band percentage to suit their trading style or market conditions. It is plotted as an overlay on the price chart for easy integration with other technical analysis tools.

Recommended Time Frame and Settings for Trading S&P 500 and Nasdaq-100 Futures

Based on research and market dynamics for S&P 500 (ES) and Nasdaq-100 (NQ) futures, the 5-minute chart is recommended as the optimal time frame for day trading with this indicator. This time frame strikes a balance between capturing intraday trends and filtering out excessive noise, which is critical for futures trading due to their high volatility and leverage. The 5-minute chart aligns well with periods of high liquidity and volatility, such as the U.S. market open (9:30 AM–11:00 AM EST) and the afternoon session (2:00 PM–4:00 PM EST), when institutional traders are most active.

Why 5-minute? It allows traders to react to short-term price movements while avoiding the rapid fluctuations of 1-minute charts, which can be prone to false signals in choppy markets. It also provides enough data points to make the SMA and bands meaningful without the lag associated with longer time frames like 15-minute or hourly charts.

Recommended Settings

SMA Length: Set to 200 periods. This longer lookback period smooths the HL2 data, reducing noise and providing a reliable trend reference for the 5-minute chart. A 200-period SMA helps identify significant trend shifts without being overly sensitive to minor price fluctuations.

Band Percentage: 0.5% is more suitable for the volatility of ES and NQ futures on a 5-minute chart, as it generates fewer but higher-probability signals. Wider bands (e.g., 1%) may miss short-term opportunities, while narrower bands (e.g., 0.1%) may produce excessive false signals.

Trading Session Recommendations

Futures markets for ES and NQ are open nearly 24 hours (Sunday 6:00 PM EST to Friday 5:00 PM EST, with a daily break from 4:00 PM–5:00 PM EST), but not all hours are equally optimal due to varying liquidity and volatility. The best times to trade with this indicator are:

U.S. Market Open (9:30 AM–11:00 AM EST): This period is characterized by high volume and volatility, driven by the opening of U.S. equity markets and economic data releases (e.g., 8:30 AM EST reports like CPI or GDP). The indicator’s signals are more reliable during this window due to strong order flow and price momentum.

Afternoon Session (2:00 PM–4:00 PM EST): After the lunchtime lull, volume picks up as institutional traders return, and news or FOMC announcements often drive price action. The indicator can capture breakout moves as prices test the upper or lower bands.

Pre-Market (7:30 AM–9:30 AM EST): For traders comfortable with lower liquidity, this period can offer opportunities, especially around 8:30 AM EST economic releases. However, use tighter risk management due to wider spreads and potential volatility spikes.

Additional Tips

Avoid Low-Volume Periods: Steer clear of trading during low-liquidity hours, such as the overnight session (11:00 PM–3:00 AM EST), when spreads widen and price movements can be erratic, leading to false signals from the indicator.

Combine with Other Tools: Enhance the indicator’s effectiveness by pairing it with support/resistance levels, Fibonacci retracements, or volume analysis to confirm signals. For example, a long entry signal above the upper band is stronger if it coincides with a breakout above a key resistance level.

Risk Management: Given the leverage in futures (e.g., Micro E-mini contracts require ~$1,200 margin for ES), use tight stop-losses (e.g., below the lower band for longs or above the upper band for shorts) to manage risk. Aim for a risk-reward ratio of at least 1:2.

Test Settings: Backtest the indicator on a demo account to optimize the SMA length and band percentage for your specific trading style and risk tolerance. Micro E-mini contracts (MES for S&P 500, MNQ for Nasdaq-100) are ideal for testing due to their lower capital requirements.

Why These Settings and Time Frame?

The 5-minute chart with a 200-period SMA and 0.5% bands is tailored for the volatility and liquidity of ES and NQ futures during peak trading hours. The longer SMA period ensures the indicator captures meaningful trends, while the 0.5% bands are tight enough to signal actionable breakouts but wide enough to avoid excessive whipsaws. Trading during high-volume sessions maximizes the likelihood of valid signals, as institutional participation drives clearer price action.

By focusing on these settings and time frames, traders can leverage the indicator to capitalize on the dynamic price movements of S&P 500 and Nasdaq-100 futures while managing the inherent risks of these markets.

US30 Smart Money 5M/4H Strategy🧠 How It Works

✅ 1. 4H Trend Bias Detection

Uses the 4-hour chart (internally) to determine if the market is in an uptrend or downtrend.

Background turns green for bullish trend, red for bearish trend.

This helps filter trades — only take longs during uptrend, shorts during downtrend.

✅ 2. Liquidity Sweeps (Stop Hunts) on 5M

Highlights candles that break previous highs/lows and then reverse (typical of institutional stop raids).

Draws a shaded red box above sweep-high candles and green box under sweep-lows.

These indicate key reversal zones.

✅ 3. Order Block Zones

Detects bullish/bearish engulfing patterns after liquidity sweeps.

Draws a supply or demand zone box extending forward.

These zones show where institutions likely placed large orders.

✅ 4. FVG Midpoint from 30-Min Chart

Detects Fair Value Gaps (imbalances) on the 30-minute chart.

Plots a line at the midpoint of the gap (EQ level), which is often revisited for entries or rejections.

✅ 5. Buy/Sell Signals (Non-Repainting)

Buy = 4H uptrend + 5M liquidity sweep low + bullish engulfing candle.

Sell = 4H downtrend + 5M liquidity sweep high + bearish engulfing.

Prints green “BUY” or red “SELL” label on the chart — these do not repaint.

📈 How to Use It

Wait for trend bias — only take trades in the direction of the 4H trend.

Watch for liquidity sweep boxes — these hint a stop hunt just occurred.

Look for a signal label (BUY/SELL) — confirms entry criteria.

Use FVG EQ lines & Order Block zones as confluence or targets.

Take trades after NY open (9:30 AM EST) for best momentum.

Global M2 10-Week Lead (for bitcoin)This script displays a combined view of the Global M2 Money Supply, converted to USD and adjusted with a configurable forward lead (default 10 weeks). It is designed to help visualize macro liquidity trends and anticipate potential impacts on Bitcoin price movements across any timeframe.

🔹 Main Features:

- Aggregates M2 data from 18 countries and regions including the USA, Eurozone, China, Japan, and more.

- All M2 values are converted to USD using respective exchange rates.

- Customizable “Slide Weeks Forward” setting lets you project global liquidity data into the future.

- Works on all timeframes by adjusting the projection logic dynamically.

- Toggle each country’s data on or off to customize the liquidity model.

💡 Use Case:

Global liquidity is often a leading indicator for major asset classes. This tool helps traders and analysts assess macro-level trends and their potential influence on Bitcoin by looking at changes in M2 money supply worldwide.

💡 Inspired By:

This tool mimics the Global M2 10-Week Lead liquidity indicator often referenced by Raoul Pal of Real Vision and Global Macro Investor, used for macro analysis and Bitcoin movement prediction.

📊 Note:

All economic and FX data is sourced from TradingView’s built-in datasets (ECONOMICS and FX_IDC). Data availability may vary depending on your plan.

Institutional Quantum Momentum Impulse [BullByte]## Overview

The Institutional Quantum Momentum Impulse (IQMI) is a sophisticated momentum oscillator designed to detect institutional-level trend strength, volatility conditions, and market regime shifts. It combines multiple advanced technical concepts, including:

- Quantum Momentum Engine (Hilbert Transform + MACD Divergence + Stochastic Energy)

- Fractal Volatility Scoring (GARCH + Keltner-based volatility)

- Dynamic Adaptive Bands (Self-adjusting thresholds based on efficiency)

- Market Phase Detection (Volume + Momentum alignment)

- Liquidity & Cumulative Delta Analysis

The indicator provides a Z-score normalized momentum reading, making it ideal for mean-reversion and trend-following strategies.

---

## Key Features

### 1. Quantum Momentum Core

- Combines Hilbert Transform, MACD divergence, and Stochastic Energy into a single composite momentum score.

- Normalized using a Z-score for statistical significance.

- Smoothed with EMA/WMA/HMA for cleaner signals.

### 2. Dynamic Adaptive Bands

- Upper/Lower bands adjust based on volatility and efficiency ratio .

- Acts as overbought/oversold zones when momentum reaches extremes.

### 3. Market Phase Detection

- Identifies bullish , bearish , or neutral phases using:

- Volume-Weighted MA alignment

- Fractal momentum extremes

### 4. Volatility & Liquidity Filters

- Fractal Volatility Score (0-100 scale) shows market instability.

- Liquidity Check ensures trades are taken in favorable spread conditions.

### 5. Dashboard & Visuals

- Real-time dashboard with key metrics:

- Momentum strength, volatility, efficiency, cumulative delta, and market regime.

- Gradient coloring for intuitive momentum visualization .

---

## Best Trade Setups

### 1. Trend-Following Entries

- Signal :

- QM crosses above zero + Market Phase = Bullish + ADX > 25

- Cumulative Delta rising (buying pressure)

- Confirmation :

- Efficiency > 0.5 (strong momentum quality)

- Liquidity = High (tight spreads)

### 2. Mean-Reversion Entries

- Signal :

- QM touches upper band + Volatility expanding

- Market Regime = Ranging (ADX < 25)

- Confirmation :

- Efficiency < 0.3 (weak momentum follow-through)

- Cumulative Delta divergence (price high but delta declining)

### 3. Breakout Confirmation

- Signal :

- QM holds above zero after a pullback

- Market Phase shifts to Bullish/Bearish

- Confirmation :

- Volatility rising (expansion phase)

- Liquidity remains high

---

## Recommended Timeframes

- Intraday (5M - 1H): Works well for scalping & swing trades.

- Swing Trading (4H - Daily): Best for trend-following setups.

- Position Trading (Weekly+): Useful for macro trend confirmation.

---

## Input Customization

- Resonance Factor (1.0 - 3.618 ): Adjusts MACD divergence sensitivity.

- Entropy Filter (0.382/0.50/0.618) : Controls stochastic damping.

- Smoothing Type (EMA/WMA/HMA) : Changes momentum responsiveness.

- Normalization Period : Adjusts Z-score lookback.

---

The IQMI is a professional-grade momentum indicator that combines institutional-level concepts into a single, easy-to-read oscillator. It works across all markets (stocks, forex, crypto) and is ideal for traders who want:

✅ Early trend detection

✅ Volatility-adjusted signals

✅ Institutional liquidity insights

✅ Clear dashboard for quick analysis

Try it on TradingView and enhance your trading edge! 🚀

Happy Trading!

- BullByte

Fib BB on VWMA*ATRThis TradingView Pine Script is designed to plot Fibonacci Bollinger Bands on a Volume Weighted Moving Average (VWMA) using the Average True Range (ATR). The script takes a higher timeframe (HTF) approach, allowing traders to analyze price action and volatility from a broader market perspective.

🔹 How It Works

Higher Timeframe Data Integration

Users can select a specific timeframe to calculate the VWMA and ATR.

This allows for a more macro perspective, avoiding the noise of lower timeframes.

Volume Weighted Moving Average (VWMA)

Unlike the Simple Moving Average (SMA), VWMA gives higher weight to price movements with larger volume.

Calculation Formula:

𝑉𝑊𝑀𝐴=∑(𝐶𝑙𝑜𝑠𝑒×𝑉𝑜𝑙𝑢𝑚𝑒) / ∑𝑉𝑜𝑙𝑢𝑚𝑒

Since VWMA accounts for volume, it is more reactive to price zones with high buying or selling activity, making it useful for identifying liquidity zones.

ATR-Based Fibonacci Bollinger Bands

The Average True Range (ATR) is used to measure market volatility.

Instead of standard deviation-based Bollinger Bands, Fibonacci multipliers (2.618, 3.0, 3.414) are applied to ATR.

These bands adjust dynamically with market volatility.

🔹 Key Findings from Exploration

Through testing and analysis, this indicator seems to effectively detect supply and demand zones, particularly at the Fibonacci levels of 2.618 to 3.414.

Price frequently reacts at these bands, indicating that they capture key liquidity zones.

Potential Order Block Detection:

The ends of the Fibonacci Bollinger Bands (especially at 2.618, 3.0, and 3.414) tend to align with order blocks—areas where institutional traders previously accumulated or distributed positions.

This is particularly useful for order flow traders who focus on unfilled institutional orders.

🔹 How to Use This Indicator?

Identifying Order Blocks

When price reaches the upper or lower bands, check if there was a strong reaction (rejection or consolidation).

If price rapidly moves away from a band, that level might be an order block.

Spotting Liquidity Pools

VWMA’s nature enhances liquidity detection since it emphasizes high-volume price action.

If a price level repeatedly touches the band without breaking through, it suggests institutional orders may be absorbing liquidity there.

Trend Confirmation

If VWMA is trending upwards and price keeps rejecting the lower bands, it confirms a strong bullish trend.