Pure Price Action Breakout with 1:5 RR

Description of the Price Action Trading Script (Pine Script v6)

Overview

This script is a pure price action-based breakout strategy designed for TradingView. It identifies key breakout levels and executes long and short trades based on market structure. The strategy ensures a minimum risk-to-reward ratio (RR) of 1:5, aiming for high profitability with well-defined stop-loss and take-profit levels.

How the Script Works

1️⃣ Breakout Identification

The script uses a lookback period to find the highest high and lowest low over the last n bars.

A bullish breakout occurs when the price closes above the previous highest high.

A bearish breakout happens when the price closes below the previous lowest low.

2️⃣ Entry & Exit Strategy

Long Entry: If a bullish breakout is detected, the script enters a long position.

Short Entry: If a bearish breakout is detected, the script enters a short position.

The stop-loss is placed at the recent swing low (for long trades) or recent swing high (for short trades).

The target price is calculated based on a risk-to-reward ratio of 1:5, ensuring profitable trades.

3️⃣ Risk Management

The stop-loss prevents excessive losses by exiting trades when the market moves unfavorably.

The strategy ensures that each trade has a reward potential at least 5 times the risk.

Positions are executed based on price action only, without indicators like moving averages or RSI.

4️⃣ Visual Representation

The script plots breakout levels to help traders visualize potential trade setups.

Entry points, stop-loss, and take-profit levels are labeled on the chart for easy tracking.

Key Features & Benefits

✔ Pure Price Action – No lagging indicators, only real-time price movements.

✔ High Risk-to-Reward Ratio (1:5) – Ensures high-profit potential trades.

✔ Real-time Entry & Exit Signals – Provides accurate trade setups.

✔ Dynamic Stop-loss Calculation – Adjusts based on recent market structure.

✔ Customizable Parameters – Lookback periods and risk ratios can be modified.

在腳本中搜尋"profit"

Enhanced Bollinger Bands Strategy with SL/TP// Title: Enhanced Bollinger Bands Strategy with SL/TP

// Description:

// This strategy is based on the classic Bollinger Bands indicator and incorporates Stop Loss (SL) and Take Profit (TP) levels for automated trading. It identifies potential long and short entry points based on price crossing the lower and upper Bollinger Bands, respectively. The strategy allows users to customize several parameters to suit different market conditions and risk tolerances.

// Key Features:

// * **Bollinger Bands:** Uses Simple Moving Average (SMA) as the basis and calculates upper and lower bands based on a user-defined standard deviation multiplier.

// * **Customizable Parameters:** Offers extensive customization, including SMA length, standard deviation multiplier, Stop Loss (SL) in pips, and Take Profit (TP) in pips.

// * **Long/Short Position Control:** Allows users to independently enable or disable long and short positions.

// * **Stop Loss and Take Profit:** Implements Stop Loss and Take Profit levels based on pip values to manage risk and secure profits. Entry prices are set to the band levels on signals.

// * **Visualizations:** Provides options to display Bollinger Bands and entry signals on the chart for easy analysis.

// Strategy Logic:

// 1. **Bollinger Bands Calculation:** The strategy calculates the Bollinger Bands using the specified SMA length and standard deviation multiplier.

// 2. **Entry Conditions:**

// * **Long Entry:** Enters a long position when the closing price crosses above the lower Bollinger Band and the `Enable Long Positions` setting is enabled.

// * **Short Entry:** Enters a short position when the closing price crosses below the upper Bollinger Band and the `Enable Short Positions` setting is enabled.

// 3. **Exit Conditions:**

// * **Stop Loss:** Exits the position if the price reaches the Stop Loss level, calculated based on the input `Stop Loss (Pips)`.

// * **Take Profit:** Exits the position if the price reaches the Take Profit level, calculated based on the input `Take Profit (Pips)`.

// Input Parameters:

// * **SMA Length (length):** The length of the Simple Moving Average used to calculate the Bollinger Bands (default: 20).

// * **Standard Deviation Multiplier (mult):** The multiplier applied to the standard deviation to determine the width of the Bollinger Bands (default: 2.0).

// * **Enable Long Positions (enableLong):** A boolean value to enable or disable long positions (default: true).

// * **Enable Short Positions (enableShort):** A boolean value to enable or disable short positions (default: true).

// * **Pip Value (pipValue):** The value of a pip for the traded instrument. This is crucial for accurate Stop Loss and Take Profit calculations (default: 0.0001 for most currency pairs). **Important: Adjust this value to match the specific instrument you are trading.**

// * **Stop Loss (Pips) (slPips):** The Stop Loss level in pips (default: 10).

// * **Take Profit (Pips) (tpPips):** The Take Profit level in pips (default: 20).

// * **Show Bollinger Bands (showBands):** A boolean value to show or hide the Bollinger Bands on the chart (default: true).

// * **Show Entry Signals (showSignals):** A boolean value to show or hide entry signals on the chart (default: true).

// How to Use:

// 1. Add the strategy to your TradingView chart.

// 2. Adjust the input parameters to optimize the strategy for your chosen instrument and timeframe. Pay close attention to the `Pip Value`.

// 3. Backtest the strategy over different periods to evaluate its performance.

// 4. Use the `Enable Long Positions` and `Enable Short Positions` settings to customize the strategy for specific market conditions (e.g., only long positions in an uptrend).

// Important Notes and Disclaimers:

// * **Backtesting Results:** Past performance is not indicative of future results. Backtesting results can be affected by various factors, including market volatility, slippage, and transaction costs.

// * **Risk Management:** This strategy is provided for informational and educational purposes only and should not be considered financial advice. Always use proper risk management techniques when trading. Adjust Stop Loss and Take Profit levels according to your risk tolerance.

// * **Slippage:** The strategy takes into account slippage by specifying a slippage parameter on the `strategy` declaration. However, real-world slippage may vary.

// * **Market Conditions:** The performance of this strategy can vary significantly depending on market conditions. It may perform well in trending markets but poorly in ranging or choppy markets.

// * **Pip Value Accuracy:** **Ensure the `Pip Value` is correctly set for the specific instrument you are trading. Incorrect pip value will result in incorrect stop loss and take profit placement.** This is critical.

// * **Broker Compatibility:** The strategy's performance may vary depending on your broker's execution policies and fees.

// * **Disclaimer:** I am not a financial advisor, and this script is not financial advice. Use this strategy at your own risk. I am not responsible for any losses incurred while using this strategy.

Altcoins DCA ScalperIntroduction

The Altcoins DCA Scalper is a Pine Strategy Script designed to automate Altcoins trading through 3Commas integration. It implements a Dollar-Cost Averaging (DCA) strategy that expands upon 3Commas' standard DCA capabilities, helping to manage risk while trading both long and short positions automatically.

This tool aims to assist both beginners exploring automated trading and experienced 3Commas users seeking dynamic DCA automation. The script is specifically designed for the 1-minute timeframe , where it has shown a good balance between performance and risk management. Complete setup typically takes less than 10 minutes, with a detailed guide making configuration straightforward for users of all experience levels.

------------------------------

🔶 What is DCA?

------------------------------

Dollar-cost averaging (DCA) refers to the practice of gradually increasing your position size at lower prices when trading long, or at higher prices when trading short, to achieve a better average entry price if the market moves against the initial entry . Instead of investing all capital at once, which could result in a significant drawdown if the price moves unfavorably, DCA spreads entries across different price levels to help manage potential drawdowns as they occur.

In this script, DCA is implemented through a system that:

🔹 Triggers safety orders only when/if needed (if take profit isn't reached quickly)

🔹 Dynamically adjusts order sizing based on market volatility

🔹 Automatically reduces take profit targets after each DCA order to increase the likelihood of a positive outcome

🔹 Can handle drawdowns depending on market volatility and settings

The images below illustrate two scenarios: one where an entry reaches the take profit directly, without activating DCA orders, and another where DCA is utilized, with the order closing positively after two DCA orders.

Case 1: Order closes in profit after entry

Case 2: Order closes in profit after 2 DCA orders (dynamically placed based on trend and volatility)

This DCA implementation aims to enhance standard 3Commas DCA by adding market-adaptive features while maintaining risk management principles.

------------------------------

🔶 Could this strategy script benefit you?

------------------------------

This script may be helpful if you are:

✅ Looking to automate your trading through 3Commas integration while maintaining full control of your assets

✅ Wanting to enhance 3Commas' standard DCA with market-adaptive features that consider:

Multi-timeframe trend analysis

Real-time volatility assessment

Dynamic safety order sizing and timing

✅ Seeking to minimize chart monitoring through full automation of:

Entry and exit decisions

Safety order management

Risk controls

✅ Interested in comprehensive performance tracking with:

Real-time position metrics

Detailed backtesting capabilities

Risk/reward analysis

Backtesting Metrics (script performance over the backtesting period - which is approx. 15 days on the 1min timeframe with the TradingView Pro Plan):

Current/Open Deal Metrics (the deal is currently under DCA, and waiting for further actions to close):

✅ Looking for trading automation that remains easy to set up and use

Note: While this script provides trading automation, successful trading requires proper education, risk management, and regular performance monitoring. No automated tool can guarantee trading success or profits.

------------------------------

🔶 How it Works

------------------------------

The Altcoins DCA Scalper provides trading automation through:

Market Analysis

* Multi-timeframe trend analysis (1m to 1d) for market direction and entry validation

* Volatility assessment (1h, 4h, 24h) benchmarked against TOTAL3 (excluding Top10 Altcoins and Stablecoins)

* Real-time adjustment of DCA parameters based on:

* Current volatility class (low/medium/high) vs. overall Altcoins market

* Market trend strength

* Price action dynamics

Trading Execution

* Position opening aligned with detected market trends

* "Beast Mode" base order sizing that increases position size during strong trends

* Dynamic take-profit targets that automatically reduce after each safety order to increase the likelihood of positive exits

* Dynamic DCA with safety orders that can:

* Adapt timing based on volatility

* Scale order sizes based on market conditions

* Handle 30-50% drawdowns depending on volatility class

* Execute up to 6 safety orders per position

Risk Management

* Emergency exits during extreme market events:

* "Black Swan" protection for long positions

* "God-Candle" protection for short positions

* Configurable stop-loss with volatility-based placement

* Trend-switch management with automated position reversal

* Position aging controls to prevent capital lock-up

* Leveraged trading protection with a pre-liquidation exit system

Integration & Automation

* Quick setup with two 3Commas bots (typically under 10 minutes)

* Fully automated signal generation and execution through 3Commas

* Detailed performance tracking including:

* Real-time position metrics

* DCA depth analysis

* Win rate and ROE calculations

* Pre-configured settings optimized for most pairs

* Multiple customization options for experienced users

Note: While this strategy employs automation and risk management, trading always carries the risk of loss. No system can guarantee profits, and market conditions significantly impact performance. Always do your own research and monitor your positions closely.

------------------------------

How to Use

------------------------------

Setting up the Altcoins DCA Scalper is quick and facilitated by the User Interface:

1️⃣ 3Commas/TradingView Setup

* Create two 3Commas accounts if using the FREE plan:

* One account for Long Bot

* One account for Short Bot

* This split allows full functionality while staying within 3Commas' free tier limits

* You do not need two separate accounts if you have a Paid 3Commas subscription

* While a free TradingView account works with the script, it limits you to one trading pair and a 4-day backtesting history. A paid TradingView subscription removes these limitations (such as the "Essential" plan).

2️⃣ Bot Configuration

* Create one Long and one Short DCA Bot in 3Commas

* Follow the setup guide available in the script itself for hassle-free configuration

* Copy Bot IDs and Email Token for script connection

* No complex settings needed - the script manages all DCA parameters by itself

3️⃣ Script Implementation

* Apply the script to your TradingView charts

* Use the built-in backtesting to analyze performance on different pairs

* Focus on USDT.P futures pairs with good volatility

4️⃣ Trading Activation

* Create TradingView alerts for each trading pair you want to activate

* Example: Set an alert for BINANCE: XRPUSDT.P following the in-script guide

* The script automatically manages all aspects:

* Entry and exit decisions

* DCA execution

* Risk management

* Position monitoring

Capital Requirements

* Important: Ensure sufficient capital to cover all activated pairs

* Consider volatility class when allocating capital to specific pairs

Once setup is complete, the script operates fully automatically while you maintain complete control of your funds through 3Commas and your exchange.

Note: While the setup is straightforward, always start with a small number of pairs and monitor performance before expanding. Trade responsibly and never risk more than you can afford to lose.

------------------------------

Explaining the Settings

------------------------------

The Altcoins DCA Scalper offers mulitple customization options during the setup process. All settings include detailed tooltips and default values.

Core Settings Sections:

1️⃣ 3Commas Connection

* Bot IDs and Email Token configuration

* Leverage settings (1x to 5x supported)

* Detailed 3Commas bot setup guide included

* Automatic bot control configuration

2️⃣ Trading Parameters

* Capital allocation per trade

* Timeframe verification

* Alert system setup

* Backtesting period control

* Performance tracking preferences

3️⃣ Advanced Features

🔹 Risk Management Suite

* Emergency exit controls (to strengthen protection against extraordinary market events)

* Customizable stop-loss system

* Trend-based exit management

* Position aging controls

* Liquidation protection features

* Advanced DCA controls

🔹 Performance Analytics

* Real-time position monitoring

* Comprehensive backtesting metrics

* DCA depth analysis

* Win rate calculations

* Capital efficiency tracking

🔹 Technical Optimizations

* Exchange minimum order adjustment

* Trading pair name override capability

* System stability controls

* Error handling mechanisms

🔹 Interface Customization

* Theme selection

* Chart overlay options

* Warning display preferences

* Performance metrics visibility

All settings come pre-configured but can be fully customized based on your trading preferences and risk tolerance. The script includes tooltips and setup guides for each option.

Note: While default settings may be tested, market conditions vary and all trading involves risk. Monitor performance and adjust settings according to your risk management requirements.

------------------------------

Frequently Asked Questions

------------------------------

Here are some common questions you may have, and our answers:

❓ Is this tool only for experts? I'm new to algo trading, can I use it?

No, the Altcoins DCA Scalper could be used by both beginners and experienced traders. The setup process is guided, and the algorithm handles all the calculations in the background.

❓ I'm not familiar with 3Commas. Is that a problem?

While the script is designed to work with 3Commas, a step-by-step guide is provided within the script to help you set up your 3Commas accounts and bots, if needed.

❓ Do I need to constantly monitor the script after it's set up?

No, after the initial setup and configuration, the script operates autonomously. It handles all aspects of trading including entries, exits, DCA management, and risk controls. However, we recommend:

* Checking performance metrics daily

* Reviewing position statistics weekly

* Adjusting pair selection monthly based on performance

* Monitoring overall market conditions that might require adjustments

❓ Can I use it with leverage?

Yes, the script is designed to work with leverage up to 5x on perpetual futures pairs (USDT.P). It includes specific features for leveraged trading:

* Dynamic safety order placement based on distance to liquidation

* Pre-liquidation exit system to minimize exchange fees

* Adjustable take-profit targets optimized for leveraged positions

* Emergency exit system for extreme market movements

* Optional risk controls specific to leverage:

* Automatic exit in the liquidation danger zone

* Position size scaling based on leverage level

* Safety order adjustments for different leverage settings

While leverage can amplify returns, it also increases risk. We recommend starting with lower leverage (2x), or no leverage at all, until familiar with the script's operation.

❓ Does this script guarantee profits?

No, no script or trading strategy can guarantee profits. The Altcoins DCA Scalper provides a framework for implementing an automated DCA strategy, but your success will depend on many different factors and conditions.

❓ Do I need to understand the complex algorithms used in the script?

No, it’s not necessary. The logic is handled by the script, and you do not need to understand every detail to use it effectively. However, a basic knowledge of DCA concepts will be beneficial.

❓ Can I use this script with spot or leveraged trades?

The script is optimized for USDT.P pairs (perpetual futures) with leverage up to 5x. This allows:

* Automatic long/short position management

* Increased capital utilization

* Full DCA functionality without holding the underlying assets

* Enhanced risk management features specific to futures

While spot trading is possible, it requires holding underlying assets for shorts and doesn't access the script's full capabilities.

❓What timeframe should I use?

This script is optimized for the 1-minute timeframe , which is the recommended setting for the best balance between performance, capital efficiency, and risk. While we recommend using the tool on the 1 minute TF, it would work on other timeframes too.

❓ What happens if my internet/computer goes down?

Since the script sends signals from Tradingview to 3Commas (which executes trades on your exchange), your positions and DCA management continue to function even if your TradingView chart is closed or your computer is off. The script only needs to be active to generate new signals.

❓ How are the DCA parameters determined?

The script dynamically adjusts DCA parameters based on:

* The pair's volatility class (compared to the overall altcoin market)

* Current market conditions and volatility

* Position direction (long/short)

* Leverage settings

* Number of safety orders already executed

This allows for adaptive/dynamic DCA compared to static or %-based parameters.

❓ What exchanges are supported?

The script works with any exchange supported by 3Commas for futures trading (approximately 15 different crypto Exchanges). However, it's optimized for Binance Futures (USDT.P pairs) due to its high liquidity and for consistency.

❓ What happens during extreme market conditions?

The script includes some (optional) protective measures that can be activated:

* Emergency exits during sharp and abnormal market moves

* Automatic adjustment of DCA parameters during high volatility

* Position closure on significant trend changes

* Special handling of aged positions

These features aim to protect capital during unusual market conditions.

❓How many pairs can I trade simultaneously?

This depends on your total capital. As a general indication, define the number of pairs to activate based on:

* Total available capital

* Desired position size per pair

* Risk tolerance

* Pairs' volatility class

------------------------------

Final Thoughts

------------------------------

We believe that your trading performance will greatly depend on your selection of appropriate trading pairs for this script (high volatility), and your commitment to regularly monitoring its performance and adjust the settings, rather than on the script alone.

------------------------------

⚠️ Risk Disclaimer

------------------------------

Remember that trading involves risk, and most day traders experience losses. This script is for educational and informational purposes only. Past performance does not guarantee future results. This is not financial advice, and you should always do your own research (DYOR). Trade responsibly with capital you can afford to lose.

The Altcoins DCA Scalper is an independent tool and is not endorsed, connected, or validated by TradingView.

3Commas is a third-party service, and TradingView is not responsible for the 3Commas integration or the performance of 3Commas bots. You are solely responsible for the security and management of your 3Commas account. Do not share your 3Commas access credentials (like login information, Bots-ID, Email Token) with anyone. The Author of the script has no access to such information, and nobody (but you) should.

DCA (ASAP) V0 PTTScript Name: DCA (ASAP) V0 PTT

Detailed Description:

This script implements the Dollar-Cost Averaging (DCA) strategy, allowing you to automatically manage buy/sell orders safely and efficiently. Below are the key features of this script:

1. Purpose and Operation:

o Supports both Long and Short trading modes.

o Designed to optimize profitability using the DCA method, where Safety Orders are triggered when the price moves against the predicted direction.

o Helps users maintain their Target Profit in various market conditions.

2. Main Features:

o Automatic Order Placement: The initial Base Order is opened as soon as no active order exists.

o Safety Order Management: Safety Orders are automatically placed when the price moves against the initial order. The volume and distance of these orders are customizable.

o Order Closing: Orders are closed upon reaching the Target Profit, accounting for transaction fees.

o Detailed Information Display: Displays open orders, trading statistics, and performance metrics directly on the chart.

3. Customizable Parameters:

o Base Order Size: The size of the initial order.

o Target Profit (%): Target profit as a percentage of the total order volume.

o Safety Order Size: The size of each Safety Order.

o Price Deviation (%): The percentage distance between consecutive Safety Orders.

o Safety Order Volume Scale: The scaling factor for increasing the volume of subsequent Safety Orders.

o Max Safety Orders: The maximum number of Safety Orders allowed per deal.

4. Unique Features:

o Backtest Range Support: Enables you to limit backtesting to a specific time range of interest.

o Comprehensive Statistics: Displays detailed tables including open trades, pending orders, ROI, trading days, and realized profit.

o Integrated Trading Fees: Includes transaction fees in profit calculations for precise results.

5. Usage Instructions:

o Select the trading mode (Long or Short) from the "Strategy" input.

o Customize parameters such as Base Order, Safety Order, and Target Profit according to your requirements and the asset being traded.

o Monitor the performance of the strategy through the displayed information tables.

Notes:

• This script does not disclose detailed calculation logic but provides an overview of the concepts and usage.

• Designed for trading on exchanges that support margin or spot trading.

Briss Thorn XtremeStrategy Description: Briss Thorn Xtreme

The Briss Thorn Xtreme is an innovative trading strategy designed to identify and capitalize on opportunities in the forex market through advanced technical analysis and dynamic risk management. This strategy combines calculations based on RSI and ATR with time and day filters, providing customized signals and real-time alerts via Discord. Ideal for traders seeking a structured and highly customizable methodology, Briss Thorn Xtreme integrates enhanced visual tools for efficient trade management.

Key Features:

RSI and ATR-Based Signals: Utilizes smoothed RSI and ATR calculations to identify trends and measure volatility, allowing for more precise detection of buy and sell opportunities.

Dynamic Stop-Loss (SL) and Take-Profit (TP) Levels: Automatically calculates SL and TP levels based on market volatility, dynamically adjusting to optimize risk management.

Advanced Discord Integration: Sends detailed alerts to your Discord channel, including information such as the asset, signal time, entry price, and SL/TP levels, facilitating real-time decision-making.

Complete Customization: Allows users to adjust key parameters such as RSI periods, smoothing factors, liquidity thresholds, trading schedules, and operation days, adapting to different trading styles and market conditions.

Enhanced Chart Visualization: Includes visual elements like candle color changes based on trend, colored boxes for SL and TP, and a summary table of recent trades, enabling quick market interpretation.

Day and Time Operation Filters: Enables selection of specific days of the week and time slots during which signals are generated, optimizing market exposure and avoiding periods of low liquidity or unwanted high volatility.

Trade Summary: Displays a summary of the last three trades directly on the chart, indicating whether TP or SL was reached, aiding in strategy performance evaluation.

Customizable Alert Messages: Allows customization of messages sent to Discord for buy and sell signals, tailoring them to your specific preferences and requirements.

Additional Visual Tools: Highlights the operational range on the chart during permitted trading hours and colors candles based on the current trend (bullish, bearish, or neutral), enhancing visibility and decision-making.

How the Strategy Works:

Technical Indicators Calculation:

- RSI (Relative Strength Index) : Calculates RSI with a defined period and smooths it using an Exponential Moving Average (EMA) to obtain a more stable and reliable signal.

- ATR (Average True Range) : Calculates ATR adjusted by a rapid liquidity factor to measure the current market volatility, thereby determining the strength of the trend.

Generating Buy and Sell Signals:

- Buy Signal: A buy signal is generated when the liquidity index surpasses the short liquidity level, indicating potential accumulation and an upward trend.

- Sell Signal: A sell signal is generated when the liquidity index falls below the long liquidity level, indicating potential distribution and a downward trend.

- Operation Conditions: Signals are only generated on selected days and times, avoiding periods of low liquidity or unwanted high volatility.

Dynamic SL and TP Levels Calculation:

- Stop-Loss (SL) and Take-Profit (TP): SL and TP levels are calculated based on the entry price and a defined number of ticks, automatically adjusting to market volatility to optimize risk management.

- SL and TP Visualization: Colored boxes are drawn on the chart for a clear visual reference of SL and TP levels, facilitating trade management.

Automatic Execution and Alerts:

- Order Execution: Upon signal generation, the strategy automatically executes a market order (buy or sell).

- Discord Alerts: Detailed alerts are sent to the configured Discord channel, providing essential information for swift decision-making, including asset, signal time, entry price, current volatility (ATR), and trend direction.

Trade Management and Monitoring:

- Trade Summary: A table on the chart displays a summary of the last three trades (Today, Yesterday, Day Before Yesterday), indicating whether TP or SL was reached, allowing real-time performance evaluation.

- Automatic Trade Closure: The strategy automatically closes trades upon reaching the established SL or TP levels, ensuring efficient risk management and preventing excessive losses.

Additional Visualization:

- Candle Coloring by Trend: Candles are colored based on the current trend (bullish, bearish, or neutral), facilitating quick identification of market direction.

- Operational Range Highlighting: The chart background is colored during permitted trading hours, highlighting active periods of the strategy and enhancing trade visibility.

---

Strategy Properties (Important)

This backtest is conducted on M17 EURUSD using the following backtesting properties:

Initial Capital: $1000

Order Size: 1% of capital

Commission: $0.20 per order

Slippage: 1 tick

Pyramiding: 1 order

Price Verification for Limit Orders: 0 ticks

Recalculate on Order Execution: Enabled

Recalculate on Every Tick: Enabled

Recalculate After Order Execution: Enabled

Bar Magnifier for Backtesting Precision: Enabled

These properties ensure a realistic preview of the backtesting system. Note that default properties may vary for different reasons:

Order Size: It is essential to calculate the contract size according to the traded asset and desired risk level.

Commission and Slippage: These costs may vary depending on the market and instrument; there is no default value that guarantees realistic results.

All users are strongly recommended to adjust the properties within the script settings to align them with their trading accounts and platforms, ensuring that strategy results are realistic.

---

Backtesting Results:

- Net Profit: $327.90 (32.79%)

- Total Closed Trades: 162

- Profit Percentage: 35.80%

- Profit Factor: 1.298

- Maximum Drawdown: $146.70 (10.27%)

- Average per Trade: $2.02 (0.02%)

- Average Bars per Trade: 22

These results were obtained under the mentioned conditions and properties, providing an overview of the strategy's historical performance.

---

Interpretation of Results:

- The strategy has demonstrated profitability over the analyzed period, albeit with a success rate of 32.79%, indicating that success depends on a favorable risk-reward ratio.

- The profit factor of 1.298 suggests that total gains exceed total losses by this proportion.

- It is crucial to consider the maximum drawdown of 10.27% when evaluating the strategy's suitability to your risk tolerance.

---

Risk Warning:

Trading with leveraged financial instruments involves a high level of risk and may not be suitable for all investors. Before deciding to trade, you should carefully consider your investment objectives, level of experience, and risk tolerance. Past performance does not guarantee future results. It is essential to perform additional testing and adjust the strategy according to your needs.

---

What Makes This Strategy Original?

Unique RSI and Liquidity Focus: Unlike conventional strategies, Briss Thorn Xtreme focuses on combining RSI analysis with liquidity parameters to reflect institutional activity and macroeconomic events that may influence the market.

Advanced Technological Integration: The combination of automatic execution and customized alerts via Discord provides an efficient and modern tool for active traders.

Customization and Adaptability: The wide range of adjustable parameters allows the strategy to adapt to different assets, time zones, and trading styles, offering flexibility and complete user control.

Enhanced Visual Tools: Integrated visual elements, such as candle coloring, SL/TP boxes, and summary tables, facilitate quick market interpretation and informed decision-making.

---

Additional Considerations

Continuous Testing and Optimization: Users are advised to perform additional backtests and optimize parameters based on their own observations and requirements.

Complementary Analysis: Use this strategy in conjunction with other indicators and fundamental analysis tools to reinforce decision-making and confirm generated signals.

Rigorous Risk Management: Ensure that SL and TP levels, as well as position sizes, are aligned with your risk management plan to avoid excessive losses.

Updates and Support: I am committed to providing updates and improvements based on community feedback. For inquiries or suggestions, feel free to contact me.

---

Example Configuration

Assuming you want to use the strategy with the following parameters:

Discord Webhook: Your unique Discord Webhook

RSI Period: 6

RSI Smoothing Factor: 5

Rapid Liquidity Factor: 5

Liquidity Threshold: 5

SL Ticks: 100

TP Ticks: 250

SL/TP Box Width: 25 bars

Trading Days: Monday, Tuesday, Wednesday, Thursday, Friday

Trading Hours: Start at 8:00, End at 11:00

Simulated Initial Capital: $1000

Risk per Trade in Simulation: 1% of capital

Slippage and Commissions in Simulation: 1 tick slippage and $0.20 commission per trade

---

Conclusion

The Briss Thorn Xtreme strategy offers an innovative approach by combining advanced technical analysis with dynamic risk management and modern technological tools. Its original and adaptable design makes it a valuable tool for traders looking to diversify their methods and capitalize on opportunities based on less conventional patterns. Ready for immediate implementation in TradingView, this strategy can enhance your trading arsenal and contribute to a more informed and structured approach in your operations.

---

Final Disclaimer:

Financial markets are volatile and can present significant risks. This strategy should be used as part of a comprehensive trading approach and does not guarantee positive results. It is always advisable to consult with a professional financial advisor before making investment decisions.

DCA Buy v1Key Features

1. Selective Entry Filters

Trend Filter

Enabled through "Enable Trend Filter?" using the "EMA Length" setting to ensure entries align with prevailing trends.

Momentum Filter

Configured using "Enable Momentum Filter?" combined with "RSI Length" and "RSI Source" to detect oversold conditions.

Bollinger Filter

Activated via "Enable Bollinger Filter?" along with "BB Length" and "BB Multiplier" to focus entries on deeper price dips below Bollinger Bands.

2. DCA Configuration

Base Order Settings

Choose between a percentage ("Base Order % of Equity/Initial Capital") or fixed value ("Base Order Value ($)").

Safety Order Settings

Fine-tune "Initial Deviation (%)" and "Price Deviation Multiplier" to control the spacing of safety orders.

Use "Volume Scaling Factor (Qty)" to scale the size of each subsequent safety order.

Customize the "First Safety Order Type" as either value-based or a multiplier of the base order using "1st Safety Order Value ($)" or "1st Safety Order Multiplier (Qty)".

Set the maximum number of safety orders through "Max Safety Orders".

3. Profit and Risk Management

Take Profit Settings

"Take Profit (%)" triggers a sell when a specific profit percentage above the average entry is reached.

Use "Trailing Take Profit (%)" to lock in profits while capturing additional upside if prices continue to rise.

Stop Loss Settings

Configure "Stop Loss (%)" to prevent excessive drawdowns by closing all positions when prices drop below a defined percentage.

4. Time Control & Visualization

Time Filters

Define trading windows with "Start Time" and "End Time".

Use "Cooldown (Seconds)" to avoid frequent entries during rapid price movements.

Visualization

Enable "Show Average Entry Price", "Show Take Profit Level", and "Show Stop Loss Level" to plot key levels on the chart for better monitoring.

5. Performance Metrics

Built-in performance tracking includes:

Net Profit (%): Measures overall profitability.

Win Rate (%): Displays the ratio of winning trades.

Max Drawdown (%): Tracks the largest equity decline.

Trading Days: Calculates the duration of active trades.

Profit/Day (%): Evaluates daily returns.

The performance table also shows average cycle duration and utilization of available capital.

[3Commas] DCA Bot TesterDCA Bot Tester

🔷What it does: A tool designed to simulate the behavior of a Dollar Cost Averaging (DCA) strategy based on input signals from a source indicator. Additionally, it enables you to send activation signals to 3Commas Bots via TradingView webhooks.

🔷Who is it for: This tool is ideal for those who want a visual representation and strategy report of how a DCA Bot would perform under specific conditions. By adjusting the parameters, you can assess whether the strategy aligns with your risk/reward expectations before implementation, helping you save time and protect your capital.

🔷How does it work: The tool leverages a pyramiding function to simulate price averaging, mimicking how a DCA Bot operates. It calculates volume-based averaging and, upon reaching the target, closes the positions. Conversely, if the target isn't reached, a Stop Loss is triggered, potentially resulting in significant losses if improperly configured.

🔷Why It’s Unique

Easy visualization of DCA Bot entry and exit points according to user preferences.

DCA Bot Summary table same as the one shown in the new 3Commas interface.

Use plots from other indicators as Entry Trigger Source, with a small modification of the code.

Option to Review message format before sending Signals to 3Commas. Compatibility with Multi-Pair, and futures contract pairs.

Option to filter signals by session and day according to the user’s timezone.

👉 Before continuing with the explanation of the tool, please take a few minutes to read this information, paying special attention to the risks of using DCA strategies.

DCA Bot: What is it, how does it work, and what are its advantages and risks?

A DCA Bot is an automated tool designed to simplify and optimize your trading operations, particularly in cryptocurrencies. Based on the concept of Dollar Cost Averaging (DCA) , this bot implements scaled strategies that allow you to distribute your investments intelligently. The key lies in dividing your capital into multiple orders, known as base orders and safety orders, which are executed at different price levels depending on market conditions.

These bots are highly customizable, meaning you can adapt them to your goals and trading style, whether you're operating Long (expecting a price increase) or Short (expecting a price decrease). Their primary purpose is to reduce the impact of entries that move against the estimated direction and ensure you achieve a more favorable average price.

🔸 Key Features of DCA Bots

Customizable configuration: DCA bots allow you to adjust the size of your initial investment, the number of safety orders, and the price levels at which these orders execute. These orders can be equal or incremental, depending on your risk tolerance.

Scaled safety orders: If the asset's price moves against your position, the bot executes safety orders at strategic levels to average your entry price and increase your chances of closing in profit.

Automatic Take Profit: When the predefined profit level is reached, the bot closes the position, ensuring net gains by averaging all entries made using the DCA strategy.

Stop Loss option: To protect your capital, you can set a stop loss level that limits losses if the market moves drastically against your position.

Flexibility: Bots can integrate with 3Commas technical indicators or external signals from TradingView, allowing you to trade in any trend, whether bullish or bearish.

Support for multiple assets: You can trade cryptocurrency pairs and exchanges compatible with 3Commas, offering a wide range of possibilities to diversify your strategies.

✅ Advantages of DCA Bots

Time-saving automation: DCA bots eliminate the need for constant market monitoring, executing your trades automatically and efficiently based on predefined settings.

Favorable averages in volatile markets: By averaging your entries, the bot can offer more competitive prices even under adverse market conditions. This increases your chances of recovering a position and closing it profitably.

Advanced capital management: With customizable settings, you can adjust the size of base and safety orders to optimize capital usage and reduce risk.

Additional protection: The ability to set a stop loss ensures your losses are limited, safeguarding your capital in extreme scenarios.

⚠️ Risks of Using a DCA Bot

Requires significant capital: Safety orders can accumulate quickly if the price moves against your position. This issue is compounded if increasing amounts are used for safety orders, which can immobilize large portions of capital in adverse markets.

Markets lacking clear direction: During consolidation periods or erratic movements, the bot may generate unrealized losses and make position recovery difficult.

Opportunity cost: Investing in an asset that doesn't show favorable behavior can prevent you from seizing opportunities in other markets.

Emotional pressure: Large investments in advanced stages of the DCA strategy can cause stress, especially if an asset takes too long to reach your take profit level.

Dependence on market recovery: DCA assumes that the price will eventually move in your favor, which does not always happen, especially in assets without solid fundamentals.

📖 Key Considerations for Effectively Using a DCA Bot

Use small amounts for your base and safety orders: Setting small initial orders not only limits capital usage but also allows you to manage multiple bots simultaneously, maximizing portfolio diversification.

Capital management: Define a clear budget and never risk more than you are willing to lose. This is essential for maintaining sustainable operations.

Select assets with strong fundamentals: Apply DCA to assets you understand and that have solid fundamentals and a proven historical growth record. Additionally, analyze each cryptocurrency's fundamentals: What problem does it solve? Does it have a clear use case? Is it viable in the long term? These questions will help you make more informed decisions.

Diversification: Do not concentrate all your capital on a single asset or strategy. Spread your risk across multiple bots or assets.

Monitor regularly: While bots are automated and eliminate the need to monitor the market constantly, it is essential to monitor the bots themselves to ensure they are performing as expected. This includes reviewing their performance and making adjustments if market conditions change. Remember, the goal is to automate trades, but active bot management is crucial to avoid surprises.

A DCA Bot is a powerful tool for traders looking to automate their strategies and reduce the impact of market fluctuations. However, like any tool, its success depends on how it is configured and used. By applying solid capital management principles, carefully selecting assets, and using small amounts in your orders, you can maximize its potential and minimize risks.

🔷FEATURES & HOW TO USE

🔸Strategy: Here you must select the type of signal you are going to analyze and send signals to the DCA Bot, either Long for buy signals or Short for sell signals. This must match the Bot created in 3Commas.

🔸Add a Source Indicator for Entry Triggers

Tradingview allows us to use indicator plots as a source in other indicators, we will use this functionality so that the buy or sell signals of an indicator are processed by the DCA Bot Tester.

In this EXAMPLE we will use a simple strategy that uses a Donchian Channel (DC) and an Exponential Moving Average (EMA).

Trigger to buy or long signal will be when: the price closes above the previous upper level and the average of the upper and lower level (basis) is greater than the EMA.

Trigger sell or short signal will be when: the price closes below the previous lower level and the average of the upper and lower level (basis) is less than the EMA.

trigger_buy = ta.crossover (close,upper ) and basis > ema and barstate.isconfirmed

trigger_sell = ta.crossunder(close,lower ) and basis < ema and barstate.isconfirmed

Then we create the plots that will be used as input source in the DCA Bot Tester indicator.

When a buy condition is given the plot "🟢 Trigger Buy" will have a value of 1 otherwise it will remain at 0.

When a sell condition is given the plot "🔴 Trigger Sell" will have a value of -1 otherwise it will remain at 0.

plot(trigger_buy ? 1 : 0 , '🟢 Trigger Buy' , color = na, display = display.data_window)

plot(trigger_sell? -1 : 0 , '🔴 Trigger Sell', color = na, display = display.data_window)

Here you have the complete code so you can use it and do tests. Basically you just have to define the buy or sell conditions of your preferred indicator or strategy and then create the plots with the same format that will be used in DCA Bot Tester.

//@version=6

indicator(title="Simple Strategy Example", overlay= false)

// Indicator and Signal Triggers

length = input.int(10, title = "DC Length" , display = display.none)

length_ema = input.int(50, title = "EMA Length", display = display.none)

lower = ta.lowest (length)

upper = ta.highest(length)

ema = ta.ema (close, length_ema)

basis = math.avg (upper, lower)

plot(basis, "Basis", color = color.orange, display = display.all-display.status_line)

plot(upper, "Upper", color = color.blue , display = display.all-display.status_line)

plot(lower, "Lower", color = color.blue , display = display.all-display.status_line)

plot(ema , "EMA" , color = color.red , display = display.all-display.status_line)

candlecol = open < close ? color.teal : color.red

plotcandle(open, high, low, close, title='Candles', color = candlecol, wickcolor = candlecol, bordercolor = candlecol, display = display.pane)

trigger_buy = ta.crossover (close,upper ) and basis > ema and barstate.isconfirmed

trigger_sell = ta.crossunder(close,lower ) and basis < ema and barstate.isconfirmed

plotshape(trigger_buy ?close:na, title="Label Buy" , style=shape.labelup , location= location.belowbar, color=color.green, text="B", textcolor=color.white, display=display.pane)

plotshape(trigger_sell?close:na, title="Label Sell", style=shape.labeldown, location= location.abovebar, color=color.red , text="S", textcolor=color.white, display=display.pane)

// ――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――

// 👇 Plots to be used in the DCA Bot Indicator as source triggers.

// ――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――――

plot(trigger_buy ? 1 : 0 , '🟢 Trigger Buy' , color = na, display = display.data_window)

plot(trigger_sell? -1 : 0 , '🔴 Trigger Sell', color = na, display = display.data_window)

To use the example code

Open the Pine Editor, paste the code and then click Add to chart.

Then in the Plot Entry Trigger Source option, we will select 🟢 Trigger Buy, as the plot that will give us the buy signals when it is worth 1, otherwise for the sell signals you must change the value to -1 in the Plot Entry Trigger Value and remember to change the strategy mode to Short.

🔸DCA Settings: Here you need to configure the DCA values of the strategy, you can see the meaning of each value in the Settings Section. Once you are satisfied with the tests configure the 3Commas DCA Bot with the same values so that the Summary Table matches the 3Commas Table. Pay close attention to the Total Volume that the Bot will use, according to the amount of Safety Orders you are going to execute, and that all the values in the table adapt to your risk tolerance.

🔸DCA Bot Deal Start: Once you create the Bot in 3Commas with the same settings it will give you a Deal Start Message, you must copy and paste it in this section, verify that it is the same in the summary table, this is used to be sent through tradingview alerts to the Bot and it can process the signals.

🔸DCA Bot Multi-Pair: A Multi-Pair Bot allows you to manage several pairs with a single bot, but you must specify which pair it will run on. You must activate it if you want to use the signals in a DCA Bot Multi-pair. In the text box you must enter (using the 3Commas format) the symbol for each pair before you create the alert so that the bot understands which pair to work on.

In the following image we would be configuring the indicator to send a signal to activate the bot in the BTCUSDT pair using the given format it would be USDT_BTC, but if we wanted to send a signal in another pair we must change the pair in the chart and also in the configuration, an example with ETHUSDT would be USDT_ETH. After this we could create the alert, and the Mult-Pair Bot would detect it correctly.

🔸Strategy Tester Filters: This is useful if you want to test the strategy's result on a certain time window, the indicator will only enter this range. If disabled it will use all historical data available on the chart. If you are going to use the tool to send signals, make sure to disable the Use Custom Test Period. If you want the entries to only run at a certain time and day, in that case make sure that the timezone matches the one you are using in the chart.

🔸Properties: Adjust your initial capital and exchange commission appropriately to achieve realistic results.

🔸Create alerts to trigger the DCA Bot

Check that the message is the same as the one indicated by the DCA Bot.

In the case of Multi-Pair, enable the option to add the symbol with the correct format.

When creating an alert, select Any alert() function call.

Enter the any name of the alert.

Open the Notifications tab and enable Webhook URL

Paste Webhook URL provided by 3Commas looking in the section How to use TradingView custom signals.

Done, alerts will be sent with the correct format automatically to 3Commas.

🔷 INDICATOR SETTINGS

🔸3Commas DCA Bot Settings

Strategy: Select the direction of the strategy to test Long or Short, this must be the same as the Bot created in 3Commas, so that the signals are processed properly.

DCA Bot Deal Start: Copy and paste the message for the deal start signal of the DCA Bot you created in 3Commas. This is the message that will be sent with the alert to the Bot, you must verify that it is the same as the 3Commas bot so that it can process properly so that it executes and starts the trade.

DCA Bot Multi-Pair: A Multi-Pair Bot allows you to manage several pairs with a single bot, but you must specify which pair it will run on.

DCA Bot Summary Table: Here you can activate the display of table as well as change the size, position, text color and background color.

🔸Source Indicator Settings

Plot Entry Trigger Source: Select a Plot for Entries of the Source Indicator. This refers to the Long or Short entry signal that the indicator will use as BO (Base Order).

Plot Entry Trigger Value: Value of the Source Indicator to Deal Start Condition Trigger. The default value is 1, this means that when a signal is given for example Long in the source indicator, we will use 1 or for Short -1 if there is no signal it will be 0 so it will not execute any entry, please review the example code and adjust the indicator you are going to use in the same way.

🔸DCA Settings

Base Order: The Base Order is the first order the bot will create when starting a new deal.

Safety Order: Enter the amount of funds your safety orders will use to average the cost of the asset being traded.Safety orders are also known as Dollar Cost Averaging and help when prices move in the opposite direction to your bot's take profit target.

Safety Orders Deviation %: Enter the percentage difference in price to create the first Safety Order. All Safety Orders are calculated from the price the initial Base Order was filled on the exchange account.

Safety Orders Max Count: This is the total number of Safety Orders the bot is allowed to use per deal that is opened. All Safety Orders created by the bot are placed as Limit Orders on the exchange's order book.

Safety Orders Volume Scale: The Safety Order Volume Scale is used to multiply the amount of funds used by the last Safety Order that was created. Using a larger amount of funds for Safety Orders allows your bot to be more aggressive at Dollar Cost Averaging the price of the asset being traded.

Safety Orders Step Scale: The Safety Order Step Scale is used to multiply the Price Deviation percentage used by the last Safety Order placed on the exchange account. Using a larger value here will reduce the amount of Safety Orders your bot will require to cover a larger move in price in the opposite direction to the active deal's take profit target.

Take Profit %: The Take Profit section offers tools for flexible management of target parameters: automatic profit upon reaching one or more target levels in percentage.

Stop Loss % | Use SL: To enable Stop Loss, please check the "Use SL" box. This is the percentage that price needs to move in the opposite direction to close the deal at a loss. This must be greater than the sum of the deviations from the safety orders.

🔸Strategy Tester Filters

Use Custom Test Period: When enabled signals only works in the selected time window.. If disabled it will use all historical data available on the chart.

Test Start and End: Once the Custom Test Period is enabled, here you select the start and end date that you want to analyze.

Session Filter | Days | Background: Here you can choose a time zone in which signals will be sent or your strategy will be tested, as well as the days and a background of it. It is important that you use the same timezone as your chart so that it matches.

👨🏻💻💭 If this tool helps you, don’t forget to give it a boost! Feel free to share in the comments how you're using it or if you have any questions.

_________________________________________________________________

The information and publications within the 3Commas TradingView account are not meant to be and do not constitute financial, investment, trading, or other types of advice or recommendations supplied or endorsed by 3Commas and any of the parties acting on behalf of 3Commas, including its employees, contractors, ambassadors, etc.

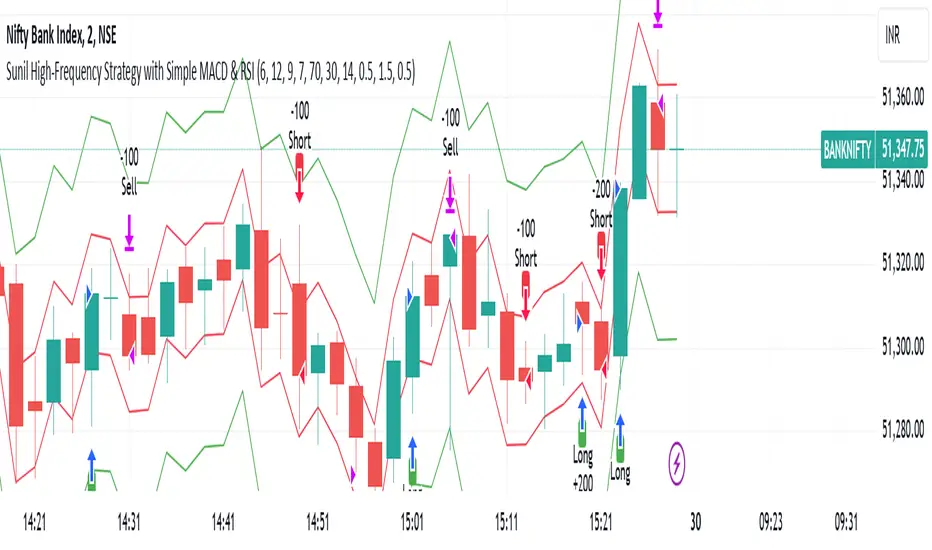

Sunil High-Frequency Strategy with Simple MACD & RSISunil High-Frequency Strategy with Simple MACD & RSI

This high-frequency trading strategy uses a combination of MACD and RSI to identify quick market opportunities. By leveraging these indicators, combined with dynamic risk management using ATR, it aims to capture small but frequent price movements while ensuring tight control over risk.

Key Features:

Indicators Used:

MACD (Moving Average Convergence Divergence): The strategy uses a shorter MACD configuration (Fast Length of 6 and Slow Length of 12) to capture quick price momentum shifts. A MACD crossover above the signal line triggers a buy signal, while a crossover below the signal line triggers a sell signal.

RSI (Relative Strength Index): A shorter RSI length of 7 is used to gauge overbought and oversold market conditions. The strategy looks for RSI confirmation, with a long trade initiated when RSI is below the overbought level (70) and a short trade initiated when RSI is above the oversold level (30).

Risk Management:

Dynamic Stop Loss and Take Profit: The strategy uses ATR (Average True Range) to calculate dynamic stop loss and take profit levels based on market volatility.

Stop Loss is set at 0.5x ATR to limit risk.

Take Profit is set at 1.5x ATR to capture reasonable price moves.

Trailing Stop: As the market moves in the strategy’s favor, the position is protected by a trailing stop set at 0.5x ATR, allowing the strategy to lock in profits as the price moves further.

Entry & Exit Signals:

Long Entry: Triggered when the MACD crosses above the signal line (bullish crossover) and RSI is below the overbought level (70).

Short Entry: Triggered when the MACD crosses below the signal line (bearish crossover) and RSI is above the oversold level (30).

Exit Conditions: The strategy exits long or short positions based on the stop loss, take profit, or trailing stop activation.

Frequent Trades:

This strategy is designed for high-frequency trading, with trade signals occurring frequently as the MACD and RSI indicators react quickly to price movements. It works best on lower timeframes such as 1-minute, 5-minute, or 15-minute charts, but can be adjusted for different timeframes based on the asset’s volatility.

Customizable Parameters:

MACD Settings: Adjust the Fast Length, Slow Length, and Signal Length to tune the MACD’s sensitivity.

RSI Settings: Customize the RSI Length, Overbought, and Oversold levels to better match your trading style.

ATR Settings: Modify the ATR Length and multipliers for Stop Loss, Take Profit, and Trailing Stop to optimize risk management according to market volatility.

Important Notes:

Market Conditions: This strategy is designed to capture smaller, quicker moves in trending markets. It may not perform well during choppy or sideways markets.

Optimizing for Asset Volatility: Adjust the ATR multipliers based on the asset’s volatility to suit the risk-reward profile that fits your trading goals.

Backtesting: It's recommended to backtest the strategy on different assets and timeframes to ensure optimal performance.

Summary:

The Sunil High-Frequency Strategy leverages a simple combination of MACD and RSI with dynamic risk management (using ATR) to trade small but frequent price movements. The strategy ensures tight stop losses and reasonable take profits, with trailing stops to lock in profits as the price moves in favor of the trade. It is ideal for scalping or intraday trading on lower timeframes, aiming for quick entries and exits with controlled risk.

TradeShields Strategy Builder🛡 WHAT IS TRADESHIELDS?

This no-code strategy builder is designed for traders on TradingView, offering an intuitive platform to create, backtest, and automate trading strategies. While identifying signals is often straightforward, the real challenge in trading lies in managing risk and knowing when not to trade. It equips users with advanced tools to address this challenge, promoting disciplined decision-making and structured trading practices.

This is not just a collection of indicators but a comprehensive toolkit that helps identify high-quality opportunities while placing risk management at the core of every strategy. By integrating customizable filters, robust controls, and automation capabilities, it empowers traders to align their strategies with their unique objectives and risk tolerance.

_____________________________________

🛡 THE GOAL: SHIELD YOUR STRATEGY

The mission is simple: to shield your strategy from bad trades . Whether you're a seasoned trader or just starting, the hardest part of trading isn’t finding signals—it’s avoiding trades that can harm your account. This framework prioritizes quality over quantity , helping filter out suboptimal setups and encouraging disciplined execution.

With tools to manage risk, avoid overtrading, and adapt to changing market conditions, it protects your strategy against impulsive decisions and market volatility.

_____________________________________

🛡 HOW TO USE IT

1. Apply Higher Timeframe Filters

Begin by analyzing broader market trends using tools like the 200 EMA, Ichimoku Cloud, or Supertrend on higher timeframes (e.g., daily or 4-hour charts).

- Example: Ensure the price is above the 200 EMA on the daily chart for long trades or below it for short trades.

2. Identify the Appropriate Entry Signal

Choose an entry signal that aligns with your model and the asset you're trading. Options include:

Supertrend changes for trend reversals.

Bollinger Band touches for mean-reversion trades.

RSI strength/weakness for overbought or oversold conditions.

Breakouts of key levels (e.g., daily or weekly highs/lows) for momentum trades.

MACD and TSI flips.

3. Determine Take-Profit and Stop-Loss Levels

Set clear exit strategies to protect your capital and lock in profits:

Use single, dual, or triple take-profit levels based on percentages or price levels.

Choose a stop-loss type, such as fixed percentage, ATR-based, or trailing stops.

Optionally, set breakeven adjustments after hitting your first take-profit target.

4. Apply Risk Management Filters

Incorporate risk controls to ensure disciplined execution:

Limit the number of trades per day, week, or month to avoid overtrading.

Use time-based filters to trade during specific sessions or custom windows.

Avoid trading around high-impact news events with region-specific filters.

5. Automate and Execute

Leverage the advanced automation features to streamline execution. Alerts are tailored specifically for each supported platform, ensuring seamless integration with tools like PineConnector, 3Commas, Zapier, and more.

_____________________________________

🛡 CORE FOCUS: RISK MANAGEMENT, AUTOMATION, AND DISCIPLINED TRADING

This builder emphasizes quality over quantity, encouraging traders to approach markets with structure and control. Its innovative tools for risk management and automation help optimize performance while reducing effort, fostering consistency and long-term success.

_____________________________________

🛡 KEY FEATURES

General Settings

Theme Customization : Light and dark themes for a tailored interface.

Timezone Adjustment : Align session times and news schedules with your local timezone.

Position Sizing : Define lot sizes to manage risk effectively.

Directional Control : Choose between long-only, short-only, or both directions for trading.

Time Filters

Day-of-Week Selection : Enable or disable trading on specific days.

Session-Based Trading : Restrict trades to major market sessions (Asia, London, New York) or custom windows.

Custom Time Windows : Precisely control the timeframes for trade execution.

Risk Management Tools

Trade Limits : Maximum trades per day, week, or month to avoid overtrading.

Automatic Trade Closures : End-of-session, end-of-day, or end-of-week options.

Duration-Based Filters : Close trades if take-profit isn’t reached within a set timeframe or if they remain unprofitable beyond a specific duration.

Stop-Loss and Take-Profit Options : Fixed percentage or ATR-based stop-losses, single/dual/triple take-profit levels, and breakeven stop adjustments.

Economic News Filters

Region-Specific Filters : Exclude trades around major news events in regions like the USA, UK, Europe, Asia, or Oceania.

News Avoidance Windows : Pause trades before and after high-impact events or automatically close trades ahead of scheduled news releases.

Higher Timeframe Filters

Multi-Timeframe Tools : Leverage EMAs, Supertrend, or Ichimoku Cloud on higher timeframes (Daily, 4-hour, etc.) for trend alignment.

Chart Timeframe Filters

Precision Filtering : Apply EMA or ADX-based conditions to refine trade setups on current chart timeframes.

Entry Signals

Customizable Options : Choose from signals like Supertrend, Bollinger Bands, RSI, MACD, Ichimoku Cloud, or EMA pullbacks.

Indicator Parameter Overrides : Fine-tune default settings for specific signals.

Exit Settings

Flexible Take-Profit Targets : Single, dual, or triple targets. Exit at significant levels like daily/weekly highs or lows.

Stop-Loss Variability : Fixed, ATR-based, or trailing stop-loss options.

Alerts and Automation

Third-Party Integrations : Seamlessly connect with platforms like PineConnector, 3Commas, Zapier, and Capitalise.ai.

Precision-Formatted Alerts : Alerts are tailored specifically for each platform, ensuring seamless execution. For example:

- PineConnector alerts include risk-per-trade parameters.

- 3Commas alerts contain bot-specific configurations.

_____________________________________

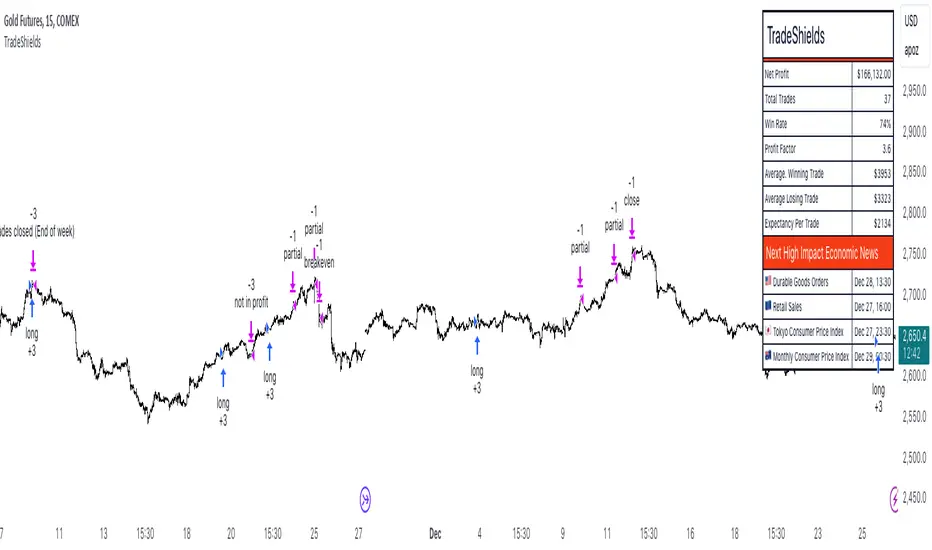

🛡 PUBLISHED CHART SETTINGS: 15m COMEX:GC1!

Time Filters : Trades are enabled from Tuesday to Friday, as Mondays often lack sufficient data coming off the weekend, and weekends are excluded due to market closures. Custom time sessions are turned off by default, allowing trades throughout the day.

Risk Filters : Risk is tightly controlled by limiting trades to a maximum of 2 per day and enabling a mechanism to close trades if they remain open too long and are unprofitable. Weekly trade closures ensure that no positions are carried over unnecessarily.

Economic News Filters : By default, trades are allowed during economic news periods, giving traders flexibility to decide how to handle volatility manually. It is recommended to enable these filters if you are creating strategies on lower timeframes.

Higher Timeframe Filters : The setup incorporates confluence from higher timeframe indicators. For example, the 200 EMA on the daily timeframe is used to establish trend direction, while the Ichimoku cloud on the 30-minute timeframe adds additional confirmation.

Entry Signals : The strategy triggers trades based on changes in the Supertrend indicator.

Exit Settings : Trades are configured to take partial profits at three levels (1%, 2%, and 3%) and use a fixed stop loss of 2%. Stops are moved to breakeven after reaching the first take profit level.

_____________________________________

🛡 WHY CHOOSE THIS STRATEGY BUILDER?

This tool transforms trading from reactive to proactive, focusing on risk management and automation as the foundation of every strategy. By helping users avoid unnecessary trades, implement robust controls, and automate execution, it fosters disciplined trading.

MultiLayer Acceleration/Deceleration Strategy [Skyrexio]Overview

MultiLayer Acceleration/Deceleration Strategy leverages the combination of Acceleration/Deceleration Indicator(AC), Williams Alligator, Williams Fractals and Exponential Moving Average (EMA) to obtain the high probability long setups. Moreover, strategy uses multi trades system, adding funds to long position if it considered that current trend has likely became stronger. Acceleration/Deceleration Indicator is used for creating signals, while Alligator and Fractal are used in conjunction as an approximation of short-term trend to filter them. At the same time EMA (default EMA's period = 100) is used as high probability long-term trend filter to open long trades only if it considers current price action as an uptrend. More information in "Methodology" and "Justification of Methodology" paragraphs. The strategy opens only long trades.

Unique Features

No fixed stop-loss and take profit: Instead of fixed stop-loss level strategy utilizes technical condition obtained by Fractals and Alligator to identify when current uptrend is likely to be over (more information in "Methodology" and "Justification of Methodology" paragraphs)

Configurable Trading Periods: Users can tailor the strategy to specific market windows, adapting to different market conditions.

Multilayer trades opening system: strategy uses only 10% of capital in every trade and open up to 5 trades at the same time if script consider current trend as strong one.

Short and long term trend trade filters: strategy uses EMA as high probability long-term trend filter and Alligator and Fractal combination as a short-term one.

Methodology

The strategy opens long trade when the following price met the conditions:

1. Price closed above EMA (by default, period = 100). Crossover is not obligatory.

2. Combination of Alligator and Williams Fractals shall consider current trend as an upward (all details in "Justification of Methodology" paragraph)

3. Acceleration/Deceleration shall create one of two types of long signals (all details in "Justification of Methodology" paragraph). Buy stop order is placed one tick above the candle's high of last created long signal.

4. If price reaches the order price, long position is opened with 10% of capital.

5. If currently we have opened position and price creates and hit the order price of another one long signal, another one long position will be added to the previous with another one 10% of capital. Strategy allows to open up to 5 long trades simultaneously.

6. If combination of Alligator and Williams Fractals shall consider current trend has been changed from up to downtrend, all long trades will be closed, no matter how many trades has been opened.

Script also has additional visuals. If second long trade has been opened simultaneously the Alligator's teeth line is plotted with the green color. Also for every trade in a row from 2 to 5 the label "Buy More" is also plotted just below the teeth line. With every next simultaneously opened trade the green color of the space between teeth and price became less transparent.

Strategy settings

In the inputs window user can setup strategy setting: EMA Length (by default = 100, period of EMA, used for long-term trend filtering EMA calculation). User can choose the optimal parameters during backtesting on certain price chart.

Justification of Methodology

Let's explore the key concepts of this strategy and understand how they work together. We'll begin with the simplest: the EMA.

The Exponential Moving Average (EMA) is a type of moving average that assigns greater weight to recent price data, making it more responsive to current market changes compared to the Simple Moving Average (SMA). This tool is widely used in technical analysis to identify trends and generate buy or sell signals. The EMA is calculated as follows:

1.Calculate the Smoothing Multiplier:

Multiplier = 2 / (n + 1), Where n is the number of periods.

2. EMA Calculation

EMA = (Current Price) × Multiplier + (Previous EMA) × (1 − Multiplier)

In this strategy, the EMA acts as a long-term trend filter. For instance, long trades are considered only when the price closes above the EMA (default: 100-period). This increases the likelihood of entering trades aligned with the prevailing trend.

Next, let’s discuss the short-term trend filter, which combines the Williams Alligator and Williams Fractals. Williams Alligator

Developed by Bill Williams, the Alligator is a technical indicator that identifies trends and potential market reversals. It consists of three smoothed moving averages:

Jaw (Blue Line): The slowest of the three, based on a 13-period smoothed moving average shifted 8 bars ahead.

Teeth (Red Line): The medium-speed line, derived from an 8-period smoothed moving average shifted 5 bars forward.

Lips (Green Line): The fastest line, calculated using a 5-period smoothed moving average shifted 3 bars forward.

When the lines diverge and align in order, the "Alligator" is "awake," signaling a strong trend. When the lines overlap or intertwine, the "Alligator" is "asleep," indicating a range-bound or sideways market. This indicator helps traders determine when to enter or avoid trades.

Fractals, another tool by Bill Williams, help identify potential reversal points on a price chart. A fractal forms over at least five consecutive bars, with the middle bar showing either:

Up Fractal: Occurs when the middle bar has a higher high than the two preceding and two following bars, suggesting a potential downward reversal.

Down Fractal: Happens when the middle bar shows a lower low than the surrounding two bars, hinting at a possible upward reversal.

Traders often use fractals alongside other indicators to confirm trends or reversals, enhancing decision-making accuracy.

How do these tools work together in this strategy? Let’s consider an example of an uptrend.

When the price breaks above an up fractal, it signals a potential bullish trend. This occurs because the up fractal represents a shift in market behavior, where a temporary high was formed due to selling pressure. If the price revisits this level and breaks through, it suggests the market sentiment has turned bullish.

The breakout must occur above the Alligator’s teeth line to confirm the trend. A breakout below the teeth is considered invalid, and the downtrend might still persist. Conversely, in a downtrend, the same logic applies with down fractals.

In this strategy if the most recent up fractal breakout occurs above the Alligator's teeth and follows the last down fractal breakout below the teeth, the algorithm identifies an uptrend. Long trades can be opened during this phase if a signal aligns. If the price breaks a down fractal below the teeth line during an uptrend, the strategy assumes the uptrend has ended and closes all open long trades.

By combining the EMA as a long-term trend filter with the Alligator and fractals as short-term filters, this approach increases the likelihood of opening profitable trades while staying aligned with market dynamics.

Now let's talk about Acceleration/Deceleration signals. AC indicator is calculated using the Awesome Oscillator, so let's first of all briefly explain what is Awesome Oscillator and how it can be calculated. The Awesome Oscillator (AO), developed by Bill Williams, is a momentum indicator designed to measure market momentum by contrasting recent price movements with a longer-term historical perspective. It helps traders detect potential trend reversals and assess the strength of ongoing trends.

The formula for AO is as follows:

AO = SMA5(Median Price) − SMA34(Median Price)

where:

Median Price = (High + Low) / 2

SMA5 = 5-period Simple Moving Average of the Median Price

SMA 34 = 34-period Simple Moving Average of the Median Price

The Acceleration/Deceleration (AC) Indicator, introduced by Bill Williams, measures the rate of change in market momentum. It highlights shifts in the driving force of price movements and helps traders spot early signs of trend changes. The AC Indicator is particularly useful for identifying whether the current momentum is accelerating or decelerating, which can indicate potential reversals or continuations. For AC calculation we shall use the AO calculated above is the following formula:

AC = AO − SMA5(AO), where SMA5(AO)is the 5-period Simple Moving Average of the Awesome Oscillator

When the AC is above the zero line and rising, it suggests accelerating upward momentum.

When the AC is below the zero line and falling, it indicates accelerating downward momentum.

When the AC is below zero line and rising it suggests the decelerating the downtrend momentum. When AC is above the zero line and falling, it suggests the decelerating the uptrend momentum.

Now we can explain which AC signal types are used in this strategy. The first type of long signal is when AC value is below zero line. In this cases we need to see three rising bars on the histogram in a row after the falling one. The second type of signals occurs above the zero line. There we need only two rising AC bars in a row after the falling one to create the signal. The signal bar is the last green bar in this sequence. The strategy places the buy stop order one tick above the candle's high, which corresponds to the signal bar on AC indicator.

After that we can have the following scenarios: