Tristan's Box: Pre-Market Range Breakout + RetestMarket Context:

This is designed for U.S. stocks, focusing on pre-market price action (4:00–9:30 AM ET) to identify key support/resistance levels before the regular session opens.

Built for 1 min and 5 min timelines, and is intended for day trading / scalping.

Core Idea:

Pre-market range (high/low) often acts as a magnet for price during regular hours.

The first breakout outside this range signals potential strong momentum in that direction.

Retest of the breakout level confirms whether the breakout is valid, avoiding false moves.

Step-by-Step Logic:

Pre-Market Range Identification:

Track high and low from 4:00–9:30 AM ET.

Draw a box spanning this range for visual reference and calculation.

Breakout Detection:

When the first candle closes above the pre-market high → long breakout.

When the first candle closes below the pre-market low → short breakout.

The first breakout candle is highlighted with a “YOLO” label for visual confirmation.

Retest Confirmation:

Identify the first candle whose wick touches the pre-market box (high touches top for short, low touches bottom for long).

Wait for the next candle: if it closes outside the box, it confirms the breakout.

Entry Execution:

Long entry: on the confirming candle after a wick-touch above the pre-market high.

Short entry: on the confirming candle after a wick-touch below the pre-market low.

Only the first valid entry per direction per day is taken.

Visuals & Alerts:

Box represents pre-market high/low.

Top/bottom box border lines show the pre-market high / low levels cleanly.

BUY/SELL markers are pinned to the confirming candle.

Added a "YOLO" marker on breakout candle.

Alert conditions trigger when a breakout is confirmed by the retest.

Strategy Type:

Momentum breakout strategy with confirmation retest.

Combines pre-market structure and risk-managed entries.

Designed to filter false breakouts by requiring confirmation on the candle after the wick-touch.

In short, it’s a pre-market breakout momentum strategy: it uses the pre-market high/low as reference, waits for a breakout, and then enters only after a confirmation retest, reducing the chance of entering on a false spike.

Always use good risk management.

在腳本中搜尋"momentum"

Disparity(20MA) ±1 × Stochastic 80/20 + ATR SL/TP[by Irum]Disparity(20MA) ±1 × Stochastic 80/20 + ATR SL/TP

사용 설명서 (KR/EN Bilingual Manual)

1) 목적 & 정의 / Purpose & Definition

KR — 목적 & 정의

이 스크립트는 이격도(Disparity) 와 스토캐스틱(80/20) 의 동시 신호를 활용해 추세 전환/지속 구간의 고확률 진입 시점을 포착하고, ATR 기반 손절/익절(고정 또는 트레일링)로 리스크를 정량화하여 운용 효율을 높이기 위해 설계되었습니다.

핵심 아이디어:

가격이 20MA 대비 ±임계값을 크로스(과열/침체 해소 신호)하고,

스토캐스틱이 80/20을 돌파/이탈(모멘텀 전환 신호)할 때,

두 신호가 동일봉 또는 N봉 내 동기화되면 진입.

청산: ATR×배수를 이용한 고정 TP/SL 또는 ATR 트레일링.

EN — Purpose & Definition

This strategy combines Disparity (price vs. 20MA) and Stochastic (80/20) to identify high-probability entries when momentum confirms mean-reversion/continuation, while ATR-based stops/take-profits (fixed or trailing) provide quantified risk control.

Core Idea:

Disparity crosses ±threshold (overbought/oversold release),

Stochastic crosses 80/20 (momentum shift),

Both conditions sync on the same bar or within N bars → entry.

Exits: Fixed ATR TP/SL or ATR trailing.

2) 신호 로직 요약 / Signal Logic Overview

KR

롱 진입: Disparity가 −임계값 상향 돌파 & Stochastic 20 상향 돌파가 syncBars 이내에 동시 충족.

숏 진입: Disparity가 +임계값 하향 돌파 & Stochastic 80 하향 돌파가 syncBars 이내에 동시 충족.

완화 옵션(useRelaxStoch): 최근 relaxLookback 내 20/80 터치 이력 + 현재 방향성만으로도 모멘텀 전환을 인정(교차 미충족 보완).

EN

Long: Disparity crosses up −threshold & Stochastic crosses up 20 within syncBars.

Short: Disparity crosses down +threshold & Stochastic crosses down 80 within syncBars.

Relaxed option (useRelaxStoch): Accepts momentum shift if 20/80 was touched in the last relaxLookback bars and the current slope confirms, even without a strict cross.

3) 설정 메뉴 안내 / Settings Menu Guide

A. 기본 / Core

기준가격 / Source (source)

설명: Disparity 계산에 쓰는 가격 소스.

입력: close, hl2, ohlc4 등.

기본값: close.

팁: 변동성 큰 종목은 hlc3/ohlc4가 노이즈를 줄이기도 함.

이격도 기준 MA 길이 / MA Length (for Disparity) (int ≥1)

설명: Disparity의 기준선이 되는 단순이동평균 길이.

기본값: 20.

영향: 길이↑ → 신호 빈도↓, 안정성↑.

이격도 임계값(±%) / Disparity Threshold (±%) (float ≥0.1, step 0.1)

설명: Disparity가 +임계값 아래로 하향 크로스(숏) 또는 −임계값 위로 상향 크로스(롱)할 때 신호.

기본값: 1.0%.

팁: 너무 크면 신호 드뭄, 너무 작으면 과다.

B. 스토캐스틱 / Stochastic

%K Length / K 길이 (int ≥1, 기본 14)

%K Smoothing / K 스무딩 (int ≥1, 기본 1)

%D Length / D 길이 (int ≥1, 기본 3)

설명: ta.stoch의 K를 스무딩한 kSlow와, 추가 스무딩한 dSlow(참조용)를 구성.

Buy Level (↑20) / 매수 기준선 (0~100, 기본 20)

Sell Level (↓80) / 매도 기준선 (0~100, 기본 80)

C. 신호 로직 / Signal Logic

Signal Sync Window (bars) / 신호 동기화 윈도우 (0~10, 기본 0)

설명: 0=두 신호가 같은 봉에서 모두 충족해야 함. N>0=최근 N봉 내에서 각각 한 번 발생하면 인정.

팁: 1~3은 현실적 체결/지연을 반영하며 과최적화 방지에 도움.

Relaxed Stochastic? (교차 완화) (bool, 기본 false)

설명: 교차 대신 최근 20/80 터치 + 현재 기울기만으로도 모멘텀 전환을 인정. 신호 빈도↑.

Relax lookback bars (int ≥1, 기본 5)

설명: 완화판정에 쓰는 최근 봉 수.

D. 리스크 / Risk (ATR)

ATR Length / ATR 길이 (int ≥1, 기본 14)

ATR Mult for Stop / 손절 ATR 배수 (float ≥0.1, 기본 1.5)

ATR Mult for Take-Profit / 익절 ATR 배수 (float ≥0.1, 기본 2.0)

설명: 진입가 ± ATR×배수로 SL/TP 설정.

팁: 변동성 큰 자산은 SL 배수↑, TP 배수도 함께 조정 권장.

Use ATR Trailing Stop? / ATR 트레일링 사용 (bool, 기본 false)

ATR Mult for Trailing / 트레일링 ATR 배수 (float ≥0.1, 기본 2.0)

설명: 고정 TP/SL 대신 추적 손절을 사용(수익 추적에 유리).

E. 시각화 / Visualization

Plot 20MA / 20MA 표시 (bool, 기본 true)

Show Entry Markers / 진입 마커 표시 (bool, 기본 true)

4) 진입·청산 규칙 / Entry & Exit Rules

KR

진입: 위 “신호 로직” 충족 시 strategy.entry("L"/"S").

청산 (고정형):

롱: Stop = 진입 − ATR×SL, TP = 진입 + ATR×TP

숏: Stop = 진입 + ATR×SL, TP = 진입 − ATR×TP

청산 (트레일링형):

ATR×trailMult로 산출한 trail_points/offset으로 추적 손절.

EN

Entry: Place strategy.entry("L"/"S") when sync conditions are met.

Exit (Fixed):

Long: Stop = Entry − ATR×SL, TP = Entry + ATR×TP

Short: Stop = Entry + ATR×SL, TP = Entry − ATR×TP

Exit (Trailing):

Use ATR×trailMult as trailing distance & offset.

5) 알림 / Alerts

조건

Long Entry (Disp −Thr & Stoch Up, sync) → longSignal

Short Entry (Disp +Thr & Stoch Down, sync) → shortSignal

메시지 포맷 / Message format

{"signal":"long|short","symbol":"{{ticker}}","price":{{close}}}

Webhook(예: 거래소·봇)에서 signal/symbol/price를 활용해 체결 로직과 연동하십시오.

6) 빠른 시작 & 권장 프리셋 / Quick Start & Suggested Presets

KR — BTC/USDT (15분봉) 제안

maLen=20, thrPct=1.0~1.5, kLen=14, kS=1, dLen=3, stBuyLv=20, stSellLv=80

syncBars=1~3 (동시성 여유), useRelaxStoch=true, relaxLookback=5

고정형: atrLen=14, atrMultSL=1.5~2.0, atrMultTP=2.0~3.0

트레일링형: useTrail=true, trailMult=2.0~3.0

EN — BTC/USDT (15-min) suggestion

Above defaults, with syncBars=1~3, useRelaxStoch=true to improve fill realism.

Increase atrMultSL on high-volatility days to reduce whipsaws.

7) 운용 팁 & 점검 / Tips & Troubleshooting

KR

신호가 안 나와요: thrPct가 지나치게 크거나 syncBars=0으로 너무 엄격할 수 있음. thrPct↓, syncBars↑ 조정.

휩쏘 과다: useRelaxStoch를 끄거나 thrPct↑, atrMultSL↑.

TP 도달 전에 청산: 트레일링 사용 시 변동성 확대로 SL이 따라붙다 체결될 수 있음 → trailMult↑ 또는 고정형 전환.

과최적화 방지: 한 구간에 과특화된 튜닝(특히 syncBars, thrPct)은 다른 시장에서 성능 저하. Walk-forward 권장.

EN

No signals: Lower thrPct and/or increase syncBars.

Too many whipsaws: Disable relaxed mode, raise thrPct and/or atrMultSL.

Stopped before TP (trailing): Increase trailMult or switch to fixed exits.

Robustness: Avoid over-tuning; validate via walk-forward testing.

Hilly's Advanced Crypto Scalping Strategy - 5 Min ChartTo determine the "best" input parameters for the Advanced Crypto Scalping Strategy on a 5-minute chart, we need to consider the goals of optimizing for profitability, minimizing false signals, and adapting to the volatile nature of cryptocurrencies. The default parameters in the script are a starting point, but the optimal values depend on the specific cryptocurrency pair, market conditions, and your risk tolerance. Below, I'll provide recommended input values based on common practices in crypto scalping, along with reasoning for each parameter. I’ll also suggest how to fine-tune them using TradingView’s backtesting and optimization tools.

Recommended Input Parameters

These values are tailored for a 5-minute chart for liquid cryptocurrencies like BTC/USD or ETH/USD on exchanges like Binance or Coinbase. They aim to balance signal frequency and accuracy for day trading.

Fast EMA Length (emaFastLen): 9

Reasoning: A 9-period EMA is commonly used in scalping to capture short-term price movements while remaining sensitive to recent price action. It reacts faster than the default 10, aligning with the 5-minute timeframe.

Slow EMA Length (emaSlowLen): 21

Reasoning: A 21-period EMA provides a good balance for identifying the broader trend on a 5-minute chart. It’s slightly longer than the default 20 to reduce noise while confirming the trend direction.

RSI Length (rsiLen): 14

Reasoning: The default 14-period RSI is a standard choice for momentum analysis. It works well for detecting overbought/oversold conditions without being too sensitive on short timeframes.

RSI Overbought (rsiOverbought): 75

Reasoning: Raising the overbought threshold to 75 (from 70) reduces false sell signals in strong bullish trends, which are common in crypto markets.

RSI Oversold (rsiOversold): 25

Reasoning: Lowering the oversold threshold to 25 (from 30) filters out weaker buy signals, ensuring entries occur during stronger reversals.

MACD Fast Length (macdFast): 12

Reasoning: The default 12-period fast EMA for MACD is effective for capturing short-term momentum shifts in crypto, aligning with scalping goals.

MACD Slow Length (macdSlow): 26

Reasoning: The default 26-period slow EMA is a standard setting that works well for confirming momentum trends without lagging too much.

MACD Signal Smoothing (macdSignal): 9

Reasoning: The default 9-period signal line is widely used and provides a good balance for smoothing MACD crossovers on a 5-minute chart.

Bollinger Bands Length (bbLen): 20

Reasoning: The default 20-period Bollinger Bands are effective for identifying volatility breakouts, which are key for scalping in crypto markets.

Bollinger Bands Multiplier (bbMult): 2.0

Reasoning: A 2.0 multiplier is standard and captures most price action within the bands. Increasing it to 2.5 could reduce signals but improve accuracy in highly volatile markets.

Stop Loss % (slPerc): 0.8%

Reasoning: A tighter stop loss of 0.8% (from 1.0%) suits the high volatility of crypto, helping to limit losses on false breakouts while keeping risk manageable.

Take Profit % (tpPerc): 1.5%

Reasoning: A 1.5% take-profit target (from 2.0%) aligns with scalping’s goal of capturing small, frequent gains. Crypto markets often see quick reversals, so a smaller target increases the likelihood of hitting profits.

Use Candlestick Patterns (useCandlePatterns): True

Reasoning: Enabling candlestick patterns (e.g., engulfing, hammer) adds confirmation to signals, reducing false entries in choppy markets.

Use Volume Filter (useVolumeFilter): True

Reasoning: The volume filter ensures signals occur during high-volume breakouts, which are more likely to sustain in crypto markets.

Signal Arrow Size (signalSize): 2.0

Reasoning: Increasing the arrow size to 2.0 (from 1.5) makes buy/sell signals more visible on the chart, especially on smaller screens or volatile price action.

Background Highlight Transparency (bgTransparency): 85

Reasoning: A slightly higher transparency (85 from 80) keeps the background highlights subtle but visible, avoiding chart clutter.

How to Apply These Parameters

Copy the Script: Use the Pine Script provided in the previous response.

Paste in TradingView: Open TradingView, go to the Pine Editor, paste the code, and click "Add to Chart."

Set Parameters: In the strategy settings, manually input the recommended values above or adjust them via the input fields.

Test on a 5-Minute Chart: Apply the strategy to a liquid crypto pair (e.g., BTC/USDT, ETH/USDT) on a 5-minute chart.

Fine-Tuning for Optimal Performance

To find the absolute best parameters for your specific trading pair and market conditions, use TradingView’s Strategy Tester and optimization features:

Backtesting:

Run the strategy on historical data for your chosen pair (e.g., BTC/USDT on Binance).

Check metrics like Net Profit, Profit Factor, Win Rate, and Max Drawdown in the Strategy Tester.

Focus on a sample period of at least 1–3 months to capture various market conditions (bull, bear, sideways).

Parameter Optimization:

In the Strategy Tester, click the settings gear next to the strategy name.

Enable optimization for key inputs like emaFastLen (test range: 7–12), emaSlowLen (15–25), slPerc (0.5–1.5), and tpPerc (1.0–3.0).

Run the optimization to find the combination with the highest net profit or best Sharpe ratio, but avoid over-optimization (curve-fitting) by testing on out-of-sample data.

Market-Specific Adjustments:

Volatile Pairs (e.g., DOGE/USDT): Use tighter stop losses (e.g., 0.5–0.7%) and smaller take-profit targets (e.g., 1.0–1.2%) to account for rapid price swings.

Stable Pairs (e.g., BTC/USDT): Slightly wider stop losses (e.g., 1.0–1.2%) and take-profit targets (e.g., 1.8–2.5%) may work better.

Trending Markets: Increase emaSlowLen (e.g., to 25–30) to follow stronger trends.

Choppy Markets: Tighten bbMult (e.g., to 1.8) and lower rsiOverbought/rsiOversold (e.g., to 70/30) to filter noise.

Forward Testing:

After backtesting, run the strategy in real-time on a demo account for 1–2 weeks to validate performance under current market conditions.

Important Notes

No Universal "Best" Numbers: Optimal parameters vary by crypto pair, exchange, and market conditions (e.g., bull vs. bear market). The suggested values are a starting point based on common scalping practices.

Risk Management: Never risk more than 1–2% of your account per trade. Adjust position sizing in TradingView’s strategy settings to align with your risk tolerance.

Market Volatility: Crypto markets are highly volatile. Test the strategy on your specific pair and adjust parameters if signals are too frequent or too rare.

Not Financial Advice: This is an educational tool. Backtest thoroughly and use a demo account before trading with real funds.

If you want me to generate a chart showing backtest performance for specific parameters or to tweak the script further (e.g., adding more indicators or adjusting signal logic), let me know!can you add clear buy ans sell signs above the candles in this codeTo add clear buy and sell signals above the candles in the provided Pine Script, I'll modify the existing code to include prominent text labels directly above (for sell signals) and below (for buy signals) the candles. These labels will be larger, color-coded, and positioned to avoid clutter, ensuring they are easily visible on the chart. The core strategy logic (EMA, RSI, MACD, Bollinger Bands, candlestick patterns, and volume filter) will remain unchanged, and I'll reuse the same artifact_id since this is an update to the previous script.AdvancedCryptoScalpingStrategy.pinex-pine

NIFTY_2min_FVG_Buy_StrategySummary

This strategy is designed for scalping Nifty on a 2-minute chart, focusing exclusively on long entries. The script's purpose is to identify and act on specific bullish reversal patterns based on volume analysis and price action.

Concept & Core Logic

The strategy operates on a two-stage confirmation process:

Volume Absorption: The initial condition seeks to identify potential bullish reversals by detecting signs of selling pressure being absorbed by buyers. This suggests that a downward move may be losing momentum.

Fair Value Gap (FVG) Confirmation: After a volume absorption signal, the strategy waits for a Fair Value Gap (FVG) to appear. A long entry signal is generated only after a candle closes above the FVG zone, serving as confirmation of bullish intent.

Risk Management

The strategy employs a fixed take profit and stop loss for each trade, based on the Nifty underlying price:

Take Profit: The exit signal is triggered when a trade reaches a 25-point profit.

Stop Loss: The exit signal is triggered when a trade reaches a 30-point loss.

Intended Use

This tool is intended for traders who:

Utilize mechanical, rule-based systems for intraday trading and scalping.

Are interested in studying a structured approach that combines volume analysis with price action inefficiencies like Fair Value Gaps.

AI KNN-Dual SuperTrend MTF - by Trading Pine Lab🇬🇧

The AI KNN-Dual SuperTrend MTF is a next-generation trading strategy that merges two higher-timeframe SuperTrends with dual KNN (K-Nearest Neighbors) classifiers, an ADX/DMI filter, and a Pivot Percentile bias module. This layered architecture ensures stronger signal confirmation by requiring consensus across AI models, multi-timeframe SuperTrends, and statistical filters.

Entries occur only when both SuperTrends align with bullish or bearish KNN labels, while the ADX/DMI filter validates momentum. Exits are managed dynamically with adaptive trailing stops (ST ± ATR × factor) or when market conditions flip according to percentile bias.

All parameters are fully configurable:

-Trading direction filter: Long / Short / Both.

-KNN classifiers: neighbors (K), dataset size (N), smoothing lengths.

-Dual SuperTrend: higher timeframes, ATR length, ATR factor, baseline type.

-ADX/DMI filter: customizable length and timeframe.

-Pivot Percentile module: multi-scale statistical bias.

-Visualization: AI markers, ribbons, aura lines, and per-trend coloring.

EMA inFusion Pro - Multiple SourcesEMA Fusion Pro: Dynamic Trend & Momentum Strategy with Three Exit Modes

EMA Fusion Pro is a highly customizable, multi-exit trend-following strategy designed for traders who value both precision and flexibility. By leveraging exponential moving averages (EMA), average directional index (ADX), and volume analysis, this strategy aims to capture trending market moves while offering three distinct exit modes for optimal risk management across varying market conditions.

Strategy Overview

This strategy systematically identifies potential entry points using a moving average crossover with highly configurable data sources (including price, volume, rate of change, or their Heikin Ashi versions) and filters signal quality with ADX trend strength and volume spikes. Each trade is managed with one of three advanced exit methodologies—reverse signal, ATR-based stop/take profit, or fixed percentage—giving you the control to adapt your risk profile to different market regimes.

Key Features

Customizable EMA Source: Calculate the core trend-filtering EMA from price (default), volume, rate of change, or their Heikin Ashi counterparts for unique market perspectives.

Trend Filter with ADX: Confirm entries only when the trend is strong, as measured by the user-adjustable ADX threshold.

Volume Spike Confirmation: Optional filter to only take trades with above-average volume activity, reducing false signals.

Three Exit Modes:

Reverse Signal: Exit trades when a new, opposite entry signal occurs.

ATR-Based Stop/Take Profit: Dynamic risk management using multiples of the average true range (ATR) for both take profit and stop loss.

Percent-Based Stop/Take Profit: Fixed-percentage risk management with user-defined thresholds.

Visual Annotations: Signal markers, EMA line color-coded by source, trend background coloring, and optional ATR/percent-based TP/SL levels.

Info Panel: Real-time display of all core indicators, current trading mode, exit parameters, and position status for quick oversight.

How It Works

Entry Logic: A crossover signal (above/below the EMA) triggers a new entry, but only if both ADX trend strength and (optionally) volume spike conditions are met.

Exit Logic: Three selectable modes allow you to exit trades on reverse signals, at a dynamic ATR-based profit or loss, or at a fixed percentage gain/loss.

Flexible Data Analysis: The EMA source can be chosen from six options—standard price, volume, rate of change, or their Heikin Ashi variants—allowing experimentation with different market dimensions.

Risk Management: All exits are precisely controlled, either by the next opposing signal, by volatility-adjusted levels, or by fixed risk/reward ratios.

Backtest & Optimization: The strategy is fully backtestable within TradingView’s Strategy Tester, with adjustable parameters for optimization.

Customization & Usage

Indicator Source: Select your preferred data type for EMA calculation, opening the door to creative strategy variations (e.g., volume momentum, pure price trend, rate of change divergence).

Filter Toggles: Enable/disable ADX and volume filters as desired—useful for different market environments.

Exit Mode Selection: Switch between reverse, ATR, or percent-based exits with a single parameter—ideal for adapting to ranging vs. trending markets.

Visual Clarity: The EMA line color reflects its underlying source, and the info panel summarizes all critical values for easy monitoring.

Who Should Use This Strategy?

Trend Followers seeking to ride strong moves with multiple exit options.

Experienced Traders who want to experiment with different data types (volume, momentum, Heikin Ashi) for trend analysis.

Algorithmic Traders looking for a robust, flexible base to build upon with their own ideas.

Getting Started

Apply the script to your chart and review default settings.

Customize parameters—EMA length, ADX threshold, volume settings, exit type—as desired.

Backtest on multiple instruments and timeframes to evaluate performance.

Optimize filters, exit rules, and risk parameters for your preferred trading style.

Monitor with the real-time info panel and trade alerts.

Disclaimer

This script is for educational and entertainment purposes only. It is not financial advice. Past performance is not indicative of future results. Always conduct thorough testing and consider your risk tolerance before trading real capital.

— Happy Trading —

Feel free to adapt, share, and contribute to this open-source strategy!

FVG Ultra Assertive - Individual Filters (mtbr)FVG Ultra Assertive - Individual Filters (mtbr)

What this script offers:

This strategy detects and highlights FVGs (Fair Value Gaps) on the chart, providing traders with a visual and systematic approach to identify potential price inefficiencies. The script plots bullish and bearish FVG zones using customizable boxes and labels, allowing users to easily spot high-probability trading areas. In addition, it opens and closes simulated trades based on the detected FVGs, enabling full backtesting and strategy performance evaluation. It integrates multiple independent filters to validate the strength of each FVG signal before entering a trade.

How it works:

The script identifies:

Bullish FVGs when the current low is higher than the high of two bars ago.

Bearish FVGs when the current high is lower than the low of two bars ago.

Once an FVG is detected, it applies three optional independent filters:

GAP/ATR Filter:

Measures the FVG size relative to the Average True Range (ATR). Only gaps exceeding a user-defined multiple of ATR are considered valid.

Support/Resistance (S/R) Filter:

Uses pivot points to check if the FVG overlaps with recent high/low pivot levels within a tolerance percentage. This ensures the gap aligns with meaningful market levels.

Stochastic Filter:

Applies a stochastic oscillator to confirm momentum. Bullish FVGs are validated when stochastic values are oversold, and bearish FVGs when overbought.

After passing the selected filters, the strategy opens trades:

LONG FVG for bullish signals (buy)

SHORT FVG for bearish signals (sell)

The strategy automatically closes positions when an opposite signal appears, generating a backtest report with trades, profits, and statistics. The final bullish or bearish FVG signals are plotted as colored boxes on the chart with labels “BULL FVG” or “BEAR FVG” for immediate visual reference.

How to configure it for use:

Use GAP/ATR Filter: Enable or disable the ATR-based filter and adjust the ATR period (ATR Length) and minimum gap multiplier (Minimum Gap x ATR).

Use S/R Filter: Enable or disable the pivot-based S/R filter. Configure the pivot lookback periods (Pivot Left and Pivot Right) and the tolerance percentage (Gap Tolerance %).

Use Stochastic Filter: Enable or disable stochastic confirmation. Adjust the K and D lengths (Stoch K Length and Stoch D Length) and the overbought/oversold thresholds (Stoch Overbought and Stoch Oversold).

Colors: Customize the colors for bullish and bearish FVGs (FVG Bull and FVG Bear) to match your chart preferences.

Usage Tips:

Apply this strategy to any timeframe; shorter timeframes generate more frequent FVGs, while higher timeframes highlight stronger gaps.

Combine FVG signals with other technical analysis tools for better trade confirmation.

Use the box and label visualization to quickly scan charts for trade opportunities without cluttering the chart.

The strategy’s trades (LONG and SHORT) provide backtesting results and performance statistics for each signal.

Signalgo Strategy ISignalgo Strategy I: Technical Overview

Signalgo Strategy I is a systematically engineered TradingView strategy script designed to automate, test, and manage trend-following trades using multi-timeframe price/volume logic, volatility-based targets, and multi-layered exit management. This summary covers its operational structure, user inputs, entry and exit methodology, unique technical features, and practical application.

Core Logic and Workflow

Multi-Timeframe Data Synthesis

User-Defined Timeframe: The user chooses a timeframe (e.g., 1H, 4H, 1D, etc.), on which all strategy signals are based.

Cross-Timeframe Inputs: The strategy imports closing price, volume, and Average True Range (ATR) for the selected interval, independently from the chart’s native timeframe, enabling robust multi-timeframe analysis.

Price Change & Volume Ratio: It calculates the percent change of price per bar and computes a volume ratio by comparing current volume to its 20-bar moving average—enabling detection of true “event” moves vs. normal market noise.

Hype Filtering

Anti-Hype Mechanism: An entry is automatically filtered out if abnormal high volume occurs without corresponding price movement, commonly observed during manipulation or announcement periods. This helps isolate genuine market-driven momentum.

User Inputs

Select Timeframe: Choose which interval drives signal generation.

Backtest Start Date: Specify from which date historical signals are included in the strategy (for precise backtests).

Take-Profit/Stop-Loss Configuration: Internally, risk levels are set as multiples of ATR and allow for three discrete profit targets.

Entry Logic

Trade Signal Criteria:

Price change magnitude in the current bar must exceed a fixed sensitivity threshold.

Volume for the bar must be significantly elevated compared to average, indicating meaningful participation.

Anti-hype check must not be triggered.

Bullish/Bearish Determination: If all conditions are met and price change direction is positive, a long signal triggers. If negative, a short signal triggers.

Signal Debouncing: Ensures a signal triggers only when a new condition emerges, avoiding duplicate entries on flat or choppy bars.

State Management: The script tracks whether an active long or short is open to avoid overlapping entries and to facilitate clean reversals.

Exit Strategy

Take-Profits: Three distinct profit targets (TP1, TP2, TP3) are calculated as fixed multiples of the ATR-based stop loss, adapting dynamically to volatility.

Reversals: If a buy signal appears while a short is open (or vice versa), the existing trade is closed and reversed in a single step.

Time-Based Exit: If, 49 bars after entry, the trade is in-profit but hasn’t reached TP1, it exits to avoid stagnation risk.

Adverse Move Exit: The position is force-closed if it suffers a 10% reversal from entry, acting as a catastrophic stop.

Visual Feedback: Each TP/SL/exit is plotted as a clear, color-coded line on the chart; no hidden logic is used.

Alerts: Built-in TradingView alert conditions allow automated notification for both entries and strategic exits.

Distinguishing Features vs. Traditional MA Strategies

Event-Based, Not Just Slope-Based: While classic moving average strategies enter trades on MA crossovers or slope changes, Signalgo Strategy I demands high-magnitude price and volume confirmation on the chosen timeframe.

Volume Filtering: Very few MA strategies independently filter for meaningful volume spikes.

Real Market Event Focus: The anti-hype filter differentiates organic market trends from manipulated “high-volume, no-move” sessions.

Three-Layer Exit Logic: Instead of a single trailing stop or fixed RR, this script manages three profit targets, time-based closures, and hard adverse thresholds.

Multi-Timeframe, Not Chart-Dependent: The “main” analytical interval can be set independently from the current chart, allowing for in-depth cross-timeframe backtests and system runs.

Reversal Handling: Automatic handling of signal reversals closes and flips positions precisely, reducing slippage and manual error.

Persistent State Tracking: Maintains variables tracking entry price, trade status, and target/stop levels independently of chart context.

Trading Application

Strategy Sandbox: Designed for robust backtesting, allowing users to simulate performance across historical data for any major asset or interval.

Active Risk Management: Trades are consistently managed for both fixed interval “stall” and significant loss, not just via trailing stops or fixed-day closes.

Alert Driven: Can power algorithmic trading bots or notify discretionary traders the moment a qualifying market event occurs.

AltCoin & MemeCoin Index Correlation [Eddie_Bitcoin]🧠 Philosophy of the Strategy

The AltCoin & MemeCoin Index Correlation Strategy by Eddie_Bitcoin is a carefully engineered trend-following system built specifically for the highly volatile and sentiment-driven world of altcoins and memecoins.

This strategy recognizes that crypto markets—especially niche sectors like memecoins—are not only influenced by individual price action but also by the relative strength or weakness of their broader sector. Hence, it attempts to improve the reliability of trading signals by requiring alignment between a specific coin’s trend and its sector-wide index trend.

Rather than treating each crypto asset in isolation, this strategy dynamically incorporates real-time dominance metrics from custom indices (OTHERS.D and MEME.D) and combines them with local price action through dual exponential moving average (EMA) crossovers. Only when both the asset and its sector are moving in the same direction does it allow for trade entries—making it a confluence-based system rather than a single-signal strategy.

It supports risk-aware capital allocation, partial exits, configurable stop loss and take profit levels, and a scalable equity-compounding model.

✅ Why did I choose OTHERS.D and MEME.D as reference indices?

I selected OTHERS.D and MEME.D because they offer a sector-focused view of crypto market dynamics, especially relevant when trading altcoins and memecoins.

🔹 OTHERS.D tracks the market dominance of all cryptocurrencies outside the top 10 by market cap.

This excludes not only BTC and ETH, but also major stablecoins like USDT and USDC, making it a cleaner indicator of risk appetite across true altcoins.

🔹 This is particularly useful for detecting "Altcoin Season"—periods where capital rotates away from Bitcoin and flows into smaller-cap coins.

A rising OTHERS.D often signals the start of broader altcoin rallies.

🔹 MEME.D, on the other hand, captures the speculative behavior of memecoin segments, which are often driven by retail hype and social media activity.

It's perfect for timing momentum shifts in high-risk, high-reward tokens.

By using these indices, the strategy aligns entries with broader sector trends, filtering out noise and increasing the probability of catching true directional moves, especially in phases of capital rotation and altcoin risk-on behavior.

📐 How It Works — Core Logic and Execution Model

At its heart, this strategy employs dual EMA crossover detection—one pair for the asset being traded and one pair for the selected market index.

A trade is only executed when both EMA crossovers agree on the direction. For example:

Long Entry: Coin's fast EMA > slow EMA and Index's fast EMA > slow EMA

Short Entry: Coin's fast EMA < slow EMA and Index's fast EMA < slow EMA

You can disable the index filter and trade solely based on the asset’s trend just to make a comparison and see if improves a classic EMA crossover strategy.

Additionally, the strategy includes:

- Adaptive position sizing, based on fixed capital or current equity (compound mode)

- Take Profit and Stop Loss in percentage terms

- Smart partial exits when trend momentum fades

- Date filtering for precise backtesting over specific timeframes

- Real-time performance stats, equity tracking, and visual cues on chart

⚙️ Parameters & Customization

🔁 EMA Settings

Each EMA pair is customizable:

Coin Fast EMA: Default = 47

Coin Slow EMA: Default = 50

Index Fast EMA: Default = 47

Index Slow EMA: Default = 50

These control the sensitivity of the trend detection. A wider spread gives smoother, slower entries; a narrower spread makes it more responsive.

🧭 Index Reference

The correlation mechanism uses CryptoCap sector dominance indexes:

OTHERS.D: Dominance of all coins EXCLUDING Top 10 ones

MEME.D: Dominance of all Meme coins

These are dynamically calculated using:

OTHERS_D = OTHERS_cap / TOTAL_cap * 100

MEME_D = MEME_cap / TOTAL_cap * 100

You can select:

Reference Index: OTHERS.D or MEME.D

Or disable the index reference completely (Don't Use Index Reference)

💰 Position Sizing & Risk Management

Two capital allocation models are supported:

- Fixed % of initial capital (default)

- Compound profits, which scales positions as equity grows

Settings:

- Compound profits?: true/false

- % of equity: Between 1% and 200% (default = 10%)

This is critical for users who want to balance growth with risk.

🎯 Take Profit / Stop Loss

Customizable thresholds determine automatic exits:

- TakeProfit: Default = 99999 (disabled)

- StopLoss: Default = 5 (%)

These exits are percentage-based and operate off the entry price vs. current close.

📉 Trend Weakening Exit (Scale Out)

If the position is in profit but the trend weakens (e.g., EMA color signals trend loss), the strategy can partially close a configurable portion of the position:

- Scale Position on Weak Trend?: true/false

- Scaled Percentage: % to close (default = 65%)

This feature is useful for preserving profits without exiting completely.

📆 Date Filter

Useful for segmenting performance over specific timeframes (e.g., bull vs bear markets):

- Filter Date Range of Backtest: ON/OFF

- Start Date and End Date: Custom time range

OTHER PARAMETERS EXPLANATION (Strategy "Properties" Tab):

- Initial Capital is set to 100 USD

- Commission is set to 0.055% (The ones I have on Bybit)

- Slippage is set to 3 ticks

- Margin (short and long) are set to 0.001% to avoid "overspending" your initial capital allocation

📊 Visual Feedback and Debug Tools

📈 EMA Trend Visualization

The slow EMA line is dynamically color-coded to visually display the alignment between the asset trend and the index trend:

Lime: Coin and index both bullish

Teal: Only coin bullish

Maroon: Only index bullish

Red: Both bearish

This allows for immediate visual confirmation of current trend strength.

💬 Real-Time PnL Labels

When a trade closes, a label shows:

Previous trade return in % (first value is the effective PL)

Green background for profit, Red for losses.

📑 Summary Table Overlay

This table appears in a corner of the chart (user-defined) and shows live performance data including:

Trade direction (yellow long, purple short)

Emojis: 💚 for current profit, 😡 for current loss

Total number of trades

Win rate

Max drawdown

Duration in days

Current trade profit/loss (absolute and %)

Cumulative PnL (absolute and %)

APR (Annualized Percentage Return)

Each metric is color-coded:

Green for strong results

Yellow/orange for average

Red/maroon for poor performance

You can select where this appears:

Top Left

Top Right

Bottom Left

Bottom Right (default)

📚 Interpretation of Key Metrics

Equity Multiplier: How many times initial capital has grown (e.g., “1.75x”)

Net Profit: Total gains including open positions

Max Drawdown: Largest peak-to-valley drop in strategy equity

APR: Annualized return calculated based on equity growth and days elapsed

Win Rate: % of profitable trades

PnL %: Percentage profit on the most recent trade

🧠 Advanced Logic & Safety Features

🛑 “Don’t Re-Enter” Filter

If a trade is closed due to StopLoss without a confirmed reversal, the strategy avoids re-entering in that same direction until conditions improve. This prevents false reversals and repetitive losses in sideways markets.

🧷 Equity Protection

No new trades are initiated if equity falls below initial_capital / 30. This avoids overleveraging or continuing to trade when capital preservation is critical.

Keep in mind that past results in no way guarantee future performance.

Eddie Bitcoin

Imbalance No SL📊 Strategy Name: Imbalance No SL

This strategy specially trades on price jumps (true imbalances) in the market, takes advantage of momentum only, and as soon as the opposite signal and profit is received, the trade is closed immediately.

Imbalance No SL strategy specially generates buy and sell signals based on "Imbalance" logic, without any fixed Stop Loss.

🔍 Core Logic

Imbalance Detection

Bullish Imbalance : When the low of the current candle is above the high of the previous candle.

(i.e. a jump type gap occurred in the market – demand is high, price went straight up)

Bearish Imbalance : When the high of the current candle is below the low of the previous candle.

(i.e. the market suddenly fell down)

Creating Visual Box and Label on Signal:

As soon as bullish imbalance is found, green box & IMB BULL label is displayed on the chart.

Bearish has red box & IMB BEAR label.

Trade Entry Logic

BUY on Bullish Imbalance: If there is already a buy or neutral position, then a new “BUY” signal will fire.

SELL on Bearish Imbalance: If already in sell or neutral position, then new “SELL” signal will fire.

You can set quantity/lot size from ‘qty’ input field.

Trade Average Calculation

Buy/Sell maintains average price and their count (so that if averaging is done then correct P&L is calculated).

Trade Exit Logic (Profit Booking/Signal Reverse)

If your buy is going on and bearish imbalance is formed + price is above your average, then buy will be closed (profit condition).

If sell is going on and bullish imbalance is formed + price is below average, then sell will be closed.

Chart Cleaning/Management

Only keep the label and box of the latest signal on the chart, old boxes/labels are automatically deleted.

Alert

You can get alert on bullish or bearish signal (by using alert feature of TradingView).

✅ Simple Explanation for User

This strategy buys or sells directly at the gap (imbalance).

Whenever there is a clear signal of momentum in the market (breakout of the gap), then the trade entry takes place.

When there is an imbalance in the opposite direction and profit is made, the system closes the trade (closes).

There is no fixed stop-loss, risk management is handled by trade averaging/close.

You will know at every point on the visually chart that at which bar the buy, sell and exit took place.

⚠️ What to remember?

If the market is in trend then this script gives very good signals.

In choppy/sideways market, some loss trades can also come because there is no SL.

Big profit or big loss – both depend on the imbalance signal and market speed.

- Trading Bot – Dynamic RSI (Professional) - Robot Strategy -1. General Concept and Philosophy

This strategy was designed for systematic traders and work especially well on short timeframes (1 to 5 minutes), who seek to capture trend reversal movements with a high degree of confirmation. The goal is not to follow the trend, but to identify precise entry points in oversold or overbought zones, and then to exit the position dynamically to adapt to changing market conditions.

The originality of Trading Bot Dynamic RSI lies not in a single indicator, but in the intelligent fusion of several concepts:

Dynamic RSI bands for both entries and exits .

A triple confirmation filter to secure trade entries.

A fully parameterizable design ready for automation .

2. Originality at the Core of the Strategy: Key Features

Dynamic Exits on RSI Bands: This is a main original feature of this script. Unlike traditional strategies that use fixed Take-Profits and Stop-Losses, this one uses an exit RSI band, calculated with parameters independent of the entry ones. This allows the strategy to:

Adapt to Volatility: In a volatile market, the exit band will move further away, allowing for the capture of larger moves. In a ranging market, it will tighten to secure smaller gains.

Optimize Profits: The exit occurs when momentum genuinely fades, not at an arbitrary price level, thus maximizing the potential of each trade.

Triple Confirmation Filter for Precise Entries: To avoid false signals, each entry is validated by the convergence of three distinct conditions:

The base signal is generated when the price reaches an overbought or oversold zone, materialized by an RSI band calculated directly on the chart.

The WaveTrend oscillator must also be in an extreme zone, confirming that the short-term momentum is ready for a reversal.

Finally, the StochRSI must validate that the RSI itself is in an overbought or oversold condition, adding an extra layer of security.

"Automation Ready" Design: The strategy was developed with automation in mind.

Customizable Alert Messages: All messages for entries and exits (Long/Short) can be formatted to be compatible with automated trade execution platforms.

Precise Capital Management: The position size calculation can be set as a fixed amount (e.g., 100 USDT), a percentage of the total capital, or of the available capital, and includes leverage. These parameters are crucial for a trading bot.

3. Detailed Operation

Entry Logic: A position is opened only if the following three conditions are met:

The market price touches (or closes below/above) the entry RSI band (lower for a buy, upper for a sell).

The WaveTrend indicator is in the oversold zone (for a buy) or overbought zone (for a sell).

The Stochastic RSI indicator is also in the oversold zone (for a buy) or overbought zone (for a sell).

The order is placed as a limit order on the RSI band, allowing for execution at the best possible price.

Exit Logic: The primary exit is dynamic.

For a Long position, the trade is closed when the price reaches the upper exit RSI band.

For a Short position, the trade is closed when the price reaches the lower exit RSI band.

Optionally, a percentage-based Stop-Loss and Take-Profit can be activated for more traditional risk management, although the dynamic exit is the recommended default mechanism.

4. Ease of Use and Customization

Despite its internal complexity, the strategy is designed to be user-friendly :

Clear Settings Panel: Parameters are grouped by function (Long Entry, Long Exit, Quantity, etc.), and each option comes with an explanatory tooltip.

Integrated Display: All key information (performance, current settings) is displayed in clean and discreet tables directly on the chart, allowing you to see at a glance how the strategy is configured.

Total Flexibility: Although default settings are provided, every parameter (RSI lengths, levels, filters) can be adjusted to optimize the strategy on any asset (cryptocurrencies, Forex, indices...) and any timeframe.

5. Detailed Guide to User Settings

A comprehensive set of parameters

To offer you complete control and maximum flexibility, the strategy exposes a comprehensive set of parameters. Here is an overview of what you can customize:

Trading Mode and Display

Trading Mode: Choose to enable only long positions ("Long Only"), only short positions ("Short Only"), or both simultaneously ("Long and Short").

Display: Manage the information panels on the chart. You can opt for a full display, a minimal window showing the profit, or hide all information for a clean chart.

Filters Smoothing (StochRSI K)

Filters Smoothing: This key parameter adjusts the smoothing of the Stochastic RSI. A lower value will make the filter more responsive, generating more signals. A higher value will make it smoother, generating fewer but potentially more reliable signals.

LONG Position Settings

Long Only mode

Entry: Define the RSI length and Oversold level that draw the lower band for long position entries.

Exit: Independently configure the RSI length and Overbought level that draw the upper band for the dynamic position exit.

Options: Optionally enable a percentage-based Take-Profit and/or Stop-Loss.

SHORT Position Settings

Short Only Mode

Entry: Define the RSI length and Overbought level for the upper entry band for short positions.

Exit: Independently configure the RSI length and Oversold level for the lower dynamic exit band.

Options: Just like for long positions, you can enable a percentage-based Take-Profit and/or Stop-Loss.

Quantity and Leverage

Quantity Type: Calculate your position size in three ways: as a fixed cash amount, as a percentage of available capital, or as a percentage of the total account balance.

Amount: Specify the dollar amount or percentage to commit per trade.

Leverage: Set the leverage to be applied. This is crucial for automation.

Backtest Period

Backtest Period: Enable this option to limit the strategy's calculations to a specific time period. This is a powerful tool for testing performance under particular market conditions.

Bot Alert Messages

Bot Alert Messages: This section is dedicated to automation. Customize the exact text messages that will be sent by TradingView alerts for each event (enter long, exit long, etc.).

Other Settings (Advanced - Optional)

Other Settings: This section allows experienced users to fine-tune the confirmation engine. You can adjust the parameters of the WaveTrend and Stochastic RSI oscillators in detail.

Spread Calculator (Informative Only)

Spread Calculator: This handy tool helps you estimate the actual fees of your exchange to run a much more realistic backtest. This panel has no impact on the trading logic itself.

Disclaimer

This strategy provides signals based on past market conditions. Past performance is not indicative of future results. Trading involves risk, and it is the responsibility of each user to manage their risk appropriately. It is strongly recommended to conduct thorough backtests and to understand the functioning of each parameter before using this strategy in live conditions or automating it. Take into account transaction fees, spread, and slippage, which can impact real results.

PowerTrend Pro Strategy – Gold OptimizedTired of false signals on Gold?

PowerTrend Pro combines VWAP, Supertrend, RSI, and smart MA filters with trailing stops & break-even logic to deliver high-probability trades on XAUUSD.

PowerTrend Pro Strategy is a professional-grade trading system designed to capture high-probability swing and intraday opportunities on XAUUSD (Gold) and other volatile markets.

🔑 Core Features

VWAP Anchoring – institutional fair value reference to filter trades.

Supertrend (ATR-based) – adaptive trend filter tuned for Gold’s volatility.

Multi-Timeframe RSI – confirms momentum alignment across intraday and higher timeframe.

EMA + SMA Combo – ensures trades follow strong directional bias, reducing false signals.

Dynamic Risk Management

Adjustable Take Profit / Stop Loss (%)

Trailing Stop that locks in profits on extended moves

Break-Even Logic (stop loss moves to entry once price is in profit)

⚡ Gold-Tuned Presets

XAUUSD 1H → tighter TP/SL & faster entries for active intraday trading.

XAUUSD 4H → wider ATR filter & trailing stops to capture bigger swings.

Generic Mode → works on Forex, Indices, and Crypto (fully customizable).

🎯 Why It Works

Gold is notoriously volatile — quick spikes wipe out weak strategies. PowerTrend Pro solves this by combining:

✅ Institutional bias (VWAP)

✅ Adaptive trend filter (Supertrend)

✅ Momentum confirmation (RSI MTF)

✅ Robust trend structure (EMA + SMA)

✅ Smart exits (TP, SL, trailing & breakeven)

This multi-layer confirmation makes entries stronger and keeps risk under control.

🛠️ Usage

Add the strategy to your chart.

Choose a preset (XAUUSD 1H, 4H, or Generic).

Run Strategy Tester for performance metrics.

Optimize TP/SL and ATR values for your broker & market conditions.

🔥 Pro Tip: Combine this strategy with a session filter (London/NY overlap) or volume confirmation to boost accuracy in Gold.

TTE Elite Market SignalsWelcome to TTE Elite Market Signals Your very own personal trading assistant

Trading today demands more than intuition—it requires exclusive access to elite-level market intelligence and the discipline to act on high-probability signals. Every professional trader seeks that decisive advantage: the clarity and confidence that separates consistent profitability from market uncertainty. The financial markets show no mercy, demanding precision, logic, and strategy grounded in institutional-grade analysis.

Human judgment, while powerful, can be compromised by fatigue and emotion, leading to costly trading errors. This is precisely where TTE Elite Market Signals excels. Our sophisticated platform combines proven trading methodologies with advanced signal generation technology, delivering market intelligence that empowers you to identify optimal entry and exit opportunities while maintaining complete control over your trading decisions.

Revolutionary Signal Intelligence

TTE Elite Market Signals features adaptive learning technology that evolves with market conditions. It continuously refines its analysis, helping you identify higher-probability setups while providing the market intelligence needed for superior risk management.

Elite Analysis Modes

Our platform adapts its signal generation to match market personalities:

- Institutional Flow Mode (MM-hybrid): Identifies manipulation patterns and tracks smart money movement with exclusive institutional-grade precision

- Momentum Adaptive Mode: Rapidly adjusts analysis when volatility and momentum shift

- Conservative Precision Mode: Steady, risk-conscious signals for consistent performance

- Adaptive Intelligence Mode: Self-refining system that enhances signal quality over time from past trades (long term of use)

Comprehensive Signal Intelligence

TTE Elite Market Signals integrates multiple sophisticated analytical systems:

- Volume Profile analysis for exclusive institutional-level market insights

- Pattern recognition enhanced by machine learning algorithms

- Intelligent exit timing that identifies optimal profit-taking opportunities

- Protection against market manipulation tactics

- Position sizing guidance that scales with trading success

- Fibonacci based reversal logic

Perfect for Your Trading Evolution

Experienced traders appreciate our sophisticated market intelligence and institutional-grade analytics that provide genuine competitive advantages.

Developing traders benefit from intelligent signal analysis that handles complex market calculations while teaching professional-level market interpretation and risk management principles via visuals on chart and descriptive panel.

All timeframes supported—from scalping to swing trading, TTE Elite Market Signals adapts to your preferred trading style via several user input selections.

Two Elite Service Modes

1. Signal Intelligence Mode: Real-time market signals with AI-driven analysis and detailed trade rationale

2. Alert Precision Mode: High-probability setup notifications with comprehensive market context and risk parameters

The Exclusive Learning Advantage

What makes TTE Elite Market Signals exceptional: it maintains a comprehensive trade memory and identifies the highest-probability signals, adapts to changing volatility patterns, and continuously refines(does not repaint) its analysis to enhance your profit potential and trading accuracy.

Built-in Professional Protection

- Advanced manipulation detection safeguards against institutional market maker(MM) tactics

- Intelligent risk assessment adjusts signal confidence based on market conditions

- Progressive scaling guidance maximizes winners while minimizing losses(educational)

- Comprehensive oversight with customizable risk parameters

Experience the Elite Difference

TTE gives you visuals on the chart of past trades and live metrics results to see what actually work and what fails, to minimize unrealistic expectations. Just sit back and watch sophisticated algorithms work tirelessly on your behalf, identifying opportunities that others miss and alerting you as signals are generated. Transforming the stressful, emotional battlefield of trading into a systematic analytical approach.

Let the System Do the Heavy Lifting

While others struggle with analysis paralysis and emotional decision-making, you'll have access to signals that have already processed hundreds of data points, identified institutional patterns, and calculated optimal risk-reward scenarios for a far less stressful trading experience.

What Elite Traders Should Know

TTE Elite Market Signals represents cutting-edge signal generation technology designed for serious market education and skill development, but it is not a black box, nor perfect for all markets. It must be adjusted to yield optimal results. While our advanced capabilities and institutional-grade features provide significant analytical advantages, trading success requires discipline and proper execution. Markets evolve, and optimal results demand understanding of signal context.

Success with TTE Elite Market Signals comes from mastering our analytical modes and using the proper entry types such as breakout entry, machine learning(ML) entry etc, utilizing and selecting the most effective risk control to optimize it, and maintaining disciplined risk management.

Join the Elite Trading Revolution

This isn't just another signal service—it equips you with the tools to do proper market analysis displaying price movement and volume profile designed for serious traders who understand that consistent profitability comes from discipline, superior market intelligence and proper interpretation, not luck.

Trade smart, stay profitable, and achieve trading excellence.

Best TTE Settings

Trade Entry Types:

1st Best Breakout Entry(out perform all others when used alone)

2nd Best ML Entry by itself or + Pattern Entry Combined

Risk Management:

ATR Multiplier 2

Enable Master Size Control

Master Size Mode

Max Risk Per Trade % 2.5

Max Multiplier Cap 1.5

Enable Growth Scaling

Growth Scaling Mode-set to Time Based or Performance

Risk Management System- set to Hybrid

Enable ML System

ML Mode-set to Auto or Quantum Learning

ML Application Strategy-set to Universal All Entries

Enable Trend Continuation

Mode- Set to Standard

Independent Entry-stays unchecked(off)

Best Performing Instruments on TTE (will update list as more are adjusted and tested)

NVDA

AMD

AMZN

TSLA

SPY

QQQ

PLTR

Ultimate Bot v5 (Full Visual + Reversal + Sustained Signals)Ultimate Bot v5 is a powerful, all-in-one Pine Script strategy designed for traders who want both clarity and precision in their charts. It combines classic momentum indicators, volatility filters, and reversal logic to highlight high-probability trade opportunities.

🔹 Key Features

Full Visual Mode – Clean and easy-to-read buy/sell markers with large arrows and labels.

EMA Trend Detection – Fast & slow EMA crossovers for trend direction.

RSI + MACD Confirmation – Confirms entries with momentum & strength checks.

Reversal Alerts – Detects sharp drops or spikes for rebound/reversal plays.

Sustained Signal Mode – Highlights stronger continuation trends, not just short-term flips.

ADX Strength Filter (optional) – Filters out weak/noisy signals during sideways markets.

ATR Dynamic Positioning – Arrows adapt to volatility so they’re always visible.

Custom Alerts – Works with TradingView alerts for buy, sell, and reversal signals.

🔹 Why Use It?

This bot is designed to help traders:

✅ Spot early reversals and potential bounce opportunities

✅ Confirm strong momentum moves with multi-indicator checks

✅ Avoid false signals in choppy markets

✅ Trade with confidence using visual clarity

TrendPilot AI v2 — Adaptive Trend Day Trading StrategyOverview

TrendPilot AI v2 is a structured, rules-based day trading strategy that identifies and follows market momentum using a sophisticated blend of technical indicators. Optimized for 15-minute and higher timeframes on high market cap cryptocurrencies (AAVE, SOL, ETH, BCH, BTC) to minimize manipulation risks, it adapts to changing market conditions with dynamic risk management and controlled re-entry logic to maximize trend participation while minimizing noise.

Core Logic

Multiple EMA Trend Confirmation — Uses three Exponential Moving Averages (fast, medium, slow) to detect robust bullish, bearish, or neutral trends, ensuring trades align with the prevailing market direction.

ADX Momentum Filter — Employs an ADX-based filter to confirm strong trends, avoiding entries in choppy or low-momentum markets.

Smart Entry Filter — Optional ATR-based buffer (period 14, multiplier 1.5) around the fast EMA prevents entries at overextended prices, enhancing trade precision.

Flexible Exit System — Offers multiple exit options: fixed take-profit (default 1.7 offset), trend-reversal exits, or ATR-based trailing stops (period 14, multiplier 2.0), with secure modes requiring candle closes for confirmation to gain Max Profit.

Controlled Re-Entry Logic — Allows re-entries after take-profit or price-based stop-loss with configurable wait periods (default 6 bars), max attempts (default 2), and EMA touch requirements (fast, medium, or slow).

State-Aware Risk Management — Tracks trend states and recent exits to adapt entries, with daily trade limits (default 5 long/short) and loss cooldowns (default 2 stop-losses) for disciplined trading.

How to Use & Configuration

Markets & Timeframes

Works with high market cap cryptocurrencies (AAVE, SOL, ETH, BCH, BTC).

Optimized for intraday charts (15m–4h) but adaptable to higher timeframes (e.g., 1h, 4h).

Trade Direction Settings

Dual Trades — Trades both long and short, quickly re-aligning after trend reversals.

Long Only — Ignores bearish signals, ideal for bullish markets or strong uptrends.

Short Only — Ignores bullish signals, suited for bearish markets or downtrends.

Risk Management Settings

Stop Loss Types

Trend Reversal — Closes positions when an opposite trend signal is confirmed (default).

Fixed Offset — Static stop at 3.5 offset from entry price (adjustable).

ATR Based — Dynamic trailing stop using ATR (period 14, multiplier 2.0), adjusting to market volatility.

Secure SL Mode — Optional setting to trigger price-based stops only on candle closes, reducing false exits.

Maximum recommended risk per trade is 5–10% of account equity.

Trade size is configurable (default 20 units) to match individual risk appetite.

Take Profit Options

Fixed Offset — Predefined target at 1.7 offset from entry (adjustable, e.g., 2.5 for SOL).

Secure TP Mode — Exits only when a candle closes beyond the target, ensuring reliable profit capture.

Trend Reversal — Exits on opposite trend signals when fixed TP is disabled, ideal for riding longer trends.

Trade Management Controls

Smart Entry Filter — Optional ATR-based buffer (period 14, multiplier 1.5) prevents chasing overextended prices.

Max Re-Entries — Limits continuation trades per trend cycle (default 2).

Daily Trade Limits — Caps long/short trades per day (default 5 each) for disciplined trading.

Daily Loss Cooldown — Pauses trading after a set number of stop-losses (default 2) per day.

Max Bars in Trade — Closes positions after a set duration (default 1440 bars) to prevent stale trades.

Configuration Steps

Apply the strategy to your chosen symbol (e.g., AAVE/USDT, SOL/USDT) and timeframe (15m or higher).

Select Trade Direction mode (Dual, Long Only, or Short Only).

Set Stop Loss (Trend Reversal, Fixed Offset, or ATR Based) and Take Profit (fixed or trend-reversal).

Adjust Smart Entry Filter, Max Re-Entries, Daily Limits, and Loss Cooldown as needed.

Test across multiple market conditions using the performance panel (top-right, showing Total Trades, Wins, Losses, Win Rate).

Enables automated trading via webhook integration with platforms like Binance Futures.

Set up alerts for long/short entries (🟢 Long, 🔴 Short) and exits (🎯 Max TP, 🛑 Max SL, 🚨 Force Exit).

Backtesting Guidance

Use realistic commission (default 0.01%) and slippage (default 2 ticks) matching your broker and instrument.

Validate performance over long historical periods (e.g., 3–6 months) to ensure >100 trades across different market regimes.

Avoid curve-fitting by testing on multiple high market cap coins (AAVE, SOL, ETH, BCH, BTC) and avoiding over-optimization.

EMA and ATR parameters are set to balanced, industry-standard values for realistic backtesting.

Best Practices, Defaults & Disclaimer

Best Practices

Use consistent and conservative position sizing (default 20 units).

Match commission and slippage to your broker’s actual rates.

Enable secure TP/SL modes for entries and exits to reduce false signals.

Test across different symbols, timeframes, and market phases before live trading.

Keep parameters simple to avoid overfitting.

Default Settings (Recommended Starting Point)

Initial Capital: $10,000

Order Size: Fixed, 20 units

Commission: 0.01%

Slippage: 2 ticks

Take Profit Offset: 1.7 (adjustable, e.g., 2.5 for SOL)

Stop Loss Type: Trend Reversal (default), Fixed Offset (3.5), or ATR Based (period 14, multiplier 2.0)

Smart Entry Filter: ATR period 14, multiplier 1.5 (optional)

Max Re-Entries: 2 per trend cycle

Daily Trade Limits: 5 long, 5 short

Daily Loss Cooldown: 2 stop-losses

Max Bars in Trade: 1440 bars

Subscription Information

TrendPilot AI v2 is an invite-only strategy, accessible only to approved subscribers.

Benefits include full access to all features, priority support, and regular updates.

Access is limited to ensure a high-quality user experience.

Compliance Status

No functional warnings in the script.

The script uses closed candle logic, ensuring no repainting or lookahead issues.

Designed for realistic backtesting with a $10,000 account and sustainable risk (≤5–10% per trade).

Disclaimer

This strategy is intended for educational and analytical purposes only. Trading involves substantial risk, and past performance does not guarantee future results. You are solely responsible for your own trading decisions and risk management.

Developed by: TrendPilotAI Team

For questions, setup guidance, or enhancement suggestions, contact TrendPilotAI Team via TradingView.

HAPI MA Crossover StrategyDescription:

This strategy implements a Moving Average (MA) crossover system to identify potential trend reversals and capture directional momentum. Two moving averages are calculated — a fast MA (shorter period) and a slow MA (longer period).

Long Entry: Triggered when the fast MA crosses above the slow MA, signaling a potential bullish trend shift.

Short Entry: Triggered when the fast MA crosses below the slow MA, signaling a potential bearish trend shift.

Exit Conditions: Positions are closed when an opposite crossover occurs or when an optional stop-loss/take-profit is hit (if enabled).

The fast and slow MA types (SMA, EMA, etc.) and periods are user-configurable for flexibility. This crossover method aims to capture medium-term price trends while avoiding minor price noise, making it suitable for trending market conditions.

Note: As with all crossover systems, performance may vary in ranging markets. Combining with additional filters (volume, volatility, higher timeframe trend) can improve results.

Elliott Wave Oscillator + PSAR + VolumeStrategy Logic

1. Indicators

Elliott Wave Oscillator (EWO): This oscillator measures the difference between a 5-period and a 35-period exponential moving average (EMA). It's used to identify momentum shifts and potential wave structures. A buy signal is triggered when the EWO crosses above its signal line (a 5-period simple moving average). A sell signal is triggered when it crosses below.

Parabolic SAR (PSAR): This indicator shows potential reversals in price direction. A buy signal requires the PSAR to be below the current price, indicating an uptrend. A sell signal requires the PSAR to be above the current price, indicating a downtrend.

Volume: The strategy checks for significant changes in volume compared to its 20-period simple moving average (SMA). A buy signal requires a volume increase of at least 20% above the SMA. A sell signal requires a volume decrease of at least 20% below the SMA.

EMA 200: This long-term moving average is used to determine the overall market trend. A buy signal is only considered when the EMA 200 is rising (uptrend). A sell signal is only considered when the EMA 200 is falling (downtrend).

2. Entry and Exit Conditions

Long (Buy) Entry: A long position is entered if all of the following conditions are met:

EWO crosses its signal line upwards.

PSAR is below the price.

Volume has increased significantly.

The EMA 200 is rising.

The current candle is a bullish candle (close > open).

Short (Sell) Entry: A short position is entered if all of the following conditions are met:

EWO crosses its signal line downwards.

PSAR is above the price.

Volume has decreased significantly.

The EMA 200 is falling.

The current candle is a bearish candle (close < open).

Exit Conditions: Both long and short positions have a fixed 1% take profit and a 1% stop loss to manage risk.

In summary, the strategy only enters trades when a combination of momentum (EWO), trend (PSAR, EMA 200), and volume indicators align in the same direction, with strict risk management in place.

FFH_Golden Gate StrategyThe FFH_Golden Gate Strategy is a method designed to help identify strong opportunities to enter and exit the market with discipline. It works by following the natural flow of price movements and identifying when prices are trending higher in a consistent way. The strategy uses a special average that adapts to the market, helping to separate meaningful trends from random fluctuations.

A buy signal is generated when the price moves significantly above this average, indicating strong upward momentum. This approach ensures that trades are only taken when the market shows clear strength, rather than during sideways or uncertain conditions.

An exit signal occurs when the price falls below the average, suggesting that the upward trend may be weakening. This allows the strategy to lock in gains and avoid holding positions when the market is turning against you.

Overall, the strategy is based on the simple idea of following the trend, entering on strength, and exiting before losses grow, providing a structured and disciplined approach to trading without relying on guesswork or emotional decisions.

No Wick Strategy (No-wick candles) — by Sh1n1gam1**No Wick Strategy - Momentum Trading System**

This strategy identifies and trades "no wick" or "minimal wick" candles, which often indicate strong directional momentum and conviction in the market.

**STRATEGY CONCEPT:**

The No Wick Strategy capitalizes on candles that show strong directional commitment - bullish candles with little to no bottom wick (buyers in control from the start) and bearish candles with little to no top wick (sellers dominating from the open).

**HOW IT WORKS:**

📈 **LONG ENTRIES:**

- Identifies bullish candles with minimal/no bottom wick

- Places buy limit order slightly below the signal candle's open

- Enters only during specified trading session

📉 **SHORT ENTRIES:**

- Identifies bearish candles with minimal/no top wick

- Places sell limit order slightly above the signal candle's close

- Enters only during specified trading session

**KEY FEATURES:**

✅ Customizable trading session (New York timezone)

✅ Flexible wick threshold (0% for strict, up to X% for flexibility)

✅ ATR-based stop loss for dynamic risk management

✅ Configurable risk-reward ratio via TP multiplier

✅ Auto-cancellation of unfilled orders after X bars

✅ Body size filters (minimum and maximum)

✅ Visual signals and pending order levels

✅ Position status display

**RISK MANAGEMENT:**

- Stop Loss: Based on ATR multiplier

- Take Profit: Multiple of stop loss distance

- One position at a time

- No pyramiding or position flipping

**RECOMMENDED TIMEFRAMES:**

- M1 and M5 for scalping

- M15 and H1 for day trading

- H4 and Daily for swing trading

**MARKETS:**

Suitable for forex pairs, indices (NQ, ES), commodities, and liquid stocks.

**DEFAULT SETTINGS:**

- Trading Session: 09:30-11:00 ET (NY morning session)

- ATR SL Multiplier: 1.5

- TP Multiplier: 2.0 (2:1 RR ratio)

- Wick Threshold: 5%

- Order Cancellation: 5 bars

**TIPS FOR OPTIMIZATION:**

1. Adjust trading session to match your market's most active hours

2. Test different wick thresholds (0-10%) based on market volatility

3. Optimize body size filters for your specific instrument

4. Backtest different ATR multipliers for your risk tolerance

5. Consider market conditions - works best in trending markets

**IMPORTANT NOTES:**

- Uses limit orders for better entry prices

- Does not close opposing positions (no position flipping)

- Respects trading session boundaries strictly

- All times are in America/New_York timezone

**AUTHOR:** Sh1n1gam1

**VERSION:** 1.0

**SUPPORT:** Comments and suggestions welcome!

Happy Trading! 📊

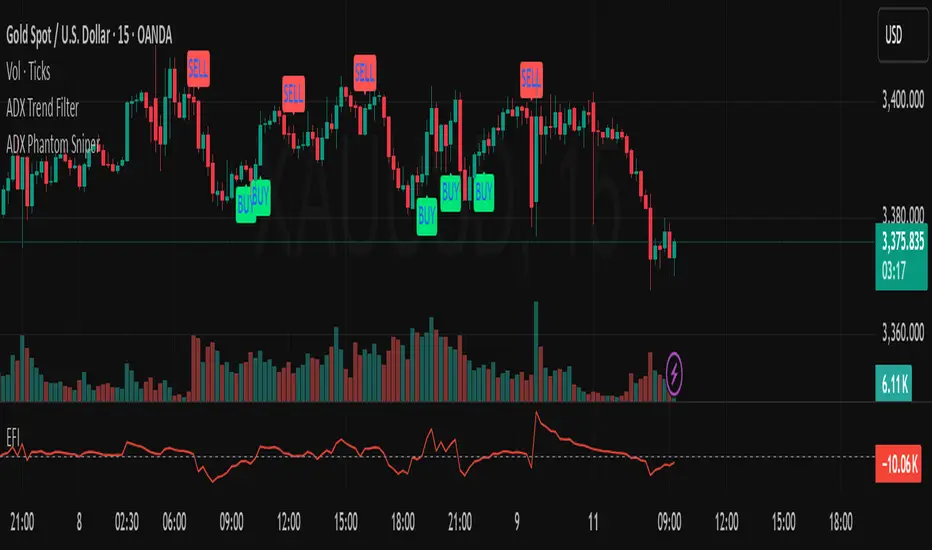

ADX Phantom SniperADX Phantom Sniper is a precision trend-following tool that combines three powerful forces:

1. ADX & DI Crossover Trigger – Detects strong directional moves only when the trend strength exceeds a defined threshold.

2. Multi-Timeframe (MTF) Confirmation – Executes on the current chart timeframe (e.g., M15) only if the higher timeframe (H1) confirms the same trend direction.

3. Force Index Momentum Filter – Filters entries based on bullish/bearish momentum to avoid weak signals.

Signal Logic:

BUY: EMA14 > EMA100, price above EMA14, +DI crosses above -DI, ADX > threshold, Stochastic crosses above signal line in the bullish zone (>50), MTF trend aligned, Force Index > 0 (optional).

SELL: EMA14 < EMA100, price below EMA14, -DI crosses above +DI, ADX > threshold, Stochastic crosses below signal line in the bearish zone (<50), MTF trend aligned, Force Index < 0 (optional).

Features:

Noise filtering with trend structure + higher timeframe alignment

On-chart BUY/SELL labels for easy signal spotting

Optional Force Index filter toggle

Adjustable ADX threshold, EMA lengths, Stochastic settings, and higher timeframe choice

Suitable for scalping and swing entries depending on timeframe

Recommended Setup:

Primary chart: M15

Higher timeframe confirmation: H1

Combine with your preferred risk management rules.

Disclaimer:

This tool is for educational purposes only and is not financial advice. Past performance does not guarantee future results. Use at your own risk.

Expanded Reversal System (4 Pattern Types)Overview

This is the final, refined version of a comprehensive candlestick reversal strategy, built with a core focus on reliability and safety. Its unique execution logic is designed to prevent common backtesting errors and ensure that the integrated risk management works precisely as intended on any timeframe.

The strategy aims to capture high-momentum reversals by identifying an expanded set of classic candlestick patterns and waiting for confirmation before entering a trade.

The "Confirm and Execute" Engine 🛡️

To eliminate bugs seen in simpler backtesting models, this strategy uses a deliberate, three-step execution process:

Signal: It first identifies a high-probability reversal pattern on a "Signal Candle."

Confirmation: It then waits for the next candle to break the high or low of the signal candle. This confirms momentum is moving in the desired direction.

Execution: Finally, it enters a market order on the open of the following candle.

This method ensures a robust and stable entry, allowing the Stop Loss and Take Profit orders to function with 100% reliability.

An Expanded Arsenal of Reversal Signals

This strategy looks for four distinct types of bullish and bearish patterns, giving it more opportunities to find valid trades:

Flexible Pin Bars: Loosened rules for Hammers and Shooting Stars to capture more opportunities.

Classic Engulfing Patterns: Identifies powerful, full-body engulfing candles.

Piercing Patterns & Dark Cloud Covers: Recognizes strong two-candle reversal signals.

Built-in Professional Risk Management 🎯

Automated Position Sizing: Every trade is automatically sized to risk exactly 2% of your current account equity.

Defined Exits: Once a trade is open, it is held until either the pre-calculated Stop Loss or Take Profit is hit. The strategy will not exit early or be influenced by new signals while in a trade.

Asymmetrical Risk/Reward: The strategy targets a 1:6 R:R for long trades and a 1:4 R:R for short trades.

How To Use

Apply the strategy to your chart.

Set your chart's timeframe. This version produced very strong results on the 3-Minute chart.

Review the detailed performance report in the 'Strategy Tester' tab.

Disclaimer: This strategy is provided for informational and educational purposes. All trading involves substantial risk, and past performance is not a guarantee of future results. Please use and adapt this tool responsibly.

ETH/SOL 1D Dynamic Trend Core - STRATEGY v 45Overview

The Dynamic Trend Core is a sophisticated, multi-layer trading engine designed to identify high-probability, trend-following opportunities. Its core philosophy is rooted in confluence, meaning it requires multiple conditions across trend, momentum, and volume to align before generating a signal. This approach aims to filter out market noise and provide a clearer view of the underlying trend.

The script includes a comprehensive backtesting engine for strategy optimization and a rich, intuitive visual interface for real-time analysis.

How It Works: Core Logic

The engine validates signals through several sequential layers:

Primary Trend Analysis (SAMA): The foundation is a Self-Adjusting Moving Average (SAMA) that dynamically determines the primary market direction (Bullish, Bearish, or Consolidation).

Momentum Confirmation: Signals are then qualified using a blend of the Natural Market Slope and a Cyclic RSI to ensure momentum is firmly aligned with the established trend.

Advanced Filtering Suite: A suite of optional filters provides robust confirmation and allows for deep customization: